Attached files

| file | filename |

|---|---|

| 10-K - Sentio Healthcare Properties Inc | v177515_10k.htm |

| EX-3.1 - Sentio Healthcare Properties Inc | v177515_ex3-1.htm |

| EX-3.2 - Sentio Healthcare Properties Inc | v177515_ex3-2.htm |

| EX-10.5 - Sentio Healthcare Properties Inc | v177515_ex10-5.htm |

| EX-21.1 - Sentio Healthcare Properties Inc | v177515_ex21-1.htm |

| EX-10.9 - Sentio Healthcare Properties Inc | v177515_ex10-9.htm |

| EX-31.2 - Sentio Healthcare Properties Inc | v177515_ex31-2.htm |

| EX-31.1 - Sentio Healthcare Properties Inc | v177515_ex31-1.htm |

| EX-10.10 - Sentio Healthcare Properties Inc | v177515_ex10-10.htm |

| EX-10.11 - Sentio Healthcare Properties Inc | v177515_ex10-11.htm |

| EX-10.12 - Sentio Healthcare Properties Inc | v177515_ex10-12.htm |

| EX-32.1 - Sentio Healthcare Properties Inc | v177515_ex32-1.htm |

Exhibit

10.6

Freddie

Mac Loan Number 534382134

MULTIFAMILY

NOTE

MULTISTATE

– FIXED RATE

(REVISION

DATE 2-15-2008)

|

US

$10,000,000.00

|

Effective

Date: December 16, 2009

|

FOR VALUE RECEIVED, the undersigned

(together with such party's or parties' successors and assigns, "Borrower") jointly and

severally (if more than one) promises to pay to the order of KEYCORP REAL ESTATE

CAPITAL MARKETS, INC., an Ohio corporation, the principal sum of Ten Million and

No/100 Dollars (US $10,000,000.00), with interest on the unpaid principal

balance, as hereinafter provided.

|

1.

|

Defined

Terms.

|

|

(a)

|

As

used in this Note:

|

"Base Recourse" means a portion of the

Indebtedness equal to zero percent (0%) of the original principal balance of

this Note.

"Business Day" means any day

other than a Saturday, a Sunday or any other day on which Lender or the national

banking associations are not open for business.

"Default Rate" means an annual

interest rate equal to four (4) percentage points above the Fixed Interest

Rate. However, at no time will the Default Rate exceed the Maximum

Interest Rate.

"Fixed Interest Rate" means the

annual interest rate of six and forty-three hundredths percent

(6.43%).

"Installment Due Date" means,

for any monthly installment of interest only or principal and interest, the date

on which such monthly installment is due and payable pursuant to Section 3 of

this Note. The "First

Installment Due Date" under this Note is February 1, 2010.

"Lender" means the holder from

time to time of this Note.

"Loan" means the loan evidenced

by this Note.

Page

A-1

"Maturity Date" means the earlier of (i) January 1, 2020 (the "Scheduled Maturity

Date"), and

(ii) the date on which the unpaid principal balance of this Note becomes due and

payable by acceleration or otherwise pursuant to the Loan Documents or the

exercise by Lender of any right or remedy under any Loan Document.

"Maximum Interest Rate" means

the rate of interest that results in the maximum amount of interest allowed by

applicable law.

"Prepayment Premium Period"

means the period during which, if a prepayment of principal occurs, a prepayment

premium will be payable by Borrower to Lender. The Prepayment Premium

Period is the period from and including the date of this Note until but not

including the first day of the Window Period.

"Security Instrument" means the

multifamily mortgage, deed to secure debt or deed of trust effective as of the

effective date of this Note, from Borrower to or for the benefit of Lender and

securing this Note.

|

|

"Treasury Security" means

the 3.625% U.S. Treasury Security due August 15,

2019

|

"Window Period" means the three

(3) consecutive calendar month period prior to the Scheduled Maturity

Date.

"Yield Maintenance Period"

means the period from and including the date of this Note until but not

including July 1, 2019.

