Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Cheniere Energy, Inc. | form_8-k.htm |

CHENIERE ENERGY

Cheniere Energy, Inc.

Corporate Presentation

June 2010

Corporate Presentation

June 2010

Forward Looking Statements

1

This presentation contains certain statements that are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of

the Securities Act and Section 21E of the Securities Exchange Act of 1933, as amended. All statements, other than statements of historical facts,

included herein are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

the Securities Act and Section 21E of the Securities Exchange Act of 1933, as amended. All statements, other than statements of historical facts,

included herein are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

§ statements that we expect to commence or complete construction of a liquefaction facility by certain dates, or at all;

§ statements that we expect to receive authorization from the Federal Energy Regulatory Commission, or FERC, or the Department of Energy, or

DOE to construct and operate a proposed liquefaction facility by a certain date, or at all;

DOE to construct and operate a proposed liquefaction facility by a certain date, or at all;

§ statements regarding future levels of domestic or foreign natural gas production and consumption, or the future level of LNG imports into North

America or exports from the U.S., or regarding projected future capacity of liquefaction or regasification facilities worldwide;

America or exports from the U.S., or regarding projected future capacity of liquefaction or regasification facilities worldwide;

§ statements regarding any financing transactions or arrangements, whether on the part of Cheniere or at the project level;

§ statements regarding any commercial arrangements marketed or potential arrangements to be performed in the future, including any cash

distributions and revenues anticipated to be received;

distributions and revenues anticipated to be received;

§ statements regarding the commercial terms and potential revenues from activities described in this presentation;

§ statements that our proposed liquefaction facility, when completed, will have certain characteristics, including a number of trains;

§ statements regarding our business strategy, our business plan or any other plans, forecasts, examples, models, forecasts or objectives: any or all of

which are subject to change;

which are subject to change;

§ statements regarding estimated corporate overhead expenses; and

§ any other statements that relate to non-historical information.

These forward-looking statements are often identified by the use of terms and phrases such as “achieve,” “anticipate,” “believe,” “estimate,” “example,”

“expect,” “forecast,” “opportunities,” “plan,” “potential,” “project,” “propose,” “subject to,” and similar terms and phrases. Although we believe that the

expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these

expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which speak only as of the date of

this presentation. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of

factors, including those discussed in “Risk Factors” in the Cheniere Energy, Inc. and Cheniere Energy Partners, L.P. Annual Reports on Form 10-K for

the year ended December 31, 2009, which are incorporated by reference into this presentation. All forward-looking statements attributable to us or

persons acting on our behalf are expressly qualified in their entirety by these ”Risk Factors”. These forward-looking statements are made as of the

date of this presentation, and we undertake no obligation to publicly update or revise any forward-looking statements.

These forward-looking statements are often identified by the use of terms and phrases such as “achieve,” “anticipate,” “believe,” “estimate,” “example,”

“expect,” “forecast,” “opportunities,” “plan,” “potential,” “project,” “propose,” “subject to,” and similar terms and phrases. Although we believe that the

expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these

expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which speak only as of the date of

this presentation. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of

factors, including those discussed in “Risk Factors” in the Cheniere Energy, Inc. and Cheniere Energy Partners, L.P. Annual Reports on Form 10-K for

the year ended December 31, 2009, which are incorporated by reference into this presentation. All forward-looking statements attributable to us or

persons acting on our behalf are expressly qualified in their entirety by these ”Risk Factors”. These forward-looking statements are made as of the

date of this presentation, and we undertake no obligation to publicly update or revise any forward-looking statements.

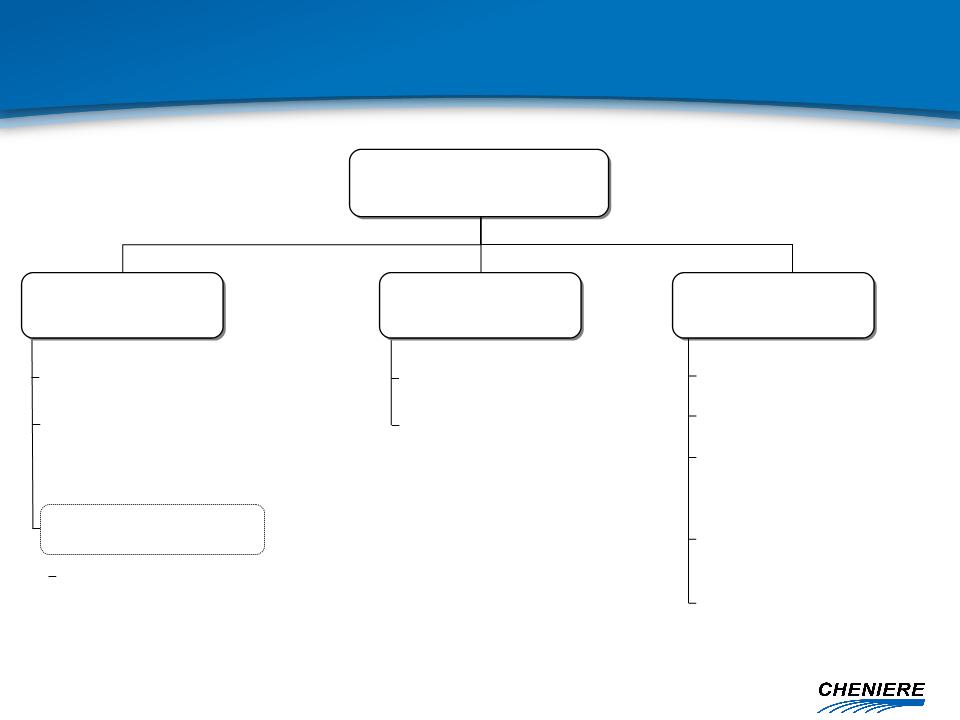

Cheniere Energy, Inc.

