Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - Altabancorp | d937142dex991.htm |

| 8-K - 8-K - Altabancorp | d937142d8k.htm |

Exhibit 99.2 Acquisition of May 18, 2021Exhibit 99.2 Acquisition of May 18, 2021

Forward-Looking Statements This presentation may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward- looking statements include, but are not limited to, statements about the Company’s plans, objectives, expectations and intentions that are not historical facts, and other statements identified by words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “should,” “projects,” “seeks,” “estimates,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are based on current beliefs and expectations of management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the Company’s control. In addition, these forward-looking statements are subject to assumptions with respect to future business strategies and decisions that are subject to change. The following factors, among others, could cause actual results to differ materially from the anticipated results (express or implied) or other expectations in the forward-looking statements, including those set forth in this presentation: 1) the occurrence of any event, change or other circumstances that could give rise to the right of one or both of the parties to terminate the definitive merger agreement between the Company and ALTA; 2) the possibility that the proposed transaction will not close when expected or at all because required regulatory, shareholder or other approvals are not received or other conditions to the closing are not satisfied on a timely basis or at all, or are obtained subject to conditions that are not anticipated; 3) the risk that any announcements relating to the proposed combination could have adverse effects on the market price of the common stock of either or both parties to the combination; 4) the possibility that the anticipated benefits of the transaction will not be realized when expected or at all, including as a result of the impact of, or problems arising from, the integration of the two companies or as a result of the strength of the economy and competitive factors in the areas where the Company and ALTA do business; 5) potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the transaction that could make it difficult to retain or hire key personnel and maintain relationships with customers; 6) the Company’s and ALTA’s success in executing their respective business plans and strategies and managing the risks involved; 7) the risk that the proposed combination may be more difficult or time- consuming than anticipated, including in areas such as asset realization, systems integration and other key strategies; 8) the unforeseen risks relating to liabilities of the Company or ALTA that may exist; 9) the Company’s success in managing risks involved in the foregoing; and 10) the effects of any reputational damage to the Company resulting from any of the foregoing. The foregoing are representative of the factors that could affect the outcome of our forward-looking statements. In addition, such statements could be affected by general industry and market conditions and growth rates, general economic and political conditions, either nationally or in the states in which the Company, ALTA or their respective subsidiaries do business, including interest rate and currency exchange rate fluctuations, changes and trends in the securities markets, changes in regulations as a result of the change in administration at the federal level, and other factors. The Company provides further detail regarding these risks and uncertainties in its latest Form 10-K and subsequent Form 10-Qs, including in the respective Risk Factors sections of such reports, as well as in subsequent SEC filings. Please take into account that forward-looking statements speak only as of the date of this presentation. Given the described uncertainties and risks, the Company cannot guarantee its future performance or results of operations and you should not place undue reliance on these forward-looking statements. The Company does not undertake any obligation to publicly correct, revise, or update any forward-looking statement if it later becomes aware that actual results are likely to differ materially from those expressed in such forward-looking statement, except as required under federal securities laws. 1 1Forward-Looking Statements This presentation may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward- looking statements include, but are not limited to, statements about the Company’s plans, objectives, expectations and intentions that are not historical facts, and other statements identified by words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “should,” “projects,” “seeks,” “estimates,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are based on current beliefs and expectations of management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the Company’s control. In addition, these forward-looking statements are subject to assumptions with respect to future business strategies and decisions that are subject to change. The following factors, among others, could cause actual results to differ materially from the anticipated results (express or implied) or other expectations in the forward-looking statements, including those set forth in this presentation: 1) the occurrence of any event, change or other circumstances that could give rise to the right of one or both of the parties to terminate the definitive merger agreement between the Company and ALTA; 2) the possibility that the proposed transaction will not close when expected or at all because required regulatory, shareholder or other approvals are not received or other conditions to the closing are not satisfied on a timely basis or at all, or are obtained subject to conditions that are not anticipated; 3) the risk that any announcements relating to the proposed combination could have adverse effects on the market price of the common stock of either or both parties to the combination; 4) the possibility that the anticipated benefits of the transaction will not be realized when expected or at all, including as a result of the impact of, or problems arising from, the integration of the two companies or as a result of the strength of the economy and competitive factors in the areas where the Company and ALTA do business; 5) potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the transaction that could make it difficult to retain or hire key personnel and maintain relationships with customers; 6) the Company’s and ALTA’s success in executing their respective business plans and strategies and managing the risks involved; 7) the risk that the proposed combination may be more difficult or time- consuming than anticipated, including in areas such as asset realization, systems integration and other key strategies; 8) the unforeseen risks relating to liabilities of the Company or ALTA that may exist; 9) the Company’s success in managing risks involved in the foregoing; and 10) the effects of any reputational damage to the Company resulting from any of the foregoing. The foregoing are representative of the factors that could affect the outcome of our forward-looking statements. In addition, such statements could be affected by general industry and market conditions and growth rates, general economic and political conditions, either nationally or in the states in which the Company, ALTA or their respective subsidiaries do business, including interest rate and currency exchange rate fluctuations, changes and trends in the securities markets, changes in regulations as a result of the change in administration at the federal level, and other factors. The Company provides further detail regarding these risks and uncertainties in its latest Form 10-K and subsequent Form 10-Qs, including in the respective Risk Factors sections of such reports, as well as in subsequent SEC filings. Please take into account that forward-looking statements speak only as of the date of this presentation. Given the described uncertainties and risks, the Company cannot guarantee its future performance or results of operations and you should not place undue reliance on these forward-looking statements. The Company does not undertake any obligation to publicly correct, revise, or update any forward-looking statement if it later becomes aware that actual results are likely to differ materially from those expressed in such forward-looking statement, except as required under federal securities laws. 1 1

Transaction Highlights Ø Glacier Bancorp, Inc. (NASDAQ: GBCI) will acquire Altabancorp (NASDAQ: ALTA), the bank holding company for Altabank, a community bank headquartered in American Fork, Utah § Altabank is the largest community bank headquartered in Utah, with $3.5 billion in total assets Ø Transaction is consistent with Glacier’s targeted financial metrics and focused M&A strategy § High quality community banks in the Western U.S. with assets between $300 million and $3+ billion Transaction § Stable, sticky and seasoned low-cost deposit franchise Overview § Pristine loan portfolio which improves Glacier’s composition mix and loan yields § Reduced integration risk with both companies utilizing Jack Henry as core processor (1) Ø Utah is one of the strongest and fastest growing states in the country – ranked #1 best economy in 2020 Ø Glacier has obtained voting agreements from ALTA’s Directors, Executive Officers and Principal Shareholders, including members of the Gunther family Ø Pricing metrics, deal structure, and conservative assumptions reflective of Glacier’s disciplined approach to acquisitions § Immediately accretive to EPS – accretion of 5.2% in 2022, or 5.8% with fully realized cost savings § Immediately accretive to tangible book value per share Financially § Internal rate of return (IRR) above 15% Attractive § Conservative cost savings, estimated at 17.5% of ALTA’s noninterest expense § Less than 15% premium to ALTA’s current stock price (2) § Pay to trade ratio of 80.1% § Achievable revenue synergies identified, but not factored into the model Source: S&P Global Market Intelligence Note: Based on GBCI closing price of $61.51 and ALTA closing stock price of $43.44 as of May 17, 2021 (1) Ranking by U.S. News and World Report (2) Ratio of the tangible book value multiple paid (based on required tangible common equity of $342.9 million) to GBCI’s tangible book 2 2 value multiple as of May 17, 2021Transaction Highlights Ø Glacier Bancorp, Inc. (NASDAQ: GBCI) will acquire Altabancorp (NASDAQ: ALTA), the bank holding company for Altabank, a community bank headquartered in American Fork, Utah § Altabank is the largest community bank headquartered in Utah, with $3.5 billion in total assets Ø Transaction is consistent with Glacier’s targeted financial metrics and focused M&A strategy § High quality community banks in the Western U.S. with assets between $300 million and $3+ billion Transaction § Stable, sticky and seasoned low-cost deposit franchise Overview § Pristine loan portfolio which improves Glacier’s composition mix and loan yields § Reduced integration risk with both companies utilizing Jack Henry as core processor (1) Ø Utah is one of the strongest and fastest growing states in the country – ranked #1 best economy in 2020 Ø Glacier has obtained voting agreements from ALTA’s Directors, Executive Officers and Principal Shareholders, including members of the Gunther family Ø Pricing metrics, deal structure, and conservative assumptions reflective of Glacier’s disciplined approach to acquisitions § Immediately accretive to EPS – accretion of 5.2% in 2022, or 5.8% with fully realized cost savings § Immediately accretive to tangible book value per share Financially § Internal rate of return (IRR) above 15% Attractive § Conservative cost savings, estimated at 17.5% of ALTA’s noninterest expense § Less than 15% premium to ALTA’s current stock price (2) § Pay to trade ratio of 80.1% § Achievable revenue synergies identified, but not factored into the model Source: S&P Global Market Intelligence Note: Based on GBCI closing price of $61.51 and ALTA closing stock price of $43.44 as of May 17, 2021 (1) Ranking by U.S. News and World Report (2) Ratio of the tangible book value multiple paid (based on required tangible common equity of $342.9 million) to GBCI’s tangible book 2 2 value multiple as of May 17, 2021

