Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE - WEST PHARMACEUTICAL SERVICES INC | pressrel.htm |

| 8-K - FORM 8K BARCLAYS CAPITAL - WEST PHARMACEUTICAL SERVICES INC | form8k.htm |

1

Donald E. Morel

Chairman and Chief Executive Officer

William J. Federici

Vice President and Chief Financial Officer

Investor Relations Contact:

Michael A. Anderson

Vice President and Treasurer

mike.anderson@westpharma.com

Barclays 2010 Global Healthcare Conference

Miami, FL

March 24, 2010

NYSE: WST

westpharma.com

All trademarks and registered trademarks are the property of West Pharmaceutical Services, Inc., unless noted otherwise.

2

This presentation contains forward-looking statements, within the meaning of Section 27A

of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act

of 1934, as amended, that are based on management’s beliefs and assumptions, current

expectations, estimates and forecasts. Statements that are not historical facts, including

statements that are preceded by, followed by, or that include, words such as “estimate,”

“expect,” “intend,” “believe,” “plan,” “anticipate” and other words and terms of similar

meaning are forward-looking statements. West’s estimated or anticipated future results,

product performance or other non-historical facts are forward-looking and reflect our

current perspective on existing trends and information.

of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act

of 1934, as amended, that are based on management’s beliefs and assumptions, current

expectations, estimates and forecasts. Statements that are not historical facts, including

statements that are preceded by, followed by, or that include, words such as “estimate,”

“expect,” “intend,” “believe,” “plan,” “anticipate” and other words and terms of similar

meaning are forward-looking statements. West’s estimated or anticipated future results,

product performance or other non-historical facts are forward-looking and reflect our

current perspective on existing trends and information.

Many of the factors that will determine the Company’s future results are beyond the ability

of the Company to control or predict. These statements are subject to known or unknown

risks or uncertainties, and therefore, actual results could differ materially from past results

and those expressed or implied in any forward-looking statement. You should bear this in

mind as you consider forward-looking statements. A non-exclusive list of important factors

that may affect future results may be found in West’s filings with the Securities and

Exchange Commission, including our annual report on Form 10-K and our periodic reports

on Form 10-Q and Form 8-K.

of the Company to control or predict. These statements are subject to known or unknown

risks or uncertainties, and therefore, actual results could differ materially from past results

and those expressed or implied in any forward-looking statement. You should bear this in

mind as you consider forward-looking statements. A non-exclusive list of important factors

that may affect future results may be found in West’s filings with the Securities and

Exchange Commission, including our annual report on Form 10-K and our periodic reports

on Form 10-Q and Form 8-K.

You should evaluate any statement in light of these important factors.

