Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - Arconic Corp | a52422293ex99_1.htm |

| 8-K - ARCONIC CORPORATION 8-K - Arconic Corp | a52422293.htm |

Exhibit 99.2

First Quarter 2021 Earnings Call Tim Myers – Chief Executive OfficerErick Asmussen – Chief Financial

Officer May 4, 2021

Important Information 2 Forward-Looking Statements This presentation contains statements that relate

to future events and expectations and, as such, constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include those containing such words as "anticipates,"

"believes," "could," "estimates," "expects," "forecasts," "goal," "guidance," "intends," "may," "outlook," "plans," "projects," "seeks," "sees," "should," "targets," "will," "would," or other words of similar meaning. All statements that

reflect Arconic’s expectations, assumptions, projections, beliefs or opinions about the future, other than statements of historical fact, are forward-looking statements, including, without limitation, statements, relating to the condition of

the ground transportation, aerospace, building and construction, industrial, packaging and other end markets; Arconic’s future financial results, operating performance, working capital, cash flows, liquidity and financial position; cost savings

and restructuring programs; Arconic's strategies, outlook, business and financial prospects; costs associated with pension and other post-retirement benefit plans; projected sources of cash flow; potential legal liability; the potential impact

of the COVID-19 pandemic; and actions to mitigate the impact of COVID-19. These statements reflect beliefs and assumptions that are based on Arconic’s perception of historical trends, current conditions and expected future developments, as well

as other factors Arconic believes are appropriate in the circumstances. Forward-looking statements are not guarantees of future performance, and actual results may differ materially from those indicated by these forward-looking statements due

to a variety of risks, uncertainties and changes in circumstances, many of which are beyond Arconic’s control. Such risks and uncertainties include, but are not limited to: (a) continuing uncertainty regarding the duration and impact of the

COVID-19 pandemic on our business and the businesses of our customers and suppliers; (b) deterioration in global economic and financial market conditions generally; (c) unfavorable changes in the end markets we serve; (d) the inability to

achieve the level of revenue growth, cash generation, cost savings, benefits of our management of legacy liabilities, improvement in profitability and margins, fiscal discipline, or strengthening of competitiveness and operations anticipated or

targeted; (e) adverse changes in discount rates or investment returns on pension assets; (f) competition from new product offerings, disruptive technologies, industry consolidation or other developments; (g) the loss of significant customers or

adverse changes in customers’ business or financial condition; (h) manufacturing difficulties or other issues that impact product performance, quality or safety; (i) the impact of pricing volatility in raw materials; (j) a significant downturn

in the business or financial condition of a key supplier or other supply chain disruptions; (k) challenges to or infringements on our intellectual property rights; (l) the inability to successfully implement our re-entry into the packaging

market or to realize the expected benefits of other strategic initiatives or projects; (m) the impact of potential cyber attacks and information technology or data security breaches; (n) geopolitical, economic, and regulatory risks relating to

our global operations, including compliance with U.S. and foreign trade and tax laws, sanctions, embargoes and other regulations; (o) the outcome of contingencies, including legal proceedings, government or regulatory investigations, and

environmental remediation and compliance matters; and (p) the other risk factors summarized in Arconic’s Form 10-K for the year ended December 31, 2020 and other reports filed with the U.S. Securities and Exchange Commission. The above list of

factors is not exhaustive or necessarily in order of importance. Market projections are subject to the risks discussed above and other risks in the market. The statements in this presentation are made as of the date of this presentation, even

if subsequently made available by Arconic on its website or otherwise. Arconic disclaims any intention or obligation to update publicly any forward-looking statements, whether in response to new information, future events, or otherwise, except

as required by applicable law.

Important Information (cont’d) 3 Non-GAAP Financial MeasuresSome of the information included in this

presentation is derived from Arconic’s consolidated financial information but is not presented in Arconic’s financial statements prepared in accordance with accounting principles generally accepted in the United States of America (GAAP).

Certain of these financial measures are considered “non-GAAP financial measures” under SEC rules. These non-GAAP financial measures supplement our GAAP disclosures and should not be considered an alternative to any measure of performance or

financial condition as determined in accordance with GAAP, and investors should consider Arconic’s performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial

condition of Arconic. Non-GAAP financial measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the results or financial condition as reported under GAAP. Non-GAAP

financial measures presented by Arconic may not be comparable to non-GAAP financial measures presented by other companies. Reconciliations to the most directly comparable GAAP financial measures and management’s rationale for the use of the

non-GAAP financial measures can be found in the appendix to this presentation. Arconic has not provided reconciliations of any forward-looking non-GAAP financial measures, such as adjusted EBITDA and free cash flow, to the most directly

comparable GAAP financial measures because such reconciliations are not available without unreasonable efforts due to the variability and complexity with respect to the charges and other components excluded from the non-GAAP measures, such as

the effects of metal price lag, foreign currency movements, gains or losses on sales of assets, taxes, and any future restructuring or impairment charges. These reconciling items are in addition to the inherent variability already included in

the GAAP measures, which includes, but is not limited to, price/mix and volume. Arconic believes such reconciliations would imply a degree of precision that would be confusing or misleading to investors.Other InformationEffective July 1, 2020,

the Company changed its inventory cost method to average cost for all U.S. inventories previously carried at last-in, first-out (LIFO) cost. The effects of the change in accounting principle from LIFO to average cost have been retrospectively

applied to all prior periods presented. See the Company’s Form 10-K for the year ended December 31, 2020 and Form 10-Q for the three months ended March 31, 2021 for further information.

