Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - CHS INC | ex-322113018.htm |

| EX-32.1 - EXHIBIT 32.1 - CHS INC | ex-321113018.htm |

| EX-31.2 - EXHIBIT 31.2 - CHS INC | ex-312113018.htm |

| EX-31.1 - EXHIBIT 31.1 - CHS INC | ex-311113018.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________

Form 10-Q

________________________________________

þ | Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended November 30, 2018. | ||

or | |||

o | Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to | ||

Commission file number: 001-36079

________________________________________

CHS Inc.

(Exact name of registrant as specified in its charter)

Minnesota (State or other jurisdiction of incorporation or organization) | 41-0251095 (I.R.S. Employer Identification Number) | |

5500 Cenex Drive Inver Grove Heights, Minnesota 55077 (Address of principal executive offices, including zip code) | (651) 355-6000 (Registrant’s telephone number, including area code) | |

________________________________________

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES þ NO o

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

YES þ NO o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ | Smaller reporting company o | Emerging growth company o |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES o NO þ

Indicate the number of shares outstanding of each of the Registrant’s classes of common stock, as of the latest practicable date: The Registrant has no common stock outstanding.

INDEX

Page No. | ||

Unless the context otherwise requires, for purposes of this Quarterly Report on Form 10-Q, the words "we," "us," "our," the "Company" and "CHS" refer to CHS Inc., a Minnesota cooperative corporation, and its subsidiaries as of November 30, 2018.

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains and our other publicly available documents may contain, and our officers, directors and other representatives may from time to time make, "forward-looking statements" within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as "anticipate," "intend," "plan," "goal," "seek," "believe," "project," "estimate," "expect," "strategy," "future," "likely," "may," "should," "will" and similar references to future periods. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our businesses, financial condition and results of operations, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not place undue reliance on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements are discussed or identified in our public filings made with the U.S. Securities and Exchange Commission, including in the "Risk Factors" discussion in Item 1A of our Annual Report on Form 10-K for the year ended August 31, 2018. Any forward-looking statements made by us in this Quarterly Report on Form 10-Q are based only on information currently available to us and speak only as of the date on which the statement is made. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise, except as required by applicable law.

1

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

CHS INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Unaudited)

November 30, 2018 | August 31, 2018 | ||||||

(Dollars in thousands) | |||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 266,152 | $ | 450,617 | |||

Receivables | 2,686,095 | 2,460,401 | |||||

Inventories | 3,184,449 | 2,768,649 | |||||

Derivative assets | 202,932 | 329,757 | |||||

Margin and related deposits | 214,594 | 151,150 | |||||

Supplier advance payments | 399,095 | 288,423 | |||||

Other current assets | 234,406 | 244,208 | |||||

Total current assets | 7,187,723 | 6,693,205 | |||||

Investments | 3,774,536 | 3,711,925 | |||||

Property, plant and equipment | 5,078,307 | 5,141,719 | |||||

Other assets | 813,190 | 834,329 | |||||

Total assets | $ | 16,853,756 | $ | 16,381,178 | |||

LIABILITIES AND EQUITIES | |||||||

Current liabilities: | |||||||

Notes payable | $ | 2,401,553 | $ | 2,272,196 | |||

Current portion of long-term debt | 167,423 | 167,565 | |||||

Customer margin deposits and credit balances | 133,698 | 137,395 | |||||

Customer advance payments | 325,817 | 409,088 | |||||

Accounts payable | 2,202,487 | 1,844,489 | |||||

Derivative liabilities | 282,557 | 438,465 | |||||

Accrued expenses | 428,940 | 511,032 | |||||

Dividends and equities payable | 311,461 | 153,941 | |||||

Total current liabilities | 6,253,936 | 5,934,171 | |||||

Long-term debt | 1,739,956 | 1,762,690 | |||||

Long-term deferred tax liabilities | 209,767 | 182,770 | |||||

Other liabilities | 358,005 | 336,519 | |||||

Commitments and contingencies (Note 15) | |||||||

Equities: | |||||||

Preferred stock | 2,264,038 | 2,264,038 | |||||

Equity certificates | 4,558,940 | 4,609,456 | |||||

Accumulated other comprehensive loss | (204,232 | ) | (199,915 | ) | |||

Capital reserves | 1,663,971 | 1,482,003 | |||||

Total CHS Inc. equities | 8,282,717 | 8,155,582 | |||||

Noncontrolling interests | 9,375 | 9,446 | |||||

Total equities | 8,292,092 | 8,165,028 | |||||

Total liabilities and equities | $ | 16,853,756 | $ | 16,381,178 | |||

The accompanying notes are an integral part of the consolidated financial statements (unaudited).

2

CHS INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

For the Three Months Ended November 30, | |||||||

2018 | (As Restated) 2017 | ||||||

(Dollars in thousands) | |||||||

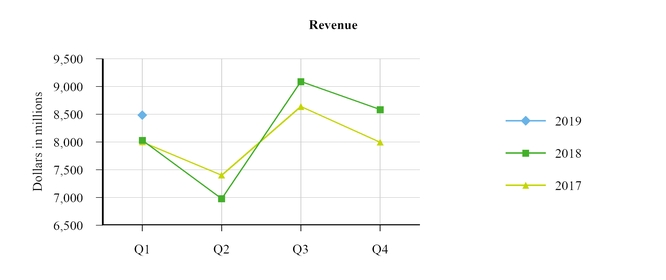

Revenues | $ | 8,484,289 | $ | 8,031,884 | |||

Cost of goods sold | 8,013,648 | 7,711,392 | |||||

Gross profit | 470,641 | 320,492 | |||||

Marketing, general and administrative | 162,496 | 140,346 | |||||

Reserve and impairment charges (recoveries), net | (6,353 | ) | (3,787 | ) | |||

Operating earnings (loss) | 314,498 | 183,933 | |||||

Interest expense | 38,908 | 40,702 | |||||

Other (income) loss | (25,134 | ) | (26,195 | ) | |||

Equity (income) loss from investments | (66,508 | ) | (38,362 | ) | |||

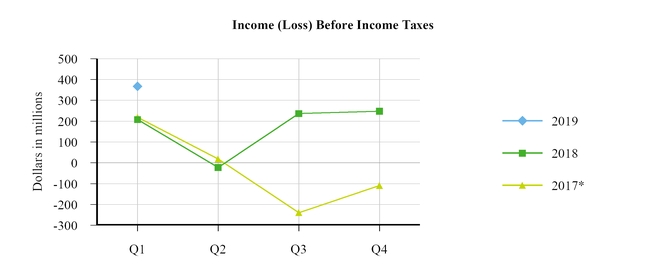

Income (loss) before income taxes | 367,232 | 207,788 | |||||

Income tax expense (benefit) | 20,117 | 20,606 | |||||

Net income (loss) | 347,115 | 187,182 | |||||

Net income (loss) attributable to noncontrolling interests | (389 | ) | (464 | ) | |||

Net income (loss) attributable to CHS Inc. | $ | 347,504 | $ | 187,646 | |||

The accompanying notes are an integral part of the consolidated financial statements (unaudited).

3

CHS INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

For the Three Months Ended November 30, | |||||||

2018 | (As Restated) 2017 | ||||||

(Dollars in thousands) | |||||||

Net income (loss) | $ | 347,115 | $ | 187,182 | |||

Other comprehensive income (loss), net of tax: | |||||||

Postretirement benefit plan activity | 2,101 | 1,594 | |||||

Unrealized net gain (loss) on available for sale investments | — | 3,640 | |||||

Cash flow hedges | (1,307 | ) | (4 | ) | |||

Foreign currency translation adjustment | (405 | ) | (2,211 | ) | |||

Other comprehensive income (loss), net of tax | 389 | 3,019 | |||||

Comprehensive income (loss) | 347,504 | 190,201 | |||||

Less: comprehensive income (loss) attributable to noncontrolling interests | (389 | ) | (464 | ) | |||

Comprehensive income (loss) attributable to CHS Inc. | $ | 347,893 | $ | 190,665 | |||

The accompanying notes are an integral part of the consolidated financial statements (unaudited).

