Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - Avery Dennison Corp | tm2025393d1_ex99-1.htm |

| 8-K - FORM 8-K - Avery Dennison Corp | tm2025393d1_8k.htm |

Exhibit 99.2

1 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Second Quarter 2020 Financial Review and Analysis (preliminary, unaudited) July 27, 2020 Supplemental Presentation Materials Unless otherwise indicated, comparisons are to the same period in the prior year.

2 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Safe Harbor Statement Certain statements contained in this document are "forward - looking statements" intended to qualify for the safe harbor from liab ility established by the Private Securities Litigation Reform Act of 1995. These forward - looking statements, and financial or other business targets, are subject to certain risks and uncertainties. We believe that the most significant risk factors that could affect our financial performance in the near - term include: (1) the impacts to our busin ess from global economic conditions, political uncertainty, and changes in governmental regulations, including as a result of the coronavirus/COVID - 19 pandemic; (2) competitor s' actions, including pricing, expansion in key markets, and product offerings; (3) the degree to which higher costs can be offset with productivity measures and/or pass ed on to customers through price increases, without a significant loss of volume; and (4) the execution and integration of acquisitions. Actual results and trends may differ materially from historical or anticipated results depending on a variety of factors, inc lud ing but are not limited to, risks and uncertainties relating to the following: the coronavirus/COVID - 19 pandemic; fluctuations in demand affecting sales to customers; worldwide and local economic and market conditions; changes in political conditions; fluctuations in foreign currency exchange rates and other risks associate d w ith foreign operations, including in emerging markets; changes in our markets due to competitive conditions, technological developments, laws and regulations, and customer pr eferences; fluctuations in the cost and availability of raw materials and energy; changes in governmental laws and regulations; the impact of competitive products an d p ricing; the financial condition and inventory strategies of customers; our ability to generate sustained productivity improvement; our ability to achieve and sus tai n targeted cost reductions; loss of significant contracts or customers; collection of receivables from customers; selling prices; business mix shift; execution and integrati on of acquisitions; product and service quality; timely development and market acceptance of new products, including sustainable or sustainably - sourced products; investment in d evelopment activities and new production facilities; amounts of future dividends and share repurchases; customer and supplier concentrations or consolidat ion s; fluctuations in interest and tax rates; changes in tax laws and regulations, and uncertainties associated with interpretations of such laws and regulations; retentio n o f tax incentives; outcome of tax audits; successful implementation of new manufacturing technologies and installation of manufacturing equipment; disruptions in infor mat ion technology systems, including cyber - attacks or other intrusions to network security; successful installation of new or upgraded information technology systems ; data security breaches; volatility of financial markets; impairment of capitalized assets, including goodwill and other intangibles; credit risks; our ability to o bta in adequate financing arrangements and maintain access to capital; the realization of deferred tax assets; fluctuations in interest rates; compliance with our debt cov enants; fluctuations in pension, insurance, and employee benefit costs; goodwill impairment; the impact of legal and regulatory proceedings, including with respect to enviro nme ntal, health and safety, anti - corruption and trade compliance; protection and infringement of intellectual property; the impact of epidemiological events on the econo my and our customers and suppliers; acts of war, terrorism, and natural disasters; and other factors. For a more detailed discussion of the more significant of these factors, see “Risk Factors” and “Management’s Discussion and Ana lysis of Results of Operations and Financial Condition” in our 2019 Form 10 - K, filed with the Securities and Exchange Commission on February 26, 2020, and subseque nt quarterly reports on Form 10 - Q. The forward - looking statements included in this document are made only as of the date of this document, and we undertake no obli gation to update these statements to reflect subsequent events or circumstances, other than as may be required by law.

