Attached files

| file | filename |

|---|---|

| EX-32.1 - LUBOA GROUP, INC. | ex32-1.htm |

| EX-31.1 - LUBOA GROUP, INC. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2019

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________ to _____________

Commission File No. 333-199210

LUBOA GROUP, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Nevada | 90-1007098 | |

| (State

or Other Jurisdiction of Incorporation or Organization) |

(I.R.S.

Employer Identification No.) |

Room 202-1, Building # 21 of Intelligence and Wealth Center

Jiaxing, Zhejiang Province, China, 314000

(Address of Principal Executive Offices)

86-537-82239727

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer [ ] | Accelerated Filer [ ] | ||

| Non-Accelerated Filer [X] | Smaller reporting company [X] | ||

| Emerging growth company [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

As of June 28, 2019 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the shares of the registrant’s common stock held by non-affiliates (based upon the last sale price of $1.65 per share) was approximately $48.4 million. Shares of the registrant’s common stock beneficially held by each executive officer and director and by each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were a total of 111,600,000 shares of the registrant’s common stock outstanding as of May 7, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

None.

LUBOA GROUP, INC.

Annual Report on Form 10-K

TABLE OF CONTENTS

| i |

INTRODUCTORY NOTE

Special Note Regarding Forward Looking Statements

In addition to historical information, this report contains forward-looking statements. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth; any projections of earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, including those identified in this annual report, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause our results to differ materially from those expressed or implied by such forward-looking statements.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

Use of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

| ● | “we,” “us,” “our,” or “our company,” are to the combined business of Luboa Group, Inc., a Nevada corporation, and its subsidiaries and other consolidated entities; | |

| ● | “Bangtong International” are to Bangtong Technology International Limited, a Republic of Seychelles company and wholly-owned subsidiary of Luboa Group, Inc.; | |

| ● | “Bangtong Development” are to Bangtong Technology Development Limited, a Republic of Seychelles company and wholly-owned subsidiary of Bangtong International; | |

| ● | “Bangtong Group” are to Bangtong Technology Group Limited, a Hong Kong company and wholly-owned subsidiary of Bangtong Development; | |

| ● | “Jiaxing Bangtong” are to Jiaxing Bangtong Electronic Technology Co., Ltd., a PRC company and wholly-owned subsidiary of Bangtong Group; | |

| ● | “Shenzhen Bangtong” are to Shenzhen Bangtong Ecommerce Co., Ltd., a PRC company and variable interest entity; | |

| ● | “Jiaxing Electronic” are to Jiaxing Bangtong Electronic Commerce Limited, a PRC company and wholly-owned subsidiary of Shenzhen Bangtong; | |

| ● | “Shenyang Bangtong” are to Shenyang Bangtong Logistics Limited, a PRC company and a 70% owned subsidiary of Shenzhen Bangtong; | |

| ● | “Hegang Bangtong” are to Hegang Bangtong Electronic Commerce Limited, a PRC company and wholly-owned subsidiary of Shenzhen Bangtong; | |

| ● | “Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China; | |

| ● | “China” and “PRC” refer to the People’s Republic of China; | |

| ● | “Renminbi” and “RMB” refer to the legal currency of China; | |

| ● | “U.S. dollars,” “dollars” and “$” refer to the legal currency of the United States; | |

| ● | “SEC” are to the U.S. Securities and Exchange Commission; | |

| ● | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; and | |

| ● | “Securities Act” are to the Securities Act of 1933, as amended. |

| 1 |

| ITEM 1. | BUSINESS. |

Our Corporate History and Background

We were incorporated on March 19, 2013 under the name “Sunrise Tours, Inc.” under the laws of the state of Nevada. We originally intended to develop and offer special services, including 3D virtual tours for companies that would like to promote their venues on the Internet and through electronic media. On January 20, 2016, we filed a Certificate of Amendment with the Secretary of State of Nevada and changed our corporate name to “Luboa Group, Inc.” Concurrently with the name change, we changed our principal business plan to developing specialized agricultural products and a carbon emission trading platform in Asia. However, since inception, we have not engaged in active business operations and have not generated significant amount of revenue.

On January 7, 2019, through a series of private transactions, our former officer and director, Mr. Feng Jiang acquired an aggregate of 10,799,000 shares of common stock of the Company, representing 93.09% of the issued and outstanding share capital of the Company on a fully-diluted basis, and accordingly became the controlling shareholder of the Company, which caused a change in control of the Company.

Upon the change of control of the Company, all of our then officers and directors resigned from their respective offices and Mr. Jiang became our President, CEO, CFO, Treasurer, Secretary and Chairman of the Board of Directors.

On April 1, 2019, we entered into the a definitive Share Exchange Agreement (the “Exchange Agreement”) with Bangtong International and holders of all outstanding capital stock of Bangtong International, pursuant to which on June 21, 2019, we acquired 100% of the outstanding capital stock of Bangtong International, and in exchange, we issued to the former shareholders of Bangtong International an aggregate of 100,000,000 shares of the Company’s common stock. As a result of the Reverse Acquisition, Bangtong International became our wholly-owned subsidiary and the former shareholders of Bangtong International became the holders of approximately 89.6% of our issued and outstanding capital stock on a fully-diluted basis. For accounting purposes, the transaction with Bangtong International was treated as a reverse acquisition, with Bangtong International as the acquirer and the Company as the acquired party. Unless the context suggests otherwise, when we refer in this report to business and financial information for periods prior to the consummation of the Reverse Acquisition, we are referring to the business and financial information of Bangtong International and its subsidiaries and consolidated entities. In connection with the Reverse Acquisition, Mr. Feng Jiang resigned from his positions as of President, CEO, CFO, Treasurer, Secretary and Chairman of the Board of Directors. Mr. Xianyi Hao was appointed as our new President, CEO, CFO, Treasurer, Secretary and Chairman of the Board of Directors.

As a result of our acquisition of Bangtong International, we now own all of the issued and outstanding shares of Bangtong International, a holding company, which in turn owns all of the equity capital of Bangtong Development and its subsidiaries.

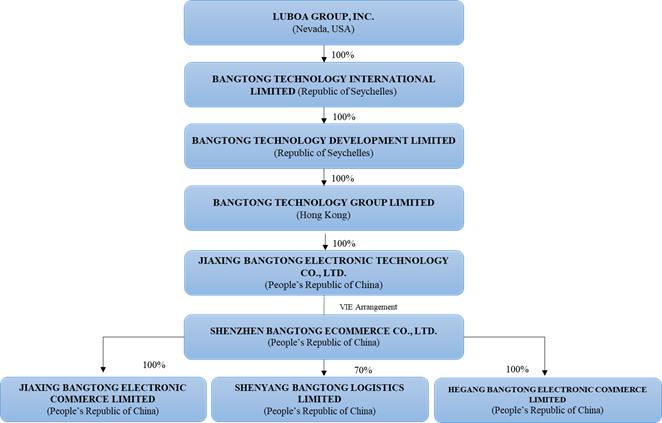

As of the date of this report, we have the following subsidiaries and affiliated entities:

Bangtong International, a Seychelles holding company, was formed on May 25, 2018. Xianyi Hao is the sole director of Bangtong International.

