Attached files

| file | filename |

|---|---|

| EX-31.2 - China Housing & Land Development, Inc. | v177342_ex31-2.htm |

| EX-21.1 - China Housing & Land Development, Inc. | v177342_ex21-1.htm |

| EX-32.1 - China Housing & Land Development, Inc. | v177342_ex32-1.htm |

| EX-31.1 - China Housing & Land Development, Inc. | v177342_ex31-1.htm |

| EX-23.1 - China Housing & Land Development, Inc. | v177342_ex23-1.htm |

| EX-32.2 - China Housing & Land Development, Inc. | v177342_ex32-2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

10-K

x ANNUAL REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE

SECURITIES

EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2009

OR

¨ TRANSITION REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES

EXCHANGE ACT OF 1934

For

the transition period from ____________ to ____________

Commission

file number: 333-105903

China

Housing & Land Development, Inc.

(Exact

name of registrant as specified in our charter)

|

NEVADA

|

20-1334845

|

|

(State

or other jurisdiction of incorporation or

organization)

|

(I.R.S.

Employer Identification No.)

|

6

Youyi Dong Lu, Han Yuan 4 Lou

Xi'an,

Shaanxi Province

China

710054

(Address

of principal executive offices) (Zip Code)

(Registrant's

telephone number, including area code)

86-29-82582632

(Former

name, former address and former fiscal year,

if

changed since last report)

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of each class

|

Name

of each exchange on

which

registered

|

|

Common

Stock, $ .001 par value per share

|

NASDAQ

Capital Market

|

Securities

registered pursuant to Section 12(g) of the Act: none.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities

Act.

Yes ¨ No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Exchange

Act.

Yes ¨ No

x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes x No

¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Website, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes ¨ No

¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

definition of “accelerated filer, large accelerated filer and smaller reporting

company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

|

Non-accelerated filer ¨

(Do not check if a smaller reporting company)

|

Smaller reporting company x

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ¨ No x

The

number of shares outstanding of our common stock as of June 30, 2009, was

30,948,340 shares. The aggregate market value of the common stock held by

non-affiliates (12,910,977 shares), based on the closing market price ($5.76 per

share) of the common stock as of June 30, 2009 was $74,367,228.

As of

March 12, 2010 the number of shares of the registrant’s classes of common stock

outstanding was 33,065,386.

DOCUMENTS

INCORPORATED BY REFERENCE

|

Document

|

Parts

Into Which Incorporated

|

|

None

|

Not

applicable

|

SPECIAL

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This

annual report includes forward-looking statements within the meaning of Section

27A of the Securities Act and Section 21E of the Securities Exchange Act of

1934, as amended. All statements, other than statements of historical fact, are

statements that could be deemed forward-looking statements, including, but not

limited to, statements regarding our future financial position, business

strategy and plans and objectives of management for future operations. When used

in this filing, the words believe, may, will, estimate, continue, anticipate,

intend, expect, and similar expressions are intended to identify forward-looking

statements.

We have

based these forward-looking statements largely on our current expectations and

projections about future events and financial trends that we believe may affect

our financial condition, results of operations, business strategy, short-term

and long-term business operations and objectives, and financial needs.

These forward-looking statements are subject to certain risks and

uncertainties that could cause our actual results to differ materially from

those reflected in the forward-looking statements. Factors that could cause or

contribute to such differences include, but are not limited to the risks

discussed under the heading “Risk Factors”. Except as required by law, we assume

no obligation to update these forward-looking statements publicly or to update

the reasons actual results could differ materially from those anticipated in

these forward-looking statements.

In light

of these risks, uncertainties, and assumptions, the forward-looking events and

circumstances discussed in this annual report may not occur and actual results

could differ materially and adversely from those anticipated or implied in the

forward-looking statements. Accordingly, readers are cautioned not to place

undue reliance on such forward-looking statements.

2

TABLE

OF CONTENT

|

PART

I

|

||

|

ITEM

1

|

BUSINESS

|

3

|

|

ITEM

1A

|

RISK

FACTORS

|

18

|

|

ITEM

2

|

PROPERTIES

|

24

|

|

ITEM

3

|

LEGAL

PROCEEDINGS

|

24

|

|

ITEM

4

|

SUBMISSION

OF MATTERS TO A VOTE OF SECURITY HOLDERS

|

24

|

|

PART

II

|

||

|

ITEM

5

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES

|

24

|

|

ITEM

6

|

SELECTED

FINANCIAL DATA

|

26

|

|

ITEM

7

|

MANAGEMENT

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

27

|

|

ITEM

7A

|

QUANTITATIVE

AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

42

|

|

ITEM

8

|

FINANCIAL

STATEMENT AND SUPPLEMENTARY DATA

|

43

|

|

ITEM

9

|

CHANGES

IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL

DISCLOSURES

|

67

|

|

ITEM

9A(T)

|

CONTROLS

AND PROCEDURES

|

67

|

|

ITEM

9B

|

OTHER

INFORMATION

|

68

|

|

PART

III

|

||

|

ITEM

10

|

DIRECTORS

AND EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

68

|

|

ITEM

11

|

EXECUTIVE

COMPENSATION

|

71

|

|

ITEM

12

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED

STOCKHOLDER MATTERS

|

72

|

|

ITEM

13

|

CERTAIN

RELATIONSHIPS AND RELATED TRANSACTIONS

|

72

|

|

ITEM

14

|

PRINCIPAL

ACCOUNTING FEES AND SERVICES

|

74

|

|

PART

IV

|

||

|

ITEM

15

|

EXHIBITS

AND REPORTS ON FORM 10-K

|

75

|

|

SIGNATURES

|

76

|

|

3

ITEM

1 BUSINESS

OUR

COMPANY

We are a

leading residential developer with focus on fast growing Tier II and Tier III

cities in Western China. We are dedicated to provide quality and affordable

housing to middle class families. The majority of our customers are first time

home buyers which, we believe, have increasing purchasing power and will benefit

from China’s rapid GDP growth.

We

commenced our operation since 1999 in Xi’an and are considered as the industry

leader and largest private residential developer in the region. We have

experienced significant growth in the past 11 years and have completed over 1.2

million square meters of residential projects. With the introduction of modern

design and technology, as well as the strict cost control system, we are able to

offer our customers high cost-effective products. Most of our projects are

designed by world-class architectures from United States and Europe that have

brought green technologies into our projects.

As we are

focusing on the demand from first time home buyers and first time up-graders in

Western China, the majority of our apartments are between 70 square

meters to 120 square meters in size, which is considered as a stable market

section in Western China. Our typical residential project have the size of

100,000 square meters and consists of multiple high-rise, middle-rise and

low-rise buildings as well as a community center, commercial units, kindergarten

and other auxiliary facilities. In addition, we provide property management

services to our developments and have an exclusive membership system for our

customers. We generated a large portion of our sales through the recommendations

of our existing customers.

We

acquired our land reserve and development site through primary land development

with local government, open-market auctions acquisition of old factories from

the government and distress assets from commercial banks. Not depending on a

single land acquisition method enables us to achieve reasonable land cost and

higher return from our developments. We intend to continue our expansion into

other strategically selected cities in Western China by leveraging our

well-recognized brand name and scalable business model.