3 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Use of Non - GAAP Financial Measures This presentation contains certain non - GAAP financial measures as defined by SEC rules. We report our financial results in conf ormity with accounting principles generally accepted in the United States of America, or GAAP, and also communicate with investors using certain non - GAAP financial measures. These non - GAAP financial measures are not in accorda nce with, nor are they a substitute for or superior to, the comparable GAAP financial measures. These non - GAAP financial measures are intended to supplement presentation of our financial results that are prepared in accordan ce with GAAP. Based upon feedback from investors and financial analysts, we believe that the supplemental non - GAAP financial measures we provide are useful to their assessment of our performance and operating trends, as w ell as liquidity. In accordance with Regulations G and S - K, reconciliations of non - GAAP financial measures to the most directly comparable GAAP financial measures, including limitations associated with these non - GAAP financial measures, are provided in the financial schedules accompanying the earnings news release for the quarter (see Attachments A - 4 through A - 9 to news release dated July 27, 2020). Our non - GAAP financial measures exclude the impact of certain events, activities or decisions. The accounting effects of these events, activities or decisions, which are included in the GAAP financial measures, may make it difficult to assess our underlying performance in a single period. By excluding the accounting effects, positive or negative, of certa in items (e.g., restructuring charges, legal settlements, certain effects of strategic transactions and related costs, losses from debt extinguishments, gains or losses from curtailment or settlement of pension obligations, gains or loss es on sales of certain assets, and other items), we believe that we are providing meaningful supplemental information that facilitates an understanding of our core operating results and liquidity measures. While some of the items w e e xclude from GAAP financial measures recur, they tend to be disparate in amount, frequency, or timing. We use these non - GAAP financial measures internally to evaluate trends in our underlying performance, as well as to facilitate c omparison to the results of competitors for a single period. We use the following non - GAAP financial measures in this presentation: • Sales change ex. currency refers to the increase or decrease in net sales excluding the estimated impact of foreign currency translation, and, where ap pl icable, currency adjustment for transitional reporting of highly inflationary economies (Argentina) and reclassification of sales between segments. The estimated impact of foreign currency translation is ca lculated on a constant currency basis, with prior period results translated at current period average exchange rates to exclude the effect of currency fluctuations. • Organic sales change refers to sales change ex. currency, excluding the estimated impact of product line exits, acquisitions and divestitures, and , where applicable, the extra week in our fiscal year. We believe that sales change ex. currency and organic sales change assist investors in evaluating the sales change from the o ngo ing activities of our businesses and enhance their ability to evaluate our results from period to period. • Adjusted operating income refers to income before taxes, interest expense, other non - operating expense, and other expense, net. • Adjusted EBITDA refers to net income before interest expense, other non - operating expense, taxes, equity method investment losses, other expens e, net, and depreciation and amortization. • Adjusted operating margin refers to adjusted operating income as a percentage of net sales. • Adjusted EBITDA margin refers to adjusted EBITDA as a percentage of net sales. • Adjusted tax rate refers to the projected full - year GAAP tax rate, adjusted to exclude certain unusual or infrequent events that are expected to s ignificantly impact that rate, such as our U.S. pension plan termination, effects of certain discrete tax planning actions, impacts related to the enactment of the U.S. Tax Cuts and Jobs Act ("TCJA"), where app lic able, and other items. • Adjusted net income refers to income before taxes, tax - effected at the adjusted tax rate, and adjusted for tax - effected restructuring charges and o ther items. • Adjusted net income per common share, assuming dilution (adjusted EPS) refers to adjusted net income divided by weighted average number of common shares outstanding, assuming dilution. We believe that adjusted operating margin, adjusted EBITDA margin, adjusted net income, and adjusted EPS assist investors in und erstanding our core operating trends and comparing our results with those of our competitors. • Net debt to adjusted EBITDA ratio refers to total debt (including finance leases) less cash and cash equivalents, divided by adjusted EBITDA. We believe that t he net debt to adjusted EBITDA ratio assists investors in assessing our leverage position. • Free cash flow refers to cash flow provided by operating activities, less payments for property, plant and equipment, software and other def er red charges, plus proceeds from sales of property, plant and equipment, plus (minus) net proceeds from insurance and sales (purchases) of investments. Free cash flow is also adjusted for, where applicable, the cas h contributions related to the termination of our U.S. pension plan. We believe that free cash flow assists investors by showing the amount of cash we have available for debt reductions, dividends, share repurchases, and acqu isi tions. This document has been furnished (not filed) on Form 8 - K with the SEC and may be found on our website at www.investors.averydenn ison.com.

