Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - FULLER H B CO | ex_133137.htm |

| EX-32.2 - EXHIBIT 32.2 - FULLER H B CO | ex_133140.htm |

| EX-32.1 - EXHIBIT 32.1 - FULLER H B CO | ex_133139.htm |

| EX-31.2 - EXHIBIT 31.2 - FULLER H B CO | ex_133138.htm |

| EX-24 - EXHIBIT 24 - FULLER H B CO | ex_133147.htm |

| EX-23 - EXHIBIT 23 - FULLER H B CO | ex_133136.htm |

| EX-21 - EXHIBIT 21 - FULLER H B CO | ex_133144.htm |

| EX-18 - EXHIBIT 18 - FULLER H B CO | ex_133165.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 1, 2018

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission file number: 001-09225

H.B. FULLER COMPANY

(Exact name of registrant as specified in its charter)

|

Minnesota |

41-0268370 |

|

|

(State or other jurisdiction of |

(I.R.S. Employer | |

|

incorporation or organization) |

Identification No.) | |

|

1200 Willow Lake Boulevard, St. Paul, Minnesota |

55110-5101 | |

|

(Address of principal executive offices) |

(Zip Code) | |

|

Registrant’s telephone number, including area code: (651) 236-5900 |

||

|

Securities registered pursuant to Section 12(b) of the Act: |

||

|

Title of each class |

Name of each exchange on which registered | |

|

Common Stock, par value $1.00 per share |

New York Stock Exchange | |

|

Preferred Stock Purchase Rights |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: none

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [X] Yes [ ] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to the Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” or “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [X] Accelerated filer [ ]

Non-accelerated filer [ ] Smaller reporting company [ ]

Emerging growth company [ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [X] No

The aggregate market value of the Common Stock, par value $1.00 per share, held by non-affiliates of the registrant as of June 1, 2018 was approximately $2,601,453,076 (based on the closing price of such stock as quoted on the New York Stock Exchange of $51.84 on such date).

The number of shares outstanding of the Registrant’s Common Stock, par value $1.00 per share, was 50,767,021 as of January 22, 2019.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference to portions of the registrant’s Proxy Statement for the Annual Meeting of Shareholders to be held on April 4, 2019.

H.B. FULLER COMPANY

2018 Annual Report on Form 10-K

|

Item 1. |

3 | |

|

Item 1A. |

7 | |

|

Item 1B. |

12 | |

|

Item 2. |

12 | |

|

Item 3. |

13 | |

|

Item 4. |

15 | |

|

Item 5. |

15 | |

|

Item 6. |

16 | |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 |

|

Item 7A. |

37 | |

|

Item 8. |

39 | |

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

92 |

|

Item 9A. |

92 | |

|

Item 9B. |

93 | |

|

Item 10. |

93 | |

|

Item 11. |

93 | |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

94 |

|

Item 13. |

Certain Relationships and Related Transactions and Director Independence |

94 |

|

Item 14. |

94 | |

|

Item 15. |

94 | |

|

Item 16. |

99 | |

|

|

Signatures | 100 |

H.B. Fuller Company was founded in 1887 and incorporated as a Minnesota corporation in 1915. Our stock is traded on the New York Stock Exchange (“NYSE”) under the ticker symbol FUL. As used herein, “H.B. Fuller”, “we”, “us”, “our”, “management” or “company” includes H.B. Fuller and its subsidiaries unless otherwise indicated. Where we refer to 2018, 2017 and 2016 herein, the reference is to our fiscal years ended December 1, 2018, December 2, 2017 and December 3, 2016, respectively.

We are a leading worldwide formulator, manufacturer and marketer of adhesives, sealants and other specialty chemical products. Sales operations span 34 countries in North America, Europe, Latin America, the Asia Pacific region, India, the Middle East and Africa. Industrial adhesives represent our core product offering. Customers use our adhesives products in manufacturing common consumer and industrial goods, including food and beverage containers, disposable diapers, windows, doors, flooring, roofing, appliances, sportswear, footwear, multi-wall bags, water filtration products, insulation, textiles, automobiles, recreational vehicles, buses, trucks and trailers, marine products, solar energy systems, electronics and products for the aerospace and defense industries. Our adhesives help improve the performance of our customers’ products or improve their manufacturing processes. We also provide our customers with technical support and unique solutions designed to address their specific needs. In addition, we have established a variety of product offerings for residential construction markets, such as tile-setting adhesives, grouts, sealants and related products.

Recent Acquisitions

Adecol

On November 1, 2017, we acquired Adecol Industria Quimica, Limitada (“Adecol”), headquartered in Guarulhos, Brazil. Adecol works with customers to develop innovative, high-quality hot melt, reactive and polymer-based adhesive solutions in the packaging, converting and durable assembly markets. The purchase price of $40.3 million was funded through borrowings on our revolving credit facility and existing cash and is reported in our Americas Adhesives operating segment.

Royal Adhesives

On October 20, 2017, we acquired Royal Adhesives and Sealants (“Royal Adhesives”), a manufacturer of high-value specialty adhesives and sealants. Royal Adhesives is a supplier of industrial adhesives in a diverse set of end markets, including aerospace, transportation, commercial roofing, insulating glass, solar, packaging and flooring applications and operates 19 manufacturing facilities in five countries. The purchase price of $1,620.3 million was funded through new debt financing. Royal Adhesives is included in multiple operating segments.

Wisdom Adhesives

On January 27, 2017, we acquired substantially all of the assets of H.E. Wisdom & Sons, Inc. and its affiliate Wisdom Adhesives Southeast, L.L.C., (“Wisdom Adhesives”) headquartered in Elgin, Illinois. Wisdom Adhesives is a provider of adhesives for the packaging, paper converting and durable assembly markets. The purchase price of $123.5 million was financed through borrowings on our revolving credit facility and is reported in our Americas Adhesives operating segment.

Non-U.S. Operations

The principal markets, products and methods of distribution outside the United States vary with each of our regional operations, generally maintaining integrated business units that contain dedicated supplier networks, manufacturing, logistics and sales organizations. The vast majority of the products sold within any region are produced within the region, and the respective regions do not import significant amounts of product from other regions. As of December 1, 2018, we had sales offices and manufacturing plants in 21 countries outside the United States and satellite sales offices in another 12 countries.

We have detailed Code of Conduct policies that we apply across all of our operations around the world. These policies represent a set of common values that apply to all employees and all of our business dealings. We have adopted policies and processes, and conduct employee training, all of which are intended to ensure compliance with various economic sanctions and export controls, including the regulations of the U.S. Treasury Department’s Office of Foreign Assets Control (“OFAC”). We do not conduct any business in the following countries that are subject to U.S. economic sanctions: Cuba; Iran; North Korea; Syria and the Crimea region of the Ukraine. See Item 3. Legal Proceedings for additional disclosures regarding past business conducted in Iran.

Competition

Many of our markets are highly competitive. However, we compete effectively due to the quality and breadth of our adhesives, sealants and specialty chemical portfolio and the experience and expertise of our commercial organizations. Within the adhesives and other specialty chemical markets, we believe few suppliers have comparable global reach and corresponding ability to deliver quality and consistency to multinational customers. Our competition is made up generally of two types of companies: (1) similar multinational suppliers and (2) regional or specialty suppliers that typically compete in only one region or within a narrow geographic area within a region. The multinational competitors typically maintain a broad product offering and range of technology, while regional or specialty companies tend to have limited or more focused product ranges and technology.

Principal competitive factors in the sale of adhesives and other specialty chemicals are product performance, supply assurance, technical service, quality, price and customer service.

