Attached files

| file | filename |

|---|---|

| EX-23.1 - Flux Power Holdings, Inc. | ex23-1.htm |

As filed with the Securities and Exchange Commission on July 21, 2020

Registration No. 333-231766

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Flux Power Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 3690 | 86-0931332 | ||

| (State or jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

2685 S. Melrose Drive

Vista, CA 92081

(877) 505-3589

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Ronald F. Dutt

Chief Executive Officer

Flux Power Holdings, Inc.

2685 S. Melrose Drive,

Vista, CA 92081

(877) 505-3589

(Name, address, including zip code, and telephone number,

Including area code, of agent for service)

Copies to:

| John P. Yung, Esq. |

| Daniel B. Eng, Esq. |

| Lewis Brisbois Bisgaard & Smith LLP |

| 333 Bush Street, Suite 1100 |

| San Francisco, CA 94104 |

| (415) 362-2580 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [ ]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] | ||

| Non-accelerated filer | [ ] | (Do not check if a smaller reporting company) | Smaller reporting company | [X] | |

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act [ ]

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 21, 2020

PROSPECTUS

[total number of shares offered] Shares

![]()

Common Stock

We are offering [total number of shares offered] shares of common stock in this offering.

Our common stock is quoted on the OTCQB marketplace under the symbol “FLUX.” On __________, 2020, the closing bid price of our common stock on the OTCQB was $_____ per share. We have applied to list our common stock on The NASDAQ Capital Market under the symbol “FLUX.”

The public offering price per share will be determined between us, the underwriters and investors based on market conditions at the time of pricing, and may be at a discount to the current market price of our common stock. Therefore, the recent market price of our common stock used throughout this prospectus may not be indicative of the actual public offering price.

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 9.

| Per Share | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting discount(1) | $ | $ | ||||||

| Proceeds to us (before expenses) | $ | $ |

| (1) | See “Underwriting” beginning on page 58 for additional information regarding the compensation payable to the underwriters. |

We have granted the underwriters a 30-day option to purchase up to an additional [___] shares from us at the public offering price, less the underwriting discount, to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Delivery of the shares of common stock is expected to be made through the facilities of the Depository Trust Company on or about , 2020.

The date of this prospectus is , 2020

Table of Contents

| i |

Neither we nor the underwriters have authorized anyone to provide you with information other than that contained in this prospectus or any free writing prospectus prepared by or on behalf of us or to which we have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the underwriters are offering to sell, and seeking offers to buy, common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date on the front cover page of this prospectus, or other earlier date stated in this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

No action is being taken in any jurisdiction outside the United States to permit a public offering of our common stock or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to that jurisdiction.

| ii |

This summary highlights information contained elsewhere or incorporated by reference in this prospectus. This summary provides an overview of selected information and does not contain all of the information you should consider before investing in our securities. You should read the entire prospectus carefully, especially the “Risk Factors,” “Management’s Discussions and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the accompanying notes to those statements, included elsewhere in this prospectus, before making an investment decision. Unless the context requires otherwise, references to the “Company,” “Flux,” “we,” “us,” and “our” refer to the combined business of Flux Power Holdings, Inc., a Nevada corporation and its wholly-owned subsidiary, Flux Power, Inc. (Flux Power), a California corporation.

Company Overview

We design, develop, manufacture, and sell advanced rechargeable lithium-ion energy storage solutions for lift trucks, and other industrial equipment including airport ground support equipment (GSE), energy storage for solar applications, and industrial robotic applications. Our “LiFT Pack” battery packs, including our proprietary (in-house developed) battery management system (BMS), provide our customers with a better performing, lower cost of ownership, and more environmentally friendly alternative, in many instances, to traditional lead-acid and propane-based solutions.

We have received Underwriters Laboratory (UL) Listing on our Class 3 Walkie Pallet Jack LiFT Pack product line, our Class 1 Counterbalance/Sit-down/Ride-on LiFT Packs, currently have in testing our Class 2 Narrow Aisle LiFT Packs, and are scheduling this year our Class 3 End Rider LiFT Pack. We believe that a UL Listing demonstrates the safety, reliability and durability of our products and gives us an important competitive advantage over other lithium-ion energy suppliers. Many of our LiFT Packs have been approved for use by leading industrial motive manufacturers, including Toyota Material Handling USA, Inc., Crown Equipment Corporation, and Raymond Corporation.

Within our industrial market segments, we believe that our LiFT Pack solutions provide cost and performance benefits over existing lead-acid power products including:

| ● | longer operation and more shifts with fewer batteries; | |

| ● | reduced energy and maintenance costs; | |

| ● | faster recharging; and | |

| ● | longer lifespan. |

Additionally, the toxic nature of lead-acid batteries presents significant safety and environmental issues as they are subject to Environmental Protection Agency lead-acid battery reporting requirements, may create an environmental hazard in the event of a cell breach, and emit combustible gases during charging.

As a result of the advantages lithium-ion battery technology provide over lead-acid batteries, we have experienced significant growth in our business. We believe we are at the very early stage of a trend toward the adoption of lithium-ion technology and the displacement of lead-acid and propane-based energy storage solutions, which based on North American sales data from the Industrial Truck Association (ITA), we estimate to be a multi-billion dollar per year market.

Critical to our success is our innovative and proprietary high power BMS that both optimizes the performance of our LiFT Packs and provides a platform for adding new battery pack features, including customized telemetry (pack data available anytime, anywhere) for customers. The BMS serves as the brain of the battery pack, managing cell balancing, charging, discharging, monitoring and communication between the pack and the forklift.

Our engineers design, develop, test, and service our products. We source our battery cells from multiple suppliers in China and the remainder of the components primarily from vendors in the United States. Final assembly, testing and shipping of our products is done from our ISO 9001 certified facility in Vista, California, which includes three assembly lines.

| 1 |

Our Strengths

We have leveraged our experience in lithium-ion technology to design and develop a suite of LiFT Pack product lines that we believe provide attractive solutions to customers seeking an alternative to lead-acid and propane-based power products. We believe that the following attributes are significant contributors to our success:

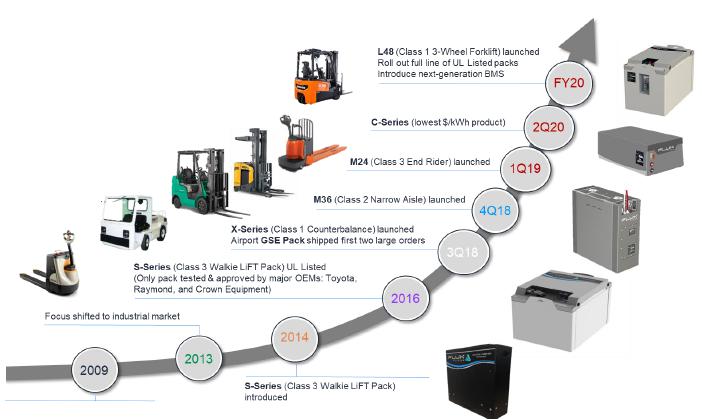

Engineering and integration experience in lithium-ion for motive applications: We have been developing lithium-ion applications for the advanced energy storage market since 2010, starting with products for automotive electric vehicle (EV) manufacturers. We believe our experience enables us to develop superior solutions as we have sold over 7,000 packs in the field to customers.

