Attached files

| file | filename |

|---|---|

| 8-K - FORM 8K FINANCIAL INFORMATION 2009 Q3 - CNO Financial Group, Inc. | form8k.htm |

| EX-99.2 - QUARTERLY FINANCIAL SUPPLEMENT - CNO Financial Group, Inc. | exh99-2.htm |

Exhibit

99.1

Third

Quarter 2009

Financial

and Operating Results

For

the period ended September 30, 2009

Conseco,

Inc.

November

5, 2009

2

Forward-Looking

Statements

Cautionary

Statement Regarding Forward-Looking Statements. Our statements,

trend analyses and other information contained in these

materials relative to markets for Conseco’s products and trends in Conseco’s operations or financial results, as well as other statements,

contain forward-looking statements within the meaning of the federal securities laws and the Private Securities Litigation Reform Act of 1995.

Forward-looking statements typically are identified by the use of terms such as “anticipate,” “believe,” “plan,” “estimate,” “expect,” “project,”

“intend,” “may,” “will,” “would,” “contemplate,” “possible,” “attempt,” “seek,” “should,” “could,” “goal,” “target,” “on track,” “comfortable with,”

“optimistic” and similar words, although some forward-looking statements are expressed differently. You should consider statements that

contain these words carefully because they describe our expectations, plans, strategies and goals and our beliefs concerning future business

conditions, our results of operations, financial position, and our business outlook or they state other ‘‘forward-looking’’ information based on

currently available information. Assumptions and other important factors that could cause our actual results to differ materially from those

anticipated in our forward-looking statements include, among other things: (i) our ability to continue to satisfy the financial ratio and balance

requirements and other covenants of our debt agreements; (ii) liquidity issues associated with the right of holders of our convertible debentures

to require us to repurchase existing debentures on September 30, 2010; (iii) general economic, market and political conditions, including the

performance and fluctuations of the financial markets which may affect our ability to raise capital or refinance existing indebtedness and the

cost of doing so; (iv) our ability to generate sufficient liquidity to meet our debt service obligations and other cash needs; (v) our ability to obtain

adequate and timely rate increases on our supplemental health products including our long-term care business; (vi) the receipt of any required

regulatory approvals for dividend and surplus debenture interest payments from our insurance subsidiaries; (vii) mortality, morbidity, the

increased cost and usage of health care services, persistency, the adequacy of our previous reserve estimates and other factors which may

affect the profitability of our insurance products; (viii) changes in our assumptions related to the cost of policies produced or the value of policies

in force at the effective date of our emergence from bankruptcy; (ix) the recoverability of our deferred tax asset and the effect of potential

ownership changes and tax rate changes on its value; (x) our assumption that the positions we take on our tax return filings, including our

position that the debentures will not be treated as stock for purposes of Section 382 of the Code and will not trigger an ownership change, will

not be successfully challenged by the Internal Revenue Service (IRS); (xi) changes in accounting principles and the interpretation thereof; (xii)

our ability to achieve anticipated expense reductions and levels of operational efficiencies including improvements in claims adjudication and

continued automation and rationalization of operating systems; (xiii) performance and valuation of our investments, including the impact of

realized losses (including other-than-temporary impairment charges); (xiv) our ability to identify products and markets in which we can compete

effectively against competitors with greater market share, higher ratings, greater financial resources and stronger brand recognition; (xv) the

ultimate outcome of lawsuits filed against us and other legal and regulatory proceedings to which we are subject; (xvi) our ability to complete the

remediation of the material weakness in internal controls over our actuarial reporting process and to maintain effective controls over financial

reporting; (xvii) our ability to continue to recruit and retain productive agents and distribution partners and customer response to new products,

distribution channels and marketing initiatives; (xviii) our ability to achieve eventual upgrades of the financial strength ratings of Conseco and

our insurance company subsidiaries as well as the impact of rating downgrades on our business and our ability to access capital; (xix) the risk

factors or uncertainties listed from time to time in our filings with the Securities and Exchange Commission; (xx) regulatory changes or actions,

including those relating to regulation of the financial affairs of our insurance companies, such as the payment of dividends and surplus

debenture interest to us, regulation of financial services affecting (among other things) bank sales and underwriting of insurance products,

regulation of the sale, underwriting and pricing of products, and health care regulation affecting health insurance products; and (xxi) changes in

the Federal income tax laws and regulations which may affect or eliminate the relative tax advantages of some of our products. Other factors

and assumptions not identified above are also relevant to the forward-looking statements, and if they prove incorrect, could also cause actual

results to differ materially from those projected. All written or oral forward-looking statements attributable to us are expressly qualified in their

entirety by the foregoing cautionary statement. Our forward-looking statements speak only as of the date made. We assume no obligation to

update or to publicly announce the results of any revisions to any of the forward-looking statements to reflect actual results, future events or

developments, changes in assumptions or changes in other factors affecting the forward-looking statements.

materials relative to markets for Conseco’s products and trends in Conseco’s operations or financial results, as well as other statements,

contain forward-looking statements within the meaning of the federal securities laws and the Private Securities Litigation Reform Act of 1995.

Forward-looking statements typically are identified by the use of terms such as “anticipate,” “believe,” “plan,” “estimate,” “expect,” “project,”

“intend,” “may,” “will,” “would,” “contemplate,” “possible,” “attempt,” “seek,” “should,” “could,” “goal,” “target,” “on track,” “comfortable with,”

“optimistic” and similar words, although some forward-looking statements are expressed differently. You should consider statements that

contain these words carefully because they describe our expectations, plans, strategies and goals and our beliefs concerning future business

conditions, our results of operations, financial position, and our business outlook or they state other ‘‘forward-looking’’ information based on

currently available information. Assumptions and other important factors that could cause our actual results to differ materially from those

anticipated in our forward-looking statements include, among other things: (i) our ability to continue to satisfy the financial ratio and balance

requirements and other covenants of our debt agreements; (ii) liquidity issues associated with the right of holders of our convertible debentures

to require us to repurchase existing debentures on September 30, 2010; (iii) general economic, market and political conditions, including the

performance and fluctuations of the financial markets which may affect our ability to raise capital or refinance existing indebtedness and the

cost of doing so; (iv) our ability to generate sufficient liquidity to meet our debt service obligations and other cash needs; (v) our ability to obtain

adequate and timely rate increases on our supplemental health products including our long-term care business; (vi) the receipt of any required

regulatory approvals for dividend and surplus debenture interest payments from our insurance subsidiaries; (vii) mortality, morbidity, the

increased cost and usage of health care services, persistency, the adequacy of our previous reserve estimates and other factors which may

affect the profitability of our insurance products; (viii) changes in our assumptions related to the cost of policies produced or the value of policies

in force at the effective date of our emergence from bankruptcy; (ix) the recoverability of our deferred tax asset and the effect of potential

ownership changes and tax rate changes on its value; (x) our assumption that the positions we take on our tax return filings, including our

position that the debentures will not be treated as stock for purposes of Section 382 of the Code and will not trigger an ownership change, will

not be successfully challenged by the Internal Revenue Service (IRS); (xi) changes in accounting principles and the interpretation thereof; (xii)

our ability to achieve anticipated expense reductions and levels of operational efficiencies including improvements in claims adjudication and

continued automation and rationalization of operating systems; (xiii) performance and valuation of our investments, including the impact of

realized losses (including other-than-temporary impairment charges); (xiv) our ability to identify products and markets in which we can compete

effectively against competitors with greater market share, higher ratings, greater financial resources and stronger brand recognition; (xv) the

ultimate outcome of lawsuits filed against us and other legal and regulatory proceedings to which we are subject; (xvi) our ability to complete the

remediation of the material weakness in internal controls over our actuarial reporting process and to maintain effective controls over financial

reporting; (xvii) our ability to continue to recruit and retain productive agents and distribution partners and customer response to new products,

distribution channels and marketing initiatives; (xviii) our ability to achieve eventual upgrades of the financial strength ratings of Conseco and

our insurance company subsidiaries as well as the impact of rating downgrades on our business and our ability to access capital; (xix) the risk

factors or uncertainties listed from time to time in our filings with the Securities and Exchange Commission; (xx) regulatory changes or actions,

including those relating to regulation of the financial affairs of our insurance companies, such as the payment of dividends and surplus

debenture interest to us, regulation of financial services affecting (among other things) bank sales and underwriting of insurance products,

regulation of the sale, underwriting and pricing of products, and health care regulation affecting health insurance products; and (xxi) changes in

the Federal income tax laws and regulations which may affect or eliminate the relative tax advantages of some of our products. Other factors

and assumptions not identified above are also relevant to the forward-looking statements, and if they prove incorrect, could also cause actual

results to differ materially from those projected. All written or oral forward-looking statements attributable to us are expressly qualified in their

entirety by the foregoing cautionary statement. Our forward-looking statements speak only as of the date made. We assume no obligation to

update or to publicly announce the results of any revisions to any of the forward-looking statements to reflect actual results, future events or

developments, changes in assumptions or changes in other factors affecting the forward-looking statements.

Non-GAAP

Measures

3

This

presentation contains the following financial measures that differ from the

comparable measures

under Generally Accepted Accounting Principles (GAAP): operating earnings measures; book value,

excluding accumulated other comprehensive income (loss) per share; operating return measures;

earnings before net realized investment gains (losses) and corporate interest and taxes; debt to capital

ratios, excluding accumulated other comprehensive income (loss); and interest-adjusted benefit ratios.

Reconciliations between those non-GAAP measures and the comparable GAAP measures are

included in the Appendix, or on the page such measure is presented.

under Generally Accepted Accounting Principles (GAAP): operating earnings measures; book value,

excluding accumulated other comprehensive income (loss) per share; operating return measures;

earnings before net realized investment gains (losses) and corporate interest and taxes; debt to capital

ratios, excluding accumulated other comprehensive income (loss); and interest-adjusted benefit ratios.

Reconciliations between those non-GAAP measures and the comparable GAAP measures are

included in the Appendix, or on the page such measure is presented.

While

management believes these measures are useful to enhance understanding and

comparability

of our financial results, these non-GAAP measures should not be considered substitutes for the most

directly comparable GAAP measures.

of our financial results, these non-GAAP measures should not be considered substitutes for the most

directly comparable GAAP measures.

Additional

information concerning non-GAAP measures is included in our periodic filings

with the

Securities and Exchange Commission that are available in the “Investor - SEC Filings” section of

Conseco’s website, www.conseco.com.

Securities and Exchange Commission that are available in the “Investor - SEC Filings” section of

Conseco’s website, www.conseco.com.

