Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - NET 1 UEPS TECHNOLOGIES INC | exhibit32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - NET 1 UEPS TECHNOLOGIES INC | exhibit31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - NET 1 UEPS TECHNOLOGIES INC | exhibit31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2018 OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934

For the transition period from ______________ To ______________

Commission file number: 000-31203

NET 1 UEPS TECHNOLOGIES,

INC.

(Exact name of registrant as specified in its

charter)

| Florida | 98-0171860 |

| (State or other jurisdiction | (IRS Employer |

| of incorporation or organization) | Identification No.) |

President Place, 4th Floor, Cnr.

Jan Smuts Avenue and Bolton Road

Rosebank, Johannesburg 2196,

South Africa

(Address of principal executive offices,

including zip code)

Registrant’s telephone number, including area code: 27-11-343-2000

Not Applicable

(Former Name, Former

Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted

electronically every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12

months (or for such shorter period that the registrant was required to submit

such files).

YES [X] NO [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act (check one):

| [ ] | Large accelerated filer | [X] | Accelerated filer |

| [ ] | Non-accelerated filer | [ ] | Smaller reporting company |

| [ ] | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Exchange Act).

YES [ ] NO [X ]

As of November 9, 2018 (the latest practicable date), 56,833,925 shares of the registrant’s common stock, par value $0.001 per share, net of treasury shares, were outstanding.

Form 10-Q

NET 1 UEPS TECHNOLOGIES, INC.

Table of Contents

1

Part I. Financial Information

Item 1. Financial Statements

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Balance Sheets

| Unaudited | As restated(A) | |||||

| September 30, | June 30, | |||||

| 2018 | 2018 | |||||

| (In thousands, except share data) | ||||||

| ASSETS | ||||||

| CURRENT ASSETS | ||||||

| Cash and cash equivalents | $ | 98,555 | $ | 90,054 | ||

| Restricted cash (Note 10) | 84,778 | - | ||||

| Pre-funded social welfare grants receivable (Note 2) | - | 2,965 | ||||

| Accounts receivable, net (Note 3) | 113,924 | 109,683 | ||||

| Finance loans receivable, net (Note 3) | 50,811 | 62,205 | ||||

| Inventory (Note 4) | 10,369 | 12,887 | ||||

| Total current assets before settlement assets | 358,437 | 277,794 | ||||

| Settlement assets (Note 5) | 68,566 | 149,047 | ||||

| Total current assets | 427,003 | 426,841 | ||||

| PROPERTY, PLANT AND EQUIPMENT, net of accumulated depreciation of – September: $130,655; June: $129,185 | 25,222 | 27,054 | ||||

| EQUITY-ACCOUNTED INVESTMENTS (Note 7) | 94,241 | 88,331 | ||||

| GOODWILL (Note 8) | 279,158 | 283,240 | ||||

| INTANGIBLE ASSETS, net (Note 8) | 121,824 | 131,132 | ||||

| DEFERRED INCOME TAXES | 8,007 | 6,312 | ||||

| OTHER LONG-TERM ASSETS, including reinsurance assets (Note 7 and Note 9) | 245,150 | 256,380 | ||||

| TOTAL ASSETS | 1,200,605 | 1,219,290 | ||||

| LIABILITIES | ||||||

| CURRENT LIABILITIES | ||||||

| Short-term credit facilities for ATM funding (Note 10) | 84,778 | - | ||||

| Short-term credit facilities (Note 10) | 3,313 | - | ||||

| Accounts payable | 23,134 | 35,055 | ||||

| Other payables | 82,292 | 47,994 | ||||

| Current portion of long-term borrowings (Note 10) | 33,937 | 44,695 | ||||

| Income taxes payable | 13,898 | 5,742 | ||||

| Total current liabilities before settlement obligations | 241,352 | 133,486 | ||||

| Settlement obligations (Note 5) | 68,566 | 149,047 | ||||

| Total current liabilities | 309,918 | 282,533 | ||||

| DEFERRED INCOME TAXES | 43,567 | 46,606 | ||||

| LONG-TERM BORROWINGS (Note 10) | 11,660 | 5,469 | ||||

| OTHER LONG-TERM LIABILITIES, including insurance policy liabilities (Note 9) | 3,419 | 38,580 | ||||

| TOTAL LIABILITIES | 368,564 | 373,188 | ||||

| COMMITMENTS AND CONTINGENCIES (Note 19) | ||||||

| REDEEMABLE COMMON STOCK | 107,672 | 107,672 | ||||

| EQUITY | ||||||

| COMMON STOCK (Note 11) | ||||||

| Authorized: 200,000,000 with

$0.001 par value; Issued and outstanding shares, net of treasury - September: 56,833,925; June: 56,685,925 |

80 | 80 | ||||

| PREFERRED STOCK | ||||||

| Authorized shares: 50,000,000

with $0.001 par value; Issued and outstanding shares, net of treasury: September: -; June: - |

- | - | ||||

| ADDITIONAL PAID-IN-CAPITAL | 276,865 | 276,201 | ||||

| TREASURY SHARES, AT COST: September: 24,891,292; June: 24,891,292 | (286,951 | ) | (286,951 | ) | ||

| ACCUMULATED OTHER COMPREHENSIVE LOSS (Note 1 and 12) | (189,528 | ) | (184,436 | ) | ||

| RETAINED EARNINGS (Note 1) | 832,426 | 837,625 | ||||

| TOTAL NET1 EQUITY | 632,892 | 642,519 | ||||

| NON-CONTROLLING INTEREST | 91,477 | 95,911 | ||||

| TOTAL EQUITY | 724,369 | 738,430 | ||||

| TOTAL

LIABILITIES, REDEEMABLE COMMON STOCK

AND SHAREHOLDERS’ EQUITY |

$ | 1,200,605 | $ | 1,219,290 | ||

(A) – Certain amounts shown here do not correspond to the Company’s 2018 financial statements and reflects an adjustment made, refer to Note 1 See Notes to Unaudited Condensed Consolidated Financial Statements

2

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Statements of Operations

| Three months ended | ||||||

| September 30, | ||||||

| 2018 | 2017 | |||||

| (In thousands, except per share | ||||||

| data) | ||||||

| REVENUE | $ | 125,884 | $ | 152,558 | ||

| EXPENSE | ||||||

| Cost of goods sold, IT processing, servicing and support | 72,316 | 74,652 | ||||

| Selling, general and administration | 41,878 | 43,934 | ||||

| Depreciation and amortization | 10,794 | 8,966 | ||||

| OPERATING INCOME | 896 | 25,006 | ||||

| INTEREST INCOME | 1,876 | 5,044 | ||||

| INTEREST EXPENSE | 2,759 | 2,121 | ||||

| INCOME BEFORE INCOME TAX EXPENSE | 13 | 27,929 | ||||

| INCOME TAX EXPENSE (Note 18) | 6,490 | 10,277 | ||||

| NET (LOSS) INCOME BEFORE EARNINGS FROM EQUITY-ACCOUNTED INVESTMENTS | (6,477 | ) | 17,652 | |||

| EARNINGS FROM EQUITY-ACCOUNTED INVESTMENTS | 1,373 | 2,075 | ||||

| NET (LOSS) INCOME | (5,104 | ) | 19,727 | |||

| NET INCOME ATTRIBUTABLE TO NON-CONTROLLING INTEREST | 95 | 244 | ||||

| NET (LOSS) INCOME ATTRIBUTABLE TO NET1 | $ | (5,199 | ) | $ | 19,483 | |

| Net (loss) income per share, in U.S. dollars (Note 14) | ||||||

| Basic (loss) earnings attributable to Net1 shareholders | $(0.09 | ) | $ | 0.34 | ||

| Diluted (loss) earnings attributable to Net1 shareholders | $(0.09 | ) | $ | 0.34 | ||

See Notes to Unaudited Condensed Consolidated Financial Statements

3

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Statements of Comprehensive Income

| Three months ended | ||||||

| September 30, | ||||||

| 2018 | 2017 | |||||

| (In thousands) | ||||||

| Net (loss) income | $ | (5,104 | ) | $ | 19,727 | |

| Other comprehensive (loss) income | ||||||

| Movement in foreign currency translation reserve | (13,322 | ) | (13,880 | ) | ||

| Movement in foreign currency translation reserve related to equity-accounted investments | 5,430 | (227 | ) | |||

| Total other comprehensive (loss) income, net of taxes | (7,892 | ) | (14,107 | ) | ||

| Comprehensive (loss) income | (12,996 | ) | 5,620 | |||

| Add (Less) comprehensive loss (income) attributable to non-controlling interest | 2,705 | (133 | ) | |||

| Comprehensive (loss) income attributable to Net1 | $ | (10,291 | ) | $ | 5,487 | |

See Notes to Unaudited Condensed Consolidated Financial Statements

4

NET 1 UEPS TECHNOLOGIES,

INC.

