Attached files

| file | filename |

|---|---|

| EX-24 - EX-24 - TRANSAMERICA LIFE INSURANCE CO | d96965dex24.htm |

| EX-3.(II) - EX-3.(II) - TRANSAMERICA LIFE INSURANCE CO | d96965dex3ii.htm |

| EX-3.(I) - EX-3.(I) - TRANSAMERICA LIFE INSURANCE CO | d96965dex3i.htm |

| EX-1.(II) - EX-1.(II) - TRANSAMERICA LIFE INSURANCE CO | d96965dex1ii.htm |

| EX-1.(I) - EX-1.(I) - TRANSAMERICA LIFE INSURANCE CO | d96965dex1i.htm |

As filed with the Securities and Exchange Commission on January 15, 2021

Registration No. 333-___________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Transamerica Life Insurance Company

(Exact Name of Registrant as specified in its charter)

| Iowa | 6311 | 39-0989781 | ||

| (State or other jurisdiction of Incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

4333 Edgewood Road, NE

Cedar Rapids, IA 52499

Telephone Number: (319) 355-8511

(Address, including zip code, and telephone number, including area code, of Principal Executive Offices)

Brian Stallworth, Esq.

Transamerica Life Insurance Company

c/o Office of the General Counsel

4333 Edgewood Road, N.E.

Cedar Rapids, IA 52499-4240

Telephone Number: (319) 355-8511

(Name, Address, including zip code, and telephone number, including area code, of Agent for Service)

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company.

| Large Accelerated Filer | ☐ | Accelerated Filer | ☐ | |||

| Non-Accelerated Filer | ☒ | Smaller Reporting Company | ☐ | |||

| Emerging Growth Company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

Calculation of Registration Fee

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be |

Proposed Maximum Per Unit* |

Proposed Maximum |

Amount of Registration Fee | ||||

| Individual Flexible Premium Deferred Annuity |

N/A | N/A | $1,000,000.00 | $109.10 | ||||

|

| ||||||||

|

| ||||||||

| * | The amount to be registered and the proposed maximum offering price per unit are not applicable because interests are not issued in predetermined amounts or units. Interests are sold on a dollar-for-dollar basis. |

| ** | The proposed maximum aggregate offering price is estimated solely for the purposes of determining the registration fee. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

[Form of Feature Sheet Prospectus Supplement]

TRANSAMERICA STRUCTURED INDEX ADVANTAGESM ANNUITY

Issued by Transamerica Life Insurance Company

FEATURE SHEET PROSPECTUS SUPPLEMENT

DISCLOSING

AVAILABLE ALLOCATION ACCOUNTS FOR NEW PREMIUM PAYMENTS

Feature Sheet Prospectus Supplement Dated [ ] to the Prospectus Dated [ ]

Effective Date: [ ]

We are issuing this Feature Sheet Prospectus Supplement to disclose the Allocation Accounts available for investment with respect to both initial and additional premium payments under the Transamerica Structured Index AdvantageSM Annuity. This Feature Sheet Prospectus Supplement should be read in conjunction with the prospectus and retained for future reference. Capitalized terms have the meanings given to them in the prospectus.

As of its effective date, this Feature Sheet Prospectus Supplement will remain in effect until it is superseded by a future Feature Sheet Prospectus Supplement. A superseding Feature Sheet Prospectus Supplement will be issued at least 10 days prior to its effective date.

If you would like another copy of the prospectus or a Feature Sheet Prospectus Supplement, please call us at (800) 525-6205 or visit www.transamerica.com. All Feature Sheet Prospectus Supplements are also available on the Securities and Exchange Commission’s EDGAR system at www.sec.gov. The EDGAR Central Index Key (CIK) for Transamerica Life Insurance Company is 0001164098.

AVAILABLE ALLOCATION ACCOUNTS AND

OTHER INFORMATION FOR NEW PREMIUM PAYMENTS

This Feature Sheet Prospectus Supplement applies to your new premium payment if:

| • | For an initial premium payment, you sign the Policy application while this Feature Sheet Prospectus Supplement is in effect. |

| • | For an additional premium payment, we receive your payment while this Feature Sheet Prospectus Supplement is in effect. |

With respect to an applicable premium payment, as described above, this Feature Sheet Prospectus Supplement discloses the following information:

| (1) | The Allocation Accounts to which the premium payment may be allocated; and |

| (2) | The Growth Opportunity Type(s) and Downside Protection Type(s) that are guaranteed to be part of at least one Index Account Option available for investment at the end of each Crediting Period. |

AVAILABLE ALLOCATION ACCOUNTS

Basic Index Account Option[s]

| Index | Crediting Period | Growth Opportunity Type |

Downside Protection Type |

Downside Protection Type Rate(s) | ||||||

| [1] | [ ] | [ ] | [ ] | [ ] | [ ] | |||||

| [2] | [ ] | [ ] | [ ] | [ ] | [ ] | |||||

| [3] | [ ] | [ ] | [ ] | [ ] | [ ] |

[Best Entry Enhanced Index Account Options]

| Index | Crediting Period |

Growth Opportunity Type |

Downside Protection Type |

Downside Protection Type Rate |

Observation Period |

Observation Frequency |

Best Entry Reset Threshold | |||||||||

| [1] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | [ ] | ||||||||

| [2] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | [ ] | ||||||||

| [3] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | [ ] |

[Buffer Auto Reset Enhanced Index Account Options]

| Index | Crediting Period |

Growth Opportunity Type |

Downside Protection Type |

Downside Protection Type Rate |

Buffer Reset Period |

Buffer Reset Trigger | ||||||||

| [1] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | |||||||

| [2] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | |||||||

| [3] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] |

[Fixed Account]

| Crediting Period[s] |

| [ ] |

GUARANTEED GROWTH OPPORTUNITY & DOWNSIDE PROTECTION TYPES

| Guaranteed Growth Opportunity Type(s)* |

Guaranteed Downside Protection Type(s)* | |

| [ ] | [ ] |

| * | Please note these guaranteed Growth Opportunity Type(s) and Downside Protection Type(s) apply only to an initial or additional premium payment made under this Feature Sheet Prospectus Supplement and any earnings under the Policy related to such premium payment. A premium payment made under a past or future Feature Sheet Prospectus Supplement is subject to the guarantees described in that Feature Sheet Prospectus Supplement. As such, the Growth Opportunity Type(s) and Downside Protection Type(s) that are guaranteed may vary by premium payment if you submit multiple premium payments. |

Important information about the current Allocation Options document:

| • | This Feature Sheet Prospectus Supplement contains only a subset of the information included in the current Allocation Options document, which is a separate document that also includes the current rates we have declared for Growth Opportunity Types, Credit Advantage Fee percentages, and current interest rates, to the extent applicable. Those declared rates may change even while this Feature Sheet Prospectus Supplement remains in effect. You should not purchase the Policy or make an additional premium payment until you have obtained and carefully reviewed the current Allocation Options document. The current Allocation Options document is available online at www.transamerica.com/[ ] and upon request by contacting our Administrative Office or your financial intermediary. |

| • | If you are a prospective purchaser of the Policy, you will receive the current Allocation Options document during the application process. In order to guarantee that the information in that Allocation Options document will apply to your initial premium payment, you must sign your application while that Allocation Options document remains in effect. After you sign your application, we must also receive your initial premium payment within 14 calendar days of your signature date (or 60 calendar days if the Policy is funded through an exchange, transfer, or rollover). If these conditions are not met, your application will be considered not in good order. If you decide to proceed with the purchase of the Policy after we determine that your application is not in good order, additional paperwork may be required to issue the Policy, and the Allocation Options document in effect at that time will apply your initial premium payment. |

| • | If you are an existing Owner of the Policy submitting an additional premium payment, the Allocation Options document in effect on the date that we receive your additional premium payment will apply. In order to guarantee the current Allocation Options document will apply to your additional premium payment, we must receive your additional premium payment while the current Allocation Options document remains in effect. |

See PREMIUM PAYMENTS – ALLOCATION OF PREMIUM PAYMENTS in the prospectus for additional information.

This Feature Sheet Prospectus Supplement must be accompanied or preceded by the current prospectus.

Please read this Supplement carefully and retain it for future reference.