(b) Other

capitalized terms used but not defined in this Note shall have the meanings

given to such terms in the Security Instrument.

2.

Address

for Payment. All payments due under this Note shall be payable

at 127 Public Square, Cleveland, Ohio 44114, or such other place as may be

designated by Notice to Borrower from or on behalf of Lender.

3.

Payments.

(a) Interest

will accrue on the outstanding principal balance of this Note at the Fixed

Interest Rate, subject to the provisions of Section 8 of this

Note.

Page

A-2

(b) Interest

under this Note shall be computed, payable and allocated on the basis of an

actual/360 interest calculation schedule (interest is payable for the actual

number of days in each month, and each month's interest is calculated by

multiplying the unpaid principal amount of this Note as of the first day of the

month for which interest is being calculated by the Fixed Interest Rate,

dividing the product by 360, and multiplying the quotient by the number of days

in the month for which interest is being calculated). The portion of

the monthly installment of principal and interest under this Note attributable

to principal and the portion attributable to interest will vary based upon the

number of days in the month for which such installment is paid. Each monthly

payment of principal and interest will first be applied to pay in full interest

due, and the balance of the monthly installment payment paid by Borrower will be

credited to principal.

(c) Unless

disbursement of principal is made by Lender to Borrower on the first day of a

calendar month, interest for the period beginning on the date of disbursement

and ending on and including the last day of such calendar month shall be payable

by Borrower simultaneously with the execution of this Note. If

disbursement of principal is made by Lender to Borrower on the first day of a

calendar month, then no payment will be due from Borrower at the time of the

execution of this Note. The Installment Due Date for the first

monthly installment payment under Section 3(d) of interest only or principal and

interest, as applicable, will be the First Installment Due Date set forth in

Section 1(a) of this Note. Except as provided in this Section 3(c)

and in Section 10, accrued interest will be payable in arrears.

(d) Beginning

on the First Installment Due Date, and continuing until and including the

monthly installment due on the Maturity Date, principal and accrued interest

shall be payable by Borrower in consecutive monthly installments due and payable

on the first day of each calendar month. The amount of the monthly

installment of principal and interest payable pursuant to this Section 3(d) on

an Installment Due Date shall be Sixty-Two Thousand Seven Hundred Forty-Seven

and 15/100 Dollars ($62,747.15).

(e) All

remaining Indebtedness, including all principal and interest, shall be due and

payable by Borrower on the Maturity Date.

(f)

All payments under this Note shall be made in

immediately available U.S. funds.

(g) Any

regularly scheduled monthly installment of interest only or principal and

interest payable pursuant to this Section 3 that is received by Lender

before the date it is due shall be deemed to have been received on the due date

for the purpose of calculating interest due.

(h) Any

accrued interest remaining past due for 30 days or more, at Lender's discretion,

may be added to and become part of the unpaid principal balance of this Note and

any reference to "accrued interest" shall refer to accrued interest which has

not become part of the unpaid principal balance. Any amount added to

principal pursuant to the Loan Documents shall bear interest at the applicable

rate or rates specified in this Note and shall be payable with such interest

upon demand by Lender and absent such demand, as provided in this Note for the

payment of principal and interest.

Page

A-3

4.

Application of

Payments. If at any time Lender receives, from Borrower or

otherwise, any amount applicable to the Indebtedness which is less than all

amounts due and payable at such time, Lender may apply the amount received to

amounts then due and payable in any manner and in any order determined by

Lender, in Lender's discretion. Borrower agrees that neither Lender's

acceptance of a payment from Borrower in an amount that is less than all amounts

then due and payable nor Lender's application of such payment shall constitute

or be deemed to constitute either a waiver of the unpaid amounts or an accord

and satisfaction.

5.

Security. The

Indebtedness is secured by, among other things, the Security Instrument, and

reference is made to the Security Instrument for other rights of Lender as to

collateral for the Indebtedness.

6.

