Attached files

| file | filename |

|---|---|

| EX-32 - SECTION 903 CERTIFICATION OF CEO - Gentor Resources, Inc. | certification906ceo.htm |

| EX-31 - SECTION 302 CERTIFICATION OF CFO - Gentor Resources, Inc. | certification302cfo.htm |

| EX-32 - SECTION 903 CERTIFICATION OF CFO - Gentor Resources, Inc. | certification906cfo.htm |

| EX-31 - SECTION 302 CERTIFICATION OF CEO - Gentor Resources, Inc. | certification302ceo.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

or

o

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period form ____________________ to ____________________.

Commission file number 333-130386

GENTOR RESOURCES, INC.

---------------------------------------------------------------------

(Exact name of registrant as specified in its charter)

Florida -------------------- | 20-2679777 -------------------------- |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2289 Pahsimeroi Road

Patterson, Idaho 83253

-------------------------------------------

(Address of principal executive offices)(Zip Code)

(406) 287-3046

-----------------------

(Registrant=s telephone number, including area code)

1

Securities registered pursuant to Section 12(b) of the Act:

Title of each Class | Name of each exchange on which registered |

None | N/A |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such reports). YES o NO o

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K (Section 229.405) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of Alarger accelerated filer,@ Aaccelerated filer@ and Asmaller reporting company@ in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o |

Non-accelerated filed o | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES o NO x

2

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2009, was $10,088,430 (based upon the last reported sale price of $1.50 per Share of Common Stock as quoted on the OTC Bulletin Board on June 30, 2009).

As of the date hereof, there were 22,500,000 shares of the registrant's $0.0001 par value Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

3

TABLE OF CONTENTS

PART I.

Item 1.

Business.

Item 1A.

Risk Factors.

Item 1B.

Unresolved Staff Comments.

Item 2.

Properties.

Item 3.

Legal Proceedings.

Item 4.

Submission of Matters to a Vote of Security Holders.

PART II.

Item 5.

Market for Registrant=s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities.

Item 6.

Selected Financial Data.

Item 7.

Management's Discussion and Analysis of Financial Condition and Results of Operations.

Item 7A.

Quantitative and Qualitative Disclosure About Market Risk.

Item 8.

Financial Statements and Supplementary Data.

Item 9.

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure.

Item 9A.

Controls and Procedures.

Item 9B.

Other Information.

PART III.

Item 10.

Directors, Executive Officers, and Corporate Governance.

Item 11.

Executive Compensation.

Item 12.

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

Item 13.

Certain Relationships and Related Transactions, and Director Independence.

Item 14

Principal Accountant Fees and Services.

Item 15.

Exhibits, Financial Statements Schedules.

4

Cautionary Statement Regarding Forward-Looking Statements

The information provided in this Form 10-K (the AReport@) may contain Aforward looking@ statements or statements which arguably imply or suggest certain things about our future. Statements, which express that we Abelieve@, Aanticipate@, Aexpect@, Aintend to@ or Aplan to@, as well as, other similar expressions and/or statements which are not historical fact, are forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on assumptions that we believe are reasonable, but a number of factors and/or risks could cause our actual results to differ materially from those expressed or implied by these statements, including, but not limited to:

$

risks related to our properties being in the exploration stage

$

risks related to our limited operating history

$

risks related to mineral exploration and development activities

$

risks related to our title and rights in and to our mineral properties

$

risks related our mineral operations being subject to government regulation

$

risks related to the competitive industry of mineral exploration

$

risks related to our ability to obtain additional capital to develop our resources, if any

$

risks related to the fluctuation of prices for precious and base metals

$

risks related the possible dilution of our common stock from additional financing activities

$

risks related to our subsidiary activities

$

risks related to our shares of common stock

The foregoing list is not exhaustive of the factors that may affect our forward-looking statements and new risk factors may emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this Report. These forward-looking statements are based on our current expectations and are subject to a number of risks and uncertainties, including those set forth above. Although we believe that the expectations reflected in these forward-looking statements are reasonable, our actual results could differ materially from those expressed in these forward-looking statements, and any events anticipated in the forward-looking statements may not actually occur. Except as required by law, we undertake no duty to update any forward-looking statements after the date of this report to conform those statements to actual results or to reflect the occurrence of unanticipated events. Furthermore, any discussion of our financial condition and results of operation should be read in conjunction with the financial statements and the notes to the financial statements included elsewhere in this Report.

PART I.

Item 1.

Business.

In this report, references to Awe,@ Aus,@ Aour@ and/or the ACompany@ refer to Gentor Resources, Inc., a Florida corporation.

Background

We are a Florida corporation formed under the name of Gentor Resources, Inc. on March 24, 2005. We have one (1) wholly owned subsidiary, Gentor Idaho, Inc., an Idaho corporation (AGentor Idaho@), which was formed on June 28, 2007.

5

We are an exploration stage company (as such term is defined in Securities Act Industry Guide 7(a)(4)(i)) which means that we are engaged in the search for mineral deposits (reserves) which are not either in the development or production stage. Our corporate strategy is to create shareholder value by acquiring and developing highly prospective mineral properties in the United States and internationally.

Since our inception, we have acquired rights to mineral properties in (i) the state of Montana (the AMontana Project@), (ii) the state of Idaho (the AIdaho Project@) and (iii) the Nunavut Territory, which is located in the eastern Canadian Arctic (the ANunavut Project@). As of the date of this Report, we have terminated our rights to explore the Montana Project and the Nunavut Project, but we still maintain our rights to explore the Idaho Project, which is a molybdenum-tungsten project located in East-Central Idaho. For a more detailed description of the Idaho Project, please see the information contained in Part I, Item 2 of this Report in the section entitled AProperties.@

Registered Offering on Form SB-2

On November 13, 2006 (the AEffective Date@), the SEC declared our registration statement on Form SB-2 (the ARegistration Statement@) effective and assigned file number 333-130386 to the Registration Statement.

On November 14, 2006, we commenced an offering (the AOffering@) of up to 5,000,000 shares (after giving effect to the March 2007 Split, as such AMarch 2007 Stock Split@ is defined below) of our common stock, at a price per share of $0.20 (after giving effect to the March 2007 Split) of our common stock, for an aggregate Offering price of $1,000,000.

On November 16, 2006, the Company sold all 5,000,000 shares (after giving effect to the March 2007 Split) of our common stock and we received aggregate Offering proceeds of $1,000,000. All of the net Offering proceeds have been used in accordance with the disclosures set forth in (i) our Form 10Q-SB for the quarterly period ending September 30, 2006 which was filed with the SEC on December 29, 2006, (ii) our Form 10K-SB for the year ending December 31, 2006 which was filed with the SEC on April 17, 2007, (iii) our Form 10Q-SB for the quarterly period ending March 31, 2007 which was filed with the SEC on May 15, 2007, and (iv) our Form 10Q-SB for the quarterly period ending June 30, 2007 which was filed with the SEC on August 14, 2007.

Stock Split

On February 26, 2007, the board of director (the ABoard of Directors@) of the Company executed a written action by unanimous written consent of the directors in lieu of a special meeting of the directors (the AStock Split Director Action@) which authorized the Company to amend and restate its Articles of Incorporation to effectuate a 25 for 1 forward split (the AMarch 2007 Split@) of our common stock and increase the authorized shares of common stock from 1,500,000 to 37,500,000. The Stock Split Director Action was approved by the holders of a majority of our common stock at such time by a written action of the shareholders in lieu of a special meeting of the shareholders (the AStock Split Shareholder Action@) and on March 1, 2007, the Company filed its amended and restated articles of incorporation (the ARestated Articles@) which provided that upon the filing of the Restated Articles with the Secretary of State of the State of Florida, each one (1) share of the $0.0001 par value common stock of the Company outstanding as of the close of business on February 28, 2007 (the ARecord Date@) was to be divided into twenty five (25) shares of the $0.0001 par value common stock of the Company.

