Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Hilltop Holdings Inc. | tm2018923-1_8k.htm |

Exhibit 99.1

Hilltop Holdings Inc.

Investor Presentation

May 7, 2020

Preface

Corporate Headquarters Additional Information

6565 Hillcrest Ave Please Contact:

Dallas, TX 75205 Erik Yohe

Phone: 214-855-2177 Phone: 214-525-4634

www.hilltop-holdings.com Email: eyohe@hilltop-holdings.com

FORWARD-LOOKING STATEMENTS

This presentation and statements made by representatives of Hilltop Holdings Inc. (“Hilltop” or the “Company”) during the course of this presentation include “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements anticipated in such statements. Forward-looking statements speak only as of the date they are made and, except as required by law, we do not assume any duty to update forward-looking statements. Such forward-looking statements include, but are not limited to, statements concerning such things as our outlook, our business strategy, our financial condition, our efforts to make strategic acquisitions, our revenue, our liquidity and sources of funding, market trends, operations and business, taxes, the impact of natural disasters or public health emergencies, such as the current coronavirus (“COVID-19”) global pandemic, the pending sale of National Lloyds Corporation and regulatory approval thereof, information technology expenses, capital levels, mortgage servicing rights (“MSR”) assets, stock repurchases, dividend payments, expectations concerning mortgage loan origination volume, loan volume and interest rate compression, expected levels of refinancing as a percentage of total loan origination volume, projected losses on mortgage loans originated, loss estimates related to natural disasters, total expenses, anticipated changes in our revenue, earnings, or taxes, the effects of government regulation applicable to our operations, the appropriateness of, and changes in, our allowance for credit losses and provision for (reversal of) credit losses, including as a result of the “current expected credit losses” (CECL) model, anticipated investment yields, expected accretion of discount on loans in future periods, the collectability of loans, cybersecurity incidents, construction costs, cost savings expected from initiatives implemented and planned, including core system upgrades and cost reduction efforts, the outcome of litigation, and our other plans, objectives, strategies, expectations and intentions and other statements that are not statements of historical fact, and may be identified by words such as “anticipates,” “believes,” “building”, “could,” “estimates,” “expects,” “forecasts,” “goal,” “guidance”, “intends,” “may,” “might,” “outlook”, “plan,” “probable,” “projects,” “seeks,” “should,” “target,” “view” or “would” or the negative of these words and phrases or similar words or phrases. The following factors, among others, could cause actual results to differ from those set forth in the forward-looking statements: (i) changes in general economic, market and business conditions in areas or markets where we compete, including changes in the price of crude oil; (ii) the COVID-19 pandemic and the response of governmental authorities to the pandemic, which have caused and are causing significant harm to the global economy and our business; (iii) the credit risks of lending activities, including our ability to estimate credit losses and increases to the allowance for credit losses as a result of the implementation of CECL; (iv) the effects of changes in the level of, and trends in, loan delinquencies and write-offs; (v) changes in the interest rate environment; (vi) the failure of the National Lloyds Corporation sale transaction to close on the expected timeline or at all; (vii) the effect of the announcement of the National Lloyds Corporation transaction on agent or customer relationships and operating results; (viii) our ability to obtain regulatory approvals and meet other closing conditions to the sale of National Lloyds Corporation; (ix) risks associated with concentration in real estate related loans; (x) effectiveness of our data security controls in the face of cyber attacks; (xi) severe catastrophic events in Texas and other areas of the southern United States; (xii) the effects of our indebtedness on our ability to manage our business successfully, including the restrictions imposed by the indenture governing our indebtedness; (xiii) cost and availability of capital; (xiv) changes in state and federal laws, regulations or policies affecting one or more of our business segments, including changes in regulatory fees, deposit insurance premiums, capital requirements and the Dodd-Frank Wall Street Reform and Consumer Protection Act; (xv) changes in key management; (xvi) competition in our banking, broker-dealer, mortgage origination and insurance segments from other banks and financial institutions, as well as investment banking and financial advisory firms, mortgage bankers, asset-based non-bank lenders, government agencies and insurance companies; (xvii) legal and regulatory proceedings; (xviii) failure of our insurance segment reinsurers to pay obligations under reinsurance contracts; (xix) risks associated with merger and acquisition integration; and (xx) our ability to use excess capital in an effective manner. For further discussion of such factors, see the risk factors described in our most recent Annual Report on Form 10-K, and subsequent Quarterly Reports on Form 10-Q and other reports, that we have filed with the Securities and Exchange Commission. All forward-looking statements are qualified in their entirety by this cautionary statement.

