Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - DUCK CREEK TECHNOLOGIES, INC. | dct-ex322_520.htm |

| EX-32.1 - EX-32.1 - DUCK CREEK TECHNOLOGIES, INC. | dct-ex321_519.htm |

| EX-31.2 - EX-31.2 - DUCK CREEK TECHNOLOGIES, INC. | dct-ex312_521.htm |

| EX-31.1 - EX-31.1 - DUCK CREEK TECHNOLOGIES, INC. | dct-ex311_522.htm |

| EX-23.1 - EX-23.1 - DUCK CREEK TECHNOLOGIES, INC. | dct-ex231_443.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒ |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended August 31, 2020

OR

|

☐ |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number 001-39449

Duck Creek Technologies, Inc.

(Exact name of Registrant as specified in its Charter)

|

Delaware |

|

84-3723837 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

22 Boston Wharf Road, Floor 10 Boston, MA |

|

02210 |

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (888) 724-3509

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Common stock, $0.01 par value per share |

|

DCT |

|

Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☐ NO ☒

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). YES ☒ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

☒ |

|

Smaller reporting company |

|

☐ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The registrant was not a public company as of the last business day of its most recently completed second fiscal quarter and, therefore, cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates as of such date.

The number of shares of Registrant’s Common Stock outstanding as of October 29, 2020 was 130,833,050.

|

|

|

Page |

|

1 |

||

|

2 |

||

|

|

|

|

|

|

|

|

|

Item 1. |

4 |

|

|

Item 1A. |

19 |

|

|

Item 1B. |

49 |

|

|

Item 2. |

49 |

|

|

Item 3. |

50 |

|

|

Item 4. |

50 |

|

|

|

|

|

|

|

|

|

|

Item 5. |

51 |

|

|

Item 6. |

53 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

55 |

|

Item 7A. |

75 |

|

|

Item 8. |

76 |

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

114 |

|

Item 9A. |

114 |

|

|

Item 9B. |

114 |

|

|

|

|

|

|

|

|

|

|

Item 10. |

115 |

|

|

Item 11. |

120 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

128 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

131 |

|

Item 14. |

136 |

|

|

|

|

|

|

|

|

|

|

Item 15. |

137 |

|

|

Item 16 |

139 |

|

i

Special Note Regarding Forward-Looking Statements

Some of the information contained in the sections entitled “Item 1. Business” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere in this Annual Report on Form 10-K contain forward-looking statements that reflect our current views with respect to, among other things, future events and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates,” “target,” “projects,” “contemplates” or the negative version of those words or other comparable words. Any forward-looking statements contained in this report are based upon our historical performance and on our current plans, estimates and expectations in light of information currently available to us. The inclusion of this forward-looking information should not be regarded as a representation by us that the future plans, estimates or expectations contemplated by us will be achieved. Such forward-looking statements are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business, prospects, growth strategy and liquidity. For more information regarding these risks and uncertainties as well as certain additional risks that we face, refer to “Item 1A. Risk Factors” as well as the factors more fully described in “Item 7. Management’s Discussion and Analysis of Financial Conditions and Results of Operations.” Accordingly, there are, or will be, important factors that could cause our actual results to differ materially from those indicated in these statements. We believe that these factors include, but are not limited to:

|

|

• |

our history of losses; |

|

|

• |

changes in our product revenue mix as we continue to focus on sales of our SaaS solutions, which will cause fluctuations in our results of operations and cash flows between periods; |

|

|

• |

our reliance on orders and renewals from a relatively small number of customers for a substantial portion of our revenue, and the substantial negotiating leverage customers have in renewing and expanding their contracts for our solutions; |

|

|

• |

the success of our growth strategy focused on SaaS solutions and our ability to develop or sell our solutions into new markets or further penetrate existing markets; |

|

|

• |

our ability to manage our expanding operations; |

|

|

• |

intense competition in our market; |

|

|

• |

third parties may assert we are infringing or violating their intellectual property rights; |

|

|

• |

U.S. and global market and economic conditions, particularly adverse in the insurance industry; |

|

|

• |

additional complexity, burdens and volatility in connection with our international sales and operations; |

|

|

• |

the length and variability of our sales and implementation cycles; |

|

|

• |

data breaches, unauthorized access to customer data or other disruptions of our solutions; |

|

|

• |

control of our Company by the Apax VIII Fund, a global private equity fund (collectively, with its affiliates, “Apax”) and Accenture plc, a public limited company incorporated in Ireland (collectively, with its affiliates, “Accenture”), and perceived conflicts of interests; |

|

|

• |

our status as a “controlled company” within the meaning of the corporate governance standards of Nasdaq; |

1

|

|

• |

the other risks and uncertainties described under “Item 1A. Risk Factors.” |

These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report. The forward-looking statements made in this report relate only to events as of the date on which the statements are made. We do not undertake any obligation to publicly update or review any forward-looking statement except as required by law, whether as a result of new information, future developments or otherwise.

If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from what we may have expressed or implied by these forward-looking statements. We caution that you should not place undue reliance on any of our forward-looking statements. You should specifically consider the factors identified in this report that could cause actual results to differ before making an investment decision to purchase our common stock. Furthermore, new risks and uncertainties arise from time to time, and it is impossible for us to predict those events or how they may affect us.

As used in this Annual Report on Form 10-K unless the context otherwise requires, references to “we,” “us,” “our,” the “Company,” “Duck Creek,” and similar references refer to Duck Creek Technologies, Inc. together with its subsidiaries, and the following terms have the meanings or are calculated as set forth below:

|

|

• |

We define “subscription revenue” as the revenue derived from the sale of our Software-as-a-service (“SaaS”) solutions through recurring fee arrangements for the period indicated. |

|

|

• |

We define “ACV” as the committed total contract value of new software sales in dollar terms divided by the corresponding minimum number of committed months, with the resultant minimum monthly commitment being multiplied by twelve. |

|

|

• |

We define “carriers” as property and casualty (“P&C”) insurance carriers. |

|

|

• |

We define “core systems” as the following key functions of carriers: policy administration, claims management and billing. |

|

|

• |

We define “customers” as buying entities that contract individually for our products and services. For example, multiple subsidiaries of a single carrier may each constitute a customer if each entity contracts with us separately. By contrast, a carrier that uses our products across multiple subsidiaries under a single enterprise license agreement would constitute a single customer. |

|

|

• |

We define “DWPs” as the gross dollar value of total premiums paid to carriers by policyholders. |

|

|

• |

Munich Re Specialty Insurance is a description for the insurance business operations of affiliated companies in the Munich Re Group that share a common directive to offer and deliver specialty property and casualty insurance products and services in North America. |

Certain monetary amounts, percentages, and other figures included in this Annual Report on Form 10-K have been subject to rounding adjustments. Percentage amounts included in this Annual Report on Form 10-K have not in all cases been calculated on the basis of such rounded figures, but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this Annual Report on Form 10-K may vary from those obtained by performing the same calculations using the figures in our consolidated financial statements included elsewhere in this Annual Report on Form 10-K. Certain other amounts that appear in this Annual Report on Form 10-K may not

2

sum due to rounding. When we state that we are the leading SaaS provider of core systems for the P&C insurance industry, we are basing our leadership on our subscription revenue for fiscal 2020.