1Q 2021 Strong Operating Performance and Contract Wins Set Foundation for Growth Rebounding Marketsand

Growing Profitability Industrial revenue grew 18% year over year, 15% organically, bolstered by U.S. trade caseGround transportation revenue grew 25% year over year, 17% organically, despite 4% North American automotive production

declineMaintained $100 million in structural cost outs and footprint right-sizing1Q 2021 Net Income was $52 million and Adjusted EBITDA was $179 million, a 19% sequential increase, or $28 million Contract Wins and End Market Trends Support

Durable Growth Negotiated agreements for $1.5 billion in packaging revenue from multiple customersSecured long-term contracts representing more than $2 billion in aerospace revenueSustainability trends support long-term growth in ground

transportation, packaging, and building and construction end markets Improving Cash Conversion and Financial Profile Cash payments on legacy obligations expected to decrease by more than $230 million in 2022 and beyondReduced ~$1.8 billion,

or 35%, of gross pension and OPEB obligations over the last 12 months and reduced net after tax liability by ~$0.7 billion, or 47%$300 million share repurchase authorization 4 See appendix for non-GAAP financial measure reconciliations.

1Q 2021 Sales Increase Sequentially Across All End Markets 1Q 2021 Organic Revenueby End Market End

Market Revenue year- over-year change Organic revenue year-over-year change Revenue sequential change Ground Transportation 25% 17% 21% Industrial Products and Other 18% 15% 22% Building and

Construction (1%) (6%) 3% Packaging 23% 16% 8% Aerospace (54%) (55%) 5% Ground TransportationSequential automotive sales increased following the Ford F-150 model changeover and improved U.S. truck and trailer demandYear-over-year

sales increased due to the continued market rebound in commercial transportation and production on 11 new or greatly expanded auto programs versus last yearIndustrial Products and OtherRamp up of Tennessee investment bolstered by trade case

driving stronger demand in the U.S.Building and ConstructionOngoing pandemic-related softness in North American non-residential construction marketsPackagingSales benefited from increased demand and non-compete expirationAerospaceAerospace

industry continues to de-stock the supply chain In 2019, Aerospace made up 18% of total revenue See appendix for non-GAAP financial measure reconciliations. 5

1Q 2021 Financial Highlights Sales of $1.7 billion, up 4% year-over-year, up 15% from prior quarter, and

down 1% organically year-over-yearNet income of $52 million, or $0.46 per share, compared with $46 million, or $0.42 per share, in first quarter 2020Adjusted EBITDA of $179 million (10.7% margin), down 12% year-over-year, and up 19% or $28

million from the prior quarterCash used for operations was $294 million, reflecting $200 million of accelerated U.S. pension contributions made in January 2021, and capital expenditures were $28 millionIssued $300 million aggregate principal

amount of the Company’s 6.125% Senior Secured Second-Lien Notes due 2028 and used $250 million for pension contribution to complete approximately $1 billion partial annuitization of U.S. pension obligationsQuarter-end cash balance was $763

million with total available liquidity of approximately $1.6 billion and gross debt was $1.6 billion Adjusted EBITDA 1Q 2020 – 1Q 2021 ($M) Approximately 90% recovery to pre-pandemic EBITDA levels despite aerospace revenue down 55%

organically versus prior year 6 See appendix for non-GAAP financial measure reconciliations.

1Q 2021 Revenue and EBITDA Revenue Adjusted EBITDA $M Year-over-Year % $M Year-over-Year

% 1Q 2020 $1,611 $204 Price 5 0% 5 2% Volume/Mix (20) (1%) (41) (20%) Net Savings - - 23 11% Divestitures (19) (1%) (2) (1%) Aluminum Price 89 6% (1) - FX/Other 9 - (9) (4%) 1Q

2021 $1,675 4% $179 (12%) 7 See appendix for non-GAAP financial measure reconciliations.

