Attached files

| file | filename |

|---|---|

| EX-21 - SUBSIDIARIES OF THE COMPANY - IOTA COMMUNICATIONS, INC. | exh21_16581.htm |

| EX-32.1 - 906 CERTIFICATION OF THE C.E.O. - IOTA COMMUNICATIONS, INC. | exh32-1_16581.htm |

| EX-31.2 - 302 CERTIFICATION OF THE C.F.O. - IOTA COMMUNICATIONS, INC. | exh31-2_16581.htm |

| EX-32.2 - 302 CERTIFICATION OF THE C.F.O. - IOTA COMMUNICATIONS, INC. | exh32-2_16581.htm |

| EX-31.1 - 302 CERTIFICATION OF THE C.E.O. - IOTA COMMUNICATIONS, INC. | exh31-1_16581.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended May 31, 2009

o TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________ to ______________

Commission file number: 0-27587

ARKADOS GROUP, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

22-3586087 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

|

220 Old New Brunswick Road, Piscataway, NJ |

08854 | |

|

(Address of principal executive offices) |

Zip code | |

|

Issuer’s telephone number: (732) 465-9300 |

||

|

Securities registered under Section 12(b) of the Exchange Act: | ||

|

Title of each class |

Name of each exchange on which registered | |

|

Securities registered under Section 12(g) of the Exchange Act: | ||

Common Stock, $.0001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

o Yes x No

Indicate by a check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past

90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. (See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act). (Check one):

|

Large accelerated filer o

Non-Accelerated filer o |

Accelerated filer o

Smaller reporting company x |

Indicate by check mark wither the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price ($.08) at which the common equity was last sold on October 12, 2009 was $ 1,746,097

The number of shares of common stock outstanding as of the latest practicable date, October 12, 2009, was 32,738,397.

_______________

(1) The information provided shall in no way be construed as an admission that any person whose holdings are excluded from the figure is not an affiliate or that any person whose holdings are included is an affiliate and any such admission is hereby disclaimed.

FISCAL 2008 FORM 10-K

INDEX

|

Item |

Page |

|

PART I |

|

|

ITEM 1: Business |

4 |

|

ITEM 1A: Risk Factors |

22 |

|

ITEM 1B: Unresolved Staff Comments |

33 |

|

ITEM 2: Properties |

33 |

|

ITEM 3: Legal Proceedings |

33 |

|

ITEM 4: Submission of Matters to a Vote of Security Holders |

33 |

|

PART II |

|

|

ITEM 5: Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

34 |

|

ITEM 6: Selected Financial Data |

36 |

|

ITEM 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations |

37 |

|

ITEM 7A:Quantitative and Qualitative Disclosures About Market Risk |

41 |

|

ITEM 8: Financial Statements and Supplementary Data |

41 |

|

ITEM 9: Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

43 |

|

ITEM 9A:Controls and Procedures |

43 |

|

ITEM 9B: Other Information |

44 |

|

PART III |

|

|

ITEM 10: Directors, Executive Officers and Corporate Governance |

45 |

|

ITEM 11: Executive Compensation |

48 |

|

ITEM 12: Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

54 |

|

ITEM 13: Certain Relationships and Related Transactions, and Director Independence |

57 |

|

ITEM 14: Principal Accountant Fees and Services |

59 |

|

PART IV |

|

|

ITEM 15: Exhibits and Financial Statement Schedules |

60 |

|

Signatures |

68 |

NOTE RE: FORWARD LOOKING INFORMATION

All statements in this annual report on Form 10-K that are not historical are forward-looking statements, including statements regarding our “expectations,” “beliefs,” “hopes,” “intentions,” “strategies,” or the like. Such statements are based on management’s current expectations

and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those set forth or implied by any forward looking statements. Some of these risks are detailed in Part I, Item 1A “Risk Factors” and elsewhere in this report. We caution investors that there can be no assurance that actual results or business conditions will not differ materially from those projected or suggested in such forward-looking statements as a result of various factors, including,

but not limited to, the risk factors discussed in this Annual Report on Form 10-K. We expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations with regard thereto or any change in events, conditions, or circumstances on which any such statements are based.

NOTE RE: CERTAIN MARKS

This Annual Report on Form 10-K contains registered and unregistered trademarks of Arkados Group, Inc and its subsidiaries and other companies, as indicated. Unless otherwise clear from the context or noted in this Annual Report, marks identified by “ ® ”

and “™” are registered marks and trademarks of Arkados Group, Inc. or its subsidiaries. All other trademarks and service marks are the property of their respective owners. iPod® is a registered trademark of Apple Computer, Inc. HomePlug® is a registered trademark of the HomePlug Powerline Alliance,

of which Arkados is a member.

|

ITEM 1. |

BUSINESS. |

General

The registrant, Arkados Group, Inc., was incorporated in the State of Delaware in 1998.

We are principally engaged in developing and marketing technology and solutions enabling broadband communication, multimedia, and networking over standard household electrical lines. We conduct these activities principally through Arkados, Inc., which is a wholly owned subsidiary. In September 2006, we changed our corporate name from CDKnet.com,

Inc., to its current form to align our corporate identity with the “Arkados” brand developed by our subsidiary. Our Arkados subsidiary is a member of the HomePlug Powerline Alliance, an independent trade organization which has developed global specifications for high-speed powerline communications, and the Institute of Electrical and Electronics Engineers (IEEE), the world’s leading professional association for the advancement of technology.

Our executive offices are located at 220 Old New Brunswick Road, Piscataway, NJ 08854. We can be reached at our principal offices by telephone at (732) 465-9300. Arkados maintains a website at www.arkados.com.

Except for the documents on our website that are expressly incorporated by reference into this report, the information contained on our website is not incorporated by reference into this report and should not be considered to be a part of this report. This includes the website referred to in the paragraph above, as well as other websites

that we refer to elsewhere in this report. All of these website addresses are included in this document as inactive textual references only.

Available Information

We file annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and all other reports, and amendments to these reports, required of public companies with the SEC. The public may read and copy the materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street NE,

Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website at http://www.sec.gov that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. Copies of our fiscal 2008 Form 10-K may also be obtained without charge by mailing a request to us at 220 Old New Brunswick Road, Piscataway, NJ 08854 or by calling us at (732) 465-9300.

Overview

Arkados provides both hardware and software engines for a wide variety of products that enable high-speed digital transmission of music, movies, video, voice, smart grid applications, and broadband data over the existing infrastructure of electrical power lines.

By combining our system-on-chip (SoC) semiconductors with software and hardware platform designs, our solutions address diverse target markets in a number of growing market categories.

