Attached files

| file | filename |

|---|---|

| EX-10.3 - EX-10.3 - NI Holdings, Inc. | ex10-2.htm |

| EX-10.1 - EX-10.1 - NI Holdings, Inc. | ex10-1.htm |

| 8-K - 8-K - NI Holdings, Inc. | form8k-24292_nih.htm |

NI Holdings, Inc. Annual Meeting of Shareholders | May 27, 2020

SAFE HARBOR STATEMENT This presentation contains “forward - looking” statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are based on our management’s beliefs and assumptions and on information currently available to management. These forward - looking statements include, without limitation, statements regarding our industry, business strategy, plans, goals, and expectations concerning our market position, product expansion, future operations, margins, profitability, future efficiencies, and other financial and operating information. When used in this discussion, the words “may,” believes,” “intends,” “seeks,” “anticipates,” “plans,” “estimates,” “expects,” “should,” “assumes,” “continues,” “potential,” “could,” “will,” “future,” and the negative of these or similar terms and phrases are intended to identify forward - looking statements. Forward - looking statements involve known and unknown risks, uncertainties, inherent risks, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward - looking statements. Forward - looking statements represent our management’s beliefs and assumptions only as of the date of this presentation. Our actual future results may be materially different from what we expect due to factors largely outside our control, including the occurrence of severe weather conditions and other catastrophes, the cyclical nature of the insurance industry, future actions by regulators, our ability to obtain reinsurance coverage at reasonable rates and the effects of competition. These and other risks and uncertainties associated with our business are described under the heading “Risk Factors” in our most recently filed Annual Report on Form 10 - K, which should be read in conjunction with this presentation. The company and subsidiaries operate in a dynamic business environment, and therefore the risks identified are not meant to be exhaustive. Risk factors change and new risks emerge frequently. Except as required by law, we assume no obligation to update these forward - looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in the forward - looking statements, even if new information becomes available in the future. 2

Non - GAAP Financial Measures NI Holdings evaluates its insurance operations in the way it believes will be most meaningful and representative of its busin ess results. Some of these measurements are “non - GAAP financial measures” under Securities and Exchange Commission rules and regulations. GAAP is the acronym for “acco unting principles generally accepted in the United States of America”. The non - GAAP financial measures that NI Holdings presents may not be compatible to s imilarly - named measures reported by other companies. The non - GAAP financial measures described in this presentation are used widely in the property and casualty insurance industry, and are the loss and LAE ratio, expense ratio, combined ratio, written premiums, and ratio of net written premiums to statutory s urp lus. Loss and LAE ratio The loss and LAE ratio is the ratio (expressed as a percentage) of losses and LAE incurred to premiums earned. NI Holdings m eas ures the loss and LAE ratio on an accident year and calendar year loss basis to measure underwriting profitability. An accident year loss ratio measures losse s a nd LAE for insured events occurring in a particular year, regardless of when they are reported, as a percentage of premiums earned during that year. A calendar year los s ratio measures losses and LAE for insured events occurring during a particular year and the change in loss reserves from prior policy years as a percentage of pre miums earned during that year. Expense ratio The expense ratio is the ratio (expressed as a percentage) of amortization of deferred policy acquisition costs and other und erw riting and general expenses (attributable to insurance operations) to premiums earned, and measures our operational efficiency in producing, underwriting , a nd administering the Company’s insurance business. Combined ratio The Company’s combined ratio is the ratio (expressed as a percentage) of the sum of losses and LAE incurred and expenses to p rem iums earned, and measures its overall underwriting profit. Generally, if the combined ratio is below 100%, NI Holdings is making an underwriting profit. If the combined ratio is above 100%, it is not profitable without investment income and may not be profitable if investment income is insufficient. Written premiums Written premiums represent a measure of business volume most relevant on an annual basis for the Company’s business model. T his measure includes the amount of premium purchased by policyholders as of the policy’s effective date, whereas premiums earned as presented in the statemen t o f operations matches the amount of premium to the period of risk for those insurance policies. The Company’s insurance policies are sold with a variety of e ffe ctive periods, including annual, semi - annual, and monthly. Net written premiums to statutory surplus ratio The net written premiums to statutory surplus ratio represents the ratio of net premiums written to statutory surplus. This rat io is designed to measure the ability of the Company to absorb above - average losses and the Company’s financial strength. In general, a low premium to surplus ratio is considered a sign of financial strength because the Company is theoretically using its capacity to write more policies. Statutory surplus is determined usi ng accounting principles prescribed or permitted by the insurance subsidiaries’ state of domicile and differs from GAAP equity. 3