Forward Looking Statements

3

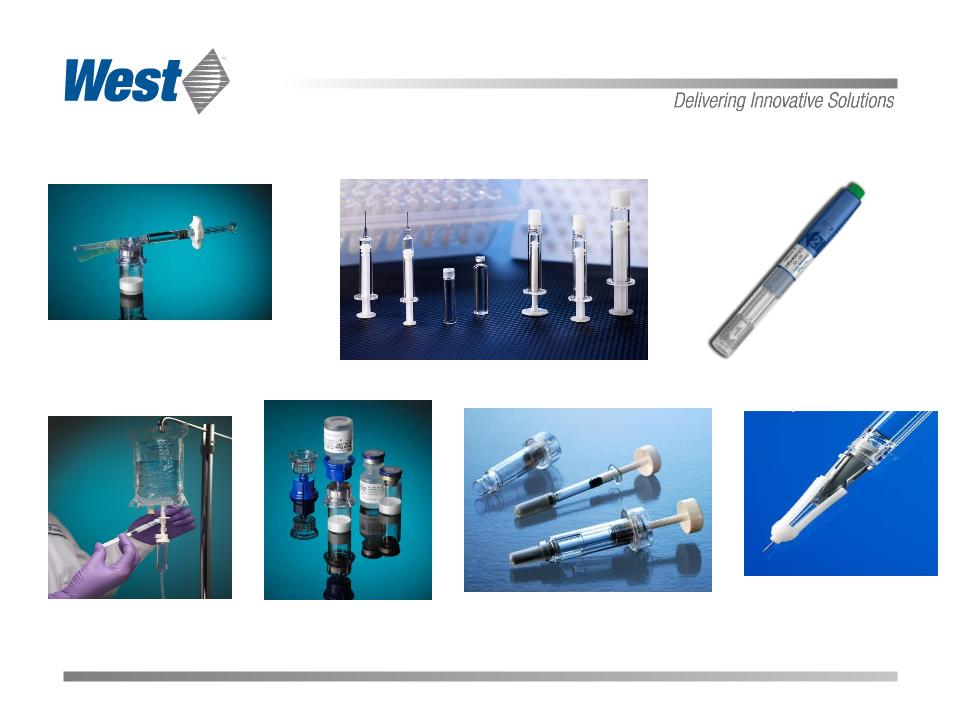

Corporate Profile

• For more than eighty years, a

global leader in the development

and manufacturing of

components and systems

for injectable drug delivery

global leader in the development

and manufacturing of

components and systems

for injectable drug delivery

– Vial

closure systems

– Prefillable

syringe components

– Components

for diagnostics

– Devices

and device sub-

assemblies

assemblies

– Safety

and administration

systems

systems

• Market capitalization $1.4 billion

• Diverse, stable customer base

• Global footprint

|

|

|

Devices |

|

Proprietary

Products |

4

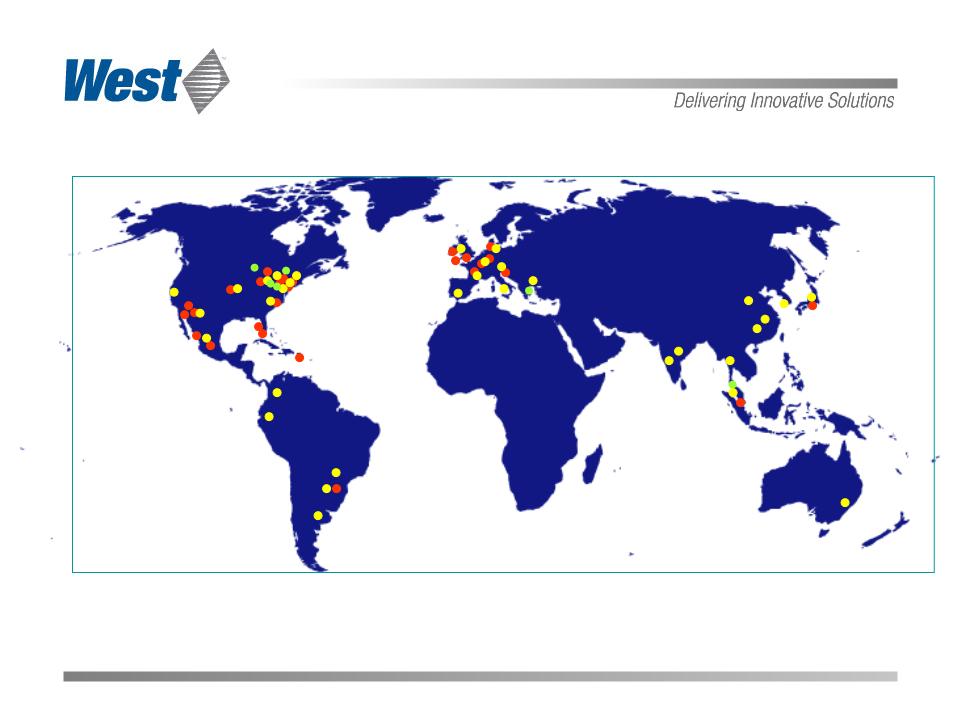

West Pharmaceutical Services Today

● 32 plants in 10 countries

● 34 sales offices

● 7 technical centers

6,000 employees worldwide

5

• Challenges:

– Adverse

effects of pension expense, currency effects

– Recession

impacted customer order patterns

• Tighter

cost, working capital and inventory management

• Some

major programs delayed or cancelled

– First

half sales declines

• Full year revenues grew by 3.5 % excluding currency

– H1N1-related

sales growth

– Customer

cyclical inventory adjustments moderating

– Year

end backlog at highest level in recent quarters

• Pharma mergers and consolidation

• Key developments:

– Validated

Daikyo Crystal Zenith 1ml single cavity manufacturing cell

• Four

cavity cell installed late Q4; commercial production should start Q3 2010

– Plastef

acquisition completed

– Officially

opened China Plastics facility

– Announced

plans to restructure and re-align operating segments in Q4

2009 in Retrospect

6

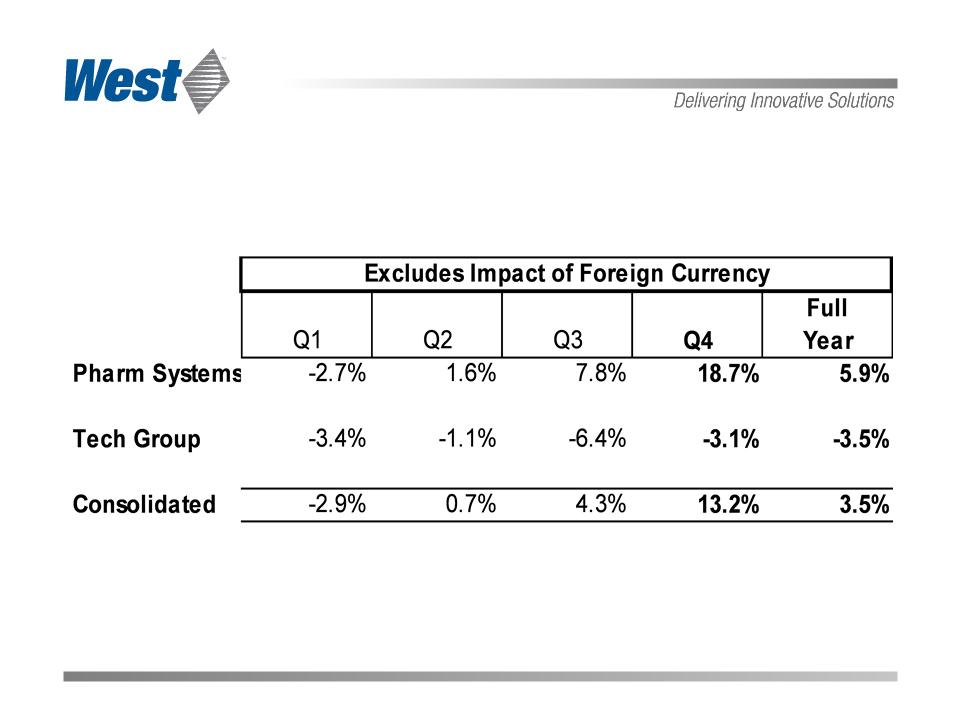

2009 Revenue Growth vs. Prior Year Period

by Business Segment

by Business Segment

7

• Ex-Currency, Growth was:

$ 32.2 Revenue (13.2%)

$ 10.2 Gross Profit (14.7%)

$ 2.2 Adjusted Operating

Profit (7.9%)

• Currency translation added:

$ 16.3 Revenue

$ 4.1 Gross Profit

$ 1.8 Operating Profit

• Major Changes:

– H1N1-related, prefillable component,

and metal seal sales

and metal seal sales

– Lower relative SG&A costs

8

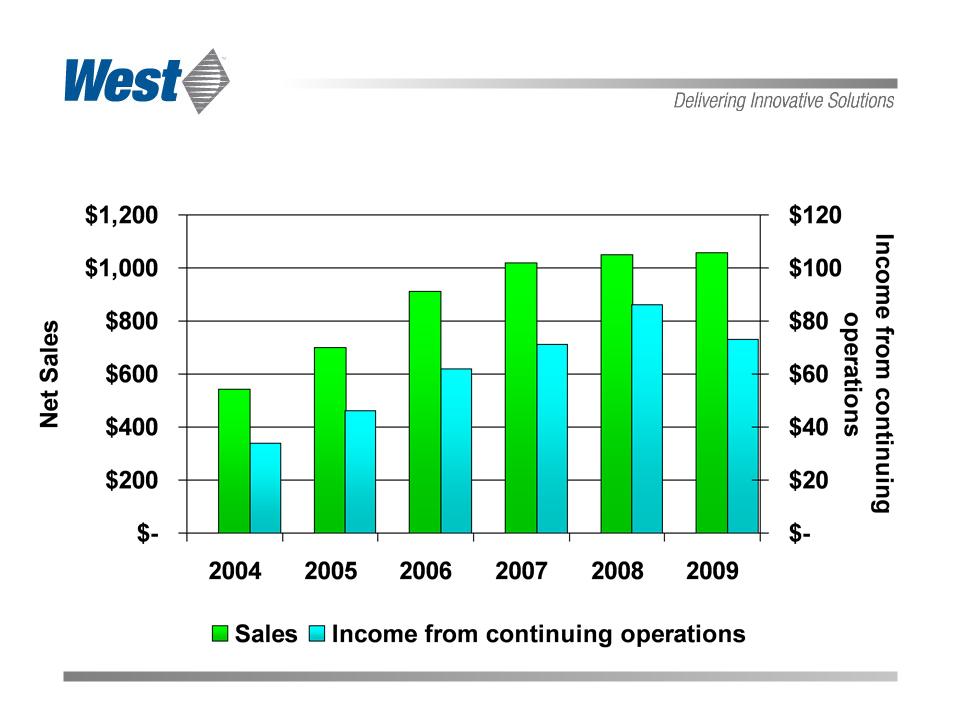

Sales and Income from Continuing Operations

($ in millions)

($ in millions)

9

• Global economic conditions remain soft, but show

signs of improvement

signs of improvement

• Analyzing future impact of US healthcare

legislation

legislation

• Global pharmaceutical revenue growth projected to

be 4-6% (per IMS) on modest unit growth

be 4-6% (per IMS) on modest unit growth

• North America growth projected at 4.5 - 5.5%

• Europe growth moderate 2-4%

• Emerging economies should grow > 10% (India,

China, Brazil)

• Return to more normalized order patterns

• Further consolidation - e.g Teva - Ratiopharm

2010 Business Environment

10

2010 Expectations and Milestones

• Revenue Growth: 3% to 5% (excluding currency)

– Consolidated revenues: $1,090 - $1,120 million1

• Consolidated Gross Margin of 30.5%

• Adjusted Diluted2 EPS: $2.19

to $2.39

• Validate new Daikyo CZ production cell

• Secure first Daikyo CZ commercial program

• Break ground on China rubber facility

1. The principal currency assumption in these estimates

is for the translation of the Euro at $1.40 for

2010.

2010.

2. “Adjusted Diluted EPS” refers to earnings

per share excluding expected restructuring charges of

between $0.02 and $0.04 per share.

between $0.02 and $0.04 per share.

11

|

Pharmaceutical Packaging

Systems (How drugs are contained) |

|

Primary Container Solutions |

|

Pharmaceutical Delivery

Systems (How drugs are administered) |

|

Administration Systems |

Business Unit Re-alignment

• Safety

systems (NovaGuard, Eris)

• Reconstitution

systems -

MediMop

MediMop

• CZ

prefillable syringe systems

• Advanced

Injection Systems

(Confidose)

(Confidose)

• Tech

Group Contract

Manufacturing

Manufacturing

• Small

volume parenteral

packaging

packaging

• Large

volume parenteral

packaging

packaging

• Prefillable

syringe components

• Disposable

medical device

components

components

• Diagnostic,

dental, veterinary

packaging

packaging

12

Five-Year Growth Opportunity

$2 billion combined markets for safety,

prefilled and auto-injectors, with unit

growth 6-12%, depending on product and

therapeutic segment

prefilled and auto-injectors, with unit

growth 6-12%, depending on product and

therapeutic segment

Strategic Planning Goals:

• Projected

2014 sales of $0.6 billion

• Projected

2014 Operating margin: 20%

$1.5 billion market for components with unit

growth 0% to 8% per year, depending on

product and therapeutic segment

growth 0% to 8% per year, depending on

product and therapeutic segment

Strategic Planning Goals:

• Projected

2014 sales of $1.0 billion

• Projected

2014 Operating margin: 20%

|

Pharmaceutical

Packaging Systems |

|

Primary Container Solutions |

|

Pharmaceutical Delivery Systems |

|

Administration Systems |

Consolidated 2014 Planning Objectives

• 2014

Sales: $1.6 billion

• 2014

Operating Margin: 19%

• 2014

Consolidated ROIC: 17%

13

Long Term Business Drivers

• Demographics

• Growth in Biologics & Vaccines

• Requirement for easy, safe,

accurate dosing

accurate dosing

• Combination product growth

• Generic growth

• Increasing global access to

advanced healthcare

advanced healthcare

West supplies sophisticated

packaging systems for the top 20

biologic drugs (by sales) currently

on the market.

packaging systems for the top 20

biologic drugs (by sales) currently

on the market.

