Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - PROGRESS SOFTWARE CORP /MA | q42018exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - PROGRESS SOFTWARE CORP /MA | q42018exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - PROGRESS SOFTWARE CORP /MA | q42018exhibit311.htm |

| EX-23.1 - EXHIBIT 23.1 - PROGRESS SOFTWARE CORP /MA | q42018exhibit231.htm |

| EX-21.1 - EXHIBIT 21.1 - PROGRESS SOFTWARE CORP /MA | q42018exhibit211.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended November 30, 2018

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from_______to_______.

Commission File Number: 0-19417

PROGRESS SOFTWARE CORPORATION

(Exact name of registrant as specified in its charter)

DELAWARE (State or other jurisdiction of incorporation or organization) | 04-2746201 (I.R.S. Employer Identification No.) | |

14 Oak Park

Bedford, Massachusetts 01730

(Address of Principal Executive Offices)

Telephone Number: (781) 280-4000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock $.01 par value | The NASDAQ Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ý | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||

Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

As of May 31, 2018 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of voting stock held by non-affiliates of the registrant was approximately $1,707,000,000.

As of January 17, 2019, there were 45,153,755 common shares outstanding.

Documents Incorporated By Reference

Certain information required in Items 10, 11, 12, 13 and 14 of Part III of this Annual Report on Form 10-K is incorporated by reference to our definitive Proxy Statement for our 2019 Annual Meeting of Stockholders to be filed pursuant to Regulation 14A (our “definitive Proxy Statement”).

PROGRESS SOFTWARE CORPORATION

FORM 10-K

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2018

INDEX

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Item 16. | ||

3

CAUTIONARY STATEMENTS

This Form 10-K, and other information provided by us or statements made by our directors, officers or employees from time to time, may contain statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other securities laws. Whenever we use words such as “believe,” “may,” “could,” “would,” “might,” “should,” “expect,” “intend,” “plan,” “estimate,” “target,” “anticipate” and negatives and derivatives of these or similar expressions, or when we make statements concerning future financial results, product offerings or other events that have not yet occurred, we are making forward-looking statements. These forward-looking statements are based upon our present intent, beliefs or expectations, but forward-looking statements are not guaranteed to occur and may not occur. Actual future results may differ materially from those contained in or implied by our forward-looking statements as a result of various factors. Such factors are more fully described in Item 1A of this Form 10-K under the heading “Risk Factors.” Although we have sought to identify the most significant risks to our business, we cannot predict whether, or to what extent, any of such risks may be realized. We also cannot assure you that we have identified all possible issues which we might face. We undertake no obligation to update any forward-looking statements that we make.

PART I

Item 1. Business

Overview

Progress Software Corporation ("Progress," the "Company," "we," "us," or "our") offers the leading platform for developing and deploying strategic business applications. We enable customers and partners to deliver modern, high-impact digital experiences with a fraction of the effort, time and cost. Progress offers powerful tools for easily building adaptive user experiences across any type of device or touchpoint, award-winning machine learning that enables cognitive capabilities to be a part of any application, the flexibility of a serverless cloud to deploy modern apps, business rules, web content management, plus leading data connectivity technology. Over 1,700 independent software vendors ("ISVs"), 100,000 enterprise customers, and 2 million developers rely on Progress to power their applications.

Our products are generally sold as perpetual licenses, but certain products also use term licensing models and our cloud-based offerings use a subscription based model. More than half of our worldwide license revenue is realized through relationships with indirect channel partners, principally application partners and original equipment manufacturers ("OEMs"). These ISVs develop and market applications using our technology and resell our products in conjunction with sales of their own products that incorporate our technology.

We operate in North America and Latin America (the "Americas"); Europe, the Middle East and Africa ("EMEA"); and the Asia Pacific region, through local subsidiaries as well as independent distributors.

Fiscal Year 2018 Highlights

The key tenets of our strategic plan and operating model are as follows:

Align Resources to Drive Profitability. Our organizational philosophy and operating principles focus primarily on customer and partner retention and success for our core products and a streamlined operating approach in order to more efficiently drive revenue.

Protect and Strengthen Our Core Business. A key element of our strategy is centered on providing the platform and tools enterprises need to build “cognitive applications,” which we believe are the future of application development. We offer this platform to both new customers and partners as well as our existing partner and customer ecosystems. Our platform for cognitive applications enables developers to build the most modern applications quickly and easily, and includes:

• | our leading UI development tools, which enable organizations to easily build engaging user interfaces for any device or front end; |

• | our NativeScript offering, which allows developers to use JavaScript to build native applications across multiple mobile platforms; |

• | our modern high productivity application development platform, Progress Kinvey, that is cloud-native, is secure, high-performing, and highly-scalable while supporting all modern user interfaces; |

• | automated and intuitive machine learning capabilities for accelerating the creation and delivery of cognitive applications; |

4

• | our data connectivity and integration capabilities; |

• | our business logic and rules capabilities; and |

• | web content management for delivering personalized and engaging digital experiences |

This strategy builds on our inherent DNA and our vast experience in application development that we’ve acquired over the past 35 years.

Holistic Capital Allocation Approach. Pursuant to our capital allocation strategy, we have targeted to return approximately 75-80% of our annual cash flows from operations to stockholders in the form of share repurchases and through dividends. We have also adopted a disciplined approach to future mergers and acquisitions. By adopting strict financial criteria for future acquisitions, these acquisitions will enable us to drive significant stockholder returns by providing scale and increased cash flows.

In fiscal 2018, we remained solidly on course with the execution of our strategic plan. Our budget and operating plan for 2018 reflected our focus on managing our business as efficiently as possible. Through our sustained focus on running lean operationally, we succeeded in reducing our expenses by almost $40 million over the past two years. Further, our strategy is producing tangible benefits for stockholders. The strength of our overall business enabled us to return over $145 million of capital to stockholders in fiscal 2018 in the form of share repurchases and dividends as described below.

Share Repurchase Authorization

In September 2017, our Board of Directors increased our total share repurchase authorization to $250.0 million. In fiscal year 2018, we repurchased and retired 2.9 million shares of our common stock for $120.0 million. As of November 30, 2018, there was $100.0 million remaining under this current authorization. We intend to repurchase $100 million in shares of our common stock in fiscal year 2019. However, the timing and amount of any shares repurchased will be determined by management based on its evaluation of market conditions and other factors, and we may choose to suspend, expand or discontinue the repurchase program at any time.

Dividend Declaration

On September 21, 2018, our Board of Directors approved an 11% increase to our quarterly cash dividend from $0.14 to $0.155 per share of common stock. We began paying quarterly cash dividends of $0.125 per share of common stock to Progress stockholders in December 2016 and increased the quarterly cash dividend to $0.14 per share in September 2017. We have declared aggregate per share quarterly cash dividends totaling $0.575, $0.515 and $0.125 for the years ended November 30, 2018, November 30, 2017 and November 30, 2016, respectively. We have paid aggregate cash dividends totaling $25.8 million, and $24.1 million for the years ended November 30, 2018 and November 30, 2017, respectively. We expect to continue paying quarterly cash dividends in subsequent quarters consistent with our capital allocation strategy. However, we may terminate or modify this program at any time.