4 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Actively managing dynamic environment through robust scenario planning and strong execution ● Safety and well - being of employees remains our top priority during continuing global health crisis ● Q2 revenue better than expected, though overall demand trends playing out largely as anticipated ○ Label & Packaging Materials (LPM) flat to prior year, as NA/EU volume surge during early stage of pandemic was partially offset by subsequent slowdown, and emerging markets declined, especially in South Asia ○ Sharp declines in April in RBIS and Graphics were followed by better - than - expected sequential improvement ● Executing well against cost saving plans, both structural and temporary ○ Now targeting $60 mil. to $70 mil. of net restructuring savings + ~$150 mil. of temporary savings in 2020 ● Strong balance sheet (net debt to adj. EBITDA ratio of 2.1) and ample liquidity ● Anticipate Q3 sales decline ex. currency of 5% to 9% (organic sales decline of 7% to 11%) ● Free cash flow strong across wide range of scenarios… targeting ~$500 mil. for 2020 ● Strategic priorities are unchanged; ringfencing key investments in high value categories, including RFID, while driving long - term profitable growth in the base

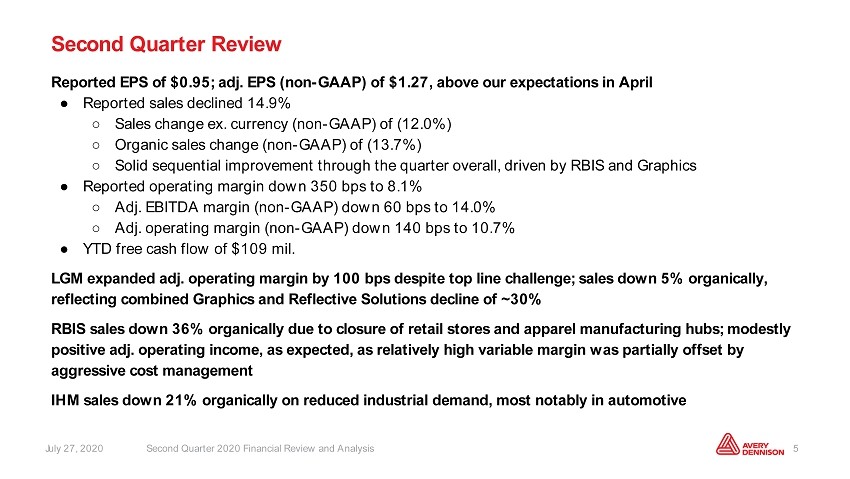

5 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Second Quarter Review Reported EPS of $0.95; adj. EPS (non - GAAP) of $1.27, above our expectations in April ● Reported sales declined 14.9% ○ Sales change ex. currency (non - GAAP) of (12.0%) ○ Organic sales change (non - GAAP) of (13.7%) ○ Solid sequential improvement through the quarter overall, driven by RBIS and Graphics ● Reported operating margin down 350 bps to 8.1% ○ Adj. EBITDA margin (non - GAAP) down 60 bps to 14.0% ○ Adj. operating margin (non - GAAP) down 140 bps to 10.7% ● YTD free cash flow of $109 mil. LGM expanded adj. operating margin by 100 bps despite top line challenge; sales down 5% organically, reflecting combined Graphics and Reflective Solutions decline of ~30% RBIS sales down 36% organically due to closure of retail stores and apparel manufacturing hubs; modestly positive adj. operating income, as expected, as relatively high variable margin was partially offset by aggressive cost management IHM sales down 21% organically on reduced industrial demand, most notably in automotive

