Attached files

| file | filename |

|---|---|

| 8-K/A - 8-K/A - SANGAMO THERAPEUTICS, INC | sgmo-8ka_20181101.htm |

| EX-99.3 - EX-99.3 - SANGAMO THERAPEUTICS, INC | sgmo-ex993_6.htm |

| EX-99.1 - EX-99.1 - SANGAMO THERAPEUTICS, INC | sgmo-ex991_7.htm |

| EX-23.1 - EX-23.1 - SANGAMO THERAPEUTICS, INC | sgmo-ex231_9.htm |

Exhibit 99.2

A French limited liability company (société anonyme) with a share capital of €5,100,180.60

Registered office: Les Cardoulines, Allée de la Nertière,

06560 Valbonne –Sophia Antipolis

Grasse Trade and Companies Register n° 435 361 209

__________________________________________________________________________________

CONDENSED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2018

|

1.1 |

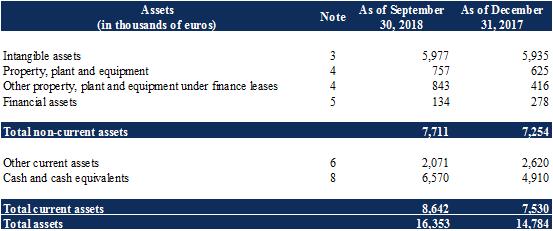

Assets |

Exhibit 99.2

Exhibit 99.2

Items of other comprehensive income / (loss):

Exhibit 99.2

Exhibit 99.2

Exhibit 99.2

|

|

Note 1 : |

The Company |

TxCell S.A. (the "Company") is a biotechnology company, listed on Euronext Paris, which develops innovative personalized cellular immunotherapies for the treatment of severe inflammatory and autoimmune diseases with high unmet medical need. TxCell S.A. targets graft rejections, as well as various autoimmune diseases (T-cell or B-cell), including multiple sclerosis, renal lupus and bullous pemphigoid.

Highlights of the period

On February 2, 2018, the Company received a zero-interest loan from Bpifrance in the gross amount of €1.2 million as part of preclinical development and non-clinical pharmaceutical development of a CAR-Treg targeting HLA-A2 for the prevention of chronic rejection after organ transplantation.

On July 23, 2018, the Company announced the acquisition by Sangamo Therapeutics, Inc. (“Sangamo”), subject to the fulfillment of conditions precedent, of approximately 53% of the Company's capital, and the intention of Sangamo, if applicable, to file a simplified cash tender offer for the remaining outstanding common shares of the Company at the same unit price of €2.58, representing an enterprise value of approximately €72 million on a basis without cash and without debt.

On July 23, 2018, the Company also announced the renegotiation of its OCABSA financing program. Subject to the effective completion of Sangamo's proposed acquisition of a majority stake in the Company, the contract provides for (i) the repurchase by the Company of 50% of the 56 unconverted OCA for a total amount of €3,080,000 (i.e. 110% of their total nominal value of €2,800,000), (ii) Yorkville's conversion of the remaining 28 OCA into 1,866,666 new shares of the Company at a fixed unit price of €1.50, and (iii) ) the repurchase by the Company of the 84 Tranche Warrants and the 1,236,350 BSA warrants currently held by Yorkville for the lump sum of one euro, with a view to their cancellation.

As at September 30, 2018, 66 Warrants have been exercised at the request of the Company which then issued 66 OCA to Yorkville for a total nominal amount of €6.6 million, from which 550,000 BSA were detached. As at September 30, 2018, there are therefore 120 Warrants in circulation. As at September 30, 2018, there are 56 outstanding notes convertible into shares (OCA) that remain to be converted, for a total nominal amount of €5.6 million.

|

|

Note 2 : |

Accounting principles and methods |

The financial statements are presented in thousands of euros, except share and per share amounts.

Figures have been rounded up or down when calculating certain financial items and other information contained in the financial statements. Consequently, the totals given in certain tables may not be the exact sum of the figures that precede them.

|

|

Note 2.1 : |

Basis of preparation of the financial statements |

These financial statements were approved on November 16, 2018 by the board of directors.

The condensed interim financial statements of the Company as at September 30, 2018 have been prepared in accordance with IAS 34 “Interim Financial Reporting”.

They do not include all the information necessary for a complete set of financial statements in accordance with IFRS and must be read in addition to the Company's annual IFRS financial statements for the year ended December 31, 2017.

They include, however, a selection of notes explaining significant events and transactions with a view to understanding the changes in the Company's financial position and performance since the last annual IFRS financial statements for the year ended December 31, 2017.

The accounting principles used to prepare the accompanying condensed interim financial statements comply with the IFRS standards and interpretations as adopted by the International Accounting Standards Board (IASB). The accounting principles used are identical to those used to prepare the IFRS

Exhibit 99.2

financial statements for the financial year ended December 31, 2017, with the exception of the application of the following new standards, amendments to standards and interpretations below and compulsory for fiscal periods after January 1, 2018:

|

|

• |

IFRS 15: “Revenue from Contracts with Customers”, |

|

|

• |

IFRS 9: “Financial Instruments”, |

|

|

• |

the annual improvements of the IFRS: 2014-2016 cycle; |

|

|

• |

amendments to IFRS 1, IFRS 12 and IAS 28; |

|

|

• |

amendments to IFRS 2: “Clarifications and classification and measurement of share-based payment transacations”. |

The application of these amendments and standards had no significant impact on the financial statements.

Furthermore, the Company decided not to proceed with the early application of new standards, amendments, revisions and interpretations if their application was compulsory after September 30, 2018, notably IFRS 16 “Leases”. IFRS 16 specifies how an entity will recognize, measure, present and disclose leases. IFRS 16 eliminates the current classification model for lessee’s lease contracts as either operating or finance leases and, instead, introduces a single lessee accounting model requiring a lessee to recognize right-of-use assets and lease liabilities for leases with a term of more than 12 months, unless the underlying asset is of low value. This brings the previous off-balance leases on the balance sheet in a manner largely comparable to current finance lease accounting. IFRS 16 will be applicable for annual reporting periods beginning on or after January 1, 2019 and the Company is still in the process of assessing the impact on the financial statements.

Principle of preparation of the financial statements

The financial statements have been prepared on a historical-cost basis, with the exception of financial assets and liabilities, which are measured at fair value, in accordance with the IFRS provisions. The categories concerned are mentioned in the following notes.

Use of judgments and estimates

Preparing the financial statements in accordance with IFRS requires the formulation of estimates and assumptions that affect the amounts and disclosures contained therein. Actual results may differ significantly from these estimates, depending on the different conditions and assumptions used, and where such differences are material, sensitivity analysis may be carried out as applicable. The main judgments and estimates are described below:

|

|

• |

Valuation of stock option subscription plans, warrants, free shares and notes convertible into shares (see Notes 2.9 and 9.3); |

|

|

• |

Recognition of deferred taxes on loss carryforwards (see Notes 2.15 and 18); |

|

|

• |

Valuation of provisions for risks and charges (see Notes 2.11.1 and 11); |

|

|

• |

Valuation of capitalized rights under the license acquired (see Note 3). |

|

|

Note 2.2 : |

Going-concern principle |

The September 30, 2018 financial statements were prepared in accordance with the going concern principle. Based on its development plan, the Company has taken into account the following factors:

|

|

• |

The Company’s historical loss-making position is the result of the innovative nature of its products, which require several years of research and development; |

Exhibit 99.2

|

|

subscription warrants (OCABSA) for a nominal amount of €6.6 million and proceeds of €4.5 million loan granted by Sangamo. |

The Company estimates, based on its growth plan and the cash and cash equivalent described above, that it is not exposed to any short-term liquidity risk for the next 12 months following the reporting date (refer to Events subsequent to the reporting period presented in Note 23).

|

|

Note 2.3 : |

Intangible assets |

In accordance with International Accounting Standard (IAS) 38 “Intangible Assets”, acquired intangible assets are recognized at acquisition cost on the statement of financial position. Impairment tests are performed on intangible, non-amortizable assets and intangible assets in progress at the end of each financial year. The method currently used for this valuation is the discounted cash flow (DCF) method.

