Attached files

| file | filename |

|---|---|

| EX-32 - EX 32.2 SEC 906 CERTIFICATION-CFO - PARALLAX HEALTH SCIENCES, INC. | ex322sect906certcfo123119.htm |

| EX-32 - EX 32.1 SEC 906 CERTIFICATION-CEO - PARALLAX HEALTH SCIENCES, INC. | ex321sect906certceo123119.htm |

| EX-31 - EX 31.2 SEC 302 CERTIFICATION-CFO - PARALLAX HEALTH SCIENCES, INC. | ex312sect302certcfo123119.htm |

| EX-31 - EX 31.1 SEC 302 CERTIFICATION-CEO - PARALLAX HEALTH SCIENCES, INC. | ex311sect302certceo123119.htm |

| EX-23 - EX 23.1 AUDITOR CONSENT - PARALLAX HEALTH SCIENCES, INC. | ex231auditorconsent.htm |

UNITED STATES

SECURITIES AD EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

Commission file number 000-52534

PARALLAX HEALTH SCIENCES, INC.

(Exact name of registrant as specified in its charter)

Nevada | 46-4733512 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

|

1327 Ocean Avenue, Suite B, Santa Monica, CA | 90401 |

(Address of principal executive offices) | (Zip Code) |

|

|

Registrant's telephone number, including area code: | (310) 899-4442 |

Copy of all Communications to:

Peter Hogan, Esq.

Buchalter

1000 Wilshire Blvd., Suite 1500

Los Angeles, CA 90017

(213) 891-0700

□ |

| Accelerated filer | □ | |

Non-accelerated filer | □ |

| Smaller reporting company | □ |

|

|

| Emerging growth company | ☒ |

The aggregate market value of Common Stock held by non-affiliates of the Registrant as of June 30, 2019, was $12,850,866, based on a closing price of $0.14 for the Common Stock on June 30, 2019, the last business day of the Registrant’s most recently completed second fiscal quarter. For purposes of this computation, all executive officers and directors have been deemed to be affiliates. Such determination should not be deemed to be an admission that such executive officers and directors are, in fact, affiliates of the Registrant.

Indicate the number of shares outstanding of each of the registrant’s

classes of Common Stock as of the latest practicable date.

270,723,289 common shares issued and outstanding as of May 15, 2020

Forward-Looking Statements

This Annual Report contains forward-looking statements. These statements relate to future events or the future financial performance of Parallax Health Sciences, Inc. (“Parallax” or the “Company”), and include statements made by the Company regarding insurance reimbursements, state licenses, product development and obtaining FDA clearances. In some cases, forward-looking statements can be identified by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors” that may cause the Company’s or its industry’s actual results, levels of activity, performance or achievements expressed or implied by these forward-looking statements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Except as required by applicable law, including the securities laws of the United States, the Company does not intend to update any of the forward-looking statements to conform these statements to actual results.

Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, it cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, the Company does not intend to update any of the forward-looking statements to conform these statements to actual results.

In this Annual Report, unless otherwise specified, all dollar amounts are expressed in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles. All references to “Common Stock” refer to the common shares; and “Preferred Stock” refer to the preferred shares; of the Company’s capital stock.

As used in this Annual Report, the terms “the Company”, “we”, “us”, “our”, and “Parallax” shall mean Parallax Health Sciences, Inc., and its wholly-owned subsidiaries, Parallax Diagnostics, Inc., Parallax Health Management, Inc., Parallax Behavioral Health, Inc., and Parallax Communications, Inc., unless otherwise indicated. The Company’s former wholly-owned subsidiary, RoxSan Pharmacy, Inc., was derecognized effective May 14, 2018. (See “RoxSan Pharmacy” and “Legal Proceedings” sections contained within this Annual Report.)

CORPORATE OVERVIEW |

Parallax Health Sciences, Inc. is a healthcare company focused on developing products and services that can provide remote communication, diagnosis, treatment, and monitoring of patients on a proprietary platform. Through its innovative technologies, both patented and patent-pending, the Company’s principal mission is to deliver solutions that empower patients, reduce costs, and improve the quality of care.

The Company’s principal executive office is located at 1327 Ocean Avenue, Suite B, Santa Monica, California, 90401, with an additional office located at 28 West 36th Street, 8th Floor, New York, NY 10018. The Company’s telephone number is (310) 899-4442.

The Company’s websites are at www.parallaxcare.com, www.parallaxhealthsciences.com, www.parallaxhealthmanagement.com, www.parallaxdiagnostics.com, and www.goodhealthoutcomes.com.

Parallax is a fully reporting company with its stock traded on the OTC Markets under the symbol “PRLX” (OTC.PRLX).

CORPORATE HISTORY

Formation and Development

The Company was incorporated in the State of Nevada on July 6, 2005. On November 1, 2012, the Company, formerly Endeavor Power Corporation, and its wholly-owned subsidiary, Endeavor Holdings, Inc., a Nevada corporation, entered into an Agreement and Plan of Merger with Parallax Diagnostics, Inc., a Nevada corporation, whereby Parallax Diagnostics became a wholly-owned subsidiary. On January 9, 2014, the Company changed its name to Parallax Health Sciences, Inc.

The Parallax business was founded on the Company’s Point-of-Care diagnostic business, Parallax Diagnostics, Inc., in 2010, when the Company acquired the right, title, and interest, through an exclusive license with Montecito BioSciences, Ltd. (“MBS”), to develop, manufacture and commercialize the Target System, an FDA-cleared 2 desktop point-of-care immunoassay diagnostic testing system. Concurrently, through an Assignment Agreement with MBS, the Company acquired the right, title, and interest to twenty-five (25) FDA-cleared 2 tests in the area of infectious disease, medical conditions, drugs of abuse, cardiac and pregnancy, that are designed to be utilized with the Target System.

2FDA 510(k) clearances do not expire. For additional information on FDA clearance and 510(k) requirements, see “FDA Clearances and Approvals” section.

- 1 -

On August 31, 2016, the Company entered into an agreement with Qolpom®, Inc., an Arizona corporation in the remote healthcare monitoring and telehealth business (“Qolpom®”) and its shareholders (the “Seller”) to purchase 100% of the issued and outstanding shares of Qolpom®’s common stock and its assets, inventory and intellectual property. The agreement was fully executed and the transaction was completed on September 20, 2016. The consideration for the acquisition resulted in a fair market value of $290,000, and goodwill of $785,060. In addition, the agreement included contingent royalties and revenue sharing for future revenues generated from the Qolpom® technology. The Qolpom® name was later changed to Parallax Health Management, Inc. (“PHM”).

On March 22, 2017, the Company formed a wholly-owned subsidiary, Parallax Behavioral Health, Inc. (“PBH”), a Delaware corporation, and on April 26, 2017, completed the asset acquisition of 100% of certain intellectual property (“Intellectual Property”) from ProEventa Inc., a Virginia Corporation (“ProEventa”), in accordance with the Intellectual Property Purchase Agreement between the Company, PBH and ProEventa (the “ProEventa Agreement”). ProEventa has an expertise in the development of behavioral health technologies, and is the wholly-owned subsidiary of Grafton Integrated Health Network, Inc., a non-profit Virginia corporation (“Grafton”). Pursuant to the ProEventa Agreement, the initial consideration for the Intellectual Property was paid to ProEventa in the form of a stock purchase agreement to purchase 2,500,000 shares of the Company’s Common Stock for $2,500, resulting in a net cost for the Intellectual Property of $622,500. In addition, the Agreement included conditional contingent royalties and revenue sharing for future revenues generated from the Intellectual Property.

On September 20, 2018, the Company formed Parallax Communications, Inc, a Delaware corporation and wholly-owned subsidiary of Parallax Health Management, Inc.

On August 28, 2019, the Company entered into a Purchase Agreement (the “Purchase Agreement”) with Global Career Networks Inc., a Delaware corporation, (“GCN”) to acquire a 19% interest in GCN. The Purchase Agreement was fully executed on September 6, 2019, with an effective date of October 15, 2019 (the “Effective Date”). Pursuant to the Purchase Agreement, in exchange for 6,666,667 shares of the Company’s restricted Common Stock, valued at $1,000,000, the Company acquired 760 shares of GCN common stock. In addition, in the event the market value of Parallax Common Stock one (1) year from Effective Date, is greater than $0.075 per share but less than $0.30 per share, the Company is required to issue GCN up to an additional 20,000,000 shares of restricted Common Stock, for an aggregate value of the Company’s Common Stock held by GCN of $2,000,000. At December 31, 2019, the Company recorded an impairment on the investment of $1,000,000.