Unaudited Condensed

Consolidated Statement of Changes in

Equity for the three months ended September 30, 2017

(dollar amounts in thousands)

| Net 1 UEPS Technologies, Inc. Shareholders | ||||||||||||||||||||||||||||||||||||

| Number | Accumulated | |||||||||||||||||||||||||||||||||||

| Number | of | Number of | Additional | Other | Total | Non- | Redeemable | |||||||||||||||||||||||||||||

| of | Treasury | Treasury | Shares, Net | Paid-In | Retained | Comprehensive | Net1 | Controlling | Common | |||||||||||||||||||||||||||

| Shares | Amount | Shares | Shares | of Treasury | Capital | Earnings | (Loss) Income | Equity | Interest | Total | Stock | |||||||||||||||||||||||||

| Balance – July 1, 2017 | 81,261,029 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,369,737 | $ | 273,733 | $ | 773,276 | $ | (162,569 | ) | $ | 597,569 | $ | 2,766 | $ | 600,335 | $ | 107,672 | ||||||||||||

| Restricted stock granted (Note 13) | 588,594 | 588,594 | - | - | ||||||||||||||||||||||||||||||||

| Stock-based compensation charge (Note 13) | 869 | 869 | 869 | |||||||||||||||||||||||||||||||||

| Reversal of stock compensation charge (Note 13) | (30,635 | ) | (30,635 | ) | (42 | ) | (42 | ) | (42 | ) | ||||||||||||||||||||||||||

| Reversal of stock based- compensation charge related to equity-accounted investment | (207 | ) | (207 | ) | (207 | ) | ||||||||||||||||||||||||||||||

| Net income | 19,483 | 19,483 | 244 | 19,727 | ||||||||||||||||||||||||||||||||

| Other comprehensive income | (13,996 | ) | (13,996 | ) | (111 | ) | (14,107 | ) | ||||||||||||||||||||||||||||

| Balance – September 30, 2017 | 81,818,988 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,927,696 | $ | 274,353 | $ | 792,759 | $ | (176,565 | ) | $ | 603,676 | $ | 2,899 | $ | 606,575 | $ | 107,672 | ||||||||||||

See Notes to Unaudited Condensed Consolidated Financial Statements

5

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed Consolidated

Statement of Changes in Equity for the three

months ended September 30, 2018 (dollar

amounts in thousands)

| Net 1 UEPS Technologies, Inc. Shareholders | ||||||||||||||||||||||||||||||||||||

| Number | Accumulated | |||||||||||||||||||||||||||||||||||

| Number | of | Number of | Additional | Other | Total | Non- | Redeemabl | |||||||||||||||||||||||||||||

| of | Treasury | Treasury | Shares, Net | Paid-In | Retained | Comprehensive | Net1 | Controlling | Common | |||||||||||||||||||||||||||

| Shares | Amount | Shares | Shares | of Treasury | Capital | Earnings | (Loss) Income | Equity | Interest | Total | Stock | |||||||||||||||||||||||||

| Balance – July 1, 2018 | 81,577,217 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,685,925 | $ | 276,201 | $ | 812,426 | $ | (159,237 | ) | $ | 642,519 | $ | 95,911 | $ | 738,430 | $ | 107,672 | ||||||||||||

| Correction of error (Note 1) | 25,199 | (25,199 | ) | - | - | |||||||||||||||||||||||||||||||

| Balance – July 1, 2018 as restated | 81,577,217 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,685,925 | $ | 276,201 | $ | 837,625 | $ | (184,436 | ) | $ | 642,519 | $ | 95,911 | $ | 738,430 | $ | 107,672 | ||||||||||||

| Restricted stock granted (Note 13) | 148,000 | 148,000 | - | - | ||||||||||||||||||||||||||||||||

| Stock-based compensation charge (Note 13) | 587 | 587 | 587 | |||||||||||||||||||||||||||||||||

| Stock-based compensation charge related to equity-accounted investment (Note 7) | 77 | 77 | 77 | |||||||||||||||||||||||||||||||||

| Dividends paid to non-controlling interest | (1,729 | ) | (1,729 | ) | ||||||||||||||||||||||||||||||||

| Net (loss) income | (5,199 | ) | (5,199 | ) | 95 | (5,104 | ) | |||||||||||||||||||||||||||||

| Other comprehensive loss income (Note 12) | (5,092 | ) | (5,092 | ) | (2,800 | ) | (7,892 | ) | ||||||||||||||||||||||||||||

| Balance – September 30, 2018 | 81,725,217 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,833,925 | $ | 276,865 | $ | 832,426 | $ | (189,528 | ) | $ | 632,892 | $ | 91,477 | $ | 724,369 | $ | 107,672 | ||||||||||||

See Notes to Unaudited Condensed Consolidated Financial Statements

6

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Statements of Cash Flows

| Three months ended | ||||||

| September 30, | ||||||

| 2018 | 2017 | |||||

| (In thousands) | ||||||

| Cash flows from operating activities | ||||||

| Net (loss) income | $ | (5,104 | ) | $ | 19,727 | |

| Depreciation and amortization | 10,794 | 8,966 | ||||

| Earnings from equity-accounted investments | (1,373 | ) | (2,075 | ) | ||

| Interest on Cedar Cell note (Note 7) | (156 | ) | - | |||

| Fair value adjustments and re-measurements | (82 | ) | 91 | |||

| Interest payable | 110 | (88 | ) | |||

| Facility fee amortized | 87 | 133 | ||||

| (Profit) Loss on disposal of property, plant and equipment | (127 | ) | 105 | |||

| Stock-based compensation charge, net (Note 13) | 587 | 827 | ||||

| Dividends received from equity accounted investments | - | 912 | ||||

| Decrease (Increase) in accounts receivable, pre-funded social welfare grants receivable and finance loans receivable | 14,296 | (39,141 | ) | |||

| Decrease (Increase) in inventory | 2,185 | (1,526 | ) | |||

| (Decrease) Increase in accounts payable and other payables | (9,480 | ) | 3,429 | |||

| Increase in taxes payable | 8,354 | 8,838 | ||||

| Decrease in deferred taxes | (3,634 | ) | (991 | ) | ||

| Net cash provided by (used in) operating activities | 16,457 | (793 | ) | |||

| Cash flows from investing activities | ||||||

| Capital expenditures | (3,118 | ) | (1,473 | ) | ||

| Proceeds from disposal of property, plant and equipment | 274 | 316 | ||||

| Proceeds on return of investment (Note 7) | 284 | - | ||||

| Investment in Cell C (Note 7) | - | (151,003 | ) | |||

| Investment in equity of equity-accounted investments (Note 7) | - | (72,846 | ) | |||

| Net change in settlement assets | 75,931 | 212,649 | ||||

| Net cash provided by (used in) investing activities | 73,371 | (12,357 | ) | |||

| Cash flows from financing activities | ||||||

| Proceeds from bank overdraft (Note 10) | 84,655 | 31,880 | ||||

| Repayment of long-term borrowings (Note 10) | (10,260 | ) | (14,260 | ) | ||

| Long-term borrowings utilized (Note 10) | 7,801 | 95,431 | ||||

| Dividends paid to non-controlling interest | (1,729 | ) | - | |||

| Payment of guarantee fee (Note 10) | (136 | ) | (552 | ) | ||

| Repayment of bank overdraft (Note 10) | - | (2,952 | ) | |||

| Net change in settlement obligations | (75,931 | ) | (212,649 | ) | ||

| Net cash provided by (used in) financing activities | 4,400 | (103,102 | ) | |||

| Effect of exchange rate changes on cash | (949 | ) | (3,846 | ) | ||

| Net increase (decrease) in cash, cash equivalents and restricted cash | 93,279 | (120,098 | ) | |||

| Cash, cash equivalents and restricted cash – beginning of period | 90,054 | 258,457 | ||||

| Cash, cash equivalents and restricted cash – end of period (1) | $ | 183,333 | $ | 138,359 | ||