(“Cheniere”)

Marketing (“CMI”)

Sabine Pass LNG (SPLNG) (90.6%)*

Approved Permits:

Creole Trail LNG

Corpus Christi LNG

Creole Trail P/L (100%)

Approved Permits:

Creole Trail P/L Phase II

Corpus Christi P/L

2 Bcf/d Capacity at SPLNG**

MSPAs with major

LNG suppliers,

merchants, utilities

LNG suppliers,

merchants, utilities

Isle of Grain Put

Option 12 Cargoes/yr

Over 100 domestic

NAESBs and ISDAs

NAESBs and ISDAs

Pipelines

Terminals

JPMorgan Arrangement

Expand services at Sabine Pass LNG:

1 Bcf/d Liquefaction Capability

Development Project

* Sabine Pass LNG owned by Cheniere Energy Partners, L.P. (“CQP”)

**Variable Capacity Rights Agreement (“VCRA”) with CQP

Cheniere Business Segments

|

TUA

|

Capacity

|

2010 Full-Year

Payments ($ in MM) |

|

Total LNG USA

Chevron USA

Cheniere Energy Investments

|

1.0 Bcf/d

1.0 Bcf/d

2.0 Bcf/d

|

$123

$128

$252

|

Aerial view of Sabine Pass LNG

3

Sabine Pass LNG

Cheniere Energy, Inc. 90.6%

Cheniere Energy, Inc. 90.6%

§ Vaporization

– ~4.3 Bcf/d peak send-out

§ Storage

– 5 tanks x 160,000 cm (16.9 Bcfe)

§ Berthing / Unloading

– Two docks

– LNG carriers up to 266,000 cm

– Four dedicated tugs

§ Land

– 853 acres in Cameron Parish, LA

§ Accessibility - Deep Water Ship Channel

– Sabine River Channel dredged to 40

feet

feet

§ Proximity

– 3.7 nautical miles from coast

– 22.8 nautical miles from outer buoy

§ LNG Re-Exporting Capability

§ Size:

– 2.0 Bcf/d

§ Diameter:

– 42-inch diameter

§ Cost:

– ~$560 million first 94 miles

§ Initial interconnects:

– 4.1 Bcf/d of interconnect

capacity

capacity

§ Provides optimal market access for LNG from the Sabine Pass terminal

§ First 94 miles complete and in-service, additional 58 miles permitted

Creole Trail Pipeline

Cheniere Energy, Inc. 100%

Cheniere Energy, Inc. 100%

Sabine Pass to become bi-directional import/export facility

* Commencement of construction is subject to regulatory approvals and a final investment decision contingent upon Cheniere obtaining

satisfactory construction contracts and long-term customer contracts sufficient to underpin financing of the project.

satisfactory construction contracts and long-term customer contracts sufficient to underpin financing of the project.

