Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - 9 METERS BIOPHARMA, INC. | ex322q32020.htm |

| EX-32.1 - EXHIBIT 32.1 - 9 METERS BIOPHARMA, INC. | ex321q32020.htm |

| EX-31.2 - EXHIBIT 31.2 - 9 METERS BIOPHARMA, INC. | ex312q32020.htm |

| EX-31.1 - EXHIBIT 31.1 - 9 METERS BIOPHARMA, INC. | ex311q32020.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2020

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to ________________

Commission file number 001-37797

9 METERS BIOPHARMA, INC.

(Exact name of registrant as specified in its charter)

Delaware | 27-3948465 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

8480 Honeycutt Road, Suite 120

Raleigh, North Carolina 27615

(Address of principal executive offices, including zip code)

(919) 275-1933

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock $0.0001 Par Value | NMTR | The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | ¨ | |

Non-accelerated filer | þ | Smaller reporting company | þ | |

Emerging growth company | þ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

As of November 4, 2020, the registrant had 150,324,757 shares of common stock, par value $0.0001 per share, issued and outstanding.

.

TABLE OF CONTENTS

2

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

9 METERS BIOPHARMA, INC.

Condensed Consolidated Balance Sheets

September 30, 2020 | December 31, 2019 | |||||||

Assets | (Unaudited) | |||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 12,435,982 | $ | 4,592,932 | ||||

Restricted deposit | 75,000 | 75,000 | ||||||

Prepaid expenses and other current assets | 1,122,196 | 555,052 | ||||||

Total current assets | 13,633,178 | 5,222,984 | ||||||

Property and equipment, net | 44,966 | 25,422 | ||||||

Right-of-use asset | 225,924 | 42,830 | ||||||

Other assets | 5,580 | 5,580 | ||||||

Total assets | $ | 13,909,648 | $ | 5,296,816 | ||||

Liabilities and Stockholders’ Equity (Deficit) | ||||||||

Current liabilities: | ||||||||

Accounts payable | $ | 2,564,565 | $ | 3,890,094 | ||||

Accrued expenses | 6,067,217 | 4,747,751 | ||||||

Convertible notes payable, net | 1,265,020 | 3,184,655 | ||||||

Derivative liabilities | 161,000 | 408,000 | ||||||

Warrant liabilities | — | 2,637,500 | ||||||

Accrued interest | 3,427 | — | ||||||

Lease liability, current portion | 47,199 | 42,830 | ||||||

Total current liabilities | 10,108,428 | 14,910,830 | ||||||

Lease liability, net of current portion | 180,645 | — | ||||||

Total liabilities | 10,289,073 | 14,910,830 | ||||||

Commitments and contingencies (Note 8) | ||||||||

Stockholders’ equity (deficit): | ||||||||

Preferred stock $0.0001 par value per share, 10,000,000 shares authorized; 0 shares issued and outstanding as of September 30, 2020 (unaudited) and December 31, 2019 | — | — | ||||||

Common stock $0.0001 par value per share, 350,000,000 shares authorized; 149,575,457 and 39,477,667 shares issued and outstanding as of September 30, 2020 (unaudited) and December 31, 2019, respectively | 14,959 | 3,948 | ||||||

Additional paid-in capital | 130,704,268 | 60,946,816 | ||||||

Accumulated deficit | (127,098,652 | ) | (70,564,778 | ) | ||||

Total stockholders’ equity (deficit) | 3,620,575 | (9,614,014 | ) | |||||

Total liabilities and stockholders’ equity (deficit) | $ | 13,909,648 | $ | 5,296,816 | ||||

See accompanying notes to these condensed consolidated financial statements.

3

9 METERS BIOPHARMA, INC.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

2020 | 2019 | 2020 | 2019 | |||||||||||||

Operating expenses: | ||||||||||||||||

Research and development | $ | 4,413,707 | $ | 3,943,420 | $ | 7,457,509 | $ | 8,215,079 | ||||||||

Acquired in-process research and development | — | — | 32,266,893 | — | ||||||||||||

General and administrative | 1,890,492 | 2,564,508 | 9,220,020 | 8,728,714 | ||||||||||||

Warrant inducement expense | — | — | 7,157,887 | — | ||||||||||||

Total operating expenses | 6,304,199 | 6,507,928 | 56,102,309 | 16,943,793 | ||||||||||||

Loss from operations | (6,304,199 | ) | (6,507,928 | ) | (56,102,309 | ) | (16,943,793 | ) | ||||||||

Other income (expense): | ||||||||||||||||

Interest income | 3,295 | 57,848 | 24,660 | 156,945 | ||||||||||||

Interest expense | (2,118,433 | ) | (472,052 | ) | (3,710,725 | ) | (1,330,923 | ) | ||||||||

Loss on extinguishment of convertible note payable | — | — | — | (1,049,166 | ) | |||||||||||

Change in fair value of derivative liability and extinguishment of derivative liability | 86,000 | 229,000 | 617,000 | 881,000 | ||||||||||||

Change in fair value of warrant liabilities | — | (2,528,100 | ) | 2,637,500 | 141,700 | |||||||||||

Total other income (expense), net | (2,029,138 | ) | (2,713,304 | ) | (431,565 | ) | (1,200,444 | ) | ||||||||

Loss before income taxes | (8,333,337 | ) | (9,221,232 | ) | (56,533,874 | ) | (18,144,237 | ) | ||||||||

Benefit from income taxes | — | — | — | — | ||||||||||||

Net loss | $ | (8,333,337 | ) | $ | (9,221,232 | ) | $ | (56,533,874 | ) | $ | (18,144,237 | ) | ||||

Net loss per common share, basic and diluted | $ | (0.06 | ) | $ | (0.26 | ) | $ | (0.65 | ) | $ | (0.56 | ) | ||||

Weighted-average common shares, basic and diluted | 141,625,796 | 35,883,953 | 87,323,241 | 32,401,624 | ||||||||||||

See accompanying notes to these condensed consolidated financial statements.

4

9 METERS BIOPHARMA, INC.

Condensed Consolidated Statements of Stockholders’ Equity (Deficit)

(Unaudited)

Three and Nine Months Ended September 30, 2020 | ||||||||||||||||||||

Series A Preferred Shares | Series A Preferred Amount | Common Stock Shares | Common Stock Amount | Additional Paid-in Capital | Accumulated Deficit | Total | ||||||||||||||

Balance as of December 31, 2019 | — | $ | — | 39,477,667 | $ | 3,948 | $ | 60,946,816 | $ | (70,564,778 | ) | $ | (9,614,014 | ) | ||||||

Warrant exchange | — | — | 1,847,309 | 185 | 690,654 | — | 690,839 | |||||||||||||

Share-based compensation | — | — | — | — | 276,000 | — | 276,000 | |||||||||||||

Stock issuance costs - Warrant exchange (FN-1) | — | — | — | — | (300,000 | ) | — | (300,000 | ) | |||||||||||

Net loss | — | — | — | — | — | (3,603,001 | ) | (3,603,001 | ) | |||||||||||

Balance as of March 31, 2020 | — | — | 41,324,976 | 4,133 | 61,613,470 | (74,167,779 | ) | (12,550,176 | ) | |||||||||||

Issuance of common stock (RDD & Naia mergers) | — | — | 42,695,948 | 4,270 | 28,749,756 | — | 28,754,026 | |||||||||||||

Issuance of preferred stock and warrants (FN-1) | 382,779 | 38 | — | — | 22,560,956 | — | 22,560,994 | |||||||||||||

Stock issuance costs | — | — | — | — | (3,589,703 | ) | — | (3,589,703 | ) | |||||||||||

Share-based compensation | — | — | — | — | 4,021,000 | — | 4,021,000 | |||||||||||||

Exercise of warrants | — | — | 12,230,418 | 1,223 | 1,217,778 | — | 1,219,001 | |||||||||||||

Inducement expense | — | — | — | — | 6,467,048 | — | 6,467,048 | |||||||||||||

Conversion of convertible debt and accrued interest | — | — | 1,287,696 | 129 | 574,871 | — | 575,000 | |||||||||||||

Beneficial conversion feature | — | — | — | — | 207,632 | — | 207,632 | |||||||||||||

Conversion of preferred stock to common stock | (382,779 | ) | (38 | ) | 38,277,900 | 3,828 | (3,790 | ) | — | — | ||||||||||

