Attached files

| file | filename |

|---|---|

| EX-23.2 - CONSENTS OF EXPERTS AND COUNSEL - Alset EHome International Inc. | hfe_ex232.htm |

| EX-5.1 - OPINION ON LEGALITY - Alset EHome International Inc. | hfe_ex51.htm |

| EX-1.1 - UNDERWRITING AGREEMENT - Alset EHome International Inc. | hfe_ex11.htm |

As

filed with the Securities and Exchange Commission on November

9, 2020.

Registration No. 333- 235693

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment

No. 5 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HF ENTERPRISES INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

6799

|

83-1079861

|

|

(State or other jurisdiction of

incorporation or organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification Number)

|

HF Enterprises Inc.

4800 Montgomery Lane, Suite 210

Bethesda, Maryland 20814

(301) 971-3940

(Address, including zip code, and telephone number, including area

code, of registrant’s principal executive

offices)

Chan Heng Fai

Chairman and Chief Executive Officer

HF Enterprises Inc.

4800 Montgomery Lane, Suite 210

Bethesda, Maryland 20814

(301) 971-3940

(Name, address, including zip code, and telephone number, including

area code, of agent for service)

Copies of all communications to:

|

Darrin M. Ocasio, Esq.

|

Thomas Poletti, Esq.

|

|

Sichenzia Ross Ference LLP

|

Katherine J. Blair, Esq.

|

|

1185 Avenue of Americas, 37th Floor

|

Manatt, Phelps & Phillips, LLP

|

|

New York, New York 10036

|

695 Town Center Drive, 14th Floor

|

|

Tel.: (212) 398-1493

|

Costa Mesa, California 92626

|

|

Fax: (212) 930-9725

|

Tel.: (714) 371-2501

|

|

Email: DMOcasio@SRF.LAW

|

Fax: (714) 371-2551

|

Approximate date of

commencement of proposed sale to the public: As soon as practicable

after the effective date of this registration

statement.

If any of the securities being registered on this

Form are to be offered on a delayed or continuous basis pursuant to

Rule 415 under the Securities Act of 1933, check the following

box. ☒

If this

Form is filed to register additional securities for an offering

pursuant to Rule 462(b) under the Securities Act, check the

following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same

offering. ☐

If this

Form is a post-effective amendment filed pursuant to Rule 462(c)

under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier

effective registration statement for the same offering.

☐

If this

Form is a post-effective amendment filed pursuant to Rule 462(d)

under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier

effective registration statement for the same offering.

☐

Indicate by check

mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated

filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange

Act.

|

Large Accelerated Filer ☐

|

Accelerated Filer ☐

|

Non-Accelerated Filer ☐

(Do not

check if a smaller reporting company)

|

Smaller Reporting Company ☒

Emerging

Growth Company ☒

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 7(a)(2)(B) of the Securities

Act. ☐

CALCULATION OF REGISTRATION FEE

|

Title

of each class of securities to be registered

|

Proposed

maximum aggregate

offering price(1)(2)

|

Amount of

registration

fee

|

|

Common Stock, par

value $0.001 per share (“Common Stock”)

|

$20,930,000

|

$2,716.71

|

|

Underwriter

Warrant

|

-

|

(3)

|

|

Common Stock

underlying Underwriter Warrant (4)

|

$ 1,465,100

|

$ 159.84

|

|

Total

|

22,395,100

|

$ 2,876.55(5)

|

(1)

Estimated solely

for the purpose of computing the amount of the registration fee

pursuant to Rule 457(0) under the Securities Act of 1933, as

amended.

(2)

Includes shares the

underwriters have the option to purchase to cover

over-allotments, if any.

(3)

No fee

pursuant to Rule 457(g) under the Securities Act.

(4)

We have

agreed to issue to the underwriters or

their designees a warrant to purchase an aggregate

number of shares of our common stock equal to 5% of the number of

shares of common stock issued in this offering, at an exercise

price per share equal to 140% of the initial public offering

price

(5)

Previously

paid.

The

registrant hereby amends this registration statement on such date

or dates as may be necessary to delay its effective date until the

registrant shall file a further amendment which specifically states

that this registration statement shall hereafter become effective

in accordance with Section 8(a) of the Securities Act of 1933

or until the registration statement shall become effective on such

date as the Commission, acting pursuant to said Section 8(a),

may determine.

The information in this preliminary prospectus is not complete and

may be changed. We may not sell these securities until the

registration statement filed with the Securities and Exchange

Commission is effective. This preliminary prospectus is not an

offer to sell nor does it seek an offer to buy these securities in

any jurisdiction where the offer or sale is not

permitted.

Subject to Completion, dated November 9,

2020

PRELIMINARY PROSPECTUS

2,600,000 Shares

HF

ENTERPRISES INC.

Common Stock

This is

the initial public offering of shares of common stock of HF

Enterprises Inc. Prior to this offering, no public market has

existed for our common stock. We are offering 2,600,000 shares. We

currently estimate that the initial public offering price will be

between $6.00 and $7.00 per share. We intend to list our shares of

common stock for trading on the Nasdaq Capital Market under the

symbol HFEN.

Investing

in our common stock involves a high degree of risk. See “Risk

Factors” beginning on page 11.

|

|

Per

Share

|

Total

|

|

Initial public

offering price

|

$

|

$

|

|

Underwriting

discounts and commissions (1)

|

$

|

$

|

|

Proceeds to us,

before expenses

|

$

|

$

|

__________________

(1) Does not

include a non-accountable expense allowance equal to 1.5% of the

gross proceeds of this offering payable to underwriters. Please see

the section of this prospectus entitled “Underwriting”

for additional information regarding underwriter

compensation.

We have

granted the underwriter the right to purchase up to 390,000

additional shares of common stock from us at the initial public

offering price less underwriting discounts and commissions to cover

over-allotments, if any. The underwriter can exercise this option

within 60 days after the date of this prospectus.

We are

an “emerging growth company” as defined under U.S.

federal securities laws and, as such, may elect to comply with

certain reduced public company reporting requirements after this

offering.

Neither

the Securities and Exchange Commission nor any other regulatory

body has approved or disapproved these securities or determined if

this prospectus is truthful or complete. Any representation to the

contrary is a criminal offense.

The

underwriters expect to deliver the shares of our

common stock to purchasers on or about _______, 2020.

|

Aegis Capital Corp.

