Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Cheniere Energy, Inc. | form_8-k.htm |

CHENIERE ENERGY

Cheniere Energy

Corporate Presentation

April 2010

Corporate Presentation

April 2010

Safe Harbor Act

1

This presentation contains certain statements that are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of

the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements, other than statements of historical facts, included herein are “forward-looking statements.”

Included among “forward-looking statements” are, among other things:

the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements, other than statements of historical facts, included herein are “forward-looking statements.”

Included among “forward-looking statements” are, among other things:

§ statements that we expect to commence or complete construction of each or any of our proposed liquefied natural gas, or LNG, receiving terminals by certain dates, or at all;

§ statements that we expect to receive authorization from the Federal Energy Regulatory Commission, or FERC, to construct and operate proposed LNG receiving terminals by a

certain date, or at all;

certain date, or at all;

§ statements regarding future levels of domestic natural gas production and consumption, or the future level of LNG imports into North America, or regarding projected future

capacity of liquefaction or regasification facilities worldwide regardless of the source of such information;

capacity of liquefaction or regasification facilities worldwide regardless of the source of such information;

§ statements regarding any financing transactions or arrangements, whether on the part of Cheniere or at the project level;

§ statements relating to the construction of our proposed LNG receiving terminals, including statements concerning estimated costs, and the engagement of any EPC contractor;

§ statements regarding any Terminal Use Agreement, or TUA, or other commercial arrangements presently contracted, optioned, marketed or potential arrangements to be performed

substantially in the future, including any cash distributions and revenues anticipated to be received; statements regarding the commercial terms and potential revenues from activities

described in this presentation;

substantially in the future, including any cash distributions and revenues anticipated to be received; statements regarding the commercial terms and potential revenues from activities

described in this presentation;

§ statements regarding the commercial terms or potential revenue from any arrangements which may arise from the marketing of uncommitted

capacity from any of the terminals, including the Creole Trail and Corpus Christi terminals which do not currently have contractual commitments;

capacity from any of the terminals, including the Creole Trail and Corpus Christi terminals which do not currently have contractual commitments;

§ statements regarding the commercial terms or potential revenue from any arrangement relating to the proposed contracting for excess or expansion

capacity for the Sabine Pass LNG Terminal described in this presentation;

capacity for the Sabine Pass LNG Terminal described in this presentation;

§ statements that our proposed LNG receiving terminals, when completed, will have certain characteristics, including amounts of regasification and

storage capacities, a number of storage tanks and docks and pipeline interconnections;

storage capacities, a number of storage tanks and docks and pipeline interconnections;

§ statements regarding Cheniere, Cheniere Energy Partners and Cheniere Marketing forecasts, and any potential revenues, cash flows and capital expenditures which may be derived

from any of Cheniere business groups;

§ statements regarding Cheniere Pipeline Company, and the capital expenditures and potential revenues related to this business group; statements

regarding our proposed LNG receiving terminals’ access to existing pipelines, and their ability to obtain transportation capacity on existing pipelines;

regarding our proposed LNG receiving terminals’ access to existing pipelines, and their ability to obtain transportation capacity on existing pipelines;

§ statements regarding possible expansions of the currently projected size of any of our proposed LNG receiving terminals;

§ statements regarding the payment by Cheniere Energy Partners, L.P. of cash distributions;

§ statements regarding our business strategy, our business plan or any other plans, forecasts, examples, models, forecasts or objectives; any or all of which are subject to change;

§ statements regarding estimated corporate overhead expenses; and

§ any other statements that relate to non-historical information.

These forward-looking statements are often identified by the use of terms and phrases such as “achieve,” “anticipate,” “believe,” “estimate,” “example,” “expect,” “forecast,” “opportunities,”

“plan,” “potential,” “project,” “propose,” “subject to,” and similar terms and phrases. Although we believe that the expectations reflected in these forward-looking statements are reasonable,

they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which

speak only as of the date of this presentation. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors,

including those discussed in “Risk Factors” in the Cheniere Energy, Inc. Annual Report on Form 10-K for the year ended December 31, 2009, which are incorporated by reference into this

presentation. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these ”Risk Factors”. These forward-looking

statements are made as of the date of this presentation, and we undertake no obligation to publicly update or revise any forward-looking statements.

These forward-looking statements are often identified by the use of terms and phrases such as “achieve,” “anticipate,” “believe,” “estimate,” “example,” “expect,” “forecast,” “opportunities,”

“plan,” “potential,” “project,” “propose,” “subject to,” and similar terms and phrases. Although we believe that the expectations reflected in these forward-looking statements are reasonable,

they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which

speak only as of the date of this presentation. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors,

including those discussed in “Risk Factors” in the Cheniere Energy, Inc. Annual Report on Form 10-K for the year ended December 31, 2009, which are incorporated by reference into this

presentation. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these ”Risk Factors”. These forward-looking

statements are made as of the date of this presentation, and we undertake no obligation to publicly update or revise any forward-looking statements.