[Form of Feature Sheet Prospectus Supplement]

TRANSAMERICA STRUCTURED INDEX ADVANTAGESM ANNUITY

Issued by Transamerica Life Insurance Company

FEATURE SHEET PROSPECTUS SUPPLEMENT

DISCLOSING

AVAILABLE ALLOCATION ACCOUNTS AT END OF CREDITING PERIOD

Feature Sheet Prospectus Supplement Dated [ ] to the Prospectus Dated [ ]

For Premium Payments [After [ ] / On or Between [ ] and [ ]]

Effective Date: [ ]

We are issuing this Feature Sheet Prospectus Supplement to disclose the Allocation Accounts available for investment at the end of a Crediting Period under the Transamerica Structured Index AdvantageSM Annuity.

As of its effective date, this Feature Sheet Prospectus Supplement will remain in effect until it is superseded by a future Feature Sheet Prospectus Supplement. A superseding Feature Sheet Prospectus Supplement will be issued at least 30 days prior to its effective date.

If you would like another copy of the prospectus or a Feature Sheet Prospectus Supplement, please call us at (800) 525-6205 or visit www.transamerica.com. All Feature Sheet Prospectus Supplements are also available on the Securities and Exchange Commission’s EDGAR system at www.sec.gov. The EDGAR Central Index Key (CIK) for Transamerica Life Insurance Company is 0001164098.

AVAILABLE ALLOCATION ACCOUNTS AT END OF CREDITING PERIOD

This Feature Sheet Prospectus Supplement discloses the Allocation Accounts that are available for investment at the end of a Crediting Period for prior premium payments and any related earnings under the Policy to which this Feature Sheet Prospectus Supplement applies.

This Feature Sheet Prospectus Supplement applies to a prior premium payment and any related earnings under the Policy, as follows:

| • | For an initial premium payment and related earnings, this Feature Sheet Prospectus Supplement applies if you signed the Policy application [after the date specified above] [between the dates specified above]. |

| • | For an additional premium payment and related earnings, this Feature Sheet Prospectus Supplement applies if we received the premium payment [after the date specified above] [between the dates specified above]. |

This Feature Sheet Prospectus Supplement does not apply to a prior premium payment that we received [before the date specified above] [outside of the dates specified above]. Nor does it apply to any future additional premium payments, including additional premium payments submitted at the end of a Crediting Period.

AVAILABLE ALLOCATION ACCOUNTS

Basic Index Account Option[s]

| Index | Crediting Period |

Growth Opportunity Type |

Downside Protection Type |

Downside Protection Type Rate(s) | ||||||

| [1] | [ ] | [ ] | [ ] | [ ] | [ ] | |||||

| [2] | [ ] | [ ] | [ ] | [ ] | [ ] | |||||

| [3] | [ ] | [ ] | [ ] | [ ] | [ ] |

[Best Entry Enhanced Index Account Options]

| Index | Crediting Period |

Growth Opportunity Type |

Downside Protection Type |

Downside Protection Type Rate |

Observation Period |

Observation Frequency |

Best Entry Reset Threshold | |||||||||

| [1] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | [ ] | ||||||||

| [2] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | [ ] | ||||||||

| [3] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | [ ] |

[Buffer Auto Reset Enhanced Index Account Options]

| Index | Crediting Period |

Growth Opportunity Type |

Downside Protection Type |

Downside Protection Type Rate |

Buffer Reset Period |

Buffer Reset Trigger | ||||||||

| [1] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | |||||||

| [2] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] | |||||||

| [3] | [ ] | [ ] | Cap | Buffer | Buffer Rate [ ] |

[ ] | [ ] |

[Fixed Account]

| Crediting Period[s] |

| [ ] |

Important information about Renewal Letters:

| • | This Feature Sheet Prospectus Supplement contains only a subset of the information included in the Renewal Letter that will be sent to you prior to the end of each Crediting Period. The Renewal Letter is a separate document that also includes the rates we have declared for Growth Opportunity Types, Credit Advantage Fee percentages, and current interest rates, to the extent applicable. Those declared rates may change even while this Feature Sheet Prospectus Supplement remains in effect. |

| • | We will send a Renewal Letter and the Feature Sheet Prospectus Supplement in effect to you at least 21 days before the end of each Crediting Period. Your Renewal Letter will be based on personal circumstances, i.e., when you made your premium payment(s). |

| • | Among other information, the Renewal Letter will: (i) remind you of your opportunity to decide how your Policy Value in the expiring Allocation Account should be re-invested; (ii) inform you of the Allocation Account(s) that will be available to you for investment, with complete information about the rates we declared for such Allocation Account(s); and (iii) remind you to submit instructions to us at least one Business Day before the end of the Crediting Period. You may also request the Renewal Letter by contacting our Administrative Office or your financial intermediary. |

This Feature Sheet Prospectus Supplement must be accompanied or preceded by the current prospectus.

Please read this Supplement carefully and retain it for future reference.

[Form of Rate Sheet Prospectus Supplement]

TRANSAMERICA STRUCTURED INDEX ADVANTAGESM ANNUITY

Issued by Transamerica Life Insurance Company

RATE SHEET PROSPECTUS SUPPLEMENT

DISCLOSING

FEE PERCENTAGES FOR GMDB RIDER ELECTIONS

Rate Sheet Prospectus Supplement Dated [ ] to the Prospectus Dated [ ]

Effective Date: [ ]

We are issuing this Rate Sheet Prospectus Supplement to disclose the fee percentages for the Guaranteed Minimum Death Benefit (GMDB) rider that we are currently offering with the Transamerica Structured Index AdvantageSM Annuity. It should be read in conjunction with the prospectus and retained for future reference. Capitalized terms have the meanings given to them in the prospectus.

As of its effective date, this Rate Sheet Prospectus Supplement will remain in effect until it is superseded by a future Rate Sheet Prospectus Supplement. A superseding Rate Sheet Prospectus Supplement will be issued at least 10 days prior to its effective date.

If you would like another copy of the prospectus or a Rate Sheet Prospectus Supplement, please call us at (800) 525-6205 or visit www.transamerica.com. All Rate Sheet Prospectus Supplements are also available on the Securities and Exchange Commission’s EDGAR system at www.sec.gov. The EDGAR Central Index Key (CIK) for Transamerica Life Insurance Company is 0001164098.

FEE PERCENTAGES FOR GMDB RIDER ELECTIONS

This Rate Sheet Prospectus Supplement applies to:

| • | Any prospective purchaser of a Policy electing the GMDB rider; |

| • | Any existing Owner of a Policy who is eligible to re-elect the GMDB rider; and |

If you are electing or re-electing the rider, only one of the fee percentages listed in the table below will apply to your rider, depending on the age of the Annuitant on the date that you sign the Policy application or at the time your re-election request is received in good order.

| Age of Annuitant |

Fee Percentage | |

| [ ] – [ ] | [ ]% | |

| [ ] – [ ] | [ ]% | |

| [ ] – [ ] | [ ]% |

Important information about electing the GMDB rider:

| • | If you do not elect the GMDB rider, your Policy will not be subject to the GMDB rider fee. If you elect the GMDB rider, the GMDB rider fee percentage applicable to your rider will not change for the life of your rider. |

| • | If you are eligible to elect or re-elect the GMDB rider and it would not subject your Policy to an additional fee, which could happen based on the age of the Annuitant, the GMDB rider will be automatically added to your Policy. We may not always offer an Annuitant age range with a 0% fee percentage. |

| • | If you are a prospective purchaser of the Policy, in order for you to receive the applicable GMDB rider fee percentage in the table above, your application must be signed while this Rate Sheet Prospectus Supplement remains in effect. We must also receive your initial premium payment within 14 calendar days of your signature date (or 60 calendar days if the Policy is funded through an exchange, transfer, or rollover). If these conditions are not met, your application will be considered not in good order. If you decide to proceed with the purchase of the Policy, additional paperwork may be required to issue the Policy and the fee percentages that we are offering at that time will apply to the GMDB rider. |

| • | If you are re-electing the GMDB rider, assuming that you are eligible to re-elect the rider, you will receive the applicable GMDB rider fee percentage that we are offering at the time your re-election request is received in good order. In order for you to receive the applicable GMDB rider fee percentage in the table above, we must receive your re-election request in good order while this Rate Sheet Prospectus Supplement remains in effect. |

This Feature Sheet Prospectus Supplement must be accompanied or preceded by the current prospectus.

