Attached files

| file | filename |

|---|---|

| EX-3.4 - COMMAND SECURITY CORP | v189015_ex3-4.htm |

| EX-31.2 - COMMAND SECURITY CORP | v189015_ex31-2.htm |

| EX-31.1 - COMMAND SECURITY CORP | v189015_ex31-1.htm |

| EX-32.1 - COMMAND SECURITY CORP | v189015_ex32-1.htm |

| EX-99.10 - COMMAND SECURITY CORP | v189015_ex99-10.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

x ANNUAL REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the

fiscal year ended March 31, 2010

or

¨ TRANSITION REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

transition period from _________ to _________

Commission

File Number: 001-33525

Command

Security Corporation

(Exact

name of registrant as specified in its charter)

|

New

York

|

14-1626307

|

|

|

(State

or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

|

|

Lexington

Park, Lagrangeville, New York 12540

(Address

of principal executive offices)

|

||

|

Registrant’s

telephone number, including area code: (845)

454-3703

|

||

|

Securities

registered pursuant to Section 12(b) of the Act:

|

||

|

Title

of each class

|

Name

of each exchange on which registered

|

|

|

Common

Stock, par value $0.0001 per share

|

American

Stock

Exchange

|

|

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes o No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes o No x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter) is not contained herein, and will not

be contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “accelerated filer,” “large

accelerated filer” and smaller reporting company in Rule 12b-2 of the Exchange

Act.

|

Large

accelerated filer ¨

|

Accelerated

filer ¨

|

Non-accelerated

filer x

|

Smaller

reporting company ¨

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act). Yes ¨ No x

The

aggregate market value of the registrant’s voting and non-voting common equity

held by non-affiliates of the registrant was $16,271,442 as of September

30, 2009.

In

determining the market value of the voting or non-voting common equity held by

non-affiliates of the registrant, securities of the registrant beneficially

owned by the directors and officers of the registrant have been

excluded. This determination of affiliate status is not necessarily a

conclusive determination for any other purpose.

There

were 10,872,098 outstanding shares of the registrant’s common stock as of June

18, 2010.

Certain

information required by Items 10, 11, 12, 13 and 14 of Form 10-K is incorporated

by reference into Part III hereof from the registrant’s proxy statement relating

to the registrant’s 2010 Annual Meeting of Shareholders, which is expected to be

filed with the Securities and Exchange Commission (the “SEC”) within 120 days of

the close of the registrant’s fiscal year ended March 31, 2010.

Command

Security Corporation

Annual

Report on Form 10-K

For

the Fiscal Year Ended March 31, 2010

Table

of Contents

|

Page

|

||

|

PART

I

|

||

|

Item

1. Business

|

1

- 3

|

|

|

Item

1A. Risk Factors

|

4

- 7

|

|

|

Item

1B. Unresolved Staff Comments

|

7

|

|

|

Item

2. Properties

|

7

- 11

|

|

|

Item

3. Legal Proceedings

|

11

|

|

|

Item

4. Submission of Matters to a Vote of Security

Holders

|

11

|

|

|

PART

II

|

||

|

Item

5. Market for the Registrant's Common Equity, Related Stockholder Matters

and Issuer Purchases of Equity Securities

|

12

- 13

|

|

|

Item

6. Selected Financial Data

|

14

|

|

|

Item

7. Management's Discussion and Analysis of Financial Condition

and Results of Operations

|

14

- 22

|

|

|

Item

7A. Quantitative and Qualitative Disclosures About Market

Risk

|

22

|

|

|

Item

8. Financial Statements and Supplementary Data

|

23

|

|

|

Item

9. Changes in and Disagreements with Accountants on Accounting

and Financial Disclosure

|

23

|

|

|

Item

9A(T). Controls and Procedures

|

23

|

|

|

Item

9B. Other Information

|

23

|

|

|

PART

III

|

||

|

Item

10. Directors, Executive Officers and Corporate

Governance

|

24

|

|

|

Item

11. Executive Compensation

|

24

|

|

|

Item

12. Security Ownership of Certain Beneficial Owners and

Management and Related Stockholder Matters

|

24

|

|

|

Item

13. Certain Relationships and Related Transactions, and

Director Independence

|

24

|

|

|

Item

14. Principal Accounting Fees and Services

|

24

|

|

|

PART

IV

|

||

|

Item

15. Exhibits, Financial Statement Schedules

|

25

|

|

|

Signatures

|

26

|

General

Command

Security Corporation (the “Company,” or “we”) principally provides uniformed

security officers, aviation security services and support security services to

commercial, financial, industrial, aviation and governmental customers

throughout the United States. We provide our security services to our

customers through our security services division, our aviation services division

and our support services division.

We

provide security services to governmental, quasi-governmental, health,

educational and financial institutions, residential and commercial property

management companies, and industrial, distribution, logistics and retail

customers through our security services division. Our security

officer services include providing armed and unarmed uniformed security

personnel for access control, mobile patrols, traffic control, security

console/system operators, fire safety directors; and communication, reception,

concierge and front desk/doorman operations. Our security services

division generated approximately $73.0 million, or 50.1% of our revenues for our

fiscal year ended March 31, 2010.

Our

aviation services division provides aviation security services to more than 100

of the largest domestic and international airlines, airports, airport

authorities and the general aviation community at approximately twenty

international airports and, to a lesser extent, five regional

airports. Our aviation security services include providing a variety

of uniformed services for domestic and international air carriers, including

security for airlines, aircraft, passengers and cargo; baggage screening,

wheelchair escort services featuring the Company’s proprietary SmartWheelTM

technology, special escort services and skycap services. Our

aviation services division generated approximately $72.5 million, or 49.7% of

our revenues for our fiscal year ended March 31, 2010.

We also

provide support services to security services firms and police departments

through our support services division. Our support services include

providing back office support services to security services firms and police

departments under administrative service agreements. Support services

generated approximately $0.2 million, or 0.1% of our revenues for our fiscal

year ended March 31, 2010.

