Attached files

| file | filename |

|---|---|

| 8-K - 8-K - GUGGENHEIM CREDIT INCOME FUND 2019 | overview2019fund2020q3.htm |

| Exhibit 99.1 | ||||||||

GUGGENHEIM CREDIT INCOME FUND

THIRD QUARTER 2020 OVERVIEW

This overview contains details about the portfolio and operating results for the quarter ended September 30, 2020 of Guggenheim Credit Income Fund ("GCIF" or the "Master Fund") and its feeder funds, Guggenheim Credit Income Fund 2019 ("GCIF 2019") and Guggenheim Credit Income Fund 2016 T ("GCIF 2016T") (together, the "Feeder Funds"). This overview should be read in conjunction with the GCIF 2019 and GCIF 2016T Quarterly Reports on Form 10-Q, which each incorporate the GCIF Quarterly Report on Form 10-Q, as filed with the U.S. Securities and Exchange Commission (the "SEC") on November 16, 2020.

Nine Months Ended September 30, 2020 Highlights

•GCIF 2019 declared distributions of $1.25 per share and GCIF 2016T declared distributions of $0.44 per share. This represented an annualized distribution rate of 7.1% on GCIF 2019’s Net Asset Value and 7.2% on GCIF 2016T’s Net Asset Value as of December 31, 2019 (1).

•GCIF's yield on total debt investments was 7.6%, compared to 8.9% as of December 31, 2019 (2).

•GCIF's yield on total investments was 7.6%, compared to 8.9% as of December 31, 2019 (3).

•GCIF's total investments at fair value totaled $329 million, of which 97% was in senior debt investments. The portfolio consisted of 150 investments across 89 portfolio companies.

•GCIF invested $60 million, 100% of which was in senior debt, with sales and paydowns totaling $91 million.

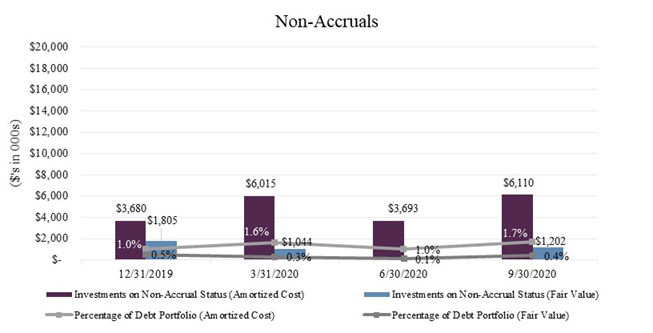

•GCIF had two debt investment on non-accrual status as of September 30, 2020. This represented 1.7% and 0.4% of the portfolio based on amortized cost and fair value, respectively.

•GCIF 2019’s net asset value per share as of September 30, 2020 was $21.81, compared to $23.37 as of December 31, 2019.

•GCIF 2016T’s net asset value per share as of September 30, 2020 was $7.68, compared to $8.24 as of December 31, 2019.

Please see below for feeder fund-specific highlights:

| Nine Months Ended September 30, 2020 | ||||||||||||||

| GCIF 2019 | GCIF 2016T | |||||||||||||

| Distributions declared per share | $1.25 | $0.44 | ||||||||||||

Total investment return (4) | (1.10) | % | (1.13) | % | ||||||||||

| Total assets ($ in thousands) | $40,449 | $130,304 | ||||||||||||

| Net asset value per share | $21.81 | $7.68 | ||||||||||||

________________________

(1)Future distributions are not guaranteed.

(2)Weighted average effective yield of the total debt investments is calculated as the effective yield of each investment and weighted by its amortized cost as compared to the aggregate amortized cost of all debt investments. Effective yield is the return earned on an investment net of any discount, premium, or issuance costs. Effective yield on total debt investments is calculated before considering the impact of leverage or any operating expenses.

(3)The total investment portfolio yield is calculated before considering the impact of leverage or any operating expenses, and includes all income generating investments, non-income generating investments and investments on non-accrual status.