Cheniere Energy

Marketing

Sabine Pass LNG (SPLNG) (90.6%)

Freeport LNG (30%)

Approved Permits:

Creole Trail LNG

Corpus Christi LNG

Creole Trail P/L (100%)

Approved Permits:

Creole Trail P/L Phase II

Corpus Christi P/L

2.0 Bcf/d SPLNG TUA

MSPAs with major

LNG suppliers,

merchants, utilities

LNG suppliers,

merchants, utilities

Isle of Grain Put

Option 12 Cargoes/yr

Over 100 domestic

NAESBs and ISDAs

NAESBs and ISDAs

Pipelines

Terminals

Cheniere Business Segments

|

TUA

|

Capacity

|

2010 Full-Year

Payments ($ in MM) |

|

Total LNG USA

Chevron USA

Cheniere Marketing

|

1.0 Bcf/d

1.0 Bcf/d

2.0 Bcf/d

|

$123

$128

$252

|

Aerial view of Sabine Pass LNG

3

Sabine Pass LNG

Cheniere Energy, Inc. 90.6%

Cheniere Energy, Inc. 90.6%

§ Vaporization

– ~4.3 Bcf/d peak send-out

§ Storage

– 5 tanks x 160,000 cm (16.9 Bcfe)

§ Berthing / Unloading

– Two docks

– LNG carriers up to 266,000 cm

– Four dedicated tugs

§ Land

– 853 acres in Cameron Parish, LA

§ Accessibility - Deep Water Ship Channel

– Sabine River Channel dredged to 40

feet

feet

§ Proximity

– 3.7 nautical miles from coast

– 22.8 nautical miles from outer buoy

§ LNG Export Licenses Approved

§ Size:

– 2.0 Bcf/d

§ Diameter:

– 42-inch diameter

§ Cost:

– ~$560 million first 94 miles

§ Initial interconnects:

– 4.1 Bcf/d of interconnect

capacity

capacity

§ Provides optimal market access for LNG from the Sabine Pass terminal

§ First 94 miles complete and in-service, additional 58 miles permitted

Creole Trail Pipeline

Cheniere Energy, Inc. 100%

Cheniere Energy, Inc. 100%

|

Sold - Terminal Use

Agreement (TUA) |

Capacity

(Bcf/d)

|

Estimated Annual

Distribution to Cheniere* |

|

Conoco

Dow

Mitsubishi

|

0.90

0.50

0.15

|

$8 - $12MM

|

*Quarterly cash distributions commenced in 1Q09 and are subject to Freeport board approval.

April 2009

Freeport LNG Development, L.P.

Cheniere Energy, Inc. 30%

Cheniere Energy, Inc. 30%

Strategic Focus

§ Commercial - monetize 2 Bcf/d regas capacity at

Sabine Pass receiving terminal held by Cheniere

Marketing

Sabine Pass receiving terminal held by Cheniere

Marketing

– International LNG marketing efforts

– Seek long-term TUAs, LNG purchase/sale agreements

– Purchase spot cargoes available in the Gulf of Mexico

§ Financial - manage liquidity

J.P. Morgan Arrangement

§ Cheniere and J.P. Morgan join LNG marketing efforts

§ CMI provides all services related to:

– sourcing deals and negotiating contracts, purchasing,

transporting, receiving, storing, regasifying and selling cargoes

of LNG and regasified LNG on an exclusive basis

transporting, receiving, storing, regasifying and selling cargoes

of LNG and regasified LNG on an exclusive basis

§ JPM provides credit support

§ JPM pays a fixed fee and may pay additional fees dependent

upon gross margins achieved

upon gross margins achieved

§ JPM acquired CMI’s commercial inventory as of April 1, 2010

§ JPM has option to sign 0.5 Bcf/d TUA at $0.32/MMBtu

Source: Poten

24.2

15

7

2

Bcf/d(e)

Supply and Demand Trends

Source: GIIGNL, Cheniere Research, 2009e

Skikda

Explosion

Explosion

Schedule slippage,

underperformance

underperformance

FMs, Maintenance

YoY Change in Supply Trends

Well-below Average for Second Year

Well-below Average for Second Year

Source: Poten

Supply growth masked

by production losses

Traditional markets offset

by traded markets

YoY Changes in LNG Supply and Demand

2009 ‘Anomaly’

Europe Oversupplied but LNG Imports Up

Europe Oversupplied but LNG Imports Up

Recession induced demand reduction ~4 Bcf/d

Med

NWE

+ 109 %

(+145 cargoes)

Note: NWE = UK, BE, + Montoir

- 1.5%

(-7 cargoes, despite

addition of Rovigo in

Italy)

addition of Rovigo in

Italy)

