Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATE PURSUANT TO SECTION 18 U.S.C. PURSUANT TO SECTION 906 OF THE SARBANE - SMITH MIDLAND CORP | smid-12312019x10kex32.htm |

| EX-31.2 - CERTIFICATION PURSUANT TO RULE 13A-14(A)/15D-14(A) CERTIFICATIONS SECTION 302 OF - SMITH MIDLAND CORP | smid-12312019x10kex312.htm |

| EX-31.1 - CERTIFICATION PURSUANT TO RULE 13A-14(A)/15D-14(A) CERTIFICATIONS SECTION 302 OF - SMITH MIDLAND CORP | smid-12312019x10kex311.htm |

| EX-23.1 - CONSENTS OF EXPERTS AND COUNSEL - SMITH MIDLAND CORP | smid-12312019x10kex231.htm |

| EX-10.12 - LINE OF CREDIT AGREEMENT - SMITH MIDLAND CORP | commerciallineofcreditagr.htm |

| EX-10.11 - EQUIPMENT LINE COMMITMENT LETTER - SMITH MIDLAND CORP | equipmentlinecommitmentle.htm |

| EX-10.10 - LINE OF CREDIT COMMITMENT LETTER - SMITH MIDLAND CORP | lineofcreditcommitmentlet.htm |

UNITED

STATES

SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C.

20549

FORM

10-K

☒

Annual Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934 For the Fiscal Year

Ended December 31,

2019

or

☐

Transition Report Pursuant to

Section 13 or 15(d) of the Securities Exchange Act of

1934

Commission File Number

1-13752

Smith-Midland

Corporation

(Exact Name of

Registrant as Specified in its Charter)

|

Delaware

|

54-1727060

|

|

(State or Other

Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer

Identification No.)

|

P.O.

Box 300, 5119 Catlett Road

Midland,

Virginia 22728

(Address of Principal Executive Offices, Zip

Code)

Registrant's telephone number,

including area code: (540) 439-3266

Securities Registered Under Section 12(b) of

the Act:

|

Title of

each class

|

Trading

Symbol

|

Name of exchange

on which registered

|

|

Common

Stock, $0.01 par value per share

|

SMID

|

OTCQX

|

Securities Registered Pursuant to Section 12(g)

of the Act: None

Indicate by check mark

if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.Yes ☐ No

☒

Indicate by check mark

if the registrant is not required to file reports pursuant to

Section 13 or 15(d) of the Act.Yes ☐ No

☒

Indicate by check mark

whether the registrant: (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days.Yes

☒ No ☐

Indicate by check mark

whether the registrant has submitted electronically every

Interactive Data File required to be submitted pursuant to Rule 405

of Regulation S-T (§232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant

was required to submit such files).Yes ☒ No

☐

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the

definitions of “large accelerated filer”,

“accelerated filer”, “smaller reporting

company”, and "emerging growth company" in Rule 12b-2 of the

Exchange Act.

|

Large accelerated

filer

|

☐

|

Accelerated

filer

|

☐

|

Non-accelerated filer

|

☐

|

Smaller

reporting company

|

☒

|

Emerging

growth company

|

☐

|

Indicate by check

mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act).Yes ☐ No

☒

The aggregate market

value of the shares of the voting and non-voting common equity held

by non-affiliates computed by reference to the average bid and

asked price of such common equity as of June 30, 2019 (the last

business day of the Company’s most recently completed second

fiscal quarter) was $30,748,256. For the sole purpose of making

this calculation, the term “non-affiliate” has been

interpreted to exclude directors, officers, and holders of 10% or

more of the Company’s common stock.

1

As of March 5,

2020, the Company had outstanding 5,164,685 shares of Common Stock,

$.01 par value per share, net of treasury shares.

Documents

Incorporated By Reference

None

2

FORWARD-LOOKING

STATEMENTS

This Annual Report and

related documents include “forward-looking statements”

within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as

amended. Forward-looking statements involve known and unknown

risks, uncertainties and other factors which could cause the

Company’s actual results, performance (financial or

operating) or achievements expressed or implied by such forward

looking statements not to occur or be realized. Such forward

looking statements generally are based upon the Company’s

best estimates of future results, performance or achievement, based

upon current conditions and the most recent results of operations.

Forward-looking statements may be identified by the use of

forward-looking terminology such as “may,”

“will,” “expect,” “believe,”

“estimate,” “anticipate,”

“continue,” or similar terms, variations of those terms

or the negative of those terms. Potential risks and uncertainties

include, among other things, such factors as:

•

Although uncertain at this time, the

coronavirus outbreak may ultimately significantly affect the

Company's financial condition, liquidity, and future results of

operations,

•

while the Company reported net income

for the years ended December 31, 2019 and 2018, there are no

assurances the Company can remain profitable in future

periods,

•

our debt level increased in 2019 and

2018, and our ability to satisfy the same cannot be

assured,

•

the continued availability of

financing in the amounts, at the times, and on the terms required,

to support our future business and capital projects,

•

while

we have expended significant funds in recent years to increase

manufacturing capacity, there is no assurance that we will achieve

significantly greater sales,

•

the extent to which we are successful

in developing, acquiring, licensing or securing patents for

proprietary products,

•

changes in economic conditions

specific to any one or more of our markets (including the

availability of public funds and grants for

construction),

•

changes in general economic

conditions in the Company's primary service areas,

•

adverse weather which inhibits the

demand for our products,

•

our compliance with governmental

regulations,

•

the outcome of future litigation, if

any,

•

on material construction projects,

our ability to produce and install product that conforms to

contract specifications and in a time frame that meets the contract

requirements,

•

the cyclical nature of the

construction industry,

•

our exposure to increased interest

expense payments should interest rates change, and

•

the other factors and information

disclosed and discussed in other sections of this

report.

Investors and

shareholders should carefully consider such risks, uncertainties

and other information, disclosures and discussions which contain

cautionary statements identifying important factors that could

cause actual results to differ materially from those provided in

the forward-looking statements. We undertake no obligation to

publicly update or revise any forward-looking statements, whether

as a result of new information, future events or

otherwise.

3

PART I

Item

1 Business

General

Smith-Midland

Corporation (the "Company") invents, develops, manufactures,

markets, leases, licenses, sells, and installs a broad array of

precast concrete products for use primarily in the construction,

highway, utilities and farming industries through its six

wholly-owned subsidiaries. The Company's precast, licensing and

barrier rental customers are primarily general contractors and

federal, state, and local transportation authorities located in the

Mid-Atlantic, Northeastern, Midwestern and Southeastern regions of

the United States. The Company's operating strategy has involved

producing innovative and proprietary products, including

SlenderWall®, a patent pending, lightweight, energy efficient

concrete and steel exterior wall panel for use in building

construction; J-J Hooks® Highway Safety Barrier, a patented,

positive-connected highway safety barrier; SoftSound™, a

proprietary sound absorptive finish used on the face of sound

barriers to absorb some of the traffic noise; Sierra Wall™, a

patented sound barrier primarily for roadside use; Easi-Set®

and Easi-Span® patented transportable concrete buildings; and

Beach Prisms™ erosion mitigating modules. In addition,

the Company's precast subsidiaries produce farm products such as

cattleguards and water and feed troughs as well as custom order

precast concrete products with various architectural surfaces, as

well as generic highway sound barriers, retaining walls and utility

vaults.