Operations

We

conduct our operations through our offices located throughout the United

States. Since March 2008, we have grown from more than 40 offices in

20 states including Arizona, California, Colorado, Connecticut, Delaware,

District of Columbia, Florida, Illinois, Maine, Maryland, Massachusetts, New

Jersey, New York, Oregon, Pennsylvania, Rhode Island, Texas,

Virginia, Washington and West Virginia. As a licensed

watch guard and patrol agency, our security services division provides security

officers to our customers to protect people and property and to prevent the

theft of property. We principally conduct our security services

business by providing security officers and other personnel who are, depending

on the particular requirements of the customer, uniformed or plain-clothed,

armed or unarmed, and who patrol in marked radio cars or stand duty on the

premises at stationary posts such as fire stations, reception areas or video

monitors. Our security officers maintain contact with their

headquarters or supervisors via car radio, hand-held radios or cell

phones. In addition to the more traditional tasks associated with

access control and theft prevention, our security officers respond to emergency

situations and report fires, natural disasters, work accidents and medical

crises to the appropriate authorities. We provide security officer

services to many of our industrial, commercial and residential property

management customers on a 24-hour basis, 365 days per year. For these

customers, security officers are on hand to provide plant security, access

control, personnel security checks and traffic and parking control and to

protect against fire, theft, sabotage and safety hazards. Our

remaining customers include retail establishments, hospitals and governmental

units. The services provided to these customers may require armed as

well as unarmed security officers. We also provide specialized

vehicle patrol and inspection services. During fiscal 2010, our

security services division has been successful in obtaining significant new

security services contracts for a large banking and financial services

organization, a world leader in electronic design automation, a worldwide

technology company, one of the world’s largest banking and financial services

organizations and the world’s largest express transportation

company.

Our

aviation services division provides a variety of uniformed services for domestic

and international air carriers, including aircraft security, access control,

wheelchair escorts, skycaps, baggage handlers and uniformed security officers

for cargo security areas. During fiscal 2010, our aviation services

division has been successful in obtaining several new airline service contracts

at existing locations and a new contract for a leading global provider in

electrical engineering and electronics.

The

nature of our business also subjects us to claims or litigation alleging that we

are liable for damages as a result of the conduct of our employees or

others. We insure against such claims and suits through general

liability policies with third-party insurance companies. Our

insurance coverage limits are currently $7,000,000 per occurrence for

non-aviation related business (with an additional excess umbrella policy of

$10,000,000) and $30,000,000 per occurrence for aviation related

business. We retain the risk for the first $25,000 per occurrence on

the non-aviation related policy which includes airport wheelchair and electric

cart operations, and $5,000 on the aviation related policy except for $25,000

for damage to aircraft and $100,000 for skycap operations.

1

To ensure

that adequate protection requirements have been established prior to commencing

service to a customer, we conduct a comprehensive security assessment of the

customer's site and prepare recommendations for any required changes to existing

security programs or services. Site assessments typically include an

examination and evaluation of perimeter controls, lighting, personnel and

vehicle identification and electronic access control, visitor controls,

electronic alarm reporting systems, safety and emergency procedures, key

controls, radio/surveillance systems and security force manning

levels. While we prepare site assessments and issue recommendations,

the security plan and coverage requirements are ultimately determined by our

customers.

We

frequently establish offices close to our customers and delegate responsibility

and decision-making authority to our local managers. Our managers

each play an important role with us and our customers, as highlighted by their

responsibility for both service quality and assisting with sales and marketing

efforts. We believe that, in most situations, providing a single

individual with responsibility for service quality results in better

supervision, quality control and greater responsiveness to customer

needs.

We

generally render our security services pursuant to a standard form security

services agreement that specifies the personnel and/or equipment to be provided

by us at designated locations and the applicable rates, which typically are

hourly rates per person. Our rates vary depending on base, overtime

and holiday time worked, and the term of engagement. We assume

responsibility for a variety of functions, including scheduling for each

customer site, paying all security officers and providing uniforms, training,

equipment, supervision, fringe benefits and workers' compensation

insurance. These security services agreements also provide our

customers with flexibility by permitting reduction or expansion of the security

force on relatively short notice. We are responsible for preventing

the interruption of security services as a consequence of illness, vacations or

resignations of our security officers. In most cases our customers

also agree not to hire any of our security personnel for at least 180 days after

the termination of the engagement. Each security services agreement

may be terminated by our customer or us, typically with not less than thirty

days prior written notice. We may also terminate an agreement

immediately upon default by the customer in payment of our fees, or if the

customer is involved in a bankruptcy or similar insolvency event.

We are

increasingly dependent on information technology networks and systems to

process, transmit and store electronic information. In particular, we

depend on our information technology infrastructure for electronic

communications among our locations around the country and between our personnel

and our customers and suppliers.

We use

sophisticated electronic security and access control equipment, including modern

computerized watchkey systems and sophisticated video surveillance

equipment. Electronic accountability technology logs officer patrols

and generates user-friendly reports for customer and internal use.

We use

state-of-the-art technology for our operational needs, and to support

efficiency, accuracy, and dependability of our general and administrative needs

and functions. Scheduling, payroll, billing, training, inventory and

e-procurement are integrated through a third party vendor software

platform. This software platform is used to provide financial, labor

and operations management products.

Employee

Recruitment and Training

We

believe that the high quality of our security officers is essential to our

ability to offer effective and reliable services to our customers. We

require all selected applicants for security officer positions to undergo a

detailed pre-employment interview and a background investigation covering such

areas as past employment, education, military service, medical history and,

subject to applicable state laws, criminal and other background

searches. Employees are selected based on a number of criteria,

including physical fitness, maturity, experience, personality, perceived

stability and reliability, among others. We frequently conduct

medical examinations and substance abuse testing on potential

candidates. Our security officers and other personnel supplied to our

customers are our employees, even though they may be stationed regularly at our

customer’s facilities.

We are

committed to ensuring that our staff not only meets all state and federal

requirements for training, but also our own rigorous standards in specialized

areas including: terrorism response, CPR, first-aid, fire safety,

crowd and riot control, media interaction, public relations, crisis management

and emergency situations. Additionally, we provide our employees with

site-specific training to meet the needs of individual industries, facilities

and customers.

We train

accepted applicants in three phases: pre-assignment, on-the-job and

refresher training. Pre-assignment training covers topics such as the

duties and powers of a security officer, report preparation, emergency

procedures, general orders, regulations, grounds for discharge, uniforms,

personal appearance and basic post responsibilities. On-the-job

assignment training covers specific duties as required by the post and job

orders. Ongoing refresher training is provided periodically as

determined by the local area supervisor and manager.

We treat

all employees and applicants for employment without unlawful discrimination as

to race, creed, color, national origin, sex, age, disability, marital status or

sexual orientation in all employment-related decisions.

Significant

Customers

For the

fiscal year ended March 31, 2010, we generated revenues of approximately

$25,177,000 from services we provided to Federal Express (“FedEx”) which

represented approximately 17% of our total revenues during such

period. See “Management's Discussion and Analysis of Financial

Condition and Results of Operations—Liquidity and Capital

Resources—Financing.”

2

Several

of our security and aviation customers filed for protection from creditors under

applicable bankruptcy and similar laws during the past three fiscal

years. The aviation industry continues to face various financial and

other challenges, including the cost of third-party services and fluctuation in

fuel prices. Additional bankruptcy filings by aviation and

non-aviation customers could have a material adverse impact on our liquidity,

results of operations and financial condition.

