Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Jefferies Financial Group Inc. | d834711d8k.htm |

EXHIBIT 99

January 8, 2020

Dear Fellow Shareholders,

We have entered a new decade and our strategy for Jefferies Financial Group is straightforward and designed to complete the transformation of Jefferies into a pure financial services firm that is a global leader in Investment Banking, Capital Markets and Asset Management:

| 1. | Most importantly, we will continue to develop and seek to realize the potential of our core businesses, with a goal to continue to build a top-tier, well-diversified, client-focused, entrepreneurially-minded, fully-integrated global financial services firm. The business of Jefferies is to deliver great insight and exceptional execution to our clients, and our brand is well-positioned to continue to gain new clients and market share. Central to our plan is to deliver a consistent double-digit return on tangible equity (“ROE”). We have work to do in this regard, know what needs to be done and are committed to achieving it. |

| 2. | We intend to continue to realize the value of each investment in our merchant banking portfolio patiently and at the right time, while maintaining a proper sense of urgency. We expect to optimize value realization through outright sales, possible distributions in kind to our shareholders, possible evolution of certain of our investments into asset management platforms within Leucadia Asset Management (“LAM”) or other creative alternatives. Future merchant banking initiatives will likely be pursued under LAM, with capital provided by Jefferies in partnership with third party long-term investors who join us to leverage our access to unique deal flow and our capability to drive value creation through our deep and diverse global platform. |

| 3. | We expect to continue to return a meaningful amount of excess capital directly to our shareholders through dividends and share repurchases. We are in the best position ever to execute this commitment, as we have fewer illiquid investments, our excess liquidity is strong and our credit ratings improving. We will continue to repurchase shares so long as we believe our stock price is highly attractive compared to opportunities to expand our franchise, and will always be mindful to maintain appropriate levels of liquidity. |

Review of 2019

In 2019, Equities, Fixed Income and Asset Management produced a strong combined 25% annual increase in net revenues at Jefferies Group. We made solid progress throughout these businesses, while our VaR, degree of Level 3 positions and overall risk exposure remained at very manageable levels.

Unfortunately, our overall performance and the achievement of a double-digit ROE in our core businesses were held back in 2019 by a 20% decline in our net revenues in Investment Banking, our largest business. This followed two years of record Investment Banking net revenues in 2017 and 2018. Despite a remarkable “melt-up” in many market indices in calendar year 2019, much of our fiscal year (which began with the very difficult month of December 2018 and then the U.S. government shutdown)

Jefferies Financial Group Inc. Annual Report 2019 1

was marked by the challenges of tariffs and trade wars, Brexit uncertainty and many other cross-currents that dampened corporate deal making. Substantially all of the decrease in our Investment Banking net revenues was a result of lower capital markets revenue, with the vast majority of shortfall related to our Leveraged Finance business. Most of this shortfall in Leveraged Finance was due to an overall slowdown in primary issuance, particularly in the single-B rated market, where most leveraged buyouts are financed, and Jefferies is a market leader. Looking beyond this short-term bump in performance, we are exceptionally proud of our entire Investment Banking team and believe we are well positioned to continue to grow our franchise.

We are hopeful that our actions are speaking much louder than our words as we execute our plan and seek to optimize value for our shareholders. At the end of 2019, we sold the final 31% of National Beef and received $970 million in cash proceeds from the sale and final distributions. When combined with our prior sale and distributions, cumulative cash realized over the eight years since we invested $868 million in National Beef is $2.9 billion. In September 2019, we decided that Spectrum Brands was no longer a core holding and elected to distribute as a dividend to our shareholders our 15% ownership position valued at $451 million, and we are pleased Spectrum’s stock price is higher today. Altogether, Jefferies returned $1.1 billion in capital to shareholders in 2019 through our $451 million dividend of Spectrum Brands, $150 million in cash dividends and the repurchase of 26 million shares at $19.52, for an aggregate of $506 million. Since our fiscal year end on November 30, 2019, we have repurchased an additional 1.7 million shares at $20.93 per share, a total of $36 million.