Our

Strategies

We are

primarily focused on the development, management and sale of residential real

estate properties to capitalize on the rising demand from China’s emerging

middle class. We strive to become the market leader in Western China

and plan to implement the following specific strategies to achieve our

goal:

Consolidate through

Acquisition and Partnership. Currently, the residential real estate

market in Western China is fragmented with many small players. We believe that

this will provide us with opportunities for acquisitions or partnering. We

believe acquisitions will provide us better leverage in negotiations and better

economies of scale.

Expand into Other Tier II

and Tier III Cities. We believe our proven business model and expertise

can be replicated in other Tier II and Tier III cities, especially in Western

China. We have identified certain cities with attractive dynamics.

Continue to Focus on the

Middle Market. We believe the emerging middle class will offer an

attractive opportunity for growth, since its purchasing power is growing and it

has a strong desire for ownership driven by the influence of Chinese culture and

values. We plan to leverage our brand name, experience and design capabilities

to meet the demand from the middle class.

Our

Competitive Strengths

We

believe we have the following competitive strengths and they will enable us to

compete effectively and to capitalize on the growth opportunities in our

market:

Leading

position in our market and industry

We are

one of the largest private residential real estate developers in Western China.

We believe that we have strong design and sales capabilities and a well

recognized brand name in the region. With strong local project experience and

long term working relationships with central and local governments, we have been

able to acquire significant land assets at reasonable costs, providing a strong

pipeline of future business and revenues over the next three to five

years.

Attractive

market opportunity

The real

estate market in Western China has grown slower than in Eastern China. We

believe the region is well positioned to grow at faster rates for the next few

years due to social, economic, regulatory and government stimulus-related

factors. Our revenue has recovered from the 2008 economic downturn with

US$73,579,325 in 2007 to US$24,306,062 in 2008 to US$78,511,269 in 2009. Our

business model has proven to be efficient and we plan to expand into other Tier

II and Tier III cities in Western China. Our growth strategy is focused on

Western China, and we believe we will significantly benefit from the Chinese

government’s “Go West” policy, which encourages economic development and

population movement to Western China.

4

Unique

and proven business model

With

strong local project experience and long term working relationships with the

central and local governments, we have been able to acquire land assets at more

attractive costs compared to our competitors. We are primarily focused on

capitalizing on rising demand for properties from China’s emerging middle class,

which has significant purchasing power and a strong demand for residential

housing. In order to leverage our brand to appeal to the middle class, we use

various advertising media to market our property developments and to reach our

target demographic, including newspapers, magazines, television, radio,

e-marketing and outdoor billboards. We believe that our brand is widely

recognized in our market, known for high quality at cost-effective

prices.

Experienced

management team

We have

an experienced management team with a proven track record of developing and

expanding our operations. Our top five managers have a total of more than 85

years of experience from developing residential properties. As a result, we have

developed extensive core competencies, supplemented by in-house training and

development programs. We believe that our management’s core competencies,

extensive industry experience and long-term vision and strategy will enable us

to benefit from growth opportunities.

Greater

access to financing through multiple channels.

We enjoy

multiple long term relationships with a number of high quality Chinese banks

which ensures timely access to capital. These facilities are mainly

used for developments and the day to day running of the business. Besides

traditional banks, we are also working with other financial institutions, such

as trust companies and real estate funds to diversify our funding channels and

risks.

Corporate

History

We are a Nevada company and

substantially conduct all of our business through our operating subsidiaries in

China. We were incorporated in the state of Nevada on July 6, 2004, as Pacific

Northwest Productions Inc. On May 4, 2006, we changed our name to China Housing

& Land Development, Inc. Currently we own 6 operating subsidiaries in

China.

On April

21, 2006, we acquired 100% shares of Xi’an Tsining Housing Development Co., Ltd

(“Tsining”) through a share purchase agreement.

On March 9, 2007, we acquired 100%

shares of Xi’an New Land Development Co., Ltd. (“New Land”).

On November 5, 2008, the Company and

Prax Capital entered into a Joint Venture agreement to set up Puhua (Xi’an) Real

Estate Development Co., Ltd.(“Puhua”). We have a 75% interest in

Puhua.

On

January 20, 2009, we signed an equity purchase agreement with the

shareholders of Xi’an Xinxing Property management Co., Ltd. (“Xinxing Property”)

and acquired 100% ownership of Xinxing Property and its 100% subsidiary Xi’an

Xinxing Hotel management Co., Ltd. (“Xinxing Hotel”).

In March,

2009, we incorporated Wayfast Holdings Limited (“Wayfast”) with its 100%

subsidiary - Clever Advance Limited (“Clever Advance”) and Gracemind Holdings

Limited (“Gracemind”) with its 100% subsidiary - Treasure Asia Holdings Limited

(“Treasure Asia”). They were holding companies and inactive during the year

ended December 31, 2009.

5

CORPORATE

STRUCTURE

BUSINESS

Overview

We are a leading real estate

development company headquartered in Xi’an and doing business primarily in the

western part of China. We are a leading residential developer and dedicated to provide quality and

affordable housing to the middle class family..

Through our subsidiaries, Tsining, New

Land, PuHua, and Xinxing Property, we are engaged in the development,

construction, and sale of residential and commercial real estate units, as well

as land development in Western China. Tsining has completed a number of

significant real estate development and construction projects in Xi’an. Through

Tsining, we expand our business into other developing urban markets in Western

China.

Our

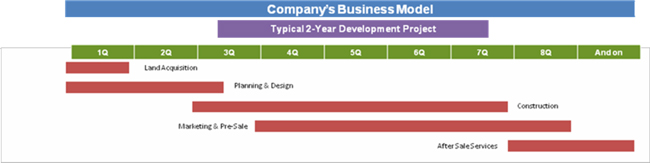

business model has proven to be efficient and profitable since its inception.

Typically, we divide each project into 5 deployment phases, spanning from land

acquisition to after sale services.

Our

average project development lasts over 2 years, and provides us with initial

cash flow after 3 quarters.

Land

Acquisition

To date,

we have been successful in acquiring land from many sources including open

market actions, co-development with local government and acquisitions of

distressed assets, such as bankrupt factories. We have achieved this through

long term working relations with the central and local

governments.

6

Planning

& Design

We work

with world class architectures for most of projects and maintain an an in-house

design team to combine our significant local knowledge. We also deploy advance

cost control system and enterprise resource planning system, which enable us to

monitor and analyze our construction cost and progress on a daily

basis.

Construction

We do not

undertake any construction– we outsource this function to qualified third

parties through competitive processes. We have a strong track record of working

with top construction companies and providing quality on-time

delivery.

Marketing

& Pre-Sales

We

initiate pre-sales once we finish the foundation construction and get the

pre-sales permit from the government– Our sales efforts are partly outsourced to

external professionals. Currently, we work with well known sales agents for our

developments, such as E-House and World Union Properties, which ranked number 1

and 2 in China, respectively. Pre-sales provide us with early income, with many

projects becoming cash flow positive within 9 months.

After

Sales Service

We always

follow up with our customers after a sale to ensure good relationships and

future recommendations. We also have a wholly-owned property management company

which performs integrated after-sales services.

Corporate

Information

Our

principal executive office is located at 6 Youyi Lu, Han Yuan 4th Floor, Xi’an,

710054, People’s Republic of China. Our telephone number at this address

is (86-29) 8258-2632 and our fax number is (86-29) 8258-2640.