14

Therapeutic Category Drivers

|

Category |

Key Customers |

Projected Growth |

|

Diabetes |

|

8 - 10% |

|

Oncology |

|

6 - 8% |

|

Vaccines |

|

4 - 6% |

|

Autoimmune |

|

6 - 8% |

15

Our Growth Strategy

West’s Competitive Advantages:

• Unmatched

expertise in drug -

material interactions

material interactions

• Market

leader in packaging for

biologics

biologics

• Protected

IP: Proprietary materials

and processing technology - Drug

Master File (DMF) 1546

and processing technology - Drug

Master File (DMF) 1546

• Regulatory

barriers to entry:

US NDAs and ANDAs

require proof of stability

require proof of stability

• Global

technical support

|

Pharmaceutical Packaging

Systems (How drugs are contained) |

|

Primary Container Solutions |

• Therapeutic

segment focus

• Generate

incremental value per

unit

unit

• Leverage

changing regulatory

environment

environment

• Optimize

manufacturing

productivity

productivity

• Strategic

acquisitions

• Geographic

expansion

• China

• India

16

Value Proposition

PROPRIETARY

PRODUCTS

Revenue and

Margin

Opportunity

Opportunity

Disposable Device

Disposable Device

Components

Components

Westar® RS

Mix2Vial®

NovaGuard™

éris™

Westar® RU

Standard

Components

Components

Standard

Components

Components

Consumer

Consumer

Products

Products

Packaging

Delivery

17

Our Growth Strategy

• Concentrate

on systems for unmet

market needs

market needs

• Build

market share in multi-

component systems for drug

administration utilizing Daikyo CZ as

a platform technology

component systems for drug

administration utilizing Daikyo CZ as

a platform technology

• Production

supported by existing

design, multi-material molding, and

assembly capabilities

design, multi-material molding, and

assembly capabilities

• Expand

through innovation and

strategic technology acquisitions

strategic technology acquisitions

|

Pharmaceutical Packaging Systems |

|

Primary Container Solutions |

|

Pharmaceutical Delivery Systems |

|

Administration Systems |

• Therapeutic

segment focus

• Generate

incremental value per

unit

unit

• Leverage

changing regulatory

environment

environment

• Optimize

manufacturing

productivity

productivity

• Strategic

acquisitions

• Geographic

expansion

• China

• India

18

Pharmaceutical Delivery Systems

Key Programs

Vial2Bag™

Mix2Vial®

MixJect®

NovaGuard™ Safety

Needle Device

Needle Device

(luer-lock syringe)

ConfiDose®

Auto-injector

Auto-injector

Daikyo Crystal Zenith®

éris™

Safety Needle Device

(fixed-needle syringe)

19

Management Focus

• Pharmaceutical Packaging Systems

– Organic

growth (on average) of 3-5% per year

– Margin

expansion through improved operating efficiency, product mix

– Capital

investments targeted at enhanced quality and value

• Pharmaceutical Delivery Systems

– Deliver

the potential of Daikyo CZ products

– Increase

healthcare-consumable contract manufacturing revenue

– Grow

proprietary safety and delivery system businesses

• Financial discipline

– Operating

cash flow: Discretionary SG&A, R&D and capital spending

that are supported by revenue growth.

that are supported by revenue growth.

– Deliver

returns on invested capital (“ROIC”) that regularly exceed

weighted average cost of capital (“WACC”).

weighted average cost of capital (“WACC”).

– Align

incentives with financial performance and value creation

20

Summary

• A valuable franchise

– Substantial

market share

– Proprietary

technology

– Diversified

Customer Base

– Global

footprint

• Positioned to grow

– Strength

in new product

pipeline

pipeline

– Preferred

products for

biologics

biologics

• With the financial strength to

invest

invest

– Reliable

operating cash

flow

flow

– Balance

sheet strength

• Led by an experienced

management team

management team

– Aligned

incentives

Injectable Container Solutions

Advanced

Injection

Systems

Injection

Systems

Prefillable Syringe Systems

Safety and

Administration Systems

Administration Systems

21

Donald E. Morel

Chairman and Chief Executive Officer

William J. Federici

Vice President and Chief Financial Officer

Investor Relations Contact:

Michael A. Anderson

Vice President and Treasurer

mike.anderson@westpharma.com

Barclays 2010 Global Healthcare Conference

Miami, FL

March 24, 2010

NYSE: WST

westpharma.com

All trademarks and registered trademarks are the property of West Pharmaceutical Services, Inc., unless noted otherwise.