Attached files

| file | filename |

|---|---|

| EX-99.2 - EX-99.2 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit992.htm |

| EX-99.1 - EX-99.1 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit991.htm |

| EX-32.2 - EX-32.2 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit322.htm |

| EX-32.1 - EX-32.1 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit321.htm |

| EX-31.2 - EX-31.2 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit312.htm |

| EX-31.1 - EX-31.1 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit311.htm |

| EX-21.1 - EX-21.1 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit211.htm |

| EX-14.2 - EX-14.2 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit142.htm |

| EX-14.1 - EX-14.1 - GOLUB CAPITAL BDC, Inc. | gbdcfy2020exhibit141.htm |

| EX-4.8 - EX-4.8 - GOLUB CAPITAL BDC, Inc. | a48descriptionofsecuri.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

______________________________________________________________________________________________________

Form 10-K

______________________________________________________________________________________________________

| (Mark One) | ||||||||

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||

| For the fiscal year ended September 30, 2020 | ||||||||

| or | ||||||||

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||

| For the transition period from to | ||||||||

______________________________________________________________________________________________________

Commission file number: 814-00794

GOLUB CAPITAL BDC, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 27-2326940 | |||||||

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||||

| 200 Park Avenue, 25th Floor, New York, NY | 10166 | |||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||

(212) 750-6060

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

| Common Stock, par value $0.001 per share | GBDC | The Nasdaq Global Select Market | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes o No ý

1

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | ||||

Non-accelerated filer o | Smaller reporting company o | ||||

Emerging growth company o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes þ No o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).Yes o No ý

The aggregate market value of common stock held by non-affiliates of the registrant on March 31, 2020 was approximately $1,597.2 million. For the purposes of calculating this amount only, all directors and executive officers of the registrant have been treated as affiliates. There were 167,259,511 shares of the registrant’s common stock outstanding as of November 30, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A in connection with the registrant’s 2021 Annual Meeting of Stockholders, which will be filed subsequent to the date hereof, are incorporated by reference into Part III of this Form 10-K. Such proxy statement will be filed with the Securities and Exchange Commission not later than 120 days following the end of the registrant’s fiscal year ended September 30, 2020.

2

| Part I. | ||||||||

| Part II. | ||||||||

| Part III. | ||||||||

| Part IV. | ||||||||

3

PART I

In this annual report on Form 10-K, except as otherwise indicated, the terms:

•“we,” “us,” “our” and “Golub Capital BDC” refer to Golub Capital BDC, Inc., a Delaware corporation, and its consolidated subsidiaries;

•“Holdings” refers to Golub Capital BDC Holdings LLC, a Delaware limited liability company, or LLC, our direct subsidiary;

•“GCIC Holdings” refers to GCIC Holdings LLC, a Delaware LLC, our direct subsidiary;

•“2014 Issuer” refers to Golub Capital BDC CLO 2014 LLC, a Delaware LLC, our direct subsidiary;

•“2018 Issuer” refers to Golub Capital BDC CLO III LLC, a Delaware LLC, our indirect subsidiary;

•“GCIC 2018 Issuer" refers to GCIC CLO II LLC, a Delaware LLC, our indirect subsidiary;

•“2020 Issuer” refers to Golub Capital BDC CLO 4 LLC, a Delaware LLC, our indirect subsidiary;

•“2018 CLO Depositor” refers to Golub Capital BDC CLO III Depositor LLC, a Delaware LLC, our direct subsidiary;

•“GCIC CLO Depositor” refers to GCIC CLO II Depositor LLC, a Delaware LLC, our direct subsidiary;

•“2020 CLO Depositor” refers to Golub Capital BDC CLO 4 Depositor LLC, a Delaware LLC, our direct subsidiary;

•“Controlling Class” refers to the most senior class of notes then outstanding of the 2014 Issuer, 2018 Issuer, GCIC 2018 Issuer or the 2020 Issuer, as applicable;

•“Funding” refers to Golub Capital BDC Funding LLC, a Delaware LLC, our direct subsidiary;

•“Funding II” refers to Golub Capital BDC Funding II LLC, a Delaware LLC, our direct subsidiary;

•“Funding Subsidiaries” refers, collectively, to, prior to termination on the Credit Facility on February 4, 2019, Funding, Funding II, GCIC Funding, GCIC Funding II and each, a “Funding Subsidiary”;

•“GCIC Funding” refers to GCIC Funding LLC, a Delaware LLC, our direct subsidiary;

•“GCIC Funding II” refers to GCIC Funding II LLC, a Delaware LLC, our direct subsidiary;

•“Merger Sub” refers to Fifth Ave Subsidiary Inc., our wholly owned subsidiary;

•“GCIC” refers to Golub Capital Investment Corporation, a Maryland corporation that we acquired on September 16, 2019 pursuant to an agreement and plan of merger by and among us, GCIC, GC Advisors, and for certain limited purposes our Administrator, or, as amended, the Merger Agreement; prior to such acquisition, which we refer to as the Merger, GCIC was an externally managed, closed-end, non-diversified management investment company that elected to be regulated as a business development company under the Investment Company Act of 1940, as amended, or the 1940 Act, and whose investment adviser was GC Advisors;

•“2014 Debt Securitization” refers to the $402.6 million term debt securitization that we completed on June 5, 2014, as most recently amended on March 23, 2018 and redeemed on August 26, 2020, in which the 2014 Issuer issued an aggregate of $402.6 million of notes, or the “2014 Notes,” including $191.0 million of Class A-1-R 2014 Notes, which bore interest at a rate of three-month LIBOR, plus 0.95%, $20.0 million of Class A-2-R 2014 Notes, which bore interest at a rate of three-month LIBOR plus 0.95%, $35.0 million of Class B-R 2014 Notes, which bore interest at a rate of three-month LIBOR plus 1.40%, $37.5 million of Class C-R 2014 Notes, which bore interest at a rate of three-month LIBOR plus 1.55%, and $119.1 million of membership interests that did not bear interest;

•“2018 Debt Securitization” refers to the $602.4 million term debt securitization that we completed on November 16, 2018, in which the 2018 Issuer issued an aggregate of $602.4 million of notes, or the “2018 Notes,” including $327.0 million of Class A 2018 Notes, which bear interest at a rate of three-month LIBOR, plus 1.48%, $61.2 million of Class B 2018 Notes, which bear interest at a rate of three-month LIBOR plus 2.10%, $20.0 million of Class C-1 2018 Notes, which bear interest at a rate of three-month LIBOR plus 2.80%, $38.8 million of Class C-2 2018 Notes, which bear interest at a rate of three-month

1

LIBOR plus 2.65%, $42.0 million of Class D 2018 Notes, which bear interest at a rate of three-month LIBOR plus 2.95%, and $113.4 million of Subordinated 2018 Notes that do not bear interest;

•“GCIC 2018 Debt Securitization” refers to the $908.2 million term debt securitization that we acquired as part of the Merger. On December 13, 2018, the GCIC 2018 Issuer issued an aggregate of $908.2 million of notes, or the "GCIC 2018 Notes", including $490.0 million of AAA/AAA Class A-1 GCIC 2018 Notes, which bear interest at a rate of three-month LIBOR plus 1.48%, $38.5 million of AAA Class A-2 GCIC 2018 Notes, which bear interest at a fixed rate of 4.67%, $18.0 million of AA Class B-1 GCIC 2018 Notes, which bear interest at a rate of three-month LIBOR plus 2.25%, $27.0 million of the Class B-2 GCIC 2018 Notes, which bear interest at a rate of three-month LIBOR plus 1.75%, $95.0 million of Class C GCIC 2018 Notes, which bear interest at a rate of three-month LIBOR plus 2.30%, $60.0 million of Class D GCIC 2018 Notes, which bear interest at a rate of three-month LIBOR plus 2.75% and $179.7 million of Subordinated GCIC 2018 Notes that do not bear interest;