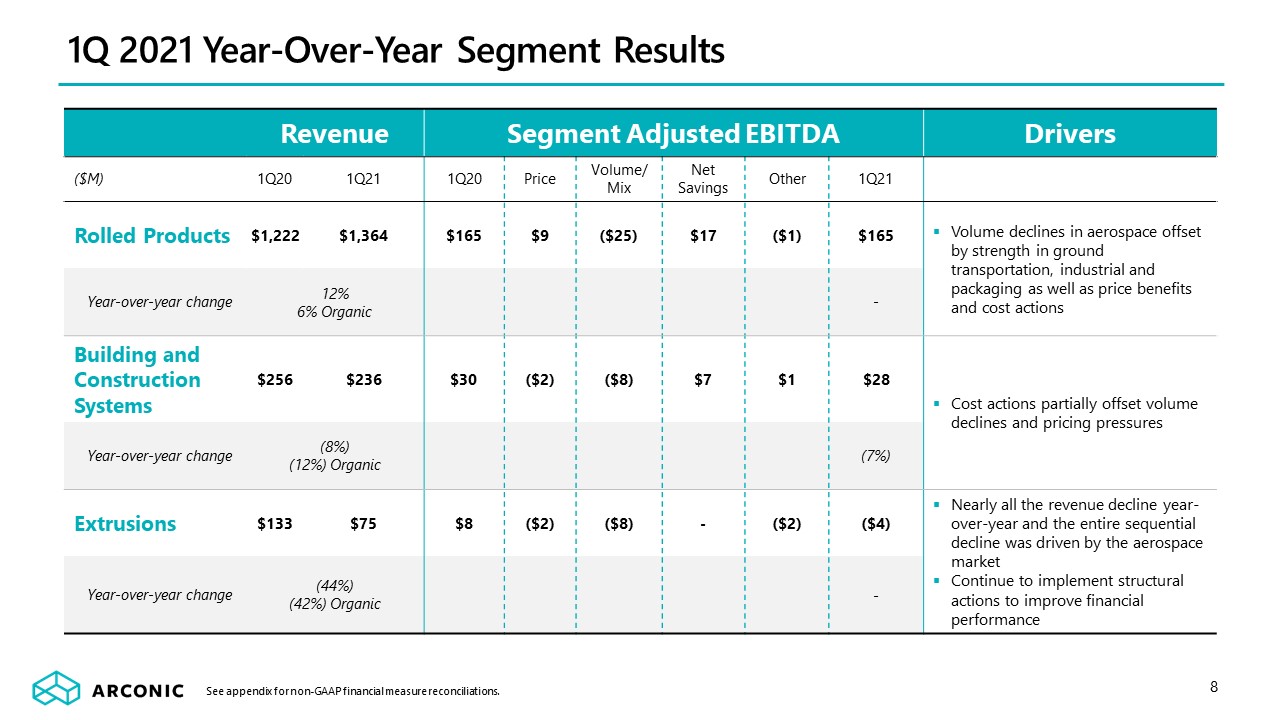

1Q 2021 Year-Over-Year Segment Results Revenue Segment Adjusted

EBITDA Drivers ($M) 1Q20 1Q21 1Q20 Price Volume/Mix Net Savings Other 1Q21 Rolled Products $1,222 $1,364 $165 $9 ($25) $17 ($1) $165 Volume declines in aerospace offset by strength in ground transportation,

industrial and packaging as well as price benefits and cost actions Year-over-year change 12%6% Organic - Building and Construction Systems $256 $236 $30 ($2) ($8) $7 $1 $28 Cost actions partially offset volume

declines and pricing pressures Year-over-year change (8%)(12%) Organic (7%) Extrusions $133 $75 $8 ($2) ($8) - ($2) ($4) Nearly all the revenue decline year-over-year and the entire sequential decline was driven

by the aerospace marketContinue to implement structural actions to improve financial performance Year-over-year change (44%)(42%) Organic - 8 See appendix for non-GAAP financial measure reconciliations.

Ground TransportationOrganic revenue growth of ~25-35% year-over-year due to strong automotive consumer

demand, new content wins, and commercial transportation recovery more than offsetting current semiconductor supply issues Industrial Products and OtherOrganic revenue growth of ~20-25% (previously ~15-20%) year-over-year, with the

Tennessee investment and impact of the U.S. trade action on 16 countries (~77% of global supply) driving North America growthEurope and Russia are benefitting from robust demand and regional trade actions targeting China Building and

ConstructionOrganic revenue expected to be roughly flat year-over-yearNorth American non-residential construction markets down year-over-year offset by modest year-over-year growth in Europe and rolled products PackagingOrganic revenue

growth of ~10-15% (previously flat or modest growth) as demand remains robust particularly in markets served by Chinese packaging assetsNorth American production impact expected in 2022 AerospaceOrganic revenue expected to be down ~25-30%

year-over-year as the industry works through supply chain surplus1H21 expected to remain depressed, with recovery expected later in the year and 2H21 expected to grow over 2H20 FY 2021 Organic Revenue Outlook by End Market FY