During the past two fiscal years, Jefferies has returned to shareholders in excess of $2.4 billion, or 31% of tangible shareholders’ equity at the beginning of the period. Even after this return of nearly one third of tangible equity to shareholders, Jefferies ended fiscal 2019 with tangible shareholders’ equity of $7.7 billion, slightly higher than the $7.6 billion at the beginning of the two fiscal years, and parent company liquidity of $2.2 billion. Our primary operating subsidiary, Jefferies Group LLC, also ended the year with record liquidity.

Outlook for 2020

In the early days of fiscal 2020, sentiment and momentum are much better than at the same time last year. Our Investment Banking backlog for the first quarter of 2020 is at a record level and well-diversified by industry, product and geography. Our Equities and Fixed Income businesses recorded a strong December. We have seen a resurgence of merger and acquisition activity, flourishing capital markets, the anticipation of a negotiated Brexit, continued strong employment numbers, accommodative global monetary support and an abundance of liquidity. The secondary market for Leveraged Finance has shown renewed strength this fiscal year, which bodes well for broadening new issue activity. The fact that 2020 is also a U.S. presidential election year generally bodes well for the economy and activity, although we will keep our eyes keenly on the burgeoning geopolitical risks.

We have made significant hires over the past few years across our firm and expect to reap the benefits in 2020. The path to a double-digit ROE is primarily dependent on realizing the business opportunity inherent in this significant investment, and we believe 2019 simply delayed the process of achieving this goal. Reasonable success in Investment Banking, coupled with continued momentum in Equities, Fixed Income and Asset Management, all executed with solid discipline on costs and capital utilization, should allow Jefferies Group to deliver strong results.

We have achieved top tier market positions in the U.S. in virtually all our business lines and have invested consistently in expanding our talent base. Our momentum across the firm is palpable.

2 Jefferies Financial Group Inc. Annual Report 2019

With our typical contrarian bent, in 2019, we continued to invest in both Europe and Asia, and we appear to be well-positioned in both regions for 2020 and beyond. Jefferies has 899 employees based across Europe, and 404 in Asia and Australia, an increase of 15% during the past year. In the face of an opening we saw in the competitive environment, we made a series of hires across Asia to strengthen our platforms in Hong Kong/China, Japan, India and Singapore. In less than two years, our entry into Australia has grown to 55 employees primarily across Investment Banking and Equities.

We have noted for several years that a number of our major competitors are experiencing challenges or changes in their business priorities that create further opportunity for us. This remains the case and we believe will continue to work to our advantage. Finally, our culture, capabilities and brand have never been stronger and, while market forces can prove challenging, we strongly believe Jefferies is in the best position possible as we start 2020 to deliver on our potential.

Long-Term Perspective

We have previously noted that Investment Banking is the fundamental driver of our core businesses. We decided several years ago, and still believe strongly, that our Investment Banking effort is readily scalable, the most differentiated of all our businesses and the most likely to deliver consistent long-term results and meaningful growth. Approximately 70% of our Investment Banking net revenues in 2019 came from repeat clients. We have refocused our Fixed Income business to reduce risk and capital utilization, and to prioritize partnership with Investment Banking. Our Equities business continues to develop well and in a capital-efficient manner, and is also closely aligned with our Investment Banking focus.

Building a world class investment banking platform is not easy to do and requires relentless effort, patience and perseverance over a long period of time and through multiple economic and market cycles. Thirty years ago, just after one of us arrived at our firm, Jefferies was a pure boutique with one real business, cash equities, which drove net earnings of $4 million on total galactic-wide revenues of $131 million. Twenty years ago, as the other of us was heading toward our firm, Jefferies was still headquartered in Los Angeles and had grown mightily to 885 employees. We were no longer a boutique, but a serious niche player that was diversifying to better serve our clients. Our net revenues were $544 million, with Equities representing 56%, or $302 million. We had $397 million in shareholders’ equity and an equity market capitalization of what we thought then to be an incredible $528 million. Ten years ago, Jefferies emerged from the Financial Crisis without requiring or receiving taxpayer support and with net revenues surpassing $2 billion. In 2010, Investment Banking represented almost half of our revenues and the balance was split roughly evenly between Equities and Fixed Income.