Competition

The

security services business is labor intensive and substantially affected by the

cost of labor and by the availability of qualified personnel. Our

ability to provide the required number of competent, trained personnel in a

timely manner is critical to retain our business, contain payroll costs and

avoid undue insurance exposure. To satisfy these requirements, we

need to successfully manage human resources, manpower planning, quality control,

risk management, general and financial management and sales and

marketing.

Although

the majority of our contracts may be terminated by us or by our customers at our

or their discretion, we believe that we can minimize customer attrition by

adhering to basic performance standards in meeting essential customer

requirements. While all security service companies experience

customer attrition, we have historically been successful in renegotiating

existing contracts.

Competition

in the security service business is intense. We believe that a

customer’s selection of a company to provide security services is based

primarily on price, quality of services provided, scope of services performed,

name recognition, recruiting, training and the extent and quality of security

officer supervision. As we have expanded our operations, we have had

to compete more frequently against larger national companies, such as Securitas

North America, the Wackenhut Corporation, AlliedBarton Security and Guardsmark,

LLC, all which have substantially greater financial and other resources,

personnel and facilities than us. These competitors also offer a

range of security and investigative services that are at least as extensive as,

and directly competitive with, the services that we offer. In

addition, we compete with many regional and local organizations that offer

substantially all of the services that we provide. Although our

management believes that, particularly with respect to certain of our markets,

we enjoy a favorable competitive position because of our emphasis on customer

service, supervision and training and are able to compete on the basis of the

quality of our service, personal relationships with customers and reputation, we

cannot assure you that we will be able to continue to effectively compete with

other companies, particularly those having greater financial and other

resources, personnel and facilities.

Government

Regulation

We are

subject to local and state firearm and occupational licensing laws that apply to

security officers and private investigators. In addition, many states

have laws requiring training and registration of security officers, regulating

the use of badges and uniforms, prescribing the use of identification cards or

badges, and imposing minimum bond, surety or insurance standards. We

are subject to penalties and fines for licensing irregularities or the

misconduct of our security officers. However, our management believes

we are in material compliance with all applicable laws and

regulations.

Employees

Our

business is labor intensive and is consequently affected by the availability of

qualified personnel and the cost of labor. Although the security

services industry is characterized by high turnover, we have not experienced any

material difficulty in hiring qualified security officers. In some

cases, when labor has been in short supply, we have been required to pay higher

wages and/or incur overtime charges. We have approximately 5,200

employees, the majority of whom are hourly service workers, and approximately

220 of whom serve as managers, administrative employees and

executives.

Approximately

70% of our employees do not belong to a labor union. The balance of

our employees are members of labor unions including, in particular, a number of

employees based in our New York City security services office and at our airport

offices at John F. Kennedy, La Guardia and Los Angeles airports. Our

unionized employees work under collective bargaining agreements with the

following unions: Allied International Union, Allied Services

Division of the Transportation Communications International Union and Special

& Superior Officers Benevolent Association. Many of our

competitor’s employees in Los Angeles and New York City are also

unionized. We have experienced no work stoppage attributable to labor

disputes. We believe that our relations with our employees are

satisfactory. The security officers and other personnel that we

provide to our customers are Company employees, even though they may be

stationed regularly at our customer's facilities.

Service

Marks

We

believe that we own the service marks “Command Security Corporation,” “CSC” and

“CSC Plus” design for security officer, detective, private investigation

services and security consulting services.

We also

believe that we own the trademarks “Smartwheel” and “Smart Tracker” for the

computer programs we use in dispatching and tracking small vehicles, such as

carts and wheelchairs at transportation terminals. The “Smartwheel”

trademark was acquired as part our acquisition of United Security Group,

Inc. We also believe that we own the service marks “STAIRS” and

“Smart Guard.”

3

ITEM

1A. RISK FACTORS.

In

addition to the other information set forth in this Annual Report on Form 10-K,

you should carefully consider the following factors that could materially and

adversely affect our business, financial condition or future operating

results. The risks described below are not the only risks facing our

Company. Additional risks and uncertainties not currently known to us

or that we currently deem to be immaterial also may materially adversely affect

our business, financial condition or operating results.

Airline

Industry Concerns

Several

of our aviation customers filed for protection from their creditors under

applicable bankruptcy and similar laws during our past three fiscal

years. The aviation industry continues to face various financial and

other challenges, including the cost of security and fluctuating fuel

prices. Additional bankruptcy filings by aviation and non-aviation

customers could have a material adverse impact on our liquidity, results of

operations and financial condition.

Acquisitions

Part of

our growth strategy involves acquiring other quality security services

companies. Our acquisition strategy entails numerous

risks. The pursuit of acquisition candidates is expensive and may not

be successful. Our ability to complete future acquisitions will

depend on our ability to identify suitable acquisition candidates, negotiate

acceptable terms for their acquisition and, if necessary, finance those

acquisitions, in each case, before any attractive candidates are purchased by

other parties, some of whom have substantially greater financial and other

resources than we have. Whether or not any particular acquisition is

successfully completed, each of these activities is expensive and time consuming

and would likely require our management to spend considerable time and effort to

complete, which would detract from our management’s ability to run our current

business. Although we may spend considerable funds and efforts to

pursue acquisitions, we may not be able to complete them. Further,

our ability to grow through acquisitions will depend in part on whether we can

identify suitable acquisition candidates upon attractive terms, including

price.

Acquisitions

could result in the occurrence of one or more of the following

events:

|

|

·

|

dilutive

issuances of equity securities;

|

|

|

·

|

incurrence

of additional debt and contingent

liabilities;

|

|

|

·

|

increased

amortization expenses related to intangible

assets;

|

|

|

·

|

difficulties

in the assimilation of the operations, technologies, services and products

of the acquired companies; and

|

|

|

·

|

diversion

of management’s attention from our other business

activities.

|

We

currently have no commitments or agreements with respect to any

acquisition. Further, we cannot assure you that we will be able to

complete additional acquisitions that we believe are necessary to complement our

growth strategy on acceptable terms, or at all. Further, if we do not

successfully integrate the operations of any companies that we have acquired or

subsequently acquire, we may not achieve the potential benefits of such

acquisitions.

Additional

Financing

We

believe that our existing funds, cash generated from operations, and existing

sources of and access to financing are adequate to satisfy our working capital,

capital expenditures and debt service requirements for the foreseeable

future. However, we cannot assure you that this will be the case, and

we may be required to obtain additional financing to maintain and expand our

existing operations through the sale of our securities, an increase in our

credit facilities or otherwise. The failure by us to obtain such

financing, if needed, would have a material adverse effect upon our business,

financial condition and results of operations.

