Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - OneWater Marine Inc. | brhc10017490_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - OneWater Marine Inc. | brhc10017490_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - OneWater Marine Inc. | brhc10017490_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - OneWater Marine Inc. | brhc10017490_ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - OneWater Marine Inc. | brhc10017490_ex23-1.htm |

| EX-21.1 - EXHIBIT 21.1 - OneWater Marine Inc. | brhc10017490_ex21-1.htm |

| EX-4.1 - EXHIBIT 4.1 - OneWater Marine Inc. | brhc10017490_ex4-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended September 30, 2020

OR

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ___________ to __________

Commission File Number 001-39213

OneWater Marine Inc.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware

|

83-4330138

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(IRS Employer Identification No.)

|

|

6275 Lanier Islands Parkway

Buford, Georgia

|

30518

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (678) 541-6300

Securities registered pursuant to Section 12(b) of the Exchange Act:

|

Title of Each Class

|

Trading Symbol(s)

|

Name of Each Exchange on Which Registered

|

||

|

Class A common stock, par value $0.01 per share

|

ONEW

|

The Nasdaq Global Market

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period

that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12

months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large

accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

Non-accelerated filer ☒

|

Smaller reporting company ☒

|

|

Emerging growth company ☒

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to

Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the

Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based on the closing price of the shares of common shares on The Nasdaq Stock Market on March 31, 2020,

was $53,880,098.

The registrant had 10,779,119 shares of Class A common stock, par value $0.01 per share, and 4,196,179 shares of Class B common stock, par value $0.01 per share, outstanding as of November 30, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement relating to the 2021 Annual Meeting of Shareholders, to be filed within 120 days of the Registrant’s fiscal year ended September 30, 2020, are incorporated by

reference into Part III of this Annual Report on Form 10-K.

|

PART I

|

|||

|

Item 1.

|

3

|

||

|

Item 1A.

|

18

|

||

|

Item 1B.

|

46

|

||

|

Item 2.

|

46

|

||

|

Item 3.

|

47 | ||

|

Item 4.

|

47 | ||

|

PART II

|

|||

|

Item 5.

|

48

|

||

|

Item 6.

|

48

|

||

|

Item 7.

|

50

|

||

|

Item 7A.

|

75

|

||

|

Item 8.

|

76 | ||

|

Item 9.

|

106

|

||

|

Item 9A.

|

106 | ||

|

Item 9B.

|

106 | ||

|

PART III

|

|||

|

Item 10.

|

107 | ||

|

Item 11.

|

107 | ||

|

Item 12.

|

107 | ||

|

Item 13.

|

107 | ||

|

Item 14.

|

107 | ||

|

PART IV

|

|||

|

Item 15.

|

108 | ||

|

Item 16.

|

111 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

The information in this Form 10-K includes “forward-looking statements.” All statements, other than statements of historical fact included in this Form 10-K, regarding our strategy, future operations, financial

position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this Form 10-K, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,”

“project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on our current expectations and

assumptions about future events and are based on currently available information as to the outcome and timing of future events. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements

described under the heading “Risk Factors,” “Business,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this Form 10-K. These forward-looking statements are based on management’s current

belief, based on currently available information, as to the outcome and timing of future events.

Forward-looking statements may include statements about:

| • |

the impact of COVID-19 on our business and results of operations;

|

| • |

general economic conditions, including changes in employment levels, consumer demand, preferences and confidence levels, fuel prices, levels of discretionary income, consumer spending patterns and uncertainty regarding the timing, pace

and extent of an economic recovery in the United States;

|

| • |

economic conditions in certain geographic regions in which we primarily generate our revenue;

|

| • |

credit markets and the availability and cost of borrowed funds;

|

| • |

our business strategy, including acquisitions and same-store growth;

|

| • |

our ability to integrate acquired dealer groups;

|

| • |

our ability to maintain our relationships with manufacturers, including meeting the requirements of our dealer agreements and receiving the benefits of certain manufacturer incentives;

|

| • |

our ability to finance working capital and capital expenditures;

|

| • |

general domestic and international political and regulatory conditions, including changes in tax or fiscal policy and the effects of current restrictions on various commercial and economic activities in response to the COVID-19 pandemic;

|

| • |

global public health concerns, including the COVID-19 pandemic;

|

| • |

demand for our products and our ability to maintain acceptable pricing for our products and services, including financing, insurance and extended service contracts;

|

| • |

our operating cash flows, the availability of capital and our liquidity;

|

| • |

our future revenue, same-store sales, income, financial condition, and operating performance;

|

| • |

our ability to sustain and improve our utilization, revenue and margins;

|

| • |

competition;

|

| • |

seasonality and inclement weather such as hurricanes, severe storms, fire and floods, generally and in certain geographic regions in which we primarily generate our revenue;

|

| • |

our ability to manage our inventory and retain key personnel;

|

| • |

environmental conditions and real or perceived human health or safety risks;

|

| • |

any potential tax savings we may realize as a result of our organizational structure;

|

| • |

uncertainty regarding our future operating results and profitability;

|

| • |

other risks associated with the COVID-19 pandemic including, among others, the ability to safely operate our stores, access to inventory and customer demand; and

|

| • |

plans, objectives, expectations and intentions contained in this Form 10-K that are not historical.

|

We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control. Should one or more of the risks

or uncertainties occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward-looking statements. These risks include, but are not limited to, decline in demand

for our products and services, the effects of the COVID-19 pandemic on the Company’s business, the seasonality and volatility of the boat industry, our acquisition strategies, the inability to comply with the financial and other covenants and

metrics in our Credit Facilities, cash flow and access to capital, the timing of development expenditures and the other risks described under “Risk Factors” in this Form 10-K.

All forward-looking statements, expressed or implied, included in this Form 10-K are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection

with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue.

Any forward-looking statement that we make in this Form 10-K speaks only as of the date of such statement. Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements,

all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this Form 10-K.

PART I

| Item 1. |

Business.

|

OneWater Marine Inc. (“OneWater Inc.”) is a holding company and the sole managing member of One Water Marine Holdings, LLC (“OneWater LLC”), which became the principal operating subsidiary of

OneWater Inc. on February 11, 2020 in the corporate reorganization (the “Reorganization”) completed in connection with OneWater Inc.’s initial public offering (the “IPO”), which closed on February 11, 2020.

Except as otherwise indicated or required by the context, all references in this Form 10-K to the “Company,” “OneWater,” “we,” “us” or “our” relate to (i) for periods after the Reorganization,

OneWater Marine Inc. and its consolidated subsidiaries, and (ii) for periods on or prior to the Reorganization, to OneWater LLC, our accounting predecessor, and its consolidated subsidiaries. References in this Form 10-K to the “Legacy Owners”

refer to the owners of OneWater LLC as they existed immediately prior to the Reorganization, including, but not limited to, certain affiliates of Goldman Sachs & Co. LLC (collectively, “Goldman”), affiliates of The Beekman Group (collectively,

“Beekman”) and certain members of our management team.