The information contained herein is preliminary and based on Company data available at the time of the earnings presentation. It speaks only as of the particular date or dates included in the accompanying slides. Hilltop Holdings does not undertake an obligation to, and disclaims any duty to, update any of the information herein.

Company Overview

Hilltop Holdings– Overview

• Hilltop Holdings is a Dallas, Texas-based diversified financial holding company with a complementary set of operating companies

• Hilltop Holdings Inc. ranked No. 35 on Forbes’ best banks listing of the Top 100 largest publicly traded banks and thrifts(1)

• Hilltop provides banking, mortgage origination, financial advisory and insurance through its subsidiaries:

• PlainsCapital Bank is a commercial bank that is the 5th largest(2) Texas-based bank with 61 locations across the state

ummary Organizational Structure

• PrimeLending is a residential mortgage originator with a 97%

customer satisfaction rating(3) and approximately 1,250 loan

officers in branches across the nation

• HilltopSecurities is a full-service brokerage firm focused on public

entities and has served as financial advisor on more municipal

bond and note transactions in the past decade than any other firm,

ranking No. 1 nationally for the 10-year period ending December

31, 2019(4); it is also the 3rd largest clearing firm(5)

FY 2019 Pre-Tax Income by Segment ($MM)(6)

• National Lloyds is a niche insurance company that provides

primarily fire and homeowners insurance for low value dwellings in

$90 $17

$300

Texas and other southern states

• Hilltop announced the sale of National Lloyds to Align

Financial Holdings, LLC on Jan. 31, 2020; the transaction is

expected to close in the second quarter of 2020, subject to

customary closing conditions, including required regulatory

approval(7)

• Hilltop’s operating subsidiaries are well positioned in their respective

markets and collectively generate strong and diversified earnings and

capital

$65 ($54)

$182

Notes:

(1)Per Forbes; based on regulatory filings for the period ending Sept. 30, 2019

(2)Per SNL Financial; based on 2019 Texas deposit market share and pro forma for pending acquisitions in Texas

(3)Survey administered and managed by an independent 3rd party following loan closing. 97% refers to rating customers give loan officers

(4)Per Ipreo MuniAnalytics; based on number of issues for the 10-year period ending Dec. 31, 2019

(5)Per Investment News; based on reported number of broker-dealer clients as of Aug. 17, 2019

(6)The sum of the period amounts may not equal the total amounts due to rounding

(7) Insurance segment results have been presented as discontinued operations starting in Q1 2020 and its assets and liabilities have been classified as held for sale for all periods presented

Hilltop Holdings – Timeline

2004 2005 2006 2007

Operated as Affordable Gerald J. Ford invested Announced the Company sold all assets

of manufactured home

Residential in ARC and joined the acquisition of

communities business

Communities (“ARC”) Board of Directors National Lloyds

(ARC) for $1.8 billion,

and completed IPO on Corporation

resulting in net cash

NYSE (completed in 2007)

balance of $550 million

2011 2012 2013 2015

Hilltop made a $50 Acquired Completed purchase Completed acquisition

and assumption

million investment in PlainsCapital of SWS Group, Inc.

transaction of First

SWS Group, Inc. Corporation for for ~$350 million

National Bank,

~$700 million

Edinburg, Texas from

FDIC, as receiver

2007

Changed name to Hilltop Holdings and began pursuit of bank acquisitions, including five FDIC failures

2018

Completed acquisition of The Bank of River Oaks for $85 million

2020

Announced the sale of

National Lloyds Corporation to Align Financial Holdings for $150 million(1)