UL Listing: We launched our Class 3 Walkie LiFT Pack product line in 2014 and obtained UL Listing for all three different power configurations in January 2016. We believe this UL Listing gives us a significant competitive advantage and provides assurance to customers that our technology has been rigorously tested by an independent third party and determined to be safe, durable and reliable. Our Class 1 LiFT Pack now has a UL Listing and we are in process with our Class 2 LiFT Pack, with our Class 3 End Rider LiFT Pack to follow shortly.

Original equipment manufacturer (OEM) approvals: Our Class 3 Walkie LiFT Packs have been tested and approved for use by Toyota Material Handling USA, Inc., Crown Equipment Corporation, and Raymond Corporation, among the top global lift truck manufacturers by revenue according to Material Handling & Logistics. We also provide a “private label” Class 3 Walkie LiFT Pack to a major forklift OEM.

Broad product offering and scalable design: We offer LiFT Packs for use in a variety of industrial motive applications. We believe that our modular and scalable design enables us to optimize design, inventory, and part count to accommodate natural product extensions of our products to meet customer requirements. Based on our Class 3 Walkie LiFT Pack design, we have expanded our product lines to include Class 1 Ride-on, Class 2 Narrow Aisle & Turret Truck, Class 3 End Rider LiFT Pack product lines as well as airport GSE Packs. Natural product extensions, based on our modular, scalable designs, recently include solar backup power for mobile charging stations and robotic warehouse equipment.

| 2 |

Significant advantages over lead-acid and propane solutions: We believe that lithium-ion battery systems have significant advantages over existing technologies and will displace lead-acid batteries and propane-based solutions, in most applications. Relative to lead-acid batteries, such advantages include environmental benefits, no water maintenance, faster charge times, greater cycle life, longer run times, and less energy used that provide operational and financial benefits to customers. Compared to propane solutions, lithium-ion systems avoid the generation of exhaust emissions and associated odor and environmental contaminates, and maintenance of an internal combustion engine, which has substantially more parts than an electric motor.

Proprietary Battery Management System: We have developed our “next generation” versatile BMS that is currently being rolled out into our full product line and provides significant product features to improve customer productivity. Our BMS serves as the brain of the battery pack, managing cell balancing, charging, discharging, monitoring and communication between the pack and the forklift. Our BMS is specifically designed for the industrial motive application environment and is adaptable to meet custom requirements. Our BMS also enables ongoing feature development for reduced cost and higher performance.

Our Products

We have developed, tested, and sold our LiFT Packs for use in a broad range of lift trucks, including Class 3 Walkie and End Riders, Class 2 Narrow Aisle, and Class 1 Ride-on, as well as for airport GSE, as outlined below. Recent product sales have now include initial sales for lithium-ion packs for solar energy storage for mobile charging stations and warehouse robotics, using our modular, scalable designs.

Our LiFT Packs use lithium iron phosphate (LiFePO4) battery cells, which we source from a variety of overseas suppliers that meet our power, reliability, safety and other specifications. Because our BMS is not designed to work with a specific battery chemistry, we believe we can readily adapt our LiFT Packs as new chemistries become available in the market or customer preferences change.

| 3 |

We also offer 24-volt onboard chargers for our Class 3 Walkie LiFT Packs, and smart “wall mounted” chargers for larger applications. Our smart charging solutions are designed to interface with our BMS and integrate easily into most all major chargers in the market.

Industry Overview

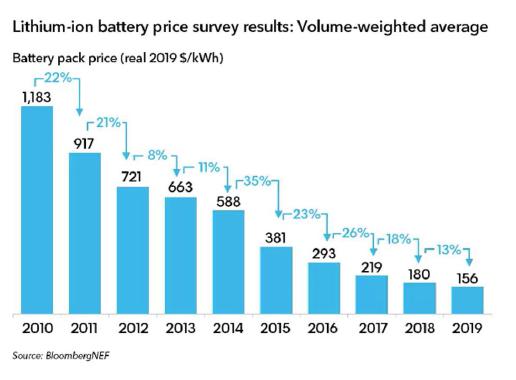

Driven by overall growth in global demand for lithium-ion battery solutions, the supply of lithium-ion batteries has rapidly expanded, leading to price declines of eighty-five percent (85%) since 2010 according to BloombergNEF. BloombergNEF also estimates that lithium-ion battery pack prices, which averaged $1,160 per kilowatt hour in 2010, $156 per kWh in 2019 and could drop below $100 in 2024.

The sharp decline in the price of lithium-ion batteries has commenced a shift in customer preferences away from lead-acid and propane-based solutions for power lift equipment to lithium-ion based solutions. We believe our position as a pioneer in the field and our extensive experience providing lithium-ion based storage solutions makes us uniquely positioned to take advantage of this shift in customer preferences.

Lift Equipment - Material Handling Equipment

We focus on energy storage solutions for lift equipment and related industrial applications because we believe they represent large and growing markets that are just beginning to adopt lithium-ion based technology. We apply our scalable, modular designs to natural product extensions in the industrial equipment market. These markets include not only the sale of lithium-ion battery solutions for new equipment but also a replacement market for existing lead-acid battery packs.

Historically, larger lift trucks were powered by internal combustion engines, using propane as a fuel, with smaller equipment powered by lead-acid batteries. Over the past thirty (30) years, there has been a significant shift toward electric power. According to Liftech/ITA, over this time period the percentage of lift trucks powered electrically has doubled from approximately thirty percent (30%) to over sixty percent (60%).

According to Modern Materials Handling, worldwide new lift truck orders reached approximately 1.4 million units in 2017. The Industrial Truck Association has estimated that approximately 200,000 lift trucks had been sold yearly since 2013 in North America (Canada, the United States and Mexico), including approximately 260,000 units sold in 2018, with sales relatively evenly distributed between electric rider (Class 1 and Class 2), motorized hand (Class 3), and internal combustion engine powered lift trucks (Class 4 and Class 5). The ITA estimates that electric products represented approximately sixty-four percent (64%) of the North American market in 2018. Driven by growth in global manufacturing, e-commerce and construction, Research and Markets expects that the global lift truck market will grow at a compound annual growth rate of six and four-tenths percent (6.4%) through 2024.

| 4 |

Customers

Some of the end users of our LiFT Packs include companies in a number of different industries, as shown in the graphic below:

Marketing and Sales

We sell our products through a number of different channels, including directly to end users, OEMs and lift equipment dealers or through battery distributors. Our direct sales staff is assigned to major geographies nation-wide to collaborate with our sales partners who have an established customer base. In addition, we have developed a nation-wide sales network of relationships with equipment OEMs, their dealers, and battery distributors.

