Attached files

| file | filename |

|---|---|

| EX-32.01 - EXHIBIT 32.01 - ACM Research, Inc. | ex32_01.htm |

| EX-31.02 - EXHIBIT 31.02 - ACM Research, Inc. | ex31_02.htm |

| EX-31.01 - EXHIBIT 31.01 - ACM Research, Inc. | ex31_01.htm |

| EX-23.01 - EXHIBIT 23.01 - ACM Research, Inc. | ex23_01.htm |

|

☑

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

Delaware

(State or Other Jurisdiction of Incorporation or Organization)

|

94-3290283

(I.R.S. Employer Identification No.)

|

|

|

42307 Osgood Road, Suite I, Fremont, California

|

94539

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

|

Title of Each Class

|

Trading Symbol

|

Name of Each Exchange on which Registered

|

||

|

Class A Common Stock, $0.0001 par value

|

ACMR

|

Nasdaq Global Market

|

|

Large accelerated filer ☐

|

Accelerated filer

|

☑ | |

|

Non-accelerated filer ☐

|

Smaller reporting company

|

☑ | |

|

Emerging growth company

|

☑ |

|

Class

|

Number of Shares Outstanding

|

|

|

Class A Common Stock, $0.0001 par value

|

16,273,528 shares outstanding as of March 17, 2020

|

|

|

Class B Common Stock, $0.0001 par value

|

1,862,608 shares outstanding as of March 17, 2020

|

| PART I | ||

|

Item 1

|

4 |

|

|

Item 1A

|

15 |

|

|

Item 2

|

42 |

|

|

Item 3

|

42 |

|

|

PART II

|

||

|

Item 5

|

43 | |

|

Item 7

|

44 |

|

|

Item 8

|

67 |

|

|

Item 9A

|

103 |

|

|

PART III

|

||

|

Item 10

|

104 |

|

|

Item 11

|

104 |

|

|

Item 12

|

104 |

|

|

Item 13

|

104 |

|

|

Item 14

|

104 |

|

|

PART IV

|

||

|

Item 15

|

105 |

|

| 107 |

||

|

●

|

Space Alternated Phase Shift, or SAPS, technology for flat and patterned wafer surfaces. Introduced in

2009, SAPS technology employs alternating phases of megasonic waves to deliver megasonic energy in a highly uniform manner on a microscopic level. We have shown SAPS technology to be more effective than conventional megasonic and

jet spray technologies in removing random defects across an entire wafer as node sizes shrink from 300 nanometers, or nm, to 20nm and lower.

|

| ● |

Timely Energized Bubble Oscillation, or TEBO, technology for patterned wafer surfaces at advanced process nodes. Introduced in March 2016, TEBO technology has been developed to provide effective, damage-free cleaning for 2D and 3D patterned wafers with fine feature sizes. We have demonstrated the damage-free cleaning capabilities of TEBO

technology on patterned wafers for feature nodes as small as 1xnm (16nm to 19nm), and we have shown TEBO technology can be applied in manufacturing processes for patterned chips with 3D architectures having aspect ratios as high as

60‑to‑1.

|

| ● |

Tahoe technology for cost and environmental savings. Introduced in 2018, Tahoe technology delivers high cleaning performance using

significantly less sulfuric acid and hydrogen peroxide than is typically consumed by conventional high-temperature single-wafer cleaning tools.

|

| ● |

Electro-Chemical Plating, or ECP, technology for advanced metal plating. Our Ultra ECP AP, or Advanced Packaging, technology was developed for back-end assembly

processes to deliver a more uniform metal layer at the notch area of wafers prior to packaging. Our Ultra ECP MAP, or Multi-Anode Partial Plating, technology was developed for front-end wafer fabrication processes to deliver advanced

electrochemical copper plating for copper interconnect applications. ECP MAP offers improved gap-filling performance for ultra-thin seed layer applications, which is critical for advanced nodes at 14nm and beyond.

|

| ● |

Post CMP: Chemical mechanical planarization, or CMP, uses an abrasive chemical slurry following other

fabrication processes, such as deposition and etching, in order to achieve a smooth wafer surface in preparation for subsequent processing steps. SAPS technology can be applied following each CMP process to remove residual random

defects deposited or formed during CMP.

|

| ● |

Post Hard Mask Deposition: As part of the photolithographical patterning process, a mask is applied with

each deposition of a material layer to prevent etching of material intended to be retained. Hard masks have been developed to etch high aspect-ratio features of advanced chips that traditional masks cannot tolerate. SAPS technology

can be applied following each deposition step involving hard masks that use nitride, oxide or carbon based materials to achieve higher etch selectivity and resolution.

|

| ● |

Post Contact/Via Etch: Wet etching processes are commonly used to create patterns of high-density contacts

and vias. SAPS technology can be applied after each such etching process to remove random defects that could otherwise lead to electrical shorts.

|

| ● |

Pre Barrier Metal Deposition: Copper wiring requires metal diffusion barriers at the top of via holes to

prevent electrical leakage. SAPS technology can be applied prior to deposition of barrier metal to remove residual oxidized copper, which otherwise would adhere poorly to the barrier and impair performance.

|

|

|

|

SAPS II (released in 2011). Highlights of our SAPS II equipment include:

|

|

|

|

|

|

● compact design, with footprint of 2.65m x 4.10m x 2.85m (WxDxH), requiring limited clean room floor space;

● up to 8 chambers, providing throughput of up to 225 wafers per hour;

● double-sided cleaning capability, with up to 5 cleaning chemicals for process flexibility;

● 2-chemical recycling capability for reduced chemical consumption;

● image wafer detection method for lowering wafer breakage rates; and

● chemical delivery module for delivery of dilute hydrofluoric acid, RCA SC-1 solution, functional de-ionized water and carbon dioxide to each of the

chambers. SAPS V (released in 2014). SAPS V includes SAPS II features with the following upgrades:

● compact design, with footprint of 2.55m x 5.1m x 2.85m (WxDxH);

● up to 12 chambers, providing throughput of up to 375 wafers per hour;

● chemical supply system integrated into mainframe;

● inline mixing method replaces tank auto-changing, reducing process time; and

● improved drying technology using hot isopropyl alcohol and de-ionized water.

|

| ● |

Memory Chips: We estimate that TEBO technology can be applied in as many as 50 steps in the fabrication of

a DRAM chip, consisting of up to 10 steps in cleaning ISO structures, 20 steps in cleaning buried gates, and 20 steps in cleaning high aspect-ratio storage nodes and stacked films.

|

| ● |

Logic Chips: In the fabrication process for a logic chip with a FinFET structure, we estimate that TEBO

technology can be used in 15 or more cleaning steps.

|

|

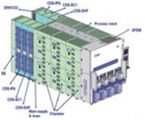

● an equipment front-end module, or EFEM, which moves wafers from chamber to chamber;

● one or more chamber modules, each equipped with a TEBO megasonic generator system;

● an electrical module to provide power for the tool; and

● a chemical delivery module.

|

|

Ultra C TEBO II (released in 2016). Highlights of our Ultra C TEBO II equipment include:

|

|

|

● compact design, with footprint of 2.25m x 2.25m x 2.85m (WxDxH);

● up to 8 chambers with an upgraded transport system and optimized robotic scheduler, providing throughput of up to 300 wafers per hour;

