Attached files

Exhibit 99.2

LIVEVOX MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Throughout this section, unless otherwise noted, “LiveVox,” “we,” “us,” and “our” refers to LiveVox Holdings, Inc., and its subsidiaries, collectively. You should read the following discussion and analysis of LiveVox’s financial condition and results of operations in conjunction with LiveVox’s unaudited consolidated interim financial statements as of March 31, 2021 and for the three-month periods ended March 31, 2021 and 2020, together with related notes thereto, and our pro forma financial information as of and for the three-month period ended March 31, 2021 included elsewhere in this current report on Form 8-K (the “Super 8-K”). This discussion and analysis should also be read together with our audited consolidated financial statements and related notes as of and for the year ended December 31, 2020 included elsewhere in the Super 8-K. In addition to historical information, the following discussion and analysis contains forward-looking statements that involve risks, uncertainties and assumptions. LiveVox’s actual results may differ materially from those anticipated in these forward-looking statements as a result of certain factors, including, but not limited to, those set forth in the section entitled “Risk Factors—Risks Related to LiveVox’s Business and Industry” and elsewhere in Crescent Acquisition Corp’s Definitive Proxy Statement (the “Proxy”) on Schedule 14A which was filed with the SEC on May 14, 2021.

Overview

LiveVox, Inc. was first incorporated in Delaware in 1998 under the name “Tools for Health” and in 2005 changed its name to “LiveVox, Inc.” LiveVox’s mission is to enable next-generation cloud contact center experiences. LiveVox offers a cloud contact-center-as-a-service (or CCaaS) platform for business processing outsourcing (BPO) organizations, enterprises, and collections agencies. Its offerings include omnichannel and artificial intelligence (AI), customer relationship management (CRM) and workforce optimization (WFO). LiveVox’s platform provides customers with a scalable, cloud-based architecture and pre-integrated AI capabilities to support enterprise-grade deployments. Additionally, LiveVox’s platform features a native CRM, which unifies disparate, department-level systems of record to present contact center agents with a single view of its customers. LiveVox has built a differentiated approach to the contact center software market and is complemented by an attractive financial model. Key highlights of LiveVox’s business and market opportunity include:

| • | Large and growing CCaaS market opportunity: The contact center market is in the early stages of a shift to cloud-based solutions and LiveVox estimates that the vast majority of contact call center agents are not using cloud-based solutions today. Various trends are driving this transition, including digital transformation, the automation of manual contact center labor, and the need for AI-enabled analytics to support omnichannel workflows and agents. LiveVox estimates this market to be approximately $27 billion for 2020, of which approximately $5 billion is comprised of cloud-based solutions. LiveVox and other industry sources estimate the total spend to reach approximately $83 billion by 2030. As enterprises continue to execute on their digital transformation strategies, LiveVox is well positioned to capture a meaningful amount of this growth as it increases its investment in sales and marketing to educate more potential customers on its platform. |

| • | Differentiated product: LiveVox offers a cloud-based, enterprise-focused contact center solution. The LiveVox platform consists of innovative cloud-based AI and omnichannel offerings, anchored by its native CRM solution. LiveVox’s products are designed to enable customers to remove legacy technology barriers and accelerate adoption of cloud-based solutions, regardless of digital transformation journey status. LiveVox’s platform is configured with features and functionalities as well as compliance standards and capabilities, and integrations with many existing third-party solutions, providing customers with a simple and scalable implementation process. LiveVox believes that its integrated offering accelerates the adoption of cloud-based contact center solutions, eliminates data silos, and allows its users to maximize engagement with their customers and create differentiated end user experiences. LiveVox believes that it is currently the only company to offer a product that integrates Omnichannel, Contact Center, CRM, WFO and AI capabilities in a single offering. |

1

| • | Attractive financial profile, underpinned by several qualities: |

| • | Recurring revenue model: LiveVox’s revenue model consists of approximately 99% recurring revenue. For the years ended December 31, 2020, 2019, 2018 and 2017, LiveVox’s revenues were $102.5 million, $92.8 million, $77.2 million and $60.6 million, respectively, representing year-over-year growth of 10%, 20% and 27%, respectively. LiveVox’s Adjusted EBITDA for the years ended December 31, 2020, 2019, 2018 and 2017 was $8.5 million, $13.3 million, $11.0 million and $3.8 million, respectively. |

| • | Attractive unit economics: LiveVox benefits from strong sales efficiency, driven by the productivity of its salesforce and flexible commercial model. This model seeks to meet customers at any stage of their digital transformation by utilizing a “land and expand” strategy that allows LiveVox to provide a subset of its full contact center solution to meet the initial requirement, and then expand that relationship by providing more features and functionality that empowers the customer to continue on their journey to greater digital and AI adoption. For the twelve months ended March 31, 2021 and March 31, 2020, LiveVox’s Last Twelve Months (“LTM”) Net Revenue Retention Rates were 99% and 118%, respectively. For the twelve |

2

| months ended December 31, 2020 and December 31, 2019, the Company’s LTM Net Revenue Retention Rates were 106% and 118%, respectively. Notwithstanding for the impact of COVID-19 on fiscal 2020, LiveVox’s average net revenue retention rate was 115% over the period 2017 to 2020. These qualities contribute to attractive unit economics. LiveVox estimates that the average calculated lifetime value of LiveVox’s customers is approximately seven times the associated cost of acquiring them for the time period from 2017 to 2020. |

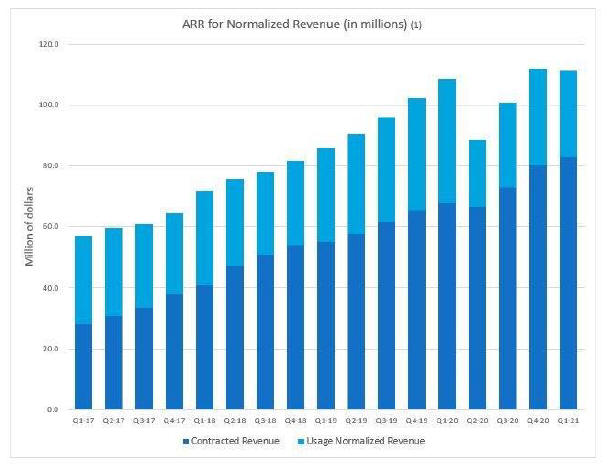

| • | Resilience: LiveVox has not experienced a sustained disruption in its overall business as a result of COVID-19. In the first half of fiscal 2020, LiveVox’s usage-based revenues were impacted due to lower volumes, although usage revenue returned to growth in the second half of fiscal 2020. The most recent stimulus packages designed to address the COVID-19 pandemic have allowed our customers to meet their goals with less effort. As a result, usage revenue declined sequentially from the fourth quarter of fiscal 2020 to the first quarter of fiscal 2021, but the relationship between contracted revenue and usage revenue is expected to recover to normal levels when the effects of the pandemic have completely dissipated. LiveVox’s contracted revenues (comprising approximately two thirds of LiveVox’s overall revenue) has grown at least 18% in each quarter of fiscal 2020 compared to the respective quarters of fiscal 2019. In the second half of fiscal 2020, LiveVox’s business rebounded to normalized levels of growth, and its bookings outperformed its budgeted plan for fiscal 2020 (that was set in fiscal 2019 and not subsequently adjusted). In the first quarter of fiscal 2021, LiveVox’s contracted revenues grew 23% over the first quarter of fiscal 2020. |

