Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT ON FORM 8K - PROASSURANCE CORP | bodyoffiling.htm |

March 8-10, 2010

W. Stancil Starnes Chairman and Chief Executive Officer

Edward L. Rand, Jr. Chief Financial Officer

Frank B. O’Neil Investor Relations Officer

Raymond James & Associates

Raymond James & Associates

31st Annual Institutional Investors Conference

31st Annual Institutional Investors Conference

2

Forward Looking Statements

This presentation contains Forward Looking Statements and other information designed

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

This presentation contains Non-GAAP measures, and we may reference

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP Measures

Year-to-Year Success Comes From

Taking a Long-Term View

Year-to-Year Success Comes From

Taking a Long-Term View

Edward L. Rand, Jr.

Chief Financial Officer

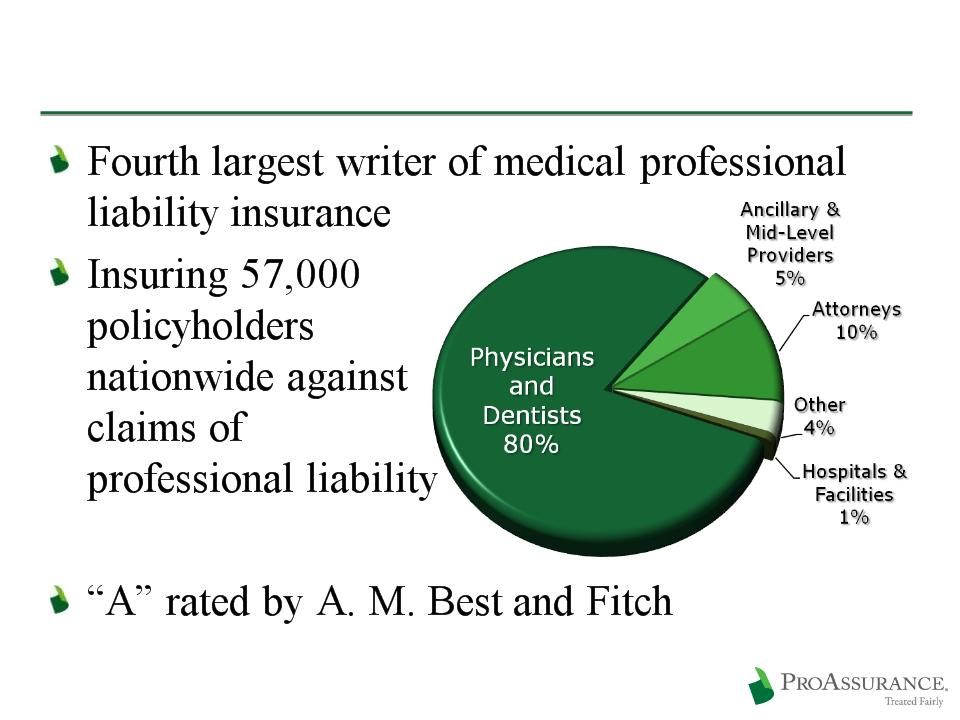

ProAssurance: Quick Facts

4

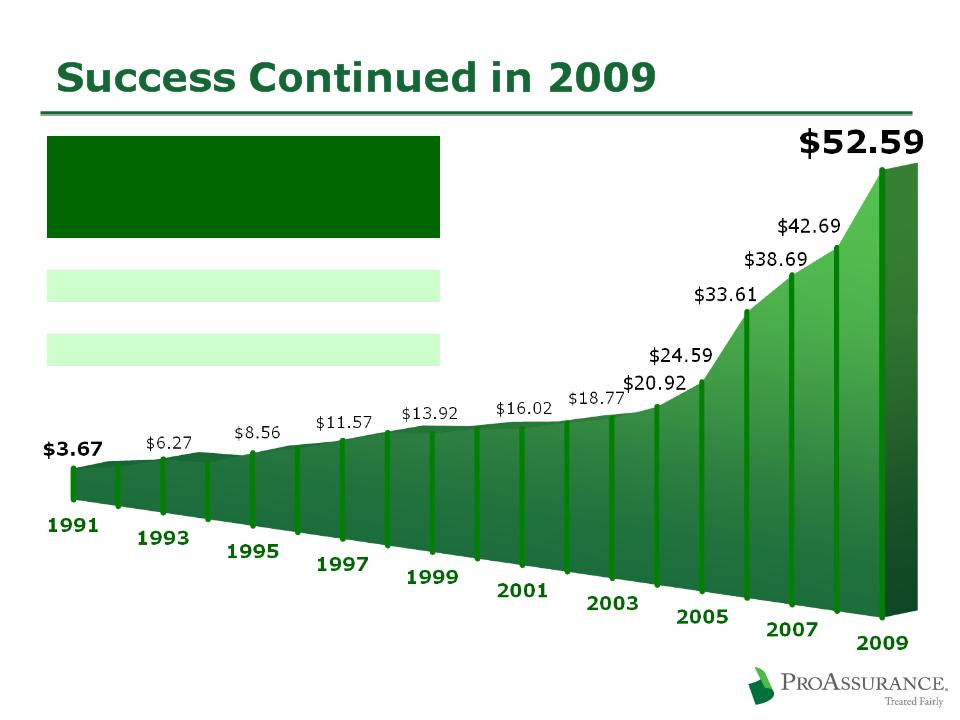

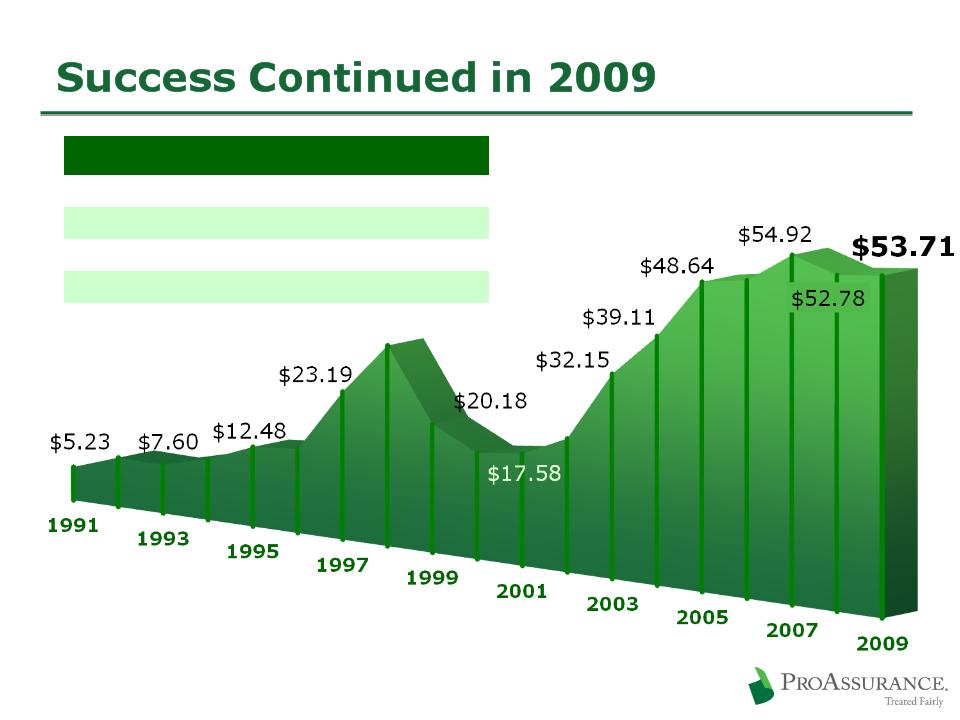

Success Continued in 2009

23% Increase in Book Value per Share in 2009

19% Increase in Revenue vs. 2008

28% Increase in Diluted EPS

Top Line Growth

$28 million of new business in our historical book

$95 million from completed M&A transactions

Three transactions completed in 2009

Outstanding performance in a challenging

financial market and a demanding line of

insurance

financial market and a demanding line of

insurance

5

|

Book Value Growth

EVERY

Year Since Inception |

||

|

|

Cumulative

|

CAGR

|

|

10 year

|

278%

|

14%

|

|

5 year

|

151%

|

20%

|

|

1 year

|

23%

|

23%

|

|

Measured through Year-End 2009

|

||

6

Book Value per Share at Year End

|

Share Prices Since Inception

|

||

|

|

Cumulative

|

CAGR

|

|

10 year

|

166%

|

10%

|

|

5 year

|

37%

|

7%

|

|

1 year

|

2%

|

2%

|

|

Measured through Year-End 2009

|

||

7

Share Price at Year End

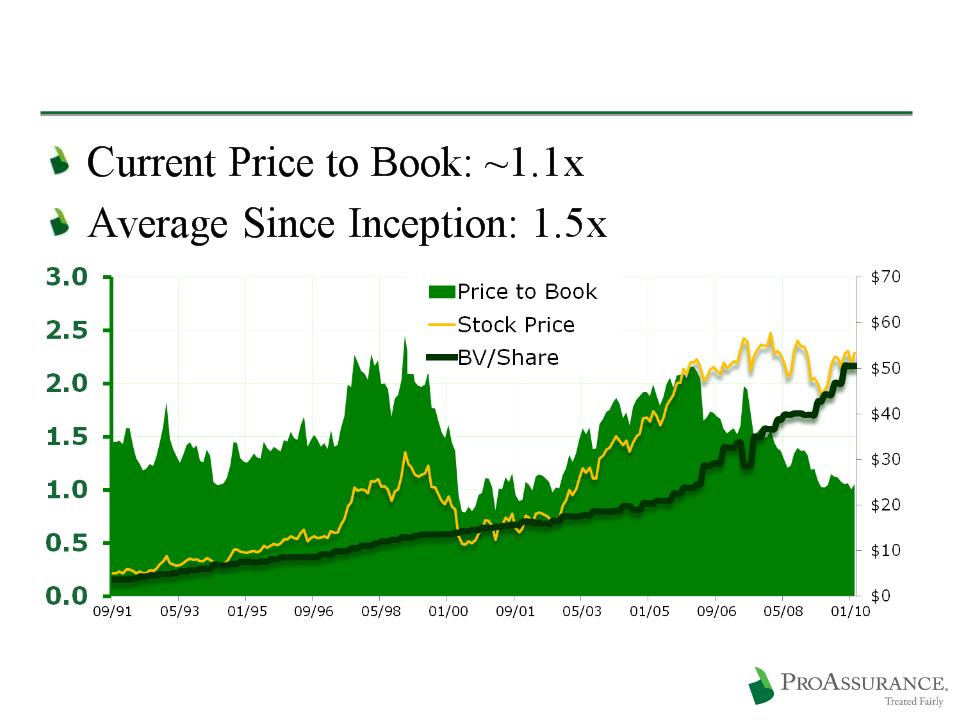

Prime Time to Invest in PRA

8

Price to Book Multiple by Month

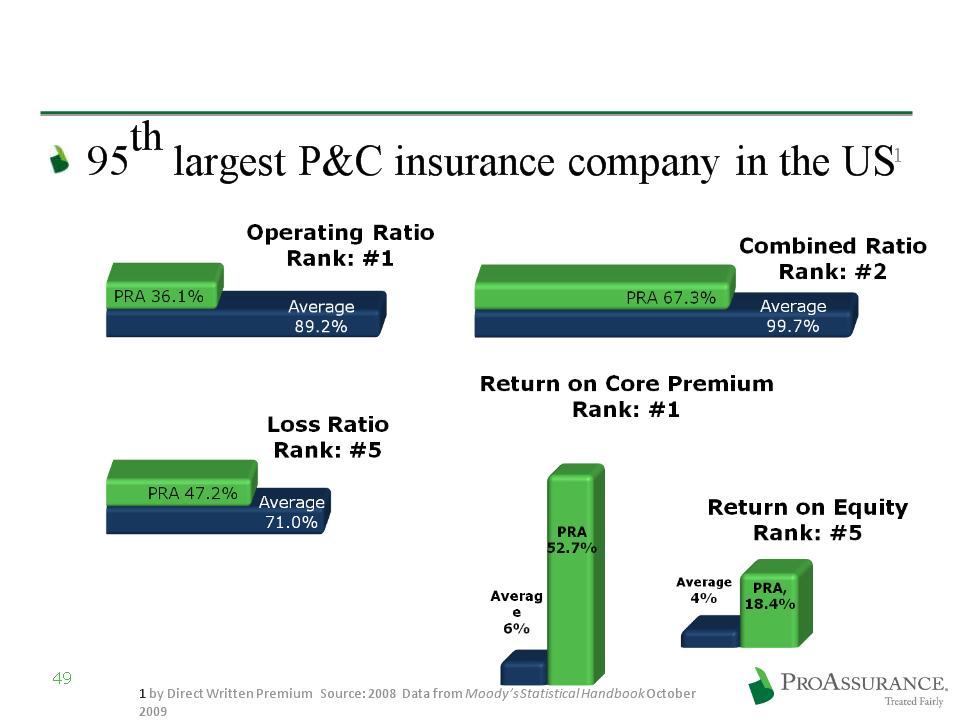

Outstanding Performance vs Industry

Moody’s rankings of the top 100 P&C

insurance companies by premium volume

insurance companies by premium volume

9

1 by Direct Written Premium Source: 2008 Data from Moody’s Statistical Handbook October