Customers

We have cultivated strong, integrated relationships with a diverse set of customers worldwide. Our customers are among the technology and market leaders in consumer goods, construction, and industrial markets. We pride ourselves on long-term, collaborative customer relationships and a diverse portfolio of customers in which no single customer accounted for more than 10 percent of consolidated net revenue.

Our leading customers include manufacturers of food and beverages, hygiene products, clothing, major appliances, electronics, automobiles, aerospace and defense products, solar energy systems, filters, construction materials, wood flooring, furniture, cabinetry, windows, doors, tissue and towel, corrugation, tube winding, packaging, labels and tapes.

Our products are delivered directly to customers primarily from our manufacturing plants, with additional deliveries made through distributors and retailers.

Backlog

No significant backlog of unfilled orders existed at December 1, 2018 or December 2, 2017.

Raw Materials

We use several principal raw materials in our manufacturing processes, including tackifying resins, polymers, synthetic rubbers, vinyl acetate monomer and plasticizers. We generally avoid sole source supplier arrangements for raw materials.

The majority of our raw materials are petroleum/natural gas based derivatives. Under normal conditions, raw materials are available on the open market. Prices and availability are subject to supply and demand market mechanisms. Raw material costs are primarily determined by the balance of supply against the aggregate demand from the adhesives industry and other industries that use the same raw material streams. The cost of crude oil and natural gas, the primary feedstocks for our raw materials, can also impact the cost of our raw materials.

Patents, Trademarks and Licenses

Much of the technology we use in our products and manufacturing processes is available in the public domain. For technology not available in the public domain, we rely on trade secrets and patents when appropriate to protect our competitive position. We also license some patented technology from other sources. Our business is not materially dependent upon licenses or similar rights or on any single patent or group of related patents.

We enter into agreements with many employees to protect rights to technology and intellectual property. Confidentiality commitments also are routinely obtained from customers, suppliers and others to safeguard proprietary information.

We own numerous trademarks and service marks in various countries. Trademarks, such as H.B. Fuller®, Swift®, Advantra®, Clarity®, Sesame®, TEC®, Foster®, Rakoll®, Rapidex®, Full-CareTM, Thermonex®, Silaprene®, Eternabond®, Cilbond®, and TONSAN® are important in marketing products. Many of our trademarks and service marks are registered. U.S. trademark registrations are for a term of ten years and are renewable every ten years as long as the trademarks are used in the regular course of trade.

Research and Development

Our investment in research and development creates new and innovative adhesive technology platforms, enhances product performance, ensures a competitive cost structure and leverages available raw materials. New product development is a key research and development outcome, providing higher-value solutions to existing customers or meeting new customers’ needs. Projects are developed in local laboratories in each region, where we understand our customer base the best. Platform developments are coordinated globally through our network of laboratories.

Through designing and developing new polymers and new formulations, we expect to continue to grow in our current markets. We also develop new applications for existing products and technologies, and improve manufacturing processes to enhance productivity and product quality. Research and development efforts are closely aligned to customer needs, but we do not engage in customer sponsored activities. We foster open innovation, seek supplier-driven new technology and use relationships with academic and other institutions to enhance our capabilities.

Environmental, Health and Safety

We comply with applicable regulations relating to environmental protection and workers' safety. This includes regular review of and upgrades to environmental, health and safety policies, practices and procedures as well as improved production methods to minimize our facilities’ outgoing waste, based on evolving societal standards and increased environmental understanding.

Expenditures to comply with environmental regulations over the next two years are estimated to be approximately $13.8 million, including approximately $1.4 million of capital expenditures. See additional disclosure under Item 3. Legal Proceedings.

Seasonality

Our operating segments have historically had lower net revenue in winter months, which is primarily our first fiscal quarter, mainly due to international holidays and the seasonal decline in construction and consumer spending activities.

Employees

We employed approximately 6,500 individuals on December 1, 2018, of which approximately 2,700 were located in the United States.

Executive Officers of the Registrant

The following table shows the name, age and business experience for the past five years of the executive officers as of January 7, 2019. Unless otherwise noted, the positions described are positions with the company or its subsidiaries.

|

Name |

Age |

Positions |

Period Served |

|

|

|

|

|

|

James J. Owens |

54 |

President and Chief Executive Officer |

November 2010 - Present |

|

|

|

|

|

|

Zhiwei Cai |

56 |

Senior Vice President, Engineering Adhesives Vice President, TONSAN and Electronics Director, Electronics Materials |

February 2016 - Present 2014 - 2016 2012 - 2014 |

|

Heather A. Campe |

45 |

Senior Vice President, Americas Adhesives Vice President, Asia Pacific |

October 2016 - Present 2013 - 2016 |

|

Theodore M. Clark |

65 |

Senior Vice President, Royal Adhesives President and CEO of Royal Adhesives and Sealants |

October 2017 - Present 2003 - 2017 |

|

Paula M. Cooney |

50 |

Vice President, Human Resources Director, Global Human Resources Strategic Programs |

April 2016 - Present 2010 - 2016 |

|

John J. Corkrean |

53 |

Executive Vice President and Chief Financial Officer |

May 2016 - Present |

| Senior Vice President, Finance - Global Energy Services, NALCO Champion, an Ecolab Inc. company (supplier of chemicals and related services to the oil and gas industry) | 2014 - 2016 | ||

| Senior Vice President and Corporate Controller, Ecolab Inc. (global provider of water, hygiene and energy technologies and services) | 2008 - 2014 | ||

|

Dietrich J. Crail |

48 |

Vice President, Asia Pacific |

October 2016 - Present |

| Vice President, Paper Converting and Construction, Henkel Corporation (global manufacturer of adhesives, sealants and surface treatments) | 2013 - 2016 | ||

| Vice President and Global Segment Leader, Pressure Sensitive Adhesives, Henkel Corporation | 2008 - 2014 | ||

|

Traci L. Jensen |

52 |

Senior Vice President, Global Construction Adhesives Senior Vice President, Americas Adhesives |

July 2016 - Present January 2013 - July 2016 |

|

|

|

|

|

|

Timothy J. Keenan |

61 |

Vice President, General Counsel and Corporate Secretary |

December 2006 - Present |

|

|

|

|

|

|

Patrick M. Kivits |

51 |

Senior Vice President, EIMEA Corporate Vice President and General Manager, Henkel Corporation (global manufacturer of adhesives, sealants and surface treatments) |

September 2015 - Present 2013 - 2015 |

|

|

|

|

|

|

David W. Moorman |

50 |

Vice President, Operations Excellence Director, Global Information Technology |

March 2017 - Present 2010 - 2017 |

|

Ebrahim Rezai |

67 |

Vice President and Chief Technology and Innovation Officer |

October 2016 - Present |

| Associate Director, Baby and Feminine Care Global Material Development and Supply Organization, Procter and Gamble (multinational manufacturer of family, personal and household care products) | 2015 - 2016 | ||

| Associate Director, Baby Care Global Material Development and Supply Organization, Procter and Gamble | 2005 - 2015 |

The Board of Directors elects the executive officers annually.

Available Information

For more information about us, visit our website at: www.hbfuller.com.

We file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”) via EDGAR. Our SEC filings are available free of charge to the public at our website as soon as reasonably practicable after they have been filed with or furnished to the SEC.

As a global manufacturer of adhesives, sealants and other specialty chemical products, we operate in a business environment that is subject to various risks and uncertainties. Below are the most significant factors that could adversely affect our business, financial condition and results of operations.

Macroeconomic and Industry Risks

Uncertainties in foreign economic, political, regulatory and social conditions and fluctuations in foreign currency may adversely affect our results.