Note 2.3.1 : Research and development expenses

Research costs are recognized as an expense when incurred.

In accordance with IAS 38, development costs are recognized in intangible assets only if the Company can demonstrate all of the following:

|

• |

the technical feasibility of completing the intangible asset so that it will be available for use or sale; |

|

• |

its intention to complete the intangible asset and use or sell it; |

|

• |

its ability to use or sell the intangible asset; |

|

• |

how the intangible asset will generate probable future economic benefits; |

|

• |

the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset; and |

|

• |

its ability to measure reliably the expenditures during its development. |

Pursuant to this standard, the Company recognizes all its research and development costs as expenses. The Company considers that the technical feasibility of its development projects is not demonstrated until the required marketing authorizations are issued, which also corresponds to the time at which virtually all of the development costs have been incurred.

Note 2.3.2 : Patents

Costs associated with filing patents, and incurred by the Company before those patents are secured, are recognized in expenses, consistent with the approach used for research and development costs.

Note 2.3.3 : Software

The costs of acquiring software licenses are recorded in assets, based on the costs incurred to acquire and use the software concerned.

Software is amortized on a straight-line basis over its estimated useful life, which is generally three years.

The software amortization charge is recognized in the “Research and development expenses” or “General and administrative expenses” category depending on the nature of the use of the software.

Note 2.3.4 : Other intangible assets

The acquisition costs of other intangible assets are recorded in assets when they can be measured reliably.

Other intangible assets are recognized as in progress up until the date when they satisfy the conditions to be used.

Exhibit 99.2

Property, plant and equipment are recognized at acquisition cost. Costs arising from major renovation and improvement work are capitalized. Costs arising from repairs, maintenance and other renovation work are expensed as they are incurred.

Assets not yet put into service are recognized as assets in progress and are not depreciated. Once they have been put into service, property, plant and equipment are depreciated on a straight-line basis over their estimated useful lives.

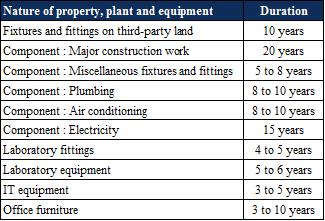

The following useful lives are applicable:

The property, plant and equipment amortization charge is recognized in the “Research and development expenses” or “General and administrative expenses” category depending on the use of the assets held.

Note 2.4.1 : Finance leases

Leased property that meets the conditions to be classified as a finance lease is capitalized at the purchase value as at the date of the lease. Each lease payment is broken down between the payable (capital amortization) and the financial cost so as to determine a constant interest rate on the remaining amounts due. The present value of lease payments is reported as finance leases liabilities. The part of the lease payment corresponding to the interest is reported under expense over the duration of the finance lease. Property, plant and equipment acquired under a finance lease is amortized over the duration of use. Lease payments due in more than one year's time are reported as Debts related to finance leases - non-current; those due in under one year are reported as Debts related to finance leases - current.

|

|

Note 2.5 : |

Financial assets |

Financial assets at fair value through profit or loss

This category includes marketable securities, cash and cash equivalents. They represent financial assets held for trading purposes, i.e., assets acquired by the Company to be sold in the short-term. They are measured at fair value and changes in fair value are recognized in the statement of operations as financial income or expense, as applicable.

Financial assets at amortized cost

This category includes Other financial assets (non-current), Trade receivables (current) and Other receivables and related accounts (current). Other financial assets (non-current) include advances and deposits granted to third parties as well as term deposits, which are not considered as cash equivalents.

Financial assets at amortized cost primarily consist of deposits and guarantees, restricted cash, trade receivables, other receivables, conditional advances and loans. They are non-derivative financial assets with fixed or determinable payments that are not listed on an active market. They are initially recognized at fair value plus transaction costs that are directly attributable to the acquisition or issue of the financial asset, except trade receivables that are initially recognized at the transaction price as defined in IFRS 15.

Exhibit 99.2

After initial recognition, these financial assets are measured at amortized cost using the effective interest rate method when both of the following conditions are met:

|

|

(a) |

the financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows; and |

|

|

(b) |

the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. |

Gains and losses are recorded in the statement of operations when they are derecognized, subject to modification of contractual cash flows and/or impaired.

IFRS 9 “Financial Instruments” requires an entity to recognize a loss allowance for expected credit losses on a financial asset at amortized cost at each Statement of Financial Position date. The amount of the loss allowance for expected credit losses equal to: (i) the 12- month expected credit losses or (ii) the full lifetime expected credit losses. The latter applies if credit risk has increased significantly since initial recognition of the financial instrument. An impairment is recognized, where applicable, on a case–by–case basis to take into account collection difficulties which are likely to occur based on information available at the time of preparation of the financial statements.

Disputed receivables are written-off when certain and precise evidence shows that recovery is impossible, and existing credit loss allowance are released.

Loans and receivables:

This category includes loans as well as deposits and guarantees recognized under non-current financial assets.

These are recognized initially at fair value and subsequently at amortized cost, calculated using the effective interest method. Short-term receivables with no stated interest rate are measured at the original invoice amount except where the application of an implied interest rate has a material effect. The effective interest rate matches the expected future cash inflows to the current net book value of the asset in order to determine its amortized cost.

Loans and receivables are monitored for objective indications of impairment. A financial asset is impaired when an impairment test establishes that its carrying amount is higher than its estimated recoverable amount. The resulting impairment loss is recognized in the statement of operations.

In accordance with IAS 32 “Financial instruments: Presentation”, treasury shares held under a liquidity contract are deducted from equity and the losses and profits realized on the sale of a part of the shares are offset in the statement of operations.

|

|

Note 2.6 : |

Recoverable value of non-current assets |

Impairment testing takes place on tangible and intangible assets with a finite useful life if doubt is cast on the recoverability of their book value by an internal or external index.

Impairment tests are carried out at the close of the financial year on non-amortized assets (irrespective of whether there is an indication of an impairment loss). An impairment test involves comparing the asset's net carrying amount tested at its recoverable value. The test was carried out at cash-generating unit (“CGU”) level, which is the smallest asset group and includes assets whose continued use generates cash inflows largely independent of those generated by other assets or asset groups. The concept of a CGU is assessed at the level of the Company taken as a whole.

Impairment is recognized up to the excess of the book value over the asset's recoverable value. The asset's recoverable value is the higher of the fair value less costs to sell and the value in use.

The fair value less exit costs is the amount which can be obtained from the sale of an asset via a transaction conducted under normal competitive conditions between well-informed, consenting parties, less exit costs.

The value in use is determined each year in accordance with IAS 36 “Impairment of Assets”: it is the discounted value of the estimated future cash flows expected from the continued use of an asset and of its exit at the end of its useful life. The value in use is determined using cash flows estimated on the

Exhibit 99.2

basis of five-year plans or budgets, with flows being further extrapolated by applying a constant or declining growth rate, and updated using the long-term market rates after tax which reflect market estimates of the time value of money and the risks specific to the assets. The residual value is determined using discounting to infinity from the last cash flows of the test (see Note 3).

|

|

Note 2.7 : |

Cash, cash equivalents and other financial assets |

Cash and cash equivalents consist of immediately available cash and short-term available-for-sale securities. Cash equivalents are held for the purpose of covering short-term liquidity requirements rather than for investment or other purposes. They can be readily converted to known amounts of cash and are not exposed to any material risk of impairment.