(4)Total investment return is a measure of the change in total value for shareholders who held the Feeder Funds' common shares at the beginning and end of the period, including distributions declared during the period. Total investment return is based on (i) net asset value per share on the first day of the period, (ii) the net asset value per share on the last day of the period, plus any shares issued in connection with the reinvestment of monthly distributions, and (iii) distributions payable relating to the ownership of shares, if any, on the last day of the period. The total investment return calculation assumes that distributions are reinvested in accordance with the Feeder Funds' distribution reinvestment plan. Since there is no public market for the Feeder Funds' shares, terminal market value per share is assumed to be equal to net asset value per share on the last day of the period presented. Investment performance is presented without regard to sales load that may be incurred by shareholders in the purchase of the Feeder Funds' common shares. Total investment return is not annualized. The Feeder Funds' performance changes over time and currently may be different than that shown above. Past performance is no guarantee of future results.

1

Business Environment

Following one of the most volatile and worst performing quarters in history in Q1 and the third strongest quarter on record in Q2, we saw Q3 begin to normalize as the market absorbed the implications of COVID-19 and the subsequent Government intervention. The continued search for yield in Q3 helped the loan market to grind higher, with the Credit Suisse Leverage Loan Index returning 4.1% during the quarter. This brought the market back into slightly positive territory for the year which is notable considering at one point bank loans were down nearly 20%.

We cannot predict the full impact of the pandemic, including its duration in the United States and worldwide, and the magnitude of the economic impact of the outbreak. As such, we are unable to predict the duration of any business disruptions, the extent to which COVID-19 will negatively affect our portfolio companies’ operating results or the impact that such disruptions may have on our results of operations and financial condition. We are taking steps in actively overseeing all our individual portfolio companies. These measures include, among other things, enhanced monitoring/credit analysis of our portfolio, assessing each portfolio company’s operational and liquidity exposure and outlook, and frequent communication with our portfolio company management teams, industry consultants, and other lenders to understand the expected financial performance impact of the pandemic.

While we remain constructive on credit and will be opportunistic during times of dislocations in the syndicated and direct markets, we are monitoring the effects of the COVID-19 pandemic closely and are adjusting our underwriting criteria to focus on companies whose revenue streams are resilient in the face of rapidly shifting consumer and business demand trends.

Investment Activity, Investment Performance, and Portfolio Update

During the three months ended September 30, 2020, 83% of the Company's investments were sourced through direct origination channels, and 17% were sourced through the syndicated channels.

The following table presents our assets as of September 30, 2020 and our investment activity during the three months ended September 30, 2020 (dollars in thousands):

| As of | |||||

| September 30, 2020 | |||||

| Total assets | $ | 349,802 | |||

| Yield on total debt investments | 7.6 | % | |||

| Yield on total investments | 7.6 | % | |||

Leverage ratio (borrowings/adjusted total assets) (5) | 43 | % | |||

| Three Months Ended | |||||

| September 30, 2020 | |||||

| Investment activity segmented by access channel: | |||||

| Direct origination | $ | 2,051 | |||

| Syndicated | 430 | ||||

| Total investment commitments entered during the period | 2,481 | ||||

| Investments sold or repaid | (9,716) | ||||

| Net investment activity | $ | (7,235) | |||

| Portfolio companies at beginning of period | 89 | ||||

| Number of added portfolio companies | 2 | ||||

| Number of exited portfolio companies | (2) | ||||

| Portfolio companies at period end | 89 | ||||

(5)We expect that the market and business disruption created by the COVID-19 pandemic will impact certain aspects of our liquidity, and we are therefore continuously monitoring our operating results, liquidity and anticipated capital requirements. As of September 30, 2020, we were in compliance with our asset coverage requirements under the 1940 Act, as well as, all financial covenants within its credit facilities as of September 30, 2020. Any breach of these requirements may adversely affect our access to sufficient debt and equity capital.