4

CHS INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

For the Three Months Ended November 30, | |||||||

2018 | (As Restated) 2017 | ||||||

(Dollars in thousands) | |||||||

Cash flows from operating activities: | |||||||

Net income (loss) | $ | 347,115 | $ | 187,182 | |||

Adjustments to reconcile net income to net cash provided by (used in) operating activities: | |||||||

Depreciation and amortization | 118,603 | 120,148 | |||||

Amortization of deferred major repair costs | 19,176 | 16,418 | |||||

Equity (income) loss from investments | (66,508 | ) | (38,362 | ) | |||

Distributions from equity investments | 18,887 | 12,514 | |||||

Provision for doubtful accounts | 5,009 | (3,601 | ) | ||||

Deferred taxes | 26,555 | 16,346 | |||||

Other, net | (3,162 | ) | 375 | ||||

Changes in operating assets and liabilities, net of acquisitions: | |||||||

Receivables | (182,767 | ) | (56,700 | ) | |||

Inventories | (416,196 | ) | (513,023 | ) | |||

Derivative assets | 139,694 | 63,926 | |||||

Margin and related deposits | (63,476 | ) | (893 | ) | |||

Supplier advance payments | (110,672 | ) | (293,536 | ) | |||

Other current assets and other assets | 12,541 | 6,323 | |||||

Customer margin deposits and credit balances | (3,697 | ) | (18,045 | ) | |||

Customer advance payments | (83,271 | ) | (10,251 | ) | |||

Accounts payable and accrued expenses | 299,741 | 453,219 | |||||

Derivative liabilities | (159,385 | ) | (99,956 | ) | |||

Other liabilities | 7,015 | 4,376 | |||||

Net cash provided by (used in) operating activities | (94,798 | ) | (153,540 | ) | |||

Cash flows from investing activities: | |||||||

Acquisition of property, plant and equipment | (104,750 | ) | (85,824 | ) | |||

Proceeds from disposition of property, plant and equipment | 5,752 | 56,079 | |||||

Proceeds from sale of business | 1,730 | 29,457 | |||||

Expenditures for major repairs | (3,441 | ) | (1,039 | ) | |||

Investments redeemed | 1,499 | 5,195 | |||||

Changes in CHS Capital notes receivable, net | (126,865 | ) | (69,227 | ) | |||

Financing extended to customers | (3,928 | ) | (15,778 | ) | |||

Payments from customer financing | 71,137 | 16,520 | |||||

Other investing activities, net | 4,090 | 1,847 | |||||

Net cash provided by (used in) investing activities | (154,776 | ) | (62,770 | ) | |||

Cash flows from financing activities: | |||||||

Proceeds from lines of credit and long-term borrowings | 4,429,276 | 8,006,980 | |||||

Payments on lines of credit, long term-debt and capital lease obligations | (4,317,479 | ) | (7,654,661 | ) | |||

Preferred stock dividends paid | (42,167 | ) | (42,167 | ) | |||

Retirements of equities | (24,072 | ) | (3,682 | ) | |||

Other financing activities, net | 3,503 | (21,257 | ) | ||||

Net cash provided by (used in) financing activities | 49,061 | 285,213 | |||||

Effect of exchange rate changes on cash and cash equivalents | (1,535 | ) | 2,236 | ||||

Net increase (decrease) in cash and cash equivalents and restricted cash | (202,048 | ) | 71,139 | ||||

Cash and cash equivalents and restricted cash at beginning of period | 543,940 | 272,272 | |||||

Cash and cash equivalents and restricted cash at end of period | $ | 341,892 | $ | 343,411 | |||

The accompanying notes are an integral part of the consolidated financial statements (unaudited).

5

CHS INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

Note 1 Basis of Presentation and Significant Accounting Policies

Basis of Presentation

The unaudited Consolidated Balance Sheet as of November 30, 2018, the Consolidated Statements of Operations for the three months ended November 30, 2018, and 2017, the Consolidated Statements of Comprehensive Income for the three months ended November 30, 2018, and 2017, and the Consolidated Statements of Cash Flows for the three months ended November 30, 2018, and 2017, reflect in the opinion of our management, all normal recurring adjustments necessary for a fair statement of the financial position, results of operations and cash flows for the interim periods presented. The results of operations and cash flows for interim periods are not necessarily indicative of results for a full fiscal year because of, among other things, the seasonal nature of our businesses. Our Consolidated Balance Sheet data as of August 31, 2018, has been derived from our audited consolidated financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States of America ("U.S. GAAP").

As described in Note 2, Restatement of Previously Issued Financial Information, the consolidated financial statements for the three months ended November 30, 2017, have been restated to reflect the correction of misstatements. We have also restated all relevant amounts impacted within the notes to the consolidated financial statements.

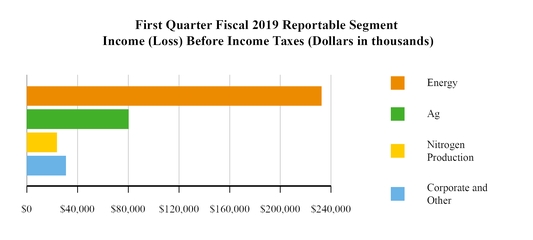

The notes to our consolidated financial statements reference our Energy, Ag and Nitrogen Production reportable segments, as well as our Corporate and Other category, which represents an aggregation of individually immaterial operating segments. See Note 12, Segment Reporting, for more information related to our reportable segments.

Our consolidated financial statements include the accounts of CHS and all of our wholly owned and majority owned subsidiaries. The effects of all significant intercompany transactions have been eliminated.

These unaudited consolidated financial statements should be read in conjunction with the consolidated financial statements and notes thereto for the year ended August 31, 2018, included in our Annual Report on Form 10-K, filed with the Securities and Exchange Commission (the "SEC").

Significant Accounting Policies

The following significant accounting policies have been updated since our Annual Report on Form 10-K for the year ended August 31, 2018, as a result of the adoption of certain new accounting pronouncements effective for us during the three months ended November 30, 2018.

Restricted Cash

Restricted cash is included in our Consolidated Balance Sheets within other current assets (current portion) and other assets (non-current portion), as appropriate, and primarily relates to customer deposits for futures and option contracts associated with regulated commodities held in separate accounts as required under federal and other regulations. Pursuant to the requirements of the Commodity Exchange Act, such funds must be carried in separate accounts that are designated as segregated customer accounts, as applicable. Restricted cash also includes funds held in escrow pursuant to applicable regulations limiting their usage.

6

The following table provides a reconciliation of cash and cash equivalents and restricted cash as reported within our Consolidated Balance Sheets that aggregates to the amount presented in our Consolidated Statements of Cash Flows. During the three months ended November 30, 2018, we updated the presentation of our Consolidated Statements of Cash Flows to include restricted cash with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on our Consolidated Statements of Cash Flows.

November 30, 2018 | August 31, 2018 | November 30, 2017 | August 31, 2017 | ||||||||||||

(Dollars in thousands) | |||||||||||||||

Cash and cash equivalents | $ | 266,152 | $ | 450,617 | $ | 249,767 | $ | 181,379 | |||||||

Restricted cash included in other current assets | 72,687 | 90,193 | 88,525 | 83,561 | |||||||||||

Restricted cash included in other assets | 3,053 | 3,130 | 5,119 | 7,332 | |||||||||||

Total Cash and cash equivalents and restricted cash | $ | 341,892 | $ | 543,940 | $ | 343,411 | $ | 272,272 | |||||||

Investments

As described in the "Recent Accounting Pronouncements" section below, we adopted Accounting Standards Update ("ASU") No. 2016-01, Recognition and Measurement of Financial Assets and Financial Liabilities, which was effective for us September 1, 2018. As a result, all equity securities that do not result in consolidation and are not accounted for under the equity method are measured at fair value with changes therein reflected in net income. We have elected to utilize the measurement alternative for equity investments that do not have readily determinable fair values and measure these investments at cost less impairment plus or minus observable price changes in orderly transactions.

