Attached files

| file | filename |

|---|---|

| EX-10.6 - RINO International CORP | v179465_ex10-6.htm |

| EX-10.5 - RINO International CORP | v179465_ex10-5.htm |

| EX-21.1 - RINO International CORP | v179465_ex21-1.htm |

| EX-31.2 - RINO International CORP | v179465_ex31-2.htm |

| EX-31.3 - RINO International CORP | v179465_ex31-3.htm |

| EX-23.1 - RINO International CORP | v179465_ex23-1.htm |

| EX-31.1 - RINO International CORP | v179465_ex31-1.htm |

| EX-32.1 - RINO International CORP | v179465_ex32-1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM 10-K

|

x

|

Annual report pursuant to

Section 13 or 15(d) of the Securities Exchange Act of

1934.

|

For

the fiscal year ended December 31, 2009

|

¨

|

Transition report pursuant to

Section 13 or

15(d) of the Securities Exchange Act of

1934.

|

Commission

file number 0-52549

RINO

International Corporation

(Exact

name of registrant as specified in its charter)

|

Nevada

|

41-1508112

|

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(I.R.S.

Employer Identification No.)

|

11

Youquan Road, Zhanqian Street, Jinzhou District

Dalian,

China 116100

(Address

of principal executive offices)

00186

411 8766 1222

(Registrant’s

telephone number)

Securities

registered pursuant to Section 12(b) of the Act:

None

Securities

registered pursuant to Section 12(g) of the Act:

|

Title

of each class

|

Name

of each exchange on which registered

|

|

Common stock, par value $.0001 per

share

|

NASDAQ Global

Market

|

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes ¨ No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the

Act. Yes ¨

No x

Indicate

by check mark whether the registrant (1) has filed all reports required to

be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant

was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes x

No ¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein and will not be contained, to the best of

registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10K or any amendment to this

Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

definition of “accelerated filer,” “large accelerated filer,” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act (Check one):

Large Accelerated Filer o Accelerated

Filer o Non-

Accelerated Filer o

Smaller Reporting Company x

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act) Yes o

No x

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the Registrant (assuming for these purposes, but without

conceding, that all executive officers and directors and 10% stockholders are

“affiliates” of the Registrant) as of June 30, 2009 (based on the closing

sale price on such date of the Registrant’s common stock, on the

Over-the-Counter Bulletin Board as reported on Yahoo Finance) was

$70,469,791.

As of

March 31, 2010, there are 28,603,321 shares of common stock of the

registrant, par value 0.0001 per share issued and outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

None

RINO

International Corporation

Annual

Report on Form 10-K

For

the Year Ended December 31, 2009

Table

of Contents

|

PART

I

|

||

|

Item

1.

|

Business

|

3

|

|

Item

1A.

|

Risk

Factors

|

14

|

|

Item

1B.

|

Unresolved

Staff Comments

|

26

|

|

Item

2.

|

Properties

|

26

|

|

Item

3.

|

Legal

Proceedings

|

27

|

|

Item

4.

|

Removed

and Reserved

|

27

|

|

PART

II

|

||

|

Item 5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

27

|

|

Item

6.

|

Selected

Financial Data

|

28

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

28

|

|

Item

8.

|

Financial

Statements and Supplementary Data

|

40

|

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

40

|

|

Item 9A.

|

Controls

and Procedures

|

40

|

|

PART

III

|

||

|

Item 10.

|

Directors,

Executive Officers and Corporate Governance

|

43

|

|

Item

11.

|

Executive

Compensation

|

46

|

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

49

|

|

Item 13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

51

|

|

Item 14.

|

Principal

Accountant Fees and Services

|

51

|

|

PART

IV

|

||

|

Item

15.

|

Exhibits

and Financial Statement Schedules

|

52

|

|

Signatures

|

54

|

|

2

PART I.

Disclosure

Regarding Forward Looking Statements

Certain

statements made in this report, and other written or oral statements made by or

on behalf of RINO International Corporation, may constitute

“forward-looking statements” under the Private Securities Litigation

Reform Act of 1995, which represent the expectations or beliefs of,

including, but not limited to, statements concerning the operations,

performance, financial condition and growth of RINO International Corporation,

together with its direct and indirect subsidiaries and controlled-affiliates.

For this purpose, any statements contained in this report that are not

statements of historical fact may be deemed

forward-looking statements. Without limiting the generality of the

foregoing, when used in this report, the word “believes,” “expects,”

“estimates,” “intends,” “will,” “may,” “anticipate,” “could,” “should,” “can,”

or “continue” or the negative or other variations thereof or comparable

terminology are intended to identify forward-looking statements. Examples of

such statements in this report include descriptions of our plans and strategies

with respect to developing certain market opportunities, our overall business

plan, our plans to develop additional strategic partnerships, our intention

to develop our products and platform technologies, our continuing growth

and our ability to contain our operating expenses. All forward-looking

statements are subject to certain risks and uncertainties that could cause

actual events to differ materially from those projected, including those

described under the caption “Risk Factors” in Item 1A of this report. We

believe that these forward-looking statements are reasonable; however, you

should not place undue reliance on such statements. These statements are based

on current expectations and speak only as of the date of such statements. We

undertake no obligation to publicly update or revise any forward-looking

statement, whether as a result of future events, new information or

otherwise.

Except

as otherwise specifically stated or unless the context otherwise requires, the

"Company", "we," "us,"and "our" refer to (i) RINO International Corporation

(formerly Jade Mountain Corporation), (ii) Innomind Group Limited (“Innomind

Group”), a wholly-owned subsidiary of RINO International Corporation organized

under the laws of the British Virgin Islands, (iii) Dalian Innomind Environment

Engineering Co., Ltd. (“Dalian Innomind”), a wholly-owned subsidiary of Innomind

Group organized under the laws of the People’s Republic of China (the “PRC” or

“China”), (iv) RINO Investment (Dalian) Co., Ltd. (“RINO Investment”),

a wholly-owned subsidiary of RINO International organized under the PRC

law, (v) Dalian RINO Heavy Industries Co., Ltd. (“RINO Heavy

Industries”), a wholly-owned subsidiary of RINO Investment, organized under

the PRC laws, (vi) Dalian RINO Environment Engineering Science and Technology

Co., Ltd., a contractually controlled affiliate of Dalian Innomind organized

under the laws of the PRC (“Dalian Rino”); (vii) RINO Technology Corporation

(“RINO Technology”), a wholly-owned subsidiary of Dalian Rino under the

laws of Nevada, and (viii) and Dalian Rino’s wholly owned

subsidiaries, Dalian Rino Environmental Engineering Project Design Co., Ltd.

(“Dalian Rino Design”) and Dalian Rino Environmental Construction &

Installation Project Co., Ltd. (“Dalian Rino Installation”).

ITEM 1. BUSINESS

Through

our contractually controlled affiliates in the People’s Republic of China, since

October 5, 2007, we have been engaged in the business of environmental

protection and remediation. Our business consists of designing, manufacturing,

installing and servicing wastewater treatment and flue gas desulphurization

equipment principally for use in China’s iron and steel industry, and

anti-oxidation products and equipment designed for use in the manufacture of hot

rolled steel plate products. At the present, RINO International’s sole business

activities are acting as a holding company of our direct and indirect

subsidiaries, Innomind Group Limited, a company organized under the laws of the

British Virgin Islands, RINO Investment (Dalian) Co., Ltd. (“RINO Investment”),

a wholly-owned subsidiary of the Company under the PRC law with its wholly-owned

subsidiary in China, Dalian RINO Heavy Industries Co., Ltd.