Our subscription revenue model includes contracted revenue and usage revenue, recognized on a monthly basis following deployment to the customer. Our revenue model consists of an optimized combination of contracted billing and usage-based billing, with products delivered through bundles that are designed to provide flexibility for customers at any stage of their cloud journey. Our contracted revenue is predominantly comprised of minimum contracted usage billing that is billed regardless of consumption, as well as our newer per-seat per-month fees. Usage revenue is billed for customer consumption above their contracted minimum, and a premium pricing model applies to this revenue exceeding contracted minimums. In addition, the minimum commitment helps drive upsell, and customers frequently move agents and units of service onto our platform as a trial, and then remain. Our contracted revenues (comprising approximately two thirds of our overall revenue) have grown at least 15% on a year-over-year basis for the last 11 quarters.

We leverage a land and expand sales model, focusing on “landing” agreements with large enterprises, and selling additional products and units of service over time. Our net revenue retention rate averaged 115% for the years ended December 31, 2017 to 2020, indicating a strong track record of growing revenue from existing customers. Going forward, we have identified opportunities we believe will allow us to expand our revenue from existing customers based on seats not currently using our software. Additionally, considerable upsell opportunity currently exists, with approximately 40% of customers using only one product as of March 31, 2021.

Our go-to-market strategy is led by a direct sales force. This team is primarily focused on enterprise and mid-market organizations, which LiveVox defines as organizations with (i) greater than 50 seats and (ii) the estimated potential to spend at least $5,000 per month on LiveVox’s services. We divided the team into three groups: (i) the National team composed of “Hunters” and “Farmers” focused on accounts greater than or equal to 250 seats (which we consider large accounts), (ii) the Mid-market Sales team composed of “Hunters” and “Farmers” focused on accounts between 50 and 250 seats as well as accounts where we estimate we do not have potential to increase the amount of business we do with such customer and (iii) an overlay team focused on facilitating channel leads and/or specific products on an as needed basis. “Hunters” are responsible for new logo generation and may keep accounts with upsell potential for the first year following initial booking. “Farmers” are responsible for upsell and retention following the transition from a “Hunter”. The overlay teams are responsible for assisting the “Hunters” in meeting the objectives for their area of expertise. In addition, we are investing in initiatives to grow our team of business consultants, technical account managers and customer success managers, build out our marketing capabilities, and continue to improve salesforce productivity.

3

Impact of COVID-19

While impacts associated with COVID-19 had certain adverse impacts on our business and operating results in the first two quarters of fiscal 2020, we have not experienced a sustained disruption in our overall business. In March 2020, we began to take measures to minimize disruptions to our products as a result of COVID-19. These measures included the drawdown on our revolving Credit Facility (as defined below) in the amount of $4.7 million on March 17, 2020. Additionally, we provided temporary relief to certain customers with business models that were impacted by COVID-19 and were not setup to work from home by removing contracted minimums in return for extending contract lengths to enable financial relief during the time required to transition to work from home agent models. This relief did not have a material impact on our financial results.

In the first half of fiscal 2020, our usage-based revenues were impacted due to lower volumes. Our new revenue bookings (which we describe as “land” bookings) in the first quarter of fiscal 2020 were impacted by the pandemic, as many customers delayed new bookings to evaluate the impact of COVID-19 on their business models. However, revenue bookings from existing customers (which we describe as “expand” bookings) remained healthy over this period. Churn rates were temporarily elevated in the second quarter of fiscal 2020 as customers with business models that were severely impacted by COVID-19 ceased operations, including one of our top 10 customers by revenue.

In the second half of fiscal 2020 and the first quarter of fiscal 2021, our business improved, and our bookings outperformed our budgeted plan for such periods (which was set in fiscal 2019 and fiscal 2020 respectively and not subsequently adjusted). In the first quarter of fiscal 2021, the most recent stimulus packages designed to address the COVID-19 pandemic have allowed our customers to meet their goals with less effort. As a result, usage revenue declined sequentially from the fourth quarter of fiscal 2020 to the first quarter of fiscal 2021. When the effects of the pandemic have completely dissipated we expect the relationship between usage and contracted revenues to recover to normal levels. Our contracted revenues (comprising approximately two thirds of our overall revenue) grew 23% for the first quarter of fiscal 2021 compared to the first quarter of fiscal 2020.

In fiscal 2020 and the first quarter of fiscal 2021, we experienced a proportion of recurring revenue to contracted revenue that was lower than historical levels. We believe that when the impacts of COVID-19 dissipate, our usage above contracted minimums and therefore the proportion of recurring revenue to contracted revenue will return to normalized historical levels. Our methodology for assessing normalized revenue adjusts for the variability in available dialing days in each monthly period and also accounts for reduced dialing behavior on weekends and holidays. Contracted revenue does not vary due to available dialing days.

Key Factors and Trends Affecting Our Business

Going forward, we expect our business to continue to be driven by the following factors:

| • | Market penetration of cloud contact center solutions: We view the market opportunity for cloud-based contact center solutions as significant. Factors such as remote working, digital transformation, and the shift to value-added services at the contact center level have driven a shift from on-premise to cloud-based solutions. We intend to continue investing in sales and marketing to reach new customers and expand our market position. |

| • | Product leadership: We have evolved from an outbound-focused software platform provider for collections agencies to an integrated omnichannel platform that addresses all aspects of the agent experience. We will continue to invest in new technologies and harness existing ones. |

4

| • | Investments in growth: We are growing our team of customer success managers and field-based representatives, building our marketing capabilities to expand our reach, and investing in initiatives to improve salesforce productivity. |

| • | Usage of our products: We employ a mix of contracted and usage-based revenue that is unique in our market. Thus, we depend on usage-based revenue for a component of our revenue. This stream of revenue provides additional upside, and over a long period of time, has generally been stable. In addition, this usage-based revenue stream allows us to grow with our customers as they scale. |

LiveVox’s Segments

LiveVox has determined that its Chief Executive Officer is its chief operating decision maker. LiveVox’s Chief Executive Officer reviews financial information presented on a consolidated basis for purposes of assessing performance and making decisions on how to allocate resources. Accordingly, LiveVox has determined that it operates in a single reportable segment.