Our fiscal year ends on August 31. Unless otherwise noted, any reference to a year preceded by the word “fiscal” refers to the fiscal year ended August 31 of that year. For example, references to “fiscal 2019” refer to the fiscal year ended August 31, 2019. Any reference to a year not preceded by “fiscal” refers to a calendar year.

MARKET AND INDUSTRY DATA

Certain market and industry data included in this Annual Report on Form 10-K has been obtained from third party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications, government publications, and third party forecasts in conjunction with our assumptions about our markets. We have not independently verified such third party information. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings “Forward-Looking Statements” and “Item1A. Risk Factors” in this Annual Report on Form 10-K.

3

Company Overview

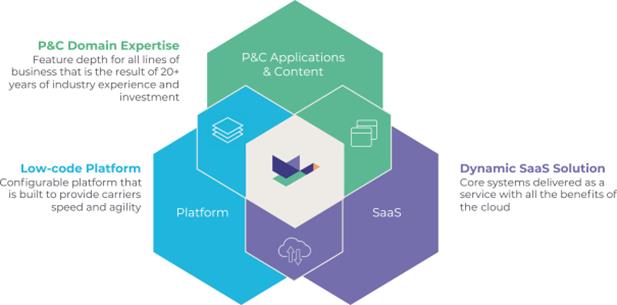

We are the leading SaaS provider of core systems for the P&C insurance industry. We have achieved our leadership position by combining over twenty years of deep domain expertise with the differentiated SaaS capabilities and low-code configurability of our technology platform. We believe we are the first company to provide carriers with an end-to-end suite of enterprise-scale core system software that is purpose-built as a SaaS solution. Our product portfolio is built on our modern technology foundation, the Duck Creek Platform, and works cohesively to improve the operational efficiency of carriers’ core processes (policy administration, claims management and billing) as well as other critical functions. The Duck Creek Platform enables our customers to be agile and rapidly capitalize on market opportunities, while reducing their total cost of technology ownership.

The core business functions of carriers are complex and data intensive, requiring large ongoing investments in domain specific technology. Heightened end-user expectations, increased competition, and new and evolving risks pose new challenges for carriers, creating the need for software that fosters agility, innovation and speed to market. However, a large portion of the P&C insurance market continues to rely on legacy technology systems that are costly and inefficient to maintain, difficult to upgrade, and lacking in functional flexibility. In recent years, some carriers have turned to newer alternatives to legacy systems. These systems have been designed for on-premise environments and lack the inherent benefits of purpose-built SaaS solutions, perpetuating the limitations, inflexibility and cost of legacy systems. By contrast, our SaaS solutions, offered through Duck Creek OnDemand, accelerate carriers’ agility and speed to market by enabling rapid, low-code product development, and protecting carriers’ unique content configurations and integrations while providing upgrades and updates via continuous delivery. We have developed a substantial SaaS customer base and believe that we have established a meaningful first-mover advantage by demonstrating the superiority of SaaS solutions for core systems in the P&C insurance industry. We began offering SaaS solutions for core systems in the P&C insurance industry in 2013 and signed our first customer in 2014. We believe competitors will have to make significant investments of time and resources in order to offer similar SaaS products.

Our deep understanding of the P&C insurance industry has enabled us to develop a single, unified suite of insurance software products that is tailored to address the key challenges faced by carriers. Our solutions promote carriers’ nimbleness by enabling rapid integration and streamlining the ability to capture, access and utilize data more effectively. The Duck Creek Suite includes several products that support the P&C insurance process lifecycle, such as:

|

|

• |

Duck Creek Policy: enables carriers to develop and launch new insurance products and manage all aspects of policy administration, from product definition to quoting, binding and servicing |

|

|

• |

Duck Creek Billing: supports fundamental payment and invoicing capabilities (such as billing and collections, commission processing, disbursement management and general ledger capabilities) for all insurance lines and bill types |

|

|

• |

Duck Creek Claims: supports the entire claims lifecycle from first notice of loss through investigation, payments, negotiations, reporting and closure |

4

In addition, we offer other innovative solutions, such as Duck Creek Rating, Duck Creek Insights, Duck Creek Digital Engagement, Duck Creek Distribution Management, Duck Creek Reinsurance Management, Duck Creek Anywhere Managed Integrations and Duck Creek Industry Content, which provide additional features and functionalities that further help our customers meet the increasing and evolving demands of the P&C industry. Our customers purchase and deploy Duck Creek OnDemand, our SaaS solution, either individually or as a suite. Historically, we have also sold our products through perpetual and term license arrangements, substantially all of which include maintenance and support arrangements. We offer professional services, primarily related to implementation of our products, in connection with both our SaaS solutions and perpetual and term license arrangements.

Substantially all of our new bookings come from the sale of SaaS subscriptions of Duck Creek OnDemand. For the fiscal years ended August 31, 2020, 2019 and 2018, SaaS ACV bookings represented 96%, 86%, and 71% of our total ACV bookings, respectively.

Our strong customer relationships are a key driver of our success. We believe these relationships are a result of our ability to develop innovative solutions that incorporate our deep domain expertise into products that serve mission critical functions in our customers’ day-to-day operations. Our customer base is comprised of a range of carriers, including some of the largest companies in the P&C insurance industry, such as Progressive, Liberty Mutual, AIG, The Hartford, Berkshire Hathaway Specialty Insurance, GEICO and Munich Re Specialty Insurance, as well as regional carriers, such as UPC, Coverys, Avant Mutual, IAT Insurance Group and Mutual Benefit Group. We have over 150 insurance customers worldwide, including the top five North American carriers. In addition, our customers have won numerous industry awards for innovative products that were developed with our solutions. For example, in 2018, AXIS and Northbridge won industry awards from Celent and Novarica for their products, which were built using Duck Creek solutions. In 2020, ProSight Insurance won an industry award from Novarica for core system transformation efforts using Duck Creek solutions.

We have a broad partner ecosystem that includes third-party solution partners who provide complementary capabilities as well as system integrators (“SIs”) who provide implementation and other related services to our customers. These partnerships help us grow our business more efficiently by enhancing our sales force through co-marketing efforts and giving us scale to service our growing customer base. We have relationships with over 50 companies across a diverse set of services and offerings, including fifteen SIs with over 4,000 Duck Creek implementation staff who help to implement our solutions. We maintain key partnerships with leading SIs, such as Accenture, Capgemini and Cognizant, as well as leading technology companies, such as Microsoft and Salesforce, and Insurtech start-ups, such as Arity, Friss, SPLICE Software, and Cape Analytics. These partnerships have allowed us to further build on our deep domain expertise in the P&C insurance industry, extend the value of our solutions and provide our customers with additional end-to-end functionality.

