Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SOUTH STATE Corp | tm2018796-1_8k.htm |

Exhibit 99.1

1 D.A. Davidson 22 nd Annual Financial Institutions Virtual Conference Thursday, May 7, 2020

2 Forward Looking Statements Cautionary Statement Regarding Forward Looking Statements Statements included in this communication, which are not historical in nature are intended to be, and are hereby identified as, forward looking statements for purposes of the safe harbor provided by Section 27 A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934 . Forward looking statements are based on, among other things, management’s beliefs, assumptions, current expectations, estimates and projections about the financial services industry, the economy and South State . Words and phrases such as “may,” “approximately,” “continue,” “should,” “expects,” “projects,” “anticipates,” “is likely,” “look ahead,” “look forward,” “believes,” “will,” “intends,” “estimates,” “strategy,” “plan,” “could,” “potential,” “possible” and variations of such words and similar expressions are intended to identify such forward - looking statements . South State cautions readers that forward looking statements are subject to certain risks, uncertainties and assumptions that are difficult to predict with regard to, among other things, timing, extent, likelihood and degree of occurrence, which could cause actual results to differ materially from anticipated results . Such risks, uncertainties and assumptions, include, among others, the following : ( 1 ) economic downturn risk, potentially resulting in deterioration in the credit markets, greater than expected noninterest expenses, excessive loan losses and other negative consequences, which risks could be exacerbated by potential negative economic developments resulting from federal spending cuts and/or one or more federal budget - related impasses or actions ; ( 2 ) increased expenses, loss of revenues, and increased regulatory scrutiny associated with our total assets having exceeded $ 10 . 0 billion ; ( 3 ) controls and procedures risk, including the potential failure or circumvention of our controls and procedures or failure to comply with regulations related to controls and procedures ; ( 4 ) ownership dilution risk associated with potential acquisitions in which South State’s stock may be issued as consideration for an acquired company ; ( 5 ) potential deterioration in real estate values ; ( 6 ) the impact of competition with other financial institutions, including pricing pressures (including those resulting from the Tax Cuts and Jobs Act) and the resulting impact, including as a result of compression to net interest margin ; ( 7 ) credit risks associated with an obligor’s failure to meet the terms of any contract with the bank or otherwise fail to perform as agreed under the terms of any loan - related document ; ( 8 ) interest risk involving the effect of a change in interest rates on the bank’s earnings, the market value of the bank’s loan and securities portfolios, and the market value of South State’s equity ; ( 9 ) liquidity risk affecting the bank’s ability to meet its obligations when they come due ; ( 10 ) risks associated with an anticipated increase in South State’s investment securities portfolio, including risks associated with acquiring and holding investment securities or potentially determining that the amount of investment securities South State desires to acquire are not available on terms acceptable to South State ; ( 11 ) price risk focusing on changes in market factors that may affect the value of traded instruments in “mark - to - market” portfolios ; ( 12 ) transaction risk arising from problems with service or product delivery ; ( 13 ) compliance risk involving risk to earnings or capital resulting from violations of or nonconformance with laws, rules, regulations, prescribed practices, or ethical standards ; ( 14 ) regulatory change risk resulting from new laws, rules, regulations, accounting principles, proscribed practices or ethical standards, including, without limitation, the possibility that regulatory agencies may require higher levels of capital above the current regulatory - mandated minimums and including the impact of the recently enacted Tax Cuts and Jobs Act, the Consumer Financial Protection Bureau rules and regulations, and the possibility of changes in accounting standards, policies, principles and practices, including changes in accounting principles relating to loan loss recognition (CECL) ; ( 15 ) strategic risk resulting from adverse business decisions or improper implementation of business decisions ; ( 16 ) reputation risk that adversely affects earnings or capital arising from negative public opinion ; ( 17 ) terrorist activities risk that results in loss of consumer confidence and economic disruptions ; ( 18 ) cybersecurity risk related to the dependence of South State on internal computer systems and the technology of outside service providers, as well as the potential impacts of third party