See Notes to Unaudited Condensed Consolidated Financial Statements

(1) Cash, cash equivalents and restricted cash as of September 30, 2018, includes restricted cash of approximately $84.8 million related to cash withdrawn from the Company’s various debt facilities to fund ATMs. This cash may only be used to fund ATMs and is considered restricted as to use and therefore is classified as restricted cash. Refer to Note 10 for additional information regarding the Company’s facilities.

7

NET 1 UEPS TECHNOLOGIES, INC.

Notes to the

Unaudited Condensed Consolidated Financial Statements

for the three

months ended September 30, 2018 and 2017

(All amounts in tables

stated in thousands or thousands of U.S. dollars, unless otherwise stated)

1. Basis of Presentation and Summary of Significant Accounting Policies

Unaudited Interim Financial Information

The accompanying unaudited condensed consolidated financial statements include all majority-owned subsidiaries over which the Company exercises control and have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) and the rules and regulations of the United States Securities and Exchange Commission for Quarterly Reports on Form 10-Q and include all of the information and disclosures required for interim financial reporting. The results of operations for the three months ended September 30, 2018 and 2017, are not necessarily indicative of the results for the full year. The Company believes that the disclosures are adequate to make the information presented not misleading.

These financial statements should be read in conjunction with the financial statements, accounting policies and financial notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended June 30, 2018. In the opinion of management, the accompanying unaudited condensed consolidated financial statements reflect all adjustments (consisting only of normal recurring adjustments), which are necessary for a fair representation of financial results for the interim periods presented.

References to the “Company” refer to Net1 and its consolidated subsidiaries, collectively, unless the context otherwise requires. References to “Net1” are references solely to Net 1 UEPS Technologies, Inc.

Restatement of Form10-K for the year ended June 30, 2018

Subsequent to the issuance of the Form 10-K, and as disclosed in the Form 8-K dated November 8, 2018, the Company announced that it would restate its consolidated financial statements for the year ended June 30, 2018, included in the Company’s Annual Report on Form 10-K for the year ended June 30, 2018, due to the identification of an error in its accounting for its investment in an equity security. The Company incorrectly classified and recorded its investment in Cell C Proprietary Limited (“Cell C”), an unlisted company that the Company elected to carry at fair value using the fair value option, as available-for-sale and recorded the change in its fair value of $25.2 million, net of taxation of $7.3 million, in other comprehensive income for the year ended June 30, 2018. The Company has now determined that the investment in Cell C should have been accounted at fair value with changes in fair value recorded in the statement of operations. The tables below present the impact of the restatement on each of the Company’s financial statements for the year ended June 30, 2018:

| Consolidated balance sheet | |||||||||

| As of June 30, 2018 | |||||||||

| As | As | ||||||||

| Reported | Correction | Restated | |||||||

| (in thousands) | |||||||||

| Accumulated other comprehensive loss | $ | (159,237 | ) | $ | (25,199 | ) | $ | (184,436 | ) |

| Retained earnings | 812,426 | 25,199 | 837,625 | ||||||

| Total equity | $ | 738,430 | $ | - | $ | 738,430 | |||

| Consolidated statement of operations | |||||||||

| Year ended June 30, 2018 | |||||||||

| As | As | ||||||||

| Reported | Correction | Restated | |||||||

| (in thousands, except per share data) | |||||||||

| Change in fair value of equity securities | $ | - | $ | 32,473 | $ | 32,473 | |||

| Income before income taxes | 67,893 | 32,473 | 100,366 | ||||||

| Income tax expense | 41,353 | 7,274 | 48,627 | ||||||

| Net income before earnings from equity-accounted investments | 26,540 | 25,199 | 51,739 | ||||||

| Net income | 38,270 | 25,199 | 63,469 | ||||||

| Net income attributable to Net1 | $ | 39,150 | $ | 25,199 | $ | 64,349 | |||

| Net income per share, in United States dollars: | |||||||||

| Basic earnings attributable to Net1 shareholders | 0.69 | 0.44 | 1.13 | ||||||

| Diluted earnings attributable to Net1 shareholders | 0.69 | 0.44 | 1.13 | ||||||

8

1. Basis of Presentation and Summary of Significant Accounting Policies (continued)

Restatement of Form10-K for the year ended June 30, 2018 (continued)

| Consolidated statement of comprehensive income | |||||||||

| Year ended June 30, 2018 | |||||||||

| As | As | ||||||||

| Reported | Correction | Restated | |||||||

| (in thousands) | |||||||||

| Net income | $ | 38,270 | $ | 25,199 | $ | 63,469 | |||

| Net unrealized income on asset available for sale, net of tax | 25,199 | (25,199 | ) | - | |||||

| Total other comprehensive income (loss) | 3,234 | (25,199 | ) | (21,965 | ) | ||||

| Comprehensive income | $ | 41,504 | $ | - | $ | 41,504 | |||

| Consolidated statement of changes in equity | ||||||

| Retained | Accumulated other | |||||

| earnings | comprehensive loss | |||||

| (in thousands) | ||||||

| As reported – June 30, 2018 | $ | 812,426 | $ | (159,237) | ||

| Correction of misstatement | 25,199 | (25,199 | ) | |||

| As restated – June 30, 2018 | $ | 837,625 | $ | (184,436 | ) | |

| Consolidated statement of cash flows | |||||||||

| Year ended June 30, 2018 | |||||||||

| As | As | ||||||||

| Reported | Correction | Restated | |||||||

| (in thousands) | |||||||||

| Net income | $ | 38,270 | $ | 25,199 | $ | 63,469 | |||

| Fair value adjustment | 212 | (32,473 | ) | (32,685 | ) | ||||

| Increase (Decrease) in deferred taxes | (1,308 | ) | 7,274 | 5,966 | |||||

| Net cash provided by operating activities | $ | 132,605 | $ | - | $ | 132,605 | |||

The restatement does not affect the current financial results reported on this Quarterly Report on Form 10-Q. For more information concerning the restatement, please see the Current Report on Form 8-K filed by the Company with the Securities and Exchange Commission (“SEC”) on November 8, 2018.

Recent accounting pronouncements adopted

In May 2014, the Financial Accounting Standards Board (“FASB”) issued guidance regarding Revenue from Contracts with Customers. This guidance requires an entity to recognize revenue when a customer obtains control of promised goods or services in an amount that reflects the consideration which the entity expects to receive in exchange for those goods or services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The guidance was originally set to be effective for the Company beginning July 1, 2017, however in August 2015, the FASB issued guidance regarding Revenue from Contracts with Customers, Deferral of the Effective Date. This guidance deferred the required implementation date specified in Revenue from Contracts with Customers to December 2017. Public companies may elect to adopt the standard along the original timeline. The guidance became effective for the Company beginning July 1, 2018. The Company elected the modified retrospective transition method upon adoption of this guidance. The adoption of this guidance did not have a material impact on the Company’s financial statements, except for the additional footnote disclosures provided.