In December 2019, an outbreak of the COVID-19 virus was reported in Wuhan, China. On March 11, 2020, the World Health Organization (“WHO”) declared the COVID-19 virus a global pandemic, and on March 13, 2020, President Donald J. Trump declared the virus a national emergency in the United States. As of the date of the filing of this Annual Report, the WHO reports over 4 million confirmed COVID-19 cases and over 275,000 deaths worldwide, including over 75,000 in the U.S. This highly contagious disease has spread to most of the countries in the world and throughout the United States, creating a serious impact on customers, workforces and suppliers, disrupting economies and financial markets, and potentially leading to a world-wide economic downturn. It has caused a disruption of the normal operations of many businesses, including the temporary closure or scale-back of business operations and/or the imposition of either quarantine or remote work or meeting requirements for employees, either by government order or on a voluntary basis.

The COVID-19 pandemic may adversely affect the Company’s customers’ operations, its employees and its employee productivity. It may also impact the ability of the Company’s subcontractors, partners, and suppliers to operate and fulfill their contractual obligations, and result in an increase in costs, delays or disruptions in performance. These effects, and the direct effect of the virus and the disruption on the Company’s employees and operations, may negatively impact both the Company’s ability to meet customer demand and its revenue and profit margins. The Company’s employees, in many cases, are working remotely and using various technologies to perform their functions. The Company might experience delays or changes in customer demand, particularly if customer funding priorities change. Further, in reaction to the spread of COVID-19 in the United States, many businesses have instituted social distancing policies, including the closure of offices and worksites and deferring planned business activity. Additionally, the disruption and volatility in the global and domestic capital markets may increase the cost of capital and limit the Company’s ability to access capital. Both the health and economic aspects of the COVID-19 virus are highly fluid and the future course of each is uncertain. For these reasons and other reasons that may come to light if the coronavirus pandemic and associated protective or preventative measures expand, the Company may experience a material adverse effect on its business operations, revenues and financial condition; however, its ultimate impact is highly uncertain and subject to change.

In response to the global need for diagnostics and personal safety during the pandemic, the Company, through its wholly-owned subsidiary, Parallax Diagnostics, Inc., has registered with the Food and Drug Administration (FDA), and has established strategic relationships with wholesale suppliers for global distribution of FDA-approved COVID-19 diagnostic test kits, and various Personal Protective Equipment (“PPE”) that meet current FDA guidelines,3 such as protective masks, sterile gowns, and eye goggles. All products distributed by the Company are inspected through an internal quality control process that ensures the products meet the FDA regulations and guidelines. The Company is also in the process of developing the SPARKS Mobile™ testing device along with a proprietary diagnostic test to be able to identify markers to the Coronavirus. Parallax is profoundly gratified by its ability to help those in need during this crisis.

3 Although FDA-approval is preferred, the FDA has issued various guidelines to follow during the COVID-19 pandemic, with consumer safety as the primary concern. This temporary guidance enables certain products, such as facial protective masks, to be distributed in order to meet the urgent demand, without the time intensive FDA-approval process.

- 2 -

On April 13, 2020, the Company received an Order of Suspension of Trading dated April 10, 2020 (the “Order”) from the United States Securities and Exchange Commission (“SEC”). The temporary suspension period was from 9:30 a.m. EDT on April 13, 2020, through 11:59 p.m. EDT on April 24, 2020. The Order referred to questions raised regarding the accuracy of the Company’s recent press releases in relation to the Company’s development of a rapid screening test for COVID-19, and the Company’s access to “large quantities of COVID-19 diagnostics testing kits and personal protective equipment.”

In an effort to protect the interests of shareholders, the SEC has issued similar orders and suspensions recently to several registrants, with concerns over the validity of claims made in connection with the availability of COVID-19 tests and supplies.

The Company, along with its counsel, is cooperating fully with the SEC to substantiate the Company’s recent public announcements and business endeavors, and is addressing any questions and/or concerns raised regarding the accuracy of the assertions made in the Company’s press releases.

Pursuant to Rule 15c2-11 under the Exchange Act, at the termination of the trading suspension, no quotation may be entered unless and until the Company has strictly complied with all provisions of the rule, including the filing of a new Form 15c2-11 with FINRA.

The Company is required to file its Annual Report with the SEC for the purposes of satisfying its financial reporting requirements. However, in addition to the Company's reporting obligations, the Company must have a FINRA Member Market Maker file a 15c2-11 with FINRA in order for the Company’s shares to resume trading on the OTCQB market. These actions do not impact or otherwise affect the Company's results of operations or disclosures as set out in this Annual Report. The Company believes that this Annual Report fully complies with the requirements of the Securities Exchange Act of 1934, as amended and, in accordance with generally accepted accounting principles, that it fairly presents, in all material respects, the financial condition and results of operations of the Company as at the relevant dates.

As of the date of filing of this Annual Report, the trading suspension period expired, and the Company is in the process compiling the information required for its 15c2-11 submission by a FINRA Member Market Maker. The Company anticipates the filing of a new Form 15c2-11 within the next 30 days. If any party has any questions as to whether the Company has complied with the rule, they should contact the staff in the Division of Trading and Markets, Office of Interpretation and Guidance, at (202) 551-5777.

These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for its common stock. Many brokers may be unwilling to engage in transactions in its common stock because of the added disclosure requirements, thereby making it more difficult for stockholders to dispose of their shares.

Changes in Management

On April 6, 2017, the Company’s board of directors (the “Board”) elected Mr. J. Michael Redmond as Chairman, to serve until the next annual meeting of the shareholders, in accordance with the Company’s bylaws, and/or until his successor is duly appointed, or a resignation is duly tendered.

Effective July 6, 2017, the Board caused the departure of Mr. Redmond from his position as President and Chief Executive Officer of the Company and RoxSan Pharmacy, Inc., and concurrently Mr. Redmond was removed from all board member seats.

Effective July 7, 2017, pursuant to a unanimous Board resolution, Mr. Paul R. Arena was appointed as the Company’s President and Chief Executive Officer, and the Board caused Mr. Arena's election to the Board and the Boards of the Company’s wholly-owned subsidiaries, Parallax Health Management, Inc. and Parallax Behavioral Health, Inc.

On July 26, 2017, Dr. Jorn Gorlach resigned as a member of the Board. This resignation did not involve any disagreement with the Company.

On June 4, 2018, Mr. Anand Kumar resigned as a member of the Board. This resignation did not involve any disagreement with the Company. Mr. Nathaniel T. Bradley, currently serving as Chief Technology Officer, succeeded him, and agreed to serve as a member of the Board until the next annual meeting of the shareholders and/or until his successor is duly appointed.

On May 15, 2019, Mr. David Appell joined the Company as its Chief Operating Officer. On February 2, 2020, Mr. Appell resigned his position. His resignation was not the result of a disagreement with the Company on any matters relating to the Company's operations, policies or practices. Concurrent with his resignation as COO, Mr. Appell will serve as Managing Director of the Company’s wholly-owned subsidiary, Parallax Communications, Inc. (“PCOM”). As Managing Director, Mr. Appell will provide business advisory and strategic planning advice to the Company with PCOM. In exchange for these services, Mr. Appell will be paid $2,000 per month plus medical benefits.

On March 1, 2020, Dr. David L. Stark was appointed as the Company’s President. In connection with the appointment, Mr. Paul R. Arena, who has held the position of President since July 2017, remains the Company’s Chief Executive Officer and Chairman of the Board of Directors, but resigned the position of President to afford Dr. Stark’s appointment.

- 3 -

In 2013, the Company identified an opportunity to acquire RoxSan Pharmacy, Inc. (“RoxSan”), a California corporation, and began the due diligence process. The Company’s initial interest centered on utilizing the acquisition as a means of accelerating the commercialization of the Company’s Target System and diagnostic platform, as RoxSan had access to a nationwide network of doctors and sales representatives. During the due diligence process, the Company became aware of numerous opportunities that RoxSan and its markets represented. On March 21, 2013, the Company entered into a Letter of Intent with Shahla Melamed, RoxSan's sole Shareholder, to acquire RoxSan. Between 2013 and 2015, four (4) amendments were also executed.

As part of the acquisition, the Company was required to obtain licensure from the State of California, and on July 31, 2015, the Company received notice that its pharmacy and sterile compounding licenses were issued by the California State Board of Pharmacy.