Acceleration. If an

Event of Default has occurred and is continuing, the entire unpaid principal

balance, any accrued interest, any prepayment premium payable under

Section 10, and all other amounts payable under this Note and any other

Loan Document, shall at once become due and payable, at the option of Lender,

without any prior notice to Borrower (except if notice is required by applicable

law, then after such notice). Lender may exercise this option to

accelerate regardless of any prior forbearance. For purposes of

exercising such option, Lender shall calculate the prepayment premium as if

prepayment occurred on the date of acceleration. If prepayment occurs

thereafter, Lender shall recalculate the prepayment premium as of the actual

prepayment date.

7.

Late Charge.

(a) If

any monthly installment of interest or principal and interest or other amount

payable under this Note or under the Security Instrument or any other Loan

Document is not received in full by Lender within ten (10) days after the

installment or other amount is due, counting from and including the date such

installment or other amount is due (unless applicable law requires a longer

period of time before a late charge may be imposed, in which event such longer

period shall be substituted), Borrower shall pay to Lender, immediately and

without demand by Lender, a late charge equal to five percent (5%) of such

installment or other amount due (unless applicable law requires a lesser amount

be charged, in which event such lesser amount shall be

substituted).

(b) Borrower

acknowledges that its failure to make timely payments will cause Lender to incur

additional expenses in servicing and processing the Loan and that it is

extremely difficult and impractical to determine those additional

expenses. Borrower agrees that the late charge payable pursuant to

this Section represents a fair and reasonable estimate, taking into account

all circumstances existing on the date of this Note, of the additional expenses

Lender will incur by reason of such late payment. The late charge is

payable in addition to, and not in lieu of, any interest payable at the Default

Rate pursuant to Section 8.

Page

A-4

8.

Default

Rate.

(a) So

long as (i) any monthly installment under this Note remains past due for

thirty (30) days or more or (ii) any other Event of Default has occurred

and is continuing, then notwithstanding anything in Section 3 of this Note to

the contrary, interest under this Note shall accrue on the unpaid principal

balance from the Installment Due Date of the first such unpaid monthly

installment or the occurrence of such other Event of Default, as applicable, at

the Default Rate.

(b) From

and after the Maturity Date, the unpaid principal balance shall continue to bear

interest at the Default Rate until and including the date on which the entire

principal balance is paid in full.

(c) Borrower

acknowledges that (i) its failure to make timely payments will cause Lender

to incur additional expenses in servicing and processing the Loan,

(ii) during the time that any monthly installment under this Note is

delinquent for thirty (30) days or more, Lender will incur additional costs and

expenses arising from its loss of the use of the money due and from the adverse

impact on Lender's ability to meet its other obligations and to take advantage

of other investment opportunities; and (iii) it is extremely difficult and

impractical to determine those additional costs and

expenses. Borrower also acknowledges that, during the time that any

monthly installment under this Note is delinquent for thirty (30) days or more

or any other Event of Default has occurred and is continuing, Lender's risk of

nonpayment of this Note will be materially increased and Lender is entitled to

be compensated for such increased risk. Borrower agrees that the

increase in the rate of interest payable under this Note to the Default Rate

represents a fair and reasonable estimate, taking into account all circumstances

existing on the date of this Note, of the additional costs and expenses Lender

will incur by reason of the Borrower's delinquent payment and the additional

compensation Lender is entitled to receive for the increased risks of nonpayment

associated with a delinquent loan.

9.

Limits on Personal

Liability.

(a) Except

as otherwise provided in this Section 9, Borrower shall have no personal

liability under this Note, the Security Instrument or any other Loan Document

for the repayment of the Indebtedness or for the performance of any other

obligations of Borrower under the Loan Documents and Lender's only recourse for

the satisfaction of the Indebtedness and the performance of such obligations

shall be Lender's exercise of its rights and remedies with respect to the

Mortgaged Property and to any other collateral held by Lender as security for

the Indebtedness. This limitation on Borrower's liability shall not

limit or impair Lender's enforcement of its rights against any guarantor of the

Indebtedness or any guarantor of any other obligations of Borrower.