Approximately 55 percent, or $1.7 billion, of our net revenue was generated outside the United States in 2018. International operations could be adversely affected by changes in economic, political, regulatory, and social conditions, especially in Brazil, Russia, China, the Middle East, including Turkey and Egypt, and other developing or emerging markets where we do business. An economic downturn in the businesses or geographic areas in which we sell our products could reduce demand for these products and result in a decrease in sales volume that could have a negative impact on our results of operations. Product demand often depends on end-use markets. Economic conditions that reduce consumer confidence or discretionary spending may reduce product demand. Challenging economic conditions may also impair the ability of our customers to pay for products they have purchased, and as a result, our reserves for doubtful accounts and write-offs of accounts receivable may increase. In addition, trade protection measures, anti-bribery and anti-corruption regulations, restrictions on repatriation of earnings, differing intellectual property rights and changes in legal and regulatory requirements that restrict the sales of products or increase costs could adversely affect our results of operations.

Fluctuations in exchange rates between the U.S. dollar and other currencies could potentially result in increases or decreases in net revenue, cost of raw materials and earnings and may adversely affect the value of our assets outside the United States. In 2018, the change in foreign currencies negatively impacted our net revenue by approximately $2.0 million. In 2018, we spent approximately $1.7 billion for raw materials worldwide of which approximately $869.1 million was purchased outside the United States. Based on 2018 financial results, a hypothetical one percent change in our cost of sales due to foreign currency rate changes would have resulted in a change in net income of approximately $8.3 million or $0.16 per diluted share. Although we utilize risk management tools, including hedging, as appropriate, to mitigate market fluctuations in foreign currencies, any changes in strategy in regard to risk management tools can also affect revenue, expenses and results of operations and there can be no assurance that such measures will result in cost savings or that all market fluctuation exposure will be eliminated.

Distressed financial markets may result in dramatic deflation of financial asset valuations and a general disruption in capital markets.

Adverse equity market conditions and volatility in the credit markets could have a negative impact on the value of our pension trust assets, our future estimated pension liabilities and other postretirement benefit plans. In addition, we could be required to provide increased pension plan funding. As a result, our financial results could be negatively impacted. Reduced access to capital markets may affect our ability to invest in strategic growth initiatives such as acquisitions. In addition, the reduced credit availability could limit our customers’ ability to invest in their businesses, refinance maturing debt obligations, or meet their ongoing working capital needs. If these customers do not have sufficient access to the financial markets, demand for our products may decline.

The interest rates of our term loans are priced using a spread over LIBOR.

LIBOR, the London interbank offered rate, is the basic rate of interest used in lending between banks on the London interbank market and is widely used as a reference for setting the interest rate on loans globally. We typically use LIBOR as a reference rate in our term loans such that the interest due to our creditors pursuant to a term loan extended to us is calculated using LIBOR. Most of our term loan agreements contain a stated minimum value for LIBOR.

On July 27, 2017, the United Kingdom’s Financial Conduct Authority, which regulates LIBOR, announced that it intends to phase out LIBOR by the end of 2021. It is unclear if at that time whether or not LIBOR will cease to exist or if new methods of calculating LIBOR will be established such that it continues to exist after 2021. The U.S. Federal Reserve, in conjunction with the Alternative Reference Rates Committee, a steering committee comprised of large U.S. financial institutions, is considering replacing U.S. dollar LIBOR with a new index calculated by short-term repurchase agreements, backed by Treasury securities (“SOFR”). SOFR is observed and backward looking, which stands in contrast with LIBOR under the current methodology, which is an estimated forward-looking rate and relies, to some degree, on the expert judgment of submitting panel members. Given that SOFR is a secured rate backed by government securities, it will be a rate that does not take into account bank credit risk (as is the case with LIBOR). SOFR is therefore likely to be lower than LIBOR and is less likely to correlate with the funding costs of financial institutions. Whether or not SOFR attains market traction as a LIBOR replacement tool remains in question. As such, the future of LIBOR at this time is uncertain. If LIBOR ceases to exist, we may need to renegotiate our credit agreements with that utilize LIBOR as a factor in determining the interest rate to replace LIBOR with the new standard that is established.

Operational Risks

Increases in prices and declines in the availability of raw materials could negatively impact our financial results.

In 2018, raw material costs made up approximately 75 percent of our cost of sales. Accordingly, changes in the cost of raw materials can significantly impact our earnings. Raw materials needed to manufacture products are obtained from a number of suppliers and many of the raw materials are petroleum and natural gas based derivatives. Under normal market conditions, these raw materials are generally available on the open market from a variety of producers. While alternate supplies of most key raw materials are available, supplier production outages may lead to strained supply-demand situations for certain raw materials. The substitution of key raw materials requires us to identify new supply sources, reformulate and re-test and may require seeking re-approval from our customers using those products. From time to time, the prices and availability of these raw materials may fluctuate, which could impair our ability to procure necessary materials, or increase the cost of manufacturing products. If the prices of raw materials increase in a short period of time, we may be unable to pass these increases on to our customers in a timely manner and could experience reductions to our profit margins. Based on 2018 financial results, a hypothetical one percent change in our raw material costs would have resulted in a change in net income of approximately $12.1 million or $0.23 per diluted share.

We experience substantial competition in each of the operating segments and geographic areas in which we operate.

Our wide variety of products are sold in numerous markets, each of which is highly competitive. Our competitive position in markets is, in part, subject to external factors. For example, supply and demand for certain of our products is driven by end-use markets and worldwide capacities which, in turn, impact demand for and pricing of our products. Many of our direct competitors are part of large multinational companies and may have more resources than we do. Any increase in competition may result in lost market share or reduced prices, which could result in reduced profit margins. This may impair the ability to grow or even to maintain current levels of revenues and earnings. While we have an extensive customer base, loss of certain top customers could adversely affect our financial condition and results of operations until such business is replaced, and no assurances can be made that we would be able to regain or replace any lost customers.

Failure to develop new products and protect our intellectual property could negatively impact our future performance and growth.

Ongoing innovation and product development are important factors in our competitiveness. Failure to create new products and generate new ideas could negatively impact our ability to grow and deliver strong financial results. We continually apply for and obtain U.S. and foreign patents to protect the results of our research for use in our operations and licensing. We are party to a number of patent licenses and other technology agreements. We rely on patents, confidentiality agreements and internal security measures to protect our intellectual property. Failure to protect this intellectual property could negatively affect our future performance and growth.

We may be required to record impairment charges on our goodwill or long-lived assets.

Weak demand may cause underutilization of our manufacturing capacity or elimination of product lines; contract terminations or customer shutdowns may force sale or abandonment of facilities and equipment; or other events associated with weak economic conditions or specific product or customer events may require us to record an impairment on tangible assets, such as facilities and equipment, as well as intangible assets, such as intellectual property or goodwill, which would have a negative impact on our financial results.

Catastrophic events could disrupt our operations or the operations of our suppliers or customers, having a negative impact on our financial results.

Unexpected events, including natural disasters and severe weather events, fires or explosions at our facilities or those of our suppliers, acts of war or terrorism, supply disruptions or breaches of security of our information technology systems could increase the cost of doing business or otherwise harm our operations, our customers and our suppliers. Such events could reduce demand for our products or make it difficult or impossible for us to receive raw materials from suppliers and deliver products to our customers.

A failure in our information technology systems could negatively impact our business.

We rely on information technology to record and process transactions, manage our business and maintain the financial accuracy of our records. Our computer systems are subject to damage or interruption from various sources, including power outages, computer and telecommunications failures, computer viruses, security breaches, vandalism, catastrophic events and human error. Interruptions of our computer systems could disrupt our business, for example by leading to plant downtime and/or power outages, and could result in the loss of business and cause us to incur additional expense.

