Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - LADISH CO INC | c97323exv21.htm |

| EX-23 - EXHIBIT 23 - LADISH CO INC | c97323exv23.htm |

| EX-32 - EXHIBIT 32 - LADISH CO INC | c97323exv32.htm |

| EX-31.B - EXHIBIT 31(B) - LADISH CO INC | c97323exv31wb.htm |

| EX-31.A - EXHIBIT 31(A) - LADISH CO INC | c97323exv31wa.htm |

| EX-10.Q - EXHIBIT 10(Q) - LADISH CO INC | c97323exv10wq.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

Form 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-34495

Ladish Co., Inc.

( Exact name of registrant as specified in its charter )

| Wisconsin ( State of Incorporation ) |

31-1145953 ( I.R.S. Employer Identification No. ) |

|

| 5481 S. Packard Avenue Cudahy, Wisconsin ( Address of principal executive offices ) |

53110 ( Zip Code ) |

Registrant’s telephone number, including area code: (414) 747-2611

Securities Registered Pursuant to Section 12(b) of the Act: None

Securities Registered Pursuant to Section 12(g) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common stock, $0.01 par value | Nasdaq |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule

405 of the Securities Act.

Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or

Section 15(d) of the Act.

Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by

Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark

whether the registrant has submitted electronically and posted on its corporate

Web site, if any, every Interactive Data File required to be submitted and

posted pursuant to Rule 405 of Regulation S-T during the preceding

12 months (or for such shorter period that the registrant was required to

submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Registration S-K

(§229.405 of this chapter) is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information

statements incorporated by reference in Part III of this Form 10-K or

any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated

filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

| Large accelerated filer o | Accelerated filer þ | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No þ |

The aggregate market value of voting stock held by non-affiliates of the Registrant was

$189,507,328 as of June 30, 2009.

15,903,004

(Number of Shares of common stock outstanding as of March 4, 2010)

(Number of Shares of common stock outstanding as of March 4, 2010)

DOCUMENTS INCORPORATED BY REFERENCE

| Part of Form 10-K into Which | ||||

| Documents* | Portions of Documents are Incorporated | |||

Proxy Statement for 2010

Annual Meeting of Stockholders

|

Part III, Item 10. | Directors and Executive Officers of the Registrant | ||

| Part III, Item 11. | Executive Compensation | |||

| Part III, Item 12. | Security Ownership of Certain Beneficial Owners and Management | |||

| Part III, Item 13. | Certain Relationships and Related Transactions | |||

| Part III, Item 14. | Principal Accountant Fees and Services | |||

| * | Only the portions of documents specifically listed herein are to be deemed incorporated by

reference. |

TABLE OF CONTENTS

Table of Contents

PART 1

Item 1. Business

General

Ladish Co., Inc. (“Ladish” or the “Company”) engineers, produces and markets high-strength,

high-technology forged and cast metal components for a wide variety of load-bearing and

fatigue-resisting applications in the jet engine, aerospace and industrial markets. Approximately

88% of the Company’s 2009 revenues were derived from the sale of jet engine parts, missile

components, landing gear, helicopter rotors and other aerospace products. Approximately 44% of the

Company’s 2009 revenues were derived from sales, directly or through prime contractors, under

United States government contracts or under contracts with allies of the United States government,

primarily covering defense equipment. Although no comprehensive trade statistics are available,

based on its experience and knowledge of the industry, management believes that the Company is the

second largest supplier of forged and cast metal components to the domestic aerospace industry,

with an estimated 25% market share in the jet engine component field.

Products and Markets

The Company markets its products primarily to manufacturers of jet engines, commercial business and

defense aircraft, helicopters, satellites, heavy-duty off-road vehicles and industrial and marine

turbines. The principal markets served by the Company are jet engine, commercial aerospace

(defined by Ladish as satellite, rocket and aircraft components other than jet engines) and general

industrial products. The amount of revenue and the revenue as a percentage of total revenue by

market were as follows for the periods indicated:

| Years Ended December 31, | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | ||||||||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||||||

Jet Engine Components |

$ | 238 | 56 | % | $ | 239 | 51 | % | $ | 193 | 55 | % | ||||||||||||

Aerospace Components |

102 | 24 | % | 124 | 26 | % | 114 | 33 | % | |||||||||||||||

General Industrial Components |

85 | 20 | % | 107 | 23 | % | 43 | 12 | % | |||||||||||||||

Total |

$ | 425 | 100 | % | $ | 470 | 100 | % | $ | 350 | 100 | % | ||||||||||||

Manufacturing

Ladish offers one of the most complete range of forging, investment casting and precision machining

services in the world. The Company employs all major forging processes, including open and

closed-die hammer and press forgings, as well as ring-rolling, and also produces near-net shape

aerospace components through isothermal forging and hot-die forging techniques. Closed-die forging

involves hammering or pressing heated metal into the required shape and size by utilizing machined

impressions in specially prepared dies which exert three-dimensional control on the heated metal.

Open-die forging involves the hammering or pressing of metal into the required shape without such

three-dimensional control, and ring-rolling involves rotating heated metal rings through presses to

produce the desired shape. Investment casting involves the creation of precise wax molds which are

dipped, autoclaved and cast to create near-net components for the aerospace industry. The

Company’s precision machining services focus on the milling and turning of components for the

aerospace industry.

2

Table of Contents

Much of the Company’s business is capital intensive, requiring large and sophisticated forging,

casting, machining and heating equipment and extensive facilities for inspection and testing of

components after

formation. Ladish believes that it has the largest forging hammer, isothermal press and ring-roll

in the world at its plant in Cudahy, Wisconsin. Its largest counterblow forging hammer has a

capacity of 125,000 mkg (meter-kilograms), and its ring-rolling equipment can produce single-piece

seamless products that weigh up to 350,000 pounds with outside diameters as large as 28 feet and

face heights up to 10 feet. Ladish’s 4,500-ton and 10,000-ton isothermal presses can produce

forgings, in superalloys as well as titanium, that weigh up to 2,000 pounds. Ladish is in the

process of qualifying a new 12,500-ton isothermal press which will be operational in 2010. Much of

the domestic forging equipment has been designed and built by Ladish. The Company also maintains

such auxiliary facilities as die-sinking, heat-treating and machining equipment and produces most

of the precision dies necessary for its forging operations. The Company considers such equipment

to be in good operating condition and adequate for the purposes for which it is being used.

Marketing and Sales

The product sales force, consisting primarily of sales engineers, is supported by the Company’s

metallurgical staff of engineers and technicians. These technically trained sales engineers,

organized along product line and customer groupings, work with customers on an ongoing basis to

monitor competitive trends and technological innovations. Additionally, sales engineers consult

with customers regarding potential projects and product development opportunities. During the past

few years, the Company has refocused its marketing efforts on the jet engine components market and

the commercial aerospace industry.

The Company is actively involved with key customers in joint cooperative research and development,

engineering, quality control, just-in-time inventory control and computerized process modeling

programs. The Company has entered into strategic contracts for a number of sole-sourced products

with each of Rolls-Royce, Sikorsky and Snecma for major programs. The Company believes that these

contracts are a reflection of the aerospace and industrial markets’ recognition of the Company’s

manufacturing and technical expertise.

The research and development of jet engine components is actively supported by the Company’s

Advanced Materials and Process Technology Group. The Company’s long-standing commitment to

research and development is evidenced by its industry-recognized materials and process

advancements. The experienced staff and fully equipped research facilities support Ladish sales

through customer-funded projects. Management believes that these research efforts position the

Company to participate in future growth in demand for critical advanced jet engine components.