Key Statistics at March 31, 2020

Total Assets ($B) $15.7

Common Equity ($B) $2.1

Employees ~4,850

Locations ~420

Note:

(1) Subject to post-closing adjustments

• After selling ARC’s assets in 2007, Hilltop had net cash of $550 million and pursued several bank acquisitions

• In November 2012, Hilltop made the transformational acquisition of PlainsCapital Corporation, while maintaining its leadership and structure

• In September 2013, Hilltop expanded its Texas banking footprint via the FDIC-assisted transaction of First National Bank

• On January 1, 2015, Hilltop closed its acquisition of SWS Group, which enhanced PlainsCapital Bank and brought together two storied broker-dealers to create a leading regional broker-dealer based in Texas

• On August 1, 2018, Hilltop completed its acquisition of The Bank of River Oaks, which substantially grew its banking presence in the Houston market

• On January 31, 2020, Hilltop announced the sale of National Lloyds Corporation to Align Financial Holdings, LLC, for $150 million(1). The transaction is expected to close in the second quarter of 2020, subject to customary closing conditions, including required regulatory approvals

• Hilltop continues to build a premier Texas-based bank and diversified financial services holding company through organic growth and acquisitions

Hilltop Holdings – Leadership

• Gerald J. Ford, Hilltop’s Chairman and largest shareholder, has successfully acquired, managed and sold banks and other financial institutions for the past 45 years

• Our senior management teams have complimentary expertise in management and acquisitions

• Hilltop Holdings

Gerald J. Ford

Chairman of the Board and Largest Shareholder

• Company Tenure: 15 years

• Financial Services Experience: 45 years

Jeremy B. Ford

President & CEO, HTH

• Company Tenure: 10 years

• Financial Services Experience: 23 years

William B. Furr

Chief Financial Officer, HTH

• Company Tenure: 4 years

• Financial Services Experience: 19 years

Darren E. Parmenter

Chief Administrative Officer, HTH

• Company Tenure: 20 years

• Financial Services Experience: 20 years

Corey G. Prestidge

General Counsel, HTH

• Company Tenure: 12 years

• Financial Services Experience: 15 years

• Subsidiary CEOs

Jerry L. Schaffner Steve Thompson Brad Winges Darren E. Parmenter

President & CEO President & CEO President & CEO President & CEO National

PlainsCapital Bank PrimeLending HilltopSecurities Lloyds Corporation

• Company Tenure: 32 • Company Tenure: 9 • Company Tenure: 1 • Company Tenure: 20

years years year years

• Financial Services • Financial Services • Financial Services • Financial Services

Experience: 38 years Experience: 33years Experience: 31 years Experience: 20 years

Hilltop Holdings – Historical Profitability

Return on Average Assets (ROAA) History

2013 - Q1 2020 Average ROAA: 1.37%

Note: 2017 includes estimated non-cash, non-recurring charges to Hilltop consolidated and banking segment results of $28.4 million and $25.7 million, respectively, primarily attributable to the revaluation of deferred tax assets as a result of the enactment of the Tax Cuts and Jobs Act of 2017 (“the Tax Legislation”). Deferred tax asset amounts recorded in December 2017 following enactment of the Tax Legislation were final as of September 30, 2018.