Jefferies today is an incredibly stronger global full-service investment banking firm, and hugely differentiated from boutiques which typically are dependent on one product and operate without direct knowledge of the broader Investment Banking and Capital Markets landscape, and from bank holding companies that generally lead with balance sheet, rather than insight, creativity or entrepreneurial agility.

Decades show true evolution, while shorter periods of time provide only an erratic glimpse. Looking back at individual years that make up each of the past three decades, one would get a limited picture of our momentum and opportunity. Some years we click on all cylinders, sometimes most of them and occasionally just a couple, but we find a way to always persevere, advance our platform and ultimately thrive.

Jefferies Financial Group Inc. Annual Report 2019 3

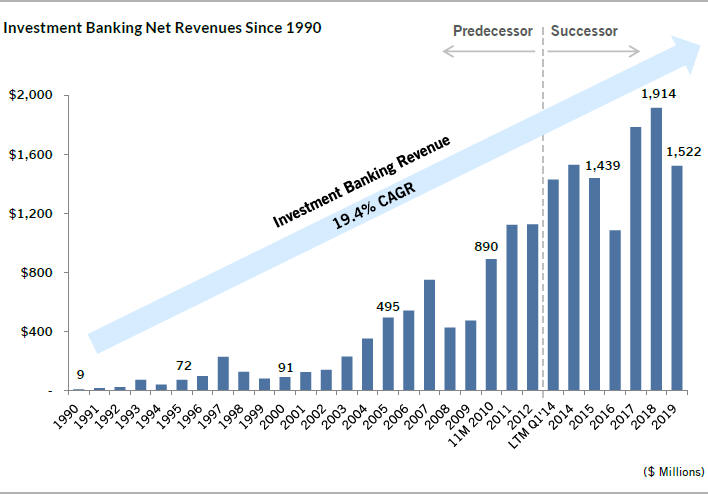

To illustrate this point, we present below the arc of our Investment Banking net revenues, which shows a consistent growth in our business, despite occasional cyclical forces such as in 1994, 1998, 2008-09, 2016 and 2019. It is not a straight arrow up over the short-term, but the intermediate and long-term periods tell a story of which all of us at Jefferies are proud:

Investment Banking

Our Investment Banking advisory business delivered solid performance in 2019, and while our revenues decreased by 6% from 2018, this was against the backdrop of an 11% decline in industry-wide M&A fees across the U.S. and Europe. We continued our trend of executing larger transactions and, in 2019, signed or completed 57 M&A transactions greater than $1 billion in size. At the same time, we maintained our leadership in middle market M&A, where we now rank among the top three firms across the U.S. and Europe in M&A market share for transactions less than $1 billion in size. Looking ahead, we expect our M&A revenues to continue to benefit from our significantly expanded sector and geographic footprint, our momentum in winning larger deals and the strength of our franchise in sell-side M&A.

We continue to make great progress in building our technology investment banking business, which is one of the largest and most rapidly growing fee pools in investment banking, as technology has become an important part of strategic activity across every industry. Over the last three years, we have significantly increased the size of our technology team across the world, and our global team now consists of over 130 investment bankers specialized in technology. During this time frame, our technology investment banking revenues have increased by approximately 70%, primarily driven by revenue growth in technology M&A and equity capital markets. Given the scale and momentum of our technology business and the size and growth of the global technology fee pool, we see the sector as an area of continued revenue growth.

4 Jefferies Financial Group Inc. Annual Report 2019

As with our technology business, we have invested heavily over the last several years in expanding our European Investment Banking effort. In 2019, this investment began to bear fruit, as Jefferies achieved record Investment Banking results in Europe, with net revenues increasing over 25% in 2019 against a backdrop of a 15% decline in European investment banking fees. Our growth in Europe has been driven primarily by our M&A business, which grew by almost 60%. An important part of this growth was our success in advising on $1 billion+ transactions, which accounted for almost half of our 2019 European M&A revenue. Looking ahead, we expect our growth in Europe to benefit from recent significant Managing Director additions across Industrials, Real Estate, Gaming and Lodging, Consumer, Energy and in U.K. M&A, and also from our recent expansion in Germany.