Strategic Rationale Ø Solidifies and ensures Glacier’s continued leadership position in the Rocky Mountain West, one of the strongest regions in the country, by establishing leadership in Utah and acquiring one of the largest banks in the region § Unique opportunity to become the leading community $23 17 218 bank in Utah – one of the fastest growing states in the BILLION country LOCATIONS BANK DIVISIONS TOTAL ASSETS § Tremendous scarcity value in Utah, a state with limited acquisition opportunities and infrequent merger activity § ALTA is the only community bank headquartered in a five-state region (UT, ID, WY, AZ, and NV) with total assets between $3 billion and $10 billion WA MT th § GBCI will become the 6 largest bank in Utah and have a (1) strong footing in every major market in the state Ø Top 5 position in Provo MSA – #1 Best-performing ID (2) large city nationwide WY Ø Top 5 position in Logan MSA – #2 Best-performing (2) small city nationwide NV nd § Utah will become GBCI’s 2 largest market with over $3 UT CO billion in deposits and $2 billion in loans § Acquisition further diversifies GBCI’s loan and deposit portfolio AZ § ALTA brings additional technology and systems that can be leveraged across the entire Glacier footprint, accelerating Glacier’s technology evolution Sources: S&P Global Market Intelligence as of March 31, 2021, FDIC deposit data as of June 30, 2020 Note: Information is pro forma for the pending ALTA acquisition (1) Excludes industrial loan companies (ILCs) 3 3 (2) Milken Institute’s 2021 Ranking of Best-Performing CitiesStrategic Rationale Ø Solidifies and ensures Glacier’s continued leadership position in the Rocky Mountain West, one of the strongest regions in the country, by establishing leadership in Utah and acquiring one of the largest banks in the region § Unique opportunity to become the leading community $23 17 218 bank in Utah – one of the fastest growing states in the BILLION country LOCATIONS BANK DIVISIONS TOTAL ASSETS § Tremendous scarcity value in Utah, a state with limited acquisition opportunities and infrequent merger activity § ALTA is the only community bank headquartered in a five-state region (UT, ID, WY, AZ, and NV) with total assets between $3 billion and $10 billion WA MT th § GBCI will become the 6 largest bank in Utah and have a (1) strong footing in every major market in the state Ø Top 5 position in Provo MSA – #1 Best-performing ID (2) large city nationwide WY Ø Top 5 position in Logan MSA – #2 Best-performing (2) small city nationwide NV nd § Utah will become GBCI’s 2 largest market with over $3 UT CO billion in deposits and $2 billion in loans § Acquisition further diversifies GBCI’s loan and deposit portfolio AZ § ALTA brings additional technology and systems that can be leveraged across the entire Glacier footprint, accelerating Glacier’s technology evolution Sources: S&P Global Market Intelligence as of March 31, 2021, FDIC deposit data as of June 30, 2020 Note: Information is pro forma for the pending ALTA acquisition (1) Excludes industrial loan companies (ILCs) 3 3 (2) Milken Institute’s 2021 Ranking of Best-Performing Cities

Utah’s Attractive Profile Ø Utah is Experiencing Exceptional GrowthØ Utah is Business Friendly § Utah is the fastest growing market in GBCI’s eight-§ Favorable business and tax climate continues to state footprint attract firms and top talent to the state nd • 2 fastest growing state in the U.S. from 2010-2021 with a • #1 Best State for Entrepreneurs in 2020 by Forbes total population of 3.3 million • #3 Best State for Business in 2019 by Forbes th • 4 highest projected household income growth between 2021- • Average corporate tax rate of 5.0% 2026 § 33 company relocations or expansions in Utah in § Most rapid housing unit growth rate in the U.S. for the rd 2019 – total of $1.2 billion in capital investments 3 consecutive year § $4.1 billion redevelopment of the Salt Lake City • 30,745 residential dwelling unit permits issued in 2020, the st highest volume since 2005 International Airport – 1 new U.S. hub airport built st in the 21 century • Permit-authorized construction peaked in 2020, totaling $10.3 billion for residential and nonresidential projects • Capacity to handle 34 million passengers per year th § 5 lowest unemployment rate in the nation Major Employers • 3.3% compared to the national average of 6.5% in 2020 Ø Utah has Nation-Leading Metropolitan Areas § St. George and Provo are #2 and #3 ranked MSAs for projected population growth in Western U.S. § 5 of the top 10 Best-Performing Cities in America in 2021 by the Milken Institute Sources: S&P Global Market Intelligence; Economic Development Corporation of Utah, U.S. Bureau of Labor Statistics, Utah Economic Council, The Salt Lake Tribune, SLC International Airport, The Tax Foundation 4 4 Note: Western U.S. states include AK, AZ, CA, CO, HI, ID, MT, NV, NM, OR, UT, WA, WYUtah’s Attractive Profile Ø Utah is Experiencing Exceptional GrowthØ Utah is Business Friendly § Utah is the fastest growing market in GBCI’s eight-§ Favorable business and tax climate continues to state footprint attract firms and top talent to the state nd • 2 fastest growing state in the U.S. from 2010-2021 with a • #1 Best State for Entrepreneurs in 2020 by Forbes total population of 3.3 million • #3 Best State for Business in 2019 by Forbes th • 4 highest projected household income growth between 2021- • Average corporate tax rate of 5.0% 2026 § 33 company relocations or expansions in Utah in § Most rapid housing unit growth rate in the U.S. for the rd 2019 – total of $1.2 billion in capital investments 3 consecutive year § $4.1 billion redevelopment of the Salt Lake City • 30,745 residential dwelling unit permits issued in 2020, the st highest volume since 2005 International Airport – 1 new U.S. hub airport built st in the 21 century • Permit-authorized construction peaked in 2020, totaling $10.3 billion for residential and nonresidential projects • Capacity to handle 34 million passengers per year th § 5 lowest unemployment rate in the nation Major Employers • 3.3% compared to the national average of 6.5% in 2020 Ø Utah has Nation-Leading Metropolitan Areas § St. George and Provo are #2 and #3 ranked MSAs for projected population growth in Western U.S. § 5 of the top 10 Best-Performing Cities in America in 2021 by the Milken Institute Sources: S&P Global Market Intelligence; Economic Development Corporation of Utah, U.S. Bureau of Labor Statistics, Utah Economic Council, The Salt Lake Tribune, SLC International Airport, The Tax Foundation 4 4 Note: Western U.S. states include AK, AZ, CA, CO, HI, ID, MT, NV, NM, OR, UT, WA, WY

