Attached files

| file | filename |

|---|---|

| 8-K - 8-K - SLM Student Loan Trust 2006-5 | brhc10013490_8k.htm |

|

Class

|

Outstanding Principal Amount

|

Interest Rate

|

Price

|

Next Reset Date

|

Legal Maturity Date

|

|||||

|

Class A-6B Notes

|

$200,000,000

|

3-month LIBOR

plus %

|

100%

|

October 26, 2020

|

October 25, 2040

|

|||||

|

Class A-6C Notes

|

$200,000,000

|

3-month LIBOR

plus %

|

100%

|

October 26, 2020

|

October 25, 2040

|

|

|

Class A-6B Notes |

Class A-6C Notes

|

|

Original principal amount

|

$200,000,000

|

$200,000,000

|

|

Current outstanding principal balance

|

$200,000,000

|

$200,000,000

|

|

Principal amount being remarketed

|

$200,000,000(1)

|

$200,000,000(1)

|

|

Remarketing Terms Determination Date

|

July 15, 2020

|

July 15, 2020

|

|

Notice Date(2)

|

July 17, 2020

|

July 17, 2020

|

|

Spread Determination Date(3)

|

On or before July 22, 2020

|

On or before July 22, 2020

|

|

Current Reset Date

|

July 27, 2020

|

July 27, 2020

|

|

All Hold Rate

|

Three-Month LIBOR plus 0.75%

|

Three-Month LIBOR plus 0.75%

|

|

Next applicable reset date

|

October 26, 2020

|

October 26, 2020

|

|

Interest rate mode

|

Floating

|

Floating

|

|

Index

|

Three-Month LIBOR(4)

|

Three-Month LIBOR(4)

|

|

Spread(5)

|

Plus %

|

Plus %

|

|

Day-count basis

|

Actual/360

|

Actual/360

|

|

Weighted average remaining life

|

(6)

|

(6)

|

|

REMARKETING TERMS SUMMARY

|

i

|

|

INTRODUCTION

|

iii

|

|

SUMMARY OF NOTE TERMS

|

1

|

|

RISK FACTORS

|

22

|

|

DEFINED TERMS

|

46 |

|

THE TRUST

|

46 |

|

USE OF PROCEEDS

|

50 |

|

AFFILIATIONS AND RELATIONS

|

51 |

|

THE DEPOSITOR

|

51 |

|

NAVIENT CORPORATION

|

53 |

|

THE SPONSOR, SERVICER AND ADMINISTRATOR

|

55 |

|

THE SELLERS

|

56 |

|

THE TRUST STUDENT LOAN POOL

|

57 |

|

THE COMPANIES’ STUDENT LOAN FINANCING BUSINESS

|

62 |

|

TRANSFER AGREEMENTS

|

66 |

|

SERVICING AND ADMINISTRATION

|

69 |

|

TRADING INFORMATION

|

80 |

|

DESCRIPTION OF THE NOTES

|

81 |

|

INDENTURE

|

116 |

|

CERTAIN LEGAL ASPECTS OF THE STUDENT LOANS

|

122 |

|

STATIC POOLS

|

127 |

|

PREPAYMENTS, EXTENSIONS, WEIGHTED AVERAGE REMAINING LIFE AND EXPECTED MATURITY OF THE CLASS A-5 NOTES

|

127 |

|

CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS

|

129 |

|

STATE AND LOCAL TAX CONSEQUENCES

|

139

|

|

ERISA CONSIDERATIONS

|

140 |

|

ACCOUNTING CONSIDERATIONS

|

143 |

|

REPORTS TO NOTEHOLDERS

|

143 |

|

REMARKETING

|

144 |

|

NOTICES TO INVESTORS

|

144 |

|

LISTING INFORMATION

|

145 |

|

DEPOSITOR AFFIRMATIONS

|

146 |

|

CERTAIN INVESTMENT COMPANY ACT CONSIDERATIONS

|

147 |

|

RATINGS

|

147 |

|

LEGAL PROCEEDINGS

|

148 |

|

LEGAL MATTERS

|

152 |

|

GLOSSARY

|

153 |

|

ANNEX A:

|

The Trust Student Loan Pool as of May 31, 2020

|

|

APPENDIX A:

|

Federal Family Education Loan Program

|

|

APPENDIX B:

|

Global Clearance, Settlement and Tax Documentation Procedures

|

|

EXHIBIT I:

|

Prepayments, Extensions, Weighted Average Remaining Life and Expected Maturity of the Class A-6B and Class A-6C Notes

|

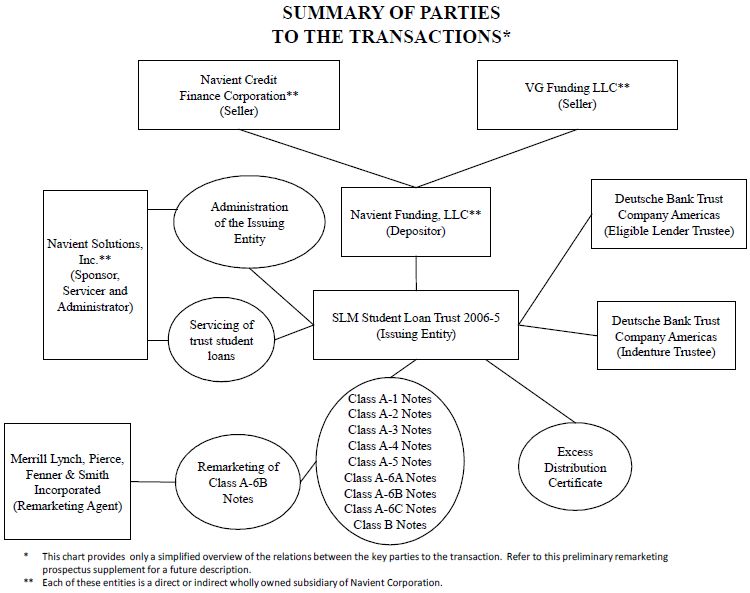

ISSUING ENTITY

SLM Student Loan Trust 2006-5.

Class A-6B AND CLASS A-6C notes

The Reset Rate Class A-6B Student Loan‑Backed Notes that are being remarketed hereunder were originally issued by the trust on June 21, 2006 in the principal amount of $200,000,000 and are currently outstanding in the same amount.

The Reset Rate Class A-6C Student Loan‑Backed Notes that are being remarketed hereunder were originally issued by the trust on June 21, 2006 in the principal amount of $200,000,000 and are currently outstanding in the same amount.

The “initial reset date” for the class A-6B notes was January 25, 2018. A failed remarketing was declared with respect to the class A-6B notes and its initial reset date and each subsequent reset date. Pursuant to the terms of these failed remarketings, (i) the holders of the class A-6B notes were required to retain their notes, (ii) the class A-6B notes were reset to bear interest at the failed remarketing rate, which is an annual rate equal to three-month LIBOR plus 0.75% and (iii) a three-month reset period ending on the next quarterly distribution date was established. The initial reset date for the class A-6C notes was April 25, 2018. A failed remarketing was declared with respect to the class A-6C notes on April 25, 2018 reset date. Pursuant to the terms of this failed remarketing, (i) the holders of the class A-6C notes were required to retain their notes, (ii) the class A-6C notes were reset to bear interest at the failed remarketing rate, which is an annual rate equal to three-month LIBOR plus 0.75% and (iii) a three-month reset period ending on the next quarterly distribution date was established. We refer to the July 27, 2020 reset date as the “current reset date” in this free-writing prospectus. The legal maturity date for the class A-6B and A-6C notes is October 25, 2040.