We began the transition from development stage company in fiscal year ended May 31, 2008 by generating revenue of $855,676 and generated $763,040 of revenue in the fiscal year ended May 31, 2009. During Fiscal 2009, we obtained a second extension of convertible subordinated notes which expired June 30, 2009, obtained a limited waiver of

anti-dilution rights held the holders of secured convertible notes to facilitate equity financing, and added Harris Cohen to our board of directors. As of September 30, 2009, $12,254,363 of secured debt, of which $3,462,067 is held by related parties, outstanding at May 31, 2009 is in default, as is $999,733 principal and interest on unsecured notes due June 29, 2009. In addition, as of September 30, 2009, $2,639,057 of salary remains due to our employees and our accounts payable was approximately

$1,751,084, of which $1,710,084 was over 90 days. We continue to negotiate with the holders of each class of debt to fashion a forbearance agreement, compromise or convert outstanding debt into equity and thereby facilitate raising additional investor capital. We have reached a general understanding with the holders of approximately 83% of secured debt as to the terms and conditions upon which they would agree to accept partial payment of principal and convert the balance of secured debt

to equity, however, there is no binding agreement on anyone’s part to do so and no assurance can be given that the terms will be acceptable to the holders of all of the secured debt. We have also received indications of interest from potential private and strategic investors concerning the terms and conditions upon which they would make an investment in Arkados, including the terms upon which the secured debt and other debt would have to be compromised and converted for them to make such investments,

but there is no binding commitment on anyone’s part to complete the transactions. Finally, without commitment on anyone’s part, we have discussed converting a substantial portion of

- 4 -

past due compensation with our employees if the financing and restructuring of our debt can be completed. Pending the completion of these transactions, we are financing operations by issuing bridge notes to investors that would participate in an equity financing if the debt can be restructured. If the financing proceeds,

these investors would be able to make the equity investment in Arkados at a discount of 33% from the price other investors are offered. In the event the financing is not completed, the bridge notes are due with interest at the annual rate of 8% on January 31, 2009.

We have designed our turnkey solutions to be used inside products for both consumers and industry. For example, consumer products can use Arkados solutions as part of a connected home entertainment and computing network, while industry can implement Arkados solutions as a part of a utility company’s “smart grid” and “green

energy” solutions.

We are a “fabless” semiconductor company, meaning we design semiconductors without the capital requirements of owning and operating a fabrication facility; Arkados semiconductors are made from our designs by independent fabricators. We offer our customers complete hardware and software design solutions that allow

them to build devices that will distribute audio, video, voice, and data content throughout the whole house, building, or “smart-grid” infrastructure.

Recent Announcements

Despite the extraordinary challenges of our financial position, Fiscal 2009 brought a number of significant announcements that solidified our relationships with STMicroelectronics, Freescale Semiconductor, and Tatung. Also, Arkados customers devolo AG, Checkolite, Russound, NuVo, and IOGEAR made announcements of products based on our chip.

In October 2008, we announced an agreement with STMicroelectronics to develop and manufacture a 200 Mbit per second, HomePlug AV wideband powerline modem System-on-Chip (SoC). Planned for availability mid-2010, the world’s first HomePlug AV SoC is designed to power applications ranging from simple Ethernet-to-powerline bridges to

full-featured products as wide ranging as HDTV distribution, digital set-top boxes, IPTV, whole-house audio, networked digital picture frames, surveillance systems, and also industrial and commercial applications, especially targeting the Smart Grid and Green Energy segments. STMicroelectronics is largest semiconductor manufacturer to announce plans to bring a HomePlug AV chip to market, and, based on announced product plans of other HomePlug members, we believe this chip will be the only chip available in the

near term that will be interoperable with three established powerline standards: TIA-1113/HomePlug 1.0, HomePlug AV, and the recently confirmed IEEE 1901 Baseline Standard.

In January 2009, Arkados announced a new initiative with Freescale Semiconductor, Inc. to bring a versatile “Whole-House Audio In a Box™” platform to market. The platform uses Arkados’ HomePlug® based multimedia streaming technology,

and Freescale’s Synkro wireless communications technology, enabling untethered devices to control and monitor the system and display live data.

In August 2008, we announced a relationship with the $7B global Original Design Manufacturer (ODM) Tatung. The collaborative relationship between Tatung and Arkados constitutes a one-stop shop for the industry’s technology and manufacturing needs for distributing digital content in homes. Together, the companies deliver complete product

solutions to consumer product manufacturers – from audio input/output devices, to integrated speakers, to control units. By coupling Tatung’s product design and manufacturing with the Arkados technology platform, the companies can deliver turnkey products to brand-name manufacturers. We announced how we have built on this relationship in June 2009 by demonstrating the capability to connect Smart Grid applications and in-home consumer applications over one network. The demonstration at Computex featured

Tatung’s smart meter connected to an Electricity Control Center via a WiMAX network, and a number of in-home entertainment applications connected via an Arkados powered HomePlug powerline network. Devices residing on the HomePlug network enable home video surveillance, control of electricity usage, and home entertainment.

The global market leader in HomePlug products, devolo AG, used the recent CeBIT 2009 show in Germany to introduce the dLAN Audio World system, which is based on Arkados solutions. It is the world’s first system to combine an iPod® dock with multiple

active speakers, using powerline communications to instantly create whole-house music.

Arkados was also recognized through awards given to the products of our customers: Checkolite International received a “CES Best of the Best” award from G4 Television for a system that combines whole-house audio with lighting control; Russound’s Collage and NuVo’s Renovia systems were each recognized as Honorees

in the 2009 CES Innovations awards.

Both the NuVo and Russound systems were displayed at the 2009 Electronic House Expo (EHX) and were singled out by CE Pro magazine in a list of Ten Products to Watch for in 2009. Each system is built around the Arkados chip and software platform. Both companies have begun significant marketing campaigns as the products plan to

begin roll out later this year.

- 5 -

The recognition of our customers’ products follows a major award received by Arkados in January 2008 from G4 Television. The Arkados HomePlug system-on-chip and software solution won the award on the strength of its embedded solution powering the IOGEAR Powerline Stereo Audio System which creates whole-house music at a fraction of the cost of dedicated installed systems. The IOGEAR

product is now on sale and has received very positive reviews, including a 4-star rating from About.com that called the product “a giant step forward in multiroom audio.”1

Arkados Products

Our highly integrated semiconductors provide the internet or network connections over existing electric lines for new consumer electronic products (such as stereo systems, television sets, intercoms and personal iPods®) and smart grid applications. Our solutions

can also be used for bridging legacy products with newer home networking and broadband communications technologies.

Arkados solutions offer a completely different approach than our competitors. Our solutions incorporate a processor and multiple interfaces into the same chip that houses HomePlug communication technology, as well as provide application-level software that runs on the chip. We believe this “system-on-a-chip”

approach provides a more cost-effective and more flexible strategy to bring products to market for our customers.

|

● |

Comprehensive platform solutions. |

Our platform solutions consist of an integrated package of hardware, firmware and software designed to enable our customers to develop differentiated products in a cost-effective manner with a short time-to-market. In addition to a high-performance SoC, we plan to provide our customers with customizable, high functionality firmware, and

software development kits to allow them to rapidly develop and differentiate their products. As a result, we would be able to reduce our customers’ investment in costly and time-consuming internal firmware and software development for their products, and from having to source different firmware and software for their end products from multiple suppliers.

|

● |

Customizable firmware and software. |

Our firmware, which is sold as a bundled solution with our SoCs, includes a real-time operating system and a set of application specific modules that support a wide range of functions including Web-based management, audio distribution, traffic classifications, etc. Our software platform includes a comprehensive suite of components, such

as device link libraries and drivers, tools, sample code and documentation to create applications that would allow a wide range of networking devices and networked multimedia appliances.

|

● |

Targeted, high-performance SoCs. |

Our SoC solutions are specifically designed for the powerline communication market. They are driven by function-specific blocks that allow simultaneous execution of complex operations, such as transmission of data over power lines and MPEG audio decoding and playback. Our SoCs support most major peripheral connection protocols,

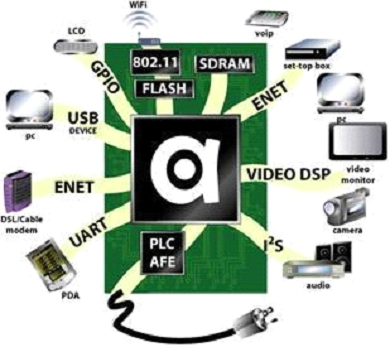

including USB, Ethernet, Infrared, I2S, and a number of specialized and general purpose interfaces. This support enables connectivity to a variety of playback, display and content creation devices including cameras, PCs, televisions and car and home audio systems.