Altabancorp (NASDAQ: ALTA) Overview Ø Headquartered in American Fork, Utah, Altabank is the largest community bank in Utah with $3.5 billion in total assets Ø 100+ year operating history in Utah and Idaho Ø Full-service bank, providing comprehensive financial services to businesses and individuals through 25 branch locations from Preston, Idaho to St. George, Utah Ø Market leader in most of the communities in which it operates Ø 1.13% ROAA in Q1 2021 despite historically low loan-to-deposit ratio of 57.1% Financial Highlights Balance Sheet (3/31/2021) Income Statement (Q1 2021) Total Assets $ 3 ,522 Net Income $ 9.4 Gross Loans $ 1 ,805 ROAA 1.13% Total Deposits $ 3,159 ROATCE 11.36% Loans / Deposits 57.1% Net Interest Margin 2.91% Non-Int. Bearing Dep. (% of Total) 35.0% Efficiency Ratio 57.5% Yield on Loans 5.32% Tangible Common Equity $ 322 Yield on Securities 0.67% Cost of Total Deposits 0.20% Tangible Common Equity Ratio 9.21% Tier 1 Common Capital (CET1) Ratio 17.15% Market Information (5/17/2021) Ticker ALTA NPAs / Total Assets 0.21% Exchange NASDAQ Loan Loss Reserves / Gross Loans (Ex. PPP) 2.35% Stock Price $ 4 3.44 Market Cap. $ 820 Price / Tg. Book Value 254.8% (1) Price / 2022E EPS 18.7x Source: S&P Global Market Intelligence, earnings release data as of 3/31/2021 Note: All dollars in millions, except per share 5 5 (1) Based on average Street estimatesAltabancorp (NASDAQ: ALTA) Overview Ø Headquartered in American Fork, Utah, Altabank is the largest community bank in Utah with $3.5 billion in total assets Ø 100+ year operating history in Utah and Idaho Ø Full-service bank, providing comprehensive financial services to businesses and individuals through 25 branch locations from Preston, Idaho to St. George, Utah Ø Market leader in most of the communities in which it operates Ø 1.13% ROAA in Q1 2021 despite historically low loan-to-deposit ratio of 57.1% Financial Highlights Balance Sheet (3/31/2021) Income Statement (Q1 2021) Total Assets $ 3 ,522 Net Income $ 9.4 Gross Loans $ 1 ,805 ROAA 1.13% Total Deposits $ 3,159 ROATCE 11.36% Loans / Deposits 57.1% Net Interest Margin 2.91% Non-Int. Bearing Dep. (% of Total) 35.0% Efficiency Ratio 57.5% Yield on Loans 5.32% Tangible Common Equity $ 322 Yield on Securities 0.67% Cost of Total Deposits 0.20% Tangible Common Equity Ratio 9.21% Tier 1 Common Capital (CET1) Ratio 17.15% Market Information (5/17/2021) Ticker ALTA NPAs / Total Assets 0.21% Exchange NASDAQ Loan Loss Reserves / Gross Loans (Ex. PPP) 2.35% Stock Price $ 4 3.44 Market Cap. $ 820 Price / Tg. Book Value 254.8% (1) Price / 2022E EPS 18.7x Source: S&P Global Market Intelligence, earnings release data as of 3/31/2021 Note: All dollars in millions, except per share 5 5 (1) Based on average Street estimates

ALTA Operating Markets Provo-Orem, UT MSA Salt Lake City, UT MSA #1 Best-Performing Large City (Provo) Strongest Job Market in U.S. Total Population: 673,743 Total Population: 1,251,413 Total Market Total Market $11.4 billion $59.7 billion Deposits: Deposits: ALTA Deposit ALTA Deposit th th 4 7 Market Rank: Market Rank: Logan and Ogden-Clearfield, UT MSAs St. George, UT MSA #2 Best-Performing Small City (Logan) Fastest Growing MSA (2010-2021) Total Population: 842,235 Total Population: 185,531 Total Market Total Market $8.9 billion $3.0 billion Deposits: Deposits: rd 3 (Logan MSA) ALTA Deposit ALTA Deposit th 7 th 10 (Ogden MSA) Market Rank: Market Rank: 6 6 Sources: S&P Global Market Intelligence, Wall Street Journal, Milken Institute, FDIC deposit data as of June 30, 2020 ALTA Operating Markets Provo-Orem, UT MSA Salt Lake City, UT MSA #1 Best-Performing Large City (Provo) Strongest Job Market in U.S. Total Population: 673,743 Total Population: 1,251,413 Total Market Total Market $11.4 billion $59.7 billion Deposits: Deposits: ALTA Deposit ALTA Deposit th th 4 7 Market Rank: Market Rank: Logan and Ogden-Clearfield, UT MSAs St. George, UT MSA #2 Best-Performing Small City (Logan) Fastest Growing MSA (2010-2021) Total Population: 842,235 Total Population: 185,531 Total Market Total Market $8.9 billion $3.0 billion Deposits: Deposits: rd 3 (Logan MSA) ALTA Deposit ALTA Deposit th 7 th 10 (Ogden MSA) Market Rank: Market Rank: 6 6 Sources: S&P Global Market Intelligence, Wall Street Journal, Milken Institute, FDIC deposit data as of June 30, 2020