2009

2009

|

Category

|

Ranking

|

|

Direct Written Premiums

|

95

|

|

Operating Ratio

|

1

|

|

Combined Ratio

|

2

|

|

Loss Ratio

|

5

|

|

ROE

|

5

|

2009 Financial Highlights

10

in millions, except per share data

Year-End

All data includes acquired entities since date of acquisition only. PICA was acquired on April 1, 2009.

1Excludes discontinued operations.

2Includes a loss on extinguishment of debt of $2.8 million for the year ended December 31, 2009 and a gain on

extinguishment of debt of $4.6 million for the year ended December 31, 2008

extinguishment of debt of $4.6 million for the year ended December 31, 2008

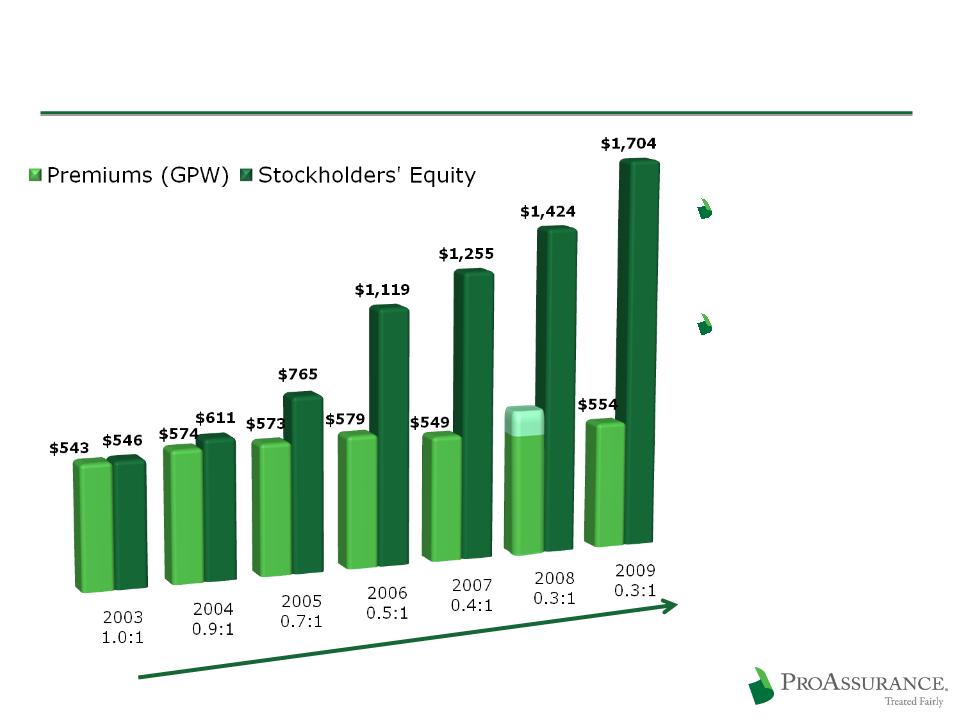

Gross Premiums Written1 $ 554 $ 471 $ 549

Net Investment Income1 151 158 171

Total Revenue1 673 567 706

Net Income (Includes Investment Losses)2 $ 222 $ 178 $ 168

Operating Income $ 215 $ 207 $ 172

Net Income/Diluted Share $ 6.70 $ 5.22 $4.78

Operating Income/Diluted Share $ 6.49 $ 6.07 $4.90

Total Assets $4,647 $ 4,281 $ 4,441

Shareowners’ Equity $1,705 $ 1,424 $ 1,255

2009 2008 2007

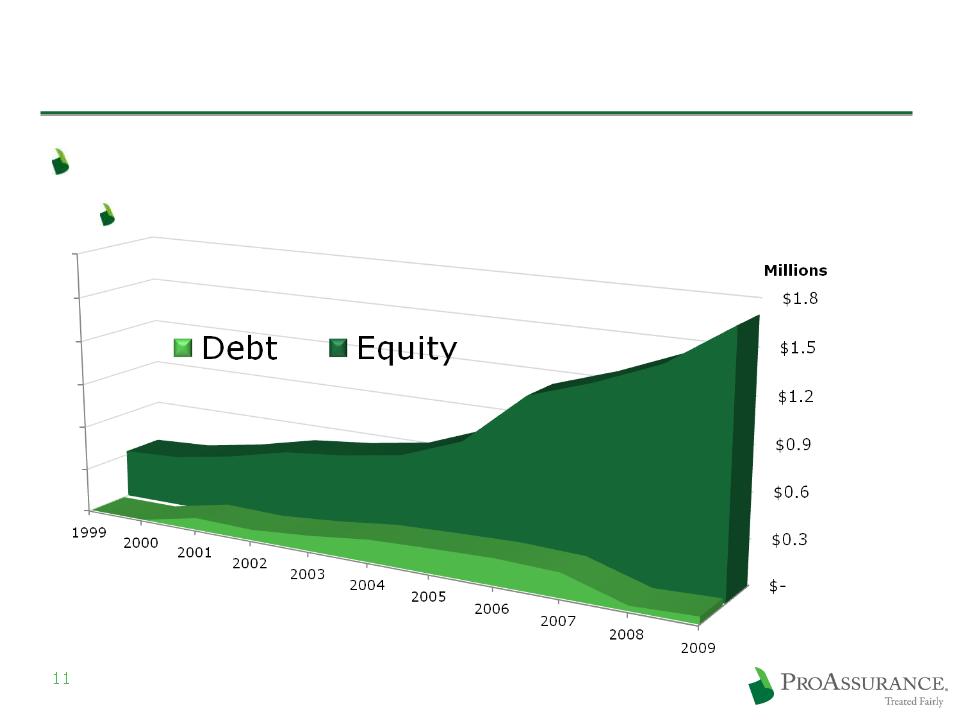

Conservative Use of Debt

Low Debt to Cap Ratio

No strain on cash flow

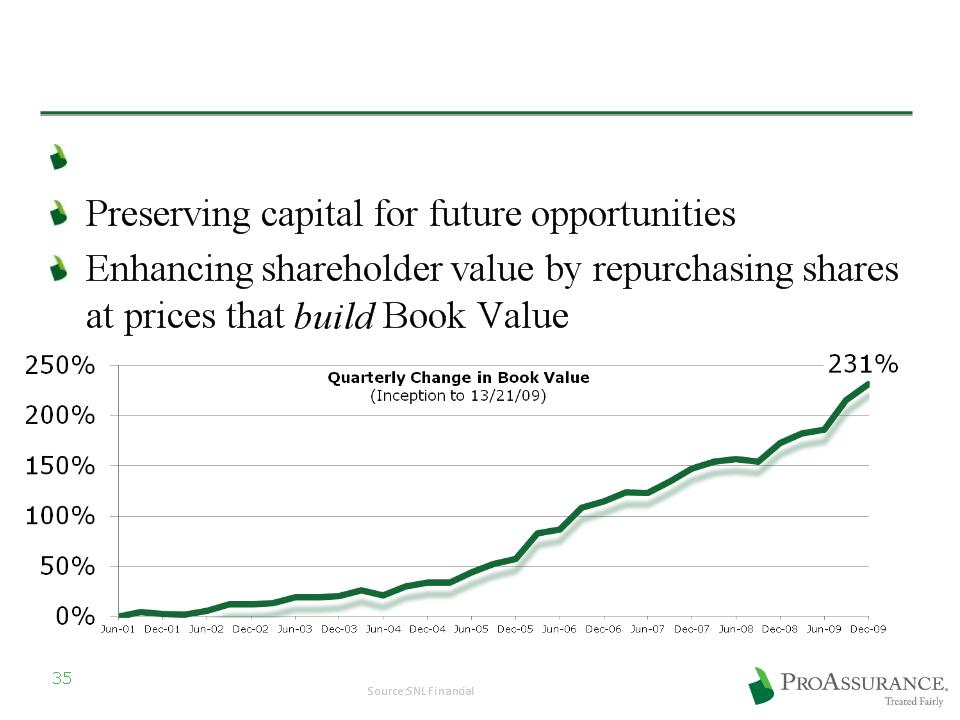

Capital Management

Active in prudent share repurchase

1.1 million shares in 2009

Board examination of capital management

alternatives

alternatives

12

Investments Balance Risk vs. Return

Key Investment Actions in Q4 09

Reduced cash and short-term

balances

balances

Added to corporate and municipal

bond holdings

bond holdings

CUSIP-level portfolio disclosure

on our website:

www.proassurance.com/investorrelations/supplemental.aspx

on our website:

www.proassurance.com/investorrelations/supplemental.aspx

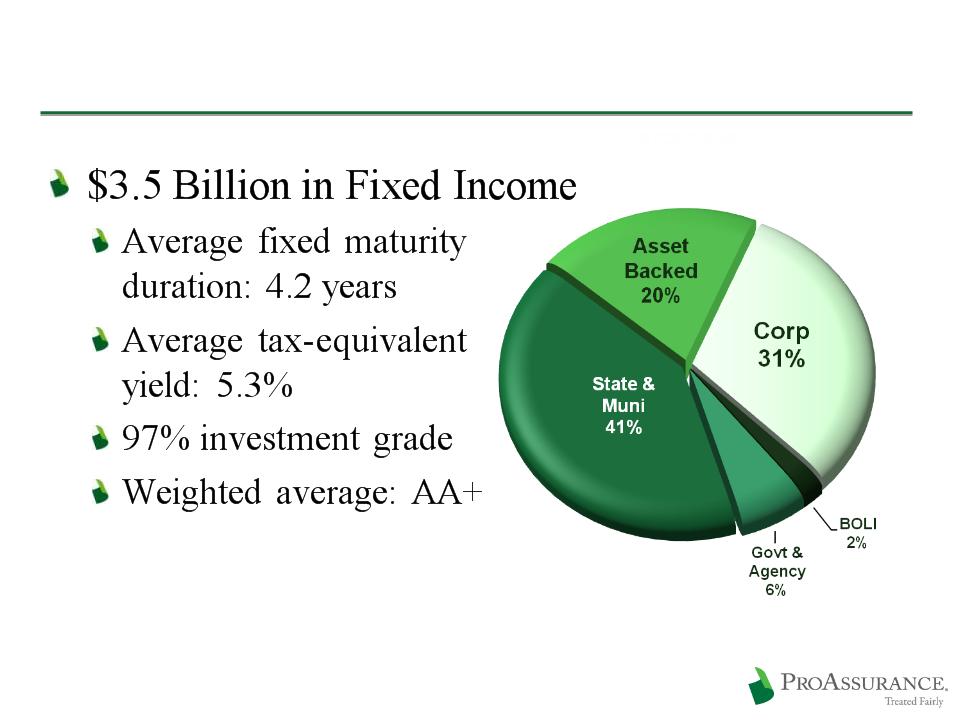

$3.8 Billion

Portfolio

Portfolio

$3.8 Billion

Portfolio

Portfolio

Fixed Income: 90%

Short Term: 5%

Short Term: 5%

Equity and Other Investments: 3%

Equity and Other Investments: 3%

BOLI: 2%

BOLI: 2%

13

12/31/09

Fixed Income Breakdown

14

12/31/09

Our Disciplined Approach Produces

Operational Excellence

Our Disciplined Approach Produces

Operational Excellence

W. Stancil Starnes, Esq.

Chairman & CEO

Producing Sustainable Results

Building on growth opportunities

Using our unparalleled market knowledge

Leveraging our unique claims expertise

Employing our not so secret weapon

16

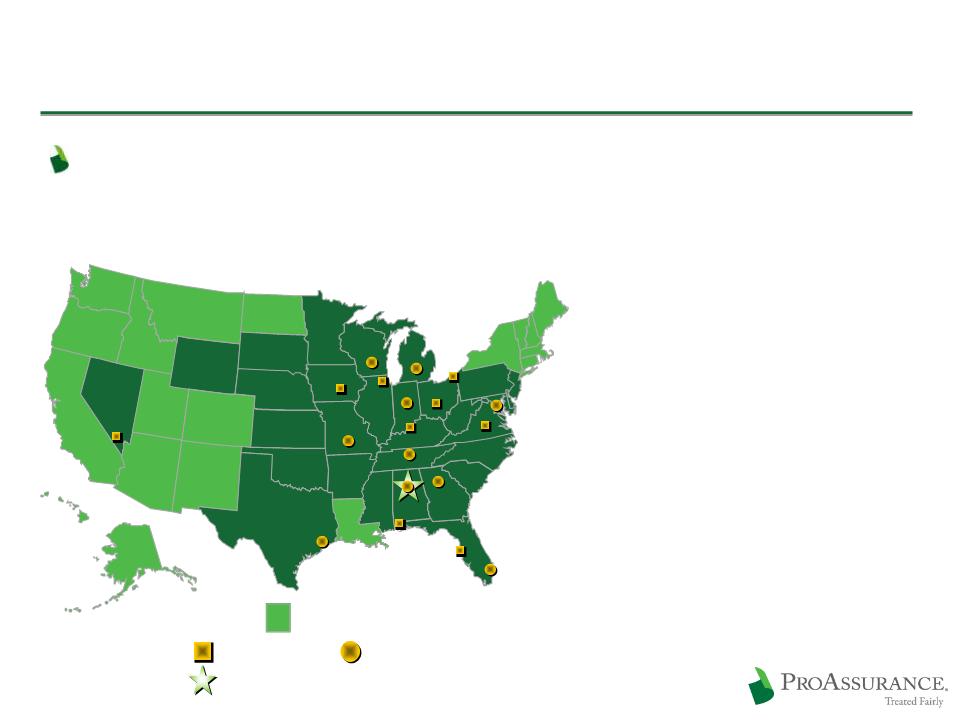

We Are a National Company

Broad geographic diversification provides an

unmatched spread of risk

unmatched spread of risk

17

Corporate Headquarters

Corporate Headquarters

Claims Offices

Claims Offices

Claims / Underwriting Offices

Claims / Underwriting Offices

PICA and/or E&S States

PICA and/or E&S States

(Birmingham)

2009 M & A Transactions

18

2009 Premium: $77 million

Significant growth in our core business

Nationwide geographical expansion

Extends our core business

Broadens our medically-related range

Geographical expansion

Broadens our medically-related range

Geographical expansion

2009 Premium: $4.0 million

Adds to our lawyers’ book

Geographical expansion

Affirms our interest in this line

2009: Consolidation of:

Mid-Continent General Agency

Mid-Continent General Agency

2009: Consolidation of:

Mid-Continent General Agency

Mid-Continent General Agency

Georgia Lawyers Insurance Co.

Georgia Lawyers Insurance Co.

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

OHIC Insurance Company

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

OHIC Insurance Company

Growth Through M&A

We’ve built a leading platform through M&A

19

1994: Consolidation of:

West Virginia Hosp. Ins Co.

West Virginia Hosp. Ins Co.

1994: Consolidation of:

West Virginia Hosp. Ins Co.

West Virginia Hosp. Ins Co.

1995: Consolidation of;

1995: Consolidation of;

Physicians Ins Co of Indiana

Physicians Ins Co of Indiana

Assumed business of:

Physicians Ins Co of Ohio

Physicians Ins Co of Ohio

Assumed business of:

Physicians Ins Co of Ohio

Physicians Ins Co of Ohio

1996: Consolidation of:

1996: Consolidation of:

Missouri Medical Ins Co

Missouri Medical Ins Co

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

Associated Physicians Ins Co. (IL)

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

Associated Physicians Ins Co. (IL)

1998: Consolidation of:

Physicians Protective Trust Fund (FL)

Physicians Protective Trust Fund (FL)

1998: Consolidation of:

Physicians Protective Trust Fund (FL)

Physicians Protective Trust Fund (FL)

1996: Assumed business of:

American Medical Ins Exchange (IN)

American Medical Ins Exchange (IN)

1996: Assumed business of:

American Medical Ins Exchange (IN)

American Medical Ins Exchange (IN)

Founding in the 1970’s

Founding in the 1970’s

1999: Assumed business of:

Medical Defense Associates (MO)

Medical Defense Associates (MO)

1999: Assumed business of:

Medical Defense Associates (MO)

Medical Defense Associates (MO)

Mutual Assurance

Physicians Ins. Co. of Michigan

Professionals Group

Creation of:

Creation of:

2005: Consolidation of:

NCRIC Group

NCRIC Group

2005: Consolidation of:

NCRIC Group

NCRIC Group

2006: Consolidation of:

PIC Wisconsin Group

PIC Wisconsin Group

2006: Consolidation of:

PIC Wisconsin Group

PIC Wisconsin Group

2007: PRI renewal rights deal

2002: SERTA renewal rights deal

2001: OUM renewal rights deal

2000: DPM Merger

1999: PACO Acquisition

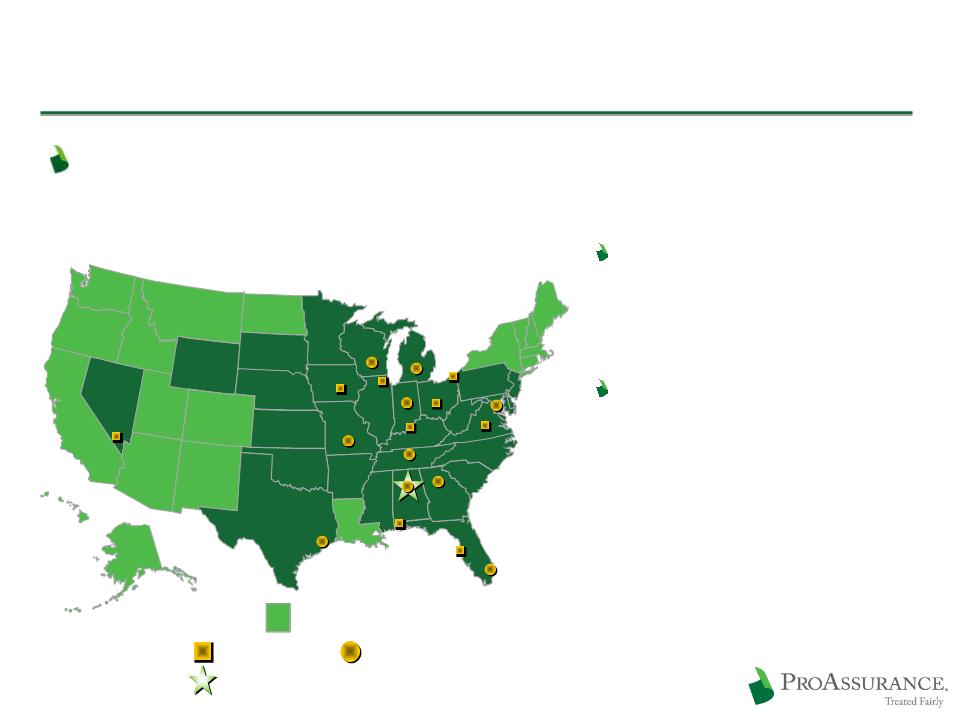

Growth Brings Size and Scope

Broad geographic diversification provides an

unmatched spread of risk

unmatched spread of risk

20

Our spread of risk provides

better market awareness and

more data points to gauge

loss trends

better market awareness and

more data points to gauge

loss trends

Our internal actuarial depth

allows us to assess emerging

trends and respond quickly

allows us to assess emerging

trends and respond quickly

Corporate Headquarters

Corporate Headquarters

Claims Offices

Claims Offices

Claims / Underwriting Offices

Claims / Underwriting Offices

PICA and/or E&S States

PICA and/or E&S States

(Birmingham)

Claims Handling Sets Us Apart

Our effective approach to handling claims sets

us apart

us apart

We price our product to offered an unfettered

defense of claims to the extent permitted by

law

defense of claims to the extent permitted by

law

Claims handling is a key to policyholder

loyalty and long-term financial success

loyalty and long-term financial success

21

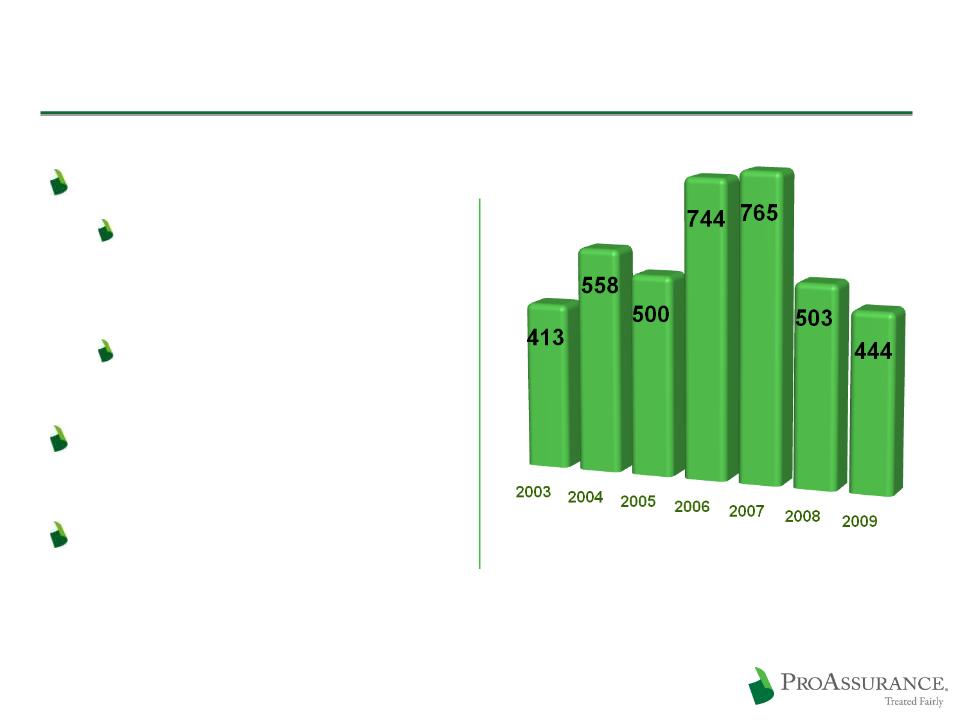

Claims Trends Remain Favorable

22

ProAssurance Claims Tried

to a Verdict

(includes PICA)

to a Verdict

(includes PICA)