Technology

Arkados is committed to building standards based solutions. Currently, Arkados SoCs are based on the specifications developed by the HomePlug Powerline Alliance and TIA-1113 standards. Our planned HomePlug® AV based AI-2100 SoC, which is being

developed and manufactured under an agreement with STMicroelectronics, is designed be interoperable with three established powerline standards: TIA-1113/HomePlug 1.0, HomePlug AV, and the recently confirmed IEEE 1901 Baseline Standard. The chip also designed to offer support for the Inter PHY Communication Protocol (IPP) as defined by the IEEE P1901 Working Group, and which is scheduled to be included in the upcoming ITU-T G.hn standard.

_______________________

1 ©2009 by Gary Altunian (http://stereos.about.com/od/reviewsandrecommendations/fr/Powerline.htm). Used with permission of About, Inc. which can be found online at www.about.com. All rights reserved.

- 6 -

System-on-Chip Semiconductors

Arkados has a number of design wins that employ our first SoC, the Arkados AI-1100, which we started marketing in Fiscal 2007. The device supports applications such as whole-house music streaming, whole-house internet access, and can be used in IPTV set-top boxes designed to decode and display standard definition video content

-- from sources as varied as surveillance cameras and YouTube -- on regular TVs throughout the home. This turnkey solution features a programmable MAC and an on-chip ARM 9 application processor. Its fully HomePlug 1.0 compliant MAC/PHY and Arkados extensions and software provide increased performance and future proofing.

Our next generation SoC, the AI-2100, will be backwards compatible with our current chip and it will feature an enhanced embedded Quality of Service (QoS) engine which supports video flows for low jitter, lip synch and low latency delivery. The chip is being developed and manufactured under an agreement with STMicroelectronics.

Software

In our view, today’s digital products are incomplete without an array of software components that enable both device-to-device communications and robust product features. We provide our customers with a host of software components that run directly on our chips, further reducing development time. These software

components include application-level features (such as our Direct-to-Speaker™ multi-channel audio synchronization, networking and internet, online gaming, etc.) embedded application support software (audio compression/decompression, internet radio support, GUI support, video drivers, etc.), Quality of Service engine, traffic management, and TCP/IP components.

Market Opportunities

Arkados solutions are offered to the following markets:

|

● |

the retail consumer electronics market and the whole-home custom installation market |

|

● |

the smart grid market |

|

● |

the subscription services market. |

The Growing Digital Home: Networked Consumer Electronics

As broadband access to the home is becoming ubiquitous, home networking and connectivity demands for digital home applications continues to grow – extending the internet, and the services that travel on it, to every corner of the house.

The promise of sending digital communications over common power lines is now being realized, and Arkados’ products serve several large and growing markets: retail consumer electronic products, whole-house audio installations, smart-grid utility company applications, broadband-over-powerline internet access, and the distribution of

internet-based services.

The Arkados AI-1100 is the first HomePlug 1.0 compliant system-on-chip targeted for the retail consumer electronics market. Coupled with software to create full turnkey solutions for its customers, the Arkados AI-1100 has already received a number of design wins, and is the engine behind the creation of reasonably-priced multi-room audio

and video distribution products for the retail consumer market. Products coming to market soon will feature iPod® docking stations and powered speakers that can be placed anywhere in the home, with no additional wiring needed.

As a subset of this market, the whole-house audio market category has been particularly active. Arkados’ solutions offer a way to create both retail and custom audio systems with features and functionality heretofore available only in multi-thousand dollar custom audio installations. Arkados’ customers include Devolo

AG, Channel Vision, IOGEAR, Gigafast, Tatung, and Zinwell.

Two customers in particular, Russound and Nuvo have begun marketing campaigns for their whole-house systems that use the Arkados chips and software. Russound’s Collage system and Nuvo’s Renovia system are planned to be available in the customer installation channels later this year.

These high-end custom audio systems, which address the existing home market (expanding from their primary market target of newly constructed homes), can feature up to 12 separate audio zones and can process a wide range of sources of audio content which can be streamed from any digital or legacy analog source.

Russound, a leading custom multi-room audio distribution system manufacturer, selected the AI-1100 for use in its iBridge Power Dock and its Collage system. Arkados has received initial volume commitments and NRE’s (Non-Recurring Engineering) valued over $1.2 million from customers in this area, of which over $602,668 has been recognized

through May 31, 2009. Arkados’ chips can also power cameras, video endpoints, and sensors for other installed home systems, such as for surveillance systems.

- 7 -

Smart Energy and Utility Company Applications

Another large potential market for Arkados’ solutions relates to energy conservation, the “green” applications that help utility companies and their customers save both money and energy. For example, “Smart Grid” applications (Green Energy, demand response, energy efficiency and grid modernization

– i.e., reduction of carbon emissions) and home/building automation (such as controlling air conditioner thermostats remotely) represent large and attractive opportunities given today’s surging energy costs. Arkados has design wins at MainNet and Corporate Systems Engineering.

Services

An additional immediate potential market for the Arkados platform is for subscription music services. Arkados software and chips enable the distribution of Internet music services (e.g., Rhapsody, Yahoo! Music, AOL Music, Shoutcast services). The Company is actively working on reference designs and business strategies to address

this rapidly developing market.

Press & Analyst Quotes about Arkados Target Markets

The following is a brief compendium of publicly available quotes that echo our beliefs in the strength of Arkados’ target markets2:

|

● |

Retail Consumer Electronics for the Digital Home Market |

|

o |

From EETimes: “Embedded processors and connectivity chips are bright spots in a semiconductor market that will see double-digit dips in computer and cellular chip sales in 2009, said Mario Morales, vice president of global semiconductor research at International Data Corp. The need for more intelligence in a broad range of embedded systems is driving

15 percent compound annual growth in embedded processors. Chip sales will rise from more than three billion in 2007 to nearly seven billion in 2012, IDC forecasts. Less than three percent of popular devices such as digital TVs and set-top boxes sport connectivity today, another ripe area for growth. Here combination chips that support multiple standards such as Bluetooth, Wi-Fi and others are rising from 20 percent of today’s connectivity chips to 60 percent by 2012, Morales predicted.” (3/5/2009) |

|

o |

iSuppli: “The next networking frontier is the home – and the ubiquitous power line is its Holy Grail,” says Steve Rago, Principal analyst and author for iSuppli’s new report ‘Home Networking Technology’s Killer Connection’. “Both the IEEE

and the ITU are driving emerging power line standards. It currently appears that the IEEE, which includes HomePlug AV technology, may have the advantage due to the timing, available silicon, and its announced supporters, including STMicroelectronics and Arkados. In its report, iSuppli forecasts 210 million power line devices will ship during 2013, a CAGR of 76% over the next five years.” (1/6/2009) |

|

● |

Smart-Grid and Utility Applications Market |

|

|

Another large potential market for Arkados’ solutions relates to energy conservation, the “green” applications that help utility companies and their customers save both money and energy. For example, “Smart Grid” applications (Green Energy, demand response, energy efficiency and grid modernization – i.e., reduction of carbon emissions) and home/building automation (such