Bangtong Development, a Seychelles holding company, was formed on May 24, 2018. Xianyi Hao is the sole director of Bangtong Development.

Bangtong Group, a Hong Kong holding company, was formed on May 30, 2018. The sole director of Bangtong Group is Xianyi Hao.

Jiaxing Bangtong, a PRC company, was formed on November 5, 2018 and is engaged in the business of electronic technology development, service and consulting. Its legal representative is Qi Wang.

Shenzhen Bangtong, a PRC company, was formed on November 27, 2015 and is engaged in the business of electronic technology development and e-commerce. Its legal representative is Xianyi Hao.

| 2 |

Jiaxing Electronic, a PRC company, was formed on September 3, 2018 and is expected to engage in the e-commerce. Its legal representative is Qi Wang.

Shenyang Bangtong, a PRC company, was formed on May 23, 2018 and is expected to engage in the logistics business with warehousing and delivery capabilities. Its legal representative is Ming Zhao.

Hegang Bangtong is a PRC trading company. We expect that Hegang Bangtong’s business will focus on our inventory procurement from Russia and other European countries. Hegang Bangtong was formed on July 13, 2018 and its legal representative is Xianyi Hao.

As described below in more detail, through our variable interest entities in PRC (“VIEs”), including Shenzhen Bangtong and its subsidiaries, Jiaxing Electronic, Shenyang Bangtong and Hegang Bangtong, which have contractual arrangements with Jiaxing Bangtong, we are a startup company developing our e-commerce business.

Our Corporate Structure

Foreign ownership of Internet-based businesses is subject to significant restrictions under current PRC laws and regulations. We, as a Nevada corporation and our subsidiaries, including Bangtong International, Bangtong Development, Bangtong Group and Jiaxing Bangtong, are all restricted from holding licenses that are necessary for our online e-commerce business in China. To comply with these restrictions, our consolidated VIEs, Shenzhen Bangtong and its subsidiaries directly operate our business. We have entered into contractual arrangements with our VIE and its shareholders. Through these arrangements, we exercise effective control over the operations of these entities and receive the economic benefits of these entities. As a result of these contractual arrangements, under U.S. GAAP, we are considered the primary beneficiary of Shenzhen Bangtong and thus consolidate its results in our consolidated financial statements.

The following is a summary of the currently effective contractual arrangements by and among our wholly-owned subsidiaries, the VIEs and the shareholders of the VIEs.

Agreements that provide us with effective control over Shenzhen Bangtong and its subsidiaries:

Loan Agreement. On November 6, 2018, Jiaxing Bangtong and each shareholder of Shenzhen Bangtong entered into a loan agreement. Pursuant to the loan agreements, Jiaxing Bangtong agreed to provide an aggregate of RMB11,930,000 of loan to the shareholders of Shenzhen Bangtong solely for the purpose of capital contribution. The shareholders of Shenzhen Bangtong should cause Shenzhen Bangtong at the request of Jiaxing Bangtong to, execute contracts on business cooperation with Jiaxing Bangtong and provide Jiaxing Bangtong with all the information on its business operations and financial condition. In addition, at the request of Jiaxing Bangtong or a party designated by Jiaxing Bangtong, the shareholders of Shenzhen Bangtong should cause Shenzhen Bangtong to appoint any persons designated by Jiaxing Bangtong as directors and/or executive director of Shenzhen Bangtong. The shareholders also agreed not to sell, transfer or dispose of any equity interests in Shenzhen Bangtong or allow the encumbrance on these equity interests. The shareholders can only repay the loan by the transfer of all their equity interests in Shenzhen Bangtong to Jiaxing Bangtong or its designated persons. The amount of RMB11,930,000 was transferred to Shenzhen Bangtong in July 2018.

Equity Interest Pledge Agreement. On November 6, 2018, Jiaxing Bangtong and Shenzhen Bangtong and each shareholder of Shenzhen Bangtong entered into an equity interest pledge agreement. Pursuant to the equity interest pledge agreements, each shareholder of Shenzhen Bangtong agreed to pledge 100% equity interests in Shenzhen Bangtong to Jiaxing Bangtong to guarantee their and Shenzhen Bangtong’s performance of their obligations under the contractual arrangements including the exclusive business cooperation agreement, the exclusive option agreement, the loan agreement and the power of attorney. In the event of a breach by Shenzhen Bangtong or its shareholders of their contractual obligations under these agreements, Jiaxing Bangtong, as pledgee, will have the right to dispose of the pledged equity interests in Shenzhen Bangtong. The shareholders of Shenzhen Bangtong also undertake that, during the term of the equity interest pledge agreements, they will not dispose of the pledged equity interests or create or allow any encumbrance on the pledged equity interests. During the term of the equity pledge agreements, Jiaxing Bangtong also has the right to receive all of the dividends distributed on the pledged equity interests. The Company has completed the registration of the equity interest pledges with the relevant office of the administration for industry and commerce in accordance with the PRC Property Rights Law.

| 3 |

Power of Attorney. On November 6, 2018, each shareholder of Shenzhen Bangtong granted irrevocable and exclusive power of attorney to Jiaxing Bangtong as his/her attorney-in-fact to exercise all shareholder rights, including, but not limited to, attending shareholders meeting of Shenzhen Bangtong, voting on their behalf on all matters of Shenzhen Bangtong, disposing of all or part of the shareholder’s equity interest in Shenzhen Bangtong, approving the amendments to Shenzhen Bangtong’s articles of association and electing, appointing or removing legal representative, directors, supervisors and executive officers of Shenzhen Bangtong. Each power of attorney will remain in force for so long as the shareholder remains a shareholder of Shenzhen Bangtong. Each shareholder has waived all the rights which have been authorized to Jiaxing Bangtong under each power of attorney.

Spouse Consent Letters. Pursuant to the spouse consent letters dated November 6, 2018, each spouse of the shareholders of Shenzhen Bangtong, if any, confirmed that his/her spouse can perform the obligations under the contractual arrangements and has sole discretion to amend and terminate the contractual arrangements. Each spouse agreed that the equity interest in Shenzhen Bangtong held by and registered in the name of his/her spouse will be disposed of pursuant to the equity interest pledge agreement, the exclusive option agreement and the power of attorney. In addition, in the event that each spouse obtains any equity interest in Shenzhen Bangtong held by his/her spouse for any reason, he/she agreed to be bound by the contractual arrangements.

Agreement that allows us to receive economic benefits from Shenzhen Bangtong:

Exclusive Business Cooperation Agreement. On November 6, 2018, Jiaxing Bangtong and Shenzhen Bangtong entered into an exclusive business cooperation agreement. Under the agreement, Jiaxing Bangtong has the exclusive right to provide Shenzhen Bangtong with comprehensive technical support, consulting services and other related services. Without Jiaxing Bangtong’s prior written consent, Shenzhen Bangtong may not accept any same or similar services provided by any third party and may not establish same or similar cooperation relationships with any third party regarding the matters contemplated by this agreement. Shenzhen Bangtong agreed to pay Jiaxing Bangtong an annual service fee, at an amount to be determined by the parties by considering, among other things, the complexity of the services, the time that may be spent for providing such services, the value and specific content of the service provided, the market price of the same types of services, and the operating condition of Shenzhen Bangtong. In addition, Jiaxing Bangtong will own the exclusive intellectual property rights created as a result of the performance of this agreement. This agreement will remain effective until terminated unilaterally by Jiaxing Bangtong or otherwise upon the expiration of the operation term of a party according to this agreement.