Issuance of RSUs | — | — | 415,948 | 42 | (42 | ) | — | — | ||||||||||||

Net loss | — | — | — | — | — | (44,597,536 | ) | (44,597,536 | ) | |||||||||||

Balance as of June 30, 2020 | — | — | 136,232,886 | 13,625 | 121,818,976 | (118,765,315 | ) | 3,067,286 | ||||||||||||

Issuance of common stock | — | — | 3,285,543 | 329 | 2,459,254 | — | 2,459,583 | |||||||||||||

Stock issuance costs | — | — | — | — | (73,149 | ) | — | (73,149 | ) | |||||||||||

Exercise of warrants | — | — | 1,403,100 | 140 | 826,847 | — | 826,987 | |||||||||||||

Conversion of convertible debt and accrued interest | — | — | 8,653,928 | 865 | 3,567,112 | — | 3,567,977 | |||||||||||||

Beneficial conversion feature | — | — | — | — | 1,903,228 | — | 1,903,228 | |||||||||||||

Share-based compensation | — | — | — | — | 202,000 | — | 202,000 | |||||||||||||

Net loss | — | — | — | — | — | (8,333,337 | ) | (8,333,337 | ) | |||||||||||

Balance as of September 30, 2020 | — | $ | — | 149,575,457 | $ | 14,959 | $ | 130,704,268 | $ | (127,098,652 | ) | $ | 3,620,575 | |||||||

See accompanying notes to these condensed consolidated financial statements.

5

Three and Nine Months Ended September 30, 2019 | |||||||||||||||||||

Common Stock Shares | Common Stock Amount | Additional Paid-in Capital | Accumulated Deficit | Total | |||||||||||||||

Balance as of December 31, 2018 | 26,088,820 | $ | 2,609 | $ | 39,854,297 | $ | (43,515,970 | ) | $ | (3,659,064 | ) | ||||||||

Issuance of common stock and warrants | 4,886,782 | 489 | 11,474,766 | — | 11,475,255 | ||||||||||||||

Allocation of warrants to liabilities | — | — | (1,970,000 | ) | — | (1,970,000 | ) | ||||||||||||

Stock issuance costs | — | — | (319,819 | ) | — | (319,819 | ) | ||||||||||||

Share-based compensation | — | — | 526,000 | — | 526,000 | ||||||||||||||

Issuance of RSUs | 90,000 | 9 | (9 | ) | — | — | |||||||||||||

Net loss | — | — | — | (4,434,765 | ) | (4,434,765 | ) | ||||||||||||

Balance as of March 31, 2019 | 31,065,602 | 3,107 | 49,565,235 | (47,950,735 | ) | 1,617,607 | |||||||||||||

Issuance of common stock and warrants | 4,318,272 | 432 | 8,744,069 | — | 8,744,501 | ||||||||||||||

Allocation of warrants to liabilities | — | — | (1,360,000 | ) | — | (1,360,000 | ) | ||||||||||||

Stock issuance costs | — | — | (389,623 | ) | — | (389,623 | ) | ||||||||||||

Exercise of stock options | 100,079 | 10 | 30,054 | — | 30,064 | ||||||||||||||

Issuance of RSUs | 400,000 | 40 | (40 | ) | — | — | |||||||||||||

Share-based compensation | — | — | 852,000 | — | 852,000 | ||||||||||||||

Net loss | — | — | — | (4,488,240 | ) | (4,488,240 | ) | ||||||||||||

Balance as of June 30, 2019 | 35,883,953 | 3,589 | 57,441,695 | (52,438,975 | ) | 5,006,309 | |||||||||||||

Share-based compensation | — | — | 900,000 | — | 900,000 | ||||||||||||||

Net loss | — | — | — | (9,221,232 | ) | (9,221,232 | ) | ||||||||||||

Balance as of September 30, 2019 | 35,883,953 | $ | 3,589 | $ | 58,341,695 | $ | (61,660,207 | ) | $ | (3,314,923 | ) | ||||||||

See accompanying notes to these condensed consolidated financial statements.

6

9 METERS BIOPHARMA, INC.

Unaudited Condensed Consolidated Statements of Cash Flows

Nine Months Ended September 30, | ||||||||

2020 | 2019 | |||||||

Cash flows from operating activities | ||||||||

Net loss | $ | (56,533,874 | ) | $ | (18,144,237 | ) | ||

Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

Share-based compensation | 4,499,000 | 2,278,000 | ||||||

Write-off of deferred offering costs | — | 100,056 | ||||||

Accrued interest on convertible notes | 298,048 | 314,721 | ||||||

Amortization of debt discount | 1,288,098 | 713,709 | ||||||

Beneficial conversion feature | 2,110,860 | — | ||||||

Depreciation | 16,883 | 16,104 | ||||||

Loss on disposal and write-offs of property and equipment | 7,031 | — | ||||||

Change in fair value of derivative liability | (617,000 | ) | (511,000 | ) | ||||

Change in fair value of warrant liability | (2,637,500 | ) | (141,700 | ) | ||||

Warrant inducement expense | 7,157,887 | — | ||||||

Acquired in-process research and development | 28,754,026 | — | ||||||

Extinguishment of derivative liability | — | (370,000 | ) | |||||

Loss on extinguishment of debt | — | 1,049,166 | ||||||

Changes in operating assets and liabilities, net of acquisitions: | ||||||||

Prepaid expenses and other assets | (498,873 | ) | (276,185 | ) | ||||

Accounts payable | (1,388,457 | ) | (708,219 | ) | ||||

Accrued expenses and other liabilities | 4,549,153 | 1,036,898 | ||||||

Accrued interest | 3,427 | (101,624 | ) | |||||

Net cash used in operating activities | (12,991,291 | ) | (14,744,311 | ) | ||||

Cash flows from investing activities | ||||||||

Purchase of property and equipment | (2,543 | ) | (9,475 | ) | ||||

Purchase of in-process research and development, net of assets acquired | (3,184,454 | ) | — | |||||

Net cash used in investing activities | (3,186,997 | ) | (9,475 | ) | ||||

Cash flows from financing activities | ||||||||

Borrowings from convertible notes | 2,500,000 | 5,000,000 | ||||||

Payments of convertible notes | (1,469,804 | ) | (6,745,833 | ) | ||||

Payments of debt issuance costs | (23,000 | ) | (57,000 | ) | ||||

Proceeds from the exercise of stock options | — | 30,064 | ||||||

Proceeds from issuance of common stock and warrants | 2,370,012 | 20,706,919 | ||||||

Proceeds from issuance of preferred stock and warrants | 22,560,994 | — | ||||||

Payment of offering costs | (3,962,852 | ) | (1,045,468 | ) | ||||

Proceeds from exercise of warrants | 2,045,988 | — | ||||||

Net cash provided by financing activities | 24,021,338 | 17,888,682 | ||||||

Net increase in cash and cash equivalents | 7,843,050 | 3,134,896 | ||||||

Cash and cash equivalents as of beginning of period | 4,592,932 | 5,728,900 | ||||||

Cash and cash equivalents as of end of period | $ | 12,435,982 | $ | 8,863,796 | ||||

Supplemental disclosure of cash flow information | ||||||||

Cash paid during the period for interest | $ | 54,578 | $ | 418,927 | ||||

Supplemental disclosure of non-cash financing activities | ||||||||

Conversion of convertible notes and accrued interest to common stock | $ | 4,142,977 | $ | — | ||||

Non-cash issuance of common stock with merger | $ | 28,754,026 | $ | — | ||||

Non-cash addition of derivative liability | $ | 370,000 | $ | 1,281,000 | ||||

Addition of non-cash stock issuance and deferred offering costs | $ | — | $ | 151,137 | ||||

See accompanying notes to these condensed consolidated financial statements.

