Attached files

| file | filename |

|---|---|

| EX-10.5 - FORM OF SERIES A WARRANT - ORIGINCLEAR, INC. | f10k2020ex10-5_originclear.htm |

| EX-32 - CERTIFICATION - ORIGINCLEAR, INC. | f10k2020ex32_originclear.htm |

| EX-31 - CERTIFICATION - ORIGINCLEAR, INC. | f10k2020ex31_originclear.htm |

| EX-21.1 - SUBSIDIARIES OF THE REGISTRANT - ORIGINCLEAR, INC. | f10k2020ex21-1_originclear.htm |

| EX-14.1 - CODE OF ETHICS - ORIGINCLEAR, INC. | f10k2020ex14-1_originclear.htm |

| EX-10.7 - FORM OF SERIES C WARRANT - ORIGINCLEAR, INC. | f10k2020ex10-7_originclear.htm |

| EX-10.6 - FORM OF SERIES B WARRANT - ORIGINCLEAR, INC. | f10k2020ex10-6_originclear.htm |

| EX-10.4 - FORM OF SUBSCRIPTION AGREEMENT FOR SERIES R PREFERRED STOCK - ORIGINCLEAR, INC. | f10k2020ex10-4_originclear.htm |

| EX-3.37 - CERTIFICATE OF DESIGNATION OF SERIES V PREFERRED STOCK - ORIGINCLEAR, INC. | f10k2020ex3-37_originclear.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

Or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

Commission file number: 333-147980

ORIGINCLEAR, INC.

(Exact name of registrant as specified in charter)

| Nevada | 26-0287664 | |

| (State or other jurisdiction

of incorporation or organization) |

(I.R.S. Employer Identification No.) |

13575 58th Street North, Suite 200, Clearwater, FL 33760

(Address of principal executive offices) (Zip Code)

Registrant’s telephone Number: (323) 939-6645

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” “smaller reporting company,” and “emerging growth company in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ☐ | Accelerated Filer ☐ |

| Non-accelerated Filer ☒ | Smaller Reporting Company ☒ |

| Emerging Growth Company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

The aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $1,211,011 based upon the closing sales price of the registrant’s common stock on June 30, 2020 of $0.105 per share.

At May 20, 2021, 151,606,607 shares of the registrant’s common stock, par value $0.0001 were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: NONE

TABLE OF CONTENTS

i

NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control, which may include statements about our:

| ● | business strategy; | |

| ● | financial strategy; | |

| ● | intellectual property; | |

| ● | production; | |

| ● | future operating results; and | |

| ● | plans, objectives, expectations and intentions contained in this report that are not historical. |

All statements, other than statements of historical fact included in this report, regarding our strategy, intellectual property, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this report, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. All forward-looking statements speak only as of the date of this report. You should not place undue reliance on these forward-looking statements. Although we believe that our plans, intentions and expectations reflected in or suggested by the forward-looking statements we make in this report are reasonable, we can give no assurance that these plans, intentions or expectations will be achieved. These statements may be found under “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and “Business,” as well as in this report generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks outlined under “Risk Factors” and matters described in this report generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur.

ii

Organizational History

OriginClear, Inc. (“we”, “us”, “our”, the “Company” or “OriginClear”) was incorporated on June 1, 2007 under the laws of the State of Nevada. We have been engaged in business operations since June 2007. In 2015, we moved into the commercialization phase of our business plan having previously been primarily involved in research, development and licensing activities. Our principal offices are located at 13575 58th Street North, Suite 200, Clearwater, FL 33760. Our main telephone number is (323) 939-6645. Our website address is www.OriginClear.com. The information contained on, connected to or that can be accessed via our website is not part of this report.

Overview of Business

OriginClear is a water technology company which has developed in-depth capabilities over its 14-year lifespan. Those technology capabilities have now been organized under the umbrella of OriginClear Tech Group™ (www.originclear.tech).

These capabilities include:

| - | The Company’s original technology developments, known as Electro Water Separation™ and Advanced Oxidation(AOx™), which are not being pursued commercially at this time. | |

| - | The Intellectual Property of Daniel M. Early, consisting of five patents and related knowhow and trade secrets, which are intended to take the place of the applications for the company’s original technology developments. | |

| - | Progressive Water Treatment Inc. (“PWT”) a wholly-owned subsidiary based in Dallas Texas, which is responsible for the bulk of the company’s revenue, specializing in Engineered Solutions (custom treatment systems). | |

| - | Modular Water Systems (“MWS”), a division based at PWT, which implements the Daniel M. Early Intellectual Property. |

Water on Demand™: a new strategic direction.

OriginClear is planning a new business, which is outsourced water treatment, intending to offer private businesses the ability to pay for their water treatment and purification services on a pay-per-gallon basis. In the water industry, this is commonly known as Design-Build-Own-Operate or DBOO. On April 13, 2021, we announced formation of a wholly-owned subsidiary called Water On Demand #1, Inc. (WOD #1) to pursue capitalization of the equipment required.

At this time, the Company does not have the ability to carry out at scale the Operation & Maintenance (O&M) activities which are required to fulfill the service obligations of DBOO contracts. Our current plan is to pursue a first DBOO contract as a use case, and thereafter either develop, contract or acquire the O&M capability. The Company is currently in discussions with prospective clients for this test DBOO contract. However, no commitments have been made, and the talks may not succeed. The outsourcing program known as Water On Demand requires both funding for WOD #1, and such a first client, to launch commercially.

Outsourcing Risk

The Company believes water is a risk that smart managers will outsource, especially with worsening inflation. Outsourcing through what we call Water on Demand™ means that these companies do not have to worry about the problem, either financing it or managing it.

As an example, in Information Technology, few companies operate their own server in-house powering their website. Rather, such servers are typically managed by professionals through a service level agreement. In the water industry, when applied to outsourced water treatment, a service level agreement is known as Operation & Maintenance (O&M) Agreement. When the vendor retains ownership of the equipment, the concept is expanded to “Own and Operate”, an extension of the basic “Design and Build”, for a full offering known as DBOO, which is very similar to the solar energy programs known as Power Purchase Agreements (PPAs).

Under such a plan, a business can now outsource its wastewater treatment by simply signing on the dotted line; instantly avoiding most capital expense, and the trouble of managing something that is a distraction from their core business.

We believe this is financially and operationally attractive to industrial, agricultural and commercial water users, while OriginClear’s Water On Demand program can potentially drive speeded-up deals and many more revenue streams from providing water treatment as a service.

The scale of these systems is relatively small: a recent analysis showed that the 74 quotes that Modular Water Systems™ has at various stages of negotiation for 2021 average only $232,246 each. But capital is scarce for such private systems, and therefore a fully outsourced solution is attractive to these businesses.

Based on its analysis, the Company believes that half of its prospective clients for Modular Water Systems would approve its quotes if they could pay for their water as a monthly bill and not a capital expense.