Expanding Operations - Liquefaction Project*

Compelling Proposition

Compelling Proposition

§ Market fundamentals create opportunity to expand into exports

§ Export services provide customers with an attractively priced

option to access U.S. natural gas supply

option to access U.S. natural gas supply

§ Sabine Pass facility location is strategically situated

– Many existing assets in place needed for an export terminal

reduces capital required, cost estimates comparable to liquefaction

expansion economics

reduces capital required, cost estimates comparable to liquefaction

expansion economics

– Abundance of supply and existing infrastructure in surrounding

regions, proximity to Henry Hub

regions, proximity to Henry Hub

§ Powerful tool for industry players to manage their portfolios

– Early indications of interest from both buyers and sellers of natural

gas and LNG

gas and LNG

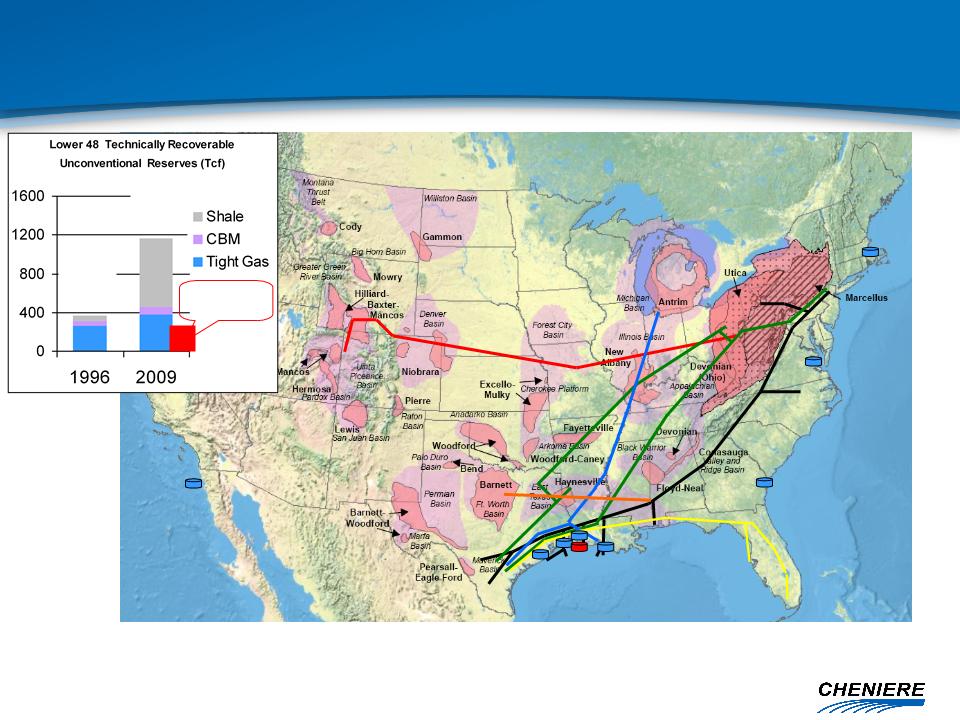

Market Fundamentals Drive Liquefaction Project

§ The U.S. has become the largest producer of natural gas in the

world and production costs rank among the lowest

world and production costs rank among the lowest

– Productive capacity at $6.50/MMBtu could reach 95 Bcf/d by 2020

§ U.S. natural gas demand not likely to keep pace with incremental

supply as demand continues to lag market forecasts, threatening to

lead to price volatility

supply as demand continues to lag market forecasts, threatening to

lead to price volatility

§ Globally, a natural gas supply gap is projected to develop in 2014-15

– Key driver is decline of UK Continental Shelf production

– Exacerbates dependency of European consumers on imported gas

– Asian consumers highly dependent on imported LNG for gas supply

§ Simultaneously, global LNG and pipeline gas suppliers continue to

enforce oil-price indexation in new contracts

enforce oil-price indexation in new contracts

– Key markets in Asia and Europe import over 70 Bcf/d of natural gas

– Imports forecast to increase by 26 Bcf/d over the next ten years

Sources: EIA (US map graphic, pipelines and LNG terminals placed by Cheniere)

Advanced Resources Intl (Lower 48 Unconventional Recoverable Reserves), ARI shale estimates updated April 2010

Depicted Pipelines: Rockies Express, Texas Eastern, Trunkline, Transco, FGT, C/P/SESH/Gulf Crossing (as a single route)

Depicted LNG terminals: Freeport, Golden Pass, Sabine Pass, Cameron, Trunkline, Elba Island, Cove Point, Everett

366

Tcf

Tcf

1,167

Tcf

Tcf

US Proved

Reserves

Reserves

U.S. Unconventional Reserves

Basins Proximate to Premium Markets and Major Pipelines

Basins Proximate to Premium Markets and Major Pipelines

3

Project Estimates:

§ Initial Phase: 1 Bcf/d (two modular trains)

§ Second Phase: Additional 1 Bcf/d

§ Estimated capex similar to liquefaction

expansion economics

expansion economics

§ Commercial start date: 2015e

Sabine Pass LNG

Proposed Liquefaction Project - Overview

Proposed Liquefaction Project - Overview

§ Leveraging existing assets

– Large acreage position (853 acres)

• Can readily accommodate 4 liquefaction trains

(up to 2 Bcf/d capacity)

(up to 2 Bcf/d capacity)

– Existing infrastructure

• 2 docks, 4 dedicated tugs

• LNG storage tanks (5 x 160,000 cm)

• Power generation

• Pipeline connections (Creole Trail)

§ Gas sourced from pipeline grid - Henry

Hub indexed pricing

Hub indexed pricing

§ “Demand Pull” model

– Global supply gap

– Diversity of supply

– Flexible processing

– Henry Hub indexation

450

400

350

300

250

200

150

100

50

0

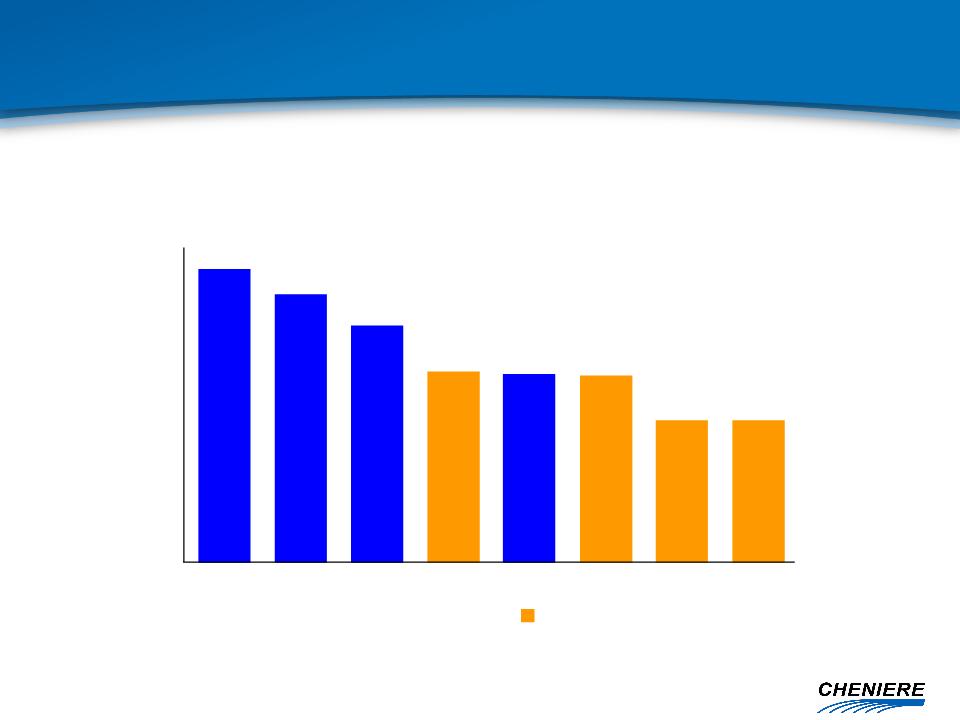

Cost

Qatargas Nigeria RasGas ELNGT1 Oman ALNGT1 ALNGT1-3 ELNGT1-2

ConocoPhillips-Bechtel - Global Liquefaction Collaboration

Source: ConocoPhillips-Bechtel

ConocoPhillips-Bechtel trains

$/Ton per Annum

Low Cost Liquefaction Facilities

Proven Technology

Proven Technology

Capacity fee includes regasification and liquefaction services -

provides customer option to import or export

Estimated cost to purchase U.S. supply:

Commercial Structure

Estimated Terms for LNG Sales Agreements

Estimated Terms for LNG Sales Agreements

Ê Capacity Fee: $1.40/MMBtu to $1.75/MMBtu

§ “Take or Pay”, permits lifting or unloading cargoes

§ Includes all facilities and Creole Trail Pipeline

Ê LNG Export Commodity Charge: $HH./MMBtu

§ Delivery Terms: FOB

§ Prevailing price for eastbound flow in local pipelines

§ Paid on a per-MMBtu basis, per cargo loaded

Ê Fuel Surcharge: 8%-12%

§ Projected based on forecast export activity

§ Trued up from period to period

2010 Financial Developments

Cheniere Energy, Inc.

Cheniere Energy, Inc.

§ Entered into marketing arrangement with JPMorgan

– Reduced working capital requirements for cargo purchases/sales

§ Sold 30% equity in Freeport to pay down debt

– Paid down $102 million of 9.75% term loan

§ Assigned CMI TUA to CQP subsidiary and entered into new variable

capacity rights agreement

capacity rights agreement

– Released TUA reserve account, funds used to pay down $64 million of

convertible senior secured notes

convertible senior secured notes

§ Continuing to address upcoming debt maturities at Cheniere

– Considering best options to maintain shareholder value

$247

$247

$502

Put option Aug-2011

2010

2011

2012

2018

Note: Balances as of June 30, 2010, reflect paydown of $64MM on convertible senior secured loans. Amounts do not include notes at CQP

JPMorgan Arrangement

§ Cheniere and JPMorgan joined LNG marketing efforts

§ CMI provides all services related to:

– sourcing deals and negotiating contracts, purchasing, transporting,

receiving, storing, regasifying and selling cargoes of LNG and regasified

LNG on an exclusive basis

receiving, storing, regasifying and selling cargoes of LNG and regasified

LNG on an exclusive basis

§ JPM provides credit support

§ JPM pays a fixed fee and additional fees dependent upon

gross margins achieved

gross margins achieved

§ JPM acquired CMI’s commercial inventory as of April 1, 2010

§ JPM has option to sign 0.5 Bcf/d TUA at $0.32/MMBtu

§ CQP: Subordination period extended - distributions to sub units dependent

on new business generated, including future CMI fees under the VCRA

on new business generated, including future CMI fees under the VCRA

§ LNG: Eliminates need for $64mm TUA reserve, funds from reserve used to

pay down $64mm on senior secured convertible loans

pay down $64mm on senior secured convertible loans

§ CMI assigned its 2.0 Bcf/d TUA with Sabine Pass LNG to direct subsidiary of

CQP, Cheniere Energy Investments, LLC (“Investments”)

CQP, Cheniere Energy Investments, LLC (“Investments”)

§ Investments will make TUA payments to Sabine Pass LNG effective 7/1/2010

§ CMI / Investments entered into a Variable Capacity Rights Agreement (“VCRA”)

that gives CMI rights provided in the TUA

that gives CMI rights provided in the TUA

§ CMI will continue marketing TUA capacity on CQP’s behalf

§ CMI will pay Investments 80% of positive gross margin for each cargo delivered

at Sabine

at Sabine

Transaction Summary

Results

* No impact to arrangement between CMI and JPMorgan or any existing agreements with other counterparties.