Q3

2009 Summary

4

CNO

§ Third

consecutive profitable quarter

• Continued

profitability in all three insurance segments

• EBIT*

of $107.0 million, up 2% over Q3 2008

• Net

income of $15.4 million, compared to net loss of $183.3

million in Q3 2008

million in Q3 2008

§ Core

sales** of $93.4 million, up 1% from Q3 2008

§ Trailing

four-quarter premium up 3% over a year ago

§ Agent

recruitment continues to be strong

*Management believes

that an analysis of earnings or loss before net realized investment gains

(losses),

discontinued

operations, corporate interest and taxes (“EBIT,” a non-GAAP financial measure)

provides a

clearer

comparison of the operating results of the company quarter-over-quarter because

it excludes:

(1)

corporate interest expense; and (2) net realized investment gains (losses) that

are unrelated to the

company’s

underlying fundamentals.

**Excludes

PFFS.

Q3

2009 Summary

5

CNO

§ Net

realized investment losses of $18.9 million

• Total

other-than-temporary impairments (OTTI) of $162.4 million

• $35.7 million

recorded in earnings

• $126.7 million

recorded in accumulated other comprehensive loss (AOCL)

§ AOCL

improved to $146 million:

• $1.6 billion

improvement from 12/31/08

• $0.9 billion

improvement from 6/30/09

§ Book

value per share:

• Excluding AOCL* rose

to $18.82 at 9/30/09, from $18.41 at 12/31/08

• Including AOCL rose

to $18.03 at 9/30/09, from $8.82 at 12/31/08

*See

Appendix for corresponding GAAP measure.

6

CNO

§ Addresses

most pressing financial priority: re-financing the

3.5% convertible debentures

3.5% convertible debentures

§ Structured

to protect NOL, while preserving ability to raise

additional common equity

additional common equity

§ Improves

financial covenant margins; increases liquidity

§ Basics

of the deal:

• Private

placement of common stock and warrants

• Issuance

of new convertible debentures to refinance existing

convertible debentures

convertible debentures

• Tender

offer for existing convertible debentures

Recapitalization

of Conseco

7

CNO

Sources

Net

Proceeds from Equity Private Placement

Net

Proceeds from New Convertible Debentures

Total

Sources

Uses

Retirement of Old

Convertible Debentures

Payment

under Credit Agreement (50% of Net

Proceeds

of Equity Private Placement)

Funds

Available for Corporate Purposes

Total

Uses

$74

281

$355

$293

37

25

$355

($

millions)

*Assumes all

debentures are tendered and extinguished as of 9/30/09. If debentures are

tendered on 10/5/10

(the latest possible date), net proceeds from the new debenture issue would be $18 million less.

(the latest possible date), net proceeds from the new debenture issue would be $18 million less.

*

Anticipated

Sources and Uses of Cash

CNO

8

Credit

Facility (matures 10/13)

6%

Senior Note ($25MM due annually beginning 11/09)

3.5%

Convertible Debentures (puttable by holders 9/10)

7.0%

Convertible Debentures (matures 12/16)

Unamortized Discount

on Convertible Debentures

Total

Corporate Notes Payable

Equity

excluding Accumulated Other Comprehensive Loss*

Accumulated Other

Comprehensive Loss (“AOCL”)

Total

Shareholders’ Equity

Total

Capital

Debt/Total

Capital (excluding AOCL)

Book

Value per Share

Book

Value per Share (excluding AOCL)

$855

125

293

-

(11)

$1,262

3,480

(146)

$3,334

$4,596

26.6%

$18.03

$18.82

Actual

9/30/09

($

millions)

*Includes

recognition of $10.4 million after-tax loss on the assumed extinguishment of all

$293 million of existing

debentures and $0.1 million after-tax loss related to the writedown of deferred issuance costs associated with

the repayment of the credit facility.

debentures and $0.1 million after-tax loss related to the writedown of deferred issuance costs associated with

the repayment of the credit facility.

$(37)

(293)

293

3

63

Recapitalization

Adjustments

$818

125

-

293

(8)

$1,228

3,543

(146)

$3,397

$4,625

25.7%

$16.88

$17.60

As

Adjusted

9/30/09

Capital

Structure

Collected

Premiums

9

CNO

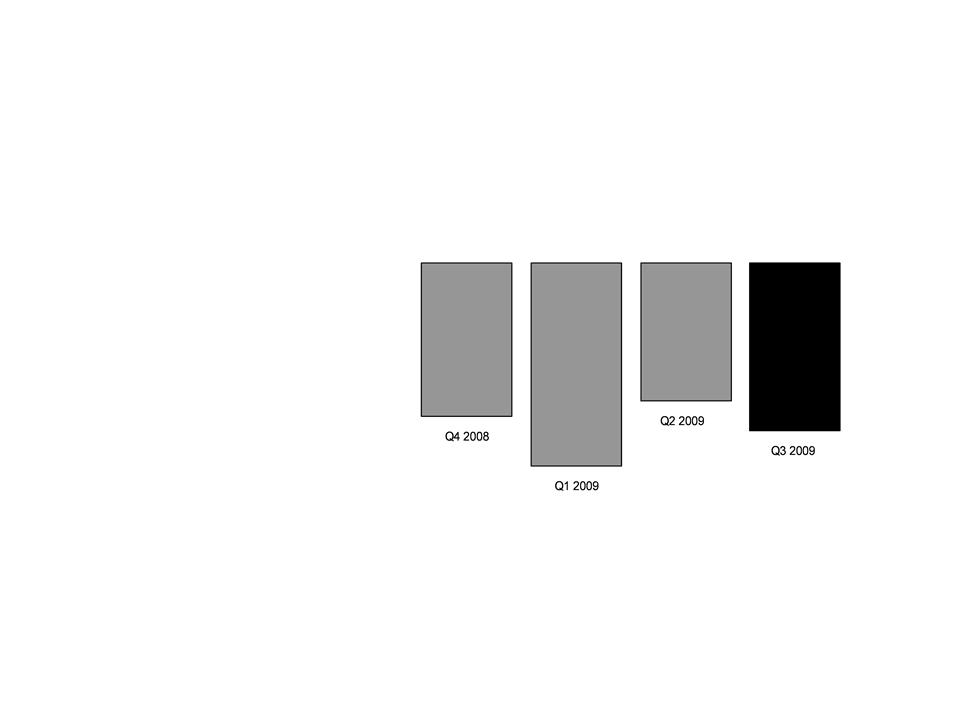

§ Total

collected premiums

for trailing 4 quarters up

3% vs comparable period

in prior year

for trailing 4 quarters up

3% vs comparable period

in prior year

§ Slight

decline at Bankers

due to termination of

PFFS group quota share

contracts

due to termination of

PFFS group quota share

contracts

§ Consistent

growth at

Colonial Penn

Colonial Penn

§ Slight

decline at CIG due

to focus on more

profitable business and

de-emphasizing annuity

sales

to focus on more

profitable business and

de-emphasizing annuity

sales

BLC

($

millions)

CP

CIG

Collected

Premiums-Trailing 4 Quarters

Q3

2008

$4,275.1

Q4

2008

$4,524.9

Q1

2009

$4,549.3

Q2

2009

$4,494.9

Q3

2009

$4,423.1

Q3

2009

Summary

of Results

10

CNO

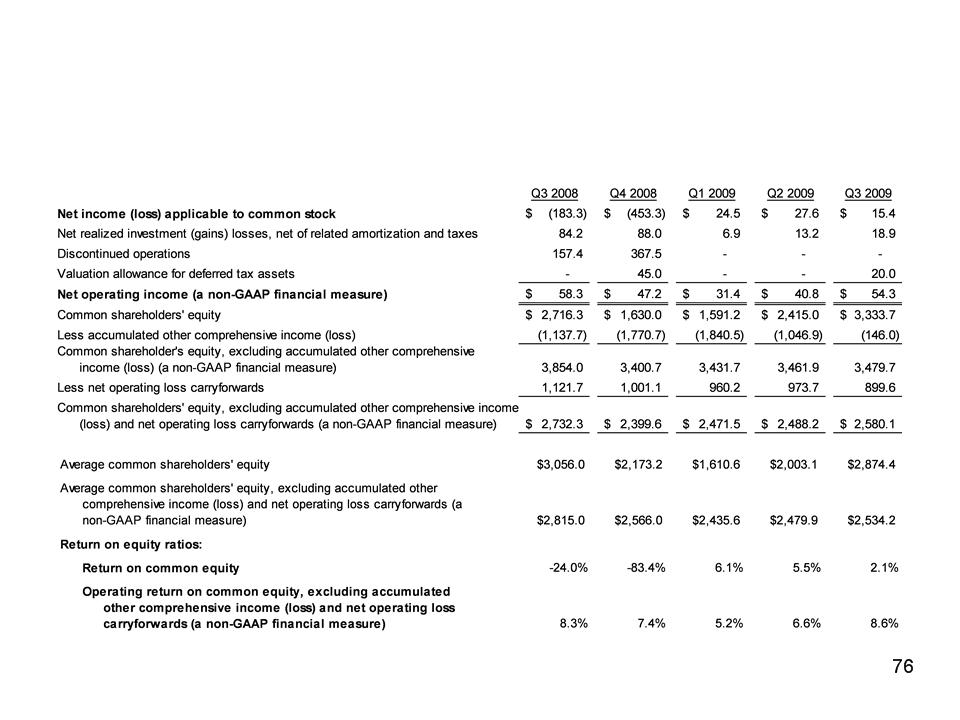

$85.4

7.4

21.6

(31.4)

$83.0

--

(18.9)

$64.1

Pre-Tax

After

Tax

EPS

($

millions, except per-share amounts)

$54.3

(20.0)

(18.9)

$15.4

$0.29

(0.11)

(0.10)

$0.08

*Management

believes that an analysis of earnings before net realized investment gains

(losses) and increases to

our

valuation allowance for deferred tax assets (a non-GAAP financial measure)

provides an alternative measure

of the

operating results of the company because such items are unrelated to the

company’s continuing operations.

The

table above provides a reconciliation to the corresponding GAAP

measure.

**See

Appendix for a reconciliation to the corresponding GAAP measure.

Bankers

Life

Colonial

Penn

Conseco

Insurance Group

Corporate operations

and interest expense

Income

before net realized investment losses

and

valuation allowance for deferred tax assets*

Valuation allowance

for deferred tax assets**

Net

realized investment losses**

Total

Q3

Earnings

11

CNO

Consolidated

*Management believes

that an analysis of earnings before net realized investment gains (losses),

losses related to

the transfer of Senior Health to an independent trust (included in Discontinued Operations) and corporate interest

and taxes (“EBIT,” a non-GAAP financial measure) provides an alternative measure to compare the operating

results of the company quarter-over-quarter because it excludes: (1) corporate interest expense; and (2) items that

are unrelated to the company’s continuing operations. The table above provides a reconciliation of EBIT to net

income (loss).

the transfer of Senior Health to an independent trust (included in Discontinued Operations) and corporate interest

and taxes (“EBIT,” a non-GAAP financial measure) provides an alternative measure to compare the operating

results of the company quarter-over-quarter because it excludes: (1) corporate interest expense; and (2) items that

are unrelated to the company’s continuing operations. The table above provides a reconciliation of EBIT to net

income (loss).