Please read this Supplement carefully and retain it for future reference.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Preliminary Prospectus Dated January 15, 2021

TRANSAMERICA STRUCTURED INDEX ADVANTAGESM ANNUITY

An Individual Flexible Premium Deferred Index-Linked Annuity Policy

Issued by Transamerica Life Insurance Company

Administrative Office

4333 Edgewood Road NE

Cedar Rapids, Iowa 52499-0001

(800) 525-6205

www.transamerica.com

This prospectus includes important information you should know before you purchase the Transamerica Structured Index AdvantageSM Annuity (the “Policy”), an individual flexible premium deferred index-linked annuity policy that you can use to accumulate funds for retirement or other long-term financial planning purposes on a tax-deferred basis. When you purchase the Policy, it is a contract between you, as the owner or joint owner, and Transamerica Life Insurance Company (“us,” “we,” “our,” or the “Company”).

The Policy allows you to allocate your premium payments and earnings (if any) among the investment options that we may make available to you, which include one or more index-linked investment options (“Index Account Options”) and a fixed account investment option (the “Fixed Account”).

| • | Each Index Account Option is linked to the performance of a specific market index or exchange-traded fund for a defined time period (a “Crediting Period”) and includes limited protection against loss. We may make various types of “Basic Index Account Options” and “Enhanced Index Account Options” available for investment. This prospectus describes the different features associated with the Index Account Options and how your gains and losses are calculated. |

| • | The Fixed Account guarantees principal and a rate of interest for a Crediting Period. |

You should not buy this Policy if you are not willing to assume its investment risks. See PRODUCT RISK FACTORS beginning on page [ ].

We periodically issue Feature Sheet Prospectus Supplements that are part of this prospectus. The Feature Sheet Prospectus Supplements disclose the investment options that are currently available for investment. We also periodically issue Rate Sheet Prospectus Supplements that are part of this prospectus and disclose the fee percentages that we are currently offering for the optional death benefit rider.

Before you select investment options under the Policy, you should carefully review the Allocation Options document or Renewal Letter that is applicable to you.

| • | The Allocation Options document will include the investment options to which initial or additional premium payments may be allocated. The current Allocation Options document is available online at www.transamerica.com/[ ] and upon request by contacting our Administrative Office or your financial intermediary. You will be provided with the current Allocation Options document during the application process. |

| • | A Renewal Letter will include the investment options that you may select for investment at the end of a Crediting Period. We will send you a personalized Renewal Letter at least 21 days before the end of each investment term. You may also request the Renewal Letter by contacting our Administrative Office or your financial intermediary. |

An Allocation Options document or Renewal Letter is distinct from a Feature Sheet Prospectus Supplement. Like a Feature Sheet Prospectus Supplement, an Allocation Options document or Renewal Letter contains the investment options that are currently available for investment, but it also contains certain rates that may change from time-to-time while a Feature Sheet Prospectus Supplement remains in effect.

Index-linked annuity contracts are complicated investments. You may lose money, including a significant amount of your principal investment. Before you purchase the Policy, you should carefully read this prospectus and speak with your financial professional about whether the Policy is appropriate for you based on your personal circumstances and financial goals. You should also consult with a tax professional.

If you are a new investor in the Policy, you may cancel your Policy within 10 days. In some states or circumstances, this cancellation period may be longer. Upon cancellation, you will receive the value of your Policy plus any fees or charges deducted under the Policy on the date of cancellation unless a different amount is required by law. You should review this prospectus, or consult with your financial professional, for additional information about the specific cancellation terms that apply.

Additional information about certain investment products, including indexed annuities, has been prepared by the SEC’s staff and is available at Investor.gov.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved these securities, or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

We are not an investment adviser nor are we registered as such with the SEC or any state securities regulatory authority. We are not acting in any fiduciary capacity with respect to your Policy, and nor are we acting in any capacity on behalf of any tax-advantaged retirement plan. This information does not constitute personalized investment advice or financial planning advice. This prospectus is not intended to provide tax, accounting, or legal advice.

Prospective purchasers may obtain an application to purchase the Policy through broker-dealers that have been appointed by us as insurance agents and that have selling agreements with Transamerica Capital, Inc. (“TCI”), the principal underwriter for the Policy. TCI is not required to sell any specific number of Policies. This prospectus is not an offer to sell the securities, and it is not soliciting an offer to buy the securities, in any state where offers or sales are not permitted.

The minimum initial premium payment is $25,000.

Prospectus Date: [ ]

TABLE OF CONTENTS

[Insert Table of Contents Once Prospectus is Finalized]

Please note this prospectus includes various special terms to describe the Policy. Often, these special terms will be defined as you read this prospectus, typically when first used. We encourage you to cross-reference the section titled GLOSSARY, which contains a list of special terms and their definitions.

SUMMARY

PURPOSE OF THE POLICY

The Transamerica Structured Index AdvantageSM Annuity is an individual flexible premium deferred index-linked annuity policy. You can use the Policy to accumulate funds for retirement or other long-term financial planning purposes on a tax-deferred basis, and you may choose to convert those accumulated funds into a stream of guaranteed income payments from us. The amount of money that you are able to accumulate under your Policy will depend upon the performance of the investment options you select, the fees and charges deducted from your Policy, and the actions that you take with respect to your Policy, such as whether and when you take withdrawals. The Policy also includes a death benefit to help you financially protect your designated beneficiaries.

This Policy may be appropriate if you have a long investment time horizon. This Policy is not designed for people who expect to take early or frequent withdrawals.

Transamerica Life Insurance Company is the issuer of the Policy. An investment in the Policy is subject to the risks related to us. Any obligations, guarantees, and benefits under the Policy are subject to our financial strength and claims-paying ability. See APPENDIX E – TRANSAMERICA LIFE INSURANCE COMPANY AND FINANCIAL STATEMENTS for detailed information about the Company, including financial information.

BUYING THE POLICY

If you, any joint Owner, and the designated Annuitant are younger than age 86, you may buy the Policy. Here is how:

| 1. | Request an Application. You may obtain an application to purchase the Policy through a financial intermediary appointed by us as an insurance agent who sells the Policy. |

| 2. | Choose Between Qualified and Non-Qualified. We currently issue Policies that are treated as qualified or non-qualified under the Internal Revenue Code. Earnings accumulate under the Policy on a tax-deferred basis and will be taxed as ordinary income only when withdrawn or otherwise paid out. If you purchase the Policy through an individual retirement account (IRA) or through a tax-qualified plan, you do not get any additional tax benefit under the Policy. |

| 3. | Choose Your Investment Options. During the application process, you will receive a list of investment options that are currently available to you (the “Allocation Options document”). You must decide how your initial premium payment will be invested among one or more of the available investment options. Your allocations must be in whole percentages and total 100%. |

| 4. | Choose Your Optional Benefits (If Desired). You may be able to elect one or more optional benefits during the application process. There may be additional charges for optional benefits. You should note whether an optional benefit can only be elected at the time you purchase the Policy, or whether you are allowed to elect it after you purchase the Policy. We may stop offering an optional benefit to new and existing investors at any time. |

| 5. | Submit the Application and Your Initial Premium Payment. Submit your completed signed application and your initial premium payment to us through your financial intermediary. The minimum initial premium payment is $25,000. |

You may return your Policy for a refund, but only if you return it within the prescribed period, which is generally 10 days after you receive the Policy (or 30 days for replacement Policies) but could vary by state. The refund will generally be the Policy Value on the date of cancellation (plus any fees or charges deducted under the Policy on the date of the cancellation), in which case you bear the risk of any decline in your Policy Value during the right to cancel period. State law may require us to refund the greater of your Policy Value or your premium payment(s). For IRAs, we will refund your premium payment(s) if cancelled within the first seven days.

| Transamerica Structured Index AdvantageSM Annuity | 1 |

PHASES OF THE POLICY

The Policy, like all deferred annuity policies, has two phases: (1) an “accumulation phase” for savings and (2) an “income phase” for a stream of income.

The Accumulation Phase

You should consider the following important features of the accumulation phase:

| • | Policy Value. At all times during the accumulation phase, the current value of your investment is reflected as your Policy Value. Your Policy Value generally equals the total value of your investment in the Policy’s investment options, as well as any amounts being held in the Fixed Holding Account. |

| • | Index-Linked and Fixed Interest Investment Options. To help you accumulate assets during the accumulation phase, you can invest your premium payments in (and at certain times transfer Policy Value among) the investment options that we make available. These investment options may include index-linked options (“Index Accounts” or “Index Account Options”) and a fixed interest option (the “Fixed Account”). |

We may also refer to these investment options individually as an “Allocation Account” and collectively as “Allocation Accounts.” The performance of your Policy will vary depending on the performance of the Allocation Accounts that you choose. Each Allocation Account has its own unique risks. Please note that a specific Allocation Account, including the Fixed Account, may not always be available for investment by new or existing investors.