6

Amendment to The Restated Articles To Increase The Authorized Capital Stock of the Company

On August 24, 2009, the Board of Director of the Company executed a written action by unanimous written consent of the directors in lieu of a special meeting of the directors (the “Capital Stock Director Action”) which authorized the Company to amend the Restated Articles to increase the authorized capital stock of the Company.

On August 25, 2009, the Capital Stock Director Action was approved by a the holders of a majority of our common stock by a written action of the shareholders in lieu of a special meeting of the shareholders (the “Capital Stock Shareholder Action”) and on September 1, 2009, the Company filed the amendment (the “Amendment”) to the Restated Articles with the Secretary of State of the State of Florida. The Amendment was deemed to be effective upon its filing with the Secretary of State of the State of Florida.

Prior to effectiveness of the Amendment, the authorized capital stock of the Company consisted of Fifty Million (50,000,000) shares, of which (i) Thirty Seven Million Five Hundred Thousand (37,500,000) shares (each with a par value of $0.0001) were designated as common stock and (ii) Twelve Million Five Hundred Thousand (12,500,000) shares (each with a par value of $0.0001) were designated as preferred stock. After the effectiveness of the Amendment, which was on September 1, 2009, the authorized capital stock of the Company was increased such that the authorized capital stock of the Company now consists of One Hundred Fifty Million (150,000,000) shares, of which (i) One Hundred Million (100,000,000) shares (each with a par value of $0.0001) is a class designated as common stock and (ii) Fifty Million (50,000,000) shares (each with a par value of $0.0001) is a class designated as preferred stock.

Our Business

We are an exploration stage company (as such term is defined in Securities Act Industry Guide 7(a)(4)(i)) which means that we are engaged in the search for mineral deposits (reserves) which are not either in the development or production stage.

Mineral exploration is a research and development activity that does not produce a specific product. Successful exploration often results in increased project value that can be realized through the optioning or selling of the claimed site to larger companies. As such, we aim to acquire properties which we believe have potential to host economic concentrations of minerals, particularly gold, molybdenum, nickle and copper. These acquisitions have and may take the form of unpatented mining claims on federal land, or leasing claims, or private property owned by others.

The Idaho Project, the Company=s only current mineral property, is without known reserves and all of our exploration activities with respect to the Idaho Project to date have been exploratory in nature. There is no assurance that a “commercially viable” mineral deposit (that is, that the potential quantity of a mineral deposit and its market value would, after consideration of the costs and expenses that would be required to explore, develop and/or extract any such mineral deposit (if any), would justify a decision to do so) exists at the Idaho Project and further exploration beyond the scope of our planned exploration activities will be required before a final evaluation as to the economic feasibility of the mining of the Idaho Project can be determined. Moreover, there is no assurance that further exploration will result in a final evaluation that a commercially viable mineral deposit exists at the Idaho Project. We do not have sufficient financing to undertake the continued exploration of the Idaho Project at the present time and there is no assurance that we will be able to obtain the necessary financing. As such, we intend to raise additional capital and/or seek a joint venture partner to finance the further exploration of the Idaho Project.

If we are able to raise additional capital and/or attract and secure a joint venture partner who can provide the additional financing necessary to enable us to continue our exploration activities, we plan to continue

7

exploration of the Idaho Project for so long as the results of the geological exploration that we complete indicate that further exploration of the Idaho Project is recommended. All exploration activities at the Idaho Project which have been completed to date are preliminary exploration activities. Advanced exploration activities, including the completion of comprehensive infill drilling programs, will be necessary before we are able to complete any feasibility studies on the Idaho Project. If our exploration activities result in an indication that the Idaho Project contains potentially commercial exploitable quantities of minerals, then we would attempt to complete feasibility studies on such property to assess whether commercial exploitation of the property would be commercially feasible. There is no assurance that commercial exploitation of the Idaho Project would be commercially feasible even if our initial exploration programs show evidence of significant mineralization. If we determine not to proceed with further exploration of the Idaho Project due to results from geological exploration that indicate that further exploration is not recommended, then we will attempt to acquire additional interests in new mineral resource properties. There is no assurance that we will be able to acquire an interest in a new property that merits further exploration. If we were to acquire an interest in a new property, then our plan would be to conduct resource exploration of the new property, to the extent that we have available resources to conduct such exploration. In any event, we anticipate that our acquisition of a new property and any exploration activities that we would undertake will be subject to our achieving additional financing, of which there is no assurance.

From December 31, 2008 to the date of this Report, the Company has not undertaken any substantive exploration activities at the Idaho Project.

Competition

There is aggressive competition within the mineral exploration industry in connection with the discovery, acquisition and development of properties considered to have commercial potential. As a young mineral exploration stage company with a limited operating history, we compete with other startup and established mineral resource exploration companies for financing and for the acquisition of new mineral properties. Many of the mineral resource exploration companies with whom we compete have greater financial and technical resources than those available to us. Accordingly, our competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on the exploration of their mineral properties and on the development of their mineral properties. In addition, our competitors may be able to afford more geological expertise in the targeting and exploration of mineral properties. This competition could result in our competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration and development. This competition could adversely impact on our ability to achieve the financing necessary for us to conduct further exploration of the Idaho Project and/or other mineral properties which we may otherwise acquire.

We also compete with other startup and established mineral exploration companies for financing from a limited number of investors that are prepared to make investments in mineral exploration companies. The presence of these competing mineral exploration companies may adversely impact on our ability to raise additional capital in order to fund our exploration programs if investors are of the view that investments in competitors are more attractive based on the merit of the mineral properties under investigation and the price of the investment offered to investors.

In addition to the fact that there is aggressive competition within the mineral exploration industry, the mining industry, in general, is a speculative venture involving substantial risk that relies on numerous untested assumptions and variables. Many exploration programs do not result in the discovery of mineralization, and any mineralization discovered may not be of sufficient quantity or quality to be profitably mined. We are unable to provide any assurance that a ready market will exist for the sale of any mineralization which might otherwise be discovered and/or extracted from the Idaho Project and/or any

8

other mineral properties which we might otherwise acquire. Furthermore, similar to other mineral exploration companies, including our competitors, we are also subject to many unforeseen risks and expenses incident to exploring and developing mineral properties such as delays in governmental or environmental permitting, changes in the legislation governing the mining industry that might alter our ability to conduct our operations as planned, the availability of reasonably priced insurance products, unexpected construction costs necessary to create and maintain a production facility, and normal fluctuations in the general markets for the minerals and/or metals to be produced. These risks and expenses, while beyond our control, can materially adversely affect our business and cause our business to fail. Moreover, the search for valuable minerals involves numerous hazards and risks, such as cave-ins, environmental pollution liability, and personal injuries. We currently have no insurance against the risks of mineral exploration, and we do not expect to obtain any such insurance in the foreseeable future, other than the liability insurance which we might otherwise be contractually required to maintain. If we were to incur such a hazard or risk, the costs of overcoming same may exceed our ability to do so, in which event we could be required to liquidate all our assets and cease our business operations.