($

millions)

Operating

ROE

12

CNO

Operating ROE*,

Trailing 4 Quarters

Operating

EPS*

13

CNO

*Operating earnings

per share exclude net realized investment gains (losses), valuation allowance

related to

deferred

tax assets and discontinued operations. See Appendix for corresponding GAAP

measure.

**Represents the

expected ratio of quarterly Operating EPS to annual Operating EPS, based

on

historical

experience.

Seasonality of Q3 Q4 Q1 Q2 Q3

Operating EPS** 23-28% 26-31% 17-22% 20-25% 23-28%

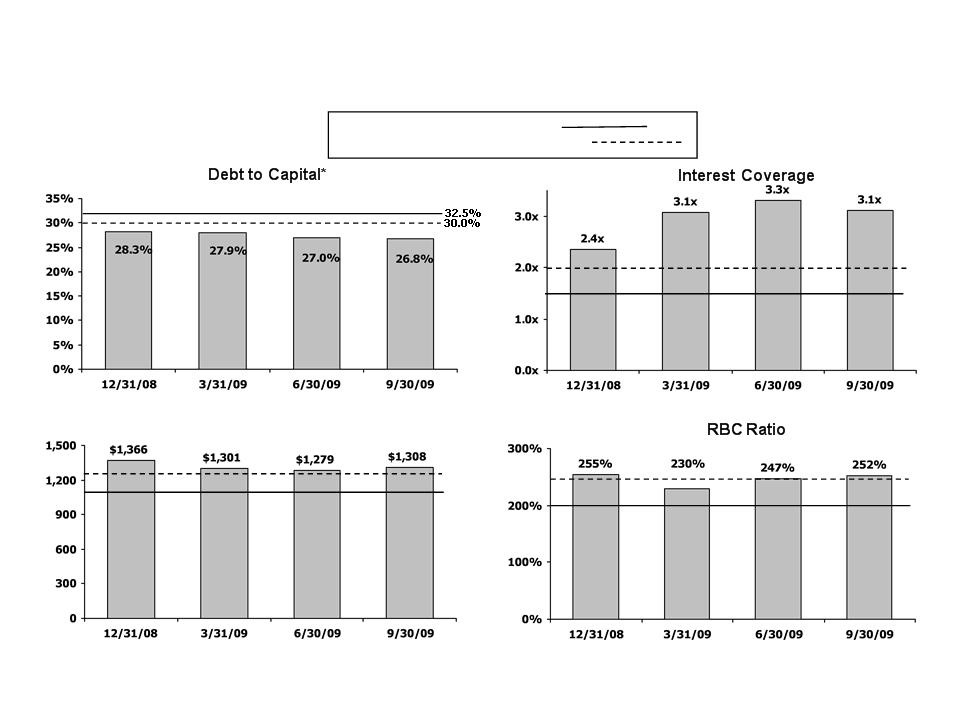

Statutory

Surplus ($ millions)

*Excludes Accumulated Other Comprehensive Loss, as defined by the senior credit facility.

$1,270

$1,100

Current

Amendment Levels

“Snapback” Levels

(effective Q3 2010)

CNO

14

250%

200%

1.5x

2.0x

Covenant

Metrics

Liquidity

Projection

For

Remainder of 2009*

15

CNO

($

millions)

Cash

Balance 9/30/09

Sources

Equity

Private Placement Proceeds, net of expenses

Net

Proceeds from New Convertible Debentures

Surplus

Debenture Interest

Management

and Investment Fees

Total

Sources

Uses

Interest

Debt

Repayments:

Senior

Credit Facility

Retirement

of Old Convertible Debentures

Senior

Health Note

Holding

Company Expenses

Total

Uses

Cash

Balance 12/31/09

$85.6

$73.7

281.3

12.2

9.0

376.2

18.9

36.8

293.0

25.0

15.1

388.8

$73.0

*Assumes 100% tender

in Q4 2009, and assumes that net equity proceeds are retained at the parent

company.

**Includes $4.3

million of expenses related to the retirement of the convertible

debentures.

**

Consolidated

RBC Ratio*

16

CNO

*Risk-Based Capital

(“RBC”) requirements provide a tool for insurance regulators to determine the

levels of

statutory

capital and surplus an insurer must maintain in relation to its insurance and

investment risks. The

RBC

ratio is the ratio of the statutory consolidated adjusted capital of our

insurance subsidiaries to RBC.

§ Q3

2009 positive impacts:

• Statutory operating

results (19 pts)

• Wilton Re

reinsurance (10 pts)

§ Q3

2009 negative impacts:

• Credit rating

migration and net

statutory capital losses (22 pts)

statutory capital losses (22 pts)

Consolidated

RBC Ratio -

Changes

Over Last Four Quarters

17

CNO

9/30/08

RBC

9/30/09

RBC

257%

252%

+45%

+11%

+4%

-50%

-48%

+17%

+9%

+5%

+2%

Capital

and

Risk

Management Initiatives

18

CNO

§ Reinsure

new and inforce business

§ Manage

investment portfolio to mitigate RBC impact of ratings

migration

migration

§ Terminate

PFFS quota share agreements with Coventry at 12/31/09 -

improves consolidated RBC by 8 pts in 2010

improves consolidated RBC by 8 pts in 2010

§ Limit

Bankers branch expansion

§ Reduce

direct marketing spending at Colonial Penn

§ Regulatory

• Merger

of three CIG insurance subsidiaries

• Deferred

tax asset

• Mortgage

Experience Adjustment Factor

• Modification

of RMBS ratings

Q3

Summary

19

Bankers

§ Earnings

of $85.4 million, up 26% over Q3 2008:

• Higher PFFS income

(+$20 million) due to mid-year premium

sweeps and favorable IBNR development

sweeps and favorable IBNR development

• Increase in COLI

surrender value (+$7 million)

• Lower LTC margins

(-$7 million) due to slightly higher interest-

adjusted benefit ratio

adjusted benefit ratio

§ Record-setting

third quarter for both Life and Med Supp sales

§ Continued

strong core sales and record agent recruiting

• 16% increase in new

agents YTD

Bankers

20

($

millions)

Quarterly Core NAP

(Excludes PFFS)

NAP-Quarterly*: $65.8 $72.8 $94.5 $69.4 $62.3

PFFS

NAP-Quarterly*: $4.6 $0.9 $34.1** $6.3 $(0.2)

*Excludes group

business not sold by Bankers agents.

**Net

of $7 million reserve for anticipated chargebacks related to sales still within

their 90-day disenrollment period.

NAP

Results

§ Core

NAP up 2% vs Q3 2008

• Strong sales of Life

(+21%) and

Med Supp (+20%), partially offset

by lower sales of Annuities (-15%)

and LTC (-14%)

Med Supp (+20%), partially offset

by lower sales of Annuities (-15%)

and LTC (-14%)

§ PFFS

YTD 2009 sales down 30%

• Changes in consumer

preferences

• Stopped selling

Coventry PFFS in

Q3 2009

Q3 2009

Q3

2009 Sales and

Distribution

Results

21

Bankers

§ Continued

growth in agent force

• Average agent count

YTD 5,186, up 10% vs. first nine months of

2008

2008

§ Branch

manager retention is strong

• Since 2004, the

annual turnover rate in our top 48 branches has

been less than 3%

been less than 3%

• Average length of

service for these top managers is 15+ years

Medicare

Advantage

22

Bankers

§ As

previously announced, Coventry is exiting PFFS business

effective 12/31/09

effective 12/31/09

• PFFS relationship

terminates; affects approximately 55,000

Bankers-sold PFFS members, partially reinsured by Bankers

Bankers-sold PFFS members, partially reinsured by Bankers

• PDP relationship

(distribution and reinsurance) remains

unchanged

unchanged

§ Coventry

policyholder progress

• Early results

indicate policyholder shift from PFFS to Med Supp;

for month of October, Med Supp sales are significantly ahead of

prior year

for month of October, Med Supp sales are significantly ahead of

prior year

§ Humana

sales begin in earnest on November 15

§ Annuity sales down

15% vs

Q3 2008

Q3 2008

§ Lower results are in

line with

overall market

overall market

§ Reduced bonus rate

to

maintain margins

maintain margins

Bankers

Annuities -

NAP*

($

millions)

23

*Calculated as 6% of

annuity deposits.

Q1

2009

$18.2

$9.0

$10.4

$18.2

$6.2

$5.0

$13.2

$6.8

$11.0

Q2

2009

$17.8

Q3

2009

$16.4

$4.8

$11.6

Annuity

Sales

Annuity

Surrenders

24

Bankers

IA

Surrenders

(annualized

quarterly rate)

Non-IA

Surrenders

(annualized

quarterly rate)

§ Both

indexed and non-indexed

annuity surrenders lower than

prior year

annuity surrenders lower than

prior year

§ Total

account value:

• IAs - $1.5

billion

• Non-IAs - $4.7

billion

§ Average

account value:

• IAs -

$41,000

• Non-IAs -

$36,000

§ Over

89% of our annuities are

still in surrender charge period:

still in surrender charge period:

• IAs -

95%

• Non-IAs -

87%

LTC

Update

25

Bankers

§ Rate

increase filings ahead of schedule (2008 round - policies

issued prior to 2002); expect to exceed original filing goals

issued prior to 2002); expect to exceed original filing goals

• Completed filing of

$102.5 million of rate increases

• As of

9/30/09:

• Approvals = $77.4

million, 109% of original goal

• Projected financial

impact = $58.1 million, 109% of original goal

§ Continued

focus on claims management/underwriting

§ New

products (as of 9/30/09)

• LTC/Annuity Combo

product launched in 31 states

• LTC product revision

launched in 19 states, with rates reflecting

current claim experience and in line with target profit margins

current claim experience and in line with target profit margins

Q3

Earnings

26

Bankers

($

millions)

Trailing

4 Quarter Operating Return on Equity: 10.0%

Management believes

that an analysis of income (loss) before net realized investment gains (losses),

net of

related amortization (a non-GAAP financial measure), is important to evaluate the financial performance of

our business, and is a measure commonly used in the life insurance industry. Management uses this

measure to evaluate performance because realized gains or losses can be affected by events that are

unrelated to a company’s underlying fundamentals. The table on Page 11 reconciles the non-GAAP measure

to the corresponding GAAP measure. See Appendix for a reconciliation of the return on equity measure to

the corresponding GAAP measure.

related amortization (a non-GAAP financial measure), is important to evaluate the financial performance of

our business, and is a measure commonly used in the life insurance industry. Management uses this

measure to evaluate performance because realized gains or losses can be affected by events that are

unrelated to a company’s underlying fundamentals. The table on Page 11 reconciles the non-GAAP measure

to the corresponding GAAP measure. See Appendix for a reconciliation of the return on equity measure to

the corresponding GAAP measure.