7

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Business Description

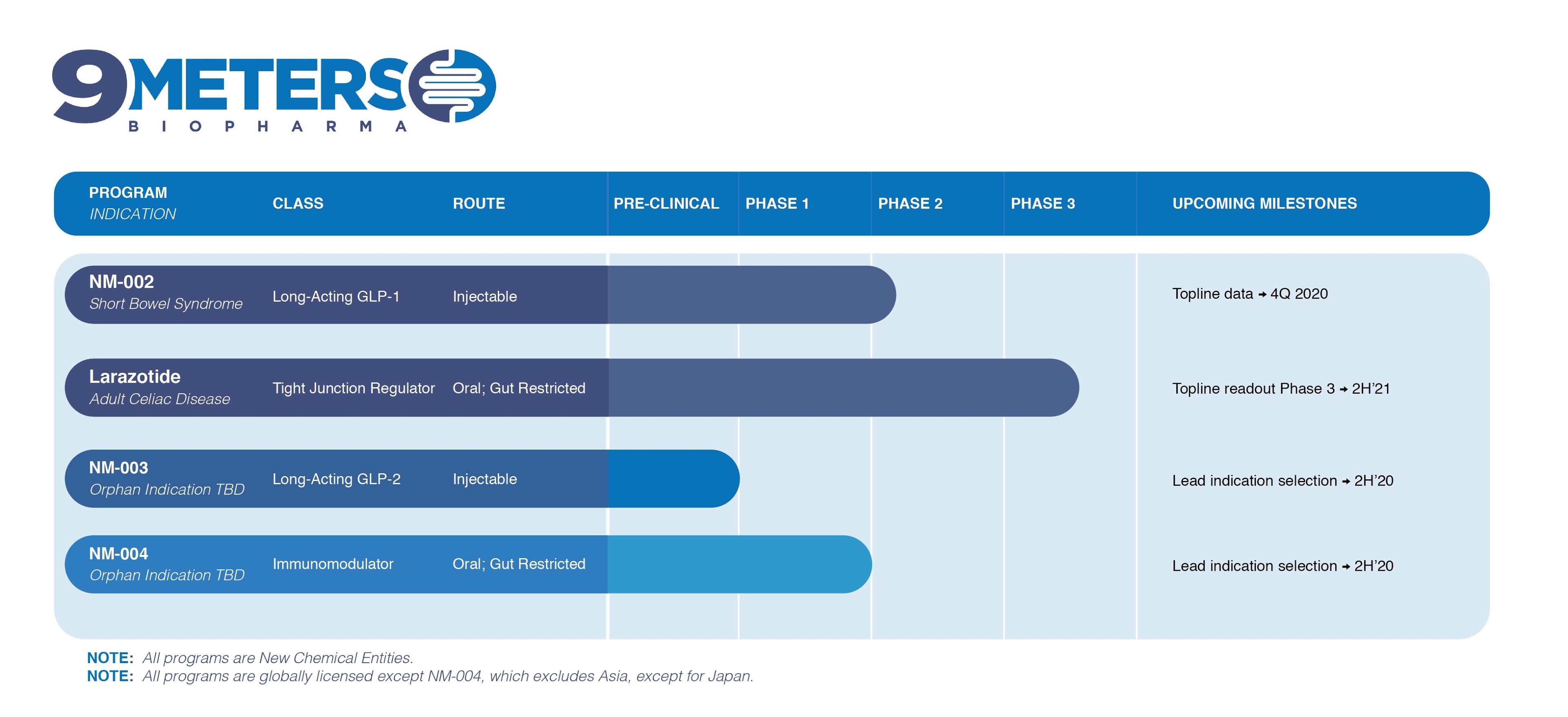

9 Meters Biopharma, Inc. (the “Company”) is a clinical-stage biopharmaceutical company focused on rare and unmet needs in gastroenterology. The Company’s pipeline includes drug candidates for NM-002, a proprietary long-acting GLP-1 agonist for short bowel syndrome (SBS), an orphan designated disease and larazotide, a Phase 3 tight junction regulator being evaluated for celiac disease.

On April 30, 2020, the Company completed its merger with privately-held RDD Pharma, Ltd., an Israel corporation (“RDD”) (the “RDD Merger”) and changed its name from Innovate Biopharmaceuticals, Inc. to 9 Meters Biopharma, Inc.

Basis of Presentation

The unaudited condensed consolidated interim financial statements have been prepared by the Company pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”) for interim financial reporting. These financial statements are unaudited and, in the opinion of management, include all adjustments (consisting of normal recurring adjustments and accruals) necessary for a fair statement of the balance sheets, operating results, and cash flows for the periods presented in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). Operating results for the three and nine months ended September 30, 2020 are not necessarily indicative of the results that may be expected for the fiscal year ending December 31, 2020 or any other future period. Certain information and footnote disclosure normally included in the annual financial statements prepared in accordance with U.S. GAAP have been omitted in accordance with the SEC’s rules and regulations for interim reporting. The Company’s financial position, results of operations and cash flows are presented in U.S. Dollars. These financial statements and related notes should be read in conjunction with the audited financial statements and related notes thereto for the year ended December 31, 2019, included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2019, filed with the SEC on March 20, 2020.

Except as noted below under the section entitled “Recently Issued Accounting Standards—Accounting Pronouncements Adopted,” there have been no material changes to the Company’s significant accounting policies during the three and nine months ended September 30, 2020, as compared to the significant accounting policies disclosed in Note 1 of the Company’s financial statements for the years ended December 31, 2019 and 2018 included in the Company’s Annual Report on Form 10-K. However, the following accounting policies are the most critical in fully understanding the Company’s financial condition and results of operations.

Basis of Consolidation

The accompanying consolidated financial statements reflect the operations of the Company and its wholly owned subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation.

Shelf Registration Filing

On March 15, 2018, the Company filed a shelf registration statement that was declared effective on July 13, 2018 (the “Prior Registration Statement”). The Prior Registration Statement did not include various types of securities as is customary and was set to expire in July 2021. On October 2, 2020, the Company filed a shelf registration statement that was declared effective on October 19, 2020 (the “Current Registration Statement”), so the Prior Registration Statement was terminated effective October 19, 2020. Pursuant to the Current Registration Statement, the Company may from time to time offer, issue and sell in one or more offerings of various types of securities up to an aggregate dollar amount of $200 million.

On July 22, 2020, the Company filed a prospectus supplement and associated sales agreement related to an ATM pursuant to which the Company may sell, from time to time, common stock with an aggregate offering price of up to $40 million through Truist Securities, Inc. (previously SunTrust Robinson Humphrey), or Truist, as sales agent, for general corporate purposes (the “Sales Agreement”). In October 2020, the Company entered into an amendment to the Sales Agreement to reflect the termination of the Prior Registration Statement and effectiveness of the Current Registration Statement. As of September 30, 2020, the Company had sold 3,246,745 shares of common stock pursuant to the Sales Agreement for net proceeds of approximately $2.4 million.

8

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

March 2019 Offering

On March 17, 2019, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with SDS Capital Partners II, LLC and certain other accredited investors, pursuant to which the Company sold, on March 18, 2019, 4,181,068 shares of common stock and issued short-term warrants (the “Short-Term Warrants”) to purchase up to 4,181,068 shares of common stock, and long-term warrants (the “March Long-Term Warrants”) to purchase up to 2,508,634 shares of common stock. Pursuant to the Purchase Agreement, the Company issued the common stock and warrants at a purchase price of $2.33 per unit for aggregate proceeds of approximately $9.7 million.

The March Long-Term Warrants issued were exercisable for five years commencing on the six-month anniversary of March 18, 2019, had an initial exercise price of $2.56 per share, subject to certain adjustments, and had an expiration date of March 18, 2024. The Short-Term Warrants were originally exercisable for a period of one year from March 18, 2019, had an expiration date of March 18, 2020 and had an initial exercise price of $4.00 per share, subject to certain adjustments. The Short-Term Warrants and March Long-Term Warrants were accounted for as warrant liabilities in accordance with Accounting Standards Codification (“ASC”) 480—Distinguishing Liabilities from Equity.

On February 6, 2020, the Company and the holders of the Company’s outstanding Short-Term Warrants amended the Short-Term Warrants to extend the exercise period of each Short-Term Warrant by six months. The Short-Term Warrants, as amended, were exercisable for up to an aggregate of 4,181,068 shares of the Company’s common stock, par value $0.0001 per share, until September 18, 2020. In addition, on February 12, 2020, the Company offered to amend outstanding warrants, including the Short-Term Warrants, to (i) shorten the exercise period to expire concurrently with the closing of the RDD Merger on April 30, 2020 and (ii) reduce the exercise price to $0.10 per share (the “Offer to Amend and Exercise”). All other terms of each Short-Term Warrant remained in full force and effect and were not impacted by this amendment. On April 29, 2020, upon closing of the Offer to Amend and Exercise, the Short-Term Warrants were fully exercised at an exercise price of $0.10 per share.