Government Regulations

General:

Any and all operations at Idaho Project will be subject to various federal and state laws and regulations in the United States which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters. We will be required to obtain those licenses, permits or other authorizations currently required to conduct exploration and other programs. There are no current orders relating to us and/or the Idaho Project with respect to the foregoing laws and regulations. If we escalate our exploration activities at the Idaho Project, it is reasonable to expect that compliance with various regulations will increase our costs. Such compliance may include feasibility studies on the impact of our proposed operations to land, water and biological resources, costs associated with minimizing surface impact, water treatment and protection, reclamation activities, including rehabilitation of various sites, on-going efforts at alleviating the mining impact on wildlife and permits or bonds as may be required to ensure our compliance with applicable regulations. It is possible that the costs and delays associated with such compliance could become so prohibitive that we may decide to not proceed with exploration, development, or mining operations on the Idaho Project. We are not presently aware of any specific material environmental constraints affecting our Idaho Project that would preclude the economic development or operation of the Idaho Project.

U.S. Federal Environmental Laws:

The U.S. Forest Service (the AUSFS@) and the U.S. Bureau of Land Management (the AUSBLM@) require that mining operations on lands subject to their respective regulations obtain an approved plan of operations that is subject to the Federal Land Policy Management Act, the Code of Federal Regulations and a review of environmental impacts under the National Environmental Policy Act. Any significant modifications to an approved plan of operations would require the submission of amendments and the completion of an environmental assessment or an Environmental Impact Statement prior to the approval of any such modification to a plan of operations. Generally, mining companies must post a bond or other surety to guarantee the cost of post mining reclamation. These requirements could add significant additional cost and delays to any mining project undertaken by us.

The U.S. Environmental Protection Agency administers the Clean Water Act. Any discharge of industrial waters or pollutants into any waters of the Unites States must be permitted under a National Pollution Discharge Elimination System (the ANPDES@) permit. Mining companies seeking to discharge mine or

9

mineral process water into waters of the United States must first obtain an NPDES permit, which may contain stipulations regarding water treatment and monitoring. These requirements could add significant additional cost and delays to any mining project undertaken by us.

Under the U.S. Resource Conservation and Recovery Act (the “RCRA”), mining companies may incur costs for generating, transporting, treating, storing, or disposing of hazardous waste, as well as for closure and post-closure maintenance once they have completed mining activities on a property. The Bevill exclusion to the RCRA excludes solid waste from the extraction, beneficiation, and processing of ores and minerals from regulation as hazardous waste under Subtitle C of the RCRA Any future mining operations at the Idaho Project may produce air emissions, including fugitive dust and other air pollutants, from stationary equipment, storage facilities, and the use of mobile sources such as trucks and heavy construction equipment which are subject to review, monitoring and/or control requirements under the Federal Clean Air Act and state air quality laws. Permitting rules may impose limitations on our production levels or create additional capital expenditures for pollution control in order to comply with the rules.

The U.S. Comprehensive Environmental Response Compensation and Liability Act of 1980, as amended, (ACERCLA@) also imposes strict joint and several liability on parties associated with releases or threats of releases of hazardous substances. Those liable groups include, among others, the current owners and operators of facilities which release hazardous substances into the environment and past owners and operators of properties who owned such properties at the time the disposal of the hazardous substances occurred. This liability could include the cost of removal or remediation of the release and damages for injury to the surrounding property. We cannot predict the potential for future CERCLA liability with respect to the Idaho Project or their respective surrounding areas.

Idaho Laws:

Mining in the State of Idaho is subject to federal, state and local law. Three types of laws are of particular importance to the Idaho Project are those affecting land ownership and mining rights, those regulating mining operations, and those dealing with environmental protection. Mineral exploration activities are not regulated by the State of Idaho. As such, we may conduct exploration activities on private properties without approval by any state government agency. However, activities that may impact streams or stream beds or banks are regulated by the Idaho Department of Environmental Quality. Therefore, in order to expand our exploration activities at the Idaho Project onto Federal land or across Patterson creek, we will be required to secure permits for bridging Patterson creek if the banks of the creek are to be disturbed, maintain approval to work on such Federal Lands from the USBLM, and secure and/or maintain any other authorizations required to conduct our exploration program.

Anticipated Costs and Effects of Compliance With Government Regulations

If we continue with our exploration activities at the Idaho Project, we anticipate that our primary near term cost of compliance with applicable environmental laws is likely to be less than $25,000. A bond in the amount of $10,000 is currently obligated for reclamation of exploration disturbances on the lands of the BLM. These costs will be primarily the costs of reclamation of disturbances on Federal Lands administered by the U.S. Bureau of Land Management and/or the U.S. Forest Service, and the provision of bonds to ensure that the reclamation is done to the satisfaction of the foregoing governmental agencies.

As of the date of this Report, our exploration activities with respect to the Idaho Project have been confined to private lands occupied by us under a lease/option to purchase agreement, as more specifically described below in Part I, Item 2 of this Report in the section entitled AProperties.@ Since out exploration activities have been confined to private lands, our operations do not require USBLM or USFS permits and are not governed by their regulations. In the event we expand our exploration activities, we have obtained

10

approval to drill additional holes on USBLM land on both sides of Patterson creek, but we have not yet accessed those sites. Access to these lands does require trespass on a USBLM administered public road. Permission by the USBLM to use this road has already been received by us. Our use of this road could result in a much higher than normal level of traffic. Higher levels of traffic could increase the potential for accidents, and could result in increased sediment being generated and possibly entering the adjacent Patterson Creek. To preclude these possibilities, the USBLM has granted us permission to conduct routine maintenance on this road, consisting of improving sight distances, constructing a cross fall away from the creek and surfacing the road where possible with rock to minimize erosion and filter sediment.

We anticipate a future need to discharge mine water to ground water on land controlled by us. Discharging mine water to groundwater requires compliance with the State of Idaho Ground Water Quality Rule which is administered by the Idaho Department of Environmental Quality. The rule does not in and of itself create a permit requirement, but it does stipulate required water quality standards which must be met. The U.S. Environmental Protection Agency (the “EPA”) does not regulate discharges to ground water but may require a demonstration that the discharge does not have a direct connection to surface water. A permit may be required from Lemhi County for the same. The U.S. Army Corps of Engineers has indicated that their approval for the project is not required. In order to meet the water quality standards established by the State of Idaho, a water treatment facility will have to be designed, constructed and operated in accordance with the instructions from the consulting engineers hired by us for these purposes.

Intellectual Property

We have not filed for any protection of our trademark for Gentor Resources. We own the copyright of all of the contents of our website, www.gentorresources.com, which we are currently developing.

Employees

We currently have zero (0) full-time employees and zero (0) part time employees. In addition, Lloyd J. Bardswich (a director and the president and treasurer of the Company), Kitt M. Dale (a director and the secretary of the Company) and Arnold T. Kondrat (a director and executive vice president of the Company) provide various engineering and management services on an as needed basis and are compensated for their respective services at standard industry rates.

Item 1A.

Risk Factors.

Since the Company is a Asmaller reporting company@ as defined by Rule 12b-2 of the Exchange Act, we are not required to provide the information required under this item.

Item 1B.

Unresolved Staff Comments.

None.

Item 2.

Properties.