On August 13, 2015, (the “Closing Date”), pursuant to a resolution of the Board, the Company entered into an Agreement to Purchase and Sell One Hundred Percent of the Issued and Outstanding Shares of RoxSan Pharmacy, Inc. (“RoxSan” or the “Pharmacy”), and its Assets and Inventory (the “Purchase Agreement”). Pursuant to the Purchase Agreement between Parallax, RoxSan and its sole shareholder, Shahla Melamed (the “Seller” or “Melamed” or “Former Owner”), in exchange for 100% of RoxSan's common stock, and its assets and inventory, Parallax, among other things, issued the Seller a Secured Promissory Note (the “Note”) dated August 13, 2015, in the amount of $20.5 million (the “Acquisition”). The Note bore interest at a rate of 6% per annum, and matured August 13, 2018 (“Maturity”). As a result of the Acquisition, effective August 13, 2015, RoxSan became a wholly-owned subsidiary of Parallax. No change in control occurred as a result of the Acquisition.

In October 2015, shortly following the Company’s acquisition of RoxSan, Shahla Melamed (“Melamed”), initiated two (2) legal actions against the Company in the Superior Court of the State of California, County of Los Angeles, West District, Shahla Melamed v. Parallax Health Sciences, Inc., action numbers SC 124873 and SC 125702. In the matter, action No. SC 124873, Melamed sought rescission of the August 13, 2015, Purchase Agreement. In the Matter, action No. SC125702, Melamed alleges that the Company is in default under the terms of the Purchase Agreement and Secured Note, and the Company’s termination of Melamed’s employment agreement.

The Company also initiated legal action against Melamed and filed a complaint in October 2015, action number SC 124898, in the Superior Court of the State of California, County of Los Angeles, West District, Parallax Health Sciences, Inc., et al. v. Shahla Melamed, et al. The complaint in that action alleges that Melamed breached several obligations under the Purchase Agreement, and the Company sought to reduce the Secured Note due to undisclosed material changes in the business.

In January 2019, Melamed requested mediation, seeking settlement of the pending litigation with the Company, including that which was initiated against the Company by her son, Hootan Melamed (Shahla and Hootan, collectively, the “Melameds”). Through mediation, the Company and the Melameds reached agreeable settlement terms, and on February 19, 2020, the Company received a counter-signed Settlement and Release Agreement (the “Settlement”). Effective February 12, 2020 (the “Effective Date”), the Settlement is by and between Parallax Health Sciences, Inc., RoxSan Pharmacy, Inc., Michael Redmond, Edward Withrow III, Huntington Chase Financial Group, LLC, Calli Bucci and Dave Engert (collectively, “Parallax”), and Shahla Melamed and Hootan Melamed (collectively, the “Melameds”), and resolves all pending lawsuits between the parties in connection with the acquisition of RoxSan Pharmacy.

In consideration of the resolution of all existing and potential claims, including the cancellation of the Note in the principal sum of $20,500,000, and accrued interest of approximately $4,500,000, and without further action or litigation and without admission of liability by either party, the Settlement terms include the following:

●A payment of $4,000,000 (the “Settlement Sum”) to the Melameds, to be paid as follows:

$1,250,000 within 90 days of the Effective Date;

$1,250,000 within one (1) year of the Effective Date;

$1,500,000 within two (2) years of the Effective Date.

●The issuance of ten (10) million shares of the Company’s Common Stock to an entity owned by Shahla Melamed.

In addition, in the event forty percent (40%) or more of the Company and/or its subsidiaries (including by way of merger) is sold within two (2) years of the Effective Date, the Company shall pay the Melameds, within two (2) weeks of receipt of the proceeds from such sale (the “Sale Proceeds”), any outstanding unpaid Settlement Sum plus an additional 10% of the Sale Proceeds received, up to a total of an additional $3,000,000 over and above the Settlement Sum.

In the event the Company fails to cure a breach of timely payment of any portion of the Settlement Sum within thirty (30) days of a notice of default, a Stipulated Judgement may be filed by Melamed in the sum of $20,000,000, less any Settlement Sum amounts previously paid by the Company.

(See ITEM 3. LEGAL PROCEEDINGS section).

- 4 -

On May 14, 2018, pursuant to unanimous resolutions of the boards of directors of RoxSan Pharmacy, Inc. and Parallax Health Sciences, Inc., RoxSan filed a Chapter 7 petition in the United States Bankruptcy Court for the Central District of California (the “Court”). Mr. Timothy Yoo was appointed trustee (“Trustee”) on May 15, 2018. In connection with this filing, RoxSan sought to discharge approximately $5 million of liabilities owed to various parties, and intercompany loans in excess of $1 million owed to Parallax. The Chapter 7 bankruptcy proceeding by RoxSan Pharmacy, Inc. was fully discharged, and the case was closed on March 13, 2019, in U.S. Bankruptcy Court, Central District of California.

Due to, among other things, the reduction in RoxSan’s cash flows during 2016 and 2017, RoxSan became delinquent in its payroll tax depository obligations, resulting in a liability owed to federal and state taxing agencies in the aggregate of $1,148,811, which includes $601,148 in taxes withheld from employees (“Trust Fund Taxes”), employer taxes of $183,172, and penalties and interest of $364,491 through December 31, 2018. The liability was included as part of the Chapter 7 bankruptcy petition, and certain portions of the liability may be discharged. However, in accordance with California bankruptcy laws, federal and state Trust Fund Taxes are not dischargeable. The Company has retained a tax resolution specialist and is in communications with the taxing agencies in order to resolve RoxSan’s liability. During the year ended December 31, 2019, payments for Trust Fund Taxes in the amount of $485,498 were made, and $115,650 in Trust Fund Taxes were outstanding at December 31, 2019.

As a result of the loss of financial control of RoxSan, the Company derecognized the subsidiary as of September 30, 2018. The derecognition resulted in a gain of $4,478,268. The Company also extinguished $22,778,281 in debt and accrued interest related to the acquisition of RoxSan.

DESCRIPTION OF BUSINESS |

Overview

The Company’s principal focus is on personalized patient care through remote healthcare services, behavioral health systems, and Point-of-Care diagnostic testing. Parallax’s current family of companies that serve as the foundation for its cross-over business model of operations include:

●Parallax Diagnostics, Inc. (“Parallax Diagnostics” or “PDI”) acquired a proprietary Point-of-Care diagnostic immunoassay testing platform and 25 test cartridges for the areas of infectious diseases, cardiac markers, drugs of abuse and various other medical conditions. PDI has recently become an FDA registered distribution partner for various lateral flow-through COVID-19 IgM/IgG antibody instant tests products. It has also registered and distributed approved Personal Protective Equipment (PPE) through an ecommerce website at GoodHealthOutcomes.com.

●Parallax Health Management, Inc. (“PHM”) develops remote patient monitoring (“RPM”) and telehealth market products and services, and commercializes them, including the Good Health Outcomes™ software platform with Fotodigm® proprietary data capture which allows for systems integration with a number of third-party services and solutions.

●Parallax Behavioral Health, Inc. (“PBH”) acquired the intellectual property known as REBOOT™, the acronym for Reliable Evidence-Based Outcomes Optimization Technologies, as well as the Intrinsic Code™ technology, a software platform specifically designed to improve health treatment outcomes through cloud-based and mobile behavioral technology systems that enable its users and user groups to more effectively achieve goals within a prescribed timeline.

The Company envisions a world where healthcare is accessible, reliable and affordable, without compromising quality and economics of the healthcare industry. Driven by a sincere desire to make people’s lives better and push back on the healthcare industry’s crippling economic outlook, the Good Health Outcomes™ platform was created; the Company’s design is for “outcomes realized through intelligent health.”

The Good Health Outcomes™ system facilitates cost-effective remote diagnosis, treatment and monitoring of patients with chronic diseases. Parallax’s integrated products and services provide Point-of-Care (“POC”) patient testing and monitoring, along with information communicated via cloud-based mobile smartphone applications that are agnostic as to operating systems and utilize sophisticated data analytics. Information is retrieved in real-time by physicians and other healthcare professionals and is integrated into electronic health records. The Company’s digital products and services capitalize on the transformation of healthcare to provide improved compliance, diagnosis, monitoring and support to patients, along with cost savings and efficiencies to healthcare systems.

Good Health Outcomes™ encompasses three separate divisions that can operate independently of one another, or integrate services to meet the various needs of the Company’s clientele: Optimized Outcomes, Connected Health and Smart Data.