Cheniere and CQP Restructure Marketing

Arrangement*

Arrangement*

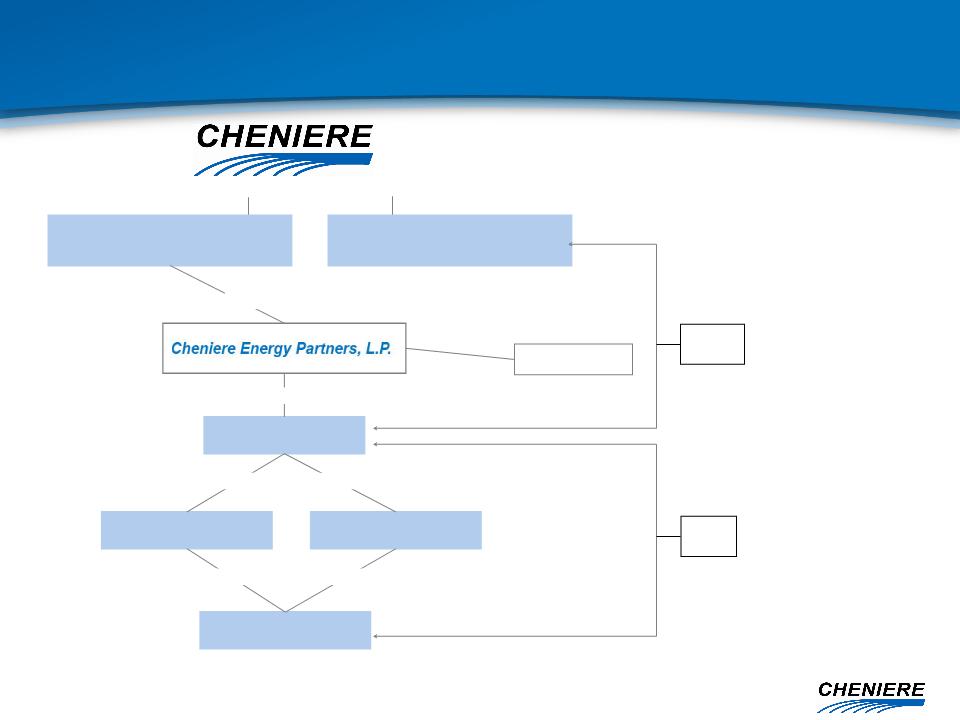

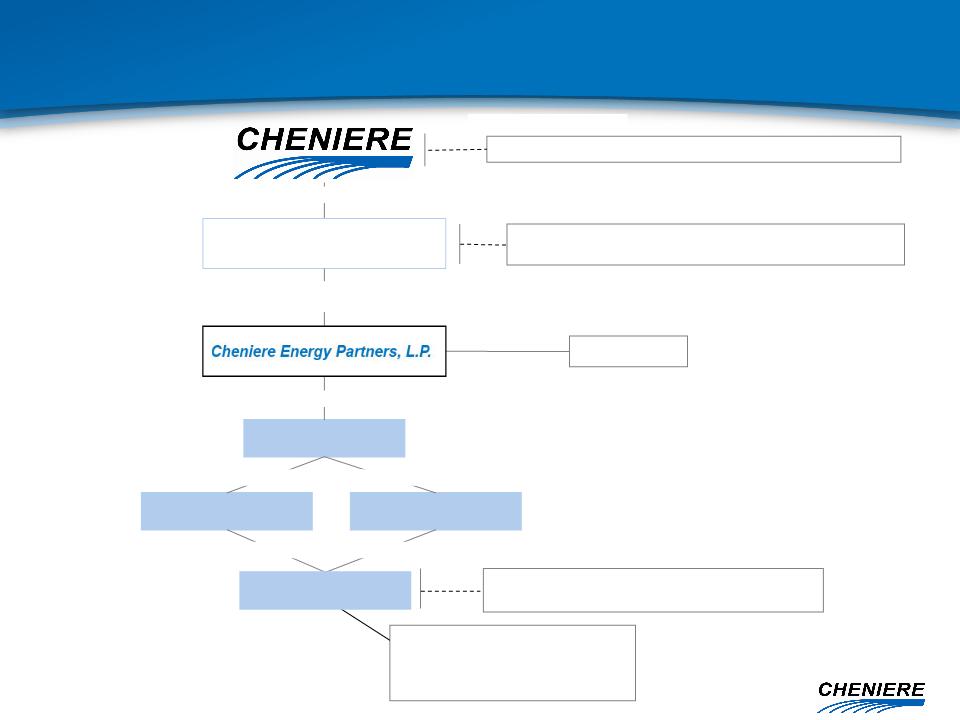

Public Unit holders

9.4% LP Interest

Cheniere Energy

Investments, LLC

Sabine Pass LNG-GP, Inc.

Sabine Pass LNG, L.P.

Sabine Pass LNG-LP, LLC

100% Ownership Interest

100% Ownership Interest

100% Ownership Interest

100% LP Interest

Non-Economic GP Interest

100% Ownership Interest

Cheniere LNG Holdings, LLC

88.6% LP Interest

100% of 2% GP Interest

100% of 2% GP Interest

NYSE Amex US: LNG

NYSE Amex US: CQP

3

Cheniere Marketing, LLC

VCRA

TUA

Organizational Structure

TUA Assignment and new VCRA

TUA Assignment and new VCRA

Disbursements

§ G&A, net Marketing 25-35

§ Pipeline & tug services 10

§ Other, incl adv tax payments 3-5

§ Debt service 34

Annualized*

($ in MM)

$45 - 55

*Estimates represent a summary of internal forecasts, are based on current assumptions and are subject to change. Actual performance may differ materially from,

and there is no plan to update the forecast. See “Forward Looking Statements” cautions. Estimates exclude earnings forecasts from operating activities.

and there is no plan to update the forecast. See “Forward Looking Statements” cautions. Estimates exclude earnings forecasts from operating activities.

**Approximately $11 million is fees for management services provided by Cheniere to CQP payable on a quarterly basis, equal to the lesser of 1) $2.5 million (subject

to inflation) or 2) such amount of CQP’s unrestricted cash and cash equivalents as remains after CQP has distributed in respect of each quarter for each common

unit then outstanding an amount equal to the IQD and the related GP distribution and adjusting for any cash needed to provide for the proper conduct of the

business of CQP, other than Sabine Pass operating cash flows reserved for distributions in respect of the next four quarters.

to inflation) or 2) such amount of CQP’s unrestricted cash and cash equivalents as remains after CQP has distributed in respect of each quarter for each common

unit then outstanding an amount equal to the IQD and the related GP distribution and adjusting for any cash needed to provide for the proper conduct of the

business of CQP, other than Sabine Pass operating cash flows reserved for distributions in respect of the next four quarters.

Net cash outflow

§ Baseline case, excludes estimates for cargo activity, Marketing margins and project development costs

Estimated Future Cash Flows

Cheniere Energy, Inc.

Cheniere Energy, Inc.

Receipts

§ Distributions from CQP (Common/GP) $ 20

§ Management fees from CQP 8-19**

Disbursements

§ Operating Expenses $34

§ Management Fees 8

§ Debt Service 165

Annualized*

($ in MM)

$51

*Estimates represent a summary of internal forecasts, are based on current assumptions and are subject to change. Actual

performance may differ materially from, and there is no plan to update the forecast. See “Forward Looking Statements” cautions.

performance may differ materially from, and there is no plan to update the forecast. See “Forward Looking Statements” cautions.