2021 Organic RevenueYear-over-Year Trajectory FY 2021 Outlook Compared to Prior Guidance 9

Poised for Substantial and Sustainable Growth

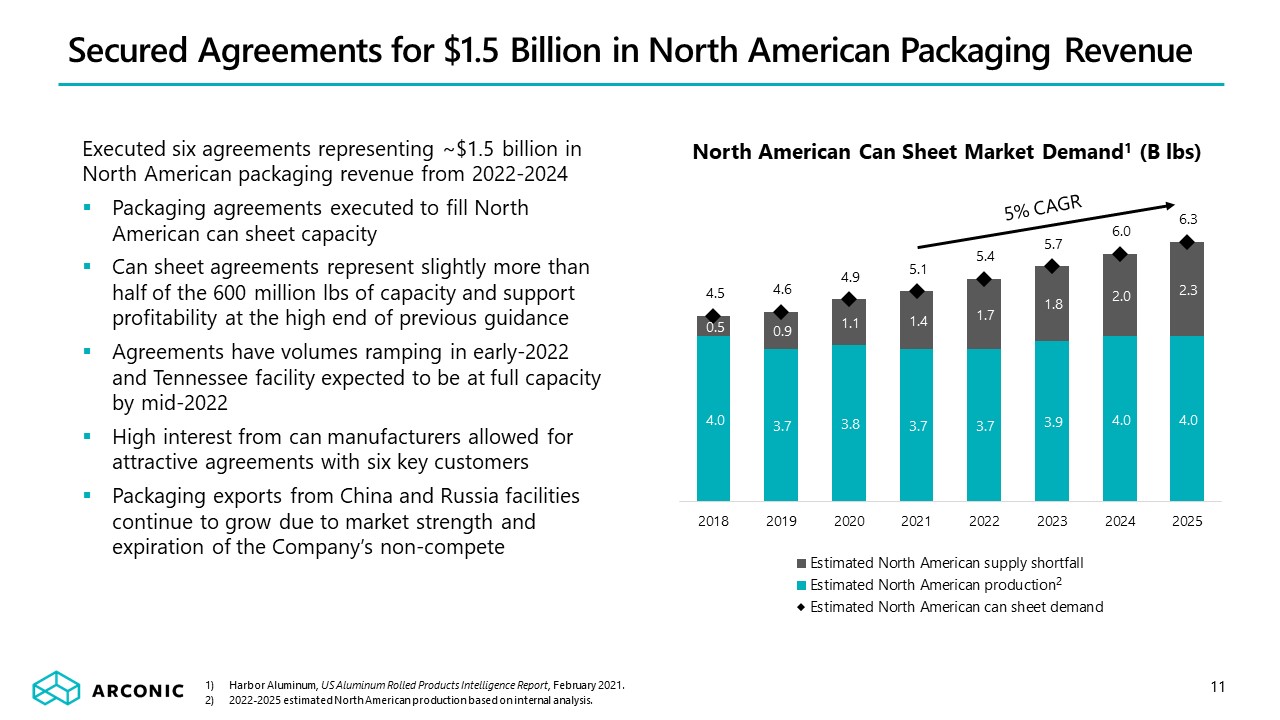

Secured Agreements for $1.5 Billion in North American Packaging Revenue Harbor Aluminum, US Aluminum

Rolled Products Intelligence Report, February 2021.2022-2025 estimated North American production based on internal analysis. Executed six agreements representing ~$1.5 billion in North American packaging revenue from 2022-2024Packaging

agreements executed to fill North American can sheet capacityCan sheet agreements represent slightly more than half of the 600 million lbs of capacity and support profitability at the high end of previous guidanceAgreements have volumes ramping

in early-2022 and Tennessee facility expected to be at full capacity by mid-2022High interest from can manufacturers allowed for attractive agreements with six key customersPackaging exports from China and Russia facilities continue to grow due

to market strength and expiration of the Company’s non-compete North American Can Sheet Market Demand1 (B lbs) 5% CAGR 2 11

Secured Long-Term Contracts for $2+ Billion in Aerospace Revenue Secured long-term contracts

representing more than $2 billion in aerospace revenue Extended long-term contracts with Boeing, Spirit AeroSystems and GulfstreamContracts collectively improve price, mix, share, volume, and durationTerms of contracts give renewed confidence

in the long-term role of the Company’s aerospace product portfolioAerospace revenues believed to have bottomed in 4Q 2020Expect aerospace recovery to 2019 levels in 2023 or 2024 Arconic Aerospace Revenue ($M) 12

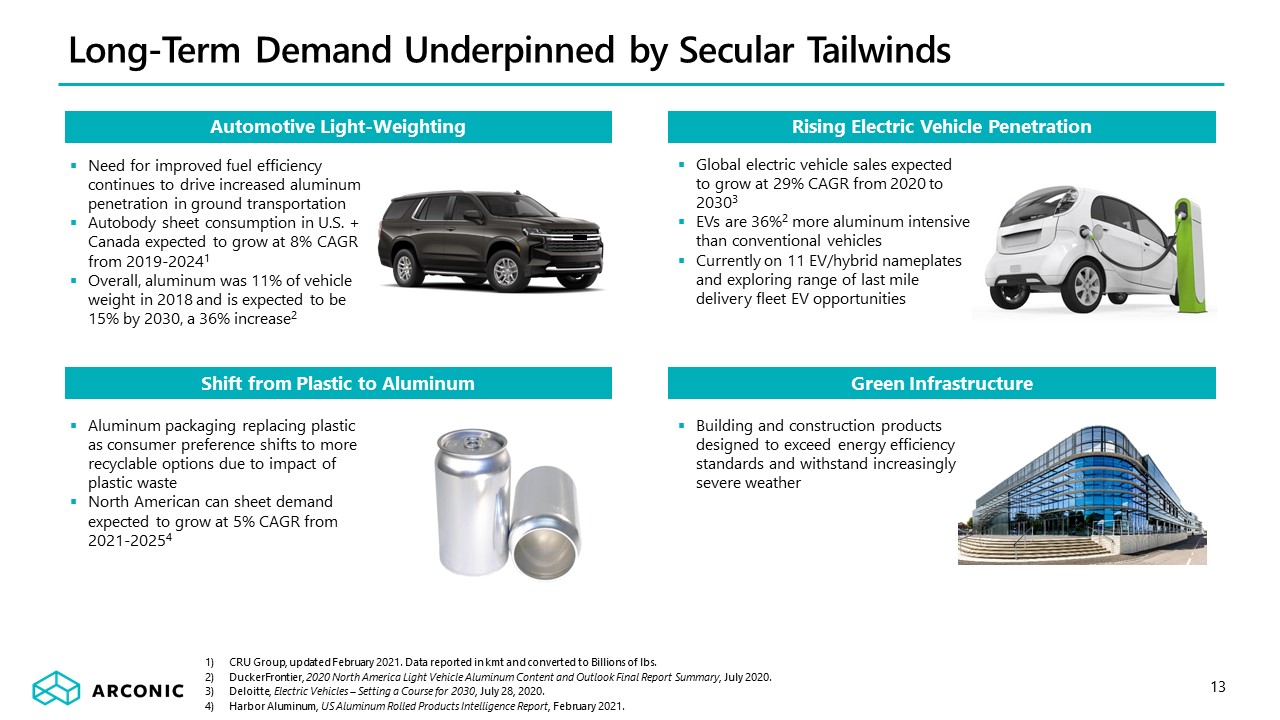

Long-Term Demand Underpinned by Secular Tailwinds CRU Group, updated February 2021. Data reported in kmt

and converted to Billions of lbs.DuckerFrontier, 2020 North America Light Vehicle Aluminum Content and Outlook Final Report Summary, July 2020.Deloitte, Electric Vehicles – Setting a Course for 2030, July 28, 2020.Harbor Aluminum, US Aluminum