In January 2016, the FASB issued guidance regarding Recognition and Measurement of Financial Assets and Financial Liabilities. The guidance primarily affects the accounting for equity investments, financial liabilities under the fair value option and the presentation and disclosure requirements for financial instruments. The guidance requires changes in the fair value of the Company’s equity investments, with certain exceptions, to be recognized through net income rather than other comprehensive income. In addition, the guidance clarifies the valuation allowance assessment when recognizing deferred tax assets resulting from unrealized losses on available-for-sale debt securities. This guidance became effective for the Company beginning July 1, 2018, and early adoption is not permitted, with certain exceptions. The amendments are required to be applied by means of a cumulative-effect adjustment on the balance sheet as of the beginning of the fiscal year of adoption. The adoption of this guidance did not have a material impact on the Company’s financial statements.

9

1. Basis of Presentation and Summary of Significant Accounting Policies (continued)

Recent accounting pronouncements adopted (continued)

Equity securities are measured at fair value. The Company may elect to measure equity securities without readily determinable fair values at cost with adjustments for observable changes in price or impairments for the identical or a similar investment of the same issuer. We perform a qualitative assessment on a quarterly basis and recognize an impairment loss if there are sufficient indicators that the fair value of the equity security is less than carrying value. There were no changes in the fair value of our equity securities recorded during the three months ended September 30, 2018. Changes in fair value will be recorded in our condensed consolidated statement of operations in future periods within a caption titled “changes in fair value of equity securities”

In June 2016, the FASB issued guidance regarding Classification of Certain Cash Receipts and Cash Payments. The guidance is intended to reduce diversity in practice and explains how certain cash receipts and payments are presented and classified in the statement of cash flows, including beneficial interests in securitization, which would impact the presentation of the deferred purchase price from sales of receivables.

This guidance became effective for the Company beginning July 1, 2018, and must be applied retrospectively. The Company has elected to classify distributions received from equity method investees using the nature of the distribution approach. This election requires the Company to evaluate each distribution received on the basis of the source of the payment and classify the distribution as either operating cash inflows or investing cash inflows. The adoption of this guidance did not have a material impact on the Company’s financial statements and the Company was not required to make any retrospective adjustments.

In January 2017, the FASB issued guidance regarding Clarifying the Definition of a Business. This guidance provides a more robust framework to use in determining when a set of assets and activities is a business. Because the current definition of a business is interpreted broadly and can be difficult to apply, stakeholders indicated that analyzing transactions is inefficient and costly and that the definition does not permit the use of reasonable judgment. The amendments provide more consistency in applying the guidance, reduce the costs of application, and make the definition of a business more operable. The guidance became effective for the Company beginning July 1, 2018. The adoption of this guidance did not have a material impact on the Company’s financial statements.

In January 2017, the FASB issued guidance regarding Simplifying the Test for Goodwill Impairment. This guidance removes the requirement for an entity to calculate the implied fair value of goodwill (as part of step 2 of the current goodwill impairment test) in measuring a goodwill impairment loss. The guidance is effective for the Company beginning July 1, 2020. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. The Company has elected to early adopt this guidance beginning July 1, 2018. The adoption of this guidance did not have a material impact on the Company’s financial statements.

In May 2017, the FASB issued guidance regarding Compensation—Stock Compensation (Topic 718): Scope of Modification Accounting. The guidance amends the scope of modification accounting for share-based payment arrangements and provides guidance on the types of changes to the terms or conditions of share-based payment awards to which an entity would be required to apply modification accounting under Accounting Standards Codification 718. Specifically, an entity would not apply modification accounting if the fair value, vesting conditions, and classification of the awards are the same immediately before and after the modification. The guidance became effective for the Company beginning July 1, 2018. The adoption of this guidance did not have a material impact on the Company’s financial statements.

In June 2018, the FASB issued guidance regarding Improvements to Nonemployee Share-Based Payment Accounting. The guidance simplifies the accounting for share-based payments granted to non-employees for goods and services and aligns the guidance for these share-based payments with guidance applicable to accounting for share-based payments granted to employees. The guidance is effective for the Company beginning July 1, 2019. Early adoption is permitted. The Company has elected to early adopt this guidance beginning July 1, 2018. The adoption of this guidance did not have a material impact on the Company’s financial statements.

Recent accounting pronouncements not yet adopted as of September 30, 2018

In February 2016, the FASB issued guidance regarding Leases. The guidance increases transparency and comparability among organizations by requiring the recognition of lease assets and lease liabilities on the balance sheet. The amendments to current lease guidance include the recognition of assets and liabilities by lessees for those leases currently classified as operating leases. The guidance also requires disclosures to meet the objective of enabling users of financial statements to assess the amount, timing, and uncertainty of cash flows arising from leases. This guidance is effective for the Company beginning July 1, 2019. Early adoption is permitted. The Company expects that this guidance may have a material impact on its financial statements and is currently evaluating the impact of this guidance on its financial statements on adoption.

10

1. Basis of Presentation and Summary of Significant Accounting Policies (continued)

Recent accounting pronouncements not yet adopted as of September 30, 2018 (continued)

In June 2016, the FASB issued guidance regarding Measurement of Credit Losses on Financial Instruments. The guidance replaces the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. For trade and other receivables, loans, and other financial instruments, an entity is required to use a forward-looking expected loss model rather than the incurred loss model for recognizing credit losses, which reflects losses that are probable. Credit losses relating to available-for-sale debt securities will also be recorded through an allowance for credit losses rather than as a reduction in the amortized cost basis of the securities. This guidance is effective for the Company beginning July 1, 2020. Early adoption is permitted beginning July 1, 2019. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

In August 2018, the FASB issued guidance regarding Disclosure Framework: Changes to the Disclosure Requirements for Fair Value Measurement. The guidance modifies the disclosure requirements related to fair value measurement. This guidance is effective for the Company beginning July 1, 2020. Early adoption is permitted. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

2. Pre-funded social welfare grants receivable

Pre-funded social welfare grants receivable represents primarily amounts pre-funded by the Company to certain merchants participating in the merchant acquiring system. The Company’s contract with the South African Social Security Agency expired on September 30, 2018, and therefore the Company no longer pre-funds social welfare grants. The July 2018 payment service commenced on July 1, 2018 but the Company pre-funded certain merchants participating in the merchant acquiring systems on the last day of June 2018.

3. Accounts receivable, net and finance loans receivable,

net

Accounts receivable, net

The Company’s accounts receivable, net, as of September 30, 2018 and June 30, 2018, is presented in the table below:

| September 30, | June 30, | ||||||||||

| 2018 | 2018 | ||||||||||

| Accounts receivable, trade, net | $ | 38,240 | $ | 49,365 | |||||||

| Accounts receivable, trade, gross | 39,632 | 50,466 | |||||||||

| Allowance for doubtful accounts receivable, end of period | 1,392 | 1,101 | |||||||||

| Beginning of year | 1,101 | 1,255 | |||||||||

| Reversed to statement of operations | (2 | ) | (47 | ) | |||||||

| Charged to statement of operations | 1,089 | 642 | |||||||||

| Utilized | (832 | ) | (776 | ) | |||||||

| Foreign currency adjustment | 36 | 27 | |||||||||

| Current portion of payments to agents in South Korea amortized over the contract period | 20,695 | 21,971 | |||||||||

| Payments to agents in South Korea amortized over the contract period | 36,641 | 39,554 | |||||||||

| Less:

Payments to agents in South Korea amortized over the contract period

included in other long-term assets (Note 7) |

15,946 | 17,582 | |||||||||

| Loans provided to Finbond | 1,074 | 1,107 | |||||||||

| Contingent purchase consideration | 8,033 | - | |||||||||

| Other receivables | 45,882 | 37,240 | |||||||||

| Total accounts receivable, net | $ | 113,924 | $ | 109,683 |

11

3. Accounts receivable, net and finance loans receivable, net (continued)

Finance loans receivable, net

The Company’s finance loans receivable, net, as of September 30, 2018 and June 30, 2018, is presented in the table below:

| September | |||||||||||

| 30, | June 30, | ||||||||||

| 2018 | 2018 | ||||||||||

| Microlending finance loans receivable, net | $ | 46,078 | $ | 57,504 | |||||||

| Microlending finance loans receivable, gross | 52,453 | 61,743 | |||||||||

| Allowance for doubtful microlending finance loans receivable, end of period | 6,375 | 4,239 | |||||||||

| Beginning of year | 4,239 | 3,717 | |||||||||

| Charged to statement of operations | 4,271 | 4,348 | |||||||||

| Utilized | (2,117 | ) | (3,588 | ) | |||||||

| Foreign currency adjustment | (18 | ) | (238 | ) | |||||||

| Working capital finance receivable, net | 3,834 | 3,959 | |||||||||

| Working capital finance receivable, gross | 16,180 | 16,123 | |||||||||

| Allowance for doubtful working capital finance receivable, end of period | 12,346 | 12,164 | |||||||||

| Beginning of year | 12,164 | 3,752 | |||||||||

| Charged to statement of operations | 181 | 8,415 | |||||||||

| Foreign currency adjustment | 1 | (3 | ) | ||||||||

| Current portion of other finance loans receivable | 899 | 742 | |||||||||

| Total other finance loans receivable | 17,060 | 13,025 | |||||||||

| Less included in other long-term assets | 16,161 | 12,283 | |||||||||

| Total finance loans receivable, net | $ | 50,811 | $ | 62,205 |

4. Inventory

The Company’s inventory comprised the following category as of September 30, 2018 and June 30, 2018.

| September 30, | June 30, | |||||

| 2018 | 2018 | |||||

| Finished goods | $ | 10,369 | $ | 12,887 | ||

| $ | 10,369 | $ | 12,887 |

5. Settlement assets and settlement obligations

Settlement assets comprise (1) cash received from the South African government that the Company holds pending disbursement to recipient cardholders of social welfare grants and (2) cash received from customers on whose behalf the Company processes payroll payments that the Company will disburse to customer employees, payroll-related payees and other payees designated by the customer.

Settlement obligations comprise (1) amounts that the Company is obligated to disburse to recipient cardholders of social welfare grants, and (2) amounts that the Company is obligated to pay to customer employees, payroll-related payees and other payees designated by the customer.

The balances at each reporting date may vary widely depending on the timing of the receipts and payments of these assets and obligations.

12

6. Fair value of financial instruments

Fair value of financial instruments

Initial recognition and measurement

Financial instruments are recognized when the Company becomes a party to the transaction. Initial measurements are at cost, which includes transaction costs.

Risk management

The Company manages its exposure to currency exchange, translation, interest rate, customer concentration, credit and equity price and liquidity risks as discussed below.

Currency exchange risk

The Company is subject to currency exchange risk because it purchases inventories that it is required to settle in other currencies, primarily the euro and U.S. dollar. The Company has used forward contracts in order to limit its exposure in these transactions to fluctuations in exchange rates between the South African rand (“ZAR”), on the one hand, and the U.S. dollar and the euro, on the other hand.

Translation risk

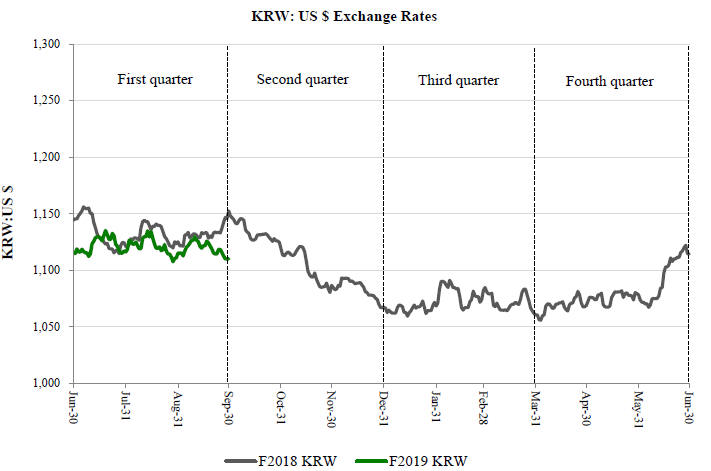

Translation risk relates to the risk that the Company’s results of operations will vary significantly as the U.S. dollar is its reporting currency, but it earns most of its revenues and incurs most of its expenses in ZAR. The U.S. dollar to ZAR exchange rate has fluctuated significantly over the past three years. As exchange rates are outside the Company’s control, there can be no assurance that future fluctuations will not adversely affect the Company’s results of operations and financial condition.

Interest rate risk

As a result of its normal borrowing and lending activities, the Company’s operating results are exposed to fluctuations in interest rates, which it manages primarily through regular financing activities. The Company generally maintains limited investments in cash equivalents and held to maturity investments and has occasionally invested in marketable securities.

Credit risk

Credit risk relates to the risk of loss that the Company would incur as a result of non-performance by counterparties. The Company maintains credit risk policies with regard to its counterparties to minimize overall credit risk. These policies include an evaluation of a potential counterparty’s financial condition, credit rating, and other credit criteria and risk mitigation tools as the Company’s management deems appropriate.

Credit risk (continued)

With respect to credit risk on financial instruments, the Company maintains a policy of entering into such transactions only with South African and European financial institutions that have a credit rating of “B” (or its equivalent) or better, as determined by credit rating agencies such as Standard & Poor’s, Moody’s and Fitch Ratings.

Microlending credit risk

The Company is exposed to credit risk in its microlending activities, which provide unsecured short-term loans to qualifying customers. The Company manages this risk by performing an affordability test for each prospective customer and assigning a “creditworthiness score”, which takes into account a variety of factors such as other debts and total expenditures on normal household and lifestyle expenses.

Equity price and liquidity risk

Equity price risk relates to the risk of loss that the Company would incur as a result of the volatility in the exchange-traded price of equity securities that it holds and the risk that it may not be able to liquidate these securities. The market price of these securities may fluctuate for a variety of reasons and, consequently, the amount that the Company may obtain in a subsequent sale of these securities may significantly differ from the reported market value.

Liquidity risk relates to the risk of loss that the Company would incur as a result of the lack of liquidity on the exchange on which these securities are listed. The Company may not be able to sell some or all of these securities at one time, or over an extended period of time without influencing the exchange traded price, or at all.

13

6. Fair value of financial instruments (continued)

Financial instruments

The following section describes the valuation methodologies the Company uses to measure its significant financial assets and liabilities at fair value.

In general, and where applicable, the Company uses quoted prices in active markets for identical assets or liabilities to determine fair value. This pricing methodology would apply to Level 1 investments. If quoted prices in active markets for identical assets or liabilities are not available to determine fair value, then the Company uses quoted prices for similar assets and liabilities or inputs other than the quoted prices that are observable either directly or indirectly. These investments would be included in Level 2 investments. In circumstances in which inputs are generally unobservable, values typically reflect management’s estimates of assumptions that market participants would use in pricing the asset or liability. The fair values are therefore determined using model-based techniques that include option pricing models, discounted cash flow models, and similar techniques. Investments valued using such techniques are included in Level 3 investments.

Asset measured at fair value using significant unobservable inputs – investment in Cell C

The Company’s Level 3 asset represents an investment of 75,000,000 class “A” shares in Cell C, a leading mobile telecoms provider in South Africa. The Company has developed an adjusted EV/EBITDA multiple valuation model in order to determine the fair value of the Cell C shares. The primary inputs to the valuation model as of September 30, 2018, are unchanged from June 30, 2018. The primary inputs to the valuation model are Cell C’s annualized adjusted EBITDA for the 11 months ended June 30, 2018, of ZAR 3.9 billion ($275.8 million, translated at exchange rates applicable as of September 30, 2018), an EBITDA multiple of 6.75, Cell C’s net external debt of ZAR 8.8 billion ($622.3 million, translated at exchange rates applicable as of September 30, 2018) and a marketability discount of 10% as Cell C is not currently listed, but has publicly stated its intention to list. The EBITDA multiple was determined based on an analysis of Cell C’s peer group, which comprises various African and emerging market mobile telecommunications operators. The fair value of Cell C utilizing the adjusted EV/EBITDA valuation model developed by the Company is sensitive to the following inputs: (i) the Company’s determination of adjusted EBITDA (ii) the EBITDA multiple used and (iii) the marketability discount used. Utilization of different inputs, or changes to these inputs, may result in significantly higher or lower fair value measurement.