Tax Reform

During the first quarter of fiscal year 2018, the Tax Cuts and Jobs Act (the "Act") was enacted in the United States. The Act reduces the U.S. federal corporate tax rate from 35% to 21% effective January 1, 2018, requires companies to pay a one-time transition tax on earnings of certain foreign subsidiaries that were previously tax deferred, and creates new taxes on certain foreign sourced earnings. Certain international provisions of the Act, including the provisions for global intangible low-taxed income and foreign-derived intangible income, will not become effective until fiscal year 2019. Refer to Note 14 to our Consolidated Financial Statements in Item 8 of this Form 10-K for additional information.

Our Business Segments

OpenEdge Business Segment

The OpenEdge business segment drives growth within OpenEdge’s large, diverse partner base by providing the technology enhancements and marketing support these partners need to sell more of their existing solutions to their customers. The OpenEdge business segment is also focused on providing partners and direct end users with a clear path to develop and integrate cloud-based applications in the future. Our professional services organization helps partners and customers leverage their core assets and develop strategies that protect current investments, while addressing changing business requirements.

5

The solutions within the OpenEdge business segment include:

Progress OpenEdge

Progress OpenEdge is development software for building dynamic multi-language applications for secure deployment across any platform, any device, and any cloud. OpenEdge provides a unified environment comprising development tools, application servers, application management tools, an embedded relational database management system, and the capability to connect and integrate with other applications and data sources independently or with other Progress products.

Progress Corticon

Progress Corticon is a market-leading Business Rules Management System that enables applications with decision automation, decision change process and decision-related insight capabilities. Corticon helps both business and IT users to quickly create or reuse business rules as well as create, improve, collaborate on, and maintain decision logic.

Progress Kinvey

Progress Kinvey is a modern platform for rapidly building complex enterprise applications and scalable consumer applications experiences. From mission-critical consumer and business experiences for global insurance, manufacturing and media companies, to HIPAA-compliant and life-critical apps for healthcare, health implant manufacturers and pharma.

NativeScript

NativeScript is an open-source application development platform that enables developers to use JavaScript to build cross-platform, native iOS and Android applications.

DataRPM

DataRPM offers an award-winning cognitive predictive maintenance solution for industrial IoT ("IIoT"). The patented platform automates predictive modeling, leveraging proprietary Meta Learning capabilities to increase quality, accuracy and timeliness of equipment failure predictions, leading to hundreds of millions of dollars in savings. The technology enables customers to predict and prevent asset failures, and increase yield and efficiencies to generate outcomes for IIoT.

Data Connectivity and Integration Business Segment

The Data Connectivity and Integration ("DCI") business segment is focused on the growth of our data assets, including the data integration components of our cloud offerings. Data is at the core of every application, and with the exponential growth in the number and volume of data sources, this business segment addresses the increasingly complex challenges that organizations have in accessing and integrating that data.

The solutions within the DCI business segment include:

Progress DataDirect Connect

Progress DataDirect Connect software provides data connectivity using industry-standard interfaces to connect applications running on various platforms to any major database, for both corporate IT organizations and software vendors. With software components embedded in the products of over 350 software companies and in the applications of thousands of large enterprises, the DataDirect Connect product set is a global leader in the data connectivity market. The primary products, in addition to other drivers we have developed, are ODBC drivers, JDBC drivers and ADO.NET providers. They provide the capability to connect and integrate with other applications and data sources independently or with our cloud-based offerings.

Progress DataDirect Hybrid Data Pipeline

Progress DataDirect Hybrid Data Pipeline is a data access service that provides simple, secure access to organizations' cloud and on-premises data sources for hybrid cloud applications, such as CRM, data management platforms or hosted analytics. It enables developers to integrate applications and data quickly, no matter whether that data lives-on-site, in the cloud or both.

6

Application Development and Deployment Business Segment

The Application Development and Deployment ("AD&D") business segment is focused on serving the evolving needs of our substantial developer community, and on generating net new customers for our application development assets. This business segment has the focus and agility of a start-up, able to react quickly to changes in this rapidly-evolving market in order to meet the demands of developers who are seeking to increase their productivity and move toward the cloud.

The solutions within the AD&D business segment include:

DevTools

DevTools is a cross-platform, user experience design, quality assurance, debugging and reporting suite for next generation web, mobile, desktop and HTML5 applications that enables developers to focus on business logic and not infrastructure. Included in DevTools are Fiddler and Kendo UI.

Sitefinity

Sitefinity is a next-generation web content management and customer analytics platform for managing and optimizing digital experiences. Sitefinity combines superior end user experience with a high level of customization capabilities for developers.

Test Studio

Test Studio is an application lifecycle management suite for testing web, mobile and desktop applications that covers the process from idea to deployment.

Product Development

Most of our products have been developed by our internal product development staff or the internal staffs of acquired companies. We believe that the features and performance of our products are competitive with those of other available development and deployment tools and that none of the current versions of our products are approaching obsolescence. However, we believe that significant investments in new product development and continuing enhancements of our current products will be required for us to maintain our competitive position.

As of November 30, 2018, we have four development offices in North America, two primary development offices in India and one primary development office in EMEA. We spent $79.7 million, $77.0 million, and $88.6 million in fiscal years 2018, 2017 and 2016, respectively, on product development, including capitalized software development costs.

Customers

We market our products globally through several channels: directly to end users and indirectly to application partners (or ISVs), OEMs, and system integrators. Sales of our solutions and products through our direct sales force have historically been to business managers or IT managers in corporations and governmental agencies. We also target developers who create business applications, from individuals to teams, within enterprises of all sizes.

We also market our products through indirect channels, primarily application partners and OEMs who embed our products as part of an integrated solution. We use international distributors in certain locations where we do not have a direct presence or where it is more economically feasible for us to do so. More than half of our license revenues are derived from indirect channels.

Application Partners

Our application partners cover a broad range of markets, offer an extensive library of business applications and are a source of recurring revenue. We have kept entry costs, consisting primarily of the initial purchase of development licenses, low to encourage a wide variety of application partners to build applications. If an application partner succeeds in marketing its applications, we obtain recurring revenue as the application partner licenses our deployment products to allow its application to be installed and used by customers. In recent years, a significantly increasing amount of our revenue from application partners has been generated from subscriptions to application partners who have chosen to enable their business applications under a software-as-a-service ("SaaS") platform.