Customers

The Company’s top three customers, Rolls-Royce, United Technologies and General Electric, accounted

for approximately 50%, 47% and 56% of the Company’s revenues in 2007, 2008 and 2009, respectively.

Net sales to Rolls-Royce were 28%, 23% and 26%, United Technologies 15%, 15% and 19% and General

Electric 7%, 9% and 11% of total Company net sales for the respective years. No other customer

accounted for ten percent or more of the Company’s net sales.

Caterpillar, Boeing, Techspace Aero, Goodrich and Snecma are also important customers of the

Company. Because of the relatively small number of customers for some of the Company’s principal

products, the Company’s largest customers exercise significant influence over the Company’s prices

and other terms of trade.

3

Table of Contents

U.S. exports accounted for approximately 49%, 46% and 46% of total Company net sales in 2007, 2008

and 2009, respectively. U.S. exports to England constituted approximately 29%, 25% and 26%,

respectively in the above years, of total Company net sales.

A substantial portion of the Company’s revenues is derived from long-term, fixed price contracts

with major engine and aircraft manufacturers. These contracts are typically “requirements”

contracts under which the purchaser commits to purchase a given portion of its requirements of a

particular component from the Company, and provide the Company with the ability to adjust prices

based on raw material price fluctuation. Actual purchase quantities are typically not determined

until shortly before the year in which products are to be delivered. The Company attempts to

minimize its risk by entering into fixed-price contracts with its raw material suppliers.

Additionally, a portion of the Company’s revenue is directly or indirectly related to government

spending, particularly military and space program spending.

Research and Development

The Company maintains a research and development department which is engaged in applied research

and development work primarily relating to the Company’s forging operations. The Company works

closely with customers, universities and government technical agencies in developing advanced

forgings, materials and processes. The Company spent approximately $2.9 million, $3.1 million and

$2.7 million on applied research and development work during 2007, 2008 and 2009, respectively.

Customers reimbursed the Company for $1.2 million, $1.3 million and $1.2 million of the foregoing

research and development expenses in 2007, 2008 and 2009, respectively.

Patents and Trademarks

Although the Company owns patents covering certain of its processes, the Company does not consider

these patents to be of material importance to the Company’s business as a whole. The Company

considers certain other information that it owns to be trade secrets and the Company takes measures

to protect the confidentiality and control the disclosure and use of such information. The Company

believes that these safeguards adequately protect its proprietary rights and the Company vigorously

defends these rights.

The Company owns or has obtained licenses for various trademarks, trademark registrations, service

marks, service mark registrations, trade names, copyrights, copyright registrations, patent

applications, inventions, know-how, trade secrets, confidential information and any other

intellectual property that is necessary for the conduct of its business (collectively,

“Intellectual Property”). The Company is not aware of any existing or threatened patent

infringement claim (or of any facts that would reasonably be expected to result in any such claim)

or any other existing or threatened challenge by any third party that would significantly limit the

rights of the Company with respect to any such Intellectual Property or to the validity or scope of

any such Intellectual Property. The Company has no pending claim against a third party with

respect to the infringement by such third party of any such Intellectual Property that, if

determined adversely to the Company, would individually or in the aggregate have a material adverse

effect on the Company’s financial condition or results of operations. While the Company considers

all of its proprietary rights as a whole to be important, the Company does not consider any single

right to be essential to its operations as a whole.

4

Table of Contents

Raw Materials

Raw materials used by the Company in its metal components include alloys of titanium, nickel,

steel, aluminum, tungsten and other high temperature alloys. The major portion of metal

requirements for forged products are purchased from major metal suppliers producing forging quality

material as needed to

fill customer orders. The Company has two or more sources of supply for all significant raw

materials, with the exception of certain nickel-based powder alloys where the Company is currently

dependent upon a single source of supply.

The titanium and nickel-based superalloys used by the Company have a relatively high dollar value.

Accordingly, the Company recovers and recycles scrap materials such as machine turnings, forging

flash, solids and test pieces (“by-products’). The proceeds from the disposition of by-products

are taken as a reduction to the Company’s cost of goods and are not treated as a part of net sales.

The Company’s most significant raw materials consist of nickel and titanium alloys. Its principal

suppliers of nickel alloys include Carpenter Technology, Special Metals Corporation and Allegheny

Technologies, Inc. (“ATI”). Its principal suppliers of titanium alloys are Titanium Metals

Corporation of America (“Timet”), ATI and RTI International. The Company typically has fixed-price

contracts with its suppliers.

In addition, the Company, its customers and suppliers have undertaken active programs for supply

chain management to reduce overall lead times and the total cost of raw materials. In 2009, the

Company experienced a decline in raw material prices and saw lead times shorten as demand for

material eased due to the global economic downturn. The Company expects raw material prices to

stabilize in 2010 as aerospace markets firm. The Company attempts to protect against raw material

price escalation by passing those price increases directly to the Company’s customers.

Energy

The Company uses a considerable amount of energy in the processing of its forged and cast metal

components. The fluctuating prices for energy, both natural gas and electricity, had a significant

impact on the Company’s 2008 and 2009 results. With the reduction of natural gas prices, the

Company expects energy to have a reduced impact on 2010 results. The Company attempts to

ameliorate the impact of these price swings by purchasing directly from producers and pre-ordering

supplies for the future, however, the level of price fluctuation and lack of availability are not

within the control of the Company.

Backlog

The average amount of time necessary to manufacture the Company’s products is five to six weeks

from the receipt of raw material. The timing of the placement and filling of specific orders may

significantly affect the Company’s backlog figures, which are subject to cancellation for a variety

of reasons. In addition, the Company typically only includes those contracts which will result in

shipments within the next 18 months when compiling backlog and does not include the out years of

long-term agreements. As a result, the Company’s backlog may not be indicative of actual results

or provide meaningful data for period-to-period comparisons. The Company’s backlog was

approximately $611 million, $629 million and $504 million as of December 31, 2007, 2008 and 2009,

respectively. In 2008, the Company received approximately $408 million in new orders and in 2009

the Company received $229 million in new orders as the backlog and order activity were negatively

impacted by 787 delays at Boeing and the unsettled economic climate.

Competition

The sale of metal components is highly competitive. Certain of the Company’s competitors are

larger than the Company and have substantially greater capital resources. Although the Company is

the sole supplier on several sophisticated components required by prime contractors under a number

of governmental programs, many of the Company’s products could be replaced with other similar

products

of its competitors. However, the significant investment in tooling, the time required and the cost

of obtaining the status of a “certified supplier” are barriers to entry. Competition is based on

quality (including advanced engineering and manufacturing capability), price and the ability to

meet delivery requirements.

5

Table of Contents

Website Access to Company Reports

The Company’s annual report is available free of charge on the Company’s website at

www.ladishco.com as soon as reasonably practicable after such material is filed electronically with

the SEC. The Company’s other filings with the SEC; Form 10-K, Form 10-Q, Form 8-K and Form 4 are

readily available at www.sec.gov/edgar or www.secfiling.com. The Company’s Form 14 Proxy Statement

for the 2010 annual stockholders’ meeting is available on the Company’s website. The Company’s

Code of Conduct is available on the Company’s website and in printed form upon request. Also,

copies of the Company’s annual report will be made available, free of charge, upon written request.

Environmental, Health and Safety Matters

The Company’s operations are subject to many federal, state and local regulations relating to the

protection of the environment and to workplace health and safety. In particular, the Company’s

operations are subject to extensive federal, state and local laws and regulations governing waste

disposal, air and water emissions, the handling of hazardous substances, environmental protection,

remediation, workplace exposure and other matters. Management believes that the Company is

presently in substantial compliance with all such laws and does not currently anticipate that the

Company will be required to expend any substantial amounts in the foreseeable future in order to

meet current environmental, workplace health or safety requirements. However, additional costs and

liabilities may be incurred to comply with current and future requirements which could have a

material adverse effect on the Company’s results of operations or financial condition.