If you invest in an Index Account, the Index Account may provide only limited protection against loss. Your losses could be significant.

| • | Crediting Periods. Each Allocation Account has an investment term, expressed in years, representing the duration of an investment in that Allocation Account (a “Crediting Period”). |

| • | For an Index Account, gain or loss is generally applied to your Policy at the end of the Crediting Period. Gain or loss may also be applied before the end of the Crediting Period when certain transactions are performed under the Policy, but there are additional risks associated with such interim gain or loss calculations that may decrease gains or increase losses. |

| • | For the Fixed Account, interest is credited to your Policy each day until the end of the Crediting Period. |

At the end of the Crediting Period for an Allocation Account, you may choose to reinvest in the same Allocation Account for another Crediting Period, based on the rates that we declare for the upcoming Crediting Period, if we make that Allocation Account available for investment. At least 21 days before the end of each Crediting Period, we will send you a personalized letter informing you, among other information, of the Allocation Accounts that will be available for investment at the end of the Crediting Period (the “Renewal Letter”).

Please note that if you invest in the same Allocation Account at different times, it is possible that you may have multiple ongoing Crediting Periods for the same Allocation Account.

| • | Transfers Between Investment Options. You may transfer Policy Value between Allocation Accounts only at certain times. You are permitted to transfer Policy Value from an Allocation Account in which you are currently invested only at the end of that Allocation Account’s Crediting Period. Policy Value transferred into an Allocation Account cannot be applied to an ongoing Crediting Period. This means when you transfer Policy Value between Allocation Accounts, it must be at the start of a new Crediting Period for the Allocation Account receiving the transfer. |

| Transamerica Structured Index AdvantageSM Annuity | 2 |

| • | Access to Your Money. You may take withdrawals from your Policy at any time during the accumulation phase. |

| • | If you take a full withdrawal from the Policy (a Surrender), you will receive your Policy’s cash value. Your cash value is equal to the Policy Value less any surrender charges, if applicable. If your cash value is lower than the Minimum Required Cash Value upon Surrender, you will receive the Minimum Required Cash Value. Your Policy will terminate upon Surrender. |

| • | If you take a withdrawal from the Policy that is less than a Surrender, the amount withdrawn will be deducted pro-rata from your Allocation Accounts unless you instruct us otherwise. In general, the minimum withdrawal amount is $500. Withdrawals may be subject to surrender charges and may trigger the deduction of other fees and charges. |

You should carefully consider the risks and consequences associated with a Surrender or withdrawal under the Policy. Surrender charges that may apply upon Surrender or withdrawal may be significant. In addition, a Surrender or withdrawal prior to the end of a Crediting Period may significantly reduce the value of your investment and result in losses.

| • | Additional Premium Payments. You may make additional premium payments during the accumulation phase, subject to certain restrictions. An additional premium payment may be invested in one or more of the Allocation Accounts that are available for investment at that time. The allocation of your additional premium payment among the Allocation Accounts must be in whole percentages and total 100%. The minimum additional premium payment is $50. |

| • | Death Benefit. The Policy includes a death benefit that will become payable if the Annuitant dies during the accumulation phase (unless the Annuitant is not the Owner). Under the Policy’s standard death benefit, for which there is no additional charge, the death benefit will be no less than the Policy Value but may be greater under certain circumstances. You may elect the optional Guaranteed Minimum Death Benefit (GMDB) rider when you purchase the Policy, which may increase the amount payable compared to the standard death benefit. Under limited circumstances, the GMDB rider may be re-elected after termination. Depending on the Annuitant’s age when you purchase the Policy (or re-elect the rider), there may be an additional fee for this optional death benefit. If your election of the GMDB rider would not subject your Policy to an additional fee, the GMDB rider will be automatically added to your Policy. |

The Income Phase

After your third Policy Anniversary (or earlier if required by state law), you may elect to annuitize your Policy, converting your accumulated assets into a stream of guaranteed income payments from us. This is the Policy’s income phase. The Policy includes multiple fixed income options from which you can select.

If you have not annuitized your Policy by the Policy Anniversary on or following the Annuitant’s 99th birthday (or earlier if required by state law), your Policy will automatically enter the income phase. If you have not elected a fixed income option at that time, the fixed income option “Life with 10 Years Certain” will be selected for you unless we agree to another method of payment.

When your Policy enters the income phase, the accumulation phase ends. You cannot invest in any Allocation Accounts during the income phase, and you cannot withdraw money from your Policy during the income phase. The death benefit from the accumulation phase terminates at the beginning of the income phase (including any optional death benefit rider), although certain fixed income options may provide for an amount payable upon death.

FEES AND CHARGES

Charges for Early Withdrawals (Surrender Charges). If you take a withdrawal from your Policy, or Surrender your Policy, during the first 6 years after you purchase the Policy or make an additional premium payment, you will be assessed a surrender charge of up to 8% (as a percentage of premium payments withdrawn), declining to 0% over that time period. For example, if you were to withdraw $100,000 during the surrender charge period, you could be assessed a charge of up to $8,000 on the amount withdrawn.

| Transamerica Structured Index AdvantageSM Annuity | 3 |

Surrender charges do not apply to certain amounts withdrawn during the surrender charge period, regardless of whether such amounts are withdrawn as part of a withdrawal or Surrender.

| • | Earnings (if any) may be withdrawn at any time without surrender charges. |

| • | Each Policy Year, up to 10% of your total premium payments (less any amounts withdrawn in the same Policy Year that were not subject to surrender charges) may be withdrawn without surrender charges. |

| • | Surrender charges will be waived if you or your spouse become confined to a hospital or nursing facility, terminally ill, or unemployed and otherwise satisfy the conditions of the waiver. Withdrawals taken to satisfy Required Minimum Distribution requirements under the Internal Revenue Code are not subject to surrender charges. See ACCESS TO YOUR MONEY – SURRRENDER CHARGE WAIVERS. |

Ongoing Fees and Charges. Listed below are the fees and charges you may pay each year under the Policy. Please refer to your Policy’s specifications page for information about the specific fees and charges that apply to you.

| • | Service Charge. We may deduct a service charge from your Policy on each Policy Anniversary prior to the Annuity Commencement Date. If we deduct this annual charge, it will not exceed 2% (as a percentage of your Policy Value) or a maximum of $50, whichever is less, and we will waive the charge if your Policy Value, or if your total premium payments minus prior withdrawals, on a Policy Anniversary is at least equal to the minimum amount specified in your Policy. This charge will be deducted on a pro-rated basis if you Surrender the Policy. |

| • | Optional Death Benefit Fee. If you elect the optional Guaranteed Minimum Death Benefit (GMDB) rider, you may be subject to an additional fee of up to 2% (as an annualized percentage of the guaranteed minimum death benefit) depending on the Annuitant’s age on the date that you sign the application for the Policy (or, under limited circumstances, apply to re-elect the GMDB rider). This fee will be deducted on a quarterly basis. This fee will be deducted on a pro-rated basis if the rider is terminated. |

The GMDB rider fee percentages that may apply to you are disclosed in a Rate Sheet Prospectus Supplement. All Rate Sheet Prospectus Supplements are available on the SEC’s EDGAR system at www.sec.gov (Central Index Key (CIK) 0001164098). You may also visit www.transamerica.com or contact our Administrative Office for the Rate Sheet Prospectus Supplement applicable to you.

Transaction Charges. Other than surrender charges, the following transaction charges may apply under the Policy:

| • | Credit Advantage Fee. If you invest in an Index Account Option with a Credit Advantage Growth Opportunity Type, you will pay an additional fee for the increased upside potential associated with that Index Account Option. The fee will not exceed 6.0% (as a percentage of your Policy Value allocated to that Index Account Option on the first day of the Crediting Period). The fee (or a portion of the fee) will also be deducted when amounts are withdrawn from the Index Account Option as a result of a Surrender or withdrawal prior to the end of the Crediting Period. |

| • | Special Service Fees. We may deduct a charge for various special services that may be requested, such as overnight delivery and duplicate policies. The fees charged for any such service will vary, but will not exceed $50. See Special Service Fees, below for more information. |

TYPES OF ACCOUNTS

Fixed Holding Account

Before an initial or additional premium payment is allocated to one or more Allocation Accounts, it will be held in the Fixed Holding Account until the next upcoming 1st, 8th, 15th, or 22nd calendar day of any month, whichever occurs first. On such day, the premium payment (plus any accrued interest) will be allocated to the appropriate Allocation Account(s) and the Crediting Period(s) will begin on that day.

| Transamerica Structured Index AdvantageSM Annuity | 4 |

If a premium payment is received on the 1st, 8th, 15th, or 22nd calendar day, it will be allocated on the next 1st, 8th, 15th, or 22nd calendar day of any month, whichever occurs first.