Information technology security threats are increasing in frequency and sophistication. Our information technology systems could be breached by unauthorized outside parties or misused by employees or other insiders intent on extracting sensitive information, corrupting information or disrupting business processes. Such unauthorized access and a failure to effectively recover from breaches could compromise confidential information, disrupt our business, harm our reputation, result in the loss of assets including trade secrets and other intellectual property, customer confidence and business, result in regulatory proceedings and legal claims, and have a negative impact on our financial results.

We are in the process of implementing a global Enterprise Resource Planning (“ERP”) system that we refer to as Project ONE, which will upgrade and standardize our information system. The North America adhesives business went live in 2014. In 2017, we began the implementation and upgrade of our ERP system in our Latin America adhesives business and implementation for all countries, with the exception of Brazil, has been completed as of the end of 2018. During 2019 and beyond, we will continue implementation in North America, EIMEA (Europe, India, Middle East and Africa) and Asia Pacific.

Any delays or other failure to achieve our implementation goals may adversely impact our financial results. In addition, the failure to either deliver the application on time or anticipate the necessary readiness and training needs could lead to business disruption and loss of business. Failure or abandonment of any part of the ERP system could result in a write-off of part or all of the costs that have been capitalized on the project.

Risks Related to Acquisitions

Risks associated with acquisitions could have an adverse effect on us and the inability to execute organizational restructuring may affect our results.

As part of our growth strategy, we have made and intend to pursue additional acquisitions of complementary businesses or products and joint ventures. The ability to grow through acquisitions or joint ventures depends upon our ability to identify, negotiate, complete and integrate suitable acquisitions or joint venture arrangements. If we fail to successfully integrate acquisitions into our existing business, our results of operations and our cash flows could be adversely affected. Our acquisition strategy also involves other risks and uncertainties, including distraction of management from current operations, greater than expected liabilities and expenses, inadequate return on capital, unidentified issues not discovered in our investigations and evaluations of those strategies and acquisitions and difficulties implementing and maintaining consistent standards, controls, procedures, policies and systems. Future acquisitions could result in debt, dilution, liabilities, increased interest expense, restructuring charges and amortization expenses related to intangible assets.

In addition, our profitability is dependent on our ability to drive sustainable productivity improvements such as cost savings through organizational restructuring. Delays or unexpected costs may prevent us from realizing the full operational and financial benefits of such restructuring initiatives and may potentially disrupt our operations.

We may not realize the revenue growth opportunities and cost synergies that are anticipated from the Royal Adhesives acquisition as we may experience difficulties in integrating Royal Adhesives’ business with ours.

The benefits that are expected to result from the Royal Adhesives acquisition will depend, in part, on our ability to realize the anticipated revenue growth opportunities and cost synergies as a result of the acquisition. Our success in realizing these revenue growth opportunities and cost synergies, and the timing of this realization, depends on the successful integration of Royal Adhesives. There is a significant degree of difficulty and management distraction inherent in the process of integrating an acquisition as sizable as Royal Adhesives. The process of integrating operations could cause an interruption of, or loss of momentum in, our Royal Adhesives’ activities. Members of our senior management may be required to devote considerable amounts of time to this integration process, which will decrease the time they will have to manage our company, service existing customers, attract new customers and develop new products or strategies. If senior management is not able to effectively manage the integration process, or if any significant business activities are interrupted as a result of the integration process, our business could suffer. There can be no assurance that we will successfully or cost-effectively integrate Royal Adhesives. The failure to do so could have a material adverse effect on our business, financial condition or results of operations.

Even if we are able to integrate Royal Adhesives successfully, this integration may not result in the realization of the full benefits of the growth opportunities and cost synergies that we currently expect from this integration, and we cannot guarantee that these benefits will be achieved within anticipated timeframes or at all. For example, we may not be able to eliminate duplicative costs. Moreover, we may incur substantial expenses in connection with the integration of Royal Adhesives. While it is anticipated that certain expenses will be incurred to achieve cost synergies, such expenses are difficult to estimate accurately, and may exceed current estimates. Accordingly, the benefits from the acquisition may be offset by costs incurred to, or delays in, integrating the businesses.

The debt incurred in connection with the Royal Adhesives acquisition could have a negative impact on our liquidity or restrict our activities.

As a result of the Royal Adhesives acquisition, our outstanding indebtedness has significantly increased. Our current indebtedness contains various covenants that limit our ability to engage in specified types of transactions. Our overall leverage and the terms of our financing arrangements could:

|

● |

limit our ability to obtain additional financing in the future for working capital, capital expenditures and acquisitions; |

|

● |

make it more difficult to satisfy our obligations under the terms of our indebtedness; |

|

● |

limit our ability to refinance our indebtedness on terms acceptable to us or at all; |

|

● |

limit our flexibility to plan for and adjust to changing business and market conditions in the industries in which we operate and increase our vulnerability to general adverse economic and industry conditions; |

|

● |

require us to dedicate a substantial portion of our cash flow to make interest and principal payments on our debt, thereby limiting the availability of our cash flow to fund future acquisitions, working capital, business activities, and other general corporate requirements; |

|

● |

limit our ability to obtain additional financing for working capital, to fund growth or for general corporate purposes, even when necessary to maintain adequate liquidity, particularly if any ratings assigned to our debt securities by rating organizations were revised downward; and |

|

● |

subject us to higher levels of indebtedness than our competitors, which may cause a competitive disadvantage and may reduce our flexibility in responding to increased competition. |

In addition, the restrictive covenants require us to maintain specified financial ratios and satisfy other financial condition tests. Our ability to meet those financial ratios and tests will depend on our ongoing financial and operating performance, which, in turn, will be subject to economic conditions and to financial, market and competitive factors, many of which are beyond our control. A breach of any of these covenants could result in a default under the instruments governing our indebtedness.

Legal and Regulatory Risks

The impact of changing laws or regulations or the manner of interpretation or enforcement of existing laws or regulations could adversely impact our financial performance and restrict our ability to operate our business or execute our strategies.

New laws or regulations, or changes in existing laws or regulations or the manner of their interpretation or enforcement, could increase our cost of doing business and restrict our ability to operate our business or execute our strategies. In addition, compliance with laws and regulations is complicated by our substantial global footprint, which will require significant and additional resources to ensure compliance with applicable laws and regulations in the various countries where we conduct business.

Our global operations expose us to trade and economic sanctions and other restrictions imposed by the U.S., the EU and other governments and organizations. The U.S. Departments of Justice, Commerce, State and Treasury and other federal agencies and authorities have a broad range of civil and criminal penalties they may seek to impose against corporations and individuals for violations of economic sanctions laws, export control laws, the Foreign Corrupt Practices Act (the “FCPA”) and other federal statutes and regulations, including those established by the Office of Foreign Assets Control (“OFAC”). Under these laws and regulations, as well as other anti-corruption laws, anti-money-laundering laws, export control laws, customs laws, sanctions laws and other laws governing our operations, various government agencies may require export licenses, may seek to impose modifications to business practices, including cessation of business activities in sanctioned countries or with sanctioned persons or entities and modifications to compliance programs, which may increase compliance costs, and may subject us to fines, penalties and other sanctions. A violation of these laws, regulations, policies or procedures could adversely impact our business, results of operations and financial condition.

Although we have implemented policies and procedures in these areas, we cannot assure you that our policies and procedures are sufficient or that directors, officers, employees, representatives, manufacturers, suppliers and agents have not engaged and will not engage in conduct in violation of such policies and procedures.

We have lawsuits and claims against us with uncertain outcomes.