WestPark

Capital, Inc.

|

The

date of this prospectus is ,

2020

TABLE OF CONTENTS

|

|

|

Page

|

|

Prospectus

Summary

|

|

1

|

|

Risk

Factors

|

|

11

|

|

Cautionary

Note Regarding Forward-Looking Statements

|

|

28

|

|

Use of

Proceeds

|

|

30

|

|

Dividend

Policy

|

|

30

|

|

Capitalization

|

|

31

|

|

Dilution

|

|

32

|

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

|

34

|

|

Business

|

|

58

|

|

Management

|

|

73

|

|

Executive

Compensation

|

|

79

|

|

Certain

Relationships and Related Party Transactions

|

|

81

|

|

Principal

Stockholders

|

|

87

|

|

Description

of Capital Stock

|

|

88

|

|

Shares

Eligible for Future Sale

|

|

91

|

|

Underwriting

|

|

93

|

|

Indemnification

for Securities Act Liabilities

|

|

97

|

|

Legal

Matters

|

|

97

|

|

Experts

|

|

97

|

|

Where

You Can Find More Information

|

|

97

|

|

Index

to Consolidated Financial Statements

|

|

F-1

|

About this Prospectus

Neither

we nor the underwriters have authorized

anyone to provide you with information that is different from that

contained in this prospectus or in any free writing prospectus we

may authorize to be delivered or made available to you. We take no

responsibility for, and can provide no assurance as to the

reliability of, any other information that others may give you. We

and the underwriters

are offering to sell shares of common stock and seeking offers to

buy shares of common stock only in jurisdictions where offers and

sales are permitted. The information contained in this prospectus

is accurate only as of the date on the front of this prospectus,

regardless of the time of delivery of this prospectus or any sale

of shares of our common stock. Our business, financial condition,

results of operations and prospects may have changed since that

date.

For

investors outside the United States: Neither we nor the

underwriters

have done anything that would permit this offering, or

possession or distribution of this prospectus, in any jurisdiction

where action for that purpose is required, other than in the United

States. Persons outside the United States who come into possession

of this prospectus must inform themselves about, and observe any

restrictions relating to, the offering of the shares of common

stock and the distribution of this prospectus outside of the United

States. See “Underwriting.”

Unless

otherwise indicated, information in this prospectus concerning

economic conditions, our industry, our markets and our competitive

position is based on a variety of sources, including information

from third-party industry analysts and publications and our own

estimates and research. Some of the industry and market data

contained in this prospectus are based on third-party industry

publications. This information involves a number of assumptions,

estimates and limitations.

The

industry publications, surveys and forecasts and other public

information generally indicate or suggest that their information

has been obtained from sources believed to be reliable. None of the

third-party industry publications used in this prospectus were

prepared on our behalf. The industry in which we operate is subject

to a high degree of uncertainty and risk due to a variety of

factors, including those described in “Risk Factors.”

These and other factors could cause results to differ materially

from those expressed in these publications.

|

|

|

|

|

|

PROSPECTUS SUMMARY

This summary highlights information contained in this prospectus

and does not contain all of the information that you should

consider in making your investment decision. Before investing in

our common stock, you should carefully read this entire prospectus,

including our consolidated financial statements and the related

notes thereto and the information set forth under the sections

“Risk Factors,” “Management’s Discussion

and Analysis of Financial Condition and Results of

Operations” and our consolidated financial statements and

related notes thereto, in each case included in this prospectus.

Some of the statements in this prospectus constitute

forward-looking statements. See “Cautionary Note Regarding

Forward-Looking Statements.”

Unless the context requires otherwise, the words “we,”

“us,” “our,” “our company,”

"the Company" and “our business” refer to HF

Enterprises Inc., a Delaware corporation, and its consolidated

subsidiaries.

Our Company

HF

Enterprises Inc. is a diversified holding company principally

engaged through its subsidiaries in property development, digital

transformation technology and biohealth activities with operations

in the United States, Singapore, Hong Kong, Australia and South

Korea. We manage our three principal businesses primarily through

our subsidiary, Alset International Limited (formerly known as

Singapore eDevelopment Limited and referred to herein as

“Alset International”), a public company traded on the

Singapore Stock Exchange. Through this subsidiary (and indirectly,

through other public and private U.S. and Asian subsidiaries), we

are actively developing two significant real estate projects near

Houston, Texas and in Frederick, Maryland in our property

development segment. We have designed applications for enterprise

messaging and e-commerce software platforms in the United States

and Asia in our digital transformation technology business unit.

Our recent foray into the biohealth segment includes research to

treat neurological and immune-related diseases, nutritional

chemistry to create a natural sugar alternative, research regarding

innovative products to slow the spread of disease, and natural

foods and supplements.

We opportunistically identify global businesses

for acquisition, incubation and corporate advisory services,

primarily related to our existing operating business segments. We

also have ownership interests outside of Alset International,

including an indirect 16.8% equity interest in Holista CollTech

Limited, a public Australian company that produces natural food

ingredients, and an indirect 13.1% equity interest in Vivacitas

Oncology Inc., a U.S.-based biopharmaceutical company, but neither

of which company has material asset value relative to our principal

businesses. Under the guidance of Chan Heng Fai, our founder,

Chairman and Chief Executive Officer, who is also our largest

stockholder, we have positioned ourselves as a participant in these

key markets through a series of strategic transactions. Our growth

strategy is both to pursue acquisition opportunities that we can

leverage on our global network using our capital and management

resources and to accelerate the expansion of our organic

businesses. From a geographical perspective, we recognized

100% and 98% of our total revenue in the years ended December 31,

2019 and 2018 in the United States, respectively, and expect that

our future revenue will continue to be concentrated in the United

States.

We

generally acquire majority and/or control stakes in innovative and

promising businesses that are expected to appreciate in value over

time. We have historically favored businesses that improve an

individual’s quality of life or that improve the efficiency

of businesses through technology in various industries. Our

involvement in various companies can usually be characterized in

one of three ways: (i) businesses (typically ones that we have

either created or acquired in their early stages) that we directly

manage, while maintaining a majority ownership position; (ii)

businesses where we hold a significant ownership position, and

share management with our partners; and (iii) businesses that we

acquire and hold a minority stake in, and where we do not manage

such entity (although an affiliate of our company may serve on the

board of directors), but where we view the financial stake as

contributing to the strategic goals of our other businesses. For

example, in our real estate business, which makes up the majority

of our assets, our company’s leadership is engaged in all

aspects of the management of our projects, and intends to remain so

engaged in the future. In our biohealth segment, we are more likely

to work with partners who will play a significant role in

management. At the present time, we do not anticipate that passive

investments, where we neither participate in management nor view

the ownership position as adding particular strategic value to

other businesses, will represent a significant portion of our

company’s assets in the future.

|

|

|

|

|

|

1

|

|

|

|

|

|

Our

focus is on businesses where our engagement will be particularly

significant for that entity’s growth prospects. Our emphasis

is on building businesses in industries where our management team

has in-depth knowledge and experience, or where our management can

provide value by advising on new markets and expansion. We have at

times provided a range of global capital and management services to

these companies in order to gain access to Asian markets. We

believe that our capital and management services provide us with a

competitive advantage in the selection of strategic acquisitions

which creates and adds value for our company and our

stockholders.

Our Current

Operations

Chan

Heng Fai has led our Alset

International subsidiary since 2014. In March 2018, Chan Heng Fai

formed our company and subsequently assigned his equity interests

in several companies, including Alset International and its

subsidiaries, to us for further expansion in the United States.

Chan Heng Fai has more than 40 years of experience serving as a

chief executive officer, director and private equity investor in

more than 35 private and publicly-held early-stage and growth

companies in the United States, Singapore and other countries. We

currently have 20 employees across four countries. We are a global company with our

corporate headquarters located in Bethesda, Maryland and additional

offices in Singapore, Magnolia, Texas, South Korea and Hong Kong.