Rolled Products Intelligence Report, February 2021. Aluminum packaging replacing plastic as consumer preference shifts to more recyclable options due to impact of plastic wasteNorth American can sheet demand expected to grow at 5% CAGR from

2021-20254 Need for improved fuel efficiency continues to drive increased aluminum penetration in ground transportationAutobody sheet consumption in U.S. + Canada expected to grow at 8% CAGR from 2019-20241Overall, aluminum was 11% of vehicle

weight in 2018 and is expected to be 15% by 2030, a 36% increase2 Building and construction products designed to exceed energy efficiency standards and withstand increasingly severe weather Global electric vehicle sales expected to grow at

29% CAGR from 2020 to 20303EVs are 36%2 more aluminum intensive than conventional vehiclesCurrently on 11 EV/hybrid nameplates and exploring range of last mile delivery fleet EV opportunities Automotive Light-Weighting Rising Electric

Vehicle Penetration Shift from Plastic to Aluminum Green Infrastructure 13

Delivering on Environmental, Social, and Governance (ESG) TRIR or Total Recordable Incident Rate =

(Number of OSHA Recordable injuries and illnesses * 200,000) / Employee total hours worked.Industry average based on internal analysis comprised of TRIR from companies associated with secondary and alloying of aluminum, aluminum sheet, plate

and foil manufacturing, other aluminum extruding and metal window and door manufacturing. Industry average TRIR2: 3.5-6.4 Diverse board of directors and management teamInitiated Arconic “Grow Together” diversity and inclusion campaign United

Nations Global Compact signatory targeting UN 2030 Sustainable Development Goals Employee Safety Remains a Priority Increasing Scrap Utilization and Sourcing Environmental Stewardship Social Responsibility Governance and

Accountability Performance Standard Certifications at four locationsWater Security score: BClimate Change score: B- 14

Organic Growth and Increased Efficiency Driving Significant EBITDA Growth 15 600M lbs/yearIncremental

Sales2 $100M-$120M Incremental North American rolling capacity expected to be deployed roughly 50% in packaging and 50% across industrial and ground transportation Productivity $70M-$80M Increased casting throughput, scrap utilization,

shop floor productivity, and asset utilization3Approximately $40 million realized in 2020 Permanent Cost Out ~$100M Approximately $60 million realized in 2020 EBITDA GROWTH1 OPPORTUNITY Compared with 2019 Adjusted EBITDA. Compared to

December 31, 2019 utilization levels.Non-North American Rolling, Building and Construction, and Extrusions facilities. BACKGROUND 2H 2022 2H 2021 YE2021 RUN RATE EXPECTED BY

Improved Cash Conversion as Cash Payments Decline Substantially in 2022+ Pro forma for $1 billion

pension annuitization executed after quarter-end and discount rate impact.Discount rates based on the 3/31/2021 yield curve, resulting in a weighted average discount rate of 3.14%.Net funded liability after 23% tax effect. Pension

Contributions and OPEB andEnvironmental Payments ($M) Nearly $300 million annual reduction of legacy cash flow obligations expected from 2020 to 2022 Gross Pension and OPEB Liability ($B) Net After-Tax Pension and OPEB Liability

($B)3 1,2 1,2 $234reduction -35% -47% $250pensioncontribution $600 ~ ~ ~ ~ ~ ~ ~ ~ ~ 16

Company’s Execution on Growth Plan Is Well Underway 17 Assumes LME aluminum price of $2,200/mt and

Midwest Premium of $430/mt for the full year versus prior assumptions for LME of $2,030/mt and Midwest Premium of $320/mt.Arconic has not provided reconciliations of any forward-looking non-GAAP financial measures, such as adjusted EBITDA and

free cash flow, to the most directly comparable GAAP financial measures because such reconciliations are not available without unreasonable efforts due to the variability and complexity with respect to the charges and other components excluded

from the non-GAAP measures, such as the effects of metal price lag, foreign currency movements, gains or losses on sales of assets, taxes, and any future restructuring or impairment charges. These reconciling items are in addition to the

inherent variability already included in the GAAP measures, which includes, but is not limited to, price/mix and volume. Arconic believes such reconciliations would imply a degree of precision that would be confusing or misleading to

investors.Includes approximately $350 million funding of legacy pension, OPEB, and environmental liabilities.Excludes $250 million contribution to U.S. pension plans in connection with the April annuitization and approximately $350 million in

other funding of legacy pension, OPEB, and environmental liabilities. Strong 1Q 2021 PerformanceSequential revenue growth in all end marketsAdjusted EBITDA up 19% quarter over quarterMaintained cost action and productivity momentumNear-Term

Opportunities for GrowthGround transportation demand supports growth despite semiconductor supply chain issuesFavorable conditions in industrial and packaging marketsWell-Positioned for 2022 and BeyondNew aerospace contracts and packaging

agreements position the company for the foreseeable futurePursuing additional opportunities for organic global capacity growth Prior Updated Revenue1 $6,600 - $6,900 $7,100 - $7,400 Adjusted

EBITDA2 $675 - $725 $710 - $750 Free cash flow2,3 ($50) - $50 Adjusted free cash flow1,2,4 $300 - $400 Updated FY 2021 Outlook ($M)