We try cases

Frequency trends are

stable after declining

since 2005/2006

stable after declining

since 2005/2006

The result is fewer

cases to try

cases to try

Severity trends also

stable

stable

Trends are much the

same in states with or

without Tort Reform

same in states with or

without Tort Reform

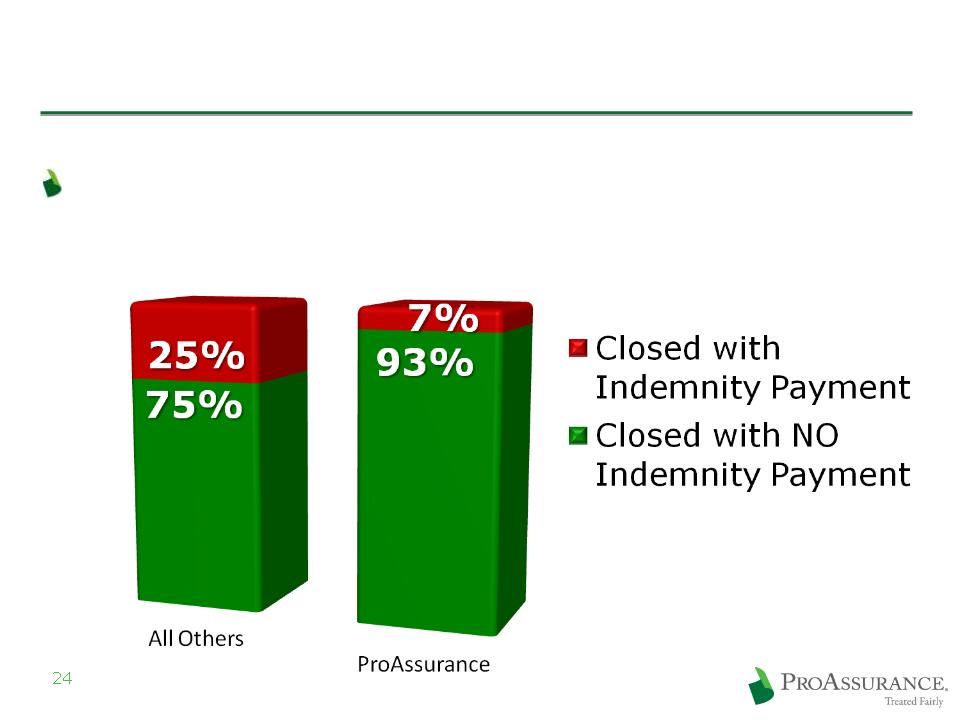

The Ohio Example

Exhaustive, reliable data provided by the Ohio

Department of Insurance

Department of Insurance

Broad range of competitors and business

approaches

approaches

Pricing

Underwriting

Claims handling

23

www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

ProAssurance closes more claims

with NO indemnity payments

with NO indemnity payments

Ohio Closed Claims 2005-2008

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

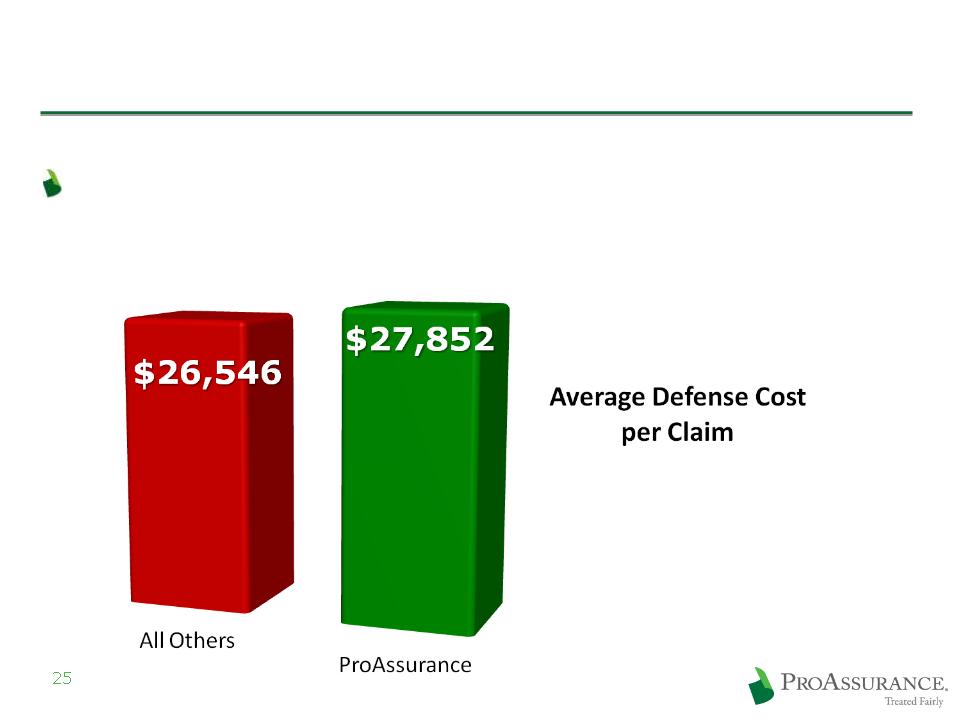

ProAssurance spends more, on average, to

defend cases—leveraging our strength

defend cases—leveraging our strength

Ohio Closed Claims 2005-2008

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

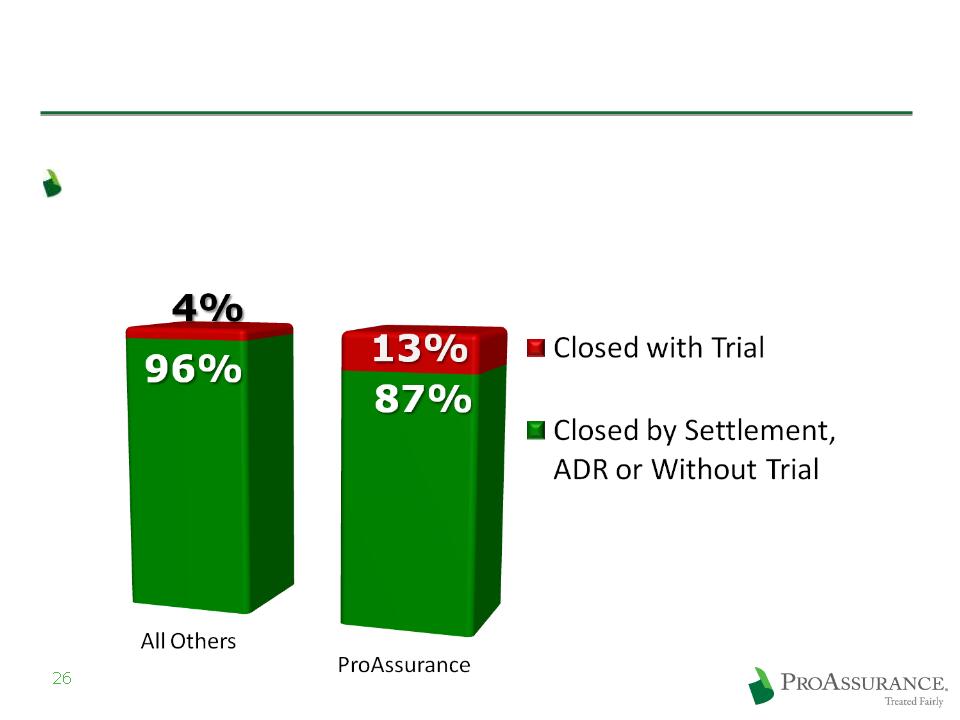

ProAssurance closes more claims at trial,

offering our insureds the chance for vindication

offering our insureds the chance for vindication

Ohio Closed Claims 2005-2008

Excludes Trials that Ended with a Directed Verdicts

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

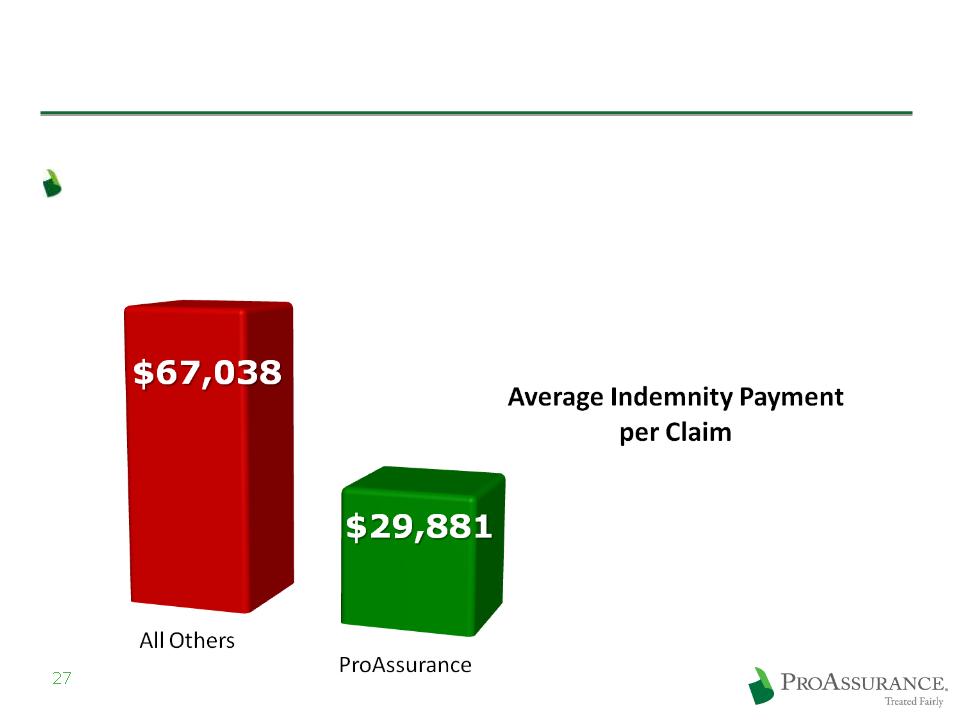

ProAssurance spends far less in average

indemnity payments

indemnity payments

Ohio Closed Claims 2005-2008

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

The Importance of Treated Fairly®

Treated Fairly® affirms our existing, enduring

commitment to every stakeholder

commitment to every stakeholder

Insureds

Agents

Investors

The public

Provides a touchstone that guides every interaction

Helps ensure that we run our business as owners

who are rewarded for long-term success

who are rewarded for long-term success