Our operations from time to time are parties to or targets of lawsuits, claims, investigations and proceedings, including product liability, personal injury, asbestos, patent and intellectual property, commercial, contract, environmental, antitrust, health and safety, and employment matters, which are handled and defended in the ordinary course of business. The results of any future litigation or settlement of such lawsuits and claims are inherently unpredictable, but such outcomes could be adverse and material in amount. See Item 3. Legal Proceedings for a discussion of current litigation.

Costs and expenses resulting from compliance with environmental laws and regulations may negatively impact our operations and financial results.

We are subject to numerous environmental laws and regulations that impose various environmental controls on us or otherwise relate to environmental protection, the sale and export of certain chemicals or hazardous materials, and various health and safety matters. The costs of complying with these laws and regulations can be significant and may increase as applicable requirements and their enforcement become more stringent and new rules are implemented. Adverse developments and/or periodic settlements could negatively impact our results of operations and cash flows. See Item 3. Legal Proceedings for a discussion of current environmental matters.

Additional income tax expense or exposure to additional income tax liabilities could have a negative impact on our financial results.

We are subject to income tax laws and regulations in the United States and various foreign jurisdictions. Significant judgment is required in evaluating and estimating our provision and accruals for these taxes. Our income tax liabilities are dependent upon the location of earnings among these different jurisdictions. Our income tax provision and income tax liabilities could be adversely affected by the jurisdictional mix of earnings, changes in valuation of deferred tax assets and liabilities and changes in tax laws and regulations. In the ordinary course of our business, we are also subject to continuous examinations of our income tax returns by tax authorities. Although we believe our tax estimates are reasonable, the final results of any tax examination or related litigation could be materially different from our related historical income tax provisions and accruals. Adverse developments in an audit, examination or litigation related to previously filed tax returns, or in the relevant jurisdiction’s tax laws, regulations, administrative practices, principles and interpretations could have a material effect on our results of operations and cash flows in the period or periods for which that development occurs, as well as for prior and subsequent periods.

Federal income tax reform could have unforeseen effects on our financial condition and results of operations.

On December 22, 2017, the President of the United States signed into law H.R. 1, originally known as the “Tax Cuts and Jobs Act”, hereafter referred to as “U.S. Tax Reform”. Since the passing of U.S. Tax Reform, additional guidance in the form of notices and proposed regulations which interpret various aspects of U.S. Tax Reform have been issued. As of the filing of this document, additional guidance is expected. Changes could be made to the proposed regulations as they become finalized, future legislation could be enacted, more regulations and notices could be issued, all of which may impact our financial results. We will continue to monitor all of these changes and will reflect the impact as appropriate in future financial statements. Many state and local tax jurisdictions are still determining how they will interpret elements of U.S. Tax Reform. Final state and local governments’ conformity, legislation and guidance relating to U.S. Tax Reform may impact our financial results.

Item 1B. Unresolved Staff Comments

None.

Principal executive offices and central research facilities are located in the St. Paul, Minnesota area. These facilities are company-owned and contain 247,630 square feet. Manufacturing operations are carried out at 38 plants located throughout the United States and at 36 plants located in 21 other countries. In addition, numerous sales and service offices are located throughout the world. We believe that the properties owned or leased are suitable and adequate for our business. Operating capacity varies by product line, but additional production capacity is available for most product lines by increasing the number of shifts worked. The following is a list of our manufacturing plants as of December 1, 2018 (each of the listed properties are owned by us, unless otherwise specified):

|

Segment |

Manufacturing Sq Ft |

Segment |

Manufacturing Sq Ft |

||||||

|

Americas Adhesives |

EIMEA |

||||||||

|

California - Roseville |

82,202 |

Egypt - 6th of October City |

8,525 | ||||||

|

Georgia - Covington |

73,500 |

France - Blois |

48,438 | ||||||

|

- Tucker |

69,000 |

- Surbourg |

21,743 | ||||||

|

- Dalton |

21,980 |

Germany - Lueneburg |

64,249 | ||||||

|

Illinois - Seneca |

24,621 |

- Nienburg |

139,248 | ||||||

|

- Elgin - River Ridge1 |

35,239 |

- Pirmasens2 |

48,438 | ||||||

|

- Elgin - Executive |

30,000 |

Germany - Langelsheim1 |

123,353 | ||||||

|

- Huntley2 |

29,000 |

- Pirmasens |

81,278 | ||||||

|

Indiana - South Bend |

128,218 |

Greece - Lamia |

11,560 | ||||||

|

Kentucky - Paducah |

252,500 |

India - Pune |

38,782 | ||||||

|

Ohio - Blue Ash |

102,000 |

Italy - Pianezze |

36,500 | ||||||

|

Michigan - Grand Rapids |

65,689 |

Portugal - Mindelo |

90,193 | ||||||

|

Minnesota - Fridley1 |

15,850 |

Kenya - Nairobi1 |

5,262 | ||||||

|

- Vadnais Heights |

53,145 |

United Kingdom - Dukinfield |

17,465 | ||||||

|

New Jersey - Wayne1 |

16,000 |

EIMEA Total |

735,034 | ||||||

|

New York - Syracuse1 |

23,000 | ||||||||

|

South Carolina - Simpsonville |

23,722 |

Asia Pacific |

|||||||

|

Texas - Mesquite |

25,000 |

Australia - Dandenong South |

43,540 | ||||||

|

Washington - Vancouver |

35,768 |

- Sydney 1 |

12,968 | ||||||

|

Argentina - Buenos Aires |

10,367 |

People's Republic of China - Guangzhou |

36,055 | ||||||

|

Brazil - Sorocaba2 |

7,535 |

- Nanjing |

55,224 | ||||||

|

- Curitiba1 |

9,896 |

- Nanjing1 |

62,430 | ||||||

|

- Guarulhos |

32,292 |

Indonesia - Mojokerto |

52,991 | ||||||

|

Chile - Maipu, Santiago |

7,539 |

Malaysia - Selongor |

21,900 | ||||||

|

Colombia - Rionegro |

17,072 |

New Zealand - Auckland1 |

7,330 | ||||||

|

Americas Adhesives Total |

1,191,135 |

Philippines - Manila |

9,295 | ||||||

|

Vietnam - Binh Duong1 |

26,156 | ||||||||

|

Construction Adhesives |

Asia Pacific Total |

327,889 | |||||||

|

California - La Mirada |

15,206 | ||||||||

|

Canada - Ontario1 |

63,020 |

Engineering Adhesives |

|||||||

|

- Toronto1 |

25,172 |

California - Irvine1 |

15,120 | ||||||

|

Florida - Gainesville |

6,800 |

- Wilmington1 |

26,373 | ||||||

|

Georgia - Dalton |

72,000 |

People's Republic of China - Beijing |

78,120 | ||||||

|

Illinois - Aurora |

149,000 |

- Beijing1 |

42,044 | ||||||

|

- Palatine2 |

55,000 |

- Suzhou |

73,622 | ||||||

|

Michigan - Michigan Center |

115,000 |

- Yantai |

23,890 | ||||||

|

New Jersey - Edison |

9,780 |

Germany - Wunstorf |

16,146 | ||||||

|

Ohio - Chagrin Falls |

16,500 |

Georgia - Norcross1 |

39,727 | ||||||

|

Pennsylvania - Fairless Hills |

19,229 |

- Ball Ground1 |

4,800 | ||||||

|

Texas - Eagle Lake |

26,000 |

Illinois - Batavia1 |

19,169 | ||||||

|

- Houston |

11,000 |

Illinois - Frankfort - Corsair |

12,500 | ||||||

|

- Mansfield |

28,790 |

- Frankfort - West Drive |

17,000 | ||||||

|

Construction Adhesives Total |

612,497 |

Massachusetts - Peabody1 |

40,000 | ||||||

|

New Hampshire - Raymond1 |

12,950 | ||||||||

|

1 Leased Property |

United Kingdom - Preston1 |

34,000 | |||||||

|

2 Idle Property |

Engineering Adhesives Total |

455,461 | |||||||

Environmental Matters

From time to time, we become aware of compliance matters relating to, or receive notices from, federal, state or local entities regarding possible or alleged violations of environmental, health or safety laws and regulations. We review the circumstances of each individual site, considering the number of parties involved, the level of potential liability or our contribution relative to the other parties, the nature and magnitude of the hazardous substances involved, the method and extent of remediation, the estimated legal and consulting expense with respect to each site and the time period over which any costs would likely be incurred. Also, from time to time, we are identified as a potentially responsible party (“PRP”) under the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”) and/or similar state laws that impose liability for costs relating to the clean up of contamination resulting from past spills, disposal or other release of hazardous substances. We are also subject to similar laws in some of the countries where current and former facilities are located. Our environmental, health and safety department monitors compliance with applicable laws on a global basis. To the extent we can reasonably estimate the amount of our probable liabilities for environmental matters, we establish a financial provision.