Investments in other cooperatives are recorded in a manner similar to equity investments without readily determinable fair values, plus patronage dividends received in the form of capital stock and other equities. Patronage dividends are recorded as a reduction to cost of goods sold at the time qualified written notices of allocation are received. Investments in debt and equity instruments are carried at amounts that approximate fair values.

Revenue Recognition

We provide a wide variety of products and services, ranging from agricultural inputs such as fuels, farm supplies and crop nutrients, to agricultural outputs that include grain and oilseed, processed grains and oilseeds and food products, and ethanol production and marketing. Revenue is recognized when performance obligations under the terms of a contract with a customer are satisfied, which generally occurs when control of the goods has transferred to the customer. For the majority of our contracts with customers, control transfers to customers at a point-in-time when the goods/services have been delivered, as that is generally when legal title, physical possession and risks and rewards of goods/services transfers to the customer. In limited arrangements, control transfers over time as the customer simultaneously receives and consumes the benefits of the service as we complete the performance obligation(s).

Revenue is recognized at the transaction price that we expect to be entitled to in exchange for transferring goods or services to a customer, excluding amounts collected on behalf of third parties. We follow a policy of recognizing revenue at the point-in-time or over the period of time we satisfy our performance obligation by transferring control over a product or service to a customer in accordance with the underlying contract. For physically settled derivative sales contracts that are outside the scope of the revenue guidance, we recognize revenue when control of the inventory is transferred within the meaning of Accounting Standards Codification ("ASC") Topic 606.

Recent Accounting Pronouncements

Adopted

In March 2017, the Financial Accounting Standards Board (the "FASB") issued Accounting Standards Update ("ASU") No. 2017-07, Compensation - Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Costs and Net Postretirement Benefit Cost. This ASU changes the presentation of net periodic pension cost and net periodic postretirement benefit cost in the Consolidated Statements of Operations. This ASU provides that the service cost component should be included in the same income statement line item as other compensation costs arising from services rendered by the employees during the period. The other components of net periodic benefit cost (such as interest, expected return on plan assets, prior service cost amortization and actuarial gain/loss amortization) are required to be presented in the Consolidated

7

Statements of Operations separately outside of operating income. Additionally, only service cost may be capitalized in assets. This ASU was effective for us beginning September 1, 2018, for our fiscal year 2019 and for interim periods within that fiscal year. The guidance on the presentation of the components of net periodic benefit cost in the Consolidated Statements of Operations has been applied retrospectively, and the guidance regarding the capitalization of the service cost component in assets has been applied prospectively. The adoption of this guidance had no impact on previously reported income (loss) before income taxes or net income attributable to CHS; however, non-service cost components of net periodic benefit costs in prior periods have been reclassified from operating expenses and are now reported outside of operating income within other (income) loss. Specifically, the retrospective adjustments recorded as a result of the adoption of this guidance resulted in an increase to cost of goods sold and marketing, general and administrative expense of $0.3 million and $0.8 million, respectively, and a corresponding increase of $1.2 million to other income during the three months ended November 30, 2017. There was no impact to previously reported income before income taxes and net income attributable to CHS as a result of adoption. The adoption of this amended guidance did not have a material impact on our consolidated financial statements.

In January 2017, the FASB issued ASU No. 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business. The amendments within this ASU narrow the existing definition of a business and provide a more robust framework for evaluating whether a transaction should be accounted for as an acquisition (or disposal) of assets or a business. The definition of a business impacts various areas of accounting, including acquisitions, disposals and goodwill. Under the new guidance, fewer acquisitions are expected to be considered businesses. This ASU was effective for us beginning September 1, 2018, for our fiscal year 2019 and for interim periods within that fiscal year. The guidance has been applied prospectively. The adoption of this amended guidance did not have a material impact on our consolidated financial statements.

In November 2016, the FASB issued ASU No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash. This ASU requires restricted cash and restricted cash equivalents to be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the Consolidated Statements of Cash Flows as well as disclosure about the nature of restrictions on cash, cash equivalents and amounts generally described as restricted cash. Additionally, the guidance requires disclosure of the total amount of cash, cash equivalents and restricted cash for each comparative period for which a Consolidated Balance Sheet is presented. This ASU was effective for us beginning September 1, 2018, for our fiscal year 2019 and for interim periods within that fiscal year. The amendments in this ASU were applied retrospectively to all periods presented. Refer to the additional disclosures pertaining to restricted cash within the Restricted Cash significant accounting policy above. The adoption of this amended guidance did not have a material impact on our Consolidated Statements of Cash Flows.

In January 2016, the FASB issued ASU No. 2016-01, Recognition and Measurement of Financial Assets and Financial Liabilities, which requires equity investments (except those accounted for under the equity method of accounting or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income. This guidance eliminates the previous cost method of accounting for certain equity securities that did not have readily determinable fair values. This guidance also simplifies the impairment assessment and allows for a fair value measurement alternative for equity investments without readily determinable fair values and includes presentation and disclosure changes. This ASU was effective for us beginning September 1, 2018, for our fiscal year 2019 and for interim periods within that fiscal year and was applied following a prospective basis. We have elected to utilize the measurement alternative for equity investments that do not have readily determinable fair values and measure these investments at cost less impairment plus or minus observable price changes in orderly transactions. As a result of the adoption of this amended guidance, we reclassified approximately $4.7 million from accumulated other comprehensive loss to the opening balance of capital reserves within our Consolidated Balance Sheet as of September 1, 2018, which did not have a material impact on our consolidated financial statements.

In August 2016, the FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments. This ASU is intended to reduce existing diversity in practice in how certain cash receipts and payments are presented and classified in the Consolidated Statements of Cash Flows. This ASU was effective for us beginning September 1, 2018, for our fiscal year 2019 and for interim periods within that fiscal year. The adoption of this amended guidance did not have a material impact on our Consolidated Statements of Cash Flows.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606). The amendments within this ASU, as well as within the additional clarifying ASUs issued by the FASB, provide a single comprehensive model to be used to determine the measurement of revenue and timing of recognition for revenue arising from contracts with customers. The core principle of the amended guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The new revenue recognition guidance includes a five-step model for the recognition of revenue, including (1) identifying the contract with a customer, (2) identifying the performance obligations in the

8

contract, (3) determining the transaction price, (4) allocating the transaction price to the performance obligations, and (5) recognizing revenue when (or as) an entity satisfies a performance obligation. This ASU was effective for us beginning September 1, 2018, for our fiscal year 2019 and for interim periods within that fiscal year, and we elected to apply the modified retrospective method of adoption to all contracts as of the date of initial application. The majority of our revenues are attributable to forward commodity sales contracts, which are considered to be physically settled derivatives under ASC 815, Derivatives and Hedging (Topic 815). Revenues arising from derivative contracts accounted for under ASC 815 are specifically outside the scope of ASC Topic 606 and therefore not subject to the provisions of the new revenue recognition guidance. As such, the impact of adoption of the new revenue guidance has only been assessed for our revenue contracts that are not accounted for as derivative arrangements. The primary impact of adoption was changes to the timing of revenue recognition for certain revenue streams that had an immaterial impact. Following the modified retrospective method of adoption, we determined the cumulative effect of adoption for all contracts with customers that had not been completed as of the adoption date was less than $1.0 million. Additionally, the impact of applying ASC Topic 606 compared to previous guidance during the three months ended November 30, 2018, was an overall decrease to revenues of $13.1 million. Our revenue recognition accounting policy and additional information related to our revenue streams and related performance obligations required to be satisfied in order to recognize revenue can be found within Note 3, Revenues.

Not Yet Adopted

In August 2018, the FASB issued ASU No. 2018-15, Intangibles - Goodwill and Other - Internal-Use Software: Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract. This ASU reduces the complexity of accounting for implementation, setup, and other upfront costs incurred in a cloud computing service arrangement that is hosted by a vendor. This ASU aligns the accounting for implementation costs of hosting arrangements, irrespective of whether the arrangements convey a license to the hosted software. This ASU permits either a prospective or retrospective transition approach. This ASU is effective for us beginning September 1, 2020, for our fiscal year 2021 and for interim periods within that fiscal year, with early adoption permitted. The adoption of this amended guidance is not expected to have a material impact on our consolidated financial statements.