Credit

and Security Agreement

Our

Credit and Security Agreement imposes operating and financial restrictions on

us, which may prevent us from capitalizing on business opportunities and taking

certain corporate actions. These restrictions limit our ability

to:

|

|

·

|

guarantee

additional indebtedness;

|

|

|

·

|

pay

dividends and make distributions;

|

|

|

·

|

make

certain investments;

|

|

|

·

|

repurchase

stock;

|

|

|

·

|

incur

liens;

|

|

|

·

|

transfer

or sell assets;

|

|

|

·

|

enter

into sale and leaseback

transactions;

|

|

|

·

|

merge

or consolidate; and

|

|

|

·

|

engage

in a materially different line of

business.

|

4

These

covenants may adversely affect our ability to finance future operations or

capital needs, pursue available business opportunities or take certain corporate

actions.

Competition

Our

assumptions regarding projected results depend largely upon our ability to

retain substantially all of our current customers and obtain new

customers. Retention is affected by several factors including, but

not limited to, regulatory limitations, the quality of the services that we

provide, the quality and pricing of comparable services offered by competitors

and continuity of our management and non-management personnel. There

are several major national competitors with substantially greater financial and

other resources than we have and that, therefore, have the ability to provide

more attractive service, cost and compensation incentives to customers and

employees than we are able to provide. Our ability to gain or

maintain sales, gross margins and/or employees may be limited as a result of

actions by our competitors.

Service

Contracts

Our

largest expenses are for payroll and related taxes and employee

benefits. Most of our service contracts provide for fixed hourly

billing rates. Competitive pressures in the security and aviation

services industries may prevent us from increasing our hourly billing rates on

contract anniversary or renewal dates. Our profitability will be

adversely affected if we are compelled to increase the wages, salaries and

related benefits of our employees in amounts that exceed the amount that we can

pass on to our customers through increased billing rates charged under our

service contracts.

In many

cases, our security and aviation services contracts require us to indemnify our

customers or may otherwise subject us to additional liability for events

occurring on customer premises. While we maintain insurance programs

that we believe provide appropriate coverage for certain liability risks,

including personal injury, death and property damage, the laws of many states

limit or prohibit insurance coverage for punitive damages arising from willful

or grossly negligent conduct. Therefore, insurance may not be

adequate to cover all potential claims or damages. If a plaintiff

brings a successful claim against us for punitive damages in excess of our

insurance coverage, then we could incur substantial liabilities that would have

a material adverse affect on our business, financial condition and results of

operations.

Staffing

Our

business involves the labor-intensive delivery of security and aviation

services. We derive our revenues primarily from services rendered by

our hourly employees. Our future performance depends in large part

upon our ability to attract, train, motivate and retain our skilled operational

and administrative staff. The loss of the services of, or the failure

to recruit, the required complement of operational and administrative staff

would have a material adverse effect on our business, financial condition and

results of operations, including our ability to secure and complete security

service contracts. Additionally, if we do not successfully manage our

existing operational and administrative staff, we may not be able to achieve the

anticipated gross margins, service quality, overtime levels and other

performance measures that are important to our business, financial condition and

results of operations.

Changes

in Accounting Standards and Taxation Requirements

New

accounting standards or pronouncements that become applicable to us and our

financial statements from time to time, and changes in the interpretation of

existing standards and pronouncements, could have a significant effect on our

reported results for the affected periods. We are also subject to

income and various other taxes in the numerous jurisdictions where we generate

revenues. Increases in income or other tax rates could reduce our

after-tax results from affected jurisdictions in which we operate.

Collective

Bargaining Agreements and Organized Labor Action

Many of

our employees at our operating locations are covered by collective bargaining

agreements. If we are unable to renew such agreements on satisfactory

terms, our labor costs could increase, which would affect our gross

margins.

The

security industry has been the subject of campaigns to increase the number of

unionized employees. In addition, strikes or work stoppages at our

locations could impair our ability to provide required services to our

customers, which would reduce our revenues and expose us to customer

claims. Although we believe that our relations with our employees are

satisfactory, we cannot assure you that organized labor action at one or more of

our operating locations will not occur, or that any such activities, or any

other labor difficulties at our operating locations, would not materially affect

our business, financial condition and results of operations.

Cost

Management

Our

ability to realize expectations will be largely dependent upon management and

our ability to maintain or increase gross margins, which in turn will be

determined in large part by management's ability to control our

expenses. However, to a significant extent, certain costs are not

within the control of management, and margins may be adversely affected by a

number of items, including litigation expenses, fees incurred in connection with

extraordinary business transactions, inflation, labor unrest, increased payroll

and related costs. Our business, financial condition and results of operations

will be adversely affected if the costs associated with these items are greater

than we anticipate.

5

Collection

of Accounts Receivable

The

aviation industry in general poses a high degree of customer credit

risk. Any default by one or more of our significant customers due to

bankruptcy or otherwise could have a material adverse impact on our liquidity,

results of operations and financial condition.

Loss

of Large Customers

Our

success depends in part upon retaining our large security and aviation services

customers. In general, security services companies such as ours face

the risk of losing customers as a result of the expiration or termination of a

contract, or as a result of a merger or acquisition or business failure

involving our large customers, or the selection by such customers of another

provider of security services. We generate a significant portion of

our revenues from large airline and security services customers, some of which

are experiencing substantial financial difficulties. We cannot assure

you that we will be able to retain all or a substantial portion of our long-term

or significant customers or develop relationships with new significant customers

in the future.

Loss

of Key Management Personnel

Our

success depends to a significant extent upon the talents and efforts of our key

management personnel, several of whom have been with our company or have worked

in our industry for decades. We have programs in place that have been

designed to motivate, reward and retain such employees, including cash bonus and

equity incentive plans. The loss or unavailability of any such

management personnel, due to retirement, resignation or otherwise could have a

material adverse effect on our business, financial condition and results of

operations if we are unable to attract and retain highly qualified replacement

personnel on a timely basis, or at all.

Concentration

of Stock Ownership

Although

none of our directors and officers has any agreement relating to the manner in

which they will vote their shares of our common stock, such parties together own

shares representing approximately 35% of the combined voting power of our

outstanding common stock. The concentration of ownership among these

shareholders could give them the power to influence the outcome of substantially

all matters subject to a vote of our shareholders, including mergers,

consolidations and the sale of all or substantially all of our

assets. Such decisions may conflict with the interests of our other

shareholders.

Stock

Price Volatility

The stock

markets have experienced price and volume fluctuations that have affected and

continue to affect the market prices of equity securities of many

companies. These fluctuations often have been unrelated or

disproportionate to the operating performance of those companies. The

market price of our common stock may also fluctuate as a result of variations in

our operating results. Due to the nature of our business, the market

price of the common stock may fall in response to a number of factors, some of

which are beyond our control, including: announcements of competitive

developments by others; changes in estimates of our financial performance or

changes in recommendations by securities analysts; a loss of a major customer;

additions or departures of key management or other personnel; future sale of our

common or preferred stock; acquisitions or strategic alliances by us or our

competitors; our historical and anticipated operating results; quarterly

fluctuations in our financial and operating results; changes in market

valuations of other companies that operate in our business markets or industry

sector; and general market and economic conditions.