Investor

inquiries should be directed to us at the address and telephone number of our

principal executive offices set forth above. Our website is http://www.chldinc.com

.

Our

Industry

We

primarily focus on the development, management and sale of residential real

estate properties in order to provide affordable housing to middle class

consumers in Western China, especially first time purchasers and first time

up-graders. Our current development projects are mainly located in

Xi’an, Shaanxi Province, the PRC. We are in the process of expanding into other

Tier II and Tier III cities in Western China.

Overall Industry

Overview

In early

2000, the Chinese real estate industry started to transition towards a

market-oriented system. Although the Chinese government still owns all urban

land in China, land use rights with terms of up to 70 years, can be granted to,

and owned or leased by, private individuals and companies. A large and active

market in the private sector has developed for sales and transfers of land use

rights which were initially granted by the Chinese government. All property

units built on such land belong to private developers for the term of period

indicated. The recent transition in the real estate industry’s structure in

China has fostered the development of real estate-related businesses, such as

property development, property management and real estate agencies.

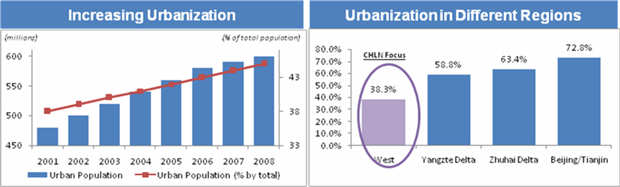

The

significant growth of the Chinese economy during the past decade has led to a

significant expansion of the real estate industry. This expansion has been

supported by other factors, including increasing urbanization, growing personal

affluence, as well as the emergence of the mortgage lending market. The

following table sets forth selected statistics for the overall real estate

industry in mainland China for the periods indicated.

|

For

the years ended December 31,

|

||||||||||||||||||||||||||||

|

2001-2008

|

||||||||||||||||||||||||||||

|

2001

|

2002

|

2003

|

2004

|

2005

|

2006

|

2007

|

2008

|

CAGR

|

||||||||||||||||||||

|

Invest

in real estate development($in billion)

|

76.6 | 94.2 | 122.5 | 158.9 | 192.2 | 290.4 | 345.4 | 417.7 | 25.20 | % | ||||||||||||||||||

|

Total

housing area (square feet in billion)

|

24.5 | 29.6 | 96.4 | 41.2 | 59.7 | 64.5 | 72.2 | 93.1 | 21.90 | % | ||||||||||||||||||

|

Average

price of properties sold($/square feet)

|

24.9 | 25.2 | 25.2 | 26.4 | 91.2 | 95.6 | 95.6 | 109.3 | 11.60 | % | ||||||||||||||||||

Source: China Statistic Year Book (all

government data is based on calendar year)

7

Growth

Drivers

West

China

We

believe the industry is well positioned to grow at comparable rates for the next

few years due to social, economic, regulatory and government stimulus-related

factors. Key growth drivers include the following:

|

|

·

|

“Go West” policy. The

"Go West" policy encourages economic development and population movement

to the West covering: 6 provinces, 5 autonomous regions and 1

municipality; this area covered 56% of mainland China with only

approximately 23% of its population. The plan was issued in 1999,

and is divided into 3 phases. Phase I form the bulk of the

strategy include infrastructure development (transport, hydropower plants,

energy, and telecommunications), introduction of foreign investment,

increased efforts on ecological protection (such as reforestation),

promotion of education, and retention of talent flowing to richer

provinces. As of 2009, over 1 trillion yuan has been spent building

infrastructure in Western China. The Western China’s GDP growth rate keeps

about 12% in the past 10 years, which is higher than the national average

(9.6%). Significant foreign and domestic investments in Xi’an

and throughout Western China are set to support the growth of the middle

income categories. The strong demand in residential properties is also

driven by increasing urbanization.

|

|

|

·

|

Increasing

Urbanization in West China. The urban

population in China has grown significantly over the past 10 years,

creating higher demand for housing in many

cities.

|

|

·

|

Urbanization

rates in the Tier II cities is higher than in the rest of

China

|

Over 300

million urban people are expected to need housing in urban areas over the next

two decades. According to data from Xi’an Statistical Bureau, in 2008 the

population of Xi’an was 8.4 million with an urbanization rate of 47%. The

government plan to increase the Xi’an population to 10.7 million with an

urbanization rate of 80% by 2020. The following table sets forth China’s urban

population, total population and urbanization rates for periods

indicated:

Source:

National Bureau of Statistics.

|

|

·

|

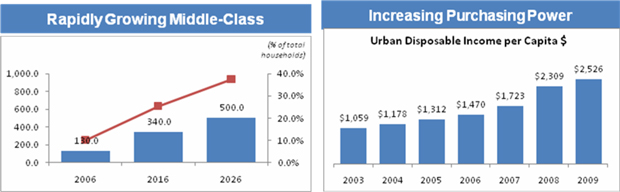

China’s

Rapidly Growing Middle-Class Population. China’s

current population stands at over 1.3 billion, and is expected to reach

1.4 billion in 2026. Among the population, the middle-class is growing

fastest with 130 million people in 2006 expected to grow to 500 million by

2026. The middle class is defined as house-holds with an annual income of

between $6,000 and $25,000, with housing being the number one spending

category. The rapid urbanization, growth in consumer spending coupled with

significant growth of urban disposable income per capita (more than

doubled from 2003 to 2009) and the low home ownership levels compared to

western countries make this population a massive driver of the future

growth of the Chinese real estate

market.

|

Source:

PRC State Council Development Research Center, and Monitor

Group.

8

|

|

·

|

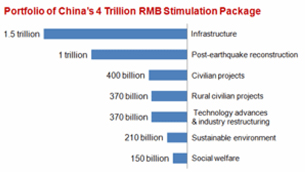

Government Stimulus. In

response to the global financial crisis, the PRC announced a 4 trillion

RMB stimulation program on November 27, 2008. Subsequently, on March 6,

2009, the National Development and Reform Commission Director, Mr. Zhang

Ping, announced a reshaping of the economic stimulus package that retained

the investment total of 4 trillion RMB but adjusted its focus. Within the

4 trillion RMB package, about 400 billion RMB will go toward civil works,

including low-income housing and renovation. Two additional categories

(370 billion RMB technology advances and 1.5 trillion RMB industry

restructuring and infrastructure) are also expected to benefit Xi’an’s

industries, and therefore further fuel demand in the city’s real estate

market.

|

Source:

Zhang Ping, National Development and Reform Commission, press conference, March

6, 2009.

Type of Cities in

China

China has

167 cities with a population of over 1 million. These cities are divided into 3

categories/tiers.

There are

significant differences distinguishing Tier I cities from Tier II cities in

China:

Tier

I

A group

of four cities, located near the East Coast, compose the group of Tier I cities:

Beijing, Shanghai, Shenzhen, and Guangzhou. These regions are more urbanized and

have higher GDP per capita. The residential real estate prices in those cities

have been skyrocketing and are the catalyst of many government policy

changes.

Tier

II and III

There are

over 35 Tier II and III cities with an accumulative population of 215 million

and demand for real estate properties in Tier II/III cities is strong.

Industrial expansion and improved infrastructure will support continued

urbanization and fuel the growth of the real estate sector in these

cities.

Typically,

housing is affordable for consumers in Tier II/III cities compared to Tier I

cities. Disposable income in Tier II/III have increased faster than real estate

prices and overall saving rates in Tier II/III cities are higher than in Tier I

cities.

