Attached files

| file | filename |

|---|---|

| EX-32 - EX-32 - CalAmp Corp. | camp-ex32_6.htm |

| EX-31.2 - EX-31.2 - CalAmp Corp. | camp-ex312_7.htm |

| EX-31.1 - EX-31.1 - CalAmp Corp. | camp-ex311_11.htm |

| EX-23.1 - EX-23.1 - CalAmp Corp. | camp-ex231_10.htm |

| EX-21 - EX-21 - CalAmp Corp. | camp-ex21_9.htm |

| EX-10.38 - EX-10.38 - CalAmp Corp. | camp-ex1038_250.htm |

| EX-4.5 - EX-4.5 - CalAmp Corp. | camp-ex45_237.htm |

| EX-3.2 - EX-3.2 - CalAmp Corp. | camp-ex32_67.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED FEBRUARY 29, 2020

COMMISSION FILE NUMBER: 0-12182

CALAMP CORP.

(Exact name of Registrant as specified in its Charter)

|

Delaware |

|

95-3647070 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

15635 Alton Parkway, Suite 250 Irvine, California |

|

|

|

|

92618 |

|

|

(Address of principal executive offices) |

|

(Zip Code) |

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE: (949) 600-5600

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

TITLE OF EACH CLASS |

|

TRADING SYMBOL(S) |

|

NAME OF EACH EXCHANGE |

|

$0.01 par value Common Stock |

|

CAMP |

|

The Nasdaq Stock Market LLC (The Nasdaq Global Select Market) |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.:

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☒ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

☐ |

|

Emerging growth company |

☐ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes ☐ No ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of August 31, 2019, the aggregate market value of shares held by non-affiliates of the registrant was approximately $264.9 million. For purposes of calculating the aggregate market value of shares held by non-affiliates, we have assumed that all outstanding shares are held by non-affiliates, except for shares held by each of our executive officers, directors and 10% or greater stockholders. These assumptions should not be deemed to constitute an admission that all executive officers, directors and 10% or greater stockholders are, in fact, affiliates of our company. As of April 30, 2020, there were 34,325,681 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the Annual Meeting of Stockholders to be held on July 29, 2020 are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this Form 10-K. This Proxy Statement will be filed within 120 days after the end of the fiscal year covered by this report.

|

|

|

|

|

Page |

|

|

|

|

|

|

|

Item 1. |

|

|

2 |

|

|

Item 1A. |

|

|

14 |

|

|

Item 1B. |

|

|

31 |

|

|

Item 2. |

|

|

31 |

|

|

Item 3. |

|

|

31 |

|

|

Item 4. |

|

|

32 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 5. |

|

|

33 |

|

|

Item 6. |

|

|

34 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

37 |

|

Item 7A. |

|

|

55 |

|

|

Item 8. |

|

|

55 |

|

|

Item 9. |

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

97 |

|

Item 9A. |

|

|

97 |

|

|

Item 9B. |

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 10. |

|

|

101 |

|

|

Item 11. |

|

|

101 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

101 |

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

101 |

|

Item 14. |

|

|

101 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 15. |

|

|

102 |

Company Overview

CalAmp Corp. (including its subsidiaries unless the context otherwise requires, “CalAmp”, “the Company”, “we”, “our”, or “us”), incorporated in 1987, is a global technology solutions pioneer leading the transformation to a mobile connected economy. We help transform businesses and improve lives around the globe with technology solutions that streamline complex mobile Internet of Things (“IoT”) deployments using wireless connectivity and data analytics.

We have created a cloud-based connected IoT ecosystem that is enhanced through our Software-as-a-Service (SaaS) subscription services and applications. Our platform provides greater visibility, scalability and connectivity across automotive, insurance, transportation and logistics, government and construction markets creating a massive global IoT ecosystem. By employing our cloud platform and SaaS subscription services, global businesses can dramatically improve their operations, streamline communications and gain critical insights from their business data that can transform the speed, cost and reliability of their services and operations.

Our unified and integrated cloud-based IoT ecosystem combines SaaS-based applications, telematics services, a scalable global cloud platform and intelligent edge computing products. Together these elements deliver a comprehensive view of vehicles, machines, drivers, assets and cargo in real time that would otherwise require multiple disparate applications. Our applications and services all tie back to our cloud platform, generating actionable data and insights that help management optimize business operations through better decision making at the edge. While each one of our offerings can be combined for a complete end-to-end telematics solution, they can also be customized and integrated with custom applications or back-office systems, without losing the actionable mobility data that only CalAmp can provide.

Our cloud platform offers valuable telematics services that provide enhanced insights to help companies more efficiently manage their assets including fleet video intelligence, remote asset monitoring, real-time crash response and driver behavior scoring. Our programmable telematics devices enable computing at the edge and capture business-critical data from mobile assets, their passengers and content anywhere in the world at any time. We call this The New How: powering autonomous IoT interaction, facilitating efficient decision making, optimizing resource utilization and improving road safety.

Economic conditions, competitive markets, global regulatory environments, the COVID-19 pandemic and the transition to 4G and 5G connectivity are challenging traditional businesses to drive operational efficiencies, track processes, reduce costs, fund business growth and innovation, and enhance profitability and cash flow. Therefore, effective management of business spend is imperative if businesses are to achieve significant profitable growth. Businesses must evaluate their underutilized resources and leverage the new connected ecosystem. CalAmp helps enterprises and mid-to-large businesses compete in the on-demand economy, and thus fulfill consumer expectations for fast, reliable and on -time products and services at their fingertips.

Our company culture is driven by our five core values:

|

|

• |

Integrity – take personal responsibility - we value our customers and look for ways to enhance our solutions to benefit them and the community. |

|

|

• |

Inspiration – foster high performance - we design all of our products and services with the highest quality, knowing that whether it’s a shipment of critical refrigerated pharmaceuticals, children on their way to school, or packages en route to a retail store, they should all be handled with care. |

|

|

• |

Innovation – bring value to our customers - optimizing businesses all over the world is at the heart of what we do and we’re always seeking ways to learn about their needs in order to improve their overall operations. |

2

|

|

• |

Excellence – exceed customer requirements by delivering best-in-class solutions - our customer-focused approach includes enabling better business outcomes by offering our customers the finest products, services and support to help them optimize their business operations. |

The successful execution of this approach, in combination with our core values, will help customers to succeed and thus drive our growth.

We have approximately 1.3 million software and service subscribers and more than 20 million products installed globally in multiple market verticals including automotive, insurance, transportation and logistics, government and construction. There are over two million Here Comes The Bus® mobile app users operated by fleet managers and school districts. We believe the installed base represents a significant recurring revenue opportunity as we strive to deliver additional over-the-top services and data monetization opportunities to subscribers in collaboration with our customers and partners.