Below is a description of our three principal

businesses.

Property

Development Business. We

initially began our real estate business in 2014, when our

51.04%-owned subsidiary Alset International started developing

property projects and participating in third-party property

development projects. LiquidValue Development

Inc.(“LiquidValue Development”), a 99.9%-owned

subsidiary of Alset International, owns, operates and manages real

estate development projects with a focus on land subdivision

developments. Development activities are generally contracted out,

including planning, design and construction, as well as other work

with engineers, surveyors, architects and general contractors. The

developed lots are then sold to builders for the construction of

new homes. LiquidValue Development’s main assets are two

subdivision development projects, one near Houston, Texas, known as

Black Oak, consisting of 162 acres and currently projected to have

approximately 550 to 600 units, and one in Frederick, Maryland,

known as Ballenger Run, consisting of 197 acres where we intend to

have 689 units. We consider projects in diverse regions across the

United States and maintain longstanding relationships with local

owners, brokers, attorneys and lenders to source projects.

LiquidValue Development will continue to focus on off-market deals

and raise appropriate financing for development activities. We

intend to embark on residential construction activities in

partnership with U.S. homebuilders and have commenced discussions

to acquire smaller U.S. residential construction projects. These

projects may be within both the for-sale and for-rent markets. We

believe these initiatives will provide a set of solutions to

stabilize the long-term revenue associated with property

development in the United States and create ancillary service

opportunities and revenue from this

business.

Digital

Transformation Technology Business. Our digital transformation technology business

unit is committed to enabling enterprises to engage in a digital

transformation by providing consulting, implementation and

development services with various technologies, including instant

messaging, blockchain, e-commerce, social media and payment

solutions. Our digital transformation technology business is

involved in mobile application product development and other

businesses, providing information technology services to end-users,

service providers and other commercial users through multiple

platforms. Our technology platform consists of instant messaging

systems, social media, e-commerce and payment systems, direct

marketing platforms, e-real estate, brand protection and

counterfeit and fraud detection. HotApp Blockchain Inc.,

(“HotApp”) a 99.8%-owned subsidiary of Alset

International, focuses on business-to-business solutions such as

enterprise messaging and workflow. Through HotApp, we have

successfully implemented several strategic platform developments

for clients, including a mobile front-end solution for network

marketing, a hotel e-commerce platform for Asia and a real estate

agent management platform in China. We have also enhanced our

technological capability from mobile application development to

include blockchain architectural design, allowing mobile-friendly

front-end solutions to integrate with blockchain

platforms.

|

|

|

|

|

|

2

|

|

|

|

|

|

Biohealth

Business. Our biohealth

business is committed to both funding research and developing and

selling products that promote a healthy lifestyle. Since Alset

International became involved in the biomedical and healthcare

market through its biohealth division – Global BioMedical

Pte. Ltd. – we have successfully formed new ventures with

biomedical companies and made headway with our research. On August

21, 2020, Impact BioMedical Inc, one of our subsidiaries, was

acquired by a subsidiary of Document Security Systems, Inc. in

exchange for securities of Document Securities Systems, Inc. A

subsidiary of Impact BioMedical is one of three shareholders in an

operating entity named Global BioLife, Inc. The other shareholders

of Global BioLife include Holista CollTech (we indirectly own 16.8%

of Holista CollTech) and an entity owned by the chief scientist

overseeing Global BioLife’s projects. Global BioLife is a

company devoted to research in three main areas: (i) the

“Linebacker” project, which aims to develop a universal

therapeutic drug platform, (ii) a new sugar substitute called

“Laetose,” and (iii) a multi-use fragrance called

“3F” (Functional Fragrance Formulation). Global BioLife

has formed a working collaboration with Chemia Corporation, a

specialty manufacturer specializing in high quality, cost effective

fragrances. Together with Chemia, we are attempting to license 3F.

Global BioLife has engaged a consulting firm in the

biopharmaceutical and life sciences industry, to assist in our goal

of licensing each of Linebacker, Laetose and

3F.

Through

our indirect 16.8% interest in Holista CollTech Limited

(“Holista CollTech”), we have collaborative biotech

operations in Australia and Malaysia, operating in three segments

– healthy food ingredients, dietary supplements and collagen.

Holista CollTech researches, develops, markets and distributes

health-oriented products to address the growing need for natural

medicine. It offers a suite of food ingredients including

low-glycemic index baked goods, low sodium salt, low-fat fried

foods and low-calorie and low-GI sugars. Holista CollTech produces

cosmetic-grade sheep (ovine) collagen using patented extraction

methods from Australia. Through Alset International, we also own

53% of iGalen International Inc., a distributor of supplements and

other health products. The remaining equity interests in iGalen

International Inc. are owned by the founder of Holista

CollTech.

Other

Business Activities. While we

have identified certain main areas of focus, we will not be limited

to these three principal businesses. Along with our ownership

stakes, we provide corporate strategy and business development

services. We also provide asset management services and corporate

restructuring and leveraged buy-out expertise. These service

offerings build relationships with promising companies for

potential future collaboration and expansion. We intend at all

times to operate our business in a manner as to not become

inadvertently subject to the regulatory requirements under the

Investment Company Act of 1940 or the Investment Advisers Act of

1940.

Our Market Opportunity

In

each of our businesses, we intend to focus on solid, growing

markets and capitalize on positive demographic and market trends.

In our property development business, we intend to develop

residential real estate properties in strategic markets where we

will be able to subdivide lots for development to meet expanding

needs for housing. In addition, we are exploring the potential to

expand our set of solutions for property development in the United

States, and we may engage in financing, home management, realtor

services, insurance and home title validation. We also intend to

embark on homebuilding activities in partnership with U.S.

homebuilders in the for-sale and for-rent sectors, and have

commenced discussions to acquire small U.S. homebuilding projects

(although no such agreements are currently in place). We believe

these initiatives have the opportunity to provide us with further

revenue streams. In our digital transformation technology business,

in response to the growth of internet technologies, we are being

increasingly called upon to provide software and services to manage

large amounts of personal data, prevent the unauthorized access of

such data and maintain and improve easily accessible and navigable

IT systems for firms and individuals. In the field of biohealth,

advances in neuroscience and molecular biology are resulting in new

generations of pharmaceutical products to treat neurological and

inflammatory-derived diseases. Through our ownership interests in

Global Biomedical Pte. Ltd. and Holista CollTech, we intend to

continue to seek ways to leverage our biomedical

research.

|

|

|

|

|

|

3

|

|

|

|

|

|

Our Growth Strategy and Competitive Advantages

Our

goal is to develop or acquire ownership interest in companies that

possess high-growth potential, and to provide those companies with

capital markets and management services that will help them grow.

