Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - QCR HOLDINGS INC | tm2034236d1_ex99-1.htm |

| 8-K - FORM 8-K - QCR HOLDINGS INC | tm2034236d1_8k.htm |

Exhibit 99.2

|

COVID-19 EXPOSURE Q3 2020 |

|

FORWARD-LOOKING STATEMENTS This document contains, and future oral and written statements of QCR Holdings, Inc. (the “Company”) and its management may contain, forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 with respect to the financial condition, results of operations, plans, objectives, future performance and business of the Company. Forward-looking statements, which may be based upon beliefs, expectations and assumptions of the Company’s management and on information currently available to management, are generally identifiable by the use of words such as “believe,” “expect,” “anticipate,” “predict,” “suggest,” “appear,” “plan,” “intend,” “estimate,” “annualize,” “may,” “will,” “would,” “could,” “should” or other similar expressions. Additionally, all statements in this document, including forward-looking statements, speak only as of the date they are made, and the Company undertakes no obligation to update any statement in light of new information or future events. A number of factors, many of which are beyond the ability of the Company to control or predict, could cause actual results to differ materially from those in its forward-looking statements. These factors include, among others, the following: (i) the strength of the local, state, national and international economies (including the impact of the 2020 presidential election and the impact of tariffs, a U.S. withdrawal from or significant renegotiation of trade agreements, trade wars and other changes in trade regulations); (ii) the economic impact of any future terrorist threats and attacks, widespread disease or pandemics (including the COVID-19 pandemic in the United States), or other adverse external events that could cause economic deterioration or instability in credit markets, and the response of local, state and national governments to any such adverse external events; (iii) changes in accounting policies and practices (including the new current expected credit loss (CECL) impairment standards, that will change how the Company estimates credit losses when implemented); (iv) changes in state and federal laws, regulations and governmental policies concerning the Company’s general business; (v) changes in interest rates and prepayment rates of the Company’s assets (including the impact of LIBOR phase-out); (vi) increased competition in the financial services sector and the inability to attract new customers; (vii) changes in technology and the ability to develop and maintain secure and reliable electronic systems; (viii) unexpected results of acquisitions, which may include failure to realize the anticipated benefits of acquisitions and the possibility that transaction costs may be greater than anticipated; (ix) the loss of key executives or employees; (x) changes in consumer spending; and (xi) unexpected outcomes of existing or new litigation involving the Company. These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. Additional information concerning the Company and its business, including additional factors that could materially affect the Company’s financial results, is included in the Company’s filings with the Securities and Exchange Commission. |

|

PPP & LRP Participation |

|

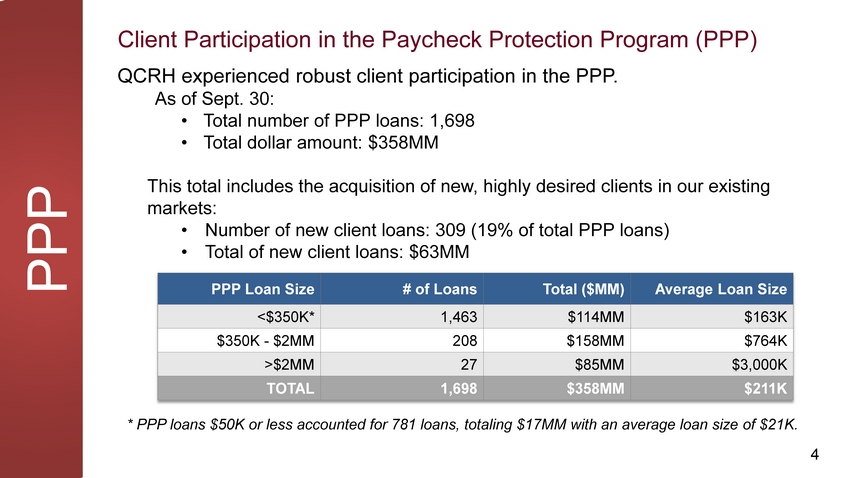

PPP QCRH experienced robust client participation in the PPP. As of Sept. 30: •Total number of PPP loans: 1,698 •Total dollar amount: $358MM This total includes the acquisition of new, highly desired clients in our existing markets: •Number of new client loans: 309 (19% of total PPP loans) •Total of new client loans: $63MM * PPP loans $50K or less accounted for 781 loans, totaling $17MM with an average loan size of $21K. |