(b) Borrower

shall be personally liable to Lender for the amount of the Base Recourse, plus

any other amounts for which Borrower has personal liability under this

Section 9.

Page

A-5

(c)

In addition to the Base Recourse, Borrower shall be personally

liable to Lender for the repayment of a further portion of the Indebtedness

equal to any loss or damage suffered by Lender as a result of the occurrence of

any of the following events:

|

|

(i)

|

Borrower

fails to pay to Lender upon demand after an Event of Default all Rents to

which Lender is entitled under Section 3(a) of the Security

Instrument and the amount of all security deposits collected by Borrower

from tenants then in residence. However, Borrower will not be

personally liable for any failure described in this subsection (i) if

Borrower is unable to pay to Lender all Rents and security deposits as

required by the Security Instrument because of a valid order issued in a

bankruptcy, receivership, or similar judicial

proceeding.

|

|

|

(ii)

|

Borrower

fails to apply all insurance proceeds and condemnation proceeds as

required by the Security Instrument. However, Borrower will not

be personally liable for any failure described in this

subsection (ii) if Borrower is unable to apply insurance or

condemnation proceeds as required by the Security Instrument because of a

valid order issued in a bankruptcy, receivership, or similar judicial

proceeding.

|

|

|

(iii)

|

Borrower

fails to comply with Section 14(g) or (h) of the Security Instrument

relating to the delivery of books and records, statements, schedules and

reports.

|

|

|

(iv)

|

Borrower

fails to pay when due in accordance with the terms of the Security

Instrument the amount of any item below marked

"Deferred"; provided however, that if no item is marked "Deferred", this

Section 9(c)(iv) shall be of no force or

effect.

|

|

|

[Collect]

|

Hazard

Insurance premiums or other insurance

premiums,

|

|

[Collect]

|

Taxes,

|

|

|

[Deferred]

|

water

and sewer charges (that could become a lien on the Mortgaged

Property),

|

|

[N/A]

|

ground

rents,

|

|

|

[Deferred]

|

assessments

or other charges (that could become a lien on the Mortgaged

Property)

|

(d)

In addition to the Base Recourse, Borrower shall be

personally liable to Lender for:

|

|

(i)

|

the

performance of all of Borrower's obligations under Section 18 of the

Security Instrument (relating to environmental

matters);

|

|

|

(ii)

|

the

costs of any audit under Section 14(g) of the Security Instrument;

and

|

Page

A-6

|

|

(iii)

|

any

costs and expenses incurred by Lender in connection with the collection of

any amount for which Borrower is personally liable under this

Section 9, including Attorneys' Fees and Costs and the costs of

conducting any independent audit of Borrower's books and records to

determine the amount for which Borrower has personal

liability.

|

(e)

All payments made by Borrower with respect to the

Indebtedness and all amounts received by Lender from the enforcement of its

rights under the Security Instrument and the other Loan Documents shall be

applied first to the portion of the Indebtedness for which Borrower has no

personal liability.

(f)

Notwithstanding the Base Recourse, Borrower shall become

personally liable to Lender for the repayment of all of the Indebtedness upon

the occurrence of any of the following Events of Default:

|

|

(i)

|

Borrower's

ownership of any property or operation of any business not permitted by

Section 33 of the Security

Instrument;

|

|

|

(ii)

|

a

Transfer (including, but not limited to, a lien or encumbrance) that is an

Event of Default under Section 21 of the Security Instrument, other

than a Transfer consisting solely of the involuntary removal or

involuntary withdrawal of a general partner in a limited partnership or a

manager in a limited liability company;

or

|

|

|

(iii)

|

fraud

or written material misrepresentation by Borrower or any officer,

director, partner, member or employee of Borrower in connection with the

application for or creation of the Indebtedness or any request for any

action or consent by Lender.

|

(g)

To the extent that Borrower has personal liability

under this Section 9, Lender may exercise its rights against Borrower

personally without regard to whether Lender has exercised any rights against the

Mortgaged Property or any other security, or pursued any rights against any

guarantor, or pursued any other rights available to Lender under this Note, the

Security Instrument, any other Loan Document or applicable law. To the

fullest extent permitted by applicable law, in any action to enforce Borrower's

personal liability under this Section 9, Borrower waives any right to set

off the value of the Mortgaged Property against such personal

liability.

