Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - Astria Therapeutics, Inc. | tm214487d1_ex99-1.htm |

| EX-10.2 - EXHIBIT 10.2 - Astria Therapeutics, Inc. | tm214487d1_ex10-2.htm |

| EX-10.1 - EXHIBIT 10.1 - Astria Therapeutics, Inc. | tm214487d1_ex10-1.htm |

| EX-3.1 - EXHIBIT 3.1 - Astria Therapeutics, Inc. | tm214487d1_ex3-1.htm |

| EX-2.1 - EXHIBIT 2.1 - Astria Therapeutics, Inc. | tm214487d1_ex2-1.htm |

| 8-K - FORM 8-K - Astria Therapeutics, Inc. | tm214487d1_8k.htm |

Exhibit 99.2

Investor Presentation January 2021

Forward Looking Statements This presentation and various remarks we make during this presentation contain forward - looking statements of Catabasis Pharmaceuticals, Inc . (“Catabasis,” the “Company,” “we”, “our” or “us”) within the meaning of the Private Securities Litigation Reform Act of 1995 , including statements with respect to : future expectations, plans and prospects for Quellis Biosciences Inc . (“Quellis”) and the combined company following the anticipated consummation of the merger transaction between the Company and Quellis (the “Merger”) ; the expected closing of the concurrent private placement ; the initial market capitalization of the combined company and the benefits of the Merger, and the milestones of the combined company ; the cash runway of the combined company ; the potential timing for the filing of an IND ; the status and plans for a Phase 1 a and Phase 1 b/ 2 clinical trial ; and the potential commercial opportunity for QLS - 215 . We use words such as “anticipate,” “believe,” “estimate,” “expect,” “hope,” “intend,” “may,” “plan,” “predict,” “project,” “target,” “potential,” “would,” “can,” “could,” “should,” “continue,” and other words and terms of similar meaning to help identify forward - looking statements, although not all forward - looking statements contain these identifying words . Actual results may differ materially from those indicated by such forward - looking statements as a result of various important factors, including risks and uncertainties related to the ability to recognize the anticipated benefits of the Merger, the outcome of any legal proceedings that may be instituted against the Company or Quellis following the announcement of the Merger and related transactions ; the ability to obtain or maintain the listing of the common stock of the combined company on The Nasdaq Stock Market following the Merger, costs related to the Merger, changes in applicable laws or regulations, the possibility that the Company or Quellis may be adversely affected by other economic, business, and/or competitive factors, including the COVID - 19 pandemic ; risks inherent in pharmaceutical research and development, such as : adverse results in our drug discovery, preclinical and clinical development activities, the risk that the results of pre - clinical studies may not be replicated in clinical studies, our ability to enroll patients in our clinical trials, and the risk that any of our clinical trials may not commence, continue or be completed on time, or at all ; decisions made by the U . S . FDA and other regulatory authorities, investigational review boards at clinical trial sites and publication review bodies with respect to our development candidates ; our ability to obtain, maintain and enforce intellectual property rights for our platform and development candidates ; our potential dependence on collaboration partners ; competition ; our ability to obtain necessary financing to conduct our planned activities and to manage unplanned cash requirements ; and general economic and market conditions ; as well as the risks and uncertainties discussed in the “Risk Factors” section of the Company’s Quarterly Report on Form 10 - Q for the period ended September 30 , 2020 , which is on file with the Securities and Exchange Commission, and in other filings that the Company may make with the Securities and Exchange Commission in the future . These forward - looking statements should not be relied upon as representing the Company’s view as of any date subsequent to the date of this presentation, and we expressly disclaim any obligation to update any forward - looking statements, whether as a result of new information, future events or otherwise, except as required by law . This presentation contains estimates and other statistical data made by independent parties and by us relating to market size and other data about our industry . This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such data and estimates . In addition, projections, assumptions and estimates of our future performance and the future performance of the markets in which we operate are necessarily subject to a high degree of uncertainty and risk . 2