We have worked directly with a number of OEMs to secure “technical approval” for compatibility of our LiFT Packs with their equipment. Once we receive that approval, we focus on developing a sales network utilizing existing battery distributors and equipment dealers, along with the OEM corporate national account sales force, to drive sales through this channel.

As our LiFT Packs have gained acceptance in the marketplace, we have seen an increase in direct-to-end-customer sales, ranging from small enterprises to Fortune 500 companies. To expand our customer reach, we have begun to market directly to end users, primarily focusing on large fleets operated by Fortune 500 companies seeking productivity improvements.

To support our products, we have a nation-wide network of service providers, typically forklift equipment dealers and battery distributors, who provide local support to large customers. We also maintain a call center and provide Tech Bulletins and training to our service and sales network out of our corporate headquarters. Our warranty policy for forklift product lines includes a limited five-year warranty for small battery packs, and up to a limited ten-year warranty for larger battery packs.

Risks Associated with Our Business

Our business is subject to a number of risks of which you should be aware before making a decision to invest in our common stock. These risks are more fully described in the section titled “Risk Factors” beginning on page 9 of this prospectus.

Recent Developments

Estimated Net Revenue for the Fourth Fiscal Quarter of 2020 and the Fiscal Year Ended June 30, 2020. Our expectations with respect to our net revenue for the fourth fiscal quarter of 2020 and the fiscal year ended June 30, 2020 discussed below are based upon management estimates for the period. Our expectations are subject to the completion of our financial closing procedures and any adjustments that may result from the completion of the audit of our consolidated financial statements for the fiscal year ended June 30, 2020. Following the completion of our financial closing process and the audit, we may report net revenue for the fourth fiscal quarter of 2020 and the fiscal year ended June 30, 2020 that could differ from our expectations, and the differences could be material.

| 5 |

The expectations set forth below have been prepared by, and are the responsibility of, our management. Squar Milner LLP has not audited, reviewed, compiled or performed any procedures with respect to the preliminary estimates. Accordingly, Squar Milner LLP does not express an opinion or any other form of assurance with respect thereto.

For the fiscal quarter ended June 30, 2020, we anticipate that our net revenue will be approximately $6.0 million, an increase of approximately 100% compared to our net revenue of approximately $3.0 million for the quarter ended June 30, 2019.

For the fiscal year ended June 30, 2020, we anticipate that our net revenue will be approximately $16.5 million, an increase of approximately 77% compared to our revenue of approximately $9.3 million for the fiscal year ended June 30, 2019.

2020 Financing. From April to July 15, 2020, pursuant to a private placement offering, we sold and issued an aggregate of 341,250 shares of common stock, at $4.00 per share, for an aggregate purchase price of $1,365,000 in cash to eight (8) accredited investors. Esenjay Investm ent, LLC (Esenjay) and Mr. Dutt, our president and chief executive officer, participated in the offering in the amount of $300,000 and $50,000, respectively. Esenjay is a majority stockholder and a company owned and controlled by Michael Johnson, our director.

LOC Conversion. On June 30, 2020, there was a partial conversion of the debt underlying the secured promissory notes issued to lenders under our line of credit for up to $12,000,000 (LOC) with Esenjay, Cleveland Capital, L.P. (Cleveland), and other unrelated parties (Cleveland and Esenjay, together with additional parties that joined and may join as additional lenders, collectively the Lenders). Certain Lenders exercised their option to convert all or a portion of their outstanding principal and accrued interest in the aggregate amount of approximately $7,383,000 into 1,845,828 shares of common stock at $4.00 per share (the Conversion). Immediately prior to the Conversion, there was an aggregate of approximately $11,791,000 in principal and accrued interest outstanding under all the secured promissory notes evidencing the advance under the LOC. The Conversion consisted of (a) partial conversion of the principal plus accrued interest under the note issued to Esenjay under the LOC (Esenjay LOC Note) in the amount of $4,400,000 into 1,100,000 shares of common stock at $4.00 per share, and (b) approximately $2,983,000 of the secured promissory notes issued in connection with the LOC, principal plus accrued interest, by other lenders, including certain assignees of the Esenjay LOC Note, into 745,828 shares of common stock. Immediately after the Conversion, there was approximately $4,792,000, principal plus accrued interest, of which approximately $823,000 was outstanding under the Esenjay LOC Note and approximately $3,968,000 was outstanding under the other Lender’s respective notes. As of June 30, 2020, the outstanding balance under the LOC, at the option of the note holders, is convertible into approximately 1,197,887 shares of common stock at $4.00 per share. As of July 15, 2020, there was approximately $7,208,000 available for draw under the LOC.

| 6 |

Esenjay Note Conversion. On June 30, 2020, two accredited individuals, who became note holders to the unsecured note for $1,400,000 originally issued to Esenjay (Esenjay Note), pursuant to the assignment of such notes by Esenjay to the note holders, elected to convert $500,000 in principal plus accrued interest, into 125,000 shares of common stock at $4.00 per share (Esenjay Note Conversion). Immediately prior to the Esenjay Note Conversion, there was an aggregate of approximately $1,447,000 in principal and accrued interest outstanding under the Esenjay Note. Immediately after the Esenjay Note Conversion, there was approximately $947,000 outstanding under the Esenjay Note, which is convertible into approximately 237,000 shares of common stock at the option of the note holder(s) at $4.00 per share.

Reverse Stock Split. We effected a 1-for-10 reverse split of our common stock and preferred stock on July 11, 2019 (2019 Reverse Split). No fractional shares were issued in connection with the 2019 Reverse Split. If, as a result of the 2019 Reverse Split, a stockholder would otherwise have been entitled to a fractional share, each fractional share was rounded up. The 2019 Reverse Split resulted in a reduction of our outstanding shares of common stock from 51,000,868 to 5,101,580. In addition, it resulted in a reduction of our authorized shares of common stock from 300,000,000 to 30,000,000, and a reduction of our authorized shares of preferred stock from 5,000,000 to 500,000. The par value of our stock remained unchanged at $0.001.

Corporate Information

We were incorporated in Nevada in 1998. In May 2012, we changed our name to Flux Power Holdings, Inc. We operate our business through our wholly-owned subsidiary, Flux Power, Inc. (Flux Power). Our principal executive office is located at 2685 S. Melrose Drive, Vista, CA 92081. The telephone number at our principal executive office is (760) 741-3589 (FLUX).

| 7 |

| Common Stock offered by us | [total number of shares offered] shares of our common stock (_____________ shares if the underwriters exercise the over-allotment option in full). | |

| Common Stock to be outstanding after this offering | ______________ shares of common stock(1) (________________ shares if the underwriters exercise the over-allotment option in full). | |

| Use of Proceeds | We intend to use the net proceeds of this offering for working capital and general corporate purposes. See ‘‘Use of Proceeds’’ on page 20 of this prospectus. | |

| Risk Factors | Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 9. | |

| OTCQB Symbol | Our common stock is quoted on the OTCQB under the symbol “FLUX.” | |

| Proposed NASDAQ Listing and symbol | We have applied to list our common stock on The NASDAQ Capital Market under the symbol “FLUX.” We will not consummate this offering unless our common stock is approved for listing on The NASDAQ Capital Market. |

(1) The table and discussion above are based on 7,419,675 shares of common stock outstanding as of July 15, 2020, and excludes the following:

● 579,584 shares of common stock issuable upon exercise of outstanding stock options at a weighted average exercise price of $11.00 per share;

● 444,057 shares of common stock remain available for grant under our Equity Incentive Plan;

● outstanding convertible notes to purchase approximately 1,045,536 shares of our common stock at a conversion price of $4.00 per share; and

● the number shares of common stock issuable under outstanding Cleveland Warrant, which number is indeterminable on July 15, 2020 and shall be determined at the closing of our private placement pursuant to the terms of the warrant.