Although we are aware of other, mostly larger companies that have

utilized comparable structures to achieve their business objectives

and will compete with us for not only promising acquisition targets

but also investor capital, we believe our services that extend from

the United States into Asian markets provide us competitive

advantages. We also believe that we can build a brand that is

synonymous with integrity, strong corporate governance and

transparency with an emphasis on social responsibility. Key

elements of our growth strategy and competitive advantages

include:

Accretive

acquisitions and strategic relationships at each level of our

company. We intend to continue

to pursue acquisitions in the United States and internationally,

that consolidate market share, expand our geographical footprint

and further our position as a participant in each of our three

principal businesses. In addition, we regularly engage in

negotiations with potential acquisition targets seeking capital and

management services. We seek to identify and partner with companies

with complementary technology and where our management’s

access to business extension opportunities in Asia could be

commercially beneficial to them.

Diverse and

competitive positioning of our companies. Our three principal businesses operate in highly

competitive but diverse markets which we believe balance the risk

profile of our company. We have positioned ourselves over the past

five years as a participant in these markets through a series of

strategic acquisitions, following a business philosophy implemented

by Chan Heng Fai, our founder, Chairman, Chief Executive Officer

and largest stockholder. Our business has historically focused on

property development and digital transformation technology. We have

more recently entered into the biohealth business, a space which we

believe has significant growth potential. We believe the diverse

and competitive positioning in these markets of our companies

serves as a competitive strength.

Operations

strategically located in key markets. By maintaining multiple offices in Singapore,

Magnolia, Texas, South Korea and Hong Kong, together with our

Bethesda, Maryland corporate headquarters, we are not dependent on

a single economic climate to ensure that our business continues to

grow. We have the financial and organizational resources to support

opportunistic business development on a global scale, and we are

highly experienced in expanding into new geographical regions and

markets. Additionally, we maintain strategic alliances within each

of our businesses affording us additional scalability. We

continually evaluate opportunities to expand our businesses in key

markets.

Aided by an

international distribution network. The strength of our global network provides us

with the unique opportunity to target multiple client sectors

simultaneously, rather than remain constrained to isolated regional

markets. Our management team has extensive global experience and

deep relationships in each of our operating markets, particularly

in Asia. By leveraging the reach of our international distribution

network across each of our three principal businesses, our products

and services reach a broad client base.

Central

capital and management support for all companies.

Our “hands-on” management

team provides centralized capital and management oversight across

our three principal businesses. We believe we can improve the

margins by controlling costs at our businesses as we centralize

business practices in functional areas including financing,

accounting, human resources, back-office administration,

information technology and risk management. These margin

improvements can be accomplished through leveraging our central

capital and management capabilities to allow our businesses to

better focus their efforts on revenue generation and product

enhancement. In addition, we seek to increase revenue for each of

our majority-owned and/or controlled operating subsidiaries by

cross-selling the complementary technical services and distribution

network of each company, particularly utilizing the resources of

our digital transformation technology business unit. Also, capital

and management oversight connect our businesses under a uniform

company culture of fairness, integrity, adaptability and results

orientation.

Strong

alignment of interests through founder’s ownership.

We believe a strong alignment of

interests with stockholders and investors exists through the

ownership of a significant percentage of our outstanding shares by

Chan Heng Fai, our founder, Chairman and Chief Executive Officer.

Chan Heng Fai has led Alset International since 2014 and has led

our company since its inception. By providing structural and

economic alignment with the performance of our company, Chan Heng

Fai’s continuing controlling interest is directly aligned

with those of our investors. We believe the combination of these

characteristics has promoted long-term planning, an enhanced

culture among all of our group of companies, strategic partners and

employees, and ultimately the creation of value for our company and

our stockholders.

|

|

|

|

|

|

4

|

|

|

|

|

|

Selected Risks Associated with Our Business

Our

business and prospects may be limited by a number of risks and

uncertainties that we currently face, including the

following:

● We

operate in the intensely competitive property development, digital

transformation technology and biohealth markets against a number of

large, well-known companies in each of those markets.

● We and

our majority-owned and/or controlled operating subsidiaries have a

limited operating history and we cannot ensure the long-term

successful operation of all of our businesses.

● We had

a net loss of $93,085 for the six months ended June 30, 2020 and

net losses of $8,053,428 and $7,490,568 for the years ended

December 31, 2019 and 2018, respectively. There can be no assurance

we will have net income in future periods.

● We are

a holding company and derive all of our operating income from, and

hold substantially all of our assets through, our U.S. and foreign

company ownership interests. The effect of this structure is that

we will depend on the earnings of our subsidiaries, and the payment

or other distributions to us of these earnings, to meet our

obligations and make capital expenditures.

● There

is no assurance that we will be able to identify appropriate

acquisition targets, successfully acquire identified targets or

successfully develop and integrate the businesses to realize their

full benefits.

● Our

business depends on the availability to us of Chan Heng Fai, our

founder, Chairman and Chief Executive Officer, who has developed

and implemented our business philosophy and who would be extremely

difficult to replace, and our business would be materially and

adversely affected if his services were to become unavailable to

us.

● We are

vulnerable to adverse changes in the economic environment in the

United States, Singapore, Hong Kong, Australia and South Korea,

particularly with respect to increases in wages for professionals,

fluctuation in the value of foreign currencies and governmental

trade policies between nations.

In

addition, we face other risks and uncertainties that may materially

affect our business prospects, financial condition and results of

operations. You should consider the risks discussed in “Risk

Factors” and elsewhere in this prospectus before investing in

our common stock.

Implications of Our Being an “Emerging Growth

Company”

As

a company with less than $1.07 billion in revenue during our last

completed fiscal year, we qualify as an “emerging growth

company” under the Jumpstart Our Business Startups Act of

2012, or the JOBS Act. An emerging growth company may take

advantage of specified reduced reporting requirements that are

otherwise generally applicable to public companies. In particular,

as an emerging growth company, we:

● are

not required to obtain an attestation and report from our auditors

on our management’s assessment of our internal control over

financial reporting pursuant to the Sarbanes-Oxley

Act;

● are

not required to provide a detailed narrative disclosure discussing

our compensation principles, objectives and elements, and analyzing

how those elements fit with our principles and objectives (commonly

referred to as “compensation discussion and

analysis”);

● are

not required to obtain a non-binding advisory vote from our

stockholders on executive compensation or golden parachute

arrangements (commonly referred to as the “say-on-pay,”

“say-on-frequency” and

“say-on-golden-parachute” votes);

● are

exempt from certain executive compensation disclosure provisions

requiring a pay-for-performance graph and CEO pay ratio

disclosure;

● may

present only two years of audited financial statements and only two

years of related Management’s Discussion and Analysis of

Financial Condition and Results of Operations, or MD&A;

and

● are

eligible to claim longer phase-in periods for the adoption of new

or revised financial accounting standards under §107 of the

JOBS Act.

|

|

|

|

|

|

5

|

|

|

|

|

|

We intend to take advantage of all of these

reduced reporting requirements and exemptions, including the longer

phase-in periods for the adoption of new or revised financial

accounting standards under §107 of the JOBS Act. Our election

to use the phase-in periods may make it difficult to compare our

financial statements to those of non-emerging growth companies and

other emerging growth companies that have opted out of the phase-in

periods under §107 of the JOBS Act. Please see “Risk

Factors” on page 22 (“We are an ‘emerging

growth company’. . . .”).