Hilltop Holdings & PlainsCapital Bank – Capital Ratios

Tier 1 Leverage Ratio

Tier 1 Capital Ratio

Common Equity Tier 1 Ratio

Total Capital Ratio

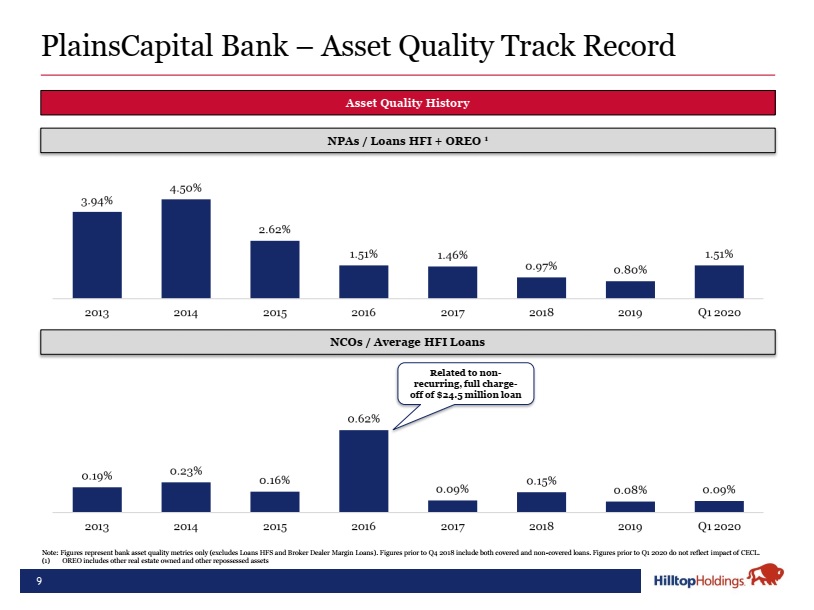

PlainsCapital Bank – Asset Quality Track Record

Asset Quality History

NPAs / Loans HFI + OREO 1

NCOs / Average HFI Loans

Related to non-recurring, full charge-off of $24.5 million loan

Note: Figures represent bank asset quality metrics only (excludes Loans HFS and Broker Dealer Margin Loans). Figures prior to Q4 2018 include both covered and non-covered loans. Figures prior to Q1 2020 do not reflect impact of CECL.

(1) OREO includes other real estate owned and other repossessed assets

COVID-19 Update

COVID-19 Response and Business Continuity

Employee

Benefits & Health

•COVID-19 testing 100% covered under employee benefits plan

• All employees continue to be paid regardless of ability to work from home

• Social distancing and no face to face meetings in offices

• Tracking COVID-19 cases and quarantining for employees

• 10 confirmed cases where employees have tested positive for COVID-19 out of ~4,850 employees

Charitable Giving

•$300,000 gift to the

Baylor Scott & White’s “Employees 1st Emergency Assistance Fund”

•$50,000 in donations to food banks across the U.S.

•Together with 19 other Lubbock banks, donated a total of $343,000 to the South Plains COVID-19 Response Fund

• Over $200,000 donated nationwide through local donations in each PrimeLending market

Remote Work

•>75% of Hilltop Holdings, HilltopSecurities, National Lloyds and PrimeLending employees working remotely

•>40% of PlainsCapital

Bank employees working remotely (essential jobs remain at offices and branches)

•Rotating employees in offices where possible (Accounts Payable, Security, IT support, etc.)

Cost and Capital

Management

• Slowed recruiting and hiring outside of certain key needs

• Reviewing overall demand and operational activity trends

• Suspension of share repurchase program

• Suspension of mortgage retention program at PlainsCapital Bank

Delivering Support To Our Impacted Banking Clients

COVID-19 Modified Loan Summary Paycheck Protection Program (PPP)

• Partnering with borrowers that have been impacted by COVID-19

• Approximately $775 million of loan modification (up to 90 days) requests in process as of April 23, 2020

• Completed principal only deferrals of approximately $219 million

• Completed principal and interest deferrals of approximately $34 million

• Remaining modifications are approved but not completed, under review, or in the pipeline to be reviewed

• All deferral requests, regardless of size, now require at least a senior credit officer approval

• PlainsCapital Bank, an SBA preferred lender, is dedicated to providing relief to small businesses in our communities

• Initial PPP effort focused on serving existing PCB clients

• Started taking PPP applications on April 3, 2020

$777 million in PPP ~3,100 applications

loans requested for PPP loans

$585 million funded 2,070 processed

through 4/23 through 4/23

PPP Funded Loan Statistics

• Average loan amount: $282k

• 1,682 loans < $350k

• 345 loans $350k to $2 million

• 45 loans > $2 million

Additional Support

Personal Banking and Loan Assistance

• Waived fees including: overdraft fees, late fees on consumer loan payments, non-PCB ATM fees, telephone transfer fee, stop payment fees, excess bill pay fees, and CD early withdrawal fees