as controlling air conditioner thermostats remotely) represent large and attractive opportunities given today’s surging energy costs. |

|

o |

From CNNMoney.com: “The Brattle Group, a think tank, estimates the nation will need to spend up to $1.5 trillion on its electricity system over the next 20 years - and that’s just enough to keep the lights on. An investment in cleaner energy could put the figure at $2 trillion, and would include building new power plants, transmission lines,

and focus on conservation. On the grid alone - the lines, towers, meters and substations - Brattle estimates the first steps towards a smart grid could cost about $900 billion over the next two decades. That includes money for computers, meters and software to digitize the grid. (1/8/2009) |

|

o |

From EE Times: “Citing various studies, Texas Instruments Fellow Dave Freeman said some 50 million analog meters in the U.S. are likely to be replaced by 2010 at a cost of about $18 billion. Worldwide, only 6 percent of electricity, 8 percent of gas and 4 percent of water meters are now automated. Freeman said that using “smart” solutions

would enable home thermostats and large appliances to communicate wirelessly or over existing power lines to help consumers conserve energy. He pointed to recent U.S. policies and incentives for developing a smart grid.” (3/18/2009) |

|

o |

From BuddeComm press release: “the urgent need to address climate change through measures such as smart grids will be the main force for deploying BPL networks. In California alone it is estimated that approximately 17.5 million smart meters will be deployed between 2008 and 2010.” |

|

o |

From EDN Magazine: “in the electric industry alone, 500 million meters worldwide could be replaced over the next 10 years, resulting in semiconductor sales of at least $7.5 billion, according to Mark Buccini, director of strategic marketing for Texas Instruments’ microcontroller products.” And continues to say “a large number of

those will be connected to a home area network, and that home network will have at least one device that can talk to the meter,” and that “the communications piece is as much as three times as big [as the $7.5B market for meters].” (6/24/2008) |

_______________________

- 8 -

|

● |

Subscription and “over the top” Services |

|

|

Many services currently available, from remotely-monitored security, to piped-in music, to health monitoring systems, require costly professional installation for communication and distribution. With the addition of a broadband pipe to the house, and the use of an in-home distribution method such as Arkados solutions provide, over-the-top (OTT) this type of solution allows the content owners to deliver

the content directly to consumers. |

|

o |

The Diffusion Group: “By 2012, approximately 190 million households will use a next-generation game console; 80% of these households – 148 million – will have this console connected to the Internet; and 75% of connected-console households – more than 110 million – will use console-based video services at least a couple times

each week.” (12/1/2008) |

|

o |

The Diffusion Group: “TDG found that 40% of broadband users are watching at least an hour of video per week on the Internet. More surprising is that 30% of those are watching 25% or more of their TV online. Imagine what will happen when tens of millions of households are capable of watching broadband video on their big-screen, high-dollar, high-definition

TVs and home theater systems.” (5/2008) |

Corporate Background

On May 24, 2004, we filed a merger certificate completing the acquisition of Miletos, Inc., a previously unaffiliated Delaware corporation (the “Merger”). The consideration for this Merger was 16,090,577 restricted shares of our common stock and the assumption of certain liabilities of Miletos’ predecessor and former controlling

equity holders. The merger was completed according to the terms of an Agreement and Plan of Merger dated as of May 7, 2004. Miletos merged into a wholly owned subsidiary we formed for the merger which then changed its name to “Arkados, Inc.”.

Simultaneously with the merger, we completed a private placement of 883,334 shares of our common stock for aggregate proceeds of $1,060,000, of which approximately $950,000 were subscriptions for cash, $50,000 (41,667 shares) was for outstanding debt of Arkados, and $59,800 (49,834 shares) was in lieu of consulting fees. The sale was made

to 10 accredited investors (“Investors”) directly by us without any general solicitation or broker. The offering is claimed to be exempt from registration pursuant to Section 4(2) under the Securities Act of 1933, as amended. In addition, we settled liabilities relating to outstanding convertible notes and payables for 700,000 common shares.

Prior to the Merger, on March 23, 2004, Miletos acquired the assets and business of Enikia, LLC, a Delaware limited liability company at a public foreclosure sale, including the intellectual property upon which Arkados’ development efforts are based. Miletos was formed in February 2004, by control affiliates of Enikia. These control

affiliates were both secured creditors of Enikia and holders of the controlling equity interest in Enikia. They contributed a secured promissory note to Miletos in the initial principal amount of $9,221,000, dated June 1, 2002. The promissory note also represents obligations to the lender for additional advances to Enikia by the control group which brought the aggregate principal due at the time of foreclosure to approximately $11,100,000. At the foreclosure sale, Miletos forgave $4,000,000 of the secured obligation

in exchange for substantially all of the assets of Enikia. The merger has been treated as a reorganization of Arkados, Inc. via a reverse merger with Arkados Group, Inc. The assets acquired at the foreclosure sale and certain liabilities assumed by Arkados Group, Inc. have been recorded as historical cost.

On March 3, 2007 we completed the merger of Arkados Wireless Technologies, Inc., our wholly owned subsidiary (“Merger Sub”) with Aster Wireless, Inc. a Delaware corporation (“Aster”) pursuant to an Agreement and Plan of Merger dated February 13, 2007 by and among Merger Sub and Arkados Group, Inc. In this merger,

we acquired synergistic talent and technology which has helped improve the reliability and quality of audio streaming in our current generation chipset and we believe will help deliver our next-generation chips to market more quickly, with richer capabilities. This will translate to a better competitive position in the marketplace. The technology enhances the reliable distribution of multimedia content, potentially over multiple distribution media, and is designed to be embedded in new consumer electronics

products and accessories for audio, video distribution, set-top boxes and other multimedia entertainment appliances.

- 9 -

Dependence on Financing Activities

Although we have started to generate revenue during the past two years, we continue to be dependent on outside sources of financing to continue the development of our semiconductors and software, and to further support sales. During fiscal 2008, we completed a series of debt financings in the aggregate principal amount of $855,000; we also

issued notes in the amount of $125,000 which were converted into equity in August 2008. Andreas Typaldos, our Chairman and one other Director loaned the Company $177,700. From June 1, 2008 to May 31, 2009, we received advances from related parties of approximately $649,000 which was converted into equity in August 2008. In addition, we received an additional $20,000 which represents borrowings from related parties.

We have sought and will continue to seek various sources of financing but there are no binding commitments from anyone to provide us with financing. In addition, there is $12,073,612 principal and interest amount of 6% Secured Convertible Debentures due June 28, 2009 (initially due December 28, 2008) issued during the period

from December 2004 to August 31, 2008 outstanding, which has been an impediment to obtaining equity financing. The documents were amended in January 2007 to eliminate the requirement that the holders of 60.1% of the outstanding principal amount consent to our issuance of shares, debt or fixed convertible securities to finance our operations, continue to contain a full “ratchet down” provision which has a dilutive effect, which is triggered by future financing at an effective price lower

than the conversion and warrant exercise price.