Currently, we are involved in various environmental investigations, clean up activities and administrative proceedings and lawsuits. In particular, we are currently deemed a PRP in conjunction with numerous other parties, in a number of government enforcement actions associated with landfills and/or hazardous waste sites. As a PRP, we may be required to pay a share of the costs of investigation and clean up of these sites.

We are engaged in environmental remediation and monitoring efforts at a number of current and former operating facilities. As of December 1, 2018, we accrued $10.7 million, which represents our best estimate of probable liabilities with respect to environmental matters. Of the amount accrued, $4.8 million is attributable to a facility we own in Simpsonville, South Carolina as a result of our Royal Adhesives acquisition that is a designated site under CERCLA. It is reasonably possible that we may have additional liabilities related to these known environmental matters. However, the full extent of our future liability for environmental matters is difficult to predict because of uncertainty as to the cost of investigation and clean up of the sites, our responsibility for such hazardous substances and the number of and financial condition of other potentially responsible parties.

While uncertainties exist with respect to the amounts and timing of the ultimate environmental liabilities, based on currently available information, we have concluded that these matters, individually or in the aggregate, will not have a material adverse effect on our results of operations, financial condition or cash flow. However, adverse developments and/or periodic settlements could negatively impact the results of operations or cash flows in one or more future periods.

Other Legal Proceedings

From time to time and in the ordinary course of business, we are a party to, or a target of, lawsuits, claims, investigations and proceedings, including product liability, personal injury, contract, patent and intellectual property, environmental, health and safety, tax and employment matters. While we are unable to predict the outcome of these matters, we have concluded, based upon currently available information, that the ultimate resolution of any pending matter, individually or in the aggregate, including the asbestos litigation described in the following paragraphs, will not have a material adverse effect on our results of operations, financial condition or cash flow.

We have been named as a defendant in lawsuits in which plaintiffs have alleged injury due to products containing asbestos manufactured more than 30 years ago. The plaintiffs generally bring these lawsuits against multiple defendants and seek damages (both actual and punitive) in very large amounts. In many cases, plaintiffs are unable to demonstrate that they have suffered any compensable injuries or that the injuries suffered were the result of exposure to products manufactured by us. We are typically dismissed as a defendant in such cases without payment. If the plaintiff presents evidence indicating that compensable injury occurred as a result of exposure to our products, the case is generally settled for an amount that reflects the seriousness of the injury, the length, intensity and character of exposure to products containing asbestos, the number and solvency of other defendants in the case, and the jurisdiction in which the case has been brought.

A significant portion of the defense costs and settlements in asbestos-related litigation is paid by third parties, including indemnification pursuant to the provisions of a 1976 agreement under which we acquired a business from a third party. Currently, this third party is defending and paying settlement amounts, under a reservation of rights, in most of the asbestos cases tendered to the third party.

In addition to the indemnification arrangements with third parties, we have insurance policies that generally provide coverage for asbestos liabilities (including defense costs). Historically, insurers have paid a significant portion of our defense costs and settlements in asbestos-related litigation. However, certain of our insurers are insolvent. We have entered into cost-sharing agreements with our insurers that provide for the allocation of defense costs and settlements and judgments in asbestos-related lawsuits. These agreements require, among other things, that we fund a share of settlements and judgments allocable to years in which the responsible insurer is insolvent.

A summary of the number of and settlement amounts for asbestos-related lawsuits and claims is as follows:

|

Year Ended |

Year Ended |

Year Ended |

||||||||||

|

December 1, |

December 2, |

December 3, |

||||||||||

|

($ in millions) |

2018 |

2017 |

2016 |

|||||||||

|

Lawsuits and claims settled |

7 | 9 | 14 | |||||||||

|

Settlement amounts |

$ | 0.4 | $ | 1.7 | $ | 1.4 | ||||||

|

Insurance payments received or expected to be received |

$ | 0.3 | $ | 1.4 | $ | 0.9 | ||||||

We do not believe that it would be meaningful to disclose the aggregate number of asbestos-related lawsuits filed against us because relatively few of these lawsuits are known to involve exposure to asbestos-containing products that we manufactured. Rather, we believe it is more meaningful to disclose the number of lawsuits that are settled and result in a payment to the plaintiff. To the extent we can reasonably estimate the amount of our probable liabilities for pending asbestos-related claims, we establish a financial provision and a corresponding receivable for insurance recoveries.

Based on currently available information, we have concluded that the resolution of any pending matter, including asbestos-related litigation, individually or in the aggregate, will not have a material adverse effect on our results of operations, financial condition or cash flow. However, adverse developments and/or periodic settlements could negatively impact the results of operations or cash flows in one or more future periods.

During 2018, we retained legal counsel to conduct an internal investigation of the possible resale of our hygiene products into Iran by certain customers of our subsidiaries in Turkey (beginning in 2011) and India (beginning in 2014), in possible violation of the economic sanctions against Iran administered by OFAC and our compliance policy. The sales to these customers represented less than one percent of our net revenue in each of our last three fiscal years. The sales to the customers who were reselling our products into Iran ceased during fiscal year 2018 and we do not currently conduct any business in Iran. In January 2018, we voluntarily contacted OFAC to advise it of this internal investigation and our intention to cooperate fully with OFAC and, in September 2018, we submitted the results and findings of our investigation to OFAC. We have not yet received a response from OFAC. At this time, we cannot predict the outcome or effect of the investigation, however, based on the results of our investigation to date, we believe we could incur penalties ranging from zero to $10.0 million.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is traded on the New York Stock Exchange under the symbol FUL. As of January 22, 2019, there were 1,490 common shareholders of record for our common stock.

Issuer Purchases of Equity Securities

Information on our purchases of equity securities during the fourth quarter of 2018 is as follows:

|

Period |

(a) Total Number of Shares Purchased1 |

(b) Average Price Paid per Share |

(c) Total Number of Shares Purchased as Part of a Publicly Announced Plan or Program |

(d) Maximum Approximate Dollar Value of Shares that may yet be Purchased Under the Plan or Program (thousands) |

||||||||||||

|

September 2, 2018 - October 6, 2018 |

2,057 | $ | 53.42 | - | $ | 187,170 | ||||||||||

|

October 7, 2018 - November 3, 2018 |

297 | $ | 45.62 | - | $ | 187,170 | ||||||||||

|

November 4, 2018 - December 1, 2018 |

254 | $ | 48.24 | - | $ | 187,170 | ||||||||||

|

1 The total number of shares purchased include shares withheld to satisfy employees’ withholding taxes upon vesting of restricted stock. |

||||||||||||||||

On April 6, 2017, the Board of Directors authorized a new share repurchase program of up to $200.0 million of our outstanding common shares. Under the program, we are authorized to repurchase shares for cash on the open market, from time to time, in privately negotiated transactions or block transactions, or through an accelerated repurchase agreement. The timing of such repurchases is dependent on price, market conditions and applicable regulatory requirements. Upon repurchase of the shares, we reduced our common stock for the par value of the shares with the excess being applied against additional paid in capital. This authorization replaces the September 30, 2010 authorization to repurchase shares.