Growth Strategy – Capitalize on $30B Total Available Market

3

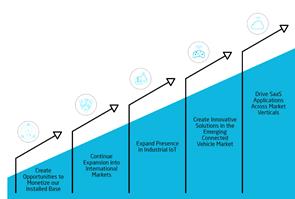

Over the past three years, we have focused on growing our new subscription-based business model. We intend to grow this core business and expand into new markets and geographic regions in the years ahead. Our business operates at the nexus of several large market opportunities including the connected vehicle ecosystem, enterprise asset tracking, and fleet management product and services markets. We believe these market opportunities constitute a total available market (“TAM”) of approximately $30 billion. In order to capitalize on this TAM, our growth strategy and the metrics by which we measure ourselves includes the following five key elements:

|

|

• |

Drive SaaS Applications Across Market Verticals. We are relentlessly pursuing our goal to grow our software and subscription services business. To accomplish this goal, our team is focused on continual product innovation across our proprietary software stack. We believe that by leveraging our existing brand presence and customer base in four market verticals including transportation, construction, government and the automotive aftermarket, we can drive growth in our SaaS applications. And as we steadily grow our base of SaaS subscribers, we’ll continue to migrate to a pure-play solution provider of subscription services by combining our broad portfolio of SaaS applications, cloud-based platform and programmable telematics devices. |

|

|

• |

Create Innovative Solutions in the Emerging Connected Vehicle Market. With the acquisition of LoJack® licensees in the U.S., U.K., Italy and Mexico, we now have a highly recognizable, consumer-facing brand as well as strong and unique relationships with law enforcement agencies (in the U.S. and other geographical regions), auto dealerships, insurance companies, rental car agencies, regional and global transportation and logistics providers, and heavy equipment original equipment manufacturers (OEMs). We plan to develop telematics applications for the connected vehicle market similar to LoJack® SureDrive™ targeting the consumer telematics segment and LoJack® LotSmart™ for automotive dealer inventory management. We plan to increase our investment in research and development to expand and enhance the features and capabilities of our products and solutions and drive further innovation through synergies created among our Synovia acquisition and LoJack subsidiaries. |

|

|

• |

Expand Presence in Industrial IoT. We believe that our current distribution footprint covers a significant portion of the global industrial IoT market due to our strong relationships with large enterprises such as Caterpillar. We believe there is an opportunity for us to leverage our core competencies of working with these global enterprises and expand our presence with other industrial OEMs. |

|

|

• |

Continue Expansion into International Markets. We are leveraging our existing customer relationships, international subscribers and recent Tracker UK and LoJack Mexico acquisitions to further expand into global markets including Latin America, Europe, Middle East, Africa and Asia Pacific. Our global expansion strategy is focused on countries with anticipated demand for our full stack of SaaS application and services, cloud platform and telematics devices. |

|

|

• |

Create Opportunities to Monetize our Installed Base. We believe that our strong and growing installed-base of over 20 million telematics devices and approximately 1.3 million unique software and services subscribers provide us with an opportunity to create additional revenue streams by delivering high-value data sources, applications and other over-the-top subscription services to enterprises in large markets such as automotive, insurance, transportation & logistics, government and construction. |

Subsidiaries and Recent Acquisitions

Synovia Solutions - In April 2019, we acquired Synovia Solutions (“Synovia”), a North American market leader in fleet safety and management for the K-12 market as well as state and local government organizations. At the forefront is Here Comes The Bus, an award-winning mobile app powered by GPS services that delivers real-time school bus and student tracking intelligence. Since the acquisition, downloads of the application have exceeded two million serving over 300 school districts in 35 states across the U.S. Synovia Solutions also provides government fleet management solutions designed to improve utilization, lower insurance premiums and enable preventative maintenance while expanding our fleet management and vehicle safety services portfolio. This acquisition also accelerates our transformation to high-value subscription-based services. Moreover, in the wake of the COVID-19 outbreak, schools districts throughout the U.S. are now using Here Comes The Bus to assist in meal delivery to students while schools remain closed.

4

LoJack Mexico - In March 2019, we acquired Car Track, S.A. de C.V. (“LoJack Mexico”), the exclusive licensee of LoJack technology for the Mexican market. LoJack Mexico is a provider of innovative automotive and stolen vehicle recovery (“SVR”) services throughout Mexico and Latin America. LoJack Mexico is leveraging CalAmp’s full stack of telematics and SaaS solutions to expand product offerings to its substantial subscriber base of consumers, auto dealers and OEMs, insurance providers and leasing companies. This acquisition provides us with a profitable business and world-class brand. With strong channels, consumer awareness and law enforcement relationships in major cities across Mexico and Latin America, LoJack Mexico boasts approximately 139,000 software and services subscribers and has announced recent partnerships with Hertz, MAN Truck, Volkswagen Financial and Dogo Informatique.

Tracker - In February 2019, CalAmp acquired Tracker Network (UK) Limited (“Tracker”), a LoJack licensee and market leader in SVR and telematics services across the United Kingdom since 1993. Tracker is strategically aligned with LoJack Italia to drive CalAmp’s European expansion by leveraging a complete, vertically integrated portfolio of SaaS applications and services, cloud platform and telematics devices to develop advanced connected car solutions for auto dealers, OEMs, insurance providers and other enterprise customers. The acquisition brings strong brand awareness across the U.K. and extensive law enforcement relationships by integrating two of Europe’s most advanced SVR and telematics solutions providers. Tracker recently announced a new SmartDealer solution for lot and fleet management, a SmartDrive connected car application as well as partnerships with Auto Capital and NG Bailey.

Extended Business Network

Because our connected IoT ecosystem is constantly collecting, monitoring and reporting business-critical information from mobile and remote assets, our customers can run their business operations more efficiently. We also make it easy for our customers to purchase our end-to-end connected fleet and supply chain solutions via a SaaS subscription-based model that enables us to create greater customer engagement and long-term enterprise relationships while driving incremental recurring revenue.

Today we sell into numerous market verticals including automotive, insurance, transportation and logistics, government, K-12 and construction in the United States, Latin America, Western Europe, Asia Pacific, Middle East and Africa. We sell our connected car applications to consumers through all of LoJack distribution channels. We serve parents, students and school administrators through our Here Comes The Bus mobile app that can be found in the App Store and Google Play Store. Our brands and technological leadership have driven the adoption of our connectivity solutions with small to midsize customers as well as large global enterprises. We also serve numerous government organizations and municipalities and over 300 school districts across North America. With our international network of LoJack subsidiaries and a strong ecosystem of industry partnerships, we bring intelligence to the edge in the mobile connected economy to help drive business efficiencies.

Our software subscription business model allows us to continuously listen to our customer’s needs and learn about their pain points and how they affect their day-to-day business. Our partnerships and acquisitions have enabled us to get in front of new customers furthering our abilities to digitize their businesses, and capitalizing on our reputation and history as a true telematics pioneer.