In July 2008, we reached an agreement with the holders of the Secured Debentures which extended the due date to June 28, 2009 capitalizing interest until the Secured Debentures are due and waiving the ratchet down anti-dilution adjustment for certain equity financings completed before October 31, 2008. The Company exchanged the

following for these amendments:

|

● |

new debentures for 25% of the outstanding principal amount of Secured Debentures ($2,845,815.25) having identical rights as the Secured Debentures, except that the conversion price is $0.25 rather than $0.85 and |

|

● |

new warrants for 25% of the existing warrants held by the holders of the Secured Debentures (2,332,131), identical to the warrants surrendered, except that the warrant exercise price is $0.25 rather than $0.85 and the new warrants are only exercisable for cash until December 1, 2008. |

On August 7, 2008, we issued 1,690,080 units (each consisting of two shares of our common stock and one warrant) to 18 accredited investors for aggregate consideration of $845,038.47. Of this consideration $762,593.66 was cash or cash advances made to us after April 15, 2008 and the balance was in exchange for prior obligations

for borrowed money and other accounts payable. The warrants are exercisable until June 30. 2013 and entitle the holder to acquire one additional share of our common stock for $0.25 per share.

While a substantial portion of the net proceeds of these financing activities was initially used to repay pre-existing debt, all of the proceeds during the fiscal year 2008 were used to support Arkados’ operations. There is no assurance that the holders of the Secured Debentures will continue to provide additional funds to us, that

future equity financing will be available or that future financing will not be impeded by the anti-dilution provisions of the documents. Our ability to continue our operations depends on our ability to obtain financing. If adequate funds are not available on acceptable terms, we may not be able to retain existing and/or attract new employees, support product development and fabrication, take advantage of market opportunities, develop or enhance new products, pursue acquisitions that would complement

our existing product offerings or enhance our technical capabilities to develop new products or execute our business strategy.

On July 2, 2009 we received notice from a law firm representing approximately 45% of our outstanding 6% secured convertible debentures due June 28, 2009 (the “Debentures”) were in default by reason of non-payment. This event triggers an “Event of Default” under the terms of the Debentures on July 8, 2009, absent

payment in full. The Event of Default entitles the holders of the Debentures to redemption at the rate of 130% of the principal and accrued interest outstanding, interest on unpaid interest and principal at the rate of 18% per annum commencing on July 8, 2009 and reimbursement for expenses incurred enforcing the obligations.

We have been negotiating for an infusion of equity capital, restructuring of our secured and unsecured debt and the holders of the Debentures have indicated that they are inclined to work with the company in this regard. Although there can be no assurance that the forbearance, financing or restructuring of our debt can be achieved,

we continue to work closely with representatives of the holders of the Debentures to maintain the company as an ongoing business, which includes preserving our current operations and relationships with existing customers, partners and suppliers.

As of July 6, 2009 the $1,066,500 principal amount of 6% Convertible Subordinated Notes (the “Notes”) due June 30, 2009 were also in default by reason on non-payment. Under the terms of the Notes, the interest rate increases to 12% during the period the Notes are in default and the holders are entitled to the costs of collection.

We plan to discuss forbearance or extension of the due dates of the Notes, as well as conversion of the Notes into equity with the holders and their representatives, but there can be no assurance that any such agreement can be reached.

- 10 -

Industry Background

Music, movies, the electrical “smart grid”, and a wide range of communication services are experiencing a fundamental shift. The distribution of content to products, and in some cases the products themselves, is transitioning from traditional methods. Digital content is requires a new digital distribution model.

Arkados’ Standards-based Solutions

Arkados’ solutions are designed to directly address this opportunity by enabling electrical power sockets to be turned into high-speed network ports, thereby providing a high-speed pathway through which digital information can travel inside a home, to the home, and on the smart grid. We believe that this shift creates demand for new

products, and new products will require new types of semiconductors that incorporate digital technologies, supporting such functions as communication, application processing, and media rendering.

Our ArkTIC® family of turnkey hardware and software solutions is designed to address these requirements. In particular, Arkados has implemented a method that uses power lines as a pathway for digital information, allowing end users to truly achieve “plug-and-play”

simplicity without the hassles of custom-installed networks, or the problems associated with wireless solutions such as dropouts, unreliable coverage, and security issues.

Standards-compliance Creates Market and Product Confidence

Members of the Arkados team have been active in establishing standards for the powerline communications industry since the year 2000.

Standards are important for a number of reasons, but especially when both consumers and service providers may be installing different pieces of the ecosystem – as in the powerline communications industry. Wireless standards, for example, have brought about a ubiquitous, interoperable and affordable standard for portable data

communication, which resulted in greatly accelerated market growth.

Members of the Arkados team participated in the creation of the HomePlug Powerline Alliance, an independent industry association. The Alliance’s mission is to enable and promote rapid availability, adoption and implementation of cost effective, interoperable and standards-based home powerline networks and products. Formed

in 2000, the Alliance developed the HomePlug 1.0 specification that unified product vendors in support of a single powerline solution for home networking. In 2008, the technology of the HomePlug 1.0 specification was adopted by the Telecommunication Industry Association as TIA-1113 standard. In 2005, the Alliance ratified HomePlug AV specification that enables 200Mbps class communication over power lines.

Market Analyst In-Stat believes that powerline communication will be a potentially important technology for multimedia networking, as the technology could provide a home network backbone. Arkados has worked in significant ways to develop the HomePlug specifications including in-home technologies (HomePlug 1.0, HomePlug AV, and HomePlug

AV2), to-the-home technologies ( HomePlug BPL for broadband over powerline), and HomePlug Command &Control (C&C) and HomePlug GP (“Green PHY”) for low-speed command and control and Smart Grid applications.

Arkados is a Contributing Member of the HomePlug alliance. Members of the Arkados team hold leadership positions in the Alliance and in several HomePlug working groups. Oleg Logvinov, our president and CEO, serves as the Chief Strategy Officer of the HomePlug Alliance. Mr. Logvinov is also a past president of the Alliance, having been succeeded

by Matthew Theall of Intel. Additionally, Jim Reeber, our Director of Marketing has served as Chair of Marketing Working Group since 2003; Grant Ogata, our Executive Vice President of Worldwide Operations, has served as the Chairman of HomePlug Command and Control Working Group and was instrumental in spearheading the alliance’s efforts to develop a specification for a low-cost command and control technology in his role as the working group chair. Recently Jim Allen, our Vice President of Standardization

and Advance Planning, has accepted the role of chair of the HomePlug Smart Energy Technical Working Group.

The HomePlug technology now dominates the marketplace. Market analyst In-Stat forecasted that by 2010, the technology based on HomePlug specifications will hold 85% of the worldwide market for powerline communications. The HomePlug Powerline Alliance has brought together both personal computer and consumer electronics companies on a global

scale. Membership in the Alliance has grown to include nearly 70 industry-leading companies. HomePlug Sponsor companies include Cisco; Comcast; GE Energy., part of General Electric Co.; Gigle Semiconductor, Intel Corporation; Intellon, Motorola; NEC Electronics, and SPiCOM Technologies. Besides Arkados, contributor members include Corporate Systems Engineering; Renesas; Texas Instruments; and YiTran Communications.

- 11 -

Arkados is also a member of the IEEE P1901 group that is focused on the development of powerline communication Physical Layer (PHY) and Media Access Control (MAC) specifications. Working with the HomePlug Powerline Alliance, the Arkados team has contributed to the development of a number of specifications that were contributed to standards organizations, such as the Telecommunications Industry

Association.

The Strategy behind Arkados Solutions

Arkados is a fabless semiconductor company that develops comprehensive platform solutions, including system-on-chip (SoC) semiconductors, and firmware and software for manufacturers of networked multimedia appliances and feature-rich networking devices. Our platform solutions are designed to enable a systems-based approach to networking

and will allow our customers to build products that are simple and intuitive to install, and easy to operate with intuitive and customizable user interfaces.

