Attached files

| file | filename |

|---|---|

| EX-21.01 - EX-21.01 - NEW FRONTIER MEDIA INC | a2197879zex-21_01.htm |

| EX-23.01 - EX-23.01 - NEW FRONTIER MEDIA INC | a2197879zex-23_01.htm |

| EX-32.01 - EX-32.01 - NEW FRONTIER MEDIA INC | a2197879zex-32_01.htm |

| EX-31.02 - EX-31.02 - NEW FRONTIER MEDIA INC | a2197879zex-31_02.htm |

| EX-32.02 - EX-32.02 - NEW FRONTIER MEDIA INC | a2197879zex-32_02.htm |

| EX-31.01 - EX-31.01 - NEW FRONTIER MEDIA INC | a2197879zex-31_01.htm |

| EX-10.46 - EX-10.46 - NEW FRONTIER MEDIA INC | a2197879zex-10_46.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

NEW FRONTIER MEDIA, INC. AND SUBSIDIARIES TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

For the Fiscal Year Ended March 31, 2010

Commission File Number: 000-23697

NEW FRONTIER MEDIA, INC.

(Exact name of registrant as specified in its charter)

| Colorado (State of Incorporation) |

84-1084061 (I.R.S. Employer I.D. Number) |

7007 Winchester Circle, Suite 200, Boulder, CO 80301

(Address of principal executive offices and Zip Code)

(303) 444-0900

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Common Stock par value $.0001 | The Nasdaq Stock Market, LLC | |

| Rights to Purchase Series A Junior Participating Preferred Stock |

Securities registered pursuant to Section 12(g) of the Exchange Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o YES ý NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. o YES ý NO

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý YES o NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). o YES o NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-Accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the Registrant's common stock held by non-affiliates of the Registrant as of September 30, 2009 was approximately $40,676,000, based on the closing price of the common stock as reported on the NASDAQ Global Select Market on such date.

The Registrant had 19,432,317 shares of its common stock outstanding on June 4, 2010.

Documents Incorporated by Reference

The information required in response to Part III of Form 10-K is hereby incorporated by reference from the Registrant's Definitive Proxy Statement to be filed with the Securities and Exchange Commission within 120 days of March 31, 2010 with respect to the Registrant's Annual Meeting of Shareholders expected to be held on or about August 23, 2010.

NEW FRONTIER MEDIA INC. AND SUBSIDIARIES

FORM 10-K

FOR THE FISCAL YEAR ENDED MARCH 31, 2010

i

Forward-Looking Statements and Other Information

This Annual Report on Form 10-K of New Frontier Media, Inc. and its consolidated subsidiaries, or the Company or the Registrant, and the information incorporated by reference includes forward-looking statements within the meaning of the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements regarding trend analysis and the Company's expected financial position and operating results, its business strategy, its financing plans and the outcome of contingencies are forward-looking statements. Forward-looking statements are also identified by the words "believe," "project," "expect," "anticipate," "estimate," "intend," "strategy," "plan," "may," "should," "could," "will," "would," and similar expressions. The forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those set forth or implied by any forward looking statements. Some of these risks are detailed in Part I, Item 1A, Risk Factors and elsewhere in this Form 10-K.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. The Company undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

Registered trademarks identified herein that are not expressly stated to be the property of the Company are the property of the respective owners of such marks.

GENERAL

We are a leader in transactional television and the distribution of general motion picture entertainment. Our key customers include large cable and satellite operators, premium movie channel providers and major Hollywood studios. We distribute content world-wide. Our three principal businesses are reflected in the Transactional TV, Film Production and Direct-to-Consumer operating segments. Our Transactional TV segment distributes adult content to cable and satellite operators who then distribute the content to retail customers via pay-per-view ("PPV") and video-on-demand ("VOD") technology. We earn revenue through contractual percentage splits of the retail price. The Transactional TV segment has historically been our most profitable segment. The Film Production segment generates revenue through the distribution of mainstream content to large cable and satellite operators, premium movie channel providers and other international content distributors. This segment also periodically provides contract film production services to major Hollywood studios ("producer-for-hire" arrangements). The Film Production segment incurred operating losses in fiscal years 2010 and 2009 primarily due to large non-cash impairment charges. Our Direct-to-Consumer segment primarily generates revenue from membership fees earned through the distribution of adult content to consumer websites. The Direct-to-Consumer segment has historically incurred operating losses and is expected to continue to incur operating losses for the foreseeable future; however, we have been focused on returning the segment to profitability through efforts described below. Our Corporate Administration segment includes all costs associated with the operation of the public holding company, New Frontier Media, Inc.

The Film Production segment continues to experience challenging market conditions, and these market conditions are expected to continue for the foreseeable future. As a result and in connection with our annual goodwill impairment testing, we recorded a goodwill impairment charge within the segment in the fourth quarter of fiscal year 2010 of approximately $4.9 million. See additional information on the goodwill impairment charge within the Film Production segment discussions below.

1

Also in the fourth quarter of fiscal year 2010, we discontinued the operations of an Internet Protocol Television ("IPTV") set-top box business within the Direct-to-Consumer segment. See Note 19—Discontinued Operations within the Notes to Consolidated Financial Statements for further discussion on our discontinuation of the IPTV set-top box business.

The business models of each of our segments are discussed in further detail below.

OPERATING SEGMENTS

Transactional TV Segment

The Transactional TV segment generated the majority of its revenue in fiscal year 2010 through the distribution of adult entertainment content on domestic VOD platforms. VOD distribution primarily occurs through cable multiple system operators, or MSOs, and telephone company operators that also provide television services. VOD presents viewers with layered menus, similar to what is traditionally found in hotel room television offerings. These menus allow users to interactively select a movie or event and then view it immediately or at a later time once the transaction has been executed. VOD tends to have a more accretive impact on our Transactional TV segment's business relative to our PPV offering because of the variety of content available through VOD platforms and because of the flexibility VOD provides in viewing times.

Our Transactional TV segment also distributes adult entertainment programming to cable and satellite television companies through nine 24/7 PPV channels. PPV offers consumers access to a timed block of programming—for example, a movie or an event—for a set fee payable to the cable or satellite providers. Our PPV programming is offered on channels that are available to viewers through the same electronic program guides that display basic cable channels. A PPV transaction allows access to the purchased content for a given period of time and is executed either by telephone, internet or instantly through the use of the viewers' remote control. Some of our distributors also offer our Transactional TV segment's channels on a monthly subscription basis. However, the large majority of the PPV revenue we generate is based on individual title purchases, and subscription revenue represents a small portion of the segment's total PPV revenue.

We earn a percentage of the revenue, or "split", from our content for each VOD or PPV transaction that is purchased on our customers' platform. Our Transactional TV segment's products typically retail for a price between $10.99 and $14.99 for a single movie or event as determined by our customers with input from us.

We believe our VOD and PPV programming provides an attractive form of entertainment because it is offered conveniently in the comfort of users' homes and can be viewed on a large, high quality television. During our fiscal years ended March 31, 2010, 2009 and 2008, 74%, 81%, and 73%, respectively, of our consolidated net revenue was attributed to our Transactional TV segment. Our Transactional TV segment distributes content to nearly every television provider in the United States including:

- •

- the two largest providers of direct broadcast satellite, or DBS, services in the U.S.; and

- •

- the top ten largest operators of cable television systems in the U.S.