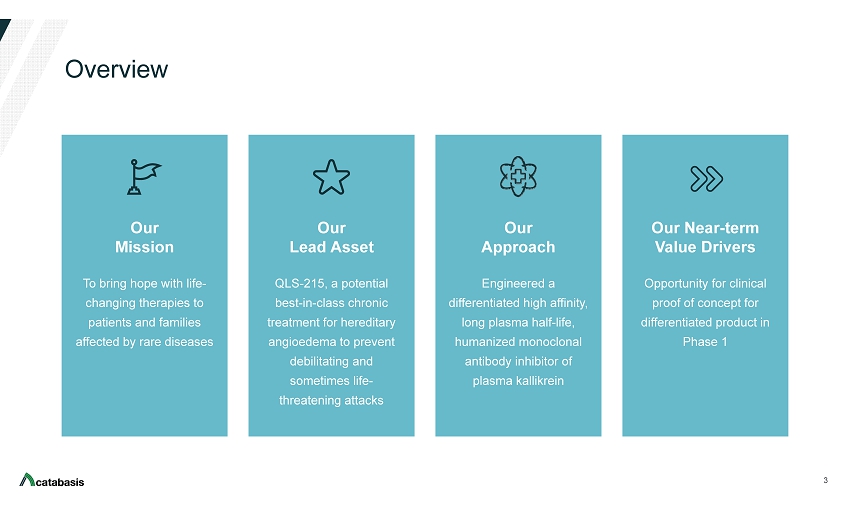

Overview 3 Our Mission T o bring hope with life - changing therapies to patients and families affected by rare diseases Our Approach Engineered a differentiated high affinity, long plasma half - life, humanized monoclonal antibody inhibitor of plasma kallikrein Our Lead Asset QLS - 215, a potential best - in - class chronic treatment for hereditary angioedema to prevent debilitating and sometimes life - threatening attacks Our Near - term Value Drivers Opportunity for clinical proof of concept for differentiated product in Phase 1