● EFEM module consisting of 4 load ports, transfer robot and 1 process robot; and

● focus on dilute chemicals contributes to environmental sustainability and lower cost of ownership.

|

|

Ultra C TEBO V (released in 2016). Highlights of our Ultra C TEBO V

equipment include:

|

|

|

● footprint of 2.45m x 5.30m x 2.85m (WxDxH);

● up to 12 chamber modules, providing throughput of up to 300 wafers per hour;

● EFEM module consisting of 4 load ports, 1 transfer robot and 1 process robot; and

● chemical delivery module for delivery of isopropyl alcohol, dilute hydrofluoric acid, RCA SC-1 solution, functional de-ionized water and carbon dioxide

to each of the chambers.

|

|

For example, our Ultra C Coater is used in applying photoresist, a light-sensitive material used in photolithography to transfer a pattern from a mask onto a wafer. Coaters typically

provide input and output elevators, shuttle systems and other devices to handle and transport wafers during the coating process. Unlike most coaters, the Ultra C Coater is fully automated. Based on requests from customers, we developed

and incorporated the special function of chamber auto-clean module into the Ultra C Coater, which further differentiates it from other products in the market. The Ultra C Coater is designed to deliver improved throughput and more

efficient tool utilization while eliminating particle generation.

|

We generate most of our revenue from a limited number of customers as the result of our strategy of initially placing single-wafer wet cleaning equipment with a small number of leading chip manufacturers that are driving technology trends and key capability implementation. In 2019, 73.8% of our revenue was derived from three customers: Yangtze Memory Technologies Co., Ltd., a leading PRC memory chip company, together with one of its subsidiaries, accounted for 27.5% of our revenue; Shanghai Huali Microelectronics Corporation and the operations of The Huahong Group, a leading PRC foundry, accounted for 26.5% of our revenue; and SK Hynix Inc., a leading Korean memory chip company, accounted for 19.8% of our revenue. In 2018, 87.6% of our revenue was derived from three customers: Yangtze Memory Technologies Co., Ltd. (together with a subsidiary) accounted for 39.6% of our revenue; Shanghai Huali Microelectronics Corporation accounted for 24.2% of our revenue; and SK Hynix Inc. accounted for 23.8% of our revenue.

| ● |

new cleaning steps for Ultra C SAPS cleaners for application in logic chips and for DRAM, 3D NAND and 3D cross point memory technologies;

|

| ● |

new cleaning steps for Ultra C TEBO cleaners for FinFET in logic chips, gates in DRAM, and deep vias in both 3D NAND and 3D cross point memory technologies;

|

| ● |

new hardware, including new system platforms, new and additional chamber structures and new chemical blending systems; and

|

| ● |

new software to integrate new functionalities to improve tool performance.

|

| ● |

better established credibility and market reputations, longer operating histories, and broader product offerings;

|

| ● |

significantly greater financial, technical, marketing and other resources, which may allow them to pursue design, development, manufacturing, sales, marketing, distribution and service support of their

products;

|

| ● |

more extensive customer and partner relationships, which may position them to identify and respond more successfully to market developments and changes in customer demands; and

|

| ● |

multiple product offerings, which may enable them to offer bundled discounts for customers purchasing multiple products or other incentives that we cannot match or offer.

|

| ● |

performance of products, including particle removal efficiency, rate of damage to wafer structures, high temperature chemistry, throughput, tool uptime and reliability, safety, chemical waste treatment,

and environmental impact;

|

| ● |

service support capability and spare parts delivery time; innovation and development of functionality and features that are must-haves for advanced fabrication nodes;

|

| ● |

ability to anticipate customer requirements, especially for advanced process nodes of less than 45nm; ability to identify new process applications;

|

| ● |

brand recognition and reputation; and

|

| ● |

skill and capability of personnel, including design engineers, manufacturing engineers and technicians, application engineers, and service engineers.

|

| ● |

achieve wider market acceptance of Ultra C equipment based on SAPS, TEBO and Tahoe technology;

|

| ● |

increase our customer base in the PRC and globally, including the establishment of relationships with companies in the United States;

|

| ● |

continue to expand our supplier relationships with third parties; and

|

| ● |

establish and maintain our reputation for providing efficient on-time delivery of high quality products.

|

| ● |

research and development, including continued investments in our research and development team;

|

| ● |

sales and marketing, including a significant expansion of our sales organization, both domestically and internationally, building our brand, and providing our single-wafer wet cleaning equipment and other

capital equipment, or tools, for evaluation by customers;

|

| ● |

the cost of goods being manufactured and sold for our installed base; and

|

| ● |

expansion of field service.

|

| ● |

our sales growth;

|

| ● |

the costs of applying our existing technologies to new or enhanced products;

|

| ● |

the costs of developing new technologies and introducing new products;

|

| ● |

the costs associated with protecting our intellectual property;

|

| ● |

the costs associated with our expansion, including capital expenditures, increasing our sales and marketing and service and support efforts, and expanding our geographic operations;

|

| ● |

our ability to continue to obtain governmental subsidies for developmental projects in the future;

|

| ● |

future debt repayment obligations; and

|

| ● |

the number and timing of any future acquisitions.

|

| ● |

the cyclicality of the semiconductor industry and the related impact on the purchase of equipment used in the manufacture of integrated circuits, or chips;

|

| ● |

the timing of purchases of our tools by chip fabricators, which order types of tools based on multi-year capital plans under which the number and dollar amount of tool purchases can vary significantly

from year to year;

|

| ● |

the relatively high average selling price of our tools and our dependence on a limited number of customers for a substantial portion of our revenue in any period, whereby the timing and volume of purchase

orders or cancellations from our customers could significantly reduce our revenue for that period;

|

| ● |

the significant expenditures required to customize our products often exceed the deposits received from our customers;

|

| ● |

the lead time required to manufacture our tools;

|

| ● |

the timing of recognizing revenue due to the timing of shipment and acceptance of our tools;

|

| ● |

our ability to sell additional tools to existing customers;

|

| ● |

the changes in customer specifications or requirements;

|

| ● |

the length of our product sales cycle;

|

| ● |

changes in our product mix, including the mix of systems, upgrades, spare parts and service;

|

| ● |

the timing of our product releases or upgrades or announcements of product releases or upgrades by us or our competitors, including changes in customer orders in anticipation of new products or product

enhancements;

|

| ● |

our ability to enhance our tools with new and better functionality that meet customer requirements and changing industry trends;

|

| ● |

constraints on our suppliers’ capacity;

|

| ● |

the timing of investments in research and development related to releasing new applications of our technologies and new products;

|

| ● |

delays in the development and manufacture of our new products and upgraded versions of our products and the market acceptance of these products when introduced;

|

| ● |

our ability to control costs, including operating expenses and the costs of the components and subassemblies used in our products;

|

| ● |

the costs related to the acquisition and integration of product lines, technologies or businesses; and

|

| ● |

the costs associated with protecting our intellectual property, including defending our intellectual property against third-party claims or litigation.

|

| ● |

our ability to demonstrate the differentiated, innovative nature of our SAPS, TEBO and Tahoe technologies and the advantages of our tools over those of our competitors;

|

| ● |

compatibility of our tools with existing or potential customers’ manufacturing processes and products;

|

| ● |

the level of customer service available to support our products; and

|

| ● |

the experiences our customers have with our products.