7

Original Equipment Manufacturers

We enter into arrangements with OEMs in which the OEM embeds our products into its solutions, typically either software or technology devices. OEMs typically license the right to embed our products into their solutions and distribute those solutions for initial terms ranging from one to three years. Historically, most of our OEMs have renewed their agreements upon the expiration of the initial term. However, there is no assurance that they will continue to renew in the future. If any of our largest OEM customers were not to renew their agreements in the future, this could materially impact our DCI segment.

No single customer or partner has accounted for more than 10% of our total revenue in any of our last three fiscal years.

Sales and Marketing

We sell our products and solutions through our direct sales force and indirect channel partners. We have sold our products and solutions to enterprises in over 180 countries. Our sales and field marketing groups are organized primarily by region. We operate by region in the Americas, EMEA and Asia Pacific. We believe this structure allows us to maintain direct contact with our customers and support their diverse market requirements. Our international operations provide focused local sales, support and marketing efforts and are able to respond directly to changes in local conditions.

In addition to our direct sales efforts, we distribute our products through systems integrators, resellers, distributors, and OEM partners in the United States and internationally. Systems integrators typically have expertise in vertical or functional markets. In some cases, they resell our products, bundling them with their broader service offerings. In other cases, they refer sales opportunities for our products to our direct sales force. Distributors sublicense our products and provide service and support within their territories. OEMs embed portions of our technology in their product offerings.

Sales personnel are responsible for developing new direct end user accounts, recruiting new indirect channel partners and new independent distributors, managing existing channel partner relationships and servicing existing customers. We actively seek to avoid conflict between the sales efforts of our application partners and our own direct sales efforts. We use our inside sales team to enhance our direct sales efforts and to generate new business and follow-on business from existing customers.

Our marketing personnel conduct a variety of marketing engagement programs designed to create demand for our products, enhance the market readiness of our products, raise the general awareness of our company and our products and solutions, generate leads for the sales organization and promote our various products. These programs include press relations, analyst relations, investor relations, digital/web marketing, marketing communications, participation in trade shows and industry conferences, and production of sales and marketing literature. We also hold and participate in global events, as well as regional user events in various locations throughout the world.

Our sales and marketing efforts with respect to certain of our products, including DevTools, differ from our traditional sales and marketing efforts because the target markets are different. For these products, we have designed our marketing and sales model to be efficient for high volumes of lower-price transactions. Our marketing efforts focus on driving traffic to our websites and on generating high quality sales leads, in many cases, consisting of developer end users who download a free evaluation of our software. Our sales efforts then focus on converting these leads into paying customers through a high volume, short duration, sales process. Of particular importance to our target market, we enable our customers to buy our products in a manner convenient to them, whether by purchase order, online with a credit card or through our channel partners.

Customer Support

Our customer support staff provides telephone and Web-based support to end users, application developers and OEMs. Customers may purchase maintenance services entitling them to software updates, technical support and technical bulletins. Maintenance is generally not required with our products and is purchased at the customer's option. We provide support to customers primarily through our main regional customer support centers in Bedford and Waltham, Massachusetts; Morrisville, North Carolina; Rotterdam, The Netherlands; Hyderabad, India; Melbourne, Australia; and Sofia, Bulgaria. Local technical support for specific products is provided in certain other countries as well.

8

Professional Services

Our global professional services organization delivers business solutions for customers through a combination of products, consulting and education. Our consulting organization offers project management, implementation services, custom development, programming and other services. Our consulting organization also provides services to Web-enable existing applications or to take advantage of the capabilities of new product releases. Our education organization offers numerous training options, from traditional instructor-led courses to advanced learning modules available via the web or on CDs.

Our services offerings include: application modernization; data management, managed database services; performance enhancements and tuning; and analytics/business intelligence.

Competition

The computer software industry is intensely competitive. We experience significant competition from a variety of sources with respect to all of our products. Factors affecting competition in the markets we serve include product performance in complex applications, breadth of application solutions, vendor experience, ease of integration, price, training and support.

We compete in various markets with a number of entities, such as salesforce.com, Inc., Amazon.com, Inc., Software AG, RedHat, Inc., Pivotal Software, Inc., Microsoft Corporation, Oracle Corporation and other smaller firms. Many of these vendors offer platform-as-a-service, application development, data integration and other tools in conjunction with their CRM, web services, operating systems and relational database management systems. We believe that IBM Corporation, Microsoft Corporation and Oracle Corporation currently dominate the relational database market. We do not believe that there is a dominant vendor in the other infrastructure software markets, including application development. Some of our competitors have greater financial, marketing or technical resources than we have and/or may have experience in, or be able to adapt more quickly to new or emerging technologies and changes in customer requirements or to devote greater resources to the development, promotion and sale of their products than we can. Increased competition could make it more difficult for us to maintain our revenue and market presence.

Copyrights, Trademarks, Patents and Licenses

We rely on a combination of contractual provisions and copyright, patent, trademark and trade secret laws to protect our proprietary rights in our products. We generally distribute our products under software license agreements that grant customers a perpetual nonexclusive license to use our products and contain terms and conditions prohibiting the unauthorized reproduction or transfer of our products. We also distribute our products through various channel partners, including application partners, OEMs and system integrators. We also license our products under term or subscription arrangements. In addition, we attempt to protect our trade secrets and other proprietary information through agreements with employees, consultants and channel partners. Although we intend to protect our rights vigorously, there is no assurance that these measures will be successful.

We seek to protect the source code of our products as trade secrets and as unpublished copyrighted works. We hold numerous patents covering portions of our products. We also have several patent applications for some of our other product technologies. Where possible, we seek to obtain protection of our product names and service offerings through trademark registration and other similar procedures throughout the world.

We believe that due to the rapid pace of innovation within our industry, factors such as the technological and creative skills of our personnel are as important in establishing and maintaining a leadership position within the industry as are the various legal protections of our technology. In addition, we believe that the nature of our customers, the importance of our products to them and their need for continuing product support may reduce the risk of unauthorized reproduction, although no assurances can be made in this regard.

Business Segment and Geographical Information

We operate and report as three distinct business segments: OpenEdge, Data Connectivity and Integration, and Application Development and Deployment. For additional information on our business segments as well as our geographical financial information, see Note 16 to our Consolidated Financial Statements in Item 8 of this Form 10-K.

9

Employees

As of November 30, 2018, we had 1,412 employees worldwide, including 408 in sales and marketing, 208 in customer support and services, 613 in product development and 183 in administration.

None of our U.S. employees are subject to a collective bargaining agreement. Employees in certain foreign jurisdictions are represented by local workers’ councils and/or collective bargaining agreements as may be customary or required in those jurisdictions. We have experienced no work stoppages and believe our relations with employees are good.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, including exhibits, and amendments to those reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge on our website at www.progress.com as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the SEC. The information posted on our website is not incorporated into this Annual Report.

Our Code of Conduct is also available on our website. Additional information about this code and amendments and waivers thereto can be found below in Part III, Item 10 of this Form 10-K.