Enterprise Customers - We sell our products and services directly to large global enterprises and industrial OEM customers. These customers require very different selling approaches and support requirements, and we have organized our teams to address these different requirements. Additionally, certain customers often have unique technical requirements and manufacturing processes, and may request specific product configurations, feature sets and designs. Sales to large enterprise customers often involve complex program management and long sales cycles, and require close cooperation between sales, operations and engineering personnel. As such, we have developed teams of key account managers and business development managers to serve the unique requirements of these customers. Some of the global enterprises we serve include Amazon, Caterpillar, Hertz, Omnitracs, Pioneer, Toyota, TransUnion, Trimble and Volkswagen Financial.

5

Telematics Service Providers (“TSPs”) and Channel Partners - We market and sell our products and services to small- and mid-sized companies through our well-established sales team and Channel Partner Program that sells our full product portfolio into Telematics Service Providers, Value-Added Resellers (“VARs”), systems integrators and mobile network operators. These partners integrate our telematics solutions with their value-added applications to deliver purpose-built solutions that are sold through to restaurant, farming, water & waste management and construction industries among others.

Strategic Partners - CalAmp has developed third party strategic partnerships to serve a wide range of customers from enterprises to small businesses. CalAmp has established strategic partnerships with supply chain management service providers including CargoSense, Overhaul, Cryoport and RoviTracker. We also partnered with TransUnion to work with insurance companies and to provide stolen vehicle recovery services and help insurance carriers better manage risk, minimize replacement losses and improve customer service. We partner with mobile network operators including AT&T, Verizon, Sprint and Telefonica among others to provide connectivity solutions for our customers. This year we established a partnership with Sprint to deliver intelligent telematics devices and software applications, along with unique CalAmp iOn™ DaaS subscription services to expand Sprint's broad range of connected car, fleet and asset management services that drive operational efficiencies and secure high-value assets for enterprise and business customers.

Our global direct sales organization consists of teams of field salespeople, key account managers and business development managers, who work closely with product and applications specialists and other internal sales support personnel based primarily across our U.S. locations. We have organized our field sales personnel, together with internal sales and field support personnel, into teams within each business group based on their specialized knowledge and expertise relating to specific product and service areas, geographies and customer groups. These sales teams are closely aligned with their respective product management, engineering and operations organizations.

We expect that our reputation for providing innovative and high-quality solutions will continue to play a significant role in our growth and success, and that high customer satisfaction will continue to fuel referrals of our brand to new customers. Through our trademarked name – CalAmp – we have built a highly recognizable brand in the global enterprise, fleet management and supply chain market verticals. Also, in connection with the acquisitions of LoJack and Synovia Solutions, we acquired a highly recognizable consumer-facing brand in the K-12 market with Here Comes The Bus.

Customer Benefits

Our connected telematics products, software solutions and other subscription services address a wide variety of applications across key vertical markets ranging from small to large enterprises. They are in constant communication with remote and/or mobile assets as they perform business-critical tasks and services that are otherwise difficult to manage in real time on a remote basis. In such situations, our solutions provide a clear and demonstrable return on investment. Our products and solutions benefit our customers in the following ways:

|

|

• |

Increasing productivity, improving communications and optimizing performance of fleets and mobile workers. Applications include vehicle monitoring, dispatch and route optimization, fleet diagnostics and maintenance, workflow improvement, workforce communications, driver behavior monitoring, as well as training and work-alone safety initiatives. |

|

|

• |

Improving the automobile dealer, vehicle owner and vehicle insurer experience. Applications include connected car and insurance telematics solutions that expedite the claims process for insurers, improve lot management for automobile dealers and provide early warning alerts, accident reconstruction and other connected car and road safety services for consumers. |

|

|

• |

Enabling multi-modal supply chain visibility tracking and management services from the cab to the containers and cargo. Applications include local and long-haul trailer tracking, management and logistics, container tracking and status, refrigerated container monitoring and control, high-value asset & pet-tracking solutions for in-air travel, environmental condition monitoring of cargo down to the product level, and, delivery assurance combined with local and intermodal pallet and cargo logistics and tracking. |

6

|

|

• |

Facilitating comprehensive monitoring, tracking and telematics for heavy equipment and commercial trucking. Applications include heavy equipment maintenance, usage optimization and tracking, rental equipment tracking, high-value tools and asset tracking, yellow iron and attachment management, indoor/outdoor forklift and loader location, impact detection and telematics. |

|

|

• |

Enabling usage-based insurance, enhanced claims processing and delivery of comprehensive value-added services for the vehicle insurance industry. Applications include stolen vehicle recovery for insurance providers, driver behavior scoring and feedback, crash discrimination, collision alerts and reconstruction, damage assessment and estimation, teen driver tracking and management, roadside assistance and predictive maintenance. |

|

|

• |

Delivering end-to-end visibility and regulatory compliance for supply chain management. Applications include granular visibility of product location and environmental status for temperature-sensitive drugs, perishable food and high-value consumer goods. |

|

|

• |

Enabling rapid delivery of comprehensive managed services for machine and equipment OEMs. Applications include service, maintenance, tracking, monitoring and control for generators, turbines, compressors, small engines (e.g., outboard motors, ATVs and electric carts) and power tools. |

|

|

• |

Creating a safe and reliable school bus riding experience for students and parents. School bus tracking and student tracking mobile app that gives students and parents peace of mind through regular real-time tracking of pick-up and drop-off information for K-12 students all over the U.S. |

Differentiators

We pride ourselves in servicing each layer of a business’s telematics value chain, from software service applications through devices. This integrated approach puts us ahead of competitors because we can provide customers with a complete solution or a flexible, configurable solution that can easily enhance other third party applications or back-office enterprise systems.

With a trusted and growing global presence, CalAmp provides a secure, scalable, and flexible solution with application for multiple industries and continues to expand its offerings in different geographies and market segments. Our powerful technology and financial strength empower us to bring innovative solutions to market. The CalAmp mobile connected ecosystem, for example, offers a seamless, end-to-end telematics solution that addresses the most complex operational challenges.

Within the ecosystem, exists CalAmp Telematics Cloud™ (“CTC”) which captures, analyzes and transforms data from equipment and mobile assets into actionable insights. Powered by an enterprise-grade cloud platform and advanced security, CTC facilitates integration between CalAmp applications and third-party management systems to enable flexible IoT solutions and innovative telematics services. Many multinational shipping enterprises rely on CalAmp, such as Amazon which uses CTC to build a mission-critical business application that enables them to quickly develop tailored solutions designed around their own applications to meet specific use cases.

