Attached files

| file | filename |

|---|---|

| 8-K - 1st United Bancorp, Inc. | i00476_1stunited-8k.htm |

| EX-99.1 - 1st United Bancorp, Inc. | i00476_ex99-1.htm |

Nasdaq: FUBC

Forward-Looking Statements

2

This presentation includes forward-looking statements, including statements about future results. These statements are subject to

uncertainties and risks, including but not limited to our ability to integrate the business and operations of companies and banks that we have

acquired, and those we may acquire in the future; the costs of integrating our and operations with companies and banks that we have acquired,

and those we may acquire in the future may be greater than we expect; the loss of key personnel; potential customer loss, deposit attrition,

and business disruption as a result of companies and banks that we have acquired, and those we may acquire in the future; the failure to

achieve expected gains, revenue growth, and/or expense savings from companies and banks that we have acquired, and those we may acquire

in the future; our need and our ability to incur additional debt or equity financing; the strength of the United States economy in general and

the strength of the local economies in which we conduct operations; the accuracy of our financial statement estimates and assumptions; the

effects of harsh weather conditions, including hurricanes; inflation, interest rate, market and monetary fluctuations; the effects of our lack of a

diversified loan portfolio, including the risks of geographic and industry concentrations; the frequency and magnitude of foreclosure of our

loans; effect of changes in the stock market and other capital markets; legislative or regulatory changes; our ability to comply with the

extensive laws and regulations to which we are subject; the willingness of customers to accept third-party products and services rather than

our products and services and vice versa; changes in the securities and real estate markets; increased competition and its effect on pricing;

technological changes; changes in monetary and fiscal policies of the U.S. Government; the effects of security breaches and computer viruses

that may affect our computer systems; changes in consumer spending and saving habits; growth and profitability of our noninterest income;

changes in accounting principles, policies, practices or guidelines; anti-takeover provisions under Federal and state law as well as our Articles

of Incorporation and our bylaws; and our ability to manage the risks involved in the foregoing. Finally, there can be no assurance that we will

realize the anticipated benefits related to the acquisition of Republic Federal Bank, N.A.

These factors, as well as additional factors, can be found in our periodic and other filings with the SEC, which are available at the SEC’s

internet site (http://www.sec.gov). Actual results may differ materially from projections and could be affected by a variety of factors,

including factors beyond our control. In addition, forward-looking statements regarding the Republic transaction are based on currently

available information provided to us by the FDIC. Actual results could differ materially after experience with the acquisition. Forward-

looking statements in this presentation speak only as of the date of these materials, and we assume no obligation to update forward-looking

statements or the reasons why actual results could differ.

Transaction Overview

3

1st United has purchased and assumed select assets and

liabilities from the FDIC as receiver of Republic

Federal Bank, N.A. (“Republic”) – Miami, Florida

Transaction excludes most non-performing loans, ORE, acquisition, development & construction loans (“ADC”),

residential & commercial land loans, Ex-Im bank loans, and loans to

foreign nationals

1st United will receive additional indemnifications from the FDIC

Depositors of Republic Federal have become depositors of 1st United and continue to have FDIC

insurance coverage on their deposits

FDIC modified whole bank acquisition with loss sharing

Purchased assets of approximately $425 million

Includes approximately $231 million of loans covered by FDIC loss share protection

Remaining assets consist primarily of cash and securities, all transferred at fair market values

Assumption of approximately $350 million of total deposits and $75 million of FHLB borrowings

Enhances footprint in Miami-Dade County

Loss share agreement covers all purchased loans

No first loss tranche (i.e. loss sharing with FDIC commences immediately)

80% of losses covered by FDIC up to the stated threshold of $36 million; 95% of losses covered by FDIC thereafter

All regulatory approvals have been received and the transaction has closed

Stifel Nicolaus served as financial advisor and Smith MacKinnon, P.A. as legal counsel to 1

st United in

connection with this transaction

Strategic Rationale

4

FDIC assisted modified whole bank acquisition with loss sharing

Accelerates strategic growth aspirations

Adding Republic’s 4 Miami-Dade County branches enhances 1st United’s franchise in Florida’s largest

banking market

Financially compelling for shareholders

Meaningful accretion to EPS and significantly improves internal capital generation capabilities

Increased scale provides additional operating leverage that will further improve profitability

Transaction accomplished without ownership dilution to existing shareholders

Acquisition accretive to tangible book value per share

Creation of a $1 Billion balance sheet in a risk averse manner due to loss sharing support from the FDIC

Loss sharing and asset purchase discount limit the downside risk of transaction

Not expected to require additional capital

Significant capacity for additional expansion remains given existing capital base

Transaction Structure

5

$37.7 million discount on the loans

1.0% premium on assumed deposits

$121mm commercial / $110mm residential loans

$231 million of covered assets

$0 First Loss Position

FDIC assumes 80% of losses between $0 and $36 million (Stated Threshold)