|

Class

|

Spread

|

|

|

Class A-6B

|

plus %

|

|

|

Class A-6C

|

plus %

|

|

|

|

|

|

Class

|

Spread

|

|

|

Class A-6B

|

plus %

|

|

|

Class A-6C

|

plus %

|

|

|

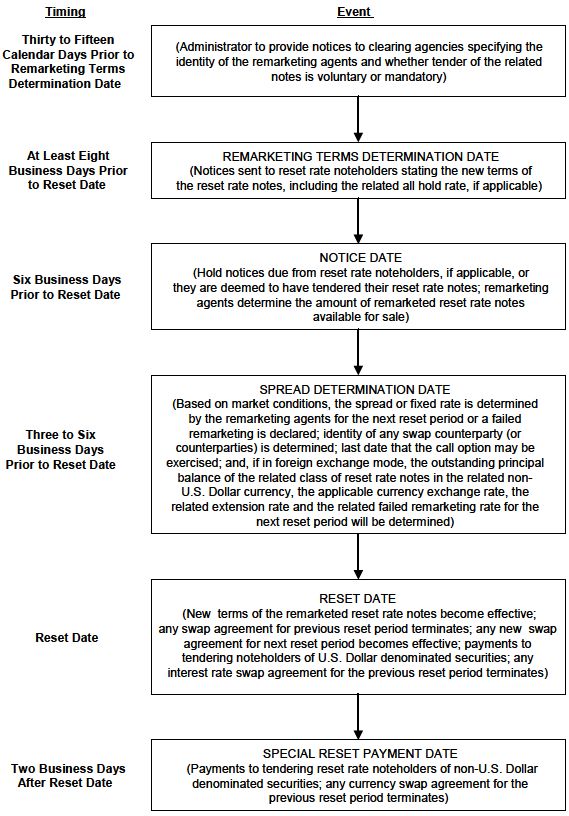

| • |

the remarketing agent, in consultation with the administrator, cannot determine the applicable required reset terms on or before the remarketing terms determination date;

|

| • |

the remarketing agent cannot establish the required spread on the spread determination date;

|

| • |

the remarketing agent is unable to remarket some or all of the tendered reset rate notes at the spread set by the remarketing agent, or one or more committed purchasers default on their purchase obligations and the remarketing agent

chooses not to purchase such reset rate notes itself;

|

| • |

any rating agency then rating the notes has not confirmed or upgraded its then-current rating of any class of notes, if such confirmation is required; or

|

| • |

certain other conditions specified in the remarketing agreement are not satisfied.

|

| • |

all holders of the applicable class will retain their reset rate notes, including in all deemed mandatory tender situations;

|

| • |

the related interest rate for the applicable class of reset rate notes will be reset to a failed remarketing rate of three-month LIBOR plus 0.75% per annum; and

|

| • |

the related reset period will be set at three months.

|

|

|

|

|

Floating Rate Class A Notes:

| • |

Class A-1 Student Loan-Backed Notes in the original principal amount of $317,000,000, none of which remain outstanding;

|

| • |

Class A-2 Student Loan-Backed Notes in the original principal amount of $482,000,000, none of which remain outstanding;

|

| • |

Class A-3 Student Loan-Backed Notes in the original principal amount of $326,000,000, none of which remain outstanding;

|

| • |

Class A-4 Student Loan-Backed Notes in the original principal amount of $507,000,000, none of which remain outstanding;

|

| • |

Class A-5 Student Loan-Backed Notes in the original principal amount of $591,000,000, and currently outstanding in the amount of $66,259,985; and

|

| • |

Class A-6A Student Loan-Backed Notes in the original principal amount of $382,946,000.00, and currently outstanding in the same amount.

|

| • |

Class B Student Loan-Backed Notes in the original principal amount of $92,968,000, and currently outstanding in the amount of $ 42,941,870.74 .

|

| • |

the floating rate class A notes and the reset rate notes collectively as the class A notes;

|

| • |

the floating rate class A notes and the class B notes as the floating rate notes; and

|

| • |

the floating rate notes and the reset rate notes as the notes.

|

|

Class

|

Spread

|

|

|

Class A‑5

|

plus 0.11%

|

|

|

Class A‑6A

|

plus 0.16%

|

|

|

Class B

|

plus 0.21%

|

|

|

| • |

first, the class A noteholders’ principal distribution amount in the following order of priority:

|

| • |

to the class A-5 notes until their principal balance is reduced to zero; and then

|

| • |

pro rata, to the class A-6A, class A-6B and class A-6C notes until their respective principal balances are reduced to zero; provided, that either (a) if the class A-6B and/or class A-6C notes are then denominated in a currency other

than U.S. Dollars and are structured to receive payments of principal on each applicable distribution date, any payments due to the related reset rate noteholders will be made to the related currency swap counterparty or (b) if the

class A-6B and/or class A-6C notes are then structured not to receive a payment of principal until the end of the related reset period, any payments due to the related reset rate noteholders will be allocated to the related accumulation

account; and

|

| • |

second, on each distribution date on and after the stepdown date, and provided that no trigger event is in effect on such distribution date, the class B noteholders’ principal distribution

amount, to the class B notes, until their principal balance is reduced to zero.

|

|

|

|

Class

|

Maturity Date

|

|

|

Class A-5

|

January 25, 2027

|

|

|

Class A-6A

|

October 25, 2040

|

|

|

Class A-6B

|

October 25, 2040

|

|

|

Class A-6C

|

October 25, 2040

|

|

|

Class B

|

October 25, 2040

|

|

|

|

|

| • |

the trust student loans;

|

| • |

collections and other payments on the trust student loans;

|

| • |

funds it currently holds or will hold from time to time in its trust accounts, including a collection account; a reserve account; one or more accumulation accounts; one or more supplemental interest accounts; an investment reserve

account; an investment premium purchase account; a remarketing fee account; and if the class A-6B or class A-6C notes are denominated in a currency other than U.S. Dollars, a currency account;

|

| • |

its rights under the transfer and servicing agreements, including the right to require VG Funding (or Navient Solutions, LLC, as servicer, acting on its behalf), Navient CFC, the depositor or the servicer to repurchase trust student

loans from it or to substitute loans under certain conditions;

|

| • |

its rights under any swap agreement or potential future interest rate cap agreement, as applicable; and

|

| • |

its rights under the guarantee agreements with guarantors.

|

|

|

|

|

| • |

on the related maturity date for each class of class A notes and upon termination of the trust, to cover shortfalls in payments of the class A noteholders’ principal and accrued interest to the related class of notes; and

|

| • |

on the class B maturity date and upon termination of the trust, to cover shortfalls in payments of the class B noteholders’ principal and accrued interest, any carryover servicing fees, any remaining swap termination payments and

remarketing fees and expenses.

|

|

|

| • |

if the applicable class of reset rate notes is then denominated in U.S. Dollars, on the next reset date, to the related reset rate noteholders, after all other required distributions have been made on that reset date; or

|

| • |

if the applicable class of reset rate notes is then denominated in a currency other than U.S. Dollars, on or about the next related reset date, to the currency swap counterparty or counterparties, which will in turn pay the applicable

currency equivalent of those amounts to the trust, for payment to the reset rate noteholders on the second business day following the related reset date, after all other required distributions have been made on that reset date.

|

|

|

|

|

|

|

| • |

the amount of specified increases in the costs incurred by the servicer;

|

| • |

the amount of specified conversion, transfer and removal fees;

|

| • |

any amounts described in the first two bullets that remain unpaid from prior distribution dates; and

|

| • |

interest on any unpaid amounts.

|

|

|

| • |

the maturity or other liquidation of the last trust student loan and the disposition of any amount received upon its liquidation; and

|

| • |

the payment of all amounts required to be paid to the noteholders.

|

| • |

pay to noteholders the interest payable on the related distribution date; and

|

| • |

reduce the outstanding principal amount of each class of notes then outstanding on the related distribution date to zero, taking into account all amounts then on deposit in the accumulation account.

|

| • |

is then structured not to receive a payment of principal until the end of the related reset period, the outstanding principal balance of the such class of reset rate notes will be deemed to have been reduced by any amounts on deposit,

exclusive of any investment earnings, in the accumulation account; and/or

|

| • |

is then denominated in a non-U.S. Dollar currency, the U.S. Dollar equivalent of the then-outstanding principal balance of such class of reset rate notes will be determined based upon the exchange rate provided for in the currency swap

agreement or agreements.