The Company was

incorporated in Delaware on August 2, 1994. Prior to a corporate

reorganization completed in October 1994, the Company conducted its

business primarily through Smith-Midland Virginia, which was

incorporated in 1960 as Smith Cattleguard Company, a Virginia

corporation, and which subsequently changed its name to

Smith-Midland Corporation in 1985. The Company’s principal

offices are located at 5119 Catlett Road, Midland, Virginia 22728

and its telephone number is 540-439-3266. As used in this report,

unless the context otherwise requires, the term the

“Company” refers to Smith-Midland Corporation and its

subsidiaries. The Company’s wholly owned subsidiaries consist

of Smith-Midland Corporation, a Virginia corporation;

Smith-Carolina Corporation, a North Carolina corporation;

Smith-Columbia Corporation, a South Carolina corporation, Easi-Set

Industries Worldwide, Inc., a Virginia corporation; Concrete Safety

Systems, Inc., a Virginia corporation; and Midland Advertising and

Design, Inc., a Virginia corporation doing business as Midland

Advertising + Design.

Market

The Company's precast

concrete products market and barrier rental market primarily

consists of general contractors performing public and private

construction contracts, including the construction of commercial

buildings, public and private roads and highways, and airports,

municipal utilities, and federal, state, and local transportation

authorities, primarily located in the Mid-Atlantic, Northeastern,

Midwestern and Southeastern states. Due to the lightweight

characteristics of the SlenderWall® exterior cladding system,

the Company has expanded its competitive services outside of the

Mid-Atlantic states. The Company's licensing subsidiary licenses

its proprietary products to precast concrete manufacturers

nationwide and internationally in Canada, Belgium, New Zealand,

Australia, Mexico, Trinidad, Spain, and Chile.

The precast concrete

products market is affected by the cyclical nature of the

construction industry. In addition, the demand for construction

varies depending upon weather conditions, the availability of

financing at reasonable interest rates, overall fluctuations in the

national and regional economies, past overbuilding, labor relations

in the construction industry, and the availability of material and

energy supplies. A substantial portion of the Company's business is

derived from local, state, and federal building projects, which are

further dependent upon budgets and, in some cases, voter-approved

bonds.

Products

The Company's precast

concrete products are cast in manufacturing facilities and

delivered to a site for installation, as contrasted to ready-mix

concrete, which is produced offsite in a “batch

plant,”and delivered with a concrete mixer truck where it is

mixed and delivered to a construction site to be poured and set at

the site. Precast concrete products are used primarily as parts of

buildings or highway structures, and may be used architecturally,

as in a decorative wall of a building. Structural uses include

building walls, frames, floors, or roofs. The Company

currently manufactures and sells a wide variety of products for use

in the construction, transportation and utility

industries.

4

SlenderWall® Lightweight

Construction Panels

The SlenderWall®

system is a patent pending prefabricated, energy-efficient,

lightweight exterior cladding system that is offered as a

cost-effective alternative to the traditional cladding used for the

exterior walls of buildings. The Company's SlenderWall® system

combines the essential components of a wall system into a single

panel ready for interior dry wall mounting upon installation. The

base components of each SlenderWall® panel consists of a

galvanized stud frame with an exterior surface of approximately

two-inch thick, steel reinforced, high-density, precast concrete

(with integral water repellent), a thermal break, and various

architectural surfaces. The exterior architectural concrete facing

is attached to the interior steel frame by use of coated stainless

steel fasteners that position the exterior concrete away from the

steel frame to provide improved thermal performance.

SlenderWall® panels

are approximately one-third the weight of traditional precast

concrete walls of equivalent size, permanence and durability, and

are also significantly improved as to permanence and

durability. The lighter weight translates into reduced

construction costs resulting from less onerous structural and

foundation requirements as well as lower shipping costs. Additional

savings result from reduced installation time, ease of erection,

and the use of smaller cranes for installation. Closed-cell foam

insulation and windows can be plant-installed further reducing cost

and construction schedules.

The Company custom

designs, manufactures, installs, and licenses the SlenderWall®

exterior cladding system. The exterior of the SlenderWall®

system can be produced in a variety of attractive architectural

finishes, such as concrete, exposed stone, granite or thin brick

and can be integrated with other cladding materials.

Sierra

Wall™

The Sierra Wall™

("Sierra Wall") combines the strength and durability of precast

concrete with a variety of finishes to provide an effective and

attractive sound and sight barrier for use alongside highways

around residential, industrial, and commercial properties. With

additional reinforcement, Sierra Wall can also be used as a

retaining wall to retain earth in both highway and residential

construction. Sierra Wall is typically constructed of four-inch

thick, steel-reinforced concrete panels with an integral column

creating a tongue and groove connection system. This tongue

and groove connection system and its foundation connection make

Sierra Wall easy to install and move if boundaries change or

highways are relocated after the completion of a project. The

patented Sierra Wall II one-piece extended post and panel design

reduces installation time and cost.

The Company custom

designs and manufactures Sierra Wall components to conform to the

specifications provided by the contractor. The width, height,

strength, and exterior finish of each wall varies depending upon

the terrain and application. The Company also produces generic

post and panel design sound barrier wall systems. These

systems are constructed of steel or precast concrete columns (the

Company manufactures the precast or prestressed columns) with

precast concrete panels which slide down into the groove in each

column.

Sierra Wall is used

primarily for highway projects as a noise barrier as well as for

residential purposes, such as privacy walls between homes, security

walls or windbreaks, and for industrial or commercial purposes,

such as to screen and protect shopping centers, industrial

operations, institutions or highways. The variety of available

finishes enables the Company to blend the Sierra Wall with local

architecture, creating an attractive, as well as functional,

barrier.

J-J

Hooks® Highway Safety Barrier

The J-J Hooks®

highway safety barriers (the "J-J Hooks Barriers") are crash-tested

(privately funded), positively connected, safety barriers that the

Company sells, rents, delivers, installs, and licenses for use on

roadways to separate lanes of traffic (in free-standing, bolted, or

pinned installations) in construction work zones or for traffic

control. Barriers are deemed to be positively connected when

the connectors on each end of the barrier sections are interlocked

with one another. J-J Hooks Barriers interlock without the need for

a separate locking device. The primary advantage of a positive

connection is that a barrier with such a connection can withstand

vehicle crashes at higher speeds without separating. The

Federal Highway Administration ("FHWA") requires that states use

only positively connected barriers, which meet NCHRP-350 or MASH

crash test requirements. J-J Hooks Barriers that meet NCHRP-350 and

MASH TL3 requirements are deemed eligible by the FHWA for

federal-aid reimbursement. The Company has been issued patents with

respect to J-J Hooks in the United States, Canada, and other

countries.

5

The Company has received

“design protection” in the U.S for the “end

taper” on each end of the barrier sections. The United States

has issued a "trade dress" registration for the "end taper" design

feature. Accordingly, in the United States, these features cannot

be legally copied by others.

The proprietary feature

of J-J Hooks Barriers is the design of its positive connection.

Protruding from each end of a J-J Hooks Barrier section is a

fabricated bent steel connector; rolled in toward the end of the

barrier, resembling the letter "J" when viewed from directly

above. The connector protruding from each end of the barrier

is rolled identically so that when one end of a barrier faces the

end of another, the resulting "J-Hook" face each other. To

connect one section of a J-J Hooks Barrier to another, a contractor

merely positions the J-Hook of an elevated section of the barrier

above the J-Hook of a set section and lowers the elevated section

into place. The positive connection is automatically engaged

using the cast-in alignment slot.