For most of its history, the Transactional TV segment has been focused on growing its distribution in the U.S. During fiscal year 2009, we began expanding our services into international markets in North America, Europe and Latin America. We believe that our business model, which we believe has been successful in the U.S., can also be successful in international markets. International expansion also provides us with an opportunity to leverage our existing content libraries and technology infrastructure. Thus far, we have had success in expanding our distribution to international markets and generated approximately $3.6 million of Transactional TV segment VOD and PPV international revenue during

2

fiscal year 2010. We plan to continue to expand our footprint to new international locations and customers, and gain additional market share and shelf space in international markets where we currently distribute content. The VOD infrastructure in many international markets is relatively undeveloped, and we expect that the development of the VOD infrastructure will continue to offer opportunities to improve our international revenue. Additionally, the revenue splits we receive internationally are typically higher than the splits we receive domestically because the international cable MSO and DBS industry has more market participants and is more fragmented, which provides us with better negotiating leverage. We have not historically operated internationally or dealt with international regulators, competitors or cultures and as a result, we may experience difficulties in increasing revenue from such operations while gaining experience with our international growth initiatives.

Programming Strategy

The Transactional TV segment's programming is designed to provide a wide variety of content to consumers while at the same time utilizing available titles from our content library. Because we do not duplicate titles across our channels or between PPV and VOD, we are able to give our consumers access to more unique titles, a wider variety of talent, and a greater variety of studio representation. We focus on prime time viewing blocks and program specific types of content in those blocks to create an appointment-viewing calendar designed to drive viewers to traditionally less popular nights of the week for viewing adult content.

Our programming department spends a significant amount of time and resources researching consumer choices and preferences. We periodically perform primary consumer research to understand buying habits and to obtain information on how we can best provide our consumers with an exceptional viewing experience. This research has enhanced our Transactional TV segment's performance and has assisted us in providing customer satisfaction. Additionally, we use this research to recommend changes to our customers' platforms in order to improve the overall performance of the adult content category.

Content Delivery System

Our Transactional TV segment delivers its PPV video programming to cable and satellite operators via satellite from our Digital Broadcast Center, or DBC, in Boulder, Colorado. The program signal is encrypted so that the signal is unintelligible unless it is passed through the properly authorized decoding devices. The signal is transmitted (uplinked) by a third party earth station to a designated transponder on a third party commercial communications satellite. The transponder receives the program signal that has been uplinked by the earth station, amplifies the program signal and then broadcasts (downlinks) the signal to commercial satellite dishes located within the satellite's area of signal coverage. The programming is downlinked by MSOs and DBS providers at their head-ends and uplink centers. This programming is received in the form of a scrambled signal. We provide these operators with decoder equipment which allows them to decode the signal and then re-distribute it via their own systems.

Our Transactional TV segment maintains a satellite transponder lease agreement for one full-time digital transponder with a total bandwidth of approximately 36 MHz on the Galaxy 23 satellite and approximately 9 MHz on the NSS 806 satellite. These transponders provide the satellite transmission necessary to broadcast our Transactional TV segment's networks. The signal of the satellites that we use covers the continental U.S., Alaska, Hawaii, Latin America and portions of the Caribbean Islands and Canada.

Our Transactional TV segment delivers its VOD service to cable MSOs via transport providers such as TVN Entertainment Corporation. In addition, our Transactional TV segment has agreements

3

with iN DEMAND L.L.C., and Global Digital Media Xchange to deliver VOD content to other cable MSOs.

Digital Broadcast Center

The 12,000 square foot DBC allows us to ingest, encode, edit, play out, store and digitally deliver our PPV and VOD services. The DBC is also home to one of the largest digital libraries of its kind. The DBC is a scalable, state of the art infrastructure, which includes playlist automation for all channels; encoding and playout to air; a storage area network for near-line content movement and storage; archiving capability in a digital format; and complete integration of our proprietary media asset management database for playlist automation and program scheduling.

Program and Content Acquisitions

We acquire our broadcast programming for each network by licensing rights from producers and producing content. The licenses generally cover a five-year term. We generally acquire and produce new premiere titles and scenes each month. In addition, we may license entire content libraries on an as-needed basis or in order to facilitate a larger transaction. Once we license a title, it undergoes rigorous quality control processes prior to broadcast in order to ensure compliance with strict internal and external broadcasting standards. We obtain age verification documentation for each title we license in accordance with federal statutes. This documentation is maintained on site for the duration of the license term in accordance with 18 U.S.C. § 2257 and 28 C.F.R. 75 et seq.

We maintain an office in California that (a) ensures all legal documentation is obtained for each title and scene licensed, (b) ensures acquired content is technically compliant, and (c) once the title is deemed acceptable, ships the title, related documentation and promotional content to our Boulder, Colorado location. Our Transactional TV segment's in-house programming and editing departments in Boulder conduct preliminary screening of potentially licensable content, license acceptable content, conform content into appropriate editing standards and program the monthly schedules for all networks and VOD services.

Competition

Our primary competitor in this segment has historically been Playboy Enterprises, Inc. ("Playboy") which, through its Playboy TV® service and its Spice Digital Networks®, has a long operating history in the adult entertainment space. Over the past several years, we have been successful in competing with Playboy, and we have experienced growth in our Transactional TV segment as a result of our ability to gain market share through the displacement of Playboy services. Other competitors, such as Hustler TV®, have also entered the market and are increasing competition.

Our content has typically outperformed our competitors' content on the majority of DBS and MSO platforms as measured by revenue per server hour. As a result, we have been able to increase our shelf space on these platforms through incremental platform hours and the replacement of our competitors' hours. We believe that some competitors have been willing to execute contracts with distributors that contain lower revenue splits and/or provide revenue guarantees in order to obtain or retain channels and VOD platform hours. While we believe that our content continues to outperform the competition, we cannot predict whether that performance advantage will insulate us from further pressure on revenue splits. If our competitors continue to provide the DBS and MSO platforms lower revenue splits and if we are unable to maintain a performance advantage or cause the DBS and MSO providers to recognize the value from this performance advantage, then our customers could put additional pressure on us to lower our revenue splits. A reduction in our revenue splits would have a material adverse impact on our results of operations and financial condition.

4

We also face competition in the adult entertainment market from other providers of adult programming including producers of adult content, adult internet sites, adult video/DVD rentals and sales, premium movie channels that broadcast adult-themed content, telephone adult chat lines, books and magazines aimed at adult consumers, and adult-oriented wireless services. Our Transactional TV segment also faces general competition from other forms of non-adult entertainment, including sporting and cultural events, other television networks, feature films, and other programming.

Film Production Segment

Our Film Production segment is a multi-faceted film production and distribution company. The Film Production segment expands our portfolio to the higher margin market for mainstream and erotic content and provides us with established relationships in international markets. Additionally, we have leveraged our existing Transactional TV segment customer relationships and deliver the Film Production segment's library of erotic and mainstream content to many of the same Transactional TV segment MSO and DBS customers.