10

Item 1A. Risk Factors

We operate in a rapidly changing environment that involves certain risks and uncertainties, some of which are beyond our control. The risks described below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially adversely affect our business, financial condition and/or operating results.

Our revenue and quarterly results may fluctuate, which could adversely affect our stock price. We have experienced, and may in the future experience, significant fluctuations in our quarterly operating results that may be caused by many factors. These factors include:

• | changes in demand for our products; |

• | introduction, enhancement or announcement of products by us or our competitors; |

• | market acceptance of our new products; |

• | the growth rates of certain market segments in which we compete; |

• | size and timing of significant orders; |

• | a high percentage of our revenue is generated in the third month of each fiscal quarter and any failure to receive, complete or process orders at the end of any quarter could cause us to fall short of our revenue targets; |

• | budgeting cycles of customers; |

• | mix of distribution channels; |

• | mix of products and services sold; |

• | mix of international and North American revenues; |

• | fluctuations in currency exchange rates; |

• | changes in the level of operating expenses; |

• | changes in management; |

• | restructuring programs; |

• | changes in our sales force; |

• | completion or announcement of acquisitions by us or our competitors; |

• | customer order deferrals in anticipation of new products announced by us or our competitors; and |

• | general economic conditions in regions in which we conduct business. |

Revenue forecasting is uncertain, and the failure to meet our forecasts could result in a decline in our stock price. Our revenues, particularly new software license revenues, are difficult to forecast. We use a pipeline system to forecast revenues and trends in our business. Our pipeline estimates may prove to be unreliable either in a particular quarter or over a longer period of time, in part because the conversion rate of the pipeline into contracts can be difficult to estimate and requires management judgment. A variation in the conversion rate could cause us to plan or budget incorrectly and materially adversely impact our business or our planned results of operations. Furthermore, most of our expenses are relatively fixed, including costs of personnel and facilities. Thus, an unexpected reduction in our revenue, or failure to achieve the anticipated rate of growth, would have a material adverse effect on our profitability. If our operating results do not meet our publicly stated guidance or the expectations of investors, our stock price may decline.

We recognize a substantial portion of our revenue from sales made through third parties, including our application partners, distributors/resellers, and OEMs, and adverse developments in the businesses of these third parties or in our relationships with them could harm our revenues and results of operations. Our future results depend in large part upon our continued successful distribution of our products through our application partner, distributor/reseller, and OEM channels. The activities of these third parties are not within our direct control. Our failure to manage our relationships with these third parties effectively could impair the success of our sales, marketing and support activities. A reduction in the sales efforts, technical capabilities or financial viability of these parties, a misalignment of interest between us and them, or a termination of our relationship with a major application partner, distributor/reseller, or OEM could have a negative effect on our sales and financial results. Any adverse effect on any of our application partners’, distributors'/resellers', or OEMs’ businesses related to competition, pricing and other factors could also have a material adverse effect on our business, financial condition and operating results.

Changes in accounting principles and guidance, or their interpretation or implementation, may materially adversely affect our reported results of operations or financial position. We prepare our consolidated financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”) These principles are subject to interpretation by the SEC and various bodies formed to create and interpret appropriate accounting principles and guidance. A change in these principles or guidance, or in their interpretations, may have a significant effect on our reported results, as well as our processes and related controls.

11

For example, in May 2014, the Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”). ASU 2014-09 outlines a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers and supersedes prior revenue recognition guidance, including industry-specific guidance. This new standard is both technical and complex. The Company adopted this ASU effective December 1, 2018 and will adjust prior period consolidated financial statements to reflect full retrospective adoption, beginning with our Quarterly Report on Form 10-Q for the first quarter of 2019. Management has substantially completed assessing the impact the adoption of this standard will have on the Company’s consolidated financial statements, which will have a material impact on our consolidated financial statements, including the way we account for arrangements involving our term licenses and perpetual licenses with maintenance and/or support. In connection with the adoption of ASU 2014-09, we are implementing new processes, systems and internal controls. Such changes and any difficulties implementing such changes could materially adversely affect our reported financial results, our ability to comply with regulatory reporting requirements, and the effectiveness of our internal controls over financial reporting. For a discussion of the potential impact that the implementation of ASU 2014-09 is expected to have on our consolidated financial statements and related disclosures, see the “Recent Accounting Pronouncements” section in this Form 10-K.

A failure of our information technology systems, including the implementation of our new financial systems platform, could have a material adverse effect on our business. A failure or prolonged interruption in our information technology systems, or any difficulty encountered in upgrading our systems or implementing new systems, that compromises our ability to meet our customers’ needs, or impairs our ability to record, process and report accurate information could have a material adverse effect on our financial condition.

We are in the process of implementing a new financial systems platform which will assist with the collection, storage, management and interpretation of data from our business activities to support future growth and to integrate significant processes. Our financial systems platform is critical to our ability to accurately maintain books and records, record transactions, provide important information to our management and prepare our consolidated financial statements. Financial systems platform implementations are complex and time-consuming and involve significant expenditures on system software and implementation activities, as well as changes in business processes.

As part of the implementation of our new financial systems platform, certain changes to our processes and procedures have and will continue to occur. These changes will result in changes to our internal control over financial reporting. This new platform is designed to strengthen our internal financial controls by automating certain manual processes and standardizing business processes and reporting across our organization. However, any disruptions, delays or deficiencies in the design and implementation of a new financial systems platform could adversely affect our ability to operate our business. Additionally, if the new platform does not operate as intended, the effectiveness of our internal control over financial reporting could be adversely affected or our ability to assess it adequately could be further impacted.

Weakness in the U.S. and international economies may result in fewer sales of our products and may otherwise harm our business. We are subject to risks arising from adverse changes in global economic conditions, especially those in the U.S., Europe and Latin America. If global economic conditions weaken, credit markets tighten and/or financial markets become unstable, customers may delay, reduce or forego technology purchases, both directly and through our application partners and OEMs. This could result in reductions in sales of our products, longer sales cycles, slower adoption of new technologies and increased price competition. Further, deteriorating economic conditions could adversely affect our customers and their ability to pay amounts owed to us. Any of these events would likely harm our business, results of operations, financial condition or cash flows.

Our international operations expose us to additional risks, and changes in global economic and political conditions could adversely affect our international operations, our revenue and our net income. Approximately 45% of our total revenue is generated from sales outside North America. Political and/or financial instability, oil price shocks and armed conflict in various regions of the world can lead to economic uncertainty and may adversely impact our business. For example, the announcement of the Referendum of the United Kingdom’s (the "U.K.") Membership of the European Union ("E.U.") (referred to as "Brexit"), advising for the exit of the U.K. from the E.U., resulted in significant volatility in global stock markets and currency exchange rate fluctuations. If customers’ buying patterns, decision-making processes, timing of expected deliveries and timing of new projects unfavorably change due to economic or political conditions, there would be a material adverse effect on our business, financial condition and operating results.