Key Operating and Non-GAAP Financial Performance Metrics

In addition to measures of financial performance presented in our consolidated financial statements, we monitor the key metrics set forth below to help us evaluate growth trends, establish budgets, measure the effectiveness of our sales and marketing efforts and assess operational efficiencies.

LTM Net Revenue Retention Rate

We believe that our LTM Net Revenue Retention Rate provides us and investors with insight into our ability to retain and grow revenue from our customers and is a meaningful measure of the long-term value of our customer relationships. LiveVox calculates LTM Net Revenue Retention Rate by dividing the recurring revenues recognized during the most recent LTM period by the recurring revenues recognized during the LTM period immediately preceding the most recent LTM period, provided, however, that recurring revenues from any customer in the most recent LTM period are excluded from the calculation if recurring revenues were not recognized from such customer in the preceding LTM period. Customers who cease using LiveVox’s products during the most recent LTM period are included in the calculation, but new customers who begin using LiveVox’s products during the most recent LTM period are not included in the calculation. For example, LTM Net Revenue Retention for the 12-month period ending December 2020 includes recurring revenues from all customers for whom revenues were recognized in 2019 regardless of whether such customers increased, decreased, or stopped their use of LiveVox’s products during 2020 (i.e., old customers), but exclude all recurring revenues from all customers who began to use LiveVox’s services during 2020 (i.e., new customers). We define monthly recurring revenue as recurring monthly contracted and usage revenue, which we calculate separately from one-time, non-recurring revenue by month by customer. We consider all contracted and usage-based revenue, which represents 99% of our revenue to be recurring revenue as all of our contracts provide for a minimum commitment amount. We consider professional services revenue and one-time adjustments, which are booked on a one-time, nonrecurring basis, to be non-recurring revenue. Professional services and other one-time adjustments are generally not material to the result of the calculation. However, one-time non-recurring revenue is important with respect to timing as we bill installation and non-standard statement of work fees immediately and recognize the revenue as the work is completed, which is generally in advance of the beginning of recurring revenue.

5

The following table shows our LTM Net Revenue Retention Rate for the periods presented:

| Twelve Months Ended March 31, |

Twelve Months Ended December 31, |

|||||||||||||||

| 2021 | 2020 | 2020 | 2019 | |||||||||||||

| LTM Net Revenue Retention Rate |

99 | % | 118 | % | 106 | % | 118 | % | ||||||||

Our LTM Net Revenue Retention Rate reflects the expansion over time of our existing customers as they add new products and additional units of service. A much higher percentage of our customers are contracted on our variable per minute pricing model with a minimum commitment as compared to our per agent pricing model with minimum commitments for both agents and units of service.

Our LTM Net Revenue Retention Rate decreased by 19%, to 99% in the twelve months ended March 31, 2021 from 118% in the twelve months ended March 31, 2020 primarily as a result of the impacts of COVID-19 in combination with contracted and usage revenue mix. Despite the decline in LTM Net Revenue Retention Rate, monthly minimum contracted revenue for customers grew by 25% from the end of the first quarter of fiscal 2020 to the end of the first quarter of fiscal 2021.

Our LTM Net Revenue Retention Rate decreased by 12%, to 106% in the twelve months ended December 31, 2020 from 118% in the twelve months ended December 31, 2019 primarily as a result of the impacts of COVID-19 in combination with contracted and usage revenue mix. Despite the decline in LTM Net Revenue Retention Rate, monthly minimum contracted revenue for customers grew by 20% from fiscal 2019 to fiscal 2020.

Adjusted EBITDA

We monitor Adjusted EBITDA, a non-generally accepted accounting principle (“Non-GAAP”) financial measure, to analyze our financial results and believe that it is useful to investors, as a supplement to U.S. GAAP measures, in evaluating our ongoing operational performance and enhancing an overall understanding of our past financial performance. We believe that Adjusted EBITDA helps illustrate underlying trends in our business that could otherwise be masked by the effect of the income or expenses that we exclude from Adjusted EBITDA. Furthermore, we use this measure to establish budgets and operational goals for managing our business and evaluating our performance. We also believe that Adjusted EBITDA provides an additional tool for investors to use in comparing our recurring core business operating results over multiple periods with other companies in our industry.

Adjusted EBITDA should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with U.S. GAAP, and our calculation of Adjusted EBITDA may differ from that of other companies in our industry. We compensate for the inherent limitations associated with using Adjusted EBITDA through disclosure of these limitations, presentation of our consolidated financial statements in accordance with U.S. GAAP and reconciliation of Adjusted EBITDA to the most directly comparable U.S. GAAP measure, net income (loss). We calculate Adjusted EBITDA as net income (loss) before (i) depreciation and amortization, (ii) stock-based compensation, (iii) interest income, expense and other, (iv) provision (benefit from) for income taxes, and (v) other items that do not directly affect what we consider to be our core operating performance.

6

The following table shows a reconciliation of net income (loss) to Adjusted EBITDA for the periods presented (in thousands):

| Three Months Ended March 31, (unaudited) |

||||||||

| 2021 | 2020 | |||||||

| Net loss |

$ | (4,175 | ) | $ | (553 | ) | ||

| Non-GAAP adjustments: |

||||||||

| Depreciation and amortization |

1,604 | 1,516 | ||||||

| Long-term equity incentive bonus and stock-based compensation expense |

139 | 184 | ||||||

| Interest expense, net |

944 | 984 | ||||||

| Other expense (income), net |

(7 | ) | 132 | |||||

| Acquisition and financing related fees and expenses |

284 | 25 | ||||||

| Transaction-related costs |

733 | — | ||||||

| Golden Gate Capital management fee expenses |

171 | 156 | ||||||

| Provision for income taxes |

35 | 60 | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | (272 | ) | $ | 2,504 | |||

|

|

|

|

|

|||||

Non-GAAP Gross Profit and Non-GAAP Gross Margin percentage

U.S. GAAP defines gross profit as revenue less cost of revenue. Cost of revenue includes all expenses associated with our various product offerings as more fully described under the caption “Components of LiveVox’s Results of Operations—Cost of Revenue” below. We define Non-GAAP gross profit as gross profit after adding back the following items:

| • | depreciation and amortization; |

| • | long-term equity incentive bonus and stock-based compensation expense; and |

| • | other non-recurring expenses |

We add back depreciation and amortization, long-term equity incentive bonus and stock-based compensation expense and other non-recurring expenses because they are one-time or non-cash items. We eliminate the impact of these one-time or non-cash items because we do not consider them indicative of our core operating performance. Their exclusion facilitates comparisons of our operating performance on a period-to-period basis. Therefore, we believe showing gross margin, as Non-GAAP to remove the impact of these one-time or non-cash expenses is helpful to investors in assessing our gross profit and gross margin performance in a way that is similar to how management assesses our performance.