6 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Operations / Market Update in Light of COVID - 19 Label and Graphic Materials (LGM) 67% of 2019 sales Retail Branding and Info. Solutions (RBIS) 23% of 2019 sales Industrial and Healthcare Materials (IHM) 10% of 2019 sales ● Most plants operational throughout crisis, with exception of sites in India, which are now up and running ● LPM volume surge in NA/EU mid - March through April, driven by food, hygiene, and pharmaceutical product labeling, as well as variable information (e.g., e - commerce labels), followed by slowdown in June. Portion of volume surge and subsequent slowdown due to inventory build/destocking throughout supply chain ● Though China demand for label materials improved following decline in Jan/Feb, balance of emerging markets deteriorated as lockdowns spread across the globe and continued through much of Q2, with India particularly hard hit early in the quarter ● Sharp decline in demand for Graphics & Reflective Solutions and material for durable label applications (e.g., consumer appliances, tires, etc.) beginning in March; sequential improvement monthly since April ● Government - mandated closures continued to impact operations in many countries during April and first few weeks of May; [all] sites now operational ○ Our global footprint providing significant competitive advantage during pandemic; key to meeting retailer/brand owner needs as they ramp back up (Smartrac acquisition further strengthening our advantage) ● Sharp decline in demand from apparel retailers and brands, reflecting widespread closure of malls and other retail outlets ● Enterprise - wide sales of RFID products up over 10% ex. currency in Q2 with benefit of Smartrac acquisition; down 20% organically, as increased penetration of market was more than offset by decline in existing programs tied to apparel ○ Project pipeline continues to expand (engagements up >35% since start of year) ○ Current environment underscoring value of RFID as key technology to improve supply chains and support customer automation over the long - term ● All plants now operational, some with limited production ● Demand for industrial categories (~60% of IHM sales in 2019) weakened further during Q2 reflecting global decline in industrial production (though timing for our business impacted by customers building some inventory in early stages of pandemic due to supply chain uncertainty) ● Medical division (~15% of IHM sales in 2019), historically focused on advanced wound care, has commercialized new personal protective equipment (PPE) solutions to address urgent need 1

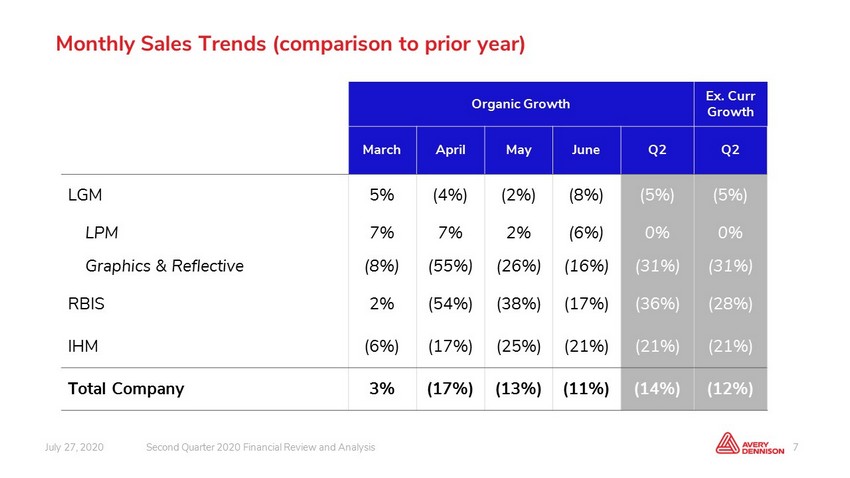

7 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Q2 LGM (5%) RBIS (36%) IHM (21%) Total Company (14%) Monthly Organic Sales Trends (comparison to prior year)

8 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Agile teams effectively managing through crisis Ensuring Safety and Well - being of Our Team ● Continue to adapt safety protocols based on new information; focus has shifted to ensuring safe “back to work” environment ● During initial weeks of facility closures, company ensured that employees continued to receive full pay ● Extended salary continuation in jurisdictions with weaker social safety nets Meeting Customer Needs ● Adapted quickly to manage peak demand in label materials, as well as to address migration of lockdowns impacting RBIS customers ● Leveraged operational excellence to maximize production capacity in label materials ● Successfully executing large new RFID rollouts ● Developed N95 masks which are being rapidly commercialized Supporting Our Communities ● Shifted resources to produce PPE and hand sanitizer to donate to local communities ● Avery Dennison Foundation increasing grants to provide employee assistance and rapid community response Mitigating Supply Chain Risk ● Partnered with suppliers (and customers) to keep supply chains open (essential business) ● Negligible disruptions to supply chain throughout pandemic ● Global footprint with dual sourcing or available alternatives for most commodities ● Selective strategic inventory build Enabling Financial Flexibility ● Curtailed capital spending plans by ~$55 mil.; heightened focus on working capital management ● Initial $500 mil. drawdown of revolver in Q1 to mitigate dependence on CP markets (repaid in Q2 as CP markets stabilized) ● Maintaining dividend rate ● Temporary pause on share repurchases