Other potential risks inherent in our international business include:

• | longer payment cycles; |

12

• | credit risk and higher levels of payment fraud; |

• | greater difficulties in accounts receivable collection; |

• | varying regulatory and legal requirements; |

• | compliance with international and local trade, labor and export control laws; |

• | compliance with U.S. laws such as the Foreign Corrupt Practices Act, and local laws prohibiting bribery and corrupt payments to government officials; |

• | restrictions on the transfer of funds; |

• | difficulties in developing, staffing, and simultaneously managing a large number of varying foreign operations as a result of distance, legal impediments and language and cultural differences; |

• | reduced or minimal protection of intellectual property rights in some countries; |

• | laws and business practices that favor local competitors or prohibit foreign ownership of certain businesses; |

• | changes in U.S. or foreign trade policies or practices that increase costs or restrict the distribution of products; |

• | seasonal reductions in business activity during the summer months in Europe and certain other parts of the world; |

• | economic instability in emerging markets; and |

• | potentially adverse tax consequences. |

Any one or more of these factors could have a material adverse effect on our international operations, and, consequently, on our business, financial condition and operating results.

Fluctuations in foreign currency exchange rates could have an adverse impact on our financial condition and results of operations. Changes in the value of foreign currencies relative to the U.S. dollar could adversely affect our results of operations and financial position. For example, during periods in which the value of the U.S. dollar strengthens in comparison to certain foreign currencies, particularly in Europe, Brazil and Australia, our reported international revenue is reduced because foreign currencies translate into fewer U.S. dollars. As approximately one-third of our revenue is denominated in foreign currencies, our revenue results have been impacted, and we expect will continue to be impacted, by fluctuations in foreign currency exchange rates.

We seek to reduce our exposure to fluctuations in exchange rates by entering into foreign exchange forward contracts to hedge certain actual and forecasted transactions of selected currencies (mainly in Europe, Brazil, India and Australia). Our currency hedging transactions may not be effective in reducing any adverse impact of fluctuations in foreign currency exchange rates. Further, the imposition of exchange or price controls or other restrictions on the conversion of foreign currencies could have a material adverse effect on our business.

Technology and customer requirements evolve rapidly in our industry, and if we do not continue to develop new products and enhance our existing products in response to these changes, our business could be harmed. Ongoing enhancements to our product sets will be required to enable us to maintain our competitive position and the competitive position of our application partners, distributors/resellers, and OEMs. We may not be successful in developing and marketing enhancements to our products on a timely basis, and any enhancements we develop may not adequately address the changing needs of the marketplace. Overlaying the risks associated with our existing products and enhancements are ongoing technological developments and rapid changes in customer and partner requirements. Our future success will depend upon our ability to develop and introduce in a timely manner new products that take advantage of technological advances and respond to new customer and partner requirements. We may not be successful in developing new products incorporating new technology on a timely basis, and any new products we develop may not adequately address the changing needs of the marketplace or may not be accepted by the market. Failure to develop new products and product enhancements that meet market needs in a timely manner could have a material adverse effect on our business, financial condition and operating results.

We are substantially dependent on our Progress OpenEdge products. We derive a significant portion of our revenue from software license and maintenance revenue attributable to our Progress OpenEdge product set. Accordingly, our future results depend on continued market acceptance of OpenEdge. If new technologies emerge that are superior to, or are more responsive to customer requirements than, OpenEdge such that we are unable to maintain OpenEdge’s competitive position within its marketplace, our business, financial condition and operating results may be materially adversely affected.

We have made significant investments in furtherance of our cognitive applications strategy and these investments may not generate the revenues we expect, which could adversely affect our business and financial results. Our cognitive applications strategy is focused on providing the platform and tools enterprises need to build next generation applications that drive their businesses, known as “cognitive applications.” Beginning in 2017, we have made significant investments in furtherance of our cognitive applications strategy, including two acquisitions.

13

We cannot guarantee that our cognitive applications strategy is the right one or that we will be effective in executing this strategy. Our strategy may not succeed for a number of reasons, including, but not limited to: general economic risks, execution risks with acquisitions, competitiveness in and the dynamic nature of the markets in which we operate, execution risks around product development, market acceptance of new products and services and risks associated with the adoption of, and demand for, our model in general. If one or more of the foregoing risks were to materialize, our business, results of operations and ability to achieve sustained profitability could be adversely affected.

The increased emphasis on a cloud strategy may give rise to risks that could harm our business. We are devoting significant resources to the development of cloud-based technologies and service offerings where we have a limited operating history. Our cloud strategy requires continued investment in product development and cloud operations as well as a change in the way we price and deliver our products. Many of our competitors may have advantages over us due to their larger presence, larger developer network, deeper experience in the cloud-based computing market, and greater sales and marketing resources. It is uncertain whether these strategies will prove successful or whether we will be able to develop the infrastructure and business models more quickly than our competitors. Our cloud strategy may give rise to a number of risks, including the following:

• | if new or current customers desire only perpetual licenses, we may not be successful in selling subscriptions; |

• | although we intend to continue to support our perpetual license business, the increased emphasis on a cloud strategy may raise concerns among our installed customer base; |

• | we may be unsuccessful in achieving our target pricing; |

• | our revenues might decline over the short or long term as a result of this strategy; |

• | our relationships with existing partners that resell perpetual licenses may be damaged; |

• | increased risk of security breaches; and |

• | we may incur costs at a higher than forecasted rate as we enhance and expand our cloud operations. |

We may make additional acquisitions or investments in new businesses, products or technologies that involve additional risks, which could disrupt our business or harm our financial condition, results of operations or cash flows. We may make acquisitions of businesses or investments in companies that offer complementary products, services and technologies. Any acquisitions that we do complete involve a number of risks, including the risks of assimilating the operations and personnel of acquired companies, realizing the value of the acquired assets relative to the price paid, distraction of management from our ongoing businesses and potential product disruptions associated with the sale of the acquired company’s products. In addition, an acquisition may not further our business strategy as we expected, may not result in revenue growth to the degree we expected or at all or may not achieve expected synergies, any of which could adversely affect our business or operating results and potentially cause impairment to assets that we recorded as a part of an acquisition including intangible assets and goodwill. These factors could have a material adverse effect on our business, financial condition, operating results and cash flows. The consideration we pay for any future acquisitions could include our stock. As a result, future acquisitions could cause dilution to existing stockholders and to earnings per share.

The segments of the software industry in which we participate are intensely competitive, and our inability to compete effectively could harm our business. We experience significant competition from a variety of sources with respect to the marketing and distribution of our products. Many of our competitors have greater financial, marketing or technical resources than we do and may be able to adapt more quickly to new or emerging technologies and changes in customer requirements or to devote greater resources to the promotion and sale of their products than we can. Increased competition could make it more difficult for us to maintain our market presence or lead to downward pricing pressure.