There are no known pending remedial actions or claims relating to environmental matters that are

expected to have a material effect on the Company’s financial position or results of operations.

All of the properties owned by the Company, however, are located in industrial areas and have a

history of heavy industrial use. These properties may potentially incur environmental liabilities

in the future that could have a material adverse effect on the Company’s financial condition or

results of operations. The Company was previously named a potentially responsible party at several

“Superfund” sites. The Company’s liability with respect to these sites has largely been resolved.

Although the Company does not believe that the amount for which it may be held liable for any

further administrative or wrap-up expense will exceed the amount it has reserved, no assurance can

be given that the amount for which the Company will be held responsible will not be significantly

greater than expected. In 2006, the Company agreed to participate in the environmental remediation

of a site near Houston, Texas. The Company’s allocated share is relatively small, less than 1%,

and its projected exposure for the site is estimated to be $0.16 million. The Company has an

accrual of $0.30 million for this site and any other environmental claims which may arise.

With respect to any past or future claim for any environmental, health or safety matter, the

Company evaluates every such claim from both a technical and legal perspective, using outside

consultants where necessary. The Company establishes a good faith estimate of its prospective risk

associated with said claim and, where material, establishes an accrual for the estimated value of

such claim.

6

Table of Contents

Forward Looking Statements

Any statements contained herein that are not historical facts are forward-looking statements within

the meaning of the Private Securities Legislation Reform Act of 1995, and involve risks and

uncertainties. These forward-looking statements include expectations, beliefs, plans, objectives,

future financial performance, estimates, projections, goals and forecasts. Potential factors which

could cause the Company’s actual results of operations to differ materially from those in the

forward-looking statements include:

| • | Market conditions and demand for the Company’s products |

|

| • | Interest rates and capital costs |

|

| • | Unstable governments and business conditions in emerging

economies |

|

| • | Health care costs |

|

| • | Legal, regulatory and environmental issues |

|

| • | Competition |

|

| • | Technologies |

|

| • | Raw material and energy prices |

|

| • | Taxes |

Any forward-looking statement speaks only as of the date on which such statement is made. The

Company undertakes no obligation to update any forward-looking statement to reflect events or

circumstances after the date on which such statement is made.

Employees

As of December 31, 2009, domestically, the Company had approximately 1,137 employees, of whom 847

were engaged in manufacturing functions, 65 in executive and administrative functions, 180 in

technical functions, and 45 in sales and sales support. At such date, approximately 517 employees,

principally those engaged in manufacturing, were represented by labor organizations under

collective bargaining agreements. Internationally, the Company had approximately 500 employees in

Poland as of December 31, 2009, approximately two-thirds of which are represented by trade unions.

| Number of Employees | ||||||

| Represented by Collective | ||||||

| Union | Expiration Date | Bargaining Agreement | ||||

International Association of Machinists & Aerospace Workers, Local 1862

|

February 26, 2012 | 193 | ||||

International Brotherhood of Boilermakers, Iron Ship Builders,

Blacksmiths, Forgers & Helpers, Subordinate Lodge 1509

|

October 1, 2012 | 145 | ||||

International Federation of Professional & Technical Engineers,

Technical Group, Local 92

|

August 19, 2012 | 92 | ||||

International Association of Machinists & Aerospace Workers, Die

Sinkers, Local 140

|

March 26, 2012 | 47 | ||||

Office

& Professional Employees International Union, Clerical Group, Local 35 |

July 15, 2013 | 16 | ||||

International Brotherhood of Electrical Workers, Local 662

|

November 11, 2012 | 20 | ||||

Service Employees International, Local 1

|

April 22, 2012 | 4 | ||||

7

Table of Contents

Executive Officers of the Company

| Name | Age | Position | ||||

Gary J. Vroman

|

50 | President & CEO and Director | ||||

Wayne E. Larsen

|

55 | Vice President Law/Finance & Secretary and Director | ||||

Lawrence C. Hammond

|

62 | Vice President, Human Resources | ||||

Randy B. Turner

|

60 | President — Pacific Cast Technologies, Inc. (“PCT”) | ||||

John Delaney

|

60 | President — Stowe Machine Co., Inc. (“Stowe”) &

Aerex LLC (“Aerex”) |

||||

Robert C. Miller

|

59 | President — Valley Machining, Inc. (“Valley”) | ||||

Jozef Burdzy

|

58 | President — Zaklad Kuznia Matrycowa Sp. z o.o. (“ZKM”) &

Zaklad Obrobki i Procesow Specjalnych Sp. z o.o. (“ZOPS”) |

||||

Shannon J. S. Ko

|

67 | President — Chen-Tech Industries, Inc. (“Chen-Tech”) | ||||

Item 1A. Risk Factors

Cyclicality of the Aerospace and Jet Engine Industries

Substantially all of our revenues are derived from the aerospace and jet engine industries, which

are cyclical in nature and subject to changes based on general economic conditions, airline

profitability, passenger ridership and international relations. The duration and severity of

upturns and downturns in these industries are influenced by a variety of factors, including those

set forth herein. Accordingly, they cannot be predicted with any certainty. Historically, orders

for new commercial aircraft and related commercial aerospace components have been driven by the

operating profits or losses of commercial airlines. Purchases by customers in the military

aerospace sector are dependent upon defense budgets. Events adversely affecting the airline

industry, such as cyclical overcapacity and inability to maintain profitable fare structures, would

likely have a material adverse effect on our financial condition and results of operations.

Reduction in Government Spending

Since 2002, approximately 25% to 40% of our annual revenues have been derived from the

government-sponsored aerospace industry, an industry that is dependent upon government budgets and,

in particular, the United States government budget. There can be no assurance that U.S. defense

and space budgets and the related demand for defense and space equipment will continue or that

sales of defense and space equipment to foreign governments will continue at present levels.

Competition

The sale of metal components for the aerospace, jet engine and industrial markets is highly

competitive. Many products we manufacture are readily interchangeable with the products

manufactured by our competitors. Many of our products are sold under long-term contracts which are

bid upon by several suppliers. Our principal competitor, Precision Castparts Corp. (“PCC”), is a

substantially larger business and has greater financial resources. In 2006, PCC purchased one of

our larger suppliers of nickel-based alloys, Special Metals Corporation.

Reliance on Major Customers

Our three largest customers accounted for approximately 50%, 47% and 56% of our revenues in 2007,

2008 and 2009, respectively. Because of the small number of customers for some of our principal

products, those customers exercise significant influence over our prices and other terms of trade.

The loss of any of our largest customers could have a material adverse effect on our financial

condition and results

of operations. The labor strike at Boeing during the second half of 2008 had a negative impact

upon the entire commercial aviation industry including the Company.

8

Table of Contents

Dependence on Key Personnel

We have been and continue to be dependent on certain key management personnel. Our ability to

maintain our competitive position will depend, in part, upon our ability to retain these key

managers and to continue to attract and retain highly qualified managerial, manufacturing and sales

and marketing personnel. There can be no assurance that the loss of key personnel would not have a

material adverse effect on our results of operations or that we will be able to recruit and retain

such personnel.

Product Liability Exposure

We produce many critical engine and structural parts for commercial and military aircraft and for

other specialty applications. As a result, we have an inherent risk of exposure to product

liability claims. We currently maintain product liability insurance, but there can be no assurance

that insurance coverage will continue to be available on terms acceptable to us or that such

coverage will be adequate for any liabilities that might be incurred.