9 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Broad exposure to diverse end markets, with ~60% tied to non - durable consumer goods, logistics & shipping, and medical products 2019 Sales by Product Category Non - durable consumer goods Retail Apparel Industrial / Durable Logistics, Shipping, & Other Variable Information Medical / Healthcare Non - durable Consumer Goods Vast majority of these sales tied to labeling of food, beverage, and home and personal care (HPC) products. Growth catalysts: Emerging markets (increased use of packaged goods with rising middle class) and labeling technology shifts to pressure - sensitive Logistics, Shipping & Other Variable Information Growth catalysts: Increase in e - commerce benefits our businesses serving variable information needs, including non - apparel RFID Retail Apparel Industrial / Durable “Discretionary staple”. Cyclical. Growth catalyst: expansion Growth catalyst: shift from of omni - channel retailing mechanical to adhesive - based fastening

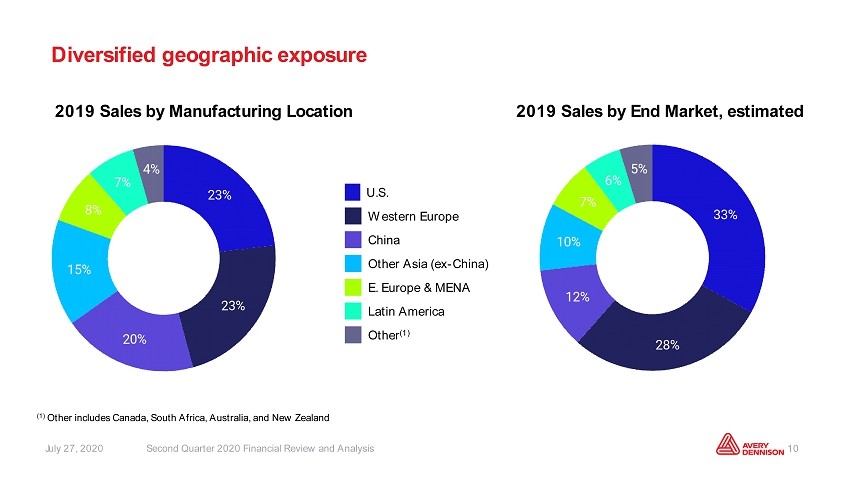

10 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Diversified geographic exposure 2019 Sales by Manufacturing Location 2019 Sales by End Market, estimated (1) Other includes Canada, South Africa, Australia, and New Zealand U.S. Western Europe China Other Asia (ex - China) E. Europe & MENA Latin America Other (1)

11 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Our businesses are resilient through economic cycles * Externally reported organic growth by segment has been adjusted to reflect divestitures and transfers between segments. Organic growth trends* during 2009/2010