In addition, the marketplace for new products is intensely competitive and characterized by low barriers to entry. For example, an increase in market acceptance of open source software may cause downward pricing pressures. As a result, new competitors possessing technological, marketing or other competitive advantages may emerge and rapidly acquire market share. In addition, current and potential competitors may make strategic acquisitions or establish cooperative relationships among themselves or with third parties, thereby increasing their ability to deliver products that better address the needs of our prospective customers. Current and potential competitors may also be more successful than we are in having their products or technologies widely accepted. We may be unable to compete successfully against current and future competitors, and our failure to do so could have a material adverse effect on our business, prospects, financial condition and operating results.

14

We rely on the experience and expertise of our skilled employees, and must continue to attract and retain qualified technical, marketing and managerial personnel in order to succeed. Our future success will depend in a large part upon our ability to attract and retain highly skilled technical, managerial, sales and marketing personnel. There is significant competition for such personnel in the software industry. We may not continue to be successful in attracting and retaining the personnel we require to develop new and enhanced products and to continue to grow and operate profitably.

Our periodic workforce restructurings can be disruptive. We have in the past restructured or made other adjustments to our workforce in response to management changes, product changes, performance issues, changes in strategy, acquisitions and other internal and external considerations. In the past, these restructurings have resulted in increased restructuring costs and have temporarily reduced productivity. These effects could recur in connection with any future restructurings or we may not achieve or sustain the expected growth or cost savings benefits of any such restructurings, or do so within the expected timeframe. As a result, our revenues and other results of operations could be negatively affected.

The loss of technology licensed from third parties could adversely affect our ability to deliver our products. We utilize certain technology that we license from third parties, including software that is integrated with internally developed software and used in our products to perform key functions. This technology, or functionally similar technology, may not continue to be available on commercially reasonable terms in the future, or at all. The loss of any significant third-party technology license could cause delays in our ability to deliver our products or services until equivalent technology is developed internally or equivalent third-party technology, if available, is identified, licensed and integrated.

Our business practices with respect to the collection, use and management of personal information could give rise to operational interruption, liabilities or reputational harm as a result of governmental regulation, legal requirements or industry standards relating to consumer privacy and data protection. As regulatory focus on privacy issues continues to increase and worldwide laws and regulations concerning the handling of personal information expand and become more complex, potential risks related to data collection and use within our business will intensify. For example, the E.U. and the United States ("U.S.") formally entered into a new framework in July 2016 that provides a mechanism for companies to transfer data from E.U. member states to the U.S. This new framework, called the Privacy Shield, is intended to address shortcomings identified by the Court of Justice of the E.U. in the previous E.U.-U.S. Safe Harbor Framework, which the Court of Justice invalidated in October 2015. The Privacy Shield and other data transfer mechanisms are likely to be reviewed by the European courts, which may lead to uncertainty about the legal basis for data transfers to the U.S. or interruption of such transfers. In the event any court blocks transfers to or from a particular jurisdiction on the basis that no transfer mechanisms are legally adequate, this could give rise to operational interruption in the performance of services for customers and internal processing of employee information, regulatory liabilities or reputational harm. In addition, U.S. and foreign governments have enacted or are considering enacting legislation or regulations, or may in the near future interpret existing legislation or regulations, in a manner that could significantly impact our ability and the ability of our customers and data partners to collect, augment, analyze, use, transfer and share personal and other information that is integral to certain services we provide.

Regulators globally are also imposing greater monetary fines for privacy violations. For example, in 2016, the E.U. adopted a new law governing data practices and privacy called the General Data Protection Regulation (GDPR), which became effective in May 2018. The law establishes new requirements regarding the handling of personal data. Non-compliance with the GDPR may result in monetary penalties of up to 4% of worldwide revenue. The GDPR and other changes in laws or regulations associated with the enhanced protection of certain types of sensitive data, such as healthcare data or other personal information, could greatly increase our cost of providing our products and services or even prevent us from offering certain services in jurisdictions that we operate.

Additionally, public perception and standards related to the privacy of personal information can shift rapidly, in ways that may affect our reputation or influence regulators to enact regulations and laws that may limit our ability to provide certain products. Any failure, or perceived failure, by us to comply with U.S. federal, state, or foreign laws and regulations, including laws and regulations regulating privacy, data security, or consumer protection, or other policies, public perception, standards, self-regulatory requirements or legal obligations, could result in lost or restricted business, proceedings, actions or fines brought against us or levied by governmental entities or others, or could adversely affect our business and harm our reputation.

If our products contain software defects or security flaws, it could harm our revenues and expose us to litigation. Our products, despite extensive testing and quality control, may contain defects or security flaws, especially when we first introduce them or when new versions are released. We may need to issue corrective releases of our software products to fix any defects or errors. The detection and correction of any security flaws can be time consuming and costly. Errors in our software products could affect the ability of our products to work with other hardware or software products, delay the development or release of new products or new versions of products, adversely affect market acceptance of our products and expose us to potential

15

litigation. If we experience errors or delays in releasing new products or new versions of products, such errors or delays could have a material adverse effect on our revenue.

We could incur substantial cost in protecting our proprietary software technology or if we fail to protect our technology, which would harm our business. We rely principally on a combination of contract provisions and copyright, trademark, patent and trade secret laws to protect our proprietary technology. Despite our efforts to protect our proprietary rights, unauthorized parties may attempt to copy aspects of our products or to obtain and use information that we regard as proprietary. Policing unauthorized use of our products is difficult. Litigation may be necessary in the future to enforce our intellectual property rights, to protect our trade secrets or to determine the validity and scope of the proprietary rights of others. This litigation could result in substantial costs and diversion of resources, whether or not we ultimately prevail on the merits. The steps we take to protect our proprietary rights may be inadequate to prevent misappropriation of our technology; moreover, others could independently develop similar technology.

We could be subject to claims that we infringe intellectual property rights of others, which could harm our business, financial condition, results of operations or cash flows. Third parties could assert infringement claims in the future with respect to our products and technology, and such claims might be successful. Litigation relating to any such claims could result in substantial costs and diversion of resources, whether or not we ultimately prevail on the merits. Any such litigation could also result in our being prohibited from selling one or more of our products, unanticipated royalty payments, reluctance by potential customers to purchase our products, or liability to our customers and could have a material adverse effect on our business, financial condition, operating results and cash flows.