security breaches, subjects each company to potential business disruptions or financial losses resulting from deliberate attacks or unintentional events ; ( 19 ) greater than expected noninterest expenses ; ( 20 ) noninterest income risk resulting from the effect of regulations that prohibit financial institutions from charging consumer fees for paying overdrafts on ATM and one - time debit card transactions, unless the consumer consents or opts - in to the overdraft service for those types of transactions ; ( 21 ) excessive loan losses ; ( 22 ) failure to realize synergies and other financial benefits from, and to limit liabilities associated with, mergers and acquisitions within the expected time frame ; ( 23 ) potential deposit attrition, higher than expected costs, customer loss and business disruption associated with merger and acquisition integration, including, without limitation, and potential difficulties in maintaining relationships with key personnel ; ( 24 ) the risks of fluctuations in market prices for South State common stock that may or may not reflect economic condition or performance of South State ; ( 25 ) the payment of dividends on South State common stock is subject to regulatory supervision as well as the discretion of the board of directors of South State, South State’s performance and other factors ; ( 26 ) operational, technological, cultural, regulatory, legal, credit and other risks associated with the exploration, consummation and integration of potential future acquisition, whether involving stock or cash consideration ; ( 27 ) major catastrophes such as earthquakes, floods or other natural or human disasters, including infectious disease outbreaks, including the recent outbreak of a novel strain of coronavirus, a respiratory illness, the related disruption to local, regional and global economic activity and financial markets, and the impact that any of the foregoing may have on South State and its customers and other constituencies ; and ( 28 ) risks related to the proposed merger of South State and CenterState Bank Corporation (“CenterState”), including, among others, (i) the risk that the cost savings and any revenue synergies from the merger may not be fully realized or may take longer than anticipated to be realized, (ii) disruption to the parties’ businesses as a result of the announcement and pendency of the merger, (iii) the occurrence of any event, change or other circumstances that could give rise to the termination of the merger agreement between CenterState and South State, (iv) the risk that the integration of each party’s operations will be materially delayed or will be more costly or difficult than expected or that the parties are otherwise unable to successfully integrate each party’s businesses into the other’s businesses, (v) the failure to obtain the necessary approvals by the shareholders of South State or CenterState, (vi) the amount of the costs, fees, expenses and charges related to the merger, (vii) the ability of each of South State and CenterState to obtain required governmental approvals of the merger (and the risk that such approvals may result in the imposition of conditions that could adversely affect the combined company or the expected benefits of the transaction), (viii) reputational risk and the reaction of each company's customers, suppliers, employees or other business partners to the merger, (ix) the failure of the closing conditions in the merger agreement to be satisfied, or any unexpected delay in closing the merger, (x) the possibility that the merger may be more expensive to complete than anticipated, including as a result of unexpected factors or events, (xi) the dilution caused by South State’s issuance of additional shares of its common stock in the merger and (xii) other factors that may affect future results of South State and CenterState, as disclosed in South State’s registration statement on Form S - 4 , as amended, Annual Report on Form 10 - K, as amended, Quarterly Reports on Form 10 - Q, and Current Reports on Form 8 - K, and CenterState’s Annual Report on Form 10 - K, Quarterly Reports on Form 10 - Q, and Current Reports on Form 8 - K, in each case filed by South State or CenterState, as applicable, with the U . S . Securities and Exchange Commission (“SEC”) and available on the SEC’s website at http : //www . sec . gov, any of which could cause actual results to differ materially from future results expressed, implied or otherwise anticipated by such forward - looking statements . All forward - looking statements speak only as of the date they are made and are based on information available at that time . South State does not undertake any obligation to update or otherwise revise any forward - looking statements, whether as a result of new information, future events, or otherwise, except as required by federal securities laws . As forward - looking statements involve significant risks and uncertainties, caution should be exercised against placing undue reliance on such statements .