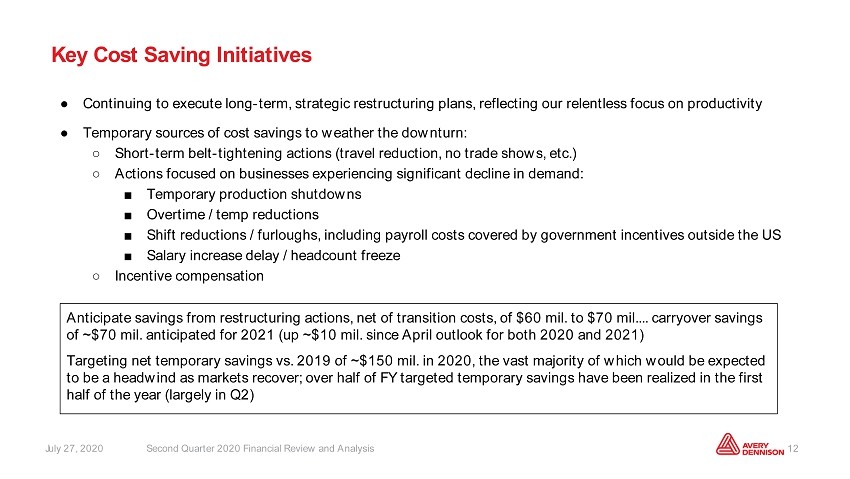

12 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Key Cost Saving Initiatives ● Continuing to execute long - term, strategic restructuring plans, reflecting our relentless focus on productivity ● Temporary sources of cost savings to weather the downturn: ○ Short - term belt - tightening actions (travel reduction, no trade shows, etc.) ○ Actions focused on businesses experiencing significant decline in demand: ■ Temporary production shutdowns ■ Overtime / temp reductions ■ Shift reductions / furloughs, including payroll costs covered by government incentives outside the US ■ Salary increase delay / headcount freeze ○ Incentive compensation Anticipate savings from restructuring actions, net of transition costs, of $60 mil. to $70 mil.... carryover savings of ~$70 mil. anticipated for 2021 (up ~$10 mil. since April outlook for both 2020 and 2021) Targeting net temporary savings vs. 2019 of ~$150 mil. in 2020, the vast majority of which would be expected to be a headwind as markets recover; over half of FY targeted temporary savings have been realized in the first half of the year (largely in Q2)

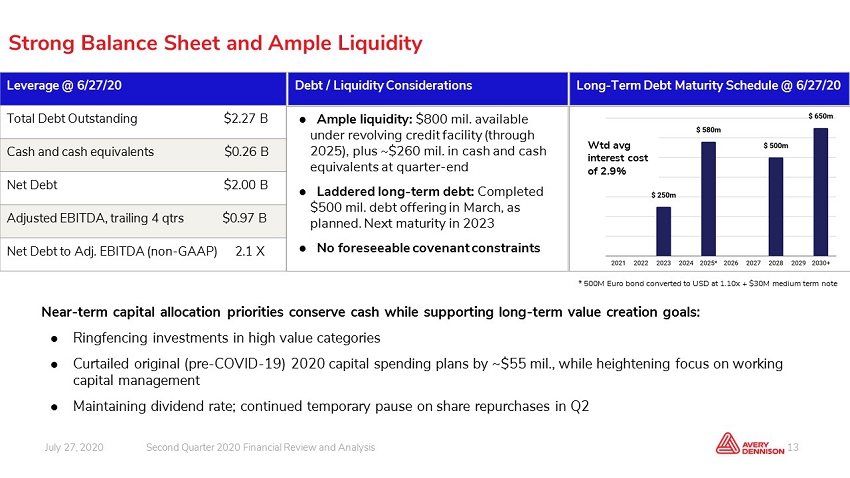

13 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Strong Balance Sheet and Ample Liquidity Leverage @ 6/27/20 Total Debt Outstanding $2.27 B Cash and cash equivalents $0.26 B Net Debt $2.00 B Adjusted EBITDA, trailing 4 qtrs $0.97B Net Debt to Adj. EBITDA (non - GAAP) 2.1 X Debt / Liquidity Considerations Long - Term Debt Maturity Schedule @ 6/27/20 ● Ample liquidity: $800 mil. available under revolving credit facility (through 2025), plus ~$260 mil. in cash and cash equivalents at quarter - end ● Laddered long - term debt: Completed $500 mil. debt offering in March, as planned. Next maturity in 2023 ● No foreseeable covenant constraints Near - term capital allocation priorities conserve cash while supporting long - term value creation goals: ● Ringfencing investments in high value categories ● Curtailed original (pre - COVID - 19) 2020 capital spending plans by ~$55 mil., while heightening focus on working capital management ● Maintaining dividend rate; continued temporary pause on share repurchases in Q2 * 500M Euro bond converted to USD at 1.10x + $30M medium term note Wtd avg interest cost of 2.9%