1

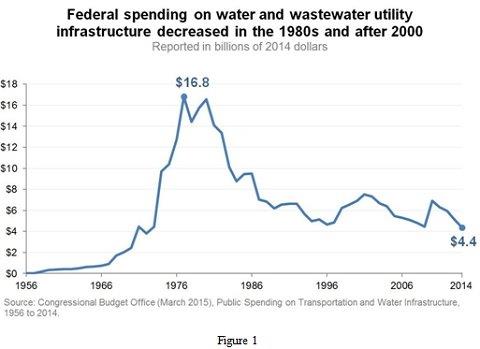

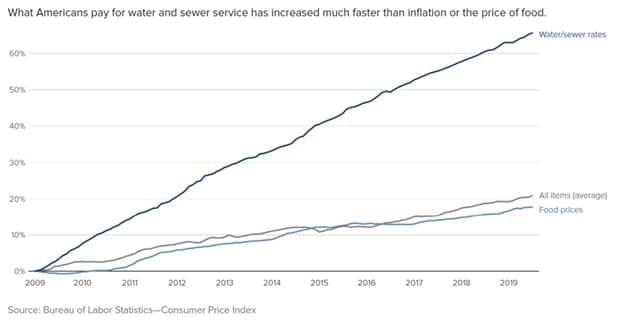

The Decentralization Megatrend

As municipalities continue to be underfunded (Figure 1) with rising water rates (Figure 2), businesses are increasingly choosing to treat and purify their own water, in a trend known as Decentralized Water, first described in the Lux Research presentation of June 28, 2016. (https://members.luxresearchinc.com/research/report/20060).

Figure 2

Small, modular systems as sold by our Modular Water Systems division meet the needs of this new segment. Indeed, an estimated two-thirds of the Modular Water Systems bidding backlog consists of such private (vs. municipal) customers.

A Company internal analysis has shown that as many as two-thirds of these prospective private customers (in other words, half of the overall backlog) could be candidates for outsourced water treatment which they would pay for by the gallon purified or treated, instead of paying for the capital expense up front. In other words, the Company believes such financing has the potential to increase the Company’s revenues substantially, with additional service fees potentially improving profits.

This is known in the water industry as Design/Build/Own/Operate (“DBOO”), or colloquially as water equipment as a service. The Company is working in this new direction under the branding Water on Demand™ (https://www.originclear.com/water-on-demand).

The bulk of such sales opportunities are in the small size systems, averaging $250,000 and larger. We believe that our ability to deliver modular systems gives us a competitive advantage over larger water companies when it comes to DBOO for smaller systems.

Also, the portable nature of these prefabricated, drop-in-place Modular Water Systems may provide a competitive benefit for a pure service model where the equipment remains the property of the Company, because their mobility enables repossession in the event the client fails to pay their monthly bill. We believe this is a key competitive advantage.

2

Implementation of Water On Demand

We have taken initial steps in this new direction. On February 3, 2021, we announced that we agreed to acquire our first real estate asset which we are currently arranging to be sold for capital to finance water projects. There is no prospective date of sale. Ivan Anz, OriginClear advisor and founder of strategic partner Philanthroinvestors® Inc. agreed to personally invest certain real estate assets through an asset purchase agreement, and these assets have been transferred, subject to certain rights of rescission.

On February 25, 2021, the company announced that it had agreed to acquire more real estate assets to finance water projects. Alfredo Guatto, partner in a US-based real estate development company continued discussions with the company to finalize a definitive agreement under which OriginClear intends to acquire the developer or its assets.

Recently, OriginClear incorporated Water On Demand #1 Inc. (“WOD#1”) in Nevada. to offer private businesses the ability to pay for their water treatment and purification services on a pay-per-gallon basis. However, the Company cautions that efforts to obtain capital to underwrite WOD #1 may not succeed.

The Company is now actively evaluating potential clients for a test of water treatment and purification services on a pay-per-gallon basis, but a first agreement has not been reached.

Advisory Support for Water On Demand

In September, 2020 OriginClear announced that Philanthroinvestors had entered a strategic agreement with OriginClear and had listed the company on its new Water Philanthroinvestors program. At the same time, OriginClear appointed Philanthroinvestors Founder, Ivan Anz and CEO, Arte Maren to OriginClear's Board of Advisors.

Mr. Anz and Mr. Maren are actively advising the Company in its development of Water On Demand.

H2O

On May 10, 2021, OriginClear announced that it had filed “System And Method For Water Treatment Incentive”, a patent application for using blockchain technology and non-fungible tokens (NFT) to simplify the distribution of payments on outsourced water treatment and purification services billed on a pay-per-gallon basis ahead of inflation, or Water On Demand.

On May 16, 2021, the Company filed a trademark for the mark $H2O (also referred to as H2O) as the blockchain system representing this activity.

The basic intended use of the blockchain system is to streamline payments and eliminate human error. In this respect we believe it is very similar to J.P. Morgan’s JPM Coin:

“In 2019, J.P. Morgan became the first global bank to design a network to facilitate instantaneous payments using blockchain technology - enabling 24/7, business-to-business money movement by unveiling JPM Coin.” (https://www.jpmorgan.com/solutions/cib/news/digital-coin-payments).

Like JPM Coin, we plan to streamline the delivery of payment contracts that, in our case, could last for decades.

Our patent application is the first step in our development process for this blockchain system, which we expect to last at least several months. We are not currently a blockchain or cryptocurrency developer and would need to develop or contract for this capability. There is no guarantee that this effort would succeed.

Depending on the final for that H2O takes, we may encounter regulatory concerns that we cannot guarantee we will overcome. In that event, we would fall back on ordinary financial payment systems.

Future Potential of H2O

We believe $H2O could be a way to package continuous contractual profit-share income for that investor or stakeholder’s share of the life of the water equipment, adjusted for inflation. And to allow the holder to transfer or “swap” it anytime and ultimately, OriginClear could accept $H2O for the funding of new Water On Demand projects, with the potential for subsidized Impact Investment.

All these scenarios are highly speculative, and none may come about. In addition, there may be regulatory restrictions on the issuance and transfer of $H2O.

Prior to the commercialization of $H2O, we intend to fully address all regulatory requirements, and as covered above, this may not be possible; in which case we would use ordinary financial systems for payments to investments and stakeholders.

Water On Demand outsourced water treatment does not rely on any blockchain system for its operation, and can accomplish its operational goals using ordinary financial and currency channels.

3

OriginClear Tech Group

As stated above, all of our technology and operations activities have been centralized under OriginClear Tech Group (“OTG”), enabling a total focus at the corporate level on the Water On Demand strategy.

The mission of OTG is to provide expertise and technology to help make clean water available for all. Specifically, OTG houses the following initiatives:

| 1. | We are building a network of customer-facing water brands to expand our global market presence and our technical expertise. These include the wholly-owned subsidiary, Progressive Water Treatment, and the Modular Water Systems brand. |

| 2. | We manage relationships with partners worldwide who are licensees and business partners. |

| 3. |

We develop new technology approaches and business models in the lab, such as Investor Water™ and WaterChain™, both of which are designed to help achieve funding for water treatment and management systems. Both projects are in a research and development phase. OTG also is actively working on the ability to deliver Operation & Maintenance (O&M) capability at scale, to support Water On Demand outsourced treatment and purification programs, and is evaluating a pilot program to achieve this. OTG intends to support the development of the $H2O blockchain system, which may replace WaterChain altogether. And in 2020, the Company also completed a pilot program with a rental program of a product known as Pool Preserver™, and developed a career-building program for entrepreneurs termed Waterpreneurs™. Water As A Career remains a pilot program and the Company does not plan to expand it at this time. |

Water is our most valuable resource, and the mission of OTG is to improve the quality of water and help return it to its original and clear condition.