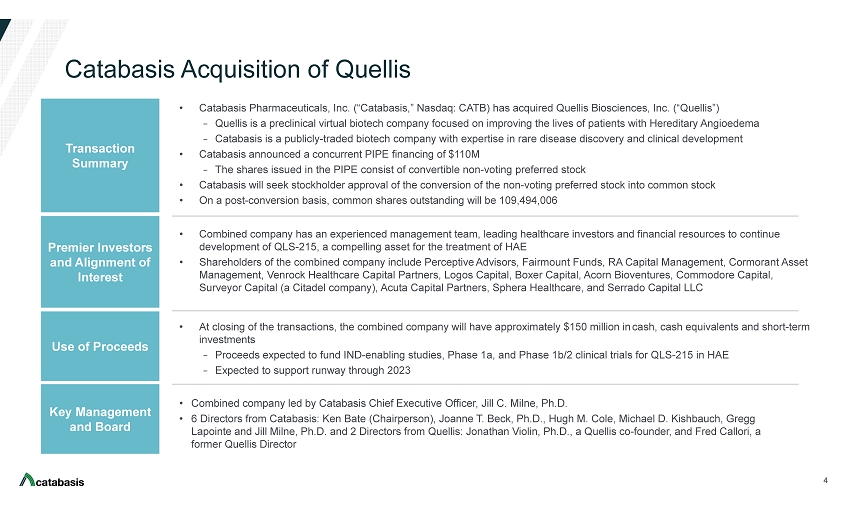

Catabasis Acquisition of Quellis 4 Transaction Summary Premier Investors and Alignment of Interest Use of Proceeds Key Management and Board • Catabasis Pharmaceuticals, Inc. (“Catabasis,” Nasdaq: CATB) has acquired Quellis Biosciences, Inc . (“Quellis”) − Quellis is a preclinical virtual biotech company focused on improving the lives of patients with Hereditary Angioedema − Catabasis is a publicly - traded biotech company with expertise in rare disease discovery and clinical development • Catabasis announced a concurrent PIPE financing of $110M − The shares issued in the PIPE consist of convertible non - voting preferred stock • Catabasis will seek stockholder approval of the conversion of the non - voting preferred stock into common stock • On a post - conversion basis, common shares outstanding will be 109,494,006 • Combined company has an experienced management team, leading healthcare investors and financial resources to continue development of QLS - 215, a compelling asset for the treatment of HAE • Shareholders of the combined company include Perceptive Advisors, Fairmount Funds, RA Capital Management, Cormorant Asset Management, Venrock Healthcare Capital Partners, Logos Capital, Boxer Capital, Acorn Bioventures , Commodore Capital, Surveyor Capital (a Citadel company), Acuta Capital Partners, Sphera Healthcare, and Serrado Capital LLC • At closing of the transactions, the combined company will have approximately $150 million in cash, cash equivalents and short - term investments − Proceeds expected to fund IND - enabling studies, Phase 1a, and Phase 1b/2 clinical trials for QLS - 215 in HAE − Expected to support runway through 2023 • Combined company led by Catabasis Chief Executive Officer, Jill C. Milne , Ph.D . • 6 Directors from Catabasis: Ken Bate (Chairperson), Joanne T. Beck, Ph.D., Hugh M. Cole, Michael D. Kishbauch, Gregg Lapointe and Jill Milne, Ph.D. and 2 Directors from Quellis: Jonathan Violin, Ph.D., a Quellis co - founder, and Fred Callori , a former Quellis Director

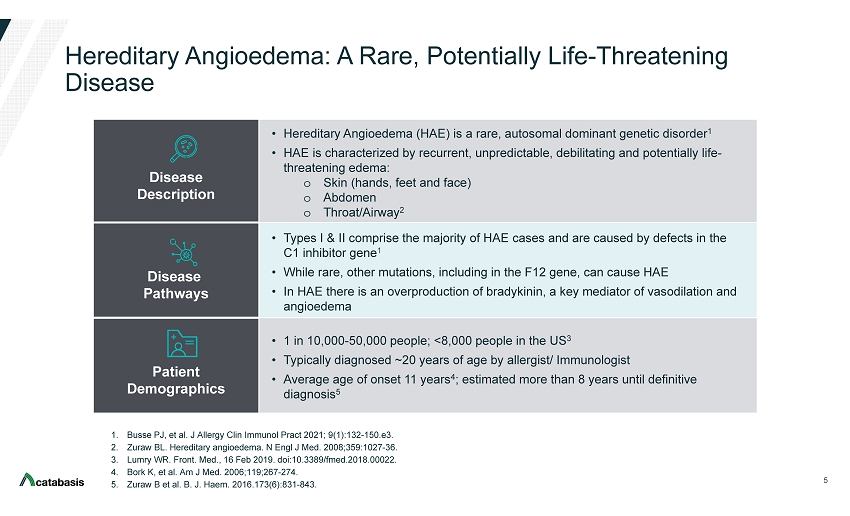

Hereditary Angioedema: A Rare, Potentially Life - Threatening Disease 5 1. Busse PJ, et al. J Allergy Clin Immunol Pract 2021; 9(1):132 - 150.e3. 2. Zuraw BL. Hereditary angioedema. N Engl J Med. 2008;359:1027 - 36. 3. Lumry WR. Front. Med., 16 Feb 2019. doi:10.3389/fmed.2018.00022. 4. Bork K, et al. Am J Med. 2006;119;267 - 274. 5. Zuraw B et al. B. J. Haem. 2016.173(6):831 - 843. Disease Description • Hereditary Angioedema (HAE) is a rare, autosomal dominant genetic disorder 1 • HAE is characterized by recurrent, unpredictable, debilitating and potentially life - threatening edema: o Skin (hands, feet and face) o Abdomen o Throat/Airway 2 Disease Pathways • Types I & II comprise the majority of HAE cases and are caused by defects in the C1 inhibitor gene 1 • While rare, other mutations, including in the F12 gene, can cause HAE • In HAE there is an overproduction of bradykinin, a key mediator of vasodilation and angioedema Patient Demographics • 1 in 10,000 - 50,000 people; <8,000 people in the US 3 • Typically diagnosed ~20 years of age by allergist/ Immunologist • Average age of onset 11 years 4 ; estimated more than 8 years until definitive diagnosis 5