28

Producing Sustainable Results

Building on growth opportunities

Using our unparalleled market knowledge

Leveraging our unique claims expertise

Employing our not so secret weapon

29

SUPPLEMENTAL

DISCUSSION

SLIDES

DISCUSSION

SLIDES

SUPPLEMENTAL

DISCUSSION

SLIDES

DISCUSSION

SLIDES

Financial

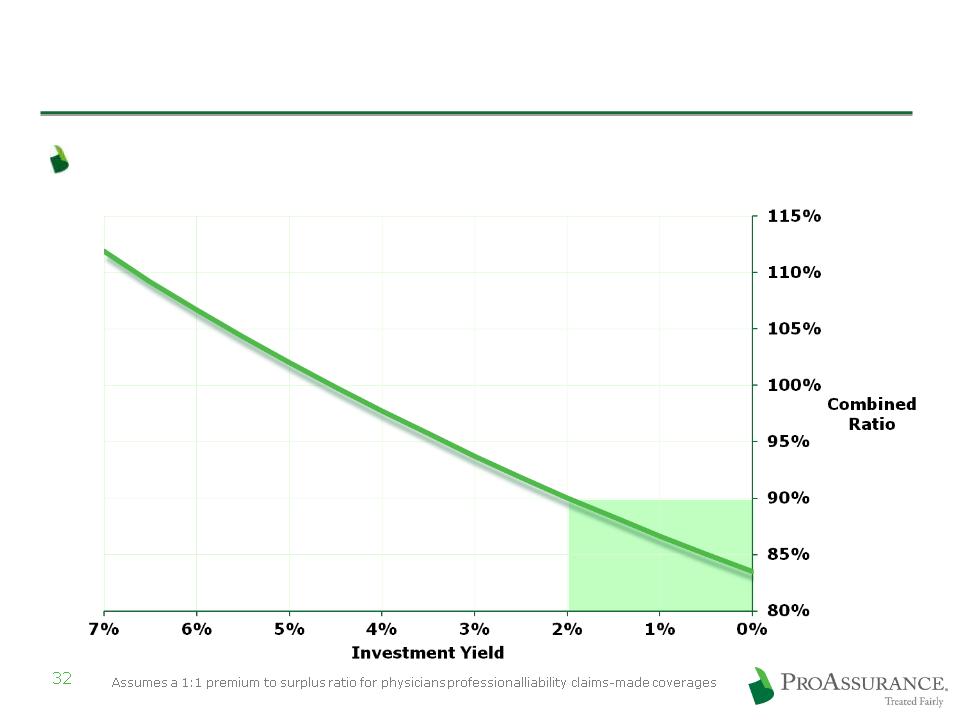

The Importance of Investment Income

Pricing discipline is even more critical

Combined Ratio

required to generate

a 13% after-tax ROE

required to generate

a 13% after-tax ROE

The Importance of Investment Income

33

Year

1

1

Year

2

2

Year

3

3

Year

4

4

Year

5

5

Year

6

6

Year

7

7

Year

8

8

Incident

Occurs

Occurs

Discovery

and

Preparation

and

Preparation

Claim

Reported

Reported

Trial

and

Appeals

Appeals

Resolution

5-6 Years

After

Claim

Reported

After

Claim

Reported

Life Cycle of a Typical Claim

The Importance of Investment Income

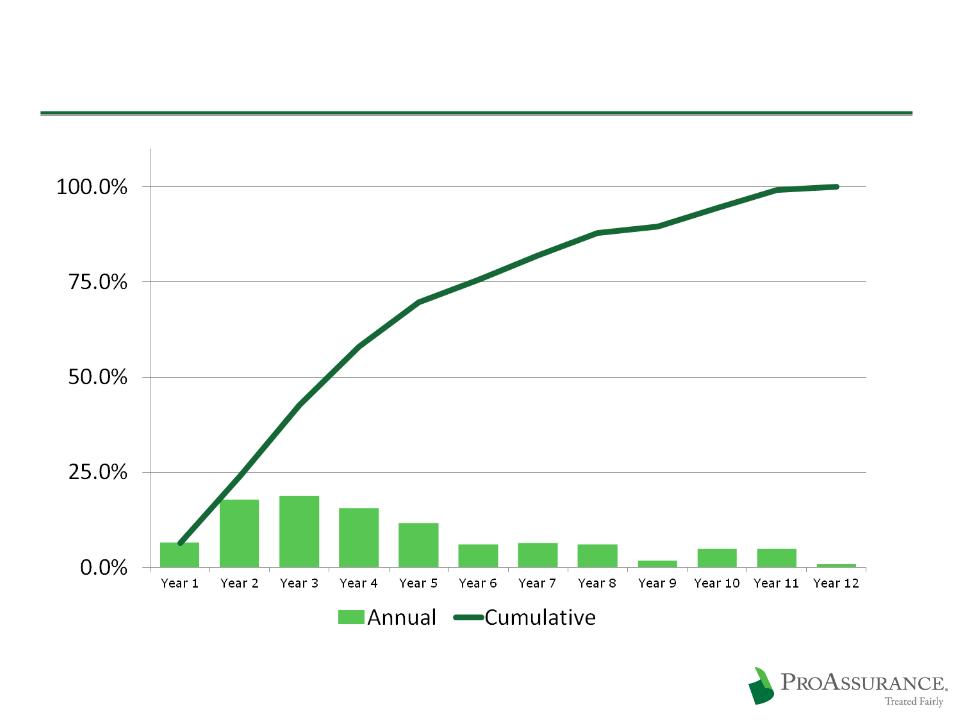

34

Typical Claims Payout Pattern

Using Capital Prudently

Using capital to build through M&A

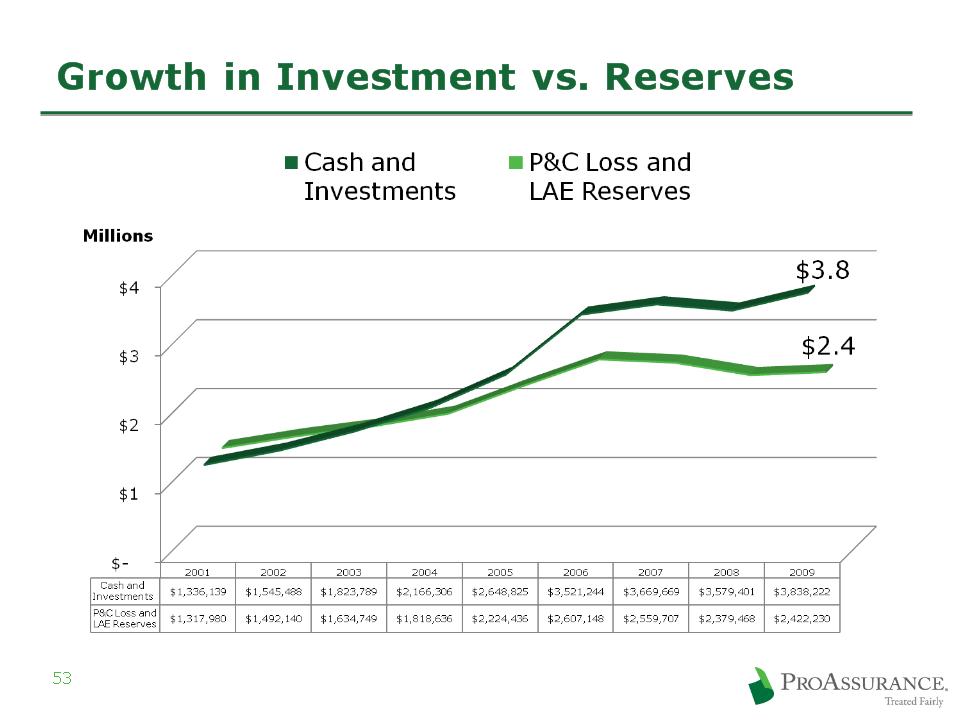

Our Strong Capital/Low Leverage Position

36

(in millions)

Prepared for an

improving market

improving market

Prudent capital

management

management

Premiums to Surplus

for Each year

for Each year

$567

$ 96

$471

($96 mil PICA pro forma in 2008)

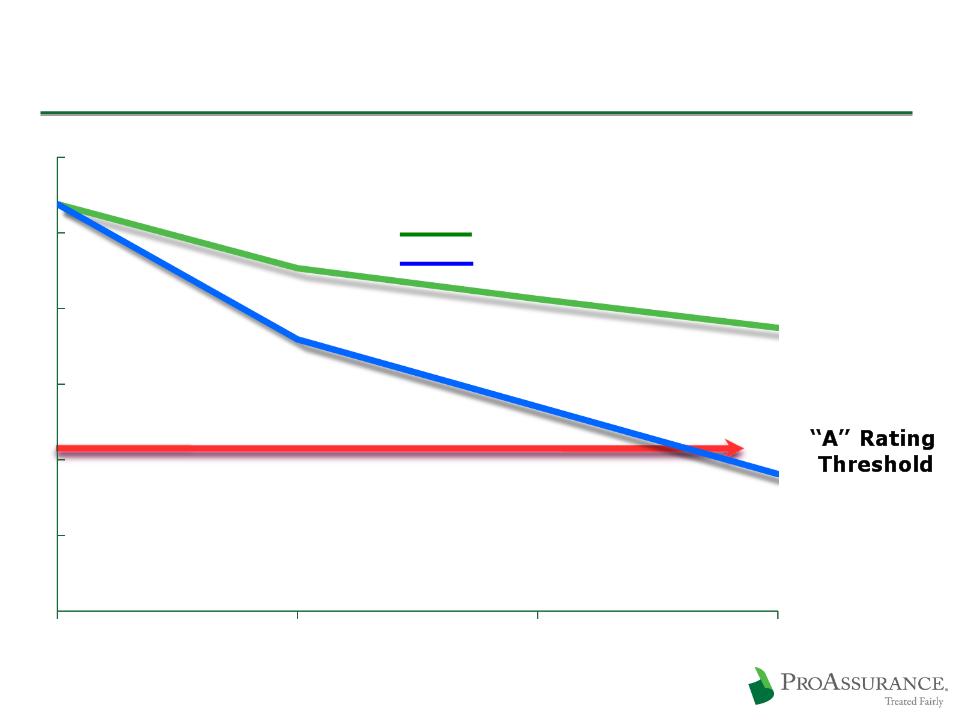

Excess Capital vs. Excess Capacity

37

Conceptual Model of Projected

A. M. Best BCAR Scores if

A. M. Best BCAR Scores if

Premiums Increase

Surplus is Reduced

Market Conditions

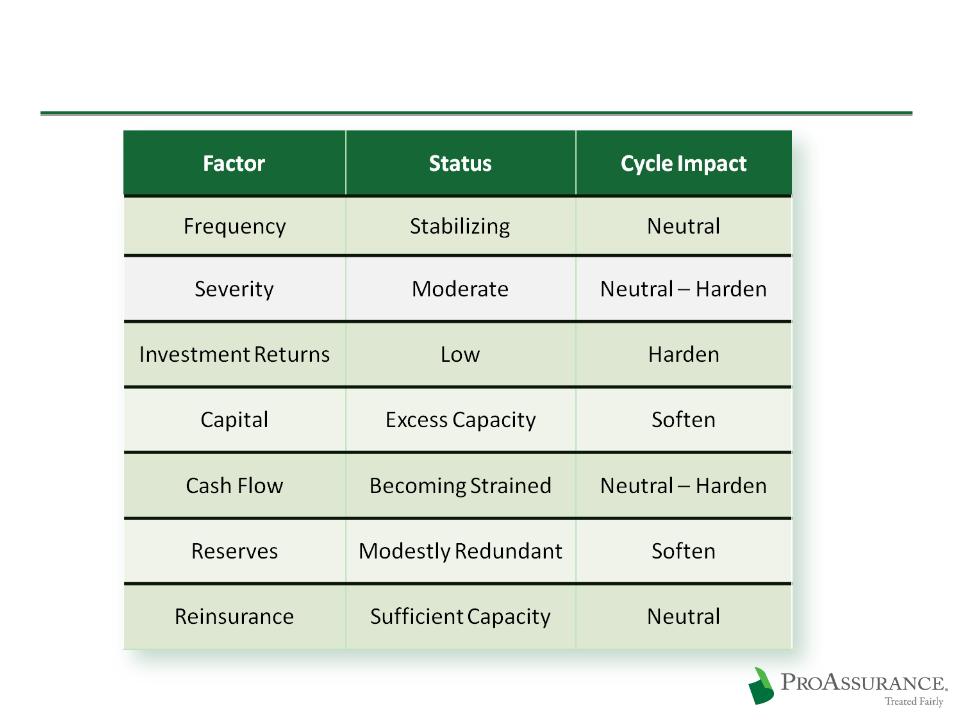

The State of the Market

Prices have been falling yet profitability

remains high

remains high

Continued low interest rates must enforce

discipline sooner or later

discipline sooner or later

Frequency is no longer declining

Only a matter of time before frequency moves

higher

higher

But when?