Information

Systems/Technology

We are

increasingly dependent on information technology networks and systems, including

the Internet, to process, transmit and store electronic

information. In particular, we depend on our information technology

infrastructure for electronic communications among our locations around the

country and between our personnel and our customers and

suppliers. Security breaches of this infrastructure can create

disruptions, shutdowns or unauthorized disclosure of confidential

information. If we are unable to prevent such breaches, our

operations could be disrupted or we may suffer financial damage or loss because

of lost or misappropriated information.

Changes

in technologies that provide alternatives to security officer services or that

decrease the number of security officers required to effectively perform their

services may decrease our customers’ demand for our security officer

services. In addition, if such technologies become available

generally for use in the industry, these technologies may be proprietary in

nature and not be available for use by us in servicing our

customers. Even if these technologies are available for use by us, we

may not be able to successfully integrate such technologies into our business or

we may be less successful in doing so than our competitors or new entrants in

the industry. A decrease in the demand for our security officer

services or our inability to effectively utilize such technologies may adversely

affect our business, financial condition and results of

operations.

6

Regulation

We are

subject to a large number of city, county and state occupational licensing laws

and regulations that apply to security officers. Any liability we may

have from our failure to comply with these regulations may materially and

adversely affect our business by restricting our operations and subjecting us to

potential penalties. If the current regulation and federalization of

pre-board screening and documentation verification services provided by us is

expanded into other areas such as general security and baggage handling at

aviation facilities, our business, financial condition and results of operations

could be materially adversely affected. In addition, our current and

future operations may be subject to additional regulation as a result of, among

other factors, new statutes and regulations and changes in the manner in which

existing statutes and regulations are or may be interpreted.

Economic

Downturn

During

economic declines, some decisions to implement security programs and install

systems may be deferred or cancelled. In other cases, customers may

increase their purchases of security systems because they fear more inventory

shrinkage and theft will occur due to increasing economic need. We

are not able to accurately predict to what extent an economic slowdown will

decrease the demand for our services. If demand for our services

decreases, then our revenues will decline and the value of your investment in

our company will be adversely affected.

Catastrophic

Events

We are

exposed to potential claims for catastrophic events, such as acts of terrorism,

or based upon allegations that we failed to perform our services in accordance

with contractual or industry standards. Our insurance coverage limits

are currently $7,000,000 per occurrence for non-aviation related business (with

an additional excess umbrella policy of $10,000,000) and $30,000,000 per

occurrence for aviation related business. We retain the risk for the

first $25,000 per occurrence on the non-aviation related policy that includes

airport wheelchair and electric cart operations and $5,000 on the aviation

related policy (except $25,000 for damage to aircraft and $100,000 for skycap

operations). The Terrorism Risk Insurance Act of 2002 established a

program within the United States Department of the Treasury, under which the

federal government and the insurance industry, share the risk of loss from

future “acts of terrorism,” as defined in such Act. We do not

currently maintain additional insurance coverage for losses arising from “acts

of terrorism.” In addition, terrorist attacks could have a material

impact on us by increasing our insurance premium costs or making adequate

insurance coverage unavailable.

ITEM

1B. UNRESOLVED STAFF COMMENTS.

None.

ITEM

2. PROPERTIES.

As of

March 31, 2010, we did not own any real property. We occupy executive

offices at Route 55, Lexington Park, Lagrangeville, New York, consisting of

approximately 6,600 square feet with a base annual rental of $105,600 under a

five-year lease expiring September 30, 2010. We are currently in

discussions with the landlord to extend the lease term on our executive

offices. We also lease office space at the following

locations:

|

Location

|

|

|

|

|

668

N. 44th

Street

|

|||

|

#300

|

|||

|

Phoenix,

AZ

|

|||

|

48521

Warm Springs Boulevard

|

|||

|

Suite

301-302

|

|||

|

Fremont,

CA

|

|||

|

8939

S. Sepulveda Boulevard

|

|||

|

Suites

201 & 208

|

|||

|

Los

Angeles, CA

|

|||

|

2194

Edison Avenue

|

|||

|

Suite

N, I & D

|

|||

|

San

Leandro, CA

|

7

|

2230

S. Fairview Avenue

|

|

|

|

|

Santa

Ana, CA

|

|||

|

3180

University Avenue

|

|||

|

Suites

100

|

|||

|

San

Diego, CA

|

|||

|

Norman

Y. Mineta San Jose Int’l Airport

|

|||

|

1661

Airport Boulevard

|

|||

|

San

Jose, CA

|

|||

|

San

Jose Int'l. Airport

|

|||

|

1400

Coleman Avenue

|

|||

|

Suites

D24 & D25

|

|||

|

Santa

Clara, CA

|

|||

|

100

N. Barrancha Avenue

|

|||

|

#900

|

|||

|

West

Covina, CA

|

|||

|

40

Richards Avenue

|

|||

|

3rd

Floor

|

|||

|

Norwalk,

CT

|

|||

|

100

Wells Street

|

|||

|

#2AB

|

|||

|

Hartford,

CT

|

|||

|

Suite

208 Wilson Building

|

|||

|

3511

Silverside Road

|

|||

|

Concord

Plaza

|

|||

|

Wilmington,

DE

|

|||

|

3333

South Congress Avenue

|

|||

|

Delray

Beach, FL

|

|||

|

800

Virginia Avenue

|

|||

|

Suite

53

|

|||

|

Ft.