Our Film Production segment derives revenue from two principal businesses: (1) the production and distribution of original motion pictures such as erotic thrillers, horror movies, and erotic, event styled content ("owned content"); and (2) the distribution of third party films where we act as a sales agent for the product ("repped content"). This segment also periodically provides contract film production services to major Hollywood studios ("producer-for-hire" arrangements).

During fiscal year 2009, the film markets were significantly impacted by the economic downturn. As a result, the Film Production segment's customers reduced their content acquisition budgets. We believe this occurred because our customers were relying upon their existing libraries to reduce spending and costs. These changes significantly impacted the Film Production segment operating results during the third quarter of fiscal year 2009 and as a result, we made material revisions to the segment's internal forecasts and engaged a third party valuation firm to assist us in performing a goodwill and intangible asset impairment analysis. Based on the analysis, we determined that the goodwill associated with the Film Production segment was impaired and recorded a $10.0 million goodwill impairment charge during the quarter ended December 31, 2008. We also recorded a film cost impairment charge of approximately $1.1 million during the quarter ended December 31, 2008 primarily as a result of the economic downturn.

Excluding goodwill and other impairment charges, the Film Production segment results in fiscal year 2010 were consistent with our internal budgets. However, industry conditions continue to be unfavorable in the film markets where we distribute content, and we believe these challenging conditions will continue for the foreseeable future. As a result, the five year internal forecast for the Film Production segment was revised downward in connection with our year end goodwill impairment testing. We engaged a third party valuation firm to assist us in performing the annual goodwill impairment analysis. Based on the analysis, we determined that the goodwill associated with the Film Production segment was impaired and recorded a $4.9 million goodwill impairment charge during the fourth quarter of fiscal year 2010. We also recorded a film cost impairment charge of approximately $1.2 million and a recoupable costs and producer advances impairment charge of approximately $0.8 million during the fourth quarter of fiscal year 2010 associated with the unfavorable film market conditions. It is reasonably possible that future unfavorable economic conditions could cause the operating results of this segment to remain depressed or decline.

Owned Content Revenue

The Film Production segment produces and distributes its owned content for three primary customer groups. The first customer group consists of cable MSO and DBS service providers. Since our acquisition of the Film Production segment, we have leveraged our existing Transactional TV segment

5

relationships and established new customer opportunities for our Film Production segment's owned content. The owned content that is distributed through PPV appears on unbranded linear channels within the mainstream or adult PPV movie location of the platform's electronic programming guide. Content that is distributed through VOD appears within menu categories such as "uncensored." Our movies and events are sold to end users at retail prices typically ranging from $7.99 to $9.99. We receive a percentage share of the revenue derived from sales on these platforms. Revenue splits are typically higher than those earned by our Transactional TV segment due to the mainstream nature of the content. Owned content is distributed to cable MSO and DBS service providers using the DBC and transport providers as described above in the Transactional TV segment discussion.

The second customer group for our owned content distribution consists of premium movie service providers such as Cinemax and Showtime. The premium movie service providers license and distribute the content as part of their late-night programming and within their subscription VOD product. The owned content is typically sold to these customers for a flat license fee.

The third customer group consists of various international distributors including international premium movie service providers. These international distributors typically re-distribute the content to end-users. We also typically charge these customers a flat license fee for the owned content.

The Film Production segment does not employ a production staff. Third-party production staff is used to produce owned content, and our employees provide in-house oversight over the critical areas of production such as scripting, casting, shoot location, and post production.

Sales Agency (Repped Content) Service Revenue

Our Film Production segment has established relationships with independent mainstream film producers. We act as a sales agent for the film producers and license both domestic and international rights to their movies under Lightning Entertainment Group. We also license titles under our Mainline Releasing Group. We earn a commission for licensing film rights on behalf of these producers. The commission we earn from domestic distribution is typically more favorable than the commission we earn from international distribution. We also earn a marketing fee for many titles that we represent. Each contract typically allows for the recoupment of any producer advances and costs incurred in preparing the title for market, including advertising costs, screening costs, costs to prepare the trailer, box art, screening material, and similar costs necessary to ensure the movie is market ready.

We generate revenue from our repped content through arrangements with mainstream distributors world-wide. Distributors deliver the repped content through various channels including theatrical, pay-television, free television and other similar distribution channels. We also recently began distribution of repped content on VOD platforms through U.S. cable MSOs. We continue to leverage the relationships we have established through the Transactional TV segment with U.S. cable and DBS providers and have successfully launched the Film Production segment's repped content in over 35 million network homes. Additionally, our repped content is distributed in large retail DVD markets through a distribution arrangement we executed with a leading independent home video/DVD entertainment partner.

Producer-for-Hire and Other Revenue

Producer-for-hire and other revenue relates to amounts earned through producer-for-hire arrangements, music royalty fees and the delivery of other miscellaneous film materials to customers. Through our producer-for-hire arrangements, we provide services and incur costs associated with the film production, and we earn a fee for our services once the film has been delivered to the customer. Although we maintain no ownership rights for the produced content, we are responsible for the management and oversight of the project and incur significant economic risk until the project is completed. The gross margins we generate from producer-for-hire arrangements are less than the

6

returns we generate from our owned content and have historically been between 10% and 20% of net revenue; however, we cannot reasonably predict whether the gross margins we receive will continue to be similar to those generated historically. We generated approximately $3.9 million of producer-for-hire services revenue during the fourth quarter of fiscal year 2010. We also expect to generate an additional $4.0 million to $4.1 million in producer-for-hire services revenue during fiscal year 2011.

Competition

For our owned content, we compete primarily with one small, privately-owned company and other branded content such as Girls Gone Wild® and Jerry Springer® Uncensored. With respect to our sales agency business, we compete with approximately 30 privately-owned companies. We compete with these companies based on licensing fees charged, content quality, ability to deliver our products on-time, relationships with decision makers in the industry, and the professionalism of our sales team. For our producer-for-hire services, we compete against a wide variety of independent movie producers.

Direct-to-Consumer Segment

Our Direct-to-Consumer segment derives revenue primarily through subscriptions to its consumer websites. Content for the websites is primarily obtained through licensing agreements executed by our Transactional TV segment for broadcast rights. Traffic to our consumer websites is primarily derived through either a targeted network of affiliates that earn a referral fee from us when diverted traffic converts into paying members, or "type-in" traffic in which users navigate directly to the sites by typing the addresses into their web browsers.

This segment also launched a test initiative related to the development of a set-top box and IPTV business model. During January 2008, we acquired certain intellectual property rights to an internet protocol set-top box. Through the set-top box, consumers could access content through the internet and view the content on their television. Based on lower than expected subscriber additions for the IPTV business model and other factors considered during the second half of fiscal year 2009, we reduced the resources allocated to the related new product offering operations. During fiscal year 2010, the IPTV business model's performance continued to be lower than expected. In the fourth quarter of fiscal year 2010, we discontinued the operations of the IPTV business model as a result of the underperformance in fiscal year 2010. See Note 19—Discontinued Operations within the Notes to Consolidated Financial Statements for further discussion on our discontinuation of the IPTV set-top box business.