Q3

Summary

27

Colonial

Penn

§ Earnings

of $7.4 million, up 14% over Q3 2008

• Increase primarily

driven by margin growth

§ Life

sales of $10.6 million, down 12% from Q3 2008

• Consistent with

reduced marketing spend as part of our capital

management efforts

management efforts

• Q3 2009 marketing

costs associated with lead-based advertising

and related fulfillment costs were reduced by $5.3 million (45%)

from Q3 2008

and related fulfillment costs were reduced by $5.3 million (45%)

from Q3 2008

§ YTD

campaign productivity remains consistent with

expectations

Q3

Earnings

28

Colonial

Penn

($

millions)

Trailing

4 Quarter Operating Return on Equity: 14.9%

Management believes

that an analysis of income (loss) before net realized investment gains (losses),

net of

related amortization (a non-GAAP financial measure), is important to evaluate the financial performance of

our business, and is a measure commonly used in the life insurance industry. Management uses this

measure to evaluate performance because realized gains or losses can be affected by events that are

unrelated to a company’s underlying fundamentals. The table on Page 11 reconciles the non-GAAP measure

to the corresponding GAAP measure. See Appendix for a reconciliation of the return on equity measure to

the corresponding GAAP measure.

related amortization (a non-GAAP financial measure), is important to evaluate the financial performance of

our business, and is a measure commonly used in the life insurance industry. Management uses this

measure to evaluate performance because realized gains or losses can be affected by events that are

unrelated to a company’s underlying fundamentals. The table on Page 11 reconciles the non-GAAP measure

to the corresponding GAAP measure. See Appendix for a reconciliation of the return on equity measure to

the corresponding GAAP measure.

Q3

Summary

29

CIG

§ Earnings

of $21.6 million, down 37% vs Q3 2008:

• Additional Universal

Life amortization expense

• Higher expenses

related to litigation settlements

§ NAP

of $20.3 million, up 7% vs Q3 2008

• Turning around three

consecutive quarters of negative sales

comparisons

comparisons

§ Continued

strong sales growth in Specified Disease products

and strong agent recruiting

and strong agent recruiting

CIG

($

millions)

§ Specified

Disease sales up 26% over Q3 2008

§ Worksite

sales continue strong momentum,

up 11% YTD

up 11% YTD

§ Strong

recruiting results in Q3 2009

§ Decrease

in Annuity sales, as expected, due

to shift in focus to Specified Disease and

Worksite sales

to shift in focus to Specified Disease and

Worksite sales

Q3

2008

Q3

2009

Q3

2009 Sales and

Distribution

Results

Annuity

Surrenders

31

CIG

IA

Surrenders

(annualized

quarterly rate)

Non-IA

Surrenders

(annualized

quarterly rate)

*Statistics based on

account value and GAAP reserves.

§ IA

surrenders down significantly

from Q2 2009

from Q2 2009

§ Non-IA

surrenders stable

§ Total

account value:

• IAs - $732

million

• Non-IAs - $370

million

§ Average

account value:*

• IAs -

$44,400

• Non-IAs -

$21,100

§ 65%

of our annuities are still in

surrender charge period:*

surrender charge period:*

• IAs -

99%

• Non-IAs -

34%

Q3

Earnings

32

CIG

Management believes

that an analysis of income (loss) before net realized investment gains (losses),

net of

related amortization (a non-GAAP financial measure), is important to evaluate the financial performance of

our business, and is a measure commonly used in the life insurance industry. Management uses this

measure to evaluate performance because realized gains or losses can be affected by events that are

unrelated to a company’s underlying fundamentals. The table on Page 11 reconciles the non-GAAP measure

to the corresponding GAAP measure. See Appendix for a reconciliation of the return on equity measure to

the corresponding GAAP measure.

related amortization (a non-GAAP financial measure), is important to evaluate the financial performance of

our business, and is a measure commonly used in the life insurance industry. Management uses this

measure to evaluate performance because realized gains or losses can be affected by events that are

unrelated to a company’s underlying fundamentals. The table on Page 11 reconciles the non-GAAP measure

to the corresponding GAAP measure. See Appendix for a reconciliation of the return on equity measure to

the corresponding GAAP measure.

($

millions)

Trailing

4 Quarter Operating Return on Equity: 2.2%

Net

Investment Income

33

CNO

($

millions)

General

Account Investment Income

|

Yield:

|

5.82%

|

5.93%

|

5.67%

|

5.65%

|

5.63%

|

§ Decreases

in 2009 primarily

due to lower new money rates

and increase in cash and short-

term investment balances

compared to prior periods

due to lower new money rates

and increase in cash and short-

term investment balances

compared to prior periods

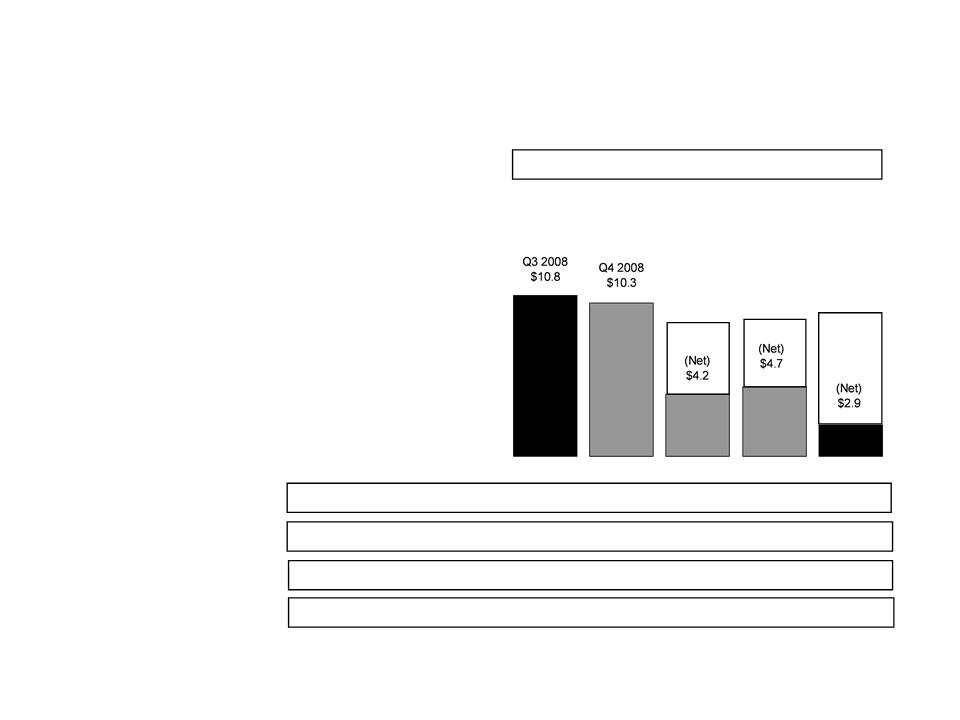

Q3

2009

Net Realized Losses

Net Realized Losses

34

CNO

Gains

on sales

Losses

on sales

Losses

due to recognition of other-

than-temporary

impairments

Amortization

adjustment to insurance

intangibles

Net

investment losses before tax

Tax

benefit

Increase to tax

valuation allowance

Net

investment losses after tax

($

millions)

-

-

$(126.7)

18.7

(108.0)

(38.8)

-

$(69.2)

$99.5

(84.1)

(162.4)

20.1

(126.9)

(45.5)

6.7

$(88.1)

$99.5

(84.1)

(35.7)

1.4

(18.9)

(6.7)

6.7

$(18.9)

Gross

Amounts

Amount

Recognized

through Accumulated

Other Comprehensive

Loss

through Accumulated

Other Comprehensive

Loss

Amount

Recognized

through Net Income

through Net Income

Q3

2009 Impairment Losses

35

CNO

IG

Corporates

Alt-A

ABS

Prime

Jumbos

Commercial Mortgage

Loans

Other

Total

($

millions)

Gross

Amounts

Amount

Recognized

through Accumulated

Other Comprehensive

Income

through Accumulated

Other Comprehensive

Income

Amount

Recognized

through Net Income

through Net Income

$5.5

35.0

14.5

88.3

12.3

6.8

$162.4

$0.0

29.9

12.7

84.1

0.0

0.0

$126.7

$5.5

5.1

1.8

4.2

12.3

6.8

$35.7

Asset

Allocation at 9/30/09*

36

CNO

($

millions)

*Excludes

investments from a variable interest entity which we consolidate under GAAP (the

related liabilities are

non-recourse to Conseco).

non-recourse to Conseco).

Investment

Quality:

Fixed

Maturities*

37

CNO

Actively Managed

Fixed Maturities by Rating at

9/30/09 (Market Value)

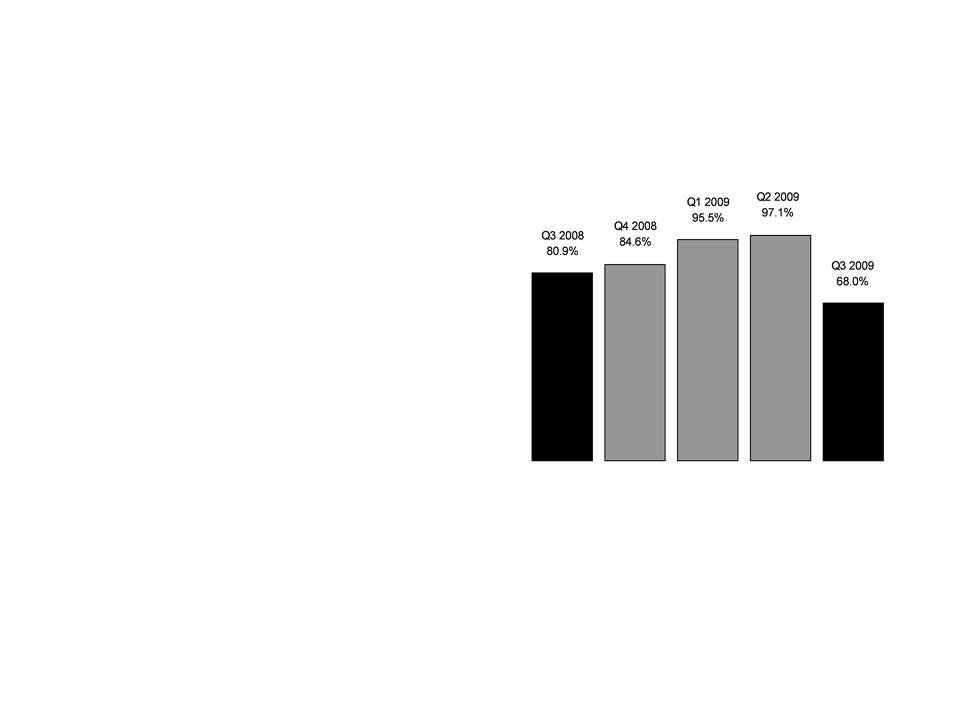

9/30/09 (Market Value)

|

%

of Bonds which are Investment Grade:

|

9/30/08

93%

|

12/31/08

92%

|

3/31/08

91%

|

6/30/09

91%

|

9/30/09

93%

|

*Excludes

investments from a variable interest entity which we consolidate under GAAP (the

related liabilities are

non-recourse to Conseco).

non-recourse to Conseco).