Overview

We believe that we are one of the largest and fastest-growing premium recreational boat retailers in the United States with 61 stores comprising 21 dealer groups in 10 states. Our dealer groups are located within

highly attractive markets throughout the Southeast, Gulf Coast, Mid-Atlantic and Northeast, including Texas, Florida, Alabama, North Carolina, South Carolina, Georgia and Ohio which represent seven of the top twenty states for marine retail

expenditures. We believe that we are a market leader by volume in sales of premium boats in 12 out of the 15 markets in which we operate. In fiscal year 2020, we sold over 10,000 new and pre-owned boats, of which we believe approximately 40% were

sold to customers who had a trade-in or with whom we otherwise had established relationships. The combination of our significant scale, diverse inventory, access to premium boat brands and meaningful dealer group brand equity enables us to provide

a consistently professional experience as reflected in the number of our repeat customers and same-store sales growth.

The following table sets forth information about stores that were part of our operations as of September 30, 2020:

|

State

|

Number of

Stores

|

Percent of 2020

Revenue

|

||||||

|

Florida

|

20

|

41.2

|

%

|

|||||

|

Texas

|

8

|

16.5

|

||||||

|

Georgia

|

10

|

11.0

|

||||||

|

Alabama

|

8

|

9.1

|

||||||

|

Ohio

|

3

|

7.1

|

||||||

|

Massachusetts

|

3

|

5.6

|

||||||

|

South Carolina

|

4

|

4.1

|

||||||

|

Maryland

|

2

|

3.5

|

||||||

|

Kentucky

|

2

|

1.1

|

||||||

|

North Carolina

|

1

|

0.5

|

||||||

|

New York

|

0

|

0.3

|

||||||

|

Total

|

61

|

100.0

|

%

|

|||||

We have a diversified revenue profile that is comprised of new boat sales, pre-owned boat sales, F&I products, repair and maintenance services, and parts and accessories. Non-boat sales were approximately 9.8% of

revenue and 28.3% of gross profit in fiscal year 2020, 11.4% of revenue and 31.1% of gross profit in fiscal year 2019 and approximately 10.5% of revenue and 26.7% of gross profit in fiscal year 2018. We offer a wide array of new boats at various

price points through relationships with 50 manufacturers covering 66 brands. We are currently a top-three customer for 28 of our 66 brands and the single largest customer for each of our top five highest-selling brands. While our order volume

amounts to between 5% to 35% of total sales for those top five brands, no single brand accounts for more than 7% of our total sales volume. Additionally, our top brand only accounts for approximately 10% of new boat sales. Our relationships with

many of our manufacturers are long-standing and have been developed over multiple decades of experience in the marine industry. We believe that the strength of our relationships combined with our scale enables us to receive among the best pricing

and terms available across all of the brands and models that we carry, and we routinely evaluate the sales performance and demand for each respective brand to ensure that the economic relationship we have in place with our manufacturers optimizes

our profitability.

We were formed in 2014 as OneWater LLC through the combination of Singleton Marine and Legendary Marine, which created a marine retail platform that collectively owned and operated 19 stores. Since the combination in

2014, we have acquired a total of 41 additional stores through 17 acquisitions. Our current portfolio as of September 30, 2020 consists of 21 different local and regional dealer groups. Because of this, we believe we are one of the largest and

fastest-growing premium recreational boat retailers in the United States based on number of stores and total boats sold. While we have opportunistically opened new stores in select markets, we believe that it is generally more effective

economically and operationally to acquire existing stores with experienced staff and established reputations.

We believe that our dealer group branding strategy, which retains the name, logo and trademarks associated with each store or dealer group at the time of acquisition, significantly differentiates us from our largest

competitors who employ singular, national branding strategies. We are committed to maintaining local and regional dealer group branding because we believe that the value of retaining the goodwill and long-standing customer relationships of these

local businesses, many of which have been built by families over decades, far exceeds the benefits of attempting to establish a potentially unfamiliar “OneWater” national brand. In addition, preserving this established identity maintains the long

term engagement of former owners because their name and reputation remain figuratively and literally “on the door.”

Summary of Financial Performance for the Fiscal Year ended September 30, 2020 and Key Metrics

We have experienced significant growth in recent periods.

| • |

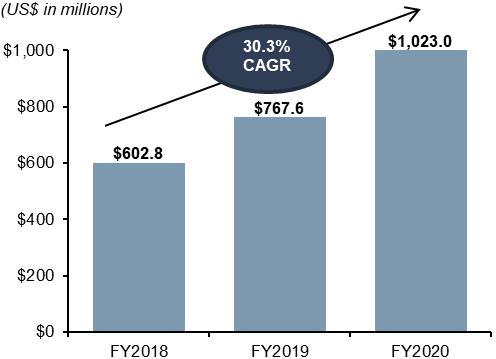

Revenue increased 33.3% to $1,023.0 million for the fiscal year ended September 30, 2020 from $767.6 million for the fiscal year ended September 30, 2019.

|

| • |

Revenue generated from same-store sales increased 24.4% for the fiscal year ended September 30, 2020 as compared to the fiscal year ended September 30, 2019.

|

| • |

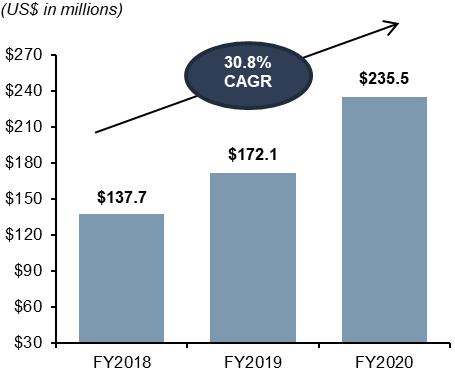

Gross profit increased 36.8% to $235.5 million for the fiscal year ended September 30, 2020 from $172.1 million for the fiscal year ended September 30, 2019.

|

| • |

Operating expenses as a percentage of revenue decreased 116 basis points for the fiscal year ended September 30, 2020 compared to the fiscal year ended September 30, 2019.

|

| • |

Net income increased to $48.5 million for the fiscal year ended September 30, 2020 from $37.3 million for the fiscal year ended September 30, 2019.

|

| • |

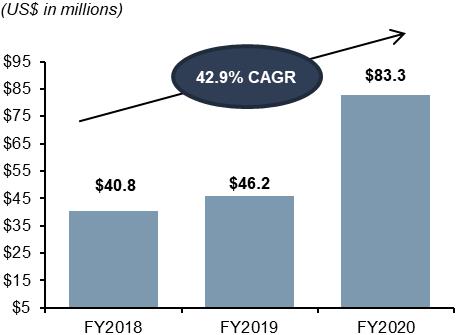

Adjusted EBITDA increased 80.1% to $83.3 million for the fiscal year ended September 30, 2020 from $46.2 million for the fiscal year ended September 30, 2019.

|

For a reconciliation of Adjusted EBITDA to net income (loss), its most directly comparable financial measure presented in accordance with GAAP, see “Management’s Discussion and Analysis of Financial Condition and

Results of Operations—Comparison of Non-GAAP Financial Measure.”

