Attached files

| file | filename |

|---|---|

| EX-10.4 - INTELLECTUAL PROPERTY LICENSE AGREEMENT - Vivakor, Inc. | vivakor_ex1004.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Vivakor, Inc. | vivakor_ex2301.htm |

| EX-21.1 - SUBSIDIARIES - Vivakor, Inc. | vivakor_ex2101.htm |

| EX-10.7 - EXECUTIVE EMPLOYMENT AGREEMENT - Vivakor, Inc. | vivakor_ex1007.htm |

| EX-10.6 - EXECUTIVE EMPLOYMENT AGREEMENT - Vivakor, Inc. | vivakor_ex1006.htm |

| EX-10.5 - PATENT AND INTELLECTUAL PROPERTY LICENSE AGREEMENT - Vivakor, Inc. | vivakor_ex1005.htm |

| EX-10.3 - LETTER OF CLARIFICATION - Vivakor, Inc. | vivakor_ex1003.htm |

| EX-10.2 - PROJECT CHARTER - Vivakor, Inc. | vivakor_ex1002.htm |

| EX-10.1 - AMENDED CONTRIBUTION AGREEMENT - Vivakor, Inc. | vivakor_ex1001.htm |

| EX-3.3 - AMENDMENTS TO THE ARTICLES OF INCORPORATION - Vivakor, Inc. | vivakor_ex0303.htm |

| EX-3.2 - AMENDED AND RESTATED BYLAWS - Vivakor, Inc. | vivakor_ex0302.htm |

| EX-3.1 - AMENDED AND RESTATED ARTICLES OF INCORPORATION - Vivakor, Inc. | vivakor_ex0301.htm |

As filed with the U.S. Securities and Exchange Commission on November 10, 2020

Registration No.

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_________________

VIVAKOR, INC.

(Exact name of registrant as specified in charter)

| Nevada | 8731 | 26-2178141 | ||

| (State or other jurisdiction of incorporation) |

(Primary Standard Classification Code Number) |

(IRS Employer I.D. Number) |

433 Lawndale Drive

South Salt Lake City, UT 84115

(949) 281-2606

(Address and telephone number of principal executive offices)

_________________

(Address of principal place of business or intended principal place of business)

_________________

Matthew Nicosia

Chief Executive Officer

433 Lawndale Drive

South Salt Lake City, UT 84115

(949) 281-2606

(Name, address, including zip code, and telephone number including area code, of agent for service)

_________________

With copies to:

|

Joseph M. Lucosky, Esq. Scott E. Linsky, Esq. |

_________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large-Accelerated Filer | ☐ | Accelerated Filer | ☐ | |||||

| Non-Accelerated Filer | ☒ | Smaller Reporting Company | ☒ | |||||

| Emerging Growth Company | ☒ |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee | ||||||

| Common Stock, par value $0.001(3) | $ | 13,800,000 | $ | 1,505.58 | ||||

| Representative’s Warrants (4) | – | – | ||||||

| Shares of common stock underlying Representative’s Warrants (5) | $ | 862,500 | $ | 94.10 | ||||

| Total | $ | 14,662,500 | $ | 1,599.68 | ||||

| ____________ |

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended (the “Securities Act”). |

| (2) | Includes initial public offering price of shares that the underwriters have the option to purchase to cover over-allotments, if any. |

| (3) | Pursuant to Rule 416 of the Securities Act, the shares of common stock registered hereby also includes an indeterminable number of additional shares of common stock as may from time to time become issuable by reason of stock splits, stock dividends, recapitalizations or other similar transactions. |

| (4) | No fee required pursuant to Rule 457(g) under the Securities Act. |

| (5) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(g) under the Securities Act. The Representative’s Warrants are exercisable for a number of shares equal to 5% of the shares of common stock offered hereby at a per share exercise price equal to 125% of the public offering price per share. As estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(g) under the Securities Act, the proposed maximum aggregate offering price of the Representative’s Warrants is $750,000, which is equal to 125% of $600,000 (5% of $12,000,000). |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information contained in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED NOVEMBER 10, 2020 |

Shares

Common Stock

![]()

Vivakor, Inc.

This is a firm commitment public offering of shares of common stock of Vivakor, Inc.

We intend to apply to list our common stock on under the symbol “VIVK”. If our listing application is not approved, we will not proceed with the offering. Our common stock is currently quoted on the OTCPink Marketplace operated by OTC Markets Group Inc. (the “OTCPink”) under the trading symbol “VIVK”. On November 6, 2020, the last reported sale price for our common stock on the OTCPink was $0.51.

We expect to effect a -for- reverse stock split of our outstanding common stock prior to the completion of this offering. We have assumed a public offering price of $ per share, the last reported sale price of our common stock on the OTCPink on , 2020 (after giving effect to the reverse stock split). The actual public offering price per share will be determined through negotiations between us and the underwriter at the time of pricing and may be at a discount to the current market price. Therefore, the assumed public offering price used throughout this prospectus may not be indicative of the final offering price.

We are an “emerging growth company” under the federal securities laws and have elected to comply with certain reduced public company reporting requirements.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 10. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

| Initial public offering price | $ | $ | ||||

| Underwriting discounts and commissions(1) | $ | $ | ||||

| Proceeds to us, before expenses | $ | $ | ||||

| (1) | Underwriting discounts and commissions do not include a non-accountable expense allowance equal to 1.0% of the initial public offering price payable to the underwriters. We refer you to “Underwriting” beginning on page 57 for additional information regarding underwriters’ compensation. |

We have granted a 45-day option to the representative of the underwriters to purchase up to additional shares of common stock solely to cover over-allotments, if any.

The underwriters expect to deliver the shares to purchasers on or about , 2020.

The date of this prospectus is , 2020

You should rely only on information contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. We have not, and the underwriters have not, authorized anyone to provide you with additional information or information different from that contained in this prospectus or in any free writing prospectus. Neither the delivery of this prospectus nor the sale of our securities means that the information contained in this prospectus or any free writing prospectus is correct after the date of this prospectus or such free writing prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy our securities in any circumstances under which the offer or solicitation is unlawful or in any state or other jurisdiction where the offer is not permitted.

No person is authorized in connection with this prospectus to give any information or to make any representations about us, the securities offered hereby or any matter discussed in this prospectus, other than the information and representations contained in this prospectus. If any other information or representation is given or made, such information or representation may not be relied upon as having been authorized by us.

Neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourself about, and to observe any restrictions relating to, this offering and the distribution of this prospectus.

We also use certain trademarks, trade names, and logos that have not been registered. We claim common law rights to these unregistered trademarks, trade names and logos.

| i |

This summary highlights selected information appearing elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information you should consider before investing in our securities. You should read this prospectus carefully, especially the risks and other information set forth under the heading “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus before making an investment decision. Our fiscal year end is December 31 and our fiscal years ended December 31, 2019 and December 31, 2018 are sometimes referred to herein as fiscal years 2019 and 2018, respectively. Some of the statements made in this prospectus discuss future events and developments, including our future strategy and our ability to generate revenue, income and cash flow. These forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those contemplated in these forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements”. Unless otherwise indicated or the context requires otherwise, the words “we,” “us,” “our,” the “Company,” or “our Company,” and “Vivakor” refer to Vivakor, Inc., a Nevada corporation, and its wholly owned subsidiaries.