Idaho Project

The Idaho Project is a molybdenum-tungsten project located in East-Central Idaho and is sometimes referred to herein as the AIMA Mine.@

11

Molybdenum is a refractory metal with very unique properties. Molybdenum, when added to plain carbon and low alloy steels, increases strength, corrosion resistance and high temperature properties of the alloy. The major applications of molybdenum containing plain and low alloy steels are automotive body panels, construction steel and oil and gas pipelines. When added to stainless steels, molybdenum imparts specialized corrosion resistance in severe corrosive environments while improving strength. The major applications of stainless steels are in industrial chemical process plants, desalinization plants, nuclear reactor cooling systems and environmental pollution abatement. When added to super alloy steels, molybdenum dramatically improves high temperature strength, creep resistance and resistance to oxidation in such applications as advanced aerospace engine critical components. The effects of molybdenum additions to steels are not readily duplicated by other elements and as such are not significantly impacted by substitution of other materials; as such, Molybdenum has few substitutes. Other uses for Molybdenum include fuel desulfurization catalysts, lubricants and alloy element in gas turbine engine components.

Location and Access

The IMA Mine is located on the western edge of Lemhi County in east Central Idaho, which is near the major communities of Salmon and Challis. U.S. Highway 93 runs between Salmon and Challis. Access to the IMA mine is obtained from Highway 93 as follows: At Mile Post 264 (which is approximately 18 miles North East of Challis), turn south on the paved Pahsimeroi Road (a.k.a. AFarm to Market Road@), then proceed southerly 24 miles to the Hamlet of Patterson, then turn East on the Patterson Creek Road (a 4x4 access road) and proceed for 1 mile to the IMA Mine.

Nature and Extent of the Company=s Rights to the Idaho Project

Effective as of March 1, 2007, Bardswich LLC, an Idaho limited liability company (ABardswich LLC@), an entity that is owned and controlled by Lloyd J. Bardswich, who is the president, treasurer, chief financial officer and a director of the Company, and IMA-1, LLC, a Montana limited liability company (the AIdaho Claim Owner@) entered into that certain Mineral Lease Agreement and Option to Purchase (the AIdaho Option Agreement@) which relates to twenty one (21) patented mining claims (the AIMA Mine@) located over approximately 376 acres of real property and four other parcels of approximately 216 acres in Lemhi County, Idaho (collectively, the AOptioned Properties@). In accordance with the terms of the Idaho Option Agreement, concurrently with the execution of the Idaho Option Agreement, Bardswich LLC paid the Idaho Claim Owner $40,000 in cash as the first Advanced Minimum Royalty Payment (as such term is defined herein).

On July 23, 2007, Bardswich LLC and Gentor Idaho entered into that certain assignment agreement (the AAssignment Agreement@) whereby Bardswich LLC assigned all of its rights, title and interest in and to the Idaho Option Agreement in exchange for $40,000 in cash and 500,000 shares of the Company=s common stock. The Idaho Option Agreement grants the Company (through Gentor Idaho) the exclusive right (the AExploration and Mineral Right@) to enter the Optioned Properties (and thus the IMA Mine) for the purpose of exploring and developing the Optioned Properties (and thus the IMA Mine), as well as, removing and selling for our own account any and all minerals, mineral substances, metals ore bearing materials and rocks of any kind. The Idaho Option Agreement also grants the Company an option (the AOption Right@) to purchase the Idaho Claim Owner=s rights to the Optioned Properties, including but not limited to the IMA Mine, for a total purchase price of $5,000,000 (the APurchase Price@), excluding therefrom the right of the Idaho Claim Owner to receive a three percent (3%) royalty on net revenue generated from the sale of any molybdenum, copper, lead, and zinc recovered from the IMA Mine and a five percent (5%) royalty on the net revenue generated from the sale of all other ores, minerals, or other products recovered from the Optioned Properties (collectively, the ANet Smelter Return Royalties@). The duration of the Idaho Option Agreement is indefinite so long as the Company makes the necessary scheduled payments of advanced minimum royalty payments (each an AAdvanced Minimum Royalty

12

Payment@) under the Idaho Option Agreement. Bardswich LLC made an initial payment of $40,000 in cash to the Idaho Claim Owner upon execution of the Idaho Option Agreement and the Company made an additional payment of $60,000 to the Idaho Claim Owner on the six month anniversary date of the signing of the original Option Agreement as well as another additional payment of $100,000 during the month of March 2008. According to the terms of the Idaho Option Agreement, additional payments of: (i) $100,000 in cash was due on or before the second anniversary of the Idaho Option Agreement (March 1, 2009), (ii) $100,000 in cash is due on or before the third anniversary of the Idaho Option Agreement (March 1, 2010), (iii) $200,000 in cash is due on or before the fourth anniversary date of the Idaho Option Agreement (March 1, 2011), and (iv) $200,000 in cash is due on or before each subsequent anniversary date of the Idaho Option Agreement thereafter until the Purchase Price is paid or the Idaho Option Agreement is terminated or cancelled. However, on March 1, 2009 (the second anniversary date of the Idaho Option Agreement), the Idaho Claim Owner agreed to accept four equal payments of $25,000 each on each of March 1, May 1, July 1, and September 1, 2009 in lieu of the $100,000 payment that was due in full on March 1, 2009. The $25,000 payments that were due, respectively, on March 1, 2009, May 1, 2009, July 1, 2009 and September 1, 2009 have been paid to the Idaho Claim Owner. Similarly, on February 14, 2010, the Idaho Claim Owner agreed to accept four equal payments of $25,000 each on each of March 1, May 1, July 1, and September 1, 2010 in lieu of the $100,000 payment that would be due in full on March 1, 2010 (the third anniversary date of the Idaho Option Agreement). The $25,000 payment that was due on March 1, 2010 has not yet been paid to the Idaho Claim Owner. In the event the Idaho Claim Owner notifies the Company in writing that the $25,000 payment has not been paid, then the Company has 20 days to cure such breach, and if the Company cannot cure such breach within the foregoing 20 day period, then the Idaho Claim Owner can terminate the Idaho Option Agreement. Even though the Idaho Claim Owner has not yet provided the Company with a written notice of default, the Company intends to pay the $25,000 payment as soon as possible and anticipates that such payment will be made to the Idaho Claim Owner before the end of June 2010. To the extent that the Company makes any Advanced Minimum Royalty Payments, the Company is entitled to receive a corresponding credit against any required Net Smelter Returns Royalties that are otherwise required to be paid to the Idaho Claim Owner under the Idaho Option Agreement. Moreover, the Company is also entitled to receive a credit equal to all Advanced Minimum Royalty Payments and payments of Net Smelter Return Royalties against the Purchase Price. In the event the Idaho Claim Owner notifies the Company that the Company has breached a term, condition or covenant of the Idaho Option Agreement (other than the payment of monies due and payable under the Idaho Option Agreement), then the Company has at least sixty (60) days (twenty (20) days for any monetary payment obligation) to cure any such breach. If the Company cannot cure, or begin to cure, any such breach within the cure period, then the Idaho Claim Owner can terminate the Idaho Option Agreement. The Company also has (i) the right to terminate the Idaho Option Agreement at any time and (ii) the right to assign all or any portion of the Idaho Option Agreement to any third party.

Also, on July 3, 2007, the Company (through Gentor Idaho, its wholly owned subsidiary) acquired fee simple title to a 75 acre parcel of land (the A75 Acre Parcel@) located in Lemhi County, Idaho from Richard Bergeman and Victoria Bergeman for a purchase price of $169,000. The 75 Acre Parcel also includes 72 miner=s inches of water rights. At or around the same time that the Company, through Gentor Idaho, acquired the 75 Acre Parcel, through a staking program, the Company also acquired 114 lode claims and 5 placer claims on federal lands (Athe Staked Claims@) located in Lemhi County, Idaho. The Company is required to pay $16,660 per annum ($140 per Staked Claim) on or before September 1st each year to the United States Department of the Interior, Bureau of Land Management, in order to retain the Staked Claims. However, on September 1, 2009, and in order to conserve working capital, the Company decided to pay $9,940 to United States Department of the Interior, Bureau of Land Management to retain 3 of the 5 placer claims and 68 of the 114 lode claims. In June 2009, the 75 Acre Parcel was sold for $169,000 to a vendor (the “Buyer”) in exchange for a reduction in accounts payable that the Company owed this vendor. However, in connection with the sale of the 75 Acre Parcel to the Buyer, the Company was granted (1) a 10-day right of first refusal to purchase the 75 Acre Parcel in the event the Buyer received a bona-fide offer

13

to sell said property and (2) an option to repurchase the 75 Acre Parcel for a purchase price of $169,000 at any time before or on December 31, 2010.