NI Holdings, Inc. At a Glance Exchange / Ticker NASDAQ: NODK Share Price (at 4/30/2020): $13.51 Shares Outstanding: 21,779,260 Market Capitalization: $294,238,000 GAAP Equity at 3/31/2020 : $301,791,000 Book Value Per Share: $13.71 NI Holdings, Inc. Westminster American Insurance Company MD Domicile A.M. Best: A (Excellent) Nodak Insurance Company ND Domicile A.M. Best: A (Excellent) American West Insurance Company ND Domicile A.M. Best: A (Excellent) Battle Creek Mutual Insurance Company NE Domicile A.M. Best: A (Excellent) Primero Insurance Company NV Domicile A.M. Best: A (Excellent) Direct Auto Insurance Company IL Domicile A.M. Best: A (Excellent) History of Organization Apr. 1946 Apr. 2001 Dec. 2010 Sept. 2014 Mar . 2 017 Mar. 13, 2017 Aug. 2018 Jan. 2020 100% of Nodak Insurance Company stock transferred to NI Holdings, Inc. Nodak Mutual Insurance Company was incorporated under the laws of North Dakota as a property and casualty insurer. American West Insurance Company, a multi - state licensed property casualty insurance company, was acquired through a stock purchase agreement. Entered into an Affiliation Agreement with Battle Creek Mutual Insurance Company, a domestic property casualty insurer under the laws of Nebraska. Primero Insurance Company, a Nevada non - standard auto insurance company, was acquired through a stock purchase agreement. Demutualization of Nodak Mutual Insurance Company. Direct Auto Insurance Company, an Illinois non - standard auto insurance company, was acquired through a stock purchase agreement. Westminster American Insurance Company, a Maryland commercial insurance company, was acquired through a stock purchase agreement. 4

Organization Structure: Experienced Management Team ▪ The majority of the current senior management team has been working together for the past fourteen years. ▪ Collectively, the senior management team represents over 100 years of industry experience. ▪ Throughout their careers, members of this team have managed through both soft and hard markets and expansion through M&A. ▪ This team, with Board support, is dedicated to appropriate pricing and achieving positive margins across all lines of business. Title Industry Experience Jim Alexander, President & CEO 30 years Brian Doom, EVP , Secretary/Treasurer & CFO 43 years Pat Duncan, VP Operations 31 years Tim Milius, VP Finance 33 years Seth Daggett, VP Strategy 16 years Brad Larson, VP Sales 28 years Joe Welsch , VP Marketing & Public Relations 25 years 5

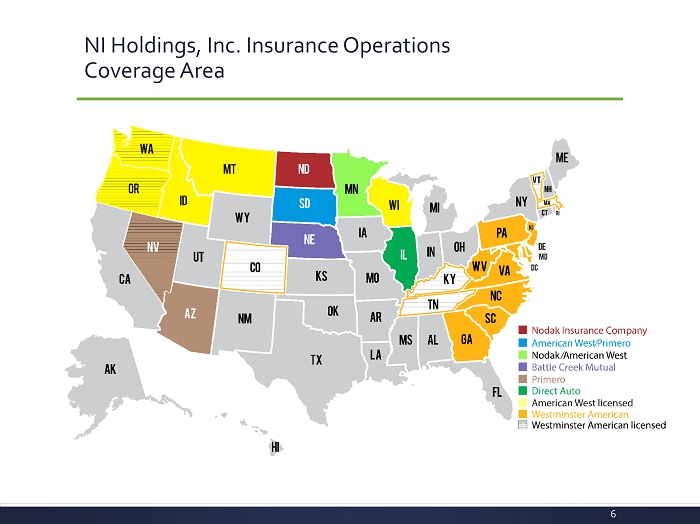

NI Holdings, Inc. Insurance Operations Coverage Area 6

NI Holdings, Inc 2019 Direct Premiums Written by State (Non - Crop Lines Only) Group 7

NI Holdings, Inc. Financial Ratios 60.8% 27.7% 88.5% 68.9% 27.3% 86.2% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0% Loss and LAE Ratio Expense Ratio Combined Ratio Year Ended December 31 2018 2019 51.9% 33.1% 85.0% 51.8% 34.3% 86.1% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0% Loss and LAE Ratio Expense Ratio Combined Ratio Three Months Ended March 31 2019 2020 8

NI Holdings, Inc. 2019 Business Mix Percent of Direct Written Premium Private Passenger Auto , 24.3% Non - standard Auto , 20.4% Home and Farm , 25.5% Crop , 13.6% Commercial , 13.3% All - Other , 2.9% 9

NI Holdings, Inc. Equity Allocation as of March 31, 2020 Insurance Subsidiaries (Statutory) $243,417 Stat to GAAP Adjustments $28,895 Holding Company $29,479 Total: $301,791 10

Award - winning workplace 11 □ Effective April 2020, AM Best assigned an A (Excellent) rating to all insurance operating entities within the NI Holdings corporate structure. This includes: • Nodak Insurance Company • American West Insurance Company • Battle Creek Mutual Insurance Company • Primero Insurance Company • Direct Auto Insurance Company • Westminster American Insurance Company □ Nodak Insurance Company is recognized as one of Ward’s 50 Top Performing Property/Casualty Insurance Companies for seven consecutive years and eight in the last nine years as of July 201 9 . □ Nodak Insurance Company is recognized by United Way of Cass - Clay as one of the top 50 most generous workplaces since 2017.