Potential Acquisitions

Outsourcing is a fast-growing reality in water treatment. Tougher regulations, water scarcities and general outsourcing trends are driving industrial and agricultural water treatment users to delegate their water problem to service providers. As Global Water Intelligence pointed out in their report on October 30, 2015, “Water is often perceived as a secondary importance, with end-users increasingly wanting to focus solely on their own core business. This is driving a move away from internal water personnel towards external service experts to take control of water aspects.” External service experts are typically small–privately owned and locally operated. Consolidating these companies, and creating new players where appropriate, could lead to enormous economies of scale through sharing of best practices, technologies, and customers.

OTG seeks to incubate or acquire businesses that help industrial water users treat their water themselves, and often reuse it. We believe that assembling a group of such water treatment and water management businesses is an opportunity for significant growth and increased Company value for the stockholders.

We are particularly interested in companies which successfully execute on Design-Build-Own-Operate or DBOO.

The Company cautions that suitable acquisition candidates may not be identified and even if identified, the Company may not have adequate capital to complete the acquisition and/or definitive agreement may not be reached. Internally-incubated businesses, similarly, may not become commercial successes.

OTG Milestones

Daniel M. Early/Modular Water Systems™

On June 22, 2018, OriginClear signed an exclusive worldwide licensing agreement with Daniel “Dan” Early for his proprietary technology for prefabricated water transport and treatment systems. On July 19, 2018, the Company began incubating its Modular Water Treatment Division (MWS) around Mr. Early’s technology and perspective customers. The Company has funded the development of this division with internal cash flow. In Q1 of 2020, the Company fully integrated MWS with wholly-owned Progressive Water Treatment Inc. Mr. Early is titled Chief Engineer of OriginClear.

WaterChain, Inc.

WaterChain, Inc. was incorporated in December, 2017 and is today a research and development project of the Company.

4

Progressive Water Treatment Inc.

On October 1, 2015, the Company completed its acquisition of Dallas-based Progressive Water Treatment Inc. (“PWT”), a designer, builder and service provider for a wide range of industrial water treatment applications.

With the PWT and future potential acquisitions, the creation of the Modular Water Systems division as an integral part of PWT, and integrating its proprietary technology, OTG aims to offer a complementary, end-to-end offering to serve growing corporate demand for outsourced water treatment.

PWT’s Business

Since 1995, PWT has been designing and manufacturing a complete line of water treatment systems for municipal, industrial and pure water applications. PWT designs and manufactures a complete line of water treatment systems for municipal, industrial and pure water applications. Its uniqueness is its ability to gain an in-depth understanding of customer’s needs and then to design and build an integrated water treatment system using multiple technologies to provide a complete, not partial solution.

To help address customer needs, PWT utilizes a wide range of technologies, including chemical injection, media filters, membrane, ion exchange and SCADA (supervisory control and data acquisition) technology in turnkey systems. The Company also offers a broad range of services including maintenance contracts, retrofits and replacement assistance. In addition, PWT rents equipment in contracts of varying duration. Customers are primarily served in the United States and Canada, with the company’s reach extending worldwide from Siberia to Argentina to the Middle East.

PWT Milestones

In the first quarter of 2019, the Company increased the number of the manufacturer’s representatives for its operating units, PWT and Modular Water Systems (“MWS”).

On Nov 7, 2019, OriginClear published a case study showing how its Modular Water System may help automotive dealership expand into rural land. The case study shows how point-of-use treatment solves lack of access to the public sewer system.

On March 5, 2020, OriginClear announced disruptive pump and lift station pricing, stating that its prefabricated modules with a lifespan of up to 100 years now compete with precast concrete.

On April 15, 2021, OriginClear announced that its Progressive Water Treatment division is now shipping BroncBoost™, its workhorse Booster Pump Station equipment line. Engineered and built in Texas, BroncBoost allows customers to control water flow rates and pressure for mission critical water distribution systems.

Modular Water Systems

On July 19, 2018, the Company launched its Modular Water Treatment Division, offering a unique product line of prefabricated water transport and treatment systems. Daniel “Dan” Early P.E. (Professional Engineer) heads the division and along with the intellectual property which the Company licensed exclusively worldwide for three years, brought a following of prospective customers. On July 25, 2018, MWS received its first order, for a brewery wastewater treatment plant.

With PWT and other companies as fabricators and assemblers, MWS designs, manufactures and delivers prefabricated water transport (pump stations) and wastewater treatment plant (“WWTP”) products to customers and end-users that have to clean their own wastewater. It uses Structurally Reinforced Thermoplastic (“SRTP”) materials to focus on patented developing water and wastewater collection, conveyance, and treatment systems that have high performance and sustainability. Typical customers may include schools, small communities, institutional facilities, real estate developments, factories, and industrial parks. Dan Early has pioneered the use of heavy reinforced plastic materials to create modular “water-systems-in-a-box”. Not only is reinforced thermoplastic faster and cheaper to build, but it can have three times the lifespan, or more, compared with concrete-and-steel construction. Mr. Early’s inventions have led to the patented Wastewater System & Method and four other patents, which OriginClear has licensed exclusively for the world.

Dan Early has been designing and building prepackaged pump stations and municipal wastewater treatment systems for over five years, with a career background of more than two decades of water engineering experience.

MWS designs, manufactures and implements advanced prepackaged wastewater treatment, pump stations and custom systems with primary focus on decentralized opportunities away from the very competitive large municipal wastewater treatment plants. These decentralized opportunities include: rural communities, housing developments, industrial sites, schools and many more.

Today, MWS is fully integrated with PWT in Texas.

5

Patents

On May 10, 2021, OriginClear announced that it had filed “System And Method For Water Treatment Incentive”, a patent application for using blockchain technology and non-fungible tokens (NFT) to simplify the distribution of payments on outsourced water treatment and purification services billed on a pay-per-gallon basis ahead of inflation.

On June 25, 2018, Dan Early granted the Company a worldwide, exclusive non-transferable license to intellectual property consisting of five issued US patents, and design software, CAD, marketing, design and specification documents (“Early IP”).

On May 20, 2020, we agreed on a renewal of the license for an additional ten years, with three-year extensions. We also gained the right to sublicense, and, with approval, to create ISO-compliant manufacturing joint ventures. All royalties surviving the 2018 license were settled.

We may contract with distribution channels (equipment distributors, oil service companies, water treatment companies, system integrators and engineering companies) of our choice to act on our behalf for the purpose of selling and integrating the Early IP.

The Early IP consists of combined protection on the materials and configurations of complete packaged water treatment systems, built into containers. The parents consist of the following:

| # | Description | Patent No. | Date Patent Issued | Expiration Date | ||||

| 1 | Wastewater System & Method | US 8,372,274 B2 Applications: WIPO, Mexico |

02/12/13 | 07/16/31 | ||||

| 2 | Steel Reinforced HDPE Rainwater Harvesting | US 8,561,633 B2 | 10/22/13 | 05/16/32 | ||||

| 3 | Wastewater Treatment System CIP | US 8,871,089 B2 | 10/28/14 | 05/07/32 | ||||

| 4 | Scum Removal System for Liquids | US 9,205,353 B2 | 12/08/15 | 02/19/34 | ||||

| 5 | Portable, Steel Reinforced HDPE Pump Station CIP | US 9,217,244 B2 | 12/22/15 | 10/20/31 |

With the rising need for local, point-of-use or point-of-discharge water treatment solutions, the Modular Water Systems licensed IP family is the core to a portable, integrated, transportable, plug-and-play system that, unlike other packaged solutions, can be manufactured in series, have a longer life and are more respectful of the environment.