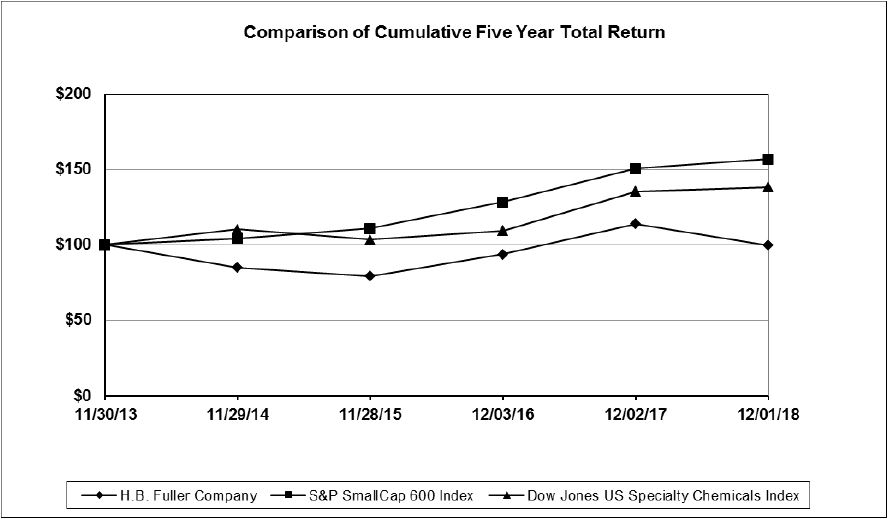

Total Shareholder Return Graph

The line graph below compares the cumulative total shareholder return on our common stock for the last five fiscal years with cumulative total return on the S&P Small Cap 600 Index and Dow Jones U.S. Specialty Chemicals Index. This graph assumes a $100 investment in each of H.B. Fuller, the S&P Small Cap 600 Index and the Dow Jones U.S. Specialty Chemicals Index at the close of trading on November 30, 2013, and also assumes the reinvestment of all dividends.

Item 6. Selected Financial Data

The table that follows presents selected financial data for each of the last five years from the Company’s consolidated financial statements and should be read in conjunction with the Company’s Consolidated Financial Statements and the related Notes and with Management’s Discussion and Analysis of Financial Condition and Results of Operations included elsewhere in this Annual Report on Form 10-K. The selected financial data set forth below as of December 1, 2018 and December 2, 2017 and for the years ended December 1, 2018, December 2, 2017 and December 3, 2016 are derived from our audited financial statements included in this Annual Report on Form 10-K. All other selected financial data set forth below is derived from our audited financial statements not included in this Annual Report on Form 10-K.

|

(Dollars in thousands, except per share amounts) |

Fiscal Years |

|||||||||||||||||||

| 2018 | 2017 4 | 2016 2,4 | 2015 3,4 | 20144 | ||||||||||||||||

|

Net revenue |

$ | 3,041,002 | $ | 2,306,043 | $ | 2,094,605 | $ | 2,083,660 | $ | 2,104,454 | ||||||||||

|

Net income including non-controlling interests1 |

$ | 171,232 | $ | 59,466 | $ | 121,917 | $ | 84,287 | $ | 51,112 | ||||||||||

|

Percent of net revenue |

5.6 | 2.6 | 5.8 | 4.0 | 2.4 | |||||||||||||||

|

Total assets |

$ | 4,175,271 | $ | 4,373,243 | $ | 2,066,565 | $ | 2,056,930 | $ | 1,890,323 | ||||||||||

|

Long-term debt, excluding current maturities |

$ | 2,141,532 | $ | 2,398,927 | $ | 585,759 | $ | 669,606 | $ | 547,735 | ||||||||||

|

Total H.B. Fuller stockholders' equity |

$ | 1,151,767 | $ | 1,051,424 | $ | 944,497 | $ | 882,006 | $ | 899,133 | ||||||||||

|

Per Common Share: |

||||||||||||||||||||

|

Basic |

$ | 3.38 | $ | 1.18 | $ | 2.43 | $ | 1.68 | $ | 1.02 | ||||||||||

|

Diluted |

$ | 3.29 | $ | 1.15 | $ | 2.37 | $ | 1.64 | $ | 1.00 | ||||||||||

|

Dividends declared and paid |

$ | 0.615 | $ | 0.590 | $ | 0.550 | $ | 0.510 | $ | 0.460 | ||||||||||

|

Book value5 |

$ | 22.70 | $ | 20.85 | $ | 18.84 | $ | 17.61 | $ | 17.87 | ||||||||||

|

Number of employees |

6,479 | 5,965 | 4,587 | 4,425 | 3,650 | |||||||||||||||

|

1 2016, 2015 and 2014 include after-tax charges of $(0.2) million, $4.7 million and $45.2 million, respectively, related to special charges, net. |

||||||||||

|

2 2016 contained 53 weeks. |

||||||||||

|

3 Amounts have been adjusted retroactively for discontinued operations. |

||||||||||

|

4 Amounts have been adjusted retrospectively for the change in accounting principle as discussed in Item 7. |

||||||||||

|

5 Book value is calculated by dividing total H.B. Fuller stockholders' equity by the number of common stock shares outstanding as of our fiscal year end. |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Overview

H.B. Fuller Company is a global formulator, manufacturer and marketer of adhesives and other specialty chemical products. For the year ended December 2, 2017, we had six reportable segments: Americas Adhesives, EIMEA, Asia Pacific, Construction Adhesives, Engineering Adhesives and Royal Adhesives. As of the beginning of fiscal 2018, in connection with the integration of the operations of Royal Adhesives with the Company’s other segments, we modified our operating segment structure by allocating the Royal Adhesives segment into each of the five other segments. We began reporting results in five segments for the quarter ended March 3, 2018: Americas Adhesives, EIMEA, Asia Pacific, Construction Adhesives and Engineering Adhesives.

The Americas Adhesives, EIMEA and Asia Pacific operating segments manufacture and supply adhesives products in the assembly, packaging, converting, nonwoven and hygiene, performance wood, insulating glass, flooring, textile, flexible packaging, graphic arts and envelope markets. The Construction Adhesives operating segment provides floor preparation, grouts and mortars for tile setting, and adhesives for soft flooring, and pressure-sensitive adhesives, tapes and sealants for the commercial roofing industry as well as sealants and related products for heating, ventilation and air conditioning installations. The Engineering Adhesives operating segment provides high-performance adhesives to the transportation, electronics, medical, clean energy, aerospace and defense, appliance and heavy machinery markets.

Total Company

When reviewing our financial statements, it is important to understand how certain external factors impact us. These factors include:

|

● |

Changes in the prices of our raw materials that are primarily derived from refining crude oil and natural gas, |

|

● |

Global supply of and demand for raw materials, |

|

● |

Economic growth rates, and |

|

● |

Currency exchange rates compared to the U.S. dollar |

We purchase thousands of raw materials, the majority of which are petroleum/natural gas derivatives. The price of these derivatives impacts the cost of our raw materials. However, the supply of and demand for key raw materials has a greater impact on our costs. As demand increases in high-growth areas, the supply of key raw materials may tighten, resulting in certain materials being put on allocation. Natural disasters, such as hurricanes, also can have an impact as key raw material producers are shut down for extended periods of time. We continually monitor capacity utilization figures, market supply and demand conditions, feedstock costs and inventory levels, as well as derivative and intermediate prices, which affect our raw materials. With approximately 75 percent of our cost of sales accounted for by raw materials, our financial results are extremely sensitive to changing costs in this area.