Except as otherwise indicated herein, all information in this prospectus assumes no exercise by the underwriters of their over-allotment option to purchase additional shares.

| 8 |

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this prospectus, before making an investment decision. If any of the following risks actually occur, our business, financial condition or results of operations could suffer. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment. You also should read the section entitled “Special Note Regarding Forward Looking Statements.”

Risk Factors Relating to Our Business

We have a history of losses and negative working capital.

For the nine months ended March 31, 2020, and the year ended June 30, 2019, we had net losses of $11,086,000 and $12,414,000 respectively. We have historically experienced net losses and until we generate sufficient revenue, we anticipate to continue to experience losses in the near future.

In addition, as of March 31, 2020 and June 30, 2019, we had a negative working capital (including short term debt) of $13,474,000 and $3,644,000, respectively. As of March 31, 2020, we had a cash balance of $106,000. We expect that our existing cash balances, credit facilities, and the expected net proceeds of this offering will be sufficient to fund our existing and planned operations for the next twelve months from the date of this prospectus. Until such time as we generate sufficient cash to fund our operations, we will need additional capital to continue our operations thereafter.

We have relied on equity financings, borrowings under short-term loans with related parties, our credit facilities and/or previous cash flows from operating activities to fund our operations. However, there is no guarantee we will be able to obtain additional funds in the future or that funds will be available on terms acceptable to us, if at all. See “Risk Factors” – “We will need to raise additional capital or financing after this offering to continue to execute and expand our business” and “We are dependent on our existing credit facility to finance our operations and in the event of default, such default could adversely affect our business, financial condition, results of operations or liquidity.”

Any future financing may result in dilution of the ownership interests of our stockholders. If such funds are not available on acceptable terms, we may be required to curtail our operations or take other actions to preserve our cash, which may have a material adverse effect on our future cash flows and results of operations.

We may need to raise additional capital or financing after this offering to continue to execute and expand our business.

While we expect that our available cash, credit facilities, and the expected net proceeds from this offering will be sufficient to sustain our operations for the next twelve months from the date of this prospectus, we may need to raise additional capital after this offering to support our operations and execute on our business plan. We may be required to pursue sources of additional capital through various means, including joint venture projects, sale and leasing arrangements, and debt or equity financings. Any new securities that we may issue in the future may be sold on terms more favorable for our new investors than the terms of this offering. Newly issued securities may include preferences, superior voting rights, and the issuance of warrants or other convertible securities that will have additional dilutive effects. We cannot assure that additional funds will be available when needed from any source or, if available, will be available on terms that are acceptable to us. Further, we may incur substantial costs in pursuing future capital and/or financing, including investment banking fees, legal fees, accounting fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition and results of operations. Our ability to obtain needed financing may be impaired by such factors as the weakness of capital markets, and the fact that we have not been profitable, which could impact the availability and cost of future financings. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, we may have to reduce our operations accordingly.

| 9 |

We are dependent on our existing credit facility and Factoring Agreement to finance our operations and in the event of default, such default could adversely affect our business, financial condition, results of operations or liquidity.

We have substantial indebtedness and have relied on our short-term loans with related parties, and credit facilities to provide working capital. As of March 31, 2020, and June 30, 2019, we had an outstanding principal balance of $11,591,000 and $6,405,000, respectively, under our line of credit for up to $12,000,000 bearing an interest rate of 15% (LOC) with Esenjay Investment, LLC (Esenjay), a majority stockholder and a company owned and controlled by Michael Johnson, our director, Cleveland, and other unrelated parties (Cleveland and Esenjay, together with additional parties that joined and may join as additional lenders, collectively the Lenders). In addition, as of March 31, 2020, we had an outstanding principal balance of $1,115,000 under our unsecured short-term promissory note with Cleveland (Cleveland Note), which note bears an interest of 15% and is due on July 31, 2020, unless repaid earlier from a percentage of proceeds from certain identified accounts receivable. In addition, as of July 15, 2020, we have an outstanding principal balance of approximately $947,000 under our unsecured short-term convertible promissory note with Esenjay, which note bears an interest rate of 15% (Esenjay Note). As of July 15, 2020, approximately $4,792,000 in principal and accrued interest is outstanding under the LOC, and approximately $7,208,000 is available for future draws. However, our ability to borrow under the LOC is at the discretion of the Lenders. Also, the Lenders have no obligation to disburse such funds and have the right not to advance funds under the LOC. In addition, as a secured party, upon an event of default, the Lenders will have a right to the collateral granted to them under the line of credit, and we may lose our ownership interest in the assets. In addition, on August 23, 2019, we entered into a Factoring Agreement (Factoring Agreement) with CSNK Working Capital Finance Corp. d/b/a Bay View Funding (CSNK) for a factoring facility under which CSNK will, from time to time, buy approved receivables from the Company. The factoring facility provides for the Company to have access to the lesser of (i) $3 million (Maximum Credit) or (ii) the sum of all undisputed receivables purchased by CSNK multiplied by 90% (which percentages may be adjusted by CSNK in its sole discretion). We have given CSNK a termination notice to terminate our Factoring Agreement effective August 30, 2020. The Lenders and CSNK have a security interest in our assets. Secured parties, upon an event of default, will have a right to the collateral granted to them under the line of credit, and we may lose our ownership interest in the assets. A loss of our collateral will have a material adverse effect on our operations, our business and financial condition.

Our independent auditors have expressed substantial doubt about our ability to continue as a going concern.

In their audit report issued in connection with our financial statements for the year ended June 30, 2019, and for the years then ended, our independent registered public accounting firm included a going concern explanatory paragraph which stated there was substantial doubt about our ability to continue as a going concern. We have prepared our financial statements on a going concern basis that contemplates the realization of assets and the satisfaction of liabilities in the normal course of business for the foreseeable future. Our financial statements do not include any adjustments that would be necessary should we be unable to continue as a going concern and, therefore, be required to liquidate our assets and discharge our liabilities in other than the normal course of business and at amounts different from those reflected in our financial statements. If we are unable to continue as a going concern, our stockholders may lose all or a substantial portion or all of their investment.