In August 2018, the FASB issued ASU No. 2018-14, Disclosure Framework - Changes to the Disclosure Requirements for Defined Benefit Plans, which amends ASC 715-20, Compensation - Retirement Benefits - Defined Benefit Plans - General. This ASU modifies the disclosure requirements for employers that sponsor defined benefit pension or other postretirement plans by removing and adding certain disclosures for these plans. The eliminated disclosures include (a) the amounts in accumulated other comprehensive income expected to be recognized in net periodic benefit costs over the next fiscal year and (b) the effects of a one-percentage-point change in assumed health care cost trend rates on the net periodic benefit costs and the benefit obligation for postretirement health care benefits. The new disclosures include the interest crediting rates for cash balance plans and an explanation of significant gains and losses related to changes in benefit obligations. This ASU is effective for us beginning September 1, 2021, for our fiscal year 2022 and for interim periods within that fiscal year, with early adoption permitted. The adoption of this amended guidance is not expected to have a material impact on our consolidated financial statements.

In August 2018, the FASB issued ASU No. 2018-13, Disclosure Framework - Changes to the Disclosure Requirements for Fair Value Measurement, which amends ASC 820, Fair Value Measurement. This ASU modifies the disclosure requirements for fair value measurements by removing, modifying and adding certain disclosures. Specifically, the guidance removes the requirement to disclose the amount and reasons for any transfers between Level 1 and Level 2 of the fair value hierarchy and removes the requirement to disclose a description of the valuation processes used to value Level 3 fair value measurements. The guidance also requires additional disclosures surrounding Level 3 changes in unrealized gains/losses included in other comprehensive income as well as the range and weighted average significant unobservable inputs calculation. This ASU is effective for us beginning September 1, 2020, for our fiscal year 2021 and for interim periods within that fiscal year. Early adoption is permitted. We elected to remove the disclosures permitted by ASU No. 2018-13 during the fourth quarter of fiscal 2018 but have not early adopted the new required additional disclosures, which is permitted by the guidance. The adoption of this amended guidance is not expected to have a material impact on our consolidated financial statements.

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. The amendments in this ASU introduce a new approach, based on expected losses, to estimate credit losses on certain types of financial instruments. This ASU is intended to provide financial statement users with more decision-useful information about the expected credit losses associated with most financial assets measured at amortized cost and certain other instruments, including trade and other receivables, loans, held-to-maturity debt securities, net investments in leases, and off-balance-sheet credit exposures. Entities are required to apply the provisions of this ASU as a cumulative-effect adjustment to retained earnings as of the beginning of the first reporting period in which the guidance is adopted. This

9

ASU is effective for us beginning September 1, 2020, for our fiscal year 2021 and for interim periods within that fiscal year. We are currently evaluating the impact the adoption will have on our consolidated financial statements.

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842), which replaces the existing guidance within ASC 840 - Leases. The amendments within this ASU, as well as within additional clarifying ASUs issued by the FASB, introduce a lessee model requiring entities to recognize assets and liabilities for most leases, but continue recognizing the associated expenses in a manner similar to existing accounting guidance. In July 2018, the FASB issued ASU No. 2018-10, Codification Improvements to Topic 842, Leases, which amends ASU No. 2016-02, Leases. This ASU is effective for us beginning September 1, 2019, for our fiscal year 2020 and for interim periods within that fiscal year. We have initiated our assessment of the new lease standard, including the utilization of surveys to gather more information about existing leases and the implementation of a new lease software to improve the collection, maintenance and aggregation of lease data necessary for the expanded reporting and disclosure requirements under the new lease standard. It is expected that the primary impact upon adoption will be the recognition, on a discounted basis, of our minimum commitments under noncancelable operating leases as right of use assets and liabilities on our Consolidated Balance Sheets. This will result in a significant increase in assets and liabilities recorded on our Consolidated Balance Sheets. Although we expect the new lease guidance will have a material impact on our Consolidated Balance Sheets, we are continuing to evaluate the practical expedient guidance provisions available and the extent of potential impacts on our consolidated financial statements, processes and internal controls.

Note 2 Restatement of Previously Issued Financial Information

The consolidated financial statements for the three months ended November 30, 2017, have been restated to reflect the correction of misstatements. We have also restated all amounts impacted within the notes to the consolidated financial statements. A description of the adjustments and their impact on the previously issued financial information are included below.

Descriptions of Restatement Adjustments

Restatement Background

During the preparation of our Annual Report on Form 10-K for the year ended August 31, 2018, we noted potentially excessive valuations in the net derivative asset valuations relating to certain rail freight contracts purchased in connection with our North American grain marketing operations. An investigation concluded that the rail freight misstatements included in our consolidated financial statements were due to intentional misconduct by a former employee in our rail freight trading operations, as well as due to rail freight contracts and certain non-rail contracts not meeting the technical accounting requirements to qualify as derivative financial instruments. The misconduct consisted of the former employee manipulating the mark-to-market valuation of rail cars that were the subject of rail freight purchase contracts and manipulating the quantity of rail cars included in the monthly mark-to-market valuation. In addition, the investigation revealed intentional misstatements were made by the former employee to our independent registered public accounting firm in connection with its audit of our consolidated financial statements for the fiscal year ended August 31, 2017. During the course of, and as a result of, the investigation, we terminated the former employee and have taken additional personnel actions.

As described in additional detail in the Explanatory Note in our Annual Report on Form 10-K for the year ended August 31, 2018, the Company restated its audited consolidated financial statements for the fiscal years ended August 31, 2017 and 2016, and our unaudited consolidated financial statements for the quarterly periods ended November 30, 2017 and 2016, February 28, 2018 and 2017, and May 31, 2018 and 2017. As a result of the misstatements, we restated our interim consolidated financial statements for the three months ended November 30, 2017. In addition to the adjustments related to freight derivatives and related misstatements, we also made adjustments related to certain intercompany balances and other historical misstatements unrelated to the freight derivatives and related misstatements.

Consolidated financial statement adjustment tables

The following tables present the impacts of the restatement adjustments to our unaudited Consolidated Statement of Operations, unaudited Consolidated Statement of Comprehensive Income and unaudited Consolidated Statement of Cash Flows for the three months ended November 30, 2017. The restatement references identified in the following tables directly correlate to the restatement adjustments detailed below.

The categories of restatement adjustments and their impact on previously reported consolidated financial statements are described below.

(a) Freight derivatives and related misstatements - Corrections for freight derivatives and related misstatements were

10

driven by the misstatement of amounts associated with both the value and quantity of rail freight contracts, as well as due to rail and certain non-rail freight contracts not meeting the technical accounting requirements to qualify as derivative financial instruments. In addition to the elimination of the underlying freight derivative assets and liabilities and related impacts on revenues and cost of goods sold, additional adjustments were recorded to account for prepaid freight capacity balances in relevant periods. Additional details related to the impact of the freight derivatives and related misstatements and their impact on each period are discussed in restatement reference (a).

(b) Intercompany misstatements - As a result of the work performed in relation to the freight misstatement, additional misstatements related to the incorrect elimination of intercompany balances were also identified and corrected within the consolidated financial statements. Certain of these intercompany misstatements resulted in a misstatement of various financial statement line items; however, the intercompany misstatements did not result in a material misstatement of income (loss) before income taxes or net income (loss). Additional details related to the impact of the intercompany misstatements and their impact on each period are discussed in restatement reference (b).

(c) Other misstatements - We made adjustments for other previously identified misstatements unrelated to the freight derivatives and related misstatements that were not material, individually or in the aggregate, to our consolidated financial statements. These other misstatements related primarily to certain misclassifications, adjustments to revenues and cost of goods sold, and adjustments to various income tax and indirect tax accrual accounts. Additional details related to the impact of the other misstatements and their impact on each period are discussed in restatement reference (c).