Additional Issuance of Warrants

On April 25, 2019, the Company entered into an amendment (the “Amendment”) to the Purchase Agreement dated as of March 17, 2019, between the Company and each purchaser party thereto. The Amendment (i) deleted Section 4.12 of the Purchase Agreement, which generally prohibited the Company from issuing, entering into agreements to issue, announcing proposed issuances, selling or granting certain securities between the date of the Purchase Agreement and the date that was 45 days following the closing date thereunder and (ii) gave each purchaser the right to purchase, for $0.125 per underlying share, an additional warrant to purchase shares of the Company’s common stock having an exercise price per share of $2.13 and otherwise having the terms of the March Long-Term Warrants (collectively, the “New Warrants”) pursuant to a securities purchase agreement entered into among the Company and each purchaser that desired to purchase the New Warrants. On May 17, 2019, the Company and each purchaser entered into such Securities Purchase Agreement (the “New Agreement”), and the Company issued New Warrants exercisable for an aggregate of 3,897,010 shares of the Company’s common stock.

The New Warrants were exercisable for five years beginning on the six-month anniversary of the date of issuance until the five-year anniversary of their date of issuance. The New Warrants had an initial exercise price equal to $2.13 per share, subject to certain adjustments. The New Warrants were accounted for as warrant liabilities in accordance with ASC 480—Distinguishing Liabilities from Equity.

Offer to Amend and Exercise

On February 12, 2020, the Company offered to amend certain outstanding warrants in the Offer to Amend and Exercise. The warrants amended included the warrants classified as equity issued in 2018 (the “2018 Equity Warrants”), the outstanding Short-Term Warrants and the outstanding March Long-Term Warrants and the New Warrants. On April 29, 2020, an aggregate of 12,230,418 shares of common stock were tendered, amended and exercised for $0.10 per share for aggregate gross proceeds of approximately $1.2 million. All of the Short-Term Warrants, March Long-Term Warrants and New Warrants were fully exercised at an exercise price of $0.10 per share.

April 2019 Offering

On April 29, 2019, the Company entered into a Securities Purchase Agreement (the “April Purchase Agreement”) with certain institutional and accredited investors providing for the sale by the Company of up to 4,318,272 shares of its common stock at a purchase price of $2.025 per share.

9

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

Pursuant to the April Purchase Agreement, the Company agreed to issue unregistered warrants (the “April Warrants”) to purchase up to 4,318,272 shares of common stock. Subject to certain ownership limitations, the April Warrants were exercisable beginning on the date of their issuance until the five-and-a-half-year anniversary of their date of issuance at an initial exercise price of $2.13 per share. The exercise price of the April Warrants was subject to adjustment for stock splits, reverse splits, and similar capital transactions as described in the April Warrants.

The net proceeds from the offering and the private placement were approximately $7.9 million, after deducting commissions and estimated offering costs. The Company granted the placement agent warrants to purchase up to 215,914 shares of common stock (the “Placement Agent Warrants”). The Placement Agent Warrants had substantially the same terms as the April Warrants, except that the Placement Agent Warrants had an exercise price of $2.53 per share and had a term of 5 years from the effective date of the offering. The Company also paid the placement agent a reimbursement for non-accountable expenses in the amount of $35,000 and a reimbursement for legal fees and expenses of the placement agent in the amount of $25,000. On December 19, 2019, the Company and each of the purchasers of the April Warrants and Placement Agent Warrants (collectively, the “Exchange Warrants”) entered into separate exchange agreements (the “Exchange Agreement”), pursuant to which the Company agreed to issue to the purchasers an aggregate of 5,441,023 shares of the Company’s common stock (the “Exchange Shares”), at a ratio of 1.2 Exchange Shares for each purchaser warrant in exchange for the cancellation and termination of all of the outstanding Exchange Warrants. See “Fair Value of Financial Instruments” below for additional details.

RDD Merger Financing

On April 29, 2020, the Company entered into a securities purchase agreement with various accredited investors pursuant to which the Company agreed to issue and sell to the investors units (“Units”) consisting of (i) one share of Series A Convertible Preferred Stock (the "Series A Preferred Stock") and (ii) one five-year warrant (the "Preferred Warrants") to purchase one share of Series A Preferred Stock (the "RDD Merger Financing"). On May 4, 2020, the Company closed the RDD Merger Financing and the Company sold an aggregate of (i) 382,779 shares of Series A Preferred Stock, par value $0.0001 per share, which converted into 38,277,900 shares of common stock on June 30, 2020, upon receipt of approval by the Company’s stockholders (the “Automatic Conversion”), and (ii) Preferred Warrants to purchase up to 382,779 shares of Series A Preferred Stock, which following the Automatic Conversion became exercisable for 38,277,900 shares of common stock. The exercise price of the Preferred Warrants was $58.94 per share of Series A Preferred Stock, and following the Automatic Conversion, became $0.5894 per share of common stock, subject to adjustments as provided under the terms of the Preferred Warrants. In addition, broker warrants covering 8,112 Units and broker warrants covering 10,899 shares of Series A Preferred Stock, which following the Automatic Conversion became exercisable for 2,712,300 shares of common stock, were issued in connection with the RDD Merger Financing. Gross proceeds from the RDD Merger Financing were approximately $22.6 million with net proceeds of approximately $19.2 million after deducting commissions and estimated offering costs. See Note 3—Merger & Acquisition for additional details.

Business Risks

The Company faces risks, including those associated with biopharmaceutical companies whose products are in various stages of development. These risks include, among others, risks related to the potential effects of the ongoing coronavirus outbreak and related mitigation efforts on the Company's clinical, financial and operational activities, the Company’s need for additional financing to achieve key development milestones, the need to defend intellectual property rights, and the dependence on key members of management. See Note 2—Liquidity and Going Concern for further discussion of the risks related to the coronavirus outbreak.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and disclosures made in the accompanying notes to the financial statements. Areas of the financial statements where estimates may have the most significant effect include accrued expenses, share-based compensation, valuation of the derivative liability and warrant liabilities, valuation allowance for income tax assets, management’s estimate of the acquisition costs associated with acquired in-process research and development and management’s assessment of the Company’s ability to continue as a going concern. Changes in the facts or circumstances underlying these estimates could result in material changes and actual results could differ from these estimates.

Accrued Expenses

The Company incurs periodic expenses such as research and development, licensing fees, salaries and benefits, and professional fees. The Company is required to estimate its expenses resulting from obligations under contracts with clinical research organizations, vendors and consulting agreements that have been incurred by the Company prior to being invoiced. This process

10

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

involves reviewing quotations and contracts, identifying services that have been performed on the Company’s behalf and estimating the level of service performed and the associated cost incurred for the service when the Company has not yet been invoiced or otherwise notified of the actual cost. The majority of the Company’s service providers invoice monthly in arrears for services performed or when contractual milestones are met. The Company estimates accrued expenses as of each balance sheet date based on facts and circumstances known at that time.

Accrued expenses consisted of the following:

September 30, 2020 (Unaudited) | December 31, 2019 | |||||||

Accrued compensation and benefits | $ | 1,210,927 | $ | 574,332 | ||||

Accrued clinical expenses | 4,591,044 | 4,143,269 | ||||||

Other accrued expenses | 265,246 | 30,150 | ||||||

Total | $ | 6,067,217 | $ | 4,747,751 | ||||

Derivative Liability

The Company accounts for derivative instruments in accordance with ASC 815, Derivative and Hedging, which establishes accounting and reporting standards for derivative instruments, including certain derivative instruments embedded in other financial instruments or contracts and requires recognition of all derivatives on the condensed consolidated balance sheet at fair value. The Company’s derivative financial instruments consist of embedded options in the Company’s convertible notes. The embedded derivatives include provisions that provide the noteholder with certain conversion and put rights at various conversion or redemption values as well as certain call options for the Company. See Note 4—Debt for further details.

Classification of Warrants

The Company accounts for warrants in accordance with ASC 480, Distinguishing Liabilities from Equity and ASC 815, Derivatives and Hedging, to determine whether the warrants should be classified as equity or liability. The warrants the Company issued during 2019 are freestanding financial instruments that contain net settlement options and may require the Company to settle these warrants in cash under certain circumstances. As such, the Company has classified these warrants as liabilities on the accompanying condensed consolidated balance sheets. The warrant liabilities were initially recorded at fair value on the date of issuance and were subsequently re-measured to fair value at each balance sheet date until the warrant liabilities were exercised. Changes in the fair value of the warrants are recognized as a non-cash component of other income and expense in the accompanying condensed consolidated statements of operations and comprehensive loss. All of the warrants accounted for as warrant liabilities have been exercised or settled as of September 30, 2020.