Agreement that provides us with the option to purchase the equity interest in Shenzhen Bangtong:

Exclusive Option Agreement. On November 6, 2018, Jiaxing Bangtong, Shenzhen Bangtong and each shareholder of Shenzhen Bangtong entered into an exclusive option agreement. Pursuant to the exclusive option agreement, each shareholder of Shenzhen Bangtong irrevocably grants Jiaxing Bangtong an exclusive option to purchase, or have its designated person to purchase, at its discretion, to the extent permitted under PRC law, all or part of the shareholder’s equity interests in Shenzhen Bangtong. In addition, the purchase price should be the amount of registered capital, which may be subject to fair value adjustments if required by the PRC laws. Without the prior written consent of Jiaxing Bangtong, the shareholders of Shenzhen Bangtong and Shenzhen Bangtong may not amend Shenzhen Bangtong’s articles of association, increase or decrease the registered capital, dispose of its assets or business, create any encumbrance on its assets or business, incur any debts or guarantee liabilities, enter into any material contracts, merger with or acquire any other persons or make any investments, provide any loans for any third parties or distribute dividends to the shareholders. Each shareholder of Shenzhen Bangtong agrees that, without the prior written consent of Jiaxing Bangtong, he/she will not dispose of his/her equity interests in Shenzhen Bangtong or create or allow any encumbrance on the equity interests. Each exclusive option agreement will remain effective until all equity interests have been transferred or assigned in accordance with the agreement.

| 4 |

The chart below presents our corporate structure as of the date of this report:

Our principal executive offices are located at Room 202-1, Building #21 of Intelligence and Wealth Center, Jiaxing, Zhejiang Province, China, 314000. The telephone number at our principal executive office is +86-537-82239727.

Our Products and Services

We are a startup e-commerce company with substantially all of our operations in China. Most of our subsidiaries and VIEs were formed in 2018. We officially launched our e-commerce platform, Ingtona(英格多纳) in fall 2019, which was formerly developed under the name of Ingertona. Through our platform, we currently offer a range of consumer products sourced from both China and abroad as well as services relating to the franchise of our offline adult products store.

Our E-Commerce Platform

On October 26, 2018, Jiaxing Bangtong entered into a strategic cooperation contract with Beijing Xietongtianxia Technology Co., Ltd. (“Beijing Xietong”), pursuant to which Beijing Xietong agreed to act as Jiaxing Bangtong’s strategic consultant for Jiaxing Bangtong’s business, including but not limited to providing technical support to Jiaxing Bangtong’s development and operation of its e-commerce platform. Upon the expiration of this contract, Jiaxing Bangtong terminated the cooperation with Beijing Xietong, and instead, shifted to developing the e-commerce platform on its own. In the second half of 2019, our e-commerce platform, Ingtona, completed initial development. Our Ingtona platform includes the following principal components:

1. Website—www.Ingtona.com. We launched the website in September 2019. The PC-based website provides a user-friendly and intuitive interface that allows consumers to conveniently search for, find and purchase products. The website features adult products, overseas products and smart robots. It displays product information, such as description, specification, pictures, price, sales volume, applicable delivery expenses and customer review. Customers can conveniently browse and search for products by keywords and can sort product listings by keywords, sales volume and price. A customer needs to create an account on our website to place orders and purchase products. Various kinds of online payment methods are offered to customers at the time of checkout, such as WeChat Pay, AliPay and UnionPay. Customers can log into their accounts to check the status of their orders. The website currently displays more than 200 adult products and over 5000 imported items that span health, dietary supplements, maternity and baby care products, cosmetics, snacks, soft drinks, household supplies, toys and clothes from the United Kingdom, Germany, Japan, Australia, South Korea, Canada, the United States, Norway, Denmark, New Zealand and other countries. In addition, it contains smart robots sold directly by Chinese and foreign makers.

| 5 |

2. Mobile app—Our mobile application, Ingtona (英格多纳), will allow consumers to conveniently search and purchase displayed products on their mobile devices. Our mobile application offers similar features as our PC-based website. We rolled out our mobile application in October 2019.

3. WeChat public account—Customers can also access our e-commerce platform through our WeChat public account. Product offerings on the “Shopping Mall” section of our WeChat public account synchronize with those on our website and are also classified into three large categories: overseas items, smart robots and adult products. The “Partners” section of our WeChat public account allows parties to conveniently contact us who are interested in setting up their own stores and selling displayed products that will be directly sourced from manufacturers. We started our WeChat public account in September 2019.

The Business Model of our E-Commerce Platform

Registered users of our Ingtona e-commerce platform can be divided into two categories – third-party merchants and customers. Third-party merchants, including enterprise merchants and individual merchants, sell various merchandise products on the platform, and customers purchase these products using the same platform. Leveraging our multifaceted e-commerce platform, we plan to offer both online marketplace and online direct sales to our online customers.

In our online marketplace business, third-party merchants may establish online stores to offer products to customers over our online marketplace. We will charge service fees on our merchants for our services, such as webpage maintenance, WeChat account access, and certain promotion activities. We intend to charge commission based on a percentage of transaction value generated on our online marketplace. In addition, we plan to provide marketing and advertisement services to our third-party merchants. Prices for advertisements on our platform network will be fixed under contracts between us and the third-party merchants. The prices will depend on the display locations, the number of time slots and the display size. We intend to review our prices periodically and make adjustments as necessary in light of market conditions.

In our online direct sales business, we plan to acquire products from suppliers and sell them directly to customers. Before ourselves can provide all fulfillment and delivery services, we may rely partially on independent couriers to deliver products. Sometimes suppliers in our direct sales operation may deliver products to our customers themselves. Third-party sellers on our marketplace may also use their own logistics network or other third-party couriers to deliver products.

Our Offline Adult Products Franchise—”Enjoy Color Space (悦色空间)”

We not only offer a diverse collection of adult products on our e-commerce platform, but also run our own and franchised offline unmanned stores that retail adult products by automatic vending machines. Three franchisees have joined us and opened three such stores in China since September 2019. Merchants registered on our website can apply to franchise with us. New franchisees are required to pay an initial fee for a franchise license and once a franchise store begins operations, franchisees are required to pay us annual royalty. We may charge reduced or waive royalties for the first few franchisees. We provide franchisees with the vending machines, products (including return/exchange services), franchise designs, site selection assistance, ongoing trainings, marketing support and access to our e-commerce platform. Generally, an investment of RMB100,000~150,000 is needed to open such a store, and we currently offer different franchise packages for varying levels of investment.