Source:

Bureau of Statistics of the above cities

Economic

Developments

Rapid

economic growth in eastern China has made Tier I cities more mature, making

second- and third-tier cities a viable alternative for companies looking to

reduce its cost bases. This has subsequently caused a movement towards these

cities. Multinational corporations have been expanding out of mega cities along

the East Coast of China, such as Beijing, Shanghai, and Shenzhen, into

neighboring and inland cities. Intel, for example, recently opened a development

center in Chengdu, while the Liberty Mutual Group, has chosen

Chongqing for its Chinese headquarters. Unilever relocated its Chinese

headquarters from Shanghai to the neighboring province of Hefei due to the lower

labor and land costs and its strategic location.

9

The

Chinese government has also been instrumental in stimulating regional growth by

designating certain second-tier regions as priority zones. These actions are

benefitting Xi’an, our primary market, coupled with local growth which saw

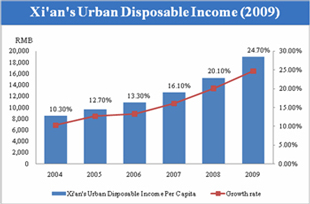

Xi’an’s urban disposable income grow 24.7 percent in 2009.

As the

ripple effect of economic growth continues to permeate second-tier cities and

create a healthy environment for real estate development, leading indicators are

signaling continuing moderate growth in local property markets.

Source:

CEIC and E-House Company Reports.

City of

Xi’an

Background

Xi’an

served as the capital of China during 13 dynasties (from West Zhou in 1066 BC to

Tang in 907 AD) and is well known for its Terracotta Army and other famous

historic landmarks. Today, the city’s economic leadership is derived from its

high-technology, pharmaceutical, military, aerospace, tourism, and advanced

education industries. The central government’s “Go West” policy has

designated Xi’an as the regional economic hub of Western China. To further

encourage Western China’s development, the central government plans to establish

the Central Shanxi Plain Economic Region that will help enable the free flow of

people, skill, capital, and trade among the western provinces. Xi’an, as the

economic center of Western China, will play a unique leadership role among the

western tier-two cities.

Xi’an is

slowly becoming an international city which boasts a large and educated work

force. The city has China’s third largest university-educated workforce, making

it a hotbed for research & development, high-technology manufacturing and

information technology solutions. Xi’an has begun to attract

high-tech companies, including IBM, Applied Materials, Micron Technology, and

Infineon. Applied Materials, for example, selected Xi’an for its $255 million

phase one R&D center that will design and develop equipment for

semiconductor chip manufacturing. In addition, Micron Technology has invested

$250 million in Xi’an for packaging and testing of semiconductor

chips.

China has

announced its intention to become a world-class center for information

technology research and development, production, outsourcing and services to

rival and potentially surpass the success of India’s IT industry. Xi’an is

expected to play an important role in that effort, having been designated by the

government as one of five China Outsourcing Bases. Similar to Bangalore and

Hyderabad, the Xi’an local government is carving out a niche in IT outsourcing

by creating the 400,000 square-meter Xi’an Software Park. The park has already

attracted top software and technology companies, including IBM, which is the

government’s joint venture partner in creating the software park. Sybase, SPSS,

Nortel, Fujouru, and NEC are already operating in the park. The Xi’an local

government anticipates that the city’s IT outsourcing workforce will grow

to 200,000 by 2010.

The Xi’an

local government has laid out a master plan through the year 2020 to foster

economic transformation and urbanization. For example, Xi’an is now limiting

development in the city’s famous historical Gated Wall City (or Inner Ring),

which will be revamped primarily for tourism. The city plans to relocate about

450,000 residents from the Inner Ring to the second, third, and fourth rings of

the city and beyond. One of the most ambitious plans is the

development of a new satellite city in the Baqiao district, about eight

kilometers from Xi’an’s center. The local government is developing the Baqiao

district into the “First Water City of the West”, complete with high-end

residential properties and hotels, international convention centers and a

high-technology industry center. The new urban area will be home for 900,000

middle-to-upper income residents and for firms in industries that include

R&D, services and high-technology, plus the potential headquarters for the

Chinese operations of multinational corporations.

Emerging

as an international city

Xi’an’s

local government has been proactive in enhancing the city’s international image

by hosting world class events like the Euro-Asia Economic Forum every second

year and the Formula One Powerboat World Championship. To attract international

tourists, Xi’an is leveraging its famous historical and cultural significance.

Xi’an has revamped its tourism infrastructure in numerous ways, including the

redevelopment of the famous Terracotta theme park. It has also selected China’s

largest construction company to build a RMB 20 billion ($2.5 billion) theme park

and a residential and commercial redevelopment project on the grounds of the

famous Da Ming Gong Palace that was built 1,300 years ago during the Tang

Dynasty. The city has also built out infrastructure to attract international

travelers and is drawing large foreign retailers. Several large retailers have

entered Xi’an, including Wal-mart, Carrefour, and Metro of Germany. Xi’an’s

historic mystique and economic potential has also lured top luxury brands,

including Louis Vuitton, Gucci, Prada and Versace to open

outlets.

10

Xi’an real estate

market

Strong

fundamentals

We

believe that demographic and economic factors, including emerging high-tech

industries and increasing foreign capital inflow will stimulate Xi’an’s future

growth. In 2008, the Xi’an population was 8.4 million, the average urban living

area per person was 26.3 square meters, lower than China’s urban average of 28

square meters per person in the same year. Xi’an has announced plans to increase

the population to 10.7 million and the average living area per person to 33

square meters by 2020, which will require an additional 132 million square

meters of new developments by 2020. Despite the solid economic growth and rising

housing demand, real estate prices in Xi’an are still less than half of those in

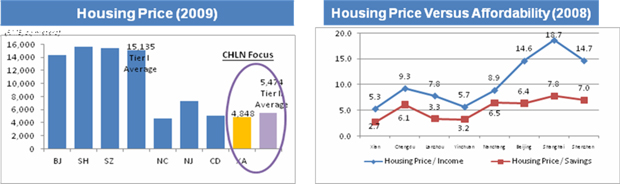

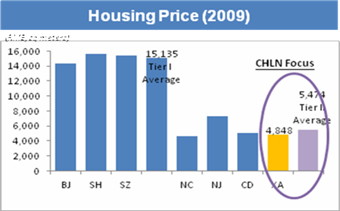

the mega cities such as Shanghai, Beijing and Shenzhen.

Sources: National Bureau of

Statistics and E-House China Real Estate Research Institute, Xi’an

Branch.