The following table presents the impact of a 0.50 increase and 0.50 decrease to the EBITDA multiple used in the Cell C valuation on the September 30, 2018, carrying value of the Company’s Cell C investment (all amounts translated at exchange rates applicable as of September 30, 2018):

| Sensitivity for | |||

| fair value of | |||

| Cell C investment | |||

| EBITDA multiple of 6.25 times | $ | 149,179 | |

| EBITDA multiple of 6.75 times | $ | 167,835 | |

| EBITDA multiple of 7.25 times | $ | 186,490 |

The fair value of the Cell C shares as of September 30, 2018, represented approximately 14% of the Company’s total assets, including these shares. The Company expects to hold these shares for an extended period of time and it is not concerned with short-term equity price volatility with respect to these shares provided that the underlying business, economic and management characteristics of the company remain sound.

Liability measured at fair value using significant unobservable inputs – DNI contingent consideration

The salient terms of the Company’s investment in DNI is described in Note 3 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2018. Under the terms of its subscription agreements with DNI, the Company has agreed to pay to DNI an additional amount of up to ZAR 400.0 million ($28.3 million, translated at exchange rates applicable as of September 30, 2018), in cash, subject to the achievement of certain performance targets by DNI. The Company expects to pay the additional amount during the first quarter of the year ended June 30, 2020, and has recorded an amount of ZAR 379.6 million ($26.8 million) and ZAR 373.6 million ($27.2 million), in other payables in its unaudited condensed consolidated balance sheet as of September 30, 2018, and in long-term liabilities as of June 30, 2018, respectively, which amount represents the present value of the ZAR 400.0 million to be paid (amounts translated at exchange rates applicable as of September 30, 2018 and June 30, 2018, respectively).

14

6. Fair value of financial instruments (continued)

Financial instruments (continued)

Liability measured at fair value using significant unobservable inputs – DNI contingent consideration (continued)

The present value of ZAR 379.6 million has been calculated using the following assumptions (a) the maximum additional amount of ZAR 400.0 million will be paid on August 1, 2019 and (b) an interest rate of 6.3 % (the rate used to calculate interest earned by the Company on its surplus South African funds) has been used to discount the ZAR 400.0 million to its present value as of September 30, 2018. Utilization of different inputs, or changes to these inputs, may result in significantly higher or lower fair value measurement.

Derivative transactions - Foreign exchange contracts

As part of the Company’s risk management strategy, the Company enters into derivative transactions to mitigate exposures to foreign currencies using foreign exchange contracts. These foreign exchange contracts are over-the-counter derivative transactions. Substantially all of the Company’s derivative exposures are with counterparties that have long-term credit ratings of “B” (or equivalent) or better. The Company uses quoted prices in active markets for similar assets and liabilities to determine fair value (Level 2). The Company has no derivatives that require fair value measurement under Level 1 or 3 of the fair value hierarchy.

The Company’s outstanding foreign exchange contracts are as follows as of September 30, 2018:

| Fair market | |||

| Notional amount | Strike price | value price | Maturity |

| USD 269,800 | ZAR 14.2023 | ZAR 14.1489 | October 2, 2018 |

| USD 280,000 | ZAR 15.2480 | ZAR 14.2466 | November 23, 2018 |

| USD 420,000 | ZAR 15.3071 | ZAR 14.2993 | December 21, 2018 |

| USD 420,000 | ZAR 15.3801 | ZAR 14.3647 | January 25, 2019 |

| USD 140,000 | ZAR 15.4386 | ZAR 14.4168 | February 22, 2019 |

| USD 420,000 | ZAR 15.4939 | ZAR 14.4652 | March 20, 2019 |

| USD 420,000 | ZAR 15.5704 | ZAR 14.5334 | April 26, 2019 |

The Company had no outstanding foreign exchange contracts as of June 30, 2018.

The following table presents the Company’s assets and liabilities measured at fair value on a recurring basis as of September 30, 2018, according to the fair value hierarchy:

| Quoted price in | Significant | ||||||||||||

| active markets | other | Significant | |||||||||||

| for identical | observable | unobservable | |||||||||||

| assets | inputs | inputs | |||||||||||

| (Level 1) | (Level 2) | (Level 3) | Total | ||||||||||

| Assets | |||||||||||||

| Investment in Cell C | $ | - | $ | - | $ | 167,835 | $ | 167,835 | |||||

| Related to insurance business: | |||||||||||||

| Cash, cash equivalents and

restricted cash (included in other long-term assets) |

598 | - | - | 598 | |||||||||

| Fixed

maturity investments (included

in cash and cash equivalents) |

7,853 | - | - | 7,853 | |||||||||

| Other | - | 18 | - | 18 | |||||||||

| Total assets at fair value | $ | 8,451 | $ | 18 | $ | 167,835 | $ | 176,304 | |||||

| Liabilities | |||||||||||||

| DNI contingent consideration | $ | - | $ | - | $ | 26,839 | $ | 26,839 | |||||

| Foreign exchange contracts | - | 152 | - | 152 | |||||||||

| Total liabilities at fair value | $ | - | $ | 152 | $ | 26,839 | $ | 26,991 |

15

6. Fair value of financial instruments (continued)

Financial instruments (continued)

The following table presents the Company’s assets and liabilities measured at fair value on a recurring basis as of June 30, 2018, according to the fair value hierarchy:

| Quoted price in | Significant | |||||||||||

| active markets | other | Significant | ||||||||||

| for identical | observable | unobservable | ||||||||||

| assets | inputs | inputs | ||||||||||

| (Level 1) | (Level 2) | (Level 3) | Total | |||||||||

| Assets | ||||||||||||

| Investment in Cell C | $ | - | $ | - | $ | 172,948 | $ | 172,948 | ||||

| Related to insurance business: | ||||||||||||

| Cash and cash

equivalents (included in

other long-term assets) |

610 | - | - | 610 | ||||||||

| Fixed maturity investments

(included in cash, cash equivalents and restricted cash) |

8,304 | - | - | 8,304 | ||||||||

| Other | - | 18 | - | 18 | ||||||||

| Total assets at fair value | $ | 8,914 | $ | 18 | $ | 172,948 | $ | 181,880 | ||||

| Liabilities | ||||||||||||

| DNI contingent consideration | $ | - | $ | - | $ | 27,222 | $ | 27,222 | ||||

| Total liabilities at fair value | $ | - | $ | - | $ | 27,222 | $ | 27,222 |

There have been no transfers in or out of Level 3 during the three months ended September 30 2018 and 2017, respectively.

Summarized below is the movement in the carrying value of assets and liabilities measured at fair value on a recurring basis, and categorized within Level 3, during the three months ended September 30, 2018:

| Assets |

Carrying value |

||

| Balance as at June 30, 2018 | $ | 172,948 | |

| Foreign currency adjustment | (5,113 | ) | |

| Balance as of September 30, 2018 | $ | 167,835 | |

| Liabilities | |||

| Balance as at June 30, 2018 | $ | 27,222 | |

| Accretion of interest | 422 | ||

| Foreign currency adjustment(1) | (805 | ) | |

| Balance as of September 30, 2018 | $ | 26,839 |

(1) The foreign currency adjustment represents the effects of the fluctuations of the South African rand and the U.S. dollar on the carrying value.

Summarized below is the movement in the carrying value of assets and liabilities measured at fair value on a recurring basis, and categorized within Level 3, during the three months ended September 30, 2017:

| Carrying value | |||

| Assets | |||

| Acquisition of investment in Cell C | $ | 151,003 | |

| Foreign currency adjustment | (3,530 | ) | |

| Balance as of September 30, 2017 | $ | 147,473 |

(1) The foreign currency adjustment represents the effects of the fluctuations of the South African rand and the U.S. dollar on the carrying value.