Glacier’s Market Leading Utah Franchise Ø Glacier’s two Utah bank divisions will have a strong presence in every major market in the state Ø Minimal overlap with Glacier’s First Community Bank division in Utah Pro Forma Utah Branch Footprint Ø Over 80% of the Utah population resides in the eight counties where the pro forma banks have branches ALTA Branches Ø Utah is ripe for community banking – money center banks control over 50% (1) FCB Branches of the Utah banking market Pro Forma Market Presence – Utah MSAs ALTA GBCI Pro Forma Deposits Deposits Deposits Mkt. MSA Branches ($MM) Branches ($MM) Branches ($MM) Rank Provo-Orem, UT 12 $ 1,525 0 $ - 12 $ 1 ,525 4 Salt Lake City, UT 6 $ 528 1 $ 28 7 $ 557 7 Logan, UT-ID 4 $ 384 0 $ - 4 $ 384 3 St. George, UT 1 $ 112 0 $ - 1 $ 112 7 Ogden-Clearfield, UT 2 $ 69 8 $ 498 10 $ 567 5 Heber, UT 0 $ - 1 $ 83 1 $ 83 7 Total 25 $ 2,618 10 $ 609 35 $ 3,227 2010-2021 Population Change Utah MSA National Avg. 40.0% 34.3% 30.4% 30.0% 27.9% 20.0% 16.5% 16.6% 15.0% 10.0% 7.2% 0.0% Provo-Orem, UT Salt Lake City, UT Logan, UT-ID St. George, UT Ogden-Clearfield, UT Herber, UT Sources: S&P Global Market Intelligence, FDIC deposit data as of June 30, 2020 (1) First Community Bank Utah (a division of Glacier Bank) 7 7 (2) Excludes industrial loan companies (ILCs)Glacier’s Market Leading Utah Franchise Ø Glacier’s two Utah bank divisions will have a strong presence in every major market in the state Ø Minimal overlap with Glacier’s First Community Bank division in Utah Pro Forma Utah Branch Footprint Ø Over 80% of the Utah population resides in the eight counties where the pro forma banks have branches ALTA Branches Ø Utah is ripe for community banking – money center banks control over 50% (1) FCB Branches of the Utah banking market Pro Forma Market Presence – Utah MSAs ALTA GBCI Pro Forma Deposits Deposits Deposits Mkt. MSA Branches ($MM) Branches ($MM) Branches ($MM) Rank Provo-Orem, UT 12 $ 1,525 0 $ - 12 $ 1 ,525 4 Salt Lake City, UT 6 $ 528 1 $ 28 7 $ 557 7 Logan, UT-ID 4 $ 384 0 $ - 4 $ 384 3 St. George, UT 1 $ 112 0 $ - 1 $ 112 7 Ogden-Clearfield, UT 2 $ 69 8 $ 498 10 $ 567 5 Heber, UT 0 $ - 1 $ 83 1 $ 83 7 Total 25 $ 2,618 10 $ 609 35 $ 3,227 2010-2021 Population Change Utah MSA National Avg. 40.0% 34.3% 30.4% 30.0% 27.9% 20.0% 16.5% 16.6% 15.0% 10.0% 7.2% 0.0% Provo-Orem, UT Salt Lake City, UT Logan, UT-ID St. George, UT Ogden-Clearfield, UT Herber, UT Sources: S&P Global Market Intelligence, FDIC deposit data as of June 30, 2020 (1) First Community Bank Utah (a division of Glacier Bank) 7 7 (2) Excludes industrial loan companies (ILCs)

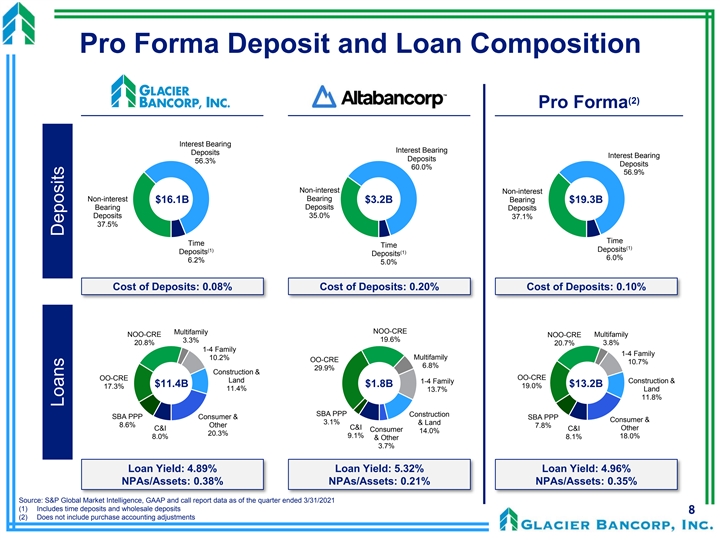

Pro Forma Deposit and Loan Composition (2) Pro Forma Interest Bearing Interest Bearing Deposits Interest Bearing Deposits 56.3% Deposits 60.0% 56.9% Non-interest Non-interest Non-interest Bearing Bearing $16.1B $3.2B $19.3B Bearing Deposits Deposits Deposits 35.0% 37.1% 37.5% Time Time Time (1) (1) Deposits Deposits (1) Deposits 6.0% 6.2% 5.0% Cost of Deposits: 0.08% Cost of Deposits: 0.20% Cost of Deposits: 0.10% Multifamily NOO-CRE NOO-CRE NOO-CRE Multifamily 19.6% 3.3% 20.8% 20.7% 3.8% 1-4 Family 1-4 Family 10.2% Multifamily OO-CRE 10.7% 6.8% 29.9% Construction & OO-CRE OO-CRE Land Construction & 1-4 Family $11.4B $1.8B $13.2B 19.0% 17.3% 11.4% 13.7% Land 11.8% SBA PPP Construction SBA PPP Consumer & SBA PPP Consumer & 3.1% & Land 8.6% Other 7.8% C&I Other C&I C&I Consumer 14.0% 20.3% 9.1% 18.0% 8.0% 8.1% & Other 3.7% Loan Yield: 4.89% Loan Yield: 5.32% Loan Yield: 4.96% NPAs/Assets: 0.38% NPAs/Assets: 0.21% NPAs/Assets: 0.35% Source: S&P Global Market Intelligence, GAAP and call report data as of the quarter ended 3/31/2021 (1) Includes time deposits and wholesale deposits 8 8 (2) Does not include purchase accounting adjustments Loans DepositsPro Forma Deposit and Loan Composition (2) Pro Forma Interest Bearing Interest Bearing Deposits Interest Bearing Deposits 56.3% Deposits 60.0% 56.9% Non-interest Non-interest Non-interest Bearing Bearing $16.1B $3.2B $19.3B Bearing Deposits Deposits Deposits 35.0% 37.1% 37.5% Time Time Time (1) (1) Deposits Deposits (1) Deposits 6.0% 6.2% 5.0% Cost of Deposits: 0.08% Cost of Deposits: 0.20% Cost of Deposits: 0.10% Multifamily NOO-CRE NOO-CRE NOO-CRE Multifamily 19.6% 3.3% 20.8% 20.7% 3.8% 1-4 Family 1-4 Family 10.2% Multifamily OO-CRE 10.7% 6.8% 29.9% Construction & OO-CRE OO-CRE Land Construction & 1-4 Family $11.4B $1.8B $13.2B 19.0% 17.3% 11.4% 13.7% Land 11.8% SBA PPP Construction SBA PPP Consumer & SBA PPP Consumer & 3.1% & Land 8.6% Other 7.8% C&I Other C&I C&I Consumer 14.0% 20.3% 9.1% 18.0% 8.0% 8.1% & Other 3.7% Loan Yield: 4.89% Loan Yield: 5.32% Loan Yield: 4.96% NPAs/Assets: 0.38% NPAs/Assets: 0.21% NPAs/Assets: 0.35% Source: S&P Global Market Intelligence, GAAP and call report data as of the quarter ended 3/31/2021 (1) Includes time deposits and wholesale deposits 8 8 (2) Does not include purchase accounting adjustments Loans Deposits