(“RINO Heavy Industries”), and Dalian Innomind Environment Engineering

Co., Ltd. (“Dalian Innomind”), a limited liability company organized under the

laws of the People’s Republic of China (“PRC”), which contractually controls and

operates our affiliate Dalian Rino Engineering Science and Technology Co., Ltd.

(“Dalian Rino”), a limited liability company organized under the laws of the

PRC, and its subsidiaries Dalian Rino Environmental Engineering Design Co.,

Ltd.(“Dalian Rino Design”), Dalian Rino Environmental Construction and

Installation Engineering Project Co., Ltd., (“Dalian Rino Installation”) and

RINO Technology Corporation, a Nevada

corporation (“RINO Technology”).

Our

History

We were

originally incorporated in Minnesota in 1984 as Applied Biometrics, Inc. In

October 2007, through a share exchange transaction, a private financing

transaction and a restructuring transaction, we, through our subsidiaries and

variable interest entities (VIEs), currently engage in design, development,

manufacture and installation of industrial equipment used mainly for

environmental protection purposes in China.

3

The

Company’s current structure is set forth in the diagram below:

Organizational

History of Innomind Group Limited (“Innomind Group”) and Dalian Innomind

Environment Engineering Co., Ltd. (Dalian Innomind”)

Innomind

Group.

Innomind

Group Limited was incorporated under the laws of the British Virgin Islands on

November 17, 2006. Until the consummation of the Share Exchange Transaction,

Innomind Group’s sole shareholder was Zhang Ze, a citizen and resident of the

PRC.

Dalian Innomind

Environment Engineering Co., Ltd. (“Dalian

Innomind”).

On July

9, 2007, Innomind Group incorporated Dalian Innomind under the laws of the PRC.

All of Dalian Innomind’s outstanding capital stock is held by Innomind, and by

virtue of such ownership Dalian Innomind is a “wholly foreign owned enterprise

(“WFOE”) under PRC law.

Dalian

Innomind through its variable interest entity (VIE), Dalian Rino Environment

Engineering Science And Technology Co., Ltd. (“Dalian Rino”) mainly engages in

design, development, manufacture and installation of industrial equipment used

mainly for environmental protection purposes in the PRC.

4

Organizational

History of Dalian Rino Engineering Science and Technology Co., Ltd (“Dalian

Rino”), Dalian Rino Environmental Engineering Project Design Co.,

Ltd. (“Dalian Rino Design”), Dalian Rino Environmental Construction

& Installation Project Co., Ltd. (“Dalian Rino Installation”) and Rino

Technology Corporation (“RINO Technology”)

Dalian

Rino Engineering Science and Technology Co., Ltd (“Dalian Rino”)

Dalian

Rino Engineering Science and Technology Co., Ltd. (unless the context indicate

otherwise, together with its subsidiaries, collectively, “Dalian Rino”) was

formed on March 5, 2003, under PRC law. Its initial registered capital was RMB

7,000,000 (approximately US $922,327), which was increased to RMB 30,500,000

(approximately US $4,018,711) on April 18, 2006. Dalian Rino is owned by its two

founders, Zou Dejun (90%) and his wife, Qiu Jianping (10%). Since its founding,

Dalian Rino has been engaged in developing, marketing and selling its three

principal products: the Lamella Inclined Tube Settler Wastewater Treatment

System (also called the “Lamella Wastewater System”), the Circulating Fluidized

Bed Flue Gas Desulphurization System (also called the “Desulphurization

System”), and the High Temperature Hot Rolled Steel Anti-Oxidation System (also

called the “Anti-Oxidation System”).

Dalian

Rino Environmental Engineering Project Design Co., Ltd. (“Dalian Rino

Design”)

On

September 24, 2008, Dalian Rino formed Dalian Rino Environmental Engineering

Project Design Co., Ltd. (“Dalian Rino Design”), as a wholly owned subsidiary

under the laws of the PRC, to focus on research, development and the technical

design aspects of our business. Pursuant to the business permits, Dalian Rino

Design’s right of operation expires on September 23, 2018 and its business

permit is renewable upon expiration.

Dalian

Rino Environmental Construction & Installation Project Co., Ltd. (“Dalian

Rino Installation”)

On

October 14, 2008, Dalian Rino formed Dalian Rino Environmental Construction

& Installation Project Co., Ltd. (“Dalian Rino Installation”), as a

wholly-owned subsidiary under the laws of the PRC. Pursuant to its

business license, Dalian Rino Installation is permitted and will focus primarily

on installation of environmental protection and energy saving equipment. Dalian

Rino Installation’s right of operation expires on October 13, 2018 and its

business permit is renewable upon expiration.

Rino

Technology Corporation (“Rino Technology”)

On August

19,2009, Daian RINO, incorporated by Rino Technology Corporation as its

wholly owned subsidiary under the laws of Nevada, to focus on corporate business

development activities. Rino Technology will assist the business of Dalian

Rino by providing access to the contacts of innovative environmental

pollution control technologies and companies.

Organizational

History of Rino Investment (Dalian) Co., Ltd. (“Rino Investment”) and

Dalian RINO Heavy Industries Co., Ltd. (“Rino Heavy Industries”)

Rino

Investment (Dalian) Co., Ltd. (“Rino Investment”)

On

November 30, 2009, the Company incorporated Rino Investment ( Dalian ) Co., Ltd.

(“Rino Investment”) under the laws of the PRC. All of Rino Investment’s

outstanding capital stock is held by Rino International Corporation, and by

virtue of such ownership Rino Investment is a “wholly foreign owned enterprise

(“WFOE”) under PRC law. Rino Investment has its office within the Dalian

Development Zone, engaged in professional investment and business

development.

Dalian

RINO Heavy Industries Co., Ltd. (“Rino Heavy Industries”)

To expand

the production capacity, Dalian Rino Heavy Industries Co., Ltd. (“Rino Heavy

Industries”), as a foreign wholly owned subsidiary under the laws of PRC, was

incorporated on December 4, 2009 by RINO Investment. Rino Heavy

Industries, located in the Dalian Changxing Island Harbor Industrial Zone,

is a heavy machinery processing enterprise, with a large scale (450m × 290m

large) heavy industrial plant, capable of processing a wide range of mainframe

parts. Rino Heavy Industries also focuses on the research and development,

manufacturing, installing and maintaining environmental protection

equipments.

Description of the

Business

We are an

industrial technology-based, PRC environmental protection and remediation

company. Specifically, through our subsidiaries and controlled affiliates in

China, we are engaged in the business of designing, manufacturing, installing

and servicing wastewater treatment and exhaust emission desulphurization

equipment principally for use in China’s iron and steel industry, and

anti-oxidation products and equipment designed for use in the manufacture of hot

rolled steel plate products. All of our products are custom-built for specific

project installations, and we execute supply contracts during the design phase

of our projects. Our products are all designed to reduce either or both

industrial pollution and energy utilization, and comply with ISO 9001 Quality

Management System and ISO 14001 Environment Management System requirements, for

which RINO received certificates in 2004 and 2008.