Overview

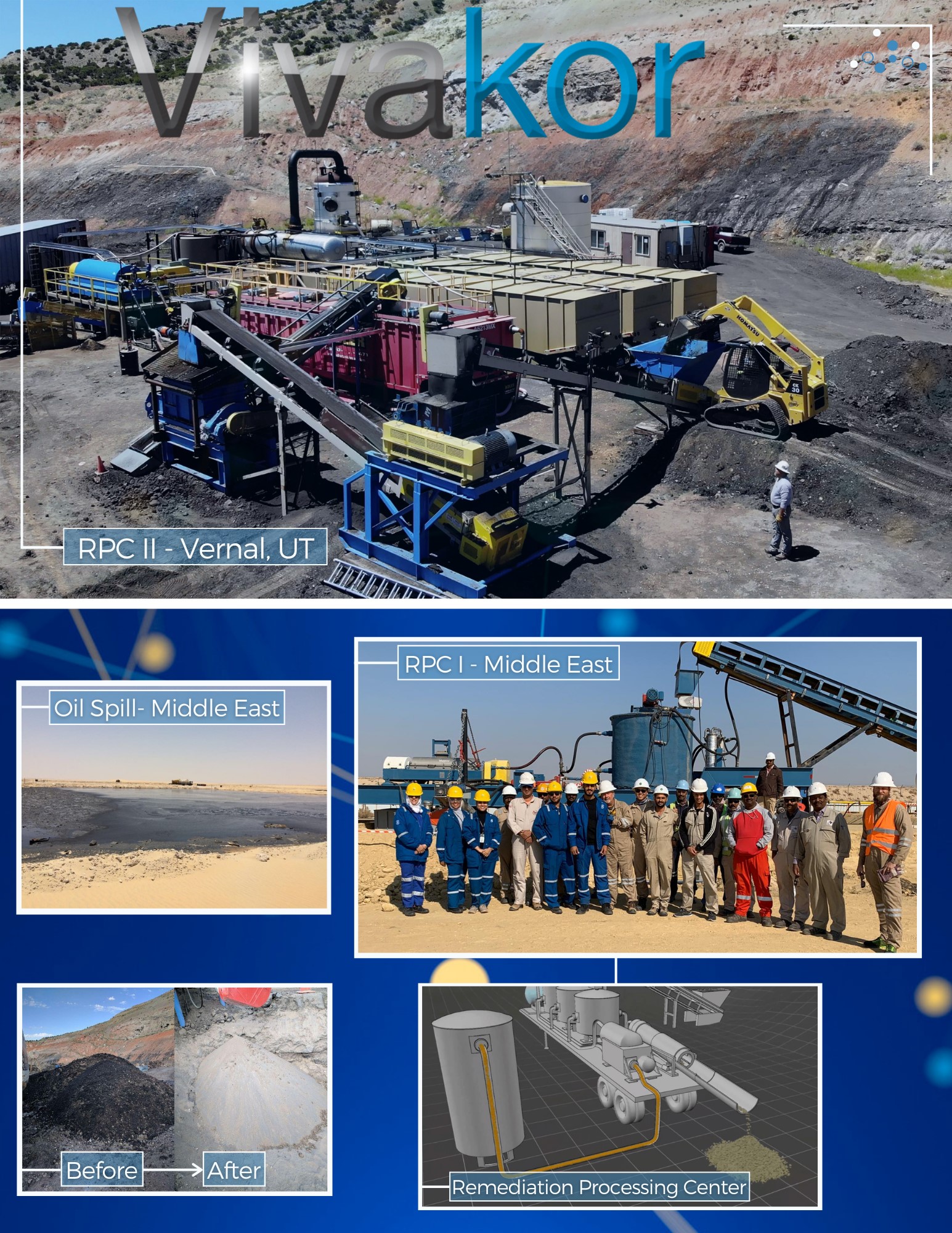

Vivakor, Inc. is a socially responsible operator, acquirer and developer of clean energy technologies and environmental solutions, primarily focused on soil remediation. We specialize in the remediation of soil and the extraction of hydrocarbons, such as oil, from properties contaminated by or laden with heavy crude oil and other hydrocarbon-based substances. Our process allows us to successfully recover hydrocarbons from the soil, which we believe could then be used to produce asphaltic cement and/or other petroleum-based products. In 2015, we acquired and improved technology aimed at remediating contaminated soil and recovering usable hydrocarbons, which we refer to as Remediation Processing Centers (“RPCs”). We presently have three patent applications pending related to our RPCs and two issued patents related to our other remediation technologies. Our RPCs each have the potential to clean a minimum of 20 tons of contaminated material per hour, depending on the oil contamination percentage in the processed material. Each RPC has the capacity to extract on a 24-hour operation 500 tons or more of contaminated material per day. The amount of extracted hydrocarbon recovered depends on the extent to which the material is contaminated. For example, we estimate that for every 500 tons of contaminated material recovered per day that contains at least 10% oil, we will recover approximately 250 barrels of extracted hydrocarbons.

We have designed our RPCs to provide an environmentally friendly solution to the remediation of hydrocarbon-contaminated soil, as they do not utilize water. Our RPCs operate by loading contaminated soil onto a feeder and conveyor system that effectively delivers the material into a fully contained, closed-loop system. Physical separation of the hydrocarbons from the contaminated soil does not utilize water or steam and is instead accomplished using a proprietary extraction fluid to dissolve the hydrocarbon components.

The entire extraction process is completed in a series of sealed chambers. The reclaimed extraction fluid is then recycled back into the process, which ensures that no toxic chemicals are released into the soil or the environment. Upon completion of our remediation and separation process, the extracted hydrocarbons are placed into holding tanks to be picked up by our customers, while clean soil is returned to the environment.

We believe our RPCs are significantly more advanced than other oil remediation technologies or offerings presently available on the market. Our RPCs have successfully cleaned contaminated soil containing greater than 7% hydrocarbon content, while, to our knowledge, our competitors are limited to projects containing less than 5% hydrocarbon contamination. We believe our ability to clean soil with more highly concentrated hydrocarbon contamination is a distinctive advantage that will allow us to operate on a global basis in any location that has suffered from oil spills or naturally occurring oil sands deposits. While our primary focus and mandate will be on the manufacture and deployment of our RPCs, we intend to continue to develop, acquire or license additional clean energy technologies and environmental solutions that will directly enhance and expand our current technologies and service offerings.

Our current focus is on the clean-up of greater than 7% hydrocarbon contaminated soil located in Kuwait as a result of the Iraqi invasion and naturally occurring oil sands deposits in Utah. We have deployed two RPC units to date, including one unit to Kuwait (for which operations have been temporarily suspended due to COVID-19) and another to Vernal, Utah (which is presently operating). We expect to deploy two additional RPCs to Vernal, Utah with the proceeds from this offering and believe that there may be an opportunity to deploy additional RPCs in Utah, as well as to Kuwait and the Middle East.

| 1 |

In April 2020, we entered into a project charter agreement with solvAQUA Inc. (“solvAQUA”), a Canadian-based clean water technology company, pursuant to which we may purchase certain wastewater removal equipment from solvAQUA. The solvAQUA Wastewater Management System (“WMS”) is a compact solution that continually processes and separates large volumes of wastewater (4,000+ m3/day for each WMS) with an ability to scale to remove any volume of oil, grease and suspended solids from wastewater, in most cases removing 99.99% of waste. The processed water stream can in some cases be discharged or reused without further treatment. We have placed our first order with solvAQUA for WMS equipment and anticipate receipt and installation of the equipment prior to December 31, 2020, with operations to commence shortly thereafter. On July 15, 2020, solvAQUA granted us an exclusive license to either incorporate solvAQUA’s technology platform into our RPCs or to use it independently. This will allow us to service remediation projects that have a combination of wet and dry opportunities. The exclusive license has an initial term of one year, which may be extended to five years upon our successful installation and deployment of the first two WMSs.