Optimized Outcomes | REBOOT™ / COMPASS™ Behavioral modification |

Connected Health | Fotodigm® platform Remote patient monitoring, telehealth, Personal Protective Equipment (PPE) and POC diagnostic testing |

Intrinsic Code™ technology Actionable insights to behavior modification |

- 5 -

Each of the Company’s divisions target a separate vertical market that complement each other and the Company value proposition. In addition, the synergistic operational cross-over affords the Company the ability to use built-in economies of scale across multiple operating platforms.

The Company believes that the solutions lay in the empowerment of the patient, the payer and the provider; creating a model of healthcare that aligns all three interests and creates a singular goal of better health outcomes, at reduced cost. The Good Health Outcomes™ platform involves these areas of focus:

●Behavioral Modification

The Company believes in working to empower the patient to modify their behavior through personal empowerment. The Company has developed and designed a revolutionary technology that will aid in the challenges of behavior modification, and improve adherence to medical regimens, which can lead to lower costs and better health.

REBOOT™, the Company’s patented cloud-based behavioral software technology, along with COMPASS™, the Company’s mobile application that incorporates REBOOT™ with unique mobile phone features, and WIZARD™, which supports scalability of the REBOOT™/COMPASS™ platform, was developed by behavioral specialists at Grafton Integrated Health Network, a multistate behavioral healthcare organization with over 60 years of clinical experience and data in behavioral health.

●Connected Health

Continually increasing healthcare costs, difficulty accessing care, and a greater need for convenience, are driving consumers to demand more value out of their healthcare dollar and seek care that meets their needs and preferences. The market is responding to this growing demand, and non-traditional care models are rapidly expanding, such as:

●Traditional providers (e.g., office-based primary care physicians (PCPs) and specialists, hospitals) are partnering with non-traditional care providers to expand reach.

●New parties, such as consumer product and technology companies, are entering this billion-dollar market.

●Non-traditional care models have the opportunity to complement traditional care models to help improve access and affordability, and to deliver a more personalized healthcare experience.

To meet these changing demands, the Company has developed Good Health Outcomes™, the Company’s proprietary connected health platform that provides remote patient monitoring, telehealth, POC diagnostics and health education products and services on a single platform. Currently in its beta stage, Fotodigm®, the integrated data capture utility, has the capability for systems integration of an unlimited number of third-party biometric measurement products, electronic health and medical record software (EHR, EMR) services and solutions. The Company is continuing the Fotodigm® beta stage to test economic models and delivery modalities in preparation for large-scale deployment of the Fotodigm® platform and the filing of 510k FDA approval of the Fotodigm® system. The Good Health Outcomes™ platform is based on the following:

●Telehealth/Remote Patient Monitoring

Improves digital connectivity among consumers, providers, health plans, and life sciences companies.

Facilitates self-managed care, with the help of technology-enabled solutions.

Provides a secure environment that protects consumer privacy.

Delivers care outside the traditional clinical setting, potentially providing better access to care at a lower cost.

Assists chronic disease management and improves population health outcomes.

Empowers patients by providing a cost-effective tool that connects them with their doctors.

Empowers doctors with improved patient scheduling flexibility and timely communications.

Provides hospitals with a tool to address the problem and economic hardship caused by readmissions.

Provides a virtual management tool for chronic disease management.

●Target System

Allows doctors to test patients in their office.

Requires only a one-time learning process to perform all tests.

Delivers test results in 12 minutes or less.

Provides patients with important information at the time of testing.

Costs less than outside lab-based tests, allowing for a reduction in payer costs and patient co-pays.

Allows doctors to earn additional revenue that they cannot participate in with outside labs and testing not performed in their offices.

Patients can test from their homes and transmit data to doctors.

The Parallax Business Model

In the past 60 years, healthcare has transitioned from a direct relationship between doctor and patient, to one that has patients separated from their doctors by the introduction of a huge number of stakeholders, ranging from health insurers, employers, pharmacy benefit managers, imaging, diagnostic testing, lawyers, specialists and a plethora of others. The patient and healthcare provider both want the same thing: information, quality of service, transparency, value for their hard-earned dollars, and more time in their day.

- 6 -

The Company has developed, acquired and licensed multiple proprietary and exclusive platforms that provide services and products, across the healthcare continuum. These platforms are designed to allow for multiple points of reciprocal consideration, through innovative business models, that provide patients with increased quality of services and products, at reduced cost of time and money. They also provide healthcare providers with increased access to their patients, the ability to deliver better and more efficient service and increase their income from the services they supply. The Company believes the Good Health Outcomes™ system will deliver solutions to problems of health and economics, while providing essential actionable data to pharmaceutical firms, payers and healthcare providers, through our:

●Patented behavioral machine learning technology;

●Patented POC diagnostic testing technology;

●Patent-pending interoperable connected health platform targeting two of healthcare’s biggest problems that, combined, address markets that represent over $1 trillion in costs 4:

Medical nonadherence

Chronic disease management; and

●Smart Data delivered through enhanced patient/disease stratification, in combination with dynamic behavioral data, relating to adherence to pharmacologic and medical therapy regimens designed to:

help patient outcomes

reduce the cost of care associated with nonadherence

deliver actionable data.

Cognitive AI

The Company is working with partners that have developed a cognitive artificial intelligence, (“Cognitive AI”) agent architecture with the interaction of emotion, motivation and cognition of situated agents, mainly based on the Psi theory of Dietrich Dörner. The Psi theory addresses emotion, perception, representation and bounded rationality, but being formulated within psychology, has had relatively little impact on the discussion of agents within computer science. Cognitive AI is a formulation of the original theory in a more abstract and formal way, at the same time enhancing it with additional concepts for memory, building of ontological categories and attention.

Big Data Opportunity

The Company’s real-time data generated from patient-users can be stripped to protect the specific patient-user identity and exchanged for historical data with Center for Disease Control, (“CDC”), National Institute of Health, (“NIH”), various universities and others to provide valuable empirical health related information to the Company’s patient-users using Cognitive AI provided by the Company’s partners and coordinated through various electronic health record organizations for which the Company is agnostic. This empirical data when it becomes available on the Company’s outcomes optimization-based platform will become a valuable tool for determining predictive and supportive diagnostics to its patient-users.

The Company’s endeavors to change the healthcare industry are strengthened by providing solutions to real problems facing healthcare stakeholders today. The Company’s products and services have been developed, and are continuing to be developed, to address these issues now. The Company’s models include revenue from, and are compatible with, both the traditional reimbursement through payers, and the new performance-based compensation and financial incentive for the adoption of healthy, preventative behavior.

The Cross-Over and Cross-Pollination Model

The Company’s business model is built on identifying opportunities represented by one market vertical that provides for a separate vertical to utilize one or more of the Company’s core operations. Although the multiple operations of Good Health Outcomes™ are focused in separate vertical markets, the Company has designed its business model to allow for cross-pollination and reciprocal transfer of value at multiple points in their respective economic food chains.

As an example of how each of the Company’s divisions can support each other utilizing the cross-over and cross-pollination model:

●The Optimized Outcomes division can provide a range of after-care products and services through the Connected Health division.

●The Connected Health division can offer telehealth and remote patient monitoring, and POC testing and diagnostics services directly to the doctors and patients of the Optimized Outcomes division. Further, remote patient monitoring customers can be offered POC testing and diagnostics, and vice versa.

●The Smart Data division can offer the Company’s software and Intrinsic Code™ technology systems to the Optimized Outcomes and/or Connected Health clientele.

4 https://www.milkeninstitute.org/publications/view/910

- 7 -

The term cross-over and cross-pollination is best demonstrated by the manner in which Parallax customers are exposed to products and services they might benefit from other than what they are seeking, and these additional products and services could augment the core product or service they receive from Parallax. The cross-over component comes from the customer, their unique situation and perspective (including socio-economic, demographic and stratified health profile), and their participation in innovation through their individual goals as it relates to their health regimen; the cross-pollination comes through the value represented by the exposure to Parallax’s product and technology offerings. By way of the cross-over and cross-pollination model, the customer is empowered and increases participation in their own health, which is one of Parallax’s core strategies.

An example of the cross-over and cross-pollination model is further illustrated as follows:

●A customer has identified Good Health Outcomes™ as a solution for Remote Monitoring of their health or medical condition (i.e. a chronic disease);

●The customer will be prescribed a medical regimen that includes prescription medication and biometric vitals (i.e. blood pressure, weight, glucose, et al);

●The opportunity is created for Parallax to introduce its Medication Adherence product to the customer.