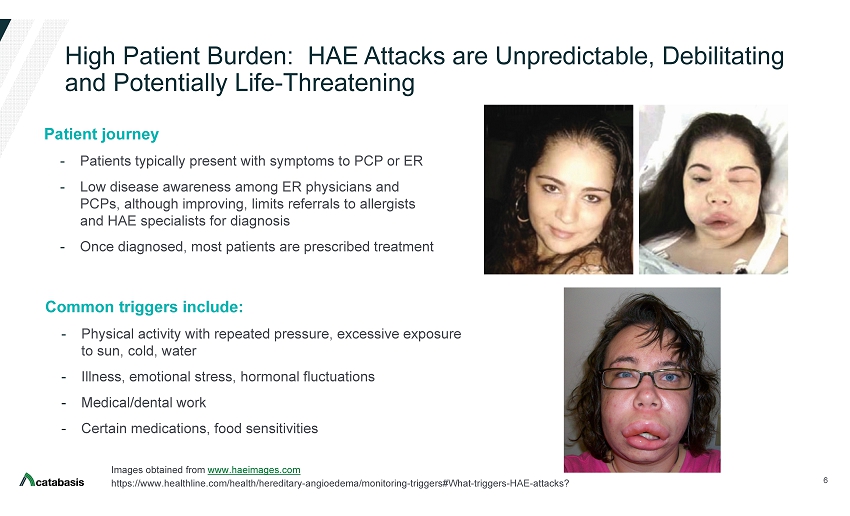

High Patient Burden: HAE Attacks are Unpredictable, Debilitating and Potentially Life - Threatening Common triggers include: - Physical activity with repeated pressure, excessive exposure to sun, cold, water - Illness, emotional stress, hormonal fluctuations - Medical/dental work - Certain medications, food sensitivities 6 Images obtained from www.haeimages.com https://www.healthline.com/health/hereditary - angioedema/monitoring - triggers#What - triggers - HAE - attacks? Patient journey - Patients typically present with symptoms to PCP or ER - Low disease awareness among ER physicians and PCPs, although improving, limits referrals to allergists and HAE specialists for diagnosis - Once diagnosed, most patients are prescribed treatment

Dysregulation of the Plasma Contact System Mediates Excessive Swelling Underlying HAE Symptoms 7 Factor XIIa pKal Activated Factor XII ( FXIIa ) produces pKal plasma kallikrein (pKal) cleaves HMWK to produce Bradykinin Bradykinin binds to receptors on endothelial cells, fluid leakage into tissues Triggers (e.g., pressure, tissue stress and damage) activate Factor XII Type I & II HAE: Patients lack functional C1 - INH, leading to dysregulation with high levels of pKal and bradykinin, causing excess fluid release and excessive swelling Contact System Healthy Contact System HAE C1 - INH Excessive pKal Swelling C1 Inhibitor (C1 INH) blocks FXII and pKal C1 INH not functional Triggers Factor XIIa C1 - INH C1 - INH C1 - INH