They are measured at fair value, and any changes in value are recorded in financial income and expense.

For the purposes of the statement of cash flows, net cash includes cash and cash equivalents as defined above.

|

|

Note 2.8 : |

Capital |

Classification under shareholders’ equity depends on the specific analysis of the features of each instrument issued. On the basis of this analysis, it was possible to classify shares as equity instruments.

Additional costs directly attributable to share issues or options are recognized in equity as deductions against the proceeds of those issues. Moreover, in the absence of clarification on IAS 32 “Financial Instruments – Presentation”, the Company has chosen to recognize these costs by deducting them from shareholders’ equity prior to the operation if a year-end takes place between the date the services were rendered and the transaction when the planned transaction is considered highly likely. If the transaction does not subsequently take place, these costs would be recorded under charges for the following financial year.

|

|

Note 2.9 : |

Share-based payments |

The Company has implemented several share-based payment plans in the form of share subscription options, share warrants (BSA) or free share awards to its employees, executive officers, members of the board of directors, members of the scientific advisory board (SAB) or consultants.

In accordance with IFRS 2, the cost of equity-settled transactions is expensed with an increase in equity over the vesting period of the equity instruments in question.

The fair value of share warrants granted to employees is determined using Monte-Carlo or Black Scholes simulation techniques, as described in Note 16.

These models require the Company to use certain calculation assumptions which can differ for each plan, such as the expected volatility of the share, the price of the share used, the risk-free rate, the turnover rate, the non-transferability discount and the acquisition assumption for these plans if applicable.

|

|

Note 2.10 : |

Measurement and recognition of financial liabilities |

Financial liabilities are measured and recognized according to IFRS 9 “Financial instruments".

Note 2.10.1 : Financial liabilities at amortized cost

Borrowings and other financial liabilities are measured initially at fair value and subsequently at amortized cost, calculated using the effective interest method.

Transaction costs directly attributable to the acquisition or issue of a financial liability are deducted from the value of said liability. These costs are then amortized over the life of the liability, using the effective interest method. The effective interest rate matches the expected future cash payments to the current net book value of the liability in order to determine its amortized cost.

Note 2.10.2 : Liabilities at fair value through the statement of operations

Liabilities at fair value through profit and loss are measured at fair value each reporting period.

Exhibit 99.2

The fair value of financial instruments traded on an active market, such as available-for-sale securities, is based on their market price at the reporting date. The market prices used for financial assets held by the Company are the market bid prices at the valuation date.

In line with the amendments to IFRS 7 “Financial instruments: disclosures”, the financial instruments are presented according to three categories based on a hierarchization of the methods used to determine the fair value:

|

|

• |

Level 1: fair value determined based on the prices quoted on the asset markets for identical assets or liabilities; |

|

|

• |

Level 2: fair value determined based on the observable data for the asset or liability concerned, either directly or indirectly; |

|

|

• |

Level 3: fair value determined using measurement techniques based wholly or partially on non-observable data; an unobservable parameter is one whose value is derived from assumptions or correlations based neither on transaction prices observable on the markets for the same instrument on the valuation date, nor on observable market data available on the same date. |

The nominal amount of current receivables and payables, less any impairment losses, is presumed to approximate the fair value of those items.

|

|

Note 2.11 : |

Provisions |

Note 2.11.1 : Provisions for risks and charges

Provisions for risks and charges correspond to financial commitments arising from various risks and legal proceedings, of an uncertain maturity and amount, which the Company may face in the course of its business.

A provision is recognized where the Company has a legal or constructive obligation to a third party resulting from a past event where it is probable or certain that payment to said third party will arise from the obligation (with no equal or greater payment expected to be received from said third party), and where future payments can be reliably estimated.

The amount recognized as a provision is management's best estimate of the amount of the expense needed to settle the liability, discounted at the reporting date as applicable.

Note 2.11.2 : Retirement benefits

The Company's employees are entitled to statutory French retirement benefits:

|

|

• |

a lump sum paid by the Company upon their retirement (defined benefit scheme); |

|

|

• |

a pension paid by the social security authorities and funded by employer and employee contributions (national defined contribution scheme). |

The cost of retirement benefits in a defined benefit scheme is estimated using the projected unit credit method pursuant to revised IAS 19 “Employee Benefits”.

Under this method, the cost is recorded in the statement of operations in such a way as to spread it evenly over the employee's career at the Company. Past-service costs, however, are recognized immediately in expenses (increase in benefits allocated) or in income (decrease in benefits allocated) as soon as a new scheme is implemented or an existing one is modified. Actuarial gains or losses are recognized immediately and in full under equity in items of other comprehensive income.

Retirement obligations are measured at the present value of estimated future payments, using the market rate based on long-term investment grade corporate bonds with a duration equal to the estimated length of the scheme.

The Company's payments under defined contribution schemes are recorded as expenses in the statement of operations for the period to which they relate.

Exhibit 99.2

More details on retirement obligations can be found in Note 11.

|

|

Note 2.12 : |

Revenue and other income |

Note 2.12.1 : Revenues

The revenue the Company is likely to generate can result from the signature of strategic partnerships and include various financial components, such as amounts payable upon entering into the agreement, amounts payable upon reaching certain predefined development, sales and production targets, as well as one-off payments to fund research and development costs and royalties on future product sales.

Revenue is recognized in accordance with IFRS 15.

Under IFRS 15, revenue is recognized when the Company satisfies a performance obligation by transferring a promised asset or service to a customer. A service is considered an asset for purpose of applying IFRS 15 even though it is not recognized as an asset by the customer as it is simultaneously received and consumed and therefore expensed as transferred. An asset is transferred when the customer obtains control of the asset (or service).

Note 2.12.2 : Other income

Other income is recognized in accordance with IAS 20 “Accounting for Government Grants and Disclosure of Government Assistance” as follows:

Grants:

Since its creation, and on account of its innovative nature, the Company has received grants and aid from French national and local government aimed at funding its operations or specific recruitment drives.

Grants are recognized where there is a reasonable assurance that:

|

|

• |

the Company will meet the conditions of the grant; and |

|

|

• |

the conditions of their receipt have been met. |

Grants are recognized under other income (see Note 13) as the associated expenses are committed and independently of the receipts, in line with the principle of linking expenses to income.

Grants receivable either as compensation for expense or losses already incurred, or as immediate financial aid with no related future costs, are recognized in income in the year in which they become receivable.

Research tax credit (RTC):

The French government awards RTC to companies to encourage them to conduct technical and scientific research. Companies that can demonstrate expenditure meeting the required criteria are eligible for a tax credit that can be offset against corporate income tax in respect of the year in which the expenditure is incurred and the following three years, or refunded where applicable (i.e. where it exceeds the amount of corporate income tax payable). Since the Company has not paid any corporate income tax since its formation, every year it receives payment of the RTC relating to the previous year from the French Treasury.

These amounts are recognized in other income for the year in which the corresponding expenses are incurred.

|

|

Note 2.13 : |

Research and development contracts |

Note 2.13.1 : Service contracts

Service contracts are recognized as they progress according to management's best estimate. Expenses can be estimated according to the period over which a service is provided or according to certain objective criteria, such as the number of patients recruited or the number of visits completed.

Any amounts payable upon the attainment of certain targets representing technical success milestones for the service provider are recognized as expenses when the milestone is reached.

Exhibit 99.2

Note 2.13.2 :Research and development agreements

Research agreements are recognized as they progress according to management's best estimates based on the information provided by external partners corroborated by internal analyses.

Development agreements can include various components, such as the amounts payable upon signature and amounts payable when certain growth targets are reached. When the concept of continued service can be determined, development agreements are recognized as they progress according to management's best estimates based on the contractual information provided by external partners corroborated by internal analyses.