If our security measures are breached, our products and services may be perceived as not being secure, customers may curtail or stop using our products and services, and we may incur significant legal and financial exposure. Our products and services involve the storage and transmission of our customers’ proprietary information and may be vulnerable to unauthorized access, computer viruses, cyber-attacks, distributed denial of service attacks and other disruptive problems Due to the actions of outside parties, employee error, malfeasance, or otherwise, an unauthorized party may obtain access to our data or our customers’ data, which could result in its theft, destruction or misappropriation. Security risks in recent years have increased significantly given the increased sophistication and activities of hackers, organized crime, including state-sponsored organizations and nation-states, and other outside parties. Cyber threats are continuously evolving, increasing the difficulty of defending against them. While we have implemented security procedures and controls to address these threats, our security measures could be compromised or could fail. Any security breach or unauthorized access could result in significant legal and financial exposure, increased costs to defend litigation, indemnity and other contractual obligations, government fines and penalties, damage to our reputation and our brand, and a loss of confidence in the security of our products and services that could potentially have an adverse effect on our business and results of operations. Breaches of our network could disrupt our internal systems and business applications, including services provided to our customers. Additionally, data breaches could compromise technical and proprietary information, harming our competitive position. We may need to spend significant capital or allocate significant resources to ensure effective ongoing protection against the threat of security breaches or to address security related concerns. If an actual or perceived breach of our security occurs, the market perception of the effectiveness of our security measures could be harmed and we could lose customers. In addition, our insurance coverage may not be adequate to cover all costs related to cybersecurity incidents and the disruptions resulting from such events.

We may have exposure to additional tax liabilities. As a multinational corporation, we are subject to income taxes in the U.S. and various foreign jurisdictions. Significant judgment is required in determining our global provision for income taxes and other tax liabilities. In the ordinary course of a global business, there are many intercompany transactions and calculations where the ultimate tax determination is uncertain. Our income tax returns are routinely subject to audits by tax authorities. Although we regularly assess the likelihood of adverse outcomes resulting from these examinations to determine our tax estimates, a final determination of tax audits that is inconsistent with such assessments or tax disputes could have an adverse effect on our financial condition, results of operations and cash flows.

We are also subject to non-income taxes, such as payroll, sales, use, value-added, net worth, property and goods and services taxes in the U.S. and various foreign jurisdictions. We are regularly under audit by tax authorities with respect to these non-income taxes and may have exposure to additional non-income tax liabilities, which could have an adverse effect on our results of operations, financial condition and cash flows.

In addition, our future effective tax rates could be favorably or unfavorably affected by changes in tax rates, changes in the valuation of our deferred tax assets or liabilities, or changes in tax laws or their interpretation. Such changes could have a material adverse impact on our financial results.

16

We are required to comply with certain financial and operating covenants under our credit facility and to make scheduled debt payments as they become due; any failure to comply with those covenants or to make scheduled payments could cause amounts borrowed under the facility to become immediately due and payable or prevent us from borrowing under the facility. In November 2017, we entered into an amended and restated credit agreement, which consists of a $123.8 million term loan and a $150.0 million revolving loan (which may be increased by an additional $125.0 million if the existing or additional lenders are willing to make such increased commitments). This facility matures in November 2022, at which time any amounts outstanding will be due and payable in full. We may wish to borrow additional amounts under the facility in the future to support our operations, including for strategic acquisitions and share repurchases.

We are required to comply with specified financial and operating covenants and to make scheduled repayments of our term loan, which may limit our ability to operate our business as we otherwise might operate it. Our failure to comply with any of these covenants or to meet any payment obligations under the facility could result in an event of default which, if not cured or waived, would result in any amounts outstanding, including any accrued interest and unpaid fees, becoming immediately due and payable. We might not have sufficient working capital or liquidity to satisfy any repayment obligations in the event of an acceleration of those obligations. In addition, if we are not in compliance with the financial and operating covenants at the time we wish to borrow funds, we will be unable to borrow funds.

Our annual operating cash flows may not be sufficient to enable us to meet our targeted capital allocation policy, which could decrease our investors expected return on investment in Progress stock. In September 2017, we announced a new capital allocation strategy in which we are targeting to return approximately 75-80% of annual cash flows from operations to stockholders through share repurchases and through dividends. Meeting these targets requires us to generate consistent cash flow and have available capital in an amount sufficient to enable us to continue investing in our business. We may not meet these targets if we do not generate the operating cash flows we expect, if we use our available cash to satisfy other priorities, if we have insufficient funds available to make such repurchases and/or dividends or if we are unable to borrow funds under our credit facility.

Our common stock price may continue to be volatile, which could result in losses for investors. The market price of our common stock, like that of other technology companies, is volatile and is subject to wide fluctuations in response to quarterly variations in operating results, announcements of technological innovations or new products by us or our competitors, changes in financial estimates by securities analysts or other events or factors. Our stock price may also be affected by broader market trends unrelated to our performance. As a result, purchasers of our common stock may be unable at any given time to sell their shares at or above the price they paid for them.

Item 1B. Unresolved Staff Comments

As of the date of this report, we do not have any open comments from the SEC related to our financial statements or periodic filings with the SEC.

Item 2. Properties

We own our principal administrative, sales, support, marketing, product development and distribution facilities, which are located in three buildings totaling approximately 258,000 square feet in Bedford, Massachusetts. As of November 30, 2018, we reclassified two of these buildings from property and equipment to assets held for sale. For further discussion, refer to Note 5 to our Consolidated Financial Statements in Item 8 of this Form 10-K.

We also maintain offices in leased facilities in various other locations in North America and outside North America, including Australia, Bulgaria, Germany, India, Netherlands, and the U.K. The terms of our leases generally range from one to seven years. We believe that our facilities are adequate for our current needs and that suitable additional space will be available as needed.

Item 3. Legal Proceedings

We are subject to various legal proceedings and claims, either asserted or unasserted, which arise in the ordinary course of business. While the outcome of these claims cannot be predicted with certainty, management does not believe that the outcome of any of these legal matters will have a material effect on our consolidated financial position, results of operations or cash flows.

17

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The following table sets forth, for the periods indicated, the range of high and low sale prices for our common stock. Our common stock trades on the NASDAQ Global Select Market under the symbol "PRGS".

Fiscal Year Ended | |||||||||||||||

November 30, 2018 | November 30, 2017 | ||||||||||||||

High | Low | High | Low | ||||||||||||

First quarter | $ | 53.60 | $ | 40.20 | $ | 32.47 | $ | 27.16 | |||||||

Second quarter | 47.21 | 35.63 | 30.70 | 27.46 | |||||||||||

Third quarter | 41.25 | 34.72 | 33.89 | 28.63 | |||||||||||

Fourth quarter | 43.07 | 30.23 | 42.97 | 33.23 | |||||||||||

On September 21, 2018, our Board of Directors approved an 11% increase to our quarterly cash dividend from $0.14 to $0.155 per share of common stock. We began paying quarterly cash dividends of $0.125 per share of common stock to Progress stockholders in December 2016 and increased the quarterly cash dividend to $0.14 per share in September 2017. On January 8, 2019, our Board of Directors declared a quarterly dividend of $0.155 per share of common stock that will be paid on March 15, 2019 to stockholders of record as of the close of business on March 1, 2019.

