Attached files

| file | filename |

|---|---|

| EX-32 - EX-32 - RICHARDSON ELECTRONICS LTD/DE | rell-ex32_10.htm |

| EX-31.2 - EX-31.2 - RICHARDSON ELECTRONICS LTD/DE | rell-ex312_8.htm |

| EX-31.1 - EX-31.1 - RICHARDSON ELECTRONICS LTD/DE | rell-ex311_7.htm |

| EX-23.1 - EX-23.1 - RICHARDSON ELECTRONICS LTD/DE | rell-ex231_6.htm |

| EX-21 - EX-21 - RICHARDSON ELECTRONICS LTD/DE | rell-ex21_9.htm |

| EX-10.2 - EX-10.2 - RICHARDSON ELECTRONICS LTD/DE | rell-ex102_14.htm |

| EX-4 - EX-4 - RICHARDSON ELECTRONICS LTD/DE | rell-ex4_91.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended May 30, 2020

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from__________ to

Commission File Number: 0-12906

(Exact name of registrant as specified in its charter)

|

Delaware |

|

36-2096643 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

40W267 Keslinger Road, P.O. Box 393, LaFox, Illinois 60147-0393

(Address of principal executive offices)

Registrant’s telephone number, including area code: (630) 208-2200

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Common stock, $0.05 Par Value |

|

RELL |

|

NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large Accelerated Filer |

☐ |

|

|

Accelerated Filer |

☒ |

|

Non-Accelerated Filer |

☐ |

|

|

Smaller reporting company |

☒ |

|

Emerging growth company |

☐ |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of November 30, 2019 was approximately $61.4 million.

As of July 27, 2020, there were outstanding 11,110,735 shares of Common Stock, $0.05 par value and 2,096,919 shares of Class B Common Stock, $0.05 par value, which are convertible into Common Stock of the registrant on a one-for-one basis.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the Annual Meeting of Stockholders scheduled to be held October 6, 2020, which will be filed pursuant to Regulation 14A, are incorporated by reference in Part III of this report. Except as specifically incorporated herein by reference, the abovementioned Proxy Statement is not deemed filed as part of this report.

|

|

|

|

Page |

|

|

|

3 |

|

|

Item 1. |

|

3 |

|

|

Item 1A. |

|

6 |

|

|

Item 1B. |

|

13 |

|

|

Item 2. |

|

14 |

|

|

Item 3. |

|

14 |

|

|

|

|

|

|

|

|

|

15 |

|

|

Item 5. |

|

15 |

|

|

Item 6. |

|

17 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

18 |

|

Item 7A. |

|

27 |

|

|

Item 8. |

|

27 |

|

|

Item 9A. |

|

57 |

|

|

Item 9B. |

|

57 |

|

|

|

|

|

|

|

|

|

58 |

|

|

Item 10. |

|

58 |

|

|

Item 11. |

|

58 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

58 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

|

58 |

|

Item 14. |

|

58 |

|

|

|

|

|

|

|

|

|

59 |

|

|

Item 15. |

|

59 |

|

|

Item 16. |

|

60 |

|

|

|

|

|

|

|

|

61 |

||

|

|

63 |

||

2

Certain statements in this report may constitute “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995. The terms “may”, “should”, “could”, “anticipate”, “believe”, “continues”, “estimate”, “expect”, “intend”, “objective”, “plan”, “potential”, “project” and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. These statements are based on management’s current expectations, intentions or beliefs and are subject to a number of factors, assumptions and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. Factors that could cause or contribute to such differences or that might otherwise impact the business include the risk factors set forth in Item 1A of this Form 10-K. We undertake no obligation to update any such factor or to publicly announce the results of any revisions to any forward-looking statements contained herein whether as a result of new information, future events, or otherwise.

In addition, while we do, from time to time, communicate with securities analysts, it is against our policy to disclose to them any material non-public information or other confidential commercial information. Accordingly, stockholders should not assume that we agree with any statement or report issued by any analyst irrespective of the content of the statement or report. Thus, to the extent that reports issued by securities analysts contain any projections, forecasts or opinions, such reports are not our responsibility.

General

Richardson Electronics, Ltd. is a leading global provider of engineered solutions, power grid and microwave tubes and related consumables; power conversion and RF and microwave components; high value flat panel detector solutions, replacement parts, tubes and service training for diagnostic imaging equipment; and customized display solutions. We serve customers in the alternative energy, healthcare, aviation, broadcast, communications, industrial, marine, medical, military, scientific and semiconductor markets. The Company’s strategy is to provide specialized technical expertise and “engineered solutions” based on our core engineering and manufacturing capabilities. The Company provides solutions and adds value through design-in support, systems integration, prototype design and manufacturing, testing, logistics, and aftermarket technical service and repair through its global infrastructure.

Our fiscal year 2020 began on June 2, 2019 and ended on May 30, 2020, our fiscal year 2019 began on June 3, 2018 and ended on June 1, 2019 and our fiscal year 2018 began on May 28, 2017 and ended on June 2, 2018. Unless otherwise noted, all references to a particular year in this document shall mean our fiscal year.

Company Response to COVID-19

On January 30, 2020, the World Health Organization (“WHO”) announced a global health emergency because of a new strain of coronavirus originating in Wuhan, China (the “COVID-19 outbreak”) and the risks to the international community as the virus spreads globally.

In March 2020, the WHO classified the COVID-19 outbreak as a pandemic based on the rapid increase in global exposure. Thereafter, most U.S. states imposed “shelter in place” directives on their populations to stem the spread of COVID-19. Of specific interest to the Company, shelter in place directives were imposed in the states of Illinois, Massachusetts and South Carolina.

The shelter in place directives generally required the closure of businesses that did not provide essential functions. The Company was considered a critical supplier of products to healthcare and critical infrastructure businesses. Several of our largest customers mandated that we continue to supply parts so as not to disrupt the supply chain and their ability to serve critical industries. As such, the Company qualified as an “Essential Business”. Essential Businesses were allowed to continue to operate during shelter in place directives. We continued our manufacturing and distribution operations even when a shelter in place directive was issued. We limited the number of people in any one of our facilities by requiring only employees who could not perform their work remotely to physically work in a Company US-based facility. The Company advised all other employees that could perform their job functions remotely to do so. As such, the Company’s operations remained operational.

3

The impact of the COVID-19 outbreak continues to evolve. As such, the full magnitude that the pandemic will have on the Company’s financial condition, liquidity and future results of operations is uncertain. Management is actively monitoring the global situation on its financial condition, liquidity, operations, suppliers, industry and workforce. As the spread of COVID-19 continues, our ability to meet customer demands for products may be impaired or, similarly, our customers may experience adverse business consequences due to COVID-19. Reduced demand for products or impaired ability to meet customer demand (including disruptions at our transportation service providers or vendors) could have a material adverse effect on our business, operations and financial performance. Some of the decline in fiscal 2020 PMT sales and the decrease in Healthcare sales was primarily due to the COVID-19 global pandemic. While we had some COVID-19 related longer lead times as well as delays impacting new product development schedules, we did not experience a major interruption in our supply chain. Given the daily evolution of the COVID-19 outbreak and the global responses to curb its spread, the Company is not presently able to estimate the effects of COVID-19 on its results of operations, financial condition or liquidity for fiscal year 2021.

