Attached files

| file | filename |

|---|---|

| EX-31 - CERTIFICATIONS PURSUANT TO RULE 13A-14(A) UNDER THE SECURITIES EXCHANGE ACT - Alpha Metallurgical Resources, Inc. | a1231201910-kaexhibit31.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K/A

(Amendment No. 1)

(Mark One) | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-38735

CONTURA ENERGY, INC.

(Exact name of registrant as specified in its charter)

Delaware | 81-3015061 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

340 Martin Luther King Jr. Blvd. | ||

Bristol, Tennessee 37620 | ||

(Address of principal executive offices, zip code) | ||

(423) 573-0300 | ||

(Registrant’s telephone number, including area code) | ||

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, par value $0.01 per share | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Sec.232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | x | |

Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Emerging growth company | ¨ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ¨Yes x No

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock | CTRA | New York Stock Exchange |

The aggregate market value of the Common Stock held by non-affiliates of the registrant (excluding outstanding shares beneficially owned by directors, executive officers, and other affiliates) on June 30, 2019, was approximately $600 million based on the closing price of the Company’s common stock as reported that date on the New York Stock Exchange of $51.90 per share. Such assumptions should not be deemed to be conclusive for any other purpose.

Number of shares of the registrant’s Common Stock, $0.01 par value, outstanding as of February 29, 2020: 18,259,421

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE

Contura Energy, Inc. (the "Company," "we," "us" or "our") filed its Annual Report on Form 10-K for the fiscal year ended December 31, 2019 ("Form 10-K") with the U.S. Securities and Exchange Commission ("SEC") on March 18, 2019. We are filing this Amendment No. 1 to the Form 10-K ("Form 10-K/A") solely for the purpose of including in Part III the information that was to be incorporated by reference from our definitive proxy statement for the 2020 annual meeting of stockholders. This Form 10-K/A hereby amends and restates in their entirety the Form 10-K cover page and Items 10 through 14 of Part III.

Pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, as amended, this Form 10-K/A also contains new certifications by the principal executive officer and the principal financial officer as required by Section 302 of the Sarbanes-Oxley Act of 2002. Accordingly, Item 15(a)(3) of Part IV is amended to include the currently dated certifications as an exhibit. Because no financial statements have been included in this Form 10-K/A and this Form 10-K/A does not contain or amend any disclosure with respect to Items 307 and 308 of Regulation S-K, paragraphs 3, 4 and 5 of the certifications have been omitted. No other amendments were made to Item 15 of Part IV.

Except as expressly noted in this Form 10-K/A, this Form 10-K/A does not reflect events occurring after the original filing of our Form 10-K or modify or update in any way any of the other disclosures contained in our Form 10-K including, without limitation, the financial statements. Accordingly, this Form 10-K/A should be read in conjunction with our Form 10-K and our other filings with the SEC.

TABLE OF CONTENTS | ||

3

Part III

Item 10. Directors, Executive Officers and Corporate Governance

ABOUT OUR MANAGEMENT TEAM

Contura is led by David J. Stetson, our chairman and chief executive officer. In addition to Mr. Stetson, whose detailed biography appears below under “Our Directors”, the following persons comprise the Company’s management committee.

Charles Andrew Eidson (44) has served as Contura’s executive vice president and chief financial officer since July 2016. From May 2019 until July 2019 he also served as interim co-chief executive officer of Contura. He previously served as executive vice president and chief financial officer of Alpha Natural Resources, Inc. prior to its emergence from bankruptcy proceedings in 2016 (“Predecessor Alpha”), a position he held from March 2016. Predecessor Alpha filed voluntary petitions for relief under Chapter 11 of the United States Bankruptcy Code on August 3, 2015. Before that Mr. Eidson was Predecessor Alpha’s senior vice president for strategy and business development from 2015 and vice president for mergers and acquisitions from 2014. Prior to joining Predecessor Alpha in July 2010, he held several financial positions across industry sectors, including at PricewaterhouseCoopers LLP, Eastman Chemical Company and Penn Virginia Resource Partners, where he led mergers and acquisitions projects for the coal segment and managed the budgeting and planning process. Mr. Eidson holds a bachelor of science degree, cum laude, in commerce and business administration from the University of Alabama and a master of business administration degree from Milligan College.

Roger L. Nicholson (59) has served as executive vice president, general counsel and secretary of Contura since December 2019. Prior to joining Contura, he practiced law as a member of Steptoe & Johnson PLLC’s Charleston office from 2015. Mr. Nicholson previously served as senior vice president, secretary and general counsel at International Coal Group, Inc. (“ICG”). Prior to his post at ICG, Mr. Nicholson served as vice president, secretary and general counsel of Massey Energy Company, in various roles in private practice and at Arch Mineral Corporation (now Arch Coal, Inc.). Mr. Nicholson holds a bachelor of arts degree from Georgetown College and earned his juris doctor degree from the University of Kentucky.

Jason E. Whitehead (42) has served as executive vice president and chief operating officer of Contura since August 2019. He was previously chief operating officer and senior vice president – operations for Alpha Natural Resources Holdings, Inc. from July 2016 until November 2018, and as vice president – operations of Predecessor Alpha from November 2012. Mr. Whitehead previously served in operations and operations-support roles, including executive roles, with Predecessor Alpha, Massey Energy Company and numerous other coal companies. He also served as an operations consultant to Contura from December 2018 through April 2019. Mr. Whitehead holds bachelor of science degrees from Bluefield State College in civil engineering technology and architectural engineering technology and a master’s degree in business administration from the University of Charleston.

ABOUT OUR BOARD OF DIRECTORS

OUR DIRECTORS

Albert E. Ferrara, Jr. (71) has served as one of Contura’s directors since July 2016 and is chair of the board’s audit committee. Mr. Ferrara has spent over forty years in the metals and related resource industry. He served in senior executive positions with AK Steel, including senior vice president finance and chief financial officer, from 2003 until his retirement in 2013. Before joining AK Steel, Mr. Ferrara spent thirty years with United States Steel Corporation/USX Corporation in a variety of roles domestically and internationally, including senior vice president - finance and treasurer. He has served since 2014 as a principal of Amelia Metals LLC, a consulting firm specializing in the metals and mining industries. Mr. Ferrara holds a bachelor of science in commerce with distinction and a juris doctor degree, both from the University of Virginia. He has been licensed to practice law in the State of Pennsylvania. For these reasons, Contura believes Mr. Ferrara is qualified to serve as a director.

Daniel J. Geiger (70) has served on Contura’s board of directors since November 2018 and is chair of the board’s safety, health and environmental committee. He previously served on the board of directors of each of ANR, Inc. and Alpha Natural Resources Holdings, Inc. after joining each in February 2018. Mr. Geiger has been a managing member of D.J. Geiger & Co., LLC, a mining consulting firm, since 2010. During his time as a managing member, from 2011 to 2012, Mr. Geiger was also the lead independent director for Lipari Energy, a major coal producer in Eastern Kentucky and a publicly traded company at that time. Prior to those positions, Mr. Geiger was the chief executive officer and chairman for Lexington Coal Company from August 2004 to July 2010. During his tenure at Lexington Coal Company, Mr. Geiger oversaw the reduction of reclamation liabilities and the eventual merger of the company into a subsidiary of a national coal production company. From 1982 to 2004, Mr. Geiger served as vice president, engineering of the James River Coal Company, and has over 35 years of experience in the coal industry. Mr. Geiger earned a bachelor of science degree in civil engineering from Ohio University, and is a registered

4

professional engineer in the states of Kentucky and West Virginia. For these reasons, Contura believes Mr. Geiger is qualified to serve as a director.