The customer type will vary, depending upon the sales and marketing approach and target audience, but is primarily comprised of:

●Patients

●Providers: Doctors, Nurses, Clinicians and Caregivers

●Payers: Insurance Companies, Corporations, Government

The Company believes that the current healthcare system is built on unsustainable models and significant challenges for all the stakeholders in the healthcare system. The Company also believes that it can deliver solutions which fill a void in the current market for high quality, high efficacy products and services delivered at reasonable and rational prices. The Company’s business strategy is to expand through organic growth, selective synergistic acquisition, and develop, license and/or acquire, quality products and or services that complement the Good Health Outcomes™ systems.

Products and Services

Parallax believes that its products and services can provide solutions that mitigate rising costs, reduce waste in spending through transparency, reduce the amount of unnecessary services, and increase the health and wellness of patients before they are sick.

Remote healthcare products include patented and patent pending software and mobile apps (to be available for iPhone on Apple App Play Store and Android on Google Play) and other services, as well as electronic kits and devices from third-party licensed platforms that are designated towards a patient’s primary health concern (i.e. diabetes, blood pressure, cardiovascular, general monitoring, etc.), and offer both audio and video options that interface with the patient’s healthcare providers. Prescription medication dosage monitoring is also available.

Behavioral health products include the proprietary behavioral health technology, REBOOT™, which powers decision support that can also be delivered securely to any internet connected device. The software can be used by an individual or an organization of any size, with the potential to transform the cost of treating and managing chronic illnesses such as pulmonary-COPD-asthma, diabetes, and cardiovascular disease by effecting the modification of behavior in patients being treated for these chronic diseases.

Diagnostics products include the Target System, the Company’s proprietary POC diagnostic immunoassay testing platform and test cartridges for the areas of infectious diseases, cardiac markers, drugs of abuse and various other medical conditions, and the patented SPARKS Mobile™, the next-generation handheld mobile analyzer currently under development. The Target System will allow doctors to test patients in their office, with test results delivered in 10 minutes or less. This allows patients to be provided with important information at the time of testing. The costs of the Target System are less than outside lab-based tests, benefiting both payers and patients. In addition, doctors will be able to generate additional revenue that would normally be paid to an outside laboratory, and patients can even perform test from their homes, with results transmitted directly to their doctor. The Company has also recently selected antigens and antibodies to be used as the markers for its rapid Coronavirus (“COVID-19”) screen test, currently in the pre-clinical stage of development, for use with its FDA-cleared Target System platform.

Through the development and design of the Good Health Outcomes™ platform, the Company’s telehealth, RPM and POC products and services are interoperable and interchangeable with any FDA cleared/approved medical device, providing ease of use and connectivity between patient and doctor. The advancement in the Company’s technology is strengthened by the ability to scale its products to meet the demands of both individuals and large groups alike.

- 8 -

Global COVID-19 Pandemic and Pandemic Viruses and Diseases of the Future

Data driven and behavioral technologies are well positioned to counter and deal with the current medical crisis within the U.S. and abroad.

The COVID-19 global pandemic is the cause of:

●Estimated $10s of trillions in economic losses on a global basis from economic closures and compound effects of COVID-19;

●Over 1.4 million reported infected in the U.S. with over 83,000 deaths, and growing.

Medication Nonadherence

Medication nonadherence is a priority public health consideration, affecting health outcomes and overall healthcare costs on a worldwide basis. Increasing adherence to medical regimens leads to better health outcomes in chronic disease and reduces the overall costs to the patient, payer and all of the stakeholders across the healthcare continuum.

Nonadherence to medication regimen in chronic disease management is the cause of 5:

●$300 billion in avoidable costs to the U.S. healthcare system annually;

●125,000 premature deaths in the U.S. annually.

Research from the World Health Organization 6 has shown that better adherence to antihypertensive treatment could prevent 89,000 deaths each year in the U.S., with a projected savings of $106 billion a year.

Chronic Disease Management

Chronic diseases are on the rise in the U.S., leaving healthcare payers with the challenge of covering care for patients with these expensive, long-term conditions. Healthcare spending reached a total of $3.2 trillion in 2015, based upon estimates from the Center for Medicare Services (“CMS”). Spending is expected to grow at an average of 5.5% through 2025, with chronic disease treatment comprising a major portion of that spending.

Based on the latest data from the Center for Disease Control (“CDC”), the top 8 most expensive chronic diseases for healthcare payers to treat are:

●Cardiovascular Disease

Cardiovascular disease (“CVD”) in the U.S. total $317 billion per year, split between $193.7 billion in direct medical costs and $123.5 billion in lost productivity. An adult in the U.S dies from CVD related health conditions every 40 seconds, with CVD deaths accounting for 31% of all U.S. deaths each year.

●Smoking-Related Health Issues

The estimated costs for smoking-related health issues in the U.S. total over $300 billion per year, split between direct healthcare expenses of $170 billion and indirect costs of roughly $156 billion.

●Alcohol-Related Health Issues

In 2010, excessive alcohol use cost the U.S. economy $249 billion, or roughly $2.05 per drink. Alcohol-related deaths totaled 88,000 people per year, and shortened the lives of working adults by an average of 30 years.

●Diabetes

As one of the most prevalent chronic conditions in healthcare, diabetes care costs reached $245 billion in 2016. Seventy-one percent of diabetes treatment costs ($176 billion) were related to direct healthcare expenses. That equates to 20 percent of U.S. healthcare spending.

●Cancer

According to the latest estimates from the CDC and the National Cancer Institute, cancer care costs are roughly $171 billion a year due to healthcare inflation over previous decades.

●Obesity

The United States spends $147 billion on healthcare related to obesity, and roughly $117 billion on costs related to inadequate physical activity. In 2006, healthcare costs for obese patients were $1,429 higher than patients at a normal weight. Obesity is implicated in the development or worsening of many other chronic conditions, including diabetes and cardiovascular disease.

The total cost of arthritis in the U.S. was an estimated $128 billion, split between $81 billion in direct medical expenses and $47 billion in related losses of productivity and care management. Arthritis affects 23 percent of adults in the U.S., or 54 million people, and is expected to rise to 78 million cases by 2040. Arthritis also occurs with other chronic conditions, as many patients are unsure on how to manage their own symptoms.

●Strokes

On its own, strokes in the U.S. create medical expenses of $33 billion annually and accounts for 1 out of 20 deaths in the country, or an estimated 130,000 deaths per year.

These nonadherence and chronic disease numbers are daunting in the best of conditions, but the reality is that the sheer volume of U.S. citizens reaching the age of 60 will impact the cost trajectory. The projected financial impact is not sustainable under the current healthcare system.

5 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3234383/#B8

6 https://www.who.int/chp/knowledge/publications/adherence_report/en/

- 9 -

Parallax is led by experienced veterans with backgrounds from the healthcare, medical devices, drug development, technology, FDA regulatory, medical insurance billing and patient management, finance and management of early stage and high growth companies. The Company’s disciplined and organized approach is balanced by its optimism for the future, and the opportunities present in the current healthcare market. The Parallax team is grounded in a belief that success in business is built on a combination of research, planning and execution.

At Parallax, management continually strives to identify solutions to the challenges facing the current healthcare system. The Company and its management team of professionals are committed to delivering the highest quality products and services to patients, payers, healthcare insurers and stakeholders that are accessible and reasonable, and are built upon sound business models and economics that are designed to provide for sustainable growth and increased value to the Company’s shareholders.

Overview

Parallax continues its focus on Point-of-Care diagnostics, with an emphasis on its Target System testing platform, including the Target Antigen Detection System, the flow-through test cartridge, and the FDA-cleared VT-1000 desktop analyzer and novel applications that detect and/or monitor infectious diseases, cardiac markers and drug of abuse assays. The Company holds exclusive licenses, in perpetuity, to a line of proprietary, patented and/or patent-pending, FDA-cleared, Point-of-Care diagnostic tests to be utilized with its single platform diagnostic testing Target System. Parallax, with its products and products in development, offers the potential to transform the diagnostic landscape by transitioning critical tests from the centralized lab directly to the hands of the physician or clinicians.