Distributable Cash Available

Distributions to GP and LP Unitholders

$46

Note: Not included in disbursements above is an estimate of up to approximately $11 million of fees payable to Cheniere for

services provided under a management services agreement. Such fees are payable on a quarterly basis equal to the lesser

of 1) $2.5 million (subject to inflation) or 2) such amount of CQP’s unrestricted cash and cash equivalents as remains after

CQP has distributed in respect of each quarter for each common unit then outstanding an amount equal to the IQD and the

related GP distribution and adjusting for any cash needed to provide for the proper conduct of the business of CQP, other

than Sabine Pass operating cash flows reserved for distributions in respect of the next four quarters.

services provided under a management services agreement. Such fees are payable on a quarterly basis equal to the lesser

of 1) $2.5 million (subject to inflation) or 2) such amount of CQP’s unrestricted cash and cash equivalents as remains after

CQP has distributed in respect of each quarter for each common unit then outstanding an amount equal to the IQD and the

related GP distribution and adjusting for any cash needed to provide for the proper conduct of the business of CQP, other

than Sabine Pass operating cash flows reserved for distributions in respect of the next four quarters.

Estimated Future Cash Flows

Cheniere Energy Partners

Cheniere Energy Partners

Receipts

§ TUA Customers $251

§ Fuel Retainage, Tugs, Other 7

Public Unit holders

9.4% LP Interest

Cheniere Energy

Investments, LLC

Sabine Pass LNG-GP, Inc.

Sabine Pass LNG-LP, LLC

100% Ownership Interest

100% Ownership Interest

100% Ownership Interest

100% LP Interest

Non-Economic GP Interest

100% Ownership Interest

Cheniere LNG Holdings, LLC

$205 mm 2.25% Convertible Senior Unsecured Notes due 2012

$550 mm 7.25% Senior Secured Notes due 2013

$1,666 mm 7.50% Senior Secured Notes due 2016

88.6% LP Interest

100% of 2% GP Interest

100% of 2% GP Interest

NYSE Amex US: LNG

NYSE Amex US: CQP

3

$298 mm 9.75% Term Loan due 2012

$247 mm 12.0% Convertible Senior Secured Loans due 2018

Note: Balances as of June 30, 2010; convertible

senior secured loans balance is proforma the

$64MM pay down from TUA reserve release.

senior secured loans balance is proforma the

$64MM pay down from TUA reserve release.

Customer Annual TUA Pmt

Total $123MM

Chevron $128MM

Investments $252MM

Sabine Pass LNG, L.P.

Organizational Structure

Appendix

Source: Poten

24.2

15

7

2

Bcf/d(e)