We calculate Non-GAAP gross margin percentage by dividing Non-GAAP gross profit by revenue, expressed as a percentage of revenue.

Management uses Non-GAAP gross profit and Non-GAAP gross margin percentage to evaluate operating performance and to determine resource allocation among our various product offerings. We believe Non-GAAP gross profit and Non-GAAP gross margin percentage provide useful information to investors and others to understand and evaluate our operating results in the same manner as our management and board of directors and

7

allows for better comparison of financial results among our competitors. Non-GAAP gross profit and Non-GAAP gross margin percentage may not be comparable to similarly titled measures of other companies because other companies may not calculate Non-GAAP gross profit and Non-GAAP gross margin percentage or similarly titled measures in the same manner as we do.

The following table shows a reconciliation of gross profit to Non-GAAP gross margin percentage for the periods presented (in thousands):

| Three Months Ended March 31, (unaudited) |

||||||||

| 2021 | 2020 | |||||||

| Gross profit |

$ | 16,765 | $ | 16,547 | ||||

| Depreciation and amortization |

944 | 969 | ||||||

| Long-term equity incentive bonus and stock-based compensation expense |

14 | 14 | ||||||

|

|

|

|

|

|||||

| Non-GAAP gross profit |

$ | 17,723 | $ | 17,530 | ||||

| Non-GAAP gross margin % |

63.4 | % | 66.1 | % | ||||

Components of LiveVox’s Results of Operations

Revenue

LiveVox derives revenues by providing products under a variety of pricing models. Voice has been historically provided under a usage-based pricing model with prices calculated on a per-minute basis with a contracted minimum commitment in accordance with the terms of the underlying pricing agreements. Voice is LiveVox’s predominant source of revenue. Other revenue sources are derived from products under the following pricing models:

| 1) | a per “unit of measure” with a minimum commitment (e.g., Speech IQ); |

| 2) | the combination of per agent and per “unit of measure” models with minimum contracted commitments for each (e.g., SMS, email, U-CRM services); |

| 3) | a per agent pricing model with a minimum agent commitment (e.g., U-Script, U-Ticket, U-Chat, U-Quality Management, U-Screen Capture, U-CSAT, U-BI); and |

| 4) | a per agent pricing model with a minimum agent commitment with a monthly maximum commitment (e.g., PDAS–our compliance product, U-BI). |

Outside of Voice, our pricing models detailed above are relatively new to the market and are not yet material to our business from a financial perspective.

Cost of Revenue

Our cost of revenue consists of personnel costs and associated costs such as travel, information technology, facility allocations and stock-based compensation for Implementation and Training Services, Customer Care, Technical Support, Professional Services, User Acceptance Quality Assurance, Technical Operations and VOIP services to our customers. Other costs of revenue include non-cash costs associated with depreciation and amortization including acquired technology; charges from telecommunication providers for communications, data center costs and costs to providers of cloud communication services, software, equipment maintenance and support costs to maintain service delivery operations.

8

Our data center costs are transitioning from a model based on maintaining a co-location facility with our own capital equipment to a cloud strategy based on monthly recurring charges for capacity added in generally small step function increments. The transition began in fiscal 2019 and is expected to be complete in fiscal 2021. As a result, we have reduced our capital expenditures for data center equipment, which has slowed growth in depreciation and increased our data center costs for our cloud provisioning. We expect feature release efficiencies for our cloud operations as research and development resources eliminate the release effort associated with our co-location deployment. We have accelerated depreciation expense associated with the change in useful life estimate of the co-location facility.

As our business grows, we expect to realize economies of scale in our cost of revenue. We use the LiveVox platform to facilitate data-driven innovations to identify and facilitate efficiency improvement to our implementation, customer care and support, and technical operations teams. Additionally, our research and development priorities include ease of implementation, reliability and ease of use objectives that reduce costs and result in economies of scale relative to revenue growth.

Operating Expenses

We classify our operating expenses as sales and marketing, general and administrative, and research and development.

Sales and Marketing. Sales and marketing expenses consist primarily of salaries and related expenses, including stock-based compensation, for personnel in sales and marketing, sales commissions, travel costs, as well as marketing pipeline management, content delivery, programs, campaigns, lead generation, and allocated overhead. We believe it is important to continue investing in sales and marketing to continue to generate revenue growth, and we expect sales and marketing expenses to increase in absolute dollars and fluctuate as a percentage of revenue as we continue to support our growth initiatives.

General and Administrative. General and administrative expenses consist primarily of salary and related expenses, including stock-based compensation, for management, finance and accounting, legal, information systems and human resources personnel, professional fees, compliance costs, other corporate expenses and allocated overhead. We expect that general and administrative expenses will fluctuate in absolute dollars from period to period but decline as a percentage of revenue over time.

Research and Development. Research and development expenses consist primarily of salary and related expenses, including stock-based compensation, for personnel related to the identification and development of improvements and expanded features for our products, as well as quality assurance, testing, product management and allocated overhead. Research and development costs are expensed as incurred. We have not performed research and development for internal-use software that would meet the qualifications for capitalization. We believe it is important to continue investing in research and development to continue to expand and improve our products and generate future revenue growth, and we expect research and development expenses to increase in absolute dollars and fluctuate as a percentage of revenue as we continue to support our growth initiatives.

9

Results of Operations

The following tables summarize key components of LiveVox’s results of operations for the periods indicated (in thousands, except per share data):

| Three Months Ended March 31, (unaudited) |

||||||||

| 2021 | 2020 | |||||||

| Revenue |

$ | 27,945 | $ | 26,519 | ||||

| Cost of revenue |

11,180 | 9,972 | ||||||

|

|

|

|

|

|||||

| Gross profit |

16,765 | 16,547 | ||||||

| Operating expenses |

||||||||

| Sales and marketing expense |

8,908 | 8,119 | ||||||

| General and administrative expense |

4,880 | 3,066 | ||||||

| Research and development expense |

6,180 | 4,738 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

19,968 | 15,923 | ||||||

|

|

|

|

|

|||||

| Income (loss) from operations |

(3,203 | ) | 624 | |||||

| Interest expense, net |

944 | 984 | ||||||

| Other expense (income), net |

(7 | ) | 132 | |||||

|

|

|

|

|

|||||

| Total other expense, net |

937 | 1,116 | ||||||

|

|

|

|

|

|||||

| Pre-tax income loss |

(4,140 | ) | (492 | ) | ||||

| Provision for income taxes |

35 | 61 | ||||||

|

|

|

|

|

|||||

| Net loss |

$ | (4,175 | ) | $ | (553 | ) | ||

| Net loss per share - basic and diluted |

$ | (4,175 | ) | $ | (553 | ) | ||

| Weighted average shares outstanding - basic and diluted |

1 | 1 | ||||||

|

|

|

|

|

|||||

Comparison of the three months ended March 31, 2021 and 2020 (in thousands)

Revenue

| Three Months Ended March 31, (unaudited) |

||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||

| Revenue |

$ | 27,945 | $ | 26,519 | $ | 1,426 | 5.4 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Revenue increased by $1.4 million, or 5.4%, to $27.9 million in the three months ended March 31, 2021 from $26.5 million in the three months ended March 31, 2020, primarily due to the acquisition of new customers and upsells to our existing customer base. The recent stimulus packages designed to address the COVID-19 pandemic have allowed our customers to meet their goals with less effort, reducing usage volumes which were more than offset by 23% growth in contracted revenue.