Competition

The adult internet industry is highly competitive and highly fragmented given the relatively low barriers to entry. Recently, the introduction of a large number of free content sites that allow users to access large libraries of content has created an even more challenging environment.

OTHER INFORMATION

Customer Concentration

We derived 52% of our total revenue for the fiscal year ended March 31, 2010 from Comcast Corporation ("Comcast"), DIRECTV Group ("DirecTV"), DISH Network ("DISH"), and Time Warner Cable Inc. ("Time Warner"). We generate revenue from these customers through our Transactional TV and Film Production segments. The loss of any of these major customers would have a material adverse effect on these segments and our Company as a whole. Specific financial information about the total revenue and outstanding accounts receivable from each of our major customers is incorporated by reference herein to Note 13—Major Customers within the Notes to Consolidated Financial Statements included herein.

7

Employees

As of March 31, 2010, we had approximately 180 employees located only in the United States. Our employees are not members of a union, and we have never suffered a work stoppage.

Financial Information about Segments and Geographic Areas

Our revenue is primarily derived from customers located in the United States. Financial information about segments and geographic areas is incorporated herein by reference to Note 12—Segment and Geographic Information within the Notes to Consolidated Financial Statements included herein.

Seasonality

Although we do not consider our business to be highly seasonal, our Film Production segment sales team attends a large proportion of film trade shows just prior to and during the third fiscal quarter. In the 2008 and 2007 fiscal years, we executed contracts at those tradeshows and subsequently delivered the related content in the third fiscal quarter resulting in higher revenue relative to other quarters. During the third quarters of the fiscal years ended March 31, 2009 and 2010, the Film Production segment's revenue has not exhibited a similar level of seasonality due to the deterioration in film markets. We believe that it is reasonably possible that the film markets will continue to experience unfavorable economic conditions which could cause the Film Production segment's revenue in the third fiscal quarter to remain depressed or decline.

Intellectual Property

During fiscal year 2008, we acquired certain intellectual property rights associated with set-top box equipment that provides customers with IPTV and other new product development. We will seek to protect our intellectual property rights. Despite our efforts, unauthorized parties may attempt to copy aspects of our products or obtain and use information that we regard as proprietary. Policing unauthorized use of our rights is difficult. Additionally, third parties might independently develop technologies that are substantially equivalent or superior to our technologies.

Government Regulation

Our Company is regulated by governmental authorities. We have historically operated only in the United States and so we were only regulated by domestic authorities. However, because we have expanded to international markets, we must comply with diverse and evolving regulations both domestically and internationally. Regulation relates to, among other things, licensing, access to satellite transponders, foreign investment, use of confidential customer information and content, including standards of decency and obscenity. Changes in the regulation of our operations or changes in interpretations of existing regulations by courts or regulators or our inability to comply with current or future regulations could have a material adverse impact on our financial position and results of operations.

Available Information

We file annual, quarterly and current reports, and amendments thereto, with the Securities and Exchange Commission ("SEC") under Section 13(a) of the Securities Exchange Act of 1934. We make these reports available free of charge on or through our internet website, www.noof.com, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the SEC. Information on our website should not be considered to be a part of this report or any other

8

SEC filing unless explicitly incorporated by reference herein. You may request a copy of these filings at no cost. Please direct your requests to:

New

Frontier Media, Inc.

Attn: CFO

7007 Winchester Circle, Suite 200

Boulder, CO 80301

You can also read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington DC 20549. You can obtain information on the operations of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site (www.sec.gov) that contains our reports, proxy and information statements and other information that we file electronically with the SEC.

EXECUTIVE OFFICERS OF THE REGISTRANT.

Our executive officers are as follows:

Name

|

Age | Position | |||

|---|---|---|---|---|---|

| Michael Weiner | 68 | Chairman of the Board, Chief Executive Officer and Secretary | |||

| Ken Boenish | 43 | President | |||

| Marc Callipari | 42 | General Counsel | |||

| Scott Piper | 47 | Chief Technology and Information Officer | |||

| Grant Williams | 34 | Chief Financial Officer | |||

Michael Weiner. Mr. Weiner was appointed President of New Frontier Media in February 2003 and was then appointed to the position of Chief Executive Officer in January 2004. Prior to being appointed President, he held the title of Executive Vice President and co-founded the Company. As Executive Vice President, Mr. Weiner oversaw content acquisitions, network programming, and all contract negotiations related to the business affairs of the Company. In addition, he was instrumental in securing over $20 million to finance the infrastructure build-out and key library acquisitions necessary to launch the Company's television networks. Mr. Weiner's experience in entertainment and educational software began with the formation of Inroads Interactive, Inc. in May 1995. Inroads Interactive, based in Boulder, Colorado, was a reference software publishing company dedicated to aggregating still picture, video, and text to create interactive, educational-based software. Among Inroads Interactive's award winning releases were titles such as Multimedia Dogs, Multimedia Photography, and Exotic Pets. These titles sold over 1 million copies throughout the world through its affiliate label status with Broderbund Software and have been translated into ten different languages. Mr. Weiner was instrumental in negotiating the sale of Inroads Interactive to Quarto Holdings PLC, a UK-based book publishing concern. Prior to Inroads Interactive, Mr. Weiner was in the real estate business for 20 years, specializing in shopping center development and redevelopment in the Southeast and Northwest United States. He was involved as an owner, developer, manager, and syndicator of real estate in excess of $250 million.

Ken Boenish. Mr. Boenish is a 20-year veteran of the cable television industry. In October 2000, he was named President of the Transactional TV segment and in June 2005 he was named President of New Frontier Media. Mr. Boenish joined New Frontier Media as the Senior Vice President of Affiliate Sales in February 1999. Prior to joining the Company, Mr. Boenish was employed by Jones Intercable ("Jones") from 1994 to 1999. While at Jones he held the positions of National Sales Manager for Superaudio, a cable radio service serving more than 9 million cable customers. He was promoted to Director of Sales for Great American Country, a then new country music video service, in 1997. While at Great American Country, Mr. Boenish was responsible for adding more than 5 million new customers to the service while competing directly with Country Music Television, a CBS cable network. From 1988 to 1994 he sold cable television advertising on systems owned by Time Warner, TCI, COX, Jones, Comcast and other cable systems. Mr. Boenish holds a bachelors degree from St. Cloud State University.

9

Marc Callipari. Mr. Callipari joined New Frontier Media in August 2006 as the Vice President of Legal Affairs and shortly thereafter was promoted to General Counsel. He is responsible for New Frontier Media's legal and human resources functions. Mr. Callipari started his legal career over 14 years ago in Washington, D.C. where he practiced commercial litigation from 1994 to 1999 with a large, international law firm and a boutique litigation firm. More recently, he served as captive outside and then in-house counsel to Level 3 Communications, an unaffiliated international communications company, from 1999 to 2006, where he was responsible for a wide range of world-wide litigation and transactional matters, including the negotiation of several multi-million dollar telecommunication infrastructure asset purchases and sales. He graduated from the University of San Diego School of Law in 1994, is a member of the Colorado, Virginia and District of Columbia Bars and has been admitted to practice before numerous federal courts throughout the United States.