The pace of economic growth directly impacts certain industries to which we supply products. For example, adhesives-related revenues from durable goods customers in areas such as appliances, furniture and other woodworking applications tend to fluctuate with the overall economic activity. In business components such as Construction Adhesives and insulating glass, revenues tend to move with more specific economic indicators such as housing starts and other construction-related activity.

The movement of foreign currency exchange rates as compared to the U.S. dollar impacts the translation of the foreign entities’ financial statements into U.S. dollars. As foreign currencies weaken against the U.S. dollar, our revenues and costs decrease as the foreign currency-denominated financial statements translate into fewer U.S. dollars. The fluctuations of the Euro and the Chinese renminbi against the U.S. dollar have the largest impact on our financial results as compared to all other currencies. In 2018, currency fluctuations had a negative impact on net revenue of approximately $2.0 million as compared to 2017.

Key financial results and transactions for 2018 included the following:

|

● |

Net revenue increased 31.9 percent from 2017 primarily driven by a 28.3 percent increase due to acquisitions, a 3.4 percent increase in product pricing, and a 0.6 percent increase due to favorable sales mix. Positive drivers of growth were partially offset by a 0.3 percent decrease in sales volume and a 0.1 percent decrease due to currency fluctuations. |

|

● |

Gross profit margin increased to 27.5 percent from 26.2 percent in 2018 primarily due to favorable product pricing, the impact of the Royal Adhesives acquisition and lower restructuring plan costs. Positive drivers of growth were partially offset by higher raw material costs. |

|

● |

Cash flow generated by operating activities was $253.3 million in 2018 as compared to $140.8 million in 2017 and $195.7 million in 2016. |

Our total year constant currency sales growth, which we define as the combined variances from sales volume, product pricing, sales mix and business acquisitions, increased 32.0 percent for 2018 compared to 2017.

In 2018, our diluted earnings per share was $3.29 compared to $1.15 in 2017 and $2.37 in 2016. The higher earnings per share in 2018 compared to 2017 was due to higher net revenue, lower transaction costs related to acquisitions, and one time discrete items related to U.S. Tax Reform, which were partially offset by higher operating expenses mainly due to the impact of acquired businesses and higher interest expense due to higher U.S. debt balances at higher interest rates from the issuance of new debt in 2017. The lower earnings per share in 2017 compared to 2016 was due to an increase in transaction costs related to acquisitions, including make-whole costs associated with the early repayment of certain outstanding debt obligations, and the implementation of the 2017 Restructuring Plan.

Change in Accounting Principle

In the fourth quarter of 2018, we elected to change our method of accounting for certain inventories in the United States within the Company’s Americas Adhesives and Construction Adhesives segments from the last-in, first-out method (“LIFO”) to weighted-average cost. We have retrospectively adjusted the Consolidated Financial Statements for all periods presented to reflect this change.

Project ONE

In December 2012, our Board of Directors approved a multi-year project to replace and enhance our existing core information technology platforms. The scope for this project includes most of the basic transaction processing for the company including customer orders, procurement, manufacturing, and financial reporting. The project envisions harmonized business processes for all of our operating segments supported with one standard software configuration. The execution of this project, which we refer to as Project ONE, is being supported by internal resources and consulting services. The North America adhesives business went live in 2014. In 2017, we began the Project ONE implementation in our Latin America adhesives business, and implementation for all countries, with the exception of Brazil, has been completed as of the end of 2018. During 2019 and beyond, we will continue implementation in North America, EIMEA (Europe, India, Middle East and Africa) and Asia Pacific.

Total expenditures for Project ONE are estimated to be $195 to $210 million, of which 50-55% is expected to be capital expenditures. Our total project-to-date expenditures are approximately $73 million, of which approximately $38 million are capital expenditures. Given the complexity of the implementation, the total investment to complete the project may exceed our estimate.

Restructuring Plans

Royal Adhesives Restructuring Plan

During the first quarter of 2018, we approved a restructuring plan consisting of consolidation plans, organizational changes and other actions related to the integration of the operations of Royal Adhesives with the operations of the Company (the “Royal Adhesives Restructuring Plan”). In implementing the Royal Adhesives Restructuring Plan, we expect to incur costs of approximately $20.0 million, which includes (i) cash expenditures of approximately $12.0 million for severance and related employee costs globally and (ii) other costs of approximately $8.0 million related to the optimization of production facilities, streamlining of processes and accelerated depreciation of long-lived assets. Approximately $14.0 million of the costs are expected to be cash costs. For the year ending December 1, 2018, we incurred costs of $6.7 million under this plan. The Royal Adhesives Restructuring Plan was implemented in the first quarter of 2018 and is currently expected to be completed by the end of fiscal year 2020.

2017 Restructuring Plan

During the first quarter of 2017, we approved a restructuring plan (the “2017 Restructuring Plan”) related to organizational changes and other actions to optimize operations. In implementing the 2017 Restructuring Plan, we incurred costs of $20.2 million as of December 1, 2018 which included cash expenditures of approximately $11.3 million for severance and related employee costs globally and $8.9 million related to the optimization of production facilities, streamlining of processes and accelerated depreciation of long-lived assets. Approximately $15.8 million of the costs were cash costs. The 2017 Restructuring Plan is substantially complete.

Federal Income Tax Reform

On December 22, 2017, the President of the United States signed into law H.R. 1, originally known as the “Tax Cuts and Jobs Act”, hereafter referred to as “U.S. Tax Reform”. Since the passing of U.S. Tax Reform, additional guidance in the form of notices and proposed regulations which interpret various aspects of U.S. Tax Reform have been issued. As of the filing of this document, additional guidance is expected. Changes could be made to the proposed regulations as they become finalized, future legislation could be enacted, more regulations and notices could be issued, all of which may impact our financial results. We will continue to monitor all of these changes and will reflect the impact as appropriate in future financial statements. Many state and local tax jurisdictions are still determining how they will interpret elements of U.S. Tax Reform. Final state and local governments’ conformity and legislation or guidance relating to U.S. Tax Reform may impact our financial results.

Given the varying effective dates of specific components of U.S. Tax Reform coupled with our fiscal year end, we will be required to consider additional elements of U.S. Tax Reform, including the significant changes related to taxation of international operations that we were not subject to during our fiscal year ended December 1, 2018. Such elements will be included for our fiscal year ended November 30, 2019.

Critical Accounting Policies and Significant Estimates

Management’s discussion and analysis of our results of operations and financial condition are based upon the Consolidated Financial Statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses and related disclosure of contingent assets and liabilities. We believe the critical accounting policies and areas that require the most significant judgments and estimates to be used in the preparation of the Consolidated Financial Statements relate to pension and other postretirement plans; goodwill impairment; long-lived assets recoverability; valuation of product, environmental and other litigation liabilities; valuation of deferred tax assets and accuracy of tax contingencies; and valuation of acquired assets and liabilities.

Pension and Other Postretirement Plan Assumptions

We sponsor defined-benefit pension plans in both the U.S. and non-U.S. entities. Also in the U.S., we sponsor other postretirement plans for health care and life insurance benefits. Expenses and liabilities for the pension plans and other postretirement plans are actuarially calculated. These calculations are based on our assumptions related to the discount rate, expected return on assets, projected salary increases and health care cost trend rates. Note 10 to the Consolidated Financial Statements includes disclosure of assumptions employed in these measurements for both the non-U.S. and U.S. plans.