10

Cost of revenue

| Three Months Ended March 31, (unaudited) |

||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||

| Cost of revenue |

$ | 11,180 | $ | 9,972 | $ | 1,208 | 12.1 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| % of revenue |

40.0 | % | 37.6 | % | ||||||||||||

Cost of revenue increased by $1.2 million, or 12.1%, to $11.2 million in the three months ended March 31, 2021 from $10.0 million in the three months ended March 31, 2020. The increase was attributable primarily to increases in cloud data center costs.

Gross profit

| Three Months Ended March 31, (unaudited) |

||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||

| Gross profit |

$ | 16,765 | $ | 16,547 | $ | 218 | 1.3 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross margin percentage |

60.0 | % | 62.4 | % | ||||||||||||

Gross profit increased by $0.2 million, or 1.3%, to $16.7 million in the three months ended March 31, 2021 from $16.5 million in the three months ended March 31, 2020. The increase in gross profit was a result of higher revenue that offset the increased cloud data center costs we experienced while transitioning from our co-location deployment.

Sales and marketing expense

| Three Months Ended March 31, (unaudited) |

||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||

| Sales and marketing expense |

$ | 8,908 | $ | 8,119 | $ | 789 | 9.7 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| % of revenue |

31.9 | % | 30.6 | % | ||||||||||||

Sales and marketing expense increased by $0.8 million, or 9.7%, to $8.9 million in the three months ended March 31, 2021 from $8.1 million in the three months ended March 31, 2020. The increase was primarily due to increased personnel costs of $1.4 million and higher marketing, promotions and tradeshows of $0.2 million. These increases were partially offset by decreased travel costs of $0.5 million and decreased miscellaneous sales and marketing costs of $0.5 million.

11

General and administrative expenses

| Three Months Ended March 31, (unaudited) |

||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||

| General and administrative expense |

$ | 4,880 | $ | 3,066 | $ | 1,814 | 59.2 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| % of revenue |

17.5 | % | 11.6 | % | ||||||||||||

General and administrative expenses increased by $1.8 million, or 59.2%, to $4.9 million in the three months ended March 31, 2021 from $3.1 million in the three months ended March 31, 2020. The increase was primarily for accounting, audit and legal fees of $0.8 million in preparation to become a public company. Additionally, personnel costs increased $0.7 million, and office space expenses increased $0.3 million.

Research and development expense

| Three Months Ended March 31, (unaudited) |

||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||

| Research and development expense |

$ | 6,180 | $ | 4,738 | $ | 1,442 | 30.4 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| % of revenue |

22.1 | % | 17.9 | % | ||||||||||||

Research and development expenses increased by $1.5 million, or 30.4%, to $6.2 million in the three months ended March 31, 2021 from $4.7 million in the three months ended March 31, 2020. The increase was primarily due to increased personnel costs of $1.0 million, driven by increased headcount and above average salary increases to retain certain essential employees. Additionally, computing costs used in the development of software increased $$0.4 million.

Interest expense, net

| Three Months Ended March 31, (unaudited) |

|

|

||||||||||||||||||

| 2021 | 2020 | $ Change | % Change | |||||||||||||||||

| Interest expense, net |

$ | 944 | $ | 984 | $ | (40 | ) | (4.1 | ) | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| % of revenue |

3.4 | % | 3.7 | % | ||||||||||||||||

Interest expense, net decreased by $0.04 million, or 4.1%, to $0.94 million in the three months ended March 31, 2021 from $0.98 million in the three months ended March 31, 2020. The decrease was attributable primarily to decreased interest expense of $0.07 million associated with the decreased outstanding principal amount of our term loan and the lower interest rates.

12

Liquidity and Capital Resources

Overview

As of March 31, 2021 and December 31, 2020, LiveVox held cash and cash equivalents of $14.2 million and $18.1 million. respectively. In addition, we had restricted cash of $0.1 million as of March 31, 2021 related to the holdback amount for one acquisition the Company made in 2019, and $1.5 million in restricted cash as of December 31, 2020 related to the holdback amount for the two acquisitions the Company made in 2019. LiveVox’s primary use of cash is for operation and administrative activities including employee related expenses, and general, operating and overhead expenses. Future capital requirements will depend on many factors, including our customer growth rate, customer retention, timing and extent of development efforts, the expansion of sales and marketing activities, the introduction of new and enhanced product offerings, the continuing market acceptance of our products, effective integration of acquisition activities, and maintaining our bank credit facility. Additionally, the duration and extent of the impact from the COVID-19 pandemic continues to depend on future developments that cannot be accurately predicted at this time, such as the ongoing severity and transmission rate of the virus, the extent and effectiveness of vaccine programs and other containment actions, the duration of social distancing, office closure and other restrictions on businesses and society at large, and the specific impact of these and other factors on LiveVox’s business, employees, customers and partners. While the COVID- 19 pandemic has caused operational difficulties, and may continue to create unprecedented challenges, it has not thus far had a substantial net impact on the Company’s liquidity position.

On February 28, 2018, LiveVox entered into an amendment to its term loan and revolving credit facility with PNC Bank originally dated November 7, 2016 (as so amended, the “Credit Facility”) to provide for a $45.0 million term loan, a $5.0 million line of credit and a $1.5 million letter of credit sub-facility. The agreement governing the Credit Facility had a five-year term ending November 7, 2021. The Credit Facility is collateralized by a first-priority perfected security interest in substantially all the assets of LiveVox and is subject to certain financial covenants before and after a covenant conversion date. Covenant conversion may be elected early by LiveVox if certain criteria are met, including, but not limited to meeting fixed charge coverage and liquidity ratio targets as of the most recent twelve-month period. Prior to the covenant conversion date, LiveVox is required to maintain minimum levels of liquidity and recurring revenue. As of the covenant conversion date, LiveVox is required to maintain the Fixed Charge Coverage Ratio and Leverage Ratio (as defined in the Credit Facility) measured on a quarter-end basis for the four-quarter period ending on each such date through the end of the agreement.