We believe that many of our customers plan to produce not just one standalone device, but they will introduce many system components that work together. An example is the audio market: Our customers would not just introduce a dock for an MP3 player, but they would also produce a variety of speakers, control units, CD players, adapters,

boom-box style rendering points, etc. Our solutions enable greater versatility and value that allows our customers to create each of those components, sometimes with only a single hardware design.

The primary goal of our solutions is to enable our customers’ plan to develop and sell end-user systems. Our customers require a lower Bill of Materials (their cost for manufacturing a product), and better ways to produce a variety of components for end-user systems more quickly. We call our solutions “turnkey” because

they enable our customers to create entire lines of products without dedicating their resources to long product development cycles, or extensive software design.

Our customers are also aware of our strategy to support a seamless transition to higher-speed technologies as they become available. This promotes long life-span of their development effort, and creates significant re-use of their software components. Our SoC includes a powerful processor that allows applications to be run directly on-chip.

Multiple vertical applications can be built by loading different firmware, compared to having to redesign circuity. This feature can broaden product offerings, and extend the product lifecycle. The Arkados implementation of HomePlug technology offers programmability that enables OEMs to extend the functionality of their products and produce a variety of products from a single design.

Key elements of our solution are as follows:

|

● |

Comprehensive platform solutions. |

|

Our platform solutions consist of an integrated package of hardware, firmware and software designed to enable our customers to develop differentiated products in a cost-effective manner with a short time-to-market. In addition to a high-performance SoC, we plan to provide our customers with customizable, high functionality firmware, and

software development kits to allow them to rapidly develop and differentiate their products. As a result, we would be able to reduce our customers’ investment in costly and time-consuming internal firmware and software development for their products, and from having to source different firmware and software for their end products from multiple suppliers. |

|

● |

Customizable firmware and software. |

|

Our firmware, which is sold as a bundled solution with our SoCs, includes a real-time operating system and a set of application specific modules that support a wide range of functions including Web-based management, audio distribution, traffic classifications, etc. Our software platform includes a comprehensive suite of components, such

as device link libraries and drivers, tools, sample code and documentation to create applications that would allow a wide range of networking devices and networked multimedia appliances. |

- 12 -

|

● |

Targeted, high-performance SoCs. |

|

Our SoC solutions are specifically designed for the powerline communication market. They are driven by function-specific blocks that allow simultaneous execution of complex operations, such as transmission of data over power lines and MPEG audio decoding and playback. Our SoCs support most major peripheral connection protocols, including

USB, Ethernet, Infrared, I2S, and a number of specialized and general purpose interfaces. This support enables connectivity to a variety of playback, display and content creation devices including cameras, PCs, televisions and car and home audio systems. |

In contrast, competitors that do not provide comprehensive platform solutions such as ours may be able to produce a greater variety of customized ICs to more specifically address the particular requirements of an OEM. In addition, solutions which do not include customizable firmware and software like ours may allow OEMs to take advantage

of a wider range of third-party developers. While, these alternative solutions may be lower in cost for simple data networking devices in comparison to our platform solutions, our solution will be more cost effective and has higher reliability and performance for multi-media networking including distributing audio and video throughout the home and outputting to existing consumer electronic products.

Key Strategic Elements

Provided we are able to continue to finance our operations, our objective is to be the leading supplier of comprehensive platform solutions for high-performance and feature-rich networked multimedia appliances and networking devices.

Key elements of our strategy are:

|

● |

Maintain a full platform solution approach with industry-leading SoCs, firmware and software. |

We plan to continue to commit the resources of each of our hardware, firmware and software teams to drive innovation so that our solutions are at the forefront of the networked multimedia appliances and networking devices industries and capture a leading market share. We intend to continue to devote resources to increase the performance

and functionality of our SoCs and expand the features and capabilities of our firmware and software. This enables great flexibility and value for our customers as they take products to consumer and enterprise markets.

|

● |

Maintain our focus on feature-rich networked multimedia appliances and networking devices. |

We intend to build on our experience as a platform provider by continuing to focus primarily on customers that produce feature-rich networked multimedia appliances and networking devices. In addition, we intend to continue to work closely with manufacturers of other media rendering components to ensure that our platform solutions interface

with their current and future technology components for optimal performance their end products.

|

● |

Maintain our focus on the integration of powerline and audio rendering functions to secure the leadership position in networked multimedia appliances and networking devices. |

We believe that the networked audio markets will continue to represent the largest near-term volume opportunity for networked multimedia appliance and networking device manufacturers. We intend to continue to focus on advancing functionality and promoting our solutions to win designs in this large and growing market. By including

these options in our platform, we create a foundation that enables our customers to incorporate new features more quickly.

|

● |

Enable new growth markets, such as photo- and video-enabled networked multimedia appliances. |

We intend to build on our existing expertise to be the leading provider of comprehensive platform solutions in new markets. We intend to continue to invest our research and development efforts and engineering resources to develop new platforms and products and to strengthen our technological expertise. One example is our reference

design that employs both our solutions as well as Blackfin® Processors by Analog Devices to provide a cost-effective platform for a variety of video applications based on powerline distribution. We believe that our focus in this area creates optimized solutions for our customers and increases the revenue potential for companies throughout the value chain.

|

● |

Expand our customer base while securing additional design wins with existing customers. |

We plan to be the leading supplier of new designs to our existing customers, and to secure a high market share with new customers entering this market. We intend to continue the expansion of our customer base by marketing our platform solutions to additional manufacturers of consumer devices. Further, we intend to broaden our reach within

our existing customer base into their adjacent product lines that can utilize technologies that we intend to implement in the near future. By providing key hardware and software components to our customers, we believe we can deliver better value and features to our customers, while reducing design and manufacturing costs.

- 13 -

|

● |

Create business arrangements with companies to better serve our common OEM customers. |

We plan to go to market together with a number of companies who target specific areas of the marketplace. Since certain companies pursue many of the same customers who approve the products destined for the end-user, we plan to take advantage of this communality and together create solutions and offer even greater turnkey value. This approach

offers OEM customers an easier point-of-contact and allows them to take advantage of efficiencies we have already built with our partners.

Our Products

We design and develop and are marketing highly integrated SoC semiconductors that are designed to cater to the markets for powerline communications. Our chip designs offer flexible solutions through programmability and remote firmware upgrades. Our customers have responded very favorably to our platform offerings which we call ArkTIC®,

which is an acronym for the Arkados Total Integration Concept.

Solutions from our ArkTIC family of converged multimedia and networking solutions targets data-, audio-, photo-, and video-enabled networked multimedia appliances and networking devices.

The ArkTIC family is a portfolio of turnkey hardware and software solutions that enable OEMs and ODMs to quickly develop digitally networked consumer electronic products with a competitive cost structure to address this rapidly developing market. Among other networking interfaces, the first member of the ArkTIC family supports a powerline

communication interface based on the HomePlug Powerline Specification 1.0.1, and our next chip will support HomePlug AV.

Arkados has a number of design wins that employ our first SoC, the Arkados AI-1100. The device supports applications such as whole-house music streaming, whole-house internet access, and can be used in IPTV set-top boxes designed to decode and display standard definition video content -- from sources as varied as surveillance

cameras and YouTube -- on regular TVs throughout the home. Checkolite, devolo AG, GigaFast, IOGEAR, NuVo, Russound, and Zinwell have either announced or are currently delivering products to the marketplace based on this chip.