Our proprietary metallic separation technology uses a thermal vapor process to extract and process micro particles of precious metals and rare earth minerals, including gold, silver, platinum, palladium and rhodium from soils. After we complete our soil remediation services, we evaluate the post-remediated soil and, if we find that the soil contains more than 1% concentration of these metals, we process it through this technology to extract and concentrate these micro particles of precious metals and rare earth minerals into a concentrated, unrefined flake form.

We have also acquired and/or licensed two separate technologies described below that will enable us to upgrade the hydrocarbons recovered from our remediation process. These processes have been proven in laboratory tests, but we have not yet performed this upgrading in a commercial setting.

We have been granted a worldwide, exclusive, non-transferable license to the intellectual property embodied in cavitation technology developed by B Green, Inc. (“B Green”) to develop, manufacture, have manufactured, use market, import, have imported, offer for sale and sell cavitation devices built from the licensed intellectual property. Third party, independent testing conducted by the University of Utah has shown that this proprietary technology increases the API gravity of hydrocarbons by elongating the hydrocarbon chains without cutting or cracking these chains. API gravity is the measure of how heavy or light petroleum liquid is compared to water and is used in the industry as the standard measure for viscosity. The API of the recovered crude is increased, allowing such crude to have additional uses and usually at higher unit prices.

We have also been granted an exclusive right to use the nano-sponge technology developed by CSS Nanotech, which essentially serves as a micro-upgrader, transforming hydrocarbon product into a more useful product, such as petroleum or gasoline, as an addition to our hydrocarbon extraction technology. The inventor of this technology subsequently joined us as our Chief Scientific Officer. This patented technology allows for hydrocarbon material to be absorbed by a specialized sponge. Low energy microwaves are then introduced into the process and the sponge, which is made of a highly thermally conductive material, absorbs this energy causing an instant thermal effect, which essentially refines the crude by cutting or cracking the carbon chains. We intend to add this system to our process of upgrading the heavy crude recovered by our RPCs.

Revenue

Our RPC situated in Vernal, Utah has the capacity to process up to 500 tons or more of naturally occurring oil sands deposits per day. We estimate that if the extracted material is composed of at least 10% oil, we will recover approximately 250 barrels of extracted hydrocarbons each day, which could then be sold for energy or converted to asphaltic cement and sold for use in roads at higher prices.

In Kuwait, where we do not have ownership of the recovered oil, we generate revenues by charging per cubic meter of soil remediated. For our current project we will generate revenues of $72 per cubic meter of contaminated material processed.

We market and sell the precious metals we extract from our remediated and waste soils. As we continue our efforts, we anticipate increased opportunities to monetize our precious metals end product. We believe that we may be able to generate proceeds of approximately $6 million from the sale of precious metals, based on indications from potential buyers.

Market Opportunity

We believe that the market for remediating oil from both soil and water is significant. According to Grandview Research, the market for environmental clean-up of oil spills will reach $177 billion by 2025. We believe that a large portion of that market will originate from contamination of more than 7% hydrocarbon content and that our technology is currently the only one that can economically remediate these environmental disasters, while allowing for the capture and reuse of the crude.

In addition, we believe that the heavy crude that we have been recovering in Utah is ideal for producing asphaltic cement. The demand for asphaltic cement in the United States is presently estimated to be $116 billion this year according to Global Market Insights. We have provided our material to asphalt companies for testing to determine what modifications, if any, would be needed to be meet their specifications. Provided we are able to produce asphaltic cement that meets our customers’ specifications, we believe that we will be able to offer our product at very competitive prices and in an environmentally friendly manner.

Competitive Strengths and Growth Strategy

We are focused on the remediation of contaminated soil and water resulting from either man-made spills or naturally occurring deposits of oil. Our primary focus has been the remediation of oil spills resulting from the Iraqi invasion of Kuwait and naturally occurring oil sands deposits in the Uinta basin located in Eastern Utah. We plan to expand into other markets, both in Utah and globally, where we believe our technology and services will provide a distinct competitive advantage over our competition.

| 2 |

Competitive Strengths

We believe the following strengths provide us with a distinct competitive advantage and will enable us to effectively compete on a global basis:

| · | Proprietary patent-pending technology; |

| · | Strong relationships with customers and regulatory agencies; and |

| · | Experienced and highly-skilled management, Board of Directors and Advisory Board. |

Proprietary Patent Pending Technology

We presently have three patent applications pending related to our RPCs and two issued patents related to our other remediation technologies.

We believe, based on direct and ongoing conversations with our customers and third-party independent test results, that our technology is the only commercially available technology that can not only clean soil that contains greater than 7% hydrocarbon, but also preserve the hydrocarbons extracted from such soil for future use. We believe that this provides us with a true competitive advantage.

We believe our technology and service offerings will position us well to conduct our business in any geographical region in which soil or water has been contaminated by hydrocarbons.

Strong Relationships with Customers and Regulatory Agencies

We have developed close relationships with customers and government agencies, including the Utah School and Institutional Trust Lands Administration (“SITLA”) and the Kuwait Oil Company (“KOC”). We anticipate receiving access to additional oil sands deposits located in Utah from SITLA, based on our existing relationship with SITLA and our conversations with them. We also anticipate receiving additional contracts from KOC to remediate contaminated properties in Kuwait, based on our existing relationship with KOC and conversations with them.

Experienced and Highly Skilled Management, Board of Directors and Advisory Board

Our management team has started and successfully grown numerous technology-based companies and has utilized this experience to develop a strategic vision for the Company. The implementation of this plan has resulted in the acquisition and in-house development of numerous technologies, which are currently in operation. We have demonstrated the effectiveness of our technologies in both Vernal, Utah and Kuwait, accomplishing the clean-up of contaminated areas while also recovering precious metals through our metallic separation technology.

Our Board of Directors is comprised of accomplished professionals who bring decades of experience to the Company. Our Board of Directors includes a director who has served as a member of the Executive Committee of one of the largest global accounting firms and has served on the Board of Directors of two multi-billion dollar publicly traded companies, a former director of technology investment banking at Goldman Sachs, a successful investor and entrepreneur who has founded and provided initial financing for numerous life science companies, several of which have grown to become multi-billion dollar publicly traded companies, and the mayor of a city in Utah.

| 3 |

In addition, we have an Advisory Board comprised of former senior members of oil and gas companies, both in the United States and in the Middle East. Our Advisory Board is led by one member who is an accomplished business professional and a member of a royal family based in the Middle East and another member who is an experienced health and safety expert operating in the oil and gas industries.

We rely on our Board of Directors and Advisory Board to provide it both high level advice and guidance along with using their contacts to help open various markets. We believe the combination of our management team, Board of Directors and Advisory Board provides us with a significant competitive advantage over our competitors due to their breadth of experiences and relationships.