Availability and Price of Raw Materials

The largest single component of our cost of goods sold is raw material costs. We manufacture

products in a wide variety of specialty metals and alloys, some of which can only be purchased from

a limited number of suppliers. We hold limited quantities of raw materials in inventory but, for

the principal part of our business, we seek to procure delivery of raw materials in quantities and

at times matching customers’ orders. We, along with other entities in the industry, have

experienced periods of increased delivery times for nickel-based and titanium alloys and certain

stainless steels, which account for a significant portion of our raw materials. Significant

scarcity of supply of raw materials used by us could have a material adverse effect on our results

of operations by affecting both the timing of delivery and the cost of purchasing such materials.

In addition, our largest competitor, PCC, has purchased one of our largest suppliers of

nickel-based alloys. Many of our products are sold pursuant to long-term agreements with our

customers, which currently provide us the right to pass through material cost increases. Any

inability to obtain such rights in future long-term agreements could have a material adverse effect

on our results of operations.

Labor Contracts

Approximately 45% of our domestic employees are represented by seven collective bargaining units.

Contracts were historically renegotiated every three years with each union. Six of the unions in

2006 and one union in 2007 entered into six-year agreements with the Company. While we do not

expect that work stoppages will arise in connection with the renewal of labor agreements expiring

in the foreseeable future, no assurance can be given that work stoppages will not occur. An

extended or widespread work stoppage could have a material adverse effect on our results of

operations.

Pension and Other Postretirement Benefit Obligations

Many of our employees are eligible to participate in various Company-sponsored pension plans. In

addition to pension benefits, we provide health care and life insurance benefits to our eligible

employees and retirees. The pension benefits have been and will continue to be funded through

contributions to pension trusts, while health care and life insurance benefits are paid as

incurred.

9

Table of Contents

We have several pension plans, all of which are underfunded. The aggregate actuarially determined

liability recorded for these pension plans on the balance sheet at December 31, 2009 was

approximately $79.3 million. The decline in the equity market in the United States in 2008 had a

negative impact upon the level of assets in the pension trust of the Company; a portion of that

decline was recovered in 2009.

The actuarially determined liability recorded for postretirement health care and life insurance

benefits on the balance sheet at December 31, 2009 was approximately $33.7 million and will be paid

as incurred.

Compliance with Environmental and Other Government Regulations

Our operations are subject to extensive environmental, health and safety laws and regulations

promulgated by federal, state and local governments. Many of these laws and regulations provide

for substantial fines and criminal sanctions for violations. The nature of our business exposes us

to risks of liability due to the use and storage of materials that can cause contamination or

personal injury if released into the environment. In addition, environmental laws may have a

significant effect on the nature, scope and cost of cleanup of contamination at operating

facilities. It is difficult to predict the future development of such laws and regulations or

their impact on future earnings and operations, but we anticipate that these standards will

continue to require continued capital expenditures. There can be no assurance that we will not

incur material costs and liabilities in the future relating to environmental matters.

Risks Related to Significant Price Concessions to Our Customers and Increased Pressure to Reduce

Our Costs

We are subject to substantial competition in all of the markets we serve, and we expect this

competition to continue. As a result, we have made significant price concessions to our customers

in the aerospace and industrial markets in recent years and we expect customer pressure for price

concessions to continue. Maintenance of our profitability will depend, in part, on our ability to

sustain a cost structure that enables us to be cost-competitive. If we are unable to adjust our

cost relative to our pricing or if we are unable to continue to compete effectively, our business

will suffer.

Our Business is Affected by Federal Rules, Regulations and Orders Applicable to Government

Contractors

A number of our products are manufactured and sold under U.S. government contracts or subcontracts.

Violation of applicable government rules and regulations could result in civil liability, in

cancellation or suspension of existing contracts or in ineligibility for future contracts or

subcontracts funded in whole or in part with federal funds.

10

Table of Contents

Risks Associated with International Operations

We purchase products from and supply products to businesses located outside of the United States.

In fiscal 2009, approximately 54% of our total sales were attributable to non-U.S. customers. A

number of risks inherent in international business could have a material adverse effect on our

future results of operations, including:

| • | currency fluctuations; |

|

| • | general economic and political uncertainties and potential for social unrest in international markets; |

|

| • | limitations on our ability to enforce legal rights and remedies; |

|

| • | changes in trade policies; |

|

| • | tariff regulations; |

|

| • | difficulties in obtaining export and import licenses; and |

|

| • | the risk of government financed competition. |

Our Business Involves Risks Associated with Complex Manufacturing Processes

Our manufacturing processes depend on certain sophisticated and high-value equipment, such as some

of our forging presses for which there may be only limited or no production alternative.

Unexpected failures of this equipment may result in production delays, revenue loss and significant

repair costs. In addition, equipment failures could result in injuries to our employees.

Moreover, the competitive nature of our business requires that we continuously implement process

changes intended to achieve product improvements and manufacturing efficiencies. These process

changes may at times result in production delays, quality concerns and increased costs. Any

disruption of operations at our facilities due to equipment failures or process interruptions could

have a material adverse effect on our business.

Acquisitions

We expect that we will continue to make acquisitions of, investments in, and strategic alliances

with complementary businesses, products and technologies to enable us to add products and services

for our core customer base and for related markets, and to expand our business geographically. The

success of this acquisition strategy will depend on our ability to: identify suitable businesses

to buy; negotiate the purchase of those businesses on terms acceptable to us; complete the

acquisitions within our expected time frame; improve the results of operations of the businesses

that we buy and successfully integrate their operations into our own; and avoid or overcome any

concerns expressed by regulators.

We may fail to properly complete any or all of these steps. We may not be able to find appropriate

acquisition candidates, acquire those candidates that we do find, obtain necessary permits or

integrate acquired businesses effectively and profitably.

Some of our competitors are also seeking to acquire similar businesses, including competitors that

have greater financial resources than we do. Increased competition may reduce the number of

acquisition targets available to us and may lead to less favorable terms as part of any

acquisition, including higher purchase prices. If acquisition candidates are unavailable or too

costly, we may need to change our business strategy.

We also cannot be certain that we will have enough capital or be able to raise enough capital on

reasonable terms, if at all, to complete the purchases of the businesses that we want to buy. Our

credit facility limits our ability to make acquisitions. Our lender may object to certain

purchases or place conditions on them that would limit their benefit to us.

If we are unsuccessful in implementing our acquisition strategy for the reasons discussed above or

otherwise, our financial condition and results of operations could be materially adversely

affected.

Item 1B. Unresolved Staff Comments

The Company has no unresolved comments from the Commission staff.

11

Table of Contents

Item 2. Properties

The following table sets forth the location and size of the Company’s seven facilities:

| Approximate Acreage | Approximate Square Footage | |||||||

Forging — Cudahy, Wisconsin |

140.0 | 1,650,000 | ||||||

Stowe — Windsor, Connecticut |

8.2 | 40,000 | ||||||

PCT — Albany, Oregon |

14.0 | 149,000 | ||||||

Valley — Coon Valley, Wisconsin |

3.0 | 40,000 | ||||||

ZKM — Stalowa Wola, Poland |

70.0 | 820,000 | ||||||

Chen-Tech — Irvine, California |

2.0 | 55,000 | ||||||

Aerex — Windsor, Connecticut |

1.0 | 15,000 | ||||||

The above facilities, except for Chen-Tech and Aerex, are owned by the Company.

The Company believes that its facilities are well maintained, are suitable to support the Company’s

business and are adequate for the Company’s present and anticipated needs. While the rate of

utilization of the Company’s manufacturing equipment is not uniform, the Company estimates that its

facilities overall are currently operating at approximately 50% of capacity.