Our Growth Strategies

The existing product offerings on our e-commerce platform are decided based on the proven popularity of purchasing these items on the internet. We plan to continuously add products and categories that appeal to our customers to our platform. In addition, we plan to expand our offerings of smart robots and intend to offer latest products in the AI smart product market sold directly by manufacturers.

| 6 |

With respect to our offline adult products franchise, we plan to open such stores across China through both franchise and our own investment.

Sales and Marketing

We plan to engage various marketing channels to expand our business to more merchants and customers. In order to attract more third-party merchants, we intend to waive platform user fees in the initial stage of platform operation. To enhance the awareness of our e-commerce platform, we intend to launch various advertising campaigns through a variety of media. We will join the offline e-commerce organizations, hold app promotion meetings and invite merchants to promote our brand image. In addition, we intend to provide various incentives to our customers to increase their spending and loyalty, and we will send online messages to our customers periodically with product recommendations or promotions.

We also intend to offer a personalized e-commerce experience to our customers by delivering targeted product recommendations based on customers’ browsing and purchase histories.

In addition to the online marketing activities, we will also utilize offline activities to attract more customers and promote our brand recognition. For example, according to customer purchasing behavior and preferences, we will divide them into different “communities” and organize parties, group tours and other social gatherings in which our registered merchants may act as sponsors by providing goods or services to the event. We may charge certain commission on products sold by our registered merchants in such activities.

Our Competition

The e-commerce industry in China is intensely competitive. The online commerce market is rapidly evolving and intensely competitive, and we expect the competition to intensify in the future. Our current or potential competitors include “Little Red Book (Xiao Hong Shu)” and “Foreign Port (Yang Ma Tou)”.

We anticipate that the e-commerce market will continually evolve and will continue to experience rapid technological change, evolving industry standards, shifting customer requirements, and frequent innovation. We must continually innovate to remain competitive. We believe that the principal competitive factors in our industry are:

| ● | brand recognition and reputation; | |

| ● | product quality and selection; | |

| ● | Convenience and pricing; | |

| ● | fulfillment capabilities; and | |

| ● | customer service. |

In respect of our offline adult products franchise business, this market is fast-growing in China. Our current or potential competitors in this segment include “Hefei Liangjiao” and “Beijing Juse Adult (www.X.com.cn).” We believe that we can compete in this market based on our superior business model and product sourcing.

Many of our current and potential competitors have longer operating histories, larger customer bases, greater brand recognition and significantly greater financial, marketing and other resources than us. In addition, online retailers may be acquired by, receive investments from or enter into other commercial relationships with larger, well-established and well-financed companies as use of the Internet and other online services increases. Some of our competitors may be able to secure merchandise from vendors on terms that are more favorable, devote greater resources to marketing and promotional campaigns, adopt more aggressive pricing or inventory availability policies and devote substantially more resources to website and systems development than our company. Increased competition may result in reduced operating margins, loss of market share and a diminished brand franchise. There can be no assurance that we will be able to compete successfully against current and future competitors, and competitive pressures faced by us may have a material adverse effect on our financial condition, operational results, business, and prospects. In addition, new and enhanced technologies may increase the competition in the online retail industry. New competitive business models may appear, for example based on new forms of social media or social commerce.

| 7 |

Our Intellectual Property

We believe that trademarks, copyrights, patents, domain names, know-how, proprietary technologies, and similar intellectual property will be critical to our success. We intend to rely on intellectual properties laws and confidentiality and non-compete agreements with our employees and others to protect our proprietary rights. Currently, we have three software copyright certificates relating to our “Ingtona e-commerce operating system V2.0.” We also have a registered domain name (www.Ingtona.com).

Regulation

Online commerce in China is subject to a number of laws and regulations. This section summarizes material PRC regulations relevant to our business and operations in China and the key provisions of such regulations.

Regulations Relating to Foreign Investment

Investment activities in the PRC by foreign investors are mainly governed by the Guidance Catalog of Industries for Foreign Investment (2017 revision), or the Catalog, which was promulgated jointly by the Ministry of Commerce and the National Development and Reform Commission on June 28, 2017 and entered into force on July 28, 2017. The Catalog divides industries into four categories in terms of foreign investment, which are “encouraged,” “restricted,” and “prohibited,” and all industries that are not listed under one of these categories are deemed to be “permitted.” Establishment of wholly foreign-owned enterprises is generally allowed in encouraged and permitted industries. Some restricted industries are limited to equity or contractual joint ventures, while in some cases Chinese partners are required to hold the majority interests in such joint ventures. In addition, foreign investment in restricted category projects is subject to government approvals. Foreign investors are not allowed to invest in industries in the prohibited category. Industries not listed in the Catalog are generally open to foreign investment unless specifically restricted by other PRC regulations.

In June 2019, MOFCOM and NDRC promulgated the Special Management Measures (Negative List) for the Access of Foreign Investment, or the Negative List, effective July 30, 2019. Foreign investment in value-added telecommunication business (excluding e-commerce business, domestic multi-party communications services, store and forward services and call center services) falls within the Negative List.

On March 15, 2019, the Standing Committee of the National People’s Congress enacted the Foreign Investment Law of PRC, which took effect on January 1, 2020, replacing the Law of the People’s Republic of China on China-Foreign Equity Joint Ventures, the Law of the People’s Republic of China on Wholly Foreign-Owned Enterprises, and the Law of the People’s Republic of China on China-Foreign Contractual Joint Ventures. On December 26, 2019, the Regulation on the Implementation of the Foreign Investment Law of the PRC, was issued by the State Council and came into force on January 1, 2020. According to the Foreign Investment Law, foreign investment shall enjoy pre-entry national treatment, except for those foreign invested entities that operate in industries deemed to be either “restricted” or “prohibited” in the “negative list.” Foreign invested entities operating in foreign “restricted” or “prohibited” industries require entry clearance and other approvals. However, the new law does not comment on the concept of “de facto control” or contractual arrangements with VIEs, although it has a catch-all provision under definition of “foreign investment” to include investments made by foreign investors in China through means stipulated by laws or administrative regulations or other methods prescribed by the State Council. Therefore, it still leaves leeway for future laws, administrative regulations or provisions to provide for contractual arrangements as a form of foreign investment. See “Risk Factors—Risks Relating to our Commercial Relationship with VIEs—Our contractual arrangement with VIEs may be affected by the newly enacted Foreign Investment Law.”

Regulations Relating to Value-Added Telecommunication Services

Among all of the applicable laws and regulations, the Telecommunication Regulations of the People’s Republic of China, or the Telecom Regulations, promulgated by the PRC State Council on September 25, 2000 and amended on July 29, 2014 and February 6, 2016, respectively, is the primary governing law, and sets out the general framework for the provision of telecommunications services by domestic PRC companies. Under the Telecom Regulations, telecommunications service providers are required to procure operating licenses prior to their commencement of operations. The Telecom Regulations distinguish “basic telecommunications services” from “value-added telecommunication services”. Value-added telecommunication services are defined as telecommunications and information services provided through public networks. The Telecom Catalogue was issued as an attachment to the Telecom Regulations to categorize telecommunications services as either basic or value-added. In February 2003 and December 2015, the Telecom Catalogue was updated, respectively, categorizing online data and transaction processing, information services, among others, as value-added telecommunication services.

| 8 |

The Administrative Measures on Telecommunications Business Operating License, promulgated by the Ministry of Industry and Information Technology in 2009 and amended in July 2017, which set forth more specific provisions regarding the types of licenses required to operate value-added telecommunication services, the qualifications and procedures for obtaining such licenses and the administration and supervision of such licenses. Under these regulations, a commercial operator of value-added telecommunication services must first obtain a license from the Ministry of Industry and Information Technology or its provincial level counterparts, otherwise such operator might be subject to sanctions including corrective orders and warnings from the competent administration authority, fines and confiscation of illegal gains and, in the case of significant infringements, the websites may be ordered to close.