Certain

of these reduced reporting requirements and exemptions were already

available to us due to the fact that we also qualify as a

“smaller reporting company” under SEC rules. For

instance, smaller reporting companies are not required to obtain an

auditor attestation and report regarding internal control over

financial reporting, are not required to provide a compensation

discussion and analysis, are not required to provide a

pay-for-performance graph or CEO pay ratio disclosure, and may

present only two years of audited financial statements and related

MD&A disclosure.

Under the JOBS Act, we may take advantage of the

above-described reduced reporting requirements and exemptions for

up to five years after our initial sale of common equity pursuant

to a registration statement declared effective under the Securities

Act of 1933, or such earlier time that we no longer meet the

definition of an emerging growth company. The JOBS Act provides

that we would cease to be an “emerging growth company”

if we have more than $1.07 billion in annual revenue, have more

than $700 million in market value of our common stock held by

non-affiliates, or issue more than $1 billion in principal

amount of non-convertible debt over a three-year period. Further,

under current SEC rules, we will continue to qualify as a

“smaller reporting company” for so long as we have a

public float (i.e., the market value of common equity held by

non-affiliates) of less than $250 million as of the last business

day of our most recently completed second fiscal

quarter.

Status as a Controlled Company

Upon

the completion of this offering, we expect to be considered a

“controlled company” within the meaning of the listing

standards of Nasdaq. Under these rules, a “controlled

company” may elect not to comply with certain corporate

governance requirements, including the requirement to have a board

that is composed of a majority of independent directors. We intend

to take advantage of these exemptions following the completion of

this offering. These exemptions do not modify the independence

requirements for our audit committee, and we intend to comply with

the applicable requirements of the Sarbanes-Oxley Act and rules

with respect to our audit committee within the applicable time

frame. For more information, please see “Management –

Status as a Controlled Company.”

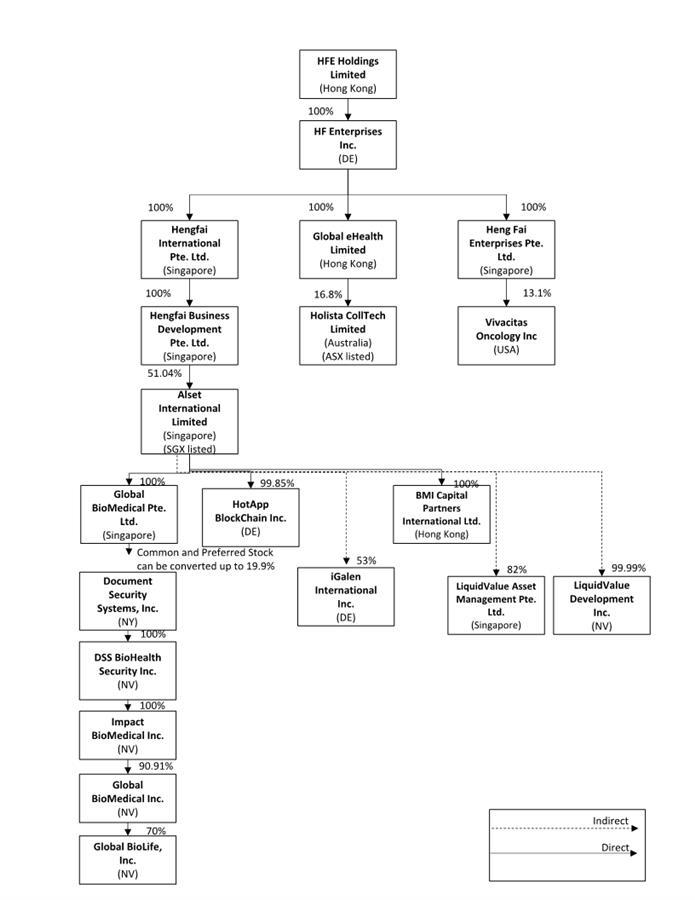

Organizational Background and Corporate Information

HF

Enterprises Inc. was incorporated in the State of Delaware on March

7, 2018. The following chart illustrates the current corporate

structure of our key operating entities:

|

|

|

|

|

|

6

|

|

|

|

|

|

|

|

|

|

|

|

7

|

|

|

|

|

|

The

percentages in the chart above indicate the ownership of such

entities. The indirect ownership omits 100% owned intermediate

holding companies. Our consolidated financial statements include

the financial results of all the entities listed except for Holista

CollTech Limited, Vivacitas Oncology Inc. and Document Security

Systems, Inc., for which we own only a minority interest. As

Impact BioMedical Inc and its majority subsidiaries were acquired

by Document Security Systems, Inc. on August 21, 2020, future

financial statements will not reflect the financial results of

those entities unless we acquire additional interests in Document

Security Systems.

This

prospectus gives effect to the following internal restructuring

transactions, completed on October 1, 2018, by which we issued a

total of 10,000,000 shares of our common stock to HFE Holdings

Limited:

● 100%

of the ownership interest in Hengfai International Pte. Ltd. was

transferred from Chan Heng Fai (an officer and director of our

company) to HF Enterprises Inc. in exchange for 8,500,000 shares of

our common stock to be held by HFE Holdings Limited. Hengfai

International Pte. Ltd., a Singapore limited company, is the sole

stockholder of Hengfai Business Development Pte. Ltd., which is the

owner of 761,150,294 ordinary shares of Alset International Limited

and warrants to purchase 359,834,471 ordinary shares of Alset

International Limited.

●

100% of the ownership interest in Global eHealth Limited was

transferred from Chan Heng Fai to HF Enterprises Inc. in exchange

for 1,000,000 shares of our common stock to be held by HFE Holdings

Limited. Global eHealth Limited, a Hong Kong company, is the owner

of 46,226,673 ordinary shares of Holista CollTech

Limited.

●

100% of the ownership interest in Heng Fai Enterprises Pte. Ltd.

was transferred from Chan Heng Fai to HF Enterprises Inc. in

exchange for 500,000 shares of our common stock to be held by HFE

Holdings Limited. Heng Fai Enterprises Pte. Ltd., a Singapore

limited company, owns 2,480,000 shares of common stock of Vivacitas

Oncology Inc.

Pursuant

to an agreement entered into by us on June 24, 2020 with our

stockholders HFE Holdings Limited and Chan Heng Fai, HFE Holdings

Limited surrendered 3,600,000 shares of our common stock to the

treasury of our company, and Chan Heng Fai surrendered 1,000 shares

of our common stock to the treasury of our company, and all such

shares were cancelled. As a result, the total number of outstanding

shares of our common stock before this offering was reduced to

6,400,000 shares from 10,001,000 shares.

On

August 20, 2020, our wholly-owned subsidiary Hengfai Business

Development Pte. Ltd. purchased 30,000,000 shares of Alset

International from our founder, Chairman, and Chief Executive

Officer, Chan Heng Fai, for S$1,860,000 Singapore Dollars

($1,333,429 U.S. Dollars). We have issued our founder a two-year,

interest-free promissory note in the amount of such purchase

price.