We are dependent on a few customers for the majority of our net revenues, and our success depends on demand from OEMs and other users of our battery products.

Historically a majority of our product sales have been generated from a small number of OEMs and end-user customers, including three customers who, on an aggregate basis, made up 76% of our sales for the nine months ended March 31, 2020, and four end-user customers who, on an aggregate basis, made up 87% of our sales for the year ended June 30, 2019. As a result, our success depends on continued demand from this small group of customers and their willingness to incorporate our battery products in their equipment. The loss of a significant customer would have an adverse effect on our revenues. There is no assurance that we will be successful in our efforts to convince end users to accept our products. Our failure to gain acceptance of our products could have a material adverse effect on our financial condition and results of operations.

Additionally, OEMs, their dealers and battery distributors may be subject to changes in demand for their equipment which could significantly affect our business, financial condition and results of operations.

Actual net revenue for fiscal year 2020 could differ from our expectations.

While we believe that our expectations for our net revenue for the fourth fiscal quarter of 2020 and the fiscal year ended June 30, 2020 are based on reasonable assumptions, our actual results may vary, and such variations may be material. Factors that could cause our expectations to differ include, but are not limited to: (i) unanticipated adjustments in the calculation of, or application of accounting principles for, our net revenue for such period and (ii) discovery of new information that affects the recognition of revenue for such period. Our expectations are also subject to a number of additional risks and uncertainties, including those identified in “Special Note Regarding Forward-Looking Statements” and “Risk Factors.” There is no assurance that such expectations will prove to be correct.

| 10 |

Our business is vulnerable to a near-term severe impact from the COVID-19 outbreak, and the continuation of the pandemic could have a material adverse impact on our operations and financial condition.

The recent outbreak of the coronavirus, COVID-19, which on March 10, 2020, has been declared by the World Health Organization to be a pandemic, has spread across the globe and is impacting worldwide economic activity. A pandemic, including COVID-19 or other public health epidemic, poses the risk that we or our employees, contractors, customers, suppliers, third party shipping carriers, government and other partners may be prevented from or limited in their ability to conduct business activities for an indefinite period of time, including due to the spread of the disease within these groups or due to shutdowns that may be requested or mandated by governmental authorities. While it is not possible at this time to estimate the impact that COVID-19 could have on our business, the continued spread of COVID-19 and the measures taken by the governments of states and countries affected could disrupt, among other things, the supply chain and the manufacture or shipment of our products. On March 19, 2020, the governor of California, the state where our facility is located, issued statewide stay-at-home orders for non-essential workers to help combat the spread of COVID-19. The Company was deemed to be an essential business consistent with announcements by Forklift OEMs and related supply chain, who support the logistics industry, critical to delivering food and supplies during COVID-19 crisis and we have instituted processes, policies and workplace procedures in an effort to keep our workers safe while productive. Our manufacturing operations may be subject to closure or shut down due to the spread of the disease within our production employees, or as part of a larger scale government recommendation or mandate. While the Company implemented COVID-19 measures in March as recommended by the CDC and governmental authorities, the Company recently had two employees tested positive for COVID-19, although manufacturing operations were not materially impacted. However, any substantial disruption in our manufacturing operations would have a material adverse effect on our business and would impede our ability to manufacture and ship products to our customers in a timely manner, or at all.

The effect of the COVID-19 pandemic and its associated restrictions may adversely impact many aspects of our business, including customer demand, the length of our sales cycles, disruptions in our supply chain, lower the operating efficiencies at our facility, worker shortages and declining staff morale, and other unforeseen disruptions. The demand for our products may significantly decline as COVID-19 continues to spread and as our customers suffer losses in their businesses. In January 2020, we received a $4,680,000 order for additional airport GSE batteries from an existing global airline customer. Due to the COVID-19 crisis and its effect to the airline segment, the customer requested that the order to be reduced to approximately $2,700,000 and be delivered in monthly shipments up to November 2020. The supply of our raw materials and our supply chain may be disrupted and adversely impacted by the pandemic. The occurrence of any of the foregoing events and their adverse effect on capital markets and investor sentiment may adversely impact our ability to raise capital when needed or on terms favorable to us and our stockholders to fund our operations, which could have a material adverse effect on our business, financial condition and results of operations. The extent to which the COVID-19 outbreak impacts our results, its effect on near or long-term value of our share price will depend on future developments that are highly uncertain and cannot be predicted, including new information that may emerge concerning the severity of the virus and the actions to contain its impact.

We do not have long term contracts with our customers.

We do not have long-term contracts with our customers. Future agreements with respect to pricing, returns, promotions, among other things, are subject to periodic negotiation with each customer. No assurance can be given that our customers will continue to do business with us. The loss of any of our significant customers will have a material adverse effect on our business, results of operations, financial condition and liquidity. In addition, the uncertainty of product orders can make it difficult to forecast our sales and allocate our resources in a manner consistent with actual sales, and our expense levels are based in part on our expectations of future sales. If our expectations regarding future sales are inaccurate, we may be unable to reduce costs in a timely manner to adjust for sales shortfalls.

| 11 |

Real or perceived hazards associated with Lithium-ion battery technology may affect demand for our products.

Press reports have highlighted situations in which lithium-ion batteries in automobiles and consumer products have caught fire or exploded. In response, the use and transportation of lithium-ion batteries has been prohibited or restricted in certain circumstances. This publicity has resulted in a public perception that lithium-ion batteries are dangerous and unpredictable. Although we believe our battery packs are safe, these perceived hazards may result in customer reluctance to adopt our lithium-ion based technology.

Our products may experience quality problems from time to time that could result in negative publicity, litigation, product recalls and warranty claims, which could result in decreased revenues and harm to our brands.

A catastrophic failure of our battery modules could cause personal or property damages for which we would be potentially liable. Damage to or the failure of our battery packs to perform to customer specifications could result in unexpected warranty expenses or result in a product recall, which would be time consuming and expensive. Such circumstances could result in negative publicity or lawsuits filed against us related to the perceived quality of our products which could harm our brand and decrease demand for our products.

We may be subject to product liability claims.

If one of our products were to cause injury to someone or cause property damage, including as a result of product malfunctions, defects, or improper installation, then we could be exposed to product liability claims. We could incur significant costs and liabilities if we are sued and if damages are awarded against us. Further, any product liability claim we face could be expensive to defend and could divert management’s attention. The successful assertion of a product liability claim against us could result in potentially significant monetary damages, penalties or fines, subject us to adverse publicity, damage our reputation and competitive position, and adversely affect sales of our products. In addition, product liability claims, injuries, defects, or other problems experienced by other companies in the solar industry could lead to unfavorable market conditions for the industry as a whole, and may have an adverse effect on our ability to attract new customers, thus harming our growth and financial performance. Although we carry product liability insurance, it may be insufficient in amount to cover our claims.

Tariffs that might be imposed on lithium-ion batteries by the United States government or a resulting trade war could have a material adverse effect on our results of operations.