The common feature of this IP family is the use of a construction material (SRTP or Structural Reinforced ThermoPlastic), for the containers that is:

| ● | more durable: an estimated 75 to 100-year life cycle as opposed to a few decades for metal, or 40 to 50 years maximum for concrete; | |

| ● | easier to manufacture: vessels manufacturing process can be automated; and | |

| ● | recyclable and can be made out of biomaterials |

In addition, patents US 8,372,274 and US 8,871,089 (1 and 3) relate to the use of vessels or containers made out of this material combined with a configuration of functional modules, or process, for general water treatment.

Other subsequent patents, while keeping the original claims and therefore making them stronger, focus on more targeted applications. These patents outline a given combination of modules engineered inside the vessel to address a specific water treatment challenge.

Expansion of the PWT and MWS Business-Lines

Beginning with its first installation, PWT built MWS components. PWT and MWS are now fully integrated as a single profit and manufacturing center.

In April 2019, we completed the expansion of our manufacturer’s representative network to serve both PWT and MWS for customer lead generation.

6

PRODUCTS, TECHNOLOGY AND SERVICES

OTG deploys advanced technologies at the point of use, with modular, prefabricated systems that create durable assets and water independence for industry, commerce and agriculture.

Failing infrastructure and the rising cost of water are driving businesses to treat their own water. OTG provides on-premise systems enabling very high purification and recycling levels that centralized systems cannot achieve.

Systems installed at the point of use become productive assets for businesses that also increase property values. And OTG helps corporations improve their environmental, social and governance (ESG) standings with water management services.

Operations & Markets

OTG focuses on meeting the needs of businesses looking for compact, advanced technologies that can be shipped to and installed at the point of use. The Company manufactures and distributes its professional-grade water treatment and conveyance products to commercial and industrial properties, fielding both direct and indirect sales channels to reach end-market clients such as hotels and resorts, real estate housing developments, office buildings, military installations, schools, farms, food and beverage manufacturers, industrial warehouse, oil and gas producers, and medical and pharmaceutical facilities.

From its Texas-based factory, OTG designs and prefabricates an entire line of plug-n-play containerized units called Modular Water Systems that enable water purification, recycling and wastewater management.

Industrial Pretreatment Waste Water Treatment Plant (WWTP) designed by Daniel M. Early for an earlier company, using reinforced thermoplastic modules.

These onsite modular products provide clients with water independence through ownership and operational control over water quality, enabling them to increase productivity while reducing environmental, health and safety risks from pollution, contamination and corrosion. Modular water products are trusted to balance performance with cost-effectiveness, enabling business users to go well beyond municipal standards for water quality, therefore achieving high levels of satisfaction for their own customers, and improved sustainability for their properties.

7

OTG’s water treatment equipment can boost real estate asset value as a fundamental capital improvement, combined with long-lasting water savings for the corporate bottom line.

Product Portfolio

OTG groups its products into three main categories:

| ● | Water Treatment: achieving high grade purification; | |

| ● | Water Conveyance: water transportation and pumping; and | |

| ● | Advanced Technologies: commercialization of innovative technologies. | |

OTG’s complete line of compact, on-site, point-of-use products include: advanced purification systems that are skid, rack-mounted and containerized for reverse osmosis, ultrafiltration, media filtration, disinfection, water softening, ion exchange and electrodeionization (EDI), combined as needed in small to medium commercial and industrial applications, and custom-build projects. Water conveyance products include pump and lifting stations, modular storage tanks, and control monitoring panels.

OTG’s line of modular water products and systems create “instant infrastructure” – fully engineered, prefabricated and prepackaged systems that use durable, sophisticated materials. The units are available in standard capacities for onsite closed-loop systems at commercial business locations.

The company’s rugged wastewater treatment plants, highly reliable pump stations, and premium water purification units typically offer 25 percent lower initial costs over conventional systems, with greater quality and full connectivity. These pump stations and wastewater treatment products utilize high density thermo-plastics (HDPE) and proprietary, innovative prefabrication methods and materials that deliver the longest life and strongest products.

Original Technologies

Electro Water Separation™ (EWS) and Advanced Oxidation (AOx™) were the Company’s original, filterless technologies.

EWS is OriginClear’s breakthrough water cleanup technology which utilizes a catalytic process to concentrate and eliminate suspended solids in the worst commercial and industrial wastewater.

AOx is OriginClear’s proprietary advanced oxidation technology which generates a dense cloud of ozone, hydrogen peroxide and hydroxyl radicals, dramatically reducing or eliminating dissolved organic microtoxins, including bacteria and viruses, hormones, drugs, pesticides such as Roundup, and synthetics. AOx has also been shown to effectively reduce harmful chemicals such as ammonia and hydrogen sulfide – the “rotten egg” smell in crude oil that reduces its value.

At this time, the Company is strictly marketing the EWS/AOx technology in the context of turnkey integrators such as Spain’s Depuporc, and India’s Permionics. In addition, US-based Algeternal is our partner for the original algae-harvesting applications of this technology, and reportedly continues to use Company equipment for this purpose. The Company does not maintain an internal technical staff to manage this technology or its implementation and has no plans to do so.

Market Opportunity

Only 20 percent of all sewage, and 30 percent of all industrial waste, are ever treated. Water leakage results in the loss of 35 percent of all clean water across the planet; cutting that number in half would provide clean water for 100 million people. This is a situation of great danger, but also great potential.

We believe businesses can no longer rely on giant, centralized water utilities to meet the challenge. That is why more and more business users are doing their own water treatment and recycling. Whether by choice or necessity, those businesses that invest in onsite water systems gain a tangible asset on their business and real estate, and can enjoy better water quality at a lower cost.

We believe self-reliant businesses are quietly building Decentralized Water Wealth™ for themselves while also helping their communities. They know that environmental, social and governance (ESG) investing guidelines, which drive about a quarter of all professionally managed assets around the world, specifically include the key factor of how well corporations manage water.

8

10,000 Gallon per Day Industrial Membrane Bioreactor Wastewater Treatment Plant designed by Daniel M. Early, PE for a previous company, using long-lived Structural Reinforced ThermoPlastic (SRTP)

OTG enables ESG water management for corporations that are increasingly responsible for what was once delegated to central utilities. For example, when a corporation manages its own water, and uses OriginClear’s proprietary hybrid treatment methods, it can significantly reduce both water use and nutrient footprints (carbon, nitrogen, and phosphorus) in one compact package.

These hybrid processes feature advanced blackwater treatment with advanced clean water processing. They can convert toxic nutrients to less harmful compounds, and even capture them for beneficial reuse purposes, as shown in OriginClear’s recent case study.

Integration of Operating Divisions

Since OriginClear acquired it in 2015, Progressive Water Treatment has evolved into the Fabrication and Manufacturing Division for the whole company. The team at Modular Water Systems, headed by OriginClear Chief Engineer Daniel M. Early, is responsible for overall design and high-level engineering, and is fully integrated with PWT. It relies on the Fabrication and Manufacturing Division to add incremental revenue for its modular product line, without requiring large increases in personnel.

OTG also seeks to acquire profitable water companies that can complement the synergy of its existing units and accelerate both revenues and profitability. However, there cannot be any assurance that the Company will be able to acquire such companies.

Supplier Relationship

PWT has been purchasing equipment from its many suppliers for over twenty years, with potential long-term benefits from the relationships.