Transaction Overview and Assumptions (2) § $930.5 million to common shareholders, or $49.03 per share (1) § $3.0 million to optionholders Transaction Value § $933.5 million total transaction value (2) § 100% stock consideration to ALTA common shareholders Consideration Mix§ 0.7971 shares of Glacier stock for each ALTA share § ALTA options will be cashed out based on the in-the-money value (3) § Fixed exchange ratio with collars set between $49.43 and $74.15 Price Protection § Consensus earnings estimates for both companies Earnings Estimates § Total gross credit mark of $34.1 million, or 1.95% ALTA’s gross loan portfolio excluding PPP loans § $31.9 million allocated to non-PCD loans; amortized into earnings over 5 years using the sum-of-the-years- Loan Credit Mark digits accelerated method Estimate § $2.2 million allocated to purchase credit deteriorated (PCD) loans, recorded into ACL § Provision expense of $31.9 million for CECL taken immediately after close; included in pro forma tangible book value § Net fair value write-up of $22.0 million on fixed assets, loans (rate mark) and time deposits Other Fair Value § Core deposit intangible of $10.5 million, or 0.35% of non-time deposits; amortized over 10 years using the sum-of-the- Estimates years digits methodology § Cost savings of 17.5% of ALTA’s non-interest expense base Cost Savings § 80.0% realized in 2022 and 100% thereafter Durbin Impact§ Estimated reduction of ALTA’s interchange income by approximately $2.0 million annually (4) Restructuring Charges§ One-time transaction costs of approximately $33.0 million, pre-tax § $342.9 million at closing Minimum Tangible § Excess capital, net of any adjustments for ALTA’s Final Transaction Related Expenses, to be paid out to ALTA Common Equity shareholders prior to closing Expected Closing§ Fourth Quarter 2021 (1) Based on GBCI closing price of $61.51 as of May 17, 2021 (2) Includes 18,876,639 ALTA shares and 101,128 unvested ALTA RSUs (3) Refer to the Plan and Agreement of Merger for complete terms relating to stock collars and termination rights 9 9 (4) Including employment and benefits plan costs, data processing conversion costs and penalties, and combined professional and advisory feesTransaction Overview and Assumptions (2) § $930.5 million to common shareholders, or $49.03 per share (1) § $3.0 million to optionholders Transaction Value § $933.5 million total transaction value (2) § 100% stock consideration to ALTA common shareholders Consideration Mix§ 0.7971 shares of Glacier stock for each ALTA share § ALTA options will be cashed out based on the in-the-money value (3) § Fixed exchange ratio with collars set between $49.43 and $74.15 Price Protection § Consensus earnings estimates for both companies Earnings Estimates § Total gross credit mark of $34.1 million, or 1.95% ALTA’s gross loan portfolio excluding PPP loans § $31.9 million allocated to non-PCD loans; amortized into earnings over 5 years using the sum-of-the-years- Loan Credit Mark digits accelerated method Estimate § $2.2 million allocated to purchase credit deteriorated (PCD) loans, recorded into ACL § Provision expense of $31.9 million for CECL taken immediately after close; included in pro forma tangible book value § Net fair value write-up of $22.0 million on fixed assets, loans (rate mark) and time deposits Other Fair Value § Core deposit intangible of $10.5 million, or 0.35% of non-time deposits; amortized over 10 years using the sum-of-the- Estimates years digits methodology § Cost savings of 17.5% of ALTA’s non-interest expense base Cost Savings § 80.0% realized in 2022 and 100% thereafter Durbin Impact§ Estimated reduction of ALTA’s interchange income by approximately $2.0 million annually (4) Restructuring Charges§ One-time transaction costs of approximately $33.0 million, pre-tax § $342.9 million at closing Minimum Tangible § Excess capital, net of any adjustments for ALTA’s Final Transaction Related Expenses, to be paid out to ALTA Common Equity shareholders prior to closing Expected Closing§ Fourth Quarter 2021 (1) Based on GBCI closing price of $61.51 as of May 17, 2021 (2) Includes 18,876,639 ALTA shares and 101,128 unvested ALTA RSUs (3) Refer to the Plan and Agreement of Merger for complete terms relating to stock collars and termination rights 9 9 (4) Including employment and benefits plan costs, data processing conversion costs and penalties, and combined professional and advisory fees

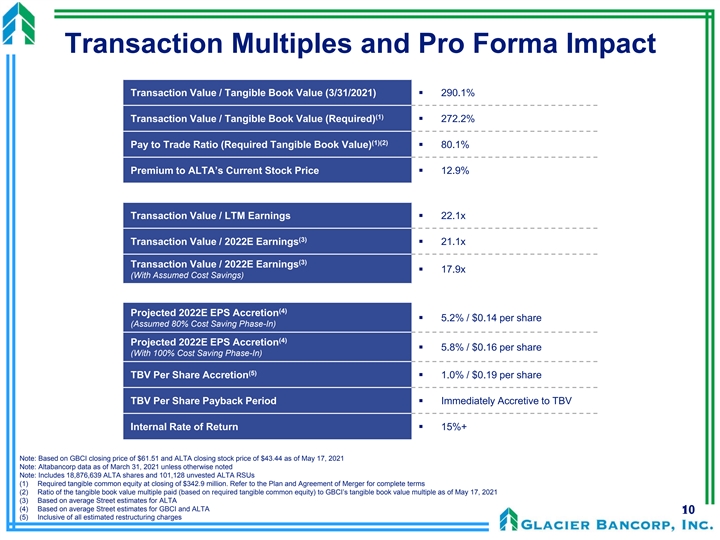

Transaction Multiples and Pro Forma Impact Transaction Value / Tangible Book Value (3/31/2021)§ 290.1% (1) Transaction Value / Tangible Book Value (Required)§ 272.2% (1)(2) Pay to Trade Ratio (Required Tangible Book Value)§ 80.1% Premium to ALTA’s Current Stock Price§ 12.9% Transaction Value / LTM Earnings§ 22.1x (3) Transaction Value / 2022E Earnings§ 21.1x (3) Transaction Value / 2022E Earnings § 17.9x (With Assumed Cost Savings) (4) Projected 2022E EPS Accretion § 5.2% / $0.14 per share (Assumed 80% Cost Saving Phase-In) (4) Projected 2022E EPS Accretion § 5.8% / $0.16 per share (With 100% Cost Saving Phase-In) (5) TBV Per Share Accretion§ 1.0% / $0.19 per share TBV Per Share Payback Period§ Immediately Accretive to TBV Internal Rate of Return§ 15%+ Note: Based on GBCI closing price of $61.51 and ALTA closing stock price of $43.44 as of May 17, 2021 Note: Altabancorp data as of March 31, 2021 unless otherwise noted Note: Includes 18,876,639 ALTA shares and 101,128 unvested ALTA RSUs (1) Required tangible common equity at closing of $342.9 million. Refer to the Plan and Agreement of Merger for complete terms (2) Ratio of the tangible book value multiple paid (based on required tangible common equity) to GBCI’s tangible book value multiple as of May 17, 2021 (3) Based on average Street estimates for ALTA (4) Based on average Street estimates for GBCI and ALTA 10 10 (5) Inclusive of all estimated restructuring chargesTransaction Multiples and Pro Forma Impact Transaction Value / Tangible Book Value (3/31/2021)§ 290.1% (1) Transaction Value / Tangible Book Value (Required)§ 272.2% (1)(2) Pay to Trade Ratio (Required Tangible Book Value)§ 80.1% Premium to ALTA’s Current Stock Price§ 12.9% Transaction Value / LTM Earnings§ 22.1x (3) Transaction Value / 2022E Earnings§ 21.1x (3) Transaction Value / 2022E Earnings § 17.9x (With Assumed Cost Savings) (4) Projected 2022E EPS Accretion § 5.2% / $0.14 per share (Assumed 80% Cost Saving Phase-In) (4) Projected 2022E EPS Accretion § 5.8% / $0.16 per share (With 100% Cost Saving Phase-In) (5) TBV Per Share Accretion§ 1.0% / $0.19 per share TBV Per Share Payback Period§ Immediately Accretive to TBV Internal Rate of Return§ 15%+ Note: Based on GBCI closing price of $61.51 and ALTA closing stock price of $43.44 as of May 17, 2021 Note: Altabancorp data as of March 31, 2021 unless otherwise noted Note: Includes 18,876,639 ALTA shares and 101,128 unvested ALTA RSUs (1) Required tangible common equity at closing of $342.9 million. Refer to the Plan and Agreement of Merger for complete terms (2) Ratio of the tangible book value multiple paid (based on required tangible common equity) to GBCI’s tangible book value multiple as of May 17, 2021 (3) Based on average Street estimates for ALTA (4) Based on average Street estimates for GBCI and ALTA 10 10 (5) Inclusive of all estimated restructuring charges