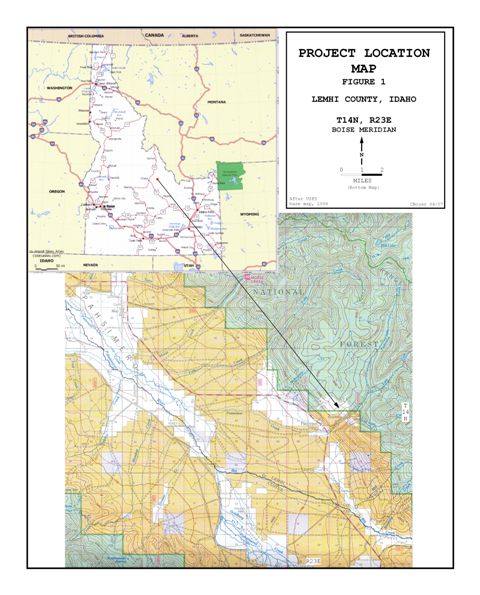

Map

Below is a map of the location of the IMA Mine.

History of Operations

The IMA Mine related to an underground mining operation that closed in 1957. Prior to its closure, the IMA Mine was the fifth largest United Stated producer of tungsten, having mined over 500,000 tons of ore between 1937 and 1952. The lowest level of the IMA Mine intersected the top of a molybdenum-bearing intrusive. From 1978 to 1981, Inspiration Development Corporation (AInspiration@), a subsidiary of Anglo-American Corporation, entered into agreements relating to the Optioned Properties in 1978 and spent Two Million Dollars ($2,000,000.00) on the Optioned Properties to ascertain the commercial viability of the tungsten potential. The work performed by Inspiration included (i) a drilling program from underground and the surface, (ii) rehabilitation of the AD@ level of the IMA Mine and (iii) completion of basic underground development for extraction of the tungsten ore.

Present Condition of the IMA Mine

We have entered into the D level and the Zero level of the IMA Mine. The D level is in good condition and the Zero Level is in poor to fair condition. The estimated costs to secure the safety of both levels to the extent necessary to satisfy general Mine Safety and Health Administration (the AMSHA@) regulations have not yet been determined. Access to the lowest level (-375) is blocked by fill. We have not attempted to enter the -375 level due to the costs anticipated and due to the fact that there is water discharging from the lower level which we believe contains metals slightly in excess of allowable limits permitted by the EPA and will require treatment to meet the allowable limits. Therefore, we do not intend to enter the -375 level and incur any liability for this water discharge until such time that we ascertain the economic merits of the property and the costs of the necessary water treatment.

Work Completed by the Company at the IMA Mine

We rehabilitated an old building of approximately 3,000 square feet on the IMA Mine-site and are presently using it for storage of materials.

We engaged contractors to drill water wells, construct water and septic sewer systems and install electrical power to both the 75 Acre Parcel and one of the valley parcels of land.

We have completed construction of a 1,000 square foot office building and a 2,000 square foot shop for core logging and sawing on one of the valley parcels of land. We were able to occupy the foregoing structure on or around March 1, 2008.

We have improved the access roads to the Zero level and the D level and have constructed drill sites and sumps.

Current State of Exploration and/or Development of the IMA Mine

As of the date of this Report, ten (10) holes have been completed.

14

Company=s Proposed Plan of Exploration and/or Development of the IMA Mine

The IMA Mine is without known reserves and our proposed exploration program is exploratory in nature.

As of the date of this Report, no material exploration activities are being conducted at Idaho Project. We intend to raise additional capital and/or seek a joint venture partner to finance the further exploration of the potentially large molybdenum bearing intrusive located below the existing mine workings of the Idaho Project. However, there is no assurance that we will be able to raise any additional capital and/or find a joint venture partner who can provide the necessary capital and/or financing. Moreover, we cannot provide any assurance that the exploration, development and/or extraction of tungsten or molybdenum would prove to be ACommercially Viable@, that is, that the potential quantity of tungsten or molybdenum and their market value would, after consideration of the costs and expenses that would be required to explore, develop and/or extract any such tungsten or molybdenum deposits (if any), would justify a decision to do so.

We have previously engaged the consulting services of Wardrop Engineering, Inc. of Toronto, Canada (AWardrop@) to review the available data on the IMA Mine and to recommend an exploration program. Based on the Wardrop recommendation, in July of 2007, we commenced a two (2) phase exploration program of the IMA Mine to assess whether any Commercially Viable tungsten or molybdenum bearing mineral deposits are present. Phase 1 of our exploration program generally consisted of surface exploration drilling and Phase 2 of our exploration program generally consisted of the same. We have completed Phase 1 and Phase 2 of our exploration program, and based on the results, data and analysis derived therefrom, we believe it is prudent to continue our exploration of the IMA Mine and we intend to commence a Phase 3 exploration program of the IMA Mine as soon as we can obtain the additional financing necessary to enable us to continue such exploration; however, there is no assurance that we will be able to obtain the necessary financing and/or commence Phase 3 of exploration program. Moreover, we may, prior to the commencement (if at all) and/or completion of Phase 3 of our exploration program, determine that Commercially Viable tungsten or molybdenum deposits do not exist within the IMA Mine, in which event we anticipate that we will terminate our proposed Phase 3 exploration program. Even if we commence and complete Phase 3 of our exploration program, we may not be able to determine if Commercially Viable tungsten or molybdenum deposits exist within the IMA Mine or if additional exploration is required to make such determination.

Plant and Equipment

Since our inception, we have purchased two (2) diamond saws for core cutting, two (2) all-terrain-vehicles for off road transport, three (3) used travel trailers for temporary living space and a bulldozer for road maintenance and snow removal. During the 2009 calendar year, we sold one (1) of the three (3) travel trailers and one (1) of the all-terrain-vehicles.

Geology and Mineralization

The IMA Mine was a producer of tungsten and closed in 1957. The tungsten was contained in quartz veins in metamorphosed sedimentary rocks. The lower levels of the mine intersected a granitic intrusive stock which was covered by the over-lying metamorphosed sedimentary rocks, Molybdenum occurs as disseminations and within quartz veins in the granite. In addition, tungsten, silver, copper, lead and zinc are also present in the intrusive itself and in the quartz veins.

15

Item 3.

Legal Proceedings.

Except as set forth below, there are no pending or threatened legal proceedings to which we are a party or of which any of our property is the subject, or to our knowledge, any proceedings contemplated by governmental authorities.

(i)

During the first quarter of 2009, the Company received a letter from counsel to Joe Antoshkiw, the owner of the Nunavut Project. The letter alleged a claim against the Company and CRVD Inco Limited in connection with that certain Assignment and Novation Agreement (the ANunavut Assignment Agreement@) and proposed a monetary settlement in the amount of $50,000 in return of a release of claims by Antoshkiw against the Company and CRVD Inco Limited. The Company has resolved the foregoing dispute and no further action has been taken against the Company.

Item 4.