MWS is positioned to take advantage of PWT’s supplier relationships, but certain components are unique to MWS’s product line. In particular, SRTP pipe is unique, for which MW has four manufacturers. MWS’s preferred SRTP supplier happens to be 40 miles south of PWT’s facility.

9

CUSTOMERS AND MARKETS

Current water and wastewater treatment infrastructure faces a crisis. The prohibitive cost of repairing buried and ageing infrastructure and the need to decrease energy use and waste in the water industry offers an opportunity for a complete design rethink. New technologies, often utilizing membranes, can decentralize water and wastewater infrastructure while improving water reuse by treating to a high standard at a small scale close to the source of generation. Additionally, new automated analytics offer solutions for these more complex decentralized solutions. (Lux Research: The Future of Decentralized Water, June 28, 2016). PWT has designed and fabricated water treatment systems for over twenty years. Major markets include:

| ● | Potable Water for Small Communities | |

| ● | Recirculated and Makeup Boiler and Cooling Tower Water | |

| ● | Produced Water &FracFlowback Water | |

| ● | Food and Beverage Feed and Effluent Waters | |

| ● | Mining Effluent | |

| ● | Ground Water Recovery | |

| ● | Agriculture Effluent | |

| ● | Environmental Water Treatment for Reuse | |

MWS manages municipal water conveyance and municipal waste water treatment, describing the water and wastewater treatment market as a pyramid with the major cities at the top, medium size cities stacked below them depending upon size and then the smaller towns, counties, cities, townships, state agencies, federal agencies, private individuals, commercial entities, industrial facilities, agriculture facilities at the base of the pyramid.

We believe there are more opportunities at the base of the pyramid. The base of the pyramid is the decentralized market opportunity now being pursued. Focusing on the base of the pyramid also avoids the very competitive, low-profit and slow-growing market in the big city municipalities.

As stated in the Global Decentralized Packaged/Containerized Water and Wastewater Treatment Systems Market, Forecast to 2023, “The decentralized packaged/containerized water and wastewater treatment systems market, covering end users segments such as municipal, industrial, and commercial. The study forecasts the global market revenue to increase from $3.99 billion in 2016 to $6.08 billion in 2023, growing at a compound annual growth rate (CAGR) of 6.2%”.

(https://www.reportbuyer.com/product/4948731/global-decentralized-packaged-containerized-water-and-wastewater-treatment-systems-market-forecast-to-2023.html).

This is the market for MWS-engineered products and infrastructure solutions. As civil infrastructure ages and fails and as the costs for new and replacement infrastructure increase year over year, we believe engineers and end-users will search for new ways and methods of deploying water and wastewater systems that are less expensive to deliver and much less expensive to own and operate with the mission intent of substantially increasing the replacement intervals currently experienced by conventional materials of construction and conventional product delivery models.

SALES AND MARKETING

PWT’s sales strategy differs from MWS’s efforts. PWT sales are very dependent upon relationships with past end-use customers and certain manufacturers’ representatives who have relationships with their regional end use customers. On the other hand, MWS’s sales strategy is based on developing relationships with consulting engineers and general contractors as opposed to end-use customers.

As MWS sales strategies develop, PWT believes it will gain recognition with various consulting engineers and general contractors. PWT and MWS are currently developing a stronger national representatives network to take advantage of the relationship the sales representatives have gained with engineers, contractors and end use customers.

10

Now operating as one integrated unit, PWT and MWS have substantial experience in the water & wastewater market and as well as: conventional technologies and their limitations, new technologies, the size and demand of the market and how products are specified and implemented. They also have a strong customer focus throughout the organization to discover and diagnose the customer needs, design and deliver comprehensive solutions.

We believe the keys to capitalizing on the market are visibility, relationships, market understanding, and direct access to the opportunities. Strong marketing programs are also essential, and include: websites with solutions & credibility, sales support tools like literature& webinars and trade show presence.

Water industry projects move slowly. Most product lines for each of PWT and MWS are considered “pipeline” products, and have a gestational period of 6 months to 3 years. We believe the best strategy to increase the pipeline of opportunities is to have more sales reps with relationships with engineers, contractors and end users.

Competition

PWT shares the market with a large number of suppliers which also provide system integration using multiple technologies. These include California’s PureAqua, Florida’s Harn RO, and Illinois’ Membrane Specialists. We believe PWT’s market share differs from those competitors in areas such as regional focus, customer loyalty, market focus, limited sales representation and other. For instance, 80%+ of PureAqua’s business in the Middle East, Harn RO focuses on drinking water systems for medium to large cities in the SE, Membrane Specialist focuses on tubular membranes and many more examples.

The Company is not aware of any direct competitors to MWS that are building complete water, wastewater treatment systems, and pump stations utilizing SRTP type materials. There are several manufacturers which build metal prepackaged systems, such as Georgia’s AdEdge; however, such companies do not offer the range of hybrid treatment processes available through MWS. The major indirect competition continues to be custom designed and on-site constructed concrete & steel systems. Some fiberglass is used but is very difficult to detail, is brittle and again, has a limited life compared to SRTP systems.

While manufacturers of SRTP pipe could be competitors, none of MWS’s suppliers, other than Contech, for a short period of time, has sold, or intends to sell, comparable systems to MWS’s. Their focus is simply to sell miles of pipe.

Growth Opportunities

National Sales Rep Network

In the first quarter of 2019, the Company worked to help PWT and MWS identify seasoned sales representatives across the country through recommendations from those with deep industry knowledge. Those particular representatives were contacted and meetings set to discuss the mutual opportunity. On February 5, 2019, the Company reported on initial positive results.

By early June of 2019, seven additional organizations had signed agreements, building on the eight that PWT and MWS had in place at the beginning of 2019. These additional organizations cover twenty-two additional states with about thirty new representatives. Training has been completed and new potential projects have been presented to PWT and MWS.

Additional sales managers, engineers and project managers will be needed for both PWT and MWS with additional production facilities necessary for PWT. The process of hiring additional personnel and obtaining additional facilities is underway.

Domestic versus International

The market opportunity for each of PWT and MWS is not limited to the United States. The US only represents 5% of the world’s population. In addition, a great deal of that population resides in undeveloped regions or regions with poor treatment systems. We believe implementing MWS’s and PWT’s decentralized technology throughout the world with joint ventures has the potential to have a significant effect on our revenue growth.

11

Standardization

MWS is developing standardized designs and commoditized product engineering (eliminating the custom consulting engineering work reduces overall project costs), the goal being to design a single product once and use said design as a blueprint for future products. Our goal is to continue driving the standardization and completion of each product’s engineer technical package, using computer design algorithms and standard design approaches, so that engineering costs may potentially decrease to less than 1% for each unit sold, with a long-term goal of less than 0.1%.

Sharing Technology & Projects

PWT’s systems remove suspended solids, oils, metals, and dissolved chemicals & salts. MWS’s focus is on the removal of organic contaminants. It is not uncommon for a waste stream of water to be contaminated with both inorganics and organics, for example, many current animal farms with large amounts of waste effluent that currently is pumped to lagoons that are no longer meeting environmental standards. In the alternative, the water can be treated in-line with MWS products to remove the organics, then PWT’s systems used to remove dissolved inorganics to create water suitable for irrigation or drinking water for the animals. In addition, OriginClear’s proprietary technologies have been shown to successfully treat problems such as animal farm effluents.

By combining these technologies, the offering to customers becomes stronger and more effective. And both companies benefit from a new opportunity.