•“2020 Debt Securitization” refers to the $330.4 million term debt securitization, of which $297.4 million was funded at closing, that we completed on August 26, 2020, in which the 2020 Issuer issued an aggregate of $330.4 million of notes, or the “2020 Notes,” including $137.5 million of AAA Class A-1 2020 Notes, which bear interest at the three-month LIBOR plus 2.35%, $10.5 million of AAA Class A-2 2020 Notes, which bear interest at the three-month LIBOR plus 2.75%, $21.0 million of AA Class B 2020 Notes, which bear interest at the three-month LIBOR plus 3.20%, up to $33.0 million A Class C 2020 Notes, which remained unfunded upon closing of the transactions, and, if funded, will bear interest at the three-month LIBOR plus a spread set in connection with the funding date but which in no event will be greater than 3.65%, and approximately $108.4 million of Subordinated 2020 Notes, which do not bear interest. As part of the 2020 Debt Securitization, we also entered into a credit agreement upon closing pursuant to which various financial institutions and other persons, which are, or may become, parties thereto as lenders committed to make $20.0 million of AAA Class A-1-L loans to the Company, or the “2020 Loans,” , which bear interest at the three-month LIBOR plus 2.35% and were fully drawn upon closing of the transactions;

•“Debt Securitizations” refers collectively to the 2014 Debt Securitization, the 2018 Debt Securitization, the GCIC 2018 Debt Securitization and the 2020 Debt Securitization and each, a “Debt Securitization;”

•“SLF” refers to Senior Loan Fund LLC, a Delaware LLC, which became our direct subsidiary as of January 1, 2020. Prior to January 1, 2020, SLF was an unconsolidated subsidiary, in which we co-invested with RGA Reinsurance Company, or RGA, primarily in senior secured loans. SLF was capitalized as transactions were completed and all portfolio and investment decisions in respect of SLF were approved by representatives of each of the members (with unanimous approval required from either (i) one representative of each of us and RGA or (ii) both representatives of each of us and RGA). Prior to January 1, 2020, we owned 87.5% of the LLC equity interests of SLF;

•“GCIC SLF” refers to GCIC Senior Loan Fund LLC, a Delaware LLC, which became our direct subsidiary as of January 1, 2020. Prior to January 1, 2020, GCIC SLF was an unconsolidated subsidiary, that we acquired as part of the Merger, in which we co-invested with Aurora National Life Assurance Company, a whollyowned subsidiary of RGA, or Aurora, primarily in senior secured loans of middle-market companies. GCIC SLF was capitalized as transactions were completed and all portfolio and investment decisions in respect of GCIC SLF were approved by the GCIC SLF investment committee, which consisted of two representatives of each of the members (with unanimous approval required from either (i) one representative of each of us and Aurora or (ii) both representatives of each of us and Aurora). Prior to January 1, 2020, we owned 87.5% of the LLC equity interests of GCIC SLF;

•“Senior Loan Funds” refers collectively to SLF and GCIC SLF, and each a "Senior Loan Fund";

•“Credit Facility” refers to the amended and restated senior secured revolving credit facility that Funding, originally entered into on July 21, 2011 and terminated on February 4, 2019, with Wells Fargo Securities, LLC, as administrative agent, and Wells Fargo Bank, N.A., as lender and collateral agent, that, as of the date of its termination, allowed for borrowing up to $170 million and bore interest at a rate of one-month LIBOR plus 2.15% per annum through the reinvestment period, which would have ended on September 20, 2019, and that would have matured on September 21, 2023;

•“WF Credit Facility” refers to the senior secured revolving credit facility that GCIC Funding originally entered into on October 10, 2014 with Wells Fargo Securities, LLC as administrative agent, and Wells

2

Fargo Bank, N.A., as lender, as most recently amended on May 29, 2019, that allowed for borrowing up to $300.0 million as of September 30, 2020 and that bears interest at a rate of one-month LIBOR plus 2.00% per annum through the maturity date, March 21, 2024;

•“DB Credit Facility” refers to the senior secured revolving credit facility that GCIC Funding II entered into on December 31, 2018, with GCIC, as equityholder and as servicer, Deutsche Bank AG, New York Branch, as facility agent, the other agents parties thereto, each of the entities from time to time party thereto as securitization subsidiaries and Wells Fargo Bank, National Association, as collateral agent and as collateral custodian, that as of September 30, 2020, allowed for borrowing up to $250.0 million and that bears interest at a rate of the applicable base rate plus 1.90% per annum through the reinvestment period, which continues through December 31, 2021. Following expiration of the reinvestment period, the interest rate on outstanding borrowings under the DB Credit Facility will reset to the applicable base rate plus 2.00% for the remaining term of the DB Credit Facility, which is scheduled to mature on December 31, 2024. The base rate under the DB Credit Facility is (i) the three-month Canadian Dollar Offered Rate with respect to any advances denominated in Canadian dollars, (ii) the three-month EURIBOR with respect to any advances denominated in euros, (iii) the three-month Bank Bill Swap Rate with respect to any advances denominated in Australian dollars and (iv) the three-month LIBOR with respect to any other advances. On October 9, 2020, all outstanding borrowings under the DB Credit Facility were repaid following which the DB Credit Facility was terminated;

•“MS Credit Facility II” refers to our senior secured revolving credit facility that Golub Capital BDC Funding II, LLC, a Delaware LLC and our direct subsidiary, entered into on February 1, 2019, with Morgan Stanley Senior Funding, Inc., as the administrative agent, each of the lenders from time to time party thereto, each of the securitization subsidiaries from time to time party thereto, and Wells Fargo Bank, N.A., as collateral agent, account bank and collateral custodian, as most recently amended on June 18, 2020, that allowed for borrowing up to $400.0 million as of September 30, 2020 and bears interest at the applicable base rate plus 2.45% per annum through the revolving period, which ends February 1, 2021, and bears interest at the applicable base rate plus 2.95% following the revolving period through the stated maturity date of February 1, 2024;

•“Revolving Credit Facilities” refers collectively to, prior to its termination on February 4, 2019, the Credit Facility, together with the WF Credit Facility, DB Credit Facility and the MS Credit Facility II, and each a “Revolving Credit Facility”;

•“2024 Unsecured Notes” refers to the issuance of $400.0 million in aggregate principal amount of unsecured notes that were issued on October 2, 2020 and mature on April 15, 2024 and bear interest at 3.375% per year. The 2024 Unsecured Notes require payment of interest semi-annually, and all principal is due upon maturity. The 2024 Notes may be redeemed in whole or in part at any time at our option at a redemption price equal to par plus a “make whole” premium, if applicable, as determined pursuant to the indenture governing the 2024 Notes, and any accrued and unpaid interest.