Since

1978, the PRC has undergone a substantial economic transformation and rapid

economic growth, becoming the world’s fourth largest national economy, with the

world’s largest and most rapidly growing iron and steel market. Through its

continuous focus on nation-wide economic development, China’s overall industrial

pollution output has become a central issue for the national government, and a

priority in the PRC’s eleventh five-year plan. For example, in 2006 China’s

industrial enterprises emitted 25.9 million tons of sulphur dioxide, the

principal cause of “acid-rain,” and the PRC has become the world’s largest

emitter of sulphur dioxide pollution. As a consequence of this and other

industrially-based environmental challenges, Dalian Rino’s customer base -

the Chinese iron and steel industry - faces governmental mandates to decrease or

eliminate water pollution and sulphur emissions, which are key applications for

our technologies.

5

Accordingly,

environmental protection and remediation is a relatively new industry in the

PRC. Nonetheless, like the Chinese economy, it is rapidly growing – we estimate

that in the next 5 years, there is a wastewater remediation market of $260

million per year and the desulphurization market will grow at approximately 5%

annually. Further, the market for the Company’s products is highly

regulated by the central PRC government, which sets specific pollution output

targets for industrial enterprises. For this reason, we believe that the demand

for our products is predictable, and will follow the growth of the PRC’s iron

and steel industry and government-mandated pollution control standards that are

being made more stringent annually. We also believe that our revenue and

profitability growth to date arises from these same factors. Our revenues

increased by 38.3% to $192.6million in fiscal year 2009 and by 119.8% to

$139.3 million for fiscal year 2008 from $63.4 million in fiscal year 2007. Our

gross profit increased by 33.1% to $72.3million in fiscal year 2009, compared to

an increase of 78.3% to $54.3 million in fiscal year 2008 and the gross

profit of $30.5 million for fiscal year 2007. Our income from operations

increased by 142.9% to $55.3million in fiscal year 2009 and by 44.0%

to $22.8 million in fiscal year 2008 from $15.8 million. Our after-tax net

income increased by 165.0% to $56.4million and 108.3% to $21.3 million in fiscal

years 2009 and 2008, respectively, compared to that of $10.2 million

in fiscal year 2007.

Principal

Products

We have

three principal products and product lines: the “Lamella Inclined Tube Settler

Waste Water Treatment System,” the “Circulating, Fluidized Bed, Flue Gas

Desulphurization System,” and the “High Temperature Anti-Oxidation System for

Hot Rolled Steel.”

Lamella Inclined Tube

Settler Waste Water Treatment System

Our core

product, the Lamella Inclined Tube Settler Waste Water Treatment System (the

“Waste Water System”), is a highly efficient wastewater treatment system that

incorporates our proprietary and patented ‘Lamella Inclined Tube Settler’

technology. We believe that the System is among the most technologically

advanced wastewater treatment systems presently in use in China’s iron and steel

industry. It includes industrial water treatment equipment, complete sets of

effluent-condensing equipment, highly efficient solid and liquid abstraction

dewatering equipment and coal gas dust removal and cleaning equipment. The

technology has received numerous regional and national design awards, and has

been successfully installed and used at some of the largest steel mills in

China, including Jinan Iron & Steel Group Co., Ltd., Benxi Iron & Steel

(Group) Co., Ltd., Handan Iron & Steel Group Co., Ltd., Tianjin Tiangang

Group Co., Ltd., Shijiazhuang Iron & Steel Group Co., Ltd., Panzhihua

Iron & Steel Group Co., Ltd., Anyang Iron & Steel Group Co., Ltd.,

Nanchang Changli Steel Co., Ltd., Shaogang Steel Co., Ltd., Linggang Steel Co.,

Ltd. Weifang Steel Group Co.,Ltd and Puyang Steel.

Our

combination of proprietary system design and patented technology allows

wastewater to flow through the system in layers while at the same time settling

particulate matter without disturbing the water flow. Operating results of the

above, Lamella Wastewater System installations, show that our technology

improves the stability of the settling deposition, increases the available

settling area, shortens the settling distance for waste particles, reduces the

settling time, and results in particle removal efficiency rates of up to 99%.

After treatment with our technology and system, coal gas wastewater and

wastewater containing iron mineral powder can be reused and returned to the

production process without further treatment, allowing users to create a

closed-loop. This lowers the overall use of industrial water for the enterprises

utilizing our technology, reduces the output of solid industrial waste, and

improves the efficient use of resources.

Compared

with alternative inclined plate technology, the Lamella Wastewater System has

several important advantages as shown in the following table:

|

Normal Inclined Plate Settling Pool

|

Lamella Inclined Tube Settler

|

|

|

Water

power staying time 30 min, surface load 3m3/m2·h, small volume, small

space use coefficient, short waterpower process (with short current in

winter).

|

Water

power staying time 45 min with surface load 8m3/㎡·h, large

use coefficient, long water power process.

|

|

|

First

settling, is not fit for a wide range wave of floats, affected by the

stability and effect of the water outlet

|

Tertiary

settling (with sludge abstraction collection system in every layer)

anti-pump load, no interference between water inlet and sludge outlet,

water outlet stable.

|

|

Water

inlet float content: SS3000 ~ 5000mg/L, water outlet float content: SS100

~ 200 mg/L, low treatment efficiency.

|

Water

inlet float content: SS3000 ~ 16000mg/L water outlet float content: SS50 ~

80 mg/L, high treatment efficiency.

|

|

|

Inclined

plate, inclining angle 60 degree, small settling deposition

area.

|

Inclined

plate, inclined tube inclining angle 450, results show that the

smaller the inclining angle of the inclined tube or plate, the smaller the

settling particles removed, the higher settling efficiency for removal of

particulate

matter.

|

6

|

Adopt

glass steel and compound Nylon Ether ketone, easy to age degrade and

become clogged with sludge, needs to be changed often, has high operation

and maintenance costs.

|

Compound

new material plate, PP inner Surface Coating, resistant corrosion, smooth

and clean surface, minimal sludge collection.

|

|

|

Small

sludge abstraction area, bad sludge water abstraction efficiency, short

life cycle of the sludge outlet, high and unstable water content of

sludge, adds difficulty to the next sludge treatment

process.

|

With

sludge water abstraction area and dust collection transmission device,

long sludge outlet circle, special sludge disposal equipment sludge

outlet, lower water content of sludge, convenient for new process to

recycle.

|

|

The

low carbon steel structures - such as pool surface frame - exposed to

humidity and high temperature, easily corrode, which greatly reduces the

life of equipment.

|

Lamella

Inclined Tube Settler system is enclosed, the high humidity of the tank

will not cause corrosion of the equipment.

|

|

|

Occupies

large area - large footprint, strict requirement for

placement.

|

Occupying

small area - small footprint - equipment can save over 30% area to treat

same amount of water and is flexible for installation.

|

|

|

Complicated

system technique, complicated equipment configuration, high maintenance,

inconvenient for use with automated control, often creates secondary

pollution.

|

Short

technical process, simple equipment, low failure rate - high MTBF, easy

maintenance, highly automated, low operational cost, closed-end

circulating treatment, without secondary

pollution.

|

Circulating, Fluidized Bed,

Flue Gas Desulphurization System

The

Circulating, Fluidized Bed, Flue Gas Desulphurization System (the

“Desulphurization System”) is a highly effective system that removes particulate

sulphur from flue gas emissions generated by the sintering process in the

production of iron and steel (a process in which sulphur and other impurities

are removed from iron ore by heating, without melting, pulverized iron ore) with

the resulting discharge meeting all relevant PRC air pollution standards.