|

| ● |

accurate anticipation of market requirements, changes in technology and evolving standards;

|

| ● |

the availability of qualified product designers and technologies needed to solve difficult design challenges in a cost-effective, reliable manner;

|

| ● |

our ability to design products that meet chip manufacturers’ cost, size, acceptance and specification criteria, and performance requirements;

|

| ● |

the ability and availability of suppliers and third-party manufacturers to manufacture and deliver the critical components and subassemblies of our tools in a timely manner;

|

| ● |

market acceptance of our customers’ products, and the lifecycle of those products; and

|

| ● |

our ability to deliver products in a timely manner within our customers’ product planning and deployment cycle.

|

| ● |

greater financial, technical, sales and marketing, manufacturing, distribution and other resources;

|

| ● |

established credibility and market reputations;

|

| ● |

longer operating histories;

|

| ● |

broader product offerings;

|

| ● |

more extensive service offerings, including the ability to have large inventories of spare parts available near, or even at, customer locations;

|

| ● |

local sales forces; and

|

| ● |

more extensive geographic coverage.

|

| ● |

efforts by our sales force;

|

| ● |

the complexity of our customers’ manufacturing processes and the compatibility of our tools with those processes;

|

| ● |

our customers’ internal technical capabilities and sophistication; and

|

| ● |

our customers’ capital spending plans and processes, including budgetary constraints, internal approvals, extended negotiations or administrative delays.

|

| ● |

our customers may delay or reject acceptance of our tools that contain defects or fail to meet their specifications;

|

| ● |

we may suffer customer dissatisfaction, negative publicity and reputational damage, resulting in reduced orders or otherwise damaging our ability to retain existing customers and attract new customers;

|

| ● |

we may incur substantial costs as a result of warranty claims or service obligations or in order to enhance the reliability of our tools;

|

| ● |

the attention of our technical and management resources may be diverted;

|

| ● |

we may be required to replace defective systems or invest significant capital to resolve these problems; and

|

| ● |

we may be required to write off inventory and other assets related to our tools.

|

| ● |

potential price increases;

|

| ● |

capacity shortages or other inability to meet any increase in demand for our products;

|

| ● |

reduced control over manufacturing process for components and subassemblies and delivery schedules;

|

| ● |

limited ability of some suppliers to manufacture and sell subassemblies or parts in the volumes we require and at acceptable quality levels and prices, due to the suppliers’ relatively small operations

and limited manufacturing resources;

|

| ● |

increased exposure to potential misappropriation of our intellectual property; and

|

| ● |

limited warranties on subassemblies and components supplied to us.

|

| ● |

hire, train, integrate and manage additional qualified engineers for research and development activities, sales and marketing personnel, service and support personnel and financial and information

technology personnel;

|

| ● |

manage multiple relationships with our customers, suppliers and other third parties; and

|

| ● |

continue to enhance our information technology infrastructure, systems and controls.

|

| ● |

the acquired product lines, technologies or businesses may not improve our financial and strategic position as planned;

|

| ● |

we may determine we have overpaid for the product lines, technologies or businesses, or that the economic conditions underlying our acquisition have changed;

|

| ● |

we may have difficulty integrating the operations and personnel of the acquired company;

|

| ● |

we may have difficulty retaining the employees with the technical skills needed to enhance and provide services with respect to the acquired product lines or technologies;

|

| ● |

the acquisition may be viewed negatively by customers, employees, suppliers, financial markets or investors;

|

| ● |

we may have difficulty incorporating the acquired product lines or technologies with our existing technologies;

|

| ● |

we may encounter a competitive response, including price competition or intellectual property litigation;

|

| ● |

we may become a party to product liability or intellectual property infringement claims as a result of our sale of the acquired company’s products;

|

| ● |

we may incur one-time write-offs, such as acquired in-process research and development costs, and restructuring charges;

|

| ● |

we may acquire goodwill and other intangible assets that are subject to impairment tests, which could result in future impairment charges;

|

| ● |

our ongoing business and management’s attention may be disrupted or diverted by transition or integration issues and the complexity of managing geographically or culturally diverse enterprises; and

|

| ● |

our due diligence process may fail to identify significant existing issues with the target business.

|

| ● |

a decline in demand for our products;

|

| ● |

an increase in reserves on accounts receivable due to our customers’ inability to pay us;

|

| ● |

an increase in reserves on inventory balances due to excess or obsolete inventory as a result of our inability to sell such inventory;

|

| ● |

valuation allowances on deferred tax assets;

|

| ● |

restructuring charges;

|

| ● |

asset impairments including the potential impairment of goodwill and other intangible assets;

|

| ● |

a decline in the value of our investments;

|

| ● |

exposure to claims from our suppliers for payment on inventory that is ordered in anticipation of customer purchases that do not come to fruition;

|

| ● |

a decline in the value of certain facilities we lease to less than our residual value guarantee with the lessor; and

|

| ● |

challenges maintaining reliable and uninterrupted sources of supply.

|

| ● |

imposition of, or adverse changes in, foreign laws or regulatory requirements, such as work stoppages and travel restrictions imposed in connection with the COVID-19 pandemic;

|

| ● |

the need to comply with the import laws and regulations of various foreign jurisdictions, including a range of U.S. import laws;

|

| ● |

potentially adverse tax consequences, including withholding tax rules that may limit the repatriation of our earnings, and higher effective income tax rates in foreign countries where we conduct business;

|

| ● |

competition from local suppliers with which potential customers may prefer to do business;

|

| ● |

seasonal reduction in business activity, such as during the Lunar New Year in parts of Asia and in other periods in various individual countries;

|

| ● |

increased exposure to foreign currency exchange rates;

|

| ● |

reduced protection for intellectual property;

|

| ● |

longer sales cycles and reliance on indirect sales in certain regions;

|

| ● |

increased length of time for shipping and acceptance of our products;

|

| ● |

greater difficulty in responding to customer requests for maintenance and spare parts on a timely basis;

|

| ● |

greater difficulty in enforcing contracts and accounts receivable collection and longer collection periods;

|

| ● |

difficulties in staffing and managing foreign operations and the increased travel, infrastructure and legal and compliance costs associated with multiple international locations;

|

| ● |

heightened risk of unfair or corrupt business practices in certain geographies and of improper or fraudulent sales arrangements that may impact financial results and result in restatements of, or

irregularities in, our consolidated financial statements; and

|

| ● |

general economic conditions, geopolitical events or natural disasters in countries where we conduct our operations or where our customers are located, including political unrest, war, acts of terrorism or

responses to such events.

|

| ● |

The U.S. Patent and Trademark Office and various foreign governmental patent agencies require compliance with a number of procedural, documentary, fee payment and other provisions during the patent

process. There are situations in which noncompliance can result in abandonment or lapse of a patent or patent application, resulting in partial or complete loss of patent rights in the relevant jurisdiction. In such an event,

competitors might be able to enter the market earlier than would otherwise have been the case.

|

| ● |

Patent applications may not result in any patents being issued.

|

| ● |

Patents that may be issued may be challenged, invalidated, modified, revoked, circumvented, found to be unenforceable or otherwise may not provide any competitive advantage.

|

| ● |

Our competitors may seek or may have already obtained patents that will limit, interfere with, or eliminate our ability to make, use and sell our potential product candidates.