Amounts held in the Fixed Holding Account are credited compound interest daily based on the fixed annual interest rate in effect at that time. We may change the current annual interest rate for the Fixed Holding Account at any time at our discretion, subject to the guaranteed minimum effective annual interest rate described in this prospectus.

Please note that while premium payments are held in the Fixed Holding Account pending their allocation to one or more Allocation Accounts, the Fixed Holding Account is not an investment option that you can select for investment.

Fixed Account

If we offer the Fixed Account and you select it for investment, we guarantee your principal and a fixed annual interest rate for the length of the applicable Crediting Period. We will credit compound interest daily throughout the Crediting Period based on the annual interest rate we declared for that Crediting Period. We may offer Crediting Periods for the Fixed Account ranging from 1 to 6 years in length.

We currently offer the Fixed Account with a 1-year Crediting Period and we may choose to offer longer Crediting Periods for the Fixed Account from time to time. We will continue to offer the Fixed Account with a 1-year Crediting Period for so long as that Allocation Account is designated by us as the Default Option.

We will declare the annual interest rate for a Crediting Period prior to the beginning of the Crediting Period. We guarantee that the annual interest rate declared for a Crediting Period will not change. However, the annual interest rates we declare may differ from Crediting Period-to-Crediting Period and may differ based on the lengths of the Crediting Periods offered.

We determine annual interest rates for the Fixed Account at our discretion, subject to the guaranteed minimum effective annual interest rate described in this prospectus.

Index Accounts

Generally. When you invest in an Index Account Option, your investment begins on the first day of the Crediting Period and generally ends on the last day of the Crediting Period. There are certain events that could end your investment before the last day of the Crediting Period, such as if you take a full withdrawal from that Index Account Option, Surrender the Policy, or annuitize the Policy, or if the death benefit becomes payable, before the end of the Crediting Period.

At the end of the Crediting Period, we apply gain or loss to your Policy based on how the Index Account Option performed. The Index Account Option’s performance is linked to the performance of a specific market index or exchange-traded fund (the “Index”). The Index’s performance is generally measured by calculating the net percentage change in the value of the Index (the “Index Change”) between the first day of the Crediting Period (the “Initial Index Value”) and the last day of the Crediting Period (the “Final Index Value”).

For example, regardless of how the Index otherwise performed between the beginning and end of the Crediting Period:

| • | If the Initial Index Value is 1000 and the Final Index Value is 1100, the Index Change would be +10% (i.e., (1100/1000) – 1 = 10%). |

| • | Likewise, if the Initial Index Value is 1000 and the Final Index Value is 900, the Index Change would be -10% (i.e., (900/1000) – 1 = -10%). |

| Transamerica Structured Index AdvantageSM Annuity | 5 |

As a general matter (excluding the impact of fees and charges):

| • | When the Index Change at the end of the Crediting Period is positive, your Policy gains value. The extent to which you participate in the positive Index performance depends on the Index Account Option’s “Growth Opportunity Type.” |

| • | When the Index Change at the end of the Crediting Period is zero, your Policy will not lose value as a result of the Index performance. Nor will your Policy gain value unless the Growth Opportunity Type for the Index Account Option provides for gain even when the Index Change is zero. |

| • | When the Index Change at the end of the Crediting Period is negative, your Policy will lose value only to the extent that the Index Account Option’s downside protection does not protect you from that loss. The downside protection provided by an Index Account Option will depend on its “Downside Protection Type.” |

Index Account Option Value. The value of your investment in an Index Account Option at the end of a Crediting Period is represented by your Index Account Option Value. Your Index Account Option Value is calculated by applying the “Index Credit Rate” to your “Index Base.”

| • | Index Credit Rate / Index Credit. The Index Credit Rate represents the percentage gain or loss that we apply to your Index Account at the end of the Crediting Period (before any fees and charges). Your gain or loss can also be expressed as a dollar amount, which we then refer to as the “Index Credit.” |

The Index Credit Rate and the Index Credit may be positive, negative, or zero.

| • | Index Base. Your Index Base generally represents your principal investment in the Index Account Option. On the first day of the Crediting Period, your Index Base equals the dollar amount that you allocated to that Index Account Option. Your Index Base for that Index Account Option will not change unless a fee or charge is deducted from that Index Account Option, or if you take a withdrawal from that Index Account Option, before the end of the Crediting Period, in which case your Index Base will be subject to a negative adjustment at that time. |

When your Index Base is subject to a negative adjustment, your Index Base will be reduced by a proportion equal to the reduction in your Interim Value (discussed below), which will be reduced dollar-for-dollar based on the amount deducted from the Index Account Option. There is no way to increase your Index Base during a Crediting Period, and therefore no way to reverse or offset the negative impact of a negative adjustment to your Index Base.

A negative adjustment to your Index Base could result in less gain (if any) or more loss at the end of a Crediting Period, perhaps significantly less gain or more loss, because the Index Credit Rate will be applied to a lower Index Base. All withdrawals taken, and fees and charges deducted, before the end of a Crediting Period will trigger a negative adjustment to your Index Base, even fees and charges that are periodically deducted from your Policy. A negative adjustment to your Index Base may be greater than the reduction in your Interim Value. See APPENDIX B: ADDITIONAL EXAMPLES FOR INDEX ACCOUNT OPTIONS for examples of how your Index Base could be negatively adjusted as a result of a fee or withdrawal.

The following is an example of how we calculate your Index Account Option Value at the end of a Crediting Period: Assume you invest $10,000 in an Index Account Option. At the beginning of the Crediting Period, your Index Base is $10,000. At the end of the Crediting Period, your Index Base is still $10,000, assuming there were no deductions for fees or withdrawals before the end of the Crediting Period. At the end of the Crediting Period, we will apply the Index Credit Rate to your Index Base to calculate your Index Account Option Value.

| • | Assuming an Index Credit Rate of +10%, your Index Account Option Value would equal $11,000 (i.e., $10,000 x (1 + 10%) = $11,000). The Index Credit is +$1,000. |

| • | Assuming an Index Credit Rate of -10%, your Index Account Option Value would equal $9,000 (i.e., $10,000 x (1 + -10%) = $9,000). The Index Credit is -$1,000. |

| Transamerica Structured Index AdvantageSM Annuity | 6 |

Interim Values. Please note that we do calculate the value of your investment in an Index Account Option each Business Day between the first and last day of the Crediting Period (each, an “Interim Value”). The Interim Value on a given Business Day determines the amount available from that Index Account Option for withdrawals, Surrender, annuitization, and the death benefit and to pay fees and charges. The Interim Value is calculated at the end of a Business Day.

Similar to the end of a Crediting Period, we calculate Interim Values by applying a percentage gain or loss to your Index Base. However, we calculate the percentage gain or loss for each Interim Value differently than the percentage gain or loss at the end of the Crediting Period. Our process for calculating Interim Values is explained in detail in APPENDIX A: INTERIM VALUE CALCULATIONS AND EXAMPLES.

Gains and losses for Interim Values are not directly tied to the performance of the Index for the Index Account Option. In general, we calculate gains and losses by using a formula that looks to the values of certain derivative and fixed income instruments, which is designed to produce an estimated fair value for your investment in the Index Account Option on that Business Day. The estimated fair value is intended to reflect factors such as the likelihood, and magnitude of, a positive or negative Index Credit Rate at the end of the Crediting Period, the length of time remaining in the Crediting Period, and the risk of loss and the possibility of gain at the end of the Crediting Period.

The Interim Value for an Index Account Option may change each Business Day, and the change may be positive or negative compared to the last Business Day (even when the Index has increased in value). You should understand that the Interim Value for an Index Account Option on a Business Day will not impact the future performance of that Index Account Option for the remainder of the Crediting Period unless one of the following occurs on that Business Day:

| • | A fee or charge is deducted from the Index Account Option; |

| • | An amount is deducted from the Index Account Option as a result of a withdrawal or Surrender; |

| • | The Policy is annuitized; or |

| • | The death benefit is paid. |

In any of those circumstances—including the deduction of a periodic fee or charge—the transaction will be processed based on the Interim Value for that Index Account Option on that Business Day. Interim Values for an Index Account Option generally reflect less upside potential and less downside protection than would otherwise apply at the end of the Crediting Period. As such, when a transaction is processed based on an Interim Value, the Interim Value could reflect less gain or more loss (perhaps significantly less gain or more loss) than would be applied at the end of the Crediting Period. This means that there could be significantly less money available under your Policy for fees and charges, withdrawals, a Surrender, annuitization, and the death benefit.