AAA

13%

AA

6%

A

31%

BBB

43%

7%

§ Investment-grade

bonds at 93%:

Impact

of Downgrades

on

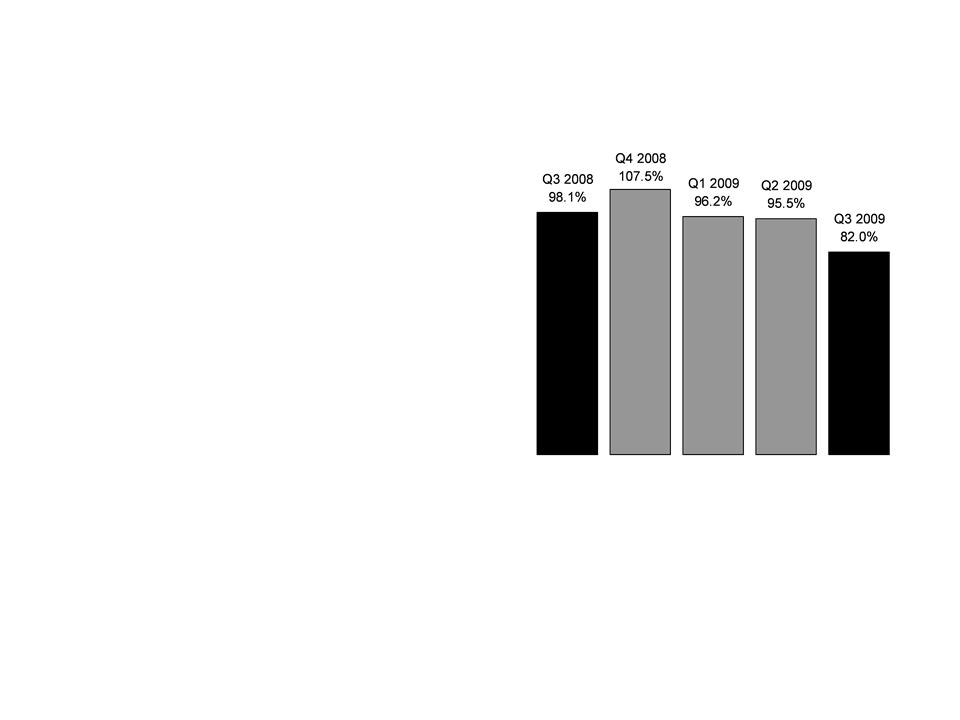

BIG Ratio*

38

CNO

*Actively managed

fixed maturities (market value).

Q3

2009 Downgrades from Investment

Grade to Below Investment Grade

Grade to Below Investment Grade

39

CNO

IG

Corporates

Alt-A

Prime

Jumbo

CMBS

Other

Total

($

millions)

$41.5

9.9

61.1

4.9

52.7

$170.1

7

1

4

2

13

27

(0.7%)

(0.6%)

(0.9%)

(0.1%)

(0.9%)

(3.2%)

Type

Statutory

Book

Value

Value

#

Issues

Effect

of

Downgrades on

Downgrades on

RBC

Ratio*

*Includes estimated

effect of covariance and tax.

RBC

Impact of Downgrades

40

CNO

$753

million

downgraded

$997

million

downgraded

$680

million

downgraded

$825

million

downgraded

§ Ratings downgrades

have resulted in a decrease to our RBC ratio of 50

percentage points over the last four quarters.

percentage points over the last four quarters.

§ Ratings

downgrades

have been significant

have been significant

Alt-A

at 9/30/09

CNO

41

AA

BBB

Total

$13.2

$44.5

$143.4

$201.1

$17.5

$49.1

$193.8

$260.4

6.6%

22.1%

71.3%

100.00%

0.06%

0.21%

0.66%

0.93%

Market

Value

(mil.)

Book

Value

(mil.)

%

of

Alt-A*

%

of

Portfolio*

Rating

§ Allocation reduced

by 46% (book value) from 12/31/08 to 9/30/09

§ No exposure to

“affordability products” - option ARMs, hybrid, neg-ams

§ While delinquencies

are higher than anticipated, collateral performing better than

overall Alt-A market in terms of average delinquency and accumulated loss

overall Alt-A market in terms of average delinquency and accumulated loss

§ Adequate credit

support inherent in structures relative to expected cumulative losses

and recoverability of book values

and recoverability of book values

693

733

710

714

Avg.

FICO

FICO

14.0%

8.2%

10.1%

9.9%

Avg.

Support

9.4%

6.6%

18.9%

15.5%

Avg.

60+

Delinq.

*Market

value.

($

millions)

1.45%

0.50%

1.46%

1.25%

Avg.

Accum.

Loss

Prime

Jumbo at 9/30/09

CNO

42

AAA

AA

A

BBB

Total

$223.8

$59.3

$76.8

$164.2

$197.0

$721.1

$247.0

$64.2

$100.3

$198.4

$314.1

$924.0

31.0%

8.2%

10.7%

22.8%

27.3%

100.00%

1.04%

0.27%

0.35%

0.76%

0.91%

3.34%

Market

Value

(mil.)

Book

Value

(mil.)

%

of

Prime

Jumbo*

Jumbo*

%

of

Portfolio*

Rating

§ 73% investment

grade

§ 3.3% of total

invested assets

§ 46 securitizations -

highly diversified

736

741

744

741

739

739

Avg.

FICO

FICO

7.9%

4.4%

4.8%

5.8%

7.9%

6.5%

Avg.

Support

1.4%

2.1%

3.4%

5.2%

9.2%

4.7%

Avg.

60+

Delinq.

*Market

value.

($

millions)

0.03%

0.11%

0.08%

0.36%

0.59%

0.27%

Avg.

Accum.

Loss

CMBS

by Vintage at 9/30/09

43

CNO

(GAAP

book value - $ millions)

$194.5

$136.0

$138.0

$0.0

$47.0

$53.1

$568.6

$556.1

$34.2

$8.8

$0.0

$14.7

$0.0

$0.0

$57.7

$45.0

$48.2

$13.1

$23.1

$15.6

$0.0

$0.0

$100.0

$60.3

$6.0

$17.2

$69.8

$15.0

$0.0

$0.0

$108.0

$36.8

$0.0

$0.0

$3.0

$3.8

$0.0

$0.0

$6.8

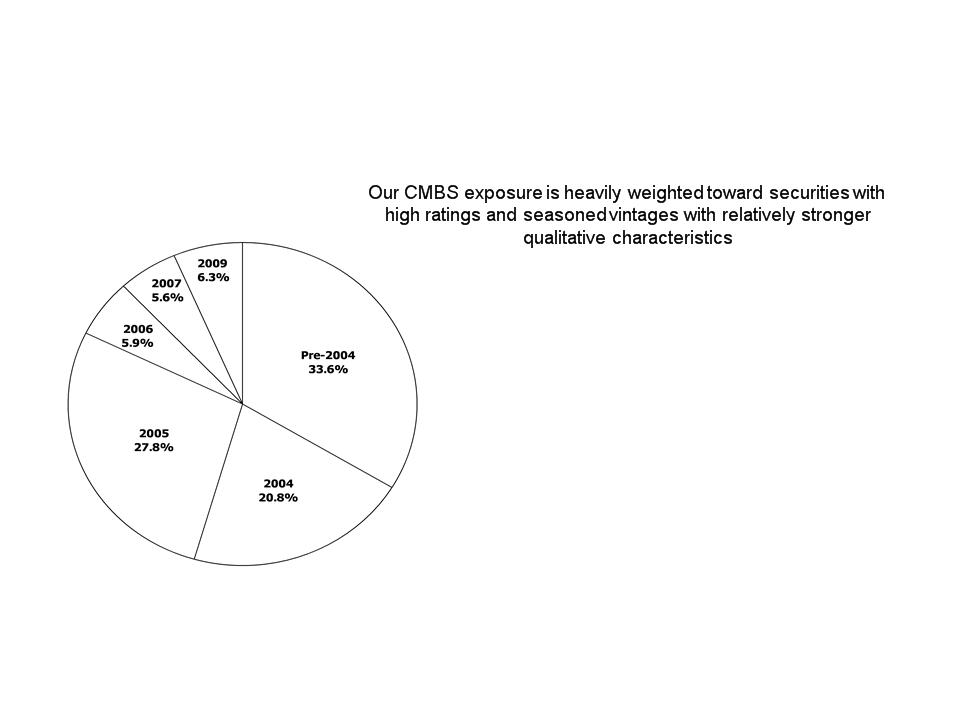

$1.6

Pre-2004

2004

2005

2006

2007

2009

Total

BV

Total

MV

AAA

AA

A

BBB

CMBS

at 9/30/09

CNO

44

AAA

AA

A

BBB

Total

$556.1

$45.0

$60.3

$36.8

$1.6

$699.8

$568.6

$57.7

$100.0

$108.0

$6.8

$841.1

79.5%

6.4%

8.6%

5.3%

0.2%

100.0%

2.57%

0.21%

0.28%

0.17%

0.01%

3.24%

Market

Value

(mil.)

Book

Value

(mil.)

%

of

CMBS*

%

of

Portfolio*

Rating

§ Collateral

performing materially better than overall CMBS market in terms of delinquency

and

cumulative loss

cumulative loss

§ Substantial credit

support inherent in structures relative to expected cumulative

losses

29.7%

22.8%

11.6%

8.6%

6.1%

26.6%

Avg.

Support

1.5%

0.8%

1.3%

1.2%

1.4%

1.4%

Avg.

60+

Del.

& FCR

*% of

market value

($

millions)

0.41%

0.07%

0.12%

0.03%

0.00%

0.34%

Avg.

Cum.

Loss

Commercial

Mortgage Loans

at

9/30/09

By

Vintage

45

CNO

§ Current LTV of

approximately 63.9%

§ Trailing debt

service coverage ratio stable relative to underwritten levels of approximately

1.55

§ Emphasis on reducing

overall allocation via prepayments, etc.

CNO

Summary

46

CNO

§ Third

consecutive quarter of net income

§ Core

sales and agent recruitment continue to improve in declining

market

market

§ Recapitalization

addresses the company’s most pressing financial

priority

priority

• Refinances the 3.5%

convertible debentures

• Structured to

protect the NOLs

• Demonstrates

investor confidence in Conseco

§ Capital

and risk management remain top priorities

• Continue to evaluate

reinsurance opportunities

• Insurance company

merger anticipated in Q1 2010

§ Favorable

target market demographics

47

Questions

and Answers

48

Appendix

Ø Agreement to sell

common stock and issue warrants

to Paulson & Co.

to Paulson & Co.