Growth Strategies

We will strive to grow our business by pursuing the following strategies:

| · | Expansion of our oil recovery projects in Utah; |

| · | Expansion of our remediation projects in Kuwait; |

| · | Expansion into new and complementary markets; |

| · | Increase of revenue via new service and product offerings; |

| · | Strategic acquisitions and licenses targeting complementary technologies; and |

| · | Redeployment of our metallic separation technologies. |

Expansion of our Oil Recovery Projects in Utah

The State of Utah has, according to the U.S. Geological Survey, approximately 14 billion barrels of measured oil in place with an additional estimated 23 to 28 billion barrels of oil contained in contaminated oil sands that are deposited near the ground surface. The majority of these oil sands deposits are located on land owned by SITLA. While our current project in Vernal, Utah is not located on SITLA land, SITLA has expressed an interest in providing us leased access to these lands in exchange for a royalty to be paid by us in an amount equal to 8% of all revenue generated from any hydrocarbon-based products produced by us from hydrocarbons extracted from these lands. All royalty payments to SITLA would result in direct funding to the State’s school system. We believe, based on the number of estimated barrels of oil contained in oil sands deposits located on SITLA property, that there may be an opportunity to deploy as many as 100 RPCs to properties containing oil sands deposits owned by the State of Utah. We will seek to acquire additional properties and mineral rights in the vicinity of Vernal, Utah from individual land owners and the State of Utah with a goal of increasing our hydrocarbon holdings to as much as one billion barrels of contingent resources containing a minimum of 10% hydrocarbon saturation.

Expansion of our Remediation Projects in Kuwait

Our RPC technology was successfully used in our initial project for KOC in Kuwait, where we removed hydrocarbons from soil with more than 7% contamination and, following the process, the hydrocarbon contamination level of the soil was reduced to less than 0.5%, which was lower than the level needed to meet the project specifications. There is still approximately 26 million cubic meters of soil contaminated by oil as a result of the Iraqi invasion of Kuwait. We intend to seek additional contracts directly from KOC to deploy our RPCs for the remediation of this contaminated soil. Under our current contract, we will charge $72 per cubic meter of soil remediated. We are currently working with KOC and other government-controlled entities to expand our remediation projects in Kuwait. We are in active negotiations to provide the technology and operations as a subcontractor to large, multinational remediation companies within the region where our technology could be used on all of the sands with contamination levels greater than 7%. Other technologies may also be used for the less contaminated soils.

Expansion into New and Complementary Markets

We intend to explore expansion opportunities on a global basis, including in places with extreme contamination such as the Ogoni Lands region of Nigeria, oil spill lakes located in Saudi Arabia and Turkmenistan, and naturally occurring oil sands deposits in Kazakhstan, where we believe our technology and service offerings may provide a distinct competitive advantage. We are currently in discussions with several groups for deploying our RPCs for remediation projects (primarily for oil spills, tank bottom sludge and drill cuttings) in Saudi Arabia, Qatar and Texas. Saudi Arabia has the objective to create a circular carbon economy that will ultimately have zero wasted hydrocarbons. Our technology is able to process tank bottom sludge, drill cuttings, and soils from hydrocarbon spills, returning the sand to less than 0.5% contamination while reclaiming the oil for waste energy use.

| 4 |

Increase of Revenue via New Service and Product Offerings.

To date, we have focused on the remediation of soil contaminated by oil. We are in the process of expanding our services to include the remediation of water and the recovery of hydrocarbons from water through our exclusive license with solvAQUA. We also intend to target other hydrocarbon remediation businesses that focus on, among other things, the cleaning of tank bottom sludge and the cleaning of the water used from drilling oil wells. Oil producers generally pay to dispose of sludge at the bottom of storage tanks and contaminated water produced from the drilling of oil wells. We believe that our technologies could be used to clean these contaminated products, while simultaneously recovering the heavy crude. We believe we will be able to offer these services at a cost that is very competitive with current methods and that our ability to recover the heavy crude for resale will give us a competitive advantage. The patent pending RPC technology, in conjunction with the enzymatic water remediation technology that we have licensed from solvAQUA, have the potential to eradicate all oil evaporation ponds and landfills in the United States presently utilized for disposal of tank bottom sludge and drill cutting waste. We are currently in early stage discussions relating to some of these remediation projects.

Strategic Acquisitions and Licenses Targeting Complementary Technologies

We intend to seek out opportunities to acquire or license only specific technologies that are either complementary to our existing product offerings or that will allow us to expand into the environmental infrastructure markets. We are currently negotiating a license for smart sensor technologies for autonomous vehicles that we believe could be embedded directly into the asphaltic cement we intend to produce from the hydrocarbons we extract, providing the basis for smart roads and infrastructure. We believe that these sensors, which are self-powered, could be used to provide information about traffic, road conditions and repair needs as well as allowing the roads to communicate directly with autonomous vehicles enabling these vehicles to sense the road in all weather conditions. By complementing the asphaltic cement we expect to produce with integrated sensors for automated vehicles, we believe that we will be able to offer a smart road technology – moving this company from one of “Waste to Road” to one of “Waste to Smart Road”.

Redeployment of our Metallic Separation Technology

Our licensed metallic separation technology has successfully recovered precious metals including, but not limited to, gold, palladium, platinum, rodium and silver. We intend to modify our existing metallic separation equipment to allow us to capture a greater amount of the precious metals, which are typically wasted. We intend to redeploy our metallic separation technology machines in conjunction with our RPC machines to locations where precious metals have been detected in the soil and to standalone locations to process mine tailings and other soils.

Risks Associated with Our Business

Our business is subject to a number of risks of which you should be aware before making a decision to invest in our common shares. The following, and other risks, are discussed more fully in the “Risk Factors” section of this prospectus:

| · | We are an early stage operating company and we are subject to substantial risks inherent in the establishment of a new business venture; | |

| · | We have historically suffered net losses and we may not be able to achieve or sustain future profitability; | |

| · | We will require additional funding beyond this contemplated offering to fund our operations generally and such funding may not be available on acceptable terms or at all; | |

| · | The COVID-19 pandemic has had and may continue to have a negative impact on our business and operations; | |

| · | We rely on the experience and knowledge of our management team, Board of Directors and Advisory Board, and the loss of one or more members of our management team, Board of Directors and/or Advisory Board would adversely impact our business; |

| 5 |

| · | Our business is subject to extensive legal regulation and unexpected changes to law or increases to fees could have a significant adverse impact on our business; | |

| · | Our primary business is impacted by the oil industry and manufacturing industry, which are subject to uncertain economic conditions; | |

| · | We currently depend and are likely to continue to depend on a limited number of customers for a significant portion of our revenues; and | |

| · | We may not be able to adequately protect our proprietary rights. |

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. See “Risk Factors — Risks Relating to Our Common Stock and the Offering — We are an ‘emerging growth company’ and will be able to avail ourselves of reduced disclosure requirements applicable to emerging growth companies, which could make our common stock less attractive to investors.” These provisions include:

| · | being permitted to provide only two years of audited financial statements in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; |

| · | reduced disclosure obligations regarding executive compensation arrangements; |

| · | not being required to hold a non-binding advisory vote on executive compensation or golden parachute arrangements; and |

| · | exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting. |

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of this offering, (b) in which we have total annual gross revenue of at least $1.07 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeded $700.0 million as of the prior June 30th, and (2) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period. We may choose to take advantage of some but not all of these exemptions. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock.