14 July 27, 2020 Second Quarter 2020 Financial Review and Analysis ● Lower sales due principally due to declining volumes and currency translation, with trough in Q2: ○ Anticipate Q3 sales decline ex. currency of 5% to 9% (organic sales decline of 7% to 11%) ○ Currency translation headwinds at recent rates of ~2% for both Q3 and FY ● Currency translation headwind to FY operating income of ~$18 mil. at recent rates (down ~$10 mil. since April outlook) ● Incremental savings of $60 mil. to $70 mil. from restructuring actions, net of transition costs (up $10 mil. since April outlook). Additional net temporary savings vs. 2019 of ~$150 mil. ● Full year adjusted tax rate in the mid - twenty percent range ● Targeting free cash flow of ~$500 mil. ○ Fixed and IT capital spend of $165 mil. to $175 mil. ○ Cash impact of restructuring charges now ~$60 mil. 2020 Outlook

15 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Q2 Results Detail

16 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Quarterly Sales Trend Analysis 2Q19 3Q19 4Q19 1Q20 2Q20 Reported Sales Change (3.2%) 0.1% 0.2% (1.0%) (14.9%) Organic Sales Change 1.6% 2.1% 2.1% 0.3% (13.7%) Acquisitions 0.7% 1.7% Sales Change Ex. Currency* 1.6% 2.1% 2.1% 1.0% (12.0%) Currency Translation (4.7%) (2.0%) (1.9%) (1.9%) (2.9%) Reported Sales Change* (3.2%) 0.1% 0.2% (1.0%) (14.9%) *Totals may not sum due to rounding.

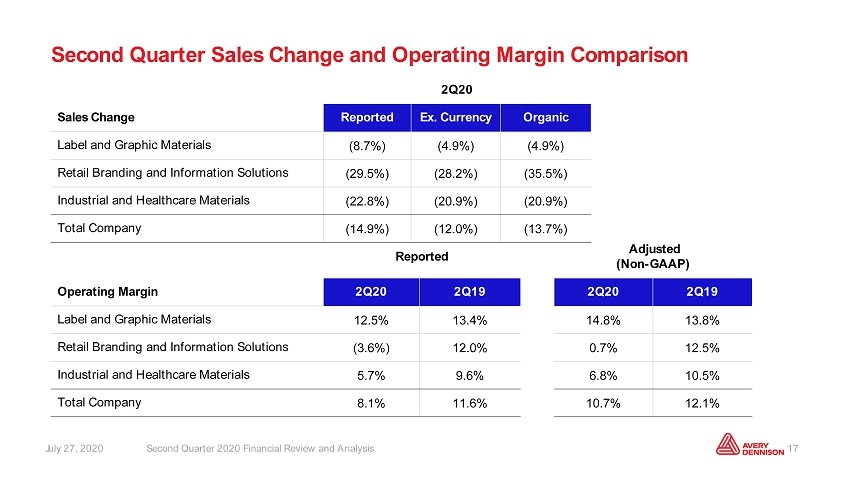

17 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Second Quarter Sales Change and Operating Margin Comparison Reported Adjusted (Non - GAAP) Operating Margin 2Q20 2Q19 2Q20 2Q19 Label and Graphic Materials 12.5% 13.4% 14.8% 13.8% Retail Branding and Information Solutions (3.6%) 12.0% 0.7% 12.5% Industrial and Healthcare Materials 5.7% 9.6% 6.8% 10.5% Total Company 8.1% 11.6% 10.7% 12.1% 2Q20 Sales Change Reported Ex. Currency Organic Label and Graphic Materials (8.7%) (4.9%) (4.9%) Retail Branding and Information Solutions (29.5%) (28.2%) (35.5%) Industrial and Healthcare Materials (22.8%) (20.9%) (20.9%) Total Company (14.9%) (12.0%) (13.7%)