John E. Lushefski (64) has served on Contura’s board of directors since November 2018. He is the board’s lead independent director and chair of its nominating and corporate governance committee. He previously served on the board of directors of each of ANR, Inc. and Alpha Natural Resources Holdings, Inc. after joining each in July 2016. Most recently, Mr. Lushefski served as senior vice president and chief financial officer of Patriot Coal Corporation from 2012 to 2015, where he also served on the board of directors. Mr. Lushefski previously held numerous management and advisory positions with several large companies. He was a partner at BVisions Advisory LLP and served as chief financial officer for both Millennium Chemicals Inc. and Peabody Holding Company Inc. Additionally, Mr. Lushefski served on the board of directors of Suburban Propane, LP and Smith Corona Corporation and on the governance committee of Equistar Chemicals, L.P. He also acted as an advisory board member for East Coast Power Systems, Inc. and Restricted Stock Systems, Inc. Mr. Lushefski is a certified public accountant and received his bachelor of science degree in business administration and accounting from Pennsylvania State University. For these reasons, Contura believes Mr. Lushefski is qualified to serve as a director.

Emily S. Medine (64) has served on Contura’s board of directors since September 2019 and is chair of the compensation committee of the board. Ms. Medine has over three decades of experience in the coal practice at Energy Ventures Analysis, Inc. (“EVA”), where she currently serves as principal. At EVA, Ms. Medine has advised U.S. and foreign coal consumers regarding, among other matters, coal markets, coal supply, fuel procurement strategies and sales and acquisitions of coal-related assets. Ms. Medine is also experienced in investment analysis, contract negotiations, procurement audits, and bankruptcy support. In addition, Ms. Medine has developed forecasts of U.S. and global solid fuel demand and prices for alternative coal types, coke and market segments. Prior to joining EVA, Ms. Medine held various sales and strategic analysis positions at CONSOL Energy, Inc. Ms. Medine earned a bachelor of arts degree in geography, magna cum laude, from Clark University, where she was a member of Phi Beta Kappa, and a master of public affairs degree from Princeton University. For these reasons, Contura believes Ms. Medine is qualified to serve as a director.

David J. Stetson (63) has served on Contura’s board of directors since November 2018. He previously served as chairman of the board of directors of each of ANR, Inc. and Alpha Natural Resources and Holdings, Inc. after joining each in July 2016. Mr. Stetson is a seasoned executive with extensive experience in management, finance, mergers and acquisitions, corporate governance, restructuring, the law and reclamation. Mr. Stetson has held a myriad of leadership positions, including chief executive officer, chief restructuring officer, and senior advisor for various energy companies, including Trinity Coal Corporation, Lexington Coal Company, and Lipari Energy Inc. Mr. Stetson earned a master of business administration degree from the University of Notre Dame, a juris doctor degree from the Brandeis School of Law at the University of Louisville, and a bachelor of science degree from Murray State University. For these reasons, Contura believes Mr. Stetson is qualified to serve as a director.

Scott D. Vogel (44) has served on Contura’s board of directors since December 2019. Mr. Vogel is managing member of Vogel Partners, LLC, a private investment and advisory firm. Before establishing his own firm, Mr. Vogel served for 14 years as managing director at Davidson Kempner Capital Management. Mr. Vogel also worked at MPF Investors as well as at the investment banking group at Chase Securities. He has served on numerous boards over the course of his career, including Arch Coal, Key Energy Services and Seadrill Ltd. Mr. Vogel currently serves on the boards of directors of Avaya, Bonanza Creek Energy and Longview Power, which is a customer of Contura. He received a bachelor’s degree from Washington University and a master of business administration degree from The Wharton School at the University of Pennsylvania. For these reasons, Contura believes Mr. Vogel is qualified to serve as a director.

Chairman of the Board

In addition to his service as chief executive officer, Mr. Stetson is also the chairman of our board of directors. The board of directors believes that unifying the roles of chairman and chief executive officer creates important efficiencies both for the management of the Company and the operation of the board. The chairman presides at all meetings of the board and stockholders. In addition, the chairman performs such other duties as are prescribed by our governing documents or that may be assigned to him by the board from time to time, including, but not limited to:

• | providing leadership to the board; |

• | approving the schedule and agenda for board meeting(s) as well as information to be sent to the board, determining whether there are major risks which the board should focus upon at the meeting(s), and facilitating communication among the directors; and |

• | directing the calling of a special meeting of the board or of the independent members of the board. |

5

Lead Independent Director

Mr. Lushefski currently serves as our board’s lead independent director. Contura’s bylaws provide that, when the chairman of the board of directors is not an independent director, the board should elect a lead independent director who has served as a director of the Company for at least one year. The Company believes that such a structure is most appropriate under those circumstances. The lead independent director has the following duties and powers:

• | serving as the liaison between the independent members of the board and the chairman; |

• | presiding at all meetings of the board of directors at which the chairman is not present, including executive sessions and meetings of non-management directors and/or independent directors; |

• | approving the agendas for board meetings and the meeting schedule to assure that there is sufficient time for discussion of all agenda items; |

• | reviewing information to be sent to the board; |

• | reviewing with the chairman whether there are major risks which the board should focus upon at such meetings; |

• | facilitating communication among the independent directors (with the chairman); |

• | directing the chief executive officer or corporate secretary to call a special meeting of the board or of the independent members of the board; |

• | consulting and communicating directly with major stockholders, when requested by management and when it is appropriate to do so; and |

• | performing such other duties as may from time to time be delegated to the lead independent director by the board. |

BOARD AND ITS COMMITTEES

Our board of directors has four standing committees: (i) an audit committee, (ii) a compensation committee, (iii) a nominating and corporate governance committee, and (iv) a safety, health and environmental committee. Each of the directors serving on these committees has been determined by the board of directors to be independent within the meaning of SEC and NYSE regulations, with the exception of Mr. Stetson, who serves on the safety, health and environmental committee. Each of these committees has adopted and acts according to a written charter. Stockholders may obtain a copy of each charter, at no cost, either on our website, www.conturaenergy.com, or upon written request to William L. Phillips III, Assistant Secretary, Contura Energy, Inc., 340 Martin Luther King, Jr. Blvd., Bristol, Tennessee 37620 (overnight courier) or P.O. Box 848, Bristol, Tennessee 37621 (U.S. mail). From time to time, our board of directors may also form special ad hoc committees to which it may delegate certain authority to administer particular duties of the board.

The board of directors held 26 meetings in 2019, either in person or by telephone. Each currently serving director attended at least 75% of the aggregate of the total number of meetings of the board of directors in 2019 (held during the periods for which he or she served as a director) and the total number of meetings held by each committee on which he or she served in 2019 (during the period that he or she served). The table below shows the committees on which each of our directors sits and the number of committee meetings held by each committee in 2019.

Audit | Compensation | Nominating and Corporate Governance | Safety, Health and Environmental | |

Albert E. Ferrara | C | M | M | M |

Daniel J. Geiger | M | M | M | C |

John E. Lushefski | M | M | C | M |

Emily S. Medine | C | M | ||

David J. Stetson | M | |||

Scott D. Vogel | M | M | ||

Meetings held in 2019 | 9 | 13 | 8 | 3 |

(C) | Committee chair |

(M) | Committee member |

Under Contura’s Corporate Governance Guidelines, directors are expected to attend stockholder meetings. All then-serving directors attended the 2019 annual meeting of stockholders. A copy of Contura’s Corporate Governance Guidelines is available at no cost either through our website, www.conturaenergy.com, or upon written request to William L. Phillips III, Assistant

6

Secretary, Contura Energy, Inc., 340 Martin Luther King, Jr. Blvd., Bristol, Tennessee 37620 (overnight courier) or P.O. Box 848, Bristol, Tennessee 37621 (U.S. mail).

Although the NYSE rules require only that the board of directors have standing audit, compensation and nominating and corporate governance committees, the board feels that it is important to maintain a safety, health and environmental committee to oversee the Company’s policies and procedures regarding these matters.