Otherwise, the non-refundable amounts payable upon signature of the contracts are recorded immediately under expense and the amounts payable upon attainment of certain targets representing scientific or regulatory milestones are recorded under expenses once the milestone has been reached.

|

|

Note 2.14 : |

Lease agreements |

Finance leases within the meaning of IAS 17 “Leases” are recorded under other property, plant and equipment upon signature, in exchange for a financial payable. Each year, amortization is allocated to the statement of operations, and the lease payments paid are allocated to financial expenses at the rate stated in the contract to offset the financial payable on the statement of financial position (see Note 2.4.1 for more detail).

Lease agreements where a significant portion of the risks and benefits is retained by the lessor are classified as operating leases. Net of any incentive, payments under an operating lease are recognized in expenses in the statement of operations on a straight-line basis over the duration of the lease.

|

|

Note 2.15 : |

Income tax |

The Company is subject to corporate income tax in France in connection with its activities.

Deferred taxes are recognized using the comprehensive asset and liability method, for all timing differences arising from the difference between the tax base and accounting base of assets and liabilities shown in the financial statements. The Company’s main timing differences relate to tax loss carryforwards. Deferred taxes are calculated based on the tax rates enacted in law at the reporting date.

Deferred tax assets mainly corresponding to tax loss carryforwards are recognized only to the extent that it is probable that future taxable profits will be available. The Company must use its judgment to determine the probability that future taxable profits will be available.

|

|

Note 2.16 : |

Segment information |

The Company considers that it operates in a single segment: research and development into pharmaceutical products with a view to their future commercialization.

The whole of the Company's research and development activity is located in France. All the Company's tangible assets are located in France. The main operational decision-makers measure the Company's performance in terms of the cash burn rate of its activities. This is why the Company's management believes it is not appropriate to break its internal reports down into separate business segments.

|

|

Note 2.17 : |

Items of other comprehensive income / (loss) |

Any components of income and expense for the period that are recognized directly in equity are posted under items of other comprehensive income / (loss). This item, for the period presented, includes the impacts of changes in actuarial assumptions for provisions for retirement indemnities.

Exhibit 99.2

Changes to intangible assets break down as follows:

Intangible assets are recognized as work-in-progress when they do not meet the conditions for bringing into use at the closing date. At September 30, 2018, they mainly correspond to the repurchase by the Company of all rights of Trizell on Ovasave. The acquisition costs for these rights, the amount and maturity of which can be fixed definitely, i.e. €6 million, were recognized as an asset and were discounted in accordance with IAS 38.

As at September 30, 2018, no indication of impairment was identified. The annual impairment test was performed on this asset on December 31, 2017, and found no impairment loss.

|

|

Note 4 : |

Property, plant and equipment |

Changes to property, plant and equipment break down as follows:

The main investments as of September 30, 2018 were:

|

• |

The purchase of laboratory equipment for (i) CAR-Treg manufacturing process development, and (ii) the manufacturing process transfer of the product candidate TX200 for the first study in the prevention of chronic rejection after organ transplantation; most of these investments were in the form of finance leases (see Note 10.1); |

|

• |

Renovations of premises, with the dual aim of grouping the two existing sites into the head office premises, and the creation of level 2 laboratories for in vivo developments of the CAR-Treg platform. |

|

|

Note 5 : |

Financial assets |

Exhibit 99.2

Non-current financial assets include the main following items:

|

|

• |

Security deposits in the amount of €38 thousand, mainly corresponding to the commercial lease of the head office, after reimbursement of the security deposits relating to the Genbiotech premises whose lease was terminated in the first quarter of 2018; |

|

|

• |

Other long-term receivables for €91 thousand corresponding to the guarantee deductions relating to partial pre-financing of the Company’s 2018 RTC (see Note 6). In the first half of 2018, the assignment of the 2017 RTC receivable was canceled at the request of the Company, which, after having repaid the Predirec fund, was able to obtain the return of the guarantee deductions and the collection of the totality of its 2017 RTC. The guarantee deductions are made up of the following: |

|

|

o |

an individual portion to cover the individual risk specific to the sum owed to the Company, returnable after the occurrence of one of these events, whichever happens first: (i) after repayment of the RTC by the French government (ii) after the tax inspection of said credit, after any adjustments are allocated, or (iii) at the end of the taxation limitation period for the credit concerned (December 31 of the third year following the date the RTC declaration is filed); and |

|

|

o |

a collective part to cover the collective risk of the receivables recorded in the portfolio of the pre-financing fund, returnable upon closure of the pre-financing fund. |

|

|

• |

During the first half of 2018, the Company terminated its liquidity contract with Kepler Cheuvreux. The treasury shares held under this liquidity contract were sold for the purpose of closing the account. The Company has been reimbursed the balance in cash, i.e. €108 thousand. |

|

|

Note 6 : |

Other current assets |

Other current assets break down as follows:

|

|

• |

Other receivables |

Since 2016, the Company has been assigning its RTC to Predirec Innovation 2020, a mutual securitization fund. In exchange, the Company benefits, subject to it meeting prior contractual conditions, from pre-financing lines for its RTC.

In the first half of 2018, the assignment of the 2017 RTC receivable was canceled at the request of the Company, which, after having repaid the Predirec fund, was able to obtain the return of the guarantee deductions and the collection of the totality of its 2017 RTC for €1.9 million.

As at September 30, 2018, the provision of the 2018 RTC amounts to €1.4 million and was partially pre-financed in the amount of €1.0 million (see Note 10.4).

|

|

• |

Prepaid expenses |

Prepaid expenses mainly relate to operating expenses.

Exhibit 99.2

Accounting standards relating to financial instruments have been applied to the following items:

|

|

(1) |

The fair value level of the instruments is presented in Note 7.1. |

At December 31, 2017, the accounting standards applicable to financial instruments were applied as follows:

|

|

(1) |

The fair value level of the instruments is presented in Note 7.1. |

|

|

Note 7.1 : |

Measurement of fair value |

Note 7.1.1 : Levels of fair value

|

|

(1) |

Level 1: the fair value of the items at fair value through the statement of operations corresponds to the market value of these assets. |

|

|

(2) |

Level 2: the fair value of the items at fair value through the statement of operations corresponds to an average market value of these assets and liabilities. |

|

|

(3) |

Level 3: no assets or liabilities were measured at level 3 fair value. |

Note 7.1.2 :Transfers between levels of fair value

No assets were transferred to a different level of fair value as of September 30, 2018.

|

|

Note 8 : |

Cash and cash equivalents |

“Cash and cash equivalents” consist of immediately available cash and short-term available-for-sale securities.

These deposits satisfy the cash and cash equivalents classification criteria described in Note 2.7.

Cash and cash equivalents break down as follows:

Exhibit 99.2

|

|

Note 9 : |

Capital |

|

|

Note 9.1 : |

Issued capital |

As at September 30, 2018, the share capital was €4,639,078.80. It is divided into 23,195,394 shares, subscribed and fully paid up, with a par value of €0.20.

This number does not include instruments convertible to Company equity which have not yet been exercised or acquired, as applicable.

The change in share capital over the period breaks down as follows:

In the first quarter of 2018, 14,678 share warrants (BSAs) issued under the capital increase with preferential subscription rights of February 2017 were exercised and resulted in the issue of a total number of 11,008 shares for a total nominal amount of €2,201.60.

In the first half of 2018, the board of directors has noted the vesting of 228,097 free shares granted to employees of the Company in 2016 and 2017, which resulted in the issuance of 234,092 new shares, i.e. a capital increase of €46,818.40 euros in nominal value, factoring in the arithmetic correction set by the board at its meeting of February 21, 2017 to take account of the capital increase with preferential subscription rights carried out in February 2017.