On May 4, 2020, the Company issued the Preferred Warrants, which are freestanding financial instruments that give the warrant holder the right but not the obligation to purchase the equity security at the warrant exercise price. The Company is not required to settle these warrants in cash and as such, the Company has classified these warrants as equity on the accompanying condensed consolidated balance sheets.

Research and Development

Research and development expenses consist of costs incurred to further the Company’s research and development activities and include salaries and related employee benefits, manufacturing of pharmaceutical active ingredients and drug products, costs associated with clinical trials, nonclinical activities, regulatory activities, research-related overhead expenses and fees paid to expert consultants, external service providers and contract research organizations which conduct certain research and development activities on behalf of the Company. Costs incurred in the research and development of products are charged to research and development expense as incurred.

Costs for preclinical studies and clinical trial activities are recognized based on an evaluation of the vendors’ progress towards completion of specific tasks, using data such as patient enrollment, clinical site activations or information provided by vendors regarding their actual costs incurred. Payments for these activities are based on the terms of individual contracts and payment timing may differ significantly from the period in which the services were performed. The Company determines accrual estimates through reports from and discussions with applicable personnel and outside service providers as to the progress or state of completion of trials, or the services completed. The estimates of accrued expenses as of each balance sheet date are based on the facts and circumstances known at the time. Although the Company does not expect its estimates to be materially different from amounts

11

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

incurred, the Company’s estimates and assumptions for clinical trial costs could differ significantly from actual costs incurred, which could result in increases or decreases in research and development expenses in future periods when actual results are known.

Nonrefundable advance payments for goods and services that will be used in future research and development activities are expensed when the goods have been received or when the activity is performed, rather than when payment is made.

Acquired In-process Research and Development

The Company has acquired, and may in the future acquire, rights to develop and commercialize new drug candidates and/or other in-process research and development assets. The up-front acquisition payments, as well as future milestone payments that are deemed probable to achieve and do not meet the definition of a derivative, are expensed as acquired in-process research and development provided that the drug has not achieved regulatory approval for marketing, and, absent obtaining such approval, have no alternative future use.

Share-Based Compensation

The Company recognizes share-based compensation expense for grants of stock options based on the grant-date fair value of those awards using the Black-Scholes option-pricing model. Share-based compensation expense is generally recognized on a straight-line basis over the requisite service period for awards expected to vest.

Share-based compensation expense includes an estimate, which is made at the time of grant, of the number of awards that are expected to be forfeited. This estimate is revised, if necessary, in subsequent periods if actual forfeitures differ from those estimates. Under the Black-Scholes option-pricing model, fair value is calculated based on assumptions with respect to:

• | Expected dividend yield. The expected dividend yield is assumed to be zero as the Company has never paid dividends and has no current plans to pay any dividends on the Company’s common stock. |

• | Expected stock-price volatility. Due to limited trading history as a public company, the expected volatility is derived from the average historical volatilities of publicly traded companies within the Company’s industry that the Company considers to be comparable to the Company’s business over a period approximately equal to the expected term. In evaluating comparable companies, the Company considers factors such as industry, stage of life cycle, financial leverage, size and risk profile. |

• | Risk-free interest rate. The risk-free interest rate is based on the U.S. Treasury yield in effect at the time of grant for zero coupon U.S. Treasury notes with maturities approximately equal to the expected term. |

• | Expected term. The expected term represents the period that the stock-based awards are expected to be outstanding. Due to limited history of stock option exercises, the Company estimates the expected term of employee stock options based on the simplified method, which calculates the expected term as the average of the time-to-vesting and the contractual life of the options. Pursuant to Accounting Standards Update (“ASU”) 2018-07, the Company has elected to use the contractual life of the option as the expected term for non-employee options. |

Periodically, the Board may approve the grant of restricted stock units (“RSUs”) pursuant to the Company’s 2012 Omnibus Incentive Plan, as amended, which represent the right to receive shares of the Company’s common stock based on terms of the agreement. The fair value of RSUs is recognized as share-based compensation expense generally on a straight-line basis over the service period, net of estimated forfeitures. The grant date fair value of an RSU represents the closing price of the Company’s common stock on the date of grant.

Fair Value of Financial Instruments

Fair value is defined as the price that would be received for sale of an asset or paid for transfer of a liability, in an orderly transaction between market participants at the measurement date. U.S. GAAP establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). Financial instruments recorded in the accompanying condensed consolidated balance sheets are categorized based on the inputs to valuation techniques as follows:

•Level 1 - defined as observable inputs based on unadjusted quoted prices for identical instruments in active markets;

12

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

•Level 2 - defined as inputs other than Level 1 that are either directly or indirectly observable in the marketplace for identical or similar instruments in markets that are not active; and

•Level 3 - defined as unobservable inputs in which little or no market data exists where valuations are derived from techniques in which one or more significant inputs are unobservable.

The fair value of the embedded derivative issued in connection with the Unsecured Convertible Note and the Additional Note, further described in Note 4—Debt, was determined by using a Monte Carlo simulation technique (“MCS”) to value the embedded derivative associated with each note. As part of the MCS valuation, a discounted cash flow (“DCF”) model is used to value the debt on a stand-alone basis and determine the discount rate to utilize in both the DCF and MCS models. The significant estimates used in the DCF model include the time to maturity of the convertible debt and calculated discount rate, which includes an estimate of the Company’s specific risk premium. The MCS methodology calculates the theoretical value of an option based on certain parameters, including: (i) the threshold of exercising the option, (ii) the price of the underlying security, (iii) the time to expiration, or expected term, (iv) the expected volatility of the underlying security, (v) the risk-free rate and (vi) the number of paths.

These valuation techniques involve management’s estimates and judgment based on unobservable inputs and are classified in Level 3. The table below summarizes the valuation inputs into the MCS model for the derivative liability associated with the Unsecured Convertible Note and the Additional Convertible Note on their respective dates of issuance as of March 8, 2019 and January 10, 2020, respectively, and at the end of the period as of September 30, 2020.

Derivative Liability | ||||

September 30, | January 10, | March 8, | ||

2020 | 2020 | 2019 | ||

Discount rate | 21.8% | 21.6% | 29.3% | |

Expected stock price volatility | 83.3% | 103.9% | 101.1% | |

Risk-free interest rate | 0.1% | 1.6% | 2.5% | |

Expected term | 1.3 years | 2 years | 2 years | |

Price of the underlying common stock | $0.82 | $0.65 | $1.99 | |

The fair values of the warrants at their respective dates of issuance further described above in the sections entitled “March 2019 Offering,” “Additional Issuance of Warrants,” and “April 2019 Offering” were determined through the use of an MCS model. The MCS methodology calculates the theoretical value of an option based on certain parameters, including (i) the threshold of exercising the option, (ii) the price of the underlying security, (iii) the time to expiration, or expected term, (iv) the expected volatility of the underlying security, (v) the risk-free interest rate and (vi) the number of paths. Given the high level of the selected volatilities, the methodology selected simulates the Company’s market value of invested capital (“MVIC”) through the maturity date of the respective warrants (ranging from one year to five-and-a-half years). Further, the estimated future stock price of the Company is calculated by subtracting the debt plus accrued interest from the MVIC. The significant estimates used in the MCS model include management’s estimated probability of future financing and liquidation events.

Upon a fundamental transaction (as defined in the applicable warrant agreement), each holder of Short-Term Warrants and each holder of the March Long-Term Warrants and New Warrants (collectively, the “Long-Term Warrants”) can elect to require the Company or a successor entity to purchase such holder’s outstanding, unexercised warrants for a cash payment (or under certain circumstances other consideration) equal to the Black-Scholes value of the warrants on the date of consummation of the fundamental transaction, calculated in accordance with the terms and using the assumptions specified in the applicable warrant agreement. Due to the RDD Merger, the Company entered into the Exchange Agreements with the holders of the Exchange Warrants, pursuant to which the Company agreed to issue the purchasers an aggregate of 5,441,023 shares in exchange for the cancellation and termination of the Exchange Warrants. On December 26, 2019, an aggregate of 2,994,762 warrants were exchanged for 3,593,714 shares of the Company’s common stock. During the nine months ended September 30, 2020, 1,539,424 warrants were exchanged for 1,847,309 shares of the Company’s common stock. In addition, the Company amended the Short-Term Warrants and Long-Term Warrants in the Offer to Amend in Exercise on February 12, 2020. Management assumed that the holders of the Short-Term Warrants and Long-Term Warrants would elect to receive cash payments under the respective warrant agreements following completion of the RDD Merger. As such, the Company determined the fair value of the Short-Term Warrants and Long-Term Warrants immediately prior to the Offer to Amend and Exercise, for financial reporting purposes, through the use of the Black-Scholes model. Subsequent to the Offer to Amend and Exercise, the Company determined the fair value of the Short-Term Warrants and Long-Term Warrants using the reduced exercise price of $0.10 as of April 28, 2020. The estimates underlying the

13

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

assumptions used in both the MCS model and Black-Scholes model are subject to risks and uncertainties and may change over time, and the assumptions used in both the MCS model and the Black-Scholes model for financial reporting purposes generally differ from the assumptions that would be applied in determining a payout under the applicable warrant agreements. These valuation techniques involve management’s estimates and judgment based on unobservable inputs and are classified in Level 3.