|

| ● |

The PRC and other countries other than the United States may have patent laws less favorable to patentees than those upheld by U.S. courts, allowing foreign competitors a better opportunity to create,

develop and market competing product candidates.

|

| ● |

be time consuming and expensive to defend, whether or not meritorious;

|

| ● |

force us to stop selling products or using technology that allegedly infringes the third party’s intellectual property rights;

|

| ● |

delay shipments of our products;

|

| ● |

require us to pay damages or settlement fees to the party claiming infringement;

|

| ● |

require us to attempt to obtain a license to the relevant intellectual property, which may not be available on reasonable terms or at all;

|

| ● |

force us to attempt to redesign products that contain the allegedly infringing technology, which could be expensive or which we may be unable to do;

|

| ● |

require us to indemnify our customers, suppliers or other third parties for any loss caused by their use of our technology that allegedly infringes the third party’s intellectual property rights; or

|

| ● |

divert the attention of our technical and managerial resources.

|

Risks Related to the COVID‑19 Outbreak

The outbreak of COVID‑19, the coronavirus, continues to grow both in the United States and globally, and related government and private sector responsive actions are adversely affecting our business operations. COVID‑19 originated in Wuhan, China, in December 2019 and has subsequently spread rapidly across the PRC and globally. A series of emergency quarantine measures taken by the PRC government disrupted domestic business activities in the PRC during the weeks after the initial outbreak of COVID‑19. Since that time, an increasing number of countries, including the United States, have imposed restrictions on travel to and from the PRC and elsewhere, as well as general movement restrictions, business closures and other measures imposed to slow the spread of COVID‑19. Despite having largely contained COVID-19, the PRC and other Asian countries are now facing a potential second COVID-19 wave, attributable to individuals entering those countries.

We have set forth below key risks from the COVID‑19 outbreak that we have identified to date. The situation continues to develop rapidly, however, and it is impossible to predict the effect and ultimate impact of the COVID‑19 outbreak on our business operations and results. While the quarantine, social distancing and other regulatory measures instituted or recommended in response to COVID‑19 are expected to be temporary, the duration of the business disruptions, and related financial impact, cannot be estimated at this time. The COVID‑19 outbreak could evolve into a worldwide health crisis that could adversely affect the economies and financial markets of many countries, resulting in an economic downturn and changes in global economic policy that could reduce demand for our products and our customers’ chips and have a material adverse impact on our business, operating results and financial condition.

Substantially all of our operations are located in the PRC and other areas impacted by the COVID‑19 outbreak, and those operations have been, and may continue to be, adversely affected by the COVID‑19 outbreak.

We conduct substantially all of our product development, manufacturing, support and services in the PRC, and those activities have been directly impacted by the COVID‑19 outbreak and related restrictions on transportation and public appearances. In February 2020 our ACM Shanghai headquarters were closed for an additional six days beyond the normal Lunar New Year Holiday in accordance with Shanghai government restrictions related to the outbreak, and we do not expect all of the staff at our Shanghai facility to return to work until the second quarter of 2020. We cannot assure you that further closures or reductions of our PRC operations or production may not be necessary in upcoming months as the result of business interruptions arising from protective measures being taken by the PRC and other governmental agencies or of other consequences of the COVID‑19 outbreak.

Our corporate headquarters are located in San Mateo County in the San Francisco Bay Area. In order to attempt to mitigate the COVID-19 pandemic, in March 2020 (a) the State of California declared a state of emergency related to the spread of COVID‑19, (b) the San Francisco Department of Public Health announced aggressive recommendations to reduce the spread of the disease, (c) the health officers of six San Francisco Bay Area counties, including San Mateo County, issued shelter-in-place orders, which (i) direct all individuals living in those counties to shelter at their places of residence (subject to limited exceptions), (ii) direct all businesses and governmental agencies to cease non-essential operations at physical locations in those counties, (iii) prohibit all non-essential gatherings of any number of individuals, and (iv) order cessation of all non-essential travel, and (d) the Governor of California and the State Public Health Officer and Director of the California Department of Public Health ordered all individuals living in the State of California to stay at their place of residence for an indefinite period of time (subject to limited exceptions). The effects of these actions may negatively impact productivity, disrupt our business and delay timelines, the magnitude of which will depend, in part, on the length and severity of the restrictions and other limitations on our ability to conduct our business in the ordinary course.

Extended periods of interruption to our corporate, development or manufacturing facilities due to the COVID‑19 outbreak could cause us to could lose revenue and market share, which would depress our financial performance and could be difficult to recapture. Our business may also be harmed if travel to or from the PRC or the United States continues to be restricted or inadvisable or if members of management and other employees are absent because they contract the coronavirus, they elect not to come to work due to the illness affecting others in our office or laboratory facilities, or they are subject to quarantines or other governmentally imposed restrictions.

A portion of the expected sales of our tools in the first quarter of 2020 have been, and additional sales may be, delayed as a result of effects of the COVID‑19 outbreak on the operations of our customers, who are located principally in the PRC and surrounding areas.

Our customers’ business operations have been, and are continuing to be, subject to business interruptions arising from the COVID‑19 outbreak. To date a majority of our revenue from sales of single-wafer wet cleaning equipment for front-end manufacturing has been derived from customers located in the PRC and surrounding areas that have been impacted by COVID‑19. Three customers that accounted for 73.8% of our revenue in 2019 and 87.6% of our revenue in 2018 are based in the PRC and Korea. One of those customers, Yangtze Memory Technologies Co., Ltd. — which accounted for 27.5% of our 2019 revenue and 39.6% of our 2018 revenue — is based in Wuhan. While Yangtze Memory Technologies Co., Ltd. and other key customers continued to operate their fabrication facilities without interruption during and after the first quarter of 2020, some customers were forced to scale down production. A portion of the revenues we expected to recognize in the first quarter of 2020 will not be recognized until later, as we have, in accordance with orders received from customers, deferred delivery of some tools from the first quarter. We continue to actively monitor the situation, but there can be no assurance that the COVID‑19 outbreak will not result in further delays, or possibly reductions, in our recognition of revenue. Moreover, because our longer-term growth strategy is based upon the assumption that demand for devices that use semiconductors will continue to grow, any slowdown in the growth of demand for chips, particularly in the PRC, as a result of COVID-19 could have a serious adverse effect on our business.

Our global supply chain may be materially adversely impacted due to the COVID‑19 outbreak.

We rely upon the facilities of our global suppliers with operations in the PRC, Japan, Taiwan and the United States to support our business. We source the substantial majority of our components from Asia. The outbreak has resulted in significant governmental measures in many countries being implemented to control the spread of COVID‑19, including restrictions on manufacturing and the movement of employees both in and out of China and within many regions of the PRC. As a result of COVID‑19 and the measures designed to contain its spread, our suppliers may not have the materials, capacity, or capability to supply our components according to our schedule and specifications. Further, there may be logistics issues, including our ability and our supply chain’s ability to quickly ramp up production, and transportation demands that may cause further delays. If our suppliers’ operations are curtailed, we may need to seek alternate sources of supply, which may be more expensive. Alternate sources may not be available or may result in delays in shipments to us from our supply chain and subsequently to our customers, each of which would affect our results of operations. While the disruptions and restrictions on the ability to travel, quarantines and temporary closures of the facilities of our suppliers, as well as general limitations on movement in the region, are expected to be temporary, the duration of the production and supply chain disruption, and related financial impact, cannot be estimated at this time. Should the production and distribution closures continue for an extended period of time, the impact on our supply chain could have a material adverse effect on our results of operations and cash flows. Business disruptions could also negatively affect the sources and availability of components and materials that are essential to the operation of our business. Moreover, our customers source a range of production equipment, supplies and services from other suppliers with operations around the world, and any reduction in supply capacity at those customers’ factories due to the COVID‑19 pandemic may reduce or even halt those customers’ production and result in a decrease in the demand for our products.