2

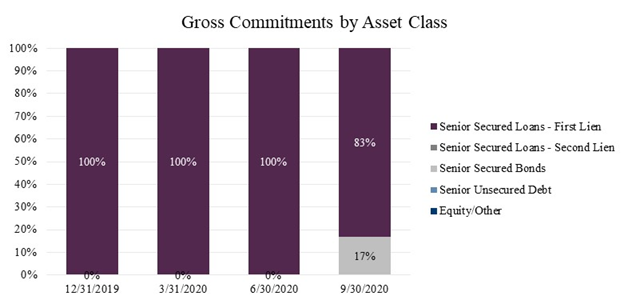

During the three months ended September 30, 2020, 83% of commitments were in senior secured first lien investments. The following chart presents the investment commitments by asset class during each of the last four quarters:

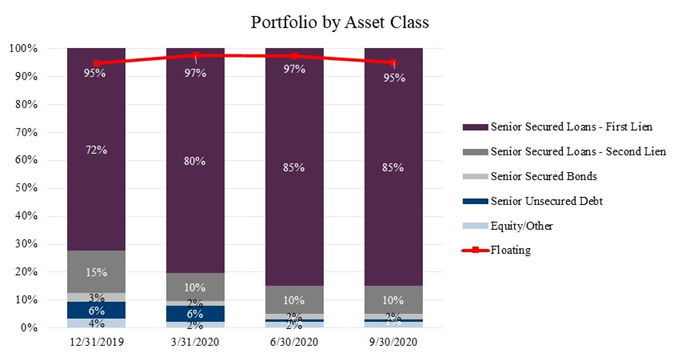

As of September 30, 2020, the investment portfolio consisted of $329 million at fair value and remained predominately invested in senior debt which represented 97% of the total portfolio at fair value. We believe senior debt investments provide for downside risk mitigation which is particularly important given today's credit environment.

The following chart presents the investment portfolio based on fair value by asset class at the end of each of the last four quarters:

3

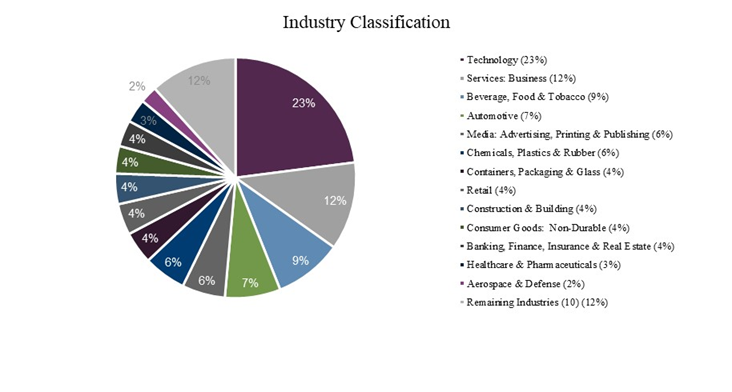

As of September 30, 2020, there were 89 portfolio companies in which GCIF held 150 investments. The weighted average portfolio company age, based on fair value, was 59 years as of September 30, 2020. Furthermore, and aligned with our strategy of seeking to mitigate industry-specific risk, the companies held in GCIF's portfolio were diversified across 22 industries.

The following chart presents the investment portfolio based on fair value by industry classification (based on Moody's standard industry classifications) as of September 30, 2020:

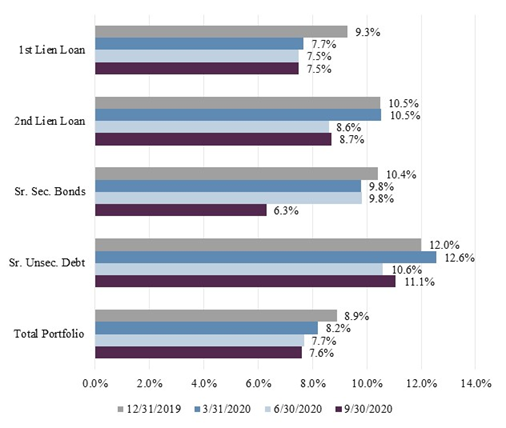

The yield on total debt investments was 7.6% as of September 30, 2020, compared to 8.9% as of December 31, 2019.