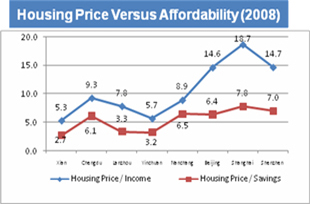

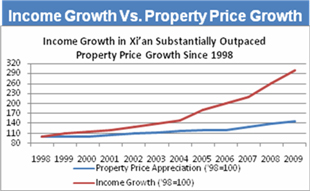

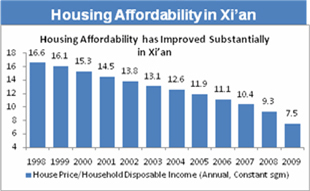

Xi’an:

Growing, leading, and still affordable

Despite

its role as the economic hub of Western China, Xi’an’s disposable income per

capita is increasing significantly over the past years, as shown below. Compared

to other cities, Xi’an is more affordable.

|

|

|

Source: Xi’an bureau of

statistics

|

Source: Bureau of statistics

of above

cities.

|

11

|

|

| Source: NBS, Xi’an Bureau of Statistics, CEIC |

Source: NBS, Xi’an Bureau of

Statistics, CEIC

|

2009 and Early 2010 Xi’an market

update

The first

half of 2008 saw a market slowdown in China’s real estate industry. In 2009,

Xi’an real estate market started to recover from 2008’s downturn. The market

boosted from the first quarter for the whole year. Both sales volume and prices

were up. The Xi’an real estate market continued to appreciate in January and

February 2010. Residential pre-sales volume, measured by per square meter sold

in the January-February 2010 period, increased 37.6 percent from the same

two-month period of 2009. Residential pre-sales average price per

square meter increased by 20.8 percent in January and by 14.3 percent in

February 2010 compared with January and February of 2009,

respectively.

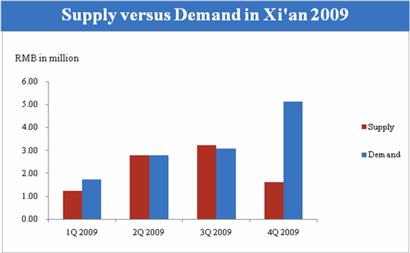

Xi’an’s

Transaction and Supply in 2009

Source:

E House (China) report.

Supply/demand

in Xi’an

According

to a CRIC’s research report, the demand and supply relationship in the Xi’an

area is considered to be in a healthy condition, with a supply/demand ratio of

0.3 at the end of 2009. During 2009, the total new supply of salable GFA to the

Xi’an market was 10.3 million square meters, and sold area has reached 14.1

million square meters. The imbalance has caused the market inventory to decrease

significantly. By December 2009, the total salable inventory in Xi’an is about

9.2 million square meters, which is estimated to be able to meet the market

demand for only 8 months, by using the average consumption rate during

2009.

Competitive

Landscape

The real

estate development business in China is organized into 4 levels under the

structure of the “Qualification Certificate for Real Estate Development

Enterprise.” The starting level is Level 4 (see table below). A company may

climb the scale to participate in larger projects. However, only one level may

be ascended per year. We had gained Level 1 status under the China Ministry of

Construction licensing policy in December 20, 2006.

12

|

Registered

Capital

(million)

|

Experience

(years)

|

Developed

Are

(square

feet)

|

||||||||||

|

Level

1

|

$ | 6.25 | 5 | 3,229,278 | ||||||||

|

Level

2

|

$ | 2.5 | 3 | 1,614,639 | ||||||||

|

Level

3

|

$ | 1 | 2 | 538,213 | ||||||||

|

Level

4

|

$ | 0.125 | 1 | N/A | ||||||||

On the

national level, there are numerous Level 1 companies involved in real estate

projects across China (to develop in multiple regions a Level 1 status is

required). There are 79 housing and land development companies listed on the

Shanghai, Shenzhen and Hong Kong Stock Exchanges. However, such companies

usually undertake large scale projects focusing on high-end families. We do not

consider these as direct competitors as we target small to medium size projects,

and focus on middle-class family.

We are

aware of two companies in Xi’an which may be considered to be direct competitors

in the small to medium sized project sector:

Xian

TANDE CO.,LTD.. (Level 1), is one of the largest real estate developers in Xian.

This company is a state-owned enterprise established in May 1991, and listed on

Shanghai Exchange in 2006( 600665, Shanghai Exchange) . The Company generally

undertakes larger scale projects and expanded their business into Shengzhen,

Suzhou and Tianjing in 2007. By the end of December, 2009, the Company had

completed five projects, with a total GFA of 1.4 million square meter. The

Company is now operating one project in Xian with a total GFA of 140,000 square

meter, one project in Shenzhen with 50,000 square meters, one project in

Tianjing with 100,000 square meter and two projects in Suzhou with 280,000

square meter. As the state-owned entity, they need to conduct some government

function including building public space and certain infrastructure work, which

hurt their profitability. In the last 3 years, their net profit rate ranged from

5% to 8%.

Xi’an

Ziwei Development Company (Level 1), is a state-owned enterprise established in

1999. This company has five projects completed with a total construction area of

around 4 million square meters. It has eight projects currently under

development with a total construction area of 1.5 million square meters. Since

the Company is controlled by the Xi’an High-Tech Zone Government most of the

Company’s developments are located in Northwest of Xi’an city. In 2009, the

Company already expanded their business to the Northern part of the Shaanxi

province.

Projects

under construction

|

Project

Name

|

Type of

Projects

|

Actual or

Estimated

Construction

Period

|

Actual or

Estimated Pre-sale

Commencement

Date

|

Total Site

Area

(m2)

|

Total

Gross

Floor Area

(m2)

|

Sold GFA

by December

31, 2009

(m2)

|

||||||||||||

|

JunJing

II

phase

one

|

Multi-Family

residential

&

Commercial

|

Q3/

2007

- Q3/2009

|

Q2/2008

|

39,524 | 136,012 | 118,961 | ||||||||||||

|

JunJing

II

phase

two

|

Multi-Family

residential

&

Commercial

|

Q2/2009

- Q2/2011

|

Q3/2009

|

29,800 | 112,556 | 55,561 | ||||||||||||

|

Puhua

Project

|

Multi-Family

residential

&

Commercial

|

Q2/2009

- Q3/2014

|

Q4/2009

|

195,582 | 610,000 | 24,129 | ||||||||||||

|

Project

name

|

Total

Number of

Units

|

Number of

Units sold by

December 31,

2009

|

Estimated

Revenue

(million)

|

Contracted

Revenue by

December 31, 2009

(million)

|

Recognized

Revenue by

December 31, 2009

(million)

|

|||||||||||||||

|

JunJing

II

phase

one

|

1,182 | 1,126 | 95.6 | 72.5 | 72.5 | |||||||||||||||

|

JunJing

II

phase

two

|

1,015 | 516 | 94.1 | 40.5 | 25.8 | |||||||||||||||

|

Puhua

Project

|

5,000 | 195 | 700.0 | 15.0 | - | |||||||||||||||

13

JunJing II: JunJing II is

located at 38 East Hujiamiao, Xi’an, with total GFA about 248,568 square meters.

It is the first Canadian style residential community with “green and

energy-saving” characteristics.” The project is divided into 2 phases, namely

JunJing II phase one and JunJing II phase two. We started the construction of

JunJing II phase one in the third quarter of 2007 and started the presale

campaign in the second quarter of 2007. Up to

December 31, 2009, our customers have signed pre-sale purchase agreements for

apartments in JunJing II phase one with purchase prices totaling $72.5 million,

of which we have recognized $72.5 million in revenues.

The

construction of Phase Two commenced in the second quarter of 2009 and pre-sales

started within the same quarter. As of December 31, 2009, the contract revenue

for Phase Two is $40.5 million, of which we have recognized $25.8 million in

revenues.

For

JunJing II and Puhua projects approximately $8.4 million of pre-sale payments

were booked as advances from costumers and will be recognized as revenues as

construction advances.