In 2018, the United States government announced tariffs on certain steel and aluminum products imported into the United States, which has led to reciprocal tariffs being imposed by the European Union and other governments on products imported from the United States. The United States government has implemented tariffs on goods imported from China, and additional tariffs on goods imported from China are under consideration.

The lithium-ion battery industry has been subjected to tariffs implemented by the United States government on goods imported from China. Further if the U.S. and China are not able to resolve their differences, new and additional tariffs may be put in place and additional products, including lithium-ion batteries, may become subject to tariffs. Since all of our lithium-ion batteries are manufactured in China, current and potential tariffs on lithium-ion batteries imported by us from China would increase our costs, require us to increase prices to our customers or, if we are unable to do so, result in lower gross margins on the products sold by us.

The President of the United States has, at times, threatened to institute even wider ranging tariffs on all goods imported from China. China has already imposed tariffs on a wide range of American products in retaliation for the American tariffs on steel and aluminum. Additional tariffs could be imposed by China in response to actual or threatened tariffs on products imported from China. The imposition of additional tariffs by the United States could trigger the adoption of tariffs by other countries as well. Any resulting escalation of trade tensions, including a “trade war,” could have a significant adverse effect on world trade and the world economy, as well as on our results of operations. At this time, we cannot predict how the recently enacted tariffs will impact our business. Tariffs on components imported by us from China could have a material adverse effect on our business and results of operations.

| 12 |

Economic conditions may adversely affect consumer spending and the overall general health of our retail customers, which, in turn, may adversely affect our financial condition, results of operations and cash resources.

Uncertainty about the existing and future global economic conditions may cause our customers to defer purchases or cancel purchase orders for our products in response to tighter credit, decreased cash availability and weakened consumer confidence. Our financial success is sensitive to changes in general economic conditions, both globally and nationally. Recessionary economic cycles, higher interest borrowing rates, higher fuel and other energy costs, inflation, increases in commodity prices, higher levels of unemployment, higher consumer debt levels, higher tax rates and other changes in tax laws or other economic factors that may affect consumer spending or buying habits could continue to adversely affect the demand for our products. If credit pressures or other financial difficulties result in insolvency for our customers it could adversely impact our financial results. There can be no assurances that government and consumer responses to the disruptions in the financial markets will restore consumer confidence.

We are dependent on a limited number of suppliers for our battery cells, and the inability of these suppliers to continue to deliver, or their refusal to deliver, our battery cells at prices and volumes acceptable to us would have a material adverse effect on our business, prospects and operating results.

We do not manufacture the battery cells used in our LiFT Packs. Our battery cells, which are an integral part of our battery products and systems, are sourced from a limited number of manufacturers located in China. While we obtain components for our products and systems from multiple sources whenever possible, we have spent a great deal of time in developing and testing our battery cells that we receive from our suppliers. We refer to the battery cell suppliers as our limited source suppliers. To date, we have not qualified alternative sources for our battery cells although we research and assess cells from other suppliers on an ongoing basis. We generally do not maintain long-term agreements with our limited source suppliers. While we believe that we will be able to establish additional supplier relationships for our battery cells, we may be unable to do so in the short term or at all at prices, quality or costs that are favorable to us.

Changes in business conditions, wars, regulatory requirements, economic conditions and cycles, governmental changes and other factors beyond our control could also affect our suppliers’ ability to deliver components to us on a timely basis or cause us to terminate our relationship with them and require us to find replacements, which we may have difficulty doing. Furthermore, if we experience significant increased demand, or need to replace our existing suppliers, there can be no assurance that additional supplies of component parts will be available when required on terms that are favorable to us, at all, or that any supplier would allocate sufficient supplies to us in order to meet our requirements or fill our orders in a timely manner. In the past, we have replaced certain suppliers because of their failure to provide components that met our quality control standards. The loss of any limited source supplier or the disruption in the supply of components from these suppliers could lead to delays in the deliveries of our battery products and systems to our customers, which could hurt our relationships with our customers and also materially adversely affect our business, prospects and operating results.

Increases in costs, disruption of supply or shortage of raw materials, in particular lithium-ion phosphate cells, could harm our business.

We may experience increases in the costs or a sustained interruption in the supply or shortage of raw materials. Any such increase or supply interruption could materially negatively impact our business, prospects, financial condition and operating results. For instance, we are exposed to multiple risks relating to price fluctuations for lithium-iron phosphate cells.

These risks include:

| ● | the inability or unwillingness of battery manufacturers to supply the number of lithium-iron phosphate cells required to support our sales as demand for such rechargeable battery cells increases; | |

| ● | disruption in the supply of cells due to quality issues or recalls by the battery cell manufacturers; and | |

| ● | an increase in the cost of raw materials, such as iron and phosphate, used in lithium-iron phosphate cells. |

| 13 |

Our success depends on our ability to develop new products and capabilities that respond to customer demand, industry trends or actions by our competitors and failure to do so may cause us to lose our competitiveness in the battery industry and may cause our profits to decline.

Our success will depend on our ability to develop new products and capabilities that respond to customer demand, industry trends or actions by our competitors. There is no assurance that we will be able to successfully develop new products and capabilities that adequately respond to these forces. In addition, changes in legislative, regulatory or industry requirements or in competitive technologies may render certain of our products obsolete or less attractive. If we are unable to offer products and capabilities that satisfy customer demand, respond adequately to changes in industry trends or legislative changes and maintain our competitive position in our markets, our financial condition and results of operations would be materially and adversely affected.

The research and development of new products and technologies is costly and time consuming, and there are no assurances that our research and development of new products will be either successful or completed within anticipated timeframes, if at all. Our failure to technologically evolve and/or develop new or enhanced products may cause us to lose competitiveness in the battery market. In addition, in order to compete effectively in the renewable battery industry, we must be able to launch new products to meet our customers’ demands in a timely manner. However, we cannot provide assurance that we will be able to install and certify any equipment needed to produce new products in a timely manner, or that the transitioning of our manufacturing facility and resources to full production under any new product programs will not impact production rates or other operational efficiency measures at our manufacturing facility. In addition, new product introductions and applications are risky, and may suffer from a lack of market acceptance, delays in related product development and failure of new products to operate properly. Any failure by us to successfully launch new products, or a failure by our customers to accept such products, could adversely affect our results.

Our business will be adversely affected if we are unable to protect our intellectual property rights from unauthorized use or infringement by third parties.

Any failure to protect our proprietary rights adequately could result in our competitors offering similar products, potentially resulting in the loss of some of our competitive advantage and a decrease in our revenue, which would adversely affect our business, prospects, financial condition and operating results. Our success depends, at least in part, on our ability to protect our core technology and intellectual property. To accomplish this, we rely on a combination of patents, patent applications, trade secrets, including know-how, employee and third-party nondisclosure agreements, copyright laws, trademarks, intellectual property licenses and other contractual rights to establish and protect our proprietary rights in our technology.