|

|

|

| • |

Special tax counsel to the trust is of the opinion that the class A-6B and class A-6C notes will be characterized as debt for United States federal income tax purposes.

|

| • |

Special tax counsel to the trust is of the opinion that the trust will not be characterized as an association or a publicly traded partnership taxable as a corporation for United States federal income tax purposes.

|

| • |

Delaware tax counsel for the trust is of the opinion that the same characterizations will apply for Delaware state income tax purposes as for federal income tax purposes and noteholders who were not otherwise subject to Delaware

taxation on income would not become subject to Delaware tax as a result of their ownership of notes.

|

|

|

| • |

an exemption from the prohibited transaction provisions of Section 406 of the Employee Retirement Income Security Act of 1974, as amended, and Section 4975 of the Internal Revenue Code of 1986, as amended, applies, so that the purchase

or holding of the class A-6B or class A-6C notes will not result in a non-exempt prohibited transaction; and

|

| • |

the purchase or holding of the class A-6B or class A-6C notes will not cause a non-exempt violation of any substantially similar federal, state, local or foreign laws.

|

| • |

class A-5 notes: “AAAsf” by Fitch, “Aaa (sf)” by Moody’s and “AAA (sf)” by S&P.

|

| • |

class A-6A notes: “AAAsf” by Fitch, “Aaa (sf)” by Moody’s and “AA+ (sf)” by S&P.

|

| • |

class A-6B notes: “AAAsf” by Fitch, “Aaa (sf)” by Moody’s and “AA+ (sf)” by S&P.

|

| • |

class A-6C notes: “AAAsf” by Fitch, “Aaa (sf)” by Moody’s and “AA+ (sf)” by S&P.

|

| • |

class B notes: “Asf” by Fitch, “A3 (sf)” by Moody’s and “AA (sf)” by S&P.

|

|

|

|

CUSIP Number

|

83149E AJ 6

|

|

International Securities Identification Number (ISIN)

|

US83149EAJ64

|

|

European Common Code

|

025895991

|

|

CUSIP Number

|

83149E AK 3

|

|

International Securities Identification Number (ISIN)

|

US83149EAK38

|

|

European Common Code

|

025896092

|

|

|

|

General Risks

|

||

|

Federal Financial Regulatory Legislation Could Have An Adverse Effect On Navient Corporation, The Sponsor, The Servicer, The Depositor, The Sellers And The Trust, Which Could Result In Losses Or Delays In

Payments On Your Notes

|

On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) to reform and strengthen supervision of the U.S. financial services

industry. The Dodd-Frank Act represents a comprehensive change to existing laws, imposing significant new regulation on almost every aspect of the U.S. financial services industry.

The Dodd-Frank Act has resulted in significant new regulation in key areas of the business of Navient Corporation, the direct parent of Navient Solutions, LLC and the indirect parent of Navient Funding, LLC,

and its affiliates and the markets in which Navient Corporation, the sponsor and their affiliates operate. Pursuant to the Dodd-Frank Act, Navient Corporation and many of its subsidiaries are subject to regulations promulgated by the

Consumer Financial Protection Bureau (the “CFPB”). The CFPB has substantial power to define the rights of consumers and the responsibilities of certain institutions, including Navient Corporation, the sponsor and their affiliates, in

connection with their education loan origination and servicing businesses. In addition, the CFPB has the authority to bring enforcement actions against student loan lenders and student loan servicers for violations of federal consumer

protection regulations and with respect to acts or practices that the CFPB determines to be unfair, deceptive or abusive.

It is likely that operational expenses of Navient Corporation, the sponsor or their affiliates will increase if new or additional compliance requirements under the Dodd-Frank Act are imposed on their

operations, and their competitiveness could be significantly affected if they are subjected to supervision and regulatory standards not otherwise applicable to their competitors.

|

|

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) was signed into law. The CARES Act provides relief to borrowers under federal direct student loans and FFELP loans owned by the U.S. Department

of Education, in the form of a 0% interest rate and a suspension of payments, until September 30, 2020. Although these borrower relief programs have not been extended to borrowers of FFELP loans held by entities other than the U.S.

Department of Education, including the trust student loans, there is no assurance that future legislation intended to mitigate the economic effects of the COVID-19 pandemic will not directly or indirectly affect the trust student loans,

or otherwise affect the servicer’s business. The majority of its implementing regulations have not yet been issued. As a result, the potential impact of the CARES Act on financial institutions and other nonbank financial companies, such

as Navient, or consumers, such as the obligors of the loans, is unknown.

|

||

|

The Bankruptcy Of The Depositor, Navient CFC Or Any Other Seller Could Delay Or Reduce Payments On Your Notes

|

We have taken steps to assure that the voluntary or involuntary application for relief by the depositor, Navient CFC, which is the sole member of the depositor, or any other applicable seller under the United

States Bankruptcy Code or other insolvency laws will not result in consolidation of the assets and liabilities of the trust with those of the depositor, Navient CFC and the other sellers. However, we cannot guarantee that the activities of

the depositor, the sellers, the sponsor or the trust will not result in a court concluding that the trust’s assets and liabilities should be consolidated with those of the depositor, Navient CFC or any other seller in a proceeding under any

insolvency law. If a court were to reach this conclusion or a filing were made under any insolvency law by or against us, or if an attempt were made to litigate this issue, then delays in distributions on the notes or reductions in these

amounts could result.

Navient CFC, the other sellers of the student loans and the depositor intend that each transfer of student loans to the trust will constitute a true sale. If such transfer constitutes a true sale, the student

loans and their proceeds would no longer be considered property of the depositor, Navient CFC or the other sellers should any such seller become subject to an insolvency law.

If the depositor, Navient CFC or any other seller were to become subject to an insolvency law, and a creditor, a trustee-in-bankruptcy or the seller itself were to take the position that the sale of student

loans from the related seller to the depositor should instead be treated as a pledge of the student loans to secure a borrowing of that seller, delays in payments on the notes could occur.

In addition, if the court ruled in favor of this position, reductions in the amount of payments on the notes could result.

|

|

The Bankruptcy Of The Servicer Could Delay The Appointment Of A Successor Servicer Or Reduce Payments on your notes

|

In the event of a default by the servicer resulting solely from certain events of insolvency or the bankruptcy of the servicer, a court, conservator, receiver or liquidator (including the FDIC) may have the

power to prevent any of the servicer, the trust, the indenture trustee or the noteholders, as applicable, from appointing a successor servicer and delays in the collection of payments on the trust student loans may occur. It may also be

difficult to find a third party to act as successor servicer, and the trust may have to increase the servicing fee in order to obtain such successor servicer. Any resulting delay in the collection of payments on the affected trust student

loans may delay or reduce payments to noteholders. In addition, in the event of an insolvency or a bankruptcy of the servicer, a court, conservator, receiver or liquidator may permit the servicer to assign its rights and obligations as

servicer to a third party without complying with the provisions of the transaction documents.

|

|

Because The Notes May Not Provide Regular Or Predictable Payments, You May Not Receive The Return On Your Investment That You Expected

|

The notes may not provide a regular or predictable schedule of payments or payment on any specific date. Accordingly, you may not receive the return on your investment that you expected.

|

|

|

The Notes Are Not Suitable Investments For All

Investors |

The reset rate notes are complex investments that should be considered only by investors who, either alone or with their financial, tax and legal advisors, have the expertise to analyze the prepayment,

reinvestment, default and market risk, and tax consequences of such an investment, as well as the interaction of these factors. You should not purchase the reset rate notes unless you understand the structural, prepayment, credit,

liquidity and market risks associated with the reset rate notes, the regulatory and enforcement risks relating to the trust student loans, the tax consequences of an investment in the reset rate notes and the interaction of the foregoing

factors. The interaction of the factors described in this free-writing prospectus and other factors that may affect the reset rate notes and their combined effects on the reset rate notes are not possible to predict with meaningful

certainty and are likely to change from time to time. As a result, an investment in the reset rate notes involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial

investment experience with similar types of securities and who have conducted an appropriate analysis of the reset rate notes. Prospective investors must be able to bear the risk of loss (including total loss) on their investment in the

reset rate notes.

|

|

Sequential Payment Of The Notes Results In A Greater Risk Of Loss

|

Holders of the class A-6B or class A-6C notes bear a greater risk of loss than do holders of the class A-5 notes because no principal will be paid to any class A-6B or class A-6C noteholders until the class

A-5 notes have been paid in full. If a failed remarketing occurs, the reset rate notes would become subject to the failed remarketing rate, which is higher than the interest rate that would otherwise be applicable to such class of notes.