Appendix

19 ($M) Quarter ended March 31, 2021 2020(1) Total Segment Adjusted

EBITDA(2),(3) $ 189 $ 203 Unallocated amounts: Corporate expenses(4) (9) (2) Stock-based compensation expense (2) (7) Metal price lag(5) 5 (4) Provision for depreciation and amortization (63) (60)

Restructuring and other charges (1) 19 Other(6) (6) (15) Operating income(3) 113 134 Interest expense (23) (35) Other expenses, net (22) (26) Provision for income taxes(3) (16) (27) Net income attributable

to noncontrolling interest – – Consolidated net income attributable to Arconic Corporation(3) $ 52 $ 46 Reconciliation of Segment Adjusted EBITDA Prior to April 1, 2020, Arconic’s financial statements were prepared on a

carve-out basis, as the underlying operations of the Company were previously consolidated as part of Arconic’s former parent company’s financial statements. Accordingly, the Company’s results of operations for the quarter ended March 31, 2020

were prepared on such basis. The carve-out financial statements of Arconic are not necessarily indicative of the Company’s consolidated results of operations had it been a standalone company during the referenced period. See the Combined

Financial Statements included in each of (i) Exhibit 99.1 to the Company’s Form 10 Registration Statement (filed on February 7, 2020), (ii) the Company’s Annual Report on Form 10-K for the year ended December 31, 2019 (filed on March 30, 2020),

and (iii) the Company’s Quarterly Report on Form 10-Q for the period ended March 31, 2020 (filed on May 18, 2020), for additional information.Effective in the second quarter of 2020, management elected to change the profit or loss measure of

the Company’s reportable segments from Segment operating profit to Segment Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) for internal reporting and performance measurement purposes. This change was made to

enhance the transparency and visibility of the underlying operating performance of each segment. Effective in the third quarter of 2020, management refined the Company’s Segment Adjusted EBITDA measure to remove the impact of metal price lag

(see footnote 5). This change was made to further enhance the transparency and visibility of the underlying operating performance of each segment by removing the volatility associated with metal prices.Arconic calculates Segment Adjusted EBITDA

as Total sales (third-party and intersegment) minus each of (i) Cost of goods sold, (ii) Selling, general administrative, and other expenses, and (iii) Research and development expenses, plus Stock-based compensation expense and Metal price

lag. Previously, the Company calculated Segment operating profit as Segment Adjusted EBITDA minus each of (i) the Provision for depreciation and amortization, (ii) Stock-based compensation expense, and (iii) Metal price lag. Arconic’s Segment

Adjusted EBITDA may not be comparable to similarly titled measures of other companies’ reportable segments.Also, effective July 1, 2020, the Company changed its inventory cost method to average cost for all U.S. inventories previously carried

at last-in, first-out (LIFO) cost. The effects of the change in accounting principle have been retrospectively applied to the Company’s Statement of Consolidated Operations for the quarter ended March 31, 2020. See footnote 3 for additional

information.Segment Adjusted EBITDA for the quarter ended March 31, 2020 was recast to reflect the new measure of segment profit or loss and the change in inventory cost method.Total Segment Adjusted EBITDA is the sum of the respective Segment

Adjusted EBITDA for each of the Company’s three reportable segments: Rolled Products, Building and Construction Systems, and Extrusions. This amount is being presented for the sole purpose of reconciling Segment Adjusted EBITDA to the Company’s

Consolidated net income.

3) Effective July 1, 2020, the Company changed its inventory cost method to average cost for all U.S.

inventories previously carried at LIFO cost. Management believes the average cost method more closely reflects the physical flow of inventories, improves comparability of the Company’s operating results with its industry peers, and provides an

increased level of consistency in the measurement of inventories in the Company’s consolidated financial statements. The effects of the change in accounting principle from LIFO to average cost have been retrospectively applied to the Company’s

Statement of Consolidated Operations for the quarter ended March 31, 2020. Accordingly, Net income attributable to Arconic Corporation decreased $14 (comprised of an $18 increase to Cost of goods sold and a $4 decrease to Provision for income

taxes) from the amount previously reported in the Company’s Quarterly Report on Form 10-Q for the period ended March 31, 2020 (filed on May 18, 2020). See the Consolidated Financial Statements included in the Company’s Annual Report on Form

10-K for the year ended December 31, 2020 (filed on February 23, 2021) for additional information.4) Corporate expenses are composed of general administrative and other expenses of operating the corporate headquarters and other global

administrative facilities, as well as research and development expenses of the corporate technical center. The amount presented for the quarter ended March 31, 2020 represents an allocation of Arconic’s former parent company’s corporate

expenses (see footnote 1).5) Metal price lag represents the financial impact of the timing difference between when aluminum prices included in Sales are recognized and when aluminum purchase prices included in Cost of goods sold are realized.