Our Market and Our Customer

Consumer spending on boats, engines, services, parts, accessories and related purchases reached $43.1 billion in 2019, up 3.1% from 2018, and has, on average, grown in excess of 5% annually since 2010. New powerboat

sales have driven market growth and reached $11.3 billion in 2019, resulting in a 12% average annual growth rate since 2010. Of the approximately one million powerboats sold in the United States each year, 80% of total units sold (approximately

809,000) are pre-owned. Relative demand for new and late-model boats has increased in recent years in part due to the continuous evolution of boat technology and design including, but not limited to, seating configurations, power, efficiency,

instrumentation and electronics, and wakesurf gates, each of which represents a material design improvement that cannot be matched by more dated boat models. We believe the increasing pace of innovation in technology and design will result in more

frequent upgrade purchases and ultimately higher sales volumes of new and late-model, pre-owned boat sales. While we continue to monitor the impact of the COVID-19 pandemic on our operations, our financial position through September 30, 2020

suggests that spending in all our regions and across product lines has proven resilient as families have increasingly focused on outdoor socially distanced recreation, driving a material increase in sales.

The boat dealership market is highly fragmented and is comprised of approximately 4,300 stores nationwide. Most competing boat retailers are operated by local business owners who own three or fewer stores, however we

do have other larger competitors including MarineMax and Bass Pro Shops. We believe we are one of the largest and fastest-growing premium recreational boat retailers in the United States. Despite our size, we comprise less than 2% of total industry

sales. Our scale and business model allow us to leverage our extensive inventory to provide consumers with the ability to find a boat that matches their preferences (e.g., make, model, color, configuration and other options) and to deliver the boat

within days while providing a personalized sales experience. We are able to operate with a comparatively higher degree of profitability than other independent retailers because we allocate support resources across our store base, focus on

high-margin products and services, utilize floor plan financing and provide core back-office functions on a scale that many independent retailers are unable to match. We seek to be the leading boat retailer by total market share within each boating

market and within the product segments in which we participate. To the extent that we are not, we will evaluate acquiring other local retailers in order to increase our sales, to add additional brands or to provide us with additional high-quality

personnel.

We believe that boating is a lifestyle that brings families and friends together regardless of their stage of life. Whether a person grew up in a household that owned a boat or experiences boating later in life, once a

person buys their first boat they often become a boating customer for life. Our customers are typically middle to upper-middle class families who either own a house on the water or live near a body of water where they can engage in boating

activities. We serve customers whose boating preferences span from general recreation and cruising to fresh and salt water fishing to watersports, including wakeboarding and wake surfing. The profile of our customers range from those in their

early-to-mid 30’s who are upgrading their house, cars and lifestyle to those who have owned multiple boats and view boating as a way of life. Our inventory and product selection allow us to cater to a highly diverse customer base with price points

and boat types that appeal to a broad spectrum of budgets and preferences. The boating industry’s and MarineMax’s average selling prices for a new boat were $56,000 in calendar year 2019 and $215,000 in fiscal year 2020, respectively. By

comparison, our average selling price for a new boat in fiscal year 2020 was $122,000.

Our Strengths

Leading Market Position and Scale: We believe we are one of the largest and fastest-growing premium recreational boat retailers in the United States, with 61 stores across 10

states. We have a strong presence in Texas, Florida, Alabama, South Carolina, Georgia, Ohio and North Carolina with 54 stores. These markets represent seven of the top twenty states for marine retail expenditures.

Differentiated Marketing and Branding Strategy: We are committed to maintaining a local and regional dealer group branding strategy and believe that retaining the goodwill and

long-standing customer relationships of dealer groups that we acquire provides significantly more value than establishing a potentially unfamiliar “OneWater” national brand across each of our stores. Preserving the existing brands enables us to

retain key staff, including senior management, which reduces or eliminates our need to hire and train new people when we complete an acquisition.

Our marketing department is able to deploy highly efficient and targeted sales campaigns due to the number of customers we have served to date and the analytics we have obtained from prior transactions. Customers who

buy boats commonly make ongoing purchases of parts, repair and maintenance services and storage. We proactively send marketing messages to anticipate when a customer may need additional repair and maintenance services in order for us to maximize

the value of a customer and to diversify our revenue streams across all revenue categories.

Seasoned Consolidator in a Highly Fragmented Market: We have an extensive acquisition track record within the boating industry and have developed a reputation for treating

sellers and their staff in an honest and fair manner. We believe our reputation and scale have positioned us as a buyer of choice for boat dealers who want to sell their businesses. To date, 100% of our acquisitions have been sourced from inbound

inquiries, and the number of annual inquiries we receive has consistently increased over time. Less than 50% of the inbound leads that we receive meet our criteria but more than 90% of the stores on which we conduct diligence are ultimately

acquired. Our acquisition and integration team has executed 17 acquisitions since 2014. Our acquisition team is typically able to convert the selling dealer groups’ back-office systems to our IT platform within approximately ten days, with full

integration of most acquisitions completed in approximately 45 days. Our strategy is to acquire stores at attractive EBITDA multiples and then grow same-store sales while benefitting from cost-reducing synergies. Historically, we have typically

acquired dealer groups for less than 4.0x EBITDA on a trailing twelve months basis and believe that we will be able to continue to make attractive acquisitions within this range.

Strong Yet Flexible Relationships with Leading Boat Manufacturers: Most of our relationships with our manufacturers are long-standing with many dating back two decades or longer.

We communicate with our manufacturers on a weekly basis to monitor our orders and make adjustments based on our current inventory levels and forecasted customer demand. Our contracts also exclude any requirements pertaining to mandatory capital

expenditures, branding and unit pricing. Furthermore, we have flexibility to change brands, subject to territory availability, at each store based on sales performance or other factors.

We are an essential customer to many of our top manufacturers and do not believe that there is a material risk that they would stop selling boats to us in any of our markets given our scale and long-standing

relationships. We were recognized as Dealer of the Year by Boating Industry in 2016 and 2017, were inducted into the Boating Industry Top 100 Hall of Fame in 2018, and have been a Top 100 dealer since 2006. Certain of our local and regional dealer

groups, including Singleton Marine, have been recognized among the top dealers worldwide for Cobalt Boats, Regal Boats, Harris and Yamaha Boats, and among the top dealers in the Southeast for Malibu and Axis. Additionally, we are also the top

Yamaha Jet Boat dealer by volume in the United States. We began selling Sunseeker yachts in the fourth quarter of fiscal year 2019 through one of our consignors that is the exclusive dealer for certain Sunseeker yachts in select states, including

Texas, certain counties in Florida, Alabama, North Carolina, South Carolina and Georgia. From time to time, we may continue to add additional manufacturers whose products match our focus on premium recreational boats.

Diversified Revenue Streams: We offer a broad range of products and services beyond new and pre-owned boats, including repair and maintenance services, parts and accessories,

F&I products and ancillary services, including storage. Although non-boat sales contributed approximately 9.8%, 11.4% and 10.5% to revenue in fiscal years 2020, 2019 and 2018, respectively, the higher gross margin on these product and service

lines resulted in non-boat sales contributing 28.3%, 31.1% and 26.7% of gross profit in fiscal years 2020, 2019 and 2018, respectively. During different phases of the economic cycle, consumer behavior may shift away from new boats; however, we are

well positioned to benefit from revenue from pre-owned boats, repair and maintenance services, and parts and accessories, which have historically increased during periods of economic uncertainty. We have also diversified our business across

geographies and dealership types (e.g., fresh water and salt water) in order to reduce the effects of seasonality. For instance, boating activity in South Florida increases during winter months, whereas freshwater boating in the Southeast,

Mid-Atlantic and Northeast peaks during late-spring and summer.