As of September 30, 2018, 10 notes (OCA) of the optional equity financing line have been converted, which resulted in the issuance of 1,136,987 new shares for a total nominal value of €227,397.40.

|

|

Note 9.2 : |

Treasury shares |

During the first half of 2018, the Company terminated its liquidity contract with Kepler Cheuvreux. The treasury shares held under this liquidity contract were sold for the purpose of closing the account. As a result, no treasury shares remained at September 30, 2018, compared to 99,318 treasury shares as at December 31, 2017. As at December 31, 2017, these treasury shares were recognized as a reduction in shareholders' equity in the financial statements established pursuant to IFRS standards, for a total amount of €276 thousand.

As of September 30, 2018, securities giving access to the Company's equity are as follows:

Exhibit 99.2

Note 9.3.1 : Stock option subscription plans

|

|

(1) |

All 2014 T1 Options are exercisable for a period of 10 years, starting from their allocation by the board of directors. Should the option holder leave the Company he or she has, from the time he or she ceases to be an eligible recipient, six months to exercise the options that would be exercisable at the time of leaving, after which the options are void. |

|

|

(2) |

The 2014 T2 and the 2015 Options are exercisable by a third at the end of each one-year period from their grant date by the board of directors, provided that the recipient is still an employee and/or corporate officer of the Company or an associated company. Should the option holder leave the Company he or she has, from the time he or she ceases to be an eligible recipient, six months to exercise the options that would be exercisable at the time of leaving, after which the options are void. |

|

|

(3) |

The SB 2015 Options can be exercised by a third at the end of each year from their allocation by the board of directors. They are subject to performance conditions, the fulfillment of which will be established by the board of directors, provided that Stéphane Boissel remains a corporate officer of the Company or one of its affiliates. Should he leave the Company, Stéphane Boissel has, from the time he ceases to be an eligible beneficiary, six months to exercise the SB 2015 Options that would be exercisable at the date of leaving, after which the Options are void. |

|

|

(4) |

Notwithstanding the above, in case of a change of control of the Company, all Options will immediately become exercisable by the beneficiary before the completion of such change of control, and the board of directors will have the choice of deciding that any Option not exercised before the completion of such change of control will automatically be void. |

|

|

(5) |

The number of Options factors in, if applicable, the conversion rate set by the board of directors at its meeting of February 21, 2017 as part of the capital increase of February 2017, in order to protect the interests of holders of share warrant, stock option and free shares. |

Exhibit 99.2

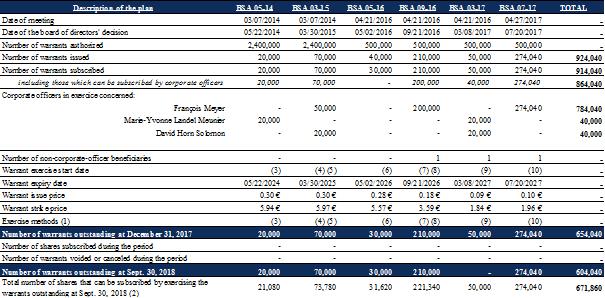

Note 9.3.2 : Warrant (BSA) plans

As of September 30, 2018, the warrants plans allocated to the Company’s employees and corporate officers and members of its Scientific Advisory Board (SAB) break down as follows:

|

|

(1) |

Should there be a change of control of the Company, all warrants granted to a recipient will immediately be exercisable by the recipient before that event transpires, and the board of directors will have the choice of deciding that any warrant not exercised before that event will automatically be void. |

|

|

(2) |

The number of Options factors in, if applicable, the conversion rate set by the board of directors at its meeting of February 21, 2017 as part of the capital increase of February 2017, in order to protect the interests of holders of share warrant, stock option and free shares. |

|

|

(3) |

The BSA 05-14 allocated to Marie-Yvonne Landel-Meunier can be exercised by a third at the end of each year from their allocation by the board of directors, subject to the beneficiary’s continuous presence on the Board of directors over the vesting period. |

|

|

(4) |

The BSA 03-15 allocated to David Horn Solomon can be exercised by a third at the end of each year from their allocation by the board of directors, subject to the beneficiary’s continuous presence on the board of directors over the vesting period. |

|

|

(5) |

The BSA 03-15 granted to François Meyer can be exercised by a third at the end of a one-year period from their grant date by the board of directors, provided he is Chairman of the board of directors on the exercise date. |

|

|

(6) |

The BSA 05-16 have been allocated to the Scientific Advisory Board (SAB) members. The 05-16 BSAs are all exercisable, provided that, at the exercise date, the beneficiary: (i) is a member or observer of the board of directors of the Company or one of its affiliates, or (ii) has entered into a service provider or consultant contract with the Company or one of its affiliates, or (iii) is a member of any committee set up by the board of directors. |

|

|

(7) |

10,000 BSA 09-16 have been allocated to a member of the Company’s Scientific Advisory Board (SAB). The BSA 09-16 are fully exercisable, provided that, on the date of exercise, the beneficiary is either: (i) is a member or observer of the board of directors of the Company or one of its affiliates, or (ii) has entered into a service provider or consultant contract with the Company or one of its affiliates, or (iii) is a member of any committee set up by the board of directors. |

Exhibit 99.2

|

|

service provider or consultant contract with the Company or one of its affiliates, or (iii) is a member of any committee set up by the board of directors. |

|

|

(9) |

10,000 BSA 03-17 have been allocated to a clinical advisor of the Company, 20,000 to Marie-Yvonne Landel-Meunier and 20,000 to David Horn Solomon. The BSA 03-17 can be exercised by a third at the end of each one-year period from their grant date by the board of directors, provided that on the exercise date, the beneficiary (i) is a member or observer of the board of directors of the Company or one of its affiliates, or (ii) has entered into a service provider or consultant contract with the Company or one of its affiliates, or (iii) is a member of any committee set up by the board of directors. |

|

|

(10) |

The BSA 07-17 have been allocated to François Meyer, on the condition precedent that he waives all rights and shares under BSA 03-14 warrants granted to him. Having noted that the condition precedent had been met, the BSA 07-17 warrants were fully subscribed by François Meyer. The BSA 07-17 warrants may be exercised according to the following schedule: 137,020 BSA warrants immediately, and 137,020 as of January 1, 2019. All of the BSA warrants may be exercised provided that, on the exercise date, the beneficiary meets one of the following criteria: (i) is a member or observer of the board of directors of the Company or of one of its subsidiaries, or (ii) is bound by a services or consultancy contract to the Company or to one of its subsidiaries, or (iii) is a member of one of the Board's committees. The exercise of the second half of the BSA warrants is dependent on performance conditions being met, as decided by the board of directors. |

Note 9.3.3 : Free share plans (AGA)

As of September 30, 2018, the free share plans allocated to the Company’s employees and corporate officers break down as follows:

|

|

(1) |

The 2016 AGA employees are acquired by a third at the end of each year from their allocation by the board of directors, provided that the acquisition is subject to a condition of presence, and, for some employees, to performance conditions, linked to the realization of annual objectives by the beneficiary, as determined by the board of directors. |

|

|

(2) |

The 2016 AGA management are acquired by a third at the end of each year from their allocation by the board of directors, provided that the acquisition is subject to a condition of presence, and to performance conditions, linked to the realization of annual objectives by the beneficiary (i.e. financing, progress on research and development programs, signature of strategic partnerships), as determined by the board of directors. |

|

|

(3) |

The first third of the allocated free shares is subject to a one-year holding period from the date of acquisition, i.e. until May 2, 2018. No holding period was set for the two other thirds, subject to the provisions applicable in case of a change of control as described in (6) below. |

|

|

(4) |

80,000 2017 AGA free shares have been granted to Stéphane Boissel, which will vest after a one year-period starting from their grant date by the board of directors, subject to continued employment in the Company. On March 8, 2018, all AGA 2017 granted to Stéphane Boissel have been vested. |