TYPES OF INDEX ACCOUNT OPTIONS

There are two categories of Index Account Options: “Basic Index Account Options” and “Enhanced Index Account Options.”

| • | Basic Index Account Options. We may offer a variety of different Basic Index Account Options. The Basic Index Account Options that we offer will have different combinations of Indexes, Crediting Periods, Growth Opportunity Types, and Downside Protection Types. |

We may also offer Basic Index Account Options for an additional fee that include “Credit Advantage” Growth Opportunity Types, which have increased upside potential compared to a Basic Index Account Option that does not have the Credit Advantage feature but is otherwise identical.

There is no guarantee that the increased upside potential of a Credit Advantage Growth Opportunity Type will result in gains at least equal to the additional fee or any gains at all. The additional fee would increase any losses or decrease any gains.

| Transamerica Structured Index AdvantageSM Annuity | 7 |

| • | Enhanced Index Account Options. Currently, we may offer two types of Enhanced Index Account Options: “Best Entry” and “Buffer Auto Reset.” We refer to these Index Account Options as “enhanced” because they include additional features that may help increase gains or decrease losses. There are no additional fees if you select an Enhanced Index Account Option. |

The following two sections, ADDITIONAL INFORMATION ABOUT BASIC INDEX ACCOUNT OPTIONS and ADDITIONAL INFORMATION ABOUT ENHANCED INDEX ACCOUNT OPTIONS, provide additional information about these two categories of Index Account Options, including how gains and losses are calculated at the end of a Crediting Period.

ADDITIONAL INFORMATION ABOUT BASIC INDEX ACCOUNT OPTIONS

Each Basic Index Account Option that we offer for investment combines one Index, one Crediting Period, one Growth Opportunity Type, and one Downside Protection Type from those listed in the tables below. For example, we may offer as a Basic Index Account Option: S&P 500® Index, 1-Year Crediting Period, Cap, and Buffer (with specific rates that we declare for the Cap and Buffer). We will typically offer a variety of Basic Index Account Options from which you may choose. However, you are not permitted to design your own Basic Index Account Options.

| Indexes |

Crediting |

Growth Opportunity Types |

Downside | |||

| • S&P 500® Index • S&P 500 Market Opportunity Allocator 1.0% Decrement Index • Fidelity World Factor Leaders IndexSM 0.5% AR • iShares® Russell 2000 ETF • iShares® U.S. Technology ETF • iShares® MSCI Emerging Markets ETF • iShares® MSCI USA ESG Select ETF |

1-10 Years | Includes no additional fee: • Cap • Cap+ Accelerator • Participation • Accelerated Tiered Participation • Value Trigger • Value Trigger+ Includes an additional fee: • Credit Advantage Cap • Credit Advantage Participation • Credit Advantage Value Trigger+ |

• Buffer • Floor • Buffer and Floor • Participation |

Calculating Gain Using the Growth Opportunity Type

At the end of the Crediting Period for a Basic Index Account Option, if the Index Change is positive or zero, we use the applicable Growth Opportunity Type to calculate your gain, if any. Each Basic Index Account Option has only one Growth Opportunity Type.

This section summarizes how we calculate an Index Credit Rate using the different Growth Opportunity Types for the Basic Index Account Options. You should refer to the examples later in this prospectus to further help you understand how an Index Credit Rate for a Basic Index Account Option will be calculated when the Index Change is positive or zero. See ADDITIONAL INFORMATION ABOUT BASIC INDEX ACCOUNT OPTIONS – CALCULATING GAIN USING THE GROWTH OPPORTUNITY TYPE later in this prospectus.

A Growth Opportunity Type may limit your participation in positive Index performance, limiting the upside potential of your investment.

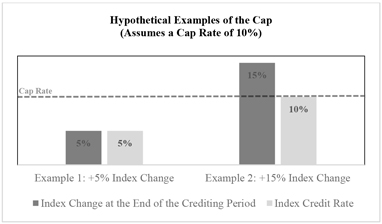

| 1. | Cap |

Cap. For a Basic Index Account Option with a Cap as its Growth Opportunity Type, if the Index Change at the end of the Crediting Period is positive, the value of your investment will increase. If the Index Change is zero, the value of your investment will neither increase nor decrease.

| Transamerica Structured Index AdvantageSM Annuity | 8 |

We calculate your Index Credit Rate using the Cap as follows:

| • | If the Index Change is positive and less than or equal to the Cap Rate, your Index Credit Rate will equal the Index Change. |

| • | If the Index Change is positive and exceeds the Cap Rate, your Index Credit Rate will equal the Cap Rate. |

| • | If the Index Change is zero, your Index Credit Rate will equal zero. |

Under this Growth Opportunity Type, you will not participate in any Index performance above the Cap Rate. The Cap Rate limits the upside potential of your investment.

Credit Advantage Cap. When we offer a Basic Index Account Option that has a Cap as its Growth Opportunity Type, we may offer for an additional fee an identical Basic Index Account Option except with a Credit Advantage Cap as its Growth Opportunity Type. We calculate the Index Credit Rate using a Credit Advantage Cap the same way as a Cap, except that the Cap Rate for the Basic Index Account Option with the Credit Advantage Cap will be higher than the otherwise identical Basic Index Account Option with the Cap. The Credit Advantage Cap therefore provides more upside potential in exchange for the additional fee.

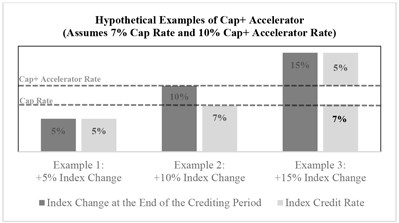

| 2. | Cap+ Accelerator |

For a Basic Index Account Option with Cap+ Accelerator as its Growth Opportunity Type, if the Index Change at the end of the Crediting Period is positive, the value of your investment will increase. If the Index Change is zero, the value of your investment will neither increase nor decrease.

We calculate your Index Credit Rate using Cap+ Accelerator as follows:

| • | If the Index Change is less than or equal to the Cap Rate, your Index Credit Rate will equal the Index Change. |

| • | If the Index Change exceeds the Cap Rate but does not exceed the Cap+ Accelerator Rate, your Index Credit Rate will equal the Cap Rate. |

| • | If the Index Change exceeds both the Cap Rate and the Cap+ Accelerator Rate, your Index Credit Rate will equal the Cap Rate plus a percentage equal to the excess Index Change over the Cap+ Accelerator Rate. |

| • | If the Index Change is zero, your Index Credit Rate will equal zero. |

While Cap+ Accelerator potentially presents more upside potential compared to the Cap Growth Opportunity Type by allowing you to potentially participate in Index performance that exceeds the Cap Rate, this Growth Opportunity Type also limits the upside potential of your investment because you will not participate in any Index performance between the Cap Rate and the Cap+ Accelerator Rate.

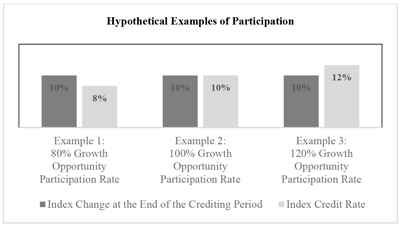

| 3. | Participation |

Participation. For a Basic Index Account Option with Participation as its Growth Opportunity Type, if the Index Change at the end of the Crediting Period is positive, the value of your investment will increase. If the Index Change is zero, the value of your investment will neither increase nor decrease.

We calculate your Index Credit Rate by multiplying the Index Change by the Growth Opportunity Participation Rate.

If the Growth Opportunity Participation Rate is less than 100%, you will not fully participate in positive Index performance, limiting the upside potential of your investment. We may offer Growth Opportunity Participation Rates greater than 100%, which would have the effect of increasing your gains relative to the Index Change.

| Transamerica Structured Index AdvantageSM Annuity | 9 |

Credit Advantage Participation. When we offer a Basic Index Account Option with Participation as its Growth Opportunity Type, we may offer for an additional fee an identical Basic Index Account Option except with Credit Advantage Participation as its Growth Opportunity Type. We calculate the Index Credit Rate using Credit Advantage Participation the same way as Participation, except that the Growth Opportunity Participation Rate for the Basic Index Account Option with Credit Advantage Participation will be higher than the Growth Opportunity Participation Rate for the otherwise identical Basic Index Account Option with Participation. Credit Advantage Participation therefore provides more upside potential in exchange for the additional fee.