• Increased daily spending limits on debit card products

• Suspended residential foreclosure activity

Recent Results & Operational

Highlights

Investor Highlights – Q1 2020

HTH Consolidated1

Continuing Operations

Net Income

$$4928..61MM

$ 46.5 MM

Diversified

Growth

EPS – Diluted ROAA ROAE

$ 0.5530 01.86%47% 95.76%38%

$ 0.51 1.41% 9.30%

• Mortgage origination volume of $3.6 billion in Q1 2020 grew by $1.2 billion, or 48%, compared to the same quarter in the prior year as rates declined

• Average loans2 grew by $378 million, or 6%, driven by National Warehouse Lending and average deposits grew by $650 million, or 8%, compared to first quarter 2019

• The Broker-Dealer segment reported a pre-tax margin of 18.3% compared to 15.8% during the first quarter 2019 as Fixed Income and Wealth Management businesses partially offset a decline in Structured Finance revenues

Value

Creation

and

Capital

Optimization

Managed

Risk

• In Q1 2020, Hilltop paid $8.2 million in stockholder dividends and returned $15 million through share repurchases

• Book value per share at March 31, 2020 grew by 12% versus March 31, 2019 to $23.71, and tangible book value per share3 increased 12% during the same period to $20.16 (HTH Consolidated)

• Hilltop maintained strong capital levels with a Tier 1 Leverage Ratio4 of 13.03% and a Common Equity Tier 1 Capital Ratio of 15.96% at March 31, 2020

• Net charge-offs in Q1 2020 equated to $1.5 million, or 9 basis points of average loans HFI

• Allowance for credit losses of $106.7 million at March 31, 2020, an increase in the reserve balance of $33.0 million from January 1, 2020 Day 1 balance

• Significant liquidity and access to secured funding sources with approximately $4.7 billion of cash, securities and secured borrowing capacity

Discontinued Operations ($ millions, except per share) Pre-tax Net Income EPS – Diluted ($)

National Lloyds Corporation $4.0 $3.2 $0.04

Notes:

(1) HTH Consolidated defined as continuing and discontinued operations.

(2) Loans reflect loans held for investment (HFI) excluding broker-dealer loans.

(3) For a reconciliation of tangible book value per share to book value per share see management’s explanation of Non-GAAP Financial Measures in Appendix.

(4) Based on the period Tier 1 capital divided by total average assets during the quarter, excluding goodwill and intangible assets..

Business Results – Q1 2020

Pre-Tax Income vs. Prior Year ($ in millions)

Business Drivers for1Q120192020

• Banking pre-tax income of $11.5 million declined by approximately $30.1 million from Q1 2019 as the first CECL-impacted provision expense equated to $34.3 million. Partially offsetting the provision expense was increased net interest income from higher asset balances and lower noninterest expenses, specifically lower professional services and occupancy expenses.

• Mortgage pre-tax income of $39.8 million was driven by higher origination volumes, which increased 48% compared to Q1 2019. Gain on sale margins declined modestly to 325 basis points, from 330 basis points in Q1 2019.

• Broker-Dealer pre-tax income increased by $1.8 million to $18.2 million compared to Q1 2019. The increase was driven by growth in Capital Markets and Retail offset by a negative mark-to-market adjustment on the Structured Finance mortgage pipeline.

• Insurance pre-tax income decline of $2.8 million compared to Q1 2019 was primarily attributable to a decline in the investment portfolio during the quarter. This decline was partially offset by lower losses and loss adjustment expenses. The loss and LAE ratio for the period was 39.7%, compared to 45.0% in Q1 2019.

Note: The sum of the period amounts may not equal the total amounts due to rounding.

(1) HTH Consolidated defined as continuing and discontinued operations.