More Specific Opportunities for PWT

We are interested in exploring the following opportunities, but we have no timeline for their implementation:

| ● | Build and promote a fleet of rental treatment systems mounted on trailers or containers. It is very common for a rental to be purchased outright. As a result, PWT’s rental fleet must be continuously replenished. | |

| ● | Develop a standard digital product line through 3-D CAD programs and market it as virtual inventory, with components on hand and engineering already done. | |

| ● | Expand production capabilities with new equipment that would lower the labor cost of production. For instance, acquire tooling that would minimize the hand tool labor. | |

| ● | Develop more services business such as membrane cleaning or resin regeneration. |

More Specific Opportunities for MWS

MWS has developed a grey/black water treatment system for forward operating basis called Expeditionary Wastewater Recycling Systems (EWRS): Patent pending, US Army Human Health Command approved, fully automated, certified wastewater recycling solution which can be sold to all DOD divisions, FEMA and NGOs.

Another new product still being incubated is building manholes utilizing SRTP versus the current precast concrete approach.

ORGANIZATION

MWS is now fully integrated with PWT. MWS personnel are primarily located in New Castle, VA remote locations.

OTG supports the combined Texas organization with various administrative, accounting and marketing functions, from its headquarters in Florida.

12

FACILITIES AND EQUIPMENT

Manufacturing

PWT currently leases its facility. The facility is located at 2535 E. University Drive, McKinney, Texas 75069. There are five buildings totaling 12,400 square feet on the 1.7 acres of land. There is additional expansion space for several more assembly buildings when and if needed.

PWT’s in-house engineers and designers utilize modern 3-D CAD programs to design all of the systems sold by PWT. They also design, program and build all of the control systems and the Internet-connected Process Logic Control (PLC) video screen interfaces.

PWT in-house craftsmen complete the metal and plastic machining, welding and assembly of PWT’s and MWS’s systems.

MWS engineering resources are provided both internally and externally. Daniel Early leads the engineering program and relies on support from engineering personnel and PWT to assist with Manufacturing Engineering. MWS subcontracts engineering support to PWT, which employs its own established and experienced engineering team. MWS also subcontracts 2D and 3D engineering design work to outside vendors to assist in the development of standardized drawings and proposals.

MWS’s specialized manufacturing is outsourced at present. PWT provides substantial critical manufacturing support to MWS; this support takes the form of various sub assembly fabrication (membrane modules, equipment skids, MWS equipment buildings, etc.). PWT is the sole source provider for MWS’s integrated control panels. In addition to PWT, heavy plastic and or custom plastic manufacturing is provided by a company in Roanoke, Virginia and another in Ontario, Canada. Additional sub-contract manufacturing is available through fabricators in Hopkins, MO, Corsicana, TX, and Vernon Hills, IL.

The Company plans to transition the plastic fabrication of MWS’s pump stations and wastewater treatment systems to PWT from subcontractors. There is no timeline for this, as it will require an additional 2,400 to 3,000 square foot building for assembly, engineers and project managers.

The components such as pumps, membranes and instruments will be acquired either through PWT’s or MWS’s normal vendors. The large diameter SRTP pipe will be acquired from the fabricator located about 40 miles south of Dallas.

The building blocks of all systems are metal reinforced or structural profile wall reinforced thermoplastics pipe (SRTP) available from one of over a half dozen pipe suppliers. Being pipes they are manufactured to be sold into high volume applications and are very economical for MWS’s high value applications. MWS purchases these plastic cylinders up to 11’ in diameter and are utilized as the vessel or housing part of the water treatment systems.

More efficient fabrication and assembly equipment are available at relatively little cost to expedite the fabrication time and improve the quality. Some of that equipment includes: CNC waterjet, large diameter core drills, fusion welders and roto molders.

13

Technology Group Milestones

The following milestones were achieved in addition to the PWT and MWs milestones stated earlier.

On December 5, 2019, OriginClear announced that its Spanish partner Depuporc unveiled an integrated manure treatment system using OriginClear technology. The demonstration system processes 30 metric tons per day, with client-validated reduction of contaminants.

On January 22, 2020, OriginClear named India’s Permionics as Strategic Partner for Asia-Pacific Region in an expansion of the existing licensing partnership intended to better address regional opportunities. Permionics is also a key channel partner for PWT.

Acquisitions

OTG’s strategy is to grow incrementally by focusing on the water treatment services market, acquiring the hands-on service suppliers in this market. It intends to develop a network of these wholly-owned water treatment companies to meet the needs of end users from all industries with a full range of treatment technologies. Due to increased regulation, water treatment recycling challenges and a need to focus on their own core business, many water users today are outsourcing their water treatment needs to outside experts. In addition, we have identified a major trend in decentralization of water treatment, which we believe will cause small water service companies to grow. There will be significant synergies within OTG as technology, manufacturing expertise, market knowledge, projects and opportunities are shared. The target acquisitions must be accretive in nature with solid sales growth and profitability. The acquired companies must have a solid management team to accelerate their previous growth with excellent customer service. Initially, the acquisition focus is in the U.S. but will be expanded internationally in a few years.

OTG believes that the policy of building business units from internal cash flow can be productive. It did so with the Daniel Early/MWS project and is now beginning the process again with Water On Demand and the $H2O blockchain system.

Technology Licensing

We may grant non-exclusive licenses to OEMs (Original Equipment Manufacturers), and participate in joint ventures, contributing our technology and our commitment to each joint venture’s business focus.

We have limited licensing and joint venture activity and do not intend to expand this activity.

Water On Demand

Our planned water outsourcing program is known as DBOO in the industry. Typically, DBOO has been done for very large municipal and national projects.

If we achieve the capital required, we plan to deliver DBOO for smaller systems in the $250,000-$2,000,000 hardware range, or treating between 5,000 and 100,000 gallons per day. With a growing number of local businesses doing their own treatment, we see this as a promising and underserved market.

Competitors

A number of providers deliver very large DBOO systems, such as Suez Water and the former Aquaventure Holdings, now part of Culligan. We do not compete with these providers.

A growing number of DBOO providers serve the smaller systems segment, such as Cambrian Innovations and Surplus Water. It is too early to tell what our competitive strengths or weaknesses could be, as we are still in the test phase of our own program.

$H2O blockchain system

The use of the blockchain to streamline payments is new to industrial water, but it is a very common application of financial services, such as with J. P. Morgan’s JPMCoin.

Competitors

We know of no blockchain system in use in the water industry. It is too early to tell what competitors may appear during the prospective development period of $H2O.

14

Intellectual Property

Status of Original Inventions:

Early developments of Intellectual Property focused on algae harvesting, beginning in 2008. Beginning in 2015, the company applied this knowledge to water treatment and began development of EWS.

In 2018, OriginClear reorganized its intellectual property portfolio to focus exclusively on its electrochemical water treatment solution, Electro Water Separation™ (EWS) with Advanced Oxidation (AOx™).

On May 25, 2019, in its Annual Report for the fiscal year ended December 31, 2018, the Company stated, “we have chosen to protect certain intellectual property with trade secrets rather than patents”.

Accordingly, OriginClear no longer actively maintains the patent applications and patents to its EWS and AOx technologies, willingly deeding them to the water industry as an open resource. The Company intends to reserve to itself and its partners the protected communication of further discoveries and trade secrets relative to the EWS and AOx technology domains.

At this time, the Company is not actively pursuing the development of the EWS or AOx technologies.