•“Initial Merger” refers to the merger, on September 16, 2019, of Merger Sub with and into GCIC, with GCIC as the surviving company;

•“Subsequent Merger” refers to the merger that occurred immediately after the Initial Merger on September 16, 2019 of GCIC, as the surviving company of the Initial Merger, with and into, with Golub Capital BDC, Inc., as the surviving company;

•“Merger” refers to the Initial Merger, together with, unless the context otherwise requires, the Subsequent Merger;

•“Merger Agreement” refers to the Agreement and Plan of Merger, dated November 27, 2018, by and among us, Merger Sub, GCIC, GC Advisors, and, for certain limited purposes, the Administrator, as amended by the First Amendment to the Agreement and Plan of Merger, dated December 21, 2018, by and among us, Merger Sub, GCIC, GC Advisors, and the Administrator and the Second Amendment to the Agreement and Plan of Merger, dated July 11, 2019, by and among us, Merger Sub, GCIC, GC Advisors, and the Administrator;

•“Adviser Revolver” refers to the line of credit with GC Advisors, which was most recently amended on October 28, 2019, and which allowed for borrowing up to $100.0 million as of September 30, 2020;

3

•“SBIC Funds” refers collectively to our consolidated subsidiaries, GC SBIC IV, L.P.,GC SBIC V, L.P. and GC SBIC VI, L.P.;

•“GC Advisors” refers to GC Advisors LLC, a Delaware LLC, our investment adviser;

•“Administrator” refers to Golub Capital LLC, a Delaware LLC, an affiliate of GC Advisors and our administrator;

•“Investment Advisory Agreement” refers to the Third Amended and Restated Investment Advisory Agreement by and between us and GC Advisors, dated as of September 16, 2019;

•“Prior Investment Advisory Agreement” refers to the Second Amended and Restated Investment Advisory Agreement by and between us and GC Advisors, dated as of August 4, 2014; and

•“Golub Capital” refers, collectively, to the activities and operations of Golub Capital LLC (formerly Golub Capital Management LLC), which entity employs all of Golub Capital’s investment professionals, GC Advisors and associated investment funds and their respective affiliates.

4

Item 1. Business

GENERAL

We are an externally managed, closed-end, non-diversified management investment company that has elected to be regulated as a business development company under the 1940 Act. In addition, for U.S. federal income tax purposes, we have elected to be treated as a regulated investment company, or RIC, under Subchapter M of the Internal Revenue Code of 1986, as amended, or the Code. We were formed in November 2009 to continue and expand the business of our predecessor, Golub Capital Master Funding LLC, which commenced operations in July 2007. We make investments primarily in one stop (a loan that combines characteristics of traditional first lien senior secured loans and second lien or subordinated loans) and other senior secured loans of middle-market companies that are, in most cases, sponsored by private equity firms. GC Advisors structures our one stop loans as senior secured loans, and we obtain security interests in the assets of the portfolio company that serve as collateral in support of the repayment of these loans. This collateral may take the form of first-priority liens on the assets of the portfolio company. In many cases, we together with our affiliates are the sole lenders of one stop loans, which can afford us additional influence over the borrower in terms of monitoring and, if necessary, remediation in the event of underperformance.

In this annual report on Form 10-K, the term “middle-market” generally refers to companies having earnings before interest, taxes, depreciation and amortization, or EBITDA, of less than $100.0 million annually.

Our investment objective is to generate current income and capital appreciation by investing primarily in one stop and other senior secured loans of U.S. middle-market companies. We may also selectively invest in second lien and subordinated loans of, and warrants and minority equity securities in, U.S. middle-market companies. We intend to achieve our investment objective by (1) accessing the established loan origination channels developed by Golub Capital, a leading lender to middle-market companies with over $30.0 billion in capital under management as of September 30, 2020, (2) selecting investments within our core middle-market company focus, (3) partnering with experienced private equity firms, or sponsors, in many cases with whom Golub Capital has invested alongside in the past, (4) implementing the disciplined underwriting standards of Golub Capital and (5) drawing upon the aggregate experience and resources of Golub Capital.

We seek to create a portfolio that includes primarily one stop and other senior secured loans by primarily investing approximately $10.0 million to $75.0 million of capital, on average, in the securities of U.S. middle-market companies. We expect to selectively invest more than $75.0 million in some of our portfolio companies and generally expect that the size of our individual investments will vary proportionately with the size of our capital base.

We generally invest in securities that have been rated below investment grade by independent rating agencies or that would be rated below investment grade if they were rated. These securities, which may be referred to as “junk,” have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. In addition, many of our debt investments have floating interest rates that reset on a periodic basis and typically do not fully pay down principal prior to maturity, which may increase our risk of losing part or all of our investment.

GCIC Acquisition

On September 16, 2019, we completed our acquisition of GCIC, pursuant to the Merger Agreement. As a result of, and as of the effective time of, the Merger, GCIC’s separate existence ceased.

In accordance with the terms of the Merger Agreement, at the effective time of the Merger, each outstanding share of GCIC’s common stock was converted into the right to receive 0.865 shares of our common stock (with GCIC’s stockholders receiving cash in lieu of fractional shares of our common stock). As a result of the Merger, we issued an aggregate of 71,779,964 shares of our common stock to former stockholders of GCIC. Upon the consummation of the Merger, we entered into the Investment Advisory Agreement, with GC Advisors, which replaced the Prior Investment Advisory Agreement.

5

SLF and GCIC SLF Purchase Agreement

On January 1, 2020, we entered into a purchase agreement, or the Purchase Agreement with RGA and Aurora, or together the Transferors, SLF, and GCIC SLF. Prior to entering into the Purchase Agreement, the Transferors owned 12.5% of the LLC equity interests in each Senior Loan Fund, while we owned the remaining 87.5% of the LLC equity interests in each Senior Loan Fund. Pursuant to the Purchase Agreement, RGA and Aurora agreed to sell their LLC equity interests in each Senior Loan Fund to us, effective as of January 1, 2020. As consideration for the purchase of the LLC equity interests, we paid each Transferor an amount, in cash, equal to the net asset value of such Transferor's Senior Loan Fund LLC equity interests as of December 31, 2019, or the Net Asset Value, along with interest on such Net Asset Value accrued from the date of the Purchase Agreement through, but excluding, the payment date at a rate equal to the short-term applicable federal rate. In February 2020, we paid an aggregate of $17.0 million to the Transferors to acquire their respective LLC interests in the Senior Loan Funds.

As a result of the Purchase Agreement, on January 1, 2020, SLF and GCIC SLF became our wholly-owned subsidiaries. In addition, our capital commitments and those of the Transferors were terminated. As wholly-owned subsidiaries, the assets, liabilities, income and expenses of the Senior Loan Funds were consolidated into our financial statements and notes thereto for periods ending on or after January 1, 2020, and are included for purposes of determining our asset coverage ratio.

Rights Offering

On May 15, 2020, we completed a transferable rights offering and issued a total of 33,451,902 shares of our

common stock. We issued to stockholders of record on April 8, 2020 one transferable right for each four shares of our common stock held on the record date. Each holder of rights was entitled to subscribe for one share of common stock for every right held at a subscription price of $9.17 per share. Net proceeds after deducting the dealer manager fees and other offering expenses were approximately $300.4 million. 3,191,448 shares of common stock were purchased in the rights offering by affiliates of GC Advisors.

Information Available

Our address is 200 Park Avenue, 25th Floor, New York, NY 10166. Our phone number is (212) 750-6060, and our internet address is www.golubcapitalbdc.com. We make available, free of charge, on our website our proxy statement, annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after we electronically file such material with, or furnish it to, the U.S. Securities and Exchange Commission, or SEC. Information contained on our website is not incorporated by reference into this annual report on Form 10-K and you should not consider information contained on our website to be part of this annual report on Form 10-K or any other report we file with the SEC.

The SEC also maintains a website that contains reports, proxy and information statements and other information we file with the SEC at www.sec.gov. Copies of these reports, proxy and information statements and other information may also be obtained, after paying a duplicating fee, by electronic request at publicinfo@sec.gov.