Submission of Matters to a Vote of Security Holders.

None.

PART II

Item 5.

Market for Registrant=s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

As of October 9, 2007, our common stock has been quoted on the over-the-counter bulletin board (the AOTCBB@) under the symbol AGNTO@. Prior to October 9, 2007, there was no public trading market for our common stock.

The following table set forth below lists the range of high and low bids for our common stock for each fiscal quarter for the last two fiscal years as reported by OTCBB. The prices in the table reflect inter-dealer prices, without retail markup, markdown or commission and may not represent actual transactions.

Year | Quarter | High | Low |

2007 | Fourth Quarter (1) | $2.10 | $0.50 |

2008 | First Quarter | $3.05 | $1.10 |

2008 | Second Quarter | $2.20 | $1.25 |

2008 | Third Quarter | $1.75 | $1.75 |

2008 | Fourth Quarter | $1.75 | $1.26 |

2009 | First Quarter | $1.75 | $1.01 |

2009 | Second Quarter | n/a | n/a |

2009 | Third Quarter | $1.01 | $1.01 |

2009 | Fourth Quarter | $1.02 | $1.02 |

2010 | First Quarter | n/a | n/a |

(1) Our common stock began to be quoted on the OTCBB on October 9, 2007.

16

Although our common stock is quoted on the OTCBB, there is a limited public market for our common stock and no assurance can be given that an active market will develop or that a stockholder will ever be able to liquidate its shares of common stock without considerable delay, if at all. The OTCBB is not a stock exchange and trading of securities on the OTCBB is often more sporadic than the trading of securities listed on exchanges like NASDAQ or the New York Stock Exchange. Many brokerage firms may not be willing to effect transactions in our securities. Even if a purchaser finds a broker willing to effect a transaction in these securities, the combination of brokerage commissions, state transfer taxes, if any, and any other selling costs may exceed the selling price. Furthermore, our stock price may be impacted by factors that are unrelated or disproportionate to our operating performance. These market fluctuations, as well as general economic, political and market conditions, such as recessions, interest rates or international currency fluctuations may adversely affect the market price and liquidity of our common stock.

Our common stock is currently considered a penny stock. Broker-dealer practices in connection with transactions in Apenny stocks@ are regulated by certain penny stock rules adopted by the Securities and Exchange Commission. Penny stocks generally are equity securities with a price of less than $5.00 (other than securities registered on certain national securities exchanges or quoted on the NASDAQ system). Penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document that provides information about penny stocks and the risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction, and monthly account statements showing the market value of each penny stock held in the customer's account. The broker-dealer must also make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction. These requirements may have the effect of reducing the level of trading activity, if any, in the secondary market for a security that becomes subject to the penny stock rules.

Holders

As of the date of this Report, there were approximately eighty (80) holders of record of our common stock.

Dividends

We have never declared or paid any cash dividends on our capital stock and do not anticipate paying any cash dividends on our capital stock in the foreseeable future. Future dividends, if any, will be determined by our Board of Directors. In addition, we may incur indebtedness in the future which may prohibit or effectively restrict the payment of dividends, although we have no current plans to do so.

Equity Compensation Plans

As of the date of this Report, the Company does not maintain any equity based compensation plans for its directors, officers, employees and/or independent consultants (if any).

Recent Sales of Unregistered Securities

None.

Item 6.

Selected Financial Data.

Since the Company is a Asmaller reporting company@ as defined by Rule 12b-2 of the Exchange Act, we are not required to provide the information required under this item.

17

Item 7.

Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion of our financial condition and results of operations constitutes management=s review of the factors that affected our financial performance for the twelve month period ended December 31, 2009 and December 31, 2008. This discussion is intended to further the reader=s understanding of the consolidated financial condition and results of operations of our Company. This discussion should be read in conjunction with the consolidated financial statements and notes thereto contained elsewhere in this report. These historical financial statements may not be indicative of our future performance.

Overview

As previously stated in this Report, we are an exploration stage company (as such term is defined in Securities Act Industry Guide 7(a)(4)(i)), which means that we are engaged in the search for mineral deposits (reserves) which are not either in the development or production stage. Our corporate strategy is to create shareholder value by acquiring and developing highly prospective mineral properties in the United States and internationally. As such, we aim to acquire properties which we believe have potential to host economic concentrations of minerals, particularly gold, molybdenum, nickel and copper.

Since our inception, we have acquired rights to the Montana Project, the Idaho Project and the Nunavut Project. As of the date of this Report, we have terminated our rights to explore the Montana Project and the Nunavut Project, but we still maintain our rights to explore the Idaho Project, which is a molybdenum-tungsten project located in East-Central Idaho.

Results of Operations

Since our inception on March 24, 2005, we have been classified as an Aexploration stage company@ (as such term is defined in Securities Act Industry Guide 7(a)(4)(i)) with no producing mines and, accordingly, we do not produce income and have not generated any revenue.

Our net loss for the twelve months ended December 31, 2009 was $564,947 as compared to a net loss of $3,189,473 for the twelve months ended December 31, 2008. The foregoing decrease in net losses is attributable primarily to the lack of any substantive exploration activity undertaken by the Company during the twelve months ended December 31, 2009.

Since essentially no exploration activities were undertaken during the twelve months ended December 31, 2009, we did not spend any substantive monies in connection with the exploration and evaluation of the Idaho Project during such time period. Even though we did not undertake any substantive exploration activities during the 2009 calendar year, we did incur corporate and administrative costs of $310,164 for the twelve months ended December 31, 2009 compared to $418,125 for the twelve months ended December 31, 2008, which is consistent with our significantly decreased activity levels. These costs include general office expense, general legal expenses, and accounting and compliance costs.

Depreciation costs for the twelve months ended December 31, 2009 was $109,505, compared to $110,176 of deprecation costs for the twelve months ended December 31, 2008. Since the Company did not undertake any substantive exploration activity during the twelve months ended December 31, 2009, the depreciation costs for twelve months ended December 31, 2009 were consistent and in-line with the depreciation costs for the twelve months ended December 31, 2008.

18

Liquidity and Capital Resources

As of the date of this Report, we do not have sufficient financing to undertake full exploration of the Idaho Project and there is no assurance that we will be able to obtain the necessary financing.

Our cash balance at December 31, 2009 was $17,547, compared to $8,502 as at December 31, 2008. Total assets at December 31, 2009 were $385,872 compared to $717,624 as at December 31, 2008. The change in these balances reflects the write down of a drill deposit and the sale of a 75 acre parcel of land located in Lemhi County, Idaho (see Notes 4 and 5 of the Condensed Consolidated Financial Statements included in this Report).

Current liabilities at December 31, 2009 were $2,304,543 compared to $2,035,341 as at December 31, 2008. This increase in current liabilities is the result of the nonpayment of accounts payable and further indicates that we believe that we will need to obtain additional financing in order to continue our exploration program.