Our enterprise customers tell us that only CalAmp offers a seamless one-stop shop for mobile asset management with these critical capabilities:

|

|

• |

Integration: CTC’s Application Development Environment (“ADE”), along with CalAmp’s broad portfolio of devices, easily links vertical, back-end applications to remote assets providing only the information needed for each key stakeholder within the organization. |

|

|

• |

Scalability: The ADE provides an embedded framework to help create tailored solutions enabling faster deployment with minimized infrastructure. Our Device-as-a-Service (“DaaS”) model minimizes costs for managing devices and telematics services as well as technical support, so customers can scale their solutions in a more cost-effective manner. |

7

|

|

• |

Speed: With CalAmp’s industry-standard APIs, customer development teams can capture the information they need from mobile assets to speed time-to-market of custom telematics solutions. |

|

|

• |

Reliability: Large global logistics companies can’t afford downtime or loss of data. This is especially imperative for surviving peak seasons in freight transportation. Data reliability and zero operational downtime on that kind of global scale only comes with experience. Our customers have come to know whom we serve and the importance and scale of those telematics deployments. Reliability comes in large part from CTC being built on one of the most reliable and scalable enterprise-grade cloud infrastructures in the business: Amazon Web Services. That kind of reliability played a part in Amazon choosing CalAmp for one of its telematics needs. |

Our Platform

CalAmp’s unified IoT ecosystem includes our SaaS-based applications, CalAmp Telematics Services, CalAmp Telematics Cloud Platform and intelligent edge computing products. Companies of all sizes leverage our integrated suite of IoT services and devices into their operational infrastructure to reliably and securely transmit business-critical data points from high-valued mobile assets to address the most complex operational challenges. This tight integration of IoT technology provides greater visibility to help meet customer expectations in the on-demand economy.

SaaS Applications. We provide our customers with intelligent analytics and reporting tools that are accessible via a single view, user-friendly interface through SaaS-based applications designed to address specific vertical market needs. CalAmp iOnTM is purpose-built for service fleets, government fleets and construction, turning multiple data feeds from previously unconnected networks of vehicles, drivers and associated assets into clear and actionable insights that optimize operations, increase productivity and deliver compelling ROI for virtually any business challenge. CalAmp SC iOn Supply Chain delivers real-time visibility about the environmental status of pharmaceuticals, electronics, food or other perishables from manufacturing to the point of purchase, helping to manage quality and compliance across land, air or sea shipments. LenderOutlookTM enables vehicle finance, automotive dealers and credit unions to secure their assets, reduce risk and build customer loyalty while driving revenue. Here Comes The Bus® is an award winning mobile application that provides real-time school bus location through push notifications and email alerts to help families monitor bus arrival and keep students safe. LoJack SureDrive is a connected car app that provides crash alerts, movement detection, arrival notifications and speed alerts to help drivers and their families save time and stay safe. LoJack LotSmart is an inventory management system that empowers dealers with vehicle location, battery level and other diagnostic information to streamline operations and improve the customer experience.

8

CalAmp Telematics Services. CalAmp delivers enhanced contextual insights that help manage mobile workers, vehicles, mobile assets, tools and cargo. Our subscription-based telematics services enable customers to optimize their operations by collecting, monitoring and effectively reporting business-critical information and desired intelligence from high-value remote and mobile assets. CalAmp iOn Vision provides fleet operators and service providers with actionable video insights to assess driver behavior, mitigate liabilities and improve fleet safety. CalAmp iOn Tag Service helps service fleets to minimize project delays and prevent loss by enabling greater visibility and control over their assets and tools. CrashBoxx provides crash detection and delivers instant crash alerts to speed life-saving assistance to drivers, expedite the claims process and reconstruct the collision to help fleet operators mitigate liability and fraud. Driver Behavior Scoring enables fleet managers to improve driver safety and identify the need for training based on speeding, harsh braking, hard cornering and other risky driving behaviors. LoJack Stolen Vehicle Recovery is the only SVR solution directly integrated with law enforcement that has a 90%+ recovery rate and over $1 billion worth of recoveries in the U.S. alone. LoJack Stolen Asset Recovery allows construction and heavy equipment rental companies to protect and recover high-value construction equipment and commercial vehicles. Security is of greatest importance to CalAmp especially in a rapidly evolving cyber threat landscape. CTC is SOC 2 certified, meaning it’s designed to securely retain data in the cloud. With this certification, organizations have the confidence their sensitive data is secure, ensuring confidentiality and availability for optimized telematics deployments.

CalAmp Telematics Cloud (“CTC”). The CalAmp Telematics Cloud is the core engine that enables seamless management of a diverse set of assets, from service vehicles to high-value equipment. CTC is an enablement platform that connects our customers to a wide range of applications and software services, which enhances the value of our telematics products and offers flexibility and scale for small to medium-sized businesses as well as global enterprise corporations. Our cloud-based platform connects our SaaS-based applications, telematics services and edge computing devices, and facilitates integration with third party applications, through open Application Programming Interfaces (“API”s). Our partners leverage multiple APIs we’ve created to rapidly deliver full-featured IoT solutions to their customers and markets. Our proven CTC is architected to integrate with numerous global Mobile Network Operator (“MNO”) account management systems and leverage these carrier backend systems to provide customers access to services that are essential for creating and managing flexible end-to-end solutions.

CalAmp Edge Computing Products. We offer a series of telematics devices and sensors that serve as the backbone of our mobile connected ecosystem by collecting data insights from vehicles, drivers, assets and cargo. These wireless networking devices--including asset tracking units, mobile telematics devices, fixed and mobile wireless gateways and routers--underpin our wide range of proprietary and third-party software applications and services for business-critical deployments demanding secure and reliable communications and controls anywhere in the world. Our customers select our products and solutions based on optimized feature sets, configurability, manageability, long-term support, reliability and, in particular, overall value.

Industry Recognition

In 2019, CalAmp received an Honorable Mention for Hello Tractor in the Fast Company World Changing Ideas award and won the IoT Platform Leadership Award for our Air Freight Visibility Solution, developed jointly with CargoSense. Here Comes The Bus and Synovia Solutions won the Mobile World Congress Barcelona Global Mobile Award, IoT Excellence Award and IHS Markit Award.

Recent Developments

In December 2019, a strain of coronavirus entitled COVID-19 emerged in China and spread to other countries including to the United States. In March 2020, the World Health Organization declared COVID-19 to be a public health pandemic of international concern, which has resulted in travel restrictions and in some cases, prohibitions of non-essential activities, disruption and shutdown of businesses and greater uncertainty in global financial markets.

In the United States and other geographies in which we and our customers, partners and service providers operate, the health concerns as well as political or governmental developments in response to COVID-19 could result in economic, social or labor instability or prolonged contractions in certain end markets which could slow the sales process, result in customers not purchasing or renewing contracts or failing to make payments. These events could have a material adverse effect on the business and results of operations and financial condition.

9

At this time, it is difficult to predict the extent to which the COVID-19 outbreak will impact our business or operating results, which is highly dependent on uncertain future developments, including the severity of the pandemic and the actions taken or to be taken by governments and private businesses in relation to its containment. Because our business is dependent on telematics product sales, device installations and related subscription-based services, the effect of the outbreak may not be fully reflected in our operating results until future periods.