11

CHS INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF OPERATIONS

(Unaudited)

For the Three Months Ended November 30, 2017 | |||||||||||||||||||||

As Previously Reported | Restatement Adjustments | As Restated | Accounting Changes* | As Presented | Restatement References | ||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||

Revenues | $ | 8,048,889 | $ | (17,005 | ) | $ | 8,031,884 | $ | — | $ | 8,031,884 | a, b, c | |||||||||

Cost of goods sold | 7,735,627 | (24,570 | ) | 7,711,057 | 335 | 7,711,392 | a, b, c | ||||||||||||||

Gross profit | 313,262 | 7,565 | 320,827 | (335 | ) | 320,492 | |||||||||||||||

Marketing, general and administrative | 140,168 | (668 | ) | 139,500 | 846 | 140,346 | c | ||||||||||||||

Reserve and impairment charges (recoveries), net | (3,787 | ) | — | (3,787 | ) | — | (3,787 | ) | |||||||||||||

Operating earnings (loss) | 176,881 | 8,233 | 185,114 | (1,181 | ) | 183,933 | |||||||||||||||

Interest expense | 40,702 | — | 40,702 | — | 40,702 | ||||||||||||||||

Other (income) loss | (25,014 | ) | — | (25,014 | ) | (1,181 | ) | (26,195 | ) | ||||||||||||

Equity (income) loss from investments | (38,362 | ) | — | (38,362 | ) | — | (38,362 | ) | |||||||||||||

Income (loss) before income taxes | 199,555 | 8,233 | 207,788 | — | 207,788 | ||||||||||||||||

Income tax expense (benefit) | 19,936 | 670 | 20,606 | — | 20,606 | a | |||||||||||||||

Net income (loss) | 179,619 | 7,563 | 187,182 | — | 187,182 | ||||||||||||||||

Net income (loss) attributable to noncontrolling interests | (464 | ) | — | (464 | ) | — | (464 | ) | |||||||||||||

Net income (loss) attributable to CHS Inc. | $ | 180,083 | $ | 7,563 | $ | 187,646 | $ | — | $ | 187,646 | |||||||||||

* Previously reported amounts have been revised to reflect the impact of adopting ASU 2017-17 retrospectively during the first quarter of fiscal 2019. Refer to details related to the adoption of new ASUs within Note 1, Basis of Presentation and Significant Accounting Policies.

Freight derivatives and related misstatements

(a) The correction of freight derivatives and related misstatements resulted in a $0.5 million reduction of income before income taxes and a $1.2 million reduction of net income. These adjustments related to a $0.5 million increase of cost of goods sold and a $0.7 million increase of income tax expense related to the tax effect of the freight derivatives and related misstatements.

Intercompany misstatements

(b) The correction of intercompany misstatements had no impact on income (loss) before income taxes or net income (loss); however, the correction resulted in an $11.4 million decrease of both revenues and cost of goods sold due to different practices of eliminating intercompany sales between CHS's businesses that existed in previous periods.

Other misstatements

(c) The correction of other misstatements resulted in an $8.8 million increase of income before income taxes and net income. The $8.8 million increase of income before income taxes relates primarily to a $6.2 million decrease of cost of goods sold related to the valuation of crack spread derivatives and a $2.6 million decrease in costs related to postretirement benefit plan activity that resulted from a timing difference associated with recording certain benefit plan expenses (included in cost of goods sold and marketing, general and administrative expenses).

Additionally, certain misclassification and offsetting adjustments were made between line items included in the Consolidated Statements of Operations primarily due to the application of differing accounting policies between businesses. These misclassification adjustments resulted in a $5.7 million decrease of revenues and cost of goods sold.

12

CHS INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(Unaudited)

For the Three Months Ended November 30, 2017 | |||||||||||||

As Previously Reported | Restatement Adjustments | As Restated | Restatement References | ||||||||||

(Dollars in thousands) | |||||||||||||

Net income (loss) | $ | 179,619 | $ | 7,563 | $ | 187,182 | a, c | ||||||

Other comprehensive income (loss), net of tax: | |||||||||||||

Postretirement benefit plan activity | 4,196 | (2,602 | ) | 1,594 | c | ||||||||

Unrealized net gain (loss) on available for sale investments | 3,640 | — | 3,640 | ||||||||||

Cash flow hedges | (4 | ) | — | (4 | ) | ||||||||

Foreign currency translation adjustment | (2,607 | ) | 396 | (2,211 | ) | a | |||||||

Other comprehensive income (loss), net of tax | 5,225 | (2,206 | ) | 3,019 | |||||||||

Comprehensive income | 184,844 | 5,357 | 190,201 | ||||||||||

Less comprehensive income attributable to noncontrolling interests | (464 | ) | — | (464 | ) | ||||||||

Comprehensive income attributable to CHS Inc. | $ | 185,308 | $ | 5,357 | $ | 190,665 | |||||||

Freight derivatives and related misstatements

(a) The correction of freight derivatives and related misstatements resulted in a $1.2 million reduction of net income. Refer to descriptions of the adjustments and their impact on net income (loss) in the Consolidated Statement of Operations section for the three months ended November 30, 2017, above. The adjustment related to foreign currency translation is attributable to the foreign currency impact associated with goodwill that was impaired during fiscal 2015.

Intercompany misstatements

(b) None

Other misstatements

(c) The correction of other misstatements resulted in an $8.8 million increase of net income. Refer to descriptions of the adjustments and their impact on net income (loss) in the Consolidated Statement of Operations section for the three months ended November 30, 2017, above. The adjustment related to postretirement benefit plan activity is attributable to a timing difference associated with recording certain benefit plan expenses.

13

CHS INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

For the Three Months Ended November 30, 2017 | |||||||||||||||||||||

As Previously Reported | Restatement Adjustments | As Restated | Accounting Changes* | As Presented | Restatement References | ||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||

Cash flows from operating activities: | |||||||||||||||||||||

Net income (loss) | $ | 179,619 | $ | 7,563 | $ | 187,182 | $ | — | $ | 187,182 | a, c | ||||||||||

Adjustments to reconcile net income to net cash provided by (used in) operating activities: | |||||||||||||||||||||

Depreciation and amortization | 120,148 | — | 120,148 | — | 120,148 | ||||||||||||||||

Amortization of deferred major repair costs | 16,418 | — | 16,418 | — | 16,418 | ||||||||||||||||

Equity (income) loss from investments | (38,362 | ) | — | (38,362 | ) | — | (38,362 | ) | |||||||||||||

Distributions from equity investments | 12,514 | — | 12,514 | — | 12,514 | ||||||||||||||||

Provision for doubtful accounts | (3,601 | ) | — | (3,601 | ) | — | (3,601 | ) | |||||||||||||

Deferred taxes | 15,044 | 1,302 | 16,346 | — | 16,346 | a | |||||||||||||||

Other, net | 2,976 | (2,601 | ) | 375 | — | 375 | c | ||||||||||||||

Changes in operating assets and liabilities, net of acquisitions: | |||||||||||||||||||||

Receivables | (80,637 | ) | 23,937 | (56,700 | ) | — | (56,700 | ) | c | ||||||||||||

Inventories | (472,180 | ) | (40,843 | ) | (513,023 | ) | — | (513,023 | ) | c | |||||||||||

Derivative assets | 67,365 | (3,439 | ) | 63,926 | — | 63,926 | a, c | ||||||||||||||

Margin and related deposits | (893 | ) | — | (893 | ) | — | (893 | ) | |||||||||||||

Supplier advance payments | (292,905 | ) | (631 | ) | (293,536 | ) | — | (293,536 | ) | b | |||||||||||

Other current assets and other assets | 2,689 | 883 | 3,572 | 2,751 | 6,323 | a | |||||||||||||||

Customer margin deposits and credit balances | (18,045 | ) | — | (18,045 | ) | — | (18,045 | ) | |||||||||||||

Customer advance payments | 1,278 | (11,529 | ) | (10,251 | ) | — | (10,251 | ) | b, c | ||||||||||||

Accounts payable and accrued expenses | 441,071 | 12,148 | 453,219 | — | 453,219 | a, c | |||||||||||||||

Derivative liabilities | (97,329 | ) | (2,627 | ) | (99,956 | ) | — | (99,956 | ) | a, c | |||||||||||

Other liabilities | 4,376 | — | 4,376 | — | 4,376 | ||||||||||||||||

Net cash provided by (used in) operating activities | (140,454 | ) | (15,837 | ) | (156,291 | ) | 2,751 | (153,540 | ) | ||||||||||||