As of the date of this Report, we intend to concentrate our available resources towards the exploration of the Idaho Project. In late July of 2007, we commenced a two (2) phase exploration program recommended by Wardrop, the Company’s consultant, in order to test for the potential of a large scale molybdenum deposit being present under the IMA Mine located at the Idaho Project. Phase 1 of our drilling program consisted of drilling five (5) core holes from surface totaling 7,200 feet in order to substantiate prior work and to test continuity along a 1,000 foot strike length. Due to frequent breakdowns of the contractor's equipment, our Phase 1 drilling program fell behind schedule. However, despite the delays during the Phase 1 drilling program, an inspection of the drill core from the first hole revealed visible molybdenum sulphide, and based on the foregoing preliminary finding, we decided to engage the services of a second drill contractor to commence Phase 2 of the drill program. Phase 2 of our drilling program consisted of drilling an additional five (5) core holes from the surface and cost approximately $2,500,000 to complete. As of the date of this Report, we have completed Phase 1 and Phase 2 of our exploration program, and based on the results, data and analysis derived therefrom, we believe it is prudent to continue our exploration of the IMA Mine and we intend to commence a Phase 3 exploration program of the Idaho Project when and if we can obtain the additional financing necessary to enable us to continue such exploration. We believe that it will cost approximately $1,000,000 to complete a revised Phase 3 exploration program; however, there is no assurance that we will be able to obtain the necessary financing and/or commence a revised Phase 3 of exploration program. Furthermore, even if were able to commence and complete a revised Phase 3 of our exploration program, we may not be able to determine if Commercially Viable tungsten or molybdenum deposits exist within the IMA Mine or if additional exploration is required to make such determination.

Furthermore, we anticipate that the Company will also require additional capital to continue payment of ongoing general, administrative and operations costs associated with supporting its planned operations, the amounts of which are presently unknown. If the Company is unable to raise sufficient quantities of capital when needed, it will be necessary to develop alternative plans that would likely delay the exploration of the Idaho Project. There is no assurance that we will be able to obtain the necessary financing for the Idaho Project on customary terms, or at all.

Going Concern

We believe that we will require a minimum of approximately $425,000 to meet our capital requirements of the next twelve months for the following estimated expenses: (i) $100,000 to maintain our rights to the Idaho Project and (ii) $325,000 for general and administrative expenses, which includes legal fees and

19

audit fees. Since our cash balance at December 31, 2009 was $17,957, we currently do not have enough cash to satisfy our minimum cash requirements for the next twelve months.

In addition to our minimum capital requirements for the next twelve months, we also believe that we will also require (i) approximately $1,000,000 to commence and complete a revised Phase 3 exploration program of the Idaho Project (of the foregoing amount, we intend to use approximately $900,000 for drilling expenses and $100,000 for geological studies expenses) and (ii) approximately $2,300,000 to discharge and/or reduce our current liabilities.

Our ability to continue as a going concern is dependent on our ability to raise additional capital and/or find a joint venture partner. We are currently seeking equity and/or debt financing, and/or a joint venture partner, to provide the requisite capital to meet our minimum capital requirements. We currently do not have any financing arrangements in place and there are no assurances that we will be able to obtain additional financing in an amount sufficient to meet our needs or on terms that are acceptable to us. If financing in the short term is not available to us on satisfactory terms, we may be forced to cease our operations and this result would have material adverse effect on our business, results of operations and financial condition, and could ultimately cause our business to fail. If we raise funds through equity or convertible securities, our existing stockholders may experience dilution and our stock price may decline.

Due to the uncertainty of our ability to meet our current operating and capital expenses, our recurring net losses and negative cash flows from operations, our independent auditors have included an explanatory paragraph in their audit report concerning these matters which raise substantial doubt about the Company=s ability to continue as a going concern. The financial statements do not include any adjustments that might be necessary if we are unable to continue as a going concern.

Off Balance Sheet Arrangements

We have no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to stockholders.

Item 7A.

Quantitative and Qualitative Disclosure About Market Risk.

Since the Company is a Asmaller reporting company@ as defined by Rule 12b-2 of the Exchange Act, we are not required to provide the information required under this item.

Item 8.

Financial Statements and Supplementary Data.

GENTOR RESOURCES, INC.

Consolidated Financial Statements

December 31, 2009 and 2008

Contents

| Page(s) |

Consolidated Balance Sheets | 22 |

Consolidated Statements of Operations | 23 |

Consolidated Statements of Cash Flows | 24-25 |

Consolidated Statements of Shareholders= Equity (Deficiency) | 26-27 |

Notes to the Consolidated Financial Statements | 27-36 |

20

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Directors and Shareholders of

Gentor Resources, Inc.

(An Exploration Stage Company)

We have audited the accompanying consolidated balance sheets of Gentor Resources, Inc. (an exploration stage company) as at December 31, 2009 and 2008 and the related consolidated statements of operations, shareholders’ equity (deficiency) and cash flows for the year ended December 31, 2009, for the year ended December 31, 2008 and for the period from March 24, 2005 (date of inception) to December 31, 2009. These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the consolidated financial statements and assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Gentor Resources, Inc. (an exploration stage company) as at December 31, 2009 and 2008 and the results of its operations and its cash flows for the year ended December 31, 2009, the year ended December 31, 2008 and for the period from March 24, 2005 (date of inception) to December 31, 2009 in conformity with accounting principles generally accepted in the United States of America.

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the consolidated financial statements, the Company has suffered recurring net losses and negative cash flows from operations. These matters raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans regarding these matters are also described in Note 1. The accompanying consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ BDO Canada LLP

Chartered Accountants, Licensed Public Accountants

Toronto, Ontario

March 4, 2010

21

GENTOR RESOURCES, INC.

(An exploration stage Corporation)

CONSOLIDATED BALANCE SHEETS

(Stated in US dollars)

ASSETS | ||

As at | December 31, 2009 | December 31, 2008 |

Current |

|

|

Cash | $17,547 | $8,502 |

Prepaid and deposits (note 4) | 10,836 | 67,588 |

| $28,383 | $76,090 |

|

|

|

Mineral Properties (note 5) | - | 169,000 |

Capital Assets (note 6) | 357,489 | 472,534 |

|

|

|

Total Assets | $385,872 | $717,624 |

| ||

LIABILITIES | ||

Current Liabilities |

|

|

Accounts payable and accrued liabilities | $818,807 | $992,229 |

Due to related parties (note 7) | 734,108 | 796,374 |

Note payable (note 8) | 715,622 | 211,441 |

Loan payable - current portion (note 9) | 36,006 | 35,297 |

| 2,304,543 | 2,035,341 |

Long Term Liabilities |

|

|

Loan payable - long term portion | 74,196 | 110,203 |

|

|

|

Total Liabilities | $2,378,739 | $2,145,544 |

| ||

SHAREHOLDERS= DEFICIENCY | ||

Authorized 100,000,000 Common Shares, $0.0001 par value 50,000,000 Preferred Shares, $0.0001 par value |

|

|

Issued and outstanding 22,500,000 Common Shares (note 10) | 2,250 | 2,250 |

Paid-in capital | 3,972,750 | 3,972,750 |

Deficit accumulated during the exploration stage | (5,967,867) | (5,402,920) |

Shareholder deficiency | (1,992,867) | (1,427,920) |

Total Liabilities and Shareholder Deficiency | $385,872 | $717,624 |

See accompanying summary of accounting policies and notes to the consolidated financial statements.

22

GENTOR RESOURCES, INC.