We have adopted several measures in response to the COVID-19 outbreak, including instructing employees to work from home, implementing certain cost and cash flow control measures to address potential declines in billings and cash collections from customers, shifting the manner in which we engage with customer and restricting non-critical business travel by our employees. As a result of the work and travel restrictions, substantially all of our sales and installation services activities are being conducted remotely.

Manufacturing and Operations

While the vast majority of our products are designed in the U.S., we currently outsource a substantial portion of our manufacturing to certain contract manufacturers, which are located primarily in Hong Kong, mainland China, Malaysia and other Pacific Rim countries. Our electronic devices, components and made-to-order assemblies used in our products can be obtained from these manufacturers, although certain components are obtained from sole source suppliers. Although we do not have any long-term purchase contracts, we have executed product supply agreements with these manufacturers, which provide for certain product quality requirements. We are not vertically integrated, which provides us with flexibility and an ability to adapt to changes in the market, product supply and pricing while keeping our fixed costs low. Our relationships with our manufacturers are critical to new product introduction and the success of our business. We have strong relationships with our manufacturers, helping us to meet our supply and support requirements. As we announced in fiscal year 2019, we commenced a plan to streamline our global operations including further outsourcing of our manufacturing functions to increase supplier diversification and reduce operating expenses. We now have full manufacturing capabilities in Taiwan, Malaysia and Mexico. Furthermore, our production and distribution facility in Oxnard California has been closed. We are now utilizing our outsourced partner in Fort Worth, Texas for certain US distribution.

We focus on driving alignment of our product roadmaps with all our manufacturers and determining what we can do collectively to reduce costs across the supply chain. Our operations team based in the U.S. coordinates with our manufacturers’ engineers and quality control personnel to develop the requisite manufacturing processes, quality checks and testing as well as general oversight of the manufacturing activities. We believe this model has allowed us to effectively deliver high quality and innovative products while enabling us to minimize costs, manage inventory risk and maintain flexibility.

We are certified to the ISO (International Organization for Standardization) 9001: 2008 Quality management systems standard.

Research and Development

We compete in markets characterized by industry disruption, rapid technological change, evolving industry standards and new product features. We believe that our future success depends upon our ability to continue to develop innovative new products and solutions as well as enhancements to our existing products and solutions with advanced functionality and ease of use to drive customer demand and to further enhance our global brand and drive recurring revenue. We will continue to focus our research and development resources primarily on developing telematics products, services and software solutions for fleet management, heavy equipment, stolen vehicle recovery, consumer aftermarket telematics, trailer & asset tracking, transportation & logistics, and industrial monitoring & controls applications. We have developed technology platforms that can be leveraged across many of our vertical markets, applications and geographic regions. These include cloud-based telematics application enablement platforms and end-user software applications, cellular and satellite communications network-based asset tracking units, as well as 3G and 4G LTE broadband router products primarily for mobile applications. In addition, our development resources have been allocated to rationalizing existing product lines, reducing product costs, and improving performance through product redesign efforts.

10

Our research and development expenses in fiscal years ended February 29, 2020, February 28, 2019 and 2018 were $29.4 million, $27.7 million and $25.8 million, respectively. During this three-year period, our research and development expenses have ranged between 7% and 8% of annual consolidated revenues.

Sales and Marketing

We market and sell our products and services through our global direct sales organization, Channel Partner Program and sales representatives as well as our websites and digital presence. Our global direct sales organization consists of teams of field salespeople, key account managers and business development managers, who work closely with product and applications specialists and other internal sales support personnel based primarily at our U.S. locations. We have organized our field sales personnel, together with internal sales and field support personnel, into teams within each business group based on their specialized knowledge and expertise relating to specific product and service areas, geographies and customer groups. These sales teams are closely aligned with their respective product management, engineering and operations organizations.

We sell our products and services to large global enterprises, small to midsize companies, channel accounts and distributors as well as industrial OEM customers. These categories of customers require very different selling approaches and support requirements, and we have organized our sales teams to address these different requirements. Additionally, certain customers often have unique technical requirements and manufacturing processes, and may request specific product configurations, feature sets and designs. Sales to large enterprise customers often involve complex program management and long sales cycles, and require close cooperation between sales, operations and engineering personnel. As such, we have developed teams of key account managers and business development managers to serve the unique requirements of these customers.

We also actively sell our products in certain markets through our LoJack subsidiaries, independent sales representatives and distributors. We have entered into agreements with substantially all of our distributors. In some cases, we have granted representatives and distributors exclusive authorization to sell certain products in a specific geographic area. These agreements generally have terms of one year, which automatically renew on an annual basis, and are generally terminable by either party for convenience following a specified notice period.

We expect that our reputation for providing innovative and high-quality products will continue to play a significant role in our growth and success, and that high customer satisfaction will continue to fuel referrals of our brand to new customers. Through our trademarked name – CalAmp – we have built a highly recognizable brand in the global enterprise asset tracking and fleet management market verticals. Also, in connection with the acquisition of LoJack, we acquired a highly recognizable consumer-facing brand in the global connected vehicle market.

We will continue our investment in sales and marketing programs that further build brand awareness, drive deeper customer engagement and foster long-term relationships with our customers. Our marketing programs are now focused on supporting multi-channel product launches in new geographic markets. With the recent acquisitions, we will drive additional sales through our Tracker and LoJack Mexico subsidiaries, which will be a primary focus throughout fiscal 2021.

Additionally, we are focused on maximizing our efficiency and reach of our marketing spend by investing in public relations, social media and digital marketing programs. These programs are developed to educate our potential customers and other industry influencers to fuel active engagement with our products and services. Our activities around public relations, thought leadership, social media and digital marketing will be aligned with our customary product launches, media campaigns and presence at tradeshows and high exposure venues such as Mobile World Congress in Barcelona, Spain, Mobile World Congress Americas in Los Angeles among other high-profile industry events. Notably, Mobile World Congress Barcelona 2020, due to be held in late February 2020, was cancelled amid the coronavirus outbreak.

Our revenues derived from customers in the U.S. represented 73%, 74% and 73% of consolidated revenues in fiscal years ended February 29, 2020, February 28, 2019 and 2018, respectively.

11

Our markets are highly competitive. We face competition from small to large public and private competitors some of which have greater financial, distribution, marketing and other resources as well as greater economies of scale than we do. We believe the principal competitive factors impacting the market for our products and services are global scale, innovation, reputation, customer service, product quality, functionality and reliability, time-to-market, responsiveness and price. We believe that we compete favorably in all of these areas. Our continued success in our vertical markets will depend in part upon our ability to continue to innovate, design quality products and deploy solutions at competitive prices and with superior support services to our customers.

Some of the more established competitors for telematics systems and related connected products include Danlaw, Mobile Devices, Orbcomm, Quake Global, Queclink, Sierra Wireless, Spireon, Teltonika, Inseego, and Xirgo. Additionally, the market for Software and Subscription Services is also highly competitive and includes well-established companies such as Geotab, Samsara, Octo Telematics, Omnitracs, OnStar, Trimble, Verizon Connect and Zonar Systems as well as numerous smaller players.