The Company recognized a gain in fair value of the Short-Term Warrants and Long-Term Warrants of approximately $2.6 million during the nine months ended September 30, 2020, and $2.5 million and $0.1 million during the three and nine months ended September 30, 2019, respectively. All of the Short-Term Warrants and Long-Term Warrants were exercised in the Offer to Amend and Exercise, which closed on April 29, 2020. During the nine months ended September 30, 2020, the Company recognized warrant inducement expense of approximately $7.2 million. There was no warrant inducement expense recognized during the three months ended September 30, 2020 or the three and nine months ended September 30, 2019. The warrant inducement expense represents the accounting fair value of consideration issued to induce conversion of the Exchange Warrants and exercise of the warrants in the Offer to Amend and Exercise.

The table below summarizes the valuation inputs into the MCS model for the Short-Term Warrants and Long-Term Warrants at their respective dates of issuance.

Short-Term Warrants | Long-Term Warrants | ||

March 18, 2019 | March 18, 2019 | May 17, 2019 | |

Conversion price | $4.00 | $2.56 | $2.13 |

Expected stock price volatility | 122.0% | 85.2% | 83.4% |

Risk-free interest rate | 2.5% | 2.2% | 2.2% |

Expected term | 1 year | 5 years | 5 years |

Price of the underlying common stock | $2.48 | $2.48 | $1.58 |

The table below summarizes the range of valuation inputs into the Black-Scholes model for the Exchange Warrants on their date of issuance and immediately prior to the exchange.

Exchange Warrants | ||

May 1, 2019 | January 6, 2020 | |

Conversion price | $ 2.13 - $ 2.53 | $2.13 |

Expected stock price volatility | 84.1% | 87.3% |

Risk-free interest rate | 2.2% | 1.7% |

Expected term | 5 - 5.5 years | 4.9 years |

Price of the underlying common stock | $1.54 | $0.58 |

The table below summarizes the range of valuation inputs into the Black-Scholes model for the warrant liabilities as of February 11, 2020, immediately prior to the reduction in exercise price pursuant to the Offer to Amend and Exercise.

Short-Term Warrants | Long-Term Warrants | |||||

February 11, 2020 | ||||||

Conversion price | $ | 4.00 | $2.13 - $2.56 | |||

Expected stock price volatility | 97.1 | % | 87.9% - 89.2% | |||

Risk-free interest rate | 1.6 | % | 1.7 | % | ||

Expected term | 7 months | 4 years 2 months | ||||

Price of the underlying common stock | $ | 0.79 | $ | 0.79 | ||

14

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

The following table summarizes the fair value hierarchy of financial liabilities measured at fair value as of September 30, 2020 and December 31, 2019, respectively.

September 30, 2020 | ||||||||||||

Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | |||||||||

Derivative liability | $ | — | $ | — | $ | 161,000 | $ | 161,000 | ||||

Warrant liabilities | — | — | — | — | ||||||||

Total liabilities at fair value | $ | — | $ | — | $ | 161,000 | $ | 161,000 | ||||

December 31, 2019 | ||||||||||||

Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | |||||||||

Derivative liability | $ | — | $ | — | $ | 408,000 | $ | 408,000 | ||||

Warrant liabilities | — | — | 2,637,500 | 2,637,500 | ||||||||

Total liabilities at fair value | $ | — | $ | — | $ | 3,045,500 | $ | 3,045,500 | ||||

The following table summarizes the changes in fair value of the derivative liability and warrant liabilities classified in Level 3. Gains and losses reported in this table include changes in fair value that are attributable to unobservable inputs.

Nine Months Ended September 30, 2020 | |||

Beginning balance as of December 31, 2019 | $ | 3,045,500 | |

Issuance of derivative liability (the Additional Note) | 370,000 | ||

Exchange of the April Warrants | (380,600 | ) | |

Change in fair value of warrant liabilities | (1,198,200 | ) | |

Change in fair value of derivative liability | (617,000 | ) | |

Exercise of the Short-Term Warrants and Long-Term Warrants | (1,058,700 | ) | |

Ending balance as of September 30, 2020 | $ | 161,000 | |

The amount of total gain for the period included in earnings attributable to the change in unrealized gains relating to the fair value liabilities still held at the end of the period | $ | 617,000 | |

The cumulative unrealized gain relating to the change in fair value of the derivative liability and warrant liabilities of $1,815,200, the gain on exercise of the warrants in the Offer to Amend and Exercise of $1,058,700 and the gain on exchange of the April Warrants of $380,600 for the nine months ended September 30, 2020 is included in other income (expense) in the condensed consolidated statements of operations and comprehensive loss.

ASC 820, Fair Value Measurement and Disclosures requires all entities to disclose the fair value of financial instruments, both assets and liabilities, for which it is practicable to estimate fair value. As of September 30, 2020 and December 31, 2019, the recorded values of cash and cash equivalents, restricted deposit, accounts payable, accrued expenses and convertible promissory notes approximated their fair values due to the short-term nature of the instruments.

15

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

Deferred Offering Costs

Deferred offering costs consist principally of legal, accounting and underwriters’ fees related to offerings or the Company’s shelf registration statement. Offering costs incurred prior to an offering are initially capitalized and then subsequently reclassified to additional paid-in capital upon completion of the offering. Deferred offering costs associated with the shelf registration statement will be charged to additional paid-in capital on a pro-rata basis in the event the Company completes an offering under the shelf registration statement.

Patent Costs

Costs associated with the submission of patent applications are expensed as incurred given the uncertainty of the future economic benefits of the patents. Patent and patent related legal and administrative costs included in general and administrative expenses were approximately $108,000 and $103,000 for the three months ended September 30, 2020 and 2019, respectively, and $300,000 and $390,000 for the nine months ended September 30, 2020 and 2019, respectively.

Net Loss Per Share

The Company calculates net loss per share as a measurement of the Company’s performance while giving effect to all potentially dilutive shares that were outstanding during the reporting period. Because the Company had a net loss for all periods presented, the inclusion of common stock options or other similar instruments would be anti-dilutive. Therefore, the weighted average shares outstanding used to calculate both basic and diluted net loss per share are the same. For the three and nine months ended September 30, 2020 and 2019, 57.1 million and 25.6 million potentially dilutive securities related to warrants and stock options issued and outstanding have been excluded from the computation of diluted weighted average shares outstanding because the effect would be anti-dilutive. The potentially dilutive securities consisted of the following:

Nine Months Ended September 30, | |||||||

2020 | 2019 | ||||||

Options outstanding under the Private Innovate Plan | 6,028,781 | 6,240,792 | |||||

Options outstanding under the Omnibus Plan | 10,524,626 | 2,295,921 | |||||

Options outstanding under the Option Grant Agreements granted to RDD Employees | 1,014,173 | — | |||||

Warrants issued at a weighted-average exercise price of $55.31 | 154,403 | 154,403 | |||||

Warrants issued at an exercise price of $2.54 | 2,233 | 349,555 | |||||

Warrants issued at an exercise price of $3.18 | 113,980 | 1,410,358 | |||||

Warrants issued at an exercise price of $0.5894 | 39,275,900 | — | |||||

Short-term warrants issued at an exercise price of $4.00 | — | 4,181,068 | |||||

Long-term warrants issued at a weighted-average exercise price of $2.24 | — | 10,939,830 | |||||

Total | 57,114,096 | 25,571,927 | |||||

Segments

Operating segments are defined as components of an enterprise engaging in business activities for which discrete financial information is available and regularly reviewed by the chief operating decision maker in deciding how to allocate resources and in assessing performance. The Company operates and manages its business as one operating segment and the Company’s primary operations are in North America.