Without treatment, flue gasses that result from sintering contain high content

of sulphur dioxide which reacts with atmospheric water and oxygen to produce

sulphuric acid that precipitates as “acid rain.” As illustrated

below, the Desulphurization System is comprised of a desulphurization agent

inlet system, circulating fluidized bed desulphurization reactor, dust removal

system, desulphurization dust removal treatment system, desulphurization wind

pump system, monitoring system, electrical control system, and smoke flue

system.

The

Desulphurization System utilizes proprietary technology jointly developed by

RINO and the Chinese Academy of Sciences. We have the right to acquire certain

related technology from the Chinese Academy of Sciences for RMB 1,000,000

pursuant to a technology transfer agreement dated May 18, 2007.

As

compared with equipment using other desulphurization technologies, our

proprietary technology has the following advantages: our equipment has a smaller

footprint, a shorter circulation process and a low calcium sulphur ratio, the

cost of operating the system is lower; the system is more efficient with higher

desulphurization rates (for coal with a high (i.e., 6%) sulphur content,

desulphurization rates can reach 92%). Our desulphurization process does not

generate wastewater, dust or other secondary pollutants. In addition, the costs

for the manufacturing and installation of the equipment are relatively

affordable to the targeted iron and steel mills.

Although

historically we have concentrated our marketing and efforts for this system in

the PRC iron and steel industry, the technology also can be widely used in

fields such as metallurgy, electrical power generation, rubbish treatment. We

plan to expand our sales and marketing to such additional applications both in

the PRC and internationally.

7

High Temperature

Anti-Oxidation System for Hot Rolled Steel

Our High

Temperature Anti-Oxidation System for Hot Rolled Steel (the “Anti-Oxidation

System”) is a set of products and a mechanized system that substantially

reduces oxidation-related output losses in the production of continuous cast,

hot rolled steel. In the process of continuous cast, hot rolled

steel, oxidation-related output loss ranges from 2% -5% on average. This

translates into a loss of production output or throughput of

2%-5%. Our Anti-Oxidation System reduces oxidation-related output

loss by over 60%, from the current level of approximately 3% to around

1.2%. In addition, oxidation in high-temperature steel production

results in the waste of water and energy and generates pollution. In

the United States, Japan, and Europe, technology has been developed to

ameliorate this problem, but the cost of the coating used in the process and the

inability of the equipment to be utilized in high temperature environments

limits its application to specialty steel products such as stainless steel, and

silicon and carbide steel products.

Our

Anti-Oxidation System is specifically designed to work effectively with hot

rolled steel product in high temperature environment. As illustrated

below, our system operates at significantly higher product temperatures than its

competitors, thereby increasing its general utility and its range of steel

product applications. We believe that in design and technology the

Anti-Oxidation System is the only anti-oxidation process available for the iron

and steel industry (both in the PRC and internationally) that can be applied in

high temperature environments, and is a unique solution to the loss of

production output due to high-temperature oxidation, which is a long-standing

problem in the world-wide iron and steel industry.

The

technology used in our Anti-Oxidation System is jointly developed by Dalian RINO

and the Chinese Academy of Sciences. In March, 2006, Dalian Rino acquired the

technology from the Chinese Academy of Sciences under an agreement that provides

for the co-ownership of the intellectual property rights to the formula for

the anti-oxidizing paint used in the system and to the spray system for applying

the paint, co-ownership of any patents granted, and the transfer to Dalian Rino

of all commercialization rights.

As hot

rolled steel consists of approximately 90% of the PRC steel production and 90%

of world-wide production, we believe that our technology has a far broader

market both in China and internationally than is the case for competing systems

and technologies.

Each unit

of our Anti-Oxidation System services one steel line and costs approximately

$1.4 million installed. The coating material developed by Dalian Rino

for use with the anti-oxidation equipment can be produced at relatively low cost

at approximately $1,264 per ton which covers approximately 1180 tons of steel.

The coating material is usable in high temperature environments and is easily

applied in a uniform manner. That coating can be directly sprayed onto hot steel

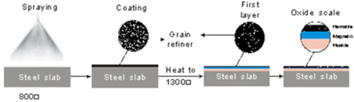

slabs at temperatures of 600°-1000° C, thereby saving the increased costs and

energy utilization that all other anti-oxidation equipment entails.

In July

2007, our Anti-Oxidation System has first been installed, tested and accepted by

Jinan Iron & Steel Group Co., a major PRC steel manufacturer. The

installation results show that the coating system fully conforms to the hot

rolling mill environment, effectively reduces oxidation loss by 60%, saves

energy, and increases production throughput.

Contract

Machining Services

In

addition to the environmental remediation and protection systems above, since

late 2005 we have also being using our over capacity during “down time” to

perform contract machining services for third-party industrial

enterprises.

The

specialized heavy machinery and equipment that we use to produce our Lamella

Wastewater System, Desulphurization System and Anti-Oxidation System also

provides us with a substantial capacity to undertake the machining of

large, high-precision and advanced structures. To this end, Dalian Rino

established and the Company maintains strategic cooperation relationships

with Dalian Heavy Industry (Zhonggong) and China First Heavy Industries with

which we contract to provide production time on our heavier machine tools,

during “down time” on our own production. For fiscal years 2007, 2008 and 2009,

such contract manufacturing business has provided the Company with $21,313,500,

$19,422,523 and $5,169,434 in revenues, respectively, and $13,134,648,

$9,322,907 and $2,311,315 in gross profit, respectively.

We expect

that as sales of its own products increase, we will reduce or eliminate

contracting the use of our machines and equipment to third parties.

New

Products and Product Development

Sludge Treatment

System

In

November 2008, Dalian University of Technology successfully developed a new

sludge treatment system with our cooperation. The new sludge treatment system

can be used to treat sludge generated by the municipal wastewater treatment

process, industrial sludge generated by the chemical industry and oil sludge

generated by oil industry. We estimate that there is a market of approximately

$28.8 billion for the treatment of sludge generated by various municipal

wastewater and industrial processing systems in the PRC market. To

treat the sludge, the first and most critical step is to remove water from the

sludge through a dehydration process, which will reduce the quantity of the

sludge and make it easier to be incinerated. Depending on the heavy metal

content of the desiccated sludge, the final product can be used as agricultural

fertilizer if the heavy metal content is low, or, after further processing, as a

component in various construction materials if

the heavy metal content is high.

8

We

believe the current best sludge treatment technology available in the PRC market

(provided by third parties) allows for a 30% reduction of water in the sludge

while our technology, using superheated steam to dehydrate sludge, provides an

improvement of 10% in water reduction. In addition, our new sludge

treatment system costs approximately 50% less than imported products and the

costs of daily operation are approximately 45% less. The Chinese government

recently promulgated a new regulation requiring at least 60% of municipal

wastewater be treated by 2010, the implementation of which is expected to

significantly increase the amount of sludge generated by the wastewater

treatment process in China in the next several years. We estimate the profit to

process one ton of sludge generated by municipal wastewater treatment process

varies between $12 and $19 depending on the steam source. Currently,

approximately 27.8 million metric tons of sludge is being generated by the

wastewater treatment process annually with a water content of approximately

80%.