BACKLOG

Total backlog for our hardware products as of February 29, 2020 and February 28, 2019 was $30.9 million and $18.4 million, respectively. Substantially all of the backlog at February 29, 2020 is expected to be shipped in fiscal 2021. Our backlog for hardware products increased year-over-year as we experienced significant supply shortages which were primarily attributable to significantly impaired production capacity from our one remaining Chinese supplier resulting from the coronavirus outbreak. We also experienced other supply shortages due to supply chain transitions, coupled with extended lead times on raw materials and components sourced from China, but used elsewhere in our global supply chain.

INTELLECTUAL PROPERTY

Intellectual property is an important aspect of our business, and we seek protection for our intellectual property as appropriate. We rely upon a combination of patent, trade secret, and trademark laws and contractual restrictions, such as confidentiality agreements and licenses, to establish and protect our proprietary rights. In addition, we often rely on inbound licenses of intellectual property for use in our business.

We own and utilize the tradenames “CalAmp” and “LoJack” as well as the related logos and trademarks on all of our products and solutions. We believe that having distinctive marks that are registered and readily identifiable is an important factor in identifying our brand. We own 223 active trademark applications and registrations throughout the world, with 35 pending and registered trademarks in the U.S.

In addition to the foregoing protections, we generally control access to and the use of our proprietary and other confidential information through the use of internal and external controls, including contractual protections with employees, manufacturers, and others. We will continue to file and prosecute patent applications when appropriate to attempt to protect our rights in our proprietary technologies.

As of February 29, 2020, we had 84 U.S. patents and 221 foreign patents. In addition to our awarded patents, we have 55 patent applications in process. Although a number of these trademarks, copyrights, and patents relate to software and products that are significant to our business and operations, we do not believe we are dependent on a single trademark, copyright or patent.

ENVIRONMENTAL REGULATION

We are subject to a variety of U.S. and foreign laws and regulations in connection with our operations and relating to the protection of the environment, including those governing discharges of pollutants into the air and water, the management and disposal of hazardous substances and the clean-up of contaminated sites. Some of our operations require environmental permits and controls to prevent and reduce air and water pollution. These permits are subject to modification, renewal and revocation by issuing authorities. We believe that we have obtained or are in the process of obtaining all necessary environmental permits for our operations.

12

We have established environmental management systems and continually update our environmental policies and standard operating procedures for our operations worldwide. We believe that our operations are in material compliance with applicable environmental laws, regulations and permits. We budget for operating and capital costs on an ongoing basis to comply with environmental laws.

CORPORATE RESPONSIBILITY AND SUSTAINABILITY

We believe responsible and sustainable business practices support our long-term success. As a company, we are deeply committed to protecting and supporting our people, our environment, and our communities. That commitment is reflected through sustainability-focused initiatives as well as day-to-day activities, including our adoption of sustainability-focused policies and procedures, our publicly-recognized focus on fostering an inclusive workplace, our constant drive toward more efficient use of materials and energy, our careful and active management of our supply chain, our products which help reduce carbon footprints and enhance road safety, and our impactful, globally-integrated ethics and compliance program.

|

|

• |

We seek to protect the human rights and civil liberties of our employees through policies, procedures, and programs that avoid risks of compulsory and child labor, both within our company and throughout our supply chain. |

|

|

• |

We foster a workplace of dignity, respect, diversity, and inclusion through our recruiting and advancement practices, internal communications, and employee resource groups. |

|

|

• |

We educate our employees annually on relevant ethics and compliance topics, publish accessible guidance on ethical issues and related company resources in our global Code of Business Conduct and Ethics, and encourage reporting of ethical concerns through any of several global and local reporting channels. |

|

|

• |

We innovate to reduce the energy used by our products, the energy used to manufacture them, and the amount of new materials required to manufacture them. |

EMPLOYEES

As of February 29, 2020, we had approximately 1,080 employees and 10 contracted workers. None of our employees or contract workers are represented by a labor union. The contracted production workers are engaged through independent temporary labor agencies.

EXECUTIVE OFFICERS

Our executive officers are as follows:

|

NAME |

|

AGE |

|

POSITION |

|

Jeffery Gardner |

|

60 |

|

Interim President and Chief Executive Officer |

|

Kurtis Binder |

|

49 |

|

Executive Vice President and Chief Financial Officer |

|

Arym Diamond |

|

41 |

|

Senior Vice President and Chief Revenue Officer |

|

Anand Rau |

|

57 |

|

Senior Vice President, Engineering |

JEFFERY GARDNER was appointed as our Interim President and CEO on March 25, 2020, and has served as a member of CalAmp’s Board since 2015. He most recently served as the President and CEO of Brinks Home Security from 2015 until February 2020. Mr. Gardner also served as President and CEO of Windstream Corporation, a leading provider of advanced network communications and technology solutions, including cloud computing and managed services. Before joining Windstream, Mr. Gardner served as Executive Vice President and CFO of Alltel Corp. Earlier in his career, Mr. Gardner held a variety of senior management positions at 360 Communications, which merged with Alltel in 1998.

13

KURTIS BINDER joined us in July 2017 and serves as our Executive Vice President and Chief Financial Officer. Prior to joining our company, he served as the Chief Financial Officer at VIZIO, Inc., a television and consumer electronics company headquartered in the United States since April 2010. Prior to joining VIZIO, Mr. Binder served as the Chief Accounting Officer for Applied Medical Resources, Inc. since December 2009. Mr. Binder was also employed in the assurance practice of Ernst & Young LLP from October 1997 to July 2009 and served as an Assurance and Advisory Business Services Partner.

ARYM DIAMOND is the Senior Vice President and Chief Revenue Officer responsible for the customer experience related to sales and support. Mr. Diamond joined CalAmp in March 2020 and brings over 20 years of experience in the enterprise software and consulting industry. Before joining CalAmp, he was part of the sales leadership team within Salesforce.com’s Einstein Analytics group where analytics and machine learning were re-imagined for the front office. Prior to that, he spent over 10 years at Oracle in various sales roles, which included being part of sales organizational alignment that came from multiple acquisitions as well as a shift from on premise to cloud-based subscriptions.

ANAND RAU is the Senior Vice President of Engineering responsible for all software and hardware product development and quality. Mr. Rau joined CalAmp in 2015 and brings 25 years of strategic management experience in delivering enterprise-class, mission-critical applications and platforms across several industry verticals including telematics, supply chain, physical resource management, industrial automation and medical products. Prior to CalAmp, Mr. Rau was the CTO at MarginPoint, a mobile inventory management and supply chain solutions company. Mr. Rau also led product development and quality assurance as Vice President of Engineering at Accruent Inc., a leader in the physical resource management vertical. He was also the co-founder and Vice President of Engineering at RiverOne (acquired by i2 technologies), where he led the team that built a supply chain solution that was adopted by companies representing approximately 25% of the global electronics industry. Rau started his career with Hewlett Packard Company in the Medical Products group, and has led the innovation and launch of technologically advanced enterprise solutions serving many markets.