Notwithstanding the above, we are also currently qualified as a “smaller reporting company” under SEC rules. In the event that we are still considered a smaller reporting company at such time as we cease to be an emerging growth company, the disclosure we will be required to provide in our filings with the SEC will increase, but will still be less than it would be if we were not considered either an emerging growth company or a smaller reporting company. Specifically, similar to emerging growth companies, smaller reporting companies are able to provide simplified executive compensation disclosures in their filings; are exempt from the provisions of Section 404(b) of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”) requiring that independent registered public accounting firms provide an attestation report on the effectiveness of their internal control over financial reporting; and have certain other decreased disclosure obligations in their SEC filings, including, among other things, only being required to provide two years of audited financial statements in their annual reports.

| 6 |

Corporate History and Information

The Company was originally organized on November 1, 2006 as a limited liability company in the State of Nevada as Genecular Holdings, LLC. The Company’s name was changed to NGI Holdings, LLC on November 3, 2006. On April 30, 2008, the Company was converted to a corporation and changed its name to Vivakor, Inc. pursuant to Articles of Conversion filed with the Nevada Secretary of State.

We have the following direct and indirect wholly-owned active subsidiaries: VivaVentures Management Company, Inc., a Nevada corporation, VivaSphere, Inc., a Nevada corporation, VivaVentures Oil Sands, Inc., a Utah corporation, and RPC Design and Manufacturing LLC, a Utah company. We have a 99.95% interest in VivaVentures Energy Group, Inc., a Nevada Corporation; the 0.05% minority interest in VivaVentures Energy Group, Inc. is held by a private investor unaffiliated with the Company. We also have an approximate 49% interest in Vivakor Middle East Limited Liability Company, a Qatar limited liability company.

The Company’s address is 433 Lawndale Drive South Salt Lake City, UT 84115. Our phone number is (949) 281-2606. Our website is: www.vivakor.com. The information on, or that can be accessed through, this website is not part of this prospectus, and you should not rely on any such information in making the decision whether to purchase the Company’s common stock.

| 7 |

| Common stock offered by us | shares of common stock, par value $0.001 | |

| Assumed public offering price | $ per share, which was the last reported sale price of our common stock on the OTCPink on , 2020 | |

| Common stock to be outstanding after the offering: | shares. If the underwriter’s over-allotment option is exercised in full, the total number of shares of our common stock outstanding immediately after this offering will be . | |

| Overallotment option: | We have granted the underwriters a 45-day option to purchase up to an additional shares of common stock to cover over-allotments, if any, at the public offering price less underwriting discounts and commissions. | |

| Use of proceeds: | We expect to use the net proceeds from this offering to purchase two RPC units, together with related equipment and enhancements, for the continued development of our hydrocarbon upgrading technologies and for working capital and other general corporate purposes including the potential repayment of outstanding bridge notes. See “Use of Proceeds.” | |

| Risk factors: | Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the information set forth in the “Risk Factors” section of this prospectus beginning on page 10 before deciding to invest in our securities. | |

| OTCPink Trading symbol: | Our common stock is currently quoted on the OTCPink under the trading symbol “VIVK”. | |

| Proposed trading symbol: | We intend to apply to to list our common stock under the symbol “VIVK.” No assurance can be given that our application will be approved. |

| ____________ |

The number of shares of common stock shown above to be outstanding after this offering is based on 323,919,665 shares outstanding as of October 30, 2020, and excludes the following:

| · | 1,060,000 shares of common stock issuable upon the exercise of outstanding warrants at a weighted average exercise price of $0.40 per share; | |

| · | 164,645 shares of common stock issuable upon the conversion of $81,201 of various convertible notes payable that convert at a range between $0.10 and $0.25 per share; | |

| · | shares of common stock issuable upon the conversion of $311,383 of certain convertible bridge notes that may, at the option of the Company, be converted into common stock at a discount of 20% to the offering price or repaid with the proceeds from this offering; | |

| · | 60,000,000 shares of common stock reserved for future issuance under the new Vivakor Inc. 2020 Equity Incentive Plan (the “Vivakor 2020 Plan”) we intend to adopt immediately prior to this offering (including 500,000 shares to be issued to a former employee, options to purchase 30,000,000 shares to be issued to LBL Professional Consulting, Inc. for consulting services and options to purchase 5,000,000 shares to be issued to Matthew Nicosia, our Chief Executive Officer, pursuant to his employment agreement, all in the form of stock options that will be issued under the Vivakor 2020 Plan); | |

| · | Any shares that may be issuable in exchange for LLC units of Vivaventures Royalty II LLC and/or Vivaventures Opportunity Fund pursuant to the respective operating agreements of such entities, as described in this prospectus. |

Prior to the consummation of this offering, we expect to effect a -for- reverse stock split of our issued and outstanding common stock (the “Reverse Stock Split”). No fractional shares of the Company’s common stock will be issued as a result of the Reverse Stock Split. Any fractional shares resulting from the Reverse Stock Split will be rounded up to the nearest whole share.

Unless otherwise stated, all information in this prospectus assumes:

| · | the automatic conversion of all outstanding shares of our Series A, Series B, Series B-1 and Series C-1 convertible preferred stock into an aggregate of 74,059,410 shares of common stock, the conversion of which will occur immediately prior to the consummation of this offering. |

| · | no exercise of the underwriters’ over-allotment option to purchase additional shares; |

| · | no exercise of the warrants to be issued to the representative of the underwriters in connection with this offering as described in the “Underwriting — Representative’s Warrants” section of this prospectus; and |

| · | the completion of the Reverse Stock Split. |

| 8 |

SUMMARY CONSOLIDATED FINANCIAL INFORMATION

The following summary consolidated statements of operations data for the periods ended June 30, 2020 (unaudited) and June 30, 2019 (unaudited) and the years ended December 31, 2019 and 2018 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The historical financial data presented below is not necessarily indicative of our financial results in future periods. You should read the summary consolidated financial data in conjunction with those financial statements and the accompanying notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Our consolidated financial statements are prepared and presented in accordance with United States generally accepted accounting principles, or U.S. GAAP. Our unaudited condensed interim consolidated financial statements have been prepared on a basis consistent with our audited financial statements and include all adjustments, consisting only of normal and recurring adjustments that we consider necessary for a fair presentation of the financial position and results of operations as of and for such periods.