Our Adviser

Our investment activities are managed by our investment adviser, GC Advisors. GC Advisors is responsible for sourcing potential investments, conducting research and due diligence on prospective investments and equity sponsors, analyzing investment opportunities, structuring our investments and monitoring our investments and portfolio companies on an ongoing basis. GC Advisors was organized in September 2008 and is a registered investment adviser under the Investment Advisers Act of 1940, as amended, or the Advisers Act. Under our amended and restated investment advisory agreement, or the Investment Advisory Agreement, with GC Advisors, we pay GC Advisors a base management fee and an incentive fee for its services. See “Business — Management Agreements — Management Fee” for a discussion of the base management fee and incentive fee, including the cumulative income incentive fee and the income and capital gains incentive fee, payable by us to GC Advisors. Unlike most closed-end funds whose fees are based on assets net of leverage, our base management fee is based on our average-adjusted gross assets (including leverage but adjusted to exclude cash and cash equivalents so that investors do not pay the base management fee on such assets) and, therefore, GC Advisors benefits when we incur debt or use leverage. For purposes of the Investment Advisory Agreement, cash equivalents means U.S. government securities and commercial paper instruments maturing within 270 days of purchase. Additionally, under the

6

incentive fee structure, GC Advisors benefits when capital gains are recognized and, because it determines when a holding is sold, GC Advisors controls the timing of the recognition of capital gains. Our board of directors is charged with protecting our interests by monitoring how GC Advisors addresses these and other conflicts of interest associated with its management services and compensation. While not expected to review or approve each borrowing, our independent directors periodically review GC Advisors’ services and fees as well as its portfolio management decisions and portfolio performance. In connection with these reviews, our independent directors consider whether our fees and expenses (including those related to leverage) remain appropriate. See “Business — Management Agreements — Board Approval of the Investment Advisory Agreement.”

GC Advisors is an affiliate of Golub Capital and pursuant to a staffing agreement, or the Staffing Agreement, Golub Capital LLC makes experienced investment professionals available to GC Advisors and provides access to the senior investment personnel of Golub Capital LLC and its affiliates. The Staffing Agreement provides GC Advisors with access to investment opportunities, which we refer to in the aggregate as deal flow, generated by Golub Capital LLC and its affiliates in the ordinary course of their businesses and commits the members of GC Advisors’ investment committee to serve in that capacity. As our investment adviser, GC Advisors is obligated to allocate investment opportunities among us and its other clients fairly and equitably over time in accordance with its allocation policy. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Related Party Transactions.” However, there can be no assurance that such opportunities will be allocated to us fairly or equitably in the short-term or over time. GC Advisors seeks to capitalize on the significant deal origination, credit underwriting, due diligence, investment structuring, execution, portfolio management and monitoring experience of Golub Capital LLC’s investment professionals.

An affiliate of GC Advisors, the Administrator, provides the administrative services necessary for us to operate. See “Business — Management Agreements — Administration Agreement” for a discussion of the fees and expenses (subject to the review and approval of our independent directors) we are required to reimburse to the Administrator.

About Golub Capital

Golub Capital, founded in 1994, is a leading lender to middle-market companies, with a long track record of investing in senior secured, one stop, second lien and subordinated loans. As of September 30, 2020, Golub Capital had over $30.0 billion of capital under management. Since its inception, Golub Capital has closed deals with over 300 middle-market sponsors and repeat transactions with over 200 sponsors.

Golub Capital’s middle-market lending group is managed by a four-member senior management team consisting of Lawrence E. Golub, David B. Golub, Andrew H. Steuerman and Gregory W. Cashman. As of September 30, 2020, Golub Capital had more than 140 investment professionals supported by more than 350 administrative and back office personnel that focus on operations, finance, legal and compliance, accounting and reporting, marketing, information technology and office management.

Investment Criteria/Guidelines

Our investment objective is to generate current income and capital appreciation by investing primarily in one stop and other senior secured loans of U.S. middle market companies. We seek to generate strong risk-adjusted net returns by assembling a portfolio of investments across a broad range of industries and private equity investors.

We primarily target U.S. middle-market companies controlled by private equity investors that require capital for growth, acquisitions, recapitalizations, refinancings and leveraged buyouts. We also make opportunistic loans to independently owned and publicly held middle-market companies. We seek to partner with strong management teams executing long-term growth strategies. Target businesses will typically exhibit some or all of the following characteristics:

•annual EBITDA of less than $100.0 million annually;

•sustainable leading positions in their respective markets;

•scalable revenues and operating cash flow;

•experienced management teams with successful track records;

•insulation from the effects of the novel coronavirus (“COVID-19”) pandemic;

•stable, predictable cash flows with low technology and market risks;

•a substantial equity cushion in the form of capital ranking junior to our investment;

•low capital expenditures requirements;

7

•a North American base of operations;

•strong customer relationships;

•products, services or distribution channels having distinctive competitive advantages;

•defensible niche strategy or other barriers to entry; and

•demonstrated growth strategies.

While we believe that the criteria listed above are important in identifying and investing in prospective portfolio companies, not all of these criteria will be met by each prospective portfolio company.

Investment Process Overview

We view our investment process as consisting of four distinct phases described below:

Origination. GC Advisors sources investment opportunities through access to a network of over 10,000 individual contacts developed in the financial services and related industries by Golub Capital and managed through a proprietary customer relationship database. Among these contacts is an extensive network of private equity firms and relationships with leading middle-market senior lenders. The senior deal professionals of Golub Capital supplement these leads through personal visits and marketing campaigns. It is their responsibility to identify specific opportunities, to refine opportunities through candid exploration of the underlying facts and circumstances and to apply creative and flexible thinking to solve clients’ financing needs. The investment professionals of Golub Capital have a long and successful track record investing in companies across many industry sectors. Collectively, these investment professionals have completed investments in over 1,000 companies at Golub Capital. Golub Capital’s investments have been made in the following industries, among others: healthcare, restaurant and retail, software, digital and technology services, specialty manufacturing, business services, consumer products and services, food and beverages, aerospace and defense and value-added distribution.

Golub Capital has principal lending offices in Chicago, New York, San Francisco and the Charlotte metropolitan area. Each of Golub Capital's originators maintains long-standing customer relationships and is responsible for covering a specified target market. We believe those originators’ strength and breadth of relationships across a wide range of markets generate numerous financing opportunities, which we believe enables GC Advisors to be highly selective in recommending investments to us.

Underwriting. We utilize the systematic, consistent approach to underwriting developed by Golub Capital, with a particular focus on determining the value of a business in a downside scenario. The key criteria that we consider include (1) strong and resilient underlying business fundamentals, (2) a substantial equity cushion in the form of capital ranking junior in right of payment to our investment and (3) a conclusion that overall “downside” risk is manageable. While the size of this equity cushion will vary over time and across industries, the equity cushion generally sought by GC Advisors today is between 35% and 45% of total portfolio capitalization. We generally focus on the criteria developed by Golub Capital for evaluating prospective portfolio companies, which uses a combination of analyses, including (1) fundamental analysis of a business’s financial statements, health, management, competitive advantages, competitors and markets; (2) analysis of opportunities in a given market based upon fluctuations due to seasonal, financial and economic factors; (3) quantitative analysis of the relative risk-return characteristics of investments and a comparison of yields between asset classes and other indicators; and (4) analysis of proprietary and secondary models. In evaluating a particular company, we put more emphasis on credit considerations (such as (1) loan-to-value ratio (which is the amount of our loan divided by the enterprise value of the company in which we are investing), (2) the ability of the company to maintain a liquidity cushion through economic cycles and in downside scenarios, (3) the ability of the company to service its fixed charge obligations under a variety of scenarios and (4) its anticipated strategic value in a downturn) than on profit potential and loan pricing. Based upon a combination of bottom-up analysis of the individual investment and GC Advisors’ expectations of future market conditions, GC Advisors seeks to assess the relative risk and reward for each investment. GC Advisors seeks to mitigate the risks of a single company or single industry through portfolio diversification. GC Advisors also considers environmental, social and governance considerations in the investment decision-making process, in accordance with its ESG policy. Golub Capital’s due diligence process for middle market credits will typically entail:

•a thorough review of historical and pro forma financial information;

•on-site visits;

8

•interviews with management and employees;

•a review of loan documents and material contracts;

•third-party “quality of earnings” accounting due diligence;

•when appropriate, background checks on key managers and research relating to the company’s business, industry, markets, customers, suppliers, products and services and competitors; and

•the commission of third-party market studies when appropriate.