Attractive Financial Profile: Since the formation of OneWater LLC in 2014, we have established a high growth financial profile driven by strong same-store sales growth and

acquisitions. This growth has resulted in a high level of cash flow generation, and allows us to maintain a conservative leverage profile. Excluding inventory financing, our business requires a low level of capital with historical maintenance

capital expenditures typically under 0.5% of revenue. We are focused on achieving profitable growth and have been able to achieve an increase in Adjusted EBITDA margins by growing revenue at a higher rate than operating expenses have increased.

|

Fiscal 2020 Revenue

|

Fiscal 2020 Gross Profit

|

|

|

Fiscal 2020 Adjusted EBITDA(1)

|

(1)

|

Adjusted EBITDA is a non-GAAP financial measure. For the definition of Adjusted EBITDA and a reconciliation to our most directly comparable financial measure calculated and presented in accordance with GAAP, please read “Management’s

Discussion and Analysis of Financial Condition and Results of Operations—Comparison of Non-GAAP Financial Measure.”

|

Highly Experienced Management Team: We have assembled an exceptional team of highly experienced professionals within the boating industry. The average industry tenure of our

executive team is 25 years and our Chief Executive Officer, Austin Singleton, who is a second generation boat dealer, has been in the industry for 32 years. In addition, our Chief Operating Officer, Anthony Aisquith, and Chief Financial Officer,

Jack Ezzell, have 25 and 18 years of industry experience, respectively.

Growth Strategy

Organic Growth Strategy: Our business model utilizes our unique scale to drive profitable same-store sales growth. We seek to gain market share by delivering high-quality

products and services, with customized attributes tailored to our customers’ product specifications. Our management team and business model are extremely agile, allowing us to target sales in specific segments of the industry that are outperforming

overall industry trends. Additionally, we are able to leverage our potential customer database to garner new sales. Sales growth from our existing stores is a core component of our current and future strategy. We believe non-boat sales will be a

driver of our organic growth strategy in the future. We have implemented a targeted marketing strategy across our platform focused on increasing new and existing customer awareness and usage of our F&I products, repair and maintenance services,

and parts and accessories products. We intend to expand our online presence and sales through a multi-phased roll out of a digital platform to engage in online new and pre-owned boat sales, as well as financing & insurance. We believe this will

further advance our long-term growth opportunity, while broadening our customer base and geographic reach. Additionally, we may also develop a dealership if an attractive acquisition is not available in a market we choose to target.

Acquisition Strategy: We believe there is a tremendous opportunity for us to expand in both existing and new markets, given that the industry is highly fragmented with most boat

retailers owning three or fewer stores. We seek to create value by implementing the best tested operational practices to family-owned and operated businesses that previously lacked the resources, management experience and expertise to maximize the

profitability of the acquired standalone businesses. We believe that the boat retail market is underpinned by strong fundamental drivers, and that, with the implementation of operational control measures and the injection of resources, local stores

can significantly increase revenues and profitability. We believe our status as a consolidator of choice is based on the expertise we have developed through completing 17 acquisitions (41 stores acquired) since the combination of Singleton Marine

and Legendary Marine in 2014, our growing cash flow and financial profile, and our footprint of retailers within prime markets. Our ability to acquire additional stores or dealer groups at attractive multiples is further enhanced by our growing

reputation for retaining the seller’s management team and keeping their branding and legacy intact. Accordingly, the sellers remain actively involved in the business. We typically enter into three-year employment agreements with the owners of the

stores or dealer groups that we acquire at salaries commensurate with their positions, although many have remained employed with us beyond the initial term of such agreements. We believe there is significant opportunity to expand our store

footprint in regions with strong boating cultures. While we have a strong presence in the Southeastern portion of the United States, there are several areas of opportunity in states adjacent to our current geographic footprint as well as states in

new regions in the Midwest and Western United States. We are targeting to complete four to eight potential acquisitions that may contribute an estimated total of $100 million to $200 million in sales over the next 24 months, though we can provide

no assurance as to the timing or completion of such acquisitions. As a result of our reputation in the market place, we expect our pipeline of potential acquisitions to grow over time.

Industry Trends and Market Opportunity

U.S. Recreational Boating Industry

Recreational boating is a well-established American pastime that attracts millions of people each year to the water. While Florida is the leading state for new boating sales and registrations due to its abundance of

both fresh water and salt water, boating is very popular throughout the United States with Texas, Michigan, North Carolina and Minnesota representing the rest of the top five states for new marine retail expenditures. There are approximately twelve

million boats registered in the United States. U.S. boat registrations have remained stable over time, and have remained above eleven million registrations since 2006. In 2019, there was one registered boat for approximately every 10 households in

the United States.

In 2019, $43 billion was spent on retail boating sales which has contributed to annual growth of just under two percent since 2006. Consumer marine spending includes purchases of new and pre-owned boats; marine

products such as engines, trailers, equipment, and accessories; and related expenditures, such as fuel, insurance, docking, storage, and repairs. New boat sales and pre-owned boat sales constituted 62% and 38% of 2019 boating retail sales,

respectively, based on industry data from the NMMA. The NMMA estimates that approximately 966,000 pre-owned boats were sold in 2019. Non-boat sales include aftermarket accessories (17.1% of total 2019 boating retail sales) and F&I and Ancillary

Services, such as insurance, maintenance and fuel (22.6% of total 2019 boating retail sales).

Boat sales volumes are correlated with consumer confidence and the availability of consumer credit. Recent growth in spending has been driven by both an increase in units sold as well as rising average selling prices.

Innovation, including updated boat configurations, hull designs, wake gates and other electronics, have contributed to shorter boat upgrade cycles which result in higher unit sales volume. Pre-owned traditional powerboat sales were approximately

$9.0 billion in 2018 and have remained relatively consistent since 2006 and through economic cycles. The boat dealership market is highly fragmented with approximately 4,300 stores nationwide and the majority of retailers are owner-operated with

three stores or fewer. Independent retailers typically offer a limited selection of boat brands, and they predominantly focus on new boat sales with less expertise and capacity to create a meaningful business from non-boat sales such as F&I

products.

Products and Services

We offer new and pre-owned recreational boats, yachts and related marine products, including parts and accessories, with a specific focus on premium brands. We also provide boat repair and maintenance services, arrange

boat financing and boat insurance and offer other ancillary services including indoor and outdoor storage, marina services, and rentals of boats and personal watercraft.

New and Pre-Owned Boat Sales

Our business focuses primarily on the sale of new and pre-owned recreational boats, including pontoon, runabout, saltwater fishing boats, wake/ski boats, and yachts. We offer products from a broad variety of

manufacturers and brands without relying on any one manufacturer or brand in particular. No single brand accounted for more than 7% of our total sales volume in fiscal year 2020. We also sell pre-owned versions of the brands we offer and pre-owned

boats of other brands we take as trade-ins or acquire. During fiscal year 2020, new boat sales accounted for approximately $717.1 million or 70.1% of our revenue, and pre-owned boat sales accounted for approximately $205.7 million or 20.1% of our

revenue.