In

addition to the named companies referenced in the chart above, we

own a number of companies that serve only to hold other entities or

are intended to hold businesses that we plan to develop at a later

date.

Our

principal executive offices are located at 4800 Montgomery Lane,

Suite 210, Bethesda, Maryland 20814, telephone (301) 971-3940. We

also maintain offices in Singapore, Magnolia, Texas, South Korea

and Hong Kong. We maintain a corporate website at

http://www.hfenterp.com. Information on our website, and any

downloadable files found there, are not part of this prospectus and

should not be relied upon with respect to this

offering.

Any

information that we consider to be material to an evaluation of our

company will be included in filings on the SEC website,

http://www.sec.gov, and may also be disseminated using our investor

relations website, http://www.hfenterp.com, and press

releases.

|

|

|

|

|

|

8

|

|

|

|

||

|

|

THE OFFERING

The

summary below describes the principal terms of this offering. The

“Description of Capital Stock” section of this

prospectus contains a more detailed description of our common

stock.

|

|

||

|

|

|

|

||

|

|

Common

stock offered by us

|

|

2,600,000

shares

|

|

|

|

|

|

|

|

|

|

Underwriters'

over-allotment option

|

|

We have

granted the underwriters

a 60-day option to purchase up to an additional 390,000 shares of

our common stock from us at the initial public offering price less

underwriting discounts and commissions, to cover over-allotments,

if any.

|

|

|

|

|

|

|

|

|

|

Common stock to be outstanding

after this offering

|

|

9,000,000

shares. (1)

|

|

|

|

|

|

|

|

|

|

Use of

proceeds after expenses

|

|

We

estimate that the net proceeds of the sale of our common stock in

this offering will be approximately $14,584,171 (or approximately

$16,891,021 if the underwriters

exercise their option in full to purchase additional

shares of our common stock), based on an assumed initial public

offering price of $6.50 per share, which is the midpoint of the

range set forth on the cover page of this prospectus, after

deducting estimated underwriting discounts and commissions and

estimated offering expenses payable by us.

We

intend to use the net proceeds of this offering (i) to fund possible acquisitions of new

companies and additional properties, and (ii) for working capital

and general corporate purposes. See “Use of Proceeds”

for more information.

|

|

|

|

|

|

|

|

|

|

Dividend

policy

|

|

We have

never declared or paid any cash dividends on our common stock. We

anticipate that we will retain any earnings to support operations

and to finance the growth and development of our business.

Accordingly, we do not expect to pay cash dividends on our common

stock in the foreseeable future.

|

|

|

|

|

|

|

|

|

|

Controlled

company

|

|

Chan

Heng Fai, through HFE Holdings Limited, controls a majority of the

combined voting power of all classes of our voting stock. As a

result, we qualify as a “controlled company” within the

meaning of the listing standards of Nasdaq. Under these rules, a

“controlled company” may elect not to comply with

certain corporate governance requirements, including the

requirement to have a board that is composed of a majority of

independent directors. We have elected to take advantage of these

exemptions.

|

|

|

|

|

|

|

|

|

|

Risk

factors

|

|

Investing

in our common stock involves a high degree of risk. See “Risk

Factors” and other information included in this prospectus

for a discussion of factors you should carefully consider before

deciding to invest in shares of our common stock.

|

|

|

|

|

|

|

|

|

|

Proposed

Nasdaq Capital Market symbol

|

|

HFEN

(2)

|

|

|

|

|

|

|

|

|

|

(1) In this

prospectus, except as otherwise indicated, the number of shares of

our common stock that will be outstanding immediately after this

offering and the other information based thereon:

● assumes

an initial public offering price of $6.50 per share of common

stock, which is the midpoint of the range set forth on the cover

page of this prospectus;

● excludes

500,000 shares of our common stock reserved for future issuance

under our 2018 Incentive Compensation Plan; and

● no

exercise of the underwriters' option to purchase up to

390,000 additional shares from us in this offering to cover

over-allotments, if any.

(2) We

have reserved the trading symbol HFEN in connection with our

application to have our common stock listed for trading on the

Nasdaq Capital Market.

|

|

||

|

|

|

|

||

|

|

|

|

||

9

|

|

|

|

|

|

SUMMARY CONSOLIDATED FINANCIAL DATA

We

derived the summary consolidated statements of operations data for

the years ended December 31, 2019 and 2018 from our audited

consolidated financial statements included elsewhere in this

prospectus. The summary consolidated statements of operations for

the six months ended June 30, 2020 and 2019 and the summary

consolidated balance sheet data as of June 30, 2020 are derived

from our unaudited condensed consolidated financial statements on

the same basis as the audited consolidated financial statements and

include, in our opinion, all adjustments consisting only of normal

recurring adjustments that we consider necessary for a fair

statement of the financial information set forth in those

statements. Our historical results are not necessarily indicative

of the results that may be expected in the future. This summary of

historical financial data should be read together with the

financial statements and the related notes, as well as

“Management’s Discussion and Analysis of Financial

Condition and Results of Operations,” appearing elsewhere in

this prospectus.

|

|

|

|

|

|

|

|

|

Six Months ended

June 30,

|

Years ended December 31,

|

|

||

|

|

Consolidated

Statements of Operations Data:

|

2020

|

2019

|

2019

|

2018

|

|

|

|

|

(unaudited)

|

|

|

|

|

|

|

Revenues

|

$5,030,996

|

$17,637,635

|

$24,257,953

|

$20,380,940

|

|

|

|

Operating

expenses

|

7,391,679

|

21,871,158

|

31,200,994

|

23,556,665

|

|

|

|

Loss from continuing

operations

|

(2,360,683)

|

(4,233,523)

|

(6,943,041)

|

(3,175,725)

|

|

|

|

Other Income

(Expense)

|

2,743,636

|

(840,339)

|

(17,527)

|

(3,116,876)

|

|

|

|

Net Income (Loss) from continuing

operations .

|

268,300

|

(5,073,862)

|

(7,391,956)

|

(6,292,601)

|

|

|

|

Loss from discontinued

operations

|

(361,385)

|

(260,377)

|

(661,472)

|

(1,197,967)

|

|

|

|

Net Loss

|

(93,085)

|

(5,334,239)

|

(8,053,428)

|

(7,490,568)

|

|

|

|

Net income (loss) attributable to

common shareholders

|

527,348

|

(3,860,856)

|

(5,230,465)

|

(4,989,870)

|

|

|

|

Income (loss) per share –

basic and diluted continuing operations

|

0.08

|

(0.37)

|

(0.47)

|

(0.42)

|

|

|

|

Income (loss) per share –

basic and diluted discontinuing operations

|

(0.03)

|

(0.02)

|

(0.05)

|

(0.08)

|

|

|

|

Net income (loss) per

share

|

0.05

|

(0.39)

|

(0.52)

|

(0.50)

|

|

|

|

Weighted average common shares

outstanding – basic and diluted

|

9,880,967

|

10,001,000

|

10,001,000

|

10,001,000

|

|

|

|

|

|||||

|

|

The

following table summarizes our consolidated balance sheet data as

of June 30, 2020, on an actual basis and on an as adjusted basis,

to give effect to the net proceeds from the sale of 2,600,000

shares of our common stock in this offering at an assumed initial

public offering price of $6.50 per share, which is the midpoint of

the range set forth on the cover page of this prospectus, after

deducting the estimated underwriting discounts and commissions and

estimated offering expenses payable by us and excluding the

exercise of the over-allotment option held by the

underwriters

with respect to this offering, as if the offering had occurred on

June 30, 2020.