Pierce, FL

|

|||

|

5775

Blue Lagoon Drive

|

|||

|

Suite

310

|

|||

|

Miami,

FL

|

|||

|

9730

South Western Avenue

|

|||

|

Evergreen

Plaza Shopping Center

|

|||

|

Suite

237

|

|||

|

Evergreen

Park, IL

|

8

|

21

Cummings Park

|

|

|

|

|

Suite

224

|

|||

|

Woburn,

MA

|

|||

|

1601

& 1605 Main Street

|

|||

|

Springfield,

MA

|

|||

|

1006

West Street

|

|||

|

First

Floor

|

|||

|

Laurel,

MD

|

|||

|

780

Elkridge Landing Road

|

|||

|

Suite

220

|

|||

|

Linthicum

Heights, MD

|

|||

|

Portland

International Airport

|

|||

|

1001

Westbrook Street

|

|||

|

Portland,

ME

|

|||

|

310

Morris Avenue

|

|||

|

Elizabeth,

NJ

|

|||

|

1767

Morris Avenue

|

|||

|

Suite

101

|

|||

|

First

Floor

|

|||

|

Union,

NJ

|

|||

|

1280

Route 46

|

|||

|

3rd

Floor

|

|||

|

Parsippany,

NJ

|

|||

|

2204

Morris Avenue

|

|||

|

Suite

302, 3rd

Floor

|

|||

|

Union,

NJ

|

|||

|

52

Oswego Street

|

|||

|

Baldwinsville,

NY

|

|||

|

2144

Doubleday Avenue

|

|||

|

Ballston

Spa, NY

|

|||

|

1458

Main Street

|

|||

|

Buffalo,

NY

|

9

|

LaGuardia

International Airport

|

|

|

|

|

United

Hangar #2, Rooms 328 & 329

|

|||

|

Flushing,

NY

|

|||

|

JFK

International Airport

|

|||

|

175-01

Rockaway Boulevard

|

|||

|

Jamaica,

NY

|

|||

|

17

Battery Place

|

|||

|

Suite

223

|

|||

|

New

York, NY

|

|||

|

720

Fifth Avenue

|

|||

|

10th

Floor

|

|||

|

New

York, NY

|

|||

|

Two

Gannett Drive

|

|||

|

Suite

208

|

|||

|

White

Plains, NY

|

|||

|

265

Sunrise Highway

|

|||

|

Suites

41 & 44

|

|||

|

Rockville

Centre, NY

|

|||

|

10121

SE Sunnyside Road

|

|||

|

Suite

300

|

|||

|

Clackamas,

OR

|

|||

|

29

Bala Avenue

|

|||

|

Suite

118

|

|||

|

Bala

Cynwyd, PA

|

|||

|

2

International Plaza

|

|||

|

Suite

242

|

|||

|

Philadelphia,

PA

|

|||

|

Pittsburgh

International Airport

|

|||

|

1000

Airport Boulevard

|

|||

|

Ticketing

Level of the Landside Terminal Building

|

|||

|

Pittsburgh,

PA

|

|||

|

4101

Chain Bridge Road

|

|||

|

Fairfax,

VA

|

|||

|

669

Elmwood Avenue

|

|||

|

Suite

B-4

|

|||

|

Providence,

RI

|

10

|

1250 Capital of Texas Highway

South

|

|

|

|

|

Building

III, Suite 400

|

|||

|

Austin,

TX

|

|||

|

Seattle-Tacoma

Int’l. Airport

|

|||

|

17801

International Boulevard

|

|||

|

Main

Terminal Building

|

|||

|

Room

MT3469B

|

|||

|

Seattle,

WA

|

We

believe that our existing properties are in good condition and are suitable for

the conduct of our business.

Except as

described below, we are not a party to any material pending legal proceedings,

other than ordinary routine litigation incidental to our business.

The

nature of our business subjects us to claims or litigation alleging that we are

liable for damages as a result of the conduct of our employees or

others. Except for such litigation incidental to our business and

other claims or actions that are not material, there are no pending legal

proceedings to which we are a party or to which any of our property is

subject.

The

nature of our business is such that there is a significant volume of routine

claims and lawsuits against us, the vast majority of which have never led to the

award of substantial damages. We maintain general liability and

workers’ compensation insurance coverage that we believe is appropriate to the

relevant level of risk and potential liability. Some of the claims

brought against us could result in significant payments; however, the exposure

to us for general liability claims is limited to the first $25,000 per

occurrence on the non-aviation and airport wheelchair and electric cart

operations related claims and $5,000 per occurrence on the aviation related

claims, except $25,000 for damage to aircraft and $100,000 for skycap operations

as well as any amount in excess of the maximum coverage provided by such

policies. Any punitive damage award would not be covered by our

general liability insurance policy. Also, the premiums we pay under

our insurance policies may be adversely affected by an unfavorable claims

history.

No

matters were submitted to a vote of our security holders during the last quarter

of our fiscal year ended March 31, 2010.

11

Our

common stock was quoted on the OTC Bulletin Board Service until June 7, 2007

under the symbol “CMMD.OB.” On June 8, 2007, our common stock began

trading on the American Stock Exchange (the “AMEX”) under the ticker symbol

“MOC.” On October 1, 2008, NYSE Euronext completed its acquisition of

the AMEX, where our common shares were traded. As a result of this

acquisition, our common shares are now traded on the NYSE Amex which is an

exchange-regulated market. The NYSE Amex is regulated by

Euronext. Shares of our common stock now trade on the NYSE Amex under

the same and previous trading symbol “MOC.”

The

following table sets forth, for the calendar periods indicated, the high and low

sales price for our common stock as reflected on the NYSE Amex for each full

quarterly period within the two most recent fiscal years.

|

Last Sales Price Period (1)

|

Common stock market price

|

|||||||

|

High

|

Low

|

|||||||

|

First

Quarter

|

$ | 3.45 | $ | 2.69 | ||||

|

Second

Quarter

|

3.33 | 2.65 | ||||||

|

Third

Quarter

|

2.73 | 1.89 | ||||||

|

Fourth

Quarter

|

2.75 | 2.37 | ||||||

|

2009

|

||||||||

|

First

Quarter

|

$ | 4.02 | $ | 2.60 | ||||

|

Second

Quarter

|

3.55 | 2.80 | ||||||

|

Third

Quarter

|

3.35 | 2.53 | ||||||

|

Fourth

Quarter

|

3.64 | 2.76 | ||||||

(1)

Reflects fiscal years ended March 31, 2010 and 2009 as indicated.

The above

quotations do not include retail mark-ups, markdowns or commissions and

represent prices between dealers and may not represent actual transactions. The

past performance of our common stock is not necessarily indicative of the price

at which it may trade in the future.

As of

June 18, 2010 there were approximately 850 holders of our common

stock.

To date,

we have neither declared nor paid any cash dividends on shares of our common

stock. Payment of dividends on our common stock, if any, will be

within the discretion of our Board of Directors and will depend, among other

factors, on the approval of our principal lender, our earnings and capital

requirements and our operating and financial condition. At present,

our anticipated capital requirements and growth plans are such that we intend to

follow a policy of retaining earnings, if any, to finance our business

operations and any growth in our business.

12

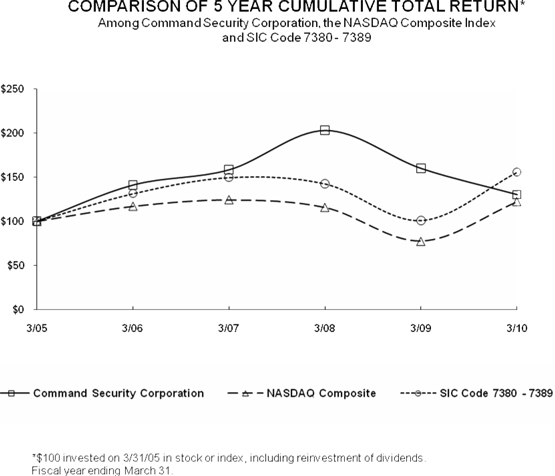

The graph

below compares the cumulative total shareholder return on our common shares with

the cumulative total return of (1) the Nasdaq Stock Market Index (U.S.) (the

“Nasdaq Index”) and (2) an index of publicly traded companies with a Standard

Industrial Classification Code (“SIC Code”) of between 7380 and 7389 (the “SIC

Code Index”). This graph assumes that $100 was invested in each of

(A) shares of our common stock, (B) the Nasdaq Index and (C) the SIC Code Index

on March 31, 2003 and reflects the return through March 31, 2010 and assumes the

reinvestment of dividends, if any. The comparisons in the graph below

are based on historical data and are not indicative of, or intended to forecast,

possible future performance of our Common Stock.