Severity is trending upward at expected,

manageable rates (4%-5%) in most states

manageable rates (4%-5%) in most states

39

The State of the Market

40

Responding to Changes in HealthCare

Projected sector growth through 20181

Physician’s Assistants 39%

Medical Assistants 36%

Licensed Nurses 34%

Chiropractors 31%

Physicians and Surgeons 22%

Podiatrists 9%

41

1Bureau of Labor Statistics 2008 to 2018 Projections

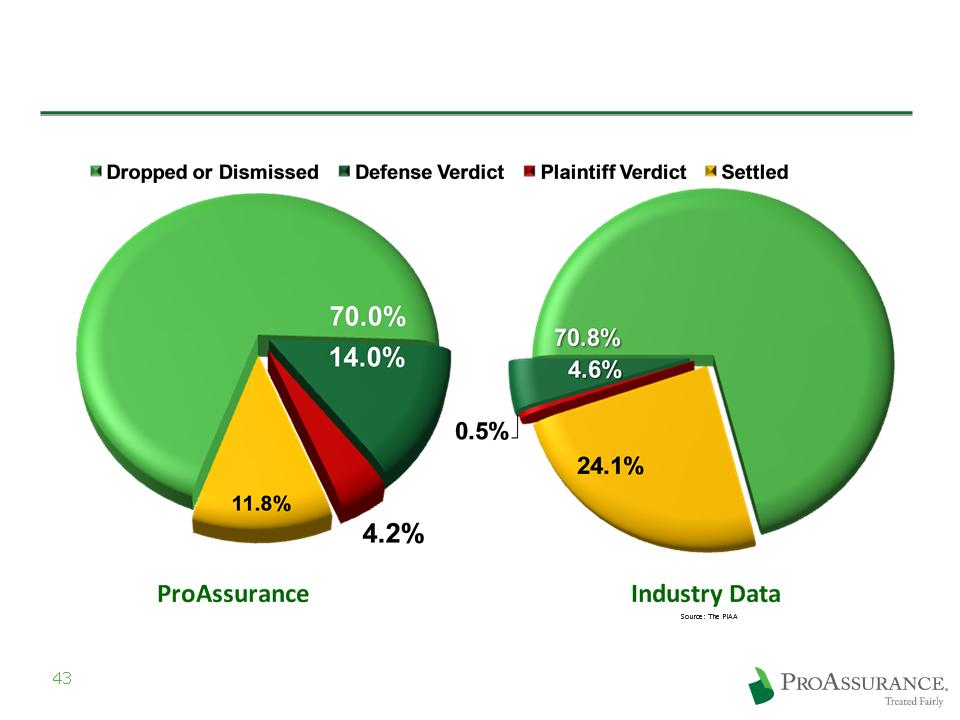

Claims

Why Claims Strategy Matters

Favorable

Outcomes:

84.0%

Outcomes:

84.0%

Favorable

Outcomes:

84.0%

Outcomes:

84.0%

Five Year Average

2004 - 2008

2004 - 2008

Favorable

Outcomes:

75.4%

Outcomes:

75.4%

Favorable

Outcomes:

75.4%

Outcomes:

75.4%

Why Claims Strategy Matters

Our ability and willingness to defend claims

allows us to achieve better results

allows us to achieve better results

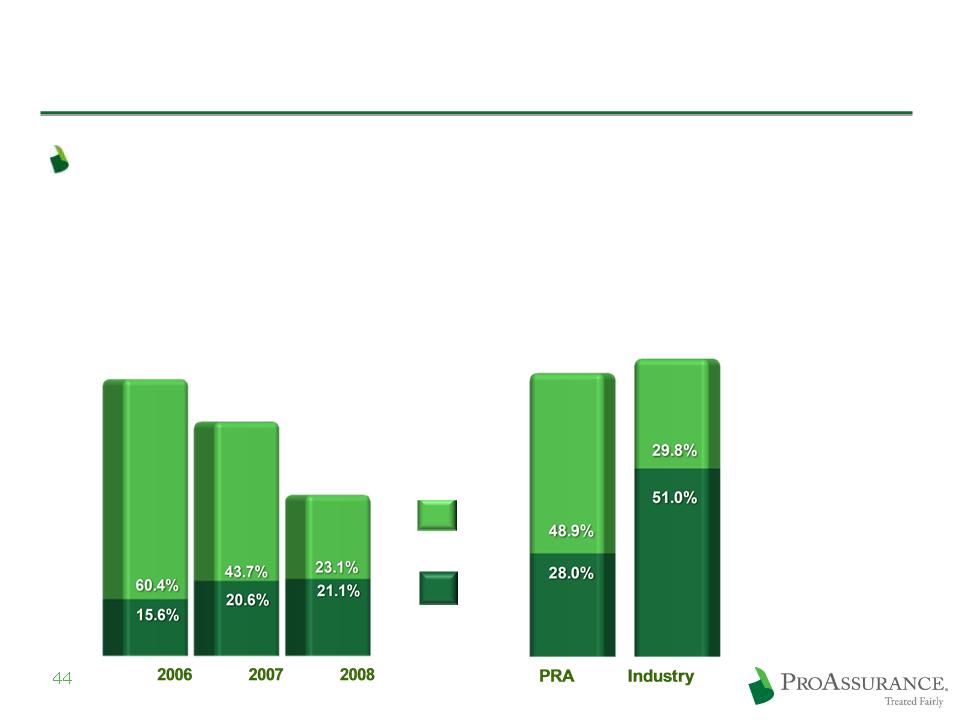

ProAssurance vs. Industry

Average Statutory Loss Ratio

Average Statutory Loss Ratio

2003-2008

Legal

Payments

Payments

Loss

Payments

Payments

Trend for ProAssurance

Stand Alone Statutory Loss Ratio

Stand Alone Statutory Loss Ratio

2006 - 2008

76.0%

*Source: A. M. Best Aggregates & Averages, Medical Malpractice Predominating

64.3%

80.8%

76.9%

44.2%

Appendix: Underwriting/Actuarial

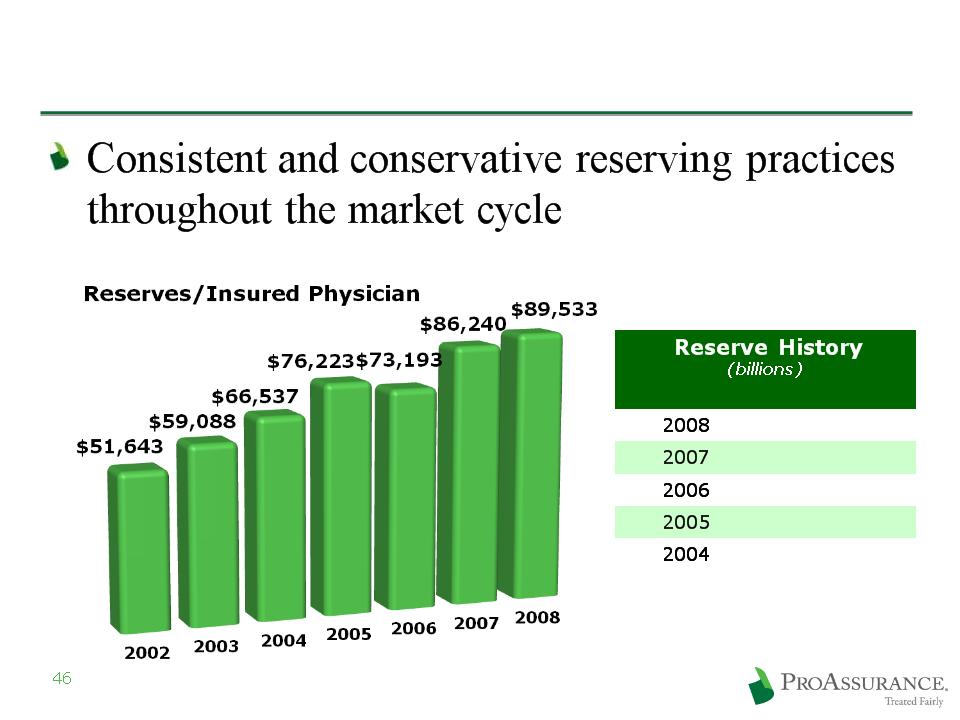

Enforce Actuarial Conservatism

|

$ 2.4

|

|

|

$ 2.6

|

|

|

$ 2.6

|

|

|

$ 2.2

|

|

|

$ 1.8

|

|

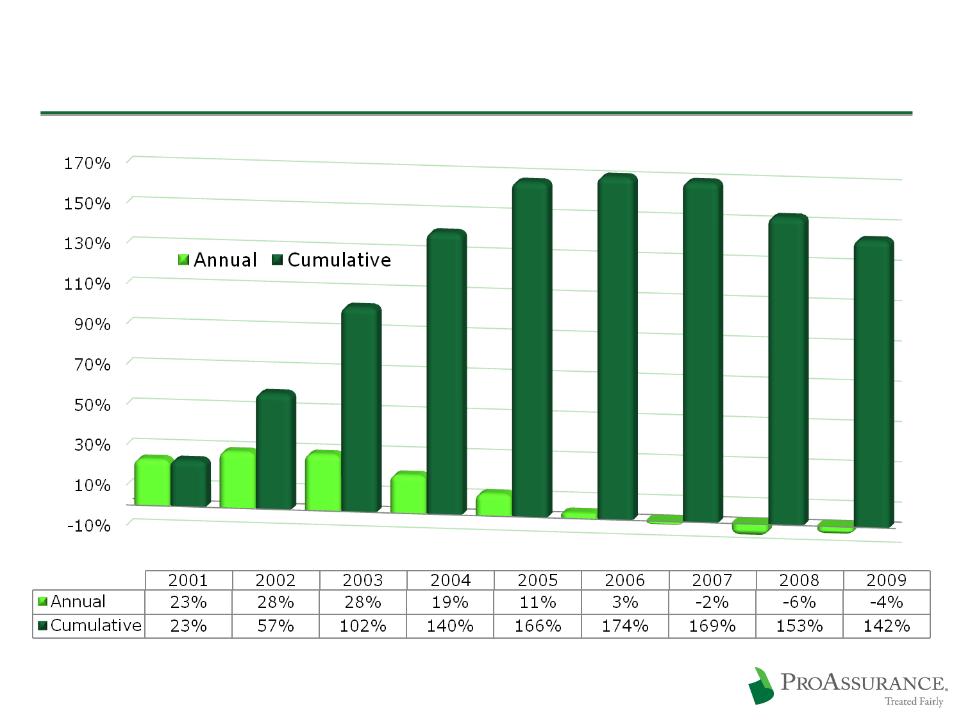

Rate Change History

47

Appendix: Moody’s Rankings

Moody’s Top 100 Ranking Data

Appendix: Investments

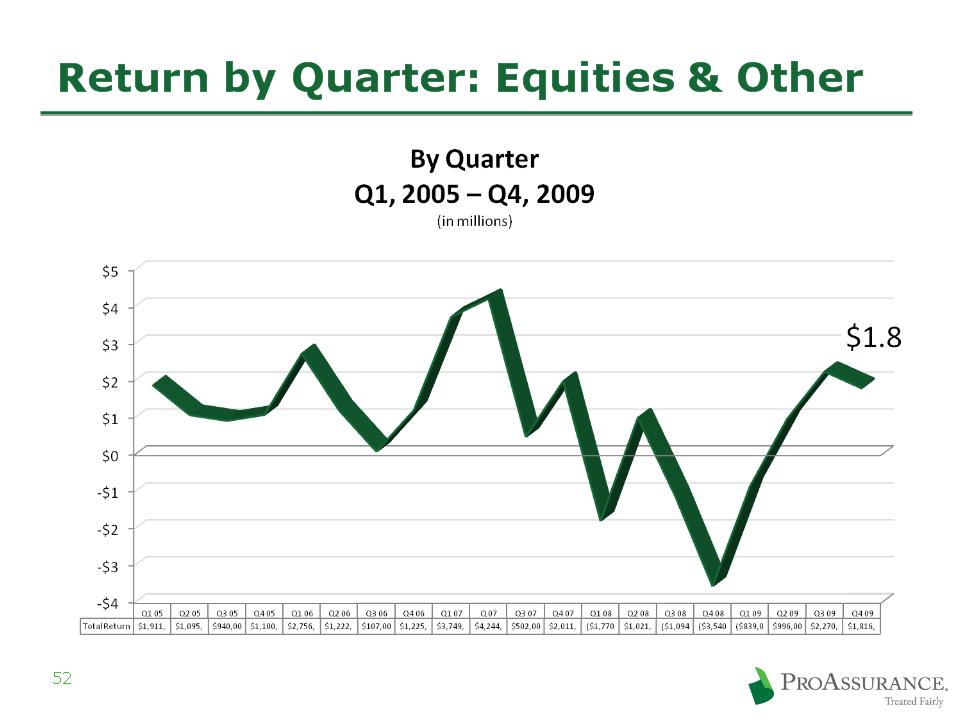

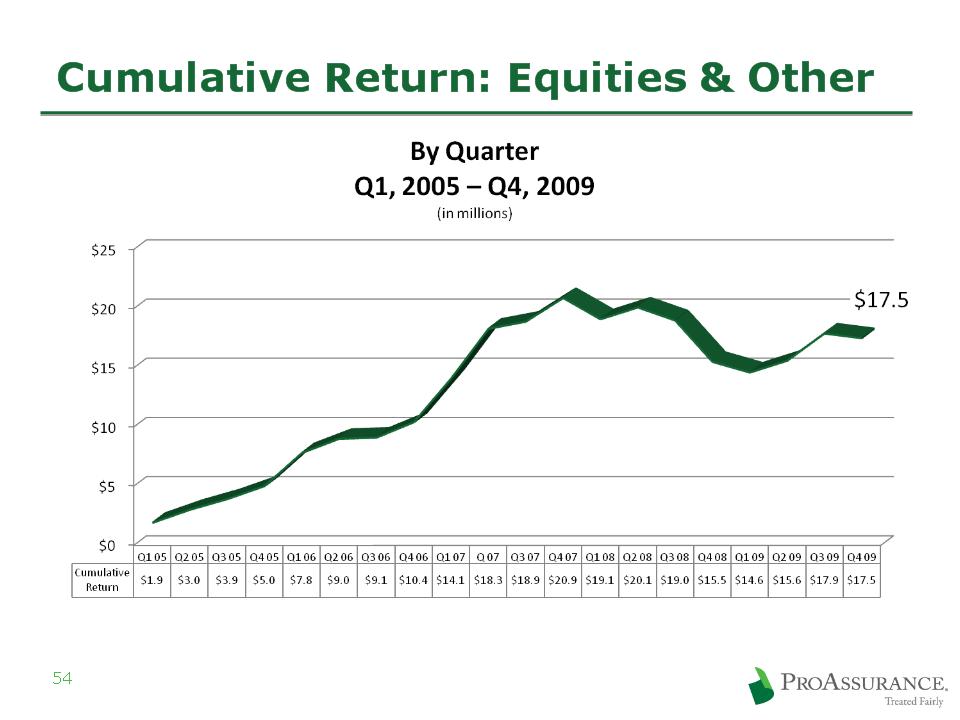

Equities & Other: $43 Million

51

12/31/09

Represents 3% of our Total Investments

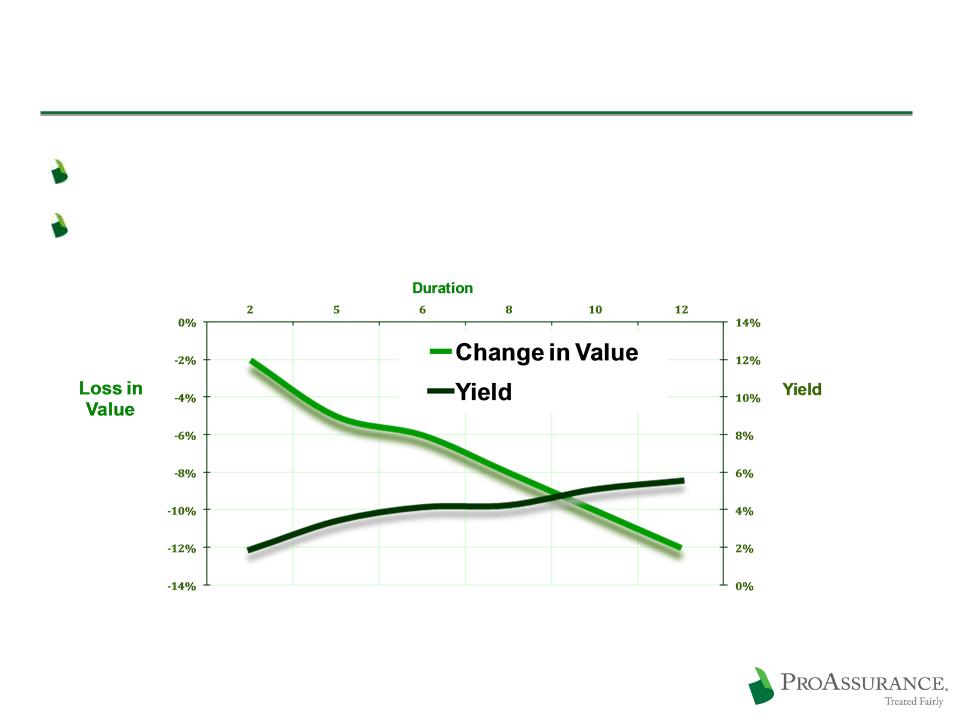

Strategy: Investment Discipline

The choice: Chase yield or extend duration

We are maintaining duration, looking for opportunities

55

Loss in value assuming a 100 basis point shift in the yield curve

Yields based on Single A composite corporate debt

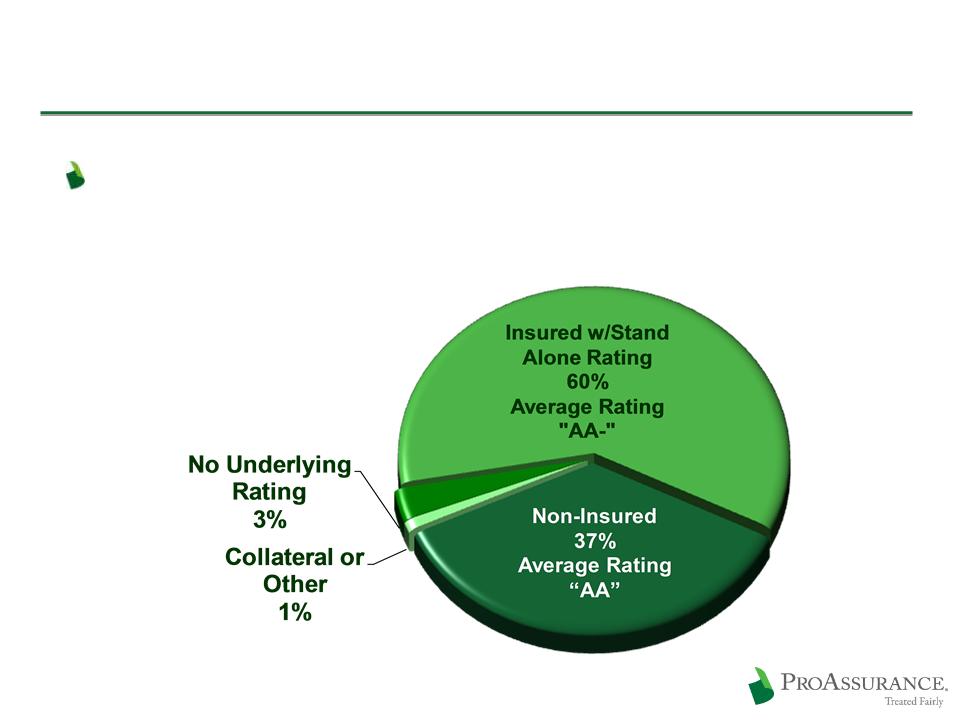

Municipals: $1.5 Billion

56

12/31/09

Investment policy has always required

investment grade rating prior to applying the

effect of insurance

investment grade rating prior to applying the

effect of insurance

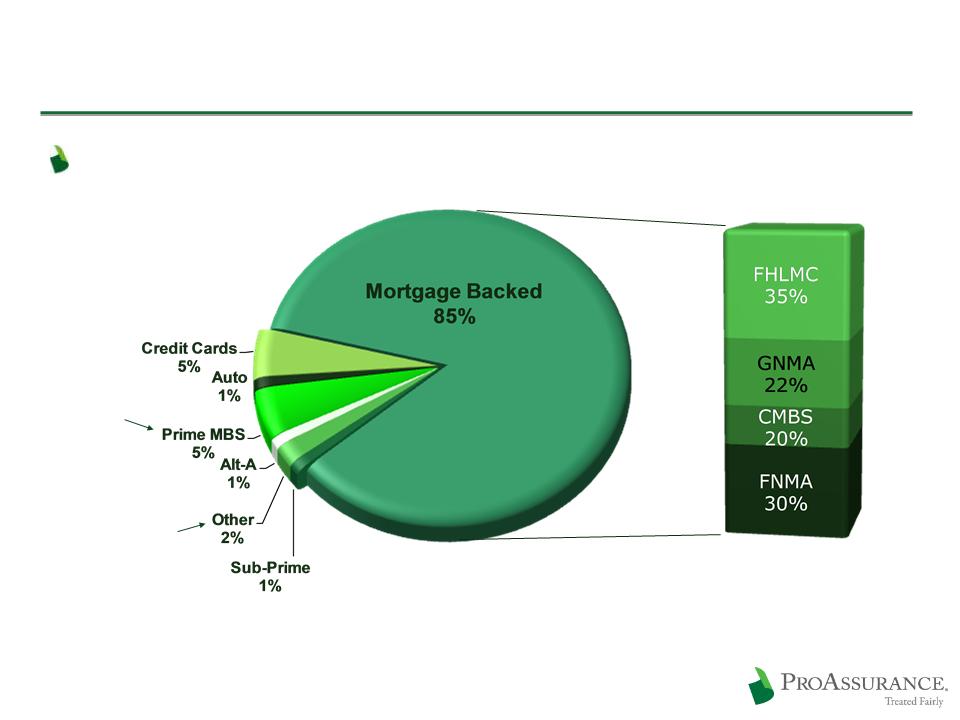

Asset Backed: $700 Million

Weighted average rating: “AA+”

Bloomberg Data

12/31/09

12/31/09

Alt-A

LTV 61%

LTV 61%

Prime MBS

LTV 57%

LTV 57%

Further Details Provided

on Sub-Prime and CMBS

on following pages

on Sub-Prime and CMBS

on following pages

57

Sub-Prime Detail

58

$7.2 million market value in AFS portfolio

$3.5 million unrealized loss

$13.3 million market value in

high-yield LP rated “A”

high-yield LP rated “A”