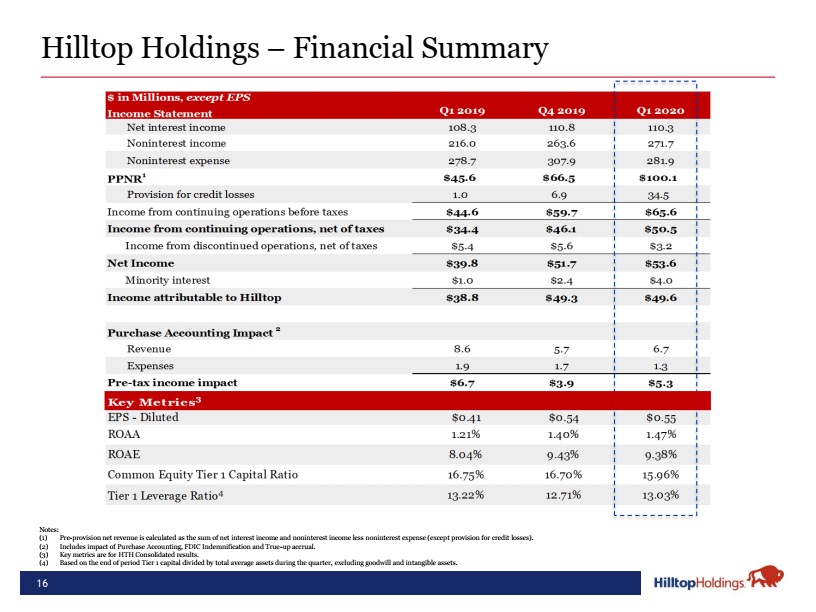

Hilltop Holdings – Financial Summary

Notes:

(1) Pre-provision net revenue is calculated as the sum of net interest income and noninterest income less noninterest expense (except provision for credit losses).

(2) Includes impact of Purchase Accounting, FDIC Indemnification and True-up accrual.

(3) Key metrics are for HTH Consolidated results.

(4) Based on the end of period Tier 1 capital divided by total average assets during the quarter, excluding goodwill and intangible assets.

CECL – Reserve Build on Loans HFI

CECL Loans HFI Rollforward 12/31/19 to 3/31/20

$16.9

3/31 Reserve Composition

$17.6

CRE 53.9

$12.6 C&I 38.6

($1.5)

Construction 6.4

$106.7 1-4 SFR 6.4

Consumer 1.2

$61.1 $73.7 Broker Dealer 0.3

Total $106.7

12/31/2019 CECL Adoption 1/1/2020Net Charge-Offs Specific Economic 3/31/2020

Impact Reserves Factors

During Q1 2020, Total Allowance for Credit Losses (ACL) on Loans HFI increased to $106.7 million

• PCB/HTS reserves on individually evaluated loans increased $17.6 million during Q1 2020

• Reserves on collectively evaluated loans increased due to the inclusion of the expected lifetime credit losses under CECL attributable to the deteriorating economic outlook compared to Day 1

• No reserves were required on the HFS/HTM securities portfolios during Q1 2020

• In recent weeks, market economic estimates have deteriorated to reflect information regarding unemployment and potential GDP declines given the impact of COVID–19

• Further deterioration from March 31 assumptions in the economic outlook may require additional credit reserves in future quarters

Hilltop Holdings – Net Interest Income & Margin

Average Earning Assets and NIM Trends

($ in billions)

3.66%

3.47% 3.43% 3.39%

3.27%

$12.9 $13.2 $12.9

$12.3

$11.8

Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020

Average Earning Assets (Gross) NIM continuing operations

Note: Figures reflect continuing operations

Net Interest Income Highlights

• Net interest income of $110.3 million increased $2.0 million, or 2%, from Q1 2019

• Q1 2020 loan accretion equated to $6.6 million, a decline of $2.0 million versus Q1 2019

• NIM expanded versus Q4 2019 as loan yields declined less than deposit yields during Q1 2020

• Loans HFI yield declined 6 basis points and Loans HFS declined 13 basis points from Q4 2019 t0 Q1 2020

• Q1 2020 interest bearing deposit costs decreased 17 basis points versus Q4 2019 to 0.97%