The Company continues to pursue viable opportunities for the commercialization of its product, including strategic partnerships with third-party companies in order to limit the Company’s capital outlay. Additionally, the Company has sought to identify strategies that would make its proposition more valuable and competitive. The Company has spent the last few years expanding its patent portfolio and further developing potential integration of new applications. The Company, through its license with Montecito BioSciences, Ltd. (“MBS”), has been issued patents on the core technology for its Target System. In addition, in 2014, 2015 and 2017, the Company, through its license with MBS, received patents on its mobile testing device, the SPARKS Mobile™ diagnostic reader, in the United States, China, Hong Kong, Macao, and India. In 2019, the Company engaged a patent attorney to identify and pursue infringements of its licensed patents around the foundational technology and the SPARKS Mobile™ diagnostic reader globally, some of which have already been identified.

The Company is also pursuing the expansion of the Target System’s test cartridges for the diagnoses of additional diseases. The Company has identified a technology previously cleared by the FDA that can be utilized as a platform for a test cartridge that will detect CD4 and CD8 cells, which in turn determine a patient’s immune status. In addition, the Company is in the process of developing a test cartridge for the diagnosis of the COVID-19 virus.

Target System Product Strategy

In recent years, there has been a continuing shift from the use of laboratory-based analyzers to point-of-care (“POC”) tests that can be performed in a matter of minutes. Unlike the centralized clinical laboratory segment of the diagnostic market, which is mature and highly competitive, the POC market is still in its relatively early stages. According to the recent worldwide research reports, however, such as the 2010 Worldwide IVD Market, by the research firm Kalorama Information, the growth rate of the POC market continues to rise. Although certain simple, single analyte diagnostic tests have been developed, such tests have remained incapable of precise and highly sensitive quantitative measurements. As a result, medical tests that require precise quantitation of the target analyte have remained the domain of immunoassay analyzers in the centralized laboratory.

Point-of-Care diagnostic kits typically consist of test strips that the healthcare provider applies a patient’s sample to and then reads the strip either visually or with an instrument in order to determine a result. They are simple to use, fast, disposable and reliable within an acceptable range. More sensitive analytes or tests requiring quantitative analysis and definitive antibody screening needed in most situations, must be sent out to a diagnostic lab, and hours or days later results arrive. These tests are comparatively complex, expensive, and time consuming; only centralized diagnostic facilities can manage sample handling and the cost of instruments and reagents. A POC instrument that has the advantage of a test strip device in terms of ease of use and rapid results along with enzyme-linked immunosorbent assay (ELISA)-like capabilities for major diseases would circumscribe diagnosis routinely within the course of a patient visit. This could disrupt the current model. The Company is planning to develop just such a device that it intends to sell to doctors and healthcare providers.

The commercial success of the current generation of small, simple to use diagnostic devices which provide rapid results in POC applications has been limited by their inability to provide precise, highly sensitive, quantitative measurement. Despite these limitations, the rapid increase in discovery of individual markers of disease processes, coupled with the advancements in rapid detection technologies, has made these tools available to medical professionals on a wide scale and POC diagnostics are quickly becoming a high growth industry.

- 10 -

The Target System (the VT-1000 Desktop Analyzer, the Target Antigen Detection Cartridge and associated reagents) technology addresses these limitations by applying sophisticated immunochemical and optical methods to detect and quantify analytes present in various human specimens, including blood, urine, and feces. Data indicates that sensitivity will be comparable to expensive and complicated laboratory-based analyzers. The Company believes that there is market potential for advanced POC diagnostic products that provide quick and accurate diagnosis during a patient visit, shortening the decision time to medical intervention and minimizing the need for additional patient follow-up, thereby reducing overall healthcare delivery costs.

The Company also believes that there is growth opportunity for the exploitation of its Target System platform in developing nations and regions such as Africa, India, South America, Eastern Europe, Russia and Asia as well as developed markets of North America and Western Europe. One of the first initiatives to be developed for this market will combine the Company’s SPARKS Mobile™ (a portable hand-held diagnostic analyzer based on the VT-1000 Desktop Analyzer), currently in development, with a test for the COVID-19 virus, as well as a test for the monitoring of AIDS/TB patients through the use of a proprietary rapid point-of-care immunoassay CD4-CD8 test called PROMISE CD4, also in development.

The Diagnostics Products

The Company’s assets include a FDA-cleared VT-1000 Desktop Analyzer and more than two dozen FDA 510(k) cleared diagnostic tests. The Desktop Analyzer and immunoassay system incorporates a flow-through rapid antigen test platform configuration that has the ability to produce high-performance quantitative blood test results with the ease of rapid qualitative diagnostic strips. The Company has patents and patent applications related to its current and future products, as well as methods for future test development. The Target VT-1000 Desktop Analyzer is ideally suited for rapid development and commercialization of all new tests that may be introduced, as well as integrating remote patient monitoring and telehealth products and services into the Target System through the SPARKS Mobile™ platform.

VT-1000 Desktop Analyzer: Quantitative and Qualitative Immunoassay

The Company’sVT-1000 Desktop Analyzer is FDA-cleared and is capable of rapidly detecting qualitative and quantitative data for its FDA-cleared Target Platform tests. The VT-1000 Desktop Analyzer is used for all Target System platform Tests, allowing for clinical personnel to be trained once and also gives consistent results for both qualitative and quantitative testing. The Company plans to develop the SPARKS Mobile™, a hand-held analyzer unit, similar in size to a mobile phone, which will be based on the VT-1000 Desktop Analyzer (see “SPARKS Mobile™: The Target System Hand-Held Analyzer).

VT-1000 Desktop Analyzer

Target Antigen Detection System (“TADS”)

The Target Antigen Detection System consists of a unique single-use cartridge with reagents capable of testing multiple test markers for qualitative testing and, when used with the VT-1000 Desktop Analyzer, provides quantitative results. The TADS requires a small amount of sample and provides results in minutes. The simplicity of the fully loaded single-use test cartridge and subsequent ease-of-use of the instrument helps to alleviate the technical burden on medical staff and makes patient diagnosis more efficient.

- 11 -

Each individual TADS test cartridge operates in a uniform fashion using a controlled flow-through rapid antigen testing system, utilizing an enzyme-linked immunosorbent assay (“ELISA”). The ELISA method is a technique used to determine if a certain substance is present within a sample. Using special antibodies that attach to the substance, the sample will generate a specific color. The amount of color indicates the amount of substance present. Another set of antibodies are used to “capture” the substance.7 The results can then be measured at specific wavelengths by an ELISA analyzer, such as the VT-1000, in two forms:

●Qualitative: Refers to whether an analyte is present and provides “positive” or “negative” results through color changes, using known positive and negative samples.

●Quantitative: Refers to how much is present and uses a series of standards to measure the unknown amount of analyte.

TADS Cartridges

The simplicity of the fully loaded single-use test cartridge, and subsequent ease-of-use of the instrument, helps to alleviate the technical burden on medical staff, and makes patient diagnosis more efficient.

The Company’s Target Antigen Detection System is a departure from the standard devices typical to the rapid testing markets and can allow for physicians to share in revenues. The device is part of the manufacturer’s qualitative and quantitative “Target System Diagnostics Platform,” which offers an array of improved modifications and features to the traditional qualitative and semi-quantitative flow-through immunoassay test. With its platform uniformity, vacuum pump, absorption layer for sample overflow, and complete compatibility with single and multi-light source reflectometer technology, the TADS cartridge is a unique collection of tests for qualitative and quantitative detection diseases and of conditions. The TADS cartridge utilizes a vacuum technology to deposit specimen samples uniformly on test membranes. The Vacuum Control Flow Device provides a vacuum pump action, which reduces test time and ensures maximum contact with the membrane antibodies. This collection device allows for numerous tests to be incorporated. The vacuum specimen filtration and excess specimen absorption is built in.