Exhibit 99.2

57,000 2017 AGA free shares have been granted to employees, of which 30,000 will vest after a one year-period starting from their grant date, and 27,000 will vest by a third at the end of each one-year period from their grant date, it being specified that the vesting of the shares is subject to continued employment.

|

|

(5) |

The 2018 AGA will vest by a third at the end of each one-year period from their grant date, it being specified that the vesting of the shares is subject to continued employment. |

|

|

(6) |

In case of a change of control at the Company, all AGA allocated to a beneficiary will immediately become vested on the later of the two following dates: (i) the first anniversary of the allocation date (the condition of presence is then lifted and the vesting period is completed with a holding period expiring on the second anniversary of the allocation date, or (ii) the date of completion of the change of control (said date marking the end of the vesting period), if necessary extended by a holding period up to the second anniversary of the allocation date. |

|

|

(7) |

The number of Options factors in the conversion rate set by the board of directors at its meeting of February 21, 2017 as part of the capital increase of February 24, 2017 of holders of share warrant, stock option and free shares. |

Note 9.3.4 : Other dilutive instruments

Note 9.3.4.1Warrants giving access to notes convertible into shares with share subscription warrants attached (Warrants or OCABSA)

The Company set up a reserved issue of 200 convertible notes with warrants (OCABSA) to an investment fund managed by the US management company Yorkville Advisors Global LP (“Yorkville”), which fully subscribed them. These notes, exercisable until August 3, 2019, require their bearer at the Company's request and provided that certain conditions are met, to subscribe for up to 200 OCA, each with a par value of €100,000, for an overall nominal value of €20 million, to which up to €10 million may be added in the event that all of the attached BSA share warrants are exercised. A prospectus regarding this operation was made available to the public and was approved by the AMF on July 27, 2016 (approval number 16-356).

In 2016, 50 Warrants were exercised on the request of the Company which then issued 50 OCA to Yorkville for a total nominal amount of €5 million, from which 686,350 BSA warrants were detached, which, if fully exercised, would generate an additional equity contribution of €2.5 million for the Company.

On October 25, 2017, the Company also signed an amendment to the initial contract of June 17, 2016, modifying some conditions attached to the 150 Warrants not yet exercised, with a view to reducing any cost to the Company as well as the dilutive impact on its shareholders. This amendment mainly consisted of:

|

- |

decrease the applicable discount on the OCA conversion price: now 5% compared to the baseline, compared with 7% before, |

|

- |

decrease the number of shares issued upon exercise of BSA attached to each tranche of OCA: now 25% of the nominal amount of the OCA tranche concerned, compared with 50% before, |

|

- |

increase the applicable issue premium on the exercise price of BSA: now 30% compared to the reference price with a floor exercise cost equal to 3 euros, compared with 15% previously without a floor exercise price, and |

|

- |

decrease the commitment commission payable to the investor: now 2% in cash of the guaranteed financing balance, compared with 5% in shares before. |

On May 17, 2018, the Company signed an amendment to the original agreement of June 17, 2016, amended on October 25, 2017, whereby the Company has the option, at any time and in its sole discretion, to redeem in cash up to 50% of notes not yet converted into shares upon the exercise of this call option, for a price equal to 110% of the nominal value of the said notes.

On July 12, 2018, the Company signed an amendment to the original agreement of June 17, 2016, amended on October 25, 2017 and May 17, 2018. Subject to the effective completion of Sangamo's proposed acquisition of a majority stake in the Company, the contract provides for (i) the repurchase by the Company of 50% of the 56 unconverted OCA for a total amount of €3,080,000 (i.e. 110% of their

Exhibit 99.2

total nominal value of €2,800,000), (ii) Yorkville's conversion of the remaining 28 OCA into 1,866,666 new shares of the Company at a fixed unit price of €1.50, and (iii) ) the repurchase by the Company of the 84 Tranche Warrants and the 1,236,350 BSA warrants currently held by Yorkville for the lump sum of one euro, with a view to their cancellation.

As of September 30, 2018, 66 Warrants were exercised on the request of the Company, which then issued 66 OCA to Yorkville for a total nominal amount of €6.6 million, of which 550,000 BSA warrants were detached.

As at September 30, 2018, 10 OCA have been converted and no share warrant has been exercised by Yorkville. It is specified that the Company has no draw obligation.

As at September 30, 2018, there remain 84 Tranche Warrants outstanding and 56 unconverted OCA.

The details of the OCA and the BSA in circulation are presented below:

|

|

a. |

Notes convertible into shares (OCA) |

At September 30, 2018, the features of the OCA issued by the Company are as follows:

|

|

(1) |

The OCAs may be converted into new ordinary Company shares at the request of the bearer, at any time from their issue and for a period of 14 months as of this date (inclusive) or if the notes convertible into shares are not exercised on their maturity date, according to the conversion rate determined using the formula below: |

N = Vn / P, where:

|

|

a. |

“N” is the number of ordinary new TxCell S.A. shares to be issued upon conversion of an OCA; |

|

|

b. |

“Vn” is the note which the OCA represents (par value of an OCA); |

|

|

c. |

“P” is 95% of the lowest volume-weighted average daily price of TxCell S.A. shares (as published by Bloomberg) over the ten (10) trading days immediately prior to the date a notice of conversion for the OCA concerned is sent. Trading days on which the holder of the note convertible into shares sold TxCell S.A. shares shall not be included. However, P cannot be less than the par value of a TxCell S.A. share, i.e. €0.20 on the date of the discount. |

|

|

(2) |

Notes convertible into shares (OCA) do not carry interest. However, in the event of default, each OCA in force will carry interest equal to 15% per annum (redeemed in cash as of the occurrence of any default until the date (i) the default is remedied or (ii) the OCA concerned is redeemed or converted). |

|

|

(3) |

On an indicative basis, theoretical number of shares issued upon conversion of all OCA issued and non converted, based on 95% of the lowest volume-weighted average price over the ten trading days prior to September 30, 2018, i.e. €2.31. As a reminder, the Company has the option, at any time and in its sole discretion, to redeem in cash up to 50% of the notes not yet converted into shares at the time of the exercise of this repurchase option, for a price equal to 110% of the nominal value of the said notes. |

Exhibit 99.2

At September 30, 2018, the features of the BSA detached from the OCA issued are as follows:

|

|

(1) |

BSA detached from the OCA are fully exercisable. |

|

|

(2) |

The number of Options factors in the conversion rate set by the board of directors at its meeting of February 21, 2017 as part of the capital increase of February 2017, in order to protect the interests of share warrant, stock option and free shareholders. |

|

|

Note 9.3.4.2 |

Other share warrants |

Following the capital increase carried out in February 2017 by public offer through the issue of new shares with share subscription warrants attached (ABSA), 5,549,300 warrants (listed warrants), with a maturity of one year, i.e. until 26 February 2018, were detached from the ABSA subscribed.

In the first half of 2018, 14,678 BSA warrants have been exercised, resulting in the issue of 11,008 shares, representing a subscription for a total of €28,620.08 including the issue premium.

On February 26, 2018, the 5,528,978 unexercised listed warrants have been canceled.