In addition, the administration of mobile Internet application, or App, information services are strengthened through the Regulations for Administration of Mobile Internet Application Information Services, or the MIAIS Regulations, which became effective on August 1, 2016. The MIAIS Regulations were enacted to regulate App, App providers (including App owners or operators) and online App stores. Information service providers that utilize Apps are required to obtain relevant qualifications pursuant to PRC laws and regulations.

The MIAIS Regulations impose certain duties on App providers, including: (i) verifying real identities with the registered users through mobile phone numbers; (ii) establishing and improving the mechanism for user information security protection; (iii) establishing and improving the verification and management mechanism for the information content; adopting proper sanctions and measures relating to the release of illegal information content; (iv) protecting and safeguarding users’ “rights to know and rights to choose” during installation or use; (v) respecting and protecting intellectual property rights of others; and (vi) keeping records of user log information for 60 days.

Regulations Relating to E-Commerce

In May 2010, the State Administration of Industry and Commerce adopted the Interim Measures for the Administration of Online Commodities Trading and Relevant Services, which took effective in July 2010. Under these measures, enterprises or other operators which engage in online commodities trading and other services and have been registered with the State Administration of Industry and Commerce or its local branches must make the information stated in their business license available to the public or provide a link to their business license on their website. Online distributors must adopt measures to ensure safe online transactions, protect online shoppers’ rights and prevent the sale of counterfeit goods. Information on products and transactions released by online distributors must be authentic, accurate, complete and sufficient.

In January 2014, the State Administration of Industry and Commerce promulgated the Administrative Measures for Online Trading, which terminated the above interim measures and became effective in March 2014. The Administrative Measures for Online Trading further strengthen the protection of consumers and impose more stringent requirements and obligations on online business operators and third-party online marketplace operators. For example, online business operators are required to issue invoices to consumers for online products and services. Consumers are generally entitled to return products purchased from online business operators within seven days upon receipt, without giving any reason. Online business operators and third-party online marketplace operators are prohibited from collecting any information on consumers and business operators, or disclosing, selling or providing any such information to any third party, or sending commercial electronic messages to consumers, without their consent. Fictitious transactions, deletion of adverse comments and technical attacks on competitors’ websites are prohibited as well. In addition, third-party online marketplace operators are required to examine and verify the identifications of the online business operators and set up and keep relevant records for at least two years. Moreover, any third-party online marketplace operator that simultaneously engages in online trading for products and services should clearly distinguish itself from other online business operators on the marketplace platform.

In March 2016, the State Administration of Taxation, the Ministry of Finance and the General Administration of Customs jointly issued the Circular on Tax Policy for Cross-Border E-commerce Retail Imports, which took effect in April 2016. Pursuant to this circular, goods imported through the cross-border e-commerce retail are subject to tariff, import value-added tax, or VAT, and consumption tax based on the types of goods. Individuals purchasing any goods imported through cross-border e-commerce retail are taxpayers, and e-commerce companies, companies operating e-commerce transaction platforms or logistic companies are required to withhold the taxes.

| 9 |

On August 31, 2018, the Standing Committee of the National People’s Congress promulgated the E-Commerce Law, which became effective on January 1, 2019. Pursuant to the E-Commerce Law, an e-commerce platform operator shall (i) collect, verify and register the truthful information submitted by the merchants that apply to sell products or provide services on its platform, including the identities, addresses, contacts and licenses, establish registration archives and update such information on a regular basis; (ii) submit the identification information of the merchants on its platform to market regulatory administrative department as required and remind the merchants to complete the registration with market regulatory administrative department; (iii) submit identification information and tax-related information to tax authorities as required in accordance with the laws and regulations regarding the administration of tax collection and remind the individual merchants to complete the tax registration; (iv) record and retain the information of the products and information on its platform and the sales information for no less than 3 years; (v) display the platform service agreement and the transaction rules or links to such information on the homepage of the platform; (vi) display the noticeable labels regarding the products or services provided by the platform operator itself on its platform, and take liabilities for such products and services; (vii) establish a credit evaluation system, display the credit evaluation rules, provide consumers with accesses to make comments on the products and services provided on its platform, and restrain from deleting such comments; and (viii) establish intellectual property protection rules, and take necessary measures when any intellectual property holder notify the platform operator that his intellectual property rights have been infringed. An e-commerce platform operator shall take joint liabilities with the relevant merchants on its platform and may be subject to warnings and fines up to RMB2,000,000 where (i) it fails to take necessary measures when it knows or should have known that the products or services provided by the merchants on its platform do not meet the personal or property safety requirements or such merchants’ other acts may infringe on the lawful rights and interests of the consumers; or (ii) it fails to take necessary measures, such as deleting and blocking information, disconnecting, terminating transactions and services, when it knows or should have known that the merchants on its platform infringe any intellectual property rights of any other third party. With respect to products or services affecting the consumers’ life and health, if an e-commerce platform operator fails to verify the merchants’ qualification or fails to fulfill its obligations to safeguard the safety of consumers, which results in damages to the consumers, it shall take corresponding liabilities and may be subject to warnings and fines up to RMB2,000,000.

We are subject to these measures as a result of our online direct sales and online marketplace.

Regulations Relating to Internet Information Security

In 1997, the Ministry of Public Security promulgated measures that prohibit use of the internet in ways which, among other things, result in a leakage of state secrets or a spread of socially destabilizing content. If an internet information service provider violates these measures, the Ministry of Public Security and the local security bureaus may revoke its operating license and shut down its websites.

Internet information in China is regulated and restricted from a national security standpoint. The Standing Committee of the National People’s Congress has enacted the Decisions on Maintaining Internet Security on December 28, 2000 and further amended on August 27, 2009, which may subject violators to criminal punishment in China for any effort to: (i) gain improper entry into a computer or system of strategic importance; (ii) disseminate politically disruptive information; (iii) leak state secrets; (iv) spread false commercial information; or (v) infringe intellectual property rights.

The PRC Cybersecurity Law was promulgated by the Standing Committee of the National People’s Congress on November 7, 2016 and became effective on June 1, 2017. Under this regulation, network operators, including online lending information service providers, shall comply with laws and regulations and fulfill their obligations to safeguard security of the network when conducting business and providing services, and take all necessary measures pursuant to laws, regulations and compulsory national requirements to safeguard the safe and stable operation of the networks, respond to network security incidents effectively, prevent illegal and criminal activities, and maintain the integrity, confidentiality and usability of network data.