3 COVID - 19 Response Team • Expanded insurance coverage for testing and treatment of COVID - 19 • Increased paid leave for team members unable to work due to lack of child or dependent care • Paid leave for team members under quarantine due to COVID - 19 exposure • Additional compensation for team members with essential in - office jobs Customers • Expanded communication through digital channels (online, mobile, app) to adjust to reduced branch interaction • Record usage of Digital channels with no service interruption • 65% increase in Mobile Deposits • 30% increase in Consumer Loan Applications • 40% increase in Bank to Bank transfers

4 COVID - 19 Impact Virginia Shelter in Place until 5/14 7 of 7 branches Open North Carolina Shelter in Place until 5/8 24 of 24 branches open Georgia Shelter in Place cancelled; limited business restrictions 30 of 31 branches open South Carolina Shelter in Place cancelled; limited business restrictions 92 of 93 branches open • Branches limited to drive - through beginning 3/19 • ~80% of Employees working from home Data as of 5/5/20. State information from state government websites.

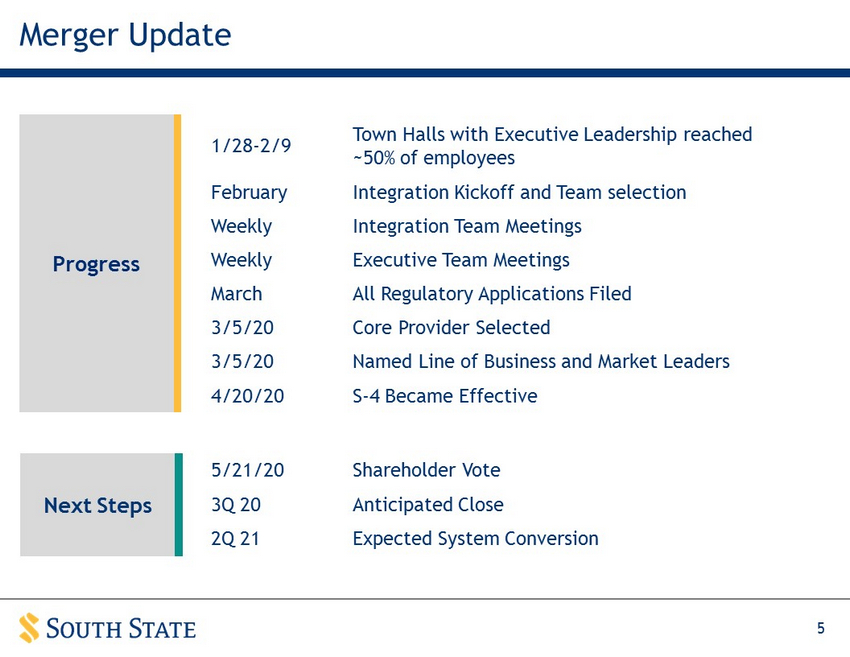

5 Merger Update Progress Next Steps 1/28 - 2/9 Town Halls with Executive Leadership reached ~50% of employees February Integration Kickoff and Team selection Weekly Integration Team Meetings Weekly Executive Team Meetings March All Regulatory Applications Filed 3/5/20 Core Provider Selected 3/5/20 Named Line of Business and Market Leaders 4/20/20 S - 4 Became Effective 5/21/20 Shareholder Vote 3Q 20 Anticipated Close 2Q 21 Expected System Conversion

6 Credit Update

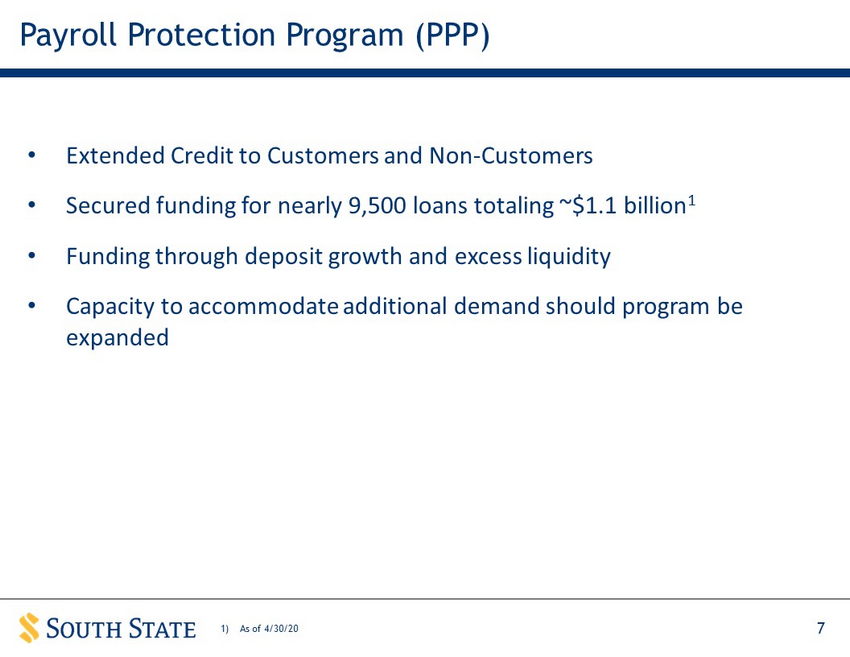

7 Payroll Protection Program (PPP) • Extended Credit to Customers and Non - Customers • Secured funding for nearly 9,500 loans totaling ~$1.1 billion 1 • Funding through deposit growth and excess liquidity • Capacity to accommodate additional demand should program be expanded 1) As of 4/30/20