Our subscription revenues have grown significantly in recent years, both in absolute terms and as a percentage of our business. For the fiscal year ended August 31, 2020, we generated subscription revenues of $84.0 million, an increase of 50% compared to subscription revenues of $55.9 million for the fiscal year ended August 31, 2019. We generated total revenues of $211.7 million for the fiscal year ended August 31, 2020, an increase of 24% compared to total revenues of $171.3 million for the fiscal year ended August 31, 2019. We have made significant investments in our software platform and sales and marketing organization and incurred net losses of $29.9 million and $16.9 million for the fiscal years ended August 31, 2020 and 2019, respectively. See “Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

5

P&C Insurance Industry Overview

The P&C insurance industry is large, complex and highly regulated. In 2019, the industry serviced approximately $2.4 trillion of DWP spanning thousands of carriers globally. In addition to being one of the largest global industries, we believe it is also one of the most resilient. For a majority of businesses and consumers, insurance is a necessity rather than an amenity. As a result, overall spend on insurance products has continued to grow steadily over the long-term, even across periods of economic volatility. The P&C insurance industry is fragmented by the geographies in which carriers operate, the lines of insurance they underwrite, the customers they target, their distribution strategy and the overall amount of DWP that they generate. DWP, which quantifies the gross dollar value of total premiums paid to carriers by policyholders, is a key measurement of scale for the P&C insurance industry.

Carriers sell products that protect policyholders from losses to property, bodily injury, litigation and other liabilities. Large carriers often have global operations and offer a wide range of insurance products. They are also required to organize and report financial information by country, and sometimes by state or province within a country. This creates a large portfolio of insurance products with different regulatory requirements. Smaller carriers generally have a narrower geographic focus and/or offer a more limited set of insurance products but often still require sophisticated capabilities to manage their businesses. The Duck Creek Suite meets the most complex and sophisticated technology needs of the largest carriers, and can also be scaled to cost-effectively serve the needs of smaller carriers.

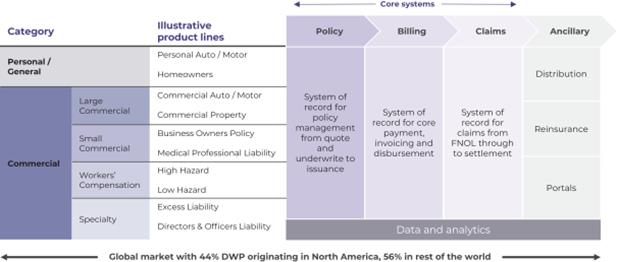

Core systems, including policy, billing and claims, power carriers’ critical operations. Core systems house the insurance product structure, such as rates, rules and forms, and generate data that allows the actuarial and underwriting staff of carriers to continuously modify and improve product offerings and provide more personalized customer service. They also manage the claims lifecycle, from first notice of loss to settlement. In addition, core systems integrate with agent and broker portals, operational data stores and data warehouses as well as business intelligence and analytics systems.

It is not uncommon for a single carrier to use multiple vendors (or internally developed applications) to provide core systems for different insurance lines or geographies, or for discrete core system processes (e.g., policy, billing, claims) within a single insurance line and geography. A carrier may use our software for certain parts of its business, and deploy solutions from different vendors for other parts of its business. As a result, we have a market opportunity to both achieve greater penetration within our existing customer base as well as increase our customer base by servicing new customers who are not currently using our products. The following diagram provides a framework for understanding the multifaceted processes of carriers:

6

Carriers invest substantial time and resources to develop and maintain their information technology (“IT”) operations. We estimate that our total addressable market, representing the portion of this spending that is focused specifically on core system software, is approximately $5.5 billion in the United States and $15 billion globally. To estimate our total addressable market, we categorized the P&C insurance market into tiers based on DWP per carrier as reported by S&P Global, A.M. Best and Swiss Re, both within the United States and globally. We then estimated average price per DWP for our core systems solutions, accounting for tiered price discounts at different tiers, and multiplied the price per DWP by the total amount of DWP at each tier available both in the United States and globally.

Challenges Facing the P&C Insurance Industry and the Limitations of Legacy Systems

We believe reliance on legacy systems and other systems designed for on-premise environments limit carriers’ ability to respond to many of the significant challenges facing their industry, including:

|

|

• |

Heightened end-user expectations. Today’s end-users expect seamless and tailored experiences with every interaction, which has led to the increase in demand for digital distribution and servicing capabilities. For instance, personal and commercial insurance end-users expect improved digital experiences with real time multi-channel service. |

|

|

• |

Increased competition in the marketplace. Carriers are diversifying into new geographies and product lines to drive profitable DWP growth. In addition, new entrants, such as upstart ‘Insurtech’ companies, are seeking to disrupt the traditional insurance market with targeted technological innovations. In response to escalating competition, carriers are investing in new technology solutions to increase speed to market and reduce operating expenses. |

|

|

• |

New and evolving risks. Carriers are under pressure to offer new and more complex insurance products in order to address evolving use cases. Emerging risk categories, such as cybersecurity, terrorism and the sharing economy (e.g. use of automobiles for personal and commercial uses), are creating demand for new insurance products. These new and evolving risks require carriers to be increasingly agile in their product development. |

|

|

• |

Increased size of losses in assets and the number of catastrophic events. The increased intricacy of assets, such as automobiles that include full onboard computers, has increased the cost of repairs and claim sizes. Additionally, natural disasters with large scale catastrophic losses have become more frequent. More than ever, carriers need access to accurate and complete data about risk in order to minimize their loss. |

|

|

• |

The rise of the IoT. Carriers have predominately relied on traditional data sources for underwriting, pricing and claims handling. The rise of IoT devices, such as sensors, telematics devices and drones, is significantly increasing the amount of data available to carriers. This is enabling carriers to assess risk on a more granular level, identify losses faster, simplify claims processing and mitigate fraud. Taking advantage of the new volumes of data requires open and flexible core systems that allow carriers to move more quickly and make powerful data-driven decisions. |

|

|

• |

Emerging capabilities and advancing technologies. Carriers can better analyze risk through enhanced pricing models, artificial intelligence and machine learning technology. These emerging technologies offer carriers the opportunity to better understand and price risk in real time and a potential competitive advantage to realize the value from data science research. As a result, carriers are more aggressively investing in technology to keep up with innovations and integrations. |

These challenges are placing increased pressure on insurance carriers to improve consumer experience, business agility and speed to market. However, many carriers rely on legacy systems or alternatives designed for on-premise environments that are difficult to change, update or integrate without significant incremental custom-code development. Carriers relying upon these systems are generally unable to manage and analyze data at the pace required to effectively guide operational and risk decisions. These systems are difficult to update without significant IT spend and efforts, resulting in higher operating costs and slower speed to market for carriers.

7

We believe that carriers will increasingly look to adopt SaaS solutions, like Duck Creek OnDemand, that are designed to enhance their organizational agility, product innovation and consumer experience, allowing them to react quickly to evolving consumer preferences and efficiently capture market opportunity, while reducing their total cost of ownership. According to an October 2020 Novarica survey, more than 70% of insurance carriers plan to expand their migration of applications to the cloud in 2021.