We offer new and pre-owned recreational boats in a broad range of market segments. We believe that the product lines and brands we offer are among the highest quality within their respective market segments, with

well-established brand recognition and reputations for quality, performance, styling and innovation.

Fishing Boats. Revenue from fishing boats comprised 35% of our new boat revenue for fiscal 2020. The fishing boats we offer range from entry-level models to advanced models,

such as Everglades, Pursuit, Scout and Sea Hunt, each designed for fishing and water sports in lakes, bays and off-shore waters, with cabins with limited live-aboard capability. The fishing boats we offer typically feature livewells, in-deck

fishboxes, rodholders, rigging stations, cockpit coaming pads and fresh and saltwater washdowns.

Pontoon Boats and Runabouts. Revenue from pontoon boats and runabouts comprised 37% of our new boat revenue for fiscal 2020. We offer a variety of some of the most innovative,

luxurious, and premium pontoon models to fit boaters’ needs, such as Bennington, Barletta and Harris. Our runabouts, such as Cobalt, Regal and Chris-Craft, target the family recreational boating markets and come in a variety of configurations to

suit each customer’s particular recreational boating style. The models we offer may include amenities such as advance navigation electronics and sound systems, a variety of hull, deck, and cockpit designs that can include a swim platform, bow

pulpit and raised bridges, and swivel bucket helm seats, lounge seats, sun pads, wet bars, built-in ice chests, and refreshment centers. With a variety of designs and options, the pontoon boats and runabouts we offer appeal to a broad audience of

boat enthusiasts and existing customers.

Wake/Ski Boats. Revenue from wake/ski boats comprised 8% of our new boat revenue for fiscal 2020. The ski boats we offer range from entry-level models to advanced models, such

as Axis and Malibu, all of which are designed to generate specific wakes for optimal skiing, surfing and wakeboarding performance and safety. With a broad range of designs and options, the ski boats we offer appeal to both competitive and

recreational users.

Yachts. Revenue from yachts comprised 12% of our new boat revenue for fiscal 2020. The yachts we offer range from entry-level models to advanced models, such as Absolute,

Riviera, Tiara and Sunseeker. The motor yacht product lines typically include state-of-the-art designs with live-aboard luxuries, offering amenities such as flybridges with extensive guest seating; covered aft deck, which may be fully or partially

enclosed, providing the boater with additional living space; an elegant salon; and multiple staterooms for accommodations.

Motors, Trailers, Personal Water Crafts (“PWC”), Wholesale and Other. Revenue from motors, trailers, PWC, wholesale and other sales comprised 8% of our new boat revenue for

fiscal 2020. The motors and trailers we offer range in size, horsepower, length and style dependent upon the type of boat our customers may own. We offer PWC, primarily including models from Yamaha and Sea Doo, which appeal to a broad audience of

customers. Wholesale sales primarily consist of transactions with other dealers and other sales include the remaining new inventory products we offer.

F&I Products

At each of our stores, our customers have the ability to finance their new or pre-owned boat purchase, purchase a third-party extended service contract and arrange insurance covering boat property, disability, gel

sealant, fabric protection and casualty insurance coverage (collectively, “F&I”). Our relationships with various national marine product lenders allow buyers to purchase retail installment contracts originated by us in accordance with existing

pre-sale agreements between us and the lenders. These retail installment contracts provide us with a portion of the expected finance charges based on a variety of factors, including the buyer’s credit rating, the annual percentage rate of the

contract and the lender’s then-existing minimum required annual percentage rate. These contracts are subject to repayment by us upon buyer prepayment or default within a designated time period (typically within 180 days). To the extent required by

applicable state law, our dealer groups are licensed to originate and sell retail installment contracts financing the sale of boats and other marine products.

We offer our customers third-party extended service contracts, which allow us to extend customers’ new boat coverage beyond the time frame or scope of the manufacturer’s standard hull and engine warranty. We also offer

purchasers of pre-owned boats the ability to purchase a third-party extended service contract, even if the applicable boat is no longer covered by the manufacturer’s warranty. We also provide the related repair services, when needed by our

customers, pursuant to the service contract guidelines during the contract term at no additional charge to the customer above a deductible. Generally, we receive a fee for arranging these extended service contracts and most of the required services

under the contracts are provided by us and paid for by the third-party contract holder.

We also assist our customers with obtaining property and casualty insurance. Property and casualty insurance covers loss or damage to their boat. We do not act as an insurance broker or agent or issue insurance

policies on behalf of insurers. We provide marketing activities and other related services to insurance companies and brokers for which we receive marketing fees. One of our strategies is to generate increased marketing fees by offering more

competitive insurance products.

Fee income generated from F&I products accounted for approximately $36.8 million or 3.6% of our revenue during fiscal year 2020, $26.2 million or 3.4% of our revenue during fiscal year 2019 and approximately $16.6

million or 2.8% of our revenue for fiscal year 2018. We believe that our customers’ ability to obtain competitive, prompt and convenient financing at our stores strengthens our ability to sell new and pre-owned boats and gives us an advantage over

many of our competitors, particularly our smaller competitors that lack the resources to arrange boat financing at their stores or that do not generate enough F&I product volume to attract the broad range of financing sources that are available

to us.

Service, Parts & Other

We provide repair and maintenance services at most of our stores. We believe that our repair and maintenance services help strengthen our customer relationships and that our quality service and emphasis on preventative

maintenance increases the quality and supply of well-maintained boats available for our pre-owned boat business. We perform both warranty and non-warranty repair services, with the cost of warranty work reimbursed by the manufacturer in accordance

with the manufacturer’s warranty reimbursement program. For any warranty work we perform, most of our manufacturers reimburse a percentage of the store’s posted service labor rates, with the percentage varying depending on the store’s customer

satisfaction index rating and attendance at service training courses. Certain other of our manufacturers reimburse warranty work at a fixed amount per repair. Because boat manufacturers require that warranty work be performed at authorized stores,

our stores receive substantially all of the warrantied repair and maintained work required for the boats we offer. We also offer third-party extended warranty contracts, which result in a continuous demand for our repair and maintenance services

for the term of the extended warranty contract. Additionally, we offer parts and accessories at our stores, primarily to retail customers to repair their current engines or other marine related parts and equipment. Our offerings include engine

parts, oils, lubricants, steering and control systems, electronics, safety products, water sport accessories (such as tubes, wakeboards, surfboards, lines, and lifejackets), products relating to docking and anchoring, boat covers, trailer parts,

and a complete line of other boating accessories.

At certain of our stores, we offer marina and boat rental services, which are generally recurring in nature and create additional opportunities to connect with potential buyers. We maintain a small fleet of rental

boats, and, after one season, the rental boats are repurposed for pre-owned sales. Additionally, we operate 15 marina locations that provide fueling, docking and indoor and outdoor storage.