The protection provided by the patent laws is and will be important to our future opportunities. However, such patents and agreements and various other measures we take to protect our intellectual property from use by others may not be effective for various reasons, including the following:

| ● | the patents we have been granted may be challenged, invalidated or circumvented because of the pre-existence of similar patented or unpatented intellectual property rights or for other reasons; | |

| ● | the costs associated with enforcing patents, confidentiality and invention agreements or other intellectual property rights may make aggressive enforcement impracticable; and | |

| ● | existing and future competitors may independently develop similar technology and/or duplicate our systems in a way that circumvents our patents. |

Our patent applications may not result in issued patents, which may have a material adverse effect on our ability to prevent others from commercially exploiting products similar to ours.

Our patent applications may not result in issued patents, which may have a material adverse effect on our ability to prevent others from commercially exploiting products similar to ours.

| 14 |

We cannot be certain that we are the first creator of inventions covered by pending patent applications or the first to file patent applications on these inventions, nor can we be certain that our pending patent applications will result in issued patents or that any of our issued patents will afford protection against a competitor. In addition, patent applications that we intend to file in foreign countries are subject to laws, rules and procedures that differ from those of the United States, and thus we cannot be certain that foreign patent applications related to issue United States patents will be issued. Furthermore, if these patent applications issue, some foreign countries provide significantly less effective patent enforcement than in the United States.

The status of patents involves complex legal and factual questions and the breadth of claims allowed is uncertain. As a result, we cannot be certain that the patent applications that we file will result in patents being issued, or that our patents and any patents that may be issued to us in the near future will afford protection against competitors with similar technology. In addition, patents issued to us may be infringed upon or designed around by others and others may obtain patents that we need to license or design around, either of which would increase costs and may adversely affect our business, prospects, financial condition and operating results.

We rely on trade secret protections through confidentiality agreements with our employees, customers and other parties; the breach of such agreements could adversely affect our business and results of operations.

We rely on trade secrets, which we seek to protect, in part, through confidentiality and non-disclosure agreements with our employees, customers and other parties. There can be no assurance that these agreements will not be breached, that we would have adequate remedies for any such breach or that our trade secrets will not otherwise become known to or independently developed by competitors. To the extent that consultants, key employees or other third parties apply technological information independently developed by them or by others to our proposed projects, disputes may arise as to the proprietary rights to such information that may not be resolved in our favor. We may be involved from time to time in litigation to determine the enforceability, scope and validity of our proprietary rights. Any such litigation could result in substantial cost and diversion of effort by our management and technical personnel.

Our business depends substantially on the continuing efforts of the members of our senior management team, and our business may be severely disrupted if we lose their services.

We believe that our success is largely dependent upon the continued service of the members of our senior management team, who are critical to establishing our corporate strategies and focus, and ensuring our continued growth. We are a smaller company with a limited number of personnel. Because of this dependence, the Company may be more adversely affected by the loss of a member of our senior management than at a larger company. Our continued success will depend on our ability to attract and retain a qualified and competent management team in order to manage our existing operations and support our expansion plans. Although we are not aware of any change, if any of the members of our senior management team are unable or unwilling to continue in their present positions, we may not be able to replace them readily. Therefore, our business may be severely disrupted, and we may incur additional expenses to recruit and retain their replacement. In addition, if any of the members of our senior management team joins a competitor or forms a competing company, we may lose some of our customers.

We may be required to obtain the approval of various government agencies to market our products.

Our products are subject to product safety regulations by Federal, state, and local organizations. Accordingly, we may be required, or may voluntarily determine to, obtain approval of our products from one or more of the organizations engaged in regulating product safety. These approvals could require significant time and resources from our technical staff, and, if redesign were necessary, could result in a delay in the introduction of our products in various markets and applications. There can be no assurance that we will obtain any or all of the approvals that may be required to market our products.

| 15 |

We may face significant costs relating to environmental regulations for the storage and shipment of our lithium-ion battery packs.

Federal, state, and local regulations impose significant environmental requirements on the manufacture, storage, transportation, and disposal of various components of advanced energy storage systems. Although we believe that our operations are in material compliance with applicable environmental regulations, there can be no assurance that changes in such laws and regulations will not impose costly compliance requirements on us or otherwise subject us to future liabilities. Moreover, Federal, state, and local governments may enact additional regulations relating to the manufacture, storage, transportation, and disposal of components of advanced energy storage systems. Compliance with such additional regulations could require us to devote significant time and resources and could adversely affect demand for our products. There can be no assurance that additional or modified regulations relating to the manufacture, storage, transportation, and disposal of components of advanced energy systems will not be imposed.

Natural disasters, public health crises, political crises and other catastrophic events or other events outside of our control may damage our sole facility or the facilities of third parties on which we depend, and could impact consumer spending.

Our sole production facility is located in southern California near major geologic faults that have experienced earthquakes in the past. An earthquake or other natural disaster or power shortages or outages could disrupt our operations or impair critical systems. Any of these disruptions or other events outside of our control could affect our business negatively, harming our operating results. In addition, if our sole facility, or the facilities of our suppliers, third-party service providers or customers, is affected by natural disasters, such as earthquakes, tsunamis, power shortages or outages, floods or monsoons, public health crises, such as pandemics and epidemics, political crises, such as terrorism, war, political instability or other conflict, or other events outside of our control, our business and operating results could suffer. Moreover, these types of events could negatively impact consumer spending in the impacted regions or, depending upon the severity, globally, which could adversely impact our operating results. Similar disasters occurring at our vendors’ manufacturing facilities could impact our reputation and our consumers’ perception of our brands.

Risks Related to the Offering, Our Common Stock and Market

If you purchase shares of common stock in this offering, you will suffer immediate and substantial dilution of your investment.

Because the public offering price per share of our common stock in this offering is expected to exceed the net tangible book value per share of our common stock, you will suffer immediate and substantial dilution in the pro forma as adjusted net tangible book value of the common stock you purchase in this offering. Therefore, if you purchase shares of our common stock in this offering, you may pay a price per share that substantially exceeds our pro forma net tangible book value per share after this offering. Assuming the sale of [total number of shares offered] shares of our common stock at a public offering price of $______ per share, the closing bid price of our common stock on the OTCQB on ____, 2020, after deducting the underwriting discount and estimated offering expenses payable by us, you will incur immediate dilution of $______ per share. See the section entitled “Dilution” below for a more detailed discussion of the dilution you will incur if you participate in this offering. To the extent shares are issued under outstanding options and warrants at exercise prices lower than the public offering price of our common stock in this offering, you will incur further dilution.

We have a substantial amount of convertible debt which may be converted into shares of our common stock at below the offering price which will cause an immediate dilution to investors participating in the offering.

As of June 30, 2020, we had approximately $5,739,000 in convertible debt, principal and accrued interest, under the Esenjay Note and the LOC, which may be converted into approximately 1,045,536 shares of our common stock at $4.00 per share at the option of the holder. If the convertible debt holders exercise their right to convert the convertible debt into shares of common stock, this will cause an immediate dilutive effect to the investors who participate in this offering. In addition, because the shares of common stock to be received upon the conversion of the convertible debt may be sold in the market in the future, the resale of a large number of shares of common stock upon the conversion of the convertible debt may adversely affect the market price of our common stock.

| 16 |

You may experience future dilution as a result of future equity offerings.