Source: Waterborne

Source: GIIGNL. Cheniere Research , 2009 Estimated

Growth Trend in Diversion of Flexible Term Supply

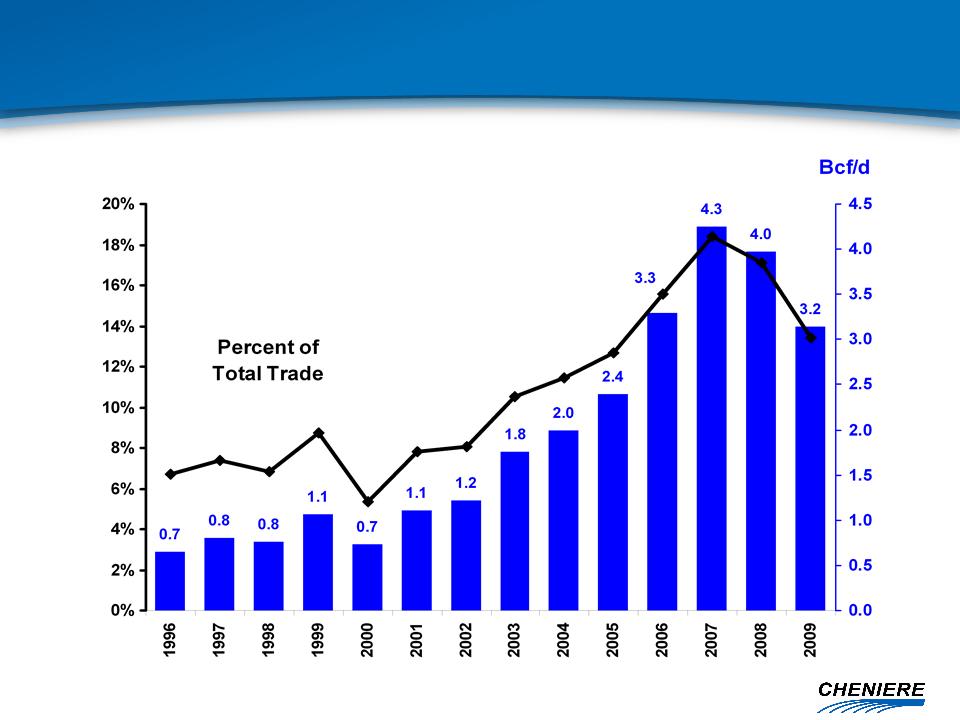

LNG Spot Trade

Source: GIIGNL. Cheniere Research , 2009e

Spot Concentrated in Atlantic Traditionally

Rapid Shift to Asia and Back

Extreme Price Movements

$20/MMBTU

$7/MMBTU

Spot Buying By Region

Traded

Liquid

Markets

Loose

Gradual Tightening

Loose

Source: GIIGNL, Cheniere Research , 2009e

Spot LNG By Destination Region

Source: Cheniere Research

Firm Liquefaction Capacity Additions

Annualized*

($ in MM)

Disbursements

§ Cheniere Marketing TUA @ Sabine Pass $252

§ G&A 30-40

§ Pipeline & tug services 10

§ Other, incl adv tax payments 3-5

§ Debt service 44

$55 - 65

*Estimates represent a summary of internal forecasts, are based on current assumptions and are subject to change. Actual

performance may differ materially from, and there is no plan to update the forecast. See “Safe Harbor” cautions. Estimates

exclude earnings forecasts from operating activities.

Net cash outflow

Estimated Future Cash Flows

Cheniere Energy, Inc.

Cheniere Energy, Inc.

Receipts

§ Freeport investment $8-12

§ Distributions from CQP 254

§ Management fees from CQP 19

Annualized*

($ in MM)

Disbursements

§ Operating Expenses $34

§ Management Fees 19

§ Debt Service 165

$285

*Estimates represent a summary of internal forecasts, are based on current assumptions and are subject to change.

Actual performance may differ materially from, and there is no plan to update the forecast. See “Safe Harbor” cautions.

Actual performance may differ materially from, and there is no plan to update the forecast. See “Safe Harbor” cautions.

Available Cash

Distributions to Unitholders

$281

Estimated Future Cash Flows

Cheniere Energy Partners

Cheniere Energy Partners

Receipts

§ TUA Customers $503

Public Unit holders

9.4% LP Interest

Cheniere Energy

Investments, LLC

Sabine Pass LNG-GP, Inc.

Sabine Pass LNG, L.P.

Sabine Pass LNG-LP, LLC

100% Ownership Interest

100% Ownership Interest

100% Ownership Interest

100% LP Interest

Non-Economic GP Interest

100% Ownership Interest

Cheniere LNG Holdings, LLC

$205 mm 2.25% Convertible Senior Unsecured Notes due 2012

$550 mm 7.25% Senior Secured Notes due 2013

$1,666 mm 7.50% Senior Secured Notes due 2016

88.6% LP Interest

100% of 2% GP Interest

100% of 2% GP Interest

NYSE Amex US: LNG

NYSE Amex US: CQP

3

$400 mm 9.75% Term Loan due 2012

$294 mm 12.0% Convertible Senior Secured Notes due

2018

2018

Note: Balances as of December 31, 2009.

Organizational Structure