This adjustment aims to remove the effect of the volatility in metal prices and the calculation of this impact considers applicable metal hedging transactions.6) Other includes certain items that impact Cost of goods sold and Selling, general

administrative, and other expenses on the Company’s Statement of Consolidated Operations that are not included in Segment Adjusted EBITDA, including those described as “Other special items” (see footnote 4 to the Reconciliation of Total Company

Adjusted EBITDA included in this presentation). 20 Reconciliation of Segment Adjusted EBITDA (cont’d)

21 Quarter ended March 31, 2021 December 31, 2020 September 30, 2020 June 30,

2020 March 31, 2020(1) ($M) Net income (loss) attributable to Arconic Corporation(2) $ 52 $ (64) $ 5 $ (96) $ 46 Add: Net income attributable to noncontrolling interest – – – – – Provision

(Benefit) for income taxes(2) 16 (4) 10 (32) 27 Other expenses, net 22 1 27 16 26 Interest expense 23 21 22 40 35 Restructuring and other charges 1 127 3 77 (19) Provision for depreciation and amortization 63

60 63 68 60 Stock-based compensation 2 5 6 5 7 Metal price lag(3) (5) (3) 16 10 4 Other special items(4) 5 8 13 11 18 Adjusted EBITDA(2) $ 179 $ 151 $ 165 $ 99 $

204 Sales $1,675 $1,462 $1,415 $1,187 $1,611 Adjusted EBITDA Margin 10.7% 10.3% 11.7% 8.3% 12.7% Arconic’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin

plus an add-back for the following items: Provision for depreciation and amortization; Stock-based compensation; Metal price lag (see below); and Other special items. Net margin is equivalent to Sales minus the following items: Cost of goods

sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation and amortization. Special items are composed of restructuring and other charges, discrete income tax items, and other

items as deemed appropriate by management. There can be no assurances that additional special items will not occur in future periods. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to

investors because Adjusted EBITDA provides additional information with respect to Arconic’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly

titled measures of other companies.Effective in the third quarter of 2020, management refined the Company’s Adjusted EBITDA measure to remove the impact of metal price lag (see footnote 3). This change was made to further enhance the

transparency and visibility of the underlying operating performance of the Company by removing the volatility associated with metal prices. Also, effective July 1, 2020, the Company changed its inventory cost method to average cost for all U.S.

inventories previously carried at last-in, first-out (LIFO) cost. The effects of the change in accounting principle have been retrospectively applied to the Company’s Statement of Consolidated Operations for the quarters ended June 30, 2020 and

March 31, 2020. See footnote 2 for additional information. Adjusted EBITDA for the quarters ended June 30, 2020 and March 31, 2020 was recast to reflect both these changes.Prior to April 1, 2020, Arconic’s financial statements were prepared on

a carve-out basis, as the underlying operations of the Company were previously consolidated as part of Arconic’s former parent company’s financial statements. Accordingly, the Company’s results of operations for the quarter ended March 31, 2020

were prepared on such basis. The carve-out financial statements of Arconic are not necessarily indicative of the Company’s consolidated results of operations had it been a standalone company during the referenced period. See the Combined

Financial Statements included in each of (i) Exhibit 99.1 to the Company’s Form 10 Registration Statement (filed on February 7, 2020), (ii) the Company’s Annual Report on Form 10-K for the year ended December 31, 2019 (filed on March 30, 2020),

and (iii) the Company’s Quarterly Report on Form 10-Q for the period ended March 31, 2020 (filed on May 18, 2020), for additional information. Reconciliation of Total Company Adjusted EBITDA

2) Effective July 1, 2020, the Company changed its inventory cost method to average cost for all U.S.

inventories previously carried at LIFO cost. Management believes the average cost method more closely reflects the physical flow of inventories, improves comparability of the Company’s operating results with its industry peers, and provides an

increased level of consistency in the measurement of inventories in the Company’s consolidated financial statements. The effects of the change in accounting principle from LIFO to average cost have been retrospectively applied to the Company’s

Statement of Consolidated Operations for the quarters ended June 30, 2020 and March 31, 2020. Accordingly, for the quarter ended June 30, 2020, Net loss attributable to Arconic Corporation increased $4 (comprised of a $5 increase to Cost of

goods sold and a $1 increase to Benefit for income taxes) from the amount previously reported in the Company’s Quarterly Report on Form 10-Q for the period ended June 30, 2020 (filed on August 4, 2020). Additionally, for the quarter ended March

31, 2020, Net income attributable to Arconic Corporation decreased $14 (comprised of an $18 increase to Cost of goods sold and a $4 decrease to Provision for income taxes) from the amount previously reported in the Company’s Quarterly Report on

Form 10-Q for the period ended March 31, 2020 (filed on May 18, 2020). See the Consolidated Financial Statements included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2020 (filed on February 23, 2021) for

additional information.3) Metal price lag represents the financial impact of the timing difference between when aluminum prices included in Sales are recognized and when aluminum purchase prices included in Cost of goods sold are realized. This

adjustment aims to remove the effect of the volatility in metal prices and the calculation of this impact considers applicable metal hedging transactions.4) Other special items include the following:• for the quarter ended March 31, 2021, costs

related to several legal matters, including Grenfell Tower ($4) and other ($1);• for the quarter ended December 31, 2020, costs related to several legal matters ($5) and other items ($3);• for the quarter ended September 30, 2020, costs related

to several legal matters, including Grenfell Tower ($4) and other ($2), a write-down of inventory related to the curtailment of the casthouse operations at the Chandler (Arizona) extrusions facility ($5), and other ($2);• for the quarter ended

June 30, 2020, costs related to several legal matters, including a customer settlement ($5), Grenfell Tower ($3), and other ($3); and• for the quarter ended March 31, 2020, an allocation of costs incurred by Arconic’s former parent company

associated with the April 1, 2020 separation of Arconic Inc. into two standalone publicly-traded companies. 22 Reconciliation of Total Company Adjusted EBITDA (cont’d)

23 Adjusted EBITDA to Free Cash Flow Bridge Quarter ended ($M) March 31, 2021 December 31,

2020 September 30, 2020 June 30, 2020 Adjusted EBITDA(1) $179 $151 $165 $99 Change in working capital(2),(4) (230) 130 185 1 Cash payments for: Environmental remediation (Grasse River) (17) (28) (33) (4)