Patents:

| ● | On May 10, 2021, OriginClear announced that it filed “System And Method For Water Treatment Incentive”, a patent application for using blockchain technology and non-fungible tokens (NFT) to simplify the distribution of payments on outsourced water treatment and purification services billed on a pay-per-gallon basis ahead of inflation. The application status is provisional. |

Trademarks:

| ● | On April 2, 2015, we filed a trademark application with the USPTO to protect the intellectual property rights for our wordmark “OriginClear”. On August 16, 2016 the wordmark was registered with Registration Number 5023444. The registration is current. | |

| ● | On April 8, 2015, we filed a trademark application with the USPTO to protect the intellectual property rights for our current company logo “OriginClear” with the stylized “O”. On August 16, 2016 the mark was registered with Registration Number 5027992. The registration is current. | |

| ● | On January 17, 2021, we filed a trademark application with the USPTO to protect the intellectual property rights for “Waterpreneur”. The current filing basis is “Use in commerce” (under Trademark Act Section 1(a)). |

| ● | On May 16, 2021, we filed a trademark application with the USPTO for the mark “$H2O”. The current filing basis is “Intent-to-use basis” (under Trademark Act Section 1(b)). |

15

Licensed Patents:

On June 25, 2018, Daniel Early granted us a worldwide, exclusive non-transferable license to intellectual property consisting of five issued US patents, and design software, CAD, marketing, design and specification documents. See “Products, Technology and Services—Patents”

Marketing Agreements:

In an Amendment dated December 2, 2019, the Company renewed the licensing agreement of Zaragoza, Spain-based Depuporc S.A. for an additional ten years, and agreed to remarket its DEPUPORC® brand animal manure treatment system worldwide, both directly and through channel partners, excluding geographical Europe and Europe-based customers. DEPUPORC, which integrates OriginClear technology under license, is protected by Spanish patent 2011311192 granted on December 12, 2013 with priority given on July 13, 2014 to MONTAJES LONGARES SL, the parent company of Depuporc.

Depuporc S.A. states that DEPUPORC is recognized by the Institute of Environmental Management of the Spanish Province of Aragon as a method of treatment and purification of liquid manure generated in pig farms in order to reduce nitrogen emissions linked to animal husbandry. DEPUPORC, likewise, has been recognized and selected by Spain’s Ministry of Agriculture, Food and Environment for CARBON FES-CO2 as a PILOT CLIMATE PROJECT in its 2012 program.

Abandonments and Transfers

Abandonment generally occurs when the Company believes it has better intellectual property in other applications, or when we have chosen to protect the IP with trade secrets instead of patents. As we disclosed in 2019, we have abandoned all patents and patent applications for our original technology, known as Electro Water Separation and Advanced Oxidation (AOx), and our policy for these inventions is to preserve our evolving knowhow through trade secrets.

Research and Development

During the years ended December 31, 2020 and 2019, we invested $110,338 and $107,351, respectively, on research and development of our technologies. Research and development costs include activities related to technology development and innovations, fabrication and scale-up of products based on this technology, development of firmware and process automation, development of new applications in industries such as aquaculture, technical support of customers, agents, joint venture partners and licensees, on-site consulting and training activities, and miscellaneous research.

Employees

As of May 20, 2021, we had 26 employees, all of whom are full-time.

OUR PROPERTY

Our principal corporate offices are located at 13575 58th Street North, Suite 200, Clearwater, FL 33760. Our Dallas based subsidiary, PWT, rents an approximately12,000 square foot facility located at 2535 E. University Drive, McKinney, TX 75069, with a current monthly rent of $7,000.

Currently, 9 employees also work from remote locations in Los Angeles, California; Pittsburgh, Pennsylvania; New Castle, Virginia; and Sarasota, Florida.

We believe these facilities are suitable and adequate to meet our current business requirements.

16

Risks Relating to Our Business

We have not been profitable.

We were formed in June 2007 and are currently developing a new technology that has not yet gained market acceptance. Since we have not been profitable, there are substantial risks, uncertainties, expenses and difficulties that we are subject to. To address these risks and uncertainties, we must do among the following:

| ● | Successfully execute our business strategy; | |

| ● | Respond to competitive developments; and | |

| ● | Attract, integrate, retain and motivate qualified personnel. |

There can be no assurance we will operate profitably or that we will have adequate working capital to meet our obligations as they become due. Investors must consider the risks and difficulties frequently encountered by early stage companies, particularly in rapidly evolving markets. We cannot be certain that our business strategy will be successful or that we will successfully address these risks. In the event that we do not successfully address these risks, our business, prospects, financial condition, and results of operations could be materially and adversely affected.

We have a history of losses and can provide no assurance of our future operating results.

We have experienced net losses and negative cash flows from operating activities since inception and we expect such losses and negative cash flows to continue in the foreseeable future. As of December 31, 2020 and 2019, we had working capital (deficit) of $(21,699,304) and $(38,598,414), respectively, and shareholders’ (deficit) of $(29,645,300) and $(44,565,901), respectively. For the years ended December 31, 2020 and 2019, we incurred net income (losses) of $13,261,365 and $(27,473,678). During the year ended December 31, 2020, we had a loss from operations of $4,711,238. As of December 31, 2020, we had an aggregate accumulated deficit of $94,020,274. We may never achieve profitability. The opinion of our independent registered public accountants on our audited financial statements as of and for the year ended December 31, 2020 contains an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is dependent upon raising capital from financing transactions and future sales.

We will need significant additional capital, which we may be unable to obtain.

Revenues generated from our operations are not presently sufficient to sustain our operations. Therefore, we will need to raise additional capital to continue our operations. There can be no assurance that additional funds will be available when needed from any source or, if available, will be available on terms that are acceptable to us. We may be required to pursue sources of additional capital through various means, including debt or equity financings. Future financings through equity investments are likely to be dilutive to existing stockholders. Also, the terms of securities we may issue in future capital transactions may be more favorable for new investors. Newly issued securities may include preferences, superior voting rights, the issuance of warrants or other derivative securities, and the issuances of incentive awards under equity employee incentive plans, which may have additional dilutive effects. Further, we may incur substantial costs in pursuing future capital and/or financing, including investment banking fees, legal fees, accounting fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition. Our ability to obtain needed financing may be impaired by such factors as the capital markets and our history of losses, which could impact the availability or cost of future financings. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, even to the extent that we reduce our operations accordingly, we may be required to cease operations. In addition, we have outstanding convertible preferred stock that are convertible into common stock at variable conversion prices and in addition, in some cases entitle certain prior investors to certain make-good shares. Our issuance of common stock upon conversion of such preferred stock will result in further dilution to our stockholders.

17

We have incurred substantial indebtedness.