As of December 31, 2018, our common stock was held by approximately 158 stockholders of record.

In September 2017, our Board of Directors increased our total share repurchase authorization to $250.0 million. In fiscal years 2018 and 2017, we repurchased and retired 2.9 million shares of our common stock for $120.0 million and 2.2 million shares of our common stock for $73.9 million, respectively. As of November 30, 2018, there was $100.0 million remaining under this current authorization.

Stock Repurchases

Information related to the repurchases of our common stock by month in the fourth quarter of fiscal year 2018 is as follows (in thousands, except per share and share data):

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet be Purchased Under the Plans or Programs (1) | ||||||||||

September 2018 | 240,998 | $ | 41.47 | 240,998 | $ | 100,000 | ||||||||

October 2018 | — | — | — | 100,000 | ||||||||||

November 2018 | — | — | — | 100,000 | ||||||||||

Total | 240,998 | $ | 41.47 | 240,998 | $ | 100,000 | ||||||||

(1) | In September 2017, our Board of Directors increased our total share repurchase authorization to $250.0 million. As of November 30, 2018, there was $100.0 million remaining under this authorization, which expires at the end of fiscal year 2019. |

18

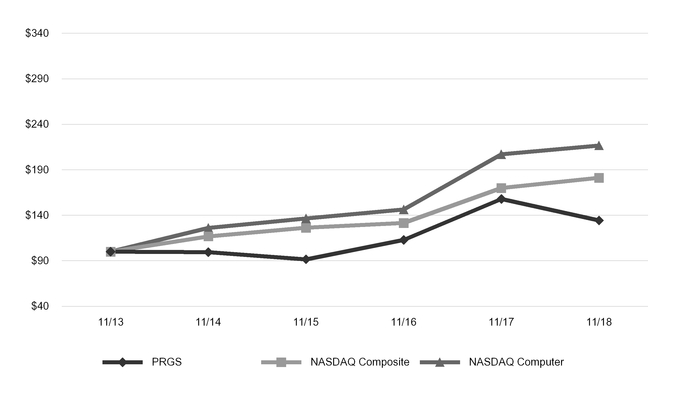

Stock Performance Graph and Cumulative Total Return

The graph below compares the cumulative total stockholder return on our common stock with the cumulative total return on the NASDAQ Composite Index and the NASDAQ Computer Index for each of the last five fiscal years ended November 30, 2018, assuming an investment of $100 at the beginning of such period and the reinvestment of any dividends.

Comparison of 5 Year Cumulative Total Return(1)

Among Progress Software Corporation, the NASDAQ Composite Index and the

NASDAQ Computer Index

(1) $100 invested on November 30, 2013 in stock or index, including reinvestment of dividends.

November 30, | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | ||||||||||||||||||

Progress Software Corporation | $ | 100.00 | $ | 99.50 | $ | 91.60 | $ | 112.91 | $ | 157.85 | $ | 134.25 | ||||||||||||

NASDAQ Composite | 100.00 | 116.86 | 126.29 | 131.60 | 169.93 | 181.21 | ||||||||||||||||||

NASDAQ Computer | 100.00 | 126.19 | 136.47 | 146.37 | 207.00 | 216.75 | ||||||||||||||||||

19

Item 6. Selected Financial Data

The following table sets forth selected financial data for the last five fiscal years (in thousands, except per share data):

Year Ended November 30, | 2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||||

Revenue | $ | 397,165 | $ | 397,572 | $ | 405,341 | $ | 377,554 | $ | 332,533 | ||||||||||

Income (loss) from operations | 85,998 | 70,614 | (29,709 | ) | 14,754 | 80,740 | ||||||||||||||

Net income (loss) | 63,491 | 37,417 | (55,726 | ) | (8,801 | ) | 49,458 | |||||||||||||

Basic earnings (loss) per share from continuing operations | 1.39 | 0.78 | (1.13 | ) | (0.17 | ) | 0.97 | |||||||||||||

Diluted earnings (loss) per share from continuing operations | 1.38 | 0.77 | (1.13 | ) | (0.17 | ) | 0.96 | |||||||||||||

Cash dividends declared per common share | 0.575 | 0.515 | 0.125 | — | — | |||||||||||||||

Cash, cash equivalents and short-term investments | 139,513 | 183,609 | 249,754 | 241,279 | 283,268 | |||||||||||||||

Total assets | 640,609 | 718,718 | 754,827 | 877,123 | 702,756 | |||||||||||||||

Long-term debt, net, including current portion | 116,089 | 121,909 | 135,000 | 144,375 | — | |||||||||||||||

Shareholders’ equity | 310,082 | 376,084 | 406,629 | 522,464 | 543,245 | |||||||||||||||

Fiscal year 2016 amounts have been impacted by a $92.0 million impairment charge related to the goodwill of the Application Development and Deployment reporting unit. Refer to Note 6 to our Consolidated Financial Statements in Item 8 of this Form 10-K for additional details.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

Certain statements below about anticipated results and our products and markets are forward-looking statements that are based on our current plans and assumptions. Important information about the bases for these plans and assumptions and factors that may cause our actual results to differ materially from these statements is contained below and in Item 1A. “Risk Factors” of this Annual Report on Form 10-K.

Use of Constant Currency

Revenue from our international operations has historically represented a substantial portion of our total revenue. As a result, our revenue results have been impacted, and we expect will continue to be impacted, by fluctuations in foreign currency exchange rates. For example, if the local currencies of our foreign subsidiaries strengthen, our consolidated results stated in U.S. dollars are positively impacted.

As exchange rates are an important factor in understanding period to period comparisons, we believe the presentation of revenue growth rates on a constant currency basis enhances the understanding of our revenue results and evaluation of our performance in comparison to prior periods. The constant currency information presented is calculated by translating current period results using prior period weighted average foreign currency exchange rates. These results should be considered in addition to, not as a substitute for, results reported in accordance with GAAP.

Overview

Progress Software Corporation ("Progress," the "Company," "we," "us," or "our") offers the leading platform for developing and deploying strategic business applications. We enable customers and partners to deliver modern, high-impact digital experiences with a fraction of the effort, time and cost. Progress offers powerful tools for easily building adaptive user experiences across any type of device or touchpoint, award-winning machine learning that enables cognitive capabilities to be a part of any application, the flexibility of a serverless cloud to deploy modern apps, business rules, web content management, plus leading data connectivity technology. Over 1,700 ISVs, 100,000 enterprise customers, and 2 million developers rely on Progress to power their applications. We operate as three distinct segments: OpenEdge, Data Connectivity and Integration, and Application Development and Deployment.

The key tenets of our strategic plan and operating model are as follows:

20

Align Resources to Drive Profitability. Our organizational philosophy and operating principles focus primarily on customer and partner retention and success for our core products and a streamlined operating approach in order to more efficiently drive revenue.