Exhibit 99.2

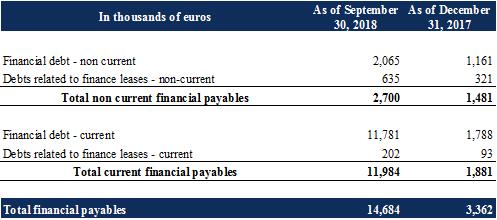

The table below shows the breakdown of financial payables by type and by maturity:

Changes in loans and financial payables broke down as follows:

|

|

Note 10.1 : |

Finance leases |

Finance leases entered into by the Company are for laboratory equipment. These contracts are for a period of five years.

|

|

Note 10.2 : |

Zero-interest innovation loan |

In 2014, the Company obtained a zero-interest innovation loan (Prêt à Taux Zéro innovation - PTZI) from Bpifrance Financement in the gross amount of €1.7 million. This sum was paid within the scope of the Phase IIb clinical trial for Ovasave, which started in December 2014. The zero-interest innovation loan is repayable over a period of eight years, with a deferred repayment of three years. The contract provides for several scenarios of early repayment, mainly relating to ’curtailment or suspension of the financed project without prior information from Bpifrance Financement or the occurrence of a major legal or financial event which has a significant impact on the Company’s operations. The Company notified Bpifrance Financement of the stoppage of Phase IIb of the Ovasave clinical trial; at the reporting date, the Company was not aware of any early repayment request. The Company thus repays this PTZI

Exhibit 99.2

in accordance with the contractual repayment schedule. In 2018, the Company repaid €255 thousand in accordance with the contractual repayment schedule.

In accordance with Note 2.10, the repayment flows for the zero-interest innovation loan are discounted on the closing date. The 10-year French Government bond rate at December 31, 2014 of 0.837% was used to discount these flows. The discounting proceeds are processed as a grant within the meaning of IAS 20 and linearized over the duration of the project to which the loan is attached. The impact of the accretion expense of the debt is recognized as a financial expense.

On February 1, 2018, the Company obtained a zero-interest innovation loan from Bpifrance Financement in the gross amount of €1.2 million. This sum was paid within the scope of preclinical development and non-clinical pharmaceutical development of a CAR-Treg targeting HLA-A2 for the prevention of chronic rejection after organ transplantation. This loan is repayable over seven and a half years, with a repayment deferral of two and a half years. The contract provides for several scenarios of early repayment, mainly relating to curtailment or suspension of the financed project without prior information from Bpifrance Financement or the occurrence of a major legal or financial event which has a significant impact on the Company’s operations.

In accordance with Note 2.10, the repayment flows for the zero-interest innovation loan are discounted on the closing date. The 10-year French Government bond rate at February 1, 2018 of 0.997% was used to discount these flows. The discounting proceeds are processed as a grant within the meaning of IAS 20 and linearized over the duration of the project to which the loan is attached. The impact of the accretion expense of the debt is recognized as a financial expense.

|

|

Note 10.3 : |

Note issue |

As of September 30, 2018, the Company issued 66 notes convertible into shares (OCA) to Yorkville for an overall nominal value of €6.6 million (see Note 9.3.4.1). 10 OCA have been converted, i.e.56 OCA remain to be converted as at September 30, 2018.

Notes convertible into shares (OCA) do not carry interest and shall be redeemed at par value. However, in the event of default, each OCA in force will carry interest equal to 15% per annum (redeemed in cash as of the occurrence of any default until the date (i) the default is remedied or (ii) the OCA concerned is redeemed or converted).

In addition, the Company has the option, at any time and in its sole discretion, to redeem in cash up to 50% of the notes not yet converted into shares upon the exercise of this call option, for a price equal to 110% of the nominal value of the said notes.

In accordance with IAS 32, notes convertible into shares (OCA) are financial instruments measured at fair value through the statement of operations.

At the time of issue, notes convertible into shares (OCA) are recognized at nominal (par) value. They are subscribed at 98% of par. The remaining 2% is recognized under other financial expenses.

At each conversion, the difference between the carrying amount of the notes convertible into shares (OCA) and their fair value, calculated using the average volume-weighted TxCell S.A. share price for the last ten trading days prior to the conversion, is recognized under other financial expenses.

Notes convertible into shares (OCA) not converted at closing are revalued at fair value through the statement of equity under other financial expenses, using the average volume-weighted TxCell S.A. share price for the last ten trading days prior to year-end. This is a level 2 measurement (see Note 7.1). For the OCA redeemable at the request of the Company, i.e. 50% of unconverted OCA at closing, the fair value is capped at the amount at which it could be repaid, i.e. 110% of their nominal value. As of September 30, 2018, the financial expenses recorded for OCA amounted to €624 thousand. These financial expenses result from IFRS accounting treatments that have no impact on the Company's cash position.

Share warrants (BSA) are recognized as zero, as the fair value of these instruments cannot be reliably measured given the very many criteria to be taken into account and their uncertainty.

Exhibit 99.2

During the first half of 2018, the Company obtained an additional pre-financing for its 2017 RTC for €0.5 million. The assignment of the 2017 RTC receivable was canceled at the request of the Company, which, after having repaid the Predirec fund, was able to obtain the return of the guarantee deductions and the collection of the totality of its 2017 RTC for €1.9 million.

As of September 30, 2018, the Company also obtained partial pre-financing of its 2018 RTC for €1.0 million.

|

|

Note 10.5 : |

Loan granted by Sangamo Therapeutics Inc. |

In order to cover for working capital expenses of the Company in the following months, Sangamo has granted a loan to the Company of an amount of €4.5 million pursuant to a loan agreement dated September 18, 2018. The loan as an annual interest rate of 2.5%, and is repayable after 6 months.

|

|

Note 11 : |

Provisions |

As at September 30, 2018, provisions for expenses correspond exclusively to a retirement benefits provision of €4 thousand, recorded in application of the IAS 19 standard. The actuarial differences relating to the variation in the discount rate and other assumptions are recognized as other items of comprehensive income / (loss) (see Note 2.17), constituting income of €1 thousand for the nine months ended September 30, 2018. The assumptions used to calculate retirement indemnities for the Company’s employees, defined in the collective bargaining agreement for the pharmaceutical industry, are as follows:

|

|

Note 12 : |

Trade payables and other current liabilities |

|

|

Note 12.1 : |

Trade payables and related accounts |

No discounting has been applied to this item, since none of the amounts in question were more than a year old at the end of each reporting period.

Exhibit 99.2

Social security payables mainly include social security, retirement and pension expenses, as well as provisions for paid leave and bonuses.

Deferred income corresponds to the advance measurement of grants for collaborative research projects.

Capital expenditures suppliers mainly correspond to the acquisition of Trizell's rights on Ovasave whose initial cost of €6 million, discounted in accordance with IAS 38, had been the subject of a first payment of €2 million upon the signing of the termination agreement on December 2, 2015. A second payment was made during the first quarter of 2018. The balance of €2 million is contractually payable upon invoicing on December 2, 2018.

|

|

Note 13 : |

Revenue and other income |

The Company did not generate any business revenues in the nine months ended September 30, 2018 and 2017.

Other income primarily comprises:

|

• |

grants in the amount of €53 thousand, compared to €172 thousand for the same period of 2017; |

|

• |

a RTC estimate as of September 30, 2018 of €1,395 thousand, compared to €1,464 thousand for the same period of 2017. |

|

|

Note 14 : |

Staff costs |

Exhibit 99.2

Changes in the average headcount were as follows:

The expenses relating to share-based payments are described in Note 16.

|

|

Note 15 : |

Breakdown of expenses by function |

|

|

Note 15.1 : |

Research and development |

For the presented periods, research and development costs were mainly attributable to:

|

|

• |

manufacturing process development programs, notably the transfer of the TX200 process to CMOs: Lentigen, for the production of the lentivirus to be integrated into TX200 and Lonza, for the actual clinical batches manufacturing of TX200; |

|

|

• |

CAR-Treg research programs, conducted internally or under research and development agreements for the generation of preclinical proof-of-concept data. |

Research and development costs break down as follows:

The increase in Purchase of raw materials is primarily due to the acceleration of the experiments necessary to develop the CAR-Treg platform: preclinical research programs and CAR-Treg manufacturing processes.

The Rent, fees and other expenses item breaks down as follows:

The decrease in Property leases item is mainly due to the end of the lease contracted with Genbiotech SAS, which ended on January 31, 2018. All activities and teams have since been consolidated at the Company's head office.