10.

Voluntary and Involuntary Prepayments.

(a) Any

receipt by Lender of principal due under this Note prior to the Maturity Date,

other than principal required to be paid in monthly installments pursuant to

Section 3, constitutes a prepayment of principal under this

Note. Without limiting the foregoing, any application by Lender,

prior to the Maturity Date, of any proceeds of collateral or other security to

the repayment of any portion of the unpaid principal balance of this Note

constitutes a prepayment under this Note.

Page

A-7

(b) Borrower

may voluntarily prepay all of the unpaid principal balance of this Note on an

Installment Due Date so long as Borrower designates the date for such prepayment

in a Notice from Borrower to Lender given at least 30 days prior to the date of

such prepayment. If an Installment Due Date (as defined in Section

1(a)) falls on a day which is not a Business Day, then with respect to payments

made under this Section 10 only, the term "Installment Due Date" shall mean the

Business Day immediately preceding the scheduled Installment Due

Date.

(c) Notwithstanding

subsection (b) above, Borrower may voluntarily prepay all of the unpaid

principal balance of this Note on a Business Day other than an Installment Due

Date if Borrower provides Lender with the Notice set forth in subsection (b) and

meets the other requirements set forth in this subsection. Borrower

acknowledges that Lender has agreed that Borrower may prepay principal on a

Business Day other than an Installment Due Date only because Lender shall deem

any prepayment received by Lender on any day other than an Installment Due Date

to have been received on the Installment Due Date immediately following such

prepayment and Borrower shall be responsible for all interest that would have

been due if the prepayment had actually been made on the Installment Due Date

immediately following such prepayment.

(d) Unless

otherwise expressly provided in the Loan Documents, Borrower may not voluntarily

prepay less than all of the unpaid principal balance of this Note. In

order to voluntarily prepay all or any part of the principal of this Note,

Borrower must also pay to Lender, together with the amount of principal

being prepaid, (i) all accrued and unpaid interest due under this Note,

plus (ii) all other sums due to Lender at the time of such prepayment, plus

(iii) any prepayment premium calculated pursuant to

Section 10(e).

(e)

Except as provided in Section 10(f), a prepayment premium

shall be due and payable by Borrower in connection with any prepayment of

principal under this Note during the Prepayment Premium Period. The

prepayment premium shall be computed as follows:

|

|

(i)

|

For

any prepayment made during the Yield Maintenance Period, the prepayment

premium shall be whichever is the greater of subsections (A) and (B)

below:

|

|

|

(A)

|

1.0%

of the amount of principal being prepaid;

or

|

|

(B)

|

the

product obtained by multiplying:

|

|

(1)

|

the

amount of principal being prepaid or accelerated,

by

|

Page

A-8

|

|

(2)

|

the

excess (if any) of the Monthly Note Rate over the Assumed Reinvestment

Rate,

by

|

|

(3)

|

the

Present Value Factor.

|

For purposes of subsection (B),

the following definitions shall apply:

|

|

Monthly Note Rate:

one-twelfth (1/12) of the Fixed Interest Rate, expressed as a decimal

calculated to five digits.

|

|

|

Prepayment

Date: in the case of a voluntary prepayment, the date on

which the prepayment is made; in the case of the application by Lender of

collateral or security to a portion of the principal balance, the date of

such application.

|

|

|

Assumed Reinvestment

Rate: one-twelfth (1/12) of the yield rate, as of the

close of the trading session which is 5 Business Days before the

Prepayment Date, on the Treasury Security, as reported in The Wall Street

Journal, expressed as a decimal calculated to five

digits. In the event that no yield is published on the

applicable date for the Treasury Security, Lender, in its discretion,

shall select the non-callable Treasury Security maturing in the same year

as the Treasury Security with the lowest yield published in The Wall Street Journal

as of the applicable date. If the publication of such yield

rates in The Wall Street

Journal is discontinued for any reason, Lender shall select a

security with a comparable rate and term to the Treasury

Security. The selection of an alternate security pursuant to

this Section shall be made in Lender’s

discretion.