Our executive officers are appointed by and serve at the discretion of the Board of Directors.

AVAILABLE INFORMATION

Our primary Internet address is www.calamp.com. We make our U.S. Securities and Exchange Commission (“SEC”) periodic reports (Forms 10-Q and Forms 10-K) and current reports (Forms 8-K) available free of charge through our website as soon as reasonably practicable after they are filed electronically with the SEC. Within the Investor Relations section of our website, we provide information concerning corporate governance, including our Corporate Governance Guidelines, Board committee charters and composition, Code of Business Conduct and Ethics, and other information. The content of our website is not incorporated by reference into this Annual Report on Form 10-K or into any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

Materials that we file with the SEC may be read and copied at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet website at http://www.sec.gov that contains reports, proxy and information statements, and other information that we file electronically with the SEC.

We operate in a rapidly changing environment that involves a number of risks and uncertainties, some of which are beyond our control. The following list describes several risk factors, which are applicable to our business and speaks as of the date of this document. These and other risks could have a material adverse effect on our business, results of operations, financial condition, and cash flows and the trading price of our common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that affect us.

14

Our accelerated supply chain diversification program, component shortages and uncertainty in international trade relations with China may adversely impact us and have a material adverse effect on our financial condition or results of operations.

We accelerated our supply chain diversification program to transition our manufacturing to tier one global contract manufacturers with facilities outside of China. This program was initiated against the backdrop of the escalation of trade tensions between the U.S. and China. These factors attributed to various supply disruptions, including component shortages, in the third and fourth quarter of fiscal 2020. Although we are taking steps to address these matters, the related operational challenges and supply chain disruptions may persist for some time.

The Coronavirus (COVID-19) pandemic could have a material adverse impact on our business, results of operations and financial condition.

In December 2019, a novel strain of coronavirus disease (“COVID-19”) was first reported in Wuhan, China. Less than four months later, on March 11, 2020, the World Health Organization declared COVID-19 a pandemic—the first pandemic caused by a coronavirus. The outbreak has reached more than 160 countries, resulting in the implementation of significant governmental measures, including lockdowns, closures, quarantines and travel bans, intended to control the spread of the virus. The COVID-19 outbreak has already caused severe global disruptions. In response to the virus, China and Italy (where we have a subsidiary in Milan) placed tens of millions of people under lockdown. Spain and France also recently implemented lockdown measures, and other countries and local governments may enact similar policies. As of April 30, 2020, the United States has temporarily restricted travel by foreign nationals into the country from a number of places, including China and Europe. In addition, on March 18, 2020, the U.S. and Canada agreed to restrict all nonessential travel across the border. We, and other companies, are also taking precautions, such as requiring employees to work remotely and imposing travel restrictions. These restrictions, and future prevention and mitigation measures, are likely to have an adverse impact on global economic conditions and consumer confidence and spending, which could materially adversely affect the supply and demand for our products and solutions. Uncertainties regarding the economic impact of COVID-19 is likely to result in sustained market turmoil, which could also negatively impact our business, financial condition and cash flows. This pandemic could negatively affect our ability to sell-through our backlog. Our ability to manage normal commercial relationships with our suppliers, contract manufacturers, and customers may suffer. Our customers could shift purchases to lower-priced or other perceived value offerings during the pandemic-caused economic downturn as a result of various factors, including workforce reductions, reduced access to credit, and changes in federal economic policy. In particular, customers may become more conservative in response to these conditions and seek to reduce their purchases and inventories. Our results of operations depend upon, among other things, our ability to maintain and increase sales volume with our existing customers, our ability to attract new consumers, and the financial condition of our customers. Decreases in demand for our products and solutions without a corresponding decrease in costs would put downward pressure on our margins and would negatively impact our financial results.

Governmental organizations, such as the U.S. Centers for Disease Control and Prevention and state and local governments, have recommended and/or imposed increased community-based interventions, including event cancellations, social distancing measures, and restrictions on gatherings of more than ten people. The governors of several states have temporarily closed bars and restaurants, and others may follow suit. As of April 30, 2020, California and New York residents were under a shelter-in-place order. On March 30, 2020, President Trump announced a shelter-in-place extension through April 30, 2020. In the future, government authorities may impose similar and/or additional restrictions on people’s movement, public gatherings and businesses. The extent of COVID-19’s effect on our operational and financial performance will depend on future developments, including the duration, spread and intensity of the outbreak, all of which are uncertain and difficult to predict considering the rapidly evolving landscape. As a result, it is not currently possible to ascertain the overall impact of COVID-19 on our business. However, if the pandemic continues to evolve into a severe worldwide health crisis, the disease could have a material adverse effect on our business, results of operations, financial condition and cash flows and adversely impact the trading price of our common stock.

15

We generally do not have long-term contracts with customers and our customers may cease purchasing our products and services at any time, which could negatively affect our business, financial condition or results of operations.

We generally do not have long-term contracts with our customers. As a result, our agreements with our customers generally do not provide us with any assurance of future sales. These customers can cease purchasing products and services from us at any time without penalty, are free to purchase products and services from our competitors, may expose us to competitive price pressure on each order and are not required to make minimum purchases. Any of these actions taken by our customers could have a material adverse effect on our business, financial condition or results of operations.

Because some of our components, assemblies and electronics manufacturing services are purchased from sole source suppliers or require long lead times, our business is subject to unexpected interruptions, which could cause our operating results to suffer.

Some of our key components are complex to manufacture and have long lead times. In the event of a reduction or interruption of supply, or degradation in quality, it could take up to six months to begin receiving adequate supplies from alternative suppliers, if any. As a result, product shipments could be delayed and revenues and profitability could suffer. Furthermore, if we receive a smaller allocation of component parts than is necessary to manufacture products in quantities sufficient to meet customer demand, customers could choose to purchase competing products and we could lose market share. Any of these events could have a material adverse effect on our business, financial condition or results of operations.

Because we depend on a few significant customers for a substantial portion of our revenues, the loss or significant decline or slowdown in growth in business of any of these customers could have an adverse effect on our business, financial condition or results of operations.

Our revenues depend on a small number of significant customers and some of them represent more than 10% of our total revenues in fiscal year 2020, 2019 and 2018 (see Note 3 to our consolidated financial statements). They are also expected to represent a substantial portion of our revenues in the near future. As a result, the loss of any one of these customers, or decline or slowdown in the growth in business of these customers, could have a material adverse effect on our business, financial condition and results of operations. In addition, because service revenue depends either partially or entirely on the usage levels of data transmission by our customers and end users, the decline or slowdown in the growth of usage patterns of these customers, which has and could continue to occur at any time and with or without a reduction in the number of our subscriber basis could have a material adverse effect on our business, financial condition and results of operations.