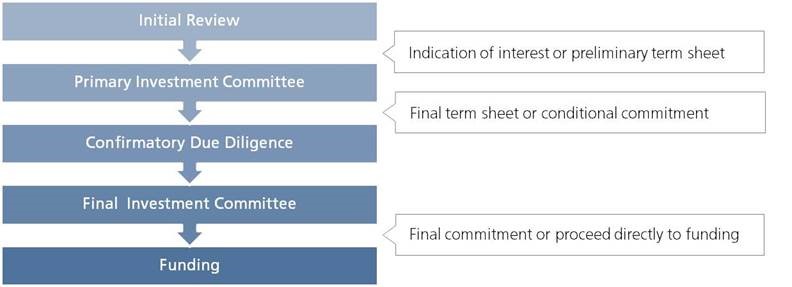

The following chart illustrates the stages of Golub Capital’s evaluation and underwriting process:

ILLUSTRATIVE DEAL EVALUATION PROCESS

Execution. In executing transactions for us, GC Advisors utilizes the due diligence process developed by Golub Capital. Through a consistent approach to underwriting and careful attention to the details of execution, it seeks to close deals as fast or faster than competitive financing providers while maintaining discipline with respect to credit, pricing and structure to ensure the ultimate success of the financing. Upon completion of due diligence, the investment team working on an investment delivers a memorandum to GC Advisors’ investment committee. Once an investment has been approved by the investment committee, it moves through a series of steps towards negotiation of final documentation. Upon completion of final documentation, a loan is funded upon the execution of an investment committee memorandum by members of GC Advisors’ investment committee.

Monitoring. We view active portfolio monitoring as a vital part of our investment process. We consider board observation rights, where appropriate, regular dialogue with company management and sponsors and detailed, internally generated monitoring reports to be critical to our performance. Golub Capital has developed a monitoring template that is designed to reasonably ensure compliance with these standards. This template is used by GC Advisors as a tool to assess investment performance relative to our investment plan. In addition, our portfolio companies often rely on GC Advisors to provide them financial and capital markets expertise.

As part of the monitoring process, GC Advisors regularly assesses the risk profile of each of our investments and rates each of them based on an internal system developed by Golub Capital and its affiliates. This system is not generally accepted in our industry or used by our competitors. It is based on the following categories, which we refer to as GC Advisors’ internal performance ratings:

9

| Internal Performance Ratings | ||||||||

| Rating | Definition | |||||||

| 5 | Involves the least amount of risk in our portfolio. The borrower is performing above expectations, and the trends and risk factors are generally favorable. | |||||||

| 4 | Involves an acceptable level of risk that is similar to the risk at the time of origination. The borrower is generally performing as expected, and the risk factors are neutral to favorable. | |||||||

| 3 | Involves a borrower performing below expectations and indicates that the loan’s risk has increased somewhat since origination. The borrower could be out of compliance with debt covenants; however, loan payments are generally not past due. | |||||||

| 2 | Involves a borrower performing materially below expectations and indicates that the loan’s risk has increased materially since origination. In addition to the borrower being generally out of compliance with debt covenants, loan payments could be past due (but generally not more than 180 days past due). | |||||||

| 1 | Involves a borrower performing substantially below expectations and indicates that the loan’s risk has substantially increased since origination. Most or all of the debt covenants are out of compliance and payments are substantially delinquent. Loans rated 1 are not anticipated to be repaid in full and we will reduce the fair market value of the loan to the amount we anticipate will be recovered. | |||||||

Our internal performance ratings do not constitute any rating of investments by a nationally recognized statistical rating organization or represent or reflect any third-party assessment of any of our investments.

For any investment rated 1, 2 or 3, GC Advisors will increase its monitoring intensity and prepare regular updates for the investment committee, summarizing current operating results and material impending events and suggesting recommended actions.

GC Advisors monitors and, when appropriate, changes the internal performance ratings assigned to each investment in our portfolio. In connection with our valuation process, GC Advisors and our board of directors review these internal performance ratings on a quarterly basis.

The following table shows the distribution of our investments on the 1 to 5 internal performance rating scale at fair value as of September 30, 2020 and 2019:

| September 30, 2020 | September 30, 2019 | |||||||||||||||||||||||||

| Internal Performance Rating | Investments at Fair Value (In thousands) | Percentage of Total Investments | Investments at Fair Value (In thousands) | Percentage of Total Investments | ||||||||||||||||||||||

| 5 | $ | 257,409 | 6.1 | $ | 115,318 | 2.7 | ||||||||||||||||||||

| 4 | 3,085,610 | 72.8 | 3,787,809 | 88.2 | ||||||||||||||||||||||

| 3 | 836,560 | 19.7 | 337,358 | 7.9 | ||||||||||||||||||||||

| 2 | 57,754 | 1.4 | 52,434 | 1.2 | ||||||||||||||||||||||

| 1 | 877 | —* | 13 | —* | ||||||||||||||||||||||

| Total | $ | 4,238,210 | 100.0 | $ | 4,292,932 | 100.0 | ||||||||||||||||||||

| * | Represents an amount less than 0.1%. | ||||

Investment Committee

GC Advisors’ investment committee, which is comprised of officers of GC Advisors, evaluates and approves all of our investments, subject to the oversight of our board of directors. The investment committee process is intended to bring the diverse experience and perspectives of the committee’s members to the analysis and consideration of each investment. The investment committee currently consists of Lawrence E. Golub, David B. Golub, Andrew H. Steuerman and Gregory W. Cashman. The investment committee serves to provide investment consistency and adherence to our core investment philosophy and policies. The investment committee also determines appropriate investment sizing and suggests ongoing monitoring requirements.

In addition to reviewing investments, investment committee meetings serve as a forum to discuss credit views and outlooks. Potential transactions and deal flow are reviewed on a regular basis. Members of the investment team are encouraged to share information and credit views with the investment committee early in their analysis. We believe this process improves the quality of the analysis and assists the deal team members to work more efficiently.

10

Each transaction is presented to the investment committee in a formal written report. All of our new investments must be approved by a consensus of the investment committee. Each member of the investment committee performs a similar role for other investment funds, accounts or other investment vehicles, collectively referred to as accounts, sponsored or managed by Golub Capital and its affiliates.

Investment Structure

Once GC Advisors determines that a prospective portfolio company is suitable for investment, GC Advisors typically works with the private equity sponsor, if applicable, the management of that company and its other capital providers to structure an investment. GC Advisors negotiates with these parties to agree on how our investment should be structured relative to the other capital in the portfolio company’s capital structure.

GC Advisors structures our investments, which typically have maturities of three to seven years as described below. Our loans typically provide for moderate loan amortization in the early years of the loan, with the majority of the amortization deferred until loan maturity, and there is a risk of loss if the borrower is unable to pay the lump sum or refinance the amount at maturity.

Senior Secured Loans. GC Advisors structures these investments as senior secured loans. We obtain security interests in the assets of the portfolio company that serve as collateral in support of the repayment of such loans. This collateral often takes the form of first-priority liens on the assets of the portfolio company borrower.