The principal executive offices of the Company are located at 5481 South Packard Avenue, Cudahy,

Wisconsin 53110. Its telephone number at such address is (414) 747-2611.

Item 3. Legal Proceedings

From time to time the Company is involved in legal proceedings relating to claims arising out of

its operations in the normal course of business. Although the Company believes that there are no

material legal proceedings pending or threatened against the Company or any of its properties, the

Company has been named as a defendant in a number of asbestos cases in Mississippi, Illinois,

Wisconsin and California. As of December 31, 2009, the Company has been dismissed from the case in

California and has 11 individual claims in Mississippi, two individual claims remaining in Illinois

and one individual claim in Wisconsin. The Company has never manufactured or processed asbestos.

The Company’s only exposure to asbestos involves products the Company purchased from third parties.

The Company has notified its insurance carriers of these claims and is vigorously defending these

actions. The Company has not made any provision in its financial statements for the asbestos

litigation.

The Company is participating in an investigation initiated by U.S. Customs & Border Protection

(“Customs”) into duty drawback claims filed on behalf of the Company by its former export agent.

The Company is cooperating with Customs in this investigation and has voluntarily suspended its

duty drawback claims. Based upon its internal investigation, the Company believes any errors or

omissions with respect to its filings were solely attributable to its former export agent. The

Company intends to continue to cooperate with Customs in resolving this matter. The Company has

not made any provision in its financial statements for the Customs investigation.

Item 4. Submission of Matters to a Vote of Security Holders

There were no matters submitted to a vote of security holders during the fourth quarter of 2009.

12

Table of Contents

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

The common stock of the Company, par value $0.01 per share, trades on the Nasdaq National Market

under the symbol “LDSH”.

The following table sets forth, for the fiscal periods indicated, the high and low closing prices

for each quarter of the years 2007, 2008 and 2009. At December 31, 2009 there were an estimated

2,500 beneficial holders of the Company’s common stock.

| Year Ended | Year Ended | Year Ended | ||||||||||||||||||||||

| December 31, 2007 | December 31, 2008 | December 31, 2009 | ||||||||||||||||||||||

| High | Low | High | Low | High | Low | |||||||||||||||||||

First quarter |

$ | 44.40 | $ | 35.08 | $ | 41.94 | $ | 32.90 | $ | 15.34 | $ | 5.36 | ||||||||||||

Second quarter |

$ | 44.39 | $ | 37.22 | $ | 37.35 | $ | 20.59 | $ | 15.04 | $ | 7.28 | ||||||||||||

Third quarter |

$ | 56.21 | $ | 40.96 | $ | 27.56 | $ | 18.75 | $ | 16.48 | $ | 10.88 | ||||||||||||

Fourth quarter |

$ | 59.30 | $ | 40.03 | $ | 19.74 | $ | 11.47 | $ | 16.03 | $ | 11.79 | ||||||||||||

The Company has not paid cash dividends and currently intends to retain all its earnings to

reduce debt and to finance its operations, its stock repurchase program and future growth. The

Company does not expect to pay dividends for the foreseeable future.

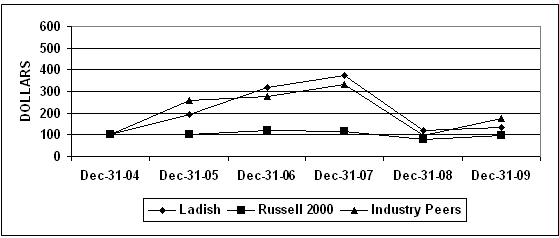

TOTAL SHAREHOLDER RETURN

The following graph compares the period percentage change in Ladish’s cumulative total

shareholder return on its common stock, assuming dividend reinvestment, with the cumulative total

return of (i) the Russell 2000 Small Cap Index, and (ii) a peer group from the Company’s industry,

for the period of December 31, 2004 to December 31, 2009. The Company’s peer group is comprised of

PCC, ATI, Timet and SIFCO Industries, Inc.

| Dec-31-04 | Dec-31-05 | Dec-31-06 | Dec-31-07 | Dec-31-08 | Dec-31-09 | |||||||||||||||||||

Ladish

|

11.60 | 22.35 | 37.08 | 43.19 | 13.85 | 15.05 | ||||||||||||||||||

Russell 2000

|

651.57 | 673.22 | 796.89 | 765.90 | 499.45 | 625.39 | ||||||||||||||||||

Industry Peers

|

26.29 | 67.53 | 73.05 | 86.93 | 24.94 | 45.51 | ||||||||||||||||||

13

Table of Contents

Item 6. Selected Financial Data

The selected financial data of the Company for each of the last five fiscal years are set forth

below.

The data below should be read in conjunction with the Financial Statements and the Notes thereto

and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”

included elsewhere in this filing.

| Year Ended December 31, | ||||||||||||||||||||

| (Dollars in millions, except earnings per share) | ||||||||||||||||||||

| INCOME STATEMENT DATA | 2005 | 2006 | 2007 | 2008 | 2009 | |||||||||||||||

Net sales |

$ | 266.841 | $ | 369.290 | $ | 424.631 | $ | 469.466 | $ | 349.832 | ||||||||||

Income from operations |

23.847 | 48.960 | 52.319 | 39.538 | 9.248 | |||||||||||||||

Interest expense |

2.072 | 3.548 | 2.528 | 1.971 | 5.050 | |||||||||||||||

Net income |

13.715 | 28.481 | 32.288 | 32.205 | 6.094 | |||||||||||||||

Basic earnings per share |

1.00 | 2.01 | 2.22 | 2.15 | 0.38 | |||||||||||||||

Diluted earnings per share |

0.98 | 2.00 | 2.22 | 2.15 | 0.38 | |||||||||||||||

Dividends paid |

— | — | — | — | — | |||||||||||||||

Shares used to compute earnings per share: |

||||||||||||||||||||

Basic |

13,781,586 | 14,136,946 | 14,516,120 | 14,998,437 | 15,901,833 | |||||||||||||||

Diluted |

13,931,539 | 14,205,641 | 14,550,258 | 15,000,844 | 15,902,246 | |||||||||||||||

| December 31, | ||||||||||||||||||||

| BALANCE SHEET DATA | 2005 | 2006 | 2007 | 2008 | 2009 | |||||||||||||||

Total assets |

$ | 296.556 | $ | 329.060 | $ | 381.833 | $ | 509.466 | $ | 469.514 | ||||||||||

Net working capital |

71.116 | 123.764 | 130.855 | 138.910 | 137.515 | |||||||||||||||

Total debt |

45.000 | 54.100 | 53.500 | 118.900 | 90.000 | |||||||||||||||

Stockholders’ equity |

117.469 | 152.670 | 201.554 | 223.411 | 225.582 | |||||||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of

Operations

Executive Overview

2009 was a transitional year for Ladish. The Company entered the year fully cognizant of the

global economic issues associated with credit and the capital markets which occurred in the second

half of 2008. However, Ladish, with $629 million of contract backlog, had yet to be significantly

impacted by the recession. The global economic slowdown began impacting Ladish in the first

quarter of 2009 as delivery schedules for products began to shrink and move out to later dates. By

June 30, 2009, the Company’s contract backlog had declined to $488 million. The third quarter was

the nadir for the Company both in terms of sales, $76.2 million, a pretax loss of $3.0 million, and

a contract backlog of $476 million. The fourth quarter brought signs of an economic recovery for

Ladish. Net sales increased to $83.2 million, pretax income was $3.3 million and contract backlog

increased to $504 million.