The COVID‑19 outbreak could negatively impact our currently planned projects and investments in the PRC, including the STAR IPO.

Our strategy includes a number of plans to support the growth of our core business. In June 2019 we began working toward the proposed STAR Listing and STAR IPO with respect to shares of ACM Shanghai, and in November 2019 ACM Shanghai entered into an agreement initiating a process intended to lead to our acquisition of land rights in the Lingang area of Shanghai where we can construct a new research and development center and factory. The extent to which COVID-19 impacts these projects will depend on future developments that are highly uncertain and cannot be predicted. If the disruptions posed by COVID‑19 and related government measures, or other matters of global concern, continue for an extensive period of time, our ability to consummate one or both of these planned projects could be materially adversely affected.

In September 2019 ACM Shanghai entered into a partnership agreement for the purposes of engaging in equity venture capital investments in strategic emerging and high-tech industries with a focus on the semiconductor industry. We cannot predict the effect that the COVID‑19 outbreak in the PRC will have on companies that would otherwise be desirable investments for the partnership, and the outbreak or related governmental actions could significantly impair the ability of the partnership to identify desirable investments or our ability to realize the anticipated benefits of the partnership.

| ● |

actual or anticipated fluctuations in our revenue and other operating results;

|

| ● |

the financial projections we may provide to the public, any changes in these projections or our failure to meet these projections;

|

| ● |

actions of securities analysts who initiate or maintain coverage of us, changes in financial estimates by any securities analysts who follow our company, or our failure to meet these estimates or the

expectations of investors;

|

| ● |

changes in projections for the chips or chip equipment industries or in the operating performance or expectations and stock market valuations of chip companies, chip equipment companies or technology

companies in general;

|

| ● |

changes in operating results;

|

| ● |

any changes in the financial projections we may provide to the public, our failure to meet these projections, or changes in recommendations by any securities analysts that elect to follow Class A common

stock;

|

| ● |

additional shares of Class A common stock being sold into the market by us or our existing stockholders or the anticipation of such sales;

|

| ● |

price and volume fluctuations in the overall stock market, including as a result of trends in the economy as a whole;

|

| ● |

lawsuits threatened or filed against us;

|

| ● |

litigation and other developments relating to our patents or other proprietary rights or those of our competitors;

|

| ● |

developments in new legislation and pending lawsuits or regulatory actions, including interim or final rulings by judicial or regulatory bodies; and

|

| ● |

general economic trends, including changes in the demand for electronics or information technology or geopolitical events such as war or acts of terrorism, or any responses to such events.

|

| ● |

our dual class common stock structure provides holders of Class B common stock with the ability to control the outcome of matters requiring stockholder approval, even if they own significantly less than a

majority of the total number of outstanding shares of Class A and Class B common stock;

|

| ● |

when the outstanding shares of Class B common stock represent less than a majority of the combined voting power of common stock;

|

| ● |

amendments to our charter or bylaws will require the approval of two-thirds of the combined vote of our then-outstanding shares of Class A and Class B common stock;

|

| ● |

vacancies on the board of directors will be able to be filled only by the board and not by stockholders;

|

| ● |

the board, which currently is not staggered, will be automatically separated into three classes with staggered three-year terms;

|

| ● |

directors will only be able to be removed from office for cause; and

|

| ● |

our stockholders will only be able to take action at a meeting and not by written consent;

|

| ● |

only our chair, our chief executive officer or a majority of our directors is authorized to call a special meeting of stockholders;

|

| ● |

advance notice procedures apply for stockholders to nominate candidates for election as directors or to bring matters before an annual meeting of stockholders;

|

| ● |

our charter authorizes undesignated preferred stock, the terms of which may be established, and shares of which may be issued, without stockholder approval; and

|

| ● |

cumulative voting in the election of directors is prohibited.

|

| ● |

any derivative action or proceeding brought on our behalf;

|

| ● |

any action asserting a claim of breach of a fiduciary duty owed to us, our stockholders, creditors or other constituents by any of our directors, officers, other employees, agents or stockholders;

|

| ● |

any action asserting a claim arising under the Delaware General Corporation Law, our charter or bylaws, or as to which the Delaware General Corporation Law confers jurisdiction on the Court of Chancery of

the State of Delaware; or

|

| ● |

any action asserting a claim that is governed by the internal affairs doctrine.

|

| ● |

We expect the bidding and negotiation process for the land will be completed by the first half of 2020. If the process is successfully completed on that schedule, ACM Shanghai would seek to begin

construction of a new research and development center and factory on the Target Plot in the second half of 2020, with the objective of commencing production at the new facility in late 2022.

|

| ● |

Pursuant to the existing agreement, ACM Shanghai is obligated to pay a performance bond of RMB 640,000 ($90,892 as of December 2, 2019) to Lingang Development. In general, if ACM

Shanghai decides not to proceed with the bidding and negotiation process for the land in accordance with the requirements of the existing agreement, Lingang Development will be entitled to keep the performance bond as liquidated

damages. Otherwise, Lingang Development generally will be obligated to return the performance bond to ACM Shanghai, including if ACM Shanghai is unsuccessful in bidding for rights to the Target Plot or is successful in entering into a

definitive agreement to acquire rights to the Target Plot.

|

We have never declared or paid cash dividends on our capital stock. We intend to retain all available funds and any future earnings to support the operation of and to finance the growth and development of our business and do not anticipate paying any cash dividends in the foreseeable future.

| ● |

Space Alternated Phase Shift, or SAPS, technology for flat and patterned wafer surfaces, which employs alternating phases of megasonic waves to

deliver megasonic energy in a highly uniform manner on a microscopic level;

|

| ● |

Timely Energized Bubble Oscillation, or TEBO, technology for patterned wafer surfaces at advanced process nodes, which provides effective,

damage-free cleaning for 2D and 3D patterned wafers with fine feature sizes;

|

| ● |

Tahoe technology for cost and environmental savings, which delivers high cleaning performance using significantly less sulfuric acid and hydrogen

peroxide than is typically consumed by conventional high-temperature single-wafer cleaning tools; and

|

| ● |

Electro-Chemical Plating, or ECP, technology for advanced metal plating, which includes Ultra ECP AP, or Advanced Packaging, technology for

back-end assembly processes and Ultra ECP MAP, or Multi-Anode Partial Plating, technology for front-end wafer fabrication processes.

|

| ● |

a listing, which we refer to as the STAR Listing, of shares of ACM Shanghai on the Shanghai Stock Exchange’s Sci-Tech innovAtion boaRd, known as the STAR Market; and

|

| ● |

a concurrent initial public offering, which we refer to as the STAR IPO, of ACM Shanghai shares in the People’s Republic of China, or the PRC, at a pre-offering valuation of not less than RMB 5.15

billion ($747.1 million).