One Stop Loans. GC Advisors structures our one-stop loans as senior secured loans. A one-stop loan is a single loan that blends the characteristics of traditional senior debt and traditional junior debt. The structure generally combines the stronger lender protections associated with senior debt with the superior economics of junior capital. We obtain security interests in the assets of the portfolio company that serve as collateral in support of the repayment of these loans. This collateral often takes the form of first-priority liens on the assets of the portfolio company. In some cases, one-stop loans are provided to borrowers experiencing high revenue growth supported by a high level of discretionary expenditures. As part of the underwriting of such loans and consistent with industry practice, we adjust our characterization of the earnings of such borrowers for a reduction or elimination of such discretionary expenses if appropriate. One-stop loans typically provide for moderate loan amortization in the initial years of the facility, with the majority of the amortization deferred until loan maturity. One-stop loans generally allow the borrower to make a large lump sum payment of principal at the end of the loan term and there is a risk of loss if the borrower is unable to pay the lump sum or refinance the amount owed at maturity. In many cases, we are the sole lender or we, together with our affiliates, are the sole lenders of one-stop loans, which can afford us additional influence over the borrower in terms of monitoring and, if necessary, remediating any underperformance.

One stop loans include loans to technology companies undergoing strong growth due to new services, increased adoption and/or entry into new markets. We refer to loans to these companies as late stage lending loans. Other targeted characteristics of late stage lending businesses include strong customer revenue retention rates, a diversified customer base and backing from growth equity or venture capital firms. In some cases, the borrower’s high revenue growth is supported by a high level of discretionary spending. As part of the underwriting of such loans and consistent with industry practice, we may adjust our characterization of the earnings of such borrowers for a reduction or elimination of such discretionary expenses, if appropriate.

Second Lien Loans. GC Advisors structures these investments as junior, secured loans. We obtain security interests in the assets of the portfolio company that serve as collateral in support of the repayment of such loans. This collateral typically takes the form of second priority liens on the assets of a portfolio company. Second lien loans typically provide for minimal loan amortization in the initial years of the facility, with the majority of the amortization deferred until loan maturity.

Subordinated Loans. GC Advisors structures these investments as unsecured, subordinated loans that provide for relatively high, fixed interest rates and provide us with significant current interest income. These loans typically require interest-only payments (often representing a combination of cash pay and PIK interest) in the early years, with amortization of principal deferred until loan maturity. Subordinated loans generally allow the borrower to make a large lump sum payment of principal at the end of the loan term, and there is a risk of loss if the borrower is unable to pay the lump sum or refinance the amount owed at maturity.

Second lien loans and subordinated loans are generally more volatile than secured loans and may involve a greater risk of loss of principal. In addition, the PIK feature of many subordinated loans, which effectively operates as negative amortization of loan principal, increases credit risk exposure over the life of the loan.

11

Equity Investments. GC Advisors structures these investments as direct or indirect minority equity co-investments in a portfolio company, usually on terms similar to the controlling private equity sponsor and in connection with our loan to such portfolio company. As a result, if a portfolio company appreciates in value, we can achieve additional investment return from these equity co-investments. GC Advisors can structure these equity co-investments to include provisions protecting our rights as a minority-interest holder, which could include a “put,” or right to sell such securities back to the issuer, upon the occurrence of specified events or demand and “piggyback” registration rights. However, because these equity co-investments will typically be in private companies, there is no guarantee that we, as a minority-interest holder, will control the timing or value of our realization of any gains on such investments. Our equity co-investments will typically include customary “tagalong” or “drag-along” rights that will permit or require us to participate in a sale of such equity co-investments at such time as the majority owners, not GC Advisors, determine.

GC Advisors tailors the terms of each investment to the facts and circumstances of the transaction and the prospective portfolio company, negotiating a structure that protects our rights and manages our risk while creating incentives for the portfolio company to achieve its business plan and improve its operating results. GC Advisors seeks to limit the downside potential of our investments by:

•selecting investments that we believe have a very low probability of loss;

•requiring a total return on our investments that we believe will compensate us appropriately for credit risk; and

•negotiating covenants in connection with our investments that afford our portfolio companies as much flexibility in managing their businesses as possible, consistent with the preservation of our capital. Such restrictions could include affirmative and negative covenants, default penalties, lien protection, change of control provisions and board rights.

We expect to hold most of our investments to maturity or repayment, but we may sell some of our investments earlier if a liquidity event occurs, such as a sale, recapitalization or worsening of the credit quality of the portfolio company.

Investments

We seek to create a portfolio that includes primarily one stop and other senior secured loans by investing approximately $10.0 million to $75.0 million of capital, on average, in the securities of middle-market companies. Set forth below is a list of our ten largest portfolio company investments as of September 30, 2020, as well as the top ten industries in which we were invested as of September 30, 2020, calculated as a percentage of our total investments at fair value as of such date.

| Portfolio Company | Investments at Fair Value (In thousands) | Percentage of Total Investments | |||||||||

| Diligent Corporation | $ | 87,659 | 2.1 | % | |||||||

| E2open, LLC | 84,174 | 2.0 | |||||||||

| Bullhorn, Inc. | 83,641 | 2.0 | |||||||||

| Transaction Data Systems, Inc. | 82,940 | 2.0 | |||||||||

| DCA Investment Holding, LLC | 81,780 | 1.9 | |||||||||

| GS Acquisitionco, Inc. | 75,924 | 1.8 | |||||||||

| Integration Appliance, Inc. | 68,822 | 1.6 | |||||||||

| Whitcraft LLC | 61,479 | 1.5 | |||||||||

| Veterinary Specialists of North America, LLC | 57,066 | 1.3 | |||||||||

| Apptio, Inc. | 57,009 | 1.3 | |||||||||

| $ | 740,494 | 17.5 | % | ||||||||

12

| Industry | Investments at Fair Value (In thousands) | Percentage of Total Investments | |||||||||

| Software | $ | 924,825 | 21.8 | % | |||||||

| Healthcare Providers and Services | 583,926 | 13.8 | |||||||||

| IT Services | 356,500 | 8.4 | |||||||||

| Specialty Retail | 311,117 | 7.3 | |||||||||

| Health Care Technology | 219,166 | 5.1 | |||||||||

| Healthcare Equipment and Supplies | 172,274 | 4.1 | |||||||||

| Hotels, Restaurants and Leisure | 165,722 | 3.9 | |||||||||

| Commercial Services and Supplies | 126,680 | 3.0 | |||||||||

| Food and Staples Retailing | 119,614 | 2.8 | |||||||||

| Insurance | 109,156 | 2.6 | |||||||||

| $ | 3,088,980 | 72.8 | % | ||||||||

Managerial Assistance

As a business development company, we offer, and must provide upon request, managerial assistance to our portfolio companies. This assistance would involve an arrangement to provide significant guidance and counsel concerning the management, operations or business objectives and policies of the portfolio company. The Administrator or an affiliate of the Administrator provides such managerial assistance on our behalf to portfolio companies that request this assistance. We could receive fees for these services and reimburse the Administrator or an affiliate of the Administrator, as applicable, for its allocated costs in providing such assistance, subject to the review and approval by our board of directors, including our independent directors.

Competition

Our primary competitors in providing financing to middle-market companies include public and private funds, other business development companies, commercial and investment banks, commercial financing companies and, to the extent they provide an alternative form of financing, private equity and hedge funds. Many of our competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. For example, we believe some competitors have access to funding sources that are not available to us. In addition, some of our competitors have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more relationships than us. Furthermore, many of our competitors are not subject to the regulatory restrictions that the 1940 Act imposes on us as a business development company or to the source-of-income, asset diversification and distribution requirements we must satisfy to maintain our qualification as a RIC.

We use the expertise of the investment professionals of Golub Capital and its affiliates to which we have access to assess investment risks and determine appropriate pricing for our investments in portfolio companies. In addition, the relationships of the senior members of Golub Capital and its affiliates enable us to learn about, and compete effectively for, financing opportunities with attractive middle-market companies in the industries in which we invest. See “Risk Factors — Risks Relating to our Business and Structure — We operate in a highly competitive market for investment opportunities, which could reduce returns and result in losses.”