Company Response to CARES Act

On March 27, 2020, Congress enacted the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act to provide certain relief as a result of the COVID-19 outbreak. The CARES Act includes provisions relating to refundable payroll tax credits, deferral of employer side social security payments, net operating loss carryback periods, alternative minimum tax credit refunds, increased limitations on qualified charitable contributions and technical corrections to tax depreciation methods for qualified improvement property. The Company continues to examine how these provisions in the CARES Act will impact its financial position, results of operations and cash flows. In fiscal 2020, the Company deferred $0.2 million of employer side social security tax payments. The Company has estimated and recorded the overall effects of the CARES Act and does not anticipate a material change.

Geography

We currently have operations in the following major geographic regions: North America, Asia/Pacific, Europe and Latin America.

Selected financial data attributable to each segment and geographic region for fiscal 2020, fiscal 2019 and fiscal 2018 is set forth in Note 11 “Segment and Geographic Information” of the notes to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K.

We have three operating and reportable segments, which we define as follows:

Power and Microwave Technologies Group

Power and Microwave Technologies Group (“PMT”) combines our core engineered solutions capabilities, power grid and microwave tube business with new RF, Wireless and Power disruptive technologies. As a designer, manufacturer, technology partner and authorized distributor, PMT’s strategy is to provide specialized technical expertise and engineered solutions based on our core engineering and manufacturing capabilities on a global basis. We provide solutions and add value through design-in support, systems integration, prototype design and manufacturing, testing, logistics and aftermarket technical service and repair—all through our existing global infrastructure. PMT’s focus is on products for power, RF and microwave applications for customers in 5G, alternative energy, aviation, broadcast, communications, industrial, marine, medical, military, scientific and semiconductor markets. PMT focuses on various applications including broadcast transmission, CO2 laser cutting, diagnostic imaging, dielectric and induction heating, high energy transfer, high voltage switching, plasma, power conversion, radar and radiation oncology. PMT also offers its customers technical services for both microwave and industrial equipment.

PMT represents leading manufacturers of electron tubes and RF, Microwave and power components used in semiconductor manufacturing equipment, RF and wireless and industrial power applications. Among the suppliers PMT supports are Amperex, CDE, CPI, Draloric, Eimac, General Electric, Hitachi, Jennings, L3, MACOM, National, NJRC, Ohmite, Qorvo, Thales, Toshiba and Vishay.

PMT’s inventory levels reflect our commitment to maintain an inventory of a broad range of products for customers who are buying products for replacement of components used in critical equipment and designing in new technologies. PMT also sells a number of products representing trailing edge technology. While the market for these trailing edge technology products is declining, PMT is increasing its market share. PMT often buys products it knows it can sell ahead of any supplier price increases and extended lead times. As manufacturers for these products exit the business, PMT has the option to purchase a substantial portion of their remaining inventory.

4

PMT has distribution agreements with many of its suppliers; most of these agreements provide exclusive distribution rights that often include global coverage. The agreements are typically long term, and usually contain provisions permitting termination by either party if there are significant breaches that are not cured within a reasonable period. Although some of these agreements allow PMT to return inventory periodically, others do not, in which case PMT may have obsolete inventory that they cannot return to the supplier.

PMT’s suppliers provide warranty coverage for the products and allow return of defective products, including those returned to PMT by its customers. For information regarding the warranty reserves, see Note 3 “Significant Accounting Policies” of the notes to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K.

In addition to third party products, we sell proprietary products principally under certain trade names we own including Amperex®, Cetron® and National®. Our proprietary products include thyratrons and rectifiers, power tubes, ignitrons, magnetrons, phototubes, microwave generators, Ultracapacitor modules and liquid crystal display monitors. The materials used in the manufacturing process consist of glass bulbs and tubing, nickel, stainless steel and other metals, plastic and metal bases, ceramics and a wide variety of fabricated metal components. These materials are generally readily available, but some components may require long lead times for production, and some materials are subject to shortages or price fluctuations based on supply and demand.

Canvys – Visual Technology Solutions

Canvys provides customized display solutions serving the corporate enterprise, financial, healthcare, industrial and medical original equipment manufacturers markets. Our engineers design, manufacture, source and support a full spectrum of solutions to match the needs of our customers. We offer long term availability and proven custom display solutions that include touch screens, protective panels, custom enclosures, All-In-One computers, specialized cabinet finishes and application specific software packages and certification services. Our volume commitments are lower than the large display manufacturers, making us the ideal choice for companies with very specific design requirements. We partner with both private label manufacturing companies and leading branded hardware vendors to offer the highest quality display and touch solutions and customized computing platforms.

We have long-standing relationships with key component and finished goods manufacturers and several key ISO 9001 and ISO 13485 certified Asian display manufacturers that manufacture products to our specifications. We believe supplier relationships, combined with our engineering design and manufacturing capabilities and private label partnerships, allow us to maintain a well-balanced and technologically advanced offering of customer specific display solutions.

Healthcare

Healthcare manufactures, repairs, refurbishes and distributes high value replacement parts and equipment for the healthcare market including hospitals, medical centers, asset management companies, independent service organizations and multi-vendor service providers. Products include diagnostic imaging replacement parts for CT and MRI systems; replacement CT and MRI tubes; CT service training; MRI coils, cold heads and RF amplifiers; hydrogen thyratrons, klystrons, magnetrons; flat panel detector upgrades; pre-owned CT systems; and additional replacement solutions currently under development for the diagnostic imaging service market. Through a combination of newly developed products and partnerships, service offerings and training programs, we believe we can help our customers improve efficiency and deliver better clinical outcomes while lowering the cost of healthcare delivery.

Sales and Product Management

We have employees, as well as authorized representatives who are not our employees, selling our products primarily in regions where we do not have a direct sales presence.

We offer various credit terms to qualifying customers as well as cash in advance and credit card terms. We establish credit limits for each customer and routinely review delinquent and aging accounts.

5

Distribution

We maintain approximately 110,700 part numbers in our product inventory database and we estimate that more than 90% of orders received by 6:00 p.m. local time are shipped complete the same day for stock product. Customers can access our products on our web sites, www.rell.com, www.rellhealthcare.com, www.canvys.com, www.rellpower.com, www.relltubes.com and www.rellaser.com, through electronic data interchange, or by telephone. Customer orders are processed by our regional sales offices and supported primarily by one of our distribution facilities in LaFox, Illinois; Fort Mill, South Carolina; Amsterdam, Netherlands; Marlborough, Massachusetts; Donaueschingen, Germany; or Singapore, Singapore. We also have satellite warehouses in Sao Paulo, Brazil; Shanghai, China; Bangkok, Thailand; and Hook, United Kingdom. Our data processing network provides on-line, real-time interconnection of all sales offices and central distribution operations, 24 hours per day, seven days per week. Information on stock availability, pricing in local currency, cross-reference information, customers and market analyses are obtainable throughout the entire distribution network.