LNG Supply and Demand Trends

Source: GIIGNL, Cheniere Research, 2009e

Skikda

Explosion

Explosion

Schedule slippage,

underperformance

underperformance

FMs, Maintenance

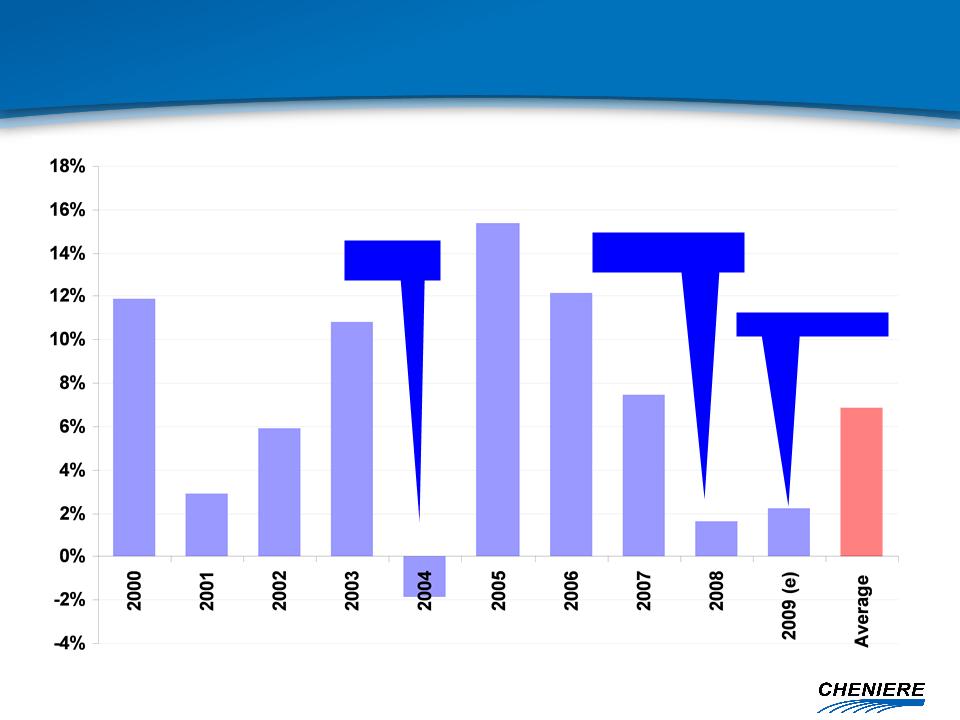

YoY Change in LNG Supply Trends

Well-below Average for Second Year

Well-below Average for Second Year

Source: Poten

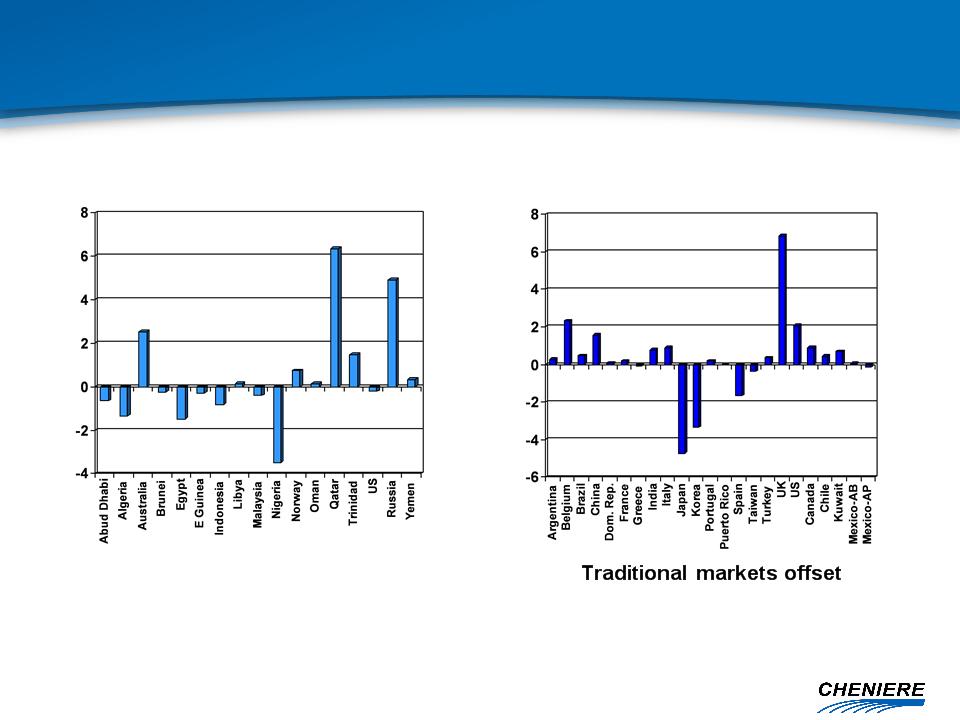

Supply growth masked

by production losses

by traded markets

Export Variance 09 v 08

Import Variance 09 v 08

MTPA

MTPA

YoY Changes in LNG Supply and Demand

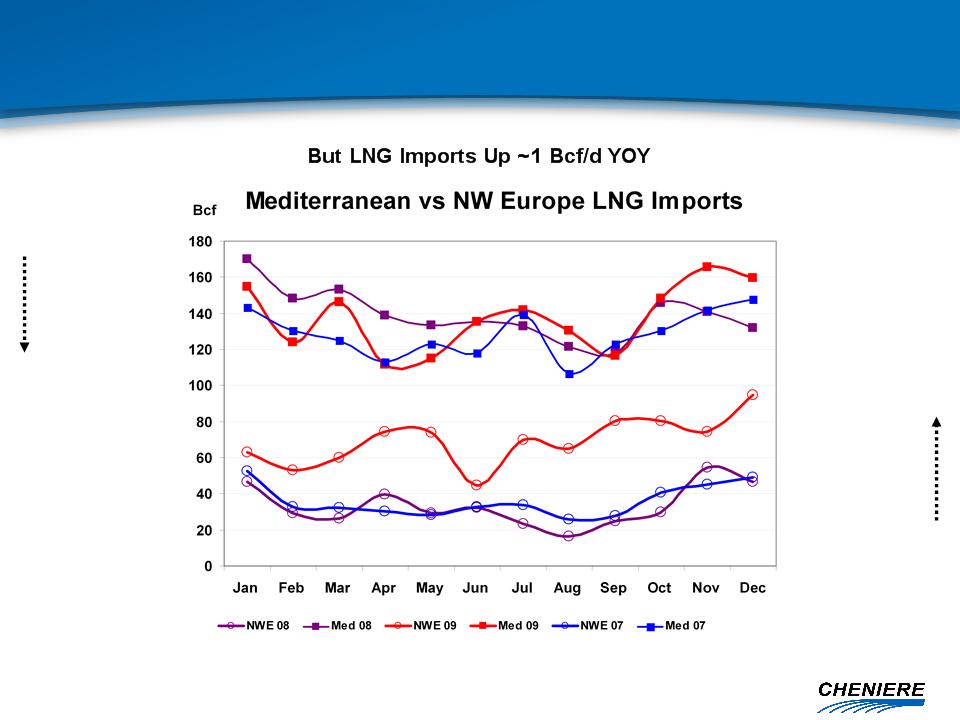

2009 ‘Anomaly’