(An exploration stage Corporation)

CONSOLIDATED STATEMENTS OF OPERATIONS

(Stated in US dollars)

| For the year ended December 31, 2009 | For the year ended December 31, 2008 | Cumulative from inception on March 24, 2005 to December 31, 2009 |

Expenses |

|

|

|

Field camps expenses | $722 | $285,947 | $348,375 |

Surveying | 1,035 | 14,532 | 50,700 |

Geochemistry | 661 | 123,880 | 145,113 |

Geology | 6,400 | 246,213 | 515,266 |

Drilling | 900 | 1,864,730 | 2,779,677 |

Environmental testing | - | 27,884 | 27,884 |

Mineral properties | 100,000 | 100,000 | 463,045 |

Consulting fees-related parties | - | - | 12,400 |

Consulting fees-others | - | 1,150 | 6,759 |

Management fees | - | - | 2,000 |

Professional fees | 174,647 | 118,996 | 752,143 |

General and administrative expenses | 135,517 | 297,979 | 605,338 |

Depreciation | 109,505 | 110,176 | 226,019 |

| (529,387) | (3,191,487) | (5,934,719) |

|

|

|

|

Rental income | 6,720 | - | 6,720 |

Gain on sale of asset | 7,720 | - | 7,720 |

Loss on deposit | (50,000) | - | (50,000) |

Other income | - | 2,014 | 2,412 |

Net Loss | $(564,947) | $(3,189,473) | $(5,967,867) |

|

|

|

|

Basic and diluted loss per common share (note 2(h)) | $(0.03) | $(0.14) |

|

Weighted average number of common shares (note 2(h)) | 22,500,000 | 22,500,000 |

|

See accompanying summary of accounting policies and notes to the consolidated financial statements.

23

GENTOR RESOURCES, INC.

(An exploration stage Corporation)

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Stated in US dollars)

| For the year ended December 31, 2009 | For the year ended December 31, 2008 | Cumulative from inception on March 24, 2005 to December 31, 2009 |

CASH PROVIDED BY (APPLIED TO): |

|

|

|

Operating activities: |

|

|

|

Adjustments required to reconcile net loss with net cash used in operating activities |

|

|

|

Net loss for the period | $(564,947) | $(3,189,473) | $(5,967,867) |

Depreciation | 109,505 | 110,176 | 226,019 |

Gain on sale of asset | (7,720) | - | (7,720) |

Loss on deposit | 50,000 | - | 50,000 |

Shares issued for mineral properties | - | - | 100,000 |

Accrued interest included in note payable | 27,791 | 11,441 | 39,232 |

|

|

|

|

Change in non cash working capital balance |

|

|

|

Accounts payable | (2,412) | 780,845 | 989,817 |

Prepaid and deposits | 6,752 | (45,774) | (50,836) |

| (381,031) | (2,332,785) | (4,621,355) |

|

|

|

|

Financing activities: |

|

|

|

Common shares issued | - | - | 3,875,000 |

Loan payable | (35,297) | - | (35,297) |

Note payable | 476,389 | 200,000 | 676,389 |

Due to related parties/advances | (62,266) | 688,043 | 734,108 |

| 378,826 | 888,043 | 5,250,200 |

|

|

|

|

Investing Activities: |

|

|

|

Purchase of capital assets | - | (249,703) | (443,548) |

Proceeds from sale of assets | 11,250 | - | 11,250 |

Mineral properties | - | - | (169,000) |

Purchase of a certificate of deposit | - | (10,000) | (10,000) |

| 11,250 | (259,703) | (611,298) |

Net increase (decrease) in cash: | 9,045 | (1,704,445) | 17,547 |

Cash, beginning of the period | 8,502 | 1,712,947 | - |

Cash, end of the period | $17,547 | $8,502 | $17,547 |

24

Non-monetary Transactions:

For the Year

For the Year

Ended 12-31-2009

Ended 12-31-2008

Sale of mineral properties

$169,000

$-

Sale of capital assets

$2,010

$-

See accompanying summary of accounting policies and notes to the consolidated financial statements.

25

GENTOR RESOURCES, INC.

(An exploration stage Corporation)

CONSOLIDATED STATEMENTS OF SHAREHOLDERS= EQUITY (DEFICIENCY)

For the years ended December 31, 2009 and 2008

(Stated in US dollars)

| Common Shares | Preferred Shares | Paid-In- Capital | Accumulated Deficit | Total Shareholders= Equity (deficit) | ||

| Shares | Amount | Shares | Amount |

|

|

|

Shares issued on March 24, 2005 at $0.004 per share | 12,500,000 | $1,250 | - | - | $48,750 | $- | $50,000 |

Net loss for the year | - | - | - | - | - | (97,637) | (97,637) |

Balance at December 31, 2005 | 12,500,000 | 1,250 | - | - | 48,750 | (97,637) | (47,637) |

Shares issued on December 15, 2006 at $0.20 per share | 5,000,000 | 500 | - | - | 999,500 | - | 1,000,000 |

Net loss for the year | - | - | - | - | - | (233,900) | (233,900) |

Balance at December 31, 2006 | 17,500,000 | 1,750 | - | - | 1,048,250 | (331,537) | 718,463 |

Shares issued on July 23, 2007 at $0.20 per share | 500,000 | 50 | - | - | 99,950 | - | 100,000 |

Shares issued on July 31, 2007 at $0.20 per share | 1,000,000 | 100 | - | - | 199,900 | - | 200,000 |

Shares issued on November 20, 2007 at $0.25 per share | 1,000,000 | 100 | - | - | 249,900 | - | 250,000 |

Shares issued on December 17, 2007 at $1.00 per share | 2,500,000 | 250 | - | - | 2,347,750 | - | 2,375,000 |

26

Net loss for the year | - | - | - | - | - | (1,881,910) | (1,881,910) |

Balance at December 31, 2007 | 22,500,000 | 2,250 | - | - | 3,972,750 | (2,213,447) | 1,761,553 |

Net loss for the year | - | - | - | - | - | (3,189,473) | (3,189,473) |

Balance at December 31, 2008 | 22,500,000 | 2,250 | - | - | $3,972,750 | $(5,402,920) | $(1,427,920) |

Net loss for the year | - | - | - | - | - | (564,947) | (564,947) |

Balance at December 31, 2009 | 22,500,000 | 2,250 | - | - | $3,972,750 | $(5,967,867) | $(1,992,867) |

See accompanying summary of accounting policies and notes to the consolidated financial statements.

GENTOR RESOURCES, INC.

(An exploration stage Corporation)

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Years Ended December 31, 2009 and 2008

(Stated in US Dollars)

1.

ORGANIZATION AND GOING CONCERN

Gentor Resources, Inc. (“the Company”) was incorporated on March 24, 2005 under the Florida Business Corporation Act. The Company is an exploration stage corporation formed for the purpose of prospecting and developing mineral properties.

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern, which contemplates, the realization of assets and satisfaction of liabilities in the normal course of business. As at December 31, 2009, the Company has a loss from operations of $564,947 and accumulated deficit of $5,967,867 which raises substantial doubt on the Company’s ability to continue as a going concern. The Company intends to fund operations through equity financing arrangements, which may be insufficient to fund its capital expenditure, working capital and other cash requirements.

The Company’s continued existence is dependent upon it emerging from the exploration stage, obtaining additional financing to continue operations, explore and develop the mining properties and the discovery, development and sale of ore reserves.

These consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from the possible inability of the Company to continue as a going concern.

27

2.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a)

BASIS OF CONSOLIDATION

On June 28, 2007, the Company incorporated a wholly-owned subsidiary Gentor Idaho, an Idaho corporation. The Company’s consolidated financial statements include the accounts of the Company and its wholly-owned subsidiary.

b)

MINERAL PROPERTIES AND EXPLORATION COSTS

Exploration costs pertaining to mineral properties with no proven reserves are charged to operations as incurred. When it is determined that mineral properties can be economically developed as a result of establishing proven and probable reserves, cost incurred to develop such properties are capitalized. Such costs will be amortized using the unit of production method over the estimated life of the probable reserves.

c)

CAPITAL ASSETS

Capital assets are recorded at cost less accumulated depreciation. Depreciation is recorded as follows:

Vehicle

-Straight line over two years

Mining equipment

-Straight line over four years

Office equipment

-Straight line over four years