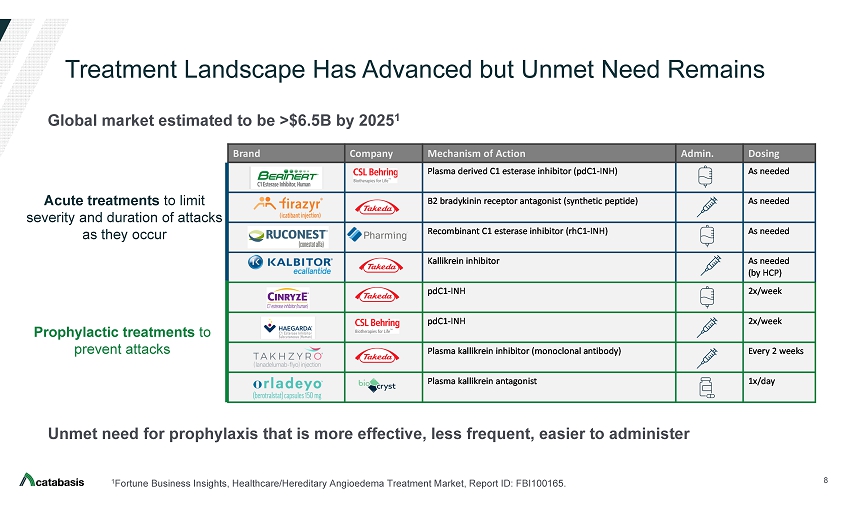

Treatment Landscape Has Advanced but Unmet Need Remains 8 1 Fortune Business Insights, Healthcare/Hereditary Angioedema Treatment Market, Report ID: FBI100165. Acute treatments to limit severity and duration of attacks as they occur Prophylactic treatments to prevent attacks Unmet need for prophylaxis that is more effective, less frequent, easier to administer Brand Company Mechanism of Action Admin. Dosing Plasma derived C1 esterase inhibitor (pdC1 - INH) As needed B2 bradykinin receptor antagonist (synthetic peptide) As needed Recombinant C1 esterase inhibitor (rhC1 - INH) As needed Kallikrein inhibitor As needed (by HCP) pdC1 - INH 2x/week pdC1 - INH 2x/week Plasma kallikrein inhibitor (monoclonal antibody) Every 2 weeks Plasma kallikrein antagonist 1x/day Acute Prophylaxis Global market estimated to be >$6.5B by 2025 1

TAKHZYRO ® (lanadelumab - flyo ) Injection Studies Have Established Plasma Kallikrein mAb as an Important Therapy for HAE 9 Banerji, A., M.A. Riedl, et al. (2018) Effect of Lanadelumab Compared With Placebo on Prevention of Hereditary Angioedema Attacks: A Randomized Clinical Trial. JAMA 320(20):2108 - 2121. https://www.takhzyro.com/ https://www.prnewswire.com/news - releases/shire - to - acquire - dyax - corp - expanding - and - extending - industry - leading - hereditary - angioedema - hae - portfolio - 539278541.html Monoclonal antibody targeting pKal • Prophylaxis to prevent HAE attacks in patients 12 years and older • SC injection every 2 weeks. Dosing every 4 weeks may be considered in some patients. • Most common AE in Phase 3 was injection site reaction (overall 52%) • Shire acquired Dyax for $5.9B after Phase 1b with lead program TAKHZYRO