|

| ● |

In June 2019 ACM Shanghai entered into agreements with seven investors, or the First Tranche Investors, pursuant to which the First Tranche Investors purchased ACM Shanghai shares for a total of RMB 187.9

million ($27.3 million as of June 12, 2019).

|

| ● |

In November 2019 ACM Shanghai entered into agreements with each of the First Tranche Investors and eight PRC-based investment firms, or the Second Tranche Investors, pursuant to which the Second Tranche

Investors subsequently purchased ACM Shanghai shares, or the Second Tranche Shares, for a total of RMB 228.2 million ($32.4 million as of November 29, 2019). The purchase price per Second Tranche Share was equal to the purchase price

per share paid by the First Tranche Investors and was based on a pre-investment enterprise valuation of ACM Shanghai of RMB 4.84 billion ($688.9 million as of November 29, 2019).

|

| ● |

Operations: We conduct substantially all of our product development, manufacturing, support and services in the PRC, and those activities have been directly

impacted by the COVID–19 outbreak and related restrictions on transportation and public appearances. In February 2020 our ACM Shanghai headquarters were closed for an additional six days beyond the normal Lunar New Year Holiday in

accordance with Shanghai government restrictions related to the outbreak. We took steps before and after the Lunar New Year to ensure no employees took unreasonable risks to rush back to work. Currently more than 90% of our staff have

returned to work at both of our Shanghai facilities. To date we have not experienced absenteeism of management or other key employees, other than certain of our executive officers being delayed in traveling back to the PRC after working

from our California office in February. Our corporate headquarters are located in San Mateo County in the San Francisco Bay Area and are the subject of a number of state and county public health directives and orders. These actions have

not negatively impacted our business to date, however, because of the limited number of employees at our headquarters and the nature of the work they generally perform.

|

| ● |

Operating Results; Customers: Our customers’ business operations have been, and are continuing to be, subject to business interruptions

arising from the COVID–19 outbreak. Historically a majority of our revenue from sales of single-wafer wet cleaning equipment for front-end manufacturing has been derived from customers located in the PRC and surrounding areas that have

been impacted by COVID–19. Three customers that accounted for 73.8% of our revenue in 2019 and 87.6% of our revenue in 2018 are based in the PRC and Korea. One of those customers, Yangtze Memory Technologies Co., Ltd. — which accounted

for 27.5% of our 2019 revenue and 39.6% of our 2018 revenue — is based in Wuhan. While Yangtze Memory Technologies Co., Ltd. and other key customers continued to operate their fabrication facilities without interruption during and after

the first quarter of 2020, they were forced to restrict access of service personnel and deliveries to and from their facilities.. A portion of the revenues we previously expected to recognize in the first quarter of 2020 will not be

recognized, as we have, in accordance with orders received from customers, deferred delivery of some tools from the first quarter. We believe these deliveries represent deferred, not lost, revenues, which we are working to recover by

increasing our manufacturing output in the second and third quarters of 2020.

|

| ● |

Suppliers: Our global supply chain includes components sourced from the PRC, Japan, Taiwan, the United States and Europe. While the COVID–19

outbreak has resulted in significant governmental measures being implemented to control the spread of COVID–19 around the world, to date we have not experienced issues with our supply chain. As with our customers, we continue to be in

close contact with our key suppliers to help ensure we are able to identify any potential supply issues that may arise.

|

| ● |

Projects: Our strategy includes a number of plans to support the growth of our core business, including the proposed STAR Listing and STAR IPO

with respect to shares of ACM Shanghai described above as well as ACM Shanghai’s proposed acquisition of land rights in the Lingang area of Shanghai where we intend to construct a new research and development center and factory. The

extent to which COVID–19 impacts these projects will depend on future developments that are highly uncertain, but to date the timing of these potential project has not been delayed or disrupted by COVID–19 or related government

measures.

|

| ● |

Sales and Development. During the sale process we may, depending on a prospective customer’s specifications

and requirements, need to perform additional research, development and testing to establish that a tool can meet the prospective customer’s requirements. We then host an in-house demonstration of the customized tool prototype. Sales

cycles for orders that require limited customization and do not require that we develop new technology usually take from 6 to 12 months, while the product life cycle, including the initial design, demonstration and final assembly

phases, for orders requiring development and testing of new technologies can take as long as 2 to 4 years. As we expand our customer base, we expect to gain more repeat purchase orders for tools that we have already developed and

tested, which will eliminate the need for a demonstration phase and shorten the development cycle.

|

| ● |

Evaluation Periods. When a chip manufacturer proposes to purchase a particular type of tool from us for

the first time, we offer the manufacturer an opportunity to evaluate the tool for a period that can extend for 24 months or longer. In some cases, we do not receive any payment on first-time purchases until the tool is accepted. As a

result, we may spend between $1.0 and $2.0 million to produce a tool without receiving payment for more than 24 months or, if the tool is not accepted, without receiving any payment. Please see “Item 1A. Risk Factors—Risks Related to

Our Business and Our Industry—We may incur significant expenses long before we can recognize revenue from new products, if at all, due to the costs and length of research, development, manufacturing and customer evaluation process

cycles.”

|

| ● |

Purchase Orders. In accordance with industry practice, sales of our tools are made pursuant to purchase

orders. Each purchase order from a customer for one of our tools contains specific technical requirements intended to ensure, among other things, that the tool will be compatible with the customer’s manufacturing process line. Until a

purchase order is received, we do not have a binding purchase commitment. Our SAPS and TEBO customers to date have provided us with non-binding one- to two-year forecasts of their anticipated demands, and we expect future customers to

furnish similar non-binding forecasts for planning purposes. Any of those forecasts would be subject to change, however, by the customer at any time, without notice to us.

|

| ● |

Fulfillment. We seek to obtain a purchase order for a tool from three to four months in advance of the

expected delivery date. Depending upon the nature of a customer’s specifications, the lead time for production of a tool generally will extend from two to four months. The lead-time can be as long as six months, however, and in some

cases we may need to begin producing a tool based on a customer’s non-binding forecast, rather than waiting to receive a binding purchase order.

|

| ● |

direct costs, which consist principally of costs of tool components and subassemblies purchased from third-party vendors;

|

| ● |

compensation of personnel associated with our manufacturing operations, including stock-based compensation;

|

| ● |

depreciation of manufacturing equipment;

|

| ● |

amortization of costs of software used for manufacturing purposes;

|

| ● |

other expenses attributable to our manufacturing department; and

|

| ● |

allocated overhead for rent and utilities.

|

| ● |

compensation of personnel associated with pre- and after-sales support and other sales and marketing activities, including stock-based compensation;

|

| ● |

sales commissions paid to independent sales representatives;

|

| ● |

fees paid to sales consultants;

|

| ● |

shipping and handling costs for transportation of products to customers;

|

| ● |

cost of trade shows;

|

| ● |

travel and entertainment; and

|

| ● |

allocated overhead for rent and utilities.

|

| ● |

compensation of personnel associated with our research and development activities, including stock-based compensation;

|

| ● |

costs of components and other research and development supplies;

|

| ● |

travel expense associated with customer support;

|

| ● |

amortization of costs of software used for research and development purposes; and

|

| ● |

allocated overhead for rent and utilities.

|

| ● |

compensation of executive, accounting and finance, human resources, information technology, and other administrative personnel, including stock-based compensation;

|

| ● |

professional fees, including accounting and legal fees;

|

| ● |

other corporate expenses; and

|

| ● |

allocated overhead for rent and utilities.