Concluding Observations Ø Altabancorp acquisition continues Glacier’s tradition of adding high quality community banks that fit the Glacier banking model Ø Pricing metrics, deal structure, and conservative assumptions reflective of Glacier’s consistent, disciplined approach to acquisitions § Immediately accretive to both earnings per share and tangible book value per share § Opportunity for significant revenue enhancement if Altabank’s loan-to-deposit ratio returns to historical levels – not factored into the model Ø Transaction will further enhance Glacier’s long-term track record of creating shareholder value Ø Unique opportunity to partner with the premier Utah community bank th th (1) § Increases Glacier’s deposit market share in Utah from 13 to 6 , with over $3 billion in pro forma deposits § Largest bank transaction in Utah since 2000 Ø Utah is a key growth market in the Glacier footprint § Acquisition builds on Glacier’s existing Utah efforts and creates opportunities for robust future growth and diversification – Utah is the fastest growing state in Glacier’s footprint § Glacier will have a significant presence in every major Utah MSA and have a top 5 market share in the Provo-Orem, Logan and Ogden-Clearfield MSAs Ø Altabancorp management and staff provide Glacier with lending talent, deep market knowledge, and strong customer relationships 11 11 (1) Excludes industrial loan companies (ILCs)Concluding Observations Ø Altabancorp acquisition continues Glacier’s tradition of adding high quality community banks that fit the Glacier banking model Ø Pricing metrics, deal structure, and conservative assumptions reflective of Glacier’s consistent, disciplined approach to acquisitions § Immediately accretive to both earnings per share and tangible book value per share § Opportunity for significant revenue enhancement if Altabank’s loan-to-deposit ratio returns to historical levels – not factored into the model Ø Transaction will further enhance Glacier’s long-term track record of creating shareholder value Ø Unique opportunity to partner with the premier Utah community bank th th (1) § Increases Glacier’s deposit market share in Utah from 13 to 6 , with over $3 billion in pro forma deposits § Largest bank transaction in Utah since 2000 Ø Utah is a key growth market in the Glacier footprint § Acquisition builds on Glacier’s existing Utah efforts and creates opportunities for robust future growth and diversification – Utah is the fastest growing state in Glacier’s footprint § Glacier will have a significant presence in every major Utah MSA and have a top 5 market share in the Provo-Orem, Logan and Ogden-Clearfield MSAs Ø Altabancorp management and staff provide Glacier with lending talent, deep market knowledge, and strong customer relationships 11 11 (1) Excludes industrial loan companies (ILCs)

Appendix 12 12Appendix 12 12

Comprehensive Due Diligence Process Ø Completed a coordinated comprehensive due diligence review with executives from GBCI and ALTA, along with advisors and consultants Ø Conducted detailed diligence calls with ALTA management to evaluate each focus area Ø Engaged consultants to complete enhanced loan review, compliance review and IT systems analysis Loan Review Process Diligence Focus Areas Asset Quality Commercial Lending Comprehensive Loan Review Analysis üü Consumer Lending Mortgage üü 1,063 $1.4 Billion Financial and Financial Reporting üü Individual loans reviewed Total loan balance reviewed Accounting and Analysis Compliance Operations üü Ø 539 credit relationships Ø 74% of total commercial loans Information Systems üü Technology Ø 60% of total loans Product Treasury Ø 100% of credits over $2 million üü Management Ø 100% of commercial loans over $1.5 million Human Resources Data Warehouse üü Ø 100% of COVID sensitive commercial loans (hotel, restaurant, travel/tourism, oil/gas, gaming) 13 13Comprehensive Due Diligence Process Ø Completed a coordinated comprehensive due diligence review with executives from GBCI and ALTA, along with advisors and consultants Ø Conducted detailed diligence calls with ALTA management to evaluate each focus area Ø Engaged consultants to complete enhanced loan review, compliance review and IT systems analysis Loan Review Process Diligence Focus Areas Asset Quality Commercial Lending Comprehensive Loan Review Analysis üü Consumer Lending Mortgage üü 1,063 $1.4 Billion Financial and Financial Reporting üü Individual loans reviewed Total loan balance reviewed Accounting and Analysis Compliance Operations üü Ø 539 credit relationships Ø 74% of total commercial loans Information Systems üü Technology Ø 60% of total loans Product Treasury Ø 100% of credits over $2 million üü Management Ø 100% of commercial loans over $1.5 million Human Resources Data Warehouse üü Ø 100% of COVID sensitive commercial loans (hotel, restaurant, travel/tourism, oil/gas, gaming) 13 13

Geographic Loan Diversification Ø Altabancorp acquisition continues to further geographically diversify Glacier’s loan portfolio Pro Forma with ALTA 12/31/2009 3/31/2021 3/31/2021 Utah Utah Idaho 17% Idaho 4% 15% Washington 13% 7% Montana Washington 62% 6% Idaho Wyoming 22% 8% Wyoming 7% Utah Colorado Montana Montana 2% 11% Colorado 39% 34% 10% Washington 1% Arizona Arizona 10% 8% Wyoming Colorado Nevada 9% Nevada 4% 6% 6% 14 14 Source: Company information as of the quarter ended 3/31/2021 Loan Geography Gross LoansGeographic Loan Diversification Ø Altabancorp acquisition continues to further geographically diversify Glacier’s loan portfolio Pro Forma with ALTA 12/31/2009 3/31/2021 3/31/2021 Utah Utah Idaho 17% Idaho 4% 15% Washington 13% 7% Montana Washington 62% 6% Idaho Wyoming 22% 8% Wyoming 7% Utah Colorado Montana Montana 2% 11% Colorado 39% 34% 10% Washington 1% Arizona Arizona 10% 8% Wyoming Colorado Nevada 9% Nevada 4% 6% 6% 14 14 Source: Company information as of the quarter ended 3/31/2021 Loan Geography Gross Loans

GBCI Acquisition History Ø ALTA continues Glacier’s tradition of adding high quality community banks that fit the Glacier banking model Total TBV/ Non-Acquired Assets Acquired Assets TBV/Share Assets ($BN) Share $23.3 $24 $20.00 $18.21 $15.61 $20 $18.5 $16.00 $13.93 $12.91 $12.51 $16 $12.11 $11.83 $13.7 $11.08 $10.96 $12.00 $12.1 $12 $9.7 $9.5 $9.1 $8.3 $8.00 $7.9 $7.7 $8 $4.00 $4 $- $- 2012 2013 2014 2015 2016 2017 2018 2019 2020 Pro Forma with ALTA May 2013 August 2014 February 2015 August 2016 April 2017 January 2018 April 2019 February 2020 $300.5 MM $349.2 MM $175.8 MM $76.2 MM $385.8 MM $551.2 MM $379.2 MM $745.4 MM $3,521.8 MM Assets Assets Assets Assets Assets Assets Assets Assets Assets July 2013 October 2015 February 2018 July 2019 $330.0 MM $270.1 MM $1,109.7 MM $977.9 MM Assets Assets Assets Assets 15 15 Source: S&P Global Market Intelligence, assets for target company based on date of deal completionGBCI Acquisition History Ø ALTA continues Glacier’s tradition of adding high quality community banks that fit the Glacier banking model Total TBV/ Non-Acquired Assets Acquired Assets TBV/Share Assets ($BN) Share $23.3 $24 $20.00 $18.21 $15.61 $20 $18.5 $16.00 $13.93 $12.91 $12.51 $16 $12.11 $11.83 $13.7 $11.08 $10.96 $12.00 $12.1 $12 $9.7 $9.5 $9.1 $8.3 $8.00 $7.9 $7.7 $8 $4.00 $4 $- $- 2012 2013 2014 2015 2016 2017 2018 2019 2020 Pro Forma with ALTA May 2013 August 2014 February 2015 August 2016 April 2017 January 2018 April 2019 February 2020 $300.5 MM $349.2 MM $175.8 MM $76.2 MM $385.8 MM $551.2 MM $379.2 MM $745.4 MM $3,521.8 MM Assets Assets Assets Assets Assets Assets Assets Assets Assets July 2013 October 2015 February 2018 July 2019 $330.0 MM $270.1 MM $1,109.7 MM $977.9 MM Assets Assets Assets Assets 15 15 Source: S&P Global Market Intelligence, assets for target company based on date of deal completion