In order to raise additional capital, we may at any time offer additional shares of our common stock or other securities convertible into or exchangeable for our common stock at prices that may not be the same as the price per share in this offering. We may sell shares or other securities in any other offering at a price per share that is less than the public offering price per share in this offering, and investors purchasing shares or other securities in the future could have rights superior to existing stockholders. The price per share at which we sell additional shares of our common stock, or securities convertible or exchangeable into common stock, in future transactions may be higher or lower than the public offering price per share paid by investors in this offering.

We have broad discretion in the use of our cash and cash equivalents, including the net proceeds we receive in this offering, and may not use them effectively.

Our management has broad discretion to use our cash and cash equivalents, including the net proceeds we receive in this offering, to fund our operations and could spend these funds in ways that do not improve our results of operations or enhance the value of our common stock, and you will not have the opportunity as part of your investment decision to assess whether the net proceeds are being used appropriately. The failure by our management to apply these funds effectively could result in financial losses that could have a material adverse effect on our business, cause the price of our common stock to decline. Pending their use to fund our operations, we may invest our cash and cash equivalents, including the net proceeds from this offering, in a manner that does not produce income or that loses value.

The market price of our common stock can become volatile, leading to the possibility of its value being depressed at a time when you may want to sell your holdings.

We have applied to list our common stock on The NASDAQ Capital Market under the symbol “FLUX.” We will not consummate this offering unless our common stock is approved for listing on The NASDAQ Capital Market. We cannot predict the extent to which investor interest in our company will lead to the development of an active trading market on that stock exchange or any other exchange in the future. The trading price of our common stock has experienced volatility while trading on the OTCQB and is likely to continue to be highly volatile in response to numerous factors, many of which are beyond our control, including, without limitation, the following:

| ● | our earnings releases, actual or anticipated changes in our earnings, fluctuations in our operating results or our failure to meet the expectations of financial market analysts and investors; | |

| ● | changes in financial estimates by us or by any securities analysts who might cover our stock; | |

| ● | speculation about our business in the press or the investment community; | |

| ● | significant developments relating to our relationships with our customers or suppliers; | |

| ● | stock market price and volume fluctuations of other publicly traded companies and, in particular, those that are in our industry; | |

| ● | limited “public float” in the hands of a small number of persons whose sales or lack of sales could result in positive or negative pricing pressure on the market price for our common stock; | |

| ● | customer demand for our products; | |

| ● | investor perceptions of our industry in general and our Company in particular; |

| 17 |

| ● | general economic conditions and trends; | |

| ● | announcements by us or our competitors of new products, significant acquisitions, strategic partnerships or divestitures; | |

| ● | changes in accounting standards, policies, guidance, interpretation or principles; |

| ● | loss of external funding sources; | |

| ● | sales of our common stock, including sales by our directors, officers or significant stockholders; and | |

| ● | additions or departures of key personnel. |

The ownership of our stock is highly concentrated in our management, and we have one controlling stockholder.

As of July 15, 2020, our directors and executive officers, and their respective affiliates beneficially owned approximately 62.0% of our outstanding common stock, including common stock underlying options, warrants and convertible debt that were exercisable or convertible or which would become exercisable or convertible within 60 days. Michael Johnson, our director and beneficial owner of Esenjay, beneficially owns approximately 60.4% of such outstanding common stock. As a result of their ownership, our directors and executive officers and their respective affiliates collectively, and Esenjay, individually, are able to significantly influence all matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions. This concentration of ownership may also have the effect of delaying or preventing a change in control.

We do not intend to pay dividends on shares of our common stock for the foreseeable future.

We have never declared or paid any cash dividends on shares of our common stock. We intend to retain any future earnings to fund the operation and expansion of our business and, therefore, we do not anticipate paying cash dividends on shares of our common stock in the foreseeable future.

Our common stock is illiquid and the lack of liquidity may adversely affect the trading price of our common stock.

We have applied to list our common stock on The NASDAQ Capital Market under the symbol “FLUX.” We will not consummate this offering unless our common stock is approved for listing on The NASDAQ Capital Market. The trading volume of our common stock on the OTCQB is relatively small. Because of the lack of liquidity in our common stock on the OTCQB, small fluctuations in the demand for our common stock may have significant impact on the trading price of our common stock. A more active market for the common stock may never develop. We cannot assure you that the volume of trading in shares of our common stock will increase in the future . The lack of liquidity may impact your ability to sell your shares of common stock at an acceptable price, if at all.

Even if we are listed on The NASDAQ Capital Market, there can be no assurance that we will be able to comply with continued listing standards of The NASDAQ Capital Market.

Even if we sustain a market price of our common stock sufficient to obtain an initial listing on The NASDAQ Capital Market, we cannot assure you that we will be able to continue to comply with the minimum bid price and the other standards that we are required to meet in order to maintain a listing of our common stock on The NASDAQ Capital Market. Our failure to continue to meet these requirements may result in our common stock being delisted from The NASDAQ Capital Market.

Preferred Stock may be issued under our Articles of Incorporation which may have superior rights to our common stock.

Our Articles of Incorporation authorize the issuance of up to 500,000 shares of preferred stock. The preferred stock may be issued in one or more series, the terms of which may be determined at the time of issuance. These terms may include voting rights including the right to vote as a series on particular matters, preferences as to dividends and liquidation, conversion rights, redemption rights and sinking fund provisions. In addition, these voting, conversion and exchange rights of preferred stock could negatively affect the voting power or other rights of our common stockholders. The issuance of any preferred stock could diminish the rights of holders of our common stock, or delay or prevent a change of control of our Company, and therefore could reduce the value of such common stock.

| 18 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. The forward-looking statements are contained principally in the sections entitled “Description of Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. These risks and uncertainties include, but are not limited to, the factors described in the section captioned “Risk Factors” below. In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would,” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. You should read these factors and the other cautionary statements made in this prospectus and in the documents we incorporate by reference into this prospectus as being applicable to all related forward-looking statements wherever they appear in this prospectus or the documents we incorporate by reference into this prospectus. If one or more of these factors materialize, or if any underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from any future results, performance or achievements expressed or implied by these forward-looking statements.

Given these uncertainties, you should not place undue reliance on these forward-looking statements. These forward-looking statements include, among other things, statements relating to:

| ● | our ability to continue as a going concern; | |

| ● | our ability to secure sufficient funding and alternative source of funding to support our current and proposed operations, which could be more difficult in light of the negative impact of the COVID-19 pandemic on investor sentiment and investing ability; | |

| ● | our anticipated growth strategies and our ability to manage the expansion of our business operations effectively; | |

| ● | our ability to maintain or increase our market share in the competitive markets in which we do business; | |

| ● | our ability to grow net revenue and increase our gross profit margin; | |