Scott Piper. Mr. Piper joined New Frontier Media in February 2007 as Chief Technology and Information Officer. Mr. Piper has been an information technology professional for approximately 20 years and has held senior leadership roles for the past 12 years. He has extensive experience in infrastructure design and delivery for large scale enterprises, including the implementation of over fifteen customer contact centers, some with as many as 1,500 seats. He was responsible for one of the first successful large voice over internet protocol ("VoIP") contact centers in the U.S. Prior to joining New Frontier Media, Mr. Piper was employed from 1994 to 2006 by EchoStar Satellite L.L.C. While employed in a variety of roles during his tenure at EchoStar, he most recently held the title of Vice President of IPTV. Mr. Piper was responsible for the launch of DISH Network's web based entertainment portal prior to his departure. Mr. Piper holds a Bachelor of Science in Marketing and Finance from the University of Colorado and a Masters in Science in Telecommunications from the University of Denver.

Grant Williams. Mr. Williams has served as Chief Financial Officer since April 2008. Mr. Williams served as the Corporate Controller of New Frontier Media from October 2006 until April 2008. From February 2004 until October 2006, Mr. Williams was employed by eFunds Corporation and served in various senior manager roles, including management of Securities and Exchange Commission filings and correspondence; financial contract management for significant transactions including business acquisitions, business dispositions, and debt financing; and financial management and analysis of the company's corporate costs. Prior to February 2004, Mr. Williams was employed by Ernst and Young, LLP as a manager within the assurance and advisory services group. Mr. Williams holds a Bachelor of Accountancy from the University of Oklahoma and is a Certified Public Accountant in Colorado and Arizona.

The loss of any of our current major customers, or our inability to maintain or negotiate at renewal or otherwise favorable contractual terms with these customers, could have a material adverse effect on our financial position and results of operations.

We have agreements with the ten largest U.S. cable MSOs and two largest U.S. DBS providers. For our fiscal year ended March 31, 2010, the aggregate revenue we received from our major customers (customers that account for 10% or more of our consolidated revenue, namely Comcast, DISH, DirecTV and Time Warner) was approximately 52% of our total company-wide revenue. Our agreements with these operators may be terminated without penalty and with little advance notice, and as a result are sometimes subject to renegotiation during their stated term. If one or more of these cable MSO or DBS operators terminates or does not renew our agreements, or negotiates mid-term or agrees only to renew the agreements on terms less favorable than those of our current agreements (including removing or replacing with a competitive offering or otherwise one or more of our PPV channels or VOD offerings from their platforms), our financial position and results of operations could be materially adversely effected.

10

For example, the largest DBS provider in the U.S., which increased our distribution from two channels to three channels during the third quarter of fiscal year 2008, reduced its carriage of our PPV channels back to two channels in November 2009. Consistent with the terms of the original agreement, the customer has the right to discontinue carriage of any of the remaining two channels without penalty and with little advance notice. The removal of the channel in November 2009 resulted in an estimated decline in our PPV revenue of approximately $0.6 million during fiscal year 2010.

We rely on third party service providers to deliver our content to our customers via satellite uplink and transport services. If these services were disrupted, it could cause us to lose subscriber revenue and adversely affect our financial position and results of operations.

Our satellite uplink and transport provider services are critical to us. If our satellite uplink or transport provider fails to provide the contracted services, our programming operations would in all likelihood be suspended, resulting in a loss of substantial revenue. If our satellite uplink provider improperly manages its uplink facilities, we could experience signal disruptions and other quality problems that, if not immediately addressed, could cause us to lose customers and the related revenue.

Our continued access to satellite transponders is critical to us. Our satellite programming operations require continued access to satellite transponders to transmit programming to our cable and DBS customers. Limitations to satellite transponder capacity could materially adversely affect our financial position and results of operations. Access to transponders may be restricted or denied if:

- •

- we or the satellite owner is indicted or otherwise charged as a defendant in a criminal proceeding;

- •

- the Federal Communications Commission issues an order initiating a proceeding to revoke the satellite owner's

authorization to operate the satellite;

- •

- the satellite owner is ordered by a court or governmental authority to deny us access to the transponder;

- •

- a governmental authority commences an investigation concerning the content of the transmissions;

- •

- we are deemed by a governmental authority to have violated any obscenity law; or

- •

- our satellite transponder provider determines that the content of our programming is harmful to its name or business.

Our ability to convince cable operators and DBS providers to carry our programming is critical to us. We can give no assurance that we will be able to continue to obtain carriage with cable operators and DBS providers in the future.

If we are unable to compete effectively with other forms of adult and non-adult entertainment, we will not be able to sustain or increase revenue.

Our ability to increase or sustain revenue is impacted by our ability to compete effectively with other forms of adult and non-adult entertainment. We face competition in the adult entertainment industry from other providers of adult programming, adult video/DVD rentals and sales, books and magazines aimed at adult consumers, adult oriented telephone chat lines, adult oriented internet services, including free website content services, premium movie channels that broadcast adult-themed content and adult oriented wireless services. To a lesser extent, we also face general competition from other forms of non-adult entertainment, including sporting and cultural events, other television networks, feature films, and other programming and entertainment options.

11

Our ability to compete depends on a variety of factors, many of which are outside of our control. These factors include the quality and appeal of our competitors' content relative to our offerings; the strength of our competitors' brands; the technology utilized by our competitors; the effectiveness of our competitors' sales, marketing efforts and the attractiveness of their product offerings; general consumer behaviors; and preferences on how consumers choose to spend their discretionary income.

Our existing competitors, as well as potential new competitors, may have significantly greater financial, technical and marketing resources, as well as better name recognition than we do. This may allow them to devote greater resources than we can to the development and promotion of their product offerings. These competitors may also engage in more extensive technology research and development, and adopt more aggressive pricing policies for their content. Additionally, increased competition could result in license fee reductions, lower margins and a negative impact on our financial position and results of operations.

The popularity and notoriety of adult entertainment through low cost and free websites has resulted in additional pressure on our business. The quality and quantity of content available on these free and low cost websites has improved. The content we sell through the Transactional TV segment typically has a retail price between $10.99 and $14.99 and is typically less explicit than the content offered on internet websites. As a result of the recent deterioration in economic conditions, customers may view internet delivered content as a replacement to our content based on the difference in cost, edit standard and availability of certain niche content that we do not distribute. A migration of customers to internet delivered content could result in a decline in our buy rates and have a negative impact on our financial position and results of operations.

The continued addition of new competitors to our business could have a material adverse affect on our operating performance.