Assets measured at fair value on a nonrecurring basis

We measure equity investments without readily determinable fair values on a nonrecurring basis. The fair values of these investments are determined based on valuation techniques using the best information available, and may include quoted market prices, market comparables, and discounted cash flow projections.

16

7. Equity-accounted investments and other long-term assets

Refer to Note 9 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2018, for additional information regarding its equity-accounted investments and other long-term assets.

Equity-accounted investments

The Company’s ownership percentage in its equity-accounted investments as of September 30, 2018 and June 30, 2018, was as follows:

| September | June 30, | ||

| 30, 2018 | 2018 | ||

| Bank Frick & Co AG (“Bank Frick”) | 35% | 35% | |

| Fanaka Holdings (Pty) Ltd (“Fanaka”) | 40% | - | |

| Finbond Group Limited (“Finbond”) | 29% | 29% | |

| OneFi Limited (formerly KZ One) (“OneFi”) | 25% | 25% | |

| SmartSwitch Namibia (Pty) Ltd (“SmartSwitch Namibia”) | 50% | 50% | |

| Speckpack Field Services (Pty) Ltd (“Speckpack”) | 50% | 50% | |

| Walletdoc Proprietary Limited (“Walletdoc”) | 20% | 20% |

Finbond

As of September 30, 2018, the Company owned 267,672,032 shares in Finbond. Finbond is listed on the Johannesburg Stock Exchange and its closing price on September 28, 2018, the last trading day of the quarter, was R3.60 per share. The market value of the Company’s holding in Finbond on September 30, 2018 was ZAR 1.0 billion ($72 million translated at exchange rates applicable as of September 30, 2018). On July 11, 2018, the Company, pursuant to its election, received an additional 6,602,551 shares in Finbond as a capitalization share issue in lieu of a dividend.

V2 Limited

On October 4, 2018, the Company acquired a 50% voting and economic interest in V2 Limited (“V2”) for $2.5 million. V2 is an Africa-focused technology provider dedicated to providing financial inclusion to the roughly one billion underbanked citizens on the continent. The Company has committed to provide V2 with a further equity contribution of $2.5 million and a working capital facility of $5.0 million, which are both subject to the achievement of certain pre-defined objectives. V2 will have access to license Zapper’s quick response (“QR”) payment technology as well as the Company’s various payment solutions such as UEPS/EMV and mobile virtual card. Zapper’s QR technology and payment platform is one of the most advanced and complete QR payment offerings, and it has operations currently in South Africa, the United Kingdom and the United States. V2 will partner with Zapper to launch ZappGroup Africa, a company focused on deploying a universal white-label QR payment solution.

17

7. Equity-accounted investments and other long-term assets (continued)

Equity-accounted investments (continued)

Summarized below is the movement in equity-accounted investments during the three months ended September 30, 2018:

| Bank | ||||||||||||

| Frick | Finbond | Other(1) | Total | |||||||||

| Investment in equity: | ||||||||||||

| Balance as of June 30, 2018 | $ | 48,129 | $ | 30,958 | $ | 6,092 | $ | 85,179 | ||||

| Acquisition of shares | - | 1,920 | - | 1,920 | ||||||||

| Stock-based compensation | - | 77 | - | 77 | ||||||||

| Comprehensive income (loss): | (588 | ) | 7,305 | 86 | 6,803 | |||||||

| Other comprehensive loss | - | 5,430 | - | 5,430 | ||||||||

| Equity accounted earnings (loss) | (588 | ) | 1,875 | 86 | 1,373 | |||||||

| Share of net income | 162 | 1,852 | 86 | 2,100 | ||||||||

| Amortization of acquired intangible assets | (189 | ) | - | - | (189 | ) | ||||||

| Deferred taxes on acquired intangible assets | 45 | - | - | 45 | ||||||||

| Dilution resulting from corporate transactions | - | 23 | - | 23 | ||||||||

| Other | (606 | ) | - | - | (606 | ) | ||||||

| Dividends received | - | (1,920 | ) | - | (1,920 | ) | ||||||

| Return on investment | - | - | (284 | ) | (284 | ) | ||||||

| Foreign currency adjustment(2) | 435 | (1,059 | ) | (57 | ) | (681 | ) | |||||

| Balance as of September 30, 2018 | $ | 47,976 | $ | 37,281 | $ | 5,837 | $ | 91,094 | ||||

| Investment in loans: | ||||||||||||

| Balance as of June 30, 2018 | $ | - | $ | - | $ | 3,152 | $ | 3,152 | ||||

| Foreign currency adjustment(2) | - | - | (5 | ) | (5 | ) | ||||||

| Balance as of September 30, 2018 | $ | - | $ | - | $ | 3,147 | $ | 3,147 |

| Equity | Loans | Total | ||||||||||

| Carrying amount as of: | ||||||||||||

| June 30, 2018 | $ | 85,179 | $ | 3,152 | $ | 88,331 | ||||||

| September 30, 2018 | $ | 91,094 | $ | 3,147 | $ | 94,241 |

(1) Includes OneFi, SmartSwitch

Namibia, Speckpack, Fanaka and Walletdoc;

(2) The foreign currency

adjustment represents the effects of the fluctuations of the South African rand,

Swiss franc, Nigerian naira and Namibian dollar, and the U.S. dollar on the

carrying value.

Other long-term assets

Summarized below is the breakdown of other long-term assets as of September 30, 2018, and June 30, 2018:

| September 30, | June 30, | |||||||

| 2018 | 2018 | |||||||

| Total equity investments | $ | 194,570 | $ | 199,865 | ||||

| Investment in 15% of Cell C, at fair value (Note 6) | 167,835 | 172,948 | ||||||

| Investment in 12% of MobiKwik, at fair value(1) | 26,735 | 26,917 | ||||||

| Total held to maturity investments | 10,551 | 10,395 | ||||||

| Investment in 7.625% of Cedar Cellular Investment 1 (RF) (Pty) Ltd 8.625% notes | 10,551 | 10,395 | ||||||

| Long-term portion of payments to agents in South Korea amortized over the contract period | 15,946 | 17,582 | ||||||

| Long-term portion of other finance loans receivable | 16,161 | 12,283 | ||||||

| Contingent purchase consideration | - | 9,064 | ||||||

| Policy holder assets under investment contracts (Note 9) | 598 | 610 | ||||||

| Reinsurance assets under insurance contracts (Note 9) | 619 | 633 | ||||||

| Other long-term assets | 6,705 | 5,948 | ||||||

| Total other long-term assets | $ | 245,150 | $ | 256,380 |

(1) The Company has determined that MobiKwik does not have readily determinable fair value and has therefore elected to recorded this investment at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or a similar investment of the same issuer. The Company accounted for its investment in MobiKwik at cost as of June 30, 2018.

18

7. Equity-accounted investments and other long-term assets (continued)

Other long-term assets (continued)

Summarized below are the components of the Company’s held to maturity investments as of September 30, 2018:

| Unrealized | Unrealized | ||||||||||||

| holding | holding | Carrying | |||||||||||

| Cost basis | gains | losses | value | ||||||||||

| Held to maturity: | |||||||||||||

| Investment in Cedar Cellular notes | $ | 9,000 | $ | 1,551 | $ | - | $ | 10,551 | |||||

| Total | $ | 9,000 | $ | 1,551 | $ | - | $ | 10,551 |

Summarized below are the components of the Company’s held to maturity investments as of June 30, 2018:

| Unrealized | Unrealized | ||||||||||||

| holding | holding | Carrying | |||||||||||

| Cost basis | gains | losses | value | ||||||||||

| Held to maturity: | |||||||||||||

| Investment in Cedar Cellular notes | $ | 9,000 | $ | 1,395 | $ | - | $ | 10,395 | |||||

| Total | $ | 9,000 | $ | 1,395 | $ | - | $ | 10,395 |

The unrealized holding gains related to the investment in Cedar Cellular notes were recorded in interest income in the consolidated statement of operations. Interest on this investment will only be paid, at Cedar Cellular’s election, on maturity in August 2022. The Company’s effective interest rate on the Cedar Cellular note is 19.15% as of September 30, 2018, and it has recognized unrealized holding gains of $0.2 million during the three months ended September 30, 2018, which includes unrealized losses attributable to changes in the effective interest rate.