Ø 16.4MM

shares

Ø 5 million warrants

with a $6.50 exercise

price expiring on 12/30/2016 and not

exercisable until 6/30/2013

price expiring on 12/30/2016 and not

exercisable until 6/30/2013

Ø Aggregate purchase

price of $78MM

Ø Closing upon first

settlement date for new

Convertible Debentures

Convertible Debentures

Ø Refinances $293

million 3.50% convertible

debentures puttable to Conseco on 9/30/2010

debentures puttable to Conseco on 9/30/2010

Ø Preserves

flexibility to raise common equity to

strengthen capital and reduce outstanding senior

secured debt

strengthen capital and reduce outstanding senior

secured debt

Ø Announced intention

to file registration

statement with respect to $200 million of

common equity in the near future

statement with respect to $200 million of

common equity in the near future

Ø Enhances the

Company’s liquidity and capital

positions

positions

Ø Demonstrates

investor confidence in Conseco

Transaction

Highlights

Sale

of Common Stock and Warrants

|

Cash

Tender Offer of Convertible Debenture

|

|

|

For “Any and

All” of 3.50% convertible debenture due 9/30/2035

|

|

|

Tender

Price

|

100% par +

accrued and unpaid interest

|

|

Launch

Date

|

10/15/2009

|

|

Expiration

|

11/12/09

|

|

Financing

|

New convertible

debentures and sale of common stock and

warrants to be issued simultaneously with closing of tender offer |

|

Convertible

Debentures

|

|

|

Total

Issuance

|

Up

to $293MM

|

|

Coupon

|

7.0%

|

|

Conversion

Price

|

$5.49

|

|

Maturity

Date

|

12/30/2016

|

|

Convertibility

|

Non-convertible

until on or after 6/30/2013

|

|

Call

Protection

|

Non-call life;

conversion feature terminable at company’s option at

any time on or after 6/30/2013 if stock trades at or above 140% of the conversion price for at least 20 trading days in a 30 consecutive trading day period |

|

Ranking

|

Senior

unsecured

|

|

Settlement:

|

In

whole or in part based upon success of one or more tender offers

and put or call of outstanding $293MM convertible debentures |

|

Forward

Purchase Commitment

|

|

|

Escrow

|

Purchase price

pre-funded into segregated deposit accounts at Bank

of New York Mellon |

|

Yield

|

7%

annual return on the proceeds in the deposit account provided in

form of discount from par when the Convertible Debentures are issued |

|

Maturity

|

No

later than 10/5/2010

|

CNO

49

Recapitalization

Summary

50

CNO

§ Plan

to file a registration statement with the SEC relating to a

proposed registered offering of common stock

proposed registered offering of common stock

§ Will

use reasonable best efforts to consummate the proposed

registered offering no later than 120 days after the settlement

of the cash tender offer (expected to be by 3/31/10)

registered offering no later than 120 days after the settlement

of the cash tender offer (expected to be by 3/31/10)

§ Required

to use half of net proceeds to pay down

indebtedness under the credit agreement

indebtedness under the credit agreement

§ Remaining

net proceeds would be used for general corporate

purposes

purposes

Proposed

Registered Offering of

Common Stock

Common Stock

Key

Debt Covenants

51

CNO

*Reflects

impact of modification to the covenants which are applicable from March 31, 2009

through June 30,

2010. Effective

with the third quarter of 2010, the covenant margins return to Q4 2008

levels.

**Calculated per

bank covenants; excludes Accumulated Other Comprehensive Loss.

($

millions)

Debt/Capital

Ratio**

Covenant

Maximum

Actual

Interest

Coverage

Covenant

Minimum

Actual

Statutory

Capital

Covenant

Minimum

Actual

RBC

Ratio

Covenant

Minimum

Actual

Q2

2009

Covenant

Margins as of 9/30/09*

Reduction to

statutory capital and

surplus of approximately $269

million, or an increase to the risk-

based capital of approximately

$134 million.

surplus of approximately $269

million, or an increase to the risk-

based capital of approximately

$134 million.

Reduction to

combined statutory

capital and surplus of

approximately $208 million.

capital and surplus of

approximately $208 million.

Reduction in cash

flows to the

holding company of

approximately $101 million.

holding company of

approximately $101 million.

Reduction to

shareholders’ equity of

approximately $831 million or

additional debt of $400 million.

approximately $831 million or

additional debt of $400 million.

Q4

2008

30.0%

28.3%

2.00X

2.35X

$1,270

$1,366

250%

255%

Q1

2009

32.5%

27.9%

1.50X

3.07X

$1,100

$1,301

200%

230%

32.5%

27.0%

1.50X

3.31X

$1,100

$1,279

200%

247%

Q3

2009

32.5%

26.8%

1.50X

3.12X

$1,100

$1,308

200%

252%

Book

Value Per Share*

52

CNO

*Book

value excludes accumulated other comprehensive income (loss). See Appendix for

corresponding GAAP

measure.

measure.

§ Increase

from Q2 2009 due to

Q3 2009 net income

Q3 2009 net income

Commercial

Mortgage Loans

at

9/30/09

Geographic

Distribution

53

CNO

Pacific

8.6%

Mountain

9.5%

West

North

Central

Central

12.7%

West

South

Central

Central

5.7%

East

North

Central

Central

22.0%

East

South

Central

Central

5.3%

New

England

8.7%

Middle

Atlantic

Atlantic

6.3%

South

Atlantic

Atlantic

21.2%

Commercial

Mortgage Loans

at

9/30/09

By

Maturity

54

CNO

($

millions)

Expenses

55

CNO

($

millions)

Adjusted Operating

Expenses*

*Adjusted operating

expenses exclude primarily acquisition costs, capitalization of software

development

costs, initial PFFS marketing costs and contractual vacancy charges related to exiting the Merchandise Mart

in Chicago. This measure is used by the Company to evaluate its progress in reducing operating expenses.

Expenses have been restated for all periods to reflect the SHIP separation.

costs, initial PFFS marketing costs and contractual vacancy charges related to exiting the Merchandise Mart

in Chicago. This measure is used by the Company to evaluate its progress in reducing operating expenses.

Expenses have been restated for all periods to reflect the SHIP separation.

§ Approximately $20

million in savings

from back-office consolidation

realized in 2007 and 2008; remaining

$5 million expected in 2009

from back-office consolidation

realized in 2007 and 2008; remaining

$5 million expected in 2009

§ Q3 2009 reflects

leveling off to more

stable level following quarter of high

taxes and insurance and premium

tax payments, and reduction of

consulting expense

stable level following quarter of high

taxes and insurance and premium

tax payments, and reduction of

consulting expense

Segment

Performance

56

Bankers

*Operating earnings

exclude net realized gains (losses). See

Appendix for corresponding GAAP measure of

our consolidated results of operations.

our consolidated results of operations.

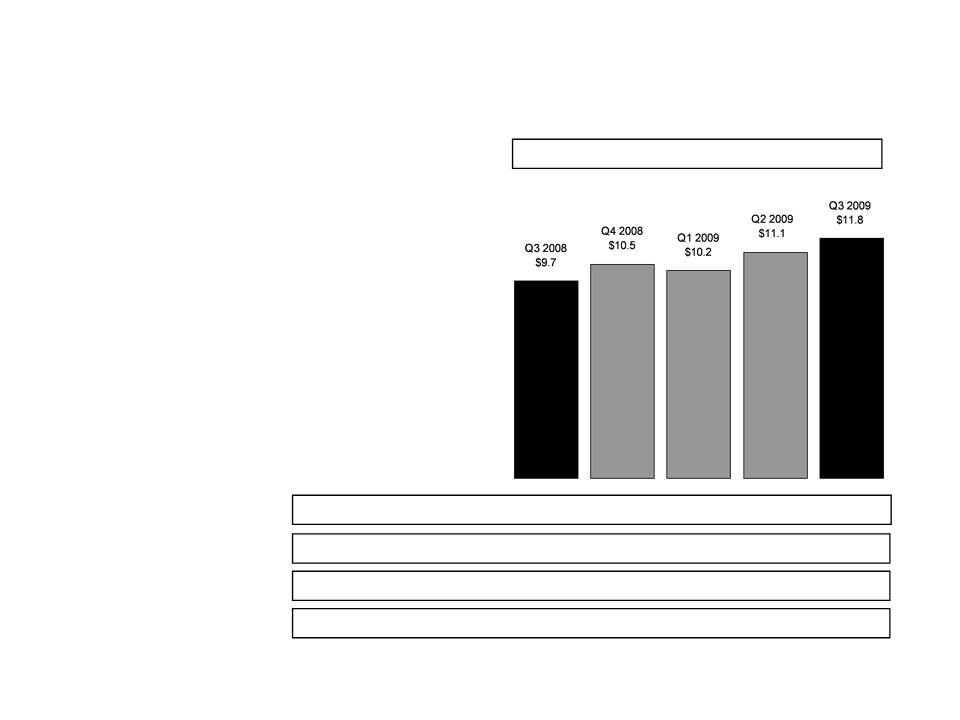

PTOI-Trailing 4

Quarters: $189.8 $171.5 $187.1 $215.8 $233.4

Revenues-Quarterly: $679.1 $691.4 $635.1 $662.8 $695.1

Pre-Tax

Operating Income*

Revenues -Tr. 4

Quarters: $2,594.5 $2,679.1 $2,686.3 $2,668.4 $2,684.4

($

millions)

§ Earnings

up 26% vs Q3 2008,

positively affected by:

positively affected by:

• Higher PFFS/PDP

income

• Increase in

COLI

§ Offset

by lower LTC margins

Premiums

-

Medicare

Supplement

57

Bankers

§ First-year

premiums up 15%

vs Q3 2008

vs Q3 2008

Med.

Supp. First-Year Prems.-Tr. 4 Qtrs: $79.3 $81.3 $81.9 $83.6 $86.5

Med.

Supp. Total Premiums-Quarterly: $153.8 $172.3 $155.8 $155.2 $168.9

Med.

Supp. NAP-Quarterly: $16.6 $27.9 $18.4 $19.2 $19.9

Med.

Supp. NAP-Trailing 4 Quarters: $73.7 $78.6 $79.9 $82.1 $85.4

($

millions)

Premiums

-

Long-Term

Care

58

Bankers

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $43.9 $42.7 $35.9 $30.0 $22.1

Total

Premiums-Quarterly: $154.8 $159.1 $145.9 $151.9 $154.3

Long-Term Care -

First-Year Premiums*

NAP-Quarterly: $11.4 $7.9 $7.5 $9.8 $9.8

NAP-Trailing 4

Quarters: $42.3 $39.4 $37.5 $36.6 $35.0

*Includes $4.4

million in both Q1 2009 and Q2 2009 and $6.6 million in Q3 2009 of premiums

ceded

under

new business reinsurance agreement.