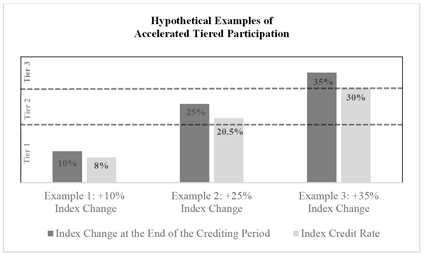

| 4. | Accelerated Tiered Participation |

For a Basic Index Account Option with Accelerated Tiered Participation as its Growth Opportunity Type, if the Index Change at the end of the Crediting Period is positive, the value of your investment will increase. If the Index Change is zero, the value of your investment will neither increase nor decrease.

We calculate your Index Credit Rate using Accelerated Tiered Participation as follows:

| • | If the Index Change does not exceed the first Tier Level, your Index Credit Rate will equal the Index Change multiplied by the Tier Participation Rate for the first Tier Level. |

| • | If the Index Change exceeds the first Tier Level and there are only two Tier Levels, your Index Credit Rate will equal the sum of (i) the portion of the Index Change within the first Tier Level multiplied by the Tier Participation Rate for that Tier Level and (ii) the portion of the Index Change within the second Tier Level multiplied by the Tier Participation Rate for that Tier Level. |

| • | If we have declared more than two Tier Levels, we calculate your Index Credit Rate using the same process, applying the additional Tier Level(s) and Tier Participation Rate(s) as appropriate based on the Index Change. |

If the Tier Participation Rate that we declare for any Tier Level is less than 100%, you may not fully participate in the positive Index performance, limiting the upside potential of your investment. We may offer Tier Participation Rates greater than 100%, which could have the effect of increasing your gains relative to the Index Change depending on the other Tier Participation Rates and the Index Change.

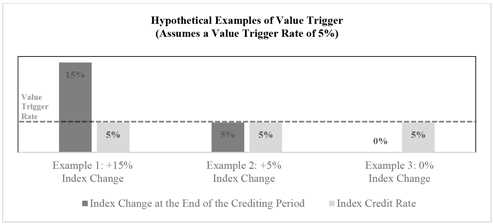

| 5. | Value Trigger |

For a Basic Index Account Option with Value Trigger as its Growth Opportunity Type, if the Index Change at the end of the Crediting Period is positive or zero, the value of your investment will increase.

Your Index Credit Rate will equal the Value Trigger Rate.

While Value Trigger will result in an increase in the value of your investment so long as the Index Change at the end of the Crediting Period is positive or zero, you will not participate in any Index performance in excess of the Value Trigger Rate, which limits the upside potential of your investment.

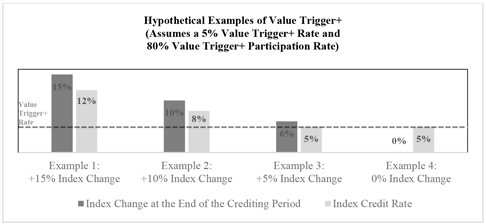

| 6. | Value Trigger+ |

Value Trigger+. For a Basic Index Account Option with Value Trigger+ as its Growth Opportunity Type, if the Index Change at the end of the Crediting Period is positive or zero, the value of your investment will increase.

Your Index Credit Rate will equal the greater of (a) the Value Trigger+ Rate or (b) the Index Change multiplied by the Value Trigger+ Participation Rate.

While Value Trigger+ potentially has increased upside potential compared to the Value Trigger Growth Opportunity Type because Value Trigger+ potentially allows you to participate in positive Index performance in excess of the Value Trigger+ Rate, this Growth Opportunity Type may also limit the upside potential of your investment. This is because you will not fully participate in any positive Index performance in excess of the Value Trigger+ Rate if the Value Trigger+ Participation Rate is less than 100%.

| Transamerica Structured Index AdvantageSM Annuity | 10 |

Credit Advantage Value Trigger+. When we offer a Basic Index Account Option with Value Trigger+ as its Growth Opportunity Type, we may offer for an additional fee an identical Basic Index Account Option except with Credit Advantage Value Trigger+ as its Growth Opportunity Type. We calculate the Index Credit Rate using Credit Advantage Value Trigger+ the same way as Value Trigger+, except that the Value Trigger+ Rate and/or Value Trigger+ Participation Rate for the Basic Index Account Option with Credit Advantage Value Trigger+ would be higher than the otherwise identical Basic Index Account Option with Value Trigger+. Credit Advantage Value Trigger+ therefore provides more upside potential in exchange for the additional fee.

Calculating Loss Using the Downside Protection Type

At the end of the Crediting Period for a Basic Index Account Option, if the Index Change is negative, we use the applicable Downside Protection Type to calculate your loss (if any). Each Basic Index Account Option has only one Downside Protection Type.

This section summarizes how we calculate an Index Credit Rate using the different Downside Protection Types for the Basic Index Account Options. You should refer to the examples later in this prospectus to further help you understand how an Index Credit Rate for a Basic Index Account Option will be calculated when the Index Change is negative. See ADDITIONAL INFORMATION ABOUT BASIC INDEX ACCOUNT OPTIONS – CALCULATING LOSS USING THE DOWNSIDE PROTECTION TYPE later in this prospectus.

A Downside Protection Type may provide only limited protection against loss. Your losses could be significant.

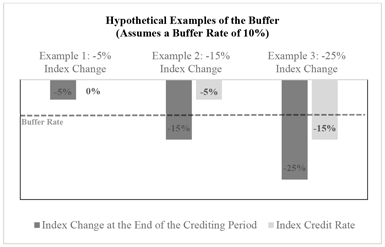

| 1. | Buffer |

For a Basic Index Account Option with a Buffer as its Downside Protection Type, if the Index Change at the end of the Crediting Period is negative, the value of your investment will decrease only to the extent that the Buffer does not protect you from loss.

We calculate your Index Credit Rate using the Buffer as follows:

| • | If the Index Change does not exceed the Buffer Rate, your Index Credit Rate will equal 0%. Under these circumstances, the Buffer would provide complete protection from loss related to the negative Index performance. |

| • | If the Index Change exceeds the Buffer Rate, your Index Credit Rate will be a percentage equal to the excess Index Change over the Buffer Rate. Under these circumstances, the Buffer would provide only partial protection from loss related to the negative Index performance. |

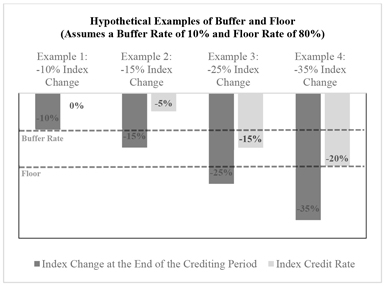

The Buffer Rate represents the percentage of your investment that is protected from loss. For instance, assuming a Buffer Rate of 10%, it is possible that you could lose 90% of your investment as a result of negative Index performance. Unlike with a Floor, however, a Buffer absorbs the impact of negative Index performance before negative Index performance impacts your Policy.

The Buffer’s downside protection is limited. You assume the risk of loss for negative Index performance in excess of the Buffer Rate. Your losses could be significant.

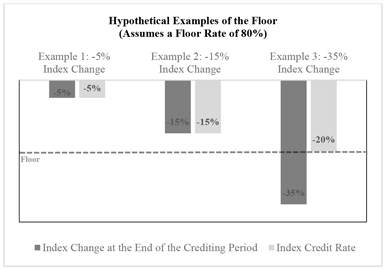

| 2. | Floor |

For a Basic Index Account Option with a Floor as its Downside Protection Type, if the Index Change at the end of the Crediting Period is negative, the value of your investment will decrease, but it will not decrease beyond the downside protection provided by the Floor.

We calculate your Index Credit Rate using the Floor as follows:

| • | If the Index Change does not exceed the Floor based on the Floor Rate, your Index Credit Rate will equal the Index Change. |

| • | If the Index Change exceeds the Floor based on the Floor Rate, your Index Credit Rate will equal the Floor. |

| Transamerica Structured Index AdvantageSM Annuity | 11 |

The Floor Rate represents the percentage of your investment that is protected from loss. For instance, assuming a Floor Rate of 80%, it is possible that you could lose up to 20% of your investment as a result of negative Index performance, which means the Index Credit Rate could be as low as -20%. Unlike with a Buffer, however, your Policy is impacted by negative Index performance before any negative Index performance is absorbed by the Floor.