16

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

Recently Issued Accounting Standards

Accounting Pronouncements Adopted

In August 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework - Changes to the Disclosure Requirements for Fair Value Measurement. This standard no longer requires public companies to disclose transfers between Level 1 and 2 of the fair value hierarchy and adds additional disclosure requirements about the range and weighted average used to develop significant unobservable inputs for Level 3 fair value measurements. The Company adopted this guidance effective January 1, 2020 and the adoption of ASU 2018-13 did not have a material impact on the Company’s consolidated financial statements.

Accounting Pronouncements being Evaluated

In December 2019, the FASB issued ASU 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes. ASU 2019-12 amends the accounting for income taxes by removing certain exceptions to the general principles in Topic 740 and improves consistent application of other areas of Topic 740 by clarifying and amending existing guidance. ASU 2019-12 is effective for fiscal years and interim periods within those fiscal years beginning after December 15, 2020. Early adoption is permitted and the Company is currently evaluating the impact this standard will have on the Company’s consolidated financial statements.

In August 2020, the FASB issued ASU 2020-06, Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity, which simplifies the accounting for certain financial instruments with characteristics of liabilities and equity, including convertible instruments and contracts in an entity’s own equity. Among other changes, ASU 2020-06 removes from U.S. GAAP the liability and equity separation model for convertible instruments with a cash conversion feature, and as a result, after adoption, entities will no longer separately present in equity an embedded conversion feature for such debt. ASU 2020-06 also enhances transparency and improves disclosures for convertible instruments and earnings per share guidance. ASU 2020-06 is effective for fiscal years beginning after December 15, 2021, with early adoption permitted for fiscal years beginning after December 15, 2020. The Company is currently evaluating the impact this standard will have on the Company’s consolidated financial statements.

NOTE 2: LIQUIDITY AND GOING CONCERN

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern, which contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. Although, the Company received gross proceeds of approximately $22.6 million upon completion of the RDD Merger Financing, as well as approximately $4.3 million in combined proceeds from the exercise of warrants and issuance of common stock under the Sales Agreement, each further described in Note 1—Summary of Significant Accounting Policies, the Company expects to incur substantial losses in the future as it conducts planned operating activities. Based on the Company’s limited operating history, recurring negative cash flows from operations, current plans and available resources, the Company will need substantial additional funding to support its planned and future operating activities, including progression of research and development programs. The Company has concluded that the prevailing conditions and ongoing liquidity risks faced by the Company raise substantial doubt about the Company’s ability to continue as a going concern for at least 1 year following the date these financial statements are issued.

The effect of the COVID-19 pandemic and its associated restrictions may increase the anticipated aggregate costs for the development of the Company's product candidates and may adversely impact the anticipated timelines for the development of the Company's product candidates by, among other things, causing disruptions in the supply chain for clinical supplies, delays in the timing and pace of subject enrollment in clinical trials and lower than anticipated subject enrollment and completion rates, delays in the review and approval of the Company’s regulatory submissions by the FDA and other agencies with respect to the Company's product candidates, and other unforeseen disruptions. The economic impact of the COVID-19 pandemic and its effect on capital markets and investor sentiment may adversely impact the Company's ability to raise capital when needed or on terms favorable to the Company and its stockholders to fund its development programs and operations. The Company does not yet know the full extent of potential delays or impacts on its business, clinical trial activities, ability to access capital or on healthcare systems or the global economy as a whole. However, these effects could have a material adverse impact on the Company's business and financial condition.

There can be no assurance that the Company will be able to obtain additional capital on terms acceptable to the Company, on a timely basis or at all. The failure to obtain sufficient additional funding or enter into strategic partnerships could adversely affect the Company’s ability to achieve its business objectives and product development timelines and could have a material adverse effect on the Company’s results of operations. The accompanying condensed consolidated financial statements do not include any adjustments that might be necessary should the Company be unable to continue as a going concern.

17

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

NOTE 3: MERGER AND ACQUISITION

RDD Merger

On April 30, 2020, the Company completed its merger with RDD. Upon closing of the RDD Merger, the Company issued the RDD shareholders upfront consideration consisting of 37,860,510 shares of the Company’s common stock. In addition, the Company assumed 1,014,173 options that had been previously issued to RDD employees. See Note 7—Share-based Compensation for additional details regarding the options assumed.

Naia Acquisition

On May 6, 2020, the Company consummated its merger with Naia Rare Diseases, Inc. in accordance with the terms of an Agreement and Plan of Merger (the “Naia Acquisition”). The consideration for the Naia Acquisition at closing consisted of $2.1 million in cash and 4,835,438 shares of common stock, plus the pre-payment of certain operating costs on behalf of Naia totaling $0.1 million. Consideration for the Naia Acquisition also included future development and sales milestone payments worth up to $80.4 million and royalties on net sales of certain products to which Naia has exclusive rights by license.

Accounting Treatment

Both the RDD Merger and the Naia Acquisition were accounted for as asset acquisitions under ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business. The net tangible and intangible assets acquired, and liabilities assumed in connection with the transactions were recorded at their estimated fair values on the respective dates of acquisition. The excess of purchase price over fair value of identified assets acquired and liabilities assumed was expensed as in-process research and development. The Company acquired the RDD net assets for shares of the Company’s common stock valued at $26.6 million and assumed liabilities of $1.3 million. The net assets received were less than $0.1 million. The Company acquired the Naia technology for $2.1 million in cash, common stock valued at $2.2 million, excluding contingent consideration, and the pre-payment of certain operating costs on behalf of Naia totaling $0.1 million. No contingent consideration associated with the Naia Acquisition was recorded at the time of acquisition because the related development and sales milestones were not deemed probable. As a result of the RDD Merger and the Naia Acquisition, approximately $32.3 million was expensed as acquired in-process research and development expense in the accompanying condensed consolidated statements of operations and comprehensive loss for the nine months ended September 30, 2020.

NOTE 4: DEBT

Senior Convertible Note

The principal amount of the senior convertible note issued on October 4, 2018 (the “Senior Convertible Note”), was $5.2 million and bore interest at a rate of eight percent (8%) per annum payable quarterly in cash, with a scheduled maturity date of October 4, 2020. The interest rate would automatically increase to 18% per annum if there was an event of default during the period.

During January 2019, the noteholder issued a redemption notice to the Company requiring the Company to repay the noteholder $1,049,167 of principal and $1,399 of accrued interest. On January 7, 2019, the Company entered into an Option to Purchase Senior Convertible Note (the “Option Agreement”) with the noteholder. The Company paid the noteholder $250,000 in consideration for the noteholder entering into the Option Agreement with the Company, which was recorded as interest expense in the accompanying statements of operations and comprehensive loss. The Option Agreement provided the Company with the ability to repay (purchase) the outstanding principal and accrued interest of the Senior Convertible Note any time from January 7, 2019 until March 31, 2019 (“Option Period”).

During March 2019, the Company exercised its repurchase rights under the Option Agreement and paid the noteholder of the Senior Convertible Note approximately $5,200,000 in principal and $60,000 in interest, which was the full purchase amount of the Senior Convertible Note pursuant to the terms of the Option Agreement. There are no further amounts outstanding under the Senior Convertible Note and the Senior Convertible Note has been canceled. The Company accounted for the repayment of the Senior Convertible Note as a liability extinguishment in accordance with ASC 405, Extinguishments of Liabilities, which resulted in the Company recording a loss on extinguishment of debt of approximately $1.0 million in the accompanying statements of operations and comprehensive loss for the nine months ended September 30, 2019.