Q2

2009

(Direct)

$9.1

Q1

2009

(Direct)

$8.6

Q3

2009

(Direct)

$9.5

§ Quarterly

first-year premium

declines due to new business

reinsurance

declines due to new business

reinsurance

§ NAP

decline attributable to three

main factors:

main factors:

• Overall industry

sales decline

• Agent force shift

toward other products

• Tightened

underwriting

Premiums

-

Life

Insurance

59

Bankers

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $81.8 $80.7 $79.0 $75.9 $79.8

Total

Premiums-Quarterly: $51.9 $55.7 $48.9 $55.3 $63.2

Life -

First-Year Premiums

NAP-Quarterly: $13.1 $11.4 $12.6 $15.6 $15.8

NAP-Trailing 4

Quarters: $53.6 $51.9 $52.8 $52.7 $55.4

SPWL

Non-

SPWL

$7.5

$12.0

Q3

2008

$19.5

Q4

2008

$20.2

$8.2

$12.0

Q1

2009

$16.8

$6.2

$10.6

Q2

2009

$19.4

$7.8

$11.6

Q3

2009

$23.4

$10.5

$12.9

§ Fluctuations

in first-year

premiums primarily reflect

variance in sales of single-

premium policies

premiums primarily reflect

variance in sales of single-

premium policies

§ Non-SPWL

premiums up 8%

vs Q3 2008

vs Q3 2008

Premiums

-

Annuity

60

Bankers

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $1,031.3 $1,220.6 $1,294.1 $1,308.7 $1,270.3

Total

Premiums-Quarterly: $323.1 $411.2 $302.1 $275.4 $284.7

Annuity

- First-Year Premiums

§ Annuity

first-year premiums

down 12% from Q3 2008

down 12% from Q3 2008

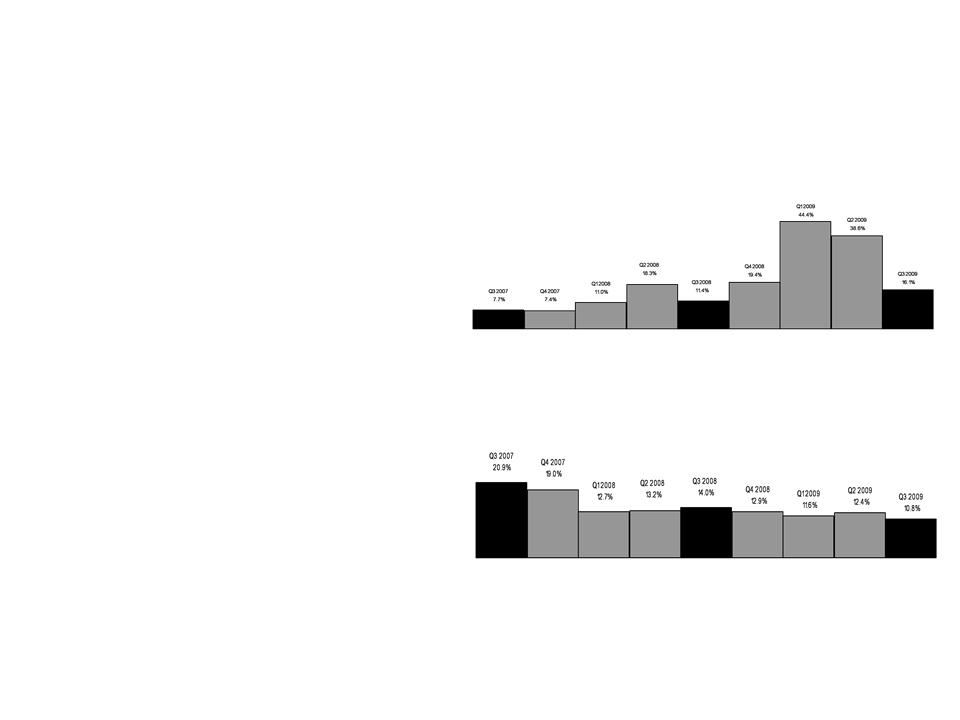

Benefit

Ratio* - PDP

61

Bankers

*We

calculate benefit ratios by dividing insurance policy benefits by insurance

policy income.

§ Down

16% vs Q3 2008

§ Impacted

by mid-year premium

sweeps and favorable claims

experience

sweeps and favorable claims

experience

Benefit

Ratio* -

PFFS

Individual Business

62

Bankers

*We

calculate benefit ratios by dividing insurance policy benefits by insurance

policy income.

§ Comparison

vs Q3 2008

impacted by premium sweeps

and favorable IBNR development

impacted by premium sweeps

and favorable IBNR development

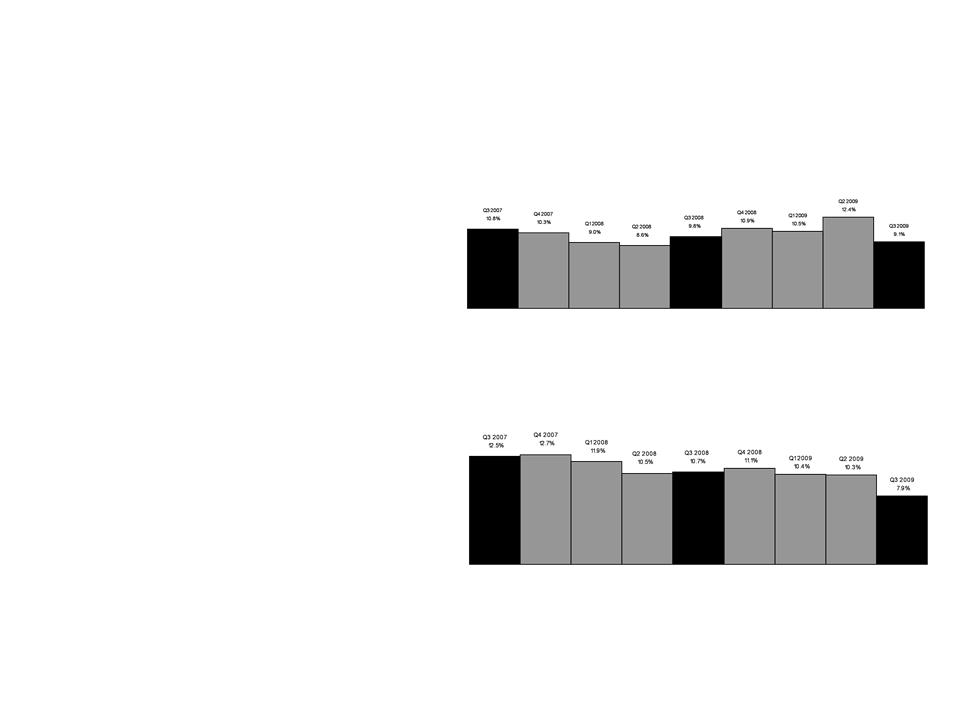

Interest-Adjusted

Benefit Ratio* -

Long

Term Care

63

Bankers

*We

calculate interest-adjusted benefit ratios by dividing insurance policy benefits

less interest income on

the accumulated assets backing the insurance liabilities by insurance policy income.

the accumulated assets backing the insurance liabilities by insurance policy income.

Trailing 4 Quarter

Avg.: 74.9% 74.0% 71.4% 67.6% 68.2%

Qtrly.

non-int. adjusted: 102.1% 102.2% 105.1% 103.2% 108.3%

§ Q3

2009 positively impacted by

continued stabilization of

incurred claims and excess

terminations

continued stabilization of

incurred claims and excess

terminations

Segment

Performance

64

Colonial

Penn

*Operating earnings

exclude net realized gains (losses). See

Appendix for corresponding GAAP measure of

our consolidated results of operations.

our consolidated results of operations.

PTOI-Trailing 4

Quarters: $18.3 $25.2 $26.6 $29.3 $30.2

Revenues-Quarterly: $57.0 $57.2 $57.1 $62.7 $58.1

Pre-Tax

Operating Income*

Revenues -Tr. 4

Quarters: $213.3 $226.2 $229.4 $234.0 $235.1

($

millions)

§ Q3

2008 to Q3 2009 change affected by

margin growth

margin growth

§ Q2

2009 to Q3 2009 change affected by:

• Lower margin from

non-recurring

reinsurance pool termination in Q2 2009

reinsurance pool termination in Q2 2009

• Lower margin due to

seasonality

• Higher amortization

charges

Premiums

-

Life

Insurance

65

Colonial

Penn

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $33.7 $35.0 $35.8 $35.3 $34.4

Total

Premiums-Quarterly: $43.6 $43.8 $47.0 $45.8 $45.6

Life -

First-Year Premiums

NAP-Quarterly: $12.1 $10.8 $12.3 $10.6 $10.6

NAP-Trailing 4

Quarters: $48.6 $50.1 $49.7 $45.8 $44.3

§ NAP:

• Quarterly and

trailing four quarters

consistent with expectations arising

from capital management

consistent with expectations arising

from capital management

§ Premium:

• First-year premium

trending lower due

to capital management

to capital management

Segment

Performance

66

CIG

*Operating earnings

exclude net realized gains (losses). See Appendix for corresponding GAAP

measure

of our consolidated results of operations.

of our consolidated results of operations.