Puhua: The Puhua project, the

Company’s 79 acre joint venture located in the Baqiao New Development Zone, has

a total land area of 192,582 square meters and an expected GFA of approximately

640,000 square meters. In November 2008, the Company entered into an agreement

with Prax Capital China Real Estate Fund I, Ltd., to form a joint venture.

The joint venture was formed in late 2008 when Prax Capital Real Estate Holdings

Limited invested US$29.3 million. The joint venture acquired the land use rights

early in the first quarter of 2009.

The

construction of the Puhua project began in June 2009. The whole project, which

consists of four phases, is expected to be completed in the third quarter of

2014, with estimated revenues of $700 million. The Company began accepting

pre-sale contracts for units in the Puhua Phase One project on October 24th,

2009. As of December 31, 2009, the contract sales for Puhua project are $15

million.

Projects

under planning and in process

|

Project

Name

|

Type

of Projects

|

Estimated

Construction

Period

|

Estimated

Pre-sale

Commencement

|

Total

Site

Area

(m2)

|

Total GFA

(m2)

|

Total

Number of

Units

|

||||||||||||

|

Baqiao

New

Development

Zone

|

Land

Development

|

2009-

2020

|

N/A | N/A | N/A | N/A | ||||||||||||

|

JunJing

III

|

Multi-Family

residential

&

Commercial

|

Q1/2010

- Q1/2012

|

Q2/2010 | 8,094 | 47,586 | 570 | ||||||||||||

|

Park

Plaza

|

Multi-Family

residential

&

Commercial

|

Q3/2010

- Q4/2014

|

Q4/2010 | 44,250 | 180,000 | 2,000 | ||||||||||||

|

Golden

Bay

|

Multi-Family

residential

&

Commercial

|

Q4/2010

- Q4/2014

|

Q1/2011 | 146,099 | 378,887 | N/A | ||||||||||||

Baqiao New Development Zone:

On March 9, 2007, we entered into a Shares Transfer Agreement with the

shareholders of Xi’an New Land Development Co., Ltd. (New Land), under which the

Company acquired 32,000,000 shares of New Land, constituting 100 percent equity

ownership of New Land. This acquisition gave the Company the exclusive right to

develop and sell 487 acres of land in a newly designated satellite city of

Xi’an.

Xi’an has

designated the Baqiao District as a major resettlement zone where the city

expects 900,000 middle to upper income inhabitants to settle. The Xi’an local

government intends to generate a success similar to that created in Pudong,

Shanghai, which has resulted in new economic opportunities and provided housing

for Shanghai’s growing population.

The Xi’an

municipal government plans investments of 50 billion RMB (over $6 billion) in

infrastructure in the Baqiao New Development Zone. The construction of a

large-scale public wetland park is well underway; it will embellish the natural

environment adjacent to China Housing’s Baqiao project.

|

Through

its New Land subsidiary, China Housing sold 18.4 acres to another

developer in 2007 and generated about $24.41 million in

revenue.

In

2008, we established a joint venture with Prax Capital Real Estate

Holdings Limited (Prax Capital) to develop 79 acres within the Baqiao

project, which will be the first phase of the Baqiao project’s

development. Prax Capital invested $29.3 million cash in the joint

venture. The project is further described in the Puhua section

below.

|

|

|

14

|

After

selling 18.4 acres and placing 79 acres in the joint venture, about 390

acres remained available for the Company to develop in the Baqiao

project.

|

||

|

JunJing III: JunJing

III is located near our JunJing II project and the city expressway. It

will have an expected total GFAof about 47,586 square meters. The

project will consist of 3 high rise buildings, each 28 to 30 stories high.

The project is targeting middle to high income customers who require a

high quality living environment and convenient transportation to the city

center. We plan to start construction during the first quarter 2010 and

expect pre-sales to begin during the second quarter of 2010.The total

estimated revenue from this project is about $46 million.

|

Park Plaza: In July 2009, the

Company entered into a Letter of Intent to acquire 44,250 square meters of land

in the center of Xi'an for the Park Plaza project. The Company intends to

develop a large mid-upper income residential and commercial development project

on this site, with a gross floor area of 162,000 square meters. The four-year

construction of Park Plaza is expected to begin in the fourth quarter 2010. We

anticipate accepting pre-sale purchase agreements in the second quarter of 2010,

and revenues from pre-sale agreements will begin to be recognized when all

revenue recognition criteria have been met. The total revenue from Park Plaza is

estimated to be $154 million.

Golden Bay: The Golden Bay

project is located within the Baqiao project, with a total GFA of 378,887 square

meters. The Golden Bay project will consist of residential buildings as well as

a commercial area. Construction is anticipated to begin in the fourth quarter of

2010, and we expect to begin accepting pre-sale purchase agreements in the first

quarter of 2011.

Completed

Projects with units available for sale

|

Project name

|

Type of

Projects

|

Completion

Date

|

|

Total Site

Area

(m2)

|

|

|

Total GFA

(m2)

|

|

|

Total

Number of

Units

|

|

|

Number of

Units sold by

December31,

2009

|

|

||||

|

Tsining

Home IN

|

Multi-Family

residential &

Commercial

|

Q4/2003

|

8,483

|

30,072

|

215

|

213

|

||||||||||||

|

Tsining-24G

|

Hotel,

Commercial

|

Q2/2006

|

8,227

|

43,563

|

773

|

748

|

||||||||||||

|

JunJing

I

|

Multi-Family

residential &

Commercial

|

Q3/2006

|

55,588

|

167,931

|

1,671

|

1,640

|

||||||||||||

|

Tsining

Gangwan

|

Multi-Family

residential &

Commercial

|

Q4/2004

|

12,184

|

41,803

|

466

|

466

|

||||||||||||

Tsining Home IN: Located near

the city center, the Home IN project consists of 215 two and three bedroom

western-style apartments. Total construction area is 30,072 square meters. The

project, completed in December 2003, generated total sales of $13.32

million.

Tsining-24G: 133 Changle

Road, Xi’an. 24G is a redevelopment of an existing 26 floor building, located in

the center of the most mature and developed commercial belt of the city. This

upscale development includes secured parking, cable TV, hot water, air

conditioning, natural gas access, internet connection, and exercise facilities.

This project was awarded “The Most Investment Potential Award in Xi’an

city” in 2006, Its target customers were white-collar workers, small

business owners, traders, and entrepreneurs. Total area available for

residential use was 43,563 square meters, covering 773 one to three bedroom

serviced apartments. The project started construction in June 2005 and was

completed in June 2006. Sales totaled $42.10 million.

Tsining JunJing Garden I: 369

North Jinhua Road, Xi’an. It is the first German style residential &

commercial community in Xi’an, designed by the world-famous WSP architectural

design house. Its target Customers were local middle income families. The

project has 15 residential apartment buildings consisting of 1,671 one to five

bedroom apartments. The Garden features secured parking, cable TV, hot water,

heating systems, and access to natural gas. Total GFA available was 167,931

square meters. JunJing Garden I was also a commercial venture that houses small

businesses serving the needs of JunJing Garden I residents and surrounding

residential communities. The project was completed in September 2006 and

generated total revenue $48.27 million.

Tsining Gang Wan: 123 Laodong

Road, Xi’an. Less than one mile from the western hi-tech industrial zone,

GangWan spans three acres and

is comprised of eight buildings with a total construction area of 41,803 square

meters. The project began in April 2003 and was

completed in December 2004. GangWan has 466 apartments ranging from one to three

bedrooms. Total sales were $18.51 million as of

December 31, 2009.