The Duck Creek Approach

Our solutions provide us with a sustainable competitive advantage by helping our customers overcome the limitations of existing systems to meet the challenges of the current P&C insurance industry.

|

|

• |

Deep domain expertise. With more than twenty years of operating experience in the P&C insurance industry, we have developed deep industry-specific domain expertise. This enables us to offer a broad range of integrated solutions embedded with smart, intuitive pre-built functionality, designed to meet the precise use-case requirements of carriers. Our software incorporates and integrates product definition templates and other key industry content from relevant third-parties (such as Insurance Services Office, Inc. and National Council on Compensation Insurance) and regulatory bodies. Our in-depth understanding of the P&C insurance industry allows us to continue to address the various and evolving needs of carriers, thereby continuing to enhance the customer experience. |

|

|

• |

Comprehensive, future-ready offerings. Our comprehensive suite of enterprise-scale core system software is comprised of leading applications that are designed to meet the full range of our customers’ needs. We deliver upgrades that can be applied across our suite, improving common functionality across our customers’ systems. We continuously update industry content, allowing our customers to efficiently keep pace with market and regulatory changes. We also develop and maintain supplementary proprietary content that allows our customers to define, sell and service complex insurance product lines in a single integrated environment. |

|

|

• |

Scalability for all carriers. Our solutions are designed to meet the most complex and sophisticated technology needs of the largest carriers but can also be scaled to cost-effectively serve the needs of smaller carriers. |

|

|

• |

Low-code configurability. Using low-code tools designed for ease, speed and accuracy, both technical and non-technical users can tailor our solutions to meet their business needs. These intuitive tools allow our customers to create new products and make changes to existing products and related workflows without custom coding, accelerating their speed to market and improving productivity. We also offer application and configuration tools for technical users who design and manage business processes, user interfaces or web applications. |

8

|

|

• |

Open architecture. Our Duck Creek Anywhere integration strategy provides fast, easy access to the third-party data and services that customers need. This is executed through a pool of APIs, integration methodologies and partner connectors, all designed to enable our customers to efficiently leverage the services that best match their strategy. |

|

|

• |

Unique insights. We enable carriers to use data as a strategic asset. Using Duck Creek Insights, carriers are able to efficiently gather a consolidated picture of their business across internal and third-party data sources (including data lakes, legacy systems, IoT, policy, claims, etc.), deliver critical information to execute business decisions and employ new methods of automated decision making. |

|

|

• |

Mission-focused organization. We are driven by our mission to empower carriers to extend and improve the coverage they provide to their customers and to enhance the end-user experience. This allows carriers to reimagine their operations and shape the future of insurance to provide every person and enterprise protection from life’s uncertainties. Our strong culture and organizational ethos, coupled with a management team that has decades of leadership in the insurance software industry and is actively involved in the development of our products, drives our company to continue to innovate and deliver high-quality tools and services to our customers. |

Our Growth Strategy

We intend to extend our position as the leading provider of SaaS solutions for the core systems of the P&C insurance industry. The key components of our strategy are:

|

|

• |

Growing our customer base. We believe there is substantial opportunity to continue to grow our customer base across the P&C insurance industry. We have over 150 insurance customers, which represents a small portion of carriers both in North America and globally. We are investing in our sales and marketing force, specifically targeting key accounts and leveraging current customers as references. |

|

|

• |

Deepening relationships with our existing customers. We have deep engagement with our customers; on average, each of our customers uses 2.8 of our products, with each SaaS customer using 5.2 of our products. Since fiscal 2017, we have generated over 49% of our bookings from sales to existing customers. In addition to pursuing new customers, we intend to leverage our track record of success with our existing customers by selling additional products and targeting new opportunities within these carriers. Many customers purchase our solutions to address a specific portion of their core system needs. We believe we will have the opportunity to further transition the remaining components of their core systems to our SaaS solutions and sell the Duck Creek Suite to additional business units within our customer base. |

|

|

• |

Expanding our partner ecosystem. We have a large and expanding network of partnerships that is comprised of third-party solution partners who provide complementary capabilities as well as third-party SIs who provide implementation and other related services to our customers. These partners help us grow our business more efficiently by enhancing our sales force through co-marketing efforts and giving us scale to service our customer base. We intend to extend our network of partners who are able to drive meaningful interest in, and adoption of, our products. |

|

|

• |

Continuing to innovate and add new solutions. We have made significant investments in research and development and intend to continue to do so. We are focused on enhancing the functionality and breadth of our current solutions as well as developing and launching new products and tools to address the evolving needs of the P&C insurance industry. For example, we introduced Anywhere Managed Integrations, which allows our customers to seamlessly connect with numerous popular third-party providers’ data and service solutions, such as Lexis Nexis, Verisk and Hyland, without having to bear the technical burden and higher cost of individually integrating them. We currently offer our customers 35 unique Anywhere Managed Integrations. |

9

|

|

• |

Transitioning our term and perpetual license customers to SaaS. Some of our customers use versions of our solutions that were purchased via perpetual or term licenses and typically are installed on-premise. We will seek to transition these customers to our current SaaS solutions, which we believe will generate increased long-term economic value. |

|

|

• |

Pursuing acquisitions. We have acquired and successfully integrated several businesses complementary to our own to enhance our software and technology capabilities. We intend to continue to pursue targeted acquisitions that further complement our product portfolio or provide us access to new markets. We will carefully evaluate acquisition opportunities to assess whether they will be successful within our business model and whether they will meet our strategic objectives. We believe that through sustained execution of our disciplined and selective acquisition strategy, we will be able to effectively integrate targeted companies or assets into our model and grow our business. |

Our Products

10

Our customers purchase and deploy our solutions either individually for a specific P&C insurance process or as part of a combined suite to manage all aspects of the core P&C insurance lifecycle. Our portfolio includes the following core system products:

|

|

• |

Duck Creek Policy. Delivers a full lifecycle solution for the development of products and quoting, binding and servicing of policies across all channels, from agents and brokers to end-users. Duck Creek Policy maintains all of the coverages, limits and exclusions that are used to create specific products. It also serves as the system of record for any endorsements, additions or changes for policies in force. We also offer Underwriting Workbench, an add-on module that extends the underwriting functionality for Duck Creek Policy by providing the ability to group quotes and policies into accounts, giving a holistic view of information relevant to underwriting. |

|

|

• |

Duck Creek Billing. Provides core payment and invoicing capabilities (such as billing and collections, commission processing, disbursement management and general ledger capabilities) for all insurance lines and bill types. Our billing system allows carriers to implement unique business rules and handle flexible payment plans to meet customer expectations and address increasingly complex billing strategies and practices. Our technology and automation allows greater control over billing processes and better management of payment collections, which can improve our customers’ financial performance and customer service. |

|

|

• |

Duck Creek Claims. Supports the entire claims lifecycle from first notice of loss through investigation, payments, negotiations, reporting and closure. Effective claims management is integral to carriers’ profitability and has become increasingly complex, time-sensitive and data-dependent. Duck Creek Claims provides enhanced technology, enabling greater information sharing and collaboration and providing a configuration toolset that gives all users power over the application data, screens and processes. |