• Total HTH interest bearing deposit betas approximately 28% since July 2019

• Average Loans HFS increased by $605 million from Q1 2019 to $1.6B

• Average Loans HFS yielded 3.86% during Q1

2020

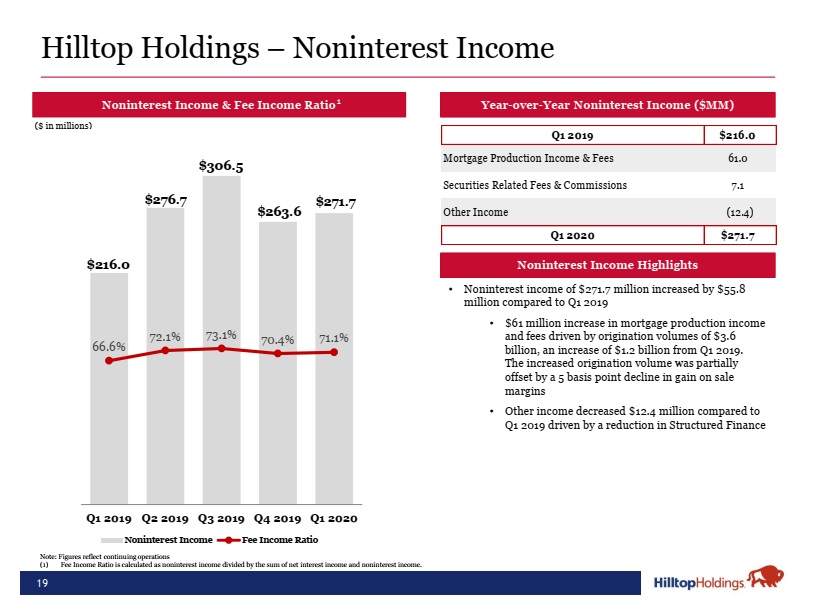

Hilltop Holdings – Noninterest Income

Noninterest Income & Fee Income Ratio1

($ in millions)

$306.5

$276.7 $271.7

$263.6

$216.0

Year-over-Year Noninterest Income ($MM)

Q1 2019 $216.0

Mortgage Production Income & Fees 61.0

Securities Related Fees & Commissions 7.1

Other Income (12.4)

Q1 2020 $271.7

Noninterest Income Highlights

66.6%

72.1% 73.1% 70.4% 71.1%

• Noninterest income of $271.7 million increased by $55.8 million compared to Q1 2019

• $61 million increase in mortgage production income and fees driven by origination volumes of $3.6 billion, an increase of $1.2 billion from Q1 2019. The increased origination volume was partially offset by a 5 basis point decline in gain on sale margins

• Other income decreased $12.4 million compared to Q1 2019 driven by a reduction in Structured Finance

Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020

Noninterest Income Fee Income Ratio

Note: Figures reflect continuing operations

Hilltop Holdings – Noninterest Expenses

oninterest Expenses and Efficiency Ratio1

($ in millions)

Selected Noninterest Expense Items Q1 2020

($ in millions)

Core system improvements $1.9

Year-over-Year Noninterest Expense ($MM)

Q1 2019 $278.7

Compensation and Benefits 9.7

Occupancy and Equipment (8.3)

Professional Services 0.7

Other Expenses 1.1

Q1 2020 $281.9

Noninterest Expense Highlights

• Total compensation increased by $9.7 million from Q1 2019 primarily driven by increased variable compensation related to higher mortgage volumes, partially offset by one-time leadership transition charges in Q1 2019

• Variable compensation increased by $16.8 million, in-line with higher mortgage origination volumes offset by lower variable compensation at HilltopSecurities

• Occupancy and Equipment expenses declined $8.3 million primarily driven by a gain on the sale of a corporate aircraft and additional cost reductions from consolidation efforts related to utilities and maintenance services

• Other expenses reflect an increase in the reserve for unfunded loan commitments of $1.3 million related to the deteriorating market conditions caused by COVID-19 during Q1 2020

Note: Figures reflect continuing operations

(1) Efficiency Ratio is calculated as noninterest expense divided by the sum of net interest income and noninterest income.

Hilltop Holdings – Loans

Loan Mix and Yield

($ in billions, ending and average balances)

Notes:

The sum of the period amounts may not equal the total amounts due to rounding.

(1) Annualized Gross Loan HFI Yield contains purchased loan portfolio.