In response to the sudden downturn in business, Ladish took a number of steps to reduce costs while

still maintaining the ability to serve customers’ shifting demands. Employment levels were reduced

from 2,039 to 1,637, a 20% decline. In addition, the Company instituted a salary freeze for 2009

and reduced certain discretionary benefits. At a number of the operating units of the Company,

weeks of lay-off and unpaid weeks were also utilized to reduce costs. During the course of this

business slowdown, the Company significantly reduced its working capital by lowering inventory by

$36.6 million and receivables by $19.3 million. Ladish also reduced its capital expenditures from

the 2008 peak of $49.8 million to $13.9 million in 2009. Through its focus on cost control and

working capital reduction in 2009, Ladish generated over $44 million of positive cash flow.

14

Table of Contents

While many businesses faced credit difficulties and shortages of liquidity in 2009, Ladish avoided

those balance sheet challenges by deleveraging itself through the repayment of $28.9 million of

senior bank debt and $1.7 million of capital leases. The Company also proactively worked with both

its senior bank lenders and the holders of its long-term notes to adjust covenants in the

respective agreements to provide the Company added operational flexibility. Ladish ended 2009 with

no bank debt, no capital leases, $90 million of long-term notes, $19.9 million in cash and in full

compliance with all covenants and requirements in its lending agreements.

Net income in 2009 had a tax benefit of $2.9 million in lieu of a tax provision. The tax benefit

resulted primarily from the decision of the Company to reverse a $5.3 million valuation allowance

for a manufacturing investment credit in Wisconsin. This decision was largely influenced by

legislative changes in Wisconsin in late 2009 along with the Company’s long-term optimistic outlook

toward full utilization of the credit. The tax credit contributed to Ladish’s $6.1 million, or

$0.38 per share, of earnings in 2009. Without the tax credit, Ladish would have had $0.8 million,

or $0.05 per share, of earnings in 2009.

All three of Ladish’s major markets declined in 2009, albeit at varying rates. In 2009, component

sales were down 8% for aerospace, 19% for jet engines and 60% for general industrial. In spite of

these declines, the Company’s domestic operations remained profitable in 2009. The Company’s

European operations are currently primarily dependent on the industrial market and could not

sufficiently offset the lack of demand in order to produce positive results.

Results of Operations

Year Ended December 31, 2009 Compared to Year Ended December 31, 2008

2009 net sales were $349.8 million, a 25.5% reduction from the $469.5 million of net sales in 2008.

The decline in sales was due to reduced demand in all of the Company’s markets. The Company’s

sales of components for jet engines, aerospace and general industrial declined 19%, 8% and 60%,

respectively, as customers reduced their build schedules and destocked their inventory. In 2009,

cost of sales at the Company increased to 92.3% of net sales in comparison to 87.4% in 2008. The

percentage increase in 2009 is directly linked to the reduction of sales with fewer sales to cover

the fixed costs at the Company.

SG&A expenses at the Company were $17.8 million in 2009, in contrast to $19.8 million of SG&A

expenses in 2008. Although the Company experienced a $2 million year-over-year reduction in SG&A,

as a percentage of sales SG&A increased to 5.1% in 2009 from 4.2% during the same period in 2008.

The increased rate of SG&A expense in 2009 is attributable to a combination of one-time charges

related to employment reductions and the reduced level of sales.

Interest expense at the Company in 2009 was $5.1 million, a $3.1 million increase from the level in

2008. The growth of interest expense in 2009 was related to a full year of interest on the Series

C long-term notes along with the reduction of capitalized interest in 2009. The Company was able

to capitalize $2.4 million of interest in 2008 while it only capitalized $1.0 million of interest

in 2009. Total interest incurred was $6.0 million and $4.4 million, respectively, in 2009 and

2008. The following table reflects the Company’s treatment of interest in 2008 and 2009:

| (Dollars in millions) | 2008 | 2009 | ||||||

Interest expensed |

$ | 1.971 | $ | 5.050 | ||||

Interest capitalized |

2.418 | 0.953 | ||||||

Total |

$ | 4.389 | $ | 6.003 | ||||

15

Table of Contents

The Company earned $3.1 million and $38.3 million of pretax income, respectively, in 2009 and 2008.

The decline in pretax income was due to decreased sales and increases in pension expense, interest

expense, depreciation expense, costs associated with downsizing operations and lower by-product

sales in 2009. These expense increases were somewhat offset by reductions in employment costs

related to lower employment levels in 2009.

In 2009, the Company reversed a valuation allowance and recognized a tax asset in the amount of

$5.3 million which resulted in a tax benefit of $2.9 million. The tax asset related to a credit

for state taxes which the Company determined it was more likely than not that the Company would

earn sufficient income to fully utilize the credit. In 2008, the Company had a tax provision of

$5.9 million for an effective rate of 15.4%.

Net income for 2009 was $6.1 million or $0.38 per share on a fully diluted basis. The decline from

2008 net income of $32.2 million was a result of reduced sales combined with increases in pension

expense of $4.4 million, interest expense of $3.1 million, depreciation expense of $2.0 million,

employment reduction expenses of $3.0 million and reduced by-product sales of $7.9 million, offset

by the recognition of the state tax credit of $5.3 million.

The Company ended 2009 with a contract backlog of $504 million, down from the 2008 ending backlog

of $629 million. In 2009, the Company booked $229 million of new orders in contrast to $408

million of new orders in 2008. The decline in new orders was related to the global slowdown in the

aerospace market associated with reduced passenger miles in 2009.

Year Ended December 31, 2008 Compared to Year Ended December 31, 2007

Net sales in 2008 were $469.5 million, a 10.6% increase over the $424.6 million of net sales in

2007. The sales growth in 2008 was due to the continued strength of Ladish’s markets and the

acquisitions of Aerex and Chen-Tech in the third quarter of 2008. In 2008, cost of sales for the

Company was 87% of net sales in comparison to 84% of net sales in 2007.

The Company’s SG&A expense in 2008 was $19.8 million, or 4.2% of net sales. In 2007, SG&A expense

was 3.9% of net sales. The percentage increase in SG&A expense is attributed to growth in

employment to support capacity expansion and higher professional fees associated with tax planning.

In 2008, the Company’s interest expense was $2.0 million in comparison to $2.5 million in 2007.

The decrease in interest expense in 2008 was the result of a larger amount of interest capitalized

associated with the capacity expansion programs at the Company. Total interest increased in 2008

as the Company incurred additional debt to support the acquisitions of Aerex and Chen-Tech. The

following table reflects the Company’s treatment of interest for the years 2007 and 2008:

| (Dollars in millions) | 2007 | 2008 | ||||||

Interest expensed |

$ | 2.528 | $ | 1.971 | ||||

Interest capitalized |

0.795 | 2.418 | ||||||

Total |

$ | 3.323 | $ | 4.389 | ||||

Pretax income in 2008 was $38.3 million, an $11.9 million reduction from the 2007 pretax income

level. The decline in pretax income was due to product mix and under-absorbed fixed costs.

Tax expense for 2008 was $5.9 million, which equated to an effective tax rate of 15.4%. In 2007,

the Company experienced an effective tax rate of 35.5%. The reduction in tax rate is mainly

attributed to the

Company recognizing a significant tax savings from the recognition of a $5.5 million research and

development tax credit in the third quarter of 2008 and a $1.9 million foreign economic zone

credit.

16

Table of Contents

Net income in 2008 was $32.2 million, which equates to $2.15 per share on a fully-diluted basis.

Net income was similar to 2007 levels but declined as a percentage of sales due to higher raw

material and energy costs, a less profitable mix of products sold and inefficiencies associated

with expanding manufacturing capacity, offset by the aforementioned tax savings and the

capitalization of interest expense to capital projects.