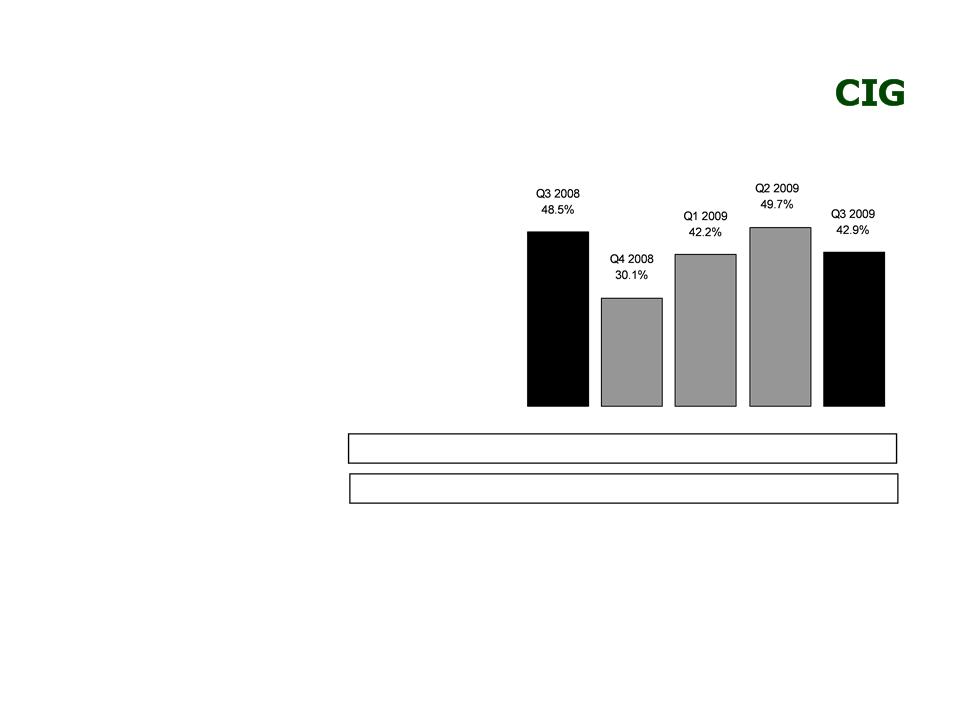

PTOI-Trailing 4

Quarters: $99.4 $121.3 $129.2 $118.1 $105.5

Revenues-Quarterly: $371.8 $382.4 $379.2 $382.5 $381.2

Pre-Tax

Operating Income*

Revenues-Tr. 4

Quarters: $1,511.3 $1,513.1 $1,511.7 $1,515.9 $1,525.3

($

millions)

§ Lower

Universal Life results

primarily due to additional

amortization expense

primarily due to additional

amortization expense

§ Higher

expenses related to

litigation settlements

litigation settlements

Premiums

-

Medicare

Supplement

67

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $10.6 $9.6 $8.3 $7.9 $8.0

Total

Premiums-Quarterly: $48.5 $52.6 $42.8 $44.4 $46.9

Medicare

Supplement -

First-Year Premiums

NAP-Quarterly: $1.8 $3.5 $1.7 $1.3 $1.3

NAP-Trailing 4

Quarters: $8.9 $8.9 $8.3 $8.3 $7.8

Premiums

-

Specified

Disease

68

CIG

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $37.6 $39.4 $40.2 $41.5 $43.6

Total

Premiums-Quarterly: $92.3 $95.6 $93.0 $95.1 $96.2

Specified

Disease -

First-Year Premiums

NAP-Quarterly: $12.8 $12.0 $11.5 $14.7 $16.1

NAP-Trailing 4

Quarters: $46.1 $46.8 $48.7 $51.0 $54.3

§ NAP

up 26% from Q3 2008:

• Increased PMA focus

on

Specified Disease products

Specified Disease products

• Increased

recruitment of Health

IMOs

IMOs

• Momentum increasing

in

Worksite market

Worksite market

Premiums

-

Annuity

69

CIG

($

millions)

First-Year

Prems.-Tr. 4 Qtrs: $155.3 $119.9 $98.5 $84.7 $83.0

Total

Premiums-Quarterly: $27.4 $23.7 $19.5 $22.3 $25.2

Annuity

- First-Year Premiums

§ First-year

collections down

7% from Q3 2008:

7% from Q3 2008:

• Discontinuance of

products due

to an annuity coinsurance

transaction

to an annuity coinsurance

transaction

• Focus on profitable

products

(i.e., Specified Disease)

(i.e., Specified Disease)

Benefit

Ratio* -

Medicare

Supplement

70

CIG

Trailing 4 Quarter

Avg.: 69.1% 68.4% 68.8% 68.6% 67.3%

*We

calculate benefit ratios by dividing insurance policy benefits by insurance

policy income.

§ In

line with expectations and

recent trends

recent trends

§ Stable

persistency

Interest-Adjusted

Benefit Ratio* -

Specified

Disease

71

Trailing 4 Quarter

Avg.: 47.4% 43.3% 41.8% 42.6% 41.2%

Qtrly.

non-int. adjusted: 82.6% 63.8% 76.0% 83.3% 76.6%

*We

calculate interest-adjusted benefit ratios by dividing insurance policy

benefits, less interest income on

the accumulated assets backing the insurance liabilities, by insurance policy income.

the accumulated assets backing the insurance liabilities, by insurance policy income.

§ Q3

2008 included recognition of

deferred ROP adjustment

related to prior periods

deferred ROP adjustment

related to prior periods

72

Information Related to Certain Non-GAAP Financial Measures

The

following provides additional information regarding certain non-GAAP measures

used in this presentation. A

non-GAAP measure is a

numerical measure of a company’s performance, financial position, or cash flows that excludes or includes amounts that are normally excluded

or included in the most directly comparable measure calculated and presented in accordance with GAAP. While management believes these

measures are useful to enhance understanding and comparability of our financial results, these non-GAAP measures should not be considered

as substitutes for the most directly comparable GAAP measures. Additional information concerning non-GAAP measures is included in our

periodic filings with the Securities and Exchange Commission that are available in the “Investor - SEC Filings” section of Conseco’s website,

www.conseco.com.

numerical measure of a company’s performance, financial position, or cash flows that excludes or includes amounts that are normally excluded

or included in the most directly comparable measure calculated and presented in accordance with GAAP. While management believes these

measures are useful to enhance understanding and comparability of our financial results, these non-GAAP measures should not be considered

as substitutes for the most directly comparable GAAP measures. Additional information concerning non-GAAP measures is included in our

periodic filings with the Securities and Exchange Commission that are available in the “Investor - SEC Filings” section of Conseco’s website,

www.conseco.com.

Operating

earnings measures

Management believes that an analysis of net income applicable to common stock before net realized gains or losses, discontinued operations

and increases to our valuation allowance for deferred tax assets (“net operating income,” a non-GAAP financial measure) is important to

evaluate the performance of the Company and is a key measure commonly used in the life insurance industry. Management uses this measure

to evaluate performance because realized investment gains or losses, discontinued operations and increases to our valuation allowance for

deferred tax assets are unrelated to the Company’s continuing operations.

Management believes that an analysis of net income applicable to common stock before net realized gains or losses, discontinued operations

and increases to our valuation allowance for deferred tax assets (“net operating income,” a non-GAAP financial measure) is important to

evaluate the performance of the Company and is a key measure commonly used in the life insurance industry. Management uses this measure

to evaluate performance because realized investment gains or losses, discontinued operations and increases to our valuation allowance for

deferred tax assets are unrelated to the Company’s continuing operations.

Information Related to Certain Non-GAAP Financial Measures

A

reconciliation of net income applicable to common stock to net operating income

(and related per-share amounts) is as follows (dollars in

millions, except per-share amounts):

millions, except per-share amounts):

Book

value, excluding accumulated other comprehensive income, per share

This non-GAAP financial measure differs from book value per diluted share because accumulated other comprehensive income has been

excluded from the book value used to determine the measure. Management believes this non-GAAP financial measure is useful because it

removes the volatility that arises from changes in accumulated other comprehensive income. Such volatility is often caused by changes in the

estimated fair value of our investment portfolio resulting from changes in general market interest rates rather than the business decisions made

by management.

This non-GAAP financial measure differs from book value per diluted share because accumulated other comprehensive income has been

excluded from the book value used to determine the measure. Management believes this non-GAAP financial measure is useful because it

removes the volatility that arises from changes in accumulated other comprehensive income. Such volatility is often caused by changes in the

estimated fair value of our investment portfolio resulting from changes in general market interest rates rather than the business decisions made

by management.

A

reconciliation from book value per share to book value per share, excluding

accumulated other comprehensive income (loss) is as follows

(dollars in millions, except per share amounts):

(dollars in millions, except per share amounts):

Information Related to Certain Non-GAAP Financial Measures

75

Operating

return measures

Management believes

that an analysis of return before net realized gains or losses, discontinued

operations and increases to our valuation

allowance for deferred tax assets (“net operating income,” a non-GAAP financial measure) is important to evaluate the performance of the

Company and is a key measure commonly used in the life insurance industry. Management uses this measure to evaluate performance

because realized investment gains or losses, discontinued operations and increases to our valuation allowance for deferred tax assets are

unrelated to the Company’s continued operations.

allowance for deferred tax assets (“net operating income,” a non-GAAP financial measure) is important to evaluate the performance of the

Company and is a key measure commonly used in the life insurance industry. Management uses this measure to evaluate performance

because realized investment gains or losses, discontinued operations and increases to our valuation allowance for deferred tax assets are

unrelated to the Company’s continued operations.

This

non-GAAP financial measure also differs from return on equity because

accumulated other comprehensive income (loss) has been

excluded from the value of equity used to determine this ratio. Management believes this non-GAAP financial measure is useful because it

removes the volatility that arises from changes in accumulated other comprehensive income (loss). Such volatility is often caused by changes in

the estimated fair value of our investment portfolio resulting from changes in general market interest rates rather than the business decisions

made by management.

excluded from the value of equity used to determine this ratio. Management believes this non-GAAP financial measure is useful because it

removes the volatility that arises from changes in accumulated other comprehensive income (loss). Such volatility is often caused by changes in

the estimated fair value of our investment portfolio resulting from changes in general market interest rates rather than the business decisions

made by management.

In

addition, our equity includes the value of significant net operating loss

carryforwards (included in income tax assets). In

accordance with

GAAP, these assets are not discounted, and accordingly will not provide a return to shareholders (until after it is realized as a reduction to taxes

that would otherwise be paid). Management believes that excluding this value from the equity component of this measure enhances the

understanding of the effect these non-discounted assets have on operating returns and the comparability of these measures from period-to-

period. Operating return measures are used in measuring the performance of our business units and are used as a basis for incentive

compensation.

GAAP, these assets are not discounted, and accordingly will not provide a return to shareholders (until after it is realized as a reduction to taxes

that would otherwise be paid). Management believes that excluding this value from the equity component of this measure enhances the

understanding of the effect these non-discounted assets have on operating returns and the comparability of these measures from period-to-

period. Operating return measures are used in measuring the performance of our business units and are used as a basis for incentive

compensation.

All

references to segment operating return measures assume a 25% debt to total

capital ratio at the segment level. Additionally,

corporate

expenses have been allocated to the segments.

expenses have been allocated to the segments.

Information Related to Certain Non-GAAP Financial Measures

A

reconciliation of return on common equity to operating return on common equity

(excluding accumulated other comprehensive income (loss) and

net operating loss carryforwards) is as follows (dollars in millions, except per share amounts):

net operating loss carryforwards) is as follows (dollars in millions, except per share amounts):

Information Related to Certain Non-GAAP Financial Measures

77

A

reconciliation of pretax operating earnings (a non-GAAP financial measure) to

segment operating income (loss) and consolidated net income

(loss) for the nine months ended September 30, 2009, is as follows (dollars in millions):

(loss) for the nine months ended September 30, 2009, is as follows (dollars in millions):

(Continued on next

page)

Information Related to Certain Non-GAAP Financial Measures

78

A

reconciliation of common shareholders’ equity, excluding accumulated other

comprehensive income (loss) and net operating loss

carryforwards (a non-GAAP financial measure) to common shareholders’ equity at September 30, 2009, is as follows (dollars in millions):