Contractual maturities of held to maturity investments

Summarized below is the contractual maturity of the Company’s held to maturity investment as of September 30, 2018:

| Estimated | ||||||

| Cost | fair | |||||

| basis | value(1) | |||||

| Due in one year or less | $ | - | $ | - | ||

| Due in one year through five years | 9,000 | 9,625 | ||||

| Due in five years through ten years | - | - | ||||

| Due after ten years | - | - | ||||

| Total | $ | 9,000 | $ | 9,625 |

(1) The estimated fair value of the Cedar Cellular note has been calculated utilizing the Company’s portion of the security provided to the Company by Cedar Cellular, namely, Cedar Cellular’s investment in Cell C.

8. Goodwill and intangible assets, net

Goodwill

Summarized below is the movement in the carrying value of goodwill for the three months ended September 30, 2018:

| Accumulated | Carrying | ||||||||

| Gross value | impairment | value | |||||||

| Balance as of June 30, 2018 | $ | 304,013 | $ | (20,773 | ) | $ | 283,240 | ||

| Foreign currency adjustment(1) | (5,152 | ) | 1,070 | (4,082 | ) | ||||

| Balance as of September 30, 2018 | $ | 298,861 | $ | (19,703 | ) | $ | 279,158 |

(1) – the foreign currency adjustment represents the effects of the fluctuations between the South African rand, the Euro and the Korean won, and the U.S. dollar on the carrying value.

19

8. Goodwill and intangible assets, net (continued) Goodwill (continued)

Goodwill has been allocated to the Company’s reportable segments as follows:

| South | Financial | |||||||||||

| African | International | inclusion and | ||||||||||

| transaction | transaction | applied | Carrying | |||||||||

| processing | processing | technologies | value | |||||||||

| Balance as of June 30, 2018 | $ | 20,946 | $ | 123,948 | $ | 138,346 | $ | 283,240 | ||||

| Foreign currency adjustment(1) | (618 | ) | 456 | (3,920 | ) | (4,082 | ) | |||||

| Balance as of September 30, 2018 | $ | 20,328 | $ | 124,404 | $ | 134,426 | $ | 279,158 |

(1) – the foreign currency adjustment represents the effects of the fluctuations between the South African rand, the Euro and the Korean won, and the U.S. dollar on the carrying value.

Intangible assets

Carrying value and amortization of intangible assets

Summarized below is the carrying value and accumulated amortization of the intangible assets as of September 30, 2018 and June 30, 2018:

| As of September 30, 2018 | As of June 30, 2018 | |||||||||||||||||

| Gross | Net | Gross | Net | |||||||||||||||

| carrying | Accumulated | carrying | carrying | Accumulated | carrying | |||||||||||||

| value | amortization | value | value | amortization | value | |||||||||||||

| Finite-lived intangible assets: | ||||||||||||||||||

| Customer relationships | $ | 193,995 | $ | (80,786 | ) | $ | 113,209 | $ | 197,676 | $ | (76,237 | ) | $ | 121,439 | ||||

| Software and unpatented technology | 34,175 | (32,546 | ) | 1,629 | 35,730 | (32,342 | ) | 3,388 | ||||||||||

| FTS patent | 2,709 | (2,709 | ) | - | 2,792 | (2,792 | ) | - | ||||||||||

| Exclusive licenses | 4,506 | (4,506 | ) | - | 4,506 | (4,506 | ) | - | ||||||||||

| Trademarks and brands | 12,345 | (6,147 | ) | 6,198 | 11,101 | (5,589 | ) | 5,512 | ||||||||||

| Total finite-lived intangible assets | 247,730 | (126,694 | ) | 121,036 | 251,805 | (121,466 | ) | 130,339 | ||||||||||

| Indefinite-lived intangible assets: | ||||||||||||||||||

| Financial institution license | 788 | - | 788 | 793 | - | 793 | ||||||||||||

| Total indefinite-lived intangible assets | 788 | - | 788 | 793 | - | 793 | ||||||||||||

| Total intangible assets | $ | 248,518 | $ | (126,694 | ) | $ | 121,824 | $ | 252,598 | $ | (121,466 | ) | $ | 131,132 | ||||

Aggregate amortization expense on the finite-lived intangible assets for the three months ended September 30, 2018 and 2017, was approximately $6.0 million and $2.8 million, respectively.

Future estimated annual amortization expense for the next five fiscal years and thereafter, assuming exchange rates that prevailed on September 30, 2018, is presented in the table below. Actual amortization expense in future periods could differ from this estimate as a result of acquisitions, changes in useful lives, exchange rate fluctuations and other relevant factors.

| Fiscal 2019 | $ | 24,469 | |

| Fiscal 2020 | 19,285 | ||

| Fiscal 2021 | 13,811 | ||

| Fiscal 2022 | 10,604 | ||

| Fiscal 2023 | 10,604 | ||

| Thereafter | 48,473 | ||

| Total future estimated annual amortization expense | $ | 127,246 |

20

9. Reinsurance assets and policyholder liabilities under insurance and investment contracts

Reinsurance assets and policyholder liabilities under insurance contracts

Summarized below is the movement in reinsurance assets and policyholder liabilities under insurance contracts during the three months ended September 30, 2018:

| Reinsurance | Insurance | |||||

| assets(1) | contracts(2) | |||||

| Balance as of June 30, 2018 | $ | 633 | $ | (2,032 | ) | |

| Increase in policyholder benefits under insurance contracts | 169 | (2,901 | ) | |||

| Claims and policyholders’ benefits under insurance contracts . | (164 | ) | 2,690 | |||

| Foreign currency adjustment(3) | (19 | ) | 61 | |||

| Balance as of September 30, 2018 | $ | 619 | $ | (2,182 | ) |

(1) Included in other long-term

assets.

(2) Included in other long-term

liabilities.

(3) Represents the effects

of the fluctuations between the ZAR and the U.S. dollar.

The Company has agreements with reinsurance companies in order to limit its losses from certain insurance contracts, however, if the reinsurer is unable to meet its obligations, the Company retains the liability.

The Company determines its reserves for policy benefits under its life insurance products using a model which estimates claims incurred that have not been reported and total present value of disability claims-in-payment at the balance sheet date. This model allows for best estimate assumptions based on experience (where sufficient) plus prescribed margins, as required in the markets in which these products are offered, namely South Africa. The best estimate assumptions include (i) mortality and morbidity assumptions reflecting the company’s most recent experience and (ii) claim reporting delays reflecting Company specific and industry experience. Most of the disability claims-in-payment reserve is reinsured and the reported values were based on the reserve held by the relevant reinsurer.

Assets and policyholder liabilities under investment contracts

Summarized below is the movement in assets and policyholder liabilities under investment contracts during the three months ended September 30, 2018:

| Investment | ||||||

| Assets(1) | contracts(2) | |||||

| Balance as of June 30, 2018 | $ | 610 | $ | (610 | ) | |

| Increase in policyholder benefits under investment contracts | 6 | (6 | ) | |||

| Foreign currency adjustment(3) | (18 | ) | 18 | |||

| Balance as of September 30, 2018 | $ | 598 | $ | (598 | ) |

(1) Included in other long-term

assets.

(2) Included in other long-term

liabilities.

(3) Represents the effects

of the fluctuations between the ZAR and the U.S. dollar.

The Company does not offer any investment products with guarantees related to capital or returns.

21

10. Borrowings

South Africa

The amounts below have been translated at exchange rates applicable as of the dates specified.

July 2017 Facilities, as amended, comprising a short-term facility and long-term borrowings

Long-term borrowings – Facilities A, B, C and D

The Company’s South African amended July 2017 Facilities agreement is described in Note 14 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2018. The carrying value of these long-term borrowings as of September 30, 2018, was ZAR 529.9 million ($37.5 million), net of deferred fