Attached files

| file | filename |

|---|---|

| EX-32 - Sintx Technologies, Inc. | ex32.htm |

| EX-31.2 - Sintx Technologies, Inc. | ex31-2.htm |

| EX-31.1 - Sintx Technologies, Inc. | ex31-1.htm |

| EX-23.1 - Sintx Technologies, Inc. | ex23-1.htm |

| EX-4.18 - Sintx Technologies, Inc. | ex4-18.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| [X] | Annual report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2019

or

| [ ] | Transition report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from _______ to _________

Commission File No. 001-33624

SINTX Technologies, Inc.

(previously known as “Amedica Corporation”)

(Exact name of registrant as specified in its charter)

| Delaware | 84-1375299 | |

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

1885 West 2100 South, Salt Lake City, UT 84119

(Address of principal executive offices and Zip Code)

(801) 839-3500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

| Common Stock, $0.01 par value | SINT | The NASDAQ Capital Market |

Securities registered under Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | [ ] | Accelerated Filer | [ ] |

| Non-Accelerated Filer | [ ] | Smaller reporting company | [X] |

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $26,936,976.

The number of shares outstanding of the registrant’s common stock, $0.01 par value per share, as of March 19, 2020 was 10,563,618.

DOCUMENTS INCORPORATED BY REFERENCE:

None

TABLE OF CONTENTS

| 2 |

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical fact are forward-looking statements. SINTX Technologies, Inc. (“we”, “us”, “ourselves”, “the Company”) has tried to identify forward-looking statements by using words such as “believe,” “may,” “might,” “could,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “plan” and similar words. These forward-looking statements are based on our current assumptions, expectations and estimates of future events and trends. Forward-looking statements are only predictions and are subject to many risks, uncertainties and other factors that may affect our businesses and operations and could cause actual results to differ materially from those predicted. These risks and uncertainties include, but are not limited to, factors affecting our quarterly and annual results, our ability to manage our growth, our ability to sustain our profitability, demand for our products, our ability to compete successfully, our ability to rapidly develop and introduce new products, our ability to develop and execute on successful business strategies, our ability to comply with changes and applicable laws and regulations that are applicable to our businesses, our ability to safeguard our intellectual property, our success in defending legal proceedings brought against us, trends in the medical device industry, and general economic conditions, and other risks set forth throughout this Annual Report, including under “Item 1, Business,” “Item 1A, Risk Factors,” and “Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and those discussed in other documents we file with the Securities and Exchange Commission (the “SEC”). Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for us to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

Given these risks and uncertainties, readers are cautioned not to place undue reliance on any forward-looking statements. Forward-looking statements contained in this Annual Report speak only as of the date of this Annual Report. We undertake no obligation to update any forward-looking statements as a result of new information, events or circumstances or other factors arising or coming to our attention after the date hereof.

WHERE YOU CAN FIND MORE INFORMATION

We are subject to the informational requirements of the Exchange Act. Accordingly, we file periodic reports and other information with the SEC. We will make our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports available through our Internet site, https://ir.sintx.com/ as soon as reasonably practicable after electronically filing such materials with the SEC. They may also be obtained free of charge by writing to SINTX Technologies, Inc., Attn: Investor Relations, 1885 West 2100 South, Salt Lake City, UT 84119. In addition, copies of these reports may be obtained through the SEC’s website at www.sec.gov or by visiting the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549 or by calling the SEC at 800-SEC-0330. Our common stock trades on The NASDAQ Capital Market under the symbol “SINT.”

Unless otherwise indicated, all information contained in this Annual Report reflects a 1-for-15 reverse split of our common stock which was effected on January 25, 2016, a 1-for-12 reverse split which was effected on November 10, 2017, and a 1-for-30 reverse split which was effected on July 26, 2019.

| 3 |

| ITEM 1. | BUSINESS |

Overview – SINTX Technologies

We are an advanced materials company focused on providing ceramic based solutions in a variety of medical and industrial applications. To date, our primary focus has been the research, development and commercialization of medical implant products manufactured with silicon nitride. We believe that silicon nitride has a superb combination of properties that make it ideally suited for long-term human implantation. Other biomaterials are based on bone grafts, metal alloys, and polymers- all of which have well-known practical limitations and disadvantages. In contrast, silicon nitride has a legacy of success in the most demanding and extreme industrial environments. As a human implant material, silicon nitride offers bone ingrowth, resistance to bacterial and viral infection, ease of diagnostic imaging, resistance to corrosion, and superior strength and fracture resistance, among other advantages, all of which claims are validated in our large and growing inventory of peer-reviewed, published literature reports. We believe that our versatile silicon nitride manufacturing expertise positions us favorably to introduce new and innovative devices in the medical and non-medical fields.

We also believe that we are the first and only company to commercialize silicon nitride medical implants. Prior to October 1, 2018, we designed, manufactured and commercialized silicon nitride products for our own behalf in the spine implant market. Over 35,000 of our spinal implants manufactured with silicon nitride have been implanted into patients, with an excellent safety record. On October 1, 2018, we sold our spine implant business to CTL Medical and now manufacture spine implants made with silicon nitride for CTL Medical. Prior to selling our spine implant business to CTL Medical, we had received 510(k) regulatory clearance in the United States, a CE mark in Europe, ANVISA approval in Brazil, and ARTG and Prostheses approvals in Australia for a number of silicon nitride spine implant products designed for spinal fusion surgery. Spine implant products manufactured by us from silicon nitride are currently marketed and sold by CTL Medical under the Valeo® brand to surgeons and hospitals in the United States and to selected markets in Europe and South America. These implants are designed for use in cervical (neck) and thoracolumbar (lower back) spine surgery. We are collaborating with CTL Medical to establish commercial partners in other parts of the world and also working with other partners to obtain regulatory approval for silicon nitride implants in Japan.

The sale of our spine implant business to CTL Medical enables us to now focus on our core competencies. These core competencies are research and development of silicon nitride and the design and manufacture of medical and nonmedical products manufactured from silicon nitride and other ceramic materials for our own account and in collaboration with other manufacturers. We are targeting original equipment manufacturer (“OEM”) – including CTL Medical - and private label partnerships in order to accelerate adoption of silicon nitride in future markets such as coating products with silicon nitride, hip and knee replacements, dental and maxillofacial implants, extremities, trauma, and sports medicine. Existing biomaterials, based on plastics, metals, and bone grafts have well-recognized limitations that we believe are addressed by silicon nitride, and we are uniquely positioned to convert existing, successful implant designs made by other companies into products manufactured with silicon nitride. OEM and private label partnerships allow us to work with a variety of partners, accelerate the adoption of silicon nitride, and realize incremental revenue at improved operating margins, when compared to the cost-intensive direct sales model.

We believe that silicon nitride addresses many of the biomaterial-related limitations in fields such as hip and knee replacements, dental and maxillofacial implants, sports medicine, extremities, and trauma surgery. We further believe that the inherent material properties of silicon nitride, and the ability to formulate the material in a variety of compositions, combined with precise control of the surface properties of the material, opens up a number of commercial opportunities across orthopedic surgery, neurological surgery, maxillofacial surgery, and other medical disciplines.

Our grade of silicon nitride is of a very high quality and is well suited for a wide variety of applications that would benefit from its mechanical, thermal, and chemical properties. We have several commercial partnerships and have opportunities ranging from low-volume, highly engineered components to high-volume simple shapes.

We operate a 30,000 square foot manufacturing, laboratory and administrative facility at our corporate headquarters in Salt Lake City, Utah, and we believe we are the only vertically integrated silicon nitride medical device manufacturer in the world.

| 4 |

Overview - Biomaterials

Biomaterials are natural or synthetic biocompatible materials that are used in virtually every medical specialty to improve or preserve body functionality. Various types of biomaterials are used as essential components in medical devices, drug delivery systems, replacement and tissue repair technologies, prostheses, and diagnostic technologies.

There are four general categories of biomaterials:

| ● | Ceramics. Ceramics are hard, non-metallic, non-corrosive, heat-resistant materials made by shaping and then applying high temperatures. Traditional ceramics commonly used as biomaterials include carbon, oxides of aluminum, zirconium and titanium, calcium phosphate and zirconia-toughened alumina. Examples of medical uses of ceramics include repair, augmentation or stabilization of fractured bones, bone and joint replacements, spinal fusion devices, dental implants and restorations, heart valves and surgical instruments. | |

| ● | Metals. Metals commonly used as biomaterials include titanium, stainless steel, cobalt, chrome, gold, silver and platinum, and alloys of these metals. Examples of medical uses of metals include the repair or stabilization of fractured bones, stents, surgical instruments, bone and joint replacements, spinal fusion devices, dental implants and restorations and heart valves. | |

| ● | Natural biomaterials. Natural biomaterials are derived from human donors, animal or plant sources and include human bone, collagen, gelatin, cellulose, chitin, alginate and hyaluronic acid. Examples of medical uses of natural biomaterials include the addition or substitution of hard and soft tissue, cornea protectors, vascular grafts, repair and replacement of tendons and ligaments, bone and joint replacements, spinal fusion devices, dental restorations and heart valves. | |

| ● | Polymers. Polymers are synthetic compounds consisting of similar molecules linked together that can be created to have specific properties. Polymers commonly used as biomaterials include nylon, silicon rubber, polyester, polyethylene, cross-linked polyethylene (a stronger version), polymethylmethacrylate, polyvinyl chloride and polyetheretherketone – which is commonly referred to as PEEK. Examples of medical uses of polymers include soft-tissue replacement, sutures, drug delivery systems, joint replacements, spinal fusion devices and dental restorations. |

Our Silicon Nitride Technology Platform

We believe we are the only FDA-cleared and ISO 13485 certified silicon nitride medical device manufacturing facility in the world, and the only provider of structural ceramics-based medical devices used for spinal fusion applications. Silicon nitride is a chemical compound comprised of the elements silicon and nitrogen, with the chemical formula Si3N4. Silicon nitride, an advanced ceramic, is lightweight, resistant to fracture and strong, and is used in many demanding mechanical, thermal and wear applications, such as in space shuttle bearings, jet engine components and body armor.

We believe our silicon nitride is ideal as an implant material and is superior to other biomaterials currently used in the market such as PEEK, allograft and autograft bone, metal and traditional oxide ceramics, none of which possess all of the favorable characteristics of silicon nitride:

| ● | Promotes Bone Growth. Our silicon nitride is osteointegrative through its inherent surface topography and surface chemistry. The surface topography provides scaffolding for new bone growth. As a hydrophilic material, silicon nitride attracts protein cells and nutrients that stimulate osteoprogenitor cells to differentiate into osteoblasts, which are needed for optimal bone growth environments. Our silicon nitride has an inherent surface chemistry that favors bone formation and healing, much more so than PEEK and metals. These properties were highlighted in an in vivo study, where we measured the force required to separate devices from the spine after being implanted for three months, which indicates the quality of osteointegration. In the absence of bacteria, the force required to separate our silicon nitride from its surrounding bone was approximately three times that of PEEK, and nearly two times that of titanium. In the presence of bacteria, the force required to separate our silicon nitride from its surrounding bone was over five times that of titanium, while there was effectively no separation force required for PEEK, indicating essentially no osteointegration in a septic environment. |

| 5 |

| ● | Antibacterial. We have demonstrated in in vitro and in vivo studies that silicon nitride has inherent surface antibacterial properties, which reduce the risk of bacterial infection and biofilm in and around a silicon nitride device. PEEK, traditional ceramics, metals and bone do not have this bacterial resistance. These properties were highlighted in an in vitro study (Acta Biomater. 2012 Dec;8(12):4447-54. doi: 10.1016/j.actbio.2012.07.038. Epub 2012 Jul 31.), where live bacteria counts were between 8 and 30 times lower on our silicon nitride than PEEK and up to 8 times lower on our silicon nitride than titanium. In addition to improving patient outcomes, we believe the antibacterial properties of our silicon nitride should make it an attractive biomaterial to hospitals and surgeons who are not reimbursed by third-party payers for the treatment of acute, implant-related infections. Additionally, silicon nitride is synthetic and, therefore, there is a lower risk of disease transmission through cross-contamination or of an adverse auto-immune response, sometimes associated with the use of allograft bone. | |

| ● | Antiviral: Solid-surface inactivation of microbial pathogens has ancient roots; the Smith Papyrus (2600~2200 B.C.) described the use of copper surfaces to sterilize chest wounds and drinking water. Today, brass and bronze on door knobs help prevent microbial spread in hospitals, and metal particles and surface coatings of selected metals are used in hygiene-sensitive environments, both as inactivators and adjuvants in inducing cellular immunity. Cellular toxicity limits these approaches because while the reactive oxygen radicals generated at metal surfaces efficiently kill bacteria and viruses, they also damage cells by oxidizing their proteins and lipids. Recent data have shown that silicon nitride surfaces are effective against several types of viruses. With surface-contact transmission of viral pathogens, particularly influenza, and the increasing use of consumer touchscreens in various retail industries, we believe that our material has value to OEM partners focused on consumer glass-based surface coatings and treatments. We have filed a U.S. patent application on this effect. | |

| ● | Antifungal: We have conducted preliminary studies which suggest that our silicon nitride may be effective against fungal microbes. Plant-based viruses, bacteria, and fungi affect some 15% of the world’s edible crops, or about 1 billion metric tons of edible produce annually, with an economic impact in the US and Canada alone estimated to be between $1.5 to $5 Billion per year. The mycotoxins produced by these plant fungi have an overall negative impact on human health and longevity. The inorganic nature of silicon nitride may prove to be more beneficial than the use of petrochemical or organometallic fungicides which are known to have residual effects in soil, on plants, and in fruit | |

| ● | Imaging Compatible. Our silicon nitride interbody spinal fusion devices are semi-radiolucent, clearly visible in X-rays, and produce no distortion under MRI and no scattering under CT. These characteristics enable an exact view of the device for precise intra-operative placement and post-operative bone fusion assessment in spinal fusion procedures. These qualities provide surgeons with greater certainty of outcomes with our silicon nitride devices than with other biomaterials, such as PEEK and metals. | |

| ● | Hard, Strong and Resistant to Fracture. Our silicon nitride is hard, strong and possesses superior resistance to fracture over traditional ceramics and greater strength than polymers currently on the market. For example, our silicon nitride’s flexural strength is more than five times that of PEEK and our silicon nitride’s compressive strength is over twenty times that of PEEK. Unlike PEEK interbody spinal fusion devices, we believe our silicon nitride interbody spinal fusion devices can withstand the forces exerted during implantation and daily activities over the long term. | |

| ● | Resistant to Wear. We believe our silicon nitride joint implant product candidates could have higher resistance to wear than metal-on-cross-linked polyethylene and traditional oxide ceramic-on-cross-linked polyethylene joint implants, the two most commonly used total hip replacement implants. Wear debris associated with metal implants increases the risk of metal sensitivity and metallosis. It is a primary reason for early failures of metal and polymer articulating joint components. | |

| ● | Non-Corrosive. Our silicon nitride does not have the drawbacks associated with the corrosive nature of metal within the body, including metal sensitivity and metallosis, nor does it result in the release of metal ions into the body. As a result, we believe our silicon nitride products will have lower revision rates and fewer complications than comparable metal and traditional oxide ceramic products. |

| 6 |

Supporting Data

We and a number of independent third parties have conducted extensive biocompatibility, biomechanical, in vivo and in vitro testing on our silicon nitride composition to establish its safety and efficacy in support of regulatory clearance of our biomaterial, products and product candidates. We have also completed additional testing of our silicon nitride products and product candidates. The results of this testing have been published in over 130 peer reviewed publications and presentations that include basic science studies, small- and large-animal data, and human clinical studies. We believe that our product development strategy is consistent with the manner in which other biomaterials have been successfully introduced into the market and adopted as the standard of care. Listed below is an overview of some of the key testing completed on our silicon nitride biomaterial, products and product candidates to date, as well as other information about our silicon nitride and other biomaterials.

Biocompatibility

Before our silicon nitride was cleared by the FDA in 2008, we conducted a series of biocompatibility tests following the guidelines of the FDA and ISO and submitted the results to the FDA as part of the regulatory clearance process. These tests confirmed that our silicon nitride products meet required biocompatibility standards for human use.

Promotion of Bone Growth

In 2012, we conducted two separate studies at Brown University, the results of which suggest that the chemistry and inherent surface topography of our solid silicon nitride provides an optimal environment for bone growth onto and around the device.

The first study was a series of in vitro analyses of protein adsorption, or presence on the surface of the biomaterial, onto silicon nitride, PEEK and titanium. The results of this study indicated that adsorption of two key proteins necessary for bone growth (fibronectin and vitronectin) were up to eight times greater on our silicon nitride than on PEEK, and up to four times greater than on titanium. A third important protein (laminin) had up to two times greater adsorption on our silicon nitride than on PEEK, and up to two-and-one-half times greater adsorption than on titanium.

The second study was an in vivo investigation of the osteointegration characteristics of these same three biomaterials after they had been surgically implanted into the skulls of laboratory rats. This study included an examination of the effect of Staphylococcus epidermidis bacteria on osteointegration. At time intervals of up to three months after implantation of the biomaterial, the amount of new bone growth within the surgical site and in direct contact with the implanted biomaterial was evaluated. In the absence of bacteria, new bone formation within the surgical site surrounding our silicon nitride was approximately 69%, compared with 36% and 24% for titanium and PEEK, respectively. Similarly, bone in direct contact, or apposition, with our silicon nitride, titanium and PEEK was 59%, 19% and 8%, respectively. As is common, in the presence of bacteria, new bone formation within the surgical site was suppressed, but still significantly greater for our silicon nitride than for the other two biomaterials. Observed new bone growth within the surgical site surrounding our silicon nitride was 41%, compared with 26% and 21% for titanium and PEEK, respectively. At the implant interface, the bone apposition for our silicon nitride, titanium and PEEK was 23%, 9% and 5%, respectively. To further characterize the extent of osteointegration, the force needed to separate each implant from its surrounding bone was measured. A larger force needed to separate the implant is an indication of improved osteointegration. At three months after implantation, in the absence of bacteria, the force required to separate our silicon nitride from its surrounding bone was approximately three times that of PEEK, and nearly two times that of titanium. In the presence of bacteria, there was effectively no separation force required for PEEK, indicating essentially no osteointegration. Our silicon nitride required over five times the force to separate it from its surrounding bone in the presence of bacteria in comparison to titanium.

| 7 |

In 2008, we conducted an animal study in which we evaluated the level of osteointegration of our porous silicon nitride with a knee-defect model in adult sheep. At three months after implantation, three out of five of the silicon nitride implants had extensive new bone formation at and into the implant surface, showing that the bone had grown into our porous silicon nitride to a depth of 3 millimeters, or mm. This animal study demonstrated the rapid osteointegration potential of our porous silicon nitride composition.

Hardness, Strength and Resistance to Fracture

Comparative Information

As shown in the table of comparative information publicly available about various biomaterials below:

| ● | the hardness, or a material’s resistance to deformity, of silicon nitride is comparable to traditional ceramics, but is substantially higher than either polymers or metals; | |

| ● | the strength of silicon nitride is comparable or higher than metals and traditional ceramics, and is about sixteen to fifty-five times stronger than highly-cross-linked polyethylene, and four to eight times stronger than PEEK; and | |

| ● | silicon nitride has the highest fracture resistance of any medical ceramic material and is three to eleven times more resistant to fracture than PEEK or highly-cross-linked polyethylene. This is due to the interwoven microstructure of silicon nitride. Metals have the highest fracture resistance. |

Comparison of Mechanical Properties Among Orthopedic Biomaterials

| Material | Hardness (GPa)(1) | Strength (MPa)(1) | Fracture Resistance (MPam1/2)(1) | |||||||||

| Silicon Nitride | 13 – 16 | 800 – 1200 | 8 – 11 | |||||||||

| Aluminum Oxide Ceramic | 14 – 19 | 300 – 500 | 3 – 5 | |||||||||

| Zirconia-Toughened Alumina Ceramic | 12 – 19 | 700 – 1150 | 5 – 10 | |||||||||

| PEEK | 0.09 – 0.28 | 160 – 180 | 2 – 3 | |||||||||

| Highly-Cross-Linked Polyethylene Polymer | 0.03 – 0.07 | 22 – 48 | 1 – 2 | |||||||||

| Cobalt-Chromium Metal | 3 – 4 | 700 – 1000 | 50 – 100 | |||||||||

| Titanium Alloy Metal | 3 – 4 | 920 – 980 | 75 | |||||||||

| (1) | GPa is a giga-pascal. Pascals are a measure of pressure. MPam1/2 is mega-pascal times a square root meter and is a measure related to the energy required to initiate fracture of a material. |

We believe that the combination of high hardness, strength and fracture resistance positions our silicon nitride as an ideal biomaterial for many medical applications.

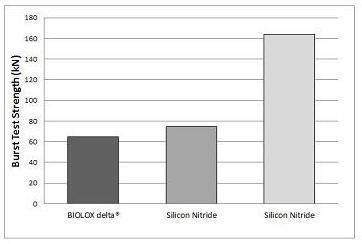

Burst Strength

In 2006, we conducted in-house comparative “burst strength” tests on femoral heads made from our silicon nitride produced by a contract manufacturer to our specifications and femoral heads made from one of the strongest commercially available ceramics, BIOLOX® delta (zirconia-toughened alumina). These tests were performed on three designs of 28 mm femoral heads using accepted testing protocols. The tests involved applying a load to each femoral head while mounted on a cobalt-chromium simulated hip implant stem, until the head burst. This enabled us to directly compare the strength of the femoral heads made of the two biomaterials. The results also provided an indication of each biomaterial’s resistance to fracture. The results of these tests are shown in the chart below.

| 8 |

The average burst test strength for the silicon nitride femoral heads in these tests was 75 kilonewtons, or kNs, compared with 65 kN for BIOLOX® delta, or about a 15% improvement. The burst strengths observed in our tests for BIOLOX® delta femoral heads are comparable to those observed by an independent party testing the same design BIOLOX® delta femoral heads as we did. We also conducted burst strength tests of 36 mm femoral heads made from our silicon nitride which showed those femoral heads had burst strengths that averaged 164 kN.

Resistance to Wear

In 2011, we commissioned an independent laboratory to conduct a wear study using our silicon nitride femoral heads. We tested our 28 mm silicon nitride femoral heads articulated against cross-linked polyethylene acetabular liners and our 40 mm silicon nitride femoral heads articulated against cross-linked polyethylene acetabular liners using well-established protocols in a hip simulator for their wear performance over 5 million cycles. We then compared the results for our silicon nitride product candidates to the results for the cobalt chrome femoral head and publicly available data from other commonly paired products. The results and comparison showed that:

| ● | our silicon nitride-on-cross-linked polyethylene had approximately half the wear rate of that publicly reported for cobalt chrome-on-cross-linked polyethylene articulating hip components; and | |

| ● | our silicon nitride-on-cross-linked polyethylene had comparable wear to that publicly reported for traditional oxide ceramic-on-cross-linked polyethylene articulating hip components. |

Antibacterial Properties

The results of the two studies at Brown University in 2012, demonstrate that our solid silicon nitride has antibacterial properties. The objective of the in vitro study was to determine how our silicon nitride, PEEK and titanium interact with bacteria, protein and bone cells without the use of antibiotics and compared the growth of five different types of bacteria on silicon nitride, PEEK and titanium over time. Live bacteria counts were between 8 to 30 times lower on silicon nitride than PEEK and up to 8 times lower on silicon nitride than titanium.

In the in vivo study, bacteria were applied to the biomaterials before implantation. Three months after implantation, no infection was observed with silicon nitride, whereas both PEEK and titanium showed infection. The data demonstrate that our silicon nitride inhibits biofilm formation and bacterial colonization around the biomaterial.

Antiviral and Antifungal Properties

Antiviral: Our data have shown that off-stoichiometric reactions at the surface of our silicon nitride can inactivate different types of single-strand RNA viruses. This antiviral property derives from reactive nitrogen species without harm to mammalian cells. Testing based on polymerase chain reaction tests of viral RNA and in situ Raman spectroscopy suggest that our material is effective in counteracting several viruses relevant to public health concerns, such as Influenza A, Feline calcivirus, and Enterovirus.

| 9 |

Antifungal: We have conducted preliminary studies which suggest that our silicon nitride may be effective against fungal microbes. After sintering and processing, powdered silicon nitride was dissolved in a 1.5 vol.% aqueous solution that underwent field testing on two species of grape vine leaves that were infected with a fungal pathogen Plasmopara viticola. After 1 minute of exposure to our silicon nitride, the infected area of the leaves was reduced by ~95%. The likely mechanism likely involves electrical attraction to, and attachment of silicon nitride particles to oppositely-charged pathogen spores.

Imaging Compatibility

In 2007, we conducted a study to compare the imaging characteristics of test blanks made of PEEK, the metals titanium and tantalum, and silicon nitride using a cadaver human vertebral body. Images of the vertebral body and the blanks were obtained using X-ray, CT and MRI under identical conditions. We assessed the radiolucent characteristics of the blanks in X-ray images quantitatively, assessed the presence of scatter in CT qualitatively and assessed distortion in MRI quantitatively. In X-ray, the metal blanks did not permit visualization of the underlying bone of the vertebral body, while PEEK was transparent, rendering its location difficult to determine. The silicon nitride blank had an intermediate radiolucency that rendered it visible and allowed a visual assessment of the underlying bone of the vertebral body. CT and MRI of the metal blanks indicated the presence of distortion while silicon nitride and PEEK exhibited no scattering.

Our Forms of Silicon Nitride

To control the quality, cost and availability of our silicon nitride products and product candidates, we operate our own manufacturing facility. Our 30,000 square foot corporate facility includes an 18,000 square foot FDA Registered and ISO 13485 certified medical device manufacturing space. It is equipped with state-of-the-art powder processing, spray drying, pressing and computerized machining equipment, sintering furnaces, and other testing equipment that enables us to control the entire manufacturing process for our silicon nitride products and product candidates. To our knowledge, we are the only vertically integrated silicon nitride orthopedic medical device manufacturer in the world. All operations with the exception of raw material production are performed in-house. We purchase raw materials, consisting of silicon nitride ceramic powder and dopant chemical compounds, from several vendors which are ISO registered and approved by us. These raw materials are characterized and tested in accordance with our specifications and then blended to formulate our silicon nitride. We believe that there are multiple vendors that can supply us these raw materials and we continually monitor the quality and pricing offered by our vendors to ensure high quality and cost-effective supply of these materials.

The chemical composition of our in-house formulation of silicon nitride and our processing and manufacturing experience allow us to produce silicon nitride in four distinct forms. This capability provides us with the ability to utilize our silicon nitride biomaterial in a variety of ways depending on the intended application, which, together with our silicon nitride’s key characteristics, distinguishes us from manufacturers of products using other biomaterials.

We currently produce silicon nitride for use in our commercial products and product candidates in the following forms:

| ● | Solid Silicon Nitride. This form of silicon nitride is a fully dense, load-bearing solid used for devices that require high strength, toughness, fracture resistance and low wear, including interbody spinal fusion devices, hip and knee replacement implants, and dental implants. | |

|

| 10 |

| ● | Porous Silicon Nitride. While this form of silicon nitride has a chemical composition that is identical to that of our monolithic solid silicon nitride, this formulation has a porous structure, which is engineered to mimic cancellous bone, the spongy bone tissue that typically makes up the interior of human bones. Our porous silicon nitride has interconnected pores ranging in size between about 90 and 600 microns, which is similar to that of cancellous bone. This form of silicon nitride can be used for the promotion of bone in-growth and attachment. We believe our porous silicon nitride can act as a substitute for the orthobiologics currently used to fill interbody devices in an effort to stimulate fusion, as a bone void filler, and as a porous scaffold for medical devices. | |

| ||

| ● | Composite of Solid and Porous Silicon Nitride. This form of silicon nitride is a combination, or composite, of our solid monolithic and porous formulations of silicon nitride. This composite may be used to manufacture devices and implants that mimic the structure of natural bone by incorporating both a fully dense, load-bearing solid component on the outside and a porous component intended to promote bone in-growth on the inside. This composite form of silicon nitride is used in interbody spinal fusion devices and can be used in components for total hip and knee replacement implants. | |

| ||

| ● | Composite of Silicon Nitride and PEEK. We have demonstrated in the laboratory that it is possible to compound our silicon nitride powder and the polymer PEEK and that the ensuing composite material maintains the bioactive properties of silicon nitride. We have engaged commercial partners to assist us in developing this technology. This composite material would allow the straightforward machinability of a complex device that would be more challenging to manufacture from silicon nitride alone. | |

| ● | Silicon Nitride Coating. With a similar chemical composition as our other forms of silicon nitride, this form of silicon nitride can be applied as an adherent coating to metallic substrates, including cobalt-chromium, titanium and steel alloys, polymers, and ceramics. We believe applying an extremely thin layer of silicon nitride as a coating may provide a highly wear-resistant articulation surface, such as on femoral heads, which may reduce problems associated with metal or polymer wear debris. We also believe that the silicon nitride coating can be applied to devices that require firm fixation and functional connections between the device or implant and the surrounding tissue, such as hip stems and screws. The use of silicon nitride coating may also create an antibacterial, antiviral, and antifungal barrier between the device and the adjacent bone or tissue. We are currently evaluating several different coating technologies. | |

|

| 11 |

Our Competitive Strengths

We believe we can use our silicon nitride technology platform to become a leading biomaterial company and have the following principal competitive strengths:

| ● | Sole Provider of Silicon Nitride Medical Devices. We believe we are the only company that designs, develops, manufactures and sells medical grade silicon nitride-based products. Due to its key characteristics, we believe our silicon nitride enables us to offer new and transformative products across multiple medical specialties. In addition, with the FDA clearance of our silicon nitride Valeo products, we are the only company to develop and manufacture a ceramic for use in FDA cleared spinal fusion medical devices in the United States. | |

| ● | In-House Manufacturing Capabilities. We operate an 18,000 square foot manufacturing facility located at our corporate headquarters in Salt Lake City, Utah. This operation complies with the FDA’s quality system regulation, or QSR, and is certified under the International Organization for Standardization’s, or ISO, standard 13485 for medical devices. This facility allows us to rapidly design and produce silicon nitride products while controlling the entire manufacturing process from raw material to finished components. | |

| ● | Extensive Network of Scientific Collaborators. We have developed strong, multi-year, collaborative relationships with surgeons who have used our products. These surgeons have supported us in collecting clinical data on silicon nitride and on reporting the successful patient outcomes they have observed. We also have long standing relations with university laboratories in Japan and the US and have recently been invited to participate in a European consortium on silicon nitride. Our partner in Japan has been at the forefront of silicon nitride biomaterial research for several years and has published extensively on the subject. | |

| ● | Highly Experienced Management and Technical Advisory Team. Members of our management team have extensive experience in silicon nitride, ceramics, research and development, manufacturing and operations, product development, launching of new products into the orthopedics market and selling to hospitals through direct sales organizations, distributors, manufacturers and other orthopedic companies. We also collaborate with a network of leading technical (academic and surgeon) advisors in the design, development and use of our silicon nitride products and product candidates. |

Our Strategy

Our goal is to become a leading biomaterial company focused on using our silicon nitride technology platform to develop, manufacture and commercialize a broad range of medical devices. Key elements of our strategy to achieve this goal are the following:

| ● | Support CTL and drive further adoption of silicon nitride interbody spinal fusion devices. We have entered into a 10-year agreement to manufacture all of CTL Medical’s requirements of silicon nitride based spinal implant products. This includes the current product line as well as new applications for silicon nitride in the spine. | |

| ● | Develop a commercial opportunity outside of spine. We have had active programs outside of spine for several years. We expect to commercialize on one or more of these in the near future. | |

| ● | Develop new silicon nitride manufacturing technologies. Our current manufacturing process has allowed us to successfully produce spinal implants for over 10 years. However, this process has limitations and we are actively pursuing other manufacturing technologies such as additive manufacturing, and surface coating technologies. | |

| ● | Make improvements to our current formulation of silicon nitride to increase the bioactive properties of the material. We have demonstrated in the laboratory that we can make our material more bioactive. This work has been independently corroborated by researchers in other parts of the world. We expect that the availability of silicon nitride with enhanced bioactivity would open up new markets to us. |

| 12 |

| ● | Apply our silicon nitride technology platform to other OEM opportunities – medical and non-medical. We believe our biomaterial expertise, flexible manufacturing process, and strong intellectual property will allow us to transition currently available medical device products made of inferior biomaterials and manufacture them using silicon nitride and our technology platform to improve their characteristics. We are seeking partnerships to utilize our capabilities and manufacture products for medical and non-medical original equipment manufacturer (“OEM”) and private label partnerships. We see specific opportunities in markets such as dental, maxillofacial, total hip and knee joint replacements, bearings, automotive and aerospace components, and cutting tools. |

Market Opportunity

Overview

We believe our silicon nitride biomaterial technology platform provides us with numerous competitive advantages in the biomaterials market. We manufactured interbody spinal fusion devices for our own retail spine business from 2008 to 2018, presently manufacture these for CTL Medical, and have a 10-year exclusive right to continue to manufacture them for CTL Medical. We are developing products on our own behalf and for third party manufacturers – including CTL Medical - for use as components in spine, total hip and knee joint replacements, as well as dental and maxillofacial applications. We believe we can also utilize our silicon nitride technology platform to develop future products in additional medical and non-medical markets.

We believe that the main drivers for growth within the orthopedic biomaterials market are the following:

| ● | Introduction of New Technologies. Better performing and longer-lasting biomaterials, improved diagnostics, and advances in surgical procedures allow for surgical intervention earlier in the continuum of care and better outcomes for patients. We believe surgical options using better performing and longer-lasting biomaterials will gain acceptance among surgeons and younger patients and drive accelerated growth and increase the size of the spinal fusion and joint replacement markets. | |

| ● | Favorable and Changing Demographics. With the growing number of elderly people, age-related ailments are expected to rise sharply, which we believe will increase the demand and need for biomaterials and devices with improved performance capabilities. Also, middle-aged and older patients increasingly expect to enjoy active lifestyles, and consequently demand effective treatments for painful spine and joint conditions, including better performing and longer-lasting interbody spinal fusion devices and joint replacements. | |

| ● | Market Expansion into New Geographic Areas. We anticipate that demand for biomaterials and the associated medical devices will increase as the applications in which biomaterials are used are introduced to and become more widely accepted in underserved countries, such as Brazil and China. We also expect to introduce our products into established markets such as Australia and Japan. |

The Interbody Spinal Fusion Market

We believe there is opportunity for significant growth in the spinal fusion market for interbody spinal fusion devices manufactured with silicon nitride. Currently, in spinal fusion procedures conducted in the United States today, a significant majority utilize interbody devices comprised of PEEK and bone, with occasional use of metals and other materials including ceramics. The market for interbody spinal fusion devices has shifted over time as new biomaterials with superior characteristics have been incorporated into these devices and have launched into the market. We believe the market has reached another inflection point as surgeons and hospitals recognized the limitations of devices currently available. Similarly, we believe silicon nitride interbody spinal fusion products address the key limitations of other biomaterials currently used in interbody spinal fusion devices and demonstrate superior characteristics needed to improve clinical outcomes.

We selected this market as the first application for our silicon nitride technology because of the limitations of currently available products, its size, and the key characteristics silicon nitride possesses, which are critical for superior interbody spinal fusion outcomes.

| 13 |

| ● | Promotion of Bone Growth. The biomaterial should be both osteoconductive and create an osteoinductive environment to promote bone growth in and around the interbody device to further support fusion and stability. Osteoconduction occurs when material serves as a scaffold to support the growth of new bone in and around the material. Osteoinduction involves the stimulation of osteoprogenitor cells to develop, or differentiate, into osteoblasts, which are cells that are needed for bone growth. A material which stimulates bone growth and accelerates fusion rates is ideal in spinal fusion procedures. | |

| ● | Antibacterial. Spinal fusion devices can become colonized with bacteria, which may limit fusion to adjacent vertebrae or cause serious infection. Treating device-related infection is costly and generally requires repeat surgery, including surgery to replace the device, referred to as revision surgery, which may extend hospital stays, suffering and disability for patients. A biomaterial that has antibacterial properties can reduce the incidence of bacteria colonization in and around the interbody device that can lead to infection, revision surgery and associated increased costs. | |

| ● | Imaging Compatibility. The biomaterial should be visible through, and not inhibit the effective use of, common surgical and diagnostic imaging techniques, such as X-ray, CT and MRI. These imaging techniques are used by surgeons during and after spinal fusion procedures to assist in the proper placement of interbody devices and to assess the quality of post-operative bone fusion. | |

| ● | Strength and Resistance to Fracture. The biomaterial should be strong and resistant to fracture during implantation of the device and to successfully restore intervertebral disc space and spinal alignment during the fusion process. The biomaterial should have high flexural strength, which is the ability to resist breakage during bending, and high compressive strength, which is the ability to resist compression under pressure, to withstand the static and dynamic forces exerted on the spine during daily activities over the long term. |

Spinal Fusion Products

Current spinal fusion products that we manufacture for CTL Medical are:

| Valeo Interbody Fusion Devices | Generation | ||

| AL: Anterior Lumbar | 2nd | ||

| PL: Posterior Lumbar | 1st and 2nd | ||

| OL: Oblique Lumbar | 1st and 2nd | ||

| TL: Transforaminal Lumbar | 1st and 2nd | ||

| LL: Lateral Lumbar | 2nd | ||

| C: Cervical | 1st and 2nd | ||

| CORP: Corpectomy | 1st | ||

| C+CSC (cleared in Australia and the EU but not the USA) | 1st | ||

| C+CSC with Lumen | 1st |

The Dental Market

We believe there is opportunity for significant growth in the dental implant market for dental implant devices manufactured with silicon nitride and are pursuing this opportunity aggressively. We have entered into a joint development agreement with a dental implant design company and distributor of dental technologies for the development of a silicon nitride based dental implant system and devices.

When a tooth is removed, one common approach to restoration is to use a multi-part construct consisting of a titanium implant (or screw), a zirconia abutment, and a crown. Potential applications for silicon nitride in this procedure include the implant and the abutment.

| 14 |

Silicon nitride is appealing because this application takes advantage of the same bioactive properties discussed in the spinal implant section:

| ● | Promotion of bone growth | |

| ● | Antibacterial | |

| ● | Imaging compatible | |

| ● | Hard, strong, resistant to fracture and wear |

We also believe it may be possible to leverage our knowledge of medical device manufacturing of ceramics and commercialize products for the dental market made from ceramics other than silicon nitride. We have engaged an investment banker to assist us in identifying partner companies for our technologies.

The Hip and Knee Joint Replacement Market

We believe there is opportunity for significant growth in the hip and knee joint replacement market for interbody devices manufactured with silicon nitride.

Total joint replacement involves removing the diseased or damaged joint and replacing it with an artificial implant consisting of components made from several different types of biomaterials. The key components of a total hip implant include an artificial femoral head, consisting of a ball mounted on an artificial stem attached to the femur, and a liner, which is placed inside a cup affixed into the pelvic bone. The femoral head and liner move against each other to replicate natural motion in what is known as an articulating implant. Total knee replacement implants also use articulating components and are comprised of the following four main components: a femoral condyle, which is a specially shaped bearing that is affixed to the lower end of the femur; a tibial tray that is affixed to the upper-end of the tibia; a tibial insert that is rigidly fixed to the tibial tray and serves as the surface against which the femoral condyle articulates; and a patella, or knee cap, which also articulates against the femoral condyle.

Implants for total hip and knee replacements are primarily differentiated by the biomaterials used in the components that articulate against one another. The combinations of biomaterials most commonly used in hip and knee replacement implants in the United States are metal-on-cross-linked polyethylene and traditional oxide ceramic-on-cross-linked polyethylene. The use of hip replacement implants incorporating metal-on-metal and traditional oxide ceramic-on-traditional ceramic biomaterials experienced a steep decline in the United States over the last several years due to their significant limitations. We believe that the most commonly used biomaterials in joint replacement implants also have limitations, and do not possess all of the following key characteristics required for optimal total joint replacement implants:

| ● | Resistance to Wear. The biomaterials should have sufficient hardness and toughness, as well as extremely smooth surfaces, to effectively resist wear. Because the articulating implants move against each other, they are subject to friction, which frequently leads to abrasive wear and the release of small wear particles. This may cause an inflammatory response which results in osteolysis, or bone loss. Surgeons have identified osteolysis as a leading cause of joint implant failure, resulting in the need for costly revision surgery to replace the failed implant. One of the most commonly used combinations of biomaterials, metal-on-cross-linked polyethylene, as well as metal-on-metal implants, tends to generate a large number of metal wear particles, which can cause osteolysis and a moderate to severe allergic reaction to the metal, referred to as metal sensitivity. While less common, metal implants may also cause a serious medical condition called metallosis, which involves the deposition and build-up of metal debris in the soft tissues of the body. Both metal sensitivity and metallosis can result in revision surgery. In addition, we believe traditional oxide ceramics currently used in total joint replacements accelerate wear of the cross-linked polyethylene liner as compared to our non-oxide ceramic composition found in our silicon nitride biomaterial platform. | |

| ● | Non-Corrosive. The biomaterials should be non-corrosive and should not cause adverse patient reactions. Metal placed in the human body corrodes over time and also results in the formation of metal ions, which leads to metal sensitivity in approximately 10% to 15% of the population and, less commonly, metallosis. As a result, there are significant increased risks from using metal-on-cross-linked polyethylene and metal-on-metal implants. | |

| ● | Hardness, Strength and Resistance to Fracture. The biomaterials should be hard, strong and resistant to fracture to adequately bear the significant loads placed on the hip and knee joints during daily activities. We believe there are strength limitations associated with traditional oxide ceramic-on-cross-linked polyethylene and traditional oxide ceramic-on-traditional oxide ceramic implants. |

| ● | Antibacterial. The biomaterials should have antibacterial properties to reduce the risk of bacteria colonization, infection, revision surgeries and associated increased costs. None of the most commonly used biomaterials in joint replacement implants have antibacterial properties. |

| 15 |

Our Total Hip Implant Product Candidates

We have developed a femoral head that is made from our solid silicon nitride, which could be used for total hip replacement product candidates. This femoral head is expected to articulate against a cross-linked polyethylene liner fixed into a metal acetabular cup. Most recently we participated in a university study that demonstrated the comparatively better behavior of silicon nitride femoral heads in taper fretting corrosion behavior study. As we continue to gather evidence that silicon nitride femoral heads are superior in terms of wear performance, taper corrosion, strength and in vitro hydrothermal stability, we eventually intend to commercialize this product in cooperation with a strategic partner. However, clearance of these types of devices by the FDA will be required. Currently, the FDA has indicated that a limited one to two-year clinical trial may be necessary to obtain clearance.

Our Total Knee Implant Product Candidates

We have developed a femoral condyle design made from our solid silicon nitride. The femoral condyle component will attach to the lower end of the femur. The femoral condyle is expected to articulate against a cross-linked polyethylene tibial insert that will attach to the tibial tray at the upper end of the tibia, which we expect will be made from metal. We have successfully made prototypes of this design. Following the potential clearance of the femoral head components (discussed above), we intend to initiate biomechanical testing with a strategic partner for silicon nitride components for use in knee replacement procedures to support a 510(k) submission to the FDA. If this clearance is eventually obtained, we intend to commercialize our products for use in total knee replacement surgeries post-FDA clearance.

Other Product Opportunities

Our silicon nitride technology platform is adaptable, and we believe it may be used to develop products to address other significant opportunities, such as in the cranial-maxillofacial, extremities, sports medicine and trauma markets.

We also believe our coating technology may be used to enhance metal products as well as other commercially available metal or PEEK spinal fusion and joint replacement products. We have produced feasibility prototypes of dental implants, other components for use in total hip implants in addition to our total hip and knee implant product candidates discussed above, a suture anchor for sports medicine applications, an osteotomy wedge for extremities applications, and prototypes of silicon nitride-coated plates for potential trauma applications. We have also developed a process to apply our silicon nitride as a coating on other materials which may find applications in markets outside of the medical device industry.

Our recent discoveries of the antiviral and antifungal properties of silicon nitride have opened up completely new opportunities for us in the consumer and agriculture markets.

The FDA has not evaluated any of these potential products and we are not currently advancing the development of any of these product candidates. We plan to collaborate with medical device companies to complete the development of and commercialize any product candidates we advance in these areas or develop any one of them ourselves if sufficient resources should become available.

We also see a wide variety of opportunities for our silicon nitride technology platform in non-medical applications. To that effect, we have begun applying our technology to the manufacture of products for several third-party ceramic companies which we are hopeful will result in commercial partnerships with opportunities ranging from low-volume, highly engineered components to high-volume simple shapes.

Intellectual Property

We rely on a combination of patents, trademarks, trade secrets, nondisclosure agreements, proprietary information ownership agreements and other intellectual property measures to protect our intellectual property rights. We believe that in order to have a competitive advantage, we must continue to develop and maintain the proprietary aspects of our technologies.

| 16 |

We have thirteen issued U.S. patents, three pending U.S. non-provisional patent applications, three pending U.S. provisional patent applications, seven pending foreign applications and two pending PCT patent applications. Our first issued patent expired in 2016, with the last of these patents expiring in 2036. The core patent (US 6,881,229) expires in 2022.

We have seven U.S. patents directed to articulating implants using our high-strength, high toughness doped silicon nitride solid ceramic. The issued patents, which include US 6,881,229; US 7,666,229; US 7,780,738; US 8,123,812; US 8,133,284; US 9,051,639; and US 9,517,136 begin to expire in 2022.

We also have two U.S. patents related to our CSC technology that are directed to implants that have both a dense load-bearing, or cortical, component and a porous, or cancellous, component, together with a surface coating. These issued patents, US 8,133,284 and US 9,649,197 will expire in 2022 and 2035, respectively.

With respect to PCT patent application serial no. PCT/US2018/014781 directed to antibacterial biomedical implants, we recently entered the national stage in Europe, Australia, Brazil, Canada, China, Japan, and South Korea in order to seek potential patent protection for our proprietary technologies in those countries.

In relation to the sale of our spine implant business to CTL Medical under the Asset Purchase Agreement dated September 5, 2018 we assigned our entire right to forty eight (48) U.S. patents, two (2) foreign patents and three (3) pending patent applications from our patent portfolio to CTL Medical under that transaction. In addition, three (3) U.S. patents (U.S. patent nos. 9,399,309; 9,517,136; and 9,649,197) directed to silicon nitride manufacturing processes were licensed to CTL Medical under an irrevocable, fully paid-up, worldwide license for a ten year term with CTL Medical also having a Right of First Negotiation to acquire these patents if SINTX decides to later sell these IP assets to a third party. The previously listed licensed patents under Schedule A that were licensed to SINTX (Amedica) by the Dr. Jackson and SMS Trust pursuant to a license agreement between the parties has been assigned to CTL Medical as part of the sale of the spine business.

Our remaining issued patents and pending applications are directed to additional aspects of our products and technologies including, among other things:

| ● | designs for intervertebral fusion devices; | |

| ● | designs for hip implants; | |

| ● | designs for knee implants; | |

| ● | implants with improved antibacterial characteristics; | |

| ● | implants with improved wear performance; and | |

| ● | Antipathogenic compositions. |

We also expect to rely on trade secrets, know-how, continuing technological innovation and in-licensing opportunities to develop and maintain our intellectual property position. However, trade secrets are difficult to protect. We seek to protect the trade secrets in our proprietary technology and processes, in part, by entering into confidentiality agreements with commercial partners, collaborators, employees, consultants, scientific advisors and other contractors and into invention assignment agreements with our employees and some of our commercial partners and consultants. These agreements are designed to protect our proprietary information and, in the case of the invention assignment agreements, to grant us ownership of the technologies that are developed.

Competition

The main alternatives to our silicon nitride biomaterial include: PEEK, which is predominantly manufactured by Invibio; BIOLOX® delta, which is a traditional oxide ceramic manufactured by CeramTec; allograft bone; metals; and coated metals.

We believe our main competitors in the orthopedic implant market, which utilize a variety of competitive biomaterials, include: Medtronic, Inc.; DePuy Synthes Companies, a group of Johnson & Johnson companies; Stryker Corporation; Biomet, Inc.; Zimmer Holdings, Inc.; Smith & Nephew plc; and Aesculap Inc. Presently, these companies buy ceramic components on an OEM basis from manufacturers such as CeramTec, Kyocera and CoorsTek, Inc., among others. We anticipate that these and other orthopedic companies and OEMs will seek to introduce new biomaterials and products that compete with ours.

| 17 |

Competition within the industry is primarily based on technology, innovation, product quality, and product awareness and acceptance by surgeons. Our principal competitors have substantially greater financial, technical and marketing resources, as well as significantly greater manufacturing capabilities than we do, and they may succeed in developing products that render our implants and product candidates non-competitive. Our ability to compete successfully will depend upon our ability to develop innovative products with advanced performance features based on our silicon nitride technologies.

Government Regulation of Medical Devices

Governmental authorities in the United States, at the federal, state and local levels, and other countries extensively regulate, among other things, the research, development, testing, manufacture, labeling, promotion, advertising, distribution, marketing and export and import of products such as those we are commercializing and developing. Failure to obtain approval or clearance to market our products and products under development and to meet the ongoing requirements of these regulatory authorities could prevent us from continuing to market or develop our products and product candidates.

United States

Pre-Marketing Regulation

In the United States, medical devices are regulated by the FDA. Unless an exemption applies, a new medical device will require either prior 510(k) clearance or approval of a premarket approval application, or PMA, before it can be marketed in the United States. The information that must be submitted to the FDA in order to obtain clearance or approval to market a new medical device varies depending on how the medical device is classified by the FDA. Medical devices are classified into one of three classes on the basis of the controls deemed by the FDA to be necessary to reasonably ensure their safety and effectiveness. Class I devices, which are those that have the lowest level or risk associated with them, are subject to general controls, including labeling, premarket notification and adherence to the QSR. Class II devices are subject to general controls and special controls, including performance standards. Class III devices, which have the highest level of risk associated with them, are subject to most of the previously identified requirements as well as to premarket approval. Most Class I devices and some Class II devices are exempt from the 510(k) requirements, although manufacturers of these devices are still subject to registration, listing, labeling and QSR requirements.

A 510(k) premarket notification must demonstrate that the device in question is substantially equivalent to another legally marketed device, or predicate device, that did not require premarket approval. In evaluating the 510(k), the FDA will determine whether the device has the same intended use as the predicate device, and (a) has the same technological characteristics as the predicate device, or (b) has different technological characteristics, and (i) the data supporting the substantial equivalence contains information, including appropriate clinical or scientific data, if deemed necessary by the FDA, that demonstrates that the device is as safe and as effective as a legally marketed device, and (ii) does not raise different questions of safety and effectiveness than the predicate device. Most 510(k)s do not require clinical data for clearance, but the FDA may request such data. The FDA’s goal is to review and act on each 510(k) within 90 days of submission, but it may take longer based on requests for additional information. In addition, requests for additional data, including clinical data, will increase the time necessary to review the notice. If the FDA does not agree that the new device is substantially equivalent to the predicate device, the new device will be classified in Class III, and the manufacturer must submit a PMA. Since July 2012, however, with the enactment of the Food and Drug Administration Safety and Innovation Act, or FDASIA, a de novo pathway is directly available for certain low to moderate risk devices that do not qualify for the 510(k) pathway due to lack of a predicate device. Modifications to a 510(k)-cleared medical device may require the submission of another 510(k) or a PMA if the changes could significantly affect the safety or effectiveness or constitute a major change in the intended use of the device.

Modifications to a 510(k)-cleared device frequently require the submission of a traditional 510(k), but modifications meeting certain conditions may be candidates for FDA review under a Special 510(k). If a device modification requires the submission of a 510(k), but the modification does not affect the intended use of the device or alter the fundamental scientific technology of the device, then summary information that results from the design control process associated with the cleared device can serve as the basis for clearing the application. A Special 510(k) allows a manufacturer to declare conformance to design controls without providing new data. When the modification involves a change in material, the nature of the “new” material will determine whether a traditional or Special 510(k) is necessary. For example, in its Device Advice on How to Prepare a Special 510(k), the FDA uses the example of a change in a material in a finger joint prosthesis from a known metal alloy to a ceramic that has not been used in a legally marketed predicate device as a type of change that should not be submitted as a Special 510(k). However, if the “new” material is a type that has been used in other legally marketed devices within the same classification for the same intended use, a Special 510(k) is appropriate. The FDA gives as an example a manufacturer of a hip implant who changes from one alloy to another that has been used in another legally marketed predicate. Special 510(k)s are typically processed within 30 days of receipt.

| 18 |

The PMA process is more complex, costly and time consuming than the 510(k) clearance procedure. A PMA must be supported by extensive data including, but not limited to, technical, preclinical, clinical, manufacturing, control and labeling information to demonstrate to the FDA’s satisfaction the safety and effectiveness of the device for its intended use. After a PMA is submitted, the FDA has 45 days to determine whether it is sufficiently complete to permit a substantive review. If the PMA is complete, the FDA will file the PMA. The FDA is subject to performance goal review times for PMAs and may issue a decision letter as a first action on a PMA within 180 days of filing, but if it has questions, it will likely issue a first major deficiency letter within 150 days of filing. It may also refer the PMA to an FDA advisory panel for additional review and will conduct a preapproval inspection of the manufacturing facility to ensure compliance with the QSR, either of which could extend the 180-day response target. While the FDA’s ability to meet its performance goals has generally improved during the past few years, it may not meet these goals in the future. A PMA can take several years to complete and there is no assurance that any submitted PMA will ever be approved. Even when approved, the FDA may limit the indication for which the medical device may be marketed or to whom it may be sold. In addition, the FDA may request additional information or request the performance of additional clinical trials before it will reconsider the approval of the PMA or as a condition of approval, in which case the trials must be completed after the PMA is approved. Changes to the device, including changes to its manufacturing process, may require the approval of a supplemental PMA.

If a medical device is determined to present a “significant risk,” the manufacturer may not begin a clinical trial until it submits an investigational device exemption, or IDE, to the FDA and obtains approval of the IDE from the FDA. The IDE must be supported by appropriate data, such as animal and laboratory testing results and include a proposed clinical protocol. These clinical trials are also subject to the review, approval and oversight of an institutional review board, or IRB, which is an independent and multi-disciplinary committee of volunteers who review and approve research proposals, and the reporting of adverse events and experiences, at each institution at which the clinical trial will be performed. The clinical trials must be conducted in accordance with applicable regulations, including but not limited to the FDA’s IDE regulations and current good clinical practices. A clinical trial may be suspended by the FDA, the IRB or the sponsor at any time for various reasons, including a belief that the risks to the study participants outweigh the benefits of participation in the trial. Even if a clinical trial is completed, the results may not demonstrate the safety and efficacy of a device or may be equivocal or otherwise not be sufficient to obtain approval.

Post-Marketing Regulation

After a device is placed on the market, numerous regulatory requirements apply. These include:

| ● | compliance with the QSR, which require manufacturers to follow stringent design, testing, control, documentation, record maintenance, including maintenance of complaint and related investigation files, and other quality assurance controls during the manufacturing process; | |

| ● | labeling regulations, which prohibit the promotion of products for uncleared or unapproved or “off-label” uses and impose other restrictions on labeling; and | |

| ● | medical device reporting obligations, which require that manufacturers investigate and report to the FDA adverse events, including deaths, or serious injuries that may have been or were caused by a medical device and malfunctions in the device that would likely cause or contribute to a death or serious injury if it were to recur. |

| 19 |

Failure to comply with applicable regulatory requirements can result in enforcement action by the FDA, which may include any of the following sanctions:

| ● | warning letters; | |

| ● | fines, injunctions, and civil penalties; | |

| ● | recall or seizure of our products; | |

| ● | operating restrictions, partial suspension or total shutdown of production; | |

| ● | refusal to grant 510(k) clearance or PMA approvals of new products; | |

| ● | withdrawal of 510(k) clearance or PMA approvals; and | |

| ● | criminal prosecution. |

To ensure compliance with regulatory requirements, medical device manufacturers are subject to market surveillance and periodic, pre-scheduled and unannounced inspections by the FDA, and these inspections may include the manufacturing facilities of our subcontractors.

International Regulation

International sales of medical devices are subject to foreign government regulations, which vary substantially from country to country. The time required to obtain approval by a foreign country may be longer or shorter than that required for FDA approval, and the requirements may differ. For example, the primary regulatory authority with respect to medical devices in Europe is that of the European Union. The European Union consists of 28 countries and has a total population of over 500 million people. The unification of these countries into a common market has resulted in the unification of laws, standards and procedures across these countries, which may expedite the introduction of medical devices like those we are offering and developing. Norway, Iceland, Lichtenstein and Switzerland are not members of the European Union but have transposed applicable European medical device laws into their national legislation. Thus, a device that is marketed in the European Union may also be recognized and accepted in those four non-member European countries as well.

The European Union has adopted numerous directives and standards regulating the design, manufacture, clinical trials, labeling and adverse event reporting for medical devices. Devices that comply with the requirements of relevant directives will be entitled to bear CE Conformity Marking, indicating that the device conforms to the essential requirements of the applicable directives and, accordingly, can be commercially distributed throughout the European Union. Actual implementation of these directives, however, may vary on a country-by-country basis. The CE Mark is a mandatory conformity mark on medical devices distributed and sold in the European Union and certifies that a medical device has met applicable requirements.