We have announced that that our upcoming HomePlug® AV based AI-2100 SoC will likely be the only chip available that will be interoperable with three established powerline standards: TIA-1113/HomePlug 1.0, HomePlug AV, and the recently confirmed IEEE 1901

Baseline Standard. The upcoming chip will also offer support for the Inter PHY Communication Protocol (IPP) as defined by the IEEE P1901 Working Group, and which is scheduled to be included in the upcoming ITU-T G.hn standard. Our next generation SoC, the AI-2100, will be backwards compatible with our current chip and it will feature an enhanced embedded Quality of Service (QoS) engine which supports video flows for low jitter, lip synch and low latency delivery. The chip is being developed and manufactured under

an agreement with STMicroelectronics.

We started marketing our AI-1100 system-on-chip in Fiscal 2007. It is designed to be embedded into various consumer electronics and multimedia networking devices and deliver high-speed Internet/Networking connectivity and multimedia over the power lines in a home. The AI-1100 chip offers a single-chip integration of HomePlug 1.0.1 powerline technology, an ARM 926-JES CPU operating at 160

MHz, dual Ethernet interfaces, an I2S Audio Interface, and a wide variety of other interfaces designed to support connected home applications. Furthermore, the programmable nature of our implementation allows ODMs/OEMs to extend the functionality of these products and HomePlug technology.

ArkTIC™ AI-1100 system-on-chip features:

- 14 -

|

· Based on HomePlug 1.0 Specification

- PHY/MAC sub-system is designed to allow for compliance with the HomePlug specification

- Arkados extensions for increased performance and future-proofing

- Programmable MAC functions for full flexibility

· ARM926 Processor

- 16k instruction cache & 4k data cache

- Memory Management Unit

- Embedded Trace Macrocell (ETM9)

· SDRAM Controller

- Supports external parts up to 256Mb

· SRAM Controller/Expansion Bus Interface

- Supports external boot Flash or external SRAM and acts as a general-purpose interface bus for external logic

· Ethernet controllers

- Standard MII port (802.3u) - or - PHY Emulation Port (PEP) MII

(emulates Ethernet PHY)

· Video/Audio DSP Interface

· USB 1.1 Device

· Serial I/O Controllers

· I2S for direct connection to audio DAC

· IrDA

- 6550d compatible UART

· GPIO Controller

· JTAG / Debug Interface

· 0.18μ CMOS, 1.8V core, 3.3v I/O

|

|

Our AI-1100 is the first in a series of devices built around existing and emerging HomePlug Powerline Alliance networking specifications. This device supports the HomePlug 1.0.1 specification along with a variety of multimedia applications. Our Direct to Speaker™ Internet Radio Reference Design (AI1100-DTS-INTR) and our Direct-to-Speaker™

MFi iPod Dock have received HomePlug 1.0 certification. Furthermore, the programmable nature of the Arkados implementation allows OEMs to extend the functionality of the HomePlug technology. The AI-2100 and future devices will include, among other enhancements, the implementation of new technologies such as HomePlug AV, HomePlug BPL, HomePlug GP, and IEEE 1901 specifications as they become available.

We have modularized a core Orthogonal Frequency Division Multiplexing (OFDM) and communication platform to rapidly develop customized solutions for each powerline market. This enables efficient reuse and repurposing of technology blocks, which can be used to create many specific solutions.

We also provide consulting, software, and applications support, thereby facilitating system integration in an effort to reduce our customers’ time-to-market and our customers’ development costs.

In the in-home networking portion of the market, we expect to deliver solutions for both computer-centric and entertainment-centric applications. Inside our chips, we combine the networking blocks and the blocks that are capable of supporting end-user applications for consumer electronics products. Our chips are designed to offer a high

degree of programmability and may become an attractive solution for a diverse range of home-networking products that merge traditional consumer electronic functions with network-centric features.

In another portion of the market, we expect to deliver highly integrated circuits that combine both networking blocks and blocks that are capable of supporting communications applications in demand from businesses such as hotels, office parks, shopping plazas, apartment buildings, etc. This is sometimes referred to as the multi-dwelling/multi-tenant

unit (MDU/MTU) or the “commercial” market. Downloadable firmware management capabilities make this an attractive solution for remote management and service applications.

In the Smart-Grid and Utility Applications portion of the market, we expect to deliver highly integrated circuits that combine both networking blocks and blocks that are capable of supporting the communications applications that are in demand from service

- 15 -

providers and utility companies. This portion includes the “Smart Energy” applications that help utility companies to conserve energy and better manage their network, such as Automated Meter Reading, Peak Shaving, and a host of other applications that provide a variety of benefits and cost-saving measures. Downloadable firmware

management capabilities would make this an attractive solution for remote management and service applications.

The application of Arkados solutions

Listed below are examples of the products that can be built based on the Arkados semiconductors by ODMs and OEMs. Our customers have already developed some of these products and either have or will be bringing them to market.

|

● |

CONSUMER ELECTRONICS - Devices that bridge current devices and content with existing and new consumer electronic products throughout the home. These devices allow users to easily distribute multimedia content, allowing them to enjoy music from iPod, internet, or PC throughout the whole house; to view videos downloaded from the

internet on a big screen TV; to access the digital photos stored on a PC and display them on a digital photo frame, or to share new photos with loved ones via the internet by displaying them directly on a digital photo frame located thousands of miles away. This is a growing market that includes audio & video devices with embedded powerline technology. We expect this market to grow over the next few years as more video and audio products are released with networking technologies built-in. Televisions,

stereos, powered speakers, receivers, DVD and CD players, digital picture frames, home intercom systems, and other products are targeted applications for powerline networking technology. Internet streaming content and home content servers should greatly increase the demand for HomePlug 1.0 and AV products. In particular, our solutions offer advanced features such as synchronized whole-house audio which, combined with its new ease of installation, may significantly broaden the marketplace for such applications. | |

|

● |

NETWORK HARDWARE - New types of routers, switches, gateways, network attached storage, surveillance cameras, and other devices that offer various types of services to the SOHO (Small Office Home Office) network. |

|

|

● |

INTERNET TELEPHONY - As companies like Vonage, Comcast, Verizon and other service providers begin to roll-out new voice services to the home, an easy-to-use and reliable home network is needed. VoIP (Voice-over-IP) phones are currently produced by several vendors and we expect to see such products with HomePlug technology embedded into

them. |

|

● |

HOME SECURITY - Many companies have created home security cameras that are networked through various means. Early market entrants GigaFast, Logitech, ST&T, and Asoka have already created powerline networked security cameras with embedded web servers that allow direct access to the camera’s feed. |

|

● |

SMART GRID – Many utility companies may implement applications that could provide benefits such as saving money due to automated operation, the ability to predict maintenance issues, implementing a self-healing grid architecture, reducing power outages, and making better use of their assets; managing the grid more intelligently to

prevent blackouts and power disruptions; recovering more quickly after a power disruption; increasing security; implementing real-time monitoring of the state of the network, and managing a response; managing the quality of the power (to deliver differentiated services for businesses with sensitive electronics and computers); implementing “green power” programs that allow consumers to manage their electricity use and costs; and integrating control systems, power electronics, and distributed resources. |

Sales & Customers

By developing solutions to facilitate our customers’ rapid development of full-featured next-generation products at reasonable prices, we position our company as a builder of bridges. Our solutions are designed to bridge entertainment and internet content to devices around the home, and to bridge between communications technologies,

such as WiFi and powerline, Ethernet and powerline, and even to-the-home, in-the-home, and smart grid powerline technologies. We believe the use of digital communications technologies will increase beyond the world of computing, until a large percentage of devices in the home seamlessly connect to some form of digital content or communications.