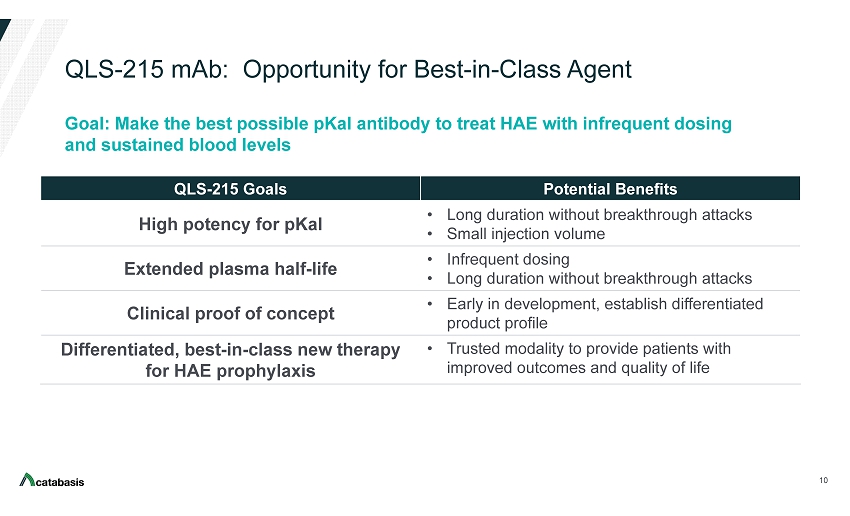

QLS - 215 mAb: Opportunity for Best - in - Class Agent 10 QLS - 215 Goals Potential Benefits High potency for pKal • Long duration without breakthrough attacks • Small injection volume Extended plasma half - life • Infrequent dosing • Long duration without breakthrough attacks Clinical proof of concept • Early in development, establish differentiated product profile Differentiated, best - in - class new therapy for HAE prophylaxis • Trusted modality to provide patients with improved outcomes and quality of life Goal: Make the best possible pKal antibody to treat HAE with infrequent dosing and sustained blood levels

QLS - 215 Designed from Inception to be Potentially a Best - in - Class Prophylactic Therapy for Patients Affected by HAE 11 >11,000 hybridomas 3840 pKal binders ~20 hits selective for pKal vs. pre - Kal 1 hit selective and inhibitory Humanized Optimized QLS - 215 Humanized monoclonal antibody having the following features: • High affinity and selectivity for plasma kallikrein (pKal) versus pre - kallikrein (pre - Kal ) • Reduced immunogenicity and CMC liabilities • Extended plasma half - life

In an in vitro Functional Assay QLS - 215 Was More Potent than Lanadelumab in Inhibiting Bradykinin Production 12 pKal levels 30 - 110nM estimated in HAE plasma (Kenniston et al JBC 2014) Lanadelumab QLS - 215 pKal IC 90 (nM) 300 30 • IC 90 determined by bradykinin ELISA to detect cleavage of high molecular weight kininogen (600 nM) by pKal (30 nM) 0 10 20 30 40 50 30 nM pKal, 600 nM HMWK [mAb], nM B r a d y k i n i n , n M DX-2930 QLS-215 1 10 100 1,0000.1 Lanadelumab Functional Assay

QLS - 215 Has Shown Substantially Prolonged Plasma Half - Life Compared to Lanadelumab in Non - Human Primates 13 Data from concurrent but independent experiments in cynomolgus monkeys Lanadelumab data are representative of 3 independent experiments that all showed t 1/2 ~10 days • FDA review documents: Lanadelumab t 1/2 9.5 - 11.5 days in cynomolgus monkeys Lanadelumab QLS - 215 Mean half - life (t 1/2 ) (SD) 10.5 (1.6) 33.6 (8.3) The picture can't be displayed.

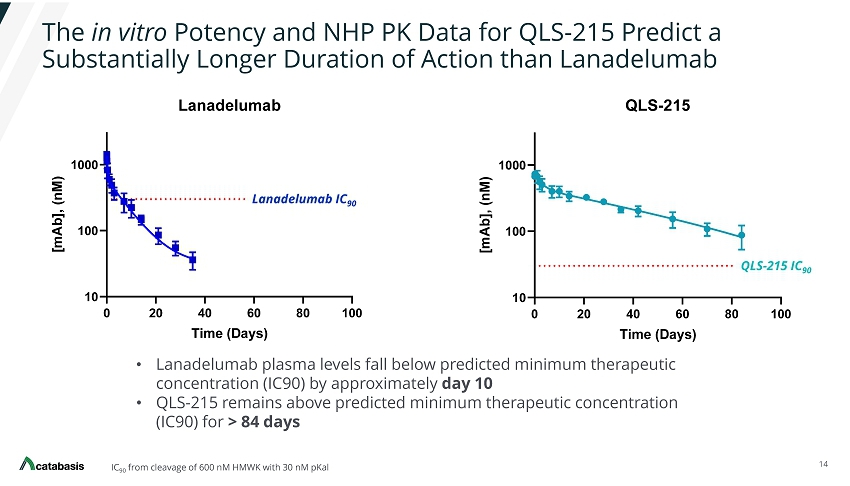

The in vitro Potency and NHP PK Data for QLS - 215 Predict a Substantially Longer Duration of Action than Lanadelumab 14 IC 90 from cleavage of 600 nM HMWK with 30 nM pKal • Lanadelumab plasma levels fall below predicted minimum therapeutic concentration (IC90) by approximately day 10 • QLS - 215 remains above predicted minimum therapeutic concentration (IC90) for > 84 days The picture can't be displayed. QLS - 215 IC 90 Lanadelumab IC 90

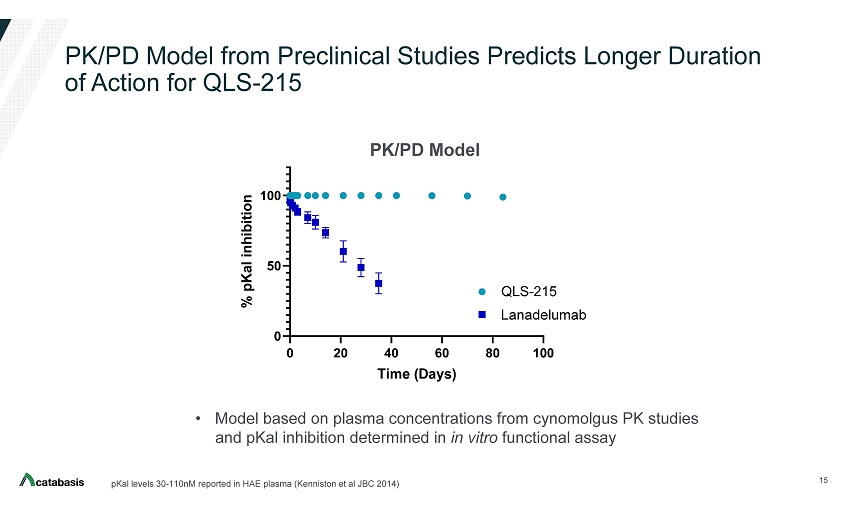

PK/PD Model from Preclinical Studies Predicts Longer Duration of Action for QLS - 215 15 pKal levels 30 - 110nM reported in HAE plasma (Kenniston et al JBC 2014) 0 20 40 60 80 100 0 50 100 NHP PK, 5 mg/kg Time (Days) % p K a l i n h i b i t i o n QLS-215 DX2930 • Model based on plasma concentrations from cynomolgus PK studies and pKal inhibition determined in in vitro functional assay Lanadelumab PK/PD Model

QLS - 215 mAb Developed with the Desired Characteristics 16 QLS - 215 Goals Status High potency for pKal Extended plasma half - life in NHP Clinical proof of concept New therapy for HAE prophylaxis Goal: Make the best possible pKal antibody to treat HAE with infrequent dosing and sustained blood levels