Our focus on customer service, which we believe is one of our core competitive advantages in the recreational boating industry, is critical to our efforts in creating and maintaining long-term customers. Service, parts

& other accounted for approximately $63.4 million or 6.2% of our revenue during fiscal year 2020, approximately $61.7 million or 8.0% of our revenue during fiscal year 2019 and approximately $46.7 million or 7.7% of our revenue during fiscal

year 2018.

Stores

We offer new and pre-owned recreational boats and other related marine products and boat services through 61 stores comprising 21 dealer groups in 10 states, including Texas, Florida, Alabama, North Carolina, South

Carolina and Georgia. Each store generally includes an indoor showroom and an outside display area for our new and pre-owned boat inventories, along with a business office to facilitate F&I products and repair and maintenance services

facilities.

Operations

Dealership Operations and Management

The operational management of our boat dealer groups is decentralized, with certain administrative functions centralized at the corporate level and the primary responsibility of day-to-day operations localized at the

store level. Each store is managed by a general manager, often a former owner, who oversees the day-to-day operations, human resources and financial performance of that particular individual store. Typically, each store also has a staff consisting

of sales representatives, an F&I manager, a service manager, a parts manager, maintenance and repair technicians and additional support personnel.

We provide employees with ongoing training, career advancement opportunities and favorable benefit packages as a part of our strategy to attract and retain high quality employees. Sales training sessions are held at

various locations, including the manufacturers facilities, and cover a broad array of topics from technical product details, features and benefits, to general sales techniques. Our highly-trained professional sales teams recognize the importance of

building relationships with customers, assisting them in selecting the boat that best fits their needs and making the entire sales process enjoyable, all of which are critical to our successful sales efforts. The overall focus of our training

program is to provide exemplary customer service.

Members of our sales teams receive compensation on primarily a commission basis. Generally, each manager within a store receives a salary along with incentive compensation based on the performance of the managed store

or their respective departments.

Sales and Marketing

Our sales strategy focuses on highlighting the joys of the boating lifestyle while also providing convenient repair and maintenance services to maintain a stress-free boating experience. Our sales strategy is built on

our high levels of customer service, hassle-free sales approach, appealing store layouts, highly-trained sales teams and the ability of our sales teams to educate customers and their families on boating. We constantly aim to provide the highest

levels of customer service and support before, during and after each sale.

Each of our stores offers our customers the opportunity to evaluate a variety of new and pre-owned boats in an environment that is convenient, comfortable and professional. Our stores provide a full-service purchasing

process, which includes attractive F&I packages and extended third-party service agreements. We have a number of waterfront stores, most of which include marina-type facilities and docks at which we display our new and pre-owned boats. These

waterfront stores and marinas are easily accessible to boating customers, operate as in-water showrooms and enable our sales team to give potential customers impromptu in-water demonstrations of our various boat models. In light of the current

environment, our sales team members are providing certain customers with virtual walkthroughs of inventory and/or private, at home or on water showings. We also intend to expand our online presence and sales through a multi-phased roll out of a

digital platform to engage in online new and pre-owned boat sales, as well as financing & insurance. In March 2020, we launched a new quoting tool for an internally developed customer relationship management system, which we expect to be

further enhanced by the acquisition of Boatsforsale.com.

We provide customers a diverse offering of boat brands, which span across a multitude of sizes, uses and activities, including leisure, fishing, watersports, luxury and vacation. We believe this diverse offering of

brands allows us to reach a broad expanse of customers and maximizes our ability to provide high quality service to each customer that walks into one of our stores.

An important part of our sales strategy is our participation in boat shows and specialized events in areas with high levels of boating activity. These shows and events help drive sales during and after the show or

event and are typically held in January, February, March and toward the end of the boating season at convention centers or marinas that have been rented out by area dealers. We rely to a certain extent on boat shows to generate sales. Our inability

to participate in boat shows in our existing target markets, including cancellation of boat shows in connection with the COVID-19 pandemic, could have a material adverse effect on our business, financial condition and results of operations. To the

extent boat shows may be delayed or cancelled, we intend to hold complementary sales events on a smaller, more personalized scale where we are able to follow stricter safety precautions and social distancing.

We focus on customer education through personalized education by our sales representatives and other professionals, before, during and after a sale through product demonstrations on the use and operation of their boat.

Typically, one of our delivery professionals or the sales representative delivers the customer’s boat to the customer’s boating location and thoroughly instructs the customer about the operation of the boat, including hands-on instructions for

docking and trailering the boat.

Suppliers and Inventory Management

We purchase substantially all of our new boat inventory directly from manufacturers. Manufacturers typically allocate new boats to stores or dealer groups based on the amount of boats sold by the store or dealer group

and their market share. We exchange new boats with other dealers to maintain flexibility, meet customer demand and balance inventory. We also display a select number of boats and yachts through consignment agreements, including with related

parties.

We offer a wide array of new boats at various price points through relationships with 50 manufacturers covering 66 brands. We are currently a top-three customer for 28 of our 66 brands and the single largest customer

for each of our top five highest-selling brands. While our order volume amounts to between 5% to 35% of total sales for those top five brands, no single brand accounts for more than 7% of our total sales volume. Additionally, our top brand only

accounts for approximately 10% of new boat sales. However, sales of new boats from the top ten brands represent approximately 41.1% of our total sales volume for fiscal year 2020.

As part of our business, we enter into renewable annual dealer agreements with boat manufacturers. Provided that we are in compliance with the material obligations of such dealer agreements, they designate an exclusive

geographical territory for our store to sell a particular boat brand and typically do not restrict our right to sell any other product lines or competing products.

Manufacturers generally establish suggested prices annually, but the actual sales prices remain subject to the sole discretion of the dealer, which highlights the advantage of our lack of reliance on any one

manufacturer. Manufacturers typically offer discounts and increased inventory financing assistance during the manufacturers’ slow season (generally October through March). We often capitalize on these opportunities to maximize our profit margins

and increase our product availability during the selling season.

We are also able to transfer boats between our stores to maintain flexibility, meet customer demand and balance inventories. This flexibility reduces delays in delivery, helps us maximize inventory turnover and assists

in minimizing potential overstock or out-of-stock situations. We actively monitor our inventory levels to maintain levels appropriate to meet current anticipated market demands. We are not bound by contractual agreements governing the amount of

inventory that we must purchase in any year from any manufacturer; however, the failure to purchase at agreed upon levels may result in the loss of certain manufacturer incentives or dealership rights.

Our inventory turnover ratio, which is calculated as cost of goods sold for the period divided by the average inventory over the same period, was 3.7x, 2.6x and 3.1x for fiscal years 2020, 2019 and 2018, respectively.

Our comparable store new boat inventory turnover ratio, which is calculated as cost of new boats sold for the relevant fiscal year minus contributions from acquisitions made during that fiscal year, divided by the average new boat inventory over

the same fiscal year without contributions from such acquisitions, was 2.4x and 2.6x for fiscal years 2019 and 2018, respectively. Our comparable store pre-owned boat inventory turnover ratio, which is calculated as cost of purchased or traded-in

pre-owned boats sold for the relevant fiscal year minus contributions from acquisitions made during that fiscal year, divided by the average purchased or traded-in pre-owned boats inventory over the same fiscal year without contributions from such

acquisitions, was 3.6x and 4.7x for fiscal years 2019 and 2018, respectively. We did not make any acquisitions during fiscal year 2020.