On December 16, 2019, LiveVox amended the Credit Facility (as amended, the “Amended Credit Facility”), increasing the term loan borrowing therein by $13.9 million to $57.6 million and amending certain terms and conditions. The Amended Credit Facility reset the minimum recurring revenue covenant and qualified cash amounts through December 31, 2021 and extended the quarterly measurement dates through September 30, 2023 and the maturity date to November 7, 2023. LiveVox was in compliance with all debt covenants at March 31, 2021 and December 31, 2020 and was in compliance with all debt covenants as of the date of issuance of these consolidated financial statements. There was no unused borrowing capacity under the term loan portion of the Amended Credit Facility at March 31, 2021 and December 31, 2020. On March 17, 2020, as a precautionary measure to ensure financial flexibility and maintain maximum liquidity in response to COVID-19 pandemic, LiveVox drew down approximately $4.7 million under the revolving portion of the Amended Credit Facility.

LiveVox’s consolidated financial statements have been prepared assuming LiveVox will continue as a going concern for the 12 months from the date of issuance of the consolidated financial statements, which contemplates the realization of assets and the settlement of liabilities and commitments in the normal course of business.

13

LiveVox’s main sources of liquidity were cash generated by operating cash flows and the term loan and revolving credit facility.

Acquisition Opportunities

We believe that there may be opportunity for further consolidation in our industry. From time to time, we evaluate potential strategic opportunities, including acquisitions of other providers of cloud-based services. We have been in, and from time to time may engage in, discussions with counterparties in respect of various potential strategic acquisition and investment transactions. Some of these transactions could be material to our business and, if completed, could be difficult to integrate, result in increased leverage or dilution and/or subject us to unexpected liabilities. In connection with evaluating potential strategic acquisition and investment transactions, we may incur significant expenses for the evaluation and due diligence investigation of these potential transactions.

Cash flow (in thousands)

| Three Months Ended March 31, (unaudited) |

||||||||

| 2021 | 2020 | |||||||

| Net cash provided by (used in) operating activities |

$ | (5,091 | ) | $ | 415 | |||

| Net cash provided by (used in) investing activities |

1,136 | (212 | ) | |||||

| Net cash provided by (used in) financing activities |

(1,319 | ) | 4,190 | |||||

| Effect of foreign currency translation |

(21 | ) | (96 | ) | ||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash, cash equivalents and restricted cash |

$ | (5,295 | ) | $ | 4,297 | |||

|

|

|

|

|

|||||

Net cash provided by (used in) operating activities

Cash flows from operating activities during the three months ended March 31, 2021 decreased by $5.5 million to $(5.1) million from $0.4 million during the same period in 2020. The decrease to net cash provided by (used in) operating activities was primarily attributable to a $3.6 million decrease to net loss and a decrease of $0.4 million in non-cash adjustments to net loss. These non-cash items primarily consisted of a $0.6 million decrease of bad debt expense being offset by a $0.1 million increase of amortization of deferred sales commissions. Net cash provided by (used in) operating activities has a decrease of $1.5 million in cash from operating assets and liabilities, primarily due to the accrued contingent considerations in asset acquisition.

Net cash provided by (used in) investing activities

Cash flows from investing activities during the three months ended March 31, 2021 increased by $1.3 million to $1.1 million from $(0.2) million during the same period in fiscal 2020. Net cash provided by investing activities during the three months ended March 31, 2021 was comprised of $1.3 million in asset acquisition, offset by $0.2 million in purchases of property and equipment.

Net cash provided by (used in) financing activities

Cash flows from financing activities during the three months ended March 31, 2021 decreased by $5.5 million, or 131.5%, to $(1.3) million from $4.2 million during the same period in 2020, reflecting a $0.9 million increase of repayment on loan payable, offset by the drawdown on the revolving portion of the Amended Credit Facility of $4.7 million in March of 2020.

14

Contractual Obligations and Commitments

Our principal contractual obligations consist of future payment obligations under our term loan, finance leases to finance computer and networking equipment, and operating leases for office facilities. Please see Note 9 to the consolidated financial statements of LiveVox included elsewhere in the Super 8-K for discussion of the contractual obligations under LiveVox’s term facility.

The following table summarizes our significant contractual obligations as of March 31, 2021 (in thousands):

| Payment Due by Period | ||||||||||||||||||||

| Total | Remaining 2021 |

1-3 Years | 4-5 Years | More than 5 Years |

||||||||||||||||

| Finance lease obligations (1) |

$ | 299 | $ | 259 | $ | 40 | $ | — | $ | — | ||||||||||

| Operating lease obligations (2) |

7,713 | 1,557 | 4,915 | 1,116 | 125 | |||||||||||||||

| Term loan (3) |

56,094 | 1,080 | 55,014 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

$ | 64,106 | $ | 2,896 | $ | 59,969 | $ | 1,116 | $ | 125 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | Represents financing of computer and networking equipment and software purchases for our co-location data centers. |

| (2) | Represents obligations to make payments under lease agreements for our corporate headquarters and worldwide offices. |

| (3) | Consists of principal payments only, excluding interest of $0.9 million. The principal amount is due November 7, 2023. |

Off-Balance Sheet Arrangements

As of March 31, 2021, we did not have any off-balance sheet arrangements, as defined in Item 303(a)(4)(ii) of SEC Regulation S-K, such as the use of unconsolidated subsidiaries, structured finance, special purpose entities or variable interest entities.

Critical Accounting Policies and Use of Estimates

The preparation of the consolidated financial statements included elsewhere in the Super 8-K in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting periods. Significant items subject to such estimates and assumptions include, but are not limited to, the determination of the useful lives of long-lived assets, allowances for doubtful accounts, fair value of goodwill and long-lived assets, fair value of incentive awards, establishing standalone selling price, valuation of deferred tax assets, income tax uncertainties, and other contingencies. Management periodically evaluates such estimates and they are adjusted prospectively based upon such periodic evaluation. Actual results could differ from those estimates. While our significant accounting policies are more fully described in the notes to its consolidated financial statements included elsewhere in the Super 8-K, we believe that the following accounting policies and estimates are critical to our business operations and understanding of its financial results.

15

Impairment of long-lived assets, including intangible assets

Long-lived assets to be held and used are reviewed for impairment whenever events or changes in circumstances indicate that the related carrying amount may not be recoverable. When required, impairment losses on assets to be held and used are recognized based on the fair value of the asset and long-lived assets to be disposed of are reported at the lower of the carrying amount or fair value. No impairment losses have been recognized in any of the periods presented.