|

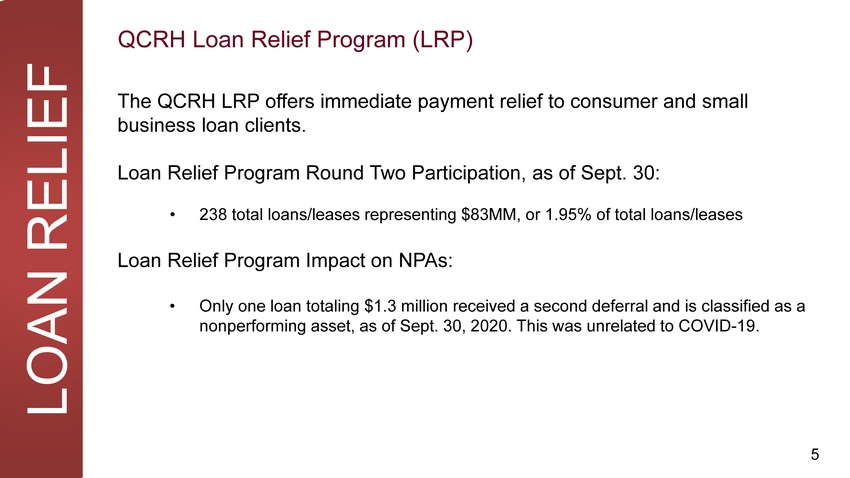

LOAN RELIEF The QCRH LRP offers immediate payment relief to consumer and small business loan clients. Loan Relief Program Round Two Participation, as of Sept. 30: •238 total loans/leases representing $83MM, or 1.95% of total loans/leases Loan Relief Program Impact on NPAs: •Only one loan totaling $1.3 million received a second deferral and is classified as a nonperforming asset, as of Sept. 30, 2020. This was unrelated to COVID-19. |