The Company booked $408 million of new orders in 2008 in comparison to $534 million of new orders

in 2007. The decline in orders was associated with the Boeing labor stoppage in the third quarter

of 2008 and general, global economic conditions.

Liquidity and Capital Resources

The Company’s cash position as of December 31, 2009 is $15 million more than its position at

December 31, 2008. The 2009 increase in cash is due to reduced capital expenditures and pension

contributions along with a reduction in working capital. Cash flow from operations in 2009 was

$29.6 million more than cash flow from operations in 2008 primarily due to working capital

reduction as the Company reduced inventories and receivables, partially offset by a reduction in

accounts payable.

On May 16, 2006, the Company sold $40 million of Series B Notes in a private placement to certain

institutional investors. The Series B Notes are unsecured and bear interest at a rate of 6.14% per

annum with interest being paid semiannually. The Series B Notes have a ten-year duration with the

principal amortizing equally over the duration after the fourth year.

On September 2, 2008, the Company sold $50 million of Series C Notes in a private placement to

certain institutional investors. The Series C Notes are unsecured and bear interest at a rate of

6.41% per annum with interest being paid semiannually. The Series C Notes have a seven-year

duration with the principal amortizing equally over the duration after the third year.

The Company’s Series B and Series C Notes contain financial covenants which (a) limit the

incurrence of certain additional debt; (b) require a certain level of consolidated adjusted net

worth; (c) require a minimum fixed charges coverage ratio; and (d) require a limited amount of

funded debt to consolidated cash flow. The covenant on incurrence of additional debt limits funded

debt to 60% of total capitalization. At December 31, 2009, funded debt at Ladish was at 21% of

total capitalization. This covenant also limits priority debt to 20% of adjusted net worth.

Ladish had no priority debt at December 31, 2009. The covenant on adjusted net worth requires a

minimum of $112.8 million. At December 31, 2009, Ladish had $259.8 million of adjusted net worth.

The covenant on fixed charges coverage ratio requires that consolidated cash flow to fixed charges

be a minimum of 2.00. The Company’s fixed charges coverage ratio at December 31, 2009 was 4.77.

The final covenant on funded debt to consolidated cash flow allows for a maximum level of 4.00. At

December 31, 2009, the Company’s actual level was 2.91. The Note Agreement for the Series B and

Series C Notes also contains customary representations and warranties and events of default.

At December 31, 2009, the Company was in compliance with all covenants in the Series B and Series C

Notes and the Facility.

In addition, the Company and a syndicate of lenders have entered into a $35 million unsecured

revolving line of credit (the “Facility”) which was most recently renewed on April 10, 2009. The

Facility bears interest at a rate of LIBOR plus 2.00% or at a base rate. At December 31, 2009,

there were no

borrowings under the Facility and $35 million of credit was available pursuant to the terms of the

Facility. The Facility has a maturity date of April 9, 2010. The Company expects to renew the

Facility on similar terms, as it has for each of the past nine years.

17

Table of Contents

On July 31, 2009, the Company and the syndicate of lenders participating in the Facility entered

into Amendment No. 1 to the Facility. This amendment, effective as of the date of execution,

modified the covenant on maximum indebtedness to EBITDA by deleting that covenant and substituting

in its place a covenant on minimum EBITDA. In addition, the lenders and the Company agreed to

modify the definition of EBITDA for this covenant by now allowing the Company to add back non-cash

charges to EBITDA.

The Facility also contains certain financial covenants which (a) require a minimum amount of

modified EBITDA and (b) require a minimum fixed charge coverage ratio of 1.7x. At December 31,

2009, the Company was in compliance with the minimum modified EBITDA and had a fixed charge

coverage ratio of 6.47x. The Facility also contains customary representations and warranties and

events of default.

During 2009, the Company applied $13.9 million of cash toward capital expenditures. These

expenditures were funded by cash from operations.

In 2008, the Company issued 1,301,961 shares of common stock in connection with the acquisitions of

Aerex and Chen-Tech.

During the years ending December 31, 2008 and 2009, the Company received $0.215 million and $0.015

million, respectively, from the exercise of employee stock options.

Given the Company’s ability to pass along raw material price increases to its customers,

inflation has not had a material effect upon the Company during the period covered by this report.

Given the rising demand for the products manufactured by the Company, and the prospects for

increases in raw material costs and possible energy cost escalation, the Company cannot determine

at this time if there will be any significant impact from inflation in the foreseeable future.

Contractual

Obligations Table

(Dollars in Millions)

(Dollars in Millions)

| Less Than | More Than | |||||||||||||||

| 1 Year | 1-3 Years | 3-5 Years | 5 Years | |||||||||||||

Senior Notes (1) |

$ | 5.715 | $ | 31.430 | $ | 31.430 | $ | 21.425 | ||||||||

Bank Facility |

— | — | — | — | ||||||||||||

Operating Leases |

.974 | 1.592 | 1.239 | 1.848 | ||||||||||||

Purchase Obligations (2) |

61.438 | 101.602 | — | — | ||||||||||||

Other Long-Term Obligations: |

||||||||||||||||

Pensions (3) |

7.456 | 26.806 | — | — | ||||||||||||

Postretirement Benefits (4) |

3.464 | 6.737 | 6.262 | 13.137 | ||||||||||||

| (1) | The Company expects to fund the payment of long-term debt through the

use of cash on hand, cash generated from operations, the reduction of working capital

and, if necessary, through access to the Facility. |

|

| (2) | The purchase obligations relate primarily to raw material purchase orders

necessary to fulfill the Company’s production backlog for the Company’s products

along with commitments for energy supplies also necessary to fulfill the Company’s

production backlog. There are no net settlement provisions under any of these

purchase orders nor is there any market for the underlying materials. |

|

| (3) | The Company’s estimated cash pension contribution is based upon the

calculation of the Company’s independent actuary for 2010. There are no estimates

beyond 2012. |

|

| (4) | The Company’s cash expenditures for Postretirement Benefits have only been

projected out through the year 2019. |

18

Table of Contents

Critical Accounting Policies

Deferred Income Taxes

The Company started 2008 with $2.1 million of domestic net operating loss (“NOL”) carryforwards

that were generated prior to its reorganization completed on April 30, 1993. These NOLs were

utilized by the Company to reduce taxable income in 2008. The Company has $3.7 million of NOL

carryforwards that were generated by its foreign operations in 2008 and 2009. These NOLs expire in

the years 2012 through 2014. The Company has total net deferred income tax assets of $31.7 million

as of December 31, 2009.

Pensions

The Company has noncontributory defined benefit pension plans (“Plans”) covering a number of its

employees. The Company contributed $8.955 million and $3.428 million, respectively, to the Plans

in 2008 and 2009. The Company intends to contribute $7.5 million, $11.8 million and $15 million to

the Plans in 2010, 2011 and 2012, respectively. The Company plans on funding those contributions

from cash on hand, cash generated from operations, working capital reductions, treasury stock

contributions and, if necessary, from the Facility. No estimates have been made for payments into

the Plans beyond 2012.

The Plans’ assets are held in a trust and are primarily invested in U.S. Government securities,

investment grade corporate bonds and marketable common stocks. The key assumptions the Company

considers with respect to the assets in the Plans and funding the liabilities associated with the

Plans are the discount rate, the long-term rate of return on Plans’ assets, the projected rate of

increase in compensation levels and the actuarial estimate of mortality of participants in the

Plans. The most sensitive assumption is the discount rate. For funding purposes, the Company’s

independent actuaries assumed an annual long-term rate of return on the Plans’ assets of 7.95% and

8.05% for 2008 and 2009, respectively. For the ten-year period ending December 31, 2009, the

Company experienced an annual rate of return on the Plans’ assets of 3.31%.