THE

INFORMATION CONTAINED IN THE STOCK PERFORMANCE GRAPH SHALL NOT BE DEEMED TO BE

“SOLICITING MATERIAL” OR TO BE FILED WITH THE SEC, NOR SHALL SUCH INFORMATION BE

INCORPORATED BY REFERENCE INTO ANY FUTURE FILING UNDER THE SECURITIES ACT OR THE

EXCHANGE ACT, EXCEPT TO THE EXTENT WE SPECIFICALLY INCORPORATE IT BY REFERENCE

INTO SUCH FILING.

13

The

financial data included in the table below has been derived from our financial

statements as of and for the fiscal years ended March 31, 2010, 2009, 2008, 2007

and 2006, which have been audited by independent certified public

accountants. This information should be read in conjunction with

“Item 7. Management’s Discussion and Analysis of Financial Condition

and Results of Operations” and with our consolidated financial statements and

related notes included in this Annual Report on

Form 10-K. The dollar amounts presented below in this Item 6 are in

thousands of dollars, except for per share data.

|

Statements of Operations Data

Years Ended March 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Revenues

|

145,695 | 130,813 | 119,404 | 98,823 | 85,209 | |||||||||||||||

|

Gross

profit

|

20,482 | 18,664 | 16,242 | 13,665 | 11,420 | |||||||||||||||

|

Operating

income

|

3,704 | 3,008 | 2,969 | 1,135 | 8 | |||||||||||||||

|

Net

income (loss)

|

1,632 | 1,282 | 2,474 | 1,240 | (100 | ) | ||||||||||||||

|

Income

(loss) per common share

|

.15 | .12 | .23 | .12 | (.01 | ) | ||||||||||||||

|

Weighted

average number of common shares

|

10,848,375 | 10,772,613 | 10,733,797 | 10,137,970 | 8,834,952 | |||||||||||||||

|

Balance Sheet Data at March 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Working

capital

|

9,423 | 7,106 | 6,097 | 6,514 | 6,838 | |||||||||||||||

|

Total

assets

|

36,715 | 34,265 | 32,786 | 25,330 | 18,113 | |||||||||||||||

|

Short-term

debt (1)

|

11,112 | 11,071 | 8,775 | 8,751 | 3,475 | |||||||||||||||

|

Long-term

debt (2)

|

43 | 109 | 18 | 16 | 57 | |||||||||||||||

|

Stockholders'

equity

|

16,783 | 14,722 | 13,360 | 9,104 | 7,625 | |||||||||||||||

|

(1)

|

Our

short-term debt includes the current maturities of long-term debt,

obligations under capital leases and short term borrowings. See Notes 7,

and 15, “Short-Term Borrowings” and “Commitments”, respectively, to the

financial statements for further

discussion.

|

|

(2)

|

Our

long-term debt includes the long-term portion of obligations under capital

leases.

|

ITEM

7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS.

This

Management's Discussion and Analysis of Financial Condition and Results of

Operations should be read in conjunction with our consolidated financial

statements and related notes thereto contained in this Annual

Report. In this discussion, the words "Company", "we", "our" and "us"

refer to Command Security Corporation.

FORWARD-

LOOKING STATEMENTS

This

section, Management's Discussion and Analysis of Financial Condition and Results

of Operations, other sections of this Annual Report on Form 10-K and other

reports and verbal statements made by our representatives from time to time may

contain forward-looking statements that are based on our assumptions,

expectations and projections about us and the security

industry. These include statements regarding our expectations about

revenues, our liquidity, or expenses and our continued growth, among others. You

can identify these statements by forward-looking words such as “may,” “expect,”

“anticipate,” “contemplate,” “believe,” “estimate,” “intends,” and “continue” or

similar words. You should read statements that contain these words

carefully because they:

|

|

·

|

discuss

future expectations;

|

|

|

·

|

contain

projections of future results of operations or financial condition;

and

|

|

|

·

|

state

other “forward-looking”

information.

|

Such

forward-looking statements by their nature involve a degree of risk and

uncertainty. We caution you to not to place undue reliance on these

forward-looking statements, which speak only as of the date of this Annual

Report. We further caution you that a variety of factors, including

but not limited to the factors described under Item 1A, “Risk Factors” and the

following, could cause business conditions and our results to differ materially

from what is contained in forward-looking statements:

|

|

·

|

changes

in general economic conditions in the United States and

abroad;

|

|

|

·

|

changes

in the financial condition of our

customers;

|

|

|

·

|

legislation

or regulatory environments, requirements or changes adversely affecting

our business or the businesses in which our customers are

engaged;

|

|

|

·

|

cancellations

and non-renewals of existing

contracts;

|

|

|

·

|

changes

in our estimates of costs;

|

14

|

|

·

|

war

and/or terrorist attacks on facilities where services are or may be

provided;

|

|

|

·

|

outcomes

of pending and future litigation;

|

|

|

·

|

increasing

competition by other companies;

|

|

|

·

|

changes

in interest rates;

|

|

|

·

|

compliance

with our loan covenants;

|

|

|

·

|

changing

interpretations of GAAP;

|

|

|

·

|

the

general volatility of the market price of our

securities;

|

|

|

·

|

the

availability of qualified

personnel;

|

|

|

·

|

recoverability

of claims against our customers and others by us and claims by third

parties against us; and

|

|

|

·

|

changes

in estimates used in our critical accounting

policies.

|

Other

factors and assumptions not identified above were also involved in the formation

of these forward-looking statements and the failure of such other assumptions to

be realized, as well as other factors, may also cause actual results to differ

materially from those projected. Most of these factors are difficult

to predict accurately and are generally beyond our control. You

should consider the areas of risk described above in connection with any

forward-looking statements that may be made by us.