International Sales

During fiscal 2020, we made approximately 59% of our sales outside the U.S. We continue to pursue new international sales to further expand our geographic reach.

Major Customers

During fiscal 2020 and fiscal 2019, no one customer accounted for more than 10 percent of the Company’s consolidated net sales. During fiscal 2018, LAM Research Corporation individually accounted for 11 percent of the Company’s consolidated net sales. No other customer accounted for more than 10 percent of the Company’s consolidated net sales in fiscal 2018. The Company believes that the loss of this customer would have a material adverse effect on the Company’s financial condition or results of operations. See Note 11 “Segment and Geographic Information” of the notes to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K for further information.

Employees

As of May 30, 2020, we employed 394 individuals. All of our employees are non-union and we consider our relationships with our employees to be good.

Website Access to SEC Reports

We maintain an Internet website at www.rell.com. Our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934 are accessible through our website, free of charge, as soon as reasonably practicable after these reports are filed electronically with the Securities and Exchange Commission. Interactive Data Files pursuant to Rule 405 of Regulation S-T, of these filing dates, formatted in Extensible Business Reporting Language (“XBRL”) are accessible as well. To access these reports, go to our website at www.rell.com. The foregoing information regarding our website is provided for convenience and the content of our website is not deemed to be incorporated by reference in this report filed with the Securities and Exchange Commission.

Investors should consider carefully the following risk factors in addition to the other information included and incorporated by reference in this Annual Report on Form 10-K that we believe are applicable to our businesses and the industries in which we operate. While we believe we have identified the key risk factors affecting our businesses, there may be additional risks and uncertainties that are not presently known or that are not currently believed to be significant that may adversely affect our results of operations.

A significant portion of our cash, cash equivalents and investments are held by our foreign subsidiaries and could affect future liquidity needs.

As of May 30, 2020, $16.2 million, or approximately 35% of our cash, cash equivalents and investments was held by our foreign subsidiaries. While we intend to use some of the cash held outside the United States to fund our international operations and growth, when we encounter a significant need for liquidity domestically or at a particular location that we cannot fulfill through other internal or external sources, our liquidity requirements could necessitate transfers of existing cash balances between our subsidiaries or to the United States. Some of these subsidiaries are located in jurisdictions that require foreign government approval before a cash repatriation can occur.

6

We may not achieve our plan for sales growth and margin targets.

We have established both margin and expense targets to grow our sales with new and existing customers. If we do not achieve our growth objectives, the complexity of our global infrastructure makes it difficult to leverage our fixed cost structure to align with the size of our operations. Factors that could have a significant effect on our ability to achieve these goals include the following:

|

|

• |

Failure to achieve our sales and margin growth objectives in our product lines and business units; |

|

|

• |

Failure to identify, consummate and successfully integrate acquisitions; |

|

|

• |

Declining gross margin reflecting competitive pricing pressures or product mix; and |

|

|

• |

Limitations on our ability to leverage our support-function cost structure while maintaining an adequate structure to achieve our growth objectives. |

We have historically incurred significant charges for inventory obsolescence, and may incur similar charges in the future.

We maintain significant inventories in an effort to ensure that customers have a reliable source of supply. Our products generally support industrial machinery powered by tube technology. As technology evolves and companies replace this capital equipment, the market for our products potentially declines. In addition, the market for many of our other products changes rapidly resulting from the development of new technologies, evolving industry standards, frequent new product introductions by some of our suppliers and changing end-user demand, which can contribute to the decline in value or obsolescence of our inventory. We do not have many long-term supply contracts with our customers. If we fail to anticipate the changing needs of our customers or we do not accurately forecast customer demand, our customers may not place orders with us, and we may accumulate significant inventories of products that we may be unable to sell or return to our vendors. This may result in a decline in the value of our inventory.

We face competitive pressures that could have a material adverse effect on our business.

Our overall competitive position depends on a number of factors including price, engineering capability, vendor representation, product diversity, lead times and the level of customer service. There are very few vacuum tube competitors in the markets we serve. There are also a limited number of Chinese manufacturers whose ability to produce vacuum tubes has progressed over the past several years. The most significant competitive risk comes from technical obsolescence. Canvys faces many competitors in the markets we serve. Increased competition may result in price reductions, reduced margins, or a loss of market share, any of which could materially and adversely affect our business, operating results, and financial condition. As we expand our business and pursue our growth initiatives, we may encounter increased competition from current and/or new competitors. Our failure to maintain and enhance our competitive position could have a material adverse effect on our business.

A single stockholder has voting control over us.

As of July 27, 2020, Edward J. Richardson, our Chairman, Chief Executive Officer and President, beneficially owned approximately 99% of the outstanding shares of our Class B common stock, representing approximately 65% of the voting power of the outstanding common stock. This share ownership permits Mr. Richardson to exert control over the outcome of stockholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests, and other significant corporate transactions.

Failure to attract and retain key skilled personnel could hurt operations.

Our success depends to a large extent upon the continued services of key management personnel, particularly Mr. Richardson. While we have employment contracts in place with several of our executive officers, we nevertheless cannot be assured that we will retain our key employees and the loss of service of any of these officers or key management personnel could have a material adverse effect on our business growth and operating results.

Our future success will require an ability to attract and retain qualified employees. Competition for such key personnel is intense and we cannot be assured that we will be successful in attracting and retaining such personnel. We cannot make assurances that key personnel will not depart in the future. Changes in the cost of providing employee benefits in order to attract and retain personnel, including changes in health care costs, could lead to increased costs in any of our operations.

7

We are dependent on a limited number of vendors to supply us with essential products.

The products we supply are currently produced by a relatively small number of manufacturers. One of our suppliers represented 16 percent of our total cost of sales. Our success depends, in large part, on maintaining current vendor relationships and developing new relationships. To the extent that our significant suppliers are unwilling or unable to continue to do business with us, extend lead times, limit supplies due to capacity constraints, or other factors, there could be a material adverse effect on our business.

International operations represent a significant percentage of our business and present a variety of risks that could impact our results.

Because we source and sell our products worldwide, our business is subject to risks associated with doing business internationally. These risks include the costs and difficulties of managing foreign entities, limitations on the repatriation and investment of funds, cultural differences that affect customer preferences and business practices, unstable political or economic conditions, trade protection measures and import or export licensing requirements, and changes in tax laws.

We also face exposure to fluctuations in foreign currency exchange rates because we conduct business outside of the United States. Price increases caused by currency exchange rate fluctuations may make our products less competitive or may have an adverse effect on our margins. Our international revenues and expenses generally are derived from sales and operations in currencies other than the U.S. dollar. Accordingly, when the U.S. dollar strengthens in relation to the base currencies of the countries in which we sell our products, our U.S. dollar reported net revenue and income would decrease. We currently do not engage in any currency hedging transactions. We cannot predict whether foreign currency exchange risks inherent in doing business in foreign countries will have a material adverse effect on our operations and financial results in the future. Further, global economic conditions may cause volatility and disruptions in the capital and credit markets. Negative or uncertain financial and macroeconomic conditions may have a significant adverse impact on our sales, profitability, and results of operations.