Administration

We do not have any direct employees, and our day-to-day investment operations are managed by GC Advisors. Our business and affairs are managed under the direction of our board of directors. We have a chief executive officer, chief financial officer, chief compliance officer, managing director and director of corporate strategy, and to the extent necessary, our board of directors can elect to appoint additional officers going forward. Our officers are officers and/or employees of Golub Capital LLC, an affiliate of GC Advisors, and our allocable portion of the cost of our chief financial officer and chief compliance officer and their respective staffs is paid by us pursuant to the administration agreement, or the Administration Agreement, with the Administrator. See “Business - Management Agreements - Administration Agreement.”

13

SUMMARY RISK FACTORS

The risk factors described below are a summary of the principal risk factors associated with an investment in us. These are not the only risks we face. You should carefully consider these risk factors, together with the risk factors set forth in Item 1A. of this Annual Report on Form 10-K and the other reports and documents filed by us with the SEC.

We are subject to risks relating to our business and structure

•We are currently operating in a period of capital markets disruption and economic uncertainty.

•Events outside of our control, including public health crises, could negatively affect our portfolio companies, our investment adviser and the results of our operations.

•We are subject to risks associated with the current interest rate environment and to the extent we use debt to finance our investments, changes in interest rates will affect our cost of capital and net investment income.

•We are subject to risks associated with the discontinuation of LIBOR, which will affect our cost of capital and net investment income.

•We are dependent upon GC Advisors for our success and upon its access to the investment professionals and partners of Golub Capital and its affiliates.

•There are significant potential conflicts of interest that could affect our investment returns, including related to obligations of GC Advisors, in the valuation of investments and any arrangements with GC Advisors.

•We and GC Advisors could be the target of litigation or regulatory investigations.

•We are subject to certain risks related to our ability to qualify as a RIC and to related to regulations governing our operation as a business development company.

•We intend to finance our investments with borrowed money, which will accelerate and increase the potential for gain or loss on amounts invested and could increase the risk of investing in us.

•We are subject to risks associated with the Debt Securitizations and the Revolving Credit Facilities as well as our SBIC Funds.

•Adverse developments in the credit markets could impair our ability to enter into new debt financing arrangements.

•New or modified laws or regulations governing our operations could adversely affect our business.

•Our board of directors could change our investment objective, operating policies and strategies without prior notice or stockholder approval.

•Each of GC Advisors and the Administrator can resign on 60 days’ notice, and we can provide no assurance that we could find a suitable replacement within that time, resulting in a disruption in our operations that could adversely affect our financial condition, business and results of operations.

•We incur significant costs as a result of being a publicly traded company.

•We are highly dependent on information systems and systems failures could significantly disrupt our business, which could, in turn, negatively affect the market price of our common stock and our ability to pay distributions.

We are subject to risks relating to our investments

•Economic recessions or downturns could impair our portfolio companies and defaults by our portfolio companies will harm our operating results.

•Our debt investments and our investments in leveraged portfolio companies are risky.

•The lack of liquidity in our investments could adversely affect our business.

•Price declines and illiquidity in the corporate debt markets could adversely affect the fair value of our portfolio investments, reducing our net asset value through increased net unrealized depreciation.

•Our portfolio companies could prepay loans, which could reduce our yields if capital returned cannot be invested in transactions with equal or greater expected yields.

•We are subject to credit and default risk and our portfolio companies could be unable to repay or refinance outstanding principal on their loans at or prior to maturity, and rising interests rates could make it more difficult for portfolio companies to make periodic payments on their loans.

•Our portfolio could be concentrated in a limited number of portfolio companies and industries, which will subject us to a risk of significant loss if any of these companies defaults on its obligations under any of its debt instruments or if there is a downturn in a particular industry.

14

•We could hold the debt securities of leveraged companies that could, due to the significant volatility of such companies, enter into bankruptcy proceedings.

•Our failure to make follow-on investments in our portfolio companies could impair the value of our portfolio.

•Because we generally do not hold controlling equity interests in our portfolio companies, we generally will not be able to exercise control over our portfolio companies or to prevent decisions by management of our portfolio companies that could decrease the value of our investments.

•Our portfolio companies could incur debt that ranks equally with, or senior to, our investments in such companies and such portfolio companies could fail to generate sufficient cash flow to service their debt obligations to us.

•The disposition of our investments could result in contingent liabilities.

•GC Advisors’ liability is limited, and we have agreed to indemnify GC Advisors against certain liabilities, which could lead GC Advisors to act in a riskier manner on our behalf than it would when acting for its own account.

•We could be subject to risks if we engage in hedging transactions and could become subject to risks if we invest in foreign securities.

•We could suffer losses from our equity investments.

•We could be subject to lender liability claims with respect to our portfolio company investments.

We are subject to risks relating to our securities

•Investing in our securities could involve an above average degree of risk.

•Shares of closed-end investment companies, including business development companies, often trade at a discount to their net asset value.

•There is a risk that investors in our equity securities may not receive distributions or that our distributions may not grow over time and a portion of our distributions may be a return of capital.

•The market price of our securities could fluctuate significantly.

•The 2024 Unsecured Notes are unsecured and therefore are effectively subordinated to any secured indebtedness we have incurred or may incur in the future.

•The 2024 Unsecured Notes are structurally subordinated to the indebtedness and other liabilities of our subsidiaries.

•The indenture governing the 2024 Unsecured Notes contains limited protection for holders of the 2024 Unsecured Notes.

•If an active trading market for the 2024 Unsecured Notes does not develop, holders may not be able to resell.

•If we default on our obligations to pay our other indebtedness, we may not be able to make payments on the 2024 Unsecured Notes.

•A downgrade, suspension or withdrawal of the credit rating assigned by a rating agency to us or the 2024 Unsecured Notes, if any, or change in the debt markets, could cause the liquidity or market value of the 2024 Unsecured Notes to decline significantly.

•An increase in market interest rates could result in a decrease in the market value of the 2024 Unsecured Notes.

•The optional redemption provision may materially adversely affect the return on the 2024 Unsecured Notes.

•We may not be able to repurchase the 2024 Unsecured Notes upon a Change of Control Repurchase Event.

•If we issue preferred stock, debt securities or convertible debt securities, the net asset value and market value of our common stock may become more volatile.

•We are a holding company and depend on payments from our subsidiaries in order to make payments on any debt securities that we may issue as well as to pay distributions on our common stock. Any debt securities that we issue will be structurally subordinated to the obligations of our subsidiaries.

•Holders of any preferred stock that we may issue will have the right to elect members of the board of directors and have class voting rights on certain matters.

•Our common stockholders’ interest in us may be diluted if they do not fully exercise subscription rights in any rights offering. In addition, if the subscription price is less than our net asset value per share, then common stockholders will experience an immediate dilution of the aggregate net asset value of your shares.

15

•Our stockholders will experience dilution in their ownership percentage if they do not participate in our dividend reinvestment plan.

•Our stockholders could receive shares of our common stock as dividends, which could result in adverse tax consequences to them.

•Sales of substantial amounts of our common stock in the public market could have an adverse effect on the market price of our common stock.

•The trading market or market value of our publicly issued debt securities may fluctuate.

•Terms relating to redemption may materially adversely affect the return on any debt securities that we may issue.