| Six Months Ended June 30, | Year Ended December 31, | |||||||||||||||

| 2020 | 2019 | 2019 | 2018 | |||||||||||||

| (unaudited) | (audited) | |||||||||||||||

| Consolidated Statements of Operations Data: | ||||||||||||||||

| Revenue | $ | 1,023,344 | $ | – | $ | – | $ | 10,179 | ||||||||

| Cost of revenues | 984,941 | – | – | 3,550 | ||||||||||||

| Gross profit | 38,403 | – | – | 6,629 | ||||||||||||

| Total operating expenses | 1,693,277 | 1,127,562 | 2,303,181 | 1,880,347 | ||||||||||||

| Operating loss | (1,654,874 | ) | (1,127,562 | ) | (2,303,181 | ) | (1,873,718 | ) | ||||||||

| Total other income (expense) | 2,117,545 | 651,852 | 618,177 | (362,282 | ) | |||||||||||

| Income (loss) before provision for income taxes | 462,671 | (475,710 | ) | (1,685,004 | ) | (2,236,000 | ) | |||||||||

| Benefit (provision) for income taxes | 8,171 | (52,831 | ) | (589,203 | ) | 36,645 | ||||||||||

| Consolidated net income (loss) | $ | 470,842 | $ | (528,541 | ) | $ | (2,274,207 | ) | $ | (2,199,355 | ) | |||||

| Net income (loss) attributable to Vivakor, Inc. | $ | 897,958 | $ | (499,365 | ) | $ | (2,159,242 | ) | $ | (2,178,345 | ) | |||||

| Basic income (loss) per common share | $ | 0.00 | $ | (0.00 | ) | $ | (0.01 | ) | $ | (0.02 | ) | |||||

| As of June 30, 2020 | ||||||||||||

| Actual | Pro Forma | Pro Forma As Adjusted(1) | ||||||||||

| Selected Balance Sheet Data (end of period): | (unaudited) | |||||||||||

| Cash and marketable securities | $ | 3,406,132 | $ | 3,406,132 | $ | |||||||

| Total assets | 42,255,722 | 42,255,722 | ||||||||||

| Total debt | 6,053,722 | 6,053,722 | ||||||||||

| Total liabilities | 14,029,768 | 14,029,768 | ||||||||||

| Total temporary equity | 15,072,298 | – | ||||||||||

| Total shareholders’ equity | 13,153,656 | 28,225,954 | ||||||||||

(1) Each $0.10 increase (decrease) in the public offering price per share would increase (decrease) each of cash and marketable securities, total assets and total shareholders’ equity by approximately $ , assuming that the number of shares we are offering, as set forth on the cover page of this prospectus, remains the same and that the underwriters do not exercise their over-allotment option. Depending on market conditions and other considerations at the time we price this offering, we may sell a greater or lesser number of shares than the number set forth on the cover page of this prospectus. An increase (decrease) of 1,000,000 in the number of shares we are offering would increase (decrease) each of cash and marketable securities, total assets and total shareholders’ equity by approximately $ , assuming the public offering price per share remains the same.

| 9 |

Investing in our common stock involves a great deal of risk. Careful consideration should be made of the following factors as well as other information included in this prospectus before deciding to purchase our common stock. There are many risks that affect our business and results of operations, some of which are beyond our control. Our business, financial condition or operating results could be materially harmed by any of these risks. This could cause the trading price of our common stock to decline, and you may lose all or part of your investment. Additional risks that we do not yet know of or that we currently think are immaterial may also affect our business and results of operations.

Risks Relating to our Business

We are at an early operational stage, and our success is subject to the substantial risks inherent in the establishment of a new business venture.

Our business and operations are in an early stage and subject to all of the risks inherent with new business ventures. Our initial operations have been focused on the remediation of soil and the extraction of hydrocarbons, such as oil, from properties contaminated by or laden with heavy crude oil and hydrocarbon-based substances. We intend to, but have not yet completed the second stage of our operational strategy, selling the asphaltic cement and/or other petroleum-based products we are able to produce from the hydrocarbons we recover.

Our business and operations may not prove to be successful. We have deployed only two RPC units to date, including one unit to Kuwait (for which operations have been temporarily suspended due to COVID-19) and another to Vernal, Utah (which is presently operating). We will need to scale our business beyond these two RPCs and demonstrate that our scaled-up recovery and remediation business can be profitable Any future success that we may enjoy will depend on many factors, some of which may be beyond our control, and others which cannot be predicted at this time. Although we began operations in 2008 as a technology acquisition company primarily focused on medical technologies, we have only been operating under our current business plan focused on soil remediation since 2011, and we have not yet proven to be profitable. We have not yet sold any substantial amount of products or services commercially and have not proven that our business model will allow us to identify and develop commercially feasible products or technologies.

We have historically suffered net losses, and we may not be able to sustain profitability.

We had an accumulated deficit of $27,015,290 as of June 30, 2020, and we expect to continue to incur significant development expenses in the foreseeable future related to the completion of the development and commercialization of our products. As a result, we are incurring operating and net losses, and it is possible that we may never be able to sustain the revenue levels necessary to achieve and sustain profitability. If we fail to generate sufficient revenues to operate profitably on a consistent basis, or if we are unable to fund our continuing losses, you could lose all or part of your investment.

We have substantial doubt in our ability to continue as a going concern.

The accompanying financial statements have been prepared assuming we will continue as a going concern, which contemplates, among other things, the realization of assets and satisfaction of liabilities in the normal course of business. Our independent registered public accounting firm has issued a report that includes an explanatory paragraph referring to our recurring losses from operations and expressing substantial doubt in our ability to continue as a going concern without additional capital becoming available.

We believe that the successful completion of this offering will eliminate this doubt and enable us to continue as a going concern; however, if we are unable to raise sufficient capital in this offering, we may need to obtain alternative financing or significantly modify our operational plans in order to continue operations.

We will need additional financing to continue to fund our operations. We may raise capital through loans from current stockholders, public or private equity or debt offerings, grants, or strategic arrangements with third parties. There can be no assurance that additional capital will be available to us on acceptable terms, or at all.

| 10 |

We rely upon a few, select key employees who are instrumental in our ability to conduct and grow our business. In the event any of those key employees would no longer be affiliated with the Company, it may have a material detrimental impact as to our ability to successfully operate our business.

Our future success will depend in large part on our ability to attract and retain high-quality management, operations, and other personnel who are in high demand, are often subject to competing employment offers, and are attractive recruiting targets for our competitors. The loss of qualified executives and key employees, or our inability to attract, retain, and motivate high-quality executives and employees required for the planned expansion of our business, may harm our operating results and impair our ability to grow.

We depend on the continued services of our key personnel, including Matthew Nicosia, our Chief Executive Officer, Tyler Nelson, our Chief Financial Officer, and Daniel Hashim, our Chief Scientific Officer. Our work with each of these key personnel are subject to changes and/or termination, and our inability to effectively retain the services of our key management personnel, could materially and adversely affect our operating results and future prospects.

We may have difficulty raising additional capital, which could deprive us of necessary resources, and you may experience dilution or subordinate stockholder rights, preferences and privileges as a result of our financing efforts.

We expect to continue to devote significant capital resources to fund the continued development of our RPCs and related technologies. In order to support the initiatives envisioned in our business plan, we will need to raise additional funds through the sale of public or private debt or equity financing or other arrangements. Our ability to raise additional financing depends on many factors beyond our control, including the state of capital markets, the market price of our common stock and the development or prospects for development of competitive technologies by others. Sufficient additional financing may not be available to us or may be available only on terms that would result in further dilution to the current owners of our common stock.

We expect to obtain additional capital during 2020 through financing lease structures for our RPCs or other financing structures related to our RPCs. We also expect that the net proceeds from this offering, along with our current cash position, will enable us to fund our operating expenses and capital expenditure requirements for the next twelve months. Thereafter, unless we can achieve and sustain profitability, we anticipate that we will need to raise additional capital to fund our operations while we implement and execute our business plan.