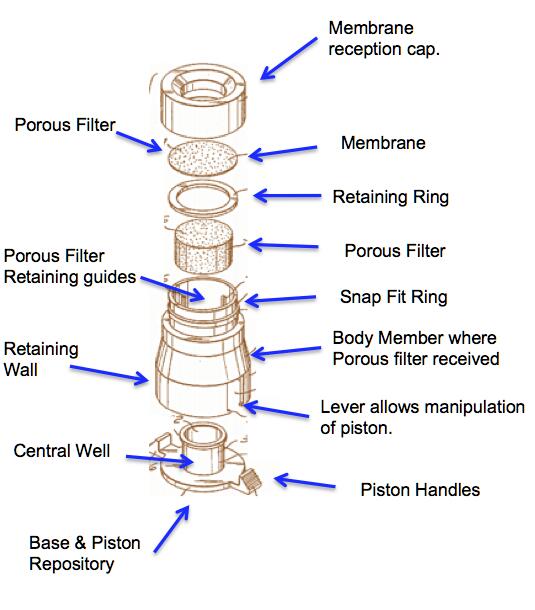

TADS Components

7 “ELISA,” Simple English Wikipedia, [website], March 2013, https://simple.wikipedia.org/wiki/ELISA

- 12 -

TADS 2.0 Flow Through Testing System with Pressure Indicator

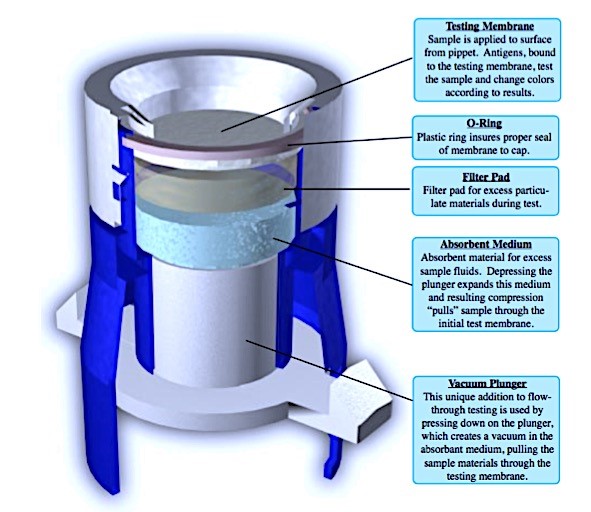

On March 3, 2017, the Company, through its licensor, Montecito BioSciences, Inc., was granted patent 9,588,114 (See “INTELLECTUAL PROPERTY SUMMARY”) for the new and improved TADS testing cartridge, which provides an assay device that has an externally manipulatable piston for creating a region of reduced air pressure beneath a membrane containing an analytic compound, preferably a receptor or antibody. The region of reduced pressure causes a fluid sample to be tested to be rapidly drawn through the membrane. To ensure that a sufficient reduction in pressure is achieved, the membrane further includes a pressure sensing means, so the entire sample contacts the analytic compound. The Company believes that obtaining the greatest level of contact where the antibody and antigen meet, is essential when striving for the best possible test results to be consistently achieved.

How the Target Antigen Detection System (“TADS”) Works

The TADS testing system performs immunoassays on analytes for determining the presence and/or amount of an analyte in a sample, and includes:

An immunosorbent membrane;

An absorbent material;

A piston component located below the absorbent material to draw analytes in a sample through the immunosorbent membrane into the absorbent material; and

Discrete groups of pressure-sensitive microcapsules located on the immunosorbent membrane.

Each group of microcapsules has a different predetermined average burst strength; and

Each group of microcapsules includes a dye that is different from the dye of any other of said groups.

The TADS testing system has an immunosorbent membrane with one or more binding agents non-diffusively bound to its upper surface. The immunosorbent membrane refers to a porous support membrane having at least one antibody (polyclonal or monoclonal antibody), antibody fragment or derivative thereof, aptamer, or other non-protein based entity (e.g., a carbohydrate or lipid), which specifically binds to a cognate epitope. In particular, the porous material is a thin disk of material such as nitrocellulose, nylon (e.g., cast from nylon 6,6 polymer) or polyvinylidene difluoride (PDVF).

A sample or analyte solution refers to any sample suspected of containing a particular analyte. It is recognized that a sample may contain no analyte, or, in other words, the test for that ligand (a molecule that binds to another molecule) is negative.

The sample can be of biological or environmental origin.

Examples of biological samples include whole blood, serum, plasma, amniocentesis fluid, pleural fluid, peritoneal fluid, sputum, urine, feces, cerebrospinal fluid, exudates, extracts of skin or tissue specimens, swabs from the throat or wounds and the like.

Examples of environmental samples include water specimens (e.g., drinking water or streams), extracts of soil samples, and swabs of shipping packages, food samples, and the like. In this respect, an “analyte” refers to any material that can be involved in an antibody/antigen reaction.

Typically the analyte will be an antigen, for example, a protein, a carbohydrate, cell walls (e.g., bacterial or fungal cell walls), virus particles and small molecule haptens. Other examples include molecules such as cocaine, morphine, progesterone, luteinizing hormone-releasing hormone, or DNA. It is also possible that the analyte is an antibody that reacts with a bound antigen or an antibody to the antibody.

Additional Tests and Products for Development

The Target System provides the platform for the development of a series of quantitative tests for important diagnostic applications that can provide results at a patient's bedside, in a doctor's office, in the emergency room, in a clinic, in an ambulance, on the battlefield, on-site agri-business locations, rural and economically disadvantaged areas. The Target System expects to meet the POC diagnostic market criteria as follows:

Rapid turnaround time

Direct application of a non-critical volume or placement of sample directly into instrument

Disposable device or minimal maintenance required

Minimal technical expertise required

Positive identification and specimen tracking strategy that eliminates specimen identification errors

Simple strategy for calibration and QC

Transferability of data to the LIS or HIS

Agreement of result with accepted “Gold Standard” tests

Affordable cost

- 13 -

The Company’s testing system is not limited to HIV or AIDS diagnostics. The Company is currently working with Naglreiter, an established medical device development company, to develop the prototype for the SPARKS Mobile™ handheld device in conjunction with a compatible rapid test cartridge for the detection of the COVID-19 virus. The rapid test is being developed using recombinant S1 and S2 glycoproteins reagents that are geared to identify the virus through the “Spike” S1 and S2 antigens in human cells. The COVID-19 Spike proteins play a key role in eliciting potent neutralizing-antibody and T-cell responses. The Spike’s receptor binding domain is the primary determinant of the virus’s ability to infect.

Diseases like COVID-19, malaria, cholera, hepatitis, yellow fever, West Nile virus, and other viral diseases present increasing health threats to large populations around the globe, with the largest problems existing at the stage of proper diagnosis. The Target System test cartridge format is readily adaptable, having been applied to viral and bacterial infections in the past such as Rubella, Rotavirus, and Streptococcus A.

The Company believes that it can adapt the VT-1000 Desktop Analyzer and SPARKS Mobile™ to the rapid, simple POC diagnosis of nearly every disease without the requirement of additional equipment. Further, the Company believes that the combination of a mobile, hand-held testing device along with test cartridges for a host of different diseases can improve disease diagnoses and healthcare in a vast majority of today’s underserved regions. In addition, the Target System platform allows for the monitoring of environmental components influencing the health of populations, such as the presence of toxins in soil and drinking water and contamination of food supply.

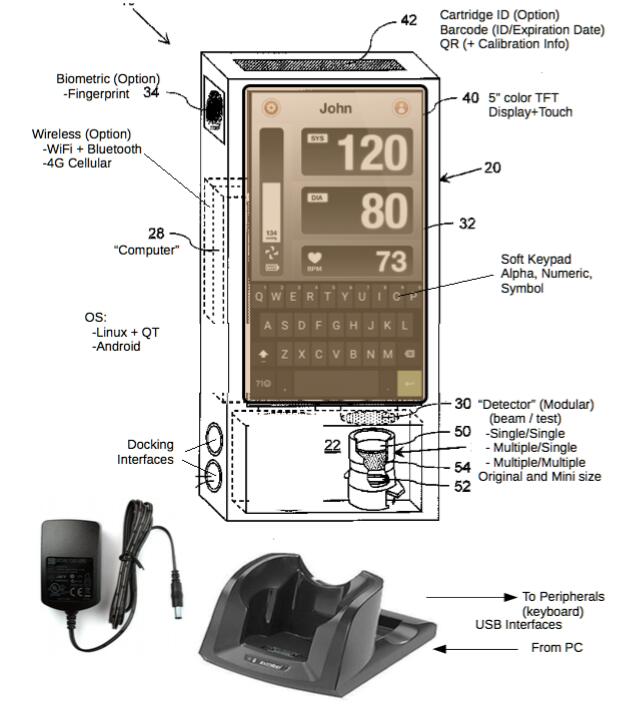

SPARKS Mobile™: The Target System Hand-Held Analyzer:

The SPARKS Mobile™ is the Company’s next-generation analyzer. Utilizing re-engineered technology of the VT-1000 Desktop Analyzer, the SPARKS Mobile™ is a handheld device that is intended to utilize the Company’s TADS test cartridges and include a small, rapid testing format, in conjunction with a data acquisition and test reading, with connectivity and features similar to a smartphone device. The SPARKS Mobile™ is currently in the design stage of the development process.