This would reduce the amount of available funds to pay interest on other classes of notes and principal on the reset rate notes. In that case, or if prepayments are much higher than anticipated, or if losses on the trust student loans are

greater than expected, you may suffer a loss.

|

|

|

Illiquid Market Conditions May Occur From Time To Time

|

From time to time, the secondary market for your class A-6B or class A-6C notes may be adversely affected by periods of general market illiquidity or by events in the global financial markets in general or in

the securitization market in particular. Accordingly, you may not be able to sell your class A-6B or class A-6C notes when you want to do so or you may be unable to obtain the price that you wish to receive for your class A-6B or class

A-6C notes and, as a result, you may suffer a loss on your investment.

|

|

|

School Closures And Unlicensed Schools May Result In Losses On Your Notes

|

Some of the trust student loans are subject to the so-called “Holder-in-Due-Course” rule of the Federal Trade Commission (the “Holder Rule”) the provisions of which are similar to those contained in the

Uniform Consumer Credit Code and in state statutes and common law of many states. The effect of these laws is to subject a seller (and certain lenders and their assignees, such as the trust) in a consumer credit transaction to all claims

and defenses which the obligor in the transaction can assert against the seller of the goods or services. Under these laws, the trust as holder of the trust student loans may be subject to any claims or defenses that the student borrower

may assert against its school for failure of the school to satisfy its obligations under the enrollment agreement with the student as a result of a school closure, a school bankruptcy or otherwise. If a student is successful in asserting

such a claim, the student may have the right to recover from the trust payments previously made on the related trust student loan and have a defense against making further payments. In this event, to the extent available funds and credit

enhancement are insufficient to cover such amounts, you may suffer a loss on your investment.

|

|

In addition, generally state law requires schools engaged in providing educational services in their state to be licensed by a state regulatory authority. In most states, if a school is not licensed at the

time the student signs the enrollment agreement, the enrollment agreement may be void and, as a result, the student will have a defense against repayment of the loan. Although each seller will represent as a condition to the sale of the

trust student loans that all of the related schools were licensed under applicable law as of the origination date of such trust student loans, to the extent that a related school became unlicensed prior to the student signing the enrollment

agreement, the related borrower may have the right to recover payments previously made on the related trust student loan and may have a defense against further payment. There is also a possibility that a school has failed to maintain its

license under applicable law since the origination of the related trust student loans, and in such event, the related borrower may be entitled to the claims or defenses with respect to payments on its trust student loan described above. In

either of these instances, to the extent available funds and credit enhancement is insufficient to cover such amounts, you may suffer a loss on your investment.

|

||

|

The Issuing Entity Will Have Limited Assets From Which To Make Payments On The Notes, Which May Result In Losses

|

The issuing entity will not have, nor will it be permitted to have, significant assets or sources of funds other than the pool of trust student loans and the related guarantee agreements. The issuing entity

will also have a reserve account established in the issuing entity’s name.

Consequently, you must rely upon payments on the trust student loans from the borrowers and guarantors, as applicable, and, if available, amounts on deposit in the trust accounts described above, and

overcollateralization to repay your notes. If these sources of funds are unavailable or insufficient to make payments on your notes, you may experience a loss on your investment.

|

|

|

Your Notes May Have A Degree Of Basis Risk, Which Could Compromise The Trust’s Ability To Pay Principal And Interest On Your Notes

|

There may be a degree of basis risk associated with the class A-6C notes. Basis risk is the risk that shortfalls might occur because, among other things, while the effective interest rates of the trust

student loans adjust on the basis of specified indices and those of the notes adjust on the basis of a different LIBOR index, different indices or, with respect to the reset rate notes at a time when such notes are in fixed rate mode, do

not adjust at all. If a shortfall were to occur, the trust’s ability to pay principal of and/or interest on your notes could be compromised. See “Annex A—The Trust Student Loan Pool—Composition of the Trust Student Loans as of the

Statistical Disclosure Date” in this free-writing prospectus which specifies the percentages of trust student loans that adjust based on LIBOR or the 91-day Treasury bill rate, as applicable.

|

|

Consequently, you must rely on other forms of credit enhancement, to the extent available, to mitigate basis risk. There can be no assurance that the amount of credit enhancement will be sufficient to cover

the basis risk associated with the notes.

|

||

|

You May Be Unable To Reinvest Principal Payments At The Yield You Earn On The Notes

|

Asset-backed notes usually produce increased principal payments to investors when market interest rates fall below the interest rates on the collateral—student loans in this case—and decreased principal

payments when market interest rates rise above the interest rates on the collateral. As a result, you are likely to receive more money to reinvest at a time when other investments generally are producing lower yields than the yield on the

notes. Similarly, you are likely to receive less money to reinvest when other investments generally are producing higher yields than the yield on the notes.

|

|

|

Withdrawal Or Downgrade Of Ratings May Decrease The Prices Of Your Notes

|

A security rating is not a recommendation to buy, sell or hold securities. Similar ratings on different types of securities do not necessarily mean the same thing. A rating agency may revise or withdraw its

rating at any time if it believes circumstances have changed. A subsequent downgrade in the rating on your notes is likely to decrease the price a subsequent purchaser will be willing to pay for your notes.

|

|

|

A Conflict Of Interest May Exist Between The Rating Agencies Engaged To Rate The Notes And The Transaction Parties

|

The SEC has taken the position that being paid by the sponsor, issuer or an underwriter to issue and/or maintain a credit rating on asset backed securities may create a conflict of interest for rating

agencies, and that this potential conflict is particularly acute because arrangers of asset-backed securities transactions provide repeat business to such rating agencies. Potential investors in the class A-6B or class A-6C notes should

make their own determinations regarding whether such a conflict of interest actually exists, whether any such potential conflict of interest impacts a rating from any retained rating agency and the weight given to any particular rating in

making an investment decision in the class A-6B or class A-6C notes.

|

|

|

A Further Lowering Of The Credit Rating of the United States Of America May Adversely Affect The Market Value Of Your Notes

|

The credit rating of the United States may potentially be downgraded by one or more nationally recognized statistical rating organizations (an “NRSRO”) within the meaning of Section 3(a)(62) of the Securities

Exchange Act of 1934, as amended (the “Exchange Act”). The impact of any such potential downgrades is unknown, and depending on any lowered rating assigned, the stated reasons for a lower rating and other factors, the liquidity, market

value and regulatory characteristics of your notes could be materially and adversely affected.

|

|

Certain Actions Can Be Taken Without Noteholder Approval

|

The transaction documents provide that certain actions may be taken based upon receipt by the indenture trustee of a confirmation from each of the rating agencies that the then-current ratings assigned by the

rating agencies then rating the notes will not be downgraded or withdrawn by those actions. In this event, such actions may be taken without the consent of noteholders.

|

|

|

LIBOR Manipulation Claims And Recent Announcements By The United Kingdom Financial Conduct Authority Regarding Changes To, Or Elimination Of, LIBOR May Affect the Interest Rate on Your Notes

|

The interest rate on the notes is based on a spread over three-month LIBOR, as set forth on the cover of this free writing prospectus and the special allowance payments on certain of the trust student loans

are based on one-month LIBOR. The London Interbank Offered Rate, or LIBOR, serves as a global benchmark for home mortgages, student loans and what various issuers pay to borrow money determining interest rates on commercial and consumer

loans, bonds, derivatives and numerous other financial instruments.

In addition, on July 27, 2017, the Chief Executive Officer of the United Kingdom Financial Conduct Authority (the “FCA”) announced that by the end of 2021 (the “London Interbank Offered Rate Phase-Out

Date”), LIBOR would no longer be sustained through the FCA’s efforts to compel banks’ participation in setting the benchmark. The FCA’s intention is that after 2021, it will no longer be necessary for the FCA to ask, or to require,

banks to submit contributions to LIBOR. The FCA does not intend to sustain LIBOR through using its influence or legal powers beyond that date. It is possible that the ICE Benchmark Administration Limited (the “IBA”), which took over

administration of LIBOR on February 1, 2014, may be willing and able to produce LIBOR rates after 2021, but we cannot assure you that LIBOR will survive in its current form, or at all. Following the London Interbank Offered Rate

Phase-Out Date or in the event of any other disruption in the London interbank market, we refer you to “Description of the Notes—Determination of Indices—LIBOR” for the process for determining

LIBOR under the indenture.

As a result of the foregoing, the rate at which your notes bear interest could be adversely affected by changes to the rate-setting process for LIBOR, or the phasing out of the rate entirely. There may be a negative effect to you if

the LIBOR global benchmark is no longer available.

|

|

The Notes Are Not A Suitable Investment for EU Institutional Investors Subject To The EU Risk Retention And Due Diligence Requirements

|

All prospective investors in the notes whose investment activities are subject to legal investment laws and regulations, regulatory capital requirements, or review by regulatory authorities should consult

with their own legal, accounting and other advisors in determining whether, and to what extent, the notes will constitute legal investments for them or are subject to investment or other restrictions, unfavorable accounting treatment,

capital charges, reserve requirements or other consequences.

Investors should be aware and in some cases are required to be aware of the risk retention and due diligence requirements (the “EU Risk Retention and Due Diligence Requirements”) which under Article 5 of

Regulation (EU) 2017/2402 (the “Securitization Regulation”) apply to certain types of EU-regulated investors including institutions for occupational retirement, credit institutions, alternative investment fund managers who manage or market

alternative investment funds in the EU, investment firms, insurance and reinsurance undertakings and management companies of UCITS funds (or internally managed UCITS) (“EU Institutional Investors”). Amongst other things, the EU Risk

Retention and Due Diligence Requirements restrict an EU Institutional Investor from investing in a securitization unless the EU Institutional Investor has verified that:

(a) the originator or original lender of the securitization grants all the credits giving rise to the underlying exposures on the basis of sound and well-defined criteria and clearly established processes

for approving, amending, renewing and financing those credits and has effective systems in place to apply those criteria and processes to ensure that credit-granting is based on a thorough assessment of the obligor’s creditworthiness;

(b) the originator, sponsor or original lender of the securitization (i) retains on an ongoing basis a material net economic interest which, in any event, shall not be less than 5%, determined in

accordance with Article 6 of the Securitization Regulation, and (ii) discloses the risk retention to EU Institutional Investors (the “EU Retention Requirement”); and

(c) the originator, sponsor or securitization special purpose entity (“SSPE”) has, where applicable, made available the information required by Article 7 of the Securitization Regulation in accordance with

the frequency and modalities provided for in Article 7 of the Securitization Regulation.

|

|

|

Failure on the part of an EU Institutional Investor to comply with the EU Risk Retention and Due Diligence Requirements may result in various penalties including, in the case of those investors subject to

regulatory capital requirements, the imposition of a punitive capital charge in respect of the investment in the securitization acquired by the relevant investor. Aspects of the requirements and what is or will be required to demonstrate

compliance to national regulators remain unclear.

None of the sponsor, the sellers, the depositor and the remarketing agents or any other person intends to retain a material net economic interest in the securitization constituted by the issuance of the notes in a manner that would

satisfy the EU Retention Requirement or to take any other action which may be required by EU Institutional Investors for the purposes of their compliance with the EU Risk Retention and Due Diligence Requirements, and no such person

assumes (i) any obligation to so retain or take any such other action or (ii) any liability whatsoever in connection with any Holder’s non-compliance with the EU Risk Retention and Due Diligence Requirements. Consequently, the notes are

not a suitable investment for EU Institutional Investors. As a result, the price and liquidity of the notes in the secondary market may be adversely affected.

|

||

|

The Notes May Be Repaid Early Due To An Auction Sale Or The Exercise Of The Optional Purchase Right. If This Happens, Your Yield May Be Affected And You Will

Bear Reinvestment Risk

|

The notes may be repaid before you expect them to be if:

• the servicer exercises its option to purchase all of the trust student loans; or

• the indenture trustee successfully conducts an auction sale.

Either event would result in the early retirement of the notes outstanding on that date. If this happens, your yield on the notes may be affected. You will bear the risk that you cannot reinvest the money

you receive in comparable notes at an equal yield.

|

|

|

Negative LIBOR Rates Would Reduce The Rate Of Interest On The Notes

|

The interest rate to be borne by each class of notes is based on a spread over LIBOR. The London Interbank Offered Rate, or LIBOR, serves as a global benchmark for home mortgages, student loans and what

various issuers pay to borrow money.

Changes in LIBOR will affect the rate at which the notes accrue interest and the amount of interest payments on the notes. To the extent that LIBOR decreases below 0.00% for any interest accrual period, LIBOR

for such interest accrual period will be deemed to be 0.00% and the rate at which each class of notes accrue interest for such interest accrual period will be deemed to be 0.00% plus the applicable spread for each such class of notes for

the related interest accrual period.

|

|

Your Notes Are Subject To A Call Option

|

Navient Corporation, or one of its wholly-owned subsidiaries, has the option to call, in full, the class A-6B or class A-6C notes in respect of each reset date, even if you have delivered a hold notice. If

this option is exercised, you will receive a payment of principal equal to the outstanding principal balance of your class A-6B or class A-6C notes, as applicable, less all amounts distributed to you as a payment of principal, plus all

accrued and unpaid interest on such distribution date. However, you may not be able to reinvest the proceeds you receive in a comparable security with an equivalent yield. For additional information concerning the call option and reset

periods, see “Description of the Notes—The Reset Rate Notes” in this free-writing prospectus.

|

|

|

You May Be Required To Continue To Hold Your Notes If A Failed Remarketing Occurs With Respect To A Reset Date

|

In connection with any remarketing of the class A-6B or class A-6C notes (including on the current reset date), if a failed remarketing is declared, your class A-6B or class A-6C notes will not be sold, even

if you attempted to tender them for remarketing or if the notes were mandatorily tendered with respect to such reset date. In this event you will be required to rely on a sale through the secondary market, which may not then exist for your

class A-6B or class A-6C notes, independent of the remarketing process.

If a failed remarketing is declared with respect to the July 27, 2020 reset date, the class A-6B and class A-6C notes will bear interest until the next reset date at the failed remarketing rate, which is

currently equal to an annual rate of three-month LIBOR plus 0.75%. We cannot assure you that the failed remarketing rate will be as high as the prevailing market rate of interest for similar securities and you may suffer a loss in

yield. For additional information concerning a failed remarketing, see “Description of the Notes—The Reset Rate Notes” in this free-writing prospectus.

|

|

|

You May Experience Notification Delays In Connection With A Remarketing Of Your Notes

|

Holders of beneficial interests in the class A-6B and class A-6C notes may not receive timely notifications of the reset terms for any reset date due to procedures used by the clearing agencies and financial

intermediaries. If you do not receive a copy of the notice delivered on the related remarketing terms determination date, you will nevertheless be deemed to have tendered your class A-6B or class A-6C notes unless the remarketing agent has

received a hold notice from you on or prior to the related notice date.

|

|

You Will Bear Prepayment And Extension Risk Due To Actions Taken By Individual Borrowers And Other Variables Beyond Our Control

|

A borrower may prepay a student loan in whole or in part at any time. The rate of prepayments on the trust student loans may be influenced by a variety of economic, social, competitive and other factors,

including changes in interest rates, the availability of alternative financings (including, without limitation, refinancings offered through the Department of Education’s Direct Loan program), regulatory changes affecting the student loan

market and the general economy. Various loan consolidation or refinance programs, including those offered by affiliates of the depositor, available to eligible borrowers may increase the likelihood of prepayments. Further, future

initiatives by Congress or future laws, executive orders or other policy statements to encourage or force consolidation, create debt forgiveness programs or establish other policies and programs including but not limited to those proposed

by several presidential campaigns could also affect prepayments on the trust student loans. In addition, the issuing entity may receive unscheduled payments due to borrower defaults and purchases by the servicer or the depositor. Because

a pool may include thousands of trust student loans, it is impossible to predict if or when or in what form any of these future actions may occur or to predict the amount and timing of payments that will be received and paid to noteholders

in any period. Consequently, the length of time that your notes are outstanding and accruing interest may be shorter than you expect.

On the other hand, borrowers of trust student loans might not choose to prepay their trust student loans or the trust student loans may be extended as a result of grace periods, deferment periods,

forbearance periods, income-driven repayment plans or repayment term or monthly payment amount modifications agreed to by the servicer in compliance with laws and regulations. This may slow the expected timing of principal payments or

lengthen the remaining term of the trust student loans and delay principal payments to you. In addition, the amount available for distribution to you will be reduced if borrowers fail to pay timely the principal and interest due on the

trust student loans. Consequently, the length of time that your notes are outstanding and accruing interest may be longer than you expect.

The optional purchase right of the servicer and the provision for the auction of the trust student loans, create additional uncertainty regarding the timing of payments to noteholders.

The effect of these factors is impossible to predict. To the extent they create reinvestment risk, you will bear that risk.

|

|

A Failure To Comply With Student Loan Origination And Servicing Procedures Could Jeopardize Guarantor, Interest Subsidy And Special Allowance Payments On The Trust Student Loans That Are FFELP Loans Or

Otherwise Have An Adverse Impact On The Trust Student Loans, Which May Result In Delays In Payment Or Losses On Your Notes

|

The rules under which the trust student loans were originated, including the Higher Education Act or the program rules require lenders making and servicing student loans and the guarantors guaranteeing those

loans to follow specified procedures, including due diligence procedures, to ensure that the student loans are properly made, disbursed and serviced.

Failure to follow these procedures may result in the Department of Education’s refusal to make reinsurance payments to the applicable guarantor or to make interest subsidy payments and special allowance

payments on the trust student loans that are FFELP Loans.

Loss of any loan program payments could adversely affect the amount of available funds and the issuing entity’s ability to pay principal and interest on your notes.

In addition, to the extent related to servicing practices of Navient Solutions, LLC with respect to FFELP loans or HEAL Program, an adverse ruling in litigation against Navient Solutions, LLC may have a

material adverse effect on the trust student loans, and the payments on your notes may be adversely affected. See “Navient Corporation” in this free-writing prospectus.

|

|

|

The Inability Of The Depositor Or The Servicer To Meet Its Repurchase Obligation May Result In Losses On Your Notes

|

Under some circumstances, the issuing entity has the right to require the depositor (and the depositor has the right to require the sellers) or the servicer to purchase a trust student loan or provide the

issuing entity with a substitute student loan. This right arises generally if a breach of the representations, warranties or covenants of the depositor or the servicer, as applicable, has a material adverse effect on the issuing entity,

and is not cured within the applicable cure period. We cannot guarantee to you, however, that the depositor (and, in turn, the sellers) or the servicer will have the financial resources to make a purchase or substitution.

For example, the depositor, the sellers, and the servicer are subsidiaries of Navient Corporation and, as a result, an adverse ruling in litigation against Navient Corporation could also give rise to an

obligation of the depositor, the servicer, or a seller to purchase, repurchase, or substitute trust student loans as set forth in the related transaction documents and may have an adverse impact on the financial ability of the depositor,

the servicer, or a seller to fulfill their respective obligations to purchase, repurchase or substitute trust student loans. See “Navient Corporation” in this free-writing prospectus.

If the depositor, the sellers, or the servicer do not have the financial resources to make a required purchase or substitution, you will bear any resulting loss.

|

|

Incentive Programs May Affect Your Notes

|

At the present time, the borrowers with respect to certain of the initial trust student loans may be eligible for various incentive programs. In addition, under the terms of the servicing agreement, the

servicer may make new incentive programs available to borrowers with trust student loans. See “The Companies’ Student Loan Financing Business—Servicing—Incentive Programs” in this free-writing

prospectus. These current or future incentive programs may affect payments on your notes.

For example, if one or more of the incentive programs which offer a principal balance reduction to borrowers are made available to borrowers with trust student loans and a higher than anticipated number of

borrowers qualify, the principal balance of the affected trust student loans may repay faster than anticipated.

Accordingly, your notes may experience faster than anticipated principal payments.

Conversely, the existence of these incentive programs may discourage a borrower from prepaying an affected trust student loan. If this were to occur, the principal balance of your notes may be reduced over a

longer period than would be the case if there were no such incentive program.

Furthermore, incentive programs may reduce the amount of funds available to make payments on your notes by reducing the principal balances and yield on the trust student loans. In that case, you will bear

the risk of any loss not covered by available credit enhancement.

|

|

|

A Servicer Default May Result In Additional Costs, Increased Servicing Fees By A Substitute Servicer Or A Diminution In Servicing Performance, Any Of Which May Have An Adverse Effect On Your Notes

|

If a servicer default occurs, the indenture trustee or the noteholders may remove the servicer without the consent of the eligible lender trustee. Only the indenture trustee or such noteholders, and not the

eligible lender trustee, has the ability to remove the servicer if a servicer default occurs. In the event of the removal of the servicer and the appointment of a successor servicer, we cannot predict:

• the ability of the successor servicer to perform the obligations and duties of the servicer under the servicing agreement; or

• the servicing fees charged by the successor servicer.

In addition, the noteholders have the ability, with some exceptions, to waive defaults by the servicer.

Furthermore, the indenture trustee or the noteholders may experience difficulties in appointing a successor servicer and during any transition phase it is possible that normal servicing activities could be

disrupted, resulting in increased delinquencies and/or defaults on the trust student loans.

|

|

The Indenture Trustee May Have Difficulty Liquidating Trust Student Loans After An Event Of Default

|

If an event of default occurs under the indenture, the indenture trustee may sell the trust student loans, without the consent of the noteholders (but only in the event that there has been a payment default

on the class A notes, and in all other cases, if the purchase price received from the sale of the trust student loans is sufficient to repay all noteholders in full). However, the indenture trustee may not be able to find a purchaser for

the trust student loans in a timely manner or the market value of those loans may not be high enough to make noteholders whole.

|

|

|

You May Incur Losses Or Delays In Payments On Your Notes If Borrowers Default On The Trust Student Loans

|

If a borrower defaults on a trust student loan that is only 98% or 97% guaranteed, the related issuing entity will experience a loss of approximately 2% or 3%, as the case may be, of the outstanding principal

and accrued interest on that student loan. If defaults occur on the trust student loans and the credit enhancement described in this free-writing prospectus is insufficient, you may suffer a delay in payment or losses on your notes.

|

|

If A Guarantor Of The Trust Student Loans Experiences Financial Deterioration Or Failure, You May Suffer Delays In Payment Or Losses On Your Notes

|

All of the trust student loans will be unsecured. As a result, the only security for payment of a FFELP guaranteed student loan is the guarantee provided by the applicable guarantor. FFELP loans acquired by

the issuing entity may be subject to guarantee agreements with a number of individual guarantors. A deterioration of a guarantor’s financial condition and ability to honor guarantee claims could result in a failure of that guarantor to

make guarantee payments to the eligible lender trustee in a timely manner, or at all. The financial condition of a guarantor could be adversely affected by a number of factors, including the amount of claims made against that guarantor as

a result of borrower defaults.

A guarantor’s financial condition and ability to honor guarantee claims with respect to FFELP loans could also be adversely affected by a number of other factors including:

• the continued voluntary waiver by the guarantor of the guarantee fee payable by a borrower upon disbursement of a student loan;

• the amount of claims made against that guarantor as a result of borrower defaults;

• the amount of claims reimbursed to that guarantor from the Department of Education, which range from 75% to 100% of the guaranteed portion of the loan, depending on the date the loan was made and the

historical performance of the guarantor; and

• changes in legislation that may reduce expenditures from the Department of Education that support federal guarantors or that may require guarantors to pay more of their reserves to the Department of

Education.

If the financial condition of a guarantor deteriorates, it may fail to make guarantee payments in a timely manner, or at all. In that event, you may suffer delays in payment or losses on your notes.

|

|

|

The Department Of Education’s Failure To Make Reinsurance Payments May Negatively Affect The Timely Payment Of Principal And Interest On Your Notes

|

If a guarantor is unable to meet its guarantee obligations, the issuing entity may submit claims directly to the Department of Education for payment. The Department of Education’s obligation to pay guarantee

claims directly is dependent upon its determination that the guarantor is unable to meet its guarantee obligations. If the Department of Education delays in making this determination, you may suffer a delay in the payment of principal and

interest on your notes. In addition, if the Department of Education determines that the guarantor is able to meet its guarantee obligations, the Department of Education will not make guarantee payments to the issuing entity. The Department

of Education may or may not make the necessary determination that the guarantor is unable to meet its guarantee obligations. If the Department of Education determines that the guarantor is unable to meet its guarantee obligations, it may

or may not make this determination or the ultimate payment of the guarantee claims in a timely manner. This could result in delays or losses on your investment.

|

|

Payment Offsets By Guarantors Or The Department Of Education Could Prevent The Issuing Entity From Paying You The Full Amount Of The Principal And Interest Due On Your Notes

|

The eligible lender trustee may use the same Department of Education lender identification number for FFELP loans of the issuing entity as it uses for other FFELP loans it holds on behalf of other issuing

entities established by the sponsor. If it does, the billings submitted by the eligible lender trustee or the servicer to the Department of Education (for items such as special allowance payments or interest subsidy payments) and the

claims submitted to the guarantors will be consolidated with the billings and claims for payments for trust student loans under other issuing entities using the same lender identification number. Payments on those billings by the Department

of Education as well as claim payments by the applicable guarantors will be made to the eligible lender trustee, or to the servicer on behalf of the eligible lender trustee, in a lump sum. Those payments must be allocated by the

administrator among the various issuing entities that reference the same lender identification number.

If the Department of Education or a guarantor determines that the eligible lender trustee owes it a liability on any trust student loan, including loans it holds on behalf of the issuing entity for your notes

or other issuing entities, the Department of Education or the applicable guarantor may seek to collect that liability by offsetting it against payments due to the eligible lender trustee of the issuing entity. Any offsetting or shortfall

of payments due to the eligible lender trustee could adversely affect the amount of available funds for any collection period and thus the issuing entity’s ability to pay you principal and interest on your notes.

The servicing agreement for your notes contains provisions for cross-indemnification concerning those payments and offsets. Such provisions require one entity to compensate the other or accept a lesser

payment to the extent the latter has been assessed for the liability of the former. Even with cross-indemnification provisions, however, the amount of funds available to the issuing entity from indemnification would not necessarily be

adequate to compensate the issuing entity and investors in the notes for any previous reduction in the available funds.

|

|

The Enactment Of The Health Care And Education Reconciliation Act Of 2010 And Any Other Future Changes In Law May Adversely Affect Student Loans, The Guarantors, The Depositor or Navient CFC And, Accordingly,

Adversely Affect Your Notes

|

On March 30, 2010, the Health Care and Education Reconciliation Act of 2010 (the “Reconciliation Act”) was enacted into law. Effective July 1, 2010, the Reconciliation Act eliminated the FFELP. The terms of

existing FFELP loans are not materially affected by the Reconciliation Act. The Higher Education Act or other relevant federal or state laws, rules and regulations may be further amended or modified in the future in a manner, including as

part of any reauthorization of the Higher Education Act, that could adversely affect the federal student loan programs as well as the student loans made under these programs and the financial condition of the guarantors. Among other

things, the level of guarantee payments may be adjusted from time to time. The elimination of FFELP and any other future changes could affect the ability of Navient CFC, the depositor or the servicer to satisfy their obligations to purchase

or substitute student loans. Future changes could also have a material adverse effect on the revenues received by the guarantors that are available to pay claims on defaulted student loans in a timely manner. We cannot predict whether any

changes will be adopted or, if adopted, what impact those changes would have on any issuing entity or the notes.

|

|

|

The Use Of Master Promissory Notes May Compromise The Indenture Trustee’s Security Interest In The Student Loans

|

For loans disbursed on or after July 1, 1999, a master promissory note evidences any student loan made to a borrower under the Federal Family Education Loan Program. When a master promissory note is used, a

borrower executes only one promissory note with each lender. Subsequent student loans from that lender are evidenced by a confirmation sent to the student. Therefore, if a lender originates multiple student loans to the same student, all of

the related student loans are evidenced by a single promissory note.

Under the Higher Education Act, each student loan made under a master promissory note may be sold independently of any other student loan made under that same master promissory note. Each student loan is

separately enforceable on the basis of an original or copy of the master promissory note.

It is possible that student loans transferred to the issuing entity may be originated under a master promissory note. If the servicer were to deliver a copy of the master promissory note, in exchange for

value, to a third-party that did not have knowledge of the indenture trustee’s lien, that third-party may also claim an interest in the student loan. It is possible that the third-party’s interest could be prior to or on parity with the

interest of the indenture trustee.

|

|

The Trust May Be Affected

By Delayed Payments From

Borrowers Called To Active Military Service

|

The Servicemembers Civil Relief Act and similar state and local laws provide payment relief to borrowers who enter active military service and to borrowers in reserve status who are called to active duty

after the origination of their trust student loans. Military operations by the United States may increase the number of citizens who are in active military service, including persons in reserve status who have been called or may be called

to active duty.

|

|

|

A Deterioration of General Economic Conditions May Reduce Payments on Your Notes

|

A deterioration in economic conditions in the United States or globally, such as an increase in unemployment levels, contraction of the availability of consumer credit or an increase in interest rates, may be

caused by a variety of factors, including but not limited to, political gridlock on United States federal budget matters (including full or partial government shutdowns), public health emergencies including the ongoing global outbreak of

the 2019 novel coronavirus disease (also known as “COVID-19”), trade disputes, terrorist events, wars, and other military or civil conflicts, price volatility in commodities, natural disasters and other disruptive political, social or

economic events. Any such disruption in economic activities may be severe or unpredictable, and could adversely affect the ability and willingness of borrowers to meet their payment obligations under the trust student loans and of the

servicer to operate its business and manage and service the trust student loans, resulting in higher rates of delinquencies experienced by the trust with respect to the trust student loans. A decrease in the amount of interest or principal

received on the trust student loans could negatively affect the ability of the trust to generate sufficient cash flow to pay its obligations or the ability of the servicer to service the interest and principal payments due on the notes,

which, in turn, may cause losses on the notes. See also “Risk Factors— Forbearances Granted As a Result of the COVID-19 Pandemic May Delay Payments of Interest and Principal” in this remarketing memorandum.