We have, in accordance with relevant provisions on network security of the PRC, established necessary mechanisms to protect information security, including, among others, adopting necessary network security protection technologies such as anti-virus firewalls, intrusion detection and data encryption, keeping record of network logs, and implementing information classification framework.

Regulations Relating to Privacy Protection

The Several Provisions on Regulating the Market Order of Internet Information Services, issued by the Ministry of Industry and Information Technology in December 2011, provide that, an internet information service provider may not collect any user personal information or provide any such information to third parties without the consent of a user. An internet information service provider must expressly inform the users of the method, content and purpose of the collection and processing of such user personal information and may only collect such information necessary for the provision of its services. An internet information service provider is also required to properly maintain the user personal information, and in case of any leak or likely leak of the user personal information, online lending service providers must take immediate remedial measures and, in severe circumstances, make an immediate report to the telecommunications regulatory authority.

| 10 |

In addition, pursuant to the Decision on Strengthening the Protection of Online Information issued by the Standing Committee of the National People’s Congress in December 2012 and the Order for the Protection of Telecommunication and Internet User Personal Information issued by the Ministry of Industry and Information Technology in July 2013, any collection and use of user personal information must be subject to the consent of the user, abide by the principles of legality, rationality and necessity and be within the specified purposes, methods and scopes.

The Guidelines jointly released by ten PRC regulatory agencies in July 2015 purport, among other things, to require service providers to improve technology security standards, and safeguard user and transaction information. The Guidelines also prohibit service providers from illegally selling or disclosing users’ personal information. Pursuant to the Ninth Amendment to the Criminal Law issued by the Standing Committee of the National People’s Congress in August 2015, which became effective in November 2015, any internet service provider that fails to fulfill the obligations related to internet information security administration as required by applicable laws and refuses to rectify upon orders is subject to criminal penalty for the result of (i) any dissemination of illegal information in large scale; (ii) any severe effect due to the leakage of the client’s information; (iii) any serious loss of criminal evidence; or (iv) other severe situation, and any individual or entity that (i) sells or provides personal information to others in a way violating the applicable law, or (ii) steals or illegally obtain any personal information is subject to criminal penalty in severe situation.

We plan to obtain consent from users to collect and use their personal information. While we plan to take measures to protect the personal information that we have access to, our security measures could be breached resulting in the leak of such confidential personal information. Security breaches or unauthorized access to confidential information could also expose us to liability related to the loss of the information, time-consuming and expensive litigation and negative publicity.

Regulations Relating to Advertising Business

The State Administration for Market Regulation is the government agency responsible for regulating advertising activities in the PRC. According to PRC laws and regulations, companies that engage in advertising activities must obtain a business license from the State Administration for Market Regulation or its local branches which specifically includes operating an advertising business within its business scope. The business license of an advertising company is valid for the duration of its existence, unless the license is suspended or revoked due to a violation of any relevant law or regulation. PRC advertising laws and regulations set forth certain content requirements for advertisements in the PRC including, among other things, prohibitions on false or misleading content, superlative wording, socially destabilizing content or content involving obscenities, superstition, violence, discrimination or infringement of the public interest. Advertisers, advertising agencies, and advertising distributors are required to ensure that the content of the advertisements they prepare or distribute is true and in full compliance with applicable law. In providing advertising services, advertising operators and advertising distributors must review the supporting documents provided by advertisers for advertisements and verify that the content of the advertisements complies with applicable PRC laws and regulations. Prior to distributing advertisements that are subject to government censorship and approval, advertising distributors are obligated to verify that such censorship has been performed and approval has been obtained. The release or delivery of advertisements through the internet must not impair the normal use of the network by users. The advertisements released in pop-up form on a webpage and other forms must show the close flag prominently and ensure one-click close. Violation of these regulations may result in penalties, including fines, confiscation of advertising income, orders to cease dissemination of the advertisements and orders to eliminate the effect of illegal advertisement. In circumstances involving serious violations, the State Administration for Market Regulation or its local branches may revoke the violators’ licenses or permits for their advertising business operations.

In July 2016, the State Administration of Industry and Commerce issued the Interim Measures for the Administration of Internet Advertising to regulate internet advertising activities. According to these measures, no advertisement of any medical treatment, medicines, food for special medical purpose, medical apparatuses, pesticides, veterinary medicines, dietary supplement or other special commodities or services subject to examination by an advertising examination authority as stipulated by laws and regulations may be published unless the advertisement has passed such examination. In addition, no entity or individual may publish any advertisement of over-the-counter medicines or tobacco on the internet. An internet advertisement must be identifiable and clearly identified as an “advertisement” to the consumers. Paid search advertisements are required to be clearly distinguished from natural search results. In addition, the following internet advertising activities are prohibited: providing or using any applications or hardware to intercept, filter, cover, fast forward or otherwise restrict any authorized advertisement of other persons; using network pathways, network equipment or applications to disrupt the normal data transmission of advertisements, alter or block authorized advertisements of other persons or load advertisements without authorization; or using fraudulent statistical data, transmission effect or matrices relating to online marketing performance to induce incorrect quotations, seek undue interests or harm the interests of others. Internet advertisement publishers are required to verify relevant supporting documents and check the content of the advertisement and are prohibited from publishing any advertisement with unverified content or without all the necessary qualifications. Internet information service providers that are not involved in internet advertising business activities but simply provide information services are required to block any attempt to publish an illegal advisement that they are aware of or should reasonably be aware of through their information services.

| 11 |

Regulations Relating to Intellectual Property

The Standing Committee of the National People’s Congress and the State Council have promulgated comprehensive laws and regulations to protect trademarks. The Trademark Law of the PRC (2013 revision) promulgated on August 23, 1982 and subsequently amended on February 22, 1993, October 27, 2001 and August 30, 2013, respectively, and the Implementation Regulation of the Trademark Law (2014 revision) issued by the State Council on August 3, 2002 and amended on April 29, 2014 are the main regulations protecting registered trademarks. The Trademark Office under the State Administration for Industry and Commerce administrates the registration of trademarks on a “first-to-file” basis, and grants a term of ten years to registered trademarks.

The PRC Copyright Law, adopted in 1990 and revised in 2001, 2010 respectively, with its implementation rules adopted on August 8, 2002 and revised in 2011 and 2013, respectively, and the Regulations for the Protection of Computer Software as promulgated on December 20, 2001 and amended in 2011 and 2013 provide protection for copyright of computer software in the PRC. Under these rules and regulations, software owners, licensees and transferees may register their rights in software with the National Copyright Administration Center or its local branches to obtain software copyright registration certificates. The term of protection for copyrighted software of legal persons is fifty years and ends on December 31 of the 50th year from the date of first publishing of the software.

The Ministry of Industry and Information Technology promulgated the Administrative Measures on Internet Domain Name on August 24, 2017 to protect domain names. According to these measures, domain name applicants are required to duly register their domain names with domain name registration service institutions. The applicants will become the holder of such domain names upon the completion of the registration procedure.