All

forward-looking statements included herein attributable to us or any person

acting on our behalf are expressly qualified in their entirety by the cautionary

statements contained or referred to in this section. We have based

the forward-looking statements included in this Annual Report on information

available to us on the date of this annual report and, except to the extent

required by applicable laws and regulations, we undertake no obligation to

update these forward-looking statements to reflect events or circumstances after

the date of this annual report or to reflect the occurrence of unanticipated

events. Although we undertake no obligation to revise or update any

forward-looking statements, whether as a result of new information, future

events or otherwise, you are advised to consult any additional disclosures that

we make directly to you or through reports that we in the future may file with

the Securities and Exchange Commission, including annual reports on Form 10-K,

quarterly reports on Form 10-Q and current reports on Form 8-K. Our

actual results could differ materially from those expressed or implied by the

forward-looking statements as a result of various factors including, but not

limited to, those presented under “Risk Factors” included in Item 1A and

elsewhere in this Annual Report.

CRITICAL

ACCOUNTING POLICIES AND ESTIMATES.

The

preparation of financial statements in conformity with accounting principles

generally accepted in the United States requires us to make estimates and

judgments that affect the reported amounts of assets, liabilities, revenues,

expenses and related disclosure of contingent assets and

liabilities. We believe the following critical accounting policies

affect our more significant judgments and estimates used in the preparation of

our financial statements. Actual results may differ from these

estimates under different assumptions and conditions.

Principles

of Consolidation

The

accompanying consolidated financial statements include our accounts and accounts

of our wholly-owned domestic subsidiaries. As of December 29, 2009,

Strategic Security Services, Inc., Rodgers Police Patrol, Inc. and Command

Security Services, Inc., the Company’s three wholly-owned subsidiaries, were

merged with and into Command Security Corporation. All significant

intercompany accounts and transactions have been eliminated in our consolidated

financial statements.

Use

of Estimates

The

preparation of financial statements in conformity with accounting principles

generally accepted in the United States requires management to make estimates

and assumptions that affect the reported amounts of assets and liabilities at

the date of the financial statements, the disclosure of contingent assets and

liabilities, and the reported amounts of revenues and expenses during the

reporting period. The estimates that we make include allowances for

doubtful accounts, depreciation and amortization, income tax assets and

insurance reserves. Estimates are based on historical experience,

where applicable or other assumptions that management believes are reasonable

under the circumstances. Due to the inherent uncertainty involved in

making estimates, actual results may differ from those estimates under different

assumptions or conditions.

Revenue

Recognition

We record

revenues as services are provided to our customers. Revenues consist

primarily of aviation and security services, which are typically billed at

hourly rates. These rates may vary depending on base, overtime and

holiday time worked. Revenue for administrative services provided to

other security companies are calculated as a percentage of the administrative

service customer's revenue and are recognized when billings for the related

security services are generated. Revenue is reported net of

applicable taxes.

Trade

Receivables

We

periodically evaluate the requirement for providing for billing adjustments

and/or credit losses on our accounts receivable. We provide for

billing adjustments where management determines that there is a likelihood of a

significant adjustment for disputed billings. Criteria used by

management to evaluate the adequacy of the allowance for doubtful accounts

include, among others, the creditworthiness of the customer, current trends,

prior payment performance, the age of the receivables and our overall historical

loss experience. Individual accounts are charged off against the

allowance as management deems them as uncollectible.

15

Intangible

Assets

Intangible

assets are stated at cost and consist primarily of customer lists and borrowing

costs that are being amortized on a straight-line basis over three to ten years

and goodwill which is reviewed annually for impairment. The life

assigned to customer lists acquired is based on management’s estimate of the

attrition rate. The attrition rate is estimated based on historical

contract longevity and management’s operating experience. We test for

impairment annually or when events and circumstances warrant such a review, if

sooner. Any potential impairment is evaluated based on anticipated

undiscounted future cash flows and actual customer attrition in accordance with

FASB ASC 360, Property, Plant,

and Equipment.

Insurance

Reserves

General

liability estimated accrued liabilities are calculated on an undiscounted basis

based on actual claim data and estimates of incurred but not reported claims

developed utilizing historical claim trends. Projected settlements

and incurred but not reported claims are estimated based on pending claims,

historical trends and data.

Workers’

compensation annual premiums are based on the incurred losses as determined at

the end of the coverage period, subject to minimum and maximum

premium. Estimated accrued liabilities are based on our historical

loss experience and the ratio of claims paid to our historical payout

profiles.

Income

Taxes

Income

taxes are based on income (loss) for financial reporting purposes and reflect a

current tax liability (asset) for the estimated taxes payable (recoverable) in

the current year tax return and changes in deferred taxes. Deferred

tax assets or liabilities are determined based on differences between financial

reporting and tax bases of assets and liabilities and are measured using enacted

tax laws and rates. A valuation allowance is provided on deferred tax

assets if it is determined that it is more likely than not that the asset will

not be realized. In the event that interest and/or penalties are

assessed in connection with our tax filings, interest will be recorded as

interest expense and penalties as selling, general and administrative

expense.

Stock Based

Compensation

FASB ASC

718, Stock

Compensation, requires all share-based payments to employees, including

grants of employee stock options, to be recognized in the financial statements

based on their fair values at grant date and the recognition of the related

expense over the period in which the share-based compensation

vests. We were required to adopt the provisions of FASB ASC 718

effective July 1, 2005 and use the modified-prospective transition

method. Under the modified-prospective transition method, we

recognize compensation expense in our financial statements issued subsequent to

the date of adoption for all share-based payments granted, modified or settled

after July 1, 2005. The adoption of FASB ASC 718 resulted in non-cash

charges of $140,528, $172,097 and $239,900 for stock based compensation for the

years ended March 31, 2010, 2009 and 2008, respectively.

OVERVIEW

We

principally provide uniformed security officers and aviation services to

commercial, residential, financial, industrial, aviation and governmental

customers through more than 40 Company-offices in 20 states throughout the

United States. In conjunction with providing these services, we

assume responsibility for a variety of functions, including recruiting, hiring,

training and supervising all operating personnel as well as paying such

personnel and providing them with uniforms, fringe benefits and workers’

compensation insurance.

Our

customer-focused mission is to provide the best personalized supervision and

management attention necessary to deliver timely and efficient security

solutions so that our customers can operate in safe environments without

disruption or loss. Technology underpins our efficiency, accuracy and

dependability. We use a sophisticated software system that integrates

scheduling, payroll and billing functions, giving customers the benefit of

customized programs using the personnel best suited to the job.

Renewing

and extending existing contracts and obtaining new contracts are crucial to our

ability to generate revenues, earnings and cash flow. In addition,

our growth strategy involves the acquisition and integration of complementary

businesses in order to increase our scale within certain geographical areas,

capture market share in the markets in which we operate and improve our

profitability. We intend to pursue acquisition opportunities for

contract security officer businesses. We frequently evaluate

acquisition opportunities and, at any given time, may be in various stages of

due diligence or preliminary discussions with respect to a number of potential

acquisitions. However, we cannot assure you that we will identify any

suitable acquisition candidates or, if identified, that we will be able to