15

Sales

and Marketing

Pre-Sales

and Sales

In China,

developers typically start to market and offer properties before construction is

completed. Under PRC pre-sales regulations, property developers must satisfy

specific conditions before they can pre-sell properties that are under

construction. These mandatory conditions include:

|

|

the

land premium must have been paid in

full;

|

|

the

land use rights certificate, the construction site planning permit, the

construction work planning permit and the construction permit must have

been obtained;

|

|

|

at

least 25% of the total project development cost must have been

incurred;

|

|

|

the

progress and the expected completion and delivery date of the construction

must be fixed;

|

|

|

the

pre-sale permit must have been obtained;

and

|

|

|

the

completion of certain milestones in the construction processes must be

specified by the local government

authorities.

|

These

mandatory conditions require a certain level of capital expenditure and

substantial progress in project construction before commencement of

pre-sales. Developers are required to file all pre-sale contracts

with local land bureaus and real estate administrations after entering into such

contracts.

We

benefit from a strong sales and marketing platform which is complemented by

professional third party sales agents for maximum impact. As we are

able to manage our customer relationship, the majority of our sales are

generated by recommendations by existing customers; the new sales initiatives of

our sales department generate approximately 44% of our total

sales. More than 70% of our customers are first time buyers (who are

looking to getting on the property ladder).

After-sale

Services and Delivery

We assist

customers in arranging financing as well as various title registration

procedures related to their properties. We have also set up an ownership

certificate team to assist purchasers to obtain property ownership

certificates.

We

closely monitor the progress of construction of our property projects and

conduct pre-delivery property inspections to ensure timely delivery. The time

frame for delivery is set out in the sale and purchase agreements entered into

with our customers, and we are subject to penalty payments to the purchasers for

any delay in delivery caused by us. Once a property development has been

completed and passed the requisite government inspections, we will notify our

customers and hand over keys and possession of the properties.

We

operate a wholly owned property management company that manages properties and

ancillary facilities. We frequently follow up with our customers after the sale

to ensure a good relationship and further recommendations.

Marketing

As of

February 28, 2010, we maintain a marketing and sales force for our development

projects with 20 personnel specializing in marketing and sales. We also train

and use outside real estate agents to market and increase the public awareness

of our products, and spread the acceptance and influence of our brand. However,

we primarily let our own sales force represent our brand and project rather than

rely on third party brokers or agents for the reason that we believe our own

dedicated sales representatives are better motivated to serve our customers and

to control our property pricing and selling expenses.

Quality

Control

We

utilize quality control to ensure that our buildings and residential units meet

high standards. Through our contractors, we provide customers with warranties

covering the building structure and certain fittings and facilities of our

property developments in accordance with the relevant regulations. To ensure

construction quality, our construction contracts contain quality warranties and

penalty provisions for poor work quality. We do not allow contractors to

subcontract or transfer their contractual arrangements to third parties. We

typically withhold 5% of the agreed construction fees for two to five years

after completion of the construction as a deposit.

Governmental

and environmental Regulations

To date,

we have been compliant with all registrations and requirements for the issuance

and maintenance of all licenses required by the applicable governing authorities

in China. These licenses include:

|

|

•

|

“Qualification

Certificate for Real Estate Development” authorized by the Shaanxi

Construction Bureau, effective from December 20, 2006 to December 20,

2009. License No: JianKaiQi (2006) 603. The housing and land development

process is regulated by the Ministry of Construction and

authorized by the local offices of the Ministry. Each development

project must obtain the following

licenses:

|

16

|

•

|

“License

for Construction Area Planning” and “License for Construction Project

Planning”, authorized by Xian Bureau of Municipal

Design;

|

|

•

|

“Building

Permit” authorized by the Committee of Municipal and Rural

Construction;

|

After

construction is complete, the project meets certain standards in order to obtain

a validation certificate. These standards are regulated by the Local Ministry of

Construction Bureau.

Housing

and land development sales companies are regulated by the Ministry of Land &

Natural Resources and authorized by the local office of the Ministry. Each

project has to be authorized and must obtain a “Commercial License for Housing

Sale” from the Real Estate Bureau.

Employees

As

of February 28, 2010, we had 714 employees, including 52 in China

Housing and Land Development, inc, 32 in Tsining, 32 in Puhua and 598 in

Xinxing Property Management.

We

believe we have a good working relationship with our employees. We are not a

party to any collective bargaining agreements. At present, no significant change

in our staffing is expected over the next 12 months, except for our acquisition

of the property management company we acquired in January 2009. All employees

are eligible for performance-based compensation.

17

ITEM

1A. RISK FACTORS

The

investment in our company has a high degree of risk. Before you invest you

should carefully consider the risks and uncertainties described below and

the other information in this filing. If any of the following risks

actually occur, our business, operating results, and financial condition could

be harmed and the value of our stock could go down. This means you

could lose all or a part of your investment.

Risks

Related to Our Business

Our

home sales and operating revenues could decline due to macro-economic and other

factors outside of our control, such as changes in consumer confidence and

declines in employment levels.

Changes

in national and regional economic conditions, as well as local economic

conditions where the Company conducts its operations and where

prospective purchasers of our homes live, may result in more caution on the

part of home buyers and consequently may make fewer home purchases. These

economic uncertainties involve, among other things, conditions of supply

and demand in local markets and changes in consumer confidence and income,

employment levels, and government regulations. These risks and

uncertainties could periodically have an adverse effect on consumer demand for

and the pricing of our homes, which could cause our operating revenues

to decline. In addition, builders are subject to various risks, many of them

outside the control of the homebuilder including competitive overbuilding,

availability and cost of building lots, materials and labor, adverse weather

conditions which can cause delays in construction schedules, cost overruns,

changes in government regulations, and increases in real estate taxes and other

local government fees. A reduction in our revenues could, in

turn, negatively affect the market price of our securities.

An increase in mortgage interest

rates or unavailability of mortgage financing may reduce consumer demand for the

Company’s homes.

Virtually

all purchasers of our homes finance their acquisitions through lenders providing

mortgage financing. A substantial increase in mortgage interest rates

or unavailability of mortgage financing would adversely affect the ability

of prospective home buyers to obtain the financing they would need in order

to purchase our homes, as well as adversely affect the ability of

prospective move-up home buyers to sell their current homes. For

example, if mortgage financing became less available, demand for our

homes could decline. A reduction in demand could also have an adverse effect on

the pricing of our homes because we and our competitors may reduce prices

in an effort to better compete for home buyers. A reduction in pricing could

result in a decline in revenues and in our margins.

We

could experience a reduction in home sales and revenues or reduced cash flows if

we are unable to obtain reasonably priced financing to support

our home building and land development activities.

The real

estate development industry is capital intensive, and development requires

significant up-front expenditures to acquire land and begin

development. Accordingly, we incur substantial indebtedness to finance our

home building and land development activities. Although we believe that

internally generated funds and current borrowing capacity will be

sufficient to fund our capital and other expenditures (including land

acquisition, development, and construction activities), the amounts

available from such sources may not be adequate to meet our needs. If such

sources are not sufficient, we would seek additional capital in the form of

debt or equity financing from a variety of potential sources, including bank

financing and or securities offerings. The availability of borrowed funds,

to be used for land acquisition, development, and construction, may be

greatly reduced, and the lending community may require increased amounts of

equity to be invested in a project by borrowers in connection with new

loans. The failure to obtain sufficient capital to fund our planned capital and

other expenditures could have a material adverse effect on our

business.