Audit Committee

Our audit committee consists of three directors: Messrs. Ferrara, Lushefski, and Geiger, with Mr. Ferrara serving as chair. Our board of directors has determined that all current members of the audit committee are financially literate under current listing standards of the NYSE. Further, our board has determined that all current members of the committee are independent within the meaning of SEC and NYSE regulations and that Mr. Ferrara qualifies as an “audit committee financial expert.”

The audit committee assists the board of directors in monitoring the quality, reliability and integrity of our accounting policies and financial statements, overseeing our compliance with legal and regulatory requirements and reviewing the independence, qualifications and performance of our internal and independent auditors. Among other matters enumerated in the audit committee charter, the committee is generally responsible for:

• | Appointing and compensating our independent auditors, including authorizing their scope of work and approving any non-audit services to be performed by them with respect to each fiscal year; |

• | Reviewing and discussing our annual audited and quarterly unaudited financial statements with our management and independent auditors, as well as a report by the independent auditor describing the firm’s internal quality control procedures, any material issues raised by the most recent internal quality control review, or peer review, of the auditing firm, and all relationships between us and the independent auditor; and |

• | Reviewing our financial press releases, as well as other financial information and earnings guidance, if given, provided to analysts and rating agencies. |

Committee Meetings

The audit committee meets at scheduled times during the year, typically prior to quarterly board meetings. However, other scheduled meetings may be conducted in person or telephonically, depending on the work tasks of the committee. The agendas for meetings are initially prepared by the general counsel in consultation with the committee’s chairman, and are also provided for comments to the chairman of the board of directors and the chief executive officer and, at times, other legal counsel. Typically, the chief executive officer, the chief financial officer, the general counsel and the leader of the Company’s internal audit function, as well as certain other members of management and representatives of the independent auditor, are invited to attend audit committee meetings. Other members of the board of directors who are not members of the audit committee also often attend its meetings. The attendance of the chief executive officer and certain other officers, principally the chief financial officer, allows the audit committee to make detailed inquiries into matters for which it is responsible and assists the committee in making informed decisions. Following regularly scheduled meetings, the committee meets privately with the independent auditor and then with the head of the Company’s internal audit function. At times it also meets privately with the chief financial officer. The actions of the audit committee are recorded in the minutes of its meetings. The committee chairman reports to the board as appropriate regarding the committee’s actions and recommendations.

CODE OF BUSINESS ETHICS

Contura has adopted a Code of Ethics that applies to all employees (including senior financial employees), officers (including the chief executive officer and chief financial officer), and directors. The Code of Ethics is available at no cost either through Contura’s website, www.conturaenergy.com, or upon written request to William L. Phillips III, Assistant Secretary, Contura Energy, Inc., 340 Martin Luther King, Jr. Blvd., Bristol, Tennessee 37620 (overnight courier) or P.O. Box 848, Bristol, Tennessee 37621 (U.S. Mail). Any amendments to, or waivers from, a provision of our Code of Business Ethics that applies to our principal executive officer, principal financial and accounting officer or persons performing similar functions and that relates to any element of the code of ethics enumerated in paragraph (b) of Item 406 of Regulation S-K shall be disclosed by posting on our website. Information on or accessible through our website is not incorporated by reference into this Form 10-K.

DELINQUENT SECTION 16(a) REPORTS

Section 16(a) of the Exchange Act requires Contura’s directors and executive officers and persons who own more than 10% of a registered class of Contura’s equity securities, to file with the SEC initial reports of ownership and reports of changes in ownership of Contura’s equity securities. Contura endeavors to assist reporting persons in making these filings. Based solely on its review of the reports filed with the SEC during 2019, Contura believes that all reporting requirements under Section

7

16(a) for the fiscal year ended December 31, 2019 were met in a timely manner by its directors, executive officers, and greater than 10% beneficial owners, except for: (1) one late Form 4 for each of Mr. Crutchfield, Mr. Eidson, Mr. Kreutzer, Mr. Manno and Kevin Stanley, relating to the withholding of shares in satisfaction of tax obligations on March 7, 2019, (2) one late Form 4 for each of Jill Harrison and Suzan Moore relating to the February 9, 2019 vesting of RSUs and associated withholding of shares in satisfaction of tax obligations, (3) one late Form 4 on behalf of Mr. Crutchfield relating to two option exercises and the associated sale of shares pursuant to a 10b5-1 plan on April 18, 2019, (4) one late Form 4 relating to the sale of shares pursuant to 10b5-1 plans for each of Mr. Eidson and Mr. Kreutzer on March 13, 2019, Mr. Geiger on March 15, 2019 and Mr. Crutchfield on March 21, 2019, and (5) one late Form 4 for Mr. Stetson relating to a July 29, 2019 grant of RSUs. Most of these delinquent filings were the result of the failure of the Company’s third party administrator to provide timely notifications to Contura regarding the occurrence of transactions. Contura subsequently took additional measures to ensure that the administrator provided timely notifications in connection with future transactions.

Item 11. Executive Compensation

DIRECTOR COMPENSATION

2019 Director Compensation

Pursuant to our Amended and Restated Non-Employee Director Compensation Policy (the “Director Policy”), we currently provide annual compensation to our non-employee directors based on an annual May 1st through April 30th compensation period (each period, a “Compensation Year”). For the Compensation Year that commenced on May 1, 2018 and the Compensation Year that commenced on May 1, 2019 (the “2019 Compensation Year”), each of our non-employee directors serving at such time received an annual equity award with a grant date fair market value of $100,000 granted in the form of restricted stock units (“RSUs”), and an annual cash retainer of $75,000. Annual cash retainers are paid in quarterly installments in arrears. For any non-employee directors appointed to the board following the commencement of a Compensation Year, the director’s cash retainer will be pro-rated for any partial quarter of service, and the compensation committee will determine in its discretion whether such director receives a full or pro-rated annual RSU retainer or a special grant of RSUs. Non-employee directors generally have the opportunity to elect to receive RSUs in lieu of the annual cash retainer. For the 2019 Compensation Year, Mr. Ward elected to receive RSUs in lieu of the $75,000 annual cash retainer.

In addition to the annual retainer, for each Compensation Year non-employee directors are entitled to receive meeting fees and additional cash retainers in connection with service as a chair or member of a committee of our board, as set forth in the following chart.

Position | Annual Fee ($) | ||

Non-Employee Chairman of the Board | 75,000 | ||

Lead Independent Director if Employee Director is Chairman of the Board | 20,000 | ||

Audit Committee Chair | 30,000 | ||

Compensation Committee Chair | 20,000 | ||

Safety, Health and Environmental Committee Chair | 15,000 | ||

Nominating and Corporate Governance Committee Chair | 12,000 | ||

Non-employee directors earn a committee retainer of $5,000 per Compensation Year for each committee on which the director serves in a non-chair capacity. Non-employee directors are also eligible to earn a meeting fee of $2,000 for each board meeting attended and a fee of $500 for each committee meeting attended, in each case, beginning with the fifth such meeting attended during the applicable Compensation Year.

Non-employee directors’ annual equity awards are currently granted in the form of RSUs. These awards are granted pursuant to RSU agreements that generally provide for vesting on the day immediately preceding the first anniversary of the grant date. The awards will accelerate and vest in full in connection with a change in control of Contura or if the director ceases to serve as a member of our board as a result of permanent disability or death. Unvested RSUs are forfeited upon a separation from service for any other reason.

Additionally, we reimburse non-employee directors for travel expenses incurred in connection with attending board, committee and stockholder meetings and for other business-related expenses in accordance with our reimbursement policies, as they may be amended from time to time.

Annual equity awards for the 2019 Compensation Year were made on May 1, 2019 for the non-employee directors serving on such date. In connection with her appointment to the board in September 2019, Ms. Medine received a pro-rated annual RSU award and pro-rated cash retainer for the then-current quarter of service. In connection with his appointment to the board

8

in December 2019, Mr. Vogel received a pro-rated cash retainer for the then-current quarter of service, and in March 2020, he received a pro-rated annual RSU award based on his service beginning in December 2019.