We may need to raise additional funds through debt or equity financings in the future to fund our domestic operations and our broader corporate initiatives, which would dilute the ownership of our existing shareholders.

If the cash generated by our domestic operations is not sufficient to fund our domestic operations and our broader corporate initiatives, such as stock repurchases, dividends, acquisitions, and other strategic opportunities, we may need to raise additional funds through public or private debt or equity financings, or we may need to obtain new credit facilities to the extent we are unable to, or choose not to, repatriate our overseas cash. Such additional financing may not be available on terms favorable to us, or at all, and any new equity financings or offerings would dilute our current stockholders’ ownership interests in us. Furthermore, lenders may not agree to extend us new, additional or continuing credit. The COVID-19 pandemic and its economic impact could result in significant or sustained disruption of global financial markets, thereby reducing our ability to access capital. In any such case, our business, operating results or financial condition could be adversely impacted.

The withdrawal by the United Kingdom from the European Union could have a material adverse effect on our business, financial position, liquidity and results of operations.

We conduct a significant portion of our business in the European Union (“EU”) and in June 2016, voters approved the withdrawal of the United Kingdom (“U.K.”) from the EU (also referred to as “Brexit”). The U.K. left the EU on January 31, 2020, and is currently in an 11-month transition period following which it will leave the single market and customs union pursuant to terms of a trade agreement currently being negotiated by the U.K. and the EU. The terms of this trade agreement are uncertain, and the political and economic instability created by Brexit caused and may continue to cause significant volatility in global markets. Further, the terms ultimately reached may result in greater restrictions on imports and exports between the U.K. and EU countries, a fluctuation in currency exchange rates and increased regulatory complexities. The impact of the withdrawal of the U.K. may adversely affect business activity, political stability and economic conditions in the U.K., the EU and elsewhere. Such developments and their ultimate impact, or the perception that any of these developments are likely to occur, could have a material adverse effect on economic growth or business activity in the U.K., the Eurozone, or the EU, and could result in the relocation of businesses, cause business interruptions, lead to economic recession or depression, and impact the stability of the financial markets, availability of credit, political systems or financial institutions and the financial and monetary system.

Such developments could have a material adverse effect on our business, financial position, liquidity and results of operations. The uncertainty concerning the terms of the exit could also have a negative impact on the growth of the European economy and cause greater volatility in all of the global currencies that we currently use to transact business.

8

We rely heavily on information technology systems that, if not properly functioning, could materially adversely affect our business.

We rely on our information technology systems to process, analyze, and manage data to facilitate the purchase, manufacture, and distribution of our products, as well as to receive, process, bill, and ship orders on a timely basis. A significant disruption or failure in the design, operation, security or support of our information technology systems could significantly disrupt our business.

Our information technology systems may be subject to cyber attacks, security breaches or computer hacking. Experienced computer programmers and hackers may be able to penetrate our security controls and misappropriate or compromise sensitive personal, proprietary or confidential information, create system disruptions or cause shutdowns. They also may be able to develop and deploy viruses, worms and other malicious software programs that attack our systems or otherwise exploit any security vulnerabilities. Additionally, third parties may attempt to fraudulently induce employees or customers into disclosing sensitive information such as user names, passwords or other information in order to gain access to our customers’ data or our data, including our intellectual property and other confidential business information, employee information or our information technology systems. Our systems and the data stored on those systems may also be vulnerable to security incidents or security attacks, acts of vandalism or theft, coordinated attacks by activist entities, misplaced or lost data, human errors, or other similar events that could negatively affect our systems and its data, as well as the data of our business partners. Further, third parties, such as hosted solution providers, that provide services to us, could also be a source of security risk in the event of a failure of their own security systems and infrastructure.

The costs to mitigate or address security threats and vulnerabilities before or after a cyber incident could be significant. Our remediation efforts may not be successful and could result in interruptions, delays or cessation of service, and loss of existing or potential suppliers or customers. In addition, breaches of our security measures and the unauthorized dissemination of sensitive personal, proprietary or confidential information about us, our business partners or other third parties could expose us to significant potential liability and reputational harm. As threats related to cyber attacks develop and grow, we may also find it necessary to make further investments to protect our data and infrastructure, which may impact our profitability. As a global enterprise, we could also be negatively impacted by existing and proposed laws and regulations, as well as government policies and practices related to cybersecurity, privacy, data localization and data protection.

Our products may be found to be defective or our services performed may result in equipment or product damage and, as a result, warranty and/or product liability claims may be asserted against us.

We sell many of our components at prices that are significantly lower than the cost of the equipment or other goods in which they are incorporated. Since a defect or failure in a product could give rise to failures in the equipment that incorporates them, we may face claims for damages that are disproportionate to the revenues and profits we receive from the components involved in the claims. While we typically have provisions in our agreements with our suppliers that hold the supplier accountable for defective products, and we and our suppliers generally exclude consequential damages in our standard terms and conditions, our ability to avoid such liabilities may be limited as a result of various factors, including the inability to exclude such damages due to the laws of some of the countries where we do business. Our business could be adversely affected as a result of a significant quality or performance issues in the components sold by us if we are required to pay for the damages. Although we have product liability insurance, such insurance is limited in coverage and amount.

Substantial defaults by our customers on our accounts receivable or the loss of significant customers could have a significant negative impact on our business.

We extend credit to our customers. The failure of a significant customer or a significant group of customers to timely pay all amounts due could have a material adverse effect on our financial condition and results of operations. The extension of credit involves considerable judgment and is based on management’s evaluation of factors that include such things as a customer’s financial condition, payment history, and the availability of collateral to secure customers’ receivables.

Failure to successfully implement our growth initiatives, or failure to realize the benefits expected from these initiatives if implemented, may create ongoing operating losses or otherwise adversely affect our business, operating results and financial condition.

Our growth strategy focuses on expanding our healthcare and our power conversion businesses. In 2015, we acquired certain assets, including inventory, receivables, fixed assets and certain other assets, of International Medical Equipment and Services, Inc. (“IMES”) and launched Power and Microwave Technologies Group (“PMT”), which combines our core engineered solutions, power grid and microwave tube business with new RF and power technologies. We may be unable to implement our growth initiatives or reach profitability in the near future or at all, due to many factors, including factors outside of our control. If our investments in these growth initiatives do not yield anticipated returns for any reason, our business, operating results and financial condition may be adversely affected.

9

We may not be successful in identifying, consummating and integrating future acquisitions.