We are subject to extensive

government regulation which could cause the Company to incur significant

liabilities or restrict its business activities.

Regulatory

requirements also could cause us to incur significant liabilities and operating

expenses and could restrict our business activities. We are subject to

statutes and rules regulating, among other things, certain developmental

matters, building and site design, and matters concerning the protection of

health and the environment. Our operating expenses may be increased by

governmental regulations such as building permit allocation ordinances and other

fees and taxes, which may be imposed to defray the cost of providing

certain governmental services and improvements. Any delay or refusal from

government agencies to grant us necessary licenses, permits, and approvals

could have an adverse effect on our operations.

18

We

may require additional capital in the future, which may not be available on

favorable terms or at all.

Our

future capital requirements will depend on many factors, including industry and

market conditions, our ability to successfully implement our new

branding and marketing initiative, and expansion of our production

capabilities. We anticipate that we may need to raise additional funds in

order to grow our business and implement our business strategy. We

anticipate that any such additional funds would be raised through equity or debt

financings. In addition, we may enter into a revolving credit facility or a

term loan facility with one or more syndicates of lenders. Any equity or debt

financing, if available at all, may be on terms that are not favorable to

us. Even if we are able to raise capital through equity or debt financings, as

to which there can be no assurance, the interest of existing shareholders

in our company may be diluted, and the securities we issue may have rights,

preferences, and privileges that are senior to those of our common stock or

may otherwise materially and adversely affect the holdings or rights of our

existing shareholders. If we cannot obtain adequate capital, we may not be able

to fully implement our business strategy, and our business, results of

operations, and financial condition would be adversely affected. See also

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations — Liquidity and Capital Resources.” In addition, we have and will

continue to raise additional capital through private placements or

registered offerings, in which broker-dealers will be engaged. The activities of

such broker-dealers are highly regulated, and we cannot assure that the

activities of such broker-dealers will not violate relevant regulations and

generate liabilities despite our expectation otherwise.

We

depend on the availability of additional human resources for future

growth.

We are

currently experiencing a period of significant growth in our sales volume. We

believe that continued expansion is essential for us to remain

competitive and to capitalize on the growth potential of our business. Such

expansion may place a significant strain on our management and operations and

financial resources. As our operations continue to grow, we will have to

continually improve our management, operational and financial systems,

procedures and controls, and other resources infrastructure, and expand our

workforce. There can be no assurance that our existing or future management,

operating and financial systems, procedures, and controls will be adequate

to support our operations, or that we will be able to recruit, retain, and

motivate employees. Further, there can be no assurance that we will be

able to establish, develop, or maintain the business relationships beneficial to

our operations, or to do so or to implement any of the above activities in

a timely manner. Failure to manage our growth effectively could have a material

adverse effect on our business and the results of our operations and

financial condition.

We

may be adversely affected by the fluctuation in raw material prices and selling

prices of our products.

Our

projects and the raw materials we use have experienced significant price

fluctuations in the past. There is no assurance that they will not be subject to

future price fluctuations or pricing control. The land and raw materials we

use may experience price volatility caused by events such as market fluctuations

or changes in governmental programs. The market price of land and raw

materials may also experience significant upward adjustment, if, for instance,

there is a material under-supply or over-demand in the market. These price

changes may ultimately result in increases in the selling prices of our

products, and may, in turn, adversely affect our sales volume, revenue, and

operating profit.

We

could be adversely affected by the occurrence of natural disasters.

From time

to time, our developed sites may experience strong winds, storms, floods, and

earthquakes. Natural disasters could impede operations and or

damage infrastructure necessary to our constructions and operations. The

occurrence of natural disasters could adversely affect our business, the results

of our operations, prospects, and financial condition, even though we

currently have insurance against damages caused by natural disasters, including

typhoons, accidents, or similar events.

We

are dependent on third-party subcontractors, manufacturers, and distributors for

all construction services and supply construction materials, and a discontinued

supply of such services and materials will adversely affect our construction

projects.

The

Company is dependent on third-party subcontractors, manufacturers, and

distributors for all construction services and supply construction materials.

Construction services or products purchased from the Company’s five largest

subcontractors/suppliers accounted for approximately 30% for the year ended

December 31, 2009. A discontinued supply of such services and materials

will adversely affect our construction projects.

Intense

competition from existing and new entities may adversely affect our revenues and

profitability.

In

general, the property development industry is intensely competitive and highly

fragmented. We compete with various companies. Many of our competitors

are more established than we are and have significantly greater financial,

technical, marketing, and other resources than we presently possess. Some of

our competitors have greater name recognition and a larger customer base.

These competitors may be able to respond more quickly to new or changing

opportunities and customer requirements and may be able to undertake more

extensive promotional activities, offer more attractive terms to customers, and

adopt more aggressive pricing policies. We intend to create greater

awareness for our brand name so that we can successfully compete with our

competitors. We cannot assure you that we will be able to compete

effectively or successfully with current or future competitors or that the

competitive pressures we face will not harm our business.

Our

operating subsidiaries must comply with environmental protection laws that could

adversely affect our profitability.

We are

required to comply with the environmental protection laws and regulations

promulgated by the national and local governments of the People’s

Republic of China (“PRC” or “China”). Some of these regulations govern the

level of fees payable to government entities providing environmental protection

services and the prescribed standards relating to the constructions.

Although our construction technologies allow us to efficiently control the level

of pollution resulting from our construction process, due to the nature of

our business, wastes are unavoidably generated in the processes. If we fail to

comply with any of these environmental laws and regulations in the PRC,

depending on the types and seriousness of the violation, we may be subject to,

among other things, warning from relevant authorities, imposition of

fines, specific performance and/or criminal liability, forfeiture of profits

made, being ordered to close down our business operations, and suspension

of relevant permits.

19

Our

success depends on our management team and other key personnel, the loss of any

of whom could disrupt our business operations.

Our

future success will depend in substantial part on the continued service of our

senior management, including Mr. Lu Pingji, our Chairman of the Board of

Directors, Mr. Feng Xiaohong, our Chief Executive Officer, and Ms. Lu Jing, our

Chief Operating Officer. The loss of the services of one or more of our

key people could impede implementation of our business plan and result

in reduced profitability. We do not carry key person life or other insurance in

respect of any of our officers or employees. Our future success will

also depend on the continued ability to attract, retain, and motivate

highly qualified technical, sales and marketing, customer support, and

other employees. Because of the rapid growth of the economy in the People’s

Republic of China, competition for qualified people is intense. We cannot

guarantee that we will be able to retain our key people or that we will be

able to attract, assimilate, or retain qualified people in the

future.

Risk

Relating to the Residential Property Industry in China

We

are heavily dependent on the performance of the residential property market in

China, which is at a relatively early development stage.

The

residential property industry in the PRC is still in a relatively early stage of

development. Although demand for residential property in the PRC has

been growing rapidly in recent years, such growth is often coupled with

volatility in market conditions and fluctuation in property prices. It is

extremely difficult to predict how much and when demand will develop, as

many social, political, economic, legal, and other factors, most of which are

beyond our control, may affect the development of the market. The level of

uncertainty is increased by the limited availability of accurate financial and