We face competition from established adult video producers, as well as independent companies that distribute adult entertainment, some of which is provided for free through internet websites. These competitors may include producers such as Hustler, Wicked Pictures and Vivid Entertainment. In the event that cable and/or satellite companies seek to purchase adult video content for their PPV or VOD service directly from adult video producers or other independent distributors of such content, our PPV and VOD business is likely to suffer. For example, an independent producer of adult content, which has historically distributed content only through the internet, replaced one of our PPV channels on the largest DBS platform in the U.S. during the third quarter of fiscal year 2010 resulting in a decrease in our revenue of approximately $0.6 million during fiscal year 2010. In addition, increased competition in the adult category could lead to downward pressure on the license fees that our customers are willing to pay for our content.

We may incur costs to defend ourselves against legal claims initiated in connection with our distribution of adult-themed content.

Because of the adult-oriented content that we distribute, we may be subject to obscenity or other legal claims by third parties. Our financial position and results of operations could be harmed if we were found liable for this content or if costs to defend such claims proved significant. Implementing measures to reduce our exposure to this liability may require us to take steps that would substantially limit the attractiveness of our content and/or its availability in various geographic areas, which would negatively impact our ability to generate revenue. Furthermore, our insurance may not adequately protect us against all of these types of claims.

12

Increased government regulation in the United States and abroad could impede our ability to deliver our content and expand our business.

New laws or regulations, or the new application of existing laws could prevent us from making our content available in various jurisdictions or otherwise have a material adverse affect on our business, financial position and operating results. These new laws or regulations may relate to liability for information retrieved from or transmitted over the internet, taxation, user privacy and other matters relating to our products and services. Moreover, the application of internet related laws governing issues such as intellectual property ownership and infringement, pornography, obscenity, libel, employment, and personal privacy is still developing.

Cable and DBS operators could become subject to new governmental regulations that could further restrict their ability to broadcast our programming. If new regulations make it more difficult for cable and DBS operators to broadcast our programming, our financial position and results of operations could be adversely affected.

Changes in our effective tax rate or assessments arising from tax audits may have an adverse impact on our results.

We are subject to taxation in various jurisdictions, both domestically and internationally, in which we conduct business. Significant judgment is required in the determination of our provision for income taxes and this determination requires the interpretation and application of complex and sometimes uncertain tax laws and regulations. Our effective tax rate may be adversely impacted by changes in the mix of earnings between jurisdictions with different statutory tax rates, in the valuation of our deferred tax assets, and by changes in tax rules and regulations. For instance, the availability and timing of lapses in the United States research and development tax credit, the accounting of uncertain tax positions and the amount of our estimated tax deduction for domestic production activities may add more variability to our future effective tax rates.

We recently filed amended and current tax returns that reflect a tax benefit associated with research and development tax credits. We are subject to examination of these amended and current tax returns and our determination of the research and development tax credits. If the Internal Revenue Service audits these returns and disallows some or all of the research and development tax credits, our financial position and results of operations could be materially adversely affected.

If the Film Production segment produces, acquires or represents film content that is not well-received by our customers, we may not be able to re-coup the investments made in the film.

We have a history of impairing titles in our content library and recoupable costs associated with our repped content when the future expected economic benefits to be derived by a particular film or event are not estimated to be sufficient to recover its related carrying value. The Film Production segment's ability to continue to create or acquire film content and obtain rights to represent content that is well-received by our customers is critical to the segment's future success. If a film produced, acquired or represented by the Film Production segment does not sell as well as anticipated, we may not be able to recover our investment in the film, including, but not limited to, the cost of producing or acquiring the film, the costs associated with promoting the film, costs associated with post-production work on the film, or advances and other recoupable costs associated with representing a film. No assurance can be given that the Film Production segment's past success in generating profits from its investment in its films will continue.

13

Antitakeover provisions in our Amended and Restated Articles of Incorporation, as amended, and our Rights Agreement may discourage or prevent a change of control.

Our charter documents may inhibit a takeover or change in control that our shareholders may consider beneficial. Provisions in our Amended and Restated Articles of Incorporation may have the effect of delaying or preventing a merger or acquisition of us, or making a merger or acquisition less desirable to a potential acquirer, even when the shareholders may consider the acquisition or merger favorable. For example, our Board of Directors, without further shareholder approval, may issue preferred stock that could delay or prevent a change of control as well as reduce the voting power of the holders of common stock, even with the effect of losing control to others. In addition, our Board of Directors has adopted a Rights Agreement, commonly known as a "poison pill," that may delay or prevent a change of control and may also make a merger or acquisition of us less desirable. If a change of control transaction perceived by the shareholders to be in their best interest were delayed or blocked by our protective measures, the value of an investment in our securities may be negatively impacted.

If we are not able to retain our key executives it will be more difficult for us to manage our operations and our financial position and result of operations could be adversely affected.

With only approximately 180 employees, our success depends greatly upon the contributions of our executive officers and our other key personnel. The loss of the services of any of our executive officers or other key personnel could have a material adverse effect on our financial position and results of operations. No assurance can be given that we will be successful in attracting and retaining these personnel.

Our inability to identify, fund the investment in, and commercially exploit new technology could have an adverse impact on our financial position and results of operations.

We are engaged in a business that has experienced tremendous technological change over the past several years and will likely continue to experience further changes. As a result, we face all the risks inherent in businesses that are subject to rapid technological advancement, such as the possibility that a technology that we have invested in becomes obsolete, our inability to identify in a timely manner emerging technologies that may impact our business, or technology advancement may make our offerings obsolete. In any such event, we may be required to invest significant amounts of capital in new technology. Our inability to identify, fund the investment in, and commercially exploit such new technology could have an adverse impact on our financial position and results of operations. Our ability to implement our business plan and to achieve the results projected by management will be dependent upon management's ability to predict technological advances and implement strategies to take advantage of such changes. We may also experience impairments related to existing investments that we have made in new technology.

Negative publicity, lawsuits or boycotts by opponents of adult content could adversely affect our financial position and results of operations and discourage investors from investing in our publicly traded securities.

We could become a target of negative publicity, lawsuits or boycotts by one or more advocacy groups who oppose the distribution of adult entertainment. These groups have mounted negative publicity campaigns, filed lawsuits and encouraged boycotts against companies whose businesses involve adult entertainment. The costs of defending against any such negative publicity, lawsuits or boycotts could be significant, could hurt our finances and could discourage investors from investing in our publicly traded securities. As a leading provider of adult entertainment, we cannot assure you that we may not become a target in the future.

14

Because we are involved in the adult programming business, it may be more difficult for us to raise money or attract market support for our stock.

Some banking entities, investors, investment banking entities, market makers, lenders and other service providers in the investment community may decide not to provide financing to us, or to participate in our public market or other activities due to the nature of our business, which, in turn, may adversely impact the value of our stock, and our ability to attract market support or obtain financing.

We may be unable to protect our intellectual property rights or others may claim that we are infringing on their intellectual property.

During fiscal year 2008, we acquired certain intellectual property rights. Third parties could assert infringement claims against our business in the future. Claims for infringement of all types of intellectual property rights are a common source of litigation. Infringement claims can require us to modify our products, services and technologies or require us to obtain a license to permit our continued use of those rights. We may not be able to perform either of these actions in a timely manner or upon reasonable terms and conditions. Failure to do so could harm our financial position and results of operations. In addition, future litigation relating to infringement claims could result in substantial costs to us and a diversion of management resources. Adverse determinations in any litigation or proceeding could also subject us to significant liabilities and could prevent us from selling some of our products, services or technologies.