Through the year ended December 31, 2019, we performed its annual impairment review of goodwill at December 31, and when a triggering event occurs between annual impairment tests. In anticipation of the reporting requirements in connection with being a public company, we changed the date of its annual goodwill impairment test to October 1, effective for the year 2020. In testing for goodwill impairment, we first assess qualitative factors. If, based on the qualitative assessment, it is determined that it is more likely than not that the fair value of the Company’s single reporting unit is less than its carrying amount, including goodwill, we will perform the quantitative impairment test in accordance with Accounting Standards Codification (“ASC”) 350-20-35, as amended by Accounting Standards Update (“ASU”) 2017-04, to determine if the fair value of the reporting unit exceeds its carrying amount. If the fair value is determined to be less than the carrying value, an impairment charge is recorded for the amount by which the reporting unit’s carrying amount exceeds its fair value, limited to the total amount of goodwill allocated to that reporting unit. No impairment losses have been recognized in any of the periods presented.

Intangible assets, consisting of acquired developed technology, corporate name, customer relationships and workforce, are carried at cost less accumulated amortization. All intangible assets have been determined to have definite lives and are amortized on a straight-line basis over their estimated remaining economic lives, ranging from three to ten years. Amortization expense related to developed technology is included in cost of revenue. Amortization expense related to customer relationships and corporate name is included in sales and marketing expense. Amortization expense related to acquired workforce is included within cost of revenue and research and development expense. Intangible assets are reviewed for impairment whenever events or changes in circumstances indicate an asset’s carrying value may not be recoverable. No impairment losses have been recognized in any of the periods presented.

Revenue Recognition

LiveVox recognizes revenue in accordance with U.S. GAAP, pursuant to ASC 606, Revenue from Contracts with Customers.

LiveVox derives substantially all of its revenues by providing cloud-based contact center voice products under a usage-based model, with prices calculated on a per-call, per-seat, or, more typically, a per-minute basis and contracted minimum usage in accordance with the terms of the underlying agreements. Other immaterial ancillary revenues are derived from call recording, local caller identification packages, performance/speech analytics, text messaging services and professional services billed monthly on primarily usage-based fees, and to a lesser extent, fixed fees. Revenues are recognized when control of these services is transferred to our customers, in an amount that reflects the consideration we expect to be entitled to in exchange for those services excluding amounts collected on behalf of third parties such as sales taxes, which are collected on behalf of and remitted to governmental authorities based on local tax law.

We determine revenue recognition through the following steps:

| a. | Identification of the contract, or contracts, with a customer; |

| b. | Identification of the performance obligations in the contract; |

16

| c. | Determination of the transaction price; |

| d. | Allocation of the transaction price to the performance obligations in the contract; and |

| e. | Recognition of revenue when, or as, the performance obligations are satisfied. |

We enter into contracts that can include various combinations of services, each of which are distinct and accounted for as separate performance obligations. Our cloud-based contact center solutions typically include a promise to provide continuous access to our hosted technology platform solutions through one of our data centers. Arrangements with customers do not provide the customer with the right to take possession of LiveVox’s software platform at any time. Our performance obligations are satisfied over time as the customer simultaneously receives and consumes the benefits as we perform our services. Our contracts typically range from annual to three-year agreements with payment terms of net 10-60 days. As the services provided by LiveVox are generally billed monthly there is not a significant financing component in LiveVox’s arrangements.

LiveVox’s arrangements typically include monthly minimum usage commitments and specify the rate at which the customer must pay for actual usage above the monthly minimum. Additional usage in excess of contractual minimum commitments are deemed to be specific to the month that the usage occurs, since the minimum usage commitments reset at the beginning of each month. We have determined these arrangements meet the variable consideration allocation exception and therefore, we recognize contractual monthly commitments and any overages as revenue in the month they are earned.

LiveVox has service-level agreements with customers warranting defined levels of uptime reliability and performance. Customers may receive credits or refunds if the Company fails to meet such levels. If the services do not meet certain criteria, fees are subject to adjustment or refund representing a form of variable consideration. LiveVox records reductions to revenue for these estimated customer credits at the time the related revenue is recognized. These customer credits are estimated based on current and historical customer trends, and communications with its customers. Such customer credits have not been significant to date.

For contracts with multiple performance obligations, we allocate the contract price to each performance obligation based on its relative standalone selling price (“SSP”). We generally determine SSP based on the prices charged to customers. In instances where SSP is not directly observable, such as when we do not sell the service separately, we determine the SSP using information that generally includes market conditions or other observable inputs.

Professional services for configuration, system integration, optimization or education are billed on a fixed-price or on a time and material basis and are performed by LiveVox directly or, alternatively, customers may also choose to perform these services themselves or engage their own third-party service providers. Professional services revenue, which represents less than 1% of revenue, is recognized over time as the services are rendered.

Deferred revenues represent billings or payments received in advance of revenue recognition and are recognized upon transfer of control. Balances consist primarily of annual or multi-year minimum usage agreements not yet provided as of the balance sheet date. Deferred revenues that will be recognized during the succeeding twelve-month period are recorded as deferred revenues, current in the consolidated balance sheets, with the remainder recorded as deferred revenue, net of current in the Company’s consolidated balance sheets.

Income Taxes

LiveVox accounts for income taxes using the asset and liability approach. Deferred tax assets and liabilities are recognized for the future tax consequences arising from the temporary differences between the tax basis of an asset or liability and its reported amount in the consolidated financial statements, as well as from net operating loss

17

and tax credit carryforwards. Deferred tax amounts are determined by using the tax rates expected to be in effect when the taxes will be paid or refunds received, as provided for under currently enacted tax law. A valuation allowance is provided for deferred tax assets that, based on available evidence, are not expected to be realized. LiveVox recognizes the effect of income tax positions only if those positions are more likely than not of being sustained. Recognized income tax positions are measured at the largest amount that is greater than 50% likely of being realized. Changes in recognition or measurement are reflected in the period in which the change in judgment occurs.

LiveVox recognizes the effect of income tax positions only if those positions are more likely than not of being sustained. LiveVox does not believe its consolidated financial statements include any uncertain tax positions. It is LiveVox’s policy to recognize interest and penalties accrued on any unrecognized tax benefit as a component of income tax expense.