As part of our growth strategy, our intent is to acquire additional businesses or assets. We may not be able to identify attractive acquisition candidates or complete the acquisition of identified candidates at favorable prices and upon advantageous terms. Also, acquisitions are accompanied by risks, such as potential exposure to unknown liabilities and the possible loss of key employees and customers of the acquired business. In addition, we may not obtain the expected benefits or cost savings from acquisitions. Acquisitions are subject to risks associated with financing the acquisition, and integrating the operations, personnel and systems of the acquired businesses. If any of these risks materialize, they may result in disruptions to our business and the diversion of management time and attention, which could increase the costs of operating our existing or acquired businesses or negate the expected benefits of the acquisitions.

Economic weakness and uncertainty could adversely affect our revenues and gross margins.

Our revenues and gross profit margins depend significantly on global economic conditions, the demand for our products and services and the financial condition of our customers. Economic weakness and uncertainty have in the past, and may in the future, result in decreased revenues and gross profit margins. Economic uncertainty also makes it more difficult for us to forecast overall supply and demand with a great deal of confidence. Financial turmoil affecting the banking system and financial markets could result in tighter credit markets and lower levels of liquidity in some financial markets. The effects of a tightened credit environment could include the insolvency of key vendors or their inability to obtain credit to finance development and/or manufacture products resulting in product delays as well as the inability of customers to obtain credit to finance operations and/or customer insolvencies. Spending and the timing thereof by our customers may have a significant impact on our results and, where such spending is delayed or cancelled, it could have a material negative impact on our operating results. Current global economic conditions remain uncertain and challenging. Weakness in the markets in which we operate could negatively impact our revenue and operating expenses, and consequently have a material adverse effect on our business, financial condition and results of operations.

Our operating results during fiscal 2020 and fiscal 2019 reflected a net loss, while we reported net income for fiscal 2018. There can be no assurance that we will experience recovery in the near future; nor is there any assurance that such worldwide economic volatility experienced recently will not continue.

Major disruptions to our logistics capability or to the operations of our key vendors or customers could have a material adverse impact on our operations.

We operate our global logistics services through specialized and centralized distribution centers. We depend on third party transportation service providers for the delivery of products to our customers. A major interruption or disruption in service at any of our distribution centers, or a disruption at the operations of any of our significant vendors or customers, for any reason, including reasons beyond our control (such as natural disasters, pandemics (such as the outbreak of a novel strain of coronavirus, now known as COVID-19), work stoppages, power loss, cyber attacks, incidents of terrorism or other significant disruptions of services from our third party providers) could cause cancellations or delays in a significant number of shipments to customers and, as a result, could have a severe impact on our business, operations and financial performance.

In December 2019, an outbreak of COVID-19 virus originated in Wuhan, China, and has since spread to a number of other countries, including the United States. The outbreak and actions taken by the Chinese government resulted in travel restrictions and extended shutdowns of certain businesses in the region. As a result, we experienced cancellations and delays in shipments to our customers in China as well as receiving shipments from our vendors in China during our third and fourth quarters of fiscal 2020. On January 30, 2020, the World Health Organization (“WHO”) announced a global health emergency and the risks to the international community as the virus spreads globally. In March 2020, the WHO classified the COVID-19 outbreak as a pandemic, based on the rapid increase in global exposure. In response, the governments of many countries, states, cities and other geographic regions (including areas in which we have operations) took preventative or protective actions, such as imposing restrictions on business operations and requiring individuals to stay at home. As the impact of the spread of the COVID-19 outbreak continues to be felt, our ability to meet customer demands for products may be impaired or, similarly, our customers may experience adverse business consequences due to COVID-19. A resulting reduced demand for products or impaired ability to meet customer demand (including disruptions at our transportation service providers or vendors) could cause a material adverse effect on our business, operations and financial performance. Even after the COVID-19 pandemic subsides, we may experience adverse impacts to our business and financial results due to any economic recession or depression that has occurred, and due to any major public health crises that may occur in the future. This is a very dynamic situation and we cannot at this time reasonably estimate the scope of its impact on our employees, operations, suppliers, or customers, or the full extent to which COVID-19 could continue to affect the global economy and our results. The potential effects of COVID-19 also could impact many of our risk factors described herein; however, as this is an unprecedented and changing situation, the potential impacts to such risk factors remain uncertain.

10

Our business and results of operations are subject to a broad range of uncertainties arising out of world and domestic events.

Our business and results of operations are subject to uncertainties arising out of world and domestic events. These uncertainties may include a global economic slowdown, pandemics and other public health issues (including the COVID-19 pandemic), natural disasters, military action, terrorist activities, political and social turmoil, civil unrest and other crises. Such conditions may impact customer demand as well as our suppliers’ ability to supply us with necessary materials and, ultimately, may have an impact on our business, financial condition, results and stock price.

We may be subject to intellectual property rights claims, which are costly to defend, could require payment of damages or licensing fees, and/or could limit our ability to use certain technologies in the future.

Substantial litigation and threats of litigation regarding intellectual property rights exist in the display systems and electronics industries. From time to time, third parties, including certain companies in the business of acquiring patents with the intention of aggressively seeking licensing revenue from purported infringers, may assert patent and/or other intellectual property rights to technologies that are important to our business. In any dispute involving products that we have sold, our customers could also become the target of litigation. We are obligated in many instances to indemnify and defend our customers if the products we sell are alleged to infringe any third party’s intellectual property rights. In some cases, depending on the nature of the claim, we may be able to seek indemnification from our suppliers for our self and our customers against such claims, but there is no assurance that we will be successful in obtaining such indemnification or that we are fully protected against such claims. Any infringement claim brought against us, regardless of the duration, outcome or size of damage award, could result in substantial cost, divert our management’s attention, be time consuming to defend, result in significant damage awards, cause product shipment delays, or require us to enter into royalty or other licensing agreements. See Note 12 “Risks and Uncertainties” of the notes to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K for further information regarding specific legal matters related to our patents.

Additionally, if an infringement claim is successful we may be required to pay damages or seek royalty or license arrangements which may not be available on commercially reasonable terms. The payment of any such damages or royalties may significantly increase our operating expenses and harm our operating results and financial condition. Also, royalty or license arrangements may not be available at all. We may have to stop selling certain products or certain technologies, which could affect our ability to compete effectively.

Potential lawsuits, with or without merit, may divert management’s attention, and we may incur significant expenses in our defense. In addition, we may be required to pay damage awards or settlements, become subject to injunctions or other equitable remedies, or determine to abandon certain lines of business, that may cause a material adverse effect on our results of operations, financial position, and cash flows.

If we fail to maintain an effective system of internal controls or discover material weaknesses in our internal controls over financial reporting, we may not be able to detect fraud or report our financial results accurately or timely.

An effective internal control environment is necessary for us to produce reliable financial reports and is an important part of our effort to prevent financial fraud. We are required to periodically evaluate the effectiveness of the design and operation of our internal controls over financial reporting. Based on these evaluations, we may conclude that enhancements, modifications, or changes to internal controls are necessary or desirable. While management evaluates the effectiveness of our internal controls on a regular basis, these controls may not always be effective. There are inherent limitations on the effectiveness of internal controls, including fraud, collusion, management override, and failure in human judgment. In addition, control procedures are designed to reduce rather than eliminate business risks.