Berkadia, our commercial real estate finance and investment sales 50/50 joint venture with Berkshire Hathaway, delivered $198 million of pre-tax income and a record $191 million of cash earnings for the year ended November 30, 2019. Strong debt origination and additional third-party loan servicing arrangements increased our servicing portfolio to $277 billion. Our servicing portfolio is at its highest level since the acquisition of Berkadia. During the year, Berkadia placed a record $26.4 billion of debt for its clients, up over 3% compared to 2018. Similarly, investment sales volumes also set a record, up almost 8% from the prior year, totaling $8.9 billion, with 37% of investment sales volume resulting in a debt placement for Berkadia. Berkadia continues to develop their existing network of mortgage bankers and investment sales advisors, as well as recruiting new members to the team to target underserved markets. The growing servicing portfolio and sales network position Berkadia for continued success.

Equities

In Equities, we recorded 2019 net revenues of $774 million, a record year and an increase of 16% from the prior year, as growth in our core equities business reflected strong performance across most businesses. We continued to gain global market share through intense client focus, enhanced capabilities and the momentum across the overall Jefferies platform. We have considerably diversified the Equities business, with non-cash products and international markets representing a larger portion of our Equities net revenues. While continuing to absorb the effects of MiFID II and general market uncertainty, Jefferies has improved its market positioning and competitive ranking, with many of our businesses being ranked within the top 10 and several being market-leading. Our prime brokerage business continues to make strong progress, with a differentiated offering that is appealing to a range of hedge fund clients.

Fixed Income

Fixed Income net revenues totaled $681 million for 2019, an increase of $121 million, or 22%, compared with net revenues of $560 million in 2018, primarily due to improving market conditions across almost all of Jefferies’ credit businesses. The investments made across these businesses led to increased client engagement and more consistent results, while we minimized increases in risk and balance sheet usage. Jefferies is gaining market share across the board with clients who count on us every day to source original alpha generating ideas and to provide liquidity in a complicated and ever-changing environment.

Asset Management

In last year’s letter, we expressed a view that our LAM business had completed its “start-up” phase and was moving to becoming a more stable contributor. This came true in 2019 as we benefited from a more diverse set of uncorrelated investments and participation in more varied fee streams.

Jefferies Financial Group Inc. Annual Report 2019 5

Our partnerships with George Weiss Associates and Schonfeld Strategic Advisors are performing well, with strong prospects for growth in assets under management (“AUM”). During 2019, we launched, with their respective management teams, Stonyrock Partners (investing in equity stakes of high-quality, middle-market alternative asset managers) and Point Bonita Capital (trade finance), both in their initial phases of capital raising, and also absorbed Solanas Capital (investing in energy equities through a long/short ESG alternative strategy, a long/short infrastructure strategy and a long only Midstream strategy) and acquired a stake in Monashee Investment Management (capital markets new issues strategy). Stonyrock recently announced its first investment, a stake in Oak Hill Capital Partners, a leading middle-market private equity manager. Last month, we closed on the first over $300 million of third party AUM to be managed by Sikra Capital (catalyst driven European long/short equity strategy focused on mid-cap companies) and expect continued near-term growth in that strategy. We are also very pleased with the investor interest in the direct lending offering from our Jefferies Finance joint venture.

We expect all of these platforms to continue to grow and diversify our revenue. To support growth in AUM, we added seven new members and one returning member to our marketing team, more than doubling the size of this critical effort.

Given the growing importance of LAM, we are pleased to announce the appointment of Nick Daraviras and Sol Kumin as co-Presidents of LAM. Nick has been with Jefferies since 2001, most recently as a partner in Merchant Banking and with oversight of LAM as it has grown, and Sol joined LAM in 2018 to drive strategy and business development, having previously been CEO of Folger Hill.