4

The following chart presents the weighted average effective yields by investment type at the end of each of the last four quarters:

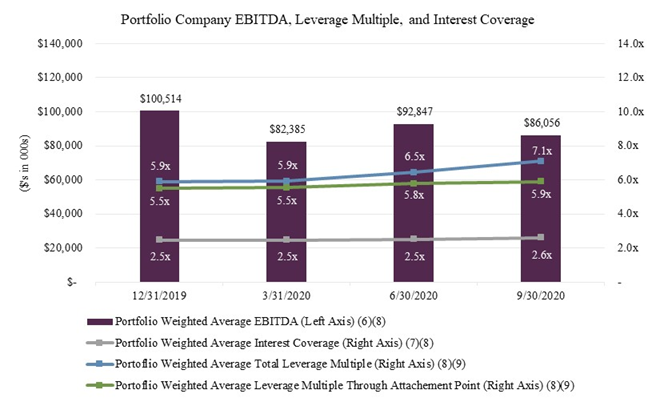

The following chart presents the weighted average EBITDA, weighted average total leverage multiple, and weighted average interest rate coverage of GCIF's portfolio companies for each of the last four quarters. We would note that the increase in Total Leverage Multiple and Leverage Through Attachment Point were both impacted this year by a material number of portfolio companies who partially or fully drew their revolvers to bolster their cash balances in response to concerns about COVID-19. The revolver draws often resulted in companies carrying higher debt balances at the end of the quarter, but our leverage calculations do not reflect the benefit of the additional cash on hand. Net leverage ratios (which reduce debt by the amount of cash on hand) did not increase to the same extent as the Total Leverage and Leverage Through Position calculations.

5

________________________

(6)Based on trailing twelve months EBITDA as most recently reported by portfolio companies. Weighted average portfolio company EBITDA is calculated using weights based on fair value. The inputs and computations of EBITDA are not consistent across all portfolio companies. EBITDA is a non-GAAP financial measure. For a particular portfolio company, EBITDA is generally defined as net income before net interest expense, income tax expense, depreciation and amortization. EBITDA amounts are estimated from the most recent portfolio company's financial statements, have not been independently verified by GCIF or its Advisor, may reflect a normalized or adjusted amounts, typically exclude expenses deemed unusual or non-recurring, and typically include add backs for items deemed appropriate to present normalized earnings. Accordingly, neither GCIF nor its Advisor makes any representation or warranty in respect of this information.

(7)Weighted average interest coverage represents the portfolio company’s EBITDA as a multiple of interest expense. Portfolio company credit statistics are derived from the most recently available portfolio company financial statements, have not been independently verified by GCIF or its Advisors, and may reflect a normalized or adjusted amount. Accordingly, neither GCIF nor its Advisors makes any representation or warranty in respect of this information.

(8)Portfolio weighted average EBITDA, weighted average total leverage multiple, weighted average leverage multiple through tranche, and weighted average interest coverage ratio data includes information solely in respect of portfolio companies in which GCIF has a debt investment.

(9)Weighted average total leverage multiple represents the portfolio company’s total debt as a multiple of EBITDA. Weighted average leverage multiple through attachment point represents the portfolio company's debt through GCIF's position in the capital structure as a multiple of EBITDA. Portfolio company credit statistics are derived from the most recently available portfolio company financial statements, have not been independently verified by GCIF or its Advisors, and may reflect a normalized or adjusted amount. Accordingly, neither GCIF nor its Advisors makes any representation or warranty in respect of this information.

6

As of September 30, 2020, there were two debt investments on non-accrual status.