Expanding in Leading Markets Ø GBCI is strategically positioned with a combined presence in 15 of the top 30 fastest growing MSAs in the Top 30 Fastest Growing MSAs – Western U.S. (1) Western U.S. 2 20 02 11 0 - - 2 20 02 26 1 P Pr ro o Ø ALTA acquisition adds three high-growth markets to the M Mk kt t.. P Pop roj ul ea ct te ion d G GB BC CII A AL LT TA A F Fo or rm ma a GBCI footprint and an enhanced presence in the Ogden R Ra an nk k M MS SA A Cha Cha ng ng e e (%) M Mk ktt.. M Mk ktt.. M Mk ktt.. and Salt Lake MSAs 1 1 S Stt.. G Ge eo or rg ge e,, U UT T 3 34 4..3 3% 3 --üüüü 2 Bozeman, MT 32.91ü -ü 2 Bozeman, MT 32.9%ü -ü 3 3 G Gr re ee elle ey y,, C CO O 33 22 .6 .6 % -- -- -- Ø Utah accounts for four of the top ten fastest growing 4 4 H He eb be er r,, U UT T 3 30 0..4 4% 1üü --üü 5 Bend, OR 28.5 - - - MSAs in the Western U.S. 5 Bend, OR 28.5% - - - 6 6 P Pr ro ov vo o- -O Or re em m,, U UT T 2 27 7..9 8% 9 --üüüü 7 7 B Bo oiis se e C Ciitty y,, IID D 2 25 5..7 7% 1üü --üü 8 Coeur d'Alene, ID 23.65ü -ü 8 Coeur d'Alene, ID 23.7%ü -ü 9 9 C Ce ed da ar r C Ciitty y,, U UT T 2 23 3..3 3% 3 -- -- -- 10 10 Fo For rtt C Co olllliin ns s,, C CO O 2 21 1..9 9% 4 -- -- -- 11 Phoenix-Mesa-Chandler, AZ 21.2ü -ü 11 Phoenix-Mesa-Chandler, AZ 21.2%ü -ü 12 12 K Ke en nn ne ew wiic ck k- -R Riic ch hlla an nd d,, W WA A 2 21 1..1 0% 5 -- -- -- 13 Ellensburg, WA 19.4 - - - 13 Ellensburg, WA 19.4% - - - 14 Las Vegas-Henderson-Paradise, NV 19.29 - - - 14 Las Vegas-Henderson-Paradise, NV 19.3% - - - 15 15 D De en nv ve er r- -A Au ur ro or ra a- -L La ak ke ew wo oo od d,, C CO O 1 19 9..1 1% 4üü --üü 16 Colorado Springs, CO 18.11ü -ü 16 Colorado Springs, CO 18.1%ü -ü 17 Prineville, OR 18.05 - - - 17 Prineville, OR 18.1% - - - 18 18 S Se ea attt tlle e- -T Ta ac co om ma a- -B Be elllle ev vu ue e,, W WA A 1 18 8..0 0% 4 -- -- -- 19 Olympia-Lacey-Tumwater, WA 17.58 - - - 19 Olympia-Lacey-Tumwater, WA 17.6% - - - 20 20 K Ka alliis sp pe ellll,, M MT T 1 17 7..0 0% 3üü --üü 21 21 IId da ah ho o Fa Falllls s,, IID D 1 16 6..6 5% 9üü --üü 22 Ogden-Clearfield, UT 16.56üüü 22 Ogden-Clearfield, UT 16.6%üüü 23 23 L Lo og ga an n,, U UT T- -IID D 1 16 6..5 5% 2 --üüüü 24 Bellingham, WA 16.26 - - - 24 Bellingham, WA 16.3% - - - 25 Jackson, WY-ID 15.44 - - - 25 Jackson, WY-ID 15.4% - - - 26 26 S Sa an nd dp po oiin ntt,, IID D 1 15 5..1 0% 7üü --üü 27 Salt Lake City, UT 15.03üüü 27 Salt Lake City, UT 15.0%üüü 28 Portland-Vancouver-Hillsboro, OR-WA 14.13 - - - 28 Portland-Vancouver-Hillsboro, OR-WA 14.1% - - - 29 29 P Pu ullllm ma an n,, W WA A 1 14 4..1 0% 8 -- -- -- GBCI MSA 30 Twin Falls, ID 13.7 - - - 30 Twin Falls, ID 13.7% - - - ALTA MSA Total Top 30 MSAs 12 5 15 Total Top 30 MSAs 12 5 15 Top 30 MSA Source: S&P Global Market Intelligence Note: Western U.S. states include AK, AZ, CA, CO, HI, ID, MT, NV, NM, OR, UT, WA, WY 16 16 (1) Based on 2010-2021 population growthExpanding in Leading Markets Ø GBCI is strategically positioned with a combined presence in 15 of the top 30 fastest growing MSAs in the Top 30 Fastest Growing MSAs – Western U.S. (1) Western U.S. 2 20 02 11 0 - - 2 20 02 26 1 P Pr ro o Ø ALTA acquisition adds three high-growth markets to the M Mk kt t.. P Pop roj ul ea ct te ion d G GB BC CII A AL LT TA A F Fo or rm ma a GBCI footprint and an enhanced presence in the Ogden R Ra an nk k M MS SA A Cha Cha ng ng e e (%) M Mk ktt.. M Mk ktt.. M Mk ktt.. and Salt Lake MSAs 1 1 S Stt.. G Ge eo or rg ge e,, U UT T 3 34 4..3 3% 3 --üüüü 2 Bozeman, MT 32.91ü -ü 2 Bozeman, MT 32.9%ü -ü 3 3 G Gr re ee elle ey y,, C CO O 33 22 .6 .6 % -- -- -- Ø Utah accounts for four of the top ten fastest growing 4 4 H He eb be er r,, U UT T 3 30 0..4 4% 1üü --üü 5 Bend, OR 28.5 - - - MSAs in the Western U.S. 5 Bend, OR 28.5% - - - 6 6 P Pr ro ov vo o- -O Or re em m,, U UT T 2 27 7..9 8% 9 --üüüü 7 7 B Bo oiis se e C Ciitty y,, IID D 2 25 5..7 7% 1üü --üü 8 Coeur d'Alene, ID 23.65ü -ü 8 Coeur d'Alene, ID 23.7%ü -ü 9 9 C Ce ed da ar r C Ciitty y,, U UT T 2 23 3..3 3% 3 -- -- -- 10 10 Fo For rtt C Co olllliin ns s,, C CO O 2 21 1..9 9% 4 -- -- -- 11 Phoenix-Mesa-Chandler, AZ 21.2ü -ü 11 Phoenix-Mesa-Chandler, AZ 21.2%ü -ü 12 12 K Ke en nn ne ew wiic ck k- -R Riic ch hlla an nd d,, W WA A 2 21 1..1 0% 5 -- -- -- 13 Ellensburg, WA 19.4 - - - 13 Ellensburg, WA 19.4% - - - 14 Las Vegas-Henderson-Paradise, NV 19.29 - - - 14 Las Vegas-Henderson-Paradise, NV 19.3% - - - 15 15 D De en nv ve er r- -A Au ur ro or ra a- -L La ak ke ew wo oo od d,, C CO O 1 19 9..1 1% 4üü --üü 16 Colorado Springs, CO 18.11ü -ü 16 Colorado Springs, CO 18.1%ü -ü 17 Prineville, OR 18.05 - - - 17 Prineville, OR 18.1% - - - 18 18 S Se ea attt tlle e- -T Ta ac co om ma a- -B Be elllle ev vu ue e,, W WA A 1 18 8..0 0% 4 -- -- -- 19 Olympia-Lacey-Tumwater, WA 17.58 - - - 19 Olympia-Lacey-Tumwater, WA 17.6% - - - 20 20 K Ka alliis sp pe ellll,, M MT T 1 17 7..0 0% 3üü --üü 21 21 IId da ah ho o Fa Falllls s,, IID D 1 16 6..6 5% 9üü --üü 22 Ogden-Clearfield, UT 16.56üüü 22 Ogden-Clearfield, UT 16.6%üüü 23 23 L Lo og ga an n,, U UT T- -IID D 1 16 6..5 5% 2 --üüüü 24 Bellingham, WA 16.26 - - - 24 Bellingham, WA 16.3% - - - 25 Jackson, WY-ID 15.44 - - - 25 Jackson, WY-ID 15.4% - - - 26 26 S Sa an nd dp po oiin ntt,, IID D 1 15 5..1 0% 7üü --üü 27 Salt Lake City, UT 15.03üüü 27 Salt Lake City, UT 15.0%üüü 28 Portland-Vancouver-Hillsboro, OR-WA 14.13 - - - 28 Portland-Vancouver-Hillsboro, OR-WA 14.1% - - - 29 29 P Pu ullllm ma an n,, W WA A 1 14 4..1 0% 8 -- -- -- GBCI MSA 30 Twin Falls, ID 13.7 - - - 30 Twin Falls, ID 13.7% - - - ALTA MSA Total Top 30 MSAs 12 5 15 Total Top 30 MSAs 12 5 15 Top 30 MSA Source: S&P Global Market Intelligence Note: Western U.S. states include AK, AZ, CA, CO, HI, ID, MT, NV, NM, OR, UT, WA, WY 16 16 (1) Based on 2010-2021 population growth