Despite our efforts to protect our intellectual property rights, third parties may infringe or misappropriate them or otherwise independently develop substantially equivalent products and services. The loss of intellectual property protection or the inability to secure or enforce intellectual property protection could harm our business.

If we experienced system failures, the services we provide to our customers could be delayed or interrupted, which could harm our business reputation and result in a loss of customers.

Our ability to provide reliable service largely depends on the efficient and uninterrupted operations of our Digital Broadcast Center and related systems. Any significant interruptions could severely harm our business and reputation and result in a loss of revenue and customers. Our systems and operations could be exposed to damage or interruption from fire, natural disaster, unlawful acts, power loss, telecommunications failure, unauthorized entry, computer viruses, or similar events. Although we have taken steps to prevent system failures, we cannot be certain that our measures will be successful and that we will not experience service interruptions. Further, our property and business interruption insurance may not be adequate to compensate us for all losses or failures that may occur.

Our goodwill, intangible assets and other long-lived assets may have further impairment losses.

We conducted our annual goodwill and intangible assets impairment tests as of March 31, 2010, 2009 and 2008. We also performed goodwill and intangible assets impairment tests as of December 31, 2008 due to events and circumstances within our Film Production segment that caused us to believe that it was more likely than not that the segment's goodwill was impaired. We also perform quarterly analyses on the valuation of long-lived assets including our content and distribution rights, film library,

15

recoupable costs and producer advances, and other long-lived assets. We recognized the following continuing operations impairment charges in our statements of operations (in thousands):

| |

Year Ended March 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | |||||||

Goodwill |

$ | 4,856 | $ | 10,009 | $ | — | ||||

Film costs |

1,207 | 1,062 | 684 | |||||||

Intangible assets |

291 | — | — | |||||||

Other long-lived assets |

831 | 236 | 466 | |||||||

Total impairment loss |

$ | 7,185 | $ | 11,307 | $ | 1,150 | ||||

If our goodwill, intangible assets or other long-lived assets' future benefit does not exceed its carrying value, we may be required to further write down the related assets. Declines in the future benefits from these assets could cause us to incur additional impairment losses, which could materially affect our financial position and results of operations. The ongoing uncertainty in general economic and market conditions could increase the likelihood of additional asset impairment losses being recorded in future periods. In addition, the determination of the fair value of goodwill, intangible assets and long-lived assets is subject to a high degree of judgment and complexity and changes in the estimates used in the determination of the fair value of these assets could materially affect our financial position and results of operations.

We may pursue acquisitions, joint ventures, new services and other strategic transactions and activities to complement or expand our business and add shareholder value which may not be successful.

Our future success may depend on opportunities to acquire or form strategic partnerships with other businesses or technologies or establish new services that could complement, enhance or expand our current business or products or that might otherwise offer us growth opportunities. We may not be able to complete such transactions or activities and such transactions or activities, if executed, could pose significant risks and could have a negative effect on our financial position and results of operations. Any transactions or activities that we are able to identify and complete may involve a number of risks, including:

- •

- the diversion of our management's attention and resources from our existing business to integrate the operations and

personnel of the acquired, combined or created business or joint venture;

- •

- the diversion of our management's attention and resources from existing business to create new services;

- •

- possible adverse effects on our financial position and results of operations during the integration process or

implementation process; and

- •

- the inability to achieve the intended objectives of the transactions or activities.

In addition, we may not be able to successfully or profitably integrate, operate, maintain and manage our newly acquired operations, employees or activities. We may not be able to maintain uniform standards, controls, procedures and policies, and this may lead to operational inefficiencies.

New acquisitions, joint ventures, new services and other transactions may require the commitment of significant capital that would otherwise be directed to investments in our existing businesses or be distributed to shareholders. Commitment of this capital may cause us to defer or suspend any common stock dividends or share repurchases that we otherwise may have made.

16

Current market volatility and difficult economic conditions may materially and adversely impact our business and results of operations.

The global capital and credit markets continue to remain depressed, resulting in the reluctance of financial institutions to lend money, an increase in commercial and consumer delinquencies, a lack of consumer confidence, and a widespread reduction generally of business activity. If these conditions continue, which may be likely for the foreseeable future, or worsen, our ability to borrow funds or obtain other financing on terms acceptable to us could be materially adversely affected. These conditions could also, among other things, negatively impact our customers' ability to pay us, the number of subscribers and purchasers of our products and services, and require us to increase our reserves for bad debt, the occurrence of any or all of which could materially and negatively impact our business, our financial condition and our results of operations.

We believe the downturn in the economy has had a negative impact on our financial results for the past two years and will also impact our fiscal year 2011 results. Our Transactional TV segment revenue decreased in fiscal year 2010 by approximately 12% despite generating incremental international revenue of $3.6 million. We experienced a downturn in our Film Production segment results during the third quarter of fiscal year 2009 and recorded goodwill and other impairment charges in connection with that segment's deterioration in performance related to the downturn in the economy in both fiscal year 2010 and 2009. Additionally, the adverse economic conditions contributed to restructuring and intangible asset impairment charges during the fourth quarter of fiscal year 2009 in connection with unfavorable results connected to an IPTV set-top box business and other initiatives within the Direct-to-Consumer segment, and we discontinued the IPTV set-top box business in the fourth quarter of fiscal year 2010. If the difficult economic conditions persist or worsen, our financial condition and results of operations would also be materially adversely impacted.

We may be unsuccessful with our initiative to expand our Transactional TV segment distribution into international markets due to our inexperience with international adult content delivery and foreign government regulations.

During fiscal year 2009, we began expanding our Transactional TV segment services into new international markets. We have not historically operated internationally or transacted with international government regulators, competitors, cultures or consumers. As a result of our inexperience, we may be unsuccessful in executing our international growth initiatives.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

We use the following principal facilities in our operations. All facilities are 100% utilized.

Colorado: We lease space in two office buildings in Boulder, Colorado. The north Boulder facility is approximately 12,000 square feet and houses our Transactional TV segment's Digital Broadcast Center, encoding and technical operations groups, content screening, and quality control functions. Our Winchester Circle facility is approximately 18,000 square feet and is used as our corporate headquarters, as well as by our Direct-to-Consumer segment's web production department and by our Transactional TV segment's marketing, sales, branding, promotions and conforming departments.

California: We lease approximately 4,600 square feet in Santa Monica, California. This facility houses our Film Production segment's production and licensing business.

We believe that our facilities are adequate to maintain our existing business activities.

17

For a discussion of legal proceedings, see Note 14—Commitments and Contingencies in the Notes to Consolidated Financial Statements included herein and incorporated herein by reference.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

No matters were submitted for a vote of the shareholders during the fourth quarter of the fiscal year covered by this report.

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Our common stock is traded on the NASDAQ Global Select Market under the symbol "NOOF".