|

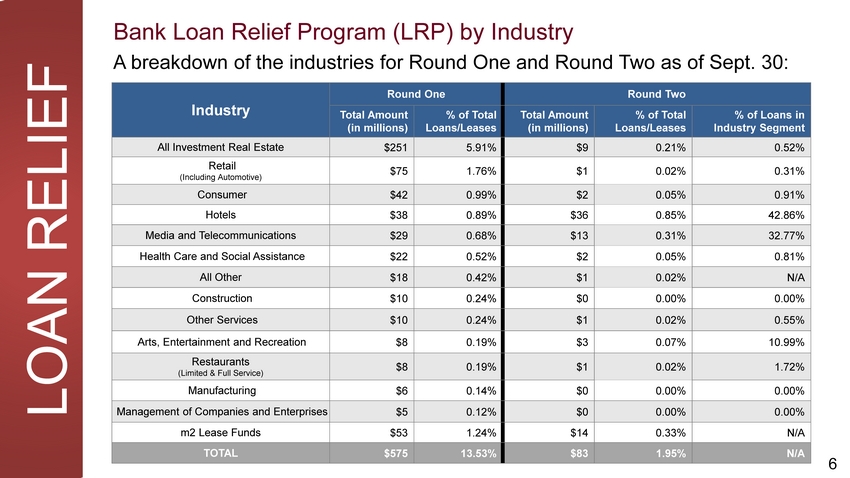

LOAN RELIEF A breakdown of the industries for Round One and Round Two as of Sept. 30: Industry Round One Round Two Total Amount (in millions) % of Total Loans/Leases Total Amount (in millions) % of Total Loans/Leases % of Loans in Industry Segment All Investment Real Estate $251 5.91% $9 0.21% 0.52% Retail (Including Automotive) $75 1.76% $1 0.02% 0.31% Consumer $42 0.99% $2 0.05% 0.91% Hotels $38 0.89% $36 0.85% 42.86% Media and Telecommunications $29 0.68% $13 0.31% 32.77% Health Care and Social Assistance $22 0.52% $2 0.05% 0.81% All Other $18 0.42% $1 0.02% N/A Construction $10 0.24% $0 0.00% 0.00% Other Services $10 0.24% $1 0.02% 0.55% Arts, Entertainment and Recreation $8 0.19% $3 0.07% 10.99% Restaurants (Limited & Full Service) $8 0.19% $1 0.02% 1.72% Manufacturing $6 0.14% $0 0.00% 0.00% Management of Companies and Enterprises $5 0.12% $0 0.00% 0.00% m2 Lease Funds $53 1.24% $14 0.33% N/A TOTAL $575 13.53% $83 1.95% N/A |

|

IndustryConcentration Disclosures |

|

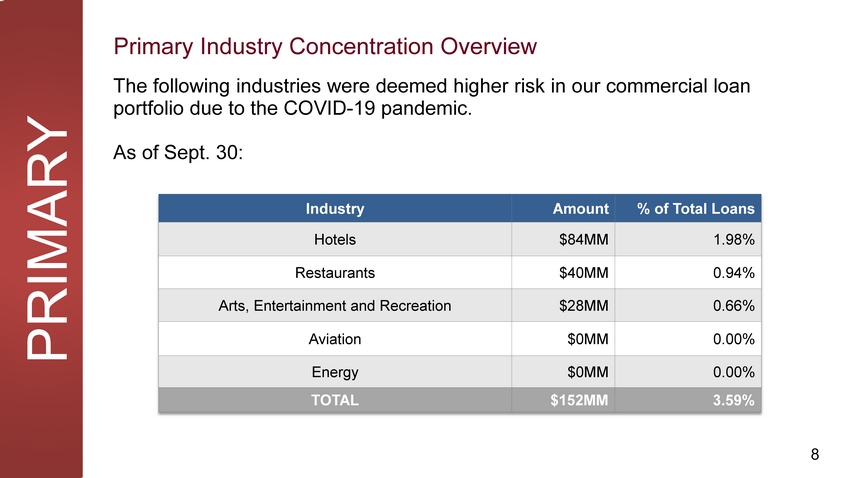

PRIMARY The following industries were deemed higher risk in our commercial loan portfolio due to the COVID-19 pandemic. As of Sept. 30: |

|

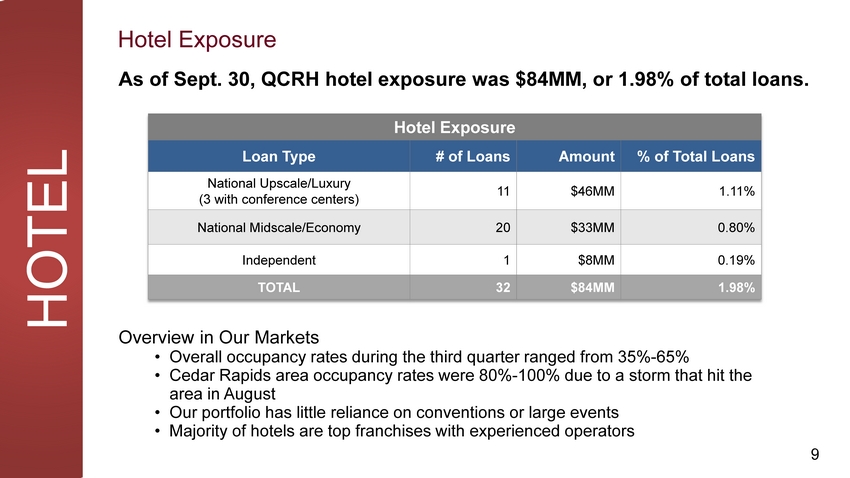

HOTEL As of Sept. 30, QCRH hotel exposure was $84MM, or 1.98% of total loans. Overview in Our Markets •Overall occupancy rates during the third quarter ranged from 35%-65% •Cedar Rapids area occupancy rates were 80%-100% due to a storm that hit the area in August •Our portfolio has little reliance on conventions or large events •Majority of hotels are top franchises with experienced operators |