Inventory Financing

Boat and related marine manufacturers customarily provide various levels of interest assistance programs to retailers, which may include periods of free financing or reduced interest rate programs. The interest

assistance may be paid directly to the retailer or the financial institution depending on the arrangements the manufacturer has established. We believe that our financing arrangements with manufacturers are standard within the industry.

We are party to our Inventory Financing Facility. The interest rate for amounts outstanding under the Inventory Financing Facility is calculated using the one month LIBOR plus an applicable margin of 2.75% to 5.00% for

new boats and at the new boat rate plus 0.25% for pre-owned boats. The collateral for the Inventory Financing Facility consists primarily of our inventory that is financed through the Inventory Financing Facility and related assets, including

accounts receivable, bank accounts, and proceeds of the foregoing, and excludes the collateral that underlies our Term and Revolver Credit Facility (as defined below). For additional information relating to the terms of our Inventory Financing

Facility, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Debt Agreements—Inventory Financing Facility.”

Customers

We are not dependent on any one customer or group of customers, and no individual customer, or together with its affiliates, contributed on an aggregate basis 10% or more to our revenues.

Seasonality

Our business, along with the entire recreational boating industry, is highly seasonal, and such seasonality varies by geographic market. With the exception of Florida, we generally realize significantly lower sales and

higher levels of inventories, and related floor plan borrowings, in the quarterly periods ending December 31 and March 31. Revenue generated from our stores in Florida serves to offset generally lower winter revenue in our other states and enables

us to maintain a more consistent revenue stream. Over the three-year period ended September 30, 2020, the average revenue for the quarters ended December 31, March 31, June 30 and September 30 represented approximately 14%, 21%, 38%, and 27%,

respectively, of our average annual revenues. Every January, the onset of consumer boat and recreation shows generally marks the beginning of an increase in boat sales which allows us to begin to reduce our inventory levels and related short-term

borrowings for the remainder of the fiscal year.

Our business is also sensitive to weather patterns, such as unseasonably cool weather, prolonged winter conditions, drought conditions (or merely reduced rainfall levels) or excessive rain, which may shorten the

selling season, limit access to certain locations for boating or render boating hazardous or inconvenient, thereby curtailing customer demand for our products and services and adversely affecting our results of operations. Additionally, hurricanes

and other storms may cause disruptions to our business operations or damage to our inventories and facilities. We believe our geographic diversity is likely to reduce the overall impact to us of adverse weather conditions in any one market area.

Environmental and Other Regulatory Issues

Our business operations, along with the entire retail recreational boating industry, are subject to numerous environmental and occupational health and safety laws and regulations that may be imposed in the United

States at the federal, state and local levels. Federal agencies that implement and enforce these laws and regulations include the U.S. Environmental Protection Agency (“EPA”) and the U.S. Occupational Safety and Health Administration (“OSHA”). The

more significant of these environmental and occupational health and safety laws and regulations include the following federal legal standards that currently exist in the United States, as amended from time to time:

| • |

the Clean Air Act (“CAA”), which restricts the emission of air pollutants from many sources, including outboard marine engines, and imposes various pre-construction, operational, monitoring, and reporting requirements, and that the EPA

has relied upon as authority for adopting climate change regulatory initiatives relating to greenhouse gas (“GHG”) emissions;

|

| • |

the Federal Water Pollution Control Act (the “Clean Water Act”), which regulates discharges of pollutants from facilities to state and federal waters and establishes the extent of which waterways are subject to federal jurisdiction and

rulemaking as protected waters of the United States;

|

| • |

the Oil Pollution Act (“OPA”), which subjects owners and operators of vessels, onshore facilities, and pipelines, as well as lessees or permittees of areas in which offshore facilities are located, to liability for removal costs and

damages arising from an oil spill in waters of the United States;

|

| • |

the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), which imposes liability on generators, transporters, disposers and arrangers of hazardous substances at sites where hazardous substance releases have

occurred or are threatening to occur;

|

| • |

the Resource Conservation and Recovery Act (“RCRA”), which governs the generation, treatment, storage, transport, and disposal of solid wastes, including hazardous wastes;

|

| • |

the Emergency Planning and Community Right-to-Know Act, which requires facilities to implement a safety hazard communication program and disseminate information to employees, local emergency planning committees, and fire departments on

toxic chemical uses and inventories; and

|

| • |

the Occupational Safety and Health Act, which establishes workplace standards for the protection of the health and safety of employees, including the implementation of hazard communications programs designed to inform employees about

hazardous substances in the workplace, potential harmful effects of these substances, and appropriate control measures.

|

Additionally, there exist state and local jurisdictions in the United States where we operate that also have, or are developing or considering developing, similar environmental and occupational health and safety laws

and regulations governing many of these same types of activities, which requirements may impose additional, or more stringent, conditions or controls than required under federal law and that can significantly alter, delay or cancel the permitting,

development, or expansion of operations or substantially increase the cost of doing business. Environmental and occupational health and safety laws and regulations, including new or amended legal requirements that may arise in the future to address

potential environmental concerns such as air and water impacts or to address perceived human health or safety-related concerns, including a global or national health crisis, are expected to continue to have a considerable impact on our operations.

As with companies in the retail recreational boat industry generally, and parts and service operations in particular, our business involves the use, handling, storage and contracting for recycling or disposal of

petroleum-based products and wastes, as well as other hazardous and toxic substances and wastes, including gasoline, diesel fuels, motor oil, waste motor oil and filters, transmission fluid, antifreeze, freon, waste paint and lacquer thinner,

batteries, solvents, lubricants, and degreasing agents. Environmental and occupational health and safety laws and regulations generally impose requirements for the use, storage, management, handling, and disposal of these materials, and restrict

the level of pollutants emitted into the environment, including into ambient air, discharges to surface water, and disposals or other releases to surface and below-ground soils and ground water. Failure to comply with these laws and regulations may

result in the assessment of sanctions, including administrative, civil, and criminal penalties or liabilities to third parties; the imposition of investigatory, remedial, and corrective action obligations or the incurrence of capital expenditures;

the occurrence of restrictions, delays or cancellations in the permitting, development, or expansion of projects; and the issuance of injunctions restricting or prohibiting some or all of our activities in a particular area. Moreover, there exist

environmental laws that provide for citizen suits, which allow individuals or organizations to act in the place of the government and sue operators for alleged violations of environmental law.

We are also subject to laws and regulations governing the investigation and remediation of contamination at the facilities we currently or formerly own or operate, as well as at third-party sites to which we send

hazardous substances or wastes for treatment, recycling or disposal. Some environmental laws, such as CERCLA and similar state statutes impose strict joint and several liability for the entire cost of investigation or remediation of a contaminated

property and for any related damages to natural resources, upon current or former site owners or operators, as well as persons who arranged for the transportation, treatment or disposal of hazardous substances. We may also be subject to third-party

claims alleging property damage and/or personal injury in connection with releases of, or exposure to, hazardous substances at our current or former properties or off-site waste disposal sites or from the products we sell.