During his service as chief executive officer, Mr. Crutchfield served as a member of our board and did not receive any additional compensation in connection with his service on our board. Mr. Stetson, who became our chief executive officer and an employee director in July 2019, had previously served as a non-employee director of our board from January 2019 through April 2019, and received compensation under the Director Policy in connection with that service. Mr. Stetson does not receive additional compensation in connection with his service as an employee director. The compensation paid to Mr. Crutchfield for his service as chief executive officer, and the compensation paid to Mr. Stetson for his service as both a non-employee director and as chief executive officer, are reported in the Summary Compensation Table and the tables that follow.

Director Stock Ownership Guidelines

To align our non-employee directors’ and executive officers’ interests with those of our stockholders, the board adopted stock ownership guidelines applicable to Contura’s non-employee directors and executive officers effective August 13, 2019 (the “Ownership Guidelines”). Generally, non-employee directors must accumulate and maintain equity ownership in Contura within five years of becoming a director with a value of no less than five times their annual cash retainer (not including meeting fees or committee chair or member compensation). In determining if a non-employee director has satisfied the Ownership Guidelines, all stock and equity interests beneficially owned by the director, or to which the director is otherwise entitled, are taken into consideration, including, without limitation, any unvested equity grants. For purposes of the Ownership Guidelines, equity ownership is measured following the end of each fiscal year of the Company, based on the average daily stock price of our common stock during the December of such fiscal year. The nominating and corporate governance committee is responsible for the administration and interpretation of the Ownership Guidelines. For a description of the Ownership Guidelines applicable to executive officers, see “Executive Stock Ownership Guidelines”.

No Hedging/Pledging Policies

The Company has adopted an insider securities trading policy that prohibits directors, officers and certain other employees from engaging in hedging transactions involving Company securities such as short selling, buying or selling publicly traded options (including puts and calls), zero-cost collar, and forward sales contracts. The policy also prohibits the holding by these persons of Contura securities in a margin account or pledging Contura securities as collateral for a loan.

2019 Director Compensation Table

The following table sets forth information concerning the compensation to our non-employee directors in respect of the fiscal year ended December 31, 2019. As noted above, the compensation paid to Mr. Stetson for his service as a non-employee director from January 2019 through April 2019 is reported in the Summary Compensation Table of this Form 10-K/A.

Name | Fees Earned or Paid in Cash ($) (1) | Stock Awards ($) (2) | Total ($) | ||||||

Albert E. Ferrara, Jr. | 167,000 | 99,965 | 266,965 | ||||||

Daniel J. Geiger | 116,500 | 99,965 | 216,465 | ||||||

John E. Lushefski | 193,548 | 99,965 | 293,513 | ||||||

Emily S. Medine (3) | 35,598 | 63,635 | 99,233 | ||||||

Scott D. Vogel (3) | - | - | - | ||||||

Anthony J. Orlando | 129,696 | 99,965 | 229,661 | ||||||

Harvey L. Tepner | 146,244 | 99,965 | 246,209 | ||||||

Neale X. Trangucci | 184,696 | 99,965 | 284,661 | ||||||

Michael J. Ward | 34,000 | 174,910 | 208,910 | ||||||

(1) | Reflects the annual cash retainer and any meeting fees and additional cash retainers paid in connection with service as a chair or member of a committee of our board, in each case for service during our fiscal year ended December 31, 2019. |

(2) | The values in this column are based on the aggregate grant date fair values of awards computed in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification, (“ASC”) Topic 718, “Compensation-Stock Compensation” (“FASB ASC Topic 718”). The values set forth in this column relate to the following: (i) 1,774 RSUs granted on May 1, 2019, to each of Messrs. Ferrara Jr., Orlando, Ward, Trangucci, Geiger, Lushefski and Tepner in connection with their annual equity awards for the 2019 Compensation Year (each with a grant date fair value of $56.35 per share); (ii) 1,330 RSUs granted to Mr. Ward on May 1, 2019, which he elected to receive in lieu of his annual cash retainer for the 2019 Compensation Year (with a grant date fair value of $56.35 per share), and (iii) 2,208 RSUs granted on September 26, 2019, to Ms. Medine, which reflected a pro-rata portion of her annual equity award for the 2019 Compensation Year (with a grant date fair value of $28.82 per share). The |

9

RSUs in the prior sentence reflect all outstanding RSUs held by Messrs. Ferrara, Geiger and Lushefski and Ms. Medine as of December 31, 2019. Upon their resignations from the board on August 12, 2019, Messrs. Orlando, Tepner, Trangucci and Ward forfeited all of their respective unvested RSUs.

(3) | Ms. Medine and Mr. Vogel were appointed to the board on September 9, 2019 and December 20, 2019, respectively. |

COMPENSATION COMMITTEE REPORT

The compensation committee has reviewed and discussed the “Compensation Discussion and Analysis” section of this Form 10-K/A with management. Based on its review and discussion with management, the compensation committee recommended to the board that the “Compensation Discussion and Analysis” section be included in this Form 10-K/A.

Emily S. Medine, Chair |

Albert E. Ferrara, Jr. |

Daniel J. Geiger |

John E. Lushefski |

Scott D. Vogel |

EXECUTIVE COMPENSATION

COMPENSATION DISCUSSION AND ANALYSIS

Compensation of our named executive officers (“NEOs”) is determined under our compensation program for executive officers. This program is overseen by the compensation committee, which determines the compensation of our executive officers.

The following discussion relates to the compensation of our NEOs whose compensation is disclosed in the tables that follow, as well as the overall principles underlying our executive compensation policies. Our NEOs for the fiscal year ended December 31, 2019 are:

• | David J. Stetson, who was named Chief Executive Officer (“CEO”) on July 29, 2019, |

• | Charles Andrew Eidson, Executive Vice President (“EVP”) and Chief Financial Officer, who also served as Interim Co-Chief Executive Officer from May 7, 2019 through July 28, 2019, and |

• | Jason Whitehead, who was named EVP and Chief Operating Officer on August 14, 2019. |

The discussion below also includes compensation information regarding the following former executive officers:

• | Kevin S. Crutchfield, Chief Executive Officer until May 6, 2019, |

• | Mark M. Manno, EVP, Chief Administrative and Legal Officer and Secretary until December 1, 2019, who also served as Interim Co-Chief Executive Officer from May 7, 2019 through July 28, 2019, |

• | J. Scott Kreutzer, EVP and Chief Operating Officer until November 15, 2019, and |

• | Kevin Stanley, EVP and Chief Commercial Officer until November 15, 2019. |

Roger L. Nicholson was named EVP, General Counsel and Secretary on December 2, 2019. Because his total compensation for 2019 did not exceed $100,000 Mr. Nicholson is not an NEO for the fiscal year ended December 31, 2019, in accordance with SEC rules.

2019 CEO Transition and Search Process

In April 2019, Kevin S. Crutchfield, our chief executive officer informed the board of directors that he intended to resign as chief executive officer on May 6, 2019 in order to pursue an opportunity outside of the coal industry.

Shortly thereafter, the board of directors retained a nationally-recognized executive placement firm and launched a comprehensive search process to identify a permanent chief executive officer. While that search was ongoing, the board also appointed Mr. Eidson, our chief financial officer, and Mr. Manno, then our chief administrative and legal officer and secretary, to serve as interim co-chief executive officers during the search, effective May 7, 2019.

On May 2, 2019, the compensation committee of the board approved changes to the compensation arrangements for each of Messrs. Eidson and Manno, effective as of May 7, 2019, to recognize the additional responsibilities each executive would take on in accepting the position of interim co-chief executive officer while also maintaining his current position and responsibilities, as well as to help ensure the executive’s retention as an executive of the Company. These changes are described in “2019 Executive Retention Awards” below.

10

Following reviews of, and interviews with, numerous candidates, on July 29, 2019, the Company announced that the board of directors had unanimously appointed Mr. Stetson as the Company’s new chief executive officer and a member of the board of directors. Mr. Stetson was selected after considering his familiarity with the Company’s operational assets, and his robust executive experience, strategic ability and natural leadership talent.

Compensation Executive Summary

Our executive compensation programs are designed to attract, retain and reward executives who create long-term stockholder value, share our mission, and perform in a manner that enables the Company to achieve its strategic goals. Our compensation programs provide a market-based total compensation program tied to financial and operating performance and aligned with the interests of our stockholders. Our compensation programs reflect, reinforce and communicate our commitment to operate safely, responsibly and ethically, and continually strive to improve and deliver quality in everything we do.

• | Our executive compensation programs are administered by our compensation committee, which is composed of independent directors appointed by our board. The compensation committee has the responsibility to review and approve executive and director compensation and ensure that our programs align with our policies and philosophies. |

• | Variable compensation, both short- and long-term, comprises the majority of the compensation opportunities for our executive team. Long-term compensation opportunity is emphasized over short-term opportunity to encourage executive retention and to align our executives’ interests with long-term results. |

• | The Contura Energy, Inc. Annual Incentive Bonus Plan (described in “2019 Annual Bonuses” below) measures both financial and operational performance goals, with an emphasis on financial measures. All executives have identical goals, consistent with our belief in the importance of teamwork among our leadership team. Pay for performance is emphasized through a plan design that includes a threshold performance level, with upside should performance exceed expectations, and by establishing maximum incentive payouts. |

• | Long-term incentives are a significant component of our total reward program. The opportunity for executives to earn equity awards, over time, aligns our executive team with the interests of our stockholders. The long-term compensation design is based on a portfolio approach, which, prior to 2019, consisted of RSUs subject to three-year time-based vesting schedules, stock options and restricted stock. In 2019, to more closely align our executives’ payments to shareholder returns, we introduced into our long-term incentive program grants of performance-based restricted stock units (“PSUs”) with three-year cliff-vesting based on the achievement of company performance metrics over a three-year performance period. |

• | We use limited perquisites to enable us to attract and retain executive talent and further our business goals. These perquisites may include special arrangements (such as the Deferred Compensation Plan described in “Deferred Compensation” below) when existing tax-qualified retirement plans are subject to limitations on benefits under the Internal Revenue Code or when significant competitive gaps exist in comparison to our industry peers. |

• | We believe our executives should own stock in the Company and have therefore adopted stock ownership guidelines applicable to our non-employee directors and executive officers. |

• | Our severance and change in control policies generally include a double trigger payout approach and do not employ tax gross-ups (in the case of a change in control or otherwise). |

Executive Compensation Process

Compensation Committee’s Role in Determining Executive Compensation

The compensation committee is responsible for ensuring that the Company’s executive compensation policies and programs reflect the short- and long-term interests of the Company’s stockholders and are competitive in the markets in which the Company competes for talent. The compensation committee reviews and approves the design of the compensation program, compensation levels, and benefit programs for the NEOs. When appropriate, the compensation committee consults with other board committees, such as the safety, health and environmental committee to determine appropriate performance targets that relate to the Company’s non-financial achievements.

In connection with the appointments of Mr. Stetson as CEO in July 2019 and Mr. Whitehead as chief operating officer in August 2019, the compensation committee, with the assistance of Pearl Meyer, reviewed and approved the annual target compensation levels of the executives based on market data.

11

The compensation committee is committed to ensuring that our compensation and benefit programs are aligned with our values and business strategy by reviewing and analyzing the competitiveness of our executive compensation programs and our performance. Each key component of compensation (base salary, short- and long-term incentives) is reviewed for both internal equity and, when appropriate comparisons are available, for external competitiveness based on industry peers and published survey data.

At the 2019 annual meeting, our shareholders approved the 2018 compensation of our NEOs by approximately 93% of the votes cast. In making decisions with respect to 2019 and 2020 compensation, the compensation committee, with the assistance of its independent compensation consultant, has carefully considered the results of the advisory vote on executive compensation.

The compensation committee also takes into account external market conditions, such as competition for executives for a particular position, and position-specific factors when approving the total compensation for each NEO. The position-specific factors influencing the compensation levels include largely qualitative factors such as experience, tenure, job performance, contributions to our financial results, scope of responsibilities, and complexity of the position.

Role of Management and CEO in Determining Executive Compensation

As part of our process for establishing executive compensation, our CEO and the human resources department provide information and recommendations to the compensation committee and compensation consultant regarding compensation program design and appropriate performance metrics. Our CEO reviews the performance of our other NEOs with the compensation committee and makes recommendations to the committee regarding compensation levels and awards for our other NEOs. The compensation committee is responsible for determining the CEO’s compensation following a review of market data provided by our compensation consultant and the committee’s evaluation of the CEO’s performance. Our CEO does not participate in meetings of the compensation committee, or portions thereof, during which the committee discusses the CEO’s compensation.

Independent Compensation Consultants

The compensation committee has engaged the services of an independent compensation consultant to assist with its work. The role of the independent compensation consultant includes, without limitation: (i) reviewing the peer group for benchmarking purposes with respect to compensation and performance, (ii) conducting a competitive assessment of each executive’s total direct compensation (e.g., base salary, annual- and long-term incentives), (iii) developing a trends report regarding executive compensation and keeping the compensation committee apprised of regulatory changes and other developments related to executive compensation, (iv) advising the compensation committee regarding annual- and long-term incentive plan design, (v) performing a competitive assessment of non-employee director compensation, and (vi) assisting with the preparation of proxy disclosures.

In 2019 the compensation committee used the services of Pearl Meyer, a nationally recognized public company compensation advisor, to advise it on executive compensation matters. Pearl Meyer reported directly to the compensation committee and, with the consent of the compensation committee, coordinated and gathered from members of management and human resources personnel information with which to advise the compensation committee. In January 2020, the compensation committee retained Meridian, a nationally recognized public company compensation advisor, to advise it on executive and director compensation matters going forward. It is the expectation of the compensation committee that Meridian will perform substantially the same services regarding executive and director compensation matters in 2020 as those performed by Pearl Meyer in 2019, described above.

Ultimately, decisions about the amount and form of executive compensation are made by the compensation committee alone and may reflect factors and considerations other than the information and advice provided by our compensation consultants or management.

Peer Group

In 2018, the committee, with the input of Pearl Meyer and management, reviewed and approved a public company peer group to be used to assist us in making compensation decisions going forward. The companies were selected from a group of public companies in the mining, metals and energy industries, taking into account market capitalization and revenues similar to ours. Our public company peer group approved by the compensation committee consisted of the following companies:

12

Arch Coal Inc. | Compass Minerals International Inc. | Suncoke Energy, Inc. | ||

Carpenter Technology Corp. | CONSOL Energy Inc. | Timkensteel Corp. | ||

Cleveland-Cliffs Inc. | Denbury Resources Inc. | Tronox Ltd. | ||

Cloud Peak Energy Inc. | Peabody Energy Corp. | Warrior Met Coal, Inc. | ||

Commercial Metals Co. | Schnitzer Steel Industries Inc. | Worthington Industries Inc. | ||

Southwestern Energy Co. | ||||

The same peer group was also used to inform compensation decisions through most of 2019. In November 2019, the compensation committee removed Cloud Peak Energy Inc. from the group following its bankruptcy.

Executive Stock Ownership Guidelines

The board of directors believes it is important for our executive officers, including our NEOs, and directors to be owners in the Company to ensure the alignment of their goals with the interests of our stockholders. In November 2019, the board adopted the Ownership Guidelines, pursuant to which the Company’s executive officers are required to hold the equivalent of three times their base salary in our common stock, except in the case of our CEO, who is required to hold five times his base salary in our common stock. Each executive officer has a transition period of five years to meet the requirements set forth in the Ownership Guidelines. In determining if an executive officer has satisfied the Ownership Guidelines, all stock and equity interests beneficially owned by the executive officer, or to which the executive officer is otherwise entitled, are taken into consideration, including certain unvested equity grants. For further information regarding the Ownership Guidelines, including a description of the terms applicable to non-employee directors, see “Director Stock Ownership Guidelines”.

2019 Primary Elements of Compensation

The 2019 compensation program for our NEOs consisted of a number of elements that support our performance and retention objectives. The compensation earned under certain components may vary significantly based on company performance. The following chart summarizes the main components of our 2019 executive compensation program and the primary objectives of each.

Compensation Element | Description | Form | Objective | |||

Base salary | Fixed based on level of responsibility, experience, tenure and qualifications | Cash | Support talent attraction and retention | |||

Annual Incentive Bonus | Variable based on the achievement of annual financial, safety and environmental metrics | Cash | Link pay and performance Drive the achievement of short-term business objectives | |||

Long-Term Incentive Awards | Variable based on the achievement of longer-term goals and stockholder value creation | RSUs that vest ratably over a three-year period PSUs that vest at the end of a three-year performance period subject to the satisfaction of total shareholder return performance metrics | Support talent attraction and retention Link pay and performance Drive the achievement of longer-term business objectives Align NEO and stockholder interests | |||

Other Compensation and Benefits Programs | Employee health, welfare and retirement benefits and deferred compensation | Group medical benefits Life and disability insurance 401(k) plan participation Deferred compensation plan | Support talent attraction and retention Provide for tax-efficient retirement savings Provide for supplemental retirement benefits | |||

13

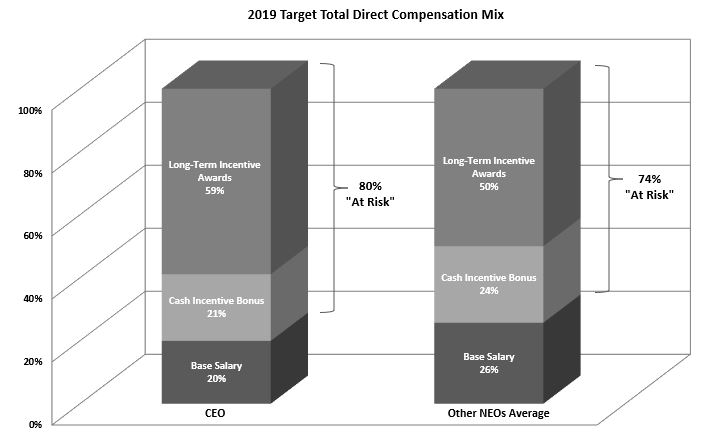

Pay Mix

As illustrated in the chart below, approximately 80% of Mr. Stetson’s and 74% of our other NEOs’ (not including Mr. Crutchfield and excluding any additional compensation paid to Messrs. Eidson and Manno in their capacity as interim co-chief executive officers) 2019 target annualized direct compensation was “at risk,” with most of the compensation subject to the achievement of short- and long-term financial or operational performance objectives. The compensation breakdown shown in the chart below reflects annualized target compensation for 2019. We believe that this balance of fixed and variable compensation is consistent with our executive compensation philosophy and maintains a strong link between the NEOs’ compensation and company performance, motivating executives to deliver strong business performance and, importantly, to create stockholder value.

Base Salary

Base salary is the fixed element of each NEO’s annual cash compensation, and the foundation upon which other primary elements of compensation are based. The compensation committee awards competitive salaries in order to assist in attracting and retaining each NEO. Base salaries are reviewed by the compensation committee annually and determined with reference to the median salaries for similarly-situated executives and also each NEO’s position-specific skills, tenure, experience, responsibility and performance. None of our NEOs received an increase in base salary from 2018 to 2019, except for Mr. Kreutzer, whose base salary increased from $400,000 to $475,000 effective January 1, 2019.

For 2019, the annual base salaries of our NEOs were as follows:

Name | 2019 Base Salary ($) | ||

David J. Stetson | 1,000,000 | ||

Charles Andrew Eidson | 500,000 | ||

Jason Whitehead | 475,000 | ||

Kevin S. Crutchfield | 1,045,000 | ||

Mark M. Manno | 500,000 | ||

J. Scott Kreutzer | 475,000 | ||

Kevin L. Stanley | 400,000 | ||

2019 Annual Bonuses

The Contura Energy, Inc. Annual Incentive Bonus Plan (the “Bonus Plan” or “CIB”) provides annual cash incentives to our executive officers and other key employees to reward performance, as measured against fundamental company financial and operational goals. During 2019, all of our NEOs except for Mr. Stetson participated in the CIB. Pursuant to the terms of his

14

employment agreement with the Company, Mr. Stetson was eligible to receive an annual bonus for 2019 in the amount of $450,000, or such higher amount as determined by the compensation committee in its discretion. Commencing with the 2020 fiscal year, Mr. Stetson’s target and maximum bonus opportunities under the CIB will be 125% and 200% of his base salary, respectively.

Performance Metrics

In establishing 2019 performance goals under the CIB, the compensation committee considered the economic environment and challenges to be faced during the fiscal year. The compensation committee designed the performance goals to ensure that performance significantly in excess of the target performance goals would be rewarded with above target payout levels, up to the cap established by the compensation committee. In setting the target goals, the compensation committee sought to establish challenging but attainable goals that would motivate and reward the NEOs for strong performance without encouraging excessive risk taking.

For 2019, the compensation committee approved a mix of performance measures based on financial metrics and operational metrics, as shown in the table below. Additional information regarding the performance metrics is included in the footnotes to the table below.

The compensation committee approved the following metrics, the respective weighting of each metric and the performance thresholds for the executives’ 2019 annual bonuses under the Bonus Plan. The metrics were intended to align annual incentive compensation for 2019 with the goals and objectives set forth in the Company’s business plan, specifically a focus on safety, environmental compliance and financial performance, especially with respect to costs. If the threshold level of performance for any of our metrics is not achieved, the resulting payout as a percentage of target is 0%, and no payouts are made under the metric.

The table below sets forth the performance metrics and their respective weightings and thresholds as well as the 2019 performance under each metric:

2019 Metric Goals | 2019 Performance | ||||||||||||||

Performance Metric | Weighting | Threshold Payout (50%) | Target Payout (100%) | Maximum Payout (200%) | Performance | Payout as % of Target | Aggregate Target Bonus % Earned | ||||||||

EBITDA(1) | 40.00% | $420.42M | $467.13M | $513.84M | $347.98M | 0.00% | 0.00% | ||||||||

Cost of Coal Sales per Ton Sold – Met(2) | 20.00% | $84.20 | $79.43 | $77.05 | $84.90 | 0.00% | 0.00% | ||||||||

Cost of Coal Sales per Ton Sold - Steam(2) | 10.00% | $44.10 | $41.60 | $40.35 | $45.01 | 0.00% | 0.00% | ||||||||

Safety – NFDL(3) | 20.00% | 2.76 | 2.51 | 2.38 | 2.04 | 200.00% | 40.00% | ||||||||

Environmental Compliance(4) | 10.00% | 114 | 88 | 75 | 35 | 200.00% | 20.00% | ||||||||

Total | 100% | 60% | |||||||||||||

(1) | CIB EBITDA was $347.98 million in 2019 under the formula adopted by the compensation committee and, as a result, the threshold performance goal was not achieved, resulting in no payout pursuant to the EBITDA metric. CIB EBITDA was calculated as follows: 2019 Income from Continuing Operations plus Interest Expense, Income Tax Expense, Depreciation, Depletion and Amortization, and Amortization of Acquired Intangibles, less Interest Income and Income Tax Benefit (“EBITDA”), and excluding the following (i) CIB, Operations, Safety, Environmental Bonus (“OSEB”), and stock compensation expenses, (ii) Impairment of tangible and intangible assets and related charges, (iii) Gains or Losses associated with Asset Retirement Obligations (“ARO”), (iv) Costs, Revenues, Gains or Losses associated with board approved future and completed business combinations, capital market transactions, reorganizations and/or restructuring programs (including severance/separation costs), and (v) Extraordinary, unusual, infrequent or non-recurring items not encompassed in the above exclusions, as determined by the board. |

(2) | CIB Cost of Coal Sales per Ton Sold was $84.90 for metallurgical coal sales and $45.01 for steam coal sales in 2019 under the formula adopted by the compensation committee and, as a result, the threshold performance goal was not achieved on either metric, resulting in no payout. CIB Cost of Coal Sales per Ton Sold was calculated as follows: Weighted Average 2019 Cost of Coal Sales per Ton Sold, excluding the following (i) CIB, OSEB, stock compensation and sales related expenses, (ii) Impairment of tangible and intangible assets and related charges, (iii) Gains or Losses associated with ARO or idled assets, (iv) Costs, Revenues, Gains or Losses associated with board approved future and completed business combinations, reorganizations and/or restructuring programs (including severance/separation costs), (v) Costs, Revenues, Gains or Losses associated with coal purchased from third parties, and (vi) Extraordinary, unusual, infrequent or non-recurring items not encompassed in the above exclusions, as determined by the board. |

(3) | CIB Non-Fatal Days Lost (“NFDL Rate”) was 2.04 in 2019, meaning that the safety objective was achieved at 118.7% of the target, which resulted in a pay-out under this objective, after interpolation, of 200% of target. NFDL Rate is a standard established by the Mine Safety and Health Administration and is widely used by coal companies to judge their safety performance. |

15

(4) | CIB Environmental Compliance, which is measured by the total number of water quality exceedances, excluding selenium, was 35 in 2019 under the formula adopted by the compensation committee and, as a result, 160% of the target performance goal was achieved resulting in a payout pursuant to this metric of 200% of target. |

Targets and Payouts for 2019

The compensation committee aims for the target amount of executives’ bonus opportunities to be at the median of competitors and industry peers. Potential 2019 bonus payouts for our NEOs who participated in the CIB ranged from 0% to 200% of the target opportunity, based on the achievement of performance metrics.

Payouts under the Bonus Plan are typically made following the completion of the applicable fiscal year, after achievement of performance metrics for the year have been determined. For 2019, performance was measured as of December 13, 2019 based on the metrics’ actuals through November and the forecasted performance for December. These payouts were made on January 3, 2020.

The following table sets forth the payouts earned by each participating NEO pursuant to the Bonus Plan for 2019. Each NEO’s annual bonus payment equaled 60% of his target bonus amount.

Officer | 2019 Base Salary ($) | 2019 Annual Target Bonus Opportunity (as a % of base salary) | 2019 Target Bonus ($) | 2019 Actual Performance as a % of Target Bonus | 2019 CIB Bonus ($) | ||||||||

Charles Andrew Eidson | 500,000 | 100% | 500,000 | 60.00% | 300,000 | ||||||||

Jason Whitehead | 475,000 | 100% | 475,000 | 60.00% | 108,300 (1) | ||||||||

Kevin S. Crutchfield | 1,045,000 | 125% | 1,306,250 | 60.00% | 0 (2) | ||||||||

Mark M. Manno | 500,000 | 100% | 500,000 | 60.00% | 458,904 (3) | ||||||||

J. Scott Kreutzer | 475,000 | 100% | 475,000 | 60.00% | 415,137 (3) | ||||||||

Kevin L. Stanley | 400,000 | 75% | 300,000 | 60.00% | 262,192 (3) | ||||||||

(1) | The 2019 CIB bonus paid to Mr. Whitehead was pro-rated to reflect his partial year of service. |

(2) | In connection with his resignation from the Company, Mr. Crutchfield forfeited his 2019 CIB bonus. See “Potential Payments on Termination and Change in Control—Chief Executive Officers—Kevin S. Crutchfield”. |

(3) | In connection with the termination of their employment from the Company and pursuant to the terms of the KESP, the 2019 bonuses paid to Messrs. Manno, Kreutzer and Stanley were based on target levels and pro-rated for the portion of 2019 each executive was employed by the Company. See “Non-CEO Severance and Change in Control Agreements”. |

Long-Term Incentive Awards

In 2016, when the Company was still private, the Company adopted, and stockholders approved, the MIP, under which grants of RSUs, restricted stock, stock options and vested shares of our common stock were made to our NEOs and other executives, non-employee directors and key employees at the time of adoption of the MIP.

The Company adopted the 2018 LTIP on April 29, 2018, pursuant to which awards of stock options, stock appreciation rights, restricted stock, RSUs, performance awards and other cash- and stock-based awards may be granted to our employees, consultants and non-employee directors. Upon becoming a public company in November 2018, we introduced a new long-term incentive program under the 2018 LTIP which consists of grants of RSUs and PSUs. In connection with his appointment as CEO in July 2019, Mr. Stetson received a sign-on RSU grant for 32,700 shares of our common stock that are scheduled to vest in equal installments on each of July 29, 2020, 2021 and 2022. Other than the retention RSUs granted to Messrs. Manno, Eidson, Kreutzer and Stanley (as described below under “2019 Executive Retention Awards”), no other RSUs were granted to our NEOs in 2019.

PSUs granted in 2019 are scheduled to vest on February 9, 2022, subject to the employee’s continued employment through such date and the satisfaction of performance conditions that are based 75% on the Company’s achievement of relative total shareholder return as compared to the median of its comparator group and 25% on the Company’s achievement of absolute total shareholder return during a three-year performance period. We chose to include PSUs in our mix of equity awards because these awards more closely align our executives’ long-term incentive compensation to shareholder returns, and reward superior performance over peer companies, while also retaining a retentive element through time-based vesting requirements. The performance period for awards granted in 2019 will be January 1, 2019 through December 31, 2021. Any vested PSUs will be paid following February 9, 2022 in the form of shares of our common stock, with potential payouts ranging from 0% to 200% of target levels for the portion of PSUs tied to absolute total shareholder return (aTSR) and 0% to 400% for the portion of PSUs

16

tied to relative total shareholder return (rTSR). The following number of target PSUs were granted to our NEOs on February 9, 2019: Kevin S. Crutchfield, 31,319 shares; Charles A. Eidson, 7,829 shares; Mark M. Manno, 7,829; and J. Scott Kreutzer: 7,438 shares; and Kevin L. Stanley: 5,480 shares. Messrs. Stetson and Whitehead did not receive PSU grants in 2019.

2019 Executive Retention Awards

In connection with their appointments as interim co-chief executive officers in May 2019, the compensation committee approved retention awards to each of Messrs. Eidson and Manno, which consisted of (i) two cash payments, each in the amount of $300,000, paid on May 7, 2019 and November 7, 2019, respectively, and (ii) a grant of 5,009 RSUs having a value of $299,989 on the grant date, scheduled to vest on May 7, 2020, subject to the executive’s continued employment through such date, except that such RSUs would become fully vested in the event of a termination of employment by the Company for any reason other than for cause.

The compensation committee also approved retention payments to each of Messrs Kreutzer and Stanley in May 2019, which consisted of (i) cash payments of $158,333 for Mr. Kreutzer and $133,333 for Mr. Stanley, each payable on November 7, 2019, (ii) additional cash payments of $158,333 for Mr. Kreutzer and $133,333 for Mr. Stanley, each scheduled to vest on May 7, 2020, subject to the executive’s continued employment through such date, except that such cash payment would be payable upon a termination of employment by the Company for any reason other than for cause and (iii) a grant of 2,643 RSUs to Mr. Kreutzer, having a value of $158,289 on the grant date, and a grant of 2,226 RSUs to Mr. Stanley, having a value of $133,315 on the grant date, each scheduled to vest on May 7, 2020, subject to the executive’s continued employment through such date, except that such RSUs would become fully vested in the event of a termination of employment by the Company for any reason other than for cause.

2020 Compensation Decisions

Based on a review of the Company’s historical grant practices and compensation objectives, the compensation committee and the board determined in February 2020 that there was an insufficient number of shares available for issuance under the 2018 LTIP to make the annual grants under the 2018 LTIP that the compensation committee believes were appropriate to fulfill the Company’s long-term compensation objectives. As a result of this shortfall, the compensation committee approved the adoption of an interim long-term incentive framework for 2020 that is comprised of a combination of both equity-based and cash-based awards, as follows: (i) 14% of each award was granted in the form of stock-settled RSUs that are scheduled to vest in equal installments on each of February 18, 2021, 2022 and 2023; (ii) 21% of each award was granted in the form of a time-based cash award that is scheduled to vest in full on February 18, 2023; and (iii) 65% of each award was granted in the form of a performance-based cash award that is scheduled to vest at the end of a three-year performance period, from January 1, 2020 through December 31, 2022, based on the achievement of safety, production and relative total shareholder return performance metrics. The performance-based component of the award will have potential payouts ranging from 0% to 200% of target levels. In February 2020, Messrs. Eidson and Whitehead received awards under this new framework having aggregate target award values of $1,000,000 and $950,000, respectively.

For 2020, Mr. Stetson’s long-term incentive award was comprised of two stock-settled components in accordance with the terms of his employment agreement, as follows: (i) 35% of his award was granted in the form of RSUs that are scheduled to vest in equal installments on each of February 18, 2021, 2022 and 2023, and (ii) 65% of the award was granted in the form of PSUs that are scheduled to vest at the end of a three-year performance period, from January 1, 2020 through December 31, 2022, based on the achievement of the same safety, production and relative total shareholder return performance metrics as for the performance-based cash awards granted to the other long-term incentive plan participants for 2020.

Deferred Compensation

Our NEOs are eligible to participate in the Deferred Compensation Plan which permits certain of our highly-compensated employees to receive supplemental retirement benefits in excess of the tax-qualified plan limits under the Internal Revenue Code. The Deferred Compensation Plan is designed to further the interests of our stockholders by helping us attract and retain key talent by providing them with these additional retirement benefits. Under the Deferred Compensation Plan, we maintain a supplemental retirement account for each participant to which we credit annual contributions equal to the sum of (i) the participant’s compensation that is in excess of the federal tax-qualified plan limit under Section 401(a)(17) of the Internal Revenue Code multiplied by the aggregate matching company contribution percentage for our tax-qualified retirement plans in effect for the applicable year (none in 2019), plus, in the discretion of our compensation committee (ii) a discretionary contribution in an amount equal to a percentage of the participant’s eligible compensation under our tax-qualified plans (none in 2019).

Upon a participant’s termination of employment without cause or by the participant for good reason, involuntary termination in connection with a change in control (as determined by the Company in its discretion prior to the change in control) or due to death or disability (all as defined in the participant’s employment agreement or the Deferred Compensation

17

Plan), the participant will receive a pro-rated credit as of December 31st of the year for which the contribution was made. All contributions made to participant accounts are fully vested when credited.

CEO Employment Agreements and Executive Offer Letters

Our chief executive officer has historically entered into an employment agreement with the Company, which is intended to retain and competitively compensate the executive for his position with the Company and provide severance benefits on specified terminations of employment. The terms of the employment agreements entered into with Messrs. Crutchfield and Stetson, including the severance amounts payable to Mr. Stetson under the terms of his employment agreement in connection with a qualifying termination of employment are described under “Potential Payments on Termination and Change in Control—Chief Executive Officers”. Mr. Crutchfield’s resignation from the Company was other than for good reason under the terms of his employment agreement. Accordingly, Mr. Crutchfield did not receive any severance payments or benefits as a result of his resignation.

No other NEOs have individual employment agreements with the Company, but all employees, including executive officers (other than our CEO), execute an offer letter with the Company upon the commencement of employment. The offer letters to executives set forth the general terms of the executive’s compensation, including annual base salary, target annual bonus opportunity under the CIB (as a percentage of base salary), target annual equity award value (as a percentage of base salary) and severance multiple under the KESP.

Non-CEO Severance and Change in Control Arrangements

Our NEOs other than Mr. Stetson are participants in our KESP, which provides participants with severance benefits following a qualifying termination of employment and enhanced benefits in connection with a change in control. The terms and estimated amounts of these benefits are described below under “Potential Payments on Termination and Change in Control—Key Employee Separation Plan”.

The compensation committee believes these change in control and termination provisions are necessary to ensure that the actions and recommendations of senior management and other employees with respect to change in control transactions are in our and our stockholders’ best interests, and to reduce the distraction regarding the impact of such a transaction on the employment status of an NEO. These programs were reviewed by our board who concluded that the terms of these programs were in line with market practices.

The CEO’s employment agreement and the KESP do not provide for payment to cover “golden parachute” excise taxes imposed under Section 4999 of the Internal Revenue Code. Rather, payments due in connection with a change of control to participants will be reduced to the extent necessary to avoid the excise tax, unless it is determined that the net after-tax benefits to a participant would be greater if the reductions were not imposed (i.e., “best net” treatment).

The departures of Messrs. Kreutzer and Stanley on November 15, 2019 and Mr. Manno on December 1, 2019 were under circumstances entitling each executive to receive the severance payments and benefits under the terms of the KESP, as set forth in the following table. Except for the COBRA Benefits and Life Insurance Benefits, as described below, and any PSUs that remain outstanding following the termination date, all amounts were paid to Messrs. Kreutzer, Stanley and Manno in a lump sum within 60 days of the termination date.

Executive | Cash Severance (1) ($) | Value of Equity Award Acceleration (2) ($) | Pro-Rata Bonus (3) ($) | COBRA Benefits and Life Insurance Benefits (4) ($) | Outplacement Services ($) | Total ($) | |||||

Mr. Kreuzter | 1,425,000 | 133,571 | 415,137 | 36,439 | 15,000 | 2,025,147 | |||||

Mr. Stanley | 1,050,000 | 131,733 | 262,192 | 36,439 | 15,000 | 1,495,364 | |||||

Mr. Manno | 1,500,000 | 201,274 | 458,904 | 36,439 | 15,000 | 2,211,617 | |||||

(1) | Reflects a lump sum cash payment equal to (x) the sum of (A) base salary plus (B) 2019 target bonus multiplied by (y) 1.5 (i.e., the executive’s severance multiple under the KESP). |

(2) | Reflects the value of accelerated vesting of any equity awards outstanding as of the applicable termination date. Outstanding PSUs continue to be subject to the attainment of the applicable performance conditions. |

(3) | Reflects the pro-rated portion of the executive’s 2019 bonus under the CIB, based on target levels. |

18

(4) | Reflects payment by the Company for Consolidated Omnibus Budget Reconciliation Act (COBRA) health and dental insurance premiums (the “COBRA Benefits”) and life insurance premiums for the executive and his dependents (the “Life Insurance Benefits”) until the earliest of the executive obtaining the age of 65, the date he becomes eligible to participate in another employer’s group health plan and 18 months following the date of termination. Mr. Manno’s COBRA Benefits did not begin until January 1, 2020. |

Retirement and Other Benefits

Our NEOs are eligible to participate in our employee benefit plans provided to other employees, including health and welfare benefits and our 401(k) plan. For 2019, we made matching contributions of up to 100% of the first 3% and 50% of next 2% (aggregate of 4%) of a participant’s contributions. For 2019, the Company did not make a qualified non-elective in addition to the matching contributions.

Tax and Accounting Considerations

We recognize a charge to earnings for accounting purposes for equity awards over their vesting period. In the past, we have not considered the accounting impact as a material factor in determining the equity award amounts for our executive officers. However, as we become a public company, we expect that the compensation committee will consider the accounting impact of equity awards in addition to considering the impact to dilution and overhang when deciding the amounts and terms of equity grants.