Employee and Non-Employee Incentive Plans

During 2014, LiveVox established two bonus incentive plans, the Value Creation Incentive Plan (which we refer to as the “VCIP”) and the Option-based Incentive Plan (which we refer to as the “OBIP”), pursuant to which eligible participants will receive a predetermined bonus based on the Company’s equity value at the time of a liquidity event, if the stockholder return associated with the liquidity event exceeds certain thresholds (as defined in the VCIP and OBIP). All of the Company’s executive officers and certain other key employees are eligible to participate in the VCIP and certain other employees are eligible to participate in the OBIP. Awards under the VCIP and OBIP are subject to both time-based and performance-based vesting conditions. Awards under the VCIP and OBIP generally time vest over 5 years and performance vest upon certain liquidity event conditions, subject to continued service through the vesting dates. Under the VCIP, the value at payoff is further adjusted based on the stockholder returns resulting from the liquidity event while the OBIP has a minimum stockholder return. For a portion of each award, the liquidity event condition can be met post termination of service, as long as the time-based vesting period has been completed. The awards under the VCIP and OBIP may be settled in cash or shares, depending on the nature of the underlying liquidity event. LiveVox also has an option to repurchase both awards at an amount deemed to be fair value for which the time-based vesting period has been completed, contingent on the employee’s termination of service. Because vesting and payment under the VCIP and OBIP is contingent upon a liquidity event, the Company will not record compensation expense until a liquidity event occurs or unless they are repurchased, in which case the Company has recorded compensation expense equal to the repurchase amount. The Company remeasures the awards’ fair value at each reporting period. These awards are reflected as Level 3 in the fair value table. The fair value used by the Company has historically been determined by the LiveVox board of directors with assistance of management. The LiveVox board of directors has determined the fair value at each reporting period by considering a number of objective and subjective factors including important developments in the Company’s operations, valuations performed by an independent third party, actual results and financial performance, the conditions in the CCaaS industry and the economy in general, volatility of comparable public companies, among other factors.

During 2019, LiveVox implemented a one-time management liquidity program, in which certain executives with time-based vested VCIP awards were liquidated and paid out in cash. LiveVox recorded this event as compensation expense within cost of revenue and operating expenses within the consolidated financial statements for the year ended December 31, 2019 in the amount of $8.7 million, of which $4.3 million is recorded in accrued bonuses and was paid out within 12 months from December 31, 2019.

During 2019, LiveVox TopCo established a Management Incentive Unit program whereby the LiveVox board of directors has the power and discretion to approve the issuance of Class B Units of LiveVox TopCo that represent management incentive units (which we call “Management Incentive Units” or “MIU”) to any manager, director, employee, officer or consultant of the Company or its Subsidiaries. Vesting begins on the date of issuance, and the

18

Management Incentive Units vest ratably over five years with 20% of the Management Incentive Units vesting on the first anniversary of a specified vesting commencement date, and then quarterly thereafter, subject to the grantee’s continued employment with the Company on the applicable vesting date. Vesting of the Management Incentive Units will accelerate upon consummation of a “sale of the company”, which is defined by the LiveVox TopCo limited liability company agreement as (i) the sale or transfer of all or substantially all of the assets of LiveVox TopCo on a consolidated basis or (ii) any direct or indirect sale or transfer of a majority of interests in LiveVox TopCo and its subsidiaries on a consolidated basis, as a result of any party other than certain affiliates of Golden Gate Capital obtaining voting power to elect the majority of LiveVox TopCo’s governing body.

If a Management Incentive Unit holder terminates employment, any vested Management Incentive Units as of the termination date will be subject to a repurchase option held by LiveVox TopCo or funds affiliated with Golden Gate Capital. The option to repurchase can be exercised for one year beginning on the latter of (a) the Management Incentive Unit holder’s termination date and (b) the 181st day following the initial acquisition of the Management Incentive Units by the Management Incentive Unit holder. The repurchased Management Incentive Units will be valued at fair market value as of the date that is 30 days prior to the date of the repurchase. However, if the fair market value is less than or equal to the participation threshold of the vested Management Incentive Units, the Management Incentive Units may be repurchased for no consideration.

The Company recognizes compensation expense on a straight-line basis over the requisite service period of five years. Stock-based compensation for Management Incentive Units is measured based on the grant date fair value of the award.

Acquisitions

The Company evaluates acquisitions of assets and other similar transactions to assess whether or not the transaction should be accounted for as a business combination or asset acquisition by first applying a screen test to determine if substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or group of similar identifiable assets. If the screen is met, the transaction is accounted for as an asset acquisition. If the screen is not met, further determination is required as to whether or not we have acquired inputs and processes that have the ability to create outputs which would meet the definition of a business. Significant judgment is required in the application of the screen test to determine whether an acquisition is a business combination or an acquisition of assets.

Recently Adopted Accounting Pronouncements

See Note 2 to our consolidated financial statements included elsewhere in the Super 8-K for recently adopted accounting pronouncements and recently issued accounting pronouncements not yet adopted as of the balance sheet date included in the Super 8-K.

Quantitative and Qualitative Disclosures about Market Risk

Concentration risk

Financial instruments that potentially subject LiveVox to significant concentrations of credit risk consist primarily of cash and accounts receivable. Risks associated with cash are mitigated using what LiveVox considers creditworthy institutions. LiveVox performs ongoing credit evaluations of its customers’ financial condition. Substantially all of LiveVox’s assets are in the United States.

As of March 31, 2021 and December 31, 2020, no single customer represented more than 10% of LiveVox’s accounts receivable. For the three months ended March 31, 2021 and 2020, no single customer represented more than 10% of LiveVox’s revenue.

19

LiveVox relies on third parties for telecommunication, bandwidth, and colocation services that are included in cost of revenue.

As of March 31, 2021, three vendors accounted for approximately 47% of the Company’s total accounts payable. No other single vendor exceeded 10% of the Company’s accounts payable at March 31, 2021. As of December 31, 2020, two vendors accounted for approximately 55% of the Company’s accounts payable. No other single vendor exceeded 10% of the Company’s accounts payable at December 31, 2020. LiveVox believes there could be a material impact on future operating results should a relationship with an existing supplier cease.

Interest rate sensitivity

The term loan portion of the Credit Facility is subject to interest rate risk, as the loan is termed as either a base rate loan or LIBOR rate loan (each as defined in the agreement governing the Credit Facility) and can be a combination of both. LIBOR interest elections are for one, two or three-month periods. Interest changes affect the fair value of the term loan but do not impact our financial position, cash flows or results of operations due to the fixed nature of the debt obligation.

Foreign exchange risk

LiveVox reports its results in U.S. dollars, which is its reporting currency. The functional currency of LiveVox’s foreign subsidiaries is their local currency. We also have international sales that are denominated in foreign currencies. For these international subsidiaries and customers, the monetary assets and liabilities are translated into U.S. dollars at the current exchange rate as of the balance sheet date, and all non-monetary assets and liabilities are translated into U.S. dollars at historical exchange rates. Revenues and expenses are translated using average rates in effect on a monthly basis. The resulting translation gain and loss adjustments are recorded directly as a separate component of stockholders’ equity (accumulated other comprehensive loss), unless there is a sale or complete liquidation of the underlying foreign investments, or the adjustment is inconsequential.

We experience fluctuations in transaction gains or losses from remeasurement of monetary assets and liabilities that are denominated in currencies other than the functional currency of the entities in which they are recorded. Exchange gains and losses resulting from foreign currency transactions were not significant in any period and are reported in other expense (income), net in the consolidated statements of operations and comprehensive loss.

20