FDIC assumes 95% of losses over $36 million

Total pre-tax 1st United portion of stated threshold (20% of $36 million) is

significantly less than the asset discount

Cash (at book value), securities (at fair market value) and other tangible assets

acquired at fair value

90-day option to purchase property & equipment or assume leases

Branches will be integrated into 1st United’s existing banking network and

reviewed for long-term strategic fit

Discount / Premium

Loss Share

Agreement

Other Assets

Loan Discount = ($37.7) million

Deposit Premium = $3.4 million

Net Bid = ($34.3) million

Loss Exposure Risk Mitigation

6

Loan discount substantially exceeds the maximum loss that 1st United could incur on covered assets

FDIC loss sharing agreement in conjunction with 1st United’s bid substantially reduces the adverse

financial impact of the credit risk associated with legacy assets

Preliminary Estimate of Accounting Impact

7

Anticipate potential one-time gain under FASB ASC Topic 805 (formerly FAS 141R) of between $10

million and $15 million pre-tax as the acquisition date fair value of the assets acquired exceeds the

liabilities assumed (“negative goodwill” or purchase gain).

The after tax gain will result in accretion to book value per share.

Transaction is essentially self-funding as anticipated after-tax gain serves to capitalize transaction.

Gain booked substantiates deferred tax asset and will enhance Tier 1 capital due to current disallowance

of a portion of 1st United’s deferred tax asset.

Above amounts subject to change as precise amount of gain is dependent on completion of final

appraisals and mark-to-market valuations of the assets and liabilities.

8

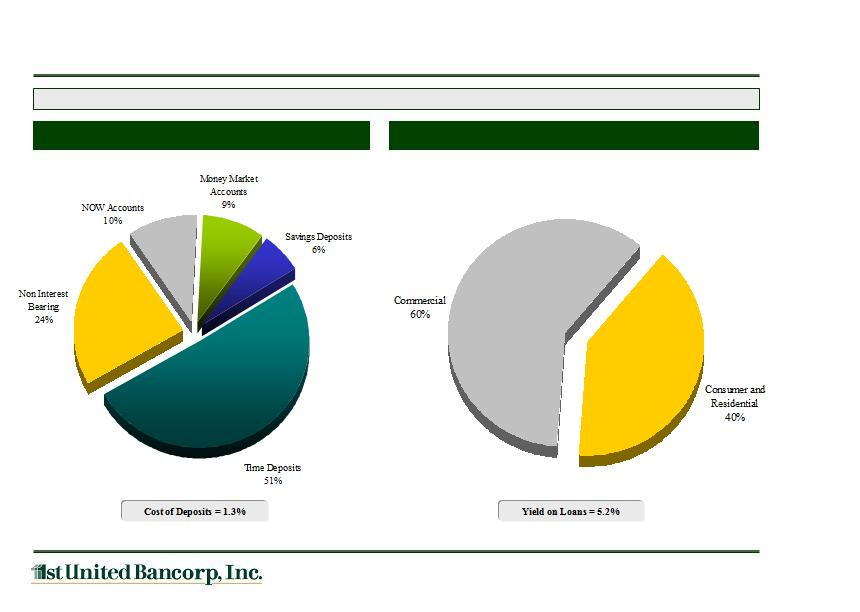

Deposits

Loan Portfolio

Composition of Acquired Loans & Assumed Deposits

Reduces 1stUnited’s loans to deposits ratio from 109% to approximately 90%

Note: Information displayed above is estimated based on information received from the FDIC and 1st United estimates.