|

|

|

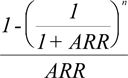

Present Value

Factor: the factor that discounts to present value the

costs resulting to Lender from the difference in interest rates during the

months remaining in the Yield Maintenance Period, using the Assumed

Reinvestment Rate as the discount rate, with monthly compounding,

expressed numerically as follows:

|

Page

A-9

|

|

n = the number of months

remaining in Yield Maintenance Period; provided, however, if a prepayment

occurs on an Installment Due Date, then the number of months remaining in

the Yield Maintenance Period shall be

calculated beginning with the month in which such prepayment occurs and if

such prepayment occurs on a Business Day other than an Installment Due

Date, then the number of months remaining in the Yield Maintenance Period

shall be calculated beginning with the month immediately following the

date of such prepayment.

|

ARR = Assumed Reinvestment

Rate

|

|

(ii)

|

For

any prepayment made after the expiration of the Yield Maintenance Period

but during the remainder of the Prepayment Premium Period, the prepayment

premium shall be 1.0% of the amount of principal being

prepaid.

|

(f)

Notwithstanding any other

provision of this Section 10, no prepayment premium shall be payable with

respect to (i) any prepayment made during the Window Period, or

(ii) any prepayment occurring as a result of the application of any

insurance proceeds or condemnation award under the Security

Instrument.

(g) Unless

Lender agrees otherwise in writing, a permitted or required prepayment of less

than the unpaid principal balance of this Note shall not extend or postpone the

due date of any subsequent monthly installments or change the amount of such

installments.

(h) Borrower

recognizes that any prepayment of any of the unpaid principal balance of this

Note, whether voluntary or involuntary or resulting from an Event of Default by

Borrower, will result in Lender's incurring loss, including reinvestment loss,

additional expense and frustration or impairment of Lender's ability to meet its

commitments to third parties. Borrower agrees to pay to Lender upon

demand damages for the detriment caused by any prepayment, and agrees that it is

extremely difficult and impractical to ascertain the extent of such

damages. Borrower therefore acknowledges and agrees that the formula

for calculating prepayment premiums set forth in this Note represents a

reasonable estimate of the damages Lender will incur because of a

prepayment. Borrower further acknowledges that the prepayment premium

provisions of this Note are a material part of the consideration for the Loan,

and that the terms of this Note are in other respects more favorable to Borrower

as a result of the Borrower's voluntary agreement to the prepayment premium

provisions.

11.

Costs and

Expenses. To the fullest extent allowed by applicable law,

Borrower shall pay all expenses and costs, including Attorneys' Fees and Costs

incurred by Lender as a result of any default under this Note or in connection

with efforts to collect any amount due under this Note, or to enforce the

provisions of any of the other Loan Documents, including those incurred in

post-judgment collection efforts and in any bankruptcy proceeding (including any

action for relief from the automatic stay of any bankruptcy proceeding) or

judicial or non-judicial foreclosure proceeding.

Page

A-10

12. Forbearance. Any

forbearance by Lender in exercising any right or remedy under this Note, the

Security Instrument, or any other Loan Document or otherwise afforded by

applicable law, shall not be a waiver of or preclude the exercise of that or any

other right or remedy. The acceptance by Lender of any payment after

the due date of such payment, or in an amount which is less than the required

payment, shall not be a waiver of Lender's right to require prompt payment when

due of all other payments or to exercise any right or remedy with respect to any

failure to make prompt payment. Enforcement by Lender of any security

for Borrower's obligations under this Note shall not constitute an election by

Lender of remedies so as to preclude the exercise of any other right or remedy

available to Lender.