The COVID-19 pandemic may adversely affect the ability of the servicer to operate its business and manage and service the trust student loans. Restrictions on movement and business activities put in place by

state and local governments may hinder the ability of the servicer and its employees to perform collection activities on the trust student loans. In addition, several states have issued guidance regarding collection practices that could

limit Navient’s collection activities for limited periods of time. As a result, the ability of the servicer to service the interest and principal payments due on the notes may be diminished, which may lead to decreased collections on the

trust student loans and may cause losses on the notes.

An improvement in economic conditions could result in prepayments by the borrowers of their payment obligations under the trust student loans. As a result, you may receive principal payments of your notes

earlier than anticipated.

|

|

Forbearances Granted As a Result of the COVID-19 Pandemic May Delay Payments of Interest and Principal

|

The Higher Education Act also permits, and in some cases requires, “forbearance” periods from loan collection in some circumstances. Interest that accrues during a forbearance period is never subsidized.

Forbearance is most often granted to borrowers for periods of economic hardship affecting the borrower, which may occur for a variety of reasons. During periods of deteriorating economic conditions in the United States or globally, such as

during disruptive political, social or economic events, forbearance requests typically increase. Forbearance is also often granted to borrowers when a federal disaster or emergency has been declared such as in response to COVID-19.

For details of forbearance policies under the FFELP, see “Appendix A—Federal Family Education Loan Program— Stafford Loans — Grace Periods, Deferral Periods and Forbearance

Periods” in this remarketing memorandum. An increase in forbearances on the trust student loans may result in a delay in payments of interest or principal on the trust student loans, which could negatively affect the ability of

the trust to generate sufficient cash flow to pay its obligations and which, in turn, may cause losses on the notes.

Forbearance requests have increased and are expected to continue increasing during the ongoing global COVID-19 pandemic. As a result of the national emergency declaration made by President Trump on March 13,

2020 in response to the continuing outbreak of COVID-19, Navient has implemented the Coronavirus Disaster Forbearance Program for its FFELP Loans. Through June 30, 2020, Navient offered up to three months of disaster forbearance to

qualified loan borrowers who request it (the “Coronavirus National Emergency Forbearance Program”). The Coronavirus National Emergency Forbearance Program brings a borrower’s eligible loans current and postpones payments for up to three

months. As of July 1, 2020, Navient began offering a short-term coronavirus forbearance to qualified loan borrowers who request it (the “Short-Term Coronavirus Forbearance Program”). The Short-Term Coronavirus Forbearance Program brings a

borrower’s eligible loans current and postpones payments for at least one full month. The Coronavirus National Emergency Forbearance Program and the Short-Term Coronavirus Forbearance Program are collectively referred to as the

“Coronavirus Disaster Forbearance Program.” During the forbearance period for the Coronavirus Disaster Forbearance Program, interest will accrue but will not be capitalized. Pursuant to the Coronavirus Forbearance granted under the

Coronavirus Disaster Forbearance Program will not count toward the total of 12 months of forbearance permitted over the life of the loan. Navient continues to monitor the changing developments with the COVID-19 pandemic, and as such, will

review and periodically revise the Coronavirus Disaster Forbearance Program to better respond to borrowers’ current needs, including without limitation to modify the forbearance period granted to borrowers.

|

|

As a result of the COVID-19 pandemic, there has been a significant increase in forbearance requests among student loans serviced by Navient. Unlike the relief options offered for natural disasters, the

COVID-19 outbreak is affecting obligors nationwide and is expected to have a materially more significant impact on portfolio performance (including the performance of the trust student loans) than even the most severe historic natural

disasters. The increase in forbearances on the trust student loans as a result of the global COVID-19 pandemic may result in a delay in payments of interest or principal received on the trust student loans, which could negatively affect the

ability of the trust to generate sufficient cash flow to pay its obligations which, in turn, may cause losses on the notes. See “Risk Factors—Current General Economic Conditions, or a Further Deterioration

of Economic Conditions May Reduce Payments on Your Notes” in this remarketing memorandum.

|

||

|

Certain Credit And Liquidity Enhancement Features Are Limited And If They Are Partially Or Fully Depleted, There May Be Shortfalls In Distributions To Noteholders

|

Certain credit and liquidity enhancement features, including the reserve account, are limited in amount. In certain circumstances, if there is a shortfall in available funds, such amounts may be partially or

fully depleted. This depletion could result in shortfalls and delays in distributions to noteholders.

|

|

|

The Notes May Be Assigned Lower Ratings Than Those Described In This Free-Writing Prospectus By Different Rating Agencies

|

The sponsor, or an affiliate, paid a fee to two or more NRSROs (the “Rating Agencies”) to assign the initial credit ratings to the notes on or before the closing date. The SEC has said that being paid by the

sponsor, issuer or remarketing agent to issue or maintain a credit rating on asset-backed securities creates a conflict of interest for NRSROs, and that this conflict is particularly acute because arrangers of asset-backed securities

transactions provide repeat business to such NRSROs.

The sponsor has not requested a rating of the notes by any NRSRO other than the Rating Agencies. However, in preparing for the offering, the sponsor may have had discussions with, and received preliminary feedback from, NSROs other

than the Rating Agencies. Other NRSROs may assign their own ratings to any class or classes of notes at any time, even prior to the closing date. NRSROs have different methodologies, criteria, models and requirements, which may result in

ratings that are lower than those assigned by the Rating Agencies. Depending upon the level of the ratings assigned, what NRSROs are involved, what their stated reasons are for assigning a lower rating, and other factors, if a NRSRO

issues a lower rating, the liquidity, market value and regulatory characteristics of the particular class or classes of notes could be materially and adversely affected. In addition, the mere possibility that such a rating could be

issued may affect price levels in any secondary market that may develop.

|

|

The Replacement of LIBOR May Result in Adverse Tax Consequences to Noteholders

|

If an alternative method or index is designated in place of LIBOR for notes that have an interest rate that currently adjusts based on LIBOR, the U.S. federal income tax consequences of such a replacement are

uncertain. If such a replacement constitutes a “significant modification” of the notes under Treasury Regulation section 1.1001-3, the replacement may result in a deemed taxable exchange of the notes and the realization of gain or loss, as

well as other corollary tax consequences.

The Internal Revenue Service and the Treasury Department have recently proposed regulations, upon which taxpayers may rely until the promulgation of final regulations, that, in certain circumstances, could reduce the likelihood that

replacing a rate based on LIBOR with an alternative method or index would constitute a “significant modification” as described above. However, we can provide no assurance that these regulations, in their current form, will provide any

relief from the tax consequences described above if such a replacement is effected with respect to the notes. Holders of the notes should consult their own tax advisors with respect to the consequences of the designation of an

alternative method or index in place of LIBOR.

|

|

|

Current General Economic Conditions, Or A Further Deterioration of Economic Conditions May Reduce Payments on Your Notes

|

Current general economic conditions, or a further deterioration in economic conditions in the United States or globally, such as a further increase in unemployment levels, contraction of the availability of

consumer credit or an increase in interest rates, may be caused by a variety of factors, including but not limited to, political gridlock on United States federal budget matters (including full or partial government shutdowns), public

health emergencies such as the ongoing global outbreak of the 2019 novel coronavirus disease (also known as “COVID-19”), trade disputes, terrorist events, wars, and other military or civil conflicts, price volatility in commodities, natural

disasters and other disruptive political, social or economic events. Any such disruption in economic activities may be severe or unpredictable, and could adversely affect the ability and willingness of borrowers to meet their payment

obligations under the trust student loans or of the servicer to operate its business and manage and service the trust student loans, possibly resulting in higher rates of delinquencies and greater losses experienced by the trust with

respect to the trust student loans. An increase in defaults on the trust student loans, or a decrease or delay in the amount of interest or principal received on the trust student loans, either alone or in combination, could negatively

affect the ability of the trust to generate sufficient cash flow to pay its obligations or the ability of the servicer to service the interest and principal payments due on the notes, which, in turn, may cause losses on the notes.

|

|

|

The ongoing global outbreak of COVID-19 has led to significant disruptions in economic activities and financial markets in the United States and around the world. The COVID-19 outbreak has been declared to be