As of December 31, 2020, we had outstanding convertible promissory notes in the amount of $3,100,503. All such debt is payable within the following thirty-six months and is convertible at a significant discount to our market price of stock. Our level of indebtedness and insufficient cash on hand increases the possibility that we may be unable to generate cash sufficient to pay, when due, the principal of, interest on or other amounts due in respect of the indebtedness. Our indebtedness, combined with other financial obligations and contractual commitments, could:

| ● | in the case of convertible debt that is converted into equity, result in a reduction in the overall percentage holdings of our stockholders, put downward pressure on the market price of our common stock, result in adjustments to conversion and exercise prices of outstanding notes and warrants and obligate us to issue additional shares of common stock to certain of our stockholders; | |

| ● | make it more difficult for us to satisfy our obligations with respect to the indebtedness and any failure to comply with the obligations under any of our debt instruments, including restrictive covenants, could result in events of default under the loan agreements and instruments governing the indebtedness; | |

| ● | require us to dedicate a substantial portion of our cash flow from operations to payments on indebtedness, thereby reducing funds available for working capital, capital expenditures, acquisitions, research and development and other corporate purposes; | |

| ● | increase our vulnerability to adverse economic and industry conditions, which could place us at a competitive disadvantage compared to competitors that have relatively less indebtedness; |

| ● | limit our flexibility in planning for, or reacting to, changes in business and the industry in which we operate; and | |

| ● | limit our ability to borrow additional funds, or to dispose of assets to raise funds, if needed, for working capital, capital expenditures, acquisitions, research and development and other corporate purposes. |

We may incur significant additional indebtedness in the future. If we incur a substantial amount of additional indebtedness, the related risks that we face could become more significant. Additionally, the terms of any future debt that we may incur may impose requirements or restrictions that further affect our financial and operating flexibility or subject us to other events of default.

Our revenues are dependent upon acceptance of our technology and products by the market; the failure of which would cause us to curtail or cease operations.

We believe that most of our future revenues will come from the sale or license of our technology and systems. As a result, we will continue to incur substantial operating losses until such time as we are able to generate revenues from the sale or license of our technology and systems. There can be no assurance that businesses and prospective customers will adopt our technology and systems, or that businesses and prospective customers will agree to pay for or license our technology and systems. In the event that we are not able to develop a customer base that purchases or licenses our technology and systems, or if we are unable to charge the necessary prices or license fees, our financial condition and results of operations will be materially and adversely affected.

We will need to increase the size of our organization, and may experience difficulties in managing growth.

We are a small company with a minimal number of employees. We expect to experience a period of significant expansion in headcount, facilities, infrastructure and overhead and anticipate that further expansion will be required to address potential growth and market opportunities. Future growth will impose significant added responsibilities on members of management, including the need to identify, recruit, maintain and integrate managers. Our future financial performance and our ability to compete effectively will depend, in part, on our ability to manage any future growth effectively.

18

We may not be able to successfully license our technology and commercialize our products which would result in continued losses and may require us to curtail or cease operations.

We are currently commercializing our technology. We are unable to project when we will achieve profitability, if at all. As is the case with any new technology, we expect the research and development process to continue. We cannot assure that our engineering resources will be able to develop our technology and systems fast enough to meet market requirements. We can also not assure that our technology and systems will gain market acceptance and that we will be able to successfully commercialize the technologies. The failure to successfully develop and commercialize the technologies would result in continued losses and may require us to curtail or cease operations.

Our ability to clean-up oil and gas and waste water and aqua-feed on a commercially viable basis is unproven, which could have a detrimental effect on our ability to generate or sustain revenues.

The technologies we use to harvest algae, clean up oil and gas water, and waste water, have never been utilized on a full-scale commercial basis. Our EWS:AOx technology was only recently developed. All of the tests conducted to date by us with respect to the technology have been performed in a limited scale or small commercial scale environment and the same or similar results may not be obtainable at competitive costs on a large-scale commercial basis. We have never employed our technology under the conditions or in the volumes that will be required for us to be profitable and cannot predict all of the difficulties that may arise. Accordingly, our technology may not perform successfully on a commercial basis and may never generate any revenues or be profitable.

If a competitor were to achieve a technological breakthrough, our operations and business could be negatively impacted.

There currently exist a number of businesses that are pursuing novel processes to clean up waste water. Should a competitor achieve a research and development, technological or biological breakthrough where process costs are significantly reduced, efficiency greatly increased over ours, or if the costs of similar competing products were to fall substantially, we may have difficulty attracting customer licensees or sales. Furthermore, competitors may have access to larger resources (capital or otherwise) that provide them with an advantage in the marketplace, which could result in a negative impact on our business.

Any competing technology that cleans or purifies water, at a superior scale and more cost efficient than ours, could render our technology obsolete. In addition, because we are the master licensee of only five issued patents, we may not be able to preclude development of even directly competing technologies using the same methods, materials and procedures as we use to achieve our results. Any of these competitive forces may inhibit or materially adversely affect our ability to attract customer licensees, or to obtain royalties or other fees from our customer licensees. This could have a material adverse effect on our business, prospects, results of operation and financial condition.

Our long-term success depends on future royalties paid to us by licensees, and we face the risks inherent in a royalty-based business model.

We intend to generate revenue through the licensing of our technology and systems, and our long-term success depends on future royalties paid to us by prospective customer licensees. We expect that the amount of royalty payments we may receive will be based upon the revenues generated by our prospective customer licensees’ operations, and so we will be dependent on the successful operations of our prospective customer licensees for a significant portion of our revenues. We face risks inherent in a royalty-based business model, many of which are outside of our control, including those arising from our reliance on the management and operating capabilities of our customer licensees and the cyclicality of supply and demand for end-products produced using our technology. Should our prospective customer licensees fail to achieve sufficient profitability in their operations, our royalty payments would be diminished and our results of operations, cash flows and financial condition could be adversely affected, and any such effects could be material.

19

We rely on strategic partners.

We rely on strategic partners to aid in the development and marketing of our technology and processes. Should our strategic partners not regard us as significant to their own businesses, they could reduce their commitment to us or terminate their relationship with us, pursue competing relationships or attempt to develop or acquire processes that compete with ours. Any such action could materially adversely affect our business.

A lack of government subsidies may hinder the usefulness of our technology.

We assemble and sell complete engineered solutions, and products, using the expertise and knowhow of PWT and MWS. Subsidies of any of the industries vary and may be reduced or eliminated, which could have a material adverse effect on our business. Likewise, regulations may become more onerous which also could have a material adverse effect on our business.

The industries in which we operate may endure deflationary cycles, affecting our ability to sell and license our systems.

It is possible that industry sector collapses and other deflationary events may impact our business materially and adversely.

If we lose key employees and consultants or are unable to attract or retain qualified personnel, our business could suffer.

Our success is highly dependent on our ability to attract and retain qualified scientific, engineering and management personnel. We are highly dependent on our management, including T. Riggs Eckelberry, who has been critical to the development of our technology and business. The loss of the services of Mr. Eckelberry would have a material adverse effect on our operations. We do not have an employment agreement with Mr. Eckelberry. Accordingly, there can be no assurance that he will remain associated with us. His efforts will be critical to us as we continue to develop our technology and as we attempt to transition to a company with profitable commercialized products and services. If we were to lose Mr. Eckelberry, or any other key employees or consultants, we may experience difficulties in competing effectively, developing our technology and implementing our business strategies.

Competition from other companies in our market may affect the market for our technology.

New companies are constantly entering the market, thus increasing the competition. Larger foreign owned and domestic companies which have been engaged in water cleanup and algae harvesting for substantially longer periods of time may have access to greater financial and other resources. These companies may have greater success in the recruitment and retention of qualified employees, as well as in conducting their own fuel manufacturing and marketing operations, which may give them a competitive advantage. In addition, actual or potential competitors may be strengthened through the acquisition of additional assets and interests. If we or our customers are unable to compete effectively or adequately respond to competitive pressures, this may materially adversely affect our results of operation and financial condition.

An occurrence of an uncontrollable event such as the COVID-19 pandemic may negatively affect our operations.