18

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

Unsecured Convertible Promissory Note

On March 8, 2019, the Company entered into a Securities Purchase Agreement (the “Note Purchase Agreement”) with a purchaser (the “Convertible Noteholder”). Pursuant to the Note Purchase Agreement, the Company issued the Convertible Noteholder an unsecured Convertible Promissory Note (the “Unsecured Convertible Note”) in the principal amount of $5.5 million. The Convertible Noteholder had the right to elect to convert all or a portion of the Unsecured Convertible Note at any time and from time to time into the Company’s common stock at a conversion price of $3.25 per share, subject to adjustment for stock splits, dividends, combinations and similar events. The Company had the right to prepay all or a portion of the Unsecured Convertible Note at any time for an amount equal to 115% of then outstanding obligations or the portion of the obligations the Company is prepaying. The purchase price of the Unsecured Convertible Note was $5.0 million, and the Unsecured Convertible Note carried an original issuance discount (“OID”) of $0.5 million, which was included in the principal amount of the Unsecured Convertible Note. In addition, the Company agreed to pay $20,000 of transaction expenses, which were netted out of the purchase price of the Unsecured Convertible Note. The Company also incurred additional transaction costs of approximately $37,000, which were recorded as debt issuance costs. As a result of the redemption features of the Unsecured Convertible Note, further described below, the Company amortized the debt issuance costs and accreted the OID to interest expense over the estimated redemption period of 15 months, using the effective interest method.

The various conversion and redemption features contained in the Unsecured Convertible Note were embedded derivative instruments, which were recorded as a debt discount and derivative liability at the issuance date at their estimated fair value of $1.3 million. Amortization of debt discount and accretion of the OID for the Unsecured Convertible Note recorded as interest expense was approximately $0.8 million for the nine months ended September 30, 2020, and $0.3 million and $0.7 million for the three and nine months ended September 30, 2019, respectively. The Unsecured Convertible Note was fully accreted as of June 30, 2020.

The Unsecured Convertible Note bore interest at the rate of 10% (which would have increased to 18% upon and during the continuance of an event of default) per annum, compounding on a daily basis. All principal and accrued interest on the Unsecured Convertible Note was due on the second-year anniversary of the Unsecured Convertible Note’s issuance. During the nine months ended September 30, 2020, the Company made principal payments of $4.1 million on the Unsecured Convertible Note, consisting of $1.5 million in cash payments and $2.6 million in stock conversions. During the nine months ended September 30, 2019, the Company made principal payments in cash of $0.5 million. During the nine months ended September 30, 2020, the remaining principal of $2.6 million and accrued interest of $0.1 million were converted into 6,583,143 shares of the Company’s common stock at a weighted-average conversion price of $0.42, which reflected a discount of approximately 38% (the “Conversion Discount”). The Conversion Discount represented a beneficial conversion feature of approximately $1.4 million which was recorded as a charge to interest expense and a credit to additional paid-in capital in the accompanying condensed consolidated financial statements. The Unsecured Convertible Note was deemed paid in full as of September 30, 2020.

Standstill Agreement

On April 3, 2020, the Company entered into a standstill agreement with the Convertible Noteholder (the “Standstill Agreement”). Pursuant to the Standstill Agreement, the Convertible Noteholder would not seek to redeem any portion of the Unsecured Convertible Note between April 1, 2020 and May 31, 2020. The outstanding balance of the Unsecured Convertible Note was increased by $150,000 on April 3, 2020 as consideration for the Standstill Agreement and was recorded as interest expense during the nine months ended September 30, 2020. All other terms of the Unsecured Convertible Note remained in full force and effect.

Additional Note

On January 10, 2020, the Company entered into an additional securities purchase agreement and unsecured convertible promissory note with the Convertible Noteholder in the principal amount of $2,750,000 (the “Additional Note”). The Convertible Noteholder may elect to convert all or a portion of the Additional Note, at any time from time to time into the Company’s common stock at a conversion price of $3.25 per share, subject to adjustment for stock splits, dividends, combinations and similar events. The Company may prepay all or a portion of the Additional Note at any time for an amount equal to 115% of then outstanding obligations or the portion of the obligations we are prepaying. The purchase price of the Additional Note was $2.5 million and carries an original issuance discount of $250,000, which is included in the principal amount of the Additional Note.

The various conversion and redemption features contained in the Additional Note are embedded derivative instruments, which were recorded as a debt discount and derivative liability at the issuance date at their estimated fair value of $0.4 million. Amortization of debt discount and accretion of the OID for the Additional Note recorded as interest expense was approximately $0.1 million and $0.4 million for the three and nine months ended September 30, 2020.

19

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

The Additional Note bears interest at the rate of 10% (which will increase to 18% upon and during the continuance of an event of default) per annum, compounding on a daily basis. All principal and accrued interest on the Additional Note is due on the second anniversary of the date of the Additional Note’s issuance. During the nine months ended September 30, 2020, the Company made principal payments on the Additional Note of approximately $1.2 million and interest of $0.2 million through conversions into 3,358,481 shares of the Company’s common stock at a weighted-average conversion price of $0.42, which reflected a discount of approximately 36%. The conversion discount represented a beneficial conversion feature of approximately $0.8 million which was recorded as a charge to interest expense and a credit to additional paid-in capital in the accompanying condensed consolidated financial statements.

At any time after the six-month anniversary of the issuance of the Additional Note, (i) if the average VWAP of the Company’s common stock over twenty trading dates exceeds $10.00 per share, the Company may generally require that the Additional Note convert into share of its common stock at the $3.25 (as adjusted) conversion rate or (ii) 80% of the average of the five lowest VWAP of the Company’s common stock over the preceding twenty trading days. The Convertible Noteholder may not redeem more than $500,000 per calendar month during the period between the six-month anniversary of the date of issuance until the first anniversary of the date of issuance and $750,000 per calendar month thereafter. The obligation or right of the Company to deliver its shares upon the conversion or redemption of the Additional Note is subject to a 19.99% cap and subject to a floor price of $3.25 (unless waived by the Company). Any amounts redeemed or converted once the cap is reached or if the market price is less than the $3.25 floor price must be paid in cash.

If there is an Event of Default under the Additional Note, the Convertible Noteholder may accelerate the Company’s obligations or the Convertible Noteholder may elect to increase the outstanding obligations under the Additional Note. The amount of the increase ranges from 15% for certain “Major Defaults,” 10% for failure to obtain the Convertible Noteholder’s approval for certain equity issuances with anti-dilution, price reset or variable pricing features of less than $2,500,000, and 5% for certain “Minor Defaults.” In addition, the Additional Note obligations will be increased if there are delays in the Company’s delivery requirements for the shares or cash issuable upon the conversion or redemption of the Additional Note in certain circumstances.

If the Company issues convertible debt in the future with any terms, including conversion terms, that are more favorable to the terms of the Additional Note, the Convertible Noteholder may elect to incorporate the more favorable terms into the Additional Note.

The convertible notes payable as of September 30, 2020 and December 31, 2019 consists of the following:

September 30, 2020 (Unaudited) | December 31, 2019 | |||||

Convertible Notes | $ | 8,400,000 | $ | 5,500,000 | ||

Less: principal payments of debt | (6,859,458 | ) | (1,544,724 | ) | ||

Less: unamortized debt discount and OID accretion | (275,522 | ) | (770,621 | ) | ||

Total | $ | 1,265,020 | $ | 3,184,655 | ||

NOTE 5: LICENSE AGREEMENTS

During 2016, the Company entered into a license agreement (the “Alba License”) with Alba Therapeutics Corporation (“Alba”) to obtain the rights to certain intellectual property relating to larazotide acetate and related compounds. The Company’s initial area of focus for these assets relates to the treatment of celiac disease.

Upon execution of the Alba License, the Company paid Alba a non-refundable license fee of $0.5 million. In addition, the Company is required to make milestone payments to Alba upon the achievement of certain clinical and regulatory milestones totaling up to $1.5 million and payments upon regulatory approval and commercial sales of a licensed product totaling up to $150 million, which is based on sales ranging from $100 million to $1.5 billion.

Upon the Company paying Alba $2.5 million for the first commercial sale of a licensed product, the Alba License becomes perpetual and irrevocable. Upon the achievement of net sales in a year exceeding $1.5 billion, the Alba License also becomes free of milestone fees. The Alba License provides Alba with certain termination rights, including failure of the Company to use Commercially Reasonable Efforts to develop the licensed products.

20

9 METERS BIOPHARMA, INC.

NOTES TO UNAUDITED CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

During 2013, the Company entered into an exclusive license agreement with Seachaid Pharmaceuticals, Inc. (the “Seachaid Agreement”) to further develop and commercialize the licensed product, the compound known as APAZA. The agreement shall continue in effect on a country-by-country basis, unless terminated sooner in accordance with the termination provisions of the agreement, until the expiration of the royalty term for such product and such country. The royalty term for each such product and such country shall continue until the earlier of the expiration of certain patent rights (as defined in the agreement) or the date that the sales for one or more generic equivalents makes up a certain percentage of sales in an applicable country during a calendar year.