|

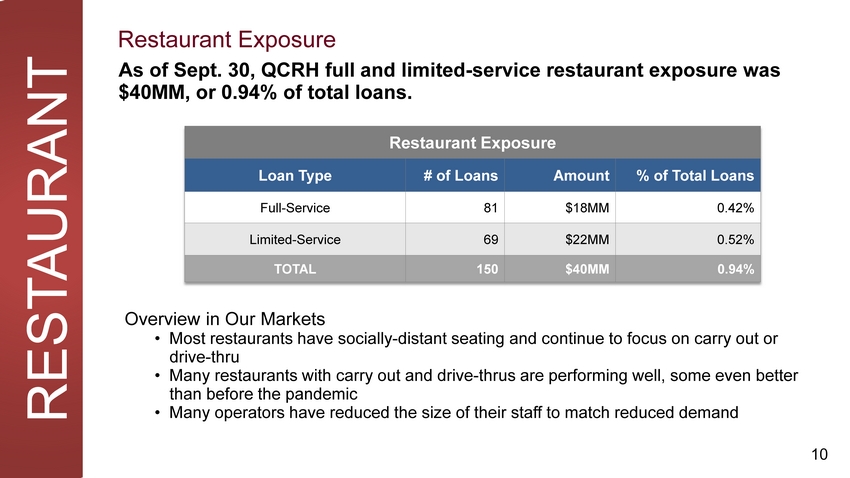

RESTAURANT As of Sept. 30, QCRH full and limited-service restaurant exposure was $40MM, or 0.94% of total loans. Overview in Our Markets •Most restaurants have socially-distant seating and continue to focus on carry out or drive-thru •Many restaurants with carry out and drive-thrus are performing well, some even better than before the pandemic •Many operators have reduced the size of their staff to match reduced demand |

|

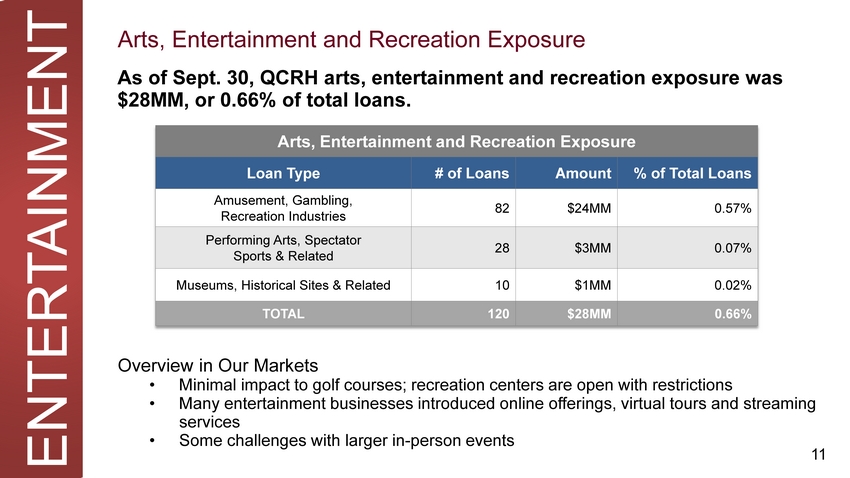

ENTERTAINMENT As of Sept. 30, QCRH arts, entertainment and recreation exposure was $28MM, or 0.66% of total loans. Overview in Our Markets •Minimal impact to golf courses; recreation centers are open with restrictions •Many entertainment businesses introduced online offerings, virtual tours and streaming services •Some challenges with larger in-person events |