We also offer the following products to further enable our customers to meet the challenges and increasing demands of the P&C insurance industry:

|

|

• |

Duck Creek Rating. Duck Creek Rating can be implemented on a standalone basis or as a component of Duck Creek Policy. Duck Creek Rating gives carriers the ability to quickly develop new rates and models and delivers accurate quotes in real-time based on the complex rating algorithms that are unique to each carrier’s line of business. To remain competitive in today’s marketplace, insurers are re-evaluating the efficacy of their rating systems. Duck Creek Rating provides insurers with more granular risk segmentation and greater pricing precision. |

|

|

• |

Duck Creek Insights. Insurance analytics solution that allows carriers to gather and analyze data from internal and external sources and facilitates rapid analysis and reporting on a single system. Duck Creek Insights allows carriers to use data as a strategic asset in real time, empowering them to quickly capture and leverage data across and beyond their organizations, deliver leaders and business users crucial information needed to execute intelligent actions and employ new methods of automated decision-making. |

|

|

• |

Duck Creek Digital Engagement. Family of offerings designed to provide intuitive, multi-channel digital interactions between P&C insurers and their agents, brokers and policyholders. Duck Creek Digital Engagement offers online digital applications, including our Duck Creek Producer, AgencyPortal, Turnstile and AgencyConnect tools. |

|

|

• |

Duck Creek Distribution Management. Automates sales channel activities for agents and brokers, including producer onboarding, compliance and compensation management, thereby reducing time spent on manual processes. Duck Creek Distribution Management helps carriers stay compliant on distribution licensing and reporting while also providing insurers the ability to quickly and effectively change producer commission plans using simple configurations. |

|

|

• |

Duck Creek Reinsurance Management. Automates critical financial and administrative functions required by primary carriers, such as contracts, bills, recoveries and payables, to manage contractual relationships and provide settlement with reinsurance providers. Duck Creek Reinsurance Management supports all reinsurance structures, provides a full audit trail and analytics and produces statements, bordereaux, cover letters, footnotes and supporting details. |

|

|

• |

Duck Creek Industry Content. Provides pre-built content (including base business rules, product designs, rating algorithms, data capture screens and workflows) for specific insurance lines of business, such as commercial auto, inland marine and workers compensation. As part of Duck Creek Industry Content, we actively maintain and update approximately 700 web-based screens and 9,000 insurance forms across several industry standard bodies such as AAIS, ACORD, ISO and NCCI, which reduces the effort required by our customers to comply with these standards. |

11

Our Unique Architecture: the Duck Creek Platform

Every carrier takes a distinct approach to designing the policies that it offers and the core business processes that it employs to support them. How a carrier chooses to assemble and rate the underlying elements of an insurance policy (such as the weighting ascribed to roof age for pricing a homeowner’s policy) represents its unique content configurations. For many carriers, these configurations have been built up over years of investment and development and represent a key competitive differentiator. These nuanced distinctions around coverages, limitations, rating factors and the data used to determine risk appetite and pricing can be the difference between a successful carrier and one facing losses. Additionally, the distinctive routing and handling of service decisions or claims triage can impact the cost and profitability for a carrier.

The Duck Creek Platform configuration layer serves as the development environment for carriers to create and modify insurance products (such as a commercial auto insurance policy), and the associated business rules and workflows that govern how insurance products are processed within a carrier:

|

|

• |

Product Design: the unique way in which carriers use individual data points (such as driving record and the make/model of a car) to design individual policies, including the coverages, limits, pricing and deductibles, such as vanishing deductibles or pay-per-mile auto policies. |

|

|

• |

Business Rules: carrier-specific criteria, including the types of policies it will write, channel and distribution rules (such as giving underwriting authority to distribution partners), and customer-specific claims handling. |

|

|

• |

Workflows: the ways in which an individual carrier manages its back office operations (such as the unique processes for handling different types of claims). |

12

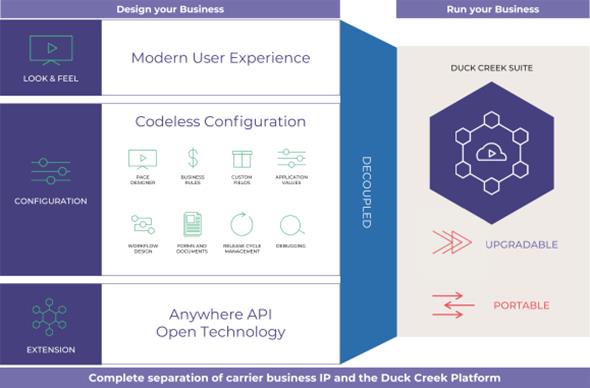

The configuration layer is separated from our solutions and platform code, and this decoupling allows customers to maintain their unique configurations even as technology advances and we provide upgrades. This architecture provides our customers with several unique advantages:

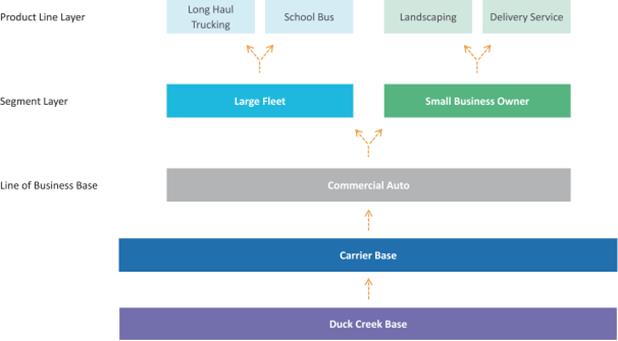

Faster innovation cycles enabled by the inheritance model. A defining characteristic of the Duck Creek Platform is our inheritance model that enables carriers to create and re-use insurance products and components of insurance products in layers which are linked together dynamically. This approach enables carriers to create new insurance products with speed and consistency.

Using the inheritance model, carriers can create a new insurance product simply by adding a new layer or tailoring a specific component in an existing layer using low-code configuration. This ensures consistency in operations across a carrier’s products using the same common base layer, while also allowing carriers to make changes efficiently across many insurance products by changing a single component within a common layer.

Importantly, our inheritance model enhances carriers’ agility and speed to market by accelerating new product development and allowing them to quickly capitalize on new and evolving opportunities while avoiding costly re-work required with legacy systems and alternative systems that were designed for on-premise environments. In addition to product designs, our inheritance model can also be applied to workflows and business rules.

Low-code configuration tools. Our low-code configuration tools allow technical and non-technical users to rapidly tailor our applications to meet their specific needs. These tools enable our customers to make meaningful changes to their products, processes or business rules with drag-and-drop authoring features and functionality without having to perform custom coding. This framework enables users to operate with speed while significantly reducing software development costs.

User Experience. Our platform enables carriers to build differentiated user experiences. Using the Duck Creek Design System along with low-code configuration tools, carriers can create experiences based on each user persona’s preferred engagement channel or deliver experiences designed using Duck Creek tools via third-party interfaces. The Duck Creek Design System encapsulates years of industry research into a best practice library that supports the needs of the various users of core systems – from agents to customer service professionals to policyholders and others.