The Company used a rate of 5.16% for its discount rate assumption for 2009, a decrease from the

6.05% rate used for 2008. An increase in the discount rate results in a decrease in the

accumulated benefit obligation at the measurement date which may also result in a decrease in the

additional minimum pension liability included as a credit to accumulated other comprehensive

income. Such an increase also results in an actuarial gain which is amortized to pension expense

in accordance with FASB ASC 715-30. A decrease in the discount rate will have the opposite effect

in the pension liability and pension expense. The Company bases its discount rate on long maturity

AA rated corporate debt securities. The Company cannot predict whether these interest rates will

increase or decrease in future years.

The Company cannot predict the level of interest rates in the future and correspondingly cannot

predict the future discount rate which will be applied to determine the Company’s projected benefit

obligation. As demonstrated in the chart below, relatively small movements in the discount rate,

up or down, can have a significant impact on the Company’s projected benefit obligation under the

Plans.

| Projected Plan Benefit Obligation as of December 31, 2009 | ||||

| (Dollars in Millions) | ||||

At 4.91% discount rate |

$ | 225.019 | ||

At 5.16% discount rate |

$ | 219.756 | ||

At 5.41% discount rate |

$ | 214.709 | ||

19

Table of Contents

Nor can the Company predict with any certainty what the actual rate of return will be for the

Plans’ assets. As demonstrated in the chart below, a modest change in the presumed rate of return

on the Plans’ assets will have a material impact upon the actual net periodic cost for the Plans.

| Net Periodic Benefit for Year Ending December 31, 2010 | ||||

| (Dollars in Millions) | ||||

7.80% expected return |

$ | 9.334 | ||

8.05% expected return |

$ | 8.954 | ||

8.30% expected return |

$ | 8.573 | ||

Fair Value Measurement of Pension Assets

FASB ASC 820-10, Fair Value Measurements and Disclosures, establishes a framework and provides

guidance on measuring the fair value of assets in a pension plan and how an employer should

disclose the same. The framework establishes a fair value hierarchy that prioritizes the inputs to

the valuation techniques used to measure fair value. The three levels of fair value hierarchy are

described as follows:

| Level 1 | Quoted prices in active markets for identical assets or liabilities. |

||

| Level 2 | Observable inputs other than Level 1 prices, such as quoted prices

for similar assets or liabilities; quoted prices in markets that

are not active; or other inputs that are observable or can be

corroborated by observable market data for substantially the full

term of the assets or liabilities. |

||

| Level 3 | Unobservable inputs that are supported by little or no market

activity and that are significant to the fair value of the assets

or liabilities. |

The following table sets forth by level (dollars in millions), within the fair value hierarchy, the

Plans’ assets at fair value as of December 31, 2009:

| Plans’ Assets | Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| $ | 142.967 |

$ | 142.967 | — | — | $ | 142.967 | ||||||||||

Goodwill and Other Intangible Assets

Goodwill represents the cost of acquired net assets in excess of their fair market values.

Goodwill and other intangible assets with indefinite useful lives are not amortized but are tested

for impairment at least annually in accordance with the provisions of FASB ASC 350-20, Intangibles

— Goodwill and Other. Intangible assets with estimable useful lives are amortized over their

respective estimated useful lives and also reviewed at least annually for impairment.

In accordance with ASC 350-20, a two-step impairment test is required to identify potential

goodwill impairment and measure the amount of the goodwill impairment loss to be recognized. In

the first step, the fair value of each reporting unit is compared to its carrying value to

determine if the goodwill is impaired. If the fair value of the reporting unit exceeds the

carrying value of the net assets assigned to that unit, then goodwill is not impaired and the

second step is not required. If the carrying value of the net assets assigned to the reporting

unit exceeds its fair value, then the second step is performed in order to determine the implied

fair value of the reporting unit’s goodwill and an impairment loss is recorded for an amount equal

to the difference between the implied fair value and the carrying value of the goodwill.

20

Table of Contents

For the purpose of goodwill analysis, the Company has only one reporting segment, as defined by ASC

350-20. Goodwill of $37.6 million represents the excess of the purchase price over the fair value

of identifiable tangible and intangible net assets relating to business acquisitions. Goodwill

increased significantly in 2008 due to the acquisitions of Aerex and Chen-Tech. It is an asset

with an indefinite life

and therefore is not amortized to expense, but is subject to annual impairment testing. The

Company tests the goodwill for impairment at least annually by fair value impairment testing. The

Company’s assessment of fair value used in the annual impairment testing takes into account a

number of factors including EBITDA and revenue multiples of transactions in the Company’s industry

as well as fair market value multiples of transactions of similarly situated enterprises. No

impairments were recognized in 2007, 2008 or 2009. Should goodwill become impaired in the future,

the amount of impairment will be charged to SG&A expense. The Company has $19.5 million of

amortizable customer relationships included in other intangible assets that are being amortized

over 50 years with annual amortization of $0.4 million.

New Accounting Pronouncements

Effective July 1, 2009, the Company adopted FASB ASC 105-10, Generally Accepted Accounting

Principles — Overall. ASC 105-10 establishes the FASB ASC as the source of authoritative

accounting principles recognized by the FASB to be applied in the preparation of financial

statements in conformity with U.S. generally accepted accounting principles (“GAAP”). The Company

has updated GAAP referencing for this report. The FASB Codification had no impact on financial

reporting of the Company.

In December 2007, the FASB issued guidance for accounting and reporting of noncontrolling interests

in financial statements, which is included in ASC 810-10, Consolidation — Overall. The objective

of ASC 810-10 is to improve the financial information provided in consolidated financial

statements. ASC 810-10 changes the way the consolidated income statement is presented, establishes

a single method of accounting for changes in a parent’s ownership interest in a subsidiary that do

not result in deconsolidation, requires that a parent recognize a gain or loss in net income when a

subsidiary is deconsolidated, and expands disclosures in the consolidated financial statements in

order to clearly identify and distinguish between the interests of the parent’s owners and the

interest of the noncontrolling owners of a subsidiary. The Company adopted ASC 810-10 effective

January 1, 2009. ASC 810-10 modified the manner in which the Company reported on the

noncontrolling interest in ZKM as the noncontrolling interest has been classified as a component of

equity.

On December 30, 2008, the FASB issued guidance related to employers’ disclosures regarding

postretirement benefit plan assets, which is included in ASC 715-20, Defined Benefit Plans —

General. ASC 715-20 provides additional guidance on employers’ disclosures about plan assets of a

defined benefit pension or other postretirement plan. The Company adopted ASC 715-20 in fiscal

year 2009. The disclosure requirements are annual and do not apply to interim financial

statements.

Effective June 30, 2009, the Company adopted FASB ASC 855-10, Subsequent Events — Overall. ASC

855-10 establishes standards for the accounting for and the disclosing of subsequent events. ASC

855-10 introduces new terminology, defines a date through which management must evaluate subsequent

events, and lists the circumstances under which an entity must recognize and disclose events or

transactions occurring after the balance sheet date.

The Company evaluated its December 31, 2009 financial statements for subsequent events through

March 4, 2010, the date the financial statements were available to be issued. The Company is not

aware of any subsequent events which would require recognition or disclosure in the financial

statements.

21

Table of Contents

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

The Company believes that its exposure to market risk related to changes in foreign currency

exchange rates and trade accounts receivable is immaterial.

Item 8. Financial Statements and Supplementary Data

The response to Item 8. Financial Statements and Supplementary Data incorporates by reference the

information listed in the consolidated financial statements and accompanying schedules beginning on

page F-1.

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial

Disclosure