LP’s focus is distressed ABS

|

At 12/31/09

|

Vintage

|

|

$4.7 Mln

|

2004 & Prior

|

|

$2.5 Mln

|

2005

|

Quality & Vintage information only on direct holdings at 12/31/09

|

At 12/31/09

|

Type

|

Quality

|

|

$3.4 Mln

|

Mortgage-Backed

|

AA- avg - LTV 71%

|

|

$3.8 Mln

|

Home Equity

|

A+ avg

|

CMBS Detail

Vintages

2005 & Prior- $71 million

2006- $21 million

Top Property Types

Office: 56% of CMBS portfolio

Retail Anchored: 34% of CMBS portfolio

Mixed Use: 6% of CMBS portfolio

Other: 4% of CMBS Portfolio

59

CMBS Detail

$93 million Fair Value in non-agency CMBS

Book Value: $94 million

3% of fixed income portfolio

60

|

At 12/31/2009

|

Quality

|

|

$89.3 Mln

|

AAA

|

|

$ 3.0 Mln

|

AA

|

|

$ 0.7 Mln

|

A

|

|

At 12/31/2009

|

Wtd Avg LTV

|

|

16%

|

<65%

|

|

48%

|

=65-70%

|

|

19%

|

<70-75%

|

|

16%

|

=75-85%

|

|

1%

|

+85%

|

|

At 12/31/2009

|

Credit Support

|

|

39%

|

>30%

|

|

46%

|

20% - 30%

|

|

11%

|

10% - 20%

|

|

4%

|

Less than 10%

|

|

At 12/31/2009

|

Deal Cumulative Delinquencies

|

|

30%

|

0.0% - 1.0%

|

|

15%

|

1.0% - 2.0%

|

|

19%

|

2.0% - 3.0%

|

|

10%

|

3.0% - 5.0%

|

|

21%

|

5.0% - 8.0%

|

|

5%

|

8.0% - 10.0%

|

|

At

12/31/2009 |

Debt Service Coverage

|

|

87%

|

=>1.5x

|

|

7%

|

1.4x-1.5x

|

|

6%

|

1.3x-1.4x

|

AT

12/31/2009

12/31/2009

Weighted Average Rating: A

28% of Total Investments

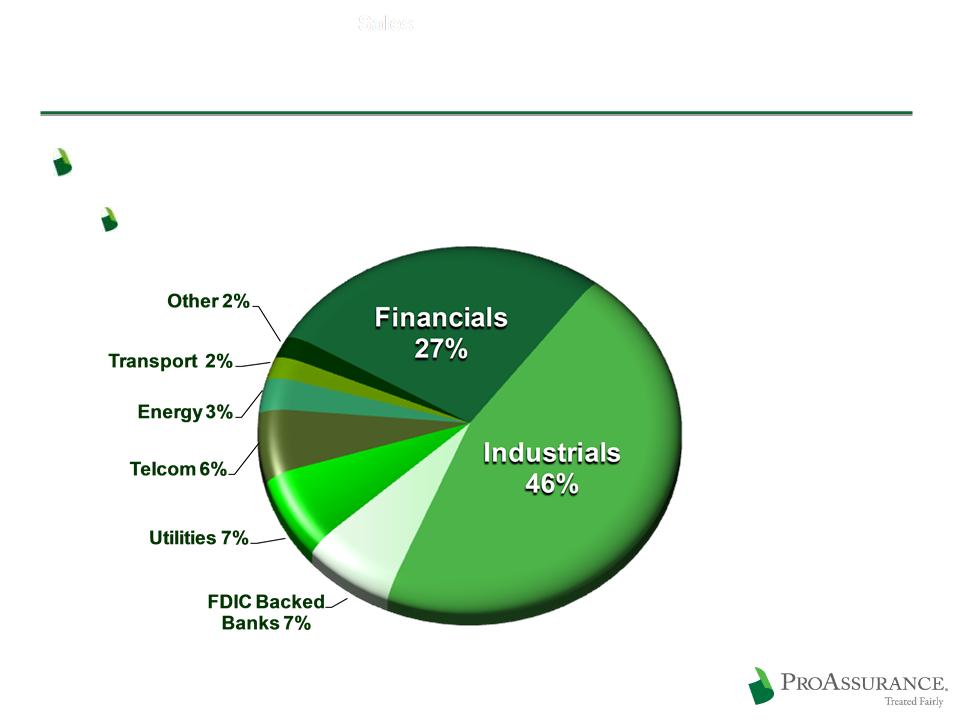

Corporates: $1.1 Billion

61

12/31/2009

Corporate: Detail on Financials

Top 20 Largest Banks/Financials: $ 267 million

$68 mm FDIC backing

|

BA $41 ($23)

|

Credit Suisse $9

|

|

MS $29 ($6)

|

Eurohypo $8

|

|

BP Cap $25

|

KEY $6 ($6)

|

|

GECC $25 ($8)

|

BNY Mellon $6

|

|

JPM $23 ($14)

|

PNC $6 ($2)

|

|

GS $18( $2)

|

US Bank $6

|

|

Amex $13

|

Deutsche Bank $5

|

|

Citi $13($5)

|

Depfa ACS -Covered $5

|

|

Wells $13

|

FMCC $5

|

|

Natl Rural $9

|

John Deere Cap $5 ($2)

|

|

FDIC backed amounts listed in parentheses

|

|

62

12/31/2009

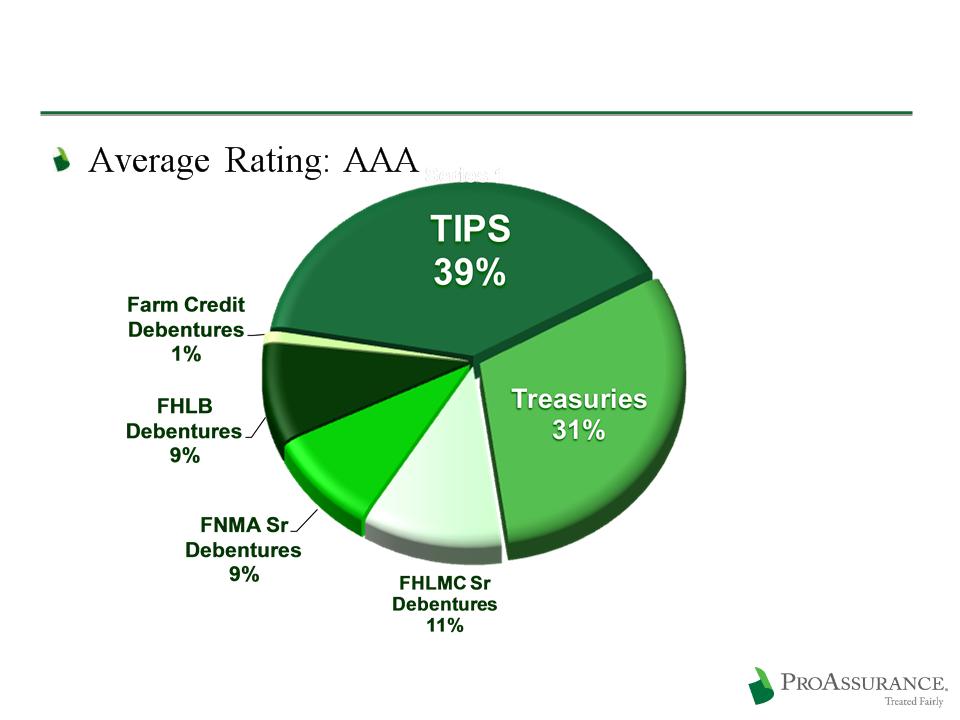

Treasury/GSE: $221 Million

63

12/31/2009

64

12/31/2009

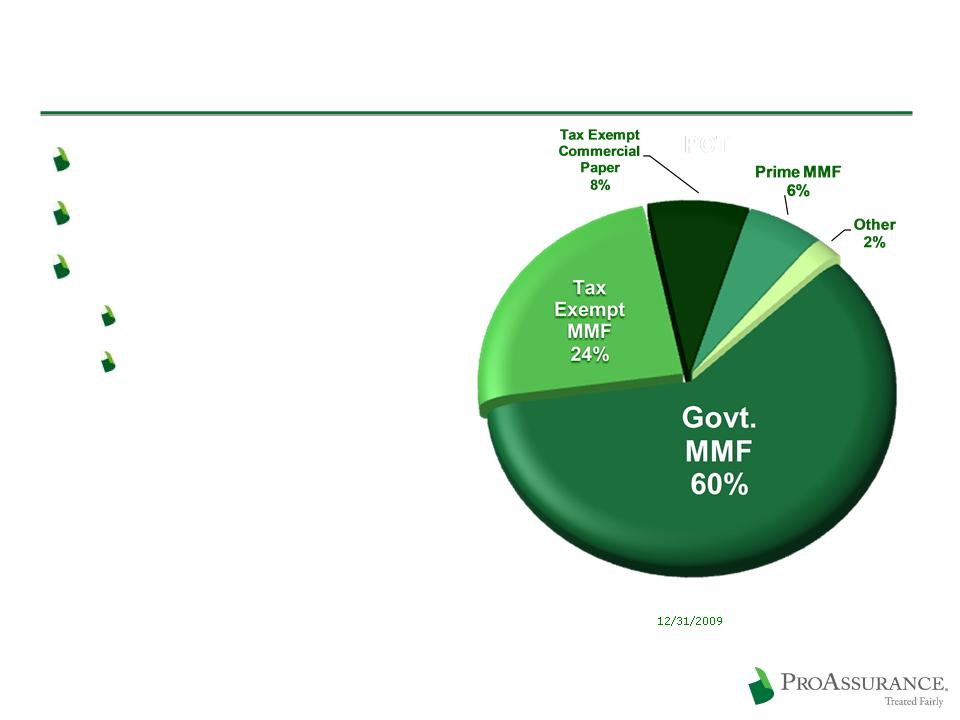

Portfolio Overview: Short Term

$187 Million

Rated A1/P1 or better

Money Markets:

Moody’s: Aaa

S&P: AAA

65

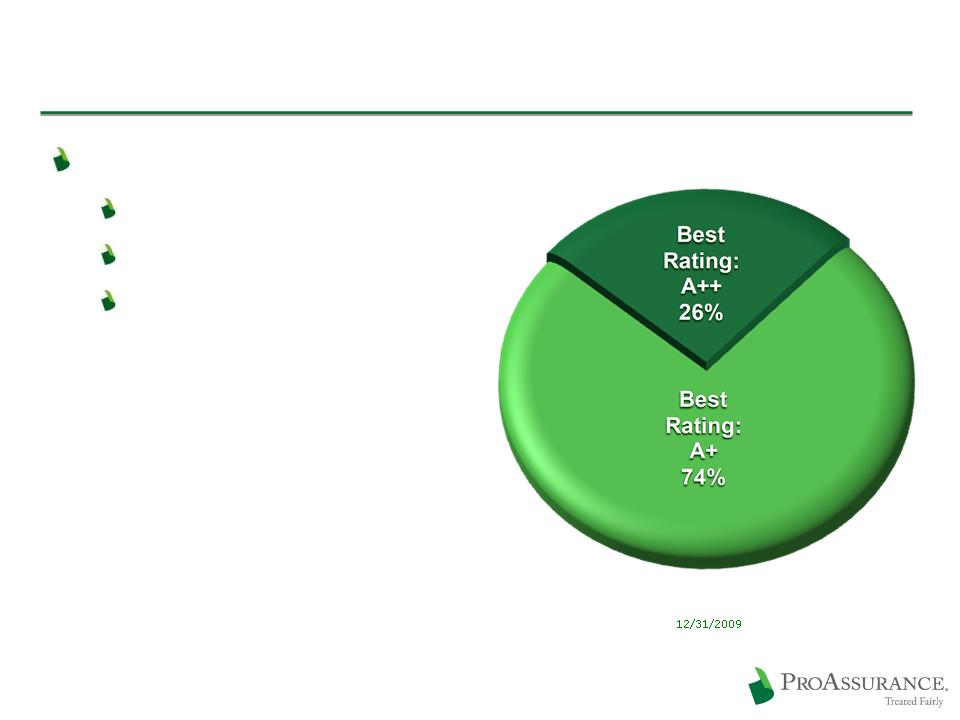

BOLI: $65 Million

Weighted average rating

Moody’s: AA3

S&P: AA-

A. M. Best: A+

66