Legacy Merchant Banking

As discussed above, 2019 was another year of progress in building and realizing the value of our legacy Merchant Banking portfolio. As demonstrated with the substantial gains realized in respect of National Beef and our earlier sales of Garcadia and Conwed, we have continued to build value in much of our Merchant Banking portfolio pending ultimate outcomes. In the case of National Beef, we realized in 2019 an aggregate of $396 million, or 57%, in excess of the estimated fair market value at the beginning of the year. The year-end fair value estimates for our remaining investments are below:

| As of November 30, 2019 | ||||||||||

| ($ Millions) | (Unaudited) Book Value |

Estimated Fair Value |

Basis for Fair Value Estimate | |||||||

| Oil and Gas (Vitesse and JETX) |

$ | 585 | $ | 732 | Income approach, market comparable and market transaction method | |||||

| Real Estate Assets (1) |

645 | 651 | Various | |||||||

| Linkem |

195 | 605 | Income approach, market comparable and market transaction method | |||||||

| Idaho Timber |

78 | 155 | Income approach, market comparable and market transaction method | |||||||

| FXCM |

129 | 134 | Income approach and market comparable method | |||||||

| The We Company |

54 | 54 | Market transaction method and option pricing theory | |||||||

| Investments in Public Companies |

179 | 179 | Mark-to-market (same for GAAP book value) | |||||||

| Other |

279 | 379 | Various | |||||||

|

|

|

|

|

|||||||

| Total Portfolio (2) |

$ | 2,144 | $ | 2,889 | ||||||

|

|

|

|

|

|||||||

| (1) | Primarily HomeFed |

| (2) | Does not include $228 million of investments held on behalf of Leucadia Asset Management |

6 Jefferies Financial Group Inc. Annual Report 2019

Annual Meeting and Investor Meeting

We look forward to answering your questions at our upcoming Annual Meeting on April 17, 2020. We also will hold our annual Jefferies Investor Meeting on October 15, 2020, at which time you will have the opportunity to hear from our senior leaders across the Jefferies platform. We thank all of you—our clients and customers, employee-partners, fellow shareholders, bondholders, vendors and all others associated with our businesses—for your continued partnership and support.

Sincerely,

|

| |

| Richard B. Handler Chief Executive Officer |

Brian P. Friedman President | |

Jefferies Financial Group Inc. Annual Report 2019 7

Appendix

The following tables reconcile financial results reported in accordance with generally accepted accounting principles (“GAAP”) to non-GAAP financial results. The shareholders’ letter contains non-GAAP financial information to aid investors in viewing our businesses and investments through the eyes of management while facilitating a comparison across historical periods. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, reported results prepared in accordance with GAAP.

Note: Berkadia is not consolidated by Jefferies Financial Group and is accounted for under the equity method. The Berkadia reconciliation below is provided for convenience only.

Jefferies Group

The Investment Banking Net Revenues since 1990 table comes from as reported numbers in Jefferies Group public filings and press releases. Excludes predecessor first quarter ending February 28, 2013. Investment Banking Revenues for the excluded quarter totaled $288 million. In the first quarter of 2018, we made changes to the presentation of our “Revenues by Source” to better align the manner in which we describe and present the results of our performance with the manner in which we manage our business activities and serve our clients. For a further discussion of these changes, see Jefferies Group LLC’s Form 8-K filed on March 20, 2018. We have presented fiscal years 2016 and 2017 to reflect results on a comparable basis, as reported in Jefferies Group public filings. Periods prior to fiscal 2016 do not reflect these “Revenues by Source” changes to the presentation.

8 Jefferies Financial Group Inc. Annual Report 2019

Cautionary Note on Forward-Looking Statements

This letter contains “forward-looking statements” within the meaning of the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Act of 1934. Forward-looking statements include statements about our future and statements that are not historical facts. These forward-looking statements are usually preceded by the words “should,” “expect,” “intend,” “may,” “will,” or similar expressions. Forward-looking statements may contain expectations regarding revenues, earnings, operations, and other results, and may include statements of future performance, plans, and objectives. Forward-looking statements also include statements pertaining to our strategies for future development of our businesses and products. Forward-looking statements represent only our belief regarding future events, many of which by their nature are inherently uncertain. It is possible that the actual results may differ, possibly materially, from the anticipated results indicated in these forward-looking statements. Information regarding important factors, including Risk Factors that could cause actual results to differ, perhaps materially, from those in our forward-looking statements is contained in reports we file with the SEC. You should read and interpret any forward-looking statement together with reports we file with the SEC.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable or equal the corresponding indicated performance level(s).

Jefferies Financial Group Inc. Annual Report 2019 9