|

| ● |

Stock-based awards granted to employees and non-employees are measured at the fair value of the awards on the grant date and are recognized as expenses either (a) immediately on grant, if no vesting

conditions are required, or (b) using the graded vesting method, net of estimated forfeitures, over the requisite service period. The fair value of stock options is determined using the Black-Scholes valuation model. Stock-based

compensation expense, when recognized, is charged to cost of revenue or to the category of operating expense corresponding to the service function of the employee or non-employee.

|

| ● |

We also grant discounts to employees when they subscribe for the new shares of ACM Shanghai, and we account for those stock-based awards in accordance with Accounting Standards

Codification, or ASC, Topic 718, Compensation—Stock Compensation

|

|

Year Ended December 31,

|

||||||||

|

2019

|

2018

|

|||||||

|

(in thousands)

|

||||||||

|

Stock-Based Compensation Expense:

|

||||||||

|

Cost of revenue

|

$

|

250

|

$

|

71

|

||||

|

Sales and marketing expense

|

328

|

120

|

||||||

|

Research and development expense

|

1093

|

255

|

||||||

|

General and administrative expense

|

1,901

|

2,917

|

||||||

|

$

|

3,572

|

$

|

3,363

|

|||||

| ● |

Government subsidies relating to current expenses are reflected as reductions of those expenses in the periods in which they are reported. Those reductions totaled $3.2 million in 2019 and $1.5 million in

2018.

|

| ● |

Government grants used to acquire depreciable assets are transferred from long-term liabilities to property, plant and equipment when the assets are acquired and then the recorded amounts of the assets

are credited to other income over the useful lives of the assets. Related government subsidies recognized as other income totaled $0.1 million in 2019 and in 2018.

|

| ● |

We define “shipments” of tools to include (a) a “repeat” delivery to a customer of a type of tool that the customer has previously accepted, for which we recognize revenue upon delivery, and (b) a

“first-time” delivery of a “first tool” to a customer on an approval basis, for which we may recognize revenue in the future if contractual conditions are met and customer acceptance is received.

|

| ● |

We define “adjusted EBITDA” as our net income excluding interest expense (net), income tax benefit (expense), depreciation and amortization, and stock-based compensation. We define adjusted EBITDA to also

exclude restructuring costs, although we have not incurred any such costs to date.

|

| ● |

We define “free cash flow” as net cash provided by operating activities less purchases of property and equipment (net of proceeds from disposals) and of intangible assets.

|

| ● |

We define “adjusted operating income (loss)” as our income (loss) from operations excluding stock-based compensation.

|

| ● |

a shipment to a customer of a type of tool that the customer has previously accepted, for which we recognize revenue when the tool is delivered; and

|

| ● |

a shipment to a customer of a type of tool that the customer is receiving and evaluating for the first time, in each case a “first tool,” for which we may recognize revenue at a later date, subject to the

customer’s acceptance of the tool upon the tool’s satisfaction of applicable contractual requirements.

|

| ● |

adjusted EBITDA excludes depreciation and amortization and, although these are non-cash expenses, the assets being depreciated or amortized may have to be replaced in the future;

|

| ● |

we exclude stock-based compensation expense from adjusted EBITDA and adjusted operating income (loss), although (a) it has been, and will continue to be for the foreseeable future, a significant recurring

expense for our business and an important part of our compensation strategy and (b) if we did not pay out a portion of our compensation in the form of stock-based compensation, the cash salary expense included in operating expenses

would be higher, which would affect our cash position;

|

| ● |

the expenses and other items that we exclude in our calculation of adjusted EBITDA may differ from the expenses and other items, if any, that other companies may exclude from adjusted EBITDA when they

report their operating results;

|

| ● |

adjusted EBITDA does not reflect changes in, or cash requirements for, working capital needs;

|

| ● |

adjusted EBITDA does not reflect interest expense, or the requirements necessary to service interest or principal payments on debt;

|

| ● |

adjusted EBITDA does not reflect income tax expense (benefit) or the cash requirements to pay taxes;

|

| ● |

adjusted EBITDA does not reflect historical cash expenditures or future requirements for capital expenditures or contractual commitments;

|

| ● |

although depreciation and amortization charges are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and adjusted EBITDA does not reflect any cash

requirements for such replacements; and

|

| ● |

adjusted EBITDA includes expense reductions and non-operating other income attributable to PRC governmental grants, which may mask the effect of underlying developments in net income (loss), including

trends in current expenses and interest expense, and free cash flow includes the PRC governmental grants, the amount and timing of which can be difficult to predict and are outside our control.

|

|

Year Ended December 31,

|

||||||||

|

2019

|

2018

|

|||||||

|

(in thousands)

|

||||||||

|

Adjusted EBITDA Data:

|

||||||||

|

Net income

|

$

|

19,458

|

$

|

6,574

|

||||

|

Interest expense, net

|

412

|

469

|

||||||

|

Income tax expense (benefit) |

(518

|

)

|

806

|

|||||

|

Depreciation and amortization

|

788

|

417

|

||||||

|

Stock based compensation

|

3,572

|

3,363

|

||||||

|

Adjusted EBITDA

|

$

|

23,712

|

$

|

11,629

|

||||

|

Year Ended December 31,

|

||||||||

|

2019

|

2018

|

|||||||

|

(in thousands)

|

||||||||

|

Free Cash Flow Data:

|

||||||||

|

Net cash provided by operating activities

|

$

|

9,403

|

$

|

6,909

|

||||

|

Purchase of property and equipment

|

(971

|

)

|

(1,830

|

)

|

||||

|

Purchase of intangible assets

|

(154

|

)

|

(241

|

)

|

||||

|

Free cash flow

|

$

|

8,278

|

$

|

4,838

|

||||

|

Year Ended December 31,

|

||||||||||||||||||||||||

|

2019

|

2018

|

|||||||||||||||||||||||

|

Actual

(GAAP)

|

SBC

|

Adjusted

(Non-GAAP)

|

Actual

(GAAP)

|

SBC

|

Adjusted

(Non-GAAP)

|

|||||||||||||||||||

|

(in thousands)

|

||||||||||||||||||||||||

|

Revenue

|

$

|

107,524

|

$

|

-

|

$

|

107,524

|

$

|

74,643

|

$

|

-

|

$

|

74,643

|

||||||||||||

|

Cost of revenue

|

(56,870

|

)

|

(250

|

)

|

(56,620

|

)

|

(40,194

|

)

|

(71

|

)

|

(40,123

|

)

|

||||||||||||

|

Gross profit

|

50,654

|

(250

|

)

|

50,904

|

34,449

|

(71

|

)

|

34,520

|

||||||||||||||||

|

Operating expenses:

|

||||||||||||||||||||||||

|

Sales and marketing

|

(11,902

|

)

|

(328

|

)

|

(11,574

|

)

|

(9,611

|

)

|

(120

|

)

|

(9,491

|

)

|

||||||||||||

|

Research and development

|

(12,900

|

)

|

(1,093

|

)

|

(11,807

|

)

|

(10,380

|

)

|

(255

|

)

|

(10,125

|

)

|

||||||||||||

|

General and administrative

|

(8,061

|

)

|

(1,901

|

)

|

(6,160

|

)

|

(7,987

|

)

|

(2,917

|

)

|

(5,070

|

)

|

||||||||||||

|

Income (loss) from operations

|

$

|

17,791

|

$

|

(3,572

|

)

|

$

|

21,363

|

$

|

6,471

|

$

|

(3,363

|

)

|

$

|

9,834

|

||||||||||

| 1. |

identify the contract(s) with a customer;

|

| 2. |

identify the performance obligations in the contract;

|

| 3. |

determine the transaction price;

|

| 4. |

allocate the transaction price to the performance obligations in the contract; and

|

| 5. |

recognize revenue when (or as) the entity satisfies a performance obligation.