The following table sets forth the range of high and low sales prices for our common stock for each quarterly period indicated, as reported on the NASDAQ Global Select Market:

Quarter Ended

|

High | Low | Quarter Ended

|

High | Low | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

June 30, 2009 |

$ | 2.95 | $ | 1.52 | June 30, 2008 | $ | 5.29 | $ | 3.31 | ||||||

September 30, 2009 |

2.50 | 1.87 | September 30, 2008 | 4.28 | 2.05 | ||||||||||

December 31, 2009 |

2.18 | 1.75 | December 31, 2008 | 2.56 | 1.27 | ||||||||||

March 31, 2010 |

2.40 | 1.76 | March 31, 2009 | 2.20 | 1.05 | ||||||||||

The high and low sales prices per share as reported on the NASDAQ Global Select Market on June 4, 2010, were $1.85 and $1.81, respectively. As of June 4, 2010, there were approximately 3,443 beneficial owners and 176 holders of record of New Frontier Media's Common Stock.

During each of the quarters in fiscal year 2008, the Company's Board of Directors declared a quarterly cash dividend of $0.125 per share of common stock. The Company paid approximately $9.0 million in cash dividends through March 31, 2008. Additionally, as of March 31, 2008, the Company had a dividend payable of $3.0 million that was subsequently paid in April 2008. The Board of Directors did not declare a quarterly dividend during fiscal year 2009 or 2010, and the payment of future quarterly dividends is at the discretion of the Board of Directors.

ISSUER PURCHASES OF EQUITY SECURITIES

From time to time, the Company has executed stock repurchase programs and stock purchase agreements based on current market conditions and the capital and financial position of the Company. This activity is conducted in a manner intended to comply with the safe harbor provisions of Rule 10b-18 promulgated under the Securities Exchange Act of 1934, as amended, and to minimize the impact of any purchases upon the market for its securities. Repurchased shares are returned to authorized but unissued shares of common stock in accordance with Colorado law.

In June 2008, the Company's Board of Directors extended a share repurchase plan allowing for the repurchase of approximately 1.1 million shares of common stock through June 2010. During the six month period ended September 30, 2008, the Company substantially completed the share repurchase plan and repurchased approximately 1.1 million shares for a total purchase price of approximately $4.3 million.

On November 14, 2008, the Company entered into a Stock Purchase Agreement pursuant to which a shareholder agreed to sell and the Company agreed to purchase approximately 2.6 million shares of the Company's common stock for a cash purchase price of $1.55 per share or an aggregate purchase

18

price for all of the shares of approximately $4.1 million. The Company funded the acquisition of the shares with available cash.

On March 11, 2009, the Company purchased through one broker in an unsolicited single block trade approximately 0.5 million shares of its common stock for a cash purchase price of $1.30 per share, or an aggregate purchase price for all of the shares of approximately $0.7 million. The acquisition was funded with available cash.

On August 28, 2009, the Company announced that its Board of Directors adopted a new stock repurchase program. Under the program, the Company may purchase with available cash and cash from operations up to 1.0 million shares of the Company's outstanding common stock, from time to time through open market or privately negotiated transactions, as market and business conditions permit. The program will expire in March 2012. Common stock purchases by the Company during the fourth quarter of fiscal year 2010 under this program were as follows (in thousands, except per share amounts):

Period

|

Total Number of Shares Purchased |

Average Price Paid Per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

January 1 - 31, 2010 |

— | $ | — | — | 971 | ||||||||

February 1 - 28, 2010 |

20 | 1.94 | 20 | 951 | |||||||||

March 1 - 31, 2010 |

13 | 2.22 | 13 | 938 | |||||||||

Total |

33 | $ | 2.05 | 33 | |||||||||

19

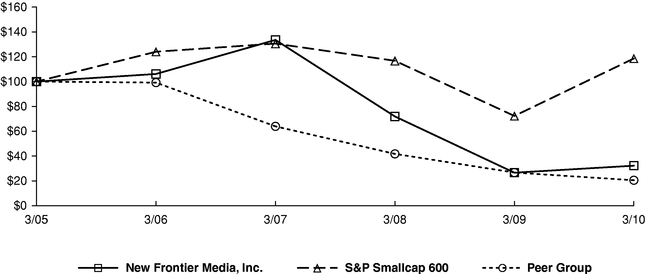

STOCK PERFORMANCE GRAPH

The following graph compares the cumulative 5-year total return provided to shareholders of New Frontier Media, Inc.'s common stock relative to the cumulative total returns of the S&P SmallCap 600 index, and a customized peer group of two companies that includes: Playboy Enterprises Inc. and Private Media Group Inc. An investment of $100 (with reinvestment of all dividends) is assumed to have been made in the Company's common stock, in the peer group, and the index on 3/31/2005 and its relative performance is tracked through 3/31/2010.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among New Frontier Media, Inc., The S&P SmallCap 600 Index

And a Peer Group

- *

- $100 invested on 3/31/05 in stock or index, including reinvestment of dividends.

Copyright© 2010 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved.

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

In accordance with the rules and regulations of the SEC, the above performance graph shall not be deemed to be "soliciting material" or deemed to be "filed" with the SEC or subject to Regulations 14A or 14C of the Securities Exchange Act of 1934, as amended, or to the liabilities of Section 18 of the Securities and Exchange Act of 1934, as amended, and shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Securities and Exchange Act of 1934, as amended, notwithstanding any general incorporation by reference of this report into any other filed document.

20

ITEM 6. SELECTED FINANCIAL DATA.

FIVE YEAR SELECTED CONSOLIDATED FINANCIAL DATA

(in thousands, except per share amounts)

| |

Year Ended March 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010(4) | 2009(3) | 2008 | 2007(2) | 2006(1) | |||||||||||

Net revenue |

$ | 50,428 | $ | 52,595 | $ | 55,911 | $ | 63,271 | $ | 46,851 | ||||||

Income (loss) from continuing operations |

$ | (1,113 | ) | $ | (2,970 | ) | $ | 8,836 | $ | 12,309 | $ | 11,283 | ||||

Income (loss) from continuing operations per basic common share |

$ | (0.06 | ) | $ | (0.13 | ) | $ | 0.37 | $ | 0.51 | $ | 0.49 | ||||

Income (loss) from continuing operations per diluted share |

$ | (0.06 | ) | $ | (0.13 | ) | $ | 0.37 | $ | 0.51 | $ | 0.48 | ||||

Weighted average diluted shares outstanding |

19,481 | 22,039 | 24,148 | 24,355 | 23,338 | |||||||||||

Total assets |

$ | 61,813 | $ | 68,539 | $ | 83,661 | $ | 88,216 | $ | 86,765 | ||||||

Long-term liabilities |

$ | 837 | $ | 1,863 | $ | 2,013 | $ | 3,684 | $ | 7,035 | ||||||

Cash dividends declared per share of common stock |

$ | — | $ | — | $ | 0.50 | $ | 0.60 | $ | — | ||||||

- (1)

- In

February 2006, the Company acquired MRG Entertainment, Inc., its subsidiaries and a related company, Lifestyles Entertainment, Inc.

("MRG").

- (2)

- Beginning

in the first quarter of fiscal year 2007, the Company adopted new standards that changed the accounting for employee equity incentive plans