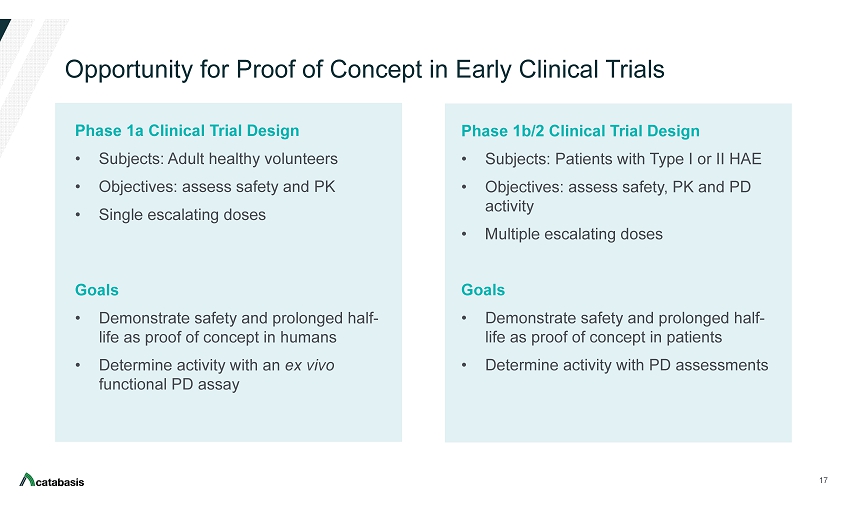

Opportunity for Proof of Concept in Early Clinical Trials Phase 1a Clinical Trial Design • Subjects: Adult healthy volunteers • Objectives: assess safety and PK • Single escalating doses Goals • Demonstrate safety and prolonged half - life as proof of concept in humans • Determine activity with an ex vivo functional PD assay 17 Phase 1b/2 Clinical Trial Design • Subjects: Patients with Type I or II HAE • Objectives: assess safety, PK and PD activity • Multiple escalating doses Goals • Demonstrate safety and prolonged half - life as proof of concept in patients • Determine activity with PD assessments

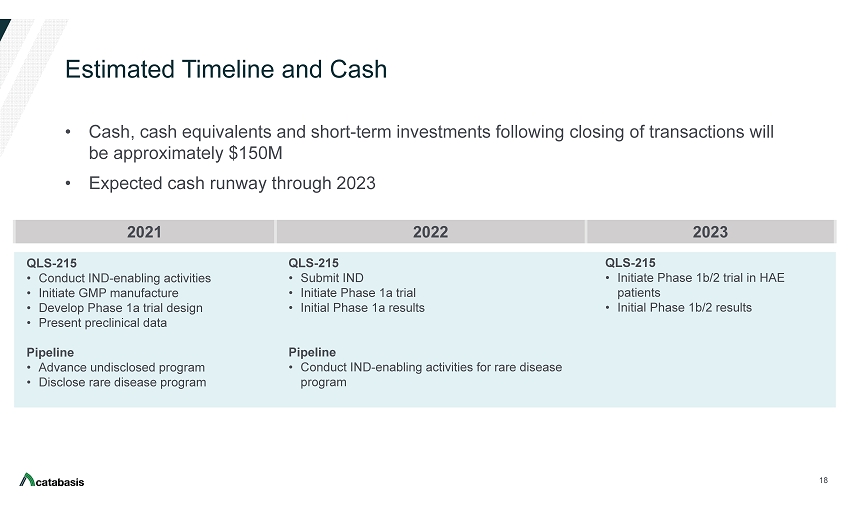

Estimated Timeline and Cash • Cash, cash equivalents and short - term investments following closing of transactions will be approximately $150M • Expected cash runway through 2023 18 2021 2022 2023 QLS - 215 • Conduct IND - enabling activities • Initiate GMP manufacture • Develop Phase 1a trial design • Present preclinical data Pipeline • Advance undisclosed program • Disclose rare disease program QLS - 215 • Submit IND • Initiate Phase 1a trial • Initial Phase 1a results Pipeline • Conduct IND - enabling activities for rare disease program QLS - 215 • Initiate Phase 1b/2 trial in HAE patients • Initial Phase 1b/2 results

QLS - 215 Opportunity 19 Treatment for rare, genetic disease with established clinical and regulatory path Targeting a clinically validated mechanism with a trusted modality Potential for best - in - class agent that provides greater efficacy and ease of use Candidate with differentiated preclinical profile in predictive models Potential to demonstrate clinical proof of concept for product profile in Phase 1

Vision for Catabasis 20 Value Time Today • Acquisition of Quellis • Advance QLS - 215 to IND - IND - enabling activities - GMP manufacture - Phase 1a design Tomorrow • Establish clinical PoC • Advance 2nd program Future • Submit QLS - 215 BLA • Expand rare disease pipeline

catabasis.com