If the Floor Rate is 100%, the Floor provides complete protection from loss related to the negative Index performance. The Index Credit Rate cannot be lower than 0% when the Floor Rate equals 100%.

When the Floor Rate is less than 100%, the Floor provides only limited downside protection. You assume the risk of loss for negative Index performance that does not exceed the Floor based on the Floor Rate. Your losses could be significant depending on the Floor Rate. A Floor Rate of 100% would provide complete protection against loss, but is likely to be part of an Index Account Option with significantly limited upside potential.

| 3. | Buffer and Floor |

The Buffer and Floor Downside Protection Type is a combination of the Buffer Downside Protection Type and the Floor Downside Protection Type. If the Index Change at the end of the Crediting Period is negative, the value of your investment may or may not decrease.

For a Basic Index Account with Buffer and Floor as its Downside Protection Type, if the Index Change at the end of the Crediting Period is negative, we will apply either the Buffer (based on the Buffer Rate) or the Floor (based on the Floor Rate) to calculate your loss (if any), whichever results in less loss (or no loss) for you.

Buffer and Floor does not provide complete downside protection. You may lose any amounts not protected by the Buffer or Floor, whichever ultimately applies. Your losses could be significant.

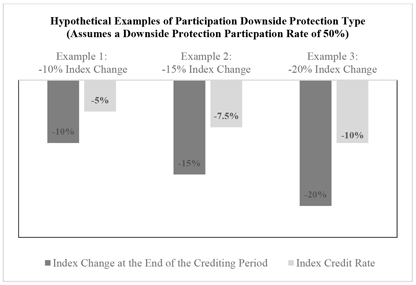

| 4. | Participation |

For a Basic Index Account Option with Participation as its Downside Protection Type, if the Index Change at the end of the Crediting Period is negative, the value of your investment will decrease, but you will participate in only a portion of the negative Index performance.

Your Index Credit Rate will equal the Index Change multiplied by the Downside Protection Participation Rate.

Participation as a Downside Protection Type does not provide complete downside protection. Participation as a Downside Protection Type provides only limited downside protection by limiting the extent to which you participate in negative Index performance. Your losses could be significant.

ADDITIONAL INFORMATION ABOUT ENHANCED INDEX ACCOUNT OPTIONS

Currently, we may offer two types of Enhanced Index Account Options. The first type is called “Best Entry.” The second type is called “Buffer Auto Reset.” Each Enhanced Index Account Option that we may currently offer includes the following four components: (1) an Index, (2) a Crediting Period, (3) a Cap for the Growth Opportunity Type, and (4) a Buffer for the Downside Protection Type, as reflected in the following tables:

| Indexes |

Crediting Periods |

Growth |

Downside | |||

| • S&P 500® Index • S&P 500 Market Opportunity Allocator 1.0% Decrement Index • Fidelity World Factor Leaders IndexSM 0.5% AR • iShares® Russell 2000 ETF • iShares® U.S. Technology ETF • iShares® MSCI Emerging Markets ETF • iShares® MSCI USA ESG Select ETF |

1-10 Years | Cap | Buffer |

| Transamerica Structured Index AdvantageSM Annuity | 12 |

In addition to the Index, Crediting Period, Growth Opportunity Type, and Downside Protection Type, each Enhanced Index Account Option includes a reset feature that may help you increase gains or decrease losses, as explained further below.

Best Entry

Best Entry includes an Initial Index Value reset feature. This feature may help you increase gains or decrease losses because the Initial Index Value used to calculate the Index Change may be lower than the Index Value on the first day of the Crediting Period. As such, at the end of the Crediting Period, this feature may result in a higher Index Change (potentially increasing your gains or decreasing your losses).

At the end of the Crediting Period, we will calculate the Index Credit Rate the same way as a Basic Index Account Option with a Cap (if the Index Change is positive or zero) or Buffer (if the Index Change is negative). The only potential difference is that the Initial Index Value used to calculate the Index Change may not equal the Index Value from the first day of the Crediting Period. It may be lower.

How the Initial Index Value reset feature works:

| • | During a defined time period starting at the beginning of the Crediting Period (the “Observation Period”), we will observe the Index Value on a periodic basis (daily, weekly, monthly, or quarterly) for the purpose of determining whether the Initial Index Value should be reset to a lower Index Value (the “Observation Frequency”). The days on which we observe the Index Value are called “Observation Days.” |

| • | Each Observation Day, the Initial Index Value will automatically reset if both (i) the value of the Index has decreased by at least a certain threshold percentage (the “Best Entry Reset Threshold”) compared to the Index Value on the first day of the Crediting Period and (ii) the Index Value on that Observation Day is lower than the current Initial Index Value (taking into account any prior reset that has occurred since the beginning of the Observation Period). |

| • | By the end of the Observation Period, the reset feature will have automatically reset the Initial Index Value to the lowest observed Index Value during the Observation Period that triggered a reset (if any). The Initial Index Value at the end of the Observation Period will be used to calculate the Index Change at the end of the Crediting Period. |

For an example of the Initial Index Value reset feature, see ADDITIONAL INFORMATION ABOUT ENHANCED INDEX ACCOUNT OPTIONS – Best Entry later in this prospectus.

While Best Entry may help you increase your gains or decrease your losses, it is subject to the same risks associated with the Cap Growth Opportunity Type and the Buffer Downside Protection Type.

| • | You will not participate in any positive Index performance above the Cap Rate. If your Initial Index Value has reset, you may be more likely to realize gains at the end of the Crediting Period than if the Initial Index Value had not been reset, but the upside potential of your investment continues to be limited by the same Cap Rate. |

| • | The Buffer provides only limited downside protection. If your Initial Index Value has reset, you may be less likely to realize loss at the end of the Crediting Period than if the Initial Index Value had not been reset, but you still assume the risk of loss for negative Index performance in excess of the same Buffer Rate. Your losses could be significant. |

| Transamerica Structured Index AdvantageSM Annuity | 13 |

Buffer Auto Reset

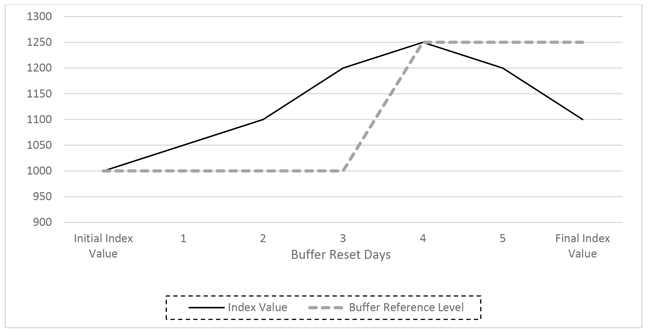

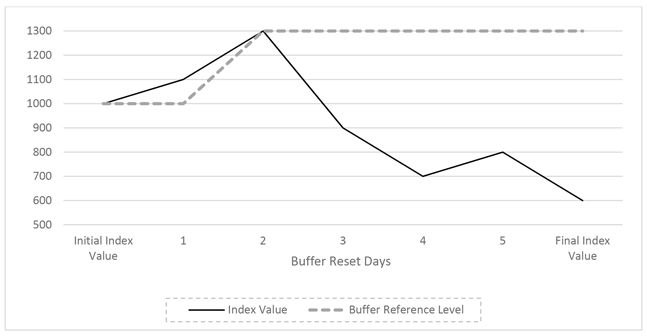

This Enhanced Index Account Option includes a Buffer reset feature. This feature utilizes the Buffer in a manner that is different than any other Index Account Option by not only providing limited protection from loss, but also potentially protecting gains.

For all other Index Account Options that have a Buffer as a Downside Protection Type, the Buffer applies only when the Index Change is negative. As a result, the Buffer for any such Index Account Option only provides downside protection. If the Index Change is positive, the Buffer for any such Index Account Option plays no role in calculating gain.

Under Buffer Auto Reset, the Buffer not only applies when the Index Change is negative, but it may also apply when the Index Change is positive. By potentially applying the Buffer when the Index Change is positive, Buffer Auto Reset may protect potential gains from downward fluctuations in the performance of an Index during a Crediting Period.

How the Buffer reset feature works:

| • | Under Buffer Auto Reset, the Buffer’s protection is tied to the “Buffer Reference Level.” At the beginning of the Crediting Period, the Buffer Reference Level will be the Initial Index Value (i.e., the Index Value on the first day of the Crediting Period). |