We

believe Northeastern China, where Dalian RINO is located, is the oil industry

center and this region generates approximately 2 million tons of oil sludge

annually. We estimate the profit to process one ton of oil sludge averages

$30.

Dalian

University of Technology has made a patent application for this technology in

China (Application number: 200710011115.0). Based our agreement with

Dalian University of Technology, Dalian Rino will pay an ongoing royalty of

approximately 5% of sales to the university. As of the date of this Report,

Dalian Rino has not paid out any royalty to Dalian University of

Technology.

DXT

System

In early

September 2009, we commenced installation of our new proprietary ammonia-based

desulphurization system (the "DXT system") on a 280 m2 sinter system at Hunan

Lianyuan Iron and Steel Company. The total contract value is

approximately $10 million with the installation scheduled to be completed during

the second quarter of 2010. The DXT system utilizes a

technology, through a contractual arrangement , that has been applied by

Baosteel Group Co., China's largest steel producer, to its manufacturing process

during the past 10 years. Our DXT system applies such technology, to

the best of our knowledge for the first time, in the desulphurization process in

China's iron and steel industry. Our new DXT operating system

utilizes coking waste ammonia in the flue gas to effectively remove the sulphur

dioxide from the sinter flue gas and produces ammonia sulfate as a by-product,

which can be used as fertilizer. We believe that in addition to our

commitment to filtering out up to 99% of the harmful sulphur

emissions, the DXT system utilizes less energy, decreases operating and

maintenance costs, and creates a sustainable revenue generating activity through

the production of fertilizer. The Chinese government strongly

supports technologies which are both environmentally friendly and

economical. Our customers in the iron and steel manufacturing

industry that use the DXT system will be eligible for tax credits and government

subsidies to offset the costs.

Environmental

Challenges in the PRC

China

currently had been in the midst of extraordinarily rapid economic growth and

reform that is closely tied to its pace of industrial development. In 2004, the

PRC’s total industrial output reached RMB 7,238.7 billion (US $934 billion).

Since 1978, China’s real GDP has grown at an average rate of approximately 11.3%

per year, while its share of world trade has risen from less than 1% to almost

8% in the same timeframe. Foreign trade growth has averaged nearly 15% over the

same period, or more than 2,700% in the aggregate. Over the last decade the PRC

has become a preferred destination for direct foreign investment, and in

2005 attracted $72.4 billion in foreign direct investment, according to the

Chinese Ministry of Commerce. China also is competitive in many advanced

technologies and continues to be a preferred destination for the relocation of

global manufacturing facilities in virtually every manufacturing sector. China

is now the fourth largest economy and the third largest trader in the

world.

With the

PRC’s rapid industrial expansion has come its inevitable by-product:

industrially generated pollution of water, the air and the environment,

generally. It is estimated that approximately 80% of China’s environmental

pollution results from industry-produced solid waste, waste water and waste gas

emissions. During the 1990’s the extent of and dangers posed by China’s

increasing levels of environmental pollution became widely perceived and

developed into a priority for the PRC’s central government. During the 2000-2005

period, China expended over $90 billion on environmental protection efforts.

Prior to the global financial crisis, for the eleventh five-year plan

(2006-2010), the PRC is expected to spend approximately $193 billion on such

efforts. The reduction or elimination of waste water and airborne pollutants has

become a key element in the country’s next five year economic plan.

In

addition, in response to the recent global financial crisis, the PRC government

introduced a 4 trillion RMB stimulus program on November 27, 2008. The stimulus

package - to be spread over a period of two years - aimed to boost the

slowing Chinese economy by spurring domestic spending and demand, as its GDP

growth slid to 9% in 2008 after years of double-digit growth. On February

26, 2009, China’s State Council reinforced China’s 2008 stimulation package by

further measures to stimulate specific industries in 2009. Specifically, 5.3% of

the total stimulus package will be spent on sustainable development that

promotes energy saving and environmental control.

Based on

the breakdown of the stimulus spending unveiled by China’s top economic planner,

the National Development and Reform Commission (NDRC), the percentage allocation

of the total stimulus package is as follows: approximately 38% to public

infrastructure (such as railway, road, irrigation, and airport construction),

25% to post-quake reconstruction (construction of low-cost housing,

rehabilitation of slums, and other social safety net projects), 9% to

technology advancement (projects to upgrade the Chinese industrial sector,

gearing towards high-end production to move away from the current

export-oriented and labor-intensive mode of growth), 5% to

sustainable development (projects to promote energy saving and cuts in harmful

gas emissions, and environmental engineering projects), 4% to educational &

cultural projects and 9% to rural development (building public facilities,

resettling nomadic people, supporting agriculture works, and providing safe

drinking water).

9

Serving

the environmental control needs for the iron and steel industries, we believe we

stand to benefit from the stimulus spending on both environment control related

projects and from the growth of the iron and steel industries which will be

beneficiaries of the infrastructural spending under the stimulus

package.

PRC

Markets for Dalian Rino’s Products and Technologies

Wastewater Treatment

Market.

China is

a country that has limited water resources, with approximately 2,200 cubic

meters per person, or one-fourth the world average. Conservation through the

improvement of usage efficiency is the fundamental way to resolve this tension

between water supply and demand. China’s very high rate of industrial water

consumption (as compared to that of developed countries) offers great potential

for water conservation and re-usage programs. Our principal target market, the

iron & steel industry, consumes large quantities of water by the nature of

the processes employed, and, therefore, has an inherent need to increase

efficiency and thereby reduce its usage costs, as well as reclamation costs and

governmental penalties.

Today,

there are approximately 730 iron-making blast furnaces over 300 cubic meters in

size operating in China. Of these, 495 have already adopted wastewater treatment

facilities, some of which are utilizing the traditional inclined plate settling

pool technology, while 235 have no wastewater treatment whatsoever. The average

cost of equipment for wastewater treatment of a blast furnace of this size is

$2,000,000. Additionally, there are 670 steel-making converters in China with a

capacity of over 75 tons. 360 of these converters have existing wastewater

treatment equipment, while 310 converters have no wastewater treatment

facilities whatsoever. The average cost of equipment for a

converter of this size is $1,700,000. The PRC government has mandated that all

blast furnaces and converters have wastewater treatment facilities in place by

2012. Accordingly, these mandates have created a $216 million annual market for

the next several years.

In

addition to the blast furnaces and converters with no wastewater treatment

facilities, we believe that there is a large replacement market potential for

those operations with wastewater treatment systems that utilize the traditional

inclined plate settling pool technology. This is older technology introduced by

the former Soviet Union in the late 1970s and applied in iron and steel industry

in the 1980s. Compared with our proprietary Lamella Wastewater System

technology, wastewater treatment systems using the traditional inclined plate

settling pool technology has lower throughput capability, a much larger

footprint and involves high maintenance requirements and expenses. Based on our

market research with our end-use customers as well as market investigation with

other iron and steel foundries and mills, we believe there will be a substantial

need to replace this aging technology in 10 years, thereby creating an

additional market of $87,900,000 for blast furnace and converter retrofits based

on an average cost of $2 million to retrofit a blast furnace and $1.7 million to

retrofit a converter.