|

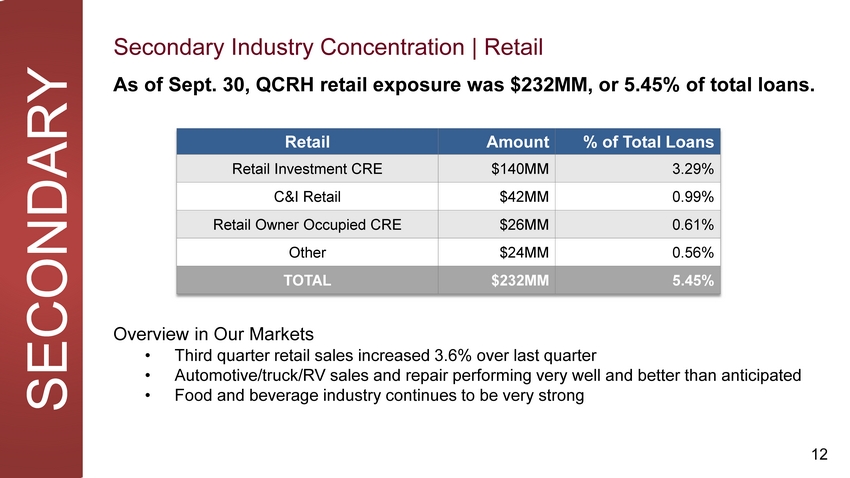

SECONDARY As of Sept. 30, QCRH retail exposure was $232MM, or 5.45% of total loans. Overview in Our Markets •Third quarter retail sales increased 3.6% over last quarter •Automotive/truck/RV sales and repair performing very well and better than anticipated •Food and beverage industry continues to be very strong |

|

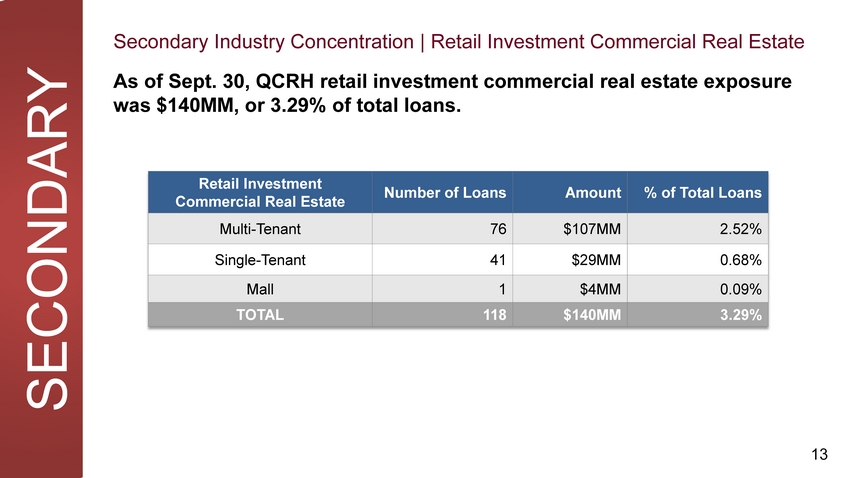

SECONDARY As of Sept. 30, QCRH retail investment commercial real estate exposure was $140MM, or 3.29% of total loans. |

|

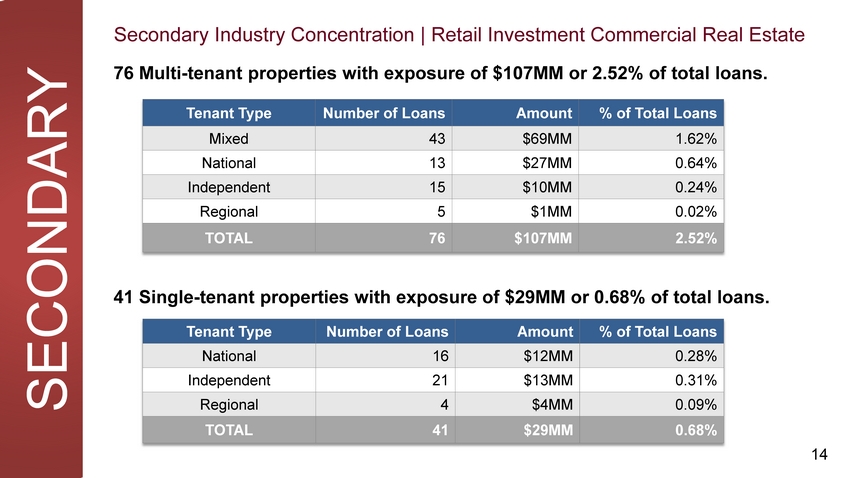

SECONDARY 76 Multi-tenant properties with exposure of $107MM or 2.52% of total loans. 41 Single-tenant properties with exposure of $29MM or 0.68% of total loans. |