If we fail to maintain an effective system of internal controls, or if management or our independent registered public accounting firm discovers material weaknesses in our internal controls, we may be unable to produce reliable financial reports or prevent fraud. In addition, we may be subject to sanctions or investigation by regulatory authorities, such as the Securities and Exchange Commission or NASDAQ. Any such actions could result in an adverse reaction in the financial markets due to a loss of confidence in the reliability of our financial statements.

If we are deemed to be an investment company, we will be required to meet burdensome compliance requirements and restrictions on our activities.

We currently have significant cash and investments. If we are deemed to be an “investment company” as defined under the Investment Company Act of 1940 (the “Investment Company Act”), the nature of our investments may be subject to various restrictions. We do not believe that our principal activities subject us to the Investment Company Act. If we are deemed to be subject to the Investment Company Act, compliance with required additional regulatory burdens would increase our operating expenses.

11

The company recorded a non-cash impairment charge for the full value of our goodwill and there remains the risk of possible additional future identifiable intangible asset impairment, which could reduce the value of our assets and reduce our net income in the year in which the write-off occurs.

In the fourth quarter of fiscal 2019, the Company recorded a non-cash goodwill impairment charge of $6.3 million for the full amount of the goodwill associated with the IMES reporting unit. The impairment resulted from fourth quarter events that decreased the forecasted future cash flows and the fair value of the IMES reporting unit below its carrying value as of the March 3, 2019 testing date. Refer to Note 7 “Goodwill and Intangible Assets” of the notes to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K. Our remaining intangible assets could become impaired, which could reduce the value of our assets and reduce our net income in the year in which the write-off occurs. We ascribe value to certain intangible assets, which consist of customer lists and trade names resulting from acquisitions. An impairment charge on intangible assets would be incurred in the event that the fair value of the intangible assets are less than their current carrying values. We evaluate whether events have occurred that indicate all, or a portion, of the carrying amount of intangible assets may no longer be recoverable. If this is the case, an impairment charge to earnings would be necessary.

We may incur substantial operational costs or be required to change our business practices to comply with the General Data Protection Regulation and similar regulations.

The EU adopted the General Data Protection Regulation (“GDPR”) which went into effect in May 2018. The GDPR includes operational requirements for companies that receive or process personal data of residents of the European Union, including more robust documentation requirements for data protection compliance programs. Specifically, the GDPR introduced numerous privacy-related changes for companies operating in the EU, including greater control for data subjects, increased data portability for EU consumers, and data breach notification requirements.

Complying with the GDPR may cause us to incur substantial operational costs or require us to change our business practices in ways that we cannot currently predict. Despite our efforts to bring our practices into compliance with the GDPR, we may not be successful. Non-compliance could result in proceedings against us by governmental entities, customers, data subjects or others. Fines of up to 20 million euros or up to 4% of the annual global revenue of the noncompliant company, whichever is greater, may be imposed for violations of certain of the GDPR’s requirements.

In addition, several other jurisdictions in the U.S. and around the world have recently enacted privacy laws or regulations similar to GDPR. For instance, California enacted the California Consumer Privacy Act (“CCPA”), which was effective January 1, 2020 and which gives consumers many of the same rights as those available under GDPR. Several laws similar to the CCPA have been proposed in the United States at both the federal and state level. The effects of the GDPR, the CCPA and other data privacy laws and regulations may be significant, and may require us to modify our data processing practices and policies and to incur substantial costs and expenses in an effort to comply. Any actual or perceived failures to comply with the GDPR, the CCPA or other data privacy laws or regulations, or related contractual or other obligations, or any perceived privacy rights violation, could lead to investigations, claims, and proceedings by governmental entities and private parties, damages for contract breach, and other significant costs, penalties, and other liabilities, as well as harm to our reputation and market position.

Our international sales and operations are subject to applicable laws relating to trade, export controls and foreign corrupt practices, the violation of which could adversely affect our operations.

We are subject to applicable export control laws and regulations of the United States and other countries. United States laws and regulations applicable to us include the Arms Export Control Act, the International Traffic in Arms Regulations (“ITAR”), the Export Administration Regulations (“EAR”) and the trade and trade sanctions laws and regulations administered by the Office of the United States Trade Representative and the United States Department of the Treasury’s Office of Foreign Assets Control. The import and export of our products are subject to international trade agreements, the modification or repeal of which could impact our business. The U.S. government agencies responsible for administering EAR and ITAR have significant discretion in the interpretation and enforcement of these regulations. Violations of these laws or regulations could result in significant additional sanctions including fines, more onerous compliance requirements, more extensive debarments from export privileges, loss of authorizations needed to conduct aspects of our international business and criminal penalties and may harm our ability to enter contracts with customers who have contracts with the U.S. government. A violation of the laws or the regulations enumerated above could materially adversely affect our business, financial condition and results of operations.

New tariffs and the evolving trade policy dispute between the United States and China may adversely affect our business.

The U.S. government has made statements and taken certain actions that have led to, and may lead to, further changes to U.S. and international trade policies, including recently imposed tariffs affecting certain products exported by a number of U.S. trading

12

partners, including China. There remains uncertainty regarding tax and trade policies, border adjustments, tariffs and government regulations affecting trade between the U.S. and other countries.

For example, during 2018, the U.S. and China each imposed new tariffs, and announced further proposed tariffs, on various products imported from China and the U.S., respectively. Between July 2018 and September 2018, the Office of the United States Trade Representative imposed tariffs of 10% and 25% on three product lists totaling approximately $250 billion in Chinese imports. These lists include some of our products. The U.S. government has also indicated a readiness to further expand the scope of the tariffs on Chinese goods and, in May 2019, there was an announcement of the United States government’s imposition of a 25% tariff on a range of products exported from China to the U.S. on or after May 10, 2019. China thereafter announced a plan to impose tariffs on imports to China of a wide range of American products, in retaliation for the American tariffs. In January 2020, China and the U.S. entered the first phase of an economic and trade agreement. There is no assurance that a broader trade agreement will be successfully negotiated between the U.S. and China to reduce or eliminate existing tariffs applicable to the business of the Company.

Furthermore, the current U.S. administration may impose additional tariffs on imports from China and there is also a concern that the imposition of additional tariffs by the United States could result in the adoption of tariffs by other countries as well. It is possible that further tariffs may be imposed on imports of our products, or that our business will be impacted by retaliatory trade measures taken by China or other countries in response to existing or future tariffs, causing us to raise prices or make changes to our operations, any of which could adversely impact demand for our products, our costs, customers, suppliers and/or the United States economy or certain sectors thereof and, thus, to adversely impact our businesses and results of operations.

Given the uncertainty regarding the scope and duration of the effective and proposed tariffs, as well as the potential for additional trade actions by the U.S. or other countries, the impact on our operations and results is uncertain and could be significant. We can provide no assurance that any strategies we implement to mitigate the impact of such tariffs or other trade actions will be successful. To the extent that our supply chain, costs, sales or profitability are negatively affected by the tariffs or other trade actions, our business, financial condition and results of operations may be materially adversely affected.

ITEM 1B. Unresolved Staff Comments

None.

13

The Company owns one facility and leases 28 facilities. We own our corporate facility and largest distribution center, which is located on approximately 100 acres in LaFox, Illinois and consists of approximately 242,000 square feet of manufacturing, warehouse and office space. We maintain geographically diverse facilities because we believe this provides value to our customers and suppliers, and limits market risk and exchange rate exposure. We believe our properties are well maintained and adequate for our present needs. The extent of utilization varies from property to property and from time to time during the year.

Our facility locations, their primary use and segments served are as follows:

|

Location |

|

Leased/Owned |

|

Use |

|

Segment |

|

Woodland Hills, California |

|

Leased |

|

Sales |

|

PMT |

|

LaFox, Illinois * |

|

Owned |

|

Corporate/Sales/Distribution/Manufacturing |

|

PMT/Canvys/Healthcare |

|

Marlborough, Massachusetts |

|

Leased |

|

Sales/Distribution/Manufacturing |

|

Canvys |

|

Fort Mill, South Carolina |

|

Leased |

|

Sales/Distribution/Testing/Repair |

|

Healthcare |

|

Murray, Utah |

|

Leased |

|

Sales/Testing/Repair |

|

Healthcare |

|

Sao Paulo, Brazil |

|

Leased |

|

Sales/Distribution |

|

PMT |

|

Beijing, China |

|

Leased |

|

Sales |

|

PMT |

|

Nanjing, China |

|

Leased |

|

Sales |

|

PMT |

|

Shanghai, China |

|

Leased |

|

Sales/Distribution |

|

PMT |

|

Shenzhen, China |

|

Leased |

|

Sales |

|

PMT |

|

Brive, France |

|

Leased |

|

Manufacturing Support/Testing |

|

PMT |

|

Nanterre, France |

|

Leased |

|

Sales |

|

PMT |

|

Donaueschingen, Germany |

|

Leased |

|

Sales/Distribution/Manufacturing |

|

Canvys |

|

Puchheim, Germany |

|

Leased |

|

Sales |

|

PMT |

|

Mumbai, India |

|

Leased |

|

Sales |

|

PMT |

|

Ramat Gan, Israel |

|

Leased |

|

Sales |

|

PMT |

|

Florence, Italy ** |

|

Leased |

|

Sales |

|

PMT |

|

Milan, Italy |

|

Leased |

|

Sales |

|

PMT |

|

Tokyo, Japan |

|

Leased |

|

Sales |

|

PMT |

|

Mexico City, Mexico |

|

Leased |

|

Sales |

|

PMT |

|

Amsterdam, Netherlands |

|

Leased |

|

Sales/Distribution/Manufacturing |

|

PMT/Healthcare |

|

Singapore, Singapore |

|

Leased |

|

Sales/Distribution |

|

PMT |

|

Seoul, South Korea |

|

Leased |

|

Sales |

|

PMT |

|

Madrid, Spain |

|

Leased |

|

Sales |

|

PMT |

|

Taipei, Taiwan |

|

Leased |

|

Sales |

|

PMT/Canvys |

|

Bangkok, Thailand |

|

Leased |

|

Sales/Distribution |

|

PMT |

|

Dubai, United Arab Emirates |

|

Leased |

|

Sales/Distribution/Testing/Repair |

|

PMT |

|

Hook, United Kingdom |

|

Leased |

|

Sales/Distribution/Testing/Repair |

|

PMT |

|

Lincoln, United Kingdom |

|

Leased |

|

Sales |

|

PMT/Canvys |

|

* |

LaFox, Illinois is also the location of our corporate headquarters. |

|

** |

Sold building June 12, 2017, currently lease separate facility. |

On October 15, 2018, Varex Imaging Corporation (“Varex”) filed its original Complaint (Case No. 1:18-cv-06911) against Richardson Electronics Ltd. (“Richardson”) in the Northern District of Illinois, which was subsequently amended on November 27, 2018. Varex alleged counts of infringement of U.S. Patent Nos. 6,456,692 and 6,519,317. Subsequently, on October 24, 2018, Varex filed a motion for preliminary injunction to stop the sale of Richardson’s ALTA750 TM product. Richardson filed an opposition to the preliminary injunction. In January 2019, the Court took evidence on the preliminary injunction issue. On September 30, 2019, the Court denied Varex’s Motion for Preliminary Injunction. Richardson believes the lawsuit to be without merit and a loss is not probable or estimable based on the information at the time the financial statements were issued.

14

ITEM 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Unregistered Sales of Equity Securities

None.

Share Repurchases

There were no share repurchases in fiscal 2020.

Dividends

Our quarterly dividend was $0.06 per common share and $0.054 per Class B common share. Annual dividend payments were approximately $3.1 million for both fiscal 2020 and fiscal 2019. All future payments of dividends are at the discretion of the Board of Directors. Dividend payments will depend on earnings, capital requirements, operating conditions and such other factors that the Board may deem relevant.

Common Stock Information

Our common stock is traded on the NASDAQ Global Select Market (“NASDAQ”) under the trading symbol (“RELL”). There is no established public trading market for our Class B common stock. As of July 27, 2020, there were approximately 491 stockholders of record for the common stock and approximately 15 stockholders of record for the Class B common stock.

15

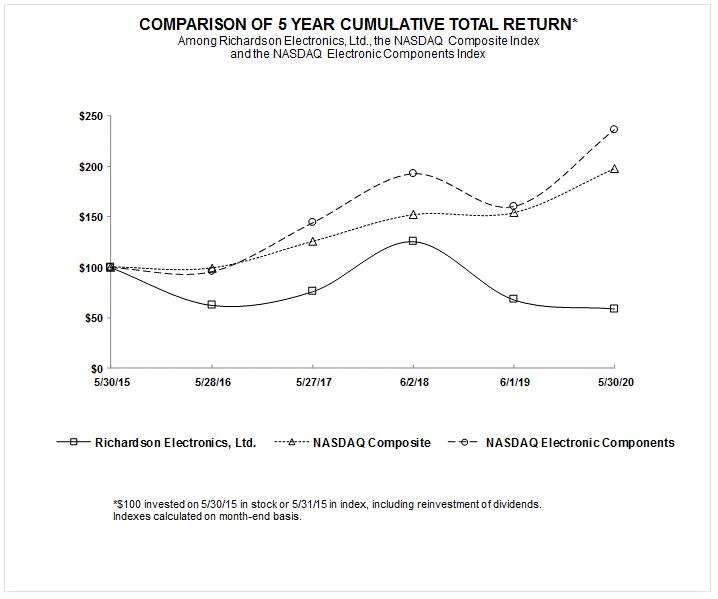

Performance Graph

The following graph compares the performance of our common stock for the periods indicated with the performance of the NASDAQ Composite Index and NASDAQ Electronic Components Index. The graph assumes $100 invested on the last day of our fiscal year 2015, in our common stock, the NASDAQ Composite Index and NASDAQ Electronic Components Index. Total return indices reflect reinvestment of dividends at the closing stock prices at the date of the dividend declaration.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN* Among Richardson Electronics, Ltd., the NASDAQ Composite Index and the NASDAQ Electronic Components Index $250 $200 $150 $100 $50 $0 5/30/15 5/28/16 5/27/17 6/2/18 6/1/19 5/30/20 Richardson Electronics, Ltd. NASDAQ Composite NASDAQ Electronic Components *$100 invested on 5/30/15 in stock or 5/31/15 in index, including reinvestment of dividends. Indexes calculated on month-end basis.