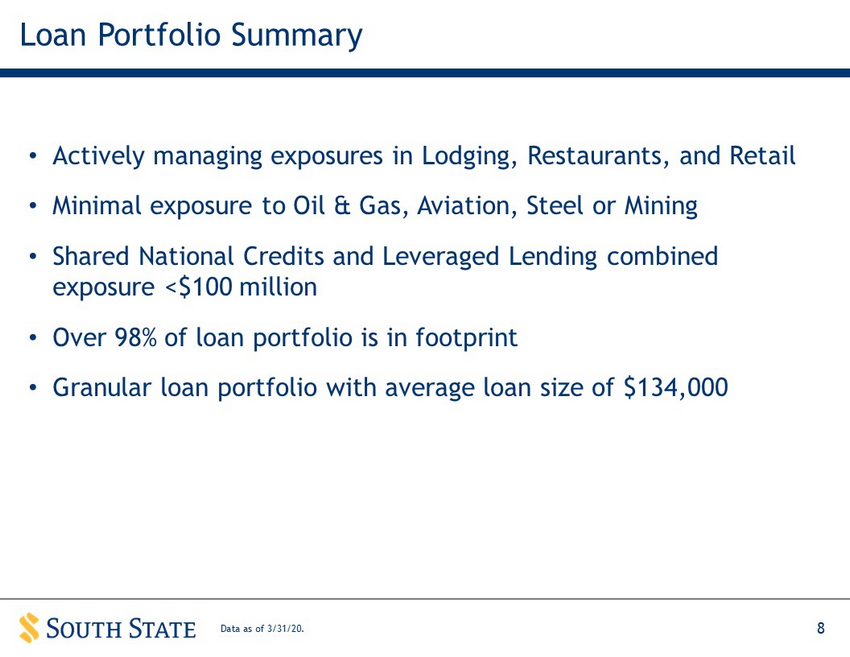

8 Loan Portfolio Summary • Actively managing exposures in Lodging, Restaurants, and Retail • Minimal exposure to Oil & Gas, Aviation, Steel or Mining • Shared National Credits and Leveraged Lending combined exposure <$100 million • Over 98% of loan portfolio is in footprint • Granular loan portfolio with average loan size of $134,000 Data as of 3/31/20.

9 Commercial 61% Consumer 12% Mortgage 27% Industry Exposure Total Portfolio $11.5 Billion Selected Industries (% of total loan portfolio) Lodging $590 5.1% Retail CRE 558 4.8 Restaurants 225 2.0 Dollars in millions. Data as of 3/31/20.

10 Loan Deferrals (1) Commercial $2,150 Consumer $32 Mortgage $265 $4 $8 $146 $240 $144 $131 $99 $242 $220 $164 $154 $123 $115 $89 $64 $51 $48 $32 $95 $39 $21 $35 $20 $12 $12 $19 $15 $27 $9 $23 $20 $15 $5 $7 Daily Request Volume • $2.4 billion total loans under deferral • Proactive communication with customers • Commercial standard deferral is 90 days P & I or 120 days principal • Consumer and Mortgage standard deferral is 120 days P & I Dollars in millions. Data as of 4/30/20.

11 Lines of Credit $1,193 $1,192 $1,200 $1,215 $1,220 $1,210 $1,208 $1,211 $1,203 $1,210 $1,204 $1,195 40.7% 40.7% 40.9% 41.4% 41.6% 41.4% 41.3% 41.5% 41.3% 41.6% 41.3% 41.0% 29-Feb 9-Mar 16-Mar 23-Mar 27-Mar 30-Mar 31-Mar 6-Apr 9-Apr 13-Apr 16-Apr 17-Apr Total Balance Utilization Dollars in millions.

12 Lodging Portfolio • Lodging is $590 million or 5.1% of the total loan p ortfolio • Average loan balance is $8.2 million • 100% of lodging p ortfolio under deferral • Weighted average LTV of 57% Marriott $234 Hilton $221 Other National Brand … Independent $63 Dollars in millions. Data as of 3/31/20.