Pension contributions(3) (201) (227) – (12) Other postretirement benefits (10) (14) (14) (13) Restructuring actions (5) (9) (5) (9) Interest (18) (21) (19) (5) Income taxes (6) (11) (3) (7) Capital

expenditures(4) (28) (37) (39) (29) Other 14 17 (36) (12) Free Cash Flow(5) $(322) $(49) $201 $9 Add-back cash payments for: Environmental remediation (Grasse River) 17 28 33 4 Pension

contributions 201 227 – 12 Other postretirement benefits 10 14 14 13 Adjusted Free Cash Flow(6) $(94) $220 $248 $38 Adjusted EBITDA is a non-GAAP financial measure. See Reconciliation of Total Company Adjusted EBITDA presented

elsewhere in this Appendix for (i) Arconic’s definition of Adjusted EBITDA, (ii) management’s rationale for the presentation of this non-GAAP measure, and (iii) a reconciliation of this non-GAAP measure to the most directly comparable GAAP

measure. Arconic’s definition of working capital is Receivables plus Inventories less Accounts payable, trade.In January 2021, the Company contributed a total of $200 to its two funded U.S. defined benefit pension plans, comprised of the

estimated minimum required funding for 2021 of $183 and an additional $17.In preparing the Statement of Consolidated Cash Flows for the nine months ended September 30, 2020, management identified a misclassification related to the non-cash

portion of properties, plants, and equipment additions. This non-cash portion is the result of the timing difference that exists between when the Company records such additions as assets on its Consolidated Balance Sheet and when such additions

have been paid in cash. As a result, the amount of (Decrease) in accounts payable, trade (included in Change in working capital) previously reported for the quarter ended June 30, 2020 was overstated by $8 and the amount of Capital expenditures

previously reported for the quarter ended June 30, 2020 was understated by $8. Accordingly, for the quarter ended June 30, 2020, management has corrected both (Decrease) in accounts payable, trade and Capital expenditures from previously

reported amounts to remove the respective effect of this $8.Arconic’s definition of Free Cash Flow is Cash from operations less capital expenditures. Free Cash Flow is a non-GAAP financial measure. Management believes that this measure is

meaningful to investors because management reviews cash flows generated from operations after taking into consideration capital expenditures, which are both necessary to maintain and expand the Company’s asset base and expected to generate

future cash flows from operations. It is important to note that Free Cash Flow does not represent the residual cash flow available for discretionary expenditures since other non-discretionary expenditures, such as mandatory debt service

requirements, are not deducted from the measure. 1Q 2021: Cash used for operations of $(294) less capital expenditures of $28 = free cash flow of $(322) 4Q 2020: Cash used for operations of $(12) less capital expenditures of $37 = free cash

flow of $(49)3Q 2020: Cash provided from operations of $240 less capital expenditures of $39 = free cash flow of $201 2Q 2020: Cash provided from operations of $38 less capital expenditures of $29 = free cash flow of $96) Adjusted Free Cash

Flow is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted Free Cash Flow provides an incremental view of the Company’s cash performance by excluding payments related to legacy

liabilities.

Reconciliation of Total Company Organic Revenue by End Market 24 Organic revenue is a non-GAAP

financial measure. Management believes this measure is meaningful to investors as it presents revenue on a comparable basis for all periods presented due to the impact of the sale of an aluminum rolling mill in Brazil (divested in February

2020), the sale of a hard alloy extrusions plant in South Korea (divested in March 2020), and the impact of changes in aluminum prices and foreign currency fluctuations relative to the prior year period. ($M) Ground Building

and Industrial and 1Q20 Transportation Construction Aerospace Packaging Other Total Revenue $529 $291 $300 $178 $313 $1,611 Less: Sales - Itapissuma 1 1 - 7 2 11 Sales -

Changwon - - - - 8 8 Organic Revenue $528 $290 $300 $171 $303 $1,592 1Q21 Revenue $662 $287 $138 $219 $369 $1,675 Less: Aluminum price impact 37 4 4 25 19 89

Foreign currency impact 6 9 (1) (4) 1 11 Organic Revenue $619 $274 $135 $198 $349 $1,575

Reconciliation of Organic Revenue by Segment 25 Organic revenue is a non-GAAP financial measure.

Management believes this measure is meaningful to investors as it presents revenue on a comparable basis for all periods presented due to the impact of the sale of an aluminum rolling mill in Brazil (divested in February 2020), the sale of a

hard alloy extrusions plant in South Korea (divested in March 2020), and the impact of changes in aluminum prices and foreign currency fluctuations relative to the prior year period. ($M) Quarter Ended March

31, 2020 2021 Arconic Corporation Revenue $1,611 $1,675 Less: Sales - Itapissuma 11 n/a Sales - Changwon 8 n/a Aluminum price impact n/a 89 Foreign currency impact n/a 11 Organic

Revenue $1,592 $1,575 Rolled Products Revenue $1,222 $1,364 Less: Sales - Itapissuma 11 n/a Aluminum price impact n/a 84 Foreign currency impact n/a 2 Organic Revenue $1,211 $1,278

Building and Construction Systems Revenue $256 $236 Less: Aluminum price impact n/a 2 Foreign currency impact n/a 9 Organic Revenue $256 $225 Extrusions Revenue $133 $75

Less: Sales - Changwon 8 n/a Aluminum price impact n/a 3 Foreign currency impact n/a - Organic Revenue $125 $72