Many of our existing and potential customers are also currently in a specific marketplace that is being affected by digital convergence and networking technologies. We believe traditional networking companies are moving into traditional consumer electronics areas, while the reverse is happening to consumer electronics companies. Arkados

provides platform solutions that allow those companies to enter the new market space with ease and speed.

- 16 -

We continue to gain considerable traction with our customers. We recently counted 34 design wins for our chip, and 26 separate products that our customers have publically announced. We and our customers have publicly displayed and announced a wide variety of potential products that include whole-house audio solutions (including music player docking stations, audio bridges, powered speakers,

computer drivers for whole-house networked distribution of sound, and internet radio), and whole-house video distribution systems (including Internet-based TV adapters, surveillance systems, and digital picture frames).

Our solutions have been shown in a number of public venues, including the 2008 and 2009 International Consumer Electronics Show, CeBIT 2009, CEDIA Expo 2009, Electronic House Expo 2009, and other conferences. Our prototypes or products have been publicly announced and/or demonstrated by Analog Devices, Channel Vision, Checkolite, Corporate

Systems Engineering, devolo AG, Freescale, GigaFast, GoodWay, IOGEAR, NuVo, Meiloon, PAC Electronics, Russound, Tatung, Zinwell, and Zylux. Many of these companies are suppliers to top tier brands in the market place. Tatung’s service provider business has used our chip in WiMAX-to-Powerline demonstrations. Several of these relationships, among others, have progressed into sales of chips, software development services, and related revenue.

We have also been involved with our customers in projects related to Smart Grid applications. Smart Grids have received increased attention due to the recently enacted American Recovery and Reinvestment Act (ARRA) of 2009. The act includes $4.5 billion focused on smart grid related activities and smart meters, and $7.3 billion to support expanding

access to broadband in underserved communities. Arkados has already reported service revenue related to smart grid development projects. As early as October 2007, Arkados and MainNet Communications announced plans to jointly develop applications to improve the reliability and efficiency of electrical grids, connect consumer electronic devices over power lines, enable energy-saving initiatives, and deliver Broadband content to homes and offices. Arkados has also provided solutions for components intended to implement

energy-saving programs (such as temperature control, smart thermostats, and demand-driven load control) that were used in trials of a “green power” application with Corporate Systems Engineering.

We are working closely with many of the leading communications, digital entertainment and consumer electronics companies some of which may result in design wins and orders for our integrated circuits. There are multiple OEMs that are sampling and testing our AI-1100 SoC chips, and one has announced a product incorporating our chip, but

factors such as design issues, compatibility issues and manufacturing errors could delay the functioning of the products and prevent us from making sales. As is evidenced by the HomePlug certification of several of our reference designs for an Internet Radio and for a whole-house connected iPod dock, we are focused on delivering a wide array of reference designs that can help guide our customers through the product-to-market cycle.

We believe our solutions create easy-to-install and easy-to-use products since connectivity occurs through the existing electrical outlets and electrical wires. For the end user, products that use Arkados solutions connect to each other by simply plugging in, while also being reliable and secure.

Strategic Relationships

Fiscal 2009 brought a number of significant announcements that solidified our relationships with STMicroelectronics, Freescale Semiconductor, and Tatung. Each of these relationships allows Arkados to bring value to our customers.

Arkados and STMicroelectronics announced an agreement to develop and manufacture a 200 Mbit per second, HomePlug AV wideband powerline modem System-on-Chip (SoC). STMicroelectronics is largest semiconductor manufacturer to announce plans to bring a HomePlug AV chip to market, and, based on announced product plans of other HomePlug members,

we believe this chip will be the only chip available in the near term that will be interoperable with three established powerline standards: TIA-1113/HomePlug 1.0, HomePlug AV, and the recently confirmed IEEE 1901 Baseline Standard. STMicroelectronics will manufacture the chip, and both STMicroelectronics and Arkados will market a version of the device specifically targeted at “bridging” applications such as Ethernet-to-Powerline adapters, or other applications where only a MAC/PHY implementation

is needed. Arkados will continue to focus on marketing the chip for more full-featured connected media applications such as whole-house audio, IPTV, and segments of the smart-grid market.

Arkados and Freescale Semiconductor, Inc. plan to bring a versatile “Whole-House Audio In a Box™” platform to market. The platform uses Arkados’ HomePlug® based multimedia streaming technology, and Freescale’s Synkro wireless

communications technology, enabling untethered devices to control and monitor the system and display live data.

We have also entered into go-to-market strategies with a number of ODMs and other technology companies. Since many companies in this space target the same customer base as we do, we plan to collaborate to create solutions and offer even greater turnkey value for OEMs. We have announced relationships and strategies with several companies,

including GigaFast and Tatung.

- 17 -

Arkados’ relationship with Tatung, the $7B global ODM, constitutes a one-stop shop for the industry’s technology and manufacturing needs for distributing digital content in homes. Together, the companies deliver complete product solutions to consumer product manufacturers.

In July 2004, Arkados entered into a Silicon Product Development and Product Collaboration Agreement with GDA Technologies, Inc., under which GDA assists Arkados in translating Arkados chip designs into a mask that can be used by a semiconductor foundry to manufacture Arkados-designed integrated circuits in a cost effective manner. We paid

GDA $175,000 under the agreement in Fiscal 2007 and will pay GDA 20% of production costs as compensation for production management services. In addition, we issued 150,000 shares of our restricted common stock to GDA for nominal consideration.

Manufacturing

We currently use Fujitsu Japan for all of our wafer fabrication and assembly, and Fujitsu and GDA Technologies for a portion of our design and testing. This “fabless” manufacturing strategy is designed to allow us to concentrate on our design strengths, minimize fixed costs and capital expenditures, access advanced manufacturing

facilities, and provide flexibility on sourcing multiple leading-edge technologies through strategic alliances. We expect to qualify each product, participate in process and package development, define and control the manufacturing process at our suppliers where possible and practicable, develop or participate in the development of test programs, and perform production testing of products in accordance with our quality management system. If possible, we plan to use multiple foundries, assembly houses, and test

houses. Our efforts to develop multiple sources of supply have been hindered by our lack of adequate working capital

In connection with the development of our next generation chip, we have entered into a development agreement with STMicroelectronics. The agreement allows Arkados to complete the design and manufacturing of without making the costly investment of taping out a new chip. STMicroelectronics is contributing to the investment for

the development and manufacturing for the Arkados-designed chip. The new chips will be sold by STMicroelectronics, under its own branding, and by Arkados as the next generation ArkTIC® chip.

Research and Development

We have focused on R&D since our inception. Our company has placed significant value on the work done by our engineering staff, and we continue to create new software solutions, technology implementations, system-on-chip semiconductors, and the creation and development of intellectual property, that focus on helping our customers to

get full-featured connected products to market quickly and at a lower cost.

We concentrate our research and development efforts on the design and development of new products for each of our principal markets. As of October 12, 2009, 12 of our 16 employees are dedicated to research and development. Research and development expenditures were $2,069,179, $1,987,313, and $1,920,898 in the years ended May