Dependence on a limited number of contract manufacturers and suppliers of manufacturing services and critical components within our supply chain may adversely affect our ability to bring products to market, damage our reputation and adversely affect our results of operations.

We operate a primarily outsourced manufacturing business model that utilizes contract manufacturers. We depend on a limited number of contract manufacturers to allocate sufficient manufacturing capacity to meet our needs, to produce products of acceptable quality at acceptable yields, and to deliver those products to us on a timely basis. In such circumstances, we may be unable to meet our customer demand and may fail to meet our contractual obligations. This could result in the payment of significant damages by us to our customers and our net revenue could decline, which could adversely affect our business, financial condition and results of operations. Any substantial disruption in our contract manufacturers’ supply as a result of a pandemic, natural disaster, trade wars, political unrest, economic instability, equipment failure or other cause, could materially harm our business, customer relationships and results of operations.

16

Because the markets in which we compete are highly competitive and some of our competitors have greater resources than us, we cannot be certain that our products and services will continue to be accepted in the marketplace or capture increased market share.

The markets for our products and services are intensely competitive and characterized by rapid technological change, evolving standards, short product life cycles, and price erosion. Given the highly competitive environment in which we operate, we cannot be sure that any competitive advantages currently enjoyed by our products and services will be sufficient to establish and sustain our products and services in the markets we serve. Any increase in price or other competition could result in erosion of our market share, to the extent we have obtained market share, and could have a negative impact on our financial condition and results of operations. We cannot provide assurance that we will have the financial resources, technical expertise or marketing and support capabilities to compete successfully. We expect competition to intensify in the future with the introduction of new technologies and market entrants and with the possible consolidation of competitors.

Information about our competitors is included in Part I, Item 1 of this Annual Report on Form 10-K under the heading “COMPETITION”.

If demand for our products and services fluctuates rapidly and unpredictably, it may be difficult to manage our business efficiently, which may result in reduced gross margins and profitability.

Our cost structure is based in part on our expectations for future demand. Many costs, particularly those relating to capital equipment and manufacturing overhead, are largely fixed. Rapid and unpredictable shifts in demand for our products and services may make it difficult to plan production capacity and business operations efficiently. If demand is significantly below expectations, we may be unable to rapidly reduce these fixed costs, which can diminish gross margins and cause losses. A sudden downturn may also leave us with excess inventory, which may be rendered obsolete if products and services evolve during the downturn and demand shifts to newer products and services. Our ability to reduce costs and expenses may be further constrained because we must continue to invest in research and development to maintain our competitive position and to maintain service and support for our existing customer base. Conversely, in the event of a sudden upturn, we may incur significant costs to rapidly expedite delivery of components, procure scarce components and outsource additional manufacturing processes. These costs could reduce our gross margins and overall profitability. Any of these results could adversely affect our business, financial condition or results of operations.

Any acquisitions we pursue could disrupt our business and harm our financial condition and results of operations.

As part of our business strategy, we review and intend to continue to review acquisition opportunities that we believe would be advantageous or complementary to the development of our business. In fiscal 2017, we acquired LoJack. In fiscal 2019, we acquired Tracker and in the first quarter of fiscal 2020, we acquired LoJack Mexico and Synovia, and we may acquire additional businesses, assets, or technologies in the future. If we make any acquisitions, we could take any or all of the following actions, any one of which could adversely affect our business, financial condition, results of operations or share price:

|

|

• |

use a substantial portion of our available cash; |

|

|

• |

require a significant devotion of management’s time and resources in the pursuit or consummation of any acquisition; |

|

|

• |

incur substantial debt, which may not be available to us on favorable terms and may adversely affect our liquidity; |

|

|

• |

issue equity or equity-based securities that would dilute existing stockholders’ ownership percentage; |

|

|

• |

assume contingent liabilities; and |

|

|

• |

take substantial charges in connection with acquired assets. |

17

Acquisitions also entail numerous other risks, including, without limitation: difficulties in assimilating acquired operations, products, technologies and personnel; unanticipated costs; diversion of management’s attention from existing operations; risks of entering markets in which we have limited or no prior experience; and potential loss of key employees from either our existing business or the acquired organization. Acquisitions may result in substantial accounting charges for restructuring and other expenses, amortization of purchased technology and intangible assets and stock-based compensation expense, any of which could materially and adversely affect our operating results. We may not be able to realize the anticipated benefits of or successfully integrate with our existing business the businesses, products, technologies or personnel that we acquire, and our failure to do so could harm our business and operating results.

Any acquisitions we make and industry consolidation could adversely affect our existing business relationships with our suppliers and customers.

If we make any acquisitions, our existing business relationships with our suppliers and customers could be adversely affected. Moreover, our industry is being affected by the trend toward consolidation and the creation of strategic relationships. If we are unable to successfully adapt to this rapidly changing environment, we could suffer a reduction in the volume of business with our customers and suppliers, or we could lose customers or suppliers entirely, which could materially and adversely affect our financial condition and operating results.

Our success depends on the attraction and retention of senior management and technical personnel with relevant expertise.

As a competitor in a highly technical market, we depend heavily upon the efforts of our existing senior management and technical teams. The loss of the services of one or more members of these teams could slow product and services development and commercialization objectives. Due to the specialized nature of our products and services, we also depend upon our ability to attract and retain qualified technical personnel with substantial industry knowledge and expertise. Competition for qualified personnel is intense, and we may not be able to continue to attract and retain qualified personnel necessary for the development of our business.

Our business is subject to many factors that could cause our quarterly or annual operating results to fluctuate and our stock price to be volatile.

Our quarterly and annual operating results have fluctuated in the past and may fluctuate significantly in the future due to a variety of factors, many of which are outside of our control. A majority of our product orders are shipped in the final month of the quarter and a significant amount in the last two weeks of the quarter. Some of the other factors that could affect our quarterly or annual operating results include:

|

|

• |

the timing and amount, or cancellation or rescheduling, of orders for our products or services; |

|

|

• |

our ability to develop, introduce, ship and support new products, services and enhancements, and manage product and services transitions; |

|

|

• |

announcements of new product and service introductions and reductions in the price of products and services offered by our competitors; |

|

|

• |

our ability to achieve cost reductions; |

|

|

• |

our ability to obtain sufficient supplies of sole or limited source components for our products; |

|

|

• |

our ability to achieve and maintain production volumes and quality levels for our products; |

|

|

• |

our ability to maintain the volume of products and services sold and the mix of distribution channels through which they are sold; |

|

|

• |

the loss of any one of our major customers or a significant reduction in orders from those customers; |

|

|

• |

increased competition, particularly from larger, better capitalized competitors; |

|

|

• |

fluctuations in demand for our products and services; and |

|

|

• |

changes in telecommunications and wireless market conditions specifically and economic conditions generally, including as a result of a pandemic or other catastrophic event. |

18