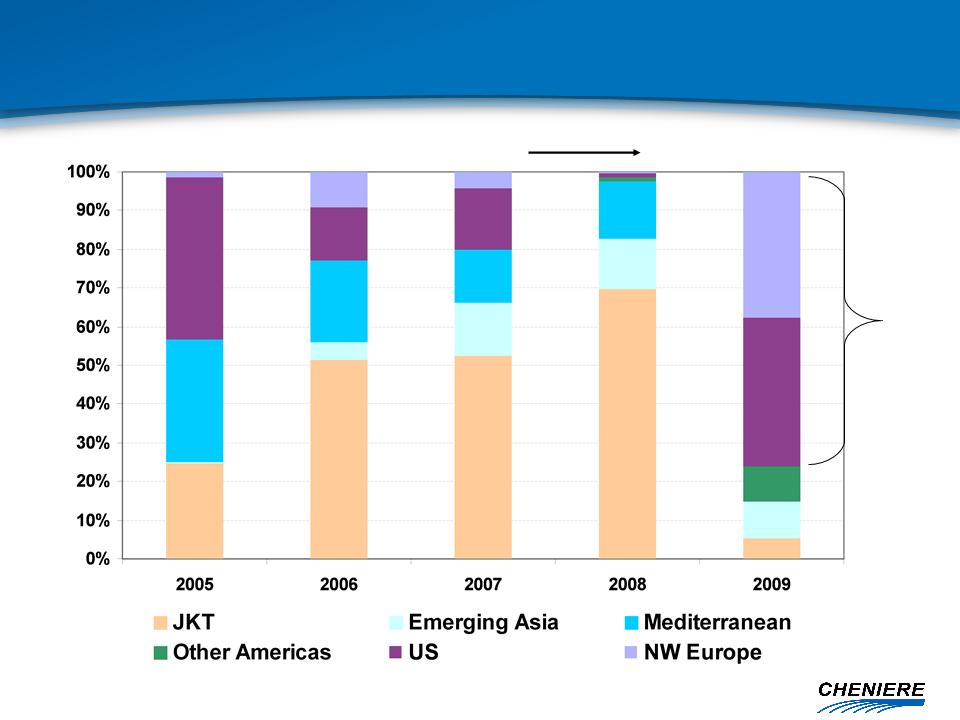

Europe Oversupplied but LNG Imports Up

Europe Oversupplied but LNG Imports Up

Recession induced demand reduction ~4 Bcf/d

Med

NWE

+ 109 %

(+145 cargoes)

Note: NWE = UK, BE, + Montoir

- 1.5%

(-7 cargoes, despite

addition of Rovigo in

Italy)

addition of Rovigo in

Italy)

Source: Waterborne

Traded

Liquid

Markets

Loose

Gradual Tightening

Loose

Source: GIIGNL, Cheniere Research , 2009e

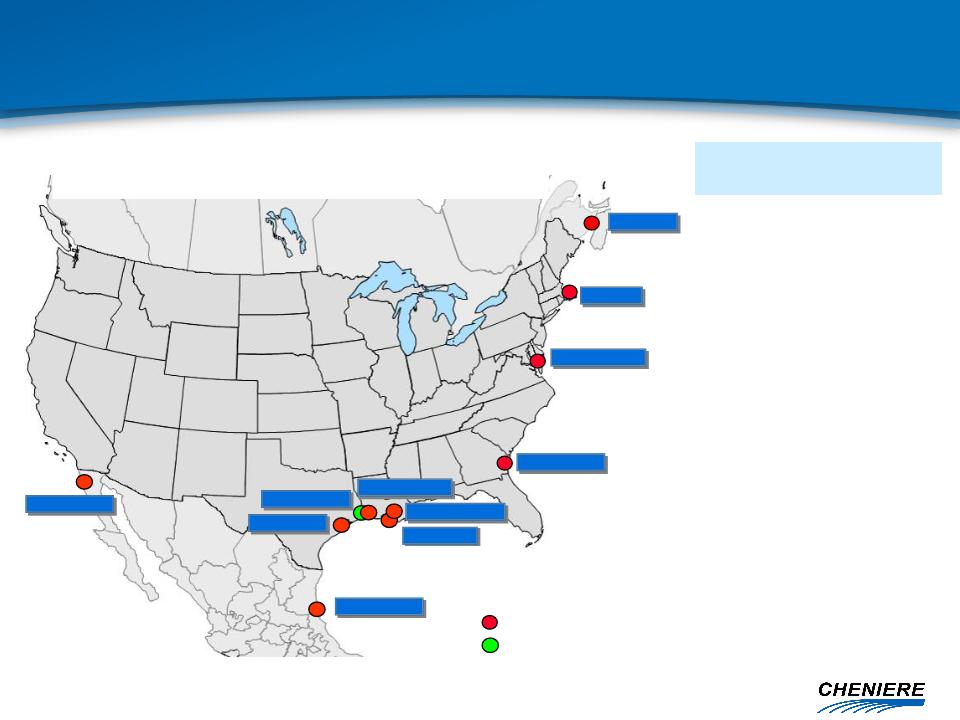

Spot LNG By Destination Region

Everett

Cove Point

Elba Island

Lake Charles

Sabine Pass

Freeport

Golden Pass

Cameron

Costa Azúl

Canaport

Existing

Under Construction

Altamira

Source: Websites of Terminal Owners

|

Terminal

Capacity Holder

|

Baseload

Sendout

(MMcf/d) |

|

Canaport 1,000

Irving, Repsol

|

|

|

Everett - Suez 700

|

|

|

Cove Point 1,800

BP, Statoil, Shell

|

|

|

Elba Island 800

BG, Marathon, Shell

|

|

|

Lake Charles - BG 1,800

|

|

|

Freeport 1,500

ConocoPhillips, Dow

|

|

|

Sabine Pass 4,000

Total, Chevron, Cheniere

|

|

|

Cameron 1,500

Sempra, ENI

|

|

|

Golden Pass 2,000

ExxonMobil, ConocoPhillips, QP

|

|

|

Altamira 700

Shell, Total

|

|

|

Costa Azul 1,000

Shell, Sempra

|

|

|

Total 16,800

|

|

15.8 Bcf/d North American Atlantic Basin

capacity @ 65% utilization = 10.3 Bcf/d

capacity @ 65% utilization = 10.3 Bcf/d

North America Onshore

Regasification Capacity By 2010

Regasification Capacity By 2010

CHENIERE ENERGY

Cheniere Energy

Investor Relations

Katie Pipkin, Vice President

(713) 375-5110 - katie.pipkin@cheniere.com

Christina Cavarretta, Manager

(713) 375-5104 - christina.cavarretta@cheniere.com