16

MANAGEMENT AGREEMENTS

GC Advisors is located at 200 Park Avenue, 25th Floor, New York, NY 10166. GC Advisors is registered as an investment adviser under the Advisers Act. The beneficial interests in GC Advisors are majority owned, indirectly, by two affiliated trusts. The trustees of those trusts are Stephen A. Kepniss and David L. Finegold. Subject to the overall supervision of our board of directors and in accordance with the 1940 Act, GC Advisors manages our day-to-day operations and provides investment advisory services to us. Under the terms of the Investment Advisory Agreement, GC Advisors:

•determines the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes;

•identifies, evaluates and negotiates the structure of the investments we make;

•executes, closes, services and monitors the investments we make;

•determines the securities and other assets that we purchase, retain or sell;

•performs due diligence on prospective portfolio companies; and

•provides us with such other investment advisory, research and related services as we, from time to time, reasonably require for the investment of our funds.

GC Advisors’ services under the Investment Advisory Agreement are not exclusive. Subject to the requirements of the 1940 Act, GC Advisors can enter into one or more sub-advisory agreements under which GC Advisors would obtain assistance in fulfilling its responsibilities under the Investment Advisory Agreement.

Management Fee

Pursuant to the Investment Advisory Agreement, we pay GC Advisors a fee for investment advisory and management services consisting of two components — a base management fee and an incentive fee. The cost of both the base management fee and the incentive fee is ultimately borne by our stockholders.

Under each of the Investment Advisory Agreement and the Prior Investment Advisory Agreement, the base management fee is calculated at an annual rate equal to 1.375% of our average adjusted gross assets at the end of the two most recently completed calendar quarters (excluding cash and cash equivalents but including assets purchased with borrowed funds and securitization-related assets and cash collateral on deposit with custodian). Additionally, GC Advisors is voluntarily excluding assets funded with secured borrowing proceeds from the management fee. For services rendered under the Investment Advisory Agreement, or the Prior Investment Advisory Agreement, the base management fee is payable quarterly in arrears. The base management fee is calculated based on the average value of our gross assets at the end of the two most recently completed calendar quarters, and appropriately adjusted for any share issuances or repurchases during a current calendar quarter. Base management fees for any partial month or quarter are appropriately pro-rated. For purposes of the Investment Advisory Agreement, cash equivalents means U.S. government securities and commercial paper instruments maturing within 270 days of purchase. To the extent that GC Advisors or any of its affiliates provides investment advisory, collateral management or other similar services to a subsidiary of ours, the base management fee shall be reduced by an amount equal to the product of (1) the total fees paid to GC Advisors by such subsidiary for such services and (2) the percentage of such subsidiary’s total equity, including membership interests and any class of notes not exclusively held by one or more third parties, that is owned, directly or indirectly, by us.

Incentive Fee

We pay GC Advisors an incentive fee. Incentive fees are calculated as described below and payable quarterly in arrears or at the end of each calendar year (or, upon termination of the Investment Advisory Agreement, as of the termination date).

Cap on Fees. We have structured the calculation of the incentive fee to include a fee limitation such that, under the Investment Advisory Agreement, an incentive fee for any quarter can only be paid to GC Advisors if, after such payment, the cumulative incentive fees paid to GC Advisors, calculated on a per share basis as described below, since April 13, 2010, the effective date of our election to become a business development company, would be less than or equal to 20.0% of our Cumulative Pre-Incentive Fee Net Income (as defined below).

17

We accomplish this limitation by subjecting each quarterly incentive fee payable under the Income and Capital Gains Incentive Fee Calculation (as defined below) to a cap, or the Incentive Fee Cap. The Incentive Fee Cap in any quarter is equal to the difference between (a) 20.0% of Cumulative Pre-Incentive Fee Net Income Per Share (as defined below) and (b) Cumulative Incentive Fees Paid Per Share (as defined below). To the extent the Incentive Fee Cap is zero or a negative value in any quarter, no incentive fee would be payable in that quarter. “Cumulative Pre-Incentive Fee Net Income Per Share” under the Investment Advisory Agreement is equal to the sum of Pre-Incentive Fee Net Income Per Share (as defined below) for each quarter since April 13, 2010. “Pre-Incentive Fee Net Income Per Share” for any quarter is equal to (a) the sum of (i) Pre-Incentive Fee Net Investment Income (as defined below) and (ii) Adjusted Capital Returns (as defined below) for the quarter divided by (b) the weighted average number of shares of our common stock outstanding during such quarter. “Adjusted Capital Returns” for any quarter shall be the sum of the realized aggregate capital gains, realized aggregate capital losses, aggregate unrealized capital depreciation and aggregate unrealized capital appreciation for such quarter; provided that the calculation of realized aggregate capital gains, realized aggregate capital losses, aggregate unrealized capital depreciation and aggregate unrealized capital appreciation shall not include any realized capital gains, realized capital losses or unrealized capital appreciation or depreciation resulting solely from the purchase accounting for any premium or discount paid for the acquisition of assets in a merger. “Cumulative Incentive Fees Paid Per Share” is equal to the sum of Incentive Fees Paid Per Share for each quarter (or portion thereof) since April 13, 2010. “Incentive Fees Paid Per Share” for any quarter is equal to the incentive fees accrued and/or payable by us for such period divided by the weighted average number of shares of our common stock outstanding during such period.

“Pre-Incentive Fee Net Investment Income” means interest income, dividend income and any other income (including any other fees such as commitment, origination, structuring, diligence and consulting fees or other fees that we receive from portfolio companies but excluding fees for providing managerial assistance) accrued during the period, minus operating expenses for the calendar quarter (including the base management fee, taxes, any expenses payable under the Investment Advisory Agreement and the Administration Agreement, any expenses of securitizations and any interest expense and dividends paid on any outstanding preferred stock, but excluding the applicable incentive fees). Pre-Incentive Fee Net Investment Income includes, in the case of investments with a deferred interest feature such as market discount, debt instruments with PIK interest, preferred stock with PIK dividends, and zero coupon securities, accrued income that we have not yet received in cash. GC Advisors does not return to us amounts paid to it on accrued income that we have not yet received in cash if such income is not ultimately received by us in cash. If we do not ultimately receive income, a loss would be recognized, reducing future fees. The Investment Advisory Agreement, as compared to the Prior Investment Advisory Agreement, excludes the impact of purchase accounting resulting from a merger, including the Merger, from the calculation of income subject to the income incentive fee payable and the calculation of the Incentive Fee Cap. As a result, under the Investment Advisory Agreement, Pre-Incentive Fee Net Investment Income does not include any realized capital gains, realized capital losses or unrealized capital appreciation or depreciation or any amortization or accretion of any purchase premium or purchase discount to interest income resulting solely from the purchase accounting for any premium or discount paid for the acquisition of assets in a merger, such as the premium to net asset value paid for the shares of GCIC common stock in the Merger.

The Investment Advisory Agreement, as compared to the Prior Investment Advisory Agreement, converts the cumulative incentive fee cap from an aggregate basis calculation to a per share calculation. Under the Prior Investment Advisory Agreement, the Incentive Fee would not be paid at any time if, after such payment, the cumulative Incentive Fees paid to date would be greater than 20.0% of our Cumulative Pre-Incentive Fee Net Income, which was defined under the Prior Investment Advisory Agreement to equal the sum of Pre-Incentive Fee Net Investment Income for each period since April 13, 2010. Under the Investment Advisory Agreement, the Incentive Fee will not be paid at any time if, after such payment, the Cumulative Incentive Fees Paid Per Share to date would be greater than 20.0% of Cumulative Pre-Incentive Fee Net Income Per Share.

If, for any relevant period, the Incentive Fee Cap calculation results in our paying less than the amount of the Incentive Fee calculated above, then the difference between (a) the Incentive Fees accrued and/or payable by us for such relevant period and (b) the Incentive Fee Cap multiplied by the weighted average number of shares of our common stock outstanding during such relevant period will not be paid by us, and will not be received by GC Advisors, as an incentive fee, either at the end of such relevant period or at the end of any future relevant period.

18

Income and Capital Gains Incentive Fee Calculation