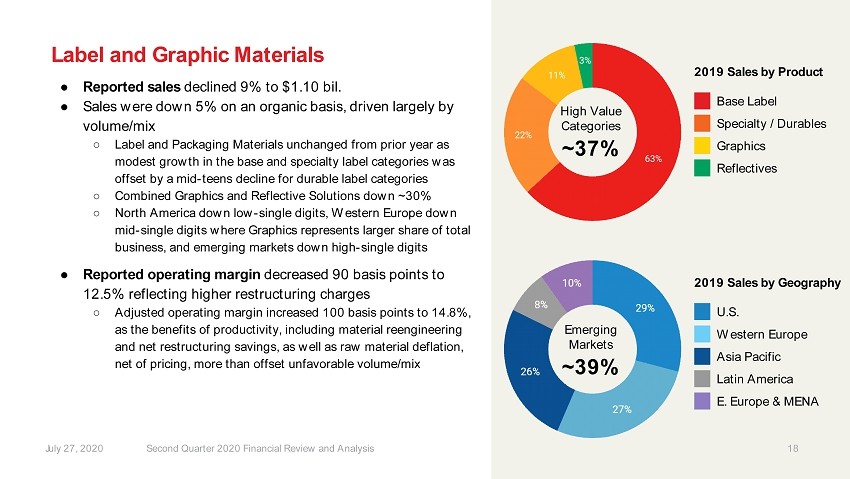

18 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Label and Graphic Materials ● Reported sales declined 9% to $1.10 bil. ● Sales were down 5% on an organic basis, driven largely by volume/mix ○ Label and Packaging Materials unchanged from prior year as modest growth in the base and specialty label categories was offset by a mid - teens decline for durable label categories ○ Combined Graphics and Reflective Solutions down ~30% ○ North America down low - single digits, Western Europe down mid - single digits where Graphics represents larger share of total business, and emerging markets down high - single digits ● Reported operating margin decreased 90 basis points to 12.5% reflecting higher restructuring charges ○ Adjusted operating margin increased 100 basis points to 14.8%, as the benefits of productivity, including material reengineering and net restructuring savings, as well as raw material deflation, net of pricing, more than offset unfavorable volume/mix 2019 Sales by Product Base Label Specialty / Durables Graphics Reflectives 2019 Sales by Geography U.S. Western Europe Asia Pacific Latin America E. Europe & MENA 18 High Value Categories ~37% Emerging Markets ~39%

19 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Retail Branding and Information Solutions ● Reported sales declined 30% to $295 mil. ● Sales were down 28% ex. currency, and down 36% on an organic basis ○ Base business down ~40% organically, driven by site closures and lower apparel demand ○ Enterprise - wide sales of RFID products were up over 10% ex. currency with benefit of Smartrac acquisition; down 20% organically, as increased penetration of market was more than offset by decline in existing programs tied to apparel ● Strong sequential improvement in demand every month since April ● Reported operating margin declined to (3.6%), including the impact of significantly higher restructuring charges ○ Adjusted operating margin declined roughly 12 points to 0.7%, reflecting reduced fixed cost leverage in this high variable margin business, which was partially offset by aggressive cost control measures 2019 Sales by Geography (end markets, estimated) U.S. Europe Asia Pacific Others 2019 Sales by Product Apparel Tags & Labels RFID Ext. Embellishment PSD (ex. RFID) High Value Categories ~27% 19

20 July 27, 2020 Second Quarter 2020 Financial Review and Analysis Industrial and Healthcare Materials ● Reported sales declined 23% to $132 mil. ● Sales declined 21% on an organic basis ○ ~30% decline in industrial categories driven by automotive ○ Healthcare categories relatively unchanged from prior year ● Demand trend somewhat choppy during quarter, as customers worked off inventory that they had built during early weeks of pandemic due to supply chain uncertainty ● Reported operating margin decreased 390 basis points to 5.7%, including slightly higher restructuring charges ○ Adjusted operating margin decreased 370 basis points to 6.8% due to reduced fixed cost leverage, partially offset by productivity 2019 Sales by Product Automotive Other Industrial Healthcare Retail 2019 Sales by Geography U.S. Europe Asia Pacific Latin America High Value Categories ~74% 20

21 July 27, 2020 Second Quarter 2020 Financial Review and Analysis © 2020 Avery Dennison Corporation. All rights reserved. Avery Dennison and all other Avery Dennison brands, product names and co des are trademarks of Avery Dennison Corporation. All other brands or product names are trademarks of their respective owners. Fortune 500® is a trademark of Time, Inc. Branding and other information on any samples depicted is fictitious. Any resemblance to actual names is purely coincidental. Thank you