Using

proprietary and patented technology which removes up to 98% of particulates,

producing 100-150 m3 of effluent water per hour with an average of 50mg/L of

particulates, we believe our Lamella Wastewater System has been a market leader

for wastewater treatment in the iron & steel industry. For fiscal

years 2008 and 2009, revenues generated from our wastewater treatment business

was $14.4 million and $46.0million, respectively, representing 10.4% and 23.9%

of our total revenues for fiscal years 2008 and 2009, respectively.

Desulphurization

Market

In China,

the main cause of airborne pollution is sulfur dioxide emissions from coal.

According to joint research by the Chinese Institute of Environmental Science

and Tsinghua University, sulphur dioxide-induced acid rain costs China over

$13.3 billion annually in various losses, and atmospheric pollution results in

an annual loss equivalent to two or three percent of China's GDP.

In 2005,

the latest year for which statistics are available, the Chinese iron & steel

industry discharged 1.24 million metric tons of sulphur dioxide into the

atmosphere. Decades of lightly monitored growth in this industry sector, with

little or no consequences attached to sulphur dioxide emissions, combined with

mandatory, industry-wide sulphur dioxide reductions over the next few years,

presents the industry with a pressing need to remediate these emissions from

iron & steel sinters.

Based on

government mandates, over the next few years, coal-fired sinters and other like

furnace operations must install desulphurization equipment or face stiff,

monthly penalties or, possibly, have their operations shut down. We believe

that, because our Desulphurization System is the only sinter processing

equipment available in the PRC market that is specifically designed for flue gas

desulphurization applications that are larger than 90 square meters - the

standard size for sinter operations in the PRC iron & steel industry - the

Company has a substantial competitive advantage over its international

competitors.

Today,

there are around 200 coal-fired sinters in China without flue gas

desulphurization equipment (this number is expected to rise along with the

expansion of China’s iron and steel industry). Prior to June 2008,

government policy only capped total gas emissions in a geographic area and there

was no restriction on the gas emissions of any individual coal-fired sinter.

Accordingly, some coal-fired sinters only had desulphurization equipment that

partially treated their gas emissions and some had no desulphurization equipment

installed so long as the emission cap in the area was not

exceeded. After June 2008, the government tightened gas emission

control and is now requiring all coal-fired sinters to have desulphurization

equipment installed. This translates into a cumulative market for our

desulphurization technology of more than $1 billion in the next few years based

on our estimate. We plan to penetrate this market aggressively by marketing the

Desulphurization System as a turn-key solution for the Chinese iron & steel

industry’s sulphur dioxide emission problems.

10

Our

desulphurization system has been installed in steel mills such as Jinan Iron

and Steel Co., Panzhihua Iron & Steel, Shengfeng Iron & Steel,

Handan Iron & Steel, Chongqing Iron & Steel. and Kunming Iron

& Steel, Hulingnianyuan Iron and Steel, Nanchangchangli Iron & Steel,

Qianjing Iron & Steel ,Yuhua Iron & Steel, Zhuhai Yueyufeng Iron &

Steel,Hefei Iron &Steel, Jiangsu Xigang Iron &Steel, Zhangdian Iron

& Steel and Hunan Lianyuan Iron &Steel . For fiscal

years 2008 and 2009, revenues generated from our desulphurization business was

$105.3 million and $116.4 million, respectively, representing 75.6% and 60.4% of

our total revenues for fiscal years 2008 and 2009, respectively.

Anti-Oxidation

Market

The

oxidation of hot rolled steel results, on average, in the loss of 3% of the

output in steel production. Although a number of U.S. and European

anti-oxidation systems are available internationally, the high costs of the

paints and coatings they use, as well as their ineffectiveness at high

temperatures, have limited their application and utility to low temperature,

specialty steel products. The suppliers of these anti-oxidation systems include

America Advanced Technical Products, ATP Metallurgical, Duffy, Condursal, and

Berktekt. Because of the high cost of usage, these paint/coating systems are all

applied on only specialty steel and additionally, have limitations of low

temperature application - they cannot be used on-line.

Importantly,

the temperature range limitations of these systems prevent them from being used

“on-line” in the high temperature ranges of hot rolled steel products, which

historically account for over 90% of the PRC’s crude steel production. China is

estimated to have produced approximately 500 million tons of steel in 2008, of

which the expected output of hot rolled steel is estimated at 450 million tons.

On this basis, it can be expected that, if not treated, China would lose

approximately 13.5 million tons from its 2008 hot rolled steel production - a

volume that is equal to a large steel producer’s annual output. Unlike its

international competition, our Anti-Oxidation System is specifically designed to

use less costly coating material and to operate effectively at temperatures

ranging from 600° - 1,000° C - the environment of hot rolled steel plate. Based

on the confirmed results of the installation of our anti-oxidation equipment and

technology at Jinan Iron & Steel in 2007, we believe that the Anti-Oxidation

System reduces hot rolled steel oxidation loss by a minimum of 60%. This would

have resulted in an increase of 8.1 million tons of China’s 2008 output, and

estimated commensurate savings in coal (6.4 million tons) and water (80 million

tons) consumption for processing and throughput.

Using the

PRC hot rolled steel estimate for 2008 as a benchmark, we estimate that the full

application of the Anti-Oxidation System to that projected production output

would result in approximately $567,000,000 in water and cost savings per

year.

With

these factors in mind, we believe that our Anti-Oxidation System can achieve a

significant degree of penetration in the PRC market, as it addresses a domestic

production need which is beyond the applicability of presently available U.S.

and European technologies and systems.

For

fiscal years 2009 and 2008, revenues generated from our anti-oxidation business

was $25.1 million and $5.7 million, respectively, representing 13.0% and 4.1% of

our total revenues for fiscal years 2009 and 2008, respectively.

Raw

Materials Supply

The

principal raw materials used in our business are steel and steel products,

ancillary components used in our final products (such as motors), electrical

cable, lubricants, cutting and welding material, and special plastic tubes used

in our wastewater treatment system. Our principal suppliers, Dalian

Shuntongda Trading Co., Ltd. and Dalian Shuangying Trading Co., Ltd., provided

approximately 93% of the Company’s purchases of raw materials for the year ended

December 31, 2009 and 88% of the Company’s purchase of raw materials for the

year ended December 31, 2008. Dalian Shuntongda is well connected in the iron

and steel industries and can obtain steel and steel products from numerous

suppliers in the PRC market at favorable (often below market)

prices. In addition, we are able to purchase steel and steel products

from other suppliers and we intend to work with other qualified suppliers if the

supply terms are more competitive than the existing terms available to

us.