|

| ● |

when the customer has previously accepted the same tool with the same specifications and we can objectively demonstrate that the tool meets all of the required acceptance criteria;

|

| ● |

when the sales contract or purchase order contains no acceptance agreement or lapsing acceptance provision and we can objectively demonstrate that the tool meets all of the required acceptance

criteria;

|

| ● |

when the customer withholds acceptance due to issues unrelated to product performance, in which case revenue is recognized when the system is performing as intended and meets predetermined

specifications; or

|

| ● |

when our sales arrangements do not include a general right of return.

|

Leases

ROU assets represent our right to use an underlying asset for the lease term and lease liabilities represent our obligation to make lease payments arising from the lease. Operating lease ROU assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. As most of our leases do not provide an implicit rate, we use our incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. We use the implicit rate when readily determinable. The operating lease ROU asset also includes any lease payments made and excludes lease incentives. Our lease terms may include options to extend or terminate the lease when it is reasonably certain that we will exercise that option. Lease expense for lease payments is recognized on a straight-line basis over the lease term.

| ● |

We use the market closing price for the Class A common stock as reported on the Nasdaq Global Market to determine the fair value of the Class A common stock.

|

| ● |

The risk-free interest rates for periods within the expected life of the option are based on the yields of zero-coupon U.S. Treasury securities.

|

| ● |

Due to a lack of company-specific historical and implied volatility data, we have based our estimate of expected volatility on the historical volatility of a group of similar companies that are

publicly traded. For these analyses, we have selected companies with comparable characteristics to ours including enterprise value, risk profile, position within the industry, and with historical share price information sufficient

to meet the expected life of the stock-based awards. We compute the historical volatility data using the daily closing prices for the selected companies’ shares during the equivalent period of the calculated expected term of our

stock-based awards. We will continue to apply this process until a sufficient amount of historical information regarding the volatility of our own stock price becomes available.

|

| ● |

The expected term represents the period of time that options are expected to be outstanding. The expected term of stock options is based on the average between the vesting period and the contractual term for each grant according

to Staff Accounting Bulletin No. 110.

|

| ● |

The expected dividend yield is assumed to be 0%, based on the fact that we have never paid cash dividends and have no present intention to pay cash dividends.

|

|

Year Ended December 31,

|

||||||||

|

2019

|

2018

|

|||||||

|

Revenue

|

100.0

|

%

|

100.0

|

%

|

||||

|

Cost of revenue

|

52.9

|

53.8

|

||||||

|

Gross margin

|

47.1

|

46.2

|

||||||

|

Operating expenses:

|

||||||||

|

Sales and marketing

|

11.1

|

12.9

|

||||||

|

Research and development

|

12.0

|

13.9

|

||||||

|

General and administrative

|

7.5

|

10.7

|

||||||

|

Total operating expenses, net

|

30.6

|

37.5

|

||||||

|

Income from operations

|

16.5

|

8.7

|

||||||

|

Interest expense, net

|

(0.4

|

)

|

(0.6

|

)

|

||||

|

Other income, net

|

1.3

|

1.7

|

||||||

|

Equity income in net income of affiliates

|

0.2

|

0.2

|

||||||

|

Income before income taxes

|

17.6

|

9.9

|

||||||

|

Income tax expense

|

0.5

|

(1.1

|

)

|

|||||

|

Net income

|

18.1

|

8.8

|

||||||

|

Less: Net income attributable to redeemable non-controlling interests

|

0.4

|

-

|

||||||

|

Net income attributable to ACM Research, Inc.

|

17.7

|

%

|

8.8

|

%

|

||||

|

Year Ended December 31,

|

||||||||||||

|

2019

|

2018

|

Y/Y %Change

|

||||||||||

|

(in thousands)

|

||||||||||||

|

Revenue

|

$

|

107,524

|

$

|

74,643

|

44.1

|

%

|

||||||

|

Year Ended December 31,

|

|||||||||||

|

2019

|

2018

|

Y/Y %Change

|

|||||||||

|

(in thousands)

|

|||||||||||

|

Cost of revenue

|

$

|

56,870

|

$

|

40,194

|

41.5

|

%

|

|||||

|

Gross profit

|

$

|

50,654

|

$

|

34,449

|

47.0

|

%

|

|||||

|

Gross margin

|

47.1

|

%

|

46.2

|

%

|

96 bps

|

||||||

|

|

Year Ended December 31,

|

|||||||||||

|

2019

|

2018

|

Y/Y %Change

|

||||||||||

|

(in thousands)

|

||||||||||||

|

Sales and marketing expense

|

$

|

11,902

|

$

|

9,611

|

23.8

|

%

|

||||||

|

Research and development expense

|

12,900

|

10,380

|

24.3

|

% | ||||||||

|

General and administrative expense

|

8,061

|

7,987

|

0.9

|

% | ||||||||

|

Total operating expenses

|

$

|

32,863

|

$

|

27,978

|

17.5

|

% | ||||||

|

Year Ended December 31,

|

Y/Y % Change

|

|||||||||||

|

2019

|

2018

|

2019 v 2018

|

||||||||||

|

(in thousands)

|

||||||||||||

|

Interest income

|

$

|

333

|

$

|

29

|

1048.3

|

%

|

||||||

|

Interest expense

|

(745

|

)

|

(498

|

)

|

49.6

|

%

|

||||||

|

Interest expense, net

|

$

|

(412

|

)

|

$

|

(469

|

)

|

(12.2

|

%)

|

||||

|

Other income, net

|

$ |

1,393

|

$ |

1,255

|

11.0

|

% |

||||||

|

Year Ended December 31,

|

||||||||

|

2019

|

2018

|

|||||||

|

Current:

|

||||||||

|

U.S. federal

|

$ |

$

|

-

|

|||||

|

U.S. state

|

- |

-

|

||||||

|

Foreign

|

(3,176

|

)

|

(1,149

|

)

|

||||

|

Total current tax expense

|

(3,176

|

)

|

(1,149

|

)

|

||||

|

Deferred:

|

||||||||

|

U.S. federal

|

3,728

|

-

|

||||||

|

U.S. state

|

- |

-

|

||||||

|

Foreign

|

(34

|

)

|

343

|

|||||

|

Total deferred tax benefit (expense)

|

3,694

|

343

|

||||||

|

Total income tax benefit (expense)

|

$

|

518

|

$

|

(806

|

)

|

|||

|

Lender

|

Agreement Date

|

Maturity Date

|

Annual

Interest Rate |

Maximum

Borrowing Amount(1) |

Amount Outstanding

at December 31, 2019 |

|||||||||||

|

(in thousands)

|

||||||||||||||||

|

Bank of Shanghai Pudong Branch

|

February 2019

|

January 2020

|

5.22

|

%