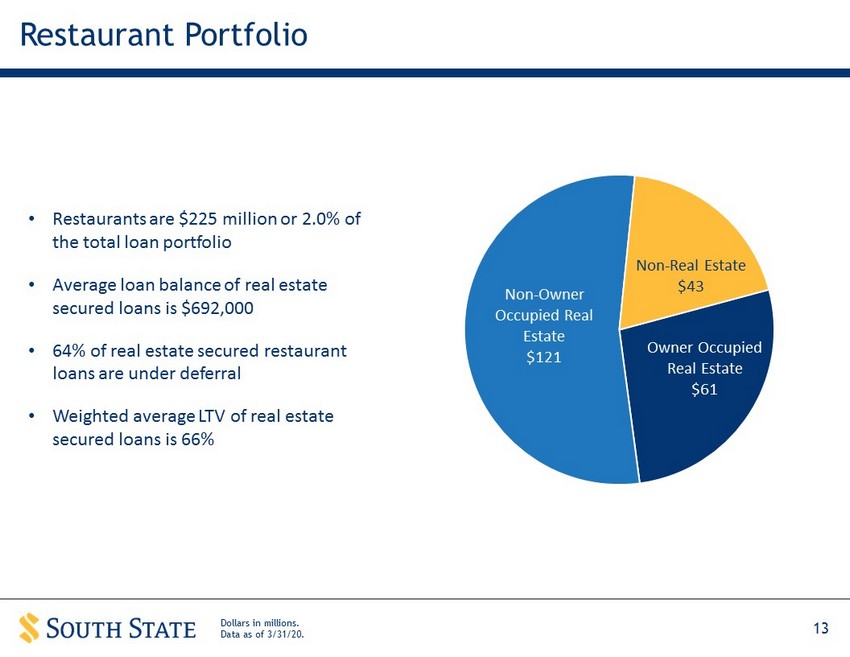

13 Restaurant Portfolio Owner Occupied Real Estate … Non - Owner Occupied Real Estate $121 Non - Real Estate $43 • Restaurants are $225 million or 2.0% of the total l oan portfolio • Average loan balance of real estate secured loans is $692,000 • 64% of real estate secured restaurant loans are under deferral • Weighted average LTV of real estate secured loans is 66% Dollars in millions. Data as of 3/31/20.

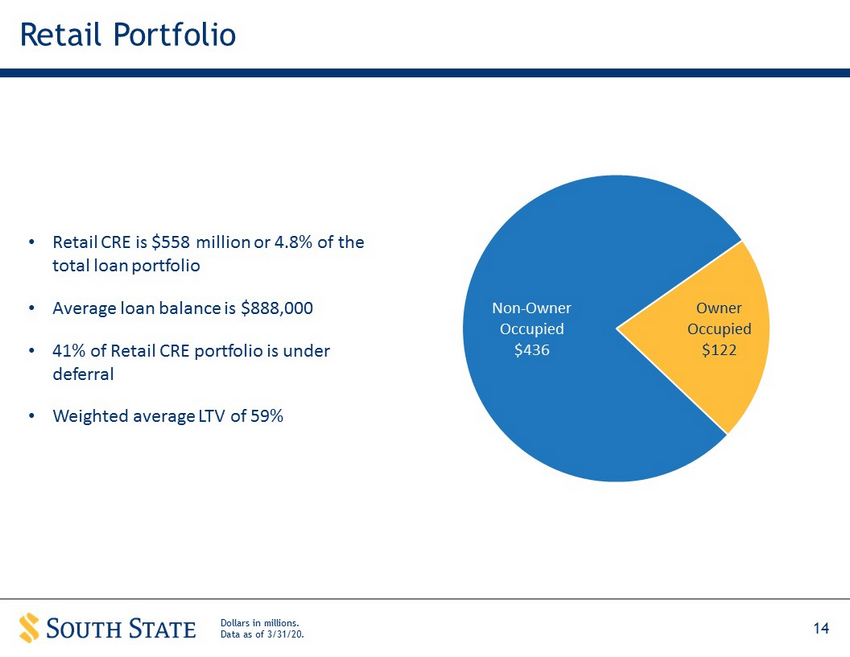

14 Retail Portfolio Owner Occupied $122 Non - Owner Occupied $436 • Retail CRE is $558 million or 4.8% of the total loan p ortfolio • Average loan balance is $888,000 • 41% of Retail CRE portfolio is under deferral • Weighted average LTV of 59% Dollars in millions. Data as of 3/31/20.