SPARKS Mobile™

Design Concept

Whether searching for markers in the blood stream, or diagnosing a pathogen in urine, the Company’s SPARKS Mobile™ will be a portable tool for rapid diagnostics. The SPARKS Mobile™ will also provide an improvement in POC diagnostics and applications in countries with limited healthcare infrastructures and geographic limitations, both of which are of paramount importance in the combat against infectious diseases and in the fight against proliferation of endemic and pandemic diseases. This innovative SPARKS Mobile™ will allow for a fast (minutes instead of hours or days) performance of tests at the point of care and will only require a test cartridge and a small number of ready-to-use solutions in preformatted quantities. Moreover, the SPARKS Mobile™ will include the ability to store patient information, test data, and QC data, and transmit data through wireless connections.

- 14 -

The SPARKS Mobile™ design goals are intended to:

●achieve a portable monitoring system, which is compatible with proven and reliable ELISA-based target system technology.

●expand readout capabilities to provide a mobile testing and monitoring platform.

●increase the economy of scale and scope of the diagnostics and monitoring platform by the development of additional utility of the device without redundant infrastructure investments (additional data acquisition of patients, additional tests for other, predominant diseases).

The densimeter/multi-light spectrum reflectometer utilizing immobilized enzyme antigens in blood plasma or urine, which is the core testing system of the VT-1000, will not change. The testing technology in the initial SPARKS Mobile™ testing device will be based upon the same FDA. 510(k) cleared technology employed in the Company’s VT-1000 Desktop Analyzer and is compatible with existing TADS test cartridges. However, a number of innovative features will be integrated into the design to meet customer and patient needs, including those included in the Company’s most recent conceptualization of design and functionality and environmental interface:

●High Infrared Light Spectrum;

●Easy Field Upgrades;

●No Change of Equipment;

●Printer Hook-up Capability;

●Low Entry Cost for New Test Development and Analysis;

●Safety, Security and Accuracy by design; and

●Desk to Docking Station: Smart Phone Capability

The SPARKS Mobile™ is being specifically designed to coordinate with the Target System and the TADS cartridges to provide reliable quantitative results within minutes, right at the point-of-care or site of testing. The continuity of the Company’s product and system upgrades and the continuous development of new tests based on an increasing point-of-care market paradigm, points to the VT-1000 Desktop Analyzer and the SPARKS Mobile™ as low cost alternatives to large laboratory analyzers and specialized training of personnel on multiple machinery. The ultimate value to the clinician or the attending physician is the ease of use, reproducibility and the history of accuracy of this type of rapid immunoassay principle in the area of quantitative analysis.

The graphics below represent the Company’s most recent conceptualization of the design components and features for the SPARKS Mobile™, its technology, operational construct and environmental interface:

SPARKS Mobile™

- 15 -

The Company has also initiated the development of telehealth, remote patient monitoring and cognitive service offering capabilities into the SPARKS Mobile™ design and business model, for the integration of the Good Health Outcomes™ (Fotodigm® and REBOOT™) and Parallax Communications products and services (see “Additional Tests and Products for Development”).

SPARKS Mobile™

Operation Concepts

- 16 -

The Company will continue to develop the design of the SPARKS Mobile™ as well as economic models designed to maximize the value of the SPARKS Mobile™. Although the Company’s 2020 budget does not include 100% of the funding resources to bring the development of the SPARKS Mobile™ to the prototype and beta stages, the Company continues to seek third-party resources, with the goal of obtaining FDA 510(k)-clearance for the SPARKS Mobile™ based upon the FDA 510(k)-cleared VT-1000.

Immunoassays: Defined 8

Immunoassays are chemical tests used to detect or quantify a specific substance, the analyte, in a blood or body fluid sample, using an immunological reaction. Immunoassays are highly sensitive and specific. Their high specificity results from the use of antibodies and purified antigens as reagents. An antibody is a protein (immunoglobulin) produced by B-lymphocytes (immune cells) in response to stimulation by an antigen. Immunoassays measure the formation of antibody-antigen complexes and detect them via an indicator reaction. High sensitivity is achieved by using an indicator system (e.g., enzyme label) that results in amplification of the measured product. Immunoassays may be qualitative (positive or negative) or quantitative (amount measured). An example of a qualitative assay is an immunoassay test for pregnancy. Pregnancy tests detect the presence of human chorionic gonadotropin (hCG) in urine or serum. Highly purified antibodies can detect pregnancy within two days of fertilization. Measuring the signal produced by the indicator reaction performs quantitative immunoassays. This same test for pregnancy can be made into a quantitative assay of hCG by measuring the concentration of product formed.

The purpose of an immunoassay is to measure (or, in a qualitative assay, to detect) an analyte. Immunoassay is the method of choice for measuring analytes normally present at very low concentrations that cannot be determined accurately by other less expensive tests. Common uses include measurement of drugs, hormones, specific proteins, tumor markers, and markers of cardiac injury. Qualitative immunoassays are often used to detect antigens on infectious agents and antibodies that the body produces to fight them. For example, immunoassays are used to detect antigens on Hemophilus, Cryptococcus, and Streptococcus organisms in the cerebrospinal fluid (CSF) of meningitis patients. They are also used to detect antigens associated with organisms that are difficult to culture, such as hepatitis B virus and Chlamydia trichomatis. Immunoassays for antibodies produced in viral hepatitis, HIV, and Lyme disease are commonly used to identify patients with these diseases.

Quantitative Immunoassay Analysis

Immunoassays are powerful techniques for understanding the role of specific components in complex systems. They work on the basis of the recognition of a specific component (target X) by an antibody or equivalent (affibody, RNA aptamer, recombinant antibody, etc.), which results in the production of a detectable signal. In most cases immunoassays are qualitative, providing information in terms of signal intensity. What is really wanted, however, is quantitative assay providing information in absolute chemical terms, namely the concentration of target X.

Quantitative Immunoassays would:

●Allow detection of the absolute concentration of components

●Reduce inter-assay variation in data

●Permit successful statistical analysis of smaller sample sets

●Permit direct comparison of data generated at independent sites or occasions.

Quantitative Immunoassays are simple to construct. They require the simultaneous analysis of experimental (or test) samples and calibration standards. The signal intensity generated by calibration standards of known concentration permits conversion of the signals generated by the test samples into absolute units of concentration.

Calibration curve

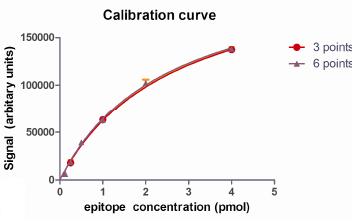

A calibration curve (or standard curve) establishes the relationship between the amount of material present and the signal intensity measured. In the case of immunoassays, this would represent the relationship between the epitope concentration and the signal intensity obtained. This relationship is often non-linear, and in many applications displays a dynamic range (or response range) of approximately two orders of magnitude in the concentration of target X.

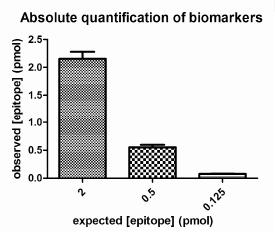

To perform a Quantitative Immunoassay, a set of "calibration standards" containing the epitope in various concentrations, are deployed in the immunoassay alongside experimental "test samples". Densitometry is performed on all data from the assay, and curve fitting used to define the relationship between epitope concentration and signal intensity. This mathematical relationship is then used to convert the signals generated by experimental samples into concentration of target X, which in the Company’s experience is highly accurate.

8 “Immunoassay tests,” Encyclopedia of Surgery, [website], 2001, https://www.surgeryencyclopedia.com/Fi-La/Immunoassay-Tests.html

- 17 -

Molecular Identity of Calibration Standards

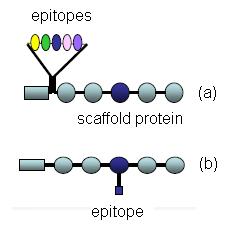

For Western Blot applications, a calibration standard is a molecule which contains the epitope feature of an immunoassay covalently bonded to a protein of known molecular weight. Two configurations of this structure are possible (Figure 1), where the epitope structure is either linked to the amino acid backbone (Fig 1a) in the form of a fusion protein or linked to a side chain of a specific amino acid (Fig 1b).

Figure 1: Schematic representation of calibration standard molecules.