Exhibit 99.2

The increase in Fees and studies is mainly due to the costs related to the transfer of the TX200 manufacturing process to the CMOs, partially offset by the decrease of expenses related to the collaboration agreement with OSR terminated in the second half of 2017.

The increase in other R&D expenses is mainly due to in vivo developments of the CAR-Treg programs and to the transfer of the manufacturing process.

The increase in Depreciation, amortization and provisions is mainly due to the increase in acquisitions of laboratory equipment, mainly in the form of finance leases contracts (see Note 10.1).

|

|

Note 15.2 : |

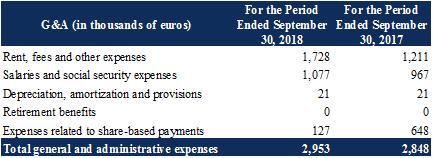

General and administrative expenses |

General and administrative expenses are presented as follows:

The Rent, fees and other expenses item breaks down as follows:

The increase in Fees was primarily attributable to non-recurring legal consultancy fees recognized nine months ended September 30, 2018, notably commitment fees paid to Yorkville in the OCABSA draw in February 2018, and fees related to the implementation of a long-term refinancing.

|

|

Note 16 : |

Share-based payments |

The Company allocated share warrants (BSA), share subscription options (Options) and free shares (AGA) to employees, executive officers, members of the board of directors, members of the Scientific Advisory Board (SAB) or consultants.

The measurement methods used to determine the fair value of plans for instruments convertible to Company equity since 2014 are as follows:

|

|

• |

the share price on the allocation date is equal to the strike price; |

|

|

• |

the risk free rate is determined from the average lifespan of the instruments, based on the borrowing rates of the GRFN index; |

|

|

• |

volatility was determined on the basis of a sample of listed companies in the biotechnology sector, both at the date on which the instruments are subscribed and over a period equivalent to the life of the options; and |

|

|

• |

the price discount linked to the non-transferability of the share subscription options compared to equivalent options without transfer restrictions has been calculated using the forward price model at the estimated borrowing rate; and |

|

|

• |

the Black Scholes model was used to measure the fair value of the plans for instruments convertible to Company equity. |

Exhibit 99.2

The parameters used to estimate and value the new free share plan are outlined below:

|

|

(1) |

No non-transferability discount was applied to the AGAs; the value of the free share after discount is thus identical to the value of the free share. |

The annual charges recognized are shown below:

Pursuant to IFRS 2, the expenses recognized take into account the adjustment of expenses on options which were not vested on the beneficiaries’ departure date.

Exhibit 99.2

Income from cash and cash equivalents corresponds to accrued interest and short-term gains on investment securities.

Financial interest corresponds to interest on credit lines to pre-finance RTC.

Other financial expenses amounted to €843 thousand for the nine months ended September 30, 2018 and mainly corresponded to:

|

|

• |

€12 thousand in accretion of finance flows linked to the zero-interest innovation loan (see Note 0.2), compared to €12 thousand for the same period in 2017; |

|

|

• |

€15 thousand in accretion of the trade payable assets (see Note 12.2) , compared to €29 thousand for the same period in 2017; |

|

|

• |

€192 thousand to losses realized under the liquidity contract, terminated in June 2018; and |

|

|

• |

€624 thousand from the fair value recognition through profit and loss of the note issues (see Note 10.3), compared to €352 thousand for the same period in 2017. |

Except for financial expenses relating to the liquidity contract, these financial expenses are due to IFRS accounting treatments and have no impact on the Company’s cash position.

|

|

Note 18 : |

Tax charge |

Based on current legislation, as of December 31, 2017, the Company has tax losses amounting to €95.3 million which can be carried forward indefinitely.

In France, losses can be carried forward against future profits with no time limit, but the amount that can be offset against profit in the fiscal year is capped at €1 million plus 50% of the taxable income exceeding €1 million in that fiscal year.

Net deferred tax assets from timing differences have not been recognized because they are not probable of being realized, in accordance with the principles described in Note 2.15.

Exhibit 99.2

|

|

Note 19.1 : |

Obligations arising from operating leases |

On December 22, 2015, the Company signed an amendment to renew the commercial lease expiring on June 30, 2016, for an annual rent of €147 thousand excluding tax (the initial index-linked rent, which is now indexed annually to the quarterly service businesses index). This commercial lease is granted for a term of nine consecutive years, with the possibility of giving notice to quit every three years as well as, exceptionally, at the end of each of the first two years of the renewed lease.

The Company contracted a short-term lease with SAS Genbiotech under the commercial lease regime effective February 1, 2016. The lease was agreed for a period of two years (from February 1, 2016 to January 31, 2018) for an annual rent of €209 thousand excluding tax the first year and €198 thousand excluding tax the second year. This lease was not renewed at the end and ended on January 31, 2018.

The amount of rent recognized in expenses during the period ended on September 30, 2018 totaled €129 thousand for the two rental contracts.

|

|

Note 19.2 : |

Obligations under the termination agreement with Trizell |

On December 2, 2015, the Company and Trizell entered into an agreement terminating their cooperation, development, option and license agreement on Ovasave, signed on December 12, 2013 and modified by a rider dated March 30, 2015. Under this agreement, the Company recovers all of Trizell’s rights over Ovasave in return for paying amounts which could reach €15 million including:

|

|

• |

a fixed €6 million, of which the Company has already paid €4 million. The balance of €2 million is contractually payable upon invoicing on December 2, 2018; |

|

|

• |

a conditional €9 million on the future revenue, if applicable, generated by Ovasave, which will be recognized if the contractual conditions are met. |

|

|

Note 19.3 : |

Obligations pursuant to intellectual property contracts |

The quantified obligations relating to the following paragraphs are not disclosed for commercial reasons.

Note 19.3.1 :Obligations pursuant to contracts for the purchase of rights over licenses

Generally, contracts for the purchase of rights over licenses make the Company responsible for patent filing, examination and extension costs, as well as costs relating to their protection; they also make the Company accountable vis-a-vis the owner of the rights to lump sums and royalties as certain milestones are reached.

Note 19.3.2 :Obligations pursuant to contracts for options over licenses

Generally, contracts for options over licenses make the Company responsible for patent filing, examination and extension costs, as well as costs relating to their protection and may require payment of a lump sum in exchange for the option, will make the Company accountable vis-a-vis the owner of the rights to lump sums and royalties as certain milestones are reached.

Note 19.3.3 :Obligations resulting from joint ownership of intellectual property rights

Joint ownership agreements, which define the joint ownership rules and sub-licensing rules of certain intellectual property rights, generally make the Company responsible for patent filing, examination and extension costs, as well as costs relating to their protection and the payment of lump sums and royalties as certain milestones are reached as payment for the license granted by the co-owner on the rights which belong to it.

|

|

Note 20 : |

Related party transactions |

|

|

Note 20.1 : |

Compensation and director's attendance fees for executive corporate officers and members of the board of directors |

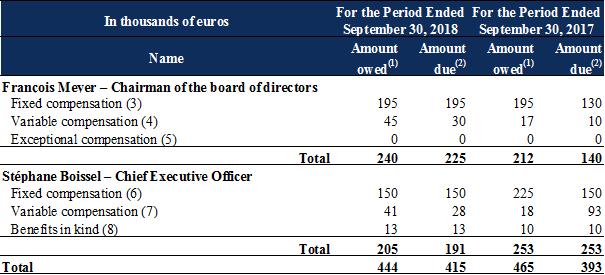

The compensation presented below was granted to executive corporate officers and members of the board of directors during the periods shown:

Exhibit 99.2

Salaries and other short-term benefits break down as follows:

|

|

(1) |

For the fiscal year. Variable compensation owed for one fiscal year is paid in the next fiscal year. |

|

|

(2) |

During the fiscal year. |

|

|

(3) |