13. Waivers. Borrower

and all endorsers and guarantors of this Note and all other third party obligors

waive presentment, demand, notice of dishonor, protest, notice of acceleration,

notice of intent to demand or accelerate payment or maturity, presentment for

payment, notice of nonpayment, grace, and diligence in collecting the

Indebtedness.

14. Loan Charges (Texas

Only). Borrower and Lender intend at all times to comply with

the law of the State of Texas governing the Maximum Interest Rate or the maximum

amount of interest payable on or in connection with this Note and the

Indebtedness (or applicable United States federal law to the extent that it

permits Lender to contract for, charge, take, reserve or receive a greater

amount of interest than under Texas law). If the applicable law is

ever judicially interpreted so as to render usurious any amount payable under

this Note or under any other Loan Document, or contracted for, charged, taken,

reserved or received with respect to the Indebtedness, or as a result of

acceleration of the maturity of this Note, or if any prepayment by Borrower

results in Borrower having paid any interest in excess of that permitted by any

applicable law, then Borrower and Lender expressly intend that all excess

amounts collected by Lender shall be applied to reduce the unpaid principal

balance of this Note (or, if this Note has been or would thereby be paid in

full, shall be refunded to Borrower), and the provisions of this Note, the

Security Instrument and any other Loan Documents immediately shall be deemed

reformed and the amounts thereafter collectible under this Note or any other

Loan Document reduced, without the necessity of the execution of any new

documents, so as to comply with any applicable law, but so as to permit the

recovery of the fullest amount otherwise payable under this Note or any other

Loan Document. The right to accelerate the Maturity Date of this Note

does not include the right to accelerate any interest, which has not otherwise

accrued on the date of such acceleration, and Lender does not intend to collect

any unearned interest in the event of acceleration. All sums paid or

agreed to be paid to Lender for the use, forbearance or detention of the

Indebtedness shall, to the extent permitted by any applicable law, be amortized,

prorated, allocated and spread throughout the full term of the Indebtedness

until payment in full so that the rate or amount of interest on account of the

Indebtedness does not exceed the applicable usury

ceiling. Notwithstanding any provision contained in this Note, the

Security Instrument or any other Loan Document that permits the compounding of

interest, including any provision by which any accrued interest is added to the

principal amount of this Note, the total amount of interest that Borrower is

obligated to pay and Lender is entitled to receive with respect to the

Indebtedness shall not exceed the amount calculated on a simple (i.e., non-compounded)

interest basis at the maximum rate on principal amounts actually advanced to or

for the account of Borrower, including all current and prior advances and any

advances made pursuant to the Security Instrument or other Loan Documents (such

as for the payment of taxes, insurance premiums and similar expenses or

costs).

Page

A-11

15. Commercial

Purpose. Borrower represents that Borrower is incurring the

Indebtedness solely for the purpose of carrying on a business or commercial

enterprise, and not for personal, family, household, or agricultural

purposes.

16. Counting of

Days. Except where otherwise specifically provided, any

reference in this Note to a period of "days" means calendar days, not Business

Days.

17. Governing Law. This

Note shall be governed by the law of the Property Jurisdiction.

18. Captions. The

captions of the Sections of this Note are for convenience only and shall be

disregarded in construing this Note.

19. Notices; Written Modifications.

(a) All

Notices, demands and other communications required or permitted to be given

pursuant to this Note shall be given in accordance with Section 31 of the

Security Instrument.

(b) Any

modification or amendment to this Note shall be ineffective unless in writing

signed by the party sought to be charged with such modification or amendment;

provided, however, in the event of a Transfer under the terms of the Security

Instrument that requires Lender's consent, any or some or all of the

Modifications to Multifamily Note set forth in Exhibit A to this Note may

be modified or rendered void by Lender at Lender's option, by Notice to Borrower

and the transferee, as a condition of Lender's consent.