15 1Q20 Financial Highlights

16 Highlights – Linked Quarter 16 * Adjusted is a Non - GAAP financial measure that excludes the impact of branch consolidation, merger related expenses, and securities gains or losses. 4Q19 1Q20 GAAP Net Income $49.1 $24.1 EPS $1.45 $0.71 Return on Average Assets 1.23% 0.60% Return on Average Tangible Equity 15.79% 8.35% Adjusted * Net Income $50.3 $27.6 EPS $1.48 $0.82 Return on Average Assets 1.26% 0.69% Return on Average Tangible Equity 16.17% 9.45% Cash Dividend per common share $0.46 $0.47

17 Net Interest Margin 3.92% 3.82% 3.73% 3.64% 3.68% $114.1 $118.0 $119.3 $119.0 $117.0 $123.3 $127.2 $127.4 $126.5 $128.0 1Q 2019 2Q 2019 3Q 2019 4Q 2019 1Q 2020 Net Interest Margin NII - Excluding Accretion Net Interest Income Dollars in millions.

18 Average Interest Earning Assets Average Balance % of Earning Assets 4Q 2019 % of Earning Assets 1Q 2020 Net Change Short-Term Investments 4.1% 574$ 3.8% 538$ (36)$ Investment Securities 13.5% 1,889 14.4% 2,023 134 Loans - Acquired 15.8% 2,224 14.4% 2,016 (208) Loans - Non-Acquired 64.6% 9,073 67.1% 9,424 351 Total Loans 80.4% 11,297$ 81.5% 11,440$ 143$ Loans Held for Sale 0.5% 74 0.3% 42 (32) Total Interest Earning Assets 13,834$ 14,043$ 209$ Dollars in millions. Quarterly averages

19 Acquired Loans 14.4% 12.5% 10.3% 6.4% 7.4% 4% 8% 12% 16% 1Q16 3Q16 1Q17 3Q17 1Q18 3Q18 1Q19 3Q19 1Q20 Accretion / Total Interest Income Dollars in millions. Income Statement (Yields Annualized) Contractual Interest Accretion Total Income Contractual Yield Total Yield 1Q 2020 $24.9 $10.9 $35.8 4.96% 7.14% 4Q 2019 $27.8 $7.4 $35.2 4.81% 6.28%

20 Acquired Loan Portfolio Dollars in millions. As of March 31, 2020 UPB Discount Carrying Value Percentage $344.1 ($32.8) $311.3 9.5% 1,652.0 (19.4) 1,632.6 1.2% $1,996.1 ($52.2) $1,943.9 2.6% (A) Represents a non-credit discount Credit Deteriorated Non-Credit Deteriorated Total Acquired Loans (A)

21 Noninterest Income 4Q 2019 1Q 2020 Net Change Fees on Deposit Accounts 19.2$ 18.1$ (1.1)$ Mortgage Banking 3.7 14.6 10.9 Wealth Management 6.9 7.4 0.5 Acquired Loan Recoveries 2.2 - (2.2) Other Income 4.3 4.0 (0.3) Total Noninterest Income 36.3$ 44.1$ 7.8$ 1 st Quarter 2020 Highlights Dollars in millions. 1) $1.2 Million in acquired loan recoveries which flow through the loan loss reserve post - CECL (1)

22 1 st Quarter 2020 Highlights Dollars in millions. * Adjusted is a Non - GAAP financial measure that excludes the impact of branch consolidation, merger related expenses, and securities gains or losses. Noninterest Expense 4Q 2019 1Q 2020 Net Change Salaries and Benefits 58.2$ 61.0$ 2.8$ Information services expense 8.9 9.3 0.4 OREO and loan related expense 1.0 0.6 (0.4) Net occupancy expense & FFE 12.1 12.3 0.2 FDIC assessment & regulatory chgs 1.3 2.1 0.8 Bankcard expense 0.6 0.5 (0.1) Amortization of intangibles 3.3 3.0 (0.3) Professional fees & marketing 4.4 3.3 (1.1) Business development and staff related 2.9 2.2 (0.7) Other 6.4 8.8 2.4 Total Adjusted* Noninterest Expense 99.1$ 103.1$ 4.0$ Consolidation and merger related costs 1.5 4.1 2.6 Total Noninterest Expense 100.6$ 107.2$ 6.6$

23 Efficiency Ratio 63.2% 66.9% 58.4% 61.6% 62.1% 62.5% 59.8% 58.4% 60.7% 59.7% 1Q 2019 2Q 2019 3Q 2019 4Q 2019 1Q 2020 Efficiency Ratio Adjusted* Efficiency Ratio * Adjusted is a Non - GAAP financial measure that excludes the impact of branch consolidation, merger related expenses, and securities gains or losses.

24 Tangible Book Value $37.15 $37.85 $38.20 $39.13 $38.01 1Q 19 2Q 19 3Q 19 4Q 19 1Q 20