Cash flows from investing activities: | |||||||||||||||||||||

Acquisition of property, plant and equipment | (85,824 | ) | — | (85,824 | ) | — | (85,824 | ) | |||||||||||||

Proceeds from disposition of property, plant and equipment | 56,079 | — | 56,079 | — | 56,079 | ||||||||||||||||

Proceeds from sale of business | 29,457 | — | 29,457 | — | 29,457 | ||||||||||||||||

Expenditures for major repairs | (1,039 | ) | — | (1,039 | ) | — | (1,039 | ) | |||||||||||||

Investments redeemed | 5,195 | — | 5,195 | — | 5,195 | ||||||||||||||||

Changes in CHS Capital notes receivable, net | (69,227 | ) | — | (69,227 | ) | — | (69,227 | ) | |||||||||||||

Financing extended to customers | (15,778 | ) | — | (15,778 | ) | — | (15,778 | ) | |||||||||||||

Payments from customer financing | 16,520 | — | 16,520 | — | 16,520 | ||||||||||||||||

Other investing activities, net | 1,847 | — | 1,847 | — | 1,847 | ||||||||||||||||

Net cash provided by (used in) investing activities | (62,770 | ) | — | (62,770 | ) | — | (62,770 | ) | |||||||||||||

Cash flows from financing activities: | |||||||||||||||||||||

Proceeds from lines of credit and long-term borrowings | 8,006,980 | — | 8,006,980 | — | 8,006,980 | ||||||||||||||||

Payments on lines of credit, long-term borrowings and capital lease obligations | (7,657,713 | ) | 3,052 | (7,654,661 | ) | — | (7,654,661 | ) | c | ||||||||||||

Preferred stock dividends paid | (42,167 | ) | — | (42,167 | ) | — | (42,167 | ) | |||||||||||||

Redemptions of equities | (3,682 | ) | — | (3,682 | ) | — | (3,682 | ) | |||||||||||||

Other financing activities, net | (31,680 | ) | 10,423 | (21,257 | ) | — | (21,257 | ) | c | ||||||||||||

Net cash provided by (used in) financing activities | 271,738 | 13,475 | 285,213 | — | 285,213 | ||||||||||||||||

Effect of exchange rate changes on cash and cash equivalents | 2,236 | — | 2,236 | — | 2,236 | ||||||||||||||||

Net increase (decrease) in cash and cash equivalents and restricted cash | 70,750 | (2,362 | ) | 68,388 | 2,751 | 71,139 | b | ||||||||||||||

Cash and cash equivalents and restricted cash at beginning of period | 181,379 | — | $ | 181,379 | 90,893 | 272,272 | |||||||||||||||

Cash and cash equivalents and restricted cash at end of period | $ | 252,129 | $ | (2,362 | ) | $ | 249,767 | $ | 93,644 | $ | 343,411 | ||||||||||

* Previously reported amounts have been revised to reflect the impact of adopting ASU 2016-18 retrospectively during the first quarter of fiscal 2019. Refer to details related to the adoption of new ASUs within Note 1, Basis of Presentation and Significant Accounting Policies.

14

Freight derivatives and related misstatements

(a) The correction of freight derivatives and related misstatements resulted in a $1.2 million reduction of net income for the three months ended November 30, 2017. Refer to descriptions of the adjustments and their impact on net income (loss) in the Consolidated Statement of Operations section for the three months ended November 30, 2017, above. The impact of the adjustments to the Consolidated Balance Sheets as of August 31, 2017, and November 30, 2017, resulted in certain misclassifications of less than $3.0 million between operating activity line items in the Consolidated Statements of Cash Flows; however, none of the freight derivatives and related misstatements impacted the classifications between operating, investing or financing activities.

Intercompany misstatements

(b) The correction of intercompany misstatements did not impact net income for the three months ended November 30, 2017; however, the impact of adjustments to the Consolidated Balance Sheets as of August 31, 2017, and November 30, 2017, resulted in certain misclassification adjustments of less than $3.0 million between line items in the Consolidated Statements of Cash Flows. None of the intercompany misstatements impacted the classifications between operating, investing or financing activities within the Consolidated Statements of Cash Flows; however, a timing difference related to the application of supplier advance payments resulted in a $2.4 million decrease of cash as of November 30, 2017.

Other misstatements

(c) The correction of other misstatements resulted in an $8.8 million increase of net income for the three months ended November 30, 2017. Refer to further details of the adjustments and their impact on net income (loss) in the Consolidated Statement of Operations section for the three months ended November 30, 2017, above. The impact of the adjustments to the Consolidated Balance Sheets as of August 31, 2017, and November 30, 2017, resulted in certain misclassification adjustments between line items in the Consolidated Statements of Cash Flows. As a result, two misclassification adjustments were made between operating and financing activities, including a $3.1 million reduction of notes payable resulting from a duplicative entry and the misclassification of a $10.4 million negative cash balance associated with a timing difference for the application of in-transit cash. In addition, various misclassification adjustments were made between operating activity lines, the most significant of which related to (1) a $24.1 million decrease of inventory and increase in accounts receivable as of August 31, 2017, due to a timing difference related to the settlement of a single ocean vessel and (2) the $18.3 million net impact associated with the decrease of inventory and increase of accounts payable that resulted from the misclassification adjustment for certain items previously included within a contra-inventory account to accounts payable as of August 31, 2017, and November 30, 2017.

15

Note 3 Revenues

Adoption of New Revenue Guidance

As described in Note 1, Basis of Presentation and Significant Accounting Policies, we adopted the guidance within ASU 2014-09 as of September 1, 2018, using the modified retrospective transition approach. Consistent with other companies that actively trade commodities, a majority of our revenues are attributable to forward commodity sales contracts that are considered to be physically settled derivatives under ASC 815, Derivatives and Hedging (ASC Topic 815) and therefore fall outside the scope of ASC Topic 606. As a result, these revenues are not subject to the provisions of the new revenue guidance and the impact of adoption is limited to our revenue streams that fall within the scope of the new revenue guidance.

The majority of our revenue streams that fall within the scope of the new revenue guidance are recognized at a point-in-time; however, the adoption of ASU 2014-09 resulted in a minimal number of changes to the timing of revenue recognition for certain revenue streams. Under the modified retrospective method of adoption, we determined the cumulative effect of adoption for all contracts with customers that had not been completed as of the adoption date and recognized an adjustment of less than $1.0 million to the opening capital reserves balance within the Consolidated Balance Sheet as of September 1, 2018. Additionally, the impact of applying ASC Topic 606 compared to previous guidance during the three months ended November 30, 2018, was an overall decrease to revenues of $13.1 million.

The change in accounting for revenue recognition under ASU 2014-09 did not have a material impact on our Consolidated Statement of Operations for the three months ended November 30, 2018, or Consolidated Balance Sheet as of November 30, 2018.

Revenue Recognition Accounting Policy and Performance Obligations

We provide a wide variety of products and services, from agricultural inputs such as fuels, farm supplies and crop nutrients, to agricultural outputs that include grain and oilseed, processed grains and oilseeds and food products, and ethanol production and marketing. We primarily conduct our operations and derive revenues within our Energy and Ag businesses. Our Energy business derives its revenues through refining, wholesaling and retailing of petroleum products. Our Ag business derives its revenues through the origination and marketing of grain, including service activities conducted at export terminals; through wholesale sales of crop nutrients and processed sunflowers; from sales of soybean meal, soybean refined oil and soyflour products; through the production and marketing of renewable fuels; and through retail sales of petroleum and agronomy products, and feed and farm supplies.

Revenue is recognized when performance obligations under the terms of a contract with a customer are satisfied, which generally occurs when control of the goods has transferred to customers. For the majority of our contracts with customers, control transfers to customers at a point-in-time when goods/services have been delivered, as that is generally when legal title, physical possession and risks and rewards of goods/services transfers to the customer. In limited arrangements, control transfers over time as the customer simultaneously receives and consumes the benefits of the service as we complete our performance obligation(s).