|

|

|

|

|

|

|

|

|

As of June 30,

2020

|

|

|

|

|

Consolidated Balance Sheet Data:

|

Actual

|

As

Adjusted

|

|

|

|

|

(unaudited)

|

|

|

|

|

Cash and restricted

cash*

|

$10,186,428

|

$24,770,599

|

|

|

|

Working capital

|

3,412,496

|

17,996,667

|

|

|

|

Total

assets

|

42,698,197

|

57,282,368

|

|

|

|

Total

indebtedness**

|

6,929,011

|

6,929,011

|

|

|

|

Total

liabilities

|

19,599,685

|

19,599,685

|

|

|

|

Total stockholders’

equity

|

23,098,512

|

37,682,683

|

|

|

|

|

|

|

|

*includes cash from discontinued operations

**Total indebtedness= Notes Payable + Accrued Interest

Pursuant to an agreement entered into by us on

June 24, 2020 with our stockholders HFE Holdings Limited and Chan

Heng Fai, HFE Holdings Limited surrendered 3,600,000 shares of our

common stock to the treasury of our company, and Chan Heng Fai

surrendered 1,000 shares of our common stock to the treasury of our

company, and all such shares were cancelled. As a result, the total

number of outstanding shares of our common stock before this

offering was reduced to 6,400,000 shares from 10,001,000 shares.

Income (loss) attributable to common shareholders –basic and

diluted would have been $0.08, $(0.60), $(0.82), and $(0.78) for

the six months ended June 30, 2020 and 2019 and the years ended

December 31, 2019 and 2018, respectively.

|

|

|

|

|

|

10

RISK FACTORS

An investment in our common stock involves a high degree of risk.

In addition to the other information contained in this prospectus,

prospective investors should carefully consider the following risks

before investing in our common stock. If any of the following risks

actually occur, as well as other risks not currently known to us or

that we currently consider immaterial, our business, operating

results and financial condition could be materially adversely

affected. As a result, the trading price of our common stock could

decline, and you may lose all or part of your investment in our

common stock. The risks discussed below also include

forward-looking statements, and our actual results may differ

substantially from those discussed in these forward-looking

statements. See “Cautionary Note Regarding Forward-looking

Statements” in this prospectus. In assessing the risks below,

you should also refer to the other information contained in this

prospectus, including the financial statements and the related

notes, before deciding to purchase any shares of our common

stock.

Risks Relating to Our Business

We have a history of annual net losses which may continue and which

may negatively impact our ability to achieve our business

objectives.

Our

property development and digital transformation technology

businesses were started in 2014 and 2015, respectively, and our

biohealth business was started in 2017. Our limited operating

history makes it difficult to evaluate our current business and

future prospects and may increase the risk of your investment. For

the six months ended June 30, 2020 and years ended December 31,

2019 and 2018, we had revenue of $5,030,996, $24,257,953 and

$20,380,940, net loss of $93,085 in the six months ended June 30,

2020 and net losses of $8,053,428 and $7,490,568 in the years ended

December 31, 2019 and 2018, respectively. Our failure to increase

our revenues or improve our gross margins will harm our business.

We may not be able to achieve, sustain or increase profitability on

a quarterly or annual basis in the future. If our revenue grows

more slowly than we anticipate, our gross margins fail to improve

or our operating expenses exceed our expectations, our operating

results will suffer. The prices we charge for our properties,

products and services may decrease, which would reduce our revenues

and harm our business. If we are unable to sell our properties,

products and services at acceptable prices relative to our costs,

or if we fail to develop and introduce on a timely basis new

products or services from which we can derive additional revenues,

our financial results will suffer.

We and our subsidiaries have limited operating histories and

therefore we cannot ensure the long-term successful operation of

our business or the execution of our growth strategy.

Our

prospects must be considered in light of the risks, expenses and

difficulties frequently encountered by growing companies in new and

rapidly evolving markets. We may meet many challenges

including:

●

establishing and

maintaining broad market acceptance of our products and services

and converting that acceptance into direct and indirect sources of

revenue;

●

establishing and

maintaining adoption of our technology on a wide variety of

platforms and devices;

●

timely and

successfully developing new products and services and increasing

the features of existing products and services;

●

developing products

and services that result in high degrees of customer satisfaction

and high levels of customer usage;

●

successfully

responding to competition, including competition from emerging

technologies and solutions;

●

developing and

maintaining strategic relationships to enhance the distribution,

features, content and utility of our products and services;

and

●

identifying,

attracting and retaining talented technical and sales services

staff at reasonable market compensation rates in the markets in

which we operate.

11

Our

growth strategy may be unsuccessful and we may be unable to address

the risks we face in a cost-effective manner, if at all. If we are

unable to successfully address these risks our business will be

harmed.

We have a holding company ownership structure and will depend on

distributions from our majority-owned and/or controlled operating

subsidiaries to meet our obligations. Contractual or legal

restrictions applicable to our subsidiaries could limit payments or

distributions from them.

We are

a holding company and derive all of our operating income from, and

hold substantially all of our assets through, our U.S. and foreign

subsidiaries, some of which are publicly held and traded. The

effect of this structure is that we will depend on the earnings of

our subsidiaries, and the payment or other distributions to us of

these earnings, to meet our obligations and make capital

expenditures. Provisions of U.S. and foreign corporate and tax law,

like those requiring that dividends are paid only out of surplus,

and provisions of any future indebtedness, may limit the ability of

our subsidiaries to make payments or other distributions to us.

Certain of our subsidiaries are minority owned and the assets of

these companies are not included in our consolidated balance

sheets. Additionally, in the event of the liquidation, dissolution

or winding up of any of our subsidiaries, creditors of that

subsidiary (including trade creditors) will generally be entitled

to payment from the assets of that subsidiary before those assets

can be distributed to us.

Our significant ownership interests in public companies listed on

limited public trading markets subjects us to risks relating to the

sale of their shares and the fluctuations in their stock

prices.

We own

indirect interests in several publicly traded companies –

most significantly, Alset International Limited, whose shares are

listed on the Singapore Stock Exchange, and Holista CollTech

Limited, whose shares are listed on the Australian Stock Exchange

(LiquidValue Development Inc. and HotApp Blockchain Inc. are not

currently traded on any exchange). Although the publicly traded

shares of Alset International and Holista CollTech Limited are

quoted on a trading market, the average trading volume of the

public shares is limited in each case. In view of the limited

public trading markets for these shares, there can be no assurance

that we would succeed in obtaining a price for these shares equal

to the price quoted for such shares in their respective trading

markets at the time of sale or that we would not incur a loss on

our shares should we determine to dispose of them in any of these

companies in the future. Additionally, on an ongoing basis,

fluctuations in the stock prices of these companies are likely to

be reflected in the market price of our common stock. Given the

limited public trading markets of these public companies, stock

price fluctuations in our price may be significant.

General political, social and economic conditions can adversely

affect our business.

Demand

for our products and services depends, to a significant degree, on

general political, social and economic conditions in our markets.

Worsening economic and market conditions, downside shocks, or a

return to recessionary economic conditions could serve to reduce

demand for our products and services and adversely affect our

operating results. In addition, an economic downturn could impact

the valuation and collectability of certain long-term receivables

held by us. We could also be adversely affected by such factors as

changes in foreign currency rates and weak economic and political

conditions in each of the countries in which we

operate.

The coronavirus or other adverse public health developments could

have a material and adverse effect on our business operations,

financial condition and results of operations.

In

December 2019, a novel strain of coronavirus (COVID-19) was first

identified in Wuhan, Hubei Province, China, and has since spread to

a number of other countries, including the United States. The

coronavirus, or other adverse public health developments, could

have a material and adverse effect on our business operations. The

coronavirus’ far-reaching impact on the global economy could

negatively affect various aspects of our business, including demand

for real estate. In addition, the coronavirus could directly impact

the ability of our staff and contractors to continue to work, and

our ability to conduct our operations in a prompt and efficient

manner. The coronavirus may adversely impact the timeliness of

local government in granting required approvals. Accordingly, the

coronavirus may cause the completion of important stages in our

projects to be delayed. The extent to which the coronavirus may

impact our business will depend on future developments, which are

highly uncertain and cannot be predicted. For more information on

this matter, see “Management’s Discussion and Analysis

of Financial Condition and Results of Operations- Financial Impact

of the COVID-19 Pandemic.”

12

We have made and expect to continue to make acquisitions as a

primary component of our growth strategy. We may not be able to

identify suitable acquisition candidates or consummate acquisitions

on acceptable terms, which could disrupt our operations and

adversely impact our business and operating results.

A

primary component of our growth strategy has been to acquire

complementary businesses to grow our company. We intend to continue

to pursue acquisitions of complementary technologies, products and

businesses as a primary component of our growth strategy to expand

our operations and customer base and provide access to new markets

and increase benefits of scale. Acquisitions involve certain known

and unknown risks that could cause our actual growth or operating

results to differ from our expectations. For example:

●

we may not be able

to identify suitable acquisition candidates or to consummate

acquisitions on acceptable terms;

●

we may pursue

international acquisitions, which inherently pose more risks than

domestic acquisitions;

●

we compete with

others to acquire complementary products, technologies and

businesses, which may result in decreased availability of, or

increased price for, suitable acquisition candidates;

●

we may not be able

to obtain the necessary financing, on favorable terms or at all, to

finance any or all of our potential acquisitions; and

●

we may ultimately

fail to consummate an acquisition even if we announce that we plan

to acquire a technology, product or business.

We may be unable to successfully integrate acquisitions, which may

adversely impact our operations.

Acquired

technologies, products or businesses may not perform as we expect

and we may fail to realize anticipated revenue and profits. In

addition, our acquisition strategy may divert management’s

attention away from our existing business, resulting in the loss of

key customers or employees, and expose us to unanticipated problems

or legal liabilities, including responsibility as a successor for

undisclosed or contingent liabilities of acquired businesses or

assets.

If we

fail to conduct due diligence on our potential targets effectively,

we may, for example, not identify problems at target companies or

fail to recognize incompatibilities or other obstacles to

successful integration. Our inability to successfully integrate

future acquisitions could impede us from realizing all of the

benefits of those acquisitions and could severely weaken our

business operations. The integration process may disrupt our

business and, if new technologies, products or businesses are not

implemented effectively, may preclude the realization of the full

benefits expected by us and could harm our results of operations.

In addition, the overall integration of new technologies, products

or businesses may result in unanticipated problems, expenses,

liabilities and competitive responses. The difficulties integrating

an acquisition include, among other things:

●

issues in

integrating the target company’s technologies, products or

businesses with ours;

●

incompatibility of

marketing and administration methods;

●

maintaining

employee morale and retaining key employees;

●

integrating the

cultures of our companies;

●

preserving

important strategic customer relationships;

●

consolidating

corporate and administrative infrastructures and eliminating

duplicative operations; and

●

coordinating and

integrating geographically separate organizations.

13

In

addition, even if the operations of an acquisition are integrated

successfully, we may not realize the full benefits of the

acquisition, including the synergies, cost savings or growth

opportunities that we expect. These benefits may not be achieved

within the anticipated time frame, or at all.

Acquisitions which we complete may have an adverse impact on our

results of operations.

Acquisitions may

cause us to:

●

issue common stock

that would dilute our current stockholders’ ownership

percentage;

●

use a substantial

portion of our cash resources;

●

increase our

interest expense, leverage and debt service requirements if we

incur additional debt to pay for an acquisition;

●

assume liabilities

for which we do not have indemnification from the former owners;

further, indemnification obligations may be subject to dispute or

concerns regarding the creditworthiness of the former

owners;

●

record goodwill and

non-amortizable intangible assets that are subject to impairment

testing and potential impairment charges;

●

experience

volatility in earnings due to changes in contingent consideration

related to acquisition earn-out liability estimates;

●

incur amortization

expenses related to certain intangible assets;

●

lose existing or

potential contracts as a result of conflict of interest

issues;

●

become subject to

adverse tax consequences or deferred compensation

charges;

●

incur large and

immediate write-offs; or

●

become subject to

litigation.

Our resources may not be sufficient to manage our expected growth;

failure to properly manage our potential growth would be

detrimental to our business.

We may

fail to adequately manage our anticipated future growth. Any growth

in our operations will place a significant strain on our

administrative, financial and operational resources and increase

demands on our management and on our operational and administrative

systems, controls and other resources. We cannot assure you that

our existing personnel, systems, procedures or controls will be

adequate to support our operations in the future or that we will be

able to successfully implement appropriate measures consistent with

our growth strategy. As part of this growth, we may have to

implement new operational and financial systems, procedures and

controls to expand, train and manage our employee base, and

maintain close coordination among our technical, accounting,

finance, marketing and sales. We cannot guarantee that we will be

able to do so, or that if we are able to do so, we will be able to

effectively integrate them into our existing staff and systems.

There may be greater strain on our systems as we acquire new

businesses, requiring us to devote significant management time and

expense to the ongoing integration and alignment of management,

systems, controls and marketing. If we are unable to manage growth

effectively, such as if our sales and marketing efforts exceed our

capacity to design and produce our products and services or if new

employees are unable to achieve performance levels, our business,

operating results and financial condition could be materially and

adversely affected.

14

Our international operations are subject to increased risks which

could harm our business, operating results and financial

condition.

In

addition to uncertainty about our ability to expand our

international market position, there are risks inherent in doing

business internationally, including:

●

trade

barriers, tariffs and changes in trade

regulations;

●

difficulties in

developing, staffing and simultaneously managing a large number of

varying foreign operations as a result of distance, language and

cultural differences;

●

the need to comply

with varied local laws and regulations;

●