Intellectual

Property

Set forth

below is a list of the patents that we own or with regard to which we have

submitted applications for patent approval:

11

|

Jurisdiction

|

Project description

|

Patent No.

|

Patent type

|

Patent Status

|

Expiration

Date

|

|||||

|

China

|

Desilting

Inclined Plate and Tube Settler in Full Automation

|

200920010319.7

|

Practical

new

|

Granted

|

January

2010

|

|||||

|

|

|

|

||||||||

|

China

|

Inclined

Plate and Tube Settler of Deposition with Three Continuous

Processes

|

200920010318.1

|

Practical

new

|

Granted

|

January

2019

|

|||||

|

China

|

Slurry

Cleaning Equipment

|

032119135

|

Practical

new

|

Granted

|

March 13, 2013

|

|||||

|

China

|

Wastewater

comprehensive treatment system and method

|

ZL03111178.5

|

Invention

patent

|

Granted

|

March

13, 2023

|

|||||

|

PCT

International

|

Antioxidation

Coating for Steel and Antioxidation Method Using the Same

|

7494692

|

Invention

patent

|

Granted

|

April

3, 2028

|

|||||

|

|

|

|

||||||||

|

China

|

Desulphurization

Process of Sintering Flue Gas

|

200810128193.3

|

Invention

patent

|

Application

under review

|

||||||

|

PCT

International

|

Inorganic

Composite Binders with High-temperature Resistance

|

PCT/CN2007/000568

|

Invention

patent

|

Application

under review

|

||||||

|

|

|

|

||||||||

|

PCT

International

|

Anti-oxidation

Spray Methods and Spray Equipment for Steel Billets

|

PCT/CN2007/001475

|

Invention

patent

|

Application

under review

|

||||||

|

China

|

Sintering

Flue Gas Desulphurization Process

|

200810128193.3

|

Invention

patent

|

Application

under review

|

||||||

|

China

|

Desulphurizing

Tower Used in Ammonia Method Desulphurization

|

200920168767.X

|

Practical

new

|

Application

under review

|

||||||

|

China

|

Municipal

Solid Waste Incineration Process and System Based on Mechanical-Biological

Pre-treatment

|

200910010923.4

|

Practical

new

|

Application

under review

|

||||||

|

China

|

Municipal

Solid Waste Incineration System Based on Mechanical-Biological

Pre-treatment

|

200920012515.8

|

Invention

patent

|

Application

under review

|

International

patent applications are administered under the Patent Cooperation Treaty (the

“PCT”). A PCT application covers all the PCT member countries, which include

most major industrialized countries. The PRC became a member of the PCT in

1994.

There are two phases in a

PCT application. The first phase is the International Phase. Under this phase,

an applicant like the Company can file an application using Chinese language in

the PRC. Then it will have one year to claim the priority of its PRC filing date

in other member countries. The main benefit of filing under the PCT instead of

directly in the member countries is to allow an applicant to delay the “National

Phase” filing in the member countries up to 30 months from the initial filing,

which is 18 months more than the applicant would normally have when filing

directly in foreign countries. During this International Phase, the applicant

can gather more market information and have more time to make decisions about

where to file patent applications. At the end of the International Phase period,

it will enter the National Phase by filing national applications in each country

in which the applicant desires a patent. The Trade-Related Aspects of

Intellectual Property Rights (the “TRIPS”) determine the term of a patent

applied under the PCT in the member countries.

Trademark and

Logo.

The

Chinese version of the “RINO” trademark, 绿诺, and associated

logo are both registered by Dalian Rino in the PRC. Their perpetual,

royalty-free use by Dalian Innomind is authorized as part of the Restructuring

Agreements.

Other Intellectual Property Rights

Protections in the PRC.

In

addition to patent protection law in the PRC, we also rely on contractual

confidentiality provisions to protect our intellectual property rights and our

brand. The Company’s research and development personnel and executive officers

are subject to confidentiality agreements to keep our proprietary information

confidential. In addition, they are subject to a three-year covenant not to

compete following the termination of employment with our Company. Further, they

agree that any work product belongs to our Company.

12

Customers

Historically,

we generate revenues from large scale projects based on long-term fixed price

contracts with customers for the manufacturing and installation of customized

industrial equipment. Due to the size of our projects, we generally

work on a limited number of projects with a limited number of customers at any

given period of time. Generally, each of our projects involves the

manufacturing, installation and testing of the equipment we sell. Due to the

size of our projects and the length of time to complete our projects (averaging

six to eight months), it appears that our revenues are generated from a limited

number of customers at any given period of time. However, we do not

rely on a limited number of customers for revenue generation over time, as they

constantly change. Nevertheless, given the cost of our Lamella

Wastewater System, Desulphurization System and Anti-Oxidation System products,

we believe that for the foreseeable future the Company will continue to rely on

large customers for a substantial portion of its gross revenues. There are

approximately 34 iron and steel companies in the PRC of a size and with annual

production levels that make our products feasible for sale and

installation. In order to expand our sales, we plan to capture

increasing numbers of these potential customers for primary product sales, and

aggressively cross-sell our products to each customer. In fiscal

years 2009 and 2008, we enlarged our customer base and revenue generation

was much less concentrated. As a result, 2009 revenues generated from

our top customers in prior years did not account for a large percentage of

total revenues in fiscal year 2009. In fiscal years 2009 and 2008, revenues

generated from our top six customers accounted for 33.38% and 34.78% of our

total gross revenues, respectively.

During

the year ended December 31, 2009 and 2008, the Company has no customer accounted

for more than 10% of the Company’s total sales.

Competition

Lamella

Wastewater System.

Prior to

Dalian Rino’s introduction of its Lamella Wastewater System, the typical

industrial wastewater treatment technology used in China relied on an inclined

“plate settling pool” process. Such systems continue to be generally available

in the PRC, and a substantial portion of them are self-installed by iron and

steel companies. The Lamella Wastewater System’s advanced technology

results in the following competitive advantages: lower installation and usage

costs, increased throughput, smaller equipment footprint, and lower ongoing

maintenance costs. We know of no comparable technology presently available in

China, and we will emphasize the foregoing cost and efficiency advantages as we

compete for customers.

Desulphurization

System.

In the

PRC, the sulphur dioxide emitted in flue gases from the sintering of iron

during steel-making, is a major component of the environmental pollution that

has followed China’s industrial expansion. Sintering is a step in steel-making,

in which sulphur and other impurities are removed from raw iron by heating

(without melting) pulverized iron ore. Removing the sulphur dioxide from a steel

mill’s hot flue gas emissions is, therefore, a principal way of controlling acid

rain.

Presently

in China, major companies engaged in the desulphurization equipment market

include: Beijing Guodian Longyuan Environmental Company, Zhejiang Feida Company,

Fujian Longjing Environmental Company, Wuhan Kaidi Electric Power Company,

Jiulong Electric Power Company, and Qinghua Tongfang Company. To the best of our

knowledge, these companies have little or no production and installation

experience in the iron and steel industry, and do not currently design or

manufacture equipment that is applicable to sintering processes. We believe we

are the first company to design, manufacture and complete an iron and steel

sinter machine desulphurization installation in the PRC. Accordingly, we do not

expect to have any direct competitors in this sector for approximately 2-3 years

- the minimum time necessary for potential competitors to complete product

development.

Anti-Oxidation

System.

We

believe that the Company’s Anti-Oxidation System is unique and virtually without

competition in the China market. We know of no entity other than the Company

that is engaged in developing or supplying anti-oxidation technology that can

operate on-line at the high temperatures (600° - 1,000° C) involved in hot

rolled steel production - which represents 90% of China’s steel output. A number

of anti-oxidation technologies are available internationally from suppliers that

include: Advanced Technical Products Company, ATP Metallurgical Coatings, Duffy

Company, Condursal and Berktekt. However, the high costs of the anti-oxidizing

coatings these technologies rely on, and most especially their ineffectiveness

at high temperatures, have limited their market to specialty steels, and have

made them ill-suited to China’s iron and steel industry.