Additionally, certain of our stores and/or repair facilities utilize underground storage tanks (“USTs”) and aboveground storage tanks (“ASTs”), primarily for storing and dispensing petroleum-based products. The USTs

and ASTs are generally subject to federal, state and local laws and regulations that require obtaining financial assurance to own or operate USTs and ASTs, testing and upgrading of tanks and remediation of contaminated soils and groundwater

resulting from leaking tanks. Additionally, if leakage from our USTs or ASTs migrates onto the property of others, we may be liable to third parties for remediation costs, natural resource damages or other damages.

For additional information relating to environmental protection, including releases, discharges and emissions into the environment, as well as worker health and safety requirements, please see “Risk Factors— Risks

Related to Our Business—Environmental and other regulatory issues may impact our operations” and “Our operations are subject to risks arising out of the threat of climate change, which could result in increased operating costs and reduced demand

for the products that we and the retail recreational boat industry provide.” Historically, our environmental compliance costs have not had a material adverse effect on our business, financial condition or results of operations; however, there can

be no assurance that such costs will not be material in the future or that such future compliance will not have a material adverse effect on our business, financial condition or results of operations.

Product Liability

Our sale and servicing of boats and other watercraft may expose us to potential liabilities for personal injury or property damage claims relating to the use of such products. Historically, product liability claims

have not materially affected our business. Our manufacturers generally maintain product liability insurance, and we maintain third-party liability insurance with respect to the sale and servicing of boats and other watercrafts, which we believe to

be adequate. However, we may experience legal claims in excess of our insurance coverage, and those claims may not be covered by insurance. Furthermore, any significant claims against us, or an increase in insurance premiums resulting from

excessive insurance claims, could adversely affect our business, financial performance and results of operations and result in negative publicity.

Competition

We operate in a highly competitive and fragmented environment. We face competition from businesses relating to recreational activities, which businesses compete for consumers’ leisure time and discretionary spending

dollars. We face intense competition within the highly fragmented recreational boat industry for customers, quality products, boat show space and suitable store locations. We rely to a certain extent on boat shows to generate sales. Our inability

to participate in boat shows in our existing or targeted markets could have a material adverse effect on our business, financial performance and results of operations.

We compete primarily with local boat dealers who own three or fewer stores, as well as with a limited number of larger operators, including MarineMax and Bass Pro Shops. With respect to sales of marine parts,

accessories, and equipment, we compete with national specialty marine parts and accessory stores, online catalog retailers, sporting goods stores, and mass merchants. Competition within the recreational boating industry is generally based on the

quality and variety of available products, the price and value of the products and services and attention to customer service. We face significant competition from our current market and will likely face significant competition in any new markets

that we may enter. We also face competition from retailers in certain markets who sell boat brands, parts and engines that we do not currently carry in such markets. Additionally, a number of our competitors are large national or regional chains

that have substantially more financial, marketing and other resources than us, especially with regard to those that sell boating accessories. We also face competition from private sellers of pre-owned boats and online merchants entering the resale

boating industry. However, we believe that our integrated corporate infrastructure, marketing and sales capabilities, cost structure, industry expertise and customer experience enable us to compete effectively against these competitors.

Intellectual Property

We rely on a number of trade names with respect to the regional dealer groups that we have acquired, which we do not re-brand under our “OneWater” mark. We cannot give any assurance that any trade name and trademark

applications that we may file in the future will be granted.

Human Capital Resources

As of November 30, 2020, we had 1,169 employees, 1,093 of whom were in store-level operations and 76 of whom were in corporate administration and management. We offer our employees a wide array of

company-paid benefits, which we believe are competitive relative to others in our industry. We are not a party to any collective bargaining agreements. We consider our relations with our employees to be excellent.

Our Offices

Our principal executive offices are located at 6275 Lanier Islands Parkway, Buford, Georgia 30518, and our telephone number at that address is 678-541-6300. Our website address is www.onewatermarine.com. Information

contained on our website does not constitute part of this prospectus.

Our Corporate Structure

OneWater Marine Inc. was incorporated as a Delaware corporation in April 2019 for the purpose of completing the IPO and related transactions. On February 12, 2020, in connection with the IPO, OneWater Inc. became a

holding company whose sole material asset consists of units in OneWater LLC (the “OneWater LLC Units”). OneWater LLC holds all of the equity interest in One Water Assets & Operations (“OWAO” or “Opco”), which owns all of our operating assets.

The remainder of the OneWater LLC Units are held by certain Legacy Owners (the “OneWater Unit Holders”).

As the sole managing member of OneWater LLC, OneWater Inc. operates and controls all of the business and affairs of OneWater LLC, and through OneWater LLC and its subsidiaries, conducts its business. As a result, we

consolidate the financial results of OneWater LLC and its subsidiaries and report temporary equity related to the portion of OneWater LLC Units not owned by us, which will reduce net income (loss) attributable to the holders of our Class A common

stock. As of November 30, 2020, OneWater Inc. owned 72.0% of OneWater LLC.

Certain of the Legacy Owners hold one share of our Class B common stock, par value $0.01 per share (the “Class B common stock”), for each OneWater LLC Unit such person holds. Each share of Class B common stock has no

economic rights but entitles its holder to one vote on all matters to be voted on by shareholders generally. Holders of Class A common stock and Class B common stock vote together as a single class on all matters presented to our stockholders for

their vote or approval, except as otherwise required by applicable law or by our amended and restated certificate of incorporation. We do not intend to list Class B common stock on any exchange.

Under the amended and restated limited liability company agreement of OneWater LLC (the “OneWater LLC Agreement”), each of the holders of OneWater LLC Units (“LLC Unitholders”) has, subject to certain limitations, the

right (the “Redemption Right”) to cause OneWater LLC to acquire all or a portion of its OneWater LLC Units for shares of Class A common stock of OneWater Inc. on a one-for-one basis or, at OneWater LLC’s election, an equivalent amount of cash.

Alternatively, upon the exercise of the Redemption Right, OneWater Inc. (instead of OneWater LLC) will have the right (the “Call Right”) to, for administrative convenience, acquire each tendered OneWater LLC Unit directly from the redeeming

OneWater Unit Holder for, at its election, (x) one share of Class A common stock, subject to conversion rate adjustments for stock splits, stock dividends and reclassification and other similar transactions, or (y) an equivalent amount of cash. In

connection with any redemption of OneWater LLC Units pursuant to the Redemption Right or the Call Right, the corresponding number of shares of Class B common stock, par value $0.01 per share, of OneWater Inc. (the “Class B common stock”) will be

cancelled; Under the Registration Rights Agreement we entered into with certain of the Legacy Owners in connection with the IPO, such Legacy Owners have the right, under certain circumstances, to cause us to register the offer and resale of their

shares of Class A common stock.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging

growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include:

| • |

We are not required to engage an auditor to report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”);

|

| • |

We are not required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board (the “PCAOB”) regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional

information about the audit and the financial statements (i.e., an auditor discussion and analysis);

|

| • |

We are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency” and “say-on-golden parachutes”; and

|

| • |