Any future equity financing may involve substantial dilution to our then existing shareholders. Any future debt financing could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities. There can be no assurance that such additional capital will be available, on a timely basis, or on terms acceptable to us. If we are unsuccessful in raising additional capital or the terms of raising such capital are unacceptable, then we may have to modify our business plan and/or curtail our planned activities and other operations.

If we raise additional funds through government or other third-party funding, collaborations, strategic alliances, licensing arrangements or marketing and distribution arrangements, we may have to relinquish valuable rights to our technologies, future revenue stream or grant licenses on terms that may not be favorable to us. If we are unable to raise additional funds through equity or debt financings when needed, we may be required to delay, limit, reduce or terminate our product development or future commercialization efforts or grant rights to develop and market products that we would otherwise prefer to develop and market ourselves.

The COVID-19 pandemic has had and may continue to have a negative impact on our business and operations.

Our Kuwait operations have been suspended to comply with the social distancing measures implemented in Kuwait. Our Utah operations were temporarily suspended from March through May 2020, but have since resumed in full. These suspensions have had a negative impact on our business and there can be no guaranty that we will not need to suspend operations again in the future as a result of the pandemic. We are closely monitoring the COVID-19 pandemic and the directives from federal and local authorities in the United States and in Kuwait affecting not only our workforce, but those of companies with whom we work.

Economic conditions in the current period of disruption and instability could adversely affect our ability to access the capital markets, in both the near and long term, and thus adversely affect our business and liquidity.

The current economic conditions related to the COVID-19 pandemic have had, and likely will continue to have for the foreseeable future a negative impact on the capital markets. Even if we are able to raise capital, it may not be at a price or on terms that are favorable to us. We cannot predict the occurrence of future disruptions or how long the current conditions may continue.

| 11 |

Failure to effectively manage our expected growth could place strains on our managerial, operational and financial resources and could adversely affect our business and operating results.

Our expected growth could place a strain on our managerial, operational and financial resources. Further, if our subsidiaries’ businesses grow, then we will be required to manage multiple relationships. Any further growth by us or our subsidiaries, or any increase in the number of our strategic relationships, will increase the strain on our managerial, operational and financial resources. This strain may inhibit our ability to achieve the rapid execution necessary to implement our business plan and could have a material adverse effect on our financial condition, business prospects and operations and the value of an investment in our company.

We will need to achieve commercial acceptance of our products to continue to generate revenues and sustain profitability.

Our goal is to ultimately produce asphaltic cement and/or other petroleum-based products from the hydrocarbons we recover and sell these products to customers; however, we may not be able to successfully commercialize our products, and even if we do, we may not be able to do so on a timely basis. Superior competitive technologies may be introduced, or customer needs may change, which will diminish or extinguish the commercial uses for our applications. We cannot predict when significant commercial market acceptance for our products will develop, if at all, and we cannot reliably estimate the projected size of any such potential market. If the markets fail to accept our products, then we may not be able to generate revenues from the commercial application of our technologies. Our revenue growth and profitability will depend substantially on our ability to manufacture and deploy additional RPCs and produce asphaltic cement to the specifications required by each of our potential customers.

We have identified certain material weakness in our internal control over financial reporting. Failure to maintain effective internal controls could cause our investors to lose confidence in us and adversely affect the market price of our common stock. If our internal controls are not effective, we may not be able to accurately report our financial results or prevent fraud.

Section 404 of the Sarbanes-Oxley Act of 2002 (“Section 404”), requires that we maintain internal control over financial reporting that meets applicable standards. We may err in the design or operation of our controls, and all internal control systems, no matter how well designed and operated, can provide only reasonable assurance that the objectives of the control system are met. Because there are inherent limitations in all control systems, there can be no assurance that all control issues have been or will be detected. If we are unable, or are perceived as unable, to produce reliable financial reports due to internal control deficiencies, investors could lose confidence in our reported financial information and operating results, which could result in a negative market reaction and a decrease in our stock price.

We have identified certain material weaknesses in our internal controls related to revenue recognition and lack of staffing in the accounting and finance organization. In connection with these material weaknesses, in 2020, we implemented remediation measures including training of accounting personnel as well as hiring additional personnel with experience in the ongoing identification, including the implementation of an audit committee, design and implementation of internal control over financial reporting. We believe that we have substantially resolved our previously identified material weaknesses in our internal controls as a result of implementation of new policies and procedures, the completion of an audit of our financial statements and the addition of experienced, independent directors and committees. There can be no assurances that weakness in our internal controls will not occur in the future.

If we identify new material weaknesses in our internal control over financial reporting, if we are unable to comply with the requirements of Section 404 in a timely manner, if we are unable to assert that our internal control over financial reporting is effective, or if our independent registered public accounting firm is unable to express an opinion as to the effectiveness of our internal control over financial reporting (if and when required), we may be late with the filing of our periodic reports, investors may lose confidence in the accuracy and completeness of our financial reports and the market price of our common stock could be negatively affected. As a result of such failures, we could also become subject to investigations by the stock exchange on which our securities are listed, the SEC, or other regulatory authorities, and become subject to litigation from investors and stockholders, which could harm our reputation, financial condition or divert financial and management resources from our core business, and would have a material adverse effect on our business, financial condition and results of operations.

| 12 |

A major portion of our business is dependent on the oil industry, which is subject to numerous worldwide variables.

Our prospective customers are concentrated in the oil industry. As a result, we will be subject to the success of the oil industry, which is subject to substantial volatility based on numerous worldwide factors. A decline in the oil industry may have a material adverse effect on our business, financial condition, results of operations and cash flows. The oil and gas industry is competitive in all its phases. Competition in the oil and gas industry is intense. We will compete with other participants in the search for oil sand properties and in the marketing of oil and other hydrocarbon products. Our customers could include competitors such as oil and gas companies that have substantially greater financial resources, staff and facilities than those of our customers and lessees. Competitive factors in the distribution and marketing of oil and other hydrocarbon products include price and methods and reliability of delivery.

Within the oil remediation market, demand for our services will be limited to a specific customer base and highly correlated to the oil industry. The oil industry’s demand for equipment is affected by a number of factors including the volatile nature of the oil industry’s business, increased use of alternative types of energy and technological developments in the oil extraction process. A significant reduction in the target market’s demand for oil would reduce the demand for the equipment, which would have a material adverse effect upon our business, financial condition, results of operations and cash flows.

Low oil prices may substantially impact our ability to generate revenues.

Low oil prices may negatively impact our ability to operate. The demand for our products and services depend, in part, on the price of oil and the margins oil producers receive on the sale of oil. Oil prices are volatile and can fluctuate widely based upon a number of factors beyond our control. Any decline in the prices of and demand for oil could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We require a variety of permits to operate our business. If we are not successful in obtaining and/or maintaining those permits it will adversely impact our operations.

Our business requires permits to operate. Our inability to obtain permits in a timely manner could result in substantial delays to our business. In addition, our customers may not receive permitting for our equipment’s specific use and we may be unable to adjust our equipment to meet our customer’s permitting needs. The issuance of permits is dependent on the applicable government agencies and is beyond our control and that of our customers. There can be no assurance that we and/or our customers will receive the permits necessary to operate, which could substantially and adversely affect our operations and financial condition.

We are required to pay permit and approval fees to operate in certain business segments and locations. If we are not able to pay those fees it would adversely impact our business.