The following chart presents debt investments on non-accrual status based on amortized cost and fair value at the end of each of the last four quarters:

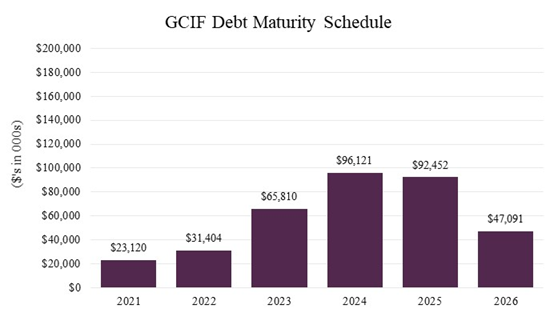

The following chart presents the maturity schedule of GCIF's debt investments, excluding unfunded commitments, based on their principal amount as of September 30, 2020.

7

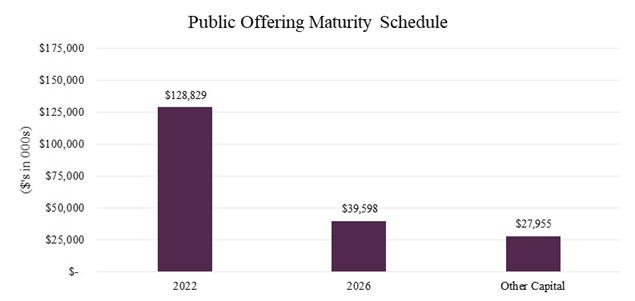

GCIF's publicly offered feeder funds, GCIF 2016 T and GCIF 2019, which have committed to seek liquidity events on or before December 31, 2022 and December 31, 2026, respectively, collectively represented 86% of GCIF's total ownership as of September 30, 2020. The following chart shows the liquidity schedule (10) of GCIF's publicly offered feeder funds based on their respective share in the net assets of GCIF as of September 30, 2020.

(10)A liquidity event is not guaranteed.

8

About Guggenheim Credit Income Fund

GCIF is a non-traded BDC that seeks to invest primarily in large, privately-negotiated loans to private middle market U.S. companies, with a focus on senior secured debt investments. GCIF is advised by Guggenheim Partners Investment Management, LLC ("Guggenheim Investments"), an affiliate of Guggenheim Partners, LLC ("Guggenheim Partners"). For more information, please visit www.GuggenheimCIF.com

GCIF 2016T is closed to new investors.

About Guggenheim Partners, LLC

Guggenheim Investments represents the investment management businesses of Guggenheim Partners and includes Guggenheim, an SEC-registered investment adviser. Guggenheim Partners is a privately-held, global financial services firm with over 2,400 employees and more than $295 billion in assets under management* as of September 30, 2020. It produces customized solutions for its clients, which include institutions, governments and agencies, corporations, insurance companies, investment advisors, family offices, and individual investors.

Guggenheim Investments manages more than $233 billion in assets** across fixed income, equity, and alternatives as of September 30, 2020. Its 300+ investment professionals perform research to understand market trends and identify undervalued opportunities in areas that are often complex and under-followed. This approach to investment management has enabled Guggenheim to deliver long-term results to its clients.

Within Guggenheim Investments is the Guggenheim Corporate Credit Team, which is responsible for all corporate credit strategies and asset management of $110 billion. A unified credit platform is utilized for all strategies and is organized by industry as opposed to asset class, which increases its ability to uncover relative value opportunities and to identify and source opportunities. The scale of the platform, combined with the expertise across a wide range of industries and in-house legal resources, allows Guggenheim to be a solution provider to the market and maintain an active pipeline of investment opportunities.

*Assets under management are as of September 30, 2020 and include consulting services for clients whose assets are valued at approximately $69bn.

**Assets under management as of September 30, 2020 and include leverage of $14bn. Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

Cautionary Statement Concerning Forward-Looking Statements

This document contains forward-looking statements within the meaning of the Federal securities laws. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. GCIF, GCIF 2019, and GCIF 2016T undertake no obligation to update any forward-looking statements contained herein to conform the statements to actual results or changes in their expectations. A number of factors may cause GCIF’s, GCIF 2019's and GCIF 2016T's actual results, performance or achievement to differ materially from those anticipated. For further information on factors that could impact GCIF, GCIF 2019, and GCIF 2016T performance, please review GCIF’s, GCIF 2019's, and GCIF 2016T's respective filings at the SEC website at www.sec.gov.

9