20. Consent to Jurisdiction and

Venue. Borrower agrees that any controversy arising under or

in relation to this Note may be litigated in the Property

Jurisdiction. The state and federal courts and authorities with

jurisdiction in the Property Jurisdiction shall have jurisdiction over all

controversies that shall arise under or in relation to this

Note. Borrower irrevocably consents to service, jurisdiction, and

venue of such courts for any such litigation and waives any other venue to which

it might be entitled by virtue of domicile, habitual residence or

otherwise. However, nothing in this Note is intended to limit any

right that Lender may have to bring any suit, action or proceeding relating to

matters arising under this Note in any court of any other

jurisdiction.

21. WAIVER

OF TRIAL BY JURY. BORROWER AND LENDER EACH (A) AGREES NOT TO

ELECT A TRIAL BY JURY WITH RESPECT TO ANY ISSUE ARISING OUT OF THIS NOTE OR THE

RELATIONSHIP BETWEEN THE PARTIES AS LENDER AND BORROWER THAT IS TRIABLE OF RIGHT

BY A JURY AND (B) WAIVES ANY RIGHT TO TRIAL BY JURY WITH RESPECT TO SUCH

ISSUE TO THE EXTENT THAT ANY SUCH RIGHT EXISTS NOW OR IN THE

FUTURE. THIS WAIVER OF RIGHT TO TRIAL BY JURY IS SEPARATELY GIVEN BY

EACH PARTY, KNOWINGLY AND VOLUNTARILY WITH THE BENEFIT OF COMPETENT LEGAL

COUNSEL.

Page

A-12

22. State-Specific

Provisions.

ATTACHED EXHIBIT. The

Exhibit noted below, if marked with an "X" in the space provided, is attached to

this Note:

[___] Exhibit

A Modifications to Multifamily

Note

Page

A-13

IN WITNESS WHEREOF, and in

consideration of the Lender's agreement to lend Borrower the principal amount

set forth above, Borrower has signed and delivered this Note under seal or has

caused this Note to be signed and delivered under seal by its duly authorized

representative. Borrower intends that this Note shall be deemed to be signed and

delivered as a sealed instrument.

|

CARUTH HAVEN L.P., a

Delaware limited partnership

|

||||

|

By:

|

CARUTH

HAVEN GP, LLC, a Delaware limited liability company,

|

|||

|

Its:

|

Sole

General Partner

|

|||

|

By:

|

CGI

Healthcare Operating Partnership, L.P., a Delaware limited

partnership

|

|||

|

Its:

|

Sole

Member

|

|||

|

By:

|

Cornerstone

Growth & Income Operating Partnership, L.P., a Delaware limited

Partnership

|

|||

|

Its:

|

Sole

General Partner

|

|||

|

By:

|

Cornerstone

Growth & Income REIT, Inc., a Maryland corporation

|

|||

|

Its:

|

Sole

General

Partner

|

|||

|

By:

|

/s/

Terry G. Roussel

|

||||

|

Name:

|

Terry

G. Roussel

|

||||

|

Title:

|

President

|

|

Borrower's

Social Security/Employer ID

Number

|

Page

A-14

PAY TO

THE ORDER OF FEDERAL HOME LOAN MORTGAGE CORPORATION WITHOUT

RECOURSE.

|

KEYCORP

REAL ESTATE CAPITAL

MARKETS,

INC., an Ohio corporation

|

|

|

By:

|

/s/

Crystal L. Williams

|

|

Name:

|

Crystal L.

Williams

|

|

Title:

|

Vice

President

|

|

Date:

|

December

16,

2009

|

Page

A-15

EXHIBIT

A

MODIFICATIONS

TO MULTIFAMILY NOTE

The

following modifications are made to the text of the Note that precedes this

Exhibit.

|

|

1.

|

Section

9(c) is modified by adding an additional subsection (v) as

follows:

|

“(v) Borrower’s

violation or breach of or other failure to comply with that certain Declaration

of Covenants, Conditions, Restrictions and Reciprocal Easements, dated effective

as of March 31, 1997 as filed September 24, 1997 in the real property records of

Dallas County, Texas in Volume 97186, Page 4996, as amended from time to

time.

Page

A-16