We are required to pay various types of permit and approval fees to the applicable governmental and quasi-governmental agencies to operate our business. These fees are subject to change at the discretion of the various agencies. Our inability to pay these permit and approval fees could substantially and adversely affect our operations and financial condition.

We, and our customers and prospective customers, are subject to numerous governmental regulations, both domestically and internationally. In order to operate successfully we must be able comply with these regulations.

Current and future government laws, regulations and other legal requirements may increase the costs of doing business or restrict business operations. Laws, regulations and other legal requirements, such as those relating to the protection of the environment and natural resources, health, business and tax have an effect on our cost of operation or those of our customers. Such governmental regulation may result in delays, cause us to incur substantial compliance and other costs and prohibit or severely restrict our business or that of our customers, which could have an adverse effect on our business, financial condition, results of operations and cash flows.

| 13 |

Based on the nature of our business we currently depend and are likely to continue to depend on a limited number of customers for a significant portion of our revenues.

We currently have two customers in Utah and a single customer in Kuwait. The failure to obtain additional customers or the loss of all or a portion of the revenues attributable to any current or future customer as a result of competition, creditworthiness, inability to negotiate extensions or replacement of contracts or otherwise could have a material adverse effect on our business, financial condition, results of operations and cash flows.

If our customers do not enter into, extend or honor their contracts with us, our profitability could be adversely affected. Our ability to receive payment for production depends on the continued solvency and creditworthiness of our customers and prospective customers. If any of our customers’ creditworthiness suffers, we may bear an increased risk with respect to payment defaults. If customers refuse to accept our equipment or make payments for which they have a contractual obligation, our revenues could be adversely affected. In addition, if a substantial portion of our contracts are modified or terminated and we are unable to replace the contracts (or if new contracts are priced at lower levels), our results of operations will be adversely affected.

Our primary business is impacted by the oil industry and the manufacturing industry, which are subject to uncertain economic conditions.

The global economy is subject to fluctuation and it is unclear how stable the oil industry and the manufacturing industry will be in the future. As a result, there can be no assurance that the business will achieve anticipated cash flow levels. Further, recent world events evolving out of trade disputes, increased terrorist activities and political and military action, and the COVID-19 pandemic, among other events, have created an air of uncertainty concerning the stability of the global economy. Historically, such events have resulted in disturbances in financial markets, and it is impossible to determine the likelihood of future events. Any negative change in the general economic conditions in the United States and globally could adversely affect the financial condition and operating results of the business. We plan to expand our level of operations. Slower economic activity, concerns about inflation or deflation, decreased consumer confidence, reduced corporate profits and capital spending, adverse business conditions and liquidity concerns in the general economy and recent international conflicts and terrorist and military activity have resulted in a downturn in worldwide economic conditions, especially in the United States. Political and social turmoil related to international conflicts and terrorist acts may place further pressure on economic conditions in the United States and worldwide. These political, social and economic conditions make it extremely difficult for us to accurately forecast and plan future business activities. If such conditions continue or worsen, then our business, financial condition and results of operations could be materially and adversely affected.

We will continue to be subject to competition in our business.

Our oil remediation equipment utilizes specific technology to extract oil from sand. Oil producers are continually investigating alternative oil production technologies with a view to reduce production costs. In addition, industries that compete with the oil industry, such as the electric power industry, also continue to innovate and create products that compete with the oil industry. There can be no assurance that superior alternative technologies will emerge, which could reduce the demand for and price of our product and services.

The market for our products and services is highly competitive and is becoming more so, which could hinder our ability to successfully market our products and services. We may not have the resources, expertise or other competitive factors to compete successfully in the future. We expect to face additional competition from existing competitors and new market entrants in the future. Many of our competitors have greater name recognition and more established relationships in the industry than we do. As a result, these competitors may be able to:

| · | develop and expand their product offerings more rapidly; |

| · | adapt to new or emerging changes in customer requirements more quickly; |

| · | take advantage of acquisition and other opportunities more readily; and |

| · | devote greater resources to the marketing and sale of their products and adopt more aggressive pricing policies than we can. |

| 14 |

We carry insurance coverage against liabilities for personal injury, death and property damage, but there is no guarantee this coverage will be sufficient to cover us against all claims.

Although, we maintain insurance coverage against liability for personal injury, death and property damage. There can be no assurance that this insurance will be sufficient to cover any such liabilities. We may not be insured or fully insured against the losses or liabilities that could arise from a casualty in the business operations. In addition, there can be no assurance that particular risks that are currently insurable will continue to be insurable on an economical basis or that the current levels of coverage will continue to be available. If a loss occurs that is partially or completely uninsured, we may incur a significant liability.

We may be unable to adequately protect our proprietary rights.

Our ability to compete partly depends on the superiority, uniqueness and value of our intellectual property. To protect our proprietary rights, we will rely on a combination of patents, copyrights and trade secrets, confidentiality agreements with our employees and third parties, and protective contractual provisions. Despite these efforts, any of the following occurrences may reduce the value of our intellectual property:

| · | Our applications for patents relating to our business may not be granted and, if granted, may be challenged or invalidated; |

| · | Issued patents may not provide us with any competitive advantages; |

| · | Our efforts to protect our intellectual property rights may not be effective in preventing misappropriation of our technology; |

| · | Our efforts may not prevent the development and design by others of products or technologies similar to or competitive with, or superior to those we develop; or |

| · | Another party may obtain a blocking patent and we would need to either obtain a license or design around the patent in order to continue to offer the contested feature or service in our products. |

We may become involved in lawsuits to protect or enforce our patents that would be expensive and time consuming.

In order to protect or enforce our patent rights, we may initiate patent litigation against third parties. In addition, we may become subject to interference or opposition proceedings conducted in patent and trademark offices to determine the priority and patentability of inventions. The defense of intellectual property rights, including patent rights through lawsuits, interference or opposition proceedings, and other legal and administrative proceedings, would be costly and divert our technical and management personnel from their normal responsibilities. An adverse determination of any litigation or defense proceedings could put our pending patent applications at risk of not being issued.

Furthermore, because of the substantial amount of discovery required in connection with intellectual property litigation, there is a risk that some of our confidential information could be compromised by disclosure during this type of litigation. For example, during the course of this type of litigation, confidential information may be inadvertently disclosed in the form of documents or testimony in connection with discovery requests, depositions or trial testimony. This disclosure could have a material adverse effect on our business and our financial results.

Our primary business operations rely on our ability to transport our equipment to different locations. Any impact on the cost, availability and reliability of transportation could adversely affect our business.

The availability and reliability of transportation and fluctuation in transportation costs could negatively impact the business. Transportation logistics play an important role in the sale of our products and services and in the oil industry generally. Delays and interruptions of transportation services because of accidents, failure to complete construction of infrastructure, infrastructure damage, lack of capacity, weather-related problems, governmental regulation, terrorism, strikes, lock-outs, third-party actions or other events could impair the operations of our customers and may also directly impair our ability to commence or complete production or services, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

| 15 |

The lands on which we conduct our business operations must be properly zoned for our services. If they aren’t then it could impact our business.

The lands on which we conduct our business operates must comply with applicable zoning regulations. Any unknown or future violations could limit or require us to cease operations.

Data security breaches are increasing worldwide. If we are the victim of such a breach it will materially impact our business.