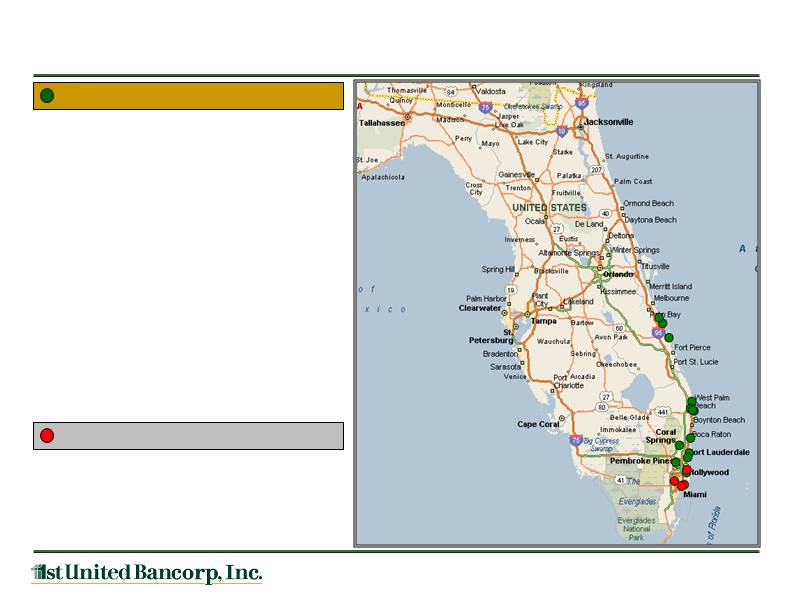

1stUnited Branch Offices

Combined Branch Footprint

9

North Miami Beach

15801 Biscayne Blvd.

North Miami Beach, FL 33162

North Palm Beach

741 US Highway One

North Palm Beach, FL 33408

Palm Beach

335 South Country Road

Palm Beach, FL 33480

Sebastian

1020 US Highway 1

Sebastian, FL 32958

Vero Beach

1717 Indian River Blvd.

Vero Beach, FL 32960

West Palm Beach

307 Evernia Street, Suite 100

West Palm Beach, FL 33401

Headquarters & Main Office

One North Federal Highway

Boca Raton, FL 33432

Barefoot Bay

1020 Buttonwood Street

Barefoot Bay, FL 32976

Cooper City

5854 South Flamingo Road

Cooper City, FL 33330

Coral Ridge

2800 East Oakland Park Blvd.

Ft. Lauderdale, FL 33306

Coral Springs

2855 North University Drive

Coral Springs, FL 33067

Fort Lauderdale Downtown

633 South Federal Highway

Ft. Lauderdale, FL 33301

Brickell

1001 Brickell Bay Drive

Miami, FL 33131

Aventura

19125 Biscayne Blvd

Aventura, FL 33180

Former Republic Branch Offices

Coral Way

2159 Coral Way

Miami, FL 33145

Doral

8484 NW 36th Street, Suite 100

Doral, FL 33166

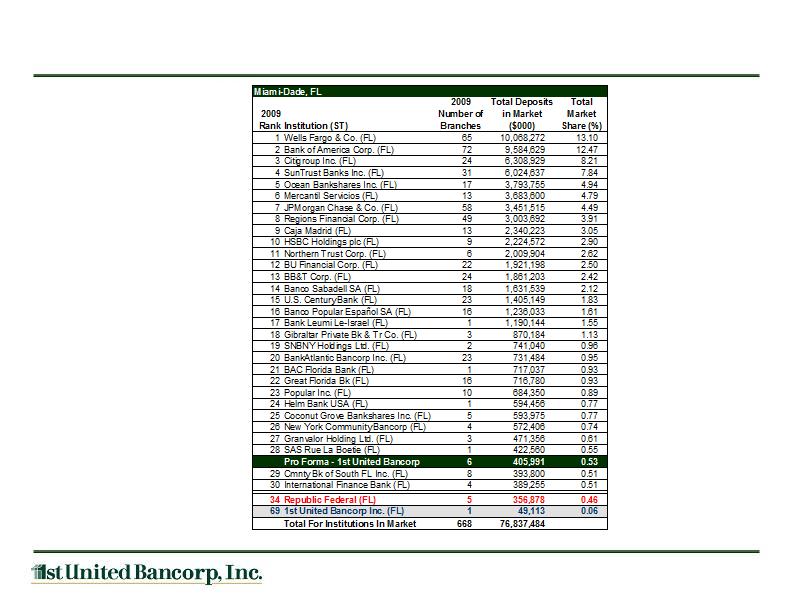

Market Share – Miami-Dade County

10

Source: SNL Financial. Data as of 6/30/2009.

Integration Plan

11

Management team adept at successfully completing and integrating M&A transactions having

been involved in 34 transactions on a combined basis

Depositors in all Republic branches have access to their funds (no interruption of service)

2010 conversion to 1st United’s IT platform, after interim servicing for FDIC concludes

Branches will be integrated into 1st United’s existing banking network and reviewed for long-

term strategic fit (90 day option to decide)

Branches will be locally managed by 1st United and Republic’s team of experienced bankers

with centralized support

1st United will leverage Republic’s experienced banking professionals and offer a broad array

of banking products and services to Republic’s customer base

Building a robust team to manage FDIC loss share compliance

Integration will be seamless to Republic customers and is already underway

Transaction Merits

12

Major growth catalyst which allows recently raised capital to remain available for

additional future strategic franchise enhancement opportunities

Pro forma balance sheet remains fortified with robust capital ratios well in excess of

“well-capitalized” thresholds

Highly accretive transaction even in stressed scenarios modeled

Extends franchise into legacy markets with significant market share opportunity

Strong pro forma liquidity and capital builds customer confidence and enables 1stUnited

to pursue additional balance sheet growth

All acquired loans covered by loss-share agreement providing for approximately 32% of

1stUnited’s loan portfolio on a pro forma basis subject to loss share

Capital creation provides sufficient value necessary to manage complexities and expense

associated with transaction