Important Information and Where You Can Find It In connection with the proposed transaction, Glacier will file with the SEC a registration statement on Form S-4 to register the shares of Glacier’s capital stock to be issued in connection with the proposed transaction. The registration statement will include a proxy statement of ALTA and a prospectus of Glacier, which will be sent to the shareholders of ALTA seeking their approval of the proposed transaction. This release does not constitute an offer to sell or a solicitation of an offer to buy any securities or a solicitation of any vote or approval. INVESTORS AND SHAREHOLDERS OF GLACIER AND ALTA AND THEIR RESPECTIVE AFFILIATES ARE URGED TO READ, WHEN AVAILABLE, THE REGISTRATION STATEMENT ON FORM S-4, THE PROXY STATEMENT/PROSPECTUS TO BE INCLUDED WITHIN THE REGISTRATION STATEMENT ON FORM S-4 AND ANY OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED TRANSACTION, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT GLACIER, ALTA AND THE PROPOSED TRANSACTION. Investors will be able to obtain a free copy of the registration statement, including the proxy statement/prospectus, as well as other relevant documents filed with the SEC containing information about Glacier and ALTA, without charge, at the SEC's website (http://www.sec.gov). Copies of the registration statement, including the proxy statement/prospectus, and the filings with the SEC that will be incorporated by reference in the proxy statement/prospectus can also be obtained, without charge, by directing a request to Glacier Bancorp, 49 Commons Loop, Kalispell, Montana 59901; Telephone (406) 751-7706, or Altabancorp, 1 East Main Street, American Fork, Utah 84003; Telephone (801) 642-3998. Glacier, ALTA and certain of their respective directors, executive officers and employees may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction under the rules of the SEC. Information regarding Glacier’s directors and executive officers is available in its definitive proxy statement, which was filed with the SEC on March 16, 2021, and certain of its Current Reports on Form 8-K. Information regarding ALTA’s directors and executive officers is available in an amendment to its Annual Report on Form 10-K/A, which was filed with the SEC on April 29, 2021, and certain of its Current Reports on Form 8-K. Other information regarding the participants in the solicitation of proxies in respect of the proposed transaction and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the proxy statement/prospectus and other relevant materials to be filed with the SEC. Free copies of these documents, when available, may be obtained as described in the preceding paragraph. 17 17Important Information and Where You Can Find It In connection with the proposed transaction, Glacier will file with the SEC a registration statement on Form S-4 to register the shares of Glacier’s capital stock to be issued in connection with the proposed transaction. The registration statement will include a proxy statement of ALTA and a prospectus of Glacier, which will be sent to the shareholders of ALTA seeking their approval of the proposed transaction. This release does not constitute an offer to sell or a solicitation of an offer to buy any securities or a solicitation of any vote or approval. INVESTORS AND SHAREHOLDERS OF GLACIER AND ALTA AND THEIR RESPECTIVE AFFILIATES ARE URGED TO READ, WHEN AVAILABLE, THE REGISTRATION STATEMENT ON FORM S-4, THE PROXY STATEMENT/PROSPECTUS TO BE INCLUDED WITHIN THE REGISTRATION STATEMENT ON FORM S-4 AND ANY OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED TRANSACTION, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT GLACIER, ALTA AND THE PROPOSED TRANSACTION. Investors will be able to obtain a free copy of the registration statement, including the proxy statement/prospectus, as well as other relevant documents filed with the SEC containing information about Glacier and ALTA, without charge, at the SEC's website (http://www.sec.gov). Copies of the registration statement, including the proxy statement/prospectus, and the filings with the SEC that will be incorporated by reference in the proxy statement/prospectus can also be obtained, without charge, by directing a request to Glacier Bancorp, 49 Commons Loop, Kalispell, Montana 59901; Telephone (406) 751-7706, or Altabancorp, 1 East Main Street, American Fork, Utah 84003; Telephone (801) 642-3998. Glacier, ALTA and certain of their respective directors, executive officers and employees may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction under the rules of the SEC. Information regarding Glacier’s directors and executive officers is available in its definitive proxy statement, which was filed with the SEC on March 16, 2021, and certain of its Current Reports on Form 8-K. Information regarding ALTA’s directors and executive officers is available in an amendment to its Annual Report on Form 10-K/A, which was filed with the SEC on April 29, 2021, and certain of its Current Reports on Form 8-K. Other information regarding the participants in the solicitation of proxies in respect of the proposed transaction and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the proxy statement/prospectus and other relevant materials to be filed with the SEC. Free copies of these documents, when available, may be obtained as described in the preceding paragraph. 17 17