Revenue is recognized at the transaction price that we expect to be entitled to in exchange for transferring goods or services to a customer, excluding amounts collected on behalf of third parties. We follow a policy of recognizing revenue at the point-in-time or over the period of time that we satisfy our performance obligation by transferring control over a product or service to a customer in accordance with the underlying contract. For physically settled derivative sales contracts that are outside the scope of the revenue guidance, we recognize revenue when control of the inventory is transferred within the meaning of ASC Topic 606.

The amount of revenue recognized during the three months ended November 30, 2018, for performance obligations that were fully satisfied in previous periods was not material.

Shipping and Handling Costs

Shipping and handling amounts billed to a customer as part of a sales transaction are included in revenues, and the related costs are included in cost of goods sold. Shipping and handling is treated as a fulfillment activity rather than a promised service, and therefore is not considered a separate performance obligation.

16

Taxes Collected from Customers and Remitted to Governmental Authorities

Revenue is recorded net of taxes collected from customers that are remitted to governmental authorities, with the collected taxes recorded as current liabilities until remitted to the relevant government authority.

Contract Costs

Commissions related to contracts with a duration of less than one year are expensed as incurred. We recognize incremental costs of obtaining contracts as an expense when incurred if the amortization period of the assets we otherwise would have recognized is one year or less.

Disaggregation of Revenues

The following table presents revenues recognized under ASC Topic 606 disaggregated by reportable segment, as well as the amount of revenues recognized under ASC Topic 815 and other applicable accounting guidance for the three months ended November 30, 2018. Other applicable accounting guidance primarily includes revenues recognized under ASC Topic 840, Leases and ASC Topic 470, Debt that fall outside the scope of ASC Topic 606.

ASC 606 | ASC 815 | Other Guidance | Total Revenues | |||||||||||||

For the Three Months Ended November 30, 2018: | (Dollars in thousands) | |||||||||||||||

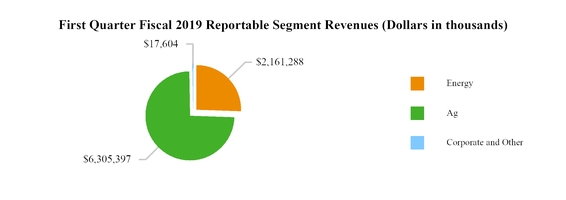

Energy | $ | 1,940,190 | $ | 221,098 | $ | — | $ | 2,161,288 | ||||||||

Ag | 1,355,826 | 4,913,428 | 36,143 | 6,305,397 | ||||||||||||

Corporate and Other | 5,234 | — | 12,370 | 17,604 | ||||||||||||

Total revenues | $ | 3,301,250 | $ | 5,134,526 | $ | 48,513 | $ | 8,484,289 | ||||||||

Less than 1% of revenues accounted for under ASC Topic 606 included within the table above are recorded over time; these revenues are primarily related to service contracts.

Our Energy segment derives its revenues through refining, wholesaling and retailing of petroleum products. Our Energy segment produces and sells (primarily wholesale) gasoline, diesel fuel, propane, asphalt, lubricants and other related products and provides transportation services. We are the nation’s largest cooperative energy company, with operations that include petroleum refining and pipelines; the supply, marketing and distribution of refined fuels (gasoline, diesel fuel and other energy products); the blending, sale and distribution of lubricants; and the wholesale supply of propane and other natural gas liquids. For the majority of revenues arising from sales to Energy customers, we satisfy our performance obligation of providing energy products such as gasoline, diesel fuel, propane, asphalt, lubricants and other related products at the point-in-time that the finished petroleum product is delivered or made available to the wholesale or retail customer, at which point control is considered to have been transferred to the customer and revenue can be recognized, as there are no remaining performance obligations that we need to satisfy in order to be entitled to the agreed-upon transaction price as stated in the contract. For fixed and provisionally-priced derivative sales contracts that are accounted for under the provisions of the derivative accounting guidance and are outside the scope of the revenue recognition guidance, we recognize revenue when control of the inventory is transferred within the meaning of ASC 606.

Our Ag segment derives its revenues through the origination and marketing of grain, including service activities conducted at export terminals; through wholesale sales of crop nutrients and processed sunflowers; from sales of soybean meal, soybean refined oil and soyflour products; through the production and marketing of renewable fuels; and through retail sales of petroleum and agronomy products, and feed and farm supplies. For the majority of revenues arising from sales to Ag customers, we satisfy our performance obligation of delivering a commodity or other agricultural end product to a customer at the point-in-time that the commodity or other end-product (wholesale grain, crop nutrients/agronomy products, soybean products, ethanol or country operations retail products) has been delivered or is made available to the customer, at which point control is considered to have been transferred to the customer and revenue can be recognized, as there are no remaining performance obligations that need to be satisfied in order to be entitled to the agreed-upon transaction price as stated in the contract. The amount of revenue recognized follows the contractually specified price, which may include freight or other contractually specified cost components. For fixed and provisionally-priced derivative sales contracts that are accounted for under the provisions of the derivative accounting guidance and are outside the scope of the revenue recognition guidance, we recognize revenue when control of the inventory is transferred within the meaning of ASC Topic 606.

17

Corporate and Other primarily consists of our financing and hedging businesses, which are presented together due to the similar nature of their products and services as well as the relatively lower amount of revenues for those businesses compared to our Ag and Energy businesses. Prior to its sale on May 4, 2018, our insurance business was also included in Corporate and Other. Revenues arising from Corporate and Other are primarily comprised of revenues generated by our hedging and financing businesses. Revenues from our hedging business are primarily recognized at the point-in-time that the hedging transaction is completed after we have fully satisfied all performance obligations under the contract, and revenues arising from our financing business are recognized in accordance with ASC Topic 470, Debt, and fall outside the scope of ASC Topic 606.

Contract Assets and Contract Liabilities

Contract assets relate to unbilled amounts arising from goods that have already been transferred to the customer where the right to payment is not conditional upon the passage of time. This results in the recognition of an asset, as the amount of revenue recognized at a certain point in time exceeds the amount billed to the customer. Contract assets are recorded in accounts receivable within our Consolidated Balance Sheets and were immaterial as of November 30, 2018, and August 31, 2018.

Contract liabilities relate to advance payments from customers for goods and services that we have yet to provide. Contract liabilities of $187.9 million and $177.9 million as of November 30, 2018, and August 31, 2018, respectively, are recorded within customer advance payments on our Consolidated Balance Sheets. For the three months ended November 30, 2018, we recognized revenues of $95.2 million, which were included in the customer advance payments balance at the beginning of the period.

Practical expedients

We applied ASC Topic 606 utilizing the following allowable exemptions or practical expedients:

• | Election to not disclose the unfulfilled performance obligation balance for contracts with an original duration of one year or less. |

• | Recognition of the incremental costs of obtaining a contract as an expense when incurred if the amortization period of the asset that would otherwise have been recognized is one year or less. |

• | Election to present revenues net of sales taxes and other similar taxes. |

• | Practical expedient to treat shipping and handling as a fulfillment activity rather than a promised service, resulting in the conclusion that shipping and handling is not a separate performance obligation. |

Note 4 Receivables

November 30, 2018 | August 31, 2018 | ||||||

(Dollars in thousands) | |||||||

Trade accounts receivable | $ | 1,743,258 | $ | 1,578,764 | |||

CHS Capital notes receivable | 683,407 | 569,379 | |||||

Other | 486,398 | 534,071 | |||||

2,913,063 | 2,682,214 | ||||||

Less: allowances and reserves | 226,968 | 221,813 | |||||

Total receivables | $ | 2,686,095 | $ | 2,460,401 | |||

Trade Accounts

Trade accounts receivable are initially recorded at a selling price, which approximates fair value, upon the sale of goods or services to customers. Subsequently, trade accounts receivable are carried at net realizable value, which includes an allowance for estimated uncollectible amounts. We calculate this allowance based on our history of write-offs, level of past due accounts, and our relationships with, and the economic status of, our customers.