Research

and Development; Growth Strategy

In 2009,

we expended approximately $0.22 million for product research and development,

approximately $0.22 million of which was directed at flue gas

desulphurization. In 2008, we expended approximately $0.7 million for

product research and development, approximately $0.6 million of which was

directed at flue gas desulphurization and approximately $0.1 million was

directed at the sludge treatment system. The Company’s continuing research and

development program is linked to our growth strategy directed towards 2010 and

several years thereafter, during which time we will develop export markets for

our products in the United States and Western Europe and seek to develop new

applications for our products suited to and targeted at these new, international

markets. In conducting our research and development, the Company

expects to continue its collaborative relationship with the Chinese Academy of

Sciences, and also collaborate with Dalian Technology University.

13

Recent

Development

Changxing Island

Land

On March

2, 2010, Rino Heavy Industry entered into a Purchase Agreement for Land Use

Right of State-Owned Construction Site (the “Agreement”) with Dalian City Land

Resources and Housing Bureau of Liaoning Province of PRC (the “Seller”) for the

land located at Enterprise District, Lingang Industrial District, Changxing

Island, Dalian (the “Changxing Island Land”). Such land is intended for

industrial use only. The purchase price for the land use right is in an

aggregate amount of RMB 51,239,320 (or approximately $ 7,516,808 based on the

exchange rate of ) (the “Purchase Price”). Under the Agreement, the Purchase

Price shall be paid off in a lump sum payment within 60 days after execution of

the Agreement. Rino Heavy Industry will be subject to penalties of 1‰ of the

Purchase Price for each day of late payment. Rino

Heavy Industry also covenants under the Agreement that total investment of the

projects to be constructed on the Changxing Island Land shall be no less than

RMB 636,532,098 (or approximately $ 93,379,259).

2009 Registered Direct

Offering

On

December 7, 2009, the Company consummated a registered direct offering (the

“2009 Registered Direct Offering”) to select investors of an aggregate of

3,252,032 shares of common stock of the Company, par value $0.0001 per share

(the “Common Stock”), Series A Common Stock Warrants, which are exercisable

within six months of the closing date, to purchase up to an aggregate of

1,138,211 shares of Common Stock at an exercise price of $34.50 per Warrant (the

“Series A Warrants”) and the Series B Common Stock Warrants, which are

exercisable beginning on the six month one day anniversary of the closing date

until the one year one day anniversary of the closing date, to purchase up to an

aggregate of 1,138,211 shares of Common Stock at an exercise price of $34.50 per

Warrant (the “Series B Warrants”; together with the Series A Warrants, the

“Warrants”). Rodman & Renshaw, LLC served as sole placement agent in the

2009 Registered Direct Offering.

Establishment of New

Subsidiaries

During

the fiscal year of 2009, we incorporated three new subsidiaries: (i) Daian

RINO incorporated Rino Technology Corporation, a Nevada corporation, (ii) Rino

Investment (Dalian) Co., Ltd. (“Rino Investment”) a PRC company; and (iii)

Dalian Rino Heavy Industries Co., Ltd. (“Rino Heavy Industries”), a PRC company.

For more details, please refer to the “Organizational History” of our

subsidiaries under Item 1”Our Business” herein.

Waiver and Reduction of

Liquidated Damages

On April

3, 2009, the Company entered into a Waiver and Amendment Agreement (the

“Amendment Agreement”) with certain holders of the shares of the Company’s

common stock representing holders of a majority in interest of the shares of the

Company’s common stock issued in the private placement transaction consummation

on October 5, 2007 (the “2007 Private Financing”). The Amendment

Agreement amends the relevant provisions of the Securities Purchase Agreement

and the Registration Rights Agreement that the Company entered into with the

investors in the Private Financing, such that (i) no amount of liquidated

damages shall have been incurred and payable to the investors due to the late

appointment of independent directors, (ii) the liquidated damages incurred due

to the late effectiveness of the registration statement shall be paid in the

form of shares of the Company’s common stock of up to 192,045 shares, or, at the

election of each investor, in cash of (up to an aggregate of $860,362 for all

investors).

Upon

effectiveness of the Amendment Agreement, each holder of the Company’s

common stock issued in the Private Financing is required to elect, by written

notice to the Company, whether to receive shares of the Company’s common stock

or cash as provided by the Amendment Agreement. Pursuant to the

Amendment Agreement, as of the date of this report, the Company issued an

aggregate of 47,854 shares of the Company’s common stock and paid an aggregate

of $606,300.66 to the investors.

ITEM

1A. RISK FACTORS

An

investment in our common stock involves a high degree of risk. You should

carefully consider the risks described below and the other information contained

in this report before deciding to invest in our common stock.

If any of

the following risks, or any other risks not described below because they are

currently unknown to us or we currently deem such risks as immaterial but they

later become material, actually occurs, it is likely that our business,

financial condition, and operating results could be seriously harmed. As a

result, the trading price of our common stock could decline and you could lose

part or all of your investment.

Risks

Related to our Business

The

recent global financial crisis could negatively affect our business,

results of operations, and financial condition.

The

recent credit crisis and turmoil in the global financial system may have an

adverse impact on our business and our financial condition, and we may face

challenges if conditions in the financial markets do not improve. Our

ability to access the capital markets may be restricted at a time when we would

like, or need, to raise capital, which could have an impact on our flexibility

to react to changing economic and business conditions. In addition,

these economic conditions also impact levels of commercial and

consumer spending, which have recently deteriorated significantly and may remain

depressed for the foreseeable future. It is uncertain how long the

global crisis in the financial services and credit markets will continue and how

much of an impact it will have on the global economy in general or the Chinese

economy in particular. If demand for our products and services

fluctuates as a result of economic conditions or otherwise, our revenue and

gross margin could be harmed.

14

Pollution

control for China’s iron and steel sector is a relatively immature and growing

sector, but we do not know how sensitive we might be to a slowdown in economic

growth or other adverse changes in the PRC economy which might affect demand for

iron and steel pollution control equipment. A slowdown in overall economic

growth, an economic downturn, a recession or other adverse economic

developments in the PRC could significantly reduce the demand for our products

and harm our business.

Although

compliance with environmental regulations suggests continued growth with respect

to our target market, we believe that the success and growth of our business for

the foreseeable future will continue to depend upon the sustained presence of

clients in our target markets, primarily associated with the iron and steel

industries. Our client's need to comply with government

regulations extends only to the degree that they survive the current economic

crisis. As such, many of our customers may be subject to

budgetary constraints and our continued performance under our contracts

could be jeopardized by spending reductions or budget cutbacks at these

clients.

Our limited operating history may

not serve as an adequate basis to judge our future prospects and results of

operations.

Dalian

Rino began its operations in 2003. Our limited operating history in the

environmental protection industry may not provide a meaningful basis on which to

evaluate our business. Although Dalian Rino’s revenues have grown rapidly since

its inception, we cannot assure you that we will maintain our

profitability or that we will not incur net losses in the future. We expect

that our operating expenses will increase as we expand. Any significant failure

to realize anticipated revenue growth could result in significant operating

losses. We will continue to encounter risks and difficulties frequently

experienced by companies at a similar stage of development, including our

potential failure to:

|

|

·

|

maintain

our cutting edge proprietary

technology;

|

|

|

·

|

expand

our product offerings and maintain the high quality of our

products;

|

|

|

·

|

manage

our expanding operations, including the integration of any future

acquisitions;

|

|

|

·

|

obtain

sufficient working capital to support our expansion and to fill customers’

orders in time;

|

|

|

·

|