We have adopted necessary mechanisms to register, maintain and enforce intellectual property rights in China. However, we cannot assure you that we can prevent our intellectual property from all the unauthorized use by any third party, neither can we promise that none of our intellectual property rights would be challenged any third party.

Regulations Relating to Employment

The PRC Labor Law and the Labor Contract Law require that employers must execute written employment contracts with full-time employees. All employers must compensate their employees with wages equal to at least the local minimum wage standards. Violations of the PRC Labor Law and the Labor Contract Law may result in the imposition of fines and other administrative sanctions, and serious violations may constitute criminal offences.

On December 28, 2012, the PRC Labor Contract Law was amended with effect on July 1, 2013 to impose more stringent requirements on labor dispatch. Under such law, dispatched workers are entitled to pay equal to that of full-time employees for equal work, but the number of dispatched workers that an employer hires may not exceed a certain percentage of its total number of employees as determined by the Ministry of Human Resources and Social Security. Additionally, dispatched workers are only permitted to engage in temporary, auxiliary or substitute work. According to the Interim Provisions on Labor Dispatch promulgated by the Ministry of Human Resources and Social Security on January 24, 2014, which became effective on March 1, 2014, the number of dispatched workers hired by an employer shall not exceed 10% of the total number of its employees (including both directly hired employees and dispatched workers). The Interim Provisions on Labor Dispatch require employers not in compliance with the PRC Labor Contract Law in this regard to reduce the number of its dispatched workers to below 10% of the total number of its employees prior to March 1, 2016.

Enterprises in China are required by PRC laws and regulations to participate in certain employee benefit plans, including social insurance funds, namely a pension plan, a medical insurance plan, an unemployment insurance plan, a work-related injury insurance plan and a maternity insurance plan, and a housing provident fund, and contribute to the plans or funds in amounts equal to certain percentages of salaries, including bonuses and allowances, of the employees as specified by the local government from time to time at locations where they operate their businesses or where they are located. The enterprise may be ordered to pay the full amount within a deadline if it fails to make adequate contributions to various employee benefit plans and may be subject to fines and other administrative sanctions.

| 12 |

According to the Interim Regulations on the Collection and Payment of Social Insurance Premiums, the Regulations on Work Injury Insurance, the Regulations on Unemployment Insurance and the Trial Measures on Employee Maternity Insurance of Enterprises, enterprises in the PRC shall provide benefit plans for their employees, which include basic pension insurance, unemployment insurance, maternity insurance, work injury insurance and basic medical insurance. An enterprise must provide social insurance by making social insurance registration with local social insurance agencies, and shall pay or withhold relevant social insurance premiums for and on behalf of employees. The Law on Social Insurance of the PRC, which was promulgated by the SCNPC on October 28, 2010, became effective on July 1, 2011, and was most recently updated on December 29, 2018, has consolidated pertinent provisions for basic pension insurance, unemployment insurance, maternity insurance, work injury insurance and basic medical insurance, and has elaborated in detail the legal obligations and liabilities of employers who do not comply with laws and regulations on social insurance.

According to the Regulations on the Administration of Housing Provident Fund, which was promulgated by the State Counsel and became effective on April 3, 1999, and was amended on March 24, 2002 and was partially revised on March 24, 2019 by the Decision of the State Council on Revising Some Administrative Regulations (Decree No. 710 of the State Council), housing provident fund contributions by an individual employee and housing provident fund contributions by his or her employer shall belong to the individual employee. Registration by PRC companies with the applicable housing provident fund management center is compulsory, and a special housing provident fund account for each of the employees shall be opened at an entrusted bank.

The employer shall timely pay up and deposit housing provident fund contributions in full amount and late or insufficient payments of such contributions are unlawful. The employer shall make the housing provident fund payment and deposit registrations with the housing provident fund administration center. With respect to companies which violate the above regulations and fail to complete housing provident fund payment and deposit registrations or open housing provident fund accounts for their employees, such companies shall be ordered by the housing provident fund administration center to complete such procedures within a designated time limit. Those who fail to complete their registrations within the designated period shall be levied a fine ranging from RMB 10,000 to RMB 50,000. When companies breach these regulations and fail to pay housing provident fund contributions in full amount that are due, the housing provident fund administration center shall order such companies to pay up within a designated period, and may further petition a People’s Court for mandatory enforcement against those who still fail to comply after the expiry of such period.

Regulations Relating to Foreign Exchange

Under the PRC Foreign Currency Administration Rules promulgated on January 29, 1996 and last amended on August 5, 2008 and various regulations issued by the State Administration of Foreign Exchange and other relevant PRC government authorities, payment of current account items in foreign currencies, such as trade and service payments, payment of interest and dividends can be made without prior approval from the State Administration of Foreign Exchange by following the appropriate procedural requirements. By contrast, the conversion of RMB into foreign currencies and remittance of the converted foreign currency outside the PRC for the purpose of capital account items, such as direct equity investments, loans and repatriation of investment, requires prior approval from the State Administration of Foreign Exchange or its local office.

On February 13, 2015, the State Administration of Foreign Exchange promulgated the Circular on Simplifying and Improving the Foreign Currency Management Policy on Direct Investment, effective from June 1, 2015, which cancels the requirement for obtaining approvals of foreign exchange registration of foreign direct investment and overseas direct investment from the State Administration of Foreign Exchange. The application for the registration of foreign exchange for the purpose of foreign direct investment and overseas direct investment may be filed with qualified banks, which, under the supervision of the State Administration of Foreign Exchange, may review the application and process the registration.

| 13 |

The Circular of the State Administration of Foreign Exchange on Reforming the Management Approach regarding the Settlement of Foreign Capital of Foreign-invested Enterprise was promulgated on March 30, 2015 and became effective on June 1, 2015. According to this Circular, a foreign-invested enterprise may, according to its actual business needs, settle with a bank the portion of the foreign exchange capital in its capital account for which the relevant foreign exchange bureau has confirmed monetary contribution rights and interests (or for which the bank has registered the account-crediting of monetary contribution). For the time being, foreign-invested enterprises are allowed to settle 100% of their foreign exchange capitals on a discretionary basis; a foreign-invested enterprise shall truthfully use its capital for its own operational purposes within the scope of business; where an ordinary foreign-invested enterprise makes domestic equity investment with the amount of foreign exchanges settled, the invested enterprise shall first go through domestic re-investment registration and open a corresponding Account for Foreign Exchange Settlement Pending Payment with the foreign exchange bureau (bank) at the place of registration. The Circular of the State Administration of Foreign Exchange on Reforming and Regulating Policies on the Control over Foreign Exchange Settlement of Capital Accounts was promulgated and became effective on June 9, 2016. According to this Circular, enterprises registered in PRC may also convert their foreign debts from foreign currency into Renminbi on self-discretionary basis. This Circular provides an integrated standard for conversion of foreign exchange under capital account items (including but not limited to foreign currency capital and foreign debts) on self—discretionary basis, which applies to all enterprises registered in the PRC. This Circular reiterates the principle that Renminbi converted from foreign currency-denominated capital of a company may not be directly or indirectly used for purposes beyond its business scope and may not be used for investments in securities or other investment with the exception of bank financial products that can guarantee the principal within the PRC unless otherwise specifically provided. Besides, the converted Renminbi shall not be used to make loans for related enterprises unless it is within the business scope or to build or to purchase any real estate that is not for the enterprise own use with the exception for the real estate enterprise.