18

CHS Capital

Notes Receivable

CHS Capital, LLC ("CHS Capital"), our wholly-owned subsidiary, has short-term notes receivable from commercial and producer borrowers. The short-term notes receivable have maturity terms of 12 months or less and are reported at their outstanding unpaid principal balances, adjusted for the allowance of loan losses, as CHS Capital has the intent and ability to hold the applicable loans for the foreseeable future or until maturity or pay-off. The carrying value of CHS Capital short-term notes receivable approximates fair value, given the notes' short duration and the use of market pricing adjusted for risk.

The notes receivable from commercial borrowers are collateralized by various combinations of mortgages, personal property, accounts and notes receivable, inventories and assignments of certain regional cooperative’s capital stock. These loans are primarily originated in the states of Minnesota, Wisconsin and North Dakota. CHS Capital also has loans receivable from producer borrowers that are collateralized by various combinations of growing crops, livestock, inventories, accounts receivable, personal property and supplemental mortgages and are originated in the same states as the commercial notes as well as in Michigan.

In addition to the short-term balances included in the table above, CHS Capital had long-term notes receivable, with durations of generally not more than 10 years, totaling $211.3 million and $203.0 million at November 30, 2018, and August 31, 2018, respectively. The long-term notes receivable are included in Other assets on our Consolidated Balance Sheets. As of November 30, 2018, and August 31, 2018, the commercial notes represented 52% and 40%, respectively, and the producer notes represented 48% and 60%, respectively, of the total CHS Capital notes receivable.

CHS Capital has commitments to extend credit to customers if there are no violations of any contractually established conditions. As of November 30, 2018, CHS Capital's customers had additional available credit of $567.4 million.

Allowance for Loan Losses and Impairments

CHS Capital maintains an allowance for loan losses which is the estimate of potential incurred losses inherent in the loans receivable portfolio. In accordance with FASB ASC 450-20, Accounting for Loss Contingencies, and ASC 310-10, Accounting by Creditors for Impairment of a Loan, the allowance for loan losses consists of general and specific components. The general component is based on historical loss experience and qualitative factors addressing operational risks and industry trends. The specific component relates to loans receivable that are classified as impaired. Additions to the allowance for loan losses are reflected within reserve and impairment charges (recoveries), net in the Consolidated Statements of Operations. The portion of loans receivable deemed uncollectible is charged off against the allowance. Recoveries of previously charged off amounts increase the allowance for loan losses. The amount of CHS Capital notes that were past due was not significant at any reporting date presented.

Interest Income

Interest income is recognized on the accrual basis using a method that computes simple interest daily. The accrual of interest on commercial loans receivable is discontinued at the time the commercial loan receivable is 90 days past due unless the credit is well-collateralized and in process of collection. Past due status is based on contractual terms of the loan. Producer loans receivable are placed in non-accrual status based on estimates and analysis due to the annual debt service terms inherent to CHS Capital’s producer loans. In all cases, loans are placed in nonaccrual status or charged off at an earlier date if collection of principal or interest is considered doubtful.

Other Receivables

Other receivables are comprised of certain other amounts recorded in the normal course of business, including receivables related to value-added taxes and pre-crop financing, primarily to Brazilian farmers, to finance a portion of supplier production costs. We do not bear any of the costs or operational risks associated with the related growing crops, though our ability to be paid depends on the crops actually produced. The financing is collateralized by future crops, land and physical assets of the suppliers, carries a local market interest rate and settles when the farmer’s crop is harvested and sold.

19

Note 5 Inventories

November 30, 2018 | August 31, 2018 | ||||||

(Dollars in thousands) | |||||||

Grain and oilseed | $ | 1,525,151 | $ | 1,298,522 | |||

Energy | 680,807 | 715,161 | |||||

Crop nutrients | 325,189 | 246,326 | |||||

Feed and farm supplies | 522,490 | 391,906 | |||||

Processed grain and oilseed | 113,138 | 99,426 | |||||

Other | 17,674 | 17,308 | |||||

Total inventories | $ | 3,184,449 | $ | 2,768,649 | |||

As of November 30, 2018, we valued approximately 14% of inventories, primarily related to our Energy segment, using the lower of cost, determined on the LIFO method, or net realizable value (16% as of August 31, 2018). If the FIFO method of accounting had been used, inventories would have been higher than the reported amount by $115.6 million and $345.0 million as of November 30, 2018, and August 31, 2018, respectively. An actual valuation of inventory under the LIFO method can be made only at the end of each year based on the inventory levels and costs at that time. Interim LIFO calculations are based on management's estimates of expected year-end inventory levels and are subject to the final year-end LIFO inventory valuation.

Note 6 Investments

November 30, 2018 | August 31, 2018 | ||||||

(Dollars in thousands) | |||||||

Equity method investments: | |||||||

CF Industries Nitrogen, LLC | $ | 2,775,989 | $ | 2,735,073 | |||

Ventura Foods, LLC | 367,429 | 360,150 | |||||

Ardent Mills, LLC | 212,887 | 205,898 | |||||

Other equity method investments | 294,130 | 288,016 | |||||

Cost method investments | 124,101 | 122,788 | |||||

Total investments | $ | 3,774,536 | $ | 3,711,925 | |||

Equity Method Investments

Joint ventures and other investments, in which we have significant ownership and influence, but not control, are accounted for in our consolidated financial statements using the equity method of accounting. Our primary equity method investments are described below.

CF Nitrogen

On February 1, 2016, we invested $2.8 billion in CF Industries Nitrogen, LLC ("CF Nitrogen"), commencing our strategic venture with CF Industries Holdings, Inc. ("CF Industries"). The investment consists of an approximate 10% membership interest (based on product tons) in CF Nitrogen. We account for this investment using the hypothetical liquidation at book value method, recognizing our share of the earnings and losses of CF Nitrogen based upon our contractual claims on the entity's net assets pursuant to the liquidation provisions of CF Nitrogen's limited liability company agreement, adjusted for the semi-annual cash distributions we receive as a result of our membership interest in CF Nitrogen. For the three months ended November 30, 2018, and 2017, this amount was $40.9 million and $20.3 million, respectively. These amounts are included as equity income from investments in our Nitrogen Production segment.

20

Ventura Foods and Ardent Mills

We have a 50% interest in Ventura Foods, LLC ("Ventura Foods"), which is a joint venture that produces and distributes primarily vegetable oil-based products, and we have a 12% interest in Ardent Mills, LLC ("Ardent Mills"), which is a joint venture with Cargill Incorporated and ConAgra Foods, Inc. that combines the North American flour milling operations of the three parent companies. We account for Ventura Foods and Ardent Mills as equity method investments included in Corporate and Other.

The following table provides aggregate summarized unaudited financial information for our equity method investments in CF Nitrogen, Ventura Foods and Ardent Mills for the three months ended November 30, 2018, and 2017:

For the Three Months Ended November 30, | |||||||

2018 | 2017 | ||||||

(Dollars in thousands) | |||||||

Net sales | $ | 2,241,539 | $ | 2,081,514 | |||

Gross profit | 339,937 | 211,432 | |||||

Net earnings | 272,736 | 112,071 | |||||

Earnings attributable to CHS Inc. | 67,668 | 28,766 | |||||

Our investments in other equity method investees are not significant in relation to our consolidated financial statements, either individually or in the aggregate.

Note 7 Goodwill and Other Intangible Assets

Goodwill of $138.5 million is included in other assets on our Consolidated Balance Sheets as of November 30, 2018, and August 31, 2018. There were no changes in the net carrying amount of goodwill for the three months ended November 30, 2018.

Intangible assets subject to amortization primarily include customer lists, trademarks and non-compete agreements, and are amortized over their respective useful lives (ranging from 2 to 30 years). Information regarding intangible assets that are included in other assets on our Consolidated Balance Sheets is as follows:

November 30, 2018 | August 31, 2018 | ||||||||||||||||||||||

Gross Carrying Amount | Accumulated Amortization | Net | Gross Carrying Amount | Accumulated Amortization | Net | ||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||||

Customer lists | $ | 40,815 | $ | (13,791 | ) | $ | 27,024 | $ | 40,815 | $ | (13,082 | ) | $ | 27,733 | |||||||||

Trademarks and other intangible assets | 6,536 | (4,990 | ) | 1,546 | 6,536 | (4,931 | ) | 1,605 | |||||||||||||||