16

ITEM 6. Selected Financial Data

Five-Year Financial Review

This information should be read in conjunction with our consolidated financial statements, accompanying notes, and Management’s Discussion and Analysis of Financial Condition and Results of Operations included elsewhere herein.

|

|

|

Fiscal Year Ended (1) |

|

|||||||||||||||||

|

|

|

(in thousands, except per share amounts ) |

|

|||||||||||||||||

|

|

|

May 30, 2020 |

|

|

June 1, 2019 |

|

|

June 2, 2018 |

|

|

May 27, 2017 |

|

|

May 28, 2016 |

|

|||||

|

Statements of (Loss) Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

|

$ |

155,898 |

|

|

$ |

166,652 |

|

|

$ |

163,212 |

|

|

$ |

136,872 |

|

|

$ |

142,016 |

|

|

Continuing Operations |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Loss) income from continuing operations before tax |

|

$ |

(1,214 |

) |

|

$ |

(6,311 |

) |

|

$ |

3,860 |

|

|

$ |

(6,116 |

) |

|

$ |

(6,220 |

) |

|

Income tax provision |

|

|

624 |

|

|

|

1,017 |

|

|

|

1,534 |

|

|

|

812 |

|

|

|

546 |

|

|

(Loss) income from continuing operations |

|

$ |

(1,838 |

) |

|

$ |

(7,328 |

) |

|

$ |

2,326 |

|

|

$ |

(6,928 |

) |

|

$ |

(6,766 |

) |

|

Discontinued Operations |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from discontinued operations |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

1,496 |

|

|

$ |

— |

|

|

$ |

— |

|

|

Net (loss) income |

|

$ |

(1,838 |

) |

|

$ |

(7,328 |

) |

|

$ |

3,822 |

|

|

$ |

(6,928 |

) |

|

$ |

(6,766 |

) |

|

Per Share Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net (loss) income per Common share - Basic: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Loss) income from continuing operations |

|

$ |

(0.14 |

) |

|

$ |

(0.57 |

) |

|

$ |

0.18 |

|

|

$ |

(0.55 |

) |

|

$ |

(0.53 |

) |

|

Income from discontinued operations |

|

|

— |

|

|

|

— |

|

|

|

0.12 |

|

|

|

— |

|

|

|

— |

|

|

Total net (loss) income per Common share - Basic |

|

$ |

(0.14 |

) |

|

$ |

(0.57 |

) |

|

$ |

0.30 |

|

|

$ |

(0.55 |

) |

|

$ |

(0.53 |

) |

|

Net (loss) income per Class B common share - Basic: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Loss) income from continuing operations |

|

$ |

(0.13 |

) |

|

$ |

(0.51 |

) |

|

$ |

0.16 |

|

|

$ |

(0.49 |

) |

|

$ |

(0.47 |

) |

|

Income from discontinued operations |

|

|

— |

|

|

|

— |

|

|

|

0.11 |

|

|

|

— |

|

|

|

— |

|

|

Total net (loss) income per Class B common share - Basic |

|

$ |

(0.13 |

) |

|

$ |

(0.51 |

) |

|

$ |

0.27 |

|

|

$ |

(0.49 |

) |

|

$ |

(0.47 |

) |

|

Net (loss) income per Common share - Diluted: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Loss) income from continuing operations |

|

$ |

(0.14 |

) |

|

$ |

(0.57 |

) |

|

$ |

0.18 |

|

|

$ |

(0.55 |

) |

|

$ |

(0.53 |

) |

|

Income from discontinued operations |

|

|

— |

|

|

|

— |

|

|

|

0.12 |

|

|

|

— |

|

|

|

— |

|

|

Total net (loss) income per Common share - Diluted |

|

$ |

(0.14 |

) |

|

$ |

(0.57 |

) |

|

$ |

0.30 |

|

|

$ |

(0.55 |

) |

|

$ |

(0.53 |

) |

|

Net (loss) income per Class B common share - Diluted: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Loss) income from continuing operations |

|

$ |

(0.13 |

) |

|

$ |

(0.51 |

) |

|

$ |

0.16 |

|

|

$ |

(0.49 |

) |

|

$ |

(0.47 |

) |

|

Income from discontinued operations |

|

|

— |

|

|

|

— |

|

|

|

0.11 |

|

|

|

— |

|

|

|

— |

|

|

Total net (loss) income per Class B common share - Diluted |

|

$ |

(0.13 |

) |

|

$ |

(0.51 |

) |

|

$ |

0.27 |

|

|

$ |

(0.49 |

) |

|

$ |

(0.47 |

) |

|

Cash Dividend Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends per common share |

|

$ |

0.24 |

|

|

$ |

0.24 |

|

|

$ |

0.24 |

|

|

$ |

0.24 |

|

|

$ |

0.24 |

|

|

Dividends per Class B common share (2) |

|

$ |

0.22 |

|

|

$ |

0.22 |

|

|

$ |

0.22 |

|

|

$ |

0.22 |

|

|

$ |

0.22 |

|

|

Balance Sheet Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ |

150,720 |

|

|

$ |

153,017 |

|

|

$ |

166,329 |

|

|

$ |

157,464 |

|

|

$ |

168,130 |

|

|

Stockholders’ equity |

|

$ |

118,660 |

|

|

$ |

123,757 |

|

|

$ |

135,181 |

|

|

$ |

132,327 |

|

|

$ |

141,675 |

|

|

(1) |

Our fiscal year ends on the Saturday nearest the end of May. Each of the fiscal years presented contain 52/53 weeks. |

|

(2) |

The dividend per Class B common share is 90% of the dividend per Class A common share. |

17

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with the consolidated financial statements and related notes.

Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) is intended to assist the reader in better understanding our business, results of operations, financial condition, changes in financial condition, critical accounting policies and estimates and significant developments. MD&A is provided as a supplement to, and should be read in conjunction with, our consolidated financial statements and the accompanying notes appearing elsewhere in this filing. This section is organized as follows:

|

|

• |

Business Overview |

|

|

• |

Results of Operations - an analysis and comparison of our consolidated results of operations for the fiscal years ended May 30, 2020, June 1, 2019 and June 2, 2018, as reflected in our consolidated statements of comprehensive (loss) income. |

|

|

• |

Liquidity, Financial Position and Capital Resources - a discussion of our primary sources and uses of cash for the fiscal years ended May 30, 2020, June 1, 2019 and June 2, 2018, and a discussion of changes in our financial position. |