On January 26, 2017, the State Administration of Foreign Exchange promulgated the Circular on Further Improving Reform of Foreign Exchange Administration and Optimizing Genuineness and Compliance Verification, which stipulates several capital control measures with respect to the outbound remittance of profits from domestic entities to offshore entities, including (i) banks must check whether the transaction is genuine by reviewing board resolutions regarding profit distribution, original copies of tax filing records and audited financial statements, and (ii) domestic entities must retain income to account for previous years’ losses before remitting any profits. Moreover, pursuant to this Circular, domestic entities must explain in detail the sources of capital and how the capital will be used, and provide board resolutions, contracts and other proof as a part of the registration procedure for outbound investment.

On October 25, 2019, SAFE promulgated the Notice on Further Facilitating Cross-Board Trade and Investment, which became effective on the same date (except for Article 8.2 thereof). The notice removed restrictions on the capital equity investment in China by non-investment foreign-invested enterprises. In addition, restrictions on the use of funds for foreign exchange settlement of domestic accounts for the realization of assets have been removed and restrictions on the use and foreign exchange settlement of foreign investors’ security deposits have been relaxed. Eligible enterprises in the pilot areas are also allowed to use revenues under capital accounts, such as capital funds, foreign debts and overseas listing revenues for domestic payments without providing materials to the bank in advance for authenticity verification on an item by item basis, while the use of funds should be true, in compliance with applicable rules and conforming to the current capital revenue management regulations.

Regulations on Foreign Exchange Registration of Overseas Investment by PRC Residents

The State Administration of Foreign Exchange issued the Circular on Relevant Issues Relating to Domestic Resident’s Investment and Financing and Roundtrip Investment through Special Purpose Vehicles, or Circular 37, which became effective in July 2014, to replace the Circular of the State Administration of Foreign Exchange on Issues Concerning the Regulation of Foreign Exchange in Equity Finance and Roundtrip Investments by Domestic Residents through Offshore Special Purpose Vehicles, to regulate foreign exchange matters in relation to the use of special purpose vehicles by PRC residents or entities to seek offshore investment and financing or conduct round trip investment in China. Circular 37 defines a “special purpose vehicle” as an offshore entity established or controlled, directly or indirectly, by PRC residents or entities for the purpose of seeking offshore financing or making offshore investment, using legitimate onshore or offshore assets or interests, while “round trip investment” is defined as direct investment in China by PRC residents or entities through special purpose vehicles, namely, establishing foreign-invested enterprises to obtain the ownership, control rights and management rights. Circular 37 stipulates that, prior to making contributions into a special purpose vehicle, PRC residents or entities be required to complete foreign exchange registration with the State Administration of Foreign Exchange or its local branch. In addition, the State Administration of Foreign Exchange promulgated the Notice on Further Simplifying and Improving the Administration of the Foreign Exchange Concerning Direct Investment in February 2015, which amended Circular 37 and became effective on June 1, 2015, requiring PRC residents or entities to register with qualified banks rather than the State Administration of Foreign Exchange in connection with their establishment or control of an offshore entity established for the purpose of overseas investment or financing.

| 14 |

PRC residents or entities who had contributed legitimate onshore or offshore interests or assets to special purpose vehicles but had not obtained registration as required before the implementation of the Circular 37 must register their ownership interests or control in the special purpose vehicles with qualified banks. An amendment to the registration is required if there is a material change with respect to the special purpose vehicle registered, such as any change of basic information (including change of the PRC residents, name and operation term), increases or decreases in investment amount, transfers or exchanges of shares, and mergers or divisions. Failure to comply with the registration procedures set forth in Circular 37 and the subsequent notice, or making misrepresentation on or failure to disclose controllers of the foreign-invested enterprise that is established through round-trip investment, may result in restrictions being imposed on the foreign exchange activities of the relevant foreign-invested enterprise, including payment of dividends and other distributions, such as proceeds from any reduction in capital, share transfer or liquidation, to its offshore parent or affiliate, and the capital inflow from the offshore parent, and may also subject relevant PRC residents or entities to penalties under PRC foreign exchange administration regulations. See “Risk Factors—Risks Related to Doing Business in China—PRC regulations relating to investments in offshore companies by PRC residents may subject our PRC-resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary or limit our PRC subsidiary’s ability to increase their registered capital or distribute profits.”

Regulations on Dividend Distribution

Distribution of dividends of foreign investment enterprises are mainly governed by the Foreign Investment Enterprise Law, issued in 1986 and amended in 2000 and 2016, respectively, and the Implementation Rules under the Foreign Investment Enterprise Law, issued in 1990 and amended in 2001 and 2014, respectively. Under these regulations, foreign investment enterprises in the PRC may distribute dividends only out of their accumulative profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, no less than 10% of the accumulated profits of the foreign investment enterprises in the PRC are required to be allocated to fund certain reserve funds each year unless these reserves have reached 50% of the registered capital of the enterprises. A PRC company is not permitted to distribute any profits until any losses from previous fiscal years have been offset. Profits retained from prior fiscal years may be distributed together with distributable profits from the current fiscal year. Under our current corporate structure, our Cayman Islands holding company may rely on dividend payments from E-Home WFOE, which is a wholly foreign-owned enterprise incorporated in China, to fund any cash and financing requirements we may have. Limitation on the ability of our consolidated VIEs to make remittance to E-Home WFOE and on the ability of E-Home WFOE to pay dividends to us could limit our ability to access cash generated by the operations of those entities. See “Risk Factors—Risks Related to Doing Business in China—Restrictions under PRC law on our PRC subsidiaries’ ability to make dividends and other distributions could materially and adversely affect our ability to grow, make investments or acquisitions that could benefit our business, pay dividends to you, and otherwise fund and conduct our business.”

Regulations Relating to Overseas Listings

On August 8, 2006, six PRC regulatory agencies, including MOFCOM, the SASAC, the State Administration of Taxation, the SAIC, the CSRC and SAFE, jointly issued the Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, or the M&A Rules, which became effective on September 8, 2006 and was amended on June 22, 2009. The M&A Rules, among other things, require that (i) PRC entities or individuals obtain MOFCOM approval before they establish or control a SPV overseas, provided that they intend to use the SPV to acquire their equity interests in a PRC company at the consideration of newly issued share of the SPV, or Share Swap, and list their equity interests in the PRC company overseas by listing the SPV in an overseas market; (ii) the SPV obtains MOFCOM’s approval before it acquires the equity interests held by the PRC entities or PRC individual in the PRC company by Share Swap; and (iii) the SPV obtains CSRC approval before it lists overseas. See “Risk Factors—Risks Related to Doing Business in China—We may be unable to complete a business combination transaction efficiently or on favorable terms due to complicated merger and acquisition regulations which became effective on September 8, 2006.”

Regulations Relating to Taxation

Dividend Withholding Tax