The Company believes

that the J-J Hooks Barrier connection design is superior to other

highway safety barriers that were positively connected through the

"eye and pin" technique. Barriers incorporating this technique

have eyes or loops protruding from each end of the barrier, which

must be aligned during the setting process. Once set, a crew

inserts pins or long bolts through the eyes which connects and

bolts the barrier sections together. Compared to this technique,

the J-J Hooks Barriers are easier and faster to install and remove,

require a smaller crew, and eliminates the need for loose hardware

to make the connection.

In March 1999, the FHWA

approved the free-standing J-J Hooks Barrier (tested in accordance

with NCHRP-350 Test Level 3) following successful crash testing in

accordance with National Cooperative Highway Research Program

requirements. In December 2012 the FHWA approved the pinned and

bolted J-J Hooks and in March 2018 approved the free-standing J-J

Hooks. In September 2018 the FHWA approved a 20-foot design

originally tested to NCHRP-350 TL3 requirements and approved by the

FHWA (tested in accordance with MASH Test Level 3) for use on

federally aided highway projects following the successful

completion of crash testing based on criteria from the AASHTO

Manual for Assessing Safety Hardware.

J-J Hooks NCHRP-350

free-standing barrier has been approved for use on state and

federally funded projects by 42 states, plus Washington, D.C. The

Company is in various stages of the application process in

additional states and believes that approval in some of the

states will be granted; however no assurance can be given that

approval will be received from any or all of the remaining states

or that such approval will result in the J-J Hooks Barrier being

used in such states. In addition, J-J Hooks Barrier has been

approved by the appropriate authorities for use in the countries of

Canada (Alberta, Nova Scotia, New Brunswick and Ontario),

Australia, New Zealand, Spain, Portugal, Belgium, Germany and

Chile.

J-J Hooks restrained

(pinned or bolted) barrier successfully passed the MASH TL3 tests

in August of 2012 and received FHWA Eligibility Letters in December

2012. Currently 33 states have approved the MASH restrained barrier

and 28 states have approved the MASH free-standing design as an

alternate to their state standard. In Canada, the provinces of

Alberta and Nova Scotia have approved the MASH tested barrier. The

new J-J Hooks free-standing barrier successfully passed the two

required MASH TL3 tests and in January 2018 and August 2018

received the FHWA federal-aid eligibility letters. The FHWA

Eligibility letters B300 and B307 have been issued as of February

2018 and September 2018, respectively.

Easi-Set

Precast Buildings and Easi-Span®

Expandable

Precast Buildings

Easi-Set Precast

Buildings are transportable, prefabricated, single-story, all

concrete buildings designed to be adaptable to a variety of uses

ranging from housing communications operations, traffic control

systems, mechanical and electrical stations, to inventory or supply

storage, restroom facilities or kiosks. Easi-Set Precast Buildings

and Restrooms are available in a variety of exterior finishes and

in 38 standard sizes, or can be custom sized. The roof and floor of

each Easi-Set Building is manufactured using the Company's second

generation post-tensioned system, which helps seal the buildings

against moisture. As freestanding units, the Easi-Set Buildings

require no poured foundations or footings and can be easily

installed within a few hours. After installation the buildings can

be moved, if desired, and reinstalled in a new location. The

Company has been issued patents in connection with this product in

the United States and Canada.

The Company also

offers Easi-Span® a line of expandable precast concrete

buildings. Easi-Span® incorporates the technology of the

Easi-Set Buildings, but are available in larger sizes and, through

its modular construction, can be combined in varied configurations

to permit expansion capabilities. Since these larger buildings

have less competition from other materials and methods, they

produce higher profit margins. Both the Easi-Span and Easi-Set

Buildings offer lines of fully-outfitted restrooms with over a

dozen standard models.

6

The Company has sold

its Easi-Set® and Easi-Span® Precast Buildings for the

following uses:

●

Communications

Operations — to house fiber optics regenerators,

switching stations and microwave transmission shelters, cellular

phone sites, and cable television repeater stations.

●

Government

Applications — to federal, state and local authorities

for uses such as weather and pollution monitoring stations;

military storage, housing and operations; park vending enclosures;

restrooms; kiosks; traffic control systems; school maintenance and

athletic storage; airport lighting control and transmitter housing;

and law enforcement evidence and ammunition storage.

●

Utilities

Installations — for electrical switching stations and

transformer housing, gas control shelters and valve enclosures,

water and sewage pumping stations, and storage of contaminated

substances or flammable materials which require spill

containment.

●

Commercial and Industrial

Locations — for electrical and mechanical housing,

cemetery maintenance storage, golf course vending enclosures,

mechanical rooms, restrooms, emergency generator shelters, gate

houses, automobile garages, hazardous materials storage, food or

bottle storage, animal shelters, and range houses.

Easi-Set

Utility Vault

The Company produces a

line of precast concrete underground utility vaults ranging in size

from 27 to 1,008 cubic feet. Each Easi-Set utility vault normally

comes with a manhole opening on the top for ingress and egress and

openings around the perimeter, in accordance with the customer's

specifications, to access water and gas pipes, electrical power

lines, telecommunications cables, or other such media of transfer.

The utility vaults may be used to house equipment such as cable,

telephone or traffic signal equipment, and for underground storage.

The Company also manufactures custom-built utility vaults for

special needs.

SoftSound™

Soundwall Panels

SoftSound™

soundwall panels utilize a “wood chip aggregate” sound

absorptive material applied to the face of soundwall panels, which

is used to absorb highway noise. SoftSound™ is a

proprietary product developed and tested by the Company and is

currently approved for use in Virginia, Maryland, seven additional

states, and the provinces of Ontario and Quebec, Canada. Approvals

are still pending in a number of additional states. The

Company introduced this product line into its licensing program and

is in the process of seeking to obtain approvals in all 50 states

and the Canadian Provinces.

Beach

Prisms™ Erosion Control Modules

In 2006, the Company

began production and launched full-scale advertising and

promotional efforts for its product, Beach Prisms™, a

shoreline erosion control product that uses the preferred natural

"soft" approach as opposed to the "hard" approach of seawalls and

jetties, to solve this worldwide problem. This product is

expected to provide a higher margin than many of the

Company’s other product lines. Beach Prisms™ work by

reducing the amount of energy in incoming waves before the waves

reach the shoreline. Waves pass through the specially designed

slots in the triangular 3-4 foot tall by 10 foot long Beach

Prisms™ modules. The success of a Beach Prisms ™

installation is dependent on the prevailing wind in relation to the

shoreline, the tides, the fetch and the availability of sand in the

surf. Beach Prisms™ are primarily for river- and bay-front

property owners who want an alternative to traditional armor stone,

or groins and jetties. The Company received “design

protection” in the United States for the Beach Prisms™

in 2010.

The Company currently

has orders and is also accepting new orders with deposits for the

Beach Prism product, and the Company is working with the states of

Virginia and Maryland to secure approval of each state’s

environmental agency. Each project must apply for approval by the

appropriate state to obtain a permit to install the Beach Prism.

Such approvals are meeting resistance from the environmental

agencies, however, the Company believes approval is forthcoming.

One permit has been received from the State of Maryland. In the

event that approvals are not timely received, these orders may be

cancelled.

7

H2Out™

Secondary Drainage System

H2Out™ is the

first "in the caulk joint" secondary drainage and street level leak

detection product for panelized exterior cladding. A second line of

caulking and drainage strip located behind the exterior line of

caulking exits all water leakage to the exterior of the building

preventing moisture and mold, and hence deterring lawsuits from

tenants and owners of buildings. H2Out™ has been added

as a feature of the SlenderWall® system and is being included

in the product literature, website, and all sales

presentations.

Although the Company

is optimistic about the success of Beach Prisms™ and

H2Out™, there can be no assurance of the commercial

acceptance of these products.

Sources of

Supply

All of the raw materials

necessary for the manufacture of the Company's products are

available from multiple sources. To date, the Company has not

experienced significant delays in obtaining materials and believes

that it will continue to be able to obtain required materials from

a number of suppliers at commercially reasonable

prices.

Licensing

The Company presently

grants licenses through its wholly-owned subsidiary Easi-Set

Industries for the manufacturing and sale rights for certain

proprietary products, such as the J-J Hooks® Barrier,

Easi-Set®/Easi-Span® Precast Buildings,

SlenderWall®, SoftSound™ and Beach Prisms™ as well

as certain non-proprietary products, such as the Company's

cattleguards. Generally, licenses are granted for a point of

manufacture. The Company receives an initial one-time training

and administration license fee varying on the product

licensed. License royalties vary depending upon the product

licensed, but the range is typically 4% to 6% of the net sales of

the licensed product. In addition,

Easi-Set®/Easi-Span® Buildings and SlenderWall®

licensees pay the Company a monthly fee for co-op advertising &

promotional programs. The Company produces and distributes

advertising & promotional materials and promotes the licensed

products through its own advertising subsidiary, Midland

Advertising + Design.

The Company maintains 57

licensing agreements in the United States, 9 in Canada, and 1 each

in Australia, Belgium, Mexico, New Zealand and Trinidad, for a

total of 71 licenses worldwide.

The Company is

continually discussing new license arrangements with potential

precast companies and, although no assurance can be given, expects

to increase its licensing activities.

Marketing and

Sales

The Company uses an

in-house sales force and, to a lesser extent, independent sales

representatives to market its precast concrete products through

trade show attendance, sales presentations, advertisements in trade

publications, and direct mail to end users.

The Company has also

established a cooperative advertising program in which the Company

and its Easi-Set®/Easi-Span® Buildings and

SlenderWall® licensees combine resources to promote certain

precast concrete products. Licensees pay a monthly fee and the

Company pays any additional amounts required to advertise the

products across the country. Although the Company advertises

nationally, the Company's precast subsidiaries marketing efforts

are concentrated within a 450 mile radius from its facilities,

which includes the majority of the eastern United

States.

The Company's precast

product sales and barrier rental sales result primarily from the

submission of estimates or proposals to general contractors who

then include the estimates in their overall bids to various

government agencies and other end users that solicit construction

contracts through a competitive bidding process. In general,

these contractors solicit and obtain their construction contracts

by submitting the most attractive bid to the party desiring the

construction. The Company's role in the bidding process is to

provide estimates to the contractors desiring to include the

Company's products or services in the contractor's bid. If a

contractor who accepts the Company's bid is selected to perform the

construction, the Company provides the agreed upon products or

services. In many instances, the Company provides estimates to

more than one of the contractors bidding on a single

project. The Company also occasionally negotiates with and

sells directly to end-users.

8

Competition

The precast concrete

industry is highly competitive and consists of a few large

companies and many small to mid-size companies, several of which

have substantially greater financial and other resources than the

Company. Nationally, several large companies dominate the

precast concrete market. However, due to the weight and costs

of delivery of precast concrete products, competition in the

industry tends to be limited by geographical location and distance

from the construction site and is fragmented with numerous

manufacturers in a large local area.

The Company believes

that the principal competitive factors for its precast products are

price, durability, ease of use and installation, speed of

manufacture and delivery time, ability to customize, FHWA and state

approval, and customer service. The Company believes that its

plants in Midland, Virginia, Reidsville, North Carolina and

Columbia, South Carolina compete favorably with respect to each of

these factors in the Mid-Atlantic and Southeastern regions of the

United States. Finally, the Company believes it offers a broad

range of products that are very competitive in these

markets.

Intellectual

Property

The Company seeks

to protect our intellectual property rights by relying on federal,

state and common law rights in the United States and other

countries, as well as contractual restrictions. Our intellectual

property assets include patents, patent applications, trade

secrets, trademarks, trade dress, copyrights, operating and

instruction manuals, non-disclosure and other contractual

arrangements.

While the Company

intends to vigorously enforce its patent rights against

infringement by third parties, no assurance can be given that the

patents or the Company's patent rights will be enforceable or

provide the Company with meaningful protection from competitors or

that its patent applications will be allowed. Even if a

competitor's products were to infringe patents held by the Company,

enforcing the patent rights in an enforcement action could be very

costly, and assuming the Company has sufficient resources, would

divert funds and resources that otherwise could be used in the

Company's operations. No assurance can be given that the

Company would be successful in enforcing such rights, that the

Company's products or processes do not infringe the patent or

intellectual property rights of a third party, or that if the

Company is not successful in a suit involving patents or other

intellectual property rights of a third party, that a license for

such technology would be available on commercially reasonable

terms, if at all.

Government

Regulation

The Company frequently

supplies products and services pursuant to agreements with general

contractors who have entered into contracts with federal or state

governmental agencies. The successful completion of the

Company’s obligations under such contracts is often subject

to the satisfactory inspection or approval of such products and

services by a representative of the contracting

agency. Although the Company endeavors to satisfy the

requirements of each such contract to which it is a party, no

assurance can be given that the necessary approval of its products

and services will be granted on a timely basis or at all and that

the Company will receive any payments due to it. Any failure

to obtain such approval and payment may have a material adverse

effect on the Company's business.

The Company's operations

are subject to extensive and stringent governmental regulations

including regulations related to the Occupational Safety and Health

Act (OSHA) and environmental protection. The Company believes

that it is substantially in compliance with all applicable

regulations. The cost of maintaining such compliance is not

considered by the Company to be significant.

9

The Company's employees

in its manufacturing division operate complicated machinery that

may cause substantial injury or death upon malfunction or improper

operation. The Company's manufacturing facilities are subject

to the workplace safety rules and regulations of OSHA. The

Company believes that it is in compliance with the requirements of

OSHA.

During the normal course

of its operations, the Company uses and disposes of materials, such

as solvents and lubricants used in equipment maintenance, that are

classified as hazardous by government agencies that regulate

environmental quality. The Company attempts to minimize the

generation of such waste as much as possible, and to recycle such

waste where possible. Remaining wastes are disposed of in

permitted disposal sites in accordance with applicable

regulations.

In the event that the

Company is unable to comply with the OSHA or environmental

requirements, the Company could be subject to substantial

sanctions, including restrictions on its business operations,

monetary liability and criminal sanctions, any of which could have

a material adverse effect upon the Company's business.

Employees

As of March 5,

2020, the Company had a total of 232 employees, of which 183 are

full-time, 7 are part-time and 42 are temporary workers, with 161

located at the Company's Midland, Virginia facility, 35 are located

at the Company's facility in Reidsville, North Carolina and 36 are

located at the Company's facility in Hopkins, South

Carolina. None of the Company's employees are represented by

labor organizations and the Company is not aware of any activities

seeking such organization. The Company considers its

relationships with its employees to be satisfactory.