13

Anywhere Integrations. In today’s insurance market, every transaction, workflow and decision must be informed by as much data and knowledge as possible and leverage services from internal and external sources to complete end-to-end processes. Openness to integration with third-party services, including the ability to work with the expanding world of Insurtech services and evolving artificial intelligence and machine learning technology, is critical to a carrier’s success. Through a robust set of REST APIs, integration accelerators and partner connectors, the open architecture of the Duck Creek Platform allows carriers to quickly and easily choose from the available services and provides them with the flexibility to leverage the tools and capabilities that best match their business strategy.

Our Customers

We have over 150 insurance customers, including the top five North American insurance carriers. Many of our customers serve multiple lines of insurance (including personal, commercial and specialty) and are leaders among each of these distinct categories. In addition, certain of our customers operate our solutions across multiple countries. Our customers, many of which we have had long-term relationships with, range from large national and multi-national carriers, such as Progressive, Liberty Mutual Insurance, AIG, The Hartford, Berkshire Hathaway Specialty Insurance, GEICO and Munich Re Specialty Insurance to regional carriers, such as UPC Insurance, Farm Bureau Financial, Avant Mutual, IAT Insurance Group and Mutual Benefit Group. Over 60 of our insurance customers use one or more of our SaaS products, including over 30 insurance customers that use our SaaS core system products.

When utilizing our solutions, products, and platform, many customers benefit from increased agility, greater flexibility, and overall lower total cost of ownership.

Sales and Marketing

We have made significant investments in our sales and marketing efforts. As of August 31, 2020, our sales and marketing organization included 160 employees. The majority of our sales and marketing strategies are focused on driving SaaS bookings growth. Our chief marketing officer and chief revenue officer, together with our sales, marketing and executive teams, promote our global brand by working to cultivate long-term relationships with current and prospective customers and other key industry influencers in each of the geographies in which we are active.

We sell our solutions and services through a direct sales team, comprised of our inside sales team, territory-based sales directors, and solutions consultants. Our inside sales team focuses on initiating contact with prospective customers and generating interest in cross-selling opportunities with existing customers. Our territory-based sales directors oversee sales to new or existing customers, and as part of the sales and marketing process, engage our solution consultants. Our solution consultants possess deep insurance domain expertise and are also experts in the technical aspects of our solutions and customer implementations. They engage with customers to understand their specific business needs and also present live demonstrations of our products that can be tailored to address those needs. Our solution consultants play a critical role in demonstrating the robust and complex features of our applications and helping carriers build an understanding of how to successfully integrate the Duck Creek Platform into their operations.

Our partnerships are also an important aspect of our sales and marketing strategy. We have a broad partner ecosystem that includes third-party solution partners who provide complementary capabilities as well as third-party SIs who provide implementation and other related services to our customers. These partnerships provide additional market validation to our offerings, enhance our sales force through co-marketing efforts and offer greater speed and efficiency of implementation capabilities and related services to our customers. We have relationships with over 50 different companies across a diverse set of services and offerings. These relationships include partnerships with leading SIs, such as Accenture, Capgemini, Cognizant and Mindtree. Over the past three fiscal years, we have grown the number of professionals in Duck Creek practices within these delivery partners from approximately 700 to over 3,000. We also maintain relationships with leading technology companies and solution providers, such as Microsoft, Salesforce, Hyland, Verisk and Lexis Nexis, and Insurtech start-ups, such as Arity, Friss, SPLICE Software, and Cape Analytics. These partnerships enhance the value of our solutions and provide our customers with additional end-to-end functionality.

14

We engage in a variety of traditional and online marketing activities designed to provide sales support, build brand recognition and enhance our reputation as an industry leader. Our marketing efforts help articulate our vision of how Duck Creek can shape the future of P&C insurance with affordable, flexible and open technology. Through our integrated marketing strategy we drive demand and brand recognition by leveraging digital advertising, search engine optimization, webinars, social media, thought leadership and various event-based marketing. We participate at industry conferences, are published frequently in the industry press and have active relationships with the major industry analysts. Additionally, we host an annual user conference, Formation, where our customers both participate in and deliver presentations on a wide range of Duck Creek and insurance technology topics. Formation facilitates discussions among industry participants and serves as a great resource for tips on using our platform and industry best practices. We also invite potential customers and partners to Formation as we believe customer references are a key component of driving new sales. We believe we are able to capitalize on the resulting network effect as we build goodwill through customer reviews and testimonials, word-of-mouth referrals and references from other industry participants.

Research and Development

Our research and development efforts focus on enhancing our offerings, in particular our SaaS solutions, to help our customers improve their operations, drive greater digital engagement with their customers, agents and brokers and gather, store and analyze data to improve business decisions. As of August 31, 2020, our research and development team was comprised of 416 employees, including product management and engineering personnel.

We make meaningful investments in developing the product definitions and integrations necessary for our solutions to meet the market requirements of each P&C insurance line-of-business and country or state in which we sell our solutions. This market-segment specific functionality must be updated regularly in order to stay current with regulatory changes in each market. We rely heavily on input from our customers in developing products that meet their needs. Our product management team leads our research and market validation efforts and provides guidance to management and our engineering team based on their collective domain expertise and in-depth knowledge and understanding of our customers, as well as their expertise in general technology advancements beyond the P&C insurance industry. As a result, our product management team engages regularly with customers, partners and other industry participants, as well as our customer service, sales and marketing and research and development organizations. Our product management team manages our development projects generally and serves to align separate functions within the company with a single strategic vision.

Our product and engineering teams are responsible for the design, development and testing of our products. They work together to launch new products and functionality as well as continuously enhance and support our existing products. These teams include both technology and insurance experts. We leverage a collaborative, team-based and test-driven approach to engineering so we can release new code frequently. We believe that the pace of change in the P&C insurance industry requires a steady stream of the continuous delivery of upgrades to our software solutions, which incrementally improve the user experience, core processes and insurance products.

SaaS Operations, Security and Compliance

We invest significantly in our Duck Creek OnDemand operations team, which is one of the fastest growing elements of our business and is responsible for all aspects of service delivery for Duck Creek OnDemand. This includes the full management of the network and cloud infrastructure that supports our applications as well as the day-to-day management to ensure the availability of applications, including through triage and ticket management to support our customers. In addition, our security team, led by the Chief Information Security Officer, manages both security operations as well as policies to ensure security is proactively built into our products and services. Our security and operations teams are based in our state-of-the-art SaaS Operations Center in Rosemont, Illinois, with additional team members located in geographies that enable around-the-clock coverage for critical customer operations. In addition to the investments we make in our security and operations teams, we continue to build on our technology tools and strong partner relationships, including our investments in best-in-class security and monitoring tools and our unique ongoing partnership with Microsoft’s Azure team, which helps us to provide for the smooth and efficient operation of Duck Creek OnDemand.