Item

1A. Risk

Factors

Not

applicable

Item

1B Unresolved

Staff Comments

Not

applicable

Item

2. Properties

Facilities

The Company operates

three manufacturing facilities. The largest manufacturing

operations facility is a 44,000 square foot manufacturing plant

located on approximately 28 acres of land in Midland, Virginia, of

which the Company owns approximately 25 acres and 3 acres are

leased from Rodney I. Smith, the Company's Chairman of the Board,

at an annual rental rate of $24,000. The manufacturing

facility houses two concrete mixers and one concrete

blender. The plant also includes two environmentally

controlled casting areas, two batch plants, a form fabrication

shop, a welding and metal fabrication facility, a carpentry shop, a

quality control center and a covered steel reinforcing fabrication

area of approximately 8,000 square feet. The Company's Midland

facility also includes a large storage yard for inventory and

stored materials. The Company owns an additional 19 acres in

Midland, Virginia, approximately two miles from the operations

facility, of which 3 acres is developed as a storage yard for the

rental barrier division.

The

Company's second manufacturing facility is located in Reidsville,

North Carolina on 46 acres of owned land and includes a 15,000

square foot manufacturing plant and administrative offices with

additional space for future expansion. This new facility began

production in the fourth quarter 2019 and is expected to double

capacity, as compared to the old facility. The old North Carolina

facility, on ten acres of owned land,

including an 8,000 square foot manufacturing plant with

administrative offices, remained operational during the

construction of the new plant with future use not determined at

this time.

The Company's third

manufacturing facility is located in Hopkins (Columbia), South

Carolina. The facility is located on 39 acres of land and has

approximately 40,000 square feet of production space and

administrative offices. The South Carolina facility gives the

Company sufficient capacity to cover additional territory from the

Atlantic Coast region to the northern part of Florida.

The Company's present

facilities are adequate for its current needs.

10

Item

3. Legal Proceedings

The Company is not

presently involved in any litigation of a material

nature.

Item

4. Mine Safety

Disclosures

Not

applicable

11

PART II

Item 5.

Market for Registrant’s

Common Equity, Related Stockholder Matters and Issuer Purchases of

Equity Securities.

The Company's Common

Stock trades on the OTCQX Markets under the symbol

"SMID".

As of March 5,

2020, there were approximately 200 record holders of the Company's

Common Stock. Management believes there are at least 800 beneficial

owners of the Company's Common Stock.

Dividends

Although the Company

paid a dividend for eight consecutive years, the Company cannot

guarantee the continued payment of dividends due to the internal

need for funds in the development and expansion of its

business. The declaration of dividends in the future will be

at the election of the Board of Directors and will depend upon

earnings, capital requirements and financial position of the

Company, bank loan covenants, general economic conditions, and

other pertinent factors.

Item

6. Selected Financial

Data

Not

applicable.

Item

7. Management's Discussion and Analysis of

Financial Condition and Results of Operations

The following discussion

should be read in conjunction with the Consolidated Financial

Statements of the Company (including the Notes thereto) included

elsewhere in this report. Dollar amounts are in thousands, except

for per share amounts.

The Company generates

revenues primarily from the sale, leasing, licensing, shipping and

installation of precast concrete products for the construction,

utility and farming industries. The Company's operating

strategy has involved producing innovative and proprietary

products, including Slenderwall™, a patent pending,

lightweight, energy efficient concrete and steel exterior wall

panel for use in building construction; J-J Hooks® Barrier, a

patented positive-connected highway safety barrier; Sierra

Wall™, a patented sound barrier primarily for roadside use;

transportable concrete buildings; and SoftSound™, a highway

sound attenuation system. In addition, the Company produces

utility vaults; farm products such as cattleguards; and custom

order precast concrete products with various architectural

surfaces.

12

As a part of the

construction industry, the Company's sales and net income may vary

greatly from quarter to quarter over a given year. Because of the

cyclical nature of the construction industry, many factors not

under our control, such as weather and project delays, affect the

Company's production schedule, possibly causing a momentary

slowdown in sales and net income. As a result of these factors, the

Company is not always able to earn a profit for each period,

therefore, please read Management's Discussion and Analysis of

Financial Condition and Results of Operations and the accompanying

financial statements with these factors in mind.

On

January 30, 2020, the World Health Organization (“WHO”)

announced a global health emergency because of a new strain of

coronavirus originating in Wuhan, China (the “COVID-19

outbreak”) and the risks to the international community as

the virus spreads globally beyond its point of origin. In March

2020, the WHO classified the COVID-19 outbreak as a pandemic, based

on the rapid increase in exposure globally.

The

full impact of the COVID-19 outbreak continues to evolve as of the

date of this report. As such, it is uncertain as to the full

magnitude that the pandemic will have on the Company’s

financial condition, liquidity, and future results of operations.

Management is actively monitoring the global situation on its

financial condition, liquidity, operations, suppliers, industry,

and workforce. Given the daily evolution of the COVID-19 outbreak

and the global responses to curb its spread, the Company is not

able to estimate the effects of the COVID-19 outbreak on its

results of operations, financial condition, or liquidity for fiscal

year 2020.

The discussions below, including without limitation with respect to outlooks by product line and liquidity, are subject to the future effects of the COVID-19 outbreak. In this respect, should the outbreak cause serious economic harm in our areas of operation, our revenue expectations are unlikely to be fulfilled.

Overview

Overall, the

Company’s financial performance was higher in 2019 when

compared to 2018. The Company had net income for 2019 in the amount

of $1,959 compared to net income of $1,687 for 2018.

Sales

increased by $6,471 to $46,691 in 2019 from $40,220 in 2018. The

increase in sales is mainly attributed to the significant increase

in Shipping and Installation revenue, which in return unfavorably

impacted gross margins, excluding royalties, with a reduction to

18% in 2019 from 23% in 2018. The Company is currently recognizing

revenue and related costs associated with the 'Sale to Customer

with a Buy-Back Guarantee' as further described under 'Revenue

Recognition' in the 'Summary of Significant Accounting Policies'

section. The Company

completed construction of the new North Carolina plant and began

production at the facility during the fourth quarter of 2019. The

new facility has the ability to double production, as compared to

the previous North Carolina facility, with additional space to

expand in the future. Currently, management expects an increase in

production in North Carolina towards the end of 2020. Also during

2019, the Company entered into an agreement to purchase barrier

previously sold to a customer. This agreement increased the barrier

rental fleet to 250,000 linear feet of barrier, and also added 75

crash cushion attenuators. The expansion of the barrier rental

fleet allows the Company to bid larger projects in the future,

while giving the Company the ability to be a full-service highway

safety supplier. The current backlog of $30.9 million as of March

5, 2020 has grown 8% since the third quarter 2019. Even with the

increase in backlog, production has been lower in the first quarter

of 2020 than expected. Although the Company has experienced a

relatively weak first quarter, management expects 2020 overall will

be another strong financial year for the Company, although no

assurance can be given.

Results of

Operations

Year ended December 31, 2019

compared to the

year ended December 31,

2018

For the year ended

December 31, 2019, the Company had total revenue of $46,691

compared to total revenue of $40,220 for the year ended

December 31, 2018, an increase of $6,471, or 16.1%. Revenue

includes product sales, barrier rentals, royalty income, and

shipping and installation revenues. Product sales are further

divided into soundwall, architectural and SlenderWall™

panels, miscellaneous wall panels, highway barrier,

Easi-Set®/Easi-Span® buildings, utility products, and

miscellaneous precast products. The following table summarizes

the revenue by type and a comparison for the years ended

December 31, 2019 and 2018 (in thousands):

|

Revenue by Type (Disaggregated

Revenue)

|

2019

|

2018

|

Change

|

%

Change

|

|

Product Sales:

|

|

|

|

|

|

Soundwall

Sales

|

$7,736

|

$9,867

|

$(2,131)

|

(21.6)%

|

|

Architectural

Sales

|

1,104

|

876

|

228

|

26.0%

|

|

SlenderWall

Sales

|

5,063

|

5,572

|

(509)

|

(9.1)%

|

|

Miscellaneous Wall

Sales

|

1,685

|

1,760

|

(75)

|

(4.3)%

|

|

Barrier

Sales

|

8,582

|

7,264

|

1,318

|

18.1%

|

|

Easi-Set and Easi-Span

Building Sales

|

5,937

|

2,114

|

3,823

|

180.8%

|

|

Utility

Sales

|

1,608

|

1,232

|

376

|

30.5%

|

|

Miscellaneous

Sales

|

513

|

474

|

39

|

8.2%

|

|

Total Product

Sales

|

32,228

|

29,159

|

3,069

|

10.5%

|

|

Barrier

Rentals

|

2,488

|

1,729

|

759

|

43.9%

|

|

Royalty

Income

|

1,672

|

1,675

|

(3)

|

(0.2)%

|

|

Shipping and

Installation Revenue

|

10,303

|

7,657

|

2,646

|

34.6%

|

|

Total Service

Revenue

|

14,463

|

11,061

|

3,402

|

30.8%

|

|

Total

Revenue

|

$46,691

|

$40,220

|

$6,471

|

16.1%

|

13

Soundwall

Sales – Soundwall panel sales decreased by 21.6% in

2019 compared to 2018 due primarily to the smaller number of

projects in production during 2019 at the North Carolina and South

Carolina facilities as compared to 2018. The Company had slightly

higher soundwall sales out of the Midland, Virginia facility which

is expected to continue through 2020. Soundwall bid projects

continue to be competitive in all regions of the Mid-Atlantic. The

Company expects 2020 soundwall sales to remain flat compared to

2019, although no assurance can be given on future

sales.

Architectural

Sales – Architectural panel sales increased by 26.0%

in 2019 compared to 2018. The Company was awarded one larger

architectural wall panel project to produce during 2019, as well as

two additional architectural wall panel projects that coincided

with SlenderWall production (see the SlenderWall section below).

The Company has recently been awarded a few architectural wall

panel projects that will be in production during 2020. Management

believes that 2020 architectural sales will exceed the 2019 sales

volume, although no assurance can be given.

SlenderWall

Sales – SlenderWall panel sales decreased by 9.1% in

2019 when compared to 2018. The Company had a total of six

SlenderWall projects in production in 2019, with a large

SlenderWall project finishing production during the first quarter.

SlenderWall sales should stay strong in 2020 with the continued

sales efforts. Management believes 2020 SlenderWall production

should be similar to 2019, although no assurance can be

given.

Miscellaneous

Wall Sales – Miscellaneous wall sales can be highly

customized precast concrete products or retaining and lagging

panels that do not fit other product categories. Miscellaneous wall

sales slightly decreased by 4.3% in 2019 when compared to 2018.

Miscellaneous wall projects are difficult to predict from year to

year, however, based on the Company's current backlog of orders and

our bid outlook, management believes that production and sales of

miscellaneous wall products in 2020 will be greater than 2019

levels, although no assurance can be given.

Barrier

Sales – Barrier sales are dependent on the number of

highway projects active during the period and whether customers are

more prone to buy barrier than to rent. The Company received two large orders and

produced the barrier during the fourth quarter 2019 driving barrier

sales ahead of the 2018 level. Barrier production was higher

in 2018 as compared to 2019, but a large portion during 2018 was

not recognized as barrier sales due to the guaranteed buy-back

agreement with a customer; a portion of the 2018 deferred revenue

is recognized in the current year as "Barrier Rentals", with

additional revenue to be recognized in future years as "Barrier

Rentals". As the Company increases the barrier rental fleet, more

projects are expected to be rented instead of sold in the future.

See "Barrier Rentals" below for more detail. Management expects

barrier sales to be lower for 2020 as compared to annual barrier

sales for 2019, although no assurance can be

given.

Easi-Set®

and Easi-Span® Building Sales – The

Easi-Set® Buildings program includes Easi-Set®, plant

assembled and Easi-Span®, site assembled, and an extensive

line of pre-engineered restrooms. Building sales increased

significantly by 180.8% in 2019 as compared to 2018. The Company

produced a large governmental building order out of multiple plants

during the third quarter 2019, which significantly boosted sales

above the prior year. Building sales are expected to be lower in

2020 as compared to 2019, although no assurance can be

given.

Utility

Sales – Utility products are mainly comprised of

underground utility vaults used in infrastructure construction.

Utility product sales increased by 30.5% in 2019 compared to 2018.

The utility market is extremely competitive, with many competitors

who specialize in lower priced utility products. The Company is

much more competitive on larger quantity projects, in which it

targeted and won more jobs during 2019. As the Company continues to

be aggressive in utility sales, 2020 should be similar or greater

than 2019 sales, although no assurance can be given.

14

Miscellaneous

Product Sales – Miscellaneous products are products

that are produced or sold that do not meet the criteria defined for

other revenue categories. Examples would include precast

concrete slabs, waste blocks or small add-on items. For 2019,

miscellaneous product sales increased by 8.2% when compared to

2018. Management expects miscellaneous product sales to be similar

in 2020 as compared to 2019, although no assurance can be given.

These products are typically small in nature and the Company

focuses it's priorities on larger, more profitable

jobs.

Barrier

Rentals – Barrier rentals increased by 43.9% in 2019

when compared to 2018. The increase resulted primarily from the

recognition of revenue under a deferred guaranteed buy-back

agreement with a customer for barrier, which will continue until

the buy-back option is either exercised or expires when the

customer completes its usage of the barrier, which is expected to

be a four year period from the date of delivery. The Company's

standard highway barrier rentals remained strong in 2019 with an

increase of 4% over 2018. Management believes standard highway

barrier rentals will continue to be strong in 2020 with the

increase its barrier rental fleet at the end of 2019. The Company

continues to pursue its rental barrier expansion plans for its

local geographical sales areas and expects its core rental business

to increase, although no assurance can be given.

Royalty

Income – Royalties decreased by 0.2% in 2019 as

compared to 2018. The decrease was a result of lower barrier

royalties, mainly from one significant licensee who did not

generate royalties during 2019, with the license being terminated

in December 2019. In 2019 the Company added a new SlenderWall

salesman to help increase sales nationwide. Management believes

that overall royalties will increase during 2020 as the

construction industry continues to expand, especially in the

infrastructure section of the market, although no assurance can be

given.

Shipping

and Installation – Shipping revenue results from

shipping our products to the customers' final destination and is

recognized when the shipping services take place. Installation

activities include installation of our products at the

customers’ construction site. Installation revenue results

when attaching architectural wall panels to a building, installing

an Easi-Set® building at a customers' site, setting highway

barrier, or setting any of our other precast products at a site

specific to the requirements of the owner. Shipping and

installation revenues increased by 34.6% for 2019 when compared to

2018. The increase was mainly due to the increase of delivery and

installation of Easi-Set buildings and an increase in SlenderWall

installation as compared to 2018. Management believes that shipping

and installation revenues for 2020 will be similar or lower to

2019, although no assurance can be given.

Cost

of Goods Sold – Total cost of goods sold for the year

ended December 31, 2019 was $36,722, an increase of $6,992, or

23.5%, from $29,730 for the year ended December 31,

2018. Total cost of goods sold, as a percentage of total

revenue not including royalties, increased to 82% for the year

ended December 31, 2019 from 77% for the year ended

December 31, 2018. The increase in the cost of goods sold

as a percentage of total revenue was mainly due to the increase in

Shipping & Installation revenues which historically carry lower

margins as compared to product sales. Raw material costs increased

slightly in 2019 over 2018 with some inflationary pressures for the

Company, although steel prices dropped during 2019 as compared to

2018. Raw material prices are expected to remain relatively flat in

2020 as compared to 2019. The Company continues to seek new vendor

partnerships to help develop a price advantage for its raw

materials as well as a continuous supply of these materials and has

changed several vendors due to better supply sources and better

pricing.

General

and Administrative Expenses – For the year ended

December 31, 2019, the Company's general and administrative

expenses decreased by $788, or 13.9%, to $4,887 from $5,675 during

the same period in 2018. The decrease in general and

administrative expenses is mainly attributed to an administrative

staffing reduction, as compared to 2018. General and administrative

expenses are expected to be similar in 2020 as compared to 2019,

although no assurance can be given.

Selling

Expenses – Selling expenses for the year ended

December 31, 2019 decreased by $63, or 2.4%, to $2,536 from

$2,599 for the year ended December 31, 2018. The decrease

was due to a slight decrease in salary and commission expense with

some of the largest sales contracts in Company history awarded in

2018. The Company recently hired a national SlenderWall salesman,

and future expenses are expected to increase with the expected

growth of the product line.

15

Operating

Income – The Company had operating income for the year

ended December 31, 2019 of $2,546 compared to operating income

of $2,216 for the year ended December 31, 2018, an increase of

$330, or 14.9%. The increase in operating income was primarily the

result of the increased sales volume and reduction in general and

administrative expenses in 2019 as compared to 2018.

Interest

Expense – Interest expense was $179 for the year ended

December 31, 2019 compared to $176 for the year ended

December 31, 2018. The increase of $3, or 1.7%, was due

primarily to the financing of the new North Carolina

facility.

Income Tax

Expense – The Company had

income tax expense of $549 for the year ended December 31,

2019 compared to income tax expense of $572 for the year ended

December 31, 2018. The Company had an effective rate of 21.9%

for the year ended December 31, 2019 compared to an effective

rate of 25.3% for the same period in

2018.

Net Income

– The Company had net income of $1,959 for the year ended

December 31, 2019, compared to net income of $1,687 for the

same period in 2018. The basic and diluted income per share

was $0.38 for 2019, compared to basic and diluted income per share

of $0.33 for the year ended December 31, 2018. There were

5,142 basic and 5,147 diluted weighted average shares outstanding

in 2019 and 5,080 basic and 5,096 diluted weighted average shares

outstanding in the 2018.

Liquidity and Capital

Resources

The Company financed its

capital expenditures requirements for 2019 with cash flows from

operations, cash balances on hand and notes payable to a bank. The

Company had $5,011 of debt obligations at December 31, 2019,

of which $925 is scheduled to mature within twelve months. During

the twelve months ended December 31, 2019, the Company made

repayments of outstanding debt in the amount $769 and received

$2,277 in proceeds of borrowings for the financing of the North

Carolina property and a vehicle. The Company had draws on the line

of credit of $500 and had repayments of $1,500 on the line of

credit during the twelve months ended December 31,

2019.

The Company has a note

payable to Summit Community Bank (the “Bank”) with a

balance of $519 as of December 31, 2019. The note has a

remaining term of approximately two years and a fixed interest rate

of 3.99% annually with monthly payments of $26 and is secured by

principally all of the assets of the Company. Under the terms

of the note, the Bank will permit chattel mortgages on purchased

equipment not to exceed $250 for any one individual loan so long as

the Company is not in default. The Company maintains a limit of

$3,500 for annual capital expenditures, excluding acquisitions and

plant expansions. At December 31, 2019, the Company was

in compliance with all covenants pursuant to the loan

agreement.

The Company has a mortgage note payable to the Bank for the

purchase of the Columbia, South Carolina facility. Such loan is

evidenced by a promissory note, dated July 19, 2016. The note

provides for a 15 year term, a fixed annual interest rate of 5.29%,

monthly fixed payments of $11 and a security interest in favor of

the Bank in respect to the land, building and fixtures purchased

with the proceeds of the loan. The balance of the loan at December

31, 2019 was $1,103.

On October 11, 2019, the

Company completed the financing for the construction of it's new

North Carolina facility with a note payable to the Bank in the

amount of $2,228. The note carries a ten year term at a fixed

interest rate of 3.64% annually per the Promissory Note Rate

Conversion Agreement, with monthly payments of $22, and is secured

by all of the assets of Smith-Carolina and a guarantee by the

Company. The balance of the note payable at December 31, 2019

was $2,197.

The Company additionally has 13 smaller installment loans with

annual interest rates between 3.49% and 5.75%, maturing between

2020 and 2024, with varying balances totaling

$1,192.

In addition to the notes

payable discussed above, the Company also has a $4,000 line of

credit with the Bank with no balance at December 31, 2019. The

line of credit is evidenced by a commercial revolving promissory

note which carries a variable interest rate of prime and matures on

October 1, 2020. The loan is collateralized by a first lien

position on the Company's accounts receivable and inventory and a

second lien position on all other business assets. Key provisions

of the line of credit require the Company, (i) to obtain bank

approval for capital expenditures in excess of $3,500 during the

term of the loan; and (ii) to obtain bank approval prior to its

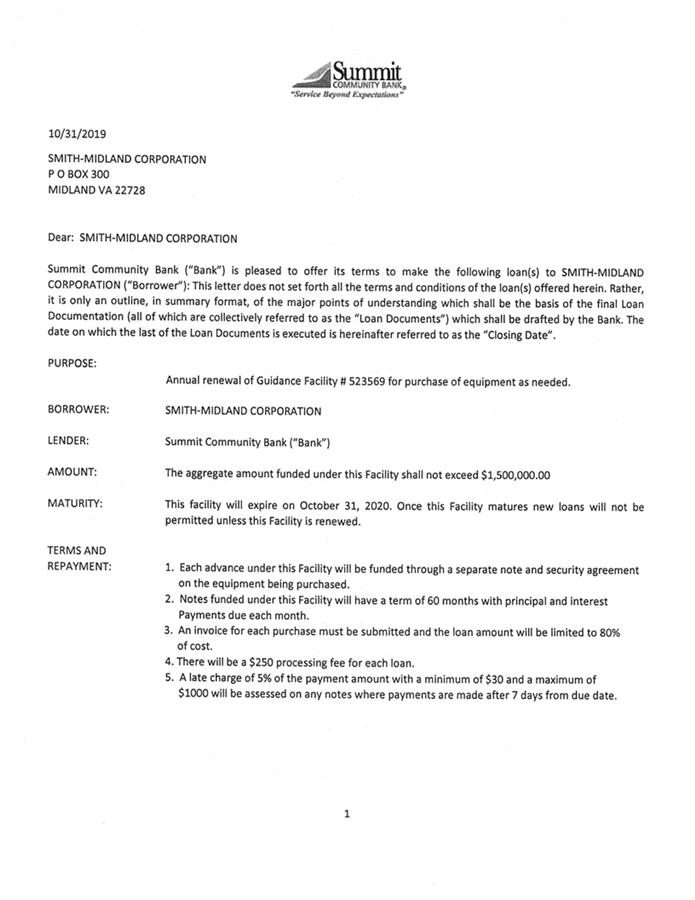

funding any acquisition. On October 31, 2019 the Company received a

Commitment Letter from the Bank to provide a guidance line of

credit specifically to purchase business equipment in an amount up

to $1,500. The commitment provides for the purchase of equipment

with minimum advances of $50 for which a note payable will be

executed with a term not to exceed five years with an interest rate

at the Wall Street Journal prime rate plus .5% with a floor of

4.49% per annum. The loan is collateralized by a first lien

position on all equipment purchased under the line. The commitment

for the guidance line of credit matures on October 31,

2020. As of December

31, 2019, the Company had not purchased any equipment pursuant to

the $1,500 commitment.

16

At December 31,

2019, the Company had cash totaling $1,364 and $1,176 of investment

securities available for sale compared to cash totaling $1,946 and

$1,107 of investment securities available for sale at

December 31, 2018. Investment securities at December 31, 2019

consist of shares of USVAX (a Virginia Bond Fund). During 2019, the

Company’s operating activities provided $3,935 of cash due

mainly to the decrease in inventories. In 2019, investing

activities used $4,744 in cash primarily for the North Carolina

expansion and for the purchase of rental barrier and capital

equipment. Financing activities provided $227 in cash in 2019,

resulting primarily from new loan for the North Carolina expansion

and the financing of capital expenditures.

Capital spending,

including financed additions, decreased from $5,234 in 2018 to

$4,513 in 2019. Capital expenditures in 2019 included spending for

the North Carolina expansion, rental barrier, and manufacturing

equipment. In 2020, the Company intends to continue to make

capital improvements which include additional yard expansions in

Virginia, along with the purchase of manufacturing equipment. While

the Company anticipates capital spending for 2020 to be $2,000,

excluding acquisitions and plant expansions (which none are

anticipated at this time), such plans may change if the Company is

adversely effected by the coronavirus outbreak.

The

Company's three mortgage notes payable are financed at fixed rates

of interest. This leaves the Company almost impervious to

fluctuating interest rates. Increases in such rates will only

slightly affect the interest paid by the Company on an annual

basis. Approximately 95% of the Company's debt obligations are

financed at a fixed interest rate so that each 1% increase in

the interest rates of the Company’s outstanding debt will

reduce income by approximately $2

annually.

The Company’s cash

flow from operations is affected by production schedules set by

contractors, which generally provide for payment 45 to 75 days

after the products are produced and with some architectural

contracts, retainage may be held until the entire project is

completed. This payment schedule could result in liquidity

problems for the Company because it must bear the cost of

production for its products before it receives payment. The

Company's days sales outstanding (DSO) in 2019 was 89 days compared

to 86 days in 2018. The DSO increased due to the increase in

retainage outstanding on large SlenderWall projects. Although no

assurance can be given, particularly in light of the coronavirus

outbreak, the Company believes that anticipated cash flow from

operations with adequate project management on jobs and the

availability under lines of credit will be sufficient to finance

the Company’s operations and necessary capital expenditures

for at least the next 12 months.

The Company’s

inventory at December 31, 2019 was $2,242 and at

December 31, 2018 was $3,560, a decrease of $1,318. The

annual inventory turns for 2019 and 2018 were 12.1 and 11.9, respectively. The

inventory turns for 2019 have increased due to the Company having

limited inventory, and all major contracts were recognized in

revenue, or as deferred revenue, as produced. Finished goods

inventory decreased for 2019 as compared to 2018 mainly due to

limited standard products produced and held at the end of

2019.

Critical Accounting

Policies

The Company’s

significant accounting policies are more fully described in its

Summary of Accounting Policies to the Company’s consolidated

financial statements. The preparation of financial statements

in conformity with accounting principles generally accepted within

the United States of America requires management to make estimates

and assumptions in certain circumstances that affect amounts

reported in the accompanying financial statements and related

notes. In preparing these consolidated financial statements,

management has made its best estimates and judgments of certain

amounts included in the consolidated financial statements, giving

due consideration to materiality. The Company does not believe

there is a great likelihood that materially different amounts would

be reported related to the accounting policies described below,

however, application of these accounting policies involves the

exercise of judgment and the use of assumptions as to future

uncertainties and as a result, actual results could differ from

these estimates.

The Company evaluates

the adequacy of its allowance for doubtful accounts at the end of

each quarter. In performing this evaluation, the Company

analyzes the payment history of its significant past due accounts,

subsequent cash collections on these accounts and comparative

accounts receivable aging statistics. Based on this

information, along with other related factors, the Company develops

what it considers to be a reasonable estimate of the uncollectible

amounts included in accounts receivable. This estimate

involves significant judgment by the management of the

Company. Actual uncollectible amounts may differ from the

Company’s estimate.

The Company recognizes

revenue on the sale of its standard precast concrete products at

shipment date, including revenue derived from any projects to be

completed under short-term contracts. Installation services

for precast concrete products, leasing and royalties are recognized

as revenue over time. Certain sales of Soundwall, Slenderwall, and

other architectural concrete products are recognized over time

because as the Company's performance creates or enhances customer

controlled assets or creates or enhances an asset with no

alternative use, and the Company has an enforceable right to

receive compensation. Over time product contracts are estimated

based on the number of units produced (output method) during the

period multiplied by the unit rate stated in the contract.

As the

output method is driven by units produced, the Company recognizes

revenues based on the value transferred to the customer relative to

the remaining value to be transferred. The Company also matches the

costs associated with the units produced. If a contract is

projected to result in a loss, the entire contract loss is

recognized in the period when the loss was first determined and the

amount of the loss updated in subsequent reporting periods. Revenue

recognition also includes an amount related to a contract asset or

contract liability. If the recognized revenue is greater than the

amount billed to the customer, a contract asset is recorded in

accounts receivable - unbilled. Conversely, if the amount billed to

the customer is greater than the recognized revenue, a contract

liability is recorded in customer deposits on uncompleted

contracts. Changes in the job performance, job conditions and final

contract settlements are factors that influence management’s

assessment of total contract value and therefore, profit and

revenue recognition.

17

Seasonality

The Company services the

construction industry primarily in areas of the United States where

construction activity may be inhibited by adverse weather during

the winter. As a result, the Company may experience reduced

revenues from December through February and realize the substantial

part of its revenues during the other months of the year. The

Company may experience lower profits, or losses, during the winter

months, and as such, must have sufficient working capital to fund

its operations at a reduced level until the spring construction

season. The failure to generate or obtain sufficient working

capital during the winter may have a material adverse effect on the

Company.

Inflation

Management believes that

the Company's operations were not significantly affected by

inflation in 2019 and 2018, particularly in the purchases of

certain raw materials such as cement and steel. The Company

believes that raw material pricing will likely remain flat or

slightly increase in 2020, although no assurance can be given

regarding future pricing.

Backlog

As of March 5, 2020

the Company's sales backlog was approximately $30.9 million as compared to

approximately $31.1 million at approximately the same time in 2019.

It is estimated that most of the projects in the sales backlog will

be produced within 12 months, but a few will be produced through

the year 2021. There has been a slight decrease in the backlog for

2020 when compared to approximately the same time in 2019, but the

Company expects it to increase with continued bidding on large

infrastructure and SlenderWall/architectural projects, although no

assurance can be given.

The risk exists that

recessionary economic conditions may adversely affect the Company

more than it has experienced to date. To mitigate these