15

The market for core system software for the P&C insurance industry is highly competitive and fragmented. Increased spending by carriers on software applications and the emergence of new platforms that have expanded from the modernization of core systems to include new digital engagement and data and analytics solutions have generated significant interest among investors and entrepreneurs. Increased capital allows market participants to adopt more aggressive go-to-market strategies, improve existing products, introduce new ones and consolidate with other vendors. This market is also subject to changing technology preferences, shifting customer needs and the introduction of new models, products and services, which fosters a highly competitive market. Additionally, existing relationships between potential customers and our competitors may make selling our solutions to such customers challenging due to the high costs and risk of business interruption associated with switching providers. Our current and future competitors vary in size and in the breadth and scope of the products and services they offer, and may be larger, have longer operating histories or have greater available financial, technical, sales, marketing and other resources than we do, as well as larger installed customer bases. Our current principal competitors include, but are not limited to:

|

|

• |

Internally Developed Technology and Software: Many large insurance companies have sufficient IT resources to develop and maintain proprietary internal systems, or to consider developing new custom systems. Often these in-house technology programs will be supported by large scale consulting firms such as IBM, Wipro, Cognizant and others. |

|

|

• |

P&C Insurance Software Vendors: Vendors such as Guidewire, Insurity, Majesco, Sapiens and others provide software products that are specifically designed to meet the needs of carriers. |

|

|

• |

Horizontal Software Vendors: Vendors such as Oracle, SAP, Pegasystems and others provide software that can be customized to address the needs of carriers. |

|

|

• |

IT Services Firms: Firms such as DXC Technology, NTT Data and Tata Consultancy Services Limited offer software and systems that can be developed for the P&C insurance industry. |

We believe the principal competitive factors in our market include, but are not limited to:

|

|

• |

breadth and depth of product functionality; |

|

|

• |

line of business support that fits the needs of each element of a carrier’s business; |

|

|

• |

total cost of ownership; |

|

|

• |

domain expertise in the P&C insurance industry; |

|

|

• |

scalability, reliability and uptime of applications; |

|

|

• |

quality of implementation and collaborative customer service, including service and support staff for users; |

|

|

• |

modern and intuitive technology and user experience; |

|

|

• |

brand awareness, reputation and customer references; and |

|

|

• |

integration with a wide variety of third-party applications and systems. |

Our ability to remain competitive in the geographies in which we are active will depend to a great extent upon our ongoing performance in these areas.

Intellectual Property

The software industry is characterized by the existence of a large number of patents and frequent claims and related litigation regarding patent and other intellectual property rights. Our success and ability to compete depend in part upon our ability to protect our proprietary technology and to establish and adequately protect our intellectual property rights. To accomplish these objectives, we rely on a combination of patent, trademark, copyright and trade secret laws in the United States and other jurisdictions, as well as license agreements and other contractual protections.

16

As of August 31, 2020, we owned 12 issued U.S. patents, one of which expired in September 2020. Our remaining 11 issued U.S. patents are scheduled to expire between October 2021 and January 2032. The competitive advantages from the rights granted under our patents and the exact protection these patents provide cannot be predicted with certainty. Our existing patents, and any future patents, may be contested, circumvented or invalidated, and we may not be able to prevent third parties from infringing these patents. We anticipate filing additional patent applications to protect our rights in the future to the extent it would be beneficial and cost effective.

We also rely on certain registered and unregistered trademarks to protect our brand. We have registered the trademarks “Duck Creek” and related design marks in the United States and certain other jurisdictions. In addition, there could be potential trade name or trademark infringement claims brought by owners of other registered tradenames or trademarks that incorporate variations of our tradenames or trademarks. Any claims or customer confusion related to our tradenames or trademarks could damage our reputation and brand and substantially harm our business and results of operations.

In addition, we seek to protect our intellectual property rights by entering into confidentiality and invention assignment agreements with our employees and contractors, and confidentiality agreements with third parties. Despite these precautions, it may be possible for unauthorized parties to copy or use our proprietary information to create products or services that compete with ours. Policing unauthorized use of our technology and intellectual property rights can be difficult. The enforcement of our intellectual property rights depends on any legal actions, which can be costly and time consuming, against infringers being successful, which may not always be the case even when our rights have been infringed.

Employees

As of August 31, 2020, we had 1,405 employees and 58 contingent employees. None of our employees are represented by a labor union or covered by a collective bargaining agreement. We consider our relationship with our employees to be good and we focus heavily on employee engagement.

Regulations

The legal environment of cloud-based software businesses is evolving in the United States and other jurisdictions, and we are subject to a variety of laws and regulations in the United States and abroad that involve matters central to our business. Many of these laws and regulations are still evolving and being tested in courts, and could be interpreted in ways that could harm our business. These may involve privacy, data protection and personal information, content, intellectual property, data security and data retention and deletion. In particular, we are subject to federal, state and foreign laws regarding privacy and protection of people’s data. Foreign data protection, privacy, content and other laws and regulations can impose different obligations or be more restrictive than those in the United States. United States federal and state and foreign laws and regulations, which in some cases can be enforced by private parties in addition to government entities, are constantly evolving and can be subject to significant change. As a result, the application, interpretation, and enforcement of these laws and regulations are often uncertain, particularly in the new and evolving industry in which we operate, and may be interpreted and applied inconsistently from country to country and inconsistently with our current policies and practices.

Our customers upload to and store customer data in our cloud-based platform. This presents legal challenges to our business and operations, such as consumer privacy rights or intellectual property rights. Both in the United States and internationally, we must monitor and comply with a wide variety of laws and regulations regarding the data stored and processed on our cloud-based platform as well as in the operation of our business. For example, the European Union’s GDPR, which became effective on May 25, 2018, and has resulted and will continue to result in significantly greater compliance burdens and costs for companies with users and operations in the European Union. Under GDPR, fines of up to 20 million Euros or up to 4% of the annual global revenues of the infringer, whichever is greater, can be imposed for violations. The GDPR imposes several stringent requirements for controllers and processors of personal data and could make it more difficult and/or more costly for us to use and share personal data. Further, Brexit has created uncertainty with regard to the regulation of data protection in the United Kingdom. In particular, it is unclear whether the United Kingdom will enact data protection laws or regulations designed to be consistent with GDPR and how data transfers to and from the United Kingdom will be regulated. In addition, the California Consumer Privacy Act (“CCPA”), which went into effect on January 1, 2020, limits how we may collect

17

and use personal data. The impact of this law on us and others in our industry is and will remain unclear until additional regulations are issued. The effects of the CCPA are potentially far-reaching, however, and may require us to modify our data processing practices and policies and incur substantial compliance-related costs and expenses. Non-compliance with these laws could result in penalties or significant legal liability. We have invested, and continue to invest, human and technology resources into our GDPR compliance efforts and our data privacy compliance efforts generally.

COVID-19 Update

In December 2019, a novel strain of coronavirus (“COVID-19”) was reported to have surfaced in Wuhan, China. In January 2020, COVID-19 spread to other countries, including the United States and others in which we operate, and efforts to contain the spread of COVID-19 intensified. In March 2020, the World Health Organization declared COVID-19 a global pandemic. The outbreak and certain preventative or protective actions that governments, businesses and individuals have taken in respect of COVID-19 have resulted in extended global business disruptions. The severity and duration of these business disruptions remain largely fluid and ultimately will depend on many factors, including the speed and effectiveness of containment efforts throughout the world.

In March 2020, we implemented various measures to ensure the safety of our employees, customers and suppliers. Over a two-day period, we shifted 100% of our employee base to work from home, which continues to be in effect. Additionally, our operational model has enabled us to minimize the impact to sales productivity or delivery of our solutions to customers to date. Since shifting to working remotely, we have successfully completed several product live launches and initiated new projects applying a fully virtual model.

While the full impact of COVID-19 remains unknown and COVID-19 has impacted certain companies’ decisions regarding technology spending, we have not experienced a material disruption on our bookings or sales to date. For the fiscal year ended August 31, 2020, we generated growth of 24% in total revenue, 50% in subscription revenue and 85% in SaaS ARR (as defined below) as compared to the fiscal year ended August 31, 2019. Our ability to grow revenue within our existing customer accounts has remained strong, with a SaaS Net Dollar Retention Rate (as defined below) of 116.8% for the quarter ended August 31, 2020. Additionally, we generated net cash provided by operating activities of $25.7 million and Free Cash Flow (as defined below) of $18.9 million for the fiscal year ended August 31, 2020, compared to $14.8 million and $6.6 million, respectively, for the fiscal year ended August 31, 2019. However, due to COVID-19 we delayed certain of our planned investments, primarily related to our international expansion initiatives.

As of August 31, 2020, we had $418.9 million of liquidity, including $389.9 million in cash and cash equivalents and $29.0 million of availability under our revolving credit facility.

The magnitude of the effect of COVID-19 on our business will depend, in part, on the length and severity of the restrictions and other limitations on our ability to conduct our business in the ordinary course. The longer the pandemic continues or resurges, the more severe the impacts described above may be on our business. In addition, because COVID-19 did not begin to affect our financial results until after the beginning of the third quarter of fiscal 2020, its impact on our results for the six months ended August 31, 2020 may not be indicative of its impact on our results for future periods. The extent, length and consequences of the pandemic, including our customers’ purchasing decisions and other reactions, are uncertain and impossible to predict, but could be material. Any reopenings followed by subsequent restrictions or closings could also have a material impact on us. See “Risk Factors—Risks Related to Our Business and Industry—Public health outbreaks, epidemics or pandemics, including the global COVID-19 outbreak, could harm our business, results of operations, and financial condition.”

Corporate Information

Duck Creek Technologies, Inc. was incorporated in Delaware in November 2019. In August 2020, we completed the initial public offering of our common stock (the “IPO”) and our common stock trades on the Nasdaq Global Select

18

Market (“Nasdaq”) under the symbol “DCT.” Our principal executive offices are located at 22 Boston Wharf Road, Floor 10, Boston, MA 02210, and our telephone number is (888) 724-3509.

Our website address is www.DuckCreek.com. We make available on or through our website certain reports and amendments to those reports that we file with or furnish to the Securities and Exchange Commission (“SEC”) in accordance with the Securities Exchange Act of 1934, as amended (Exchange Act). These include our annual reports on Form 10-K, our quarterly reports on Form 10-Q, and our current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of Securities Exchange Act of 1934, as amended (“the Exchange Act”)

Our business involves significant risks, some of which are set forth below. You should carefully consider the risks described below together with other information set forth in this Annual Report on Form 10-K and in our other public filings. If any of the following risks or uncertainties actually occur, our business, financial condition, prospects, results of operations and cash flow could be materially and adversely affected. In that case, the market price of our common stock could decline. The risks discussed below are not the only risks we face. Additional risks or uncertainties not currently known to us, or that we currently deem immaterial, may also have a material adverse effect on our business, financial condition, prospects, results of operations or cash flows, as well as the market price of our securities. We cannot assure you that any of the events discussed in the risk factors below will not occur.

Risks Related to Our Business and Industry

Public health outbreaks, epidemics or pandemics, including the global COVID-19 outbreak, could harm our business, results of operations, and financial condition.

Public health outbreaks, epidemics or pandemics, could materially and adversely impact our business. For example, in March 2020, the World Health Organization declared the COVID-19 virus outbreak a global pandemic, and numerous countries, including the United States, have declared national emergencies with respect to COVID-19. The outbreak and certain intensified preventative or protective public health measures undertaken by governments, businesses and individuals to contain the spread of COVID-19, including orders to shelter-in-place and restrictions on travel and permitted business operations, have, and continue to, result in global business disruptions that adversely affect workforces, organizations, economies, and financial markets globally, leading to an economic downturn and increased market volatility. The ongoing outbreak has disrupted, and will continue to disrupt, the normal operations of many businesses, including our customers, as well as the ability of our technical support teams and sales force to travel to existing customers and new business prospects, and the operations of our customers and SI partners. We have also limited our in-person marketing activities and expect this will continue for the foreseeable future. For example, we converted our 2020 user conference, Formation, into an online forum called vFormation. While our business has not, to date, experienced a material disruption in bookings or sales from the COVID-19 pandemic, a continued or intensifying outbreak over the short- or medium-term could result in delays in services delivery, delays in implementations, delays in critical development and commercialization activities, including delays in the introduction of new products and services and further international expansion, interruptions in sales and marketing activity, furloughs of employees and disruptions of supply chains. Additionally, we may incur increased costs in the future when employees return to work and we implement measures to ensure their safety.

The related impact on the global economy could also decrease technology spending by our existing and prospective customers and adversely affect their demand for our solutions. Further, our sales and implementation cycles could increase resulting in providing contract terms more favorable to customers and a potentially longer delay between incurring operating expenses and the generation of corresponding revenue or in difficulty in accurately predicting our financial forecasts. Additionally, the economic downturn and rising unemployment rates resulting from COVID-19 have the potential to significantly reduce individual and business disposable income and depress consumer confidence, which could limit the ability or willingness of some consumers to obtain and pay for insurance products in both the short- and medium-term, which may negatively impact the ability of our customers to pay for our services or require such customers to request amended payment terms for their outstanding invoices. Furthermore, we are unable to predict the impact that COVID-19 may have going forward on the business, results of operations or financial position of any of our major customers, which could impact each customer to varying

19

degrees and at different times and could ultimately impact our own financial performance. Certain of our competitors may also be better equipped to weather the impact of COVID-19 both domestically and abroad and better able to address changes in customer demand.

The outbreak also presents operational challenges as our workforce is currently working remotely and assisting customers who are also generally working remotely. We have also suspended international and domestic travel. We depend on key officers and employees; should any of them become ill and unable to work, it could impact our productivity and business continuity. Although we continue to monitor the situation and may adjust our current policies as more information and public health guidance become available, it is not possible for us to predict the duration or magnitude of these business disruptions and the adverse results of the outbreak, which ultimately will depend on many factors, including the speed and effectiveness of containment efforts throughout the world. These disruptions could negatively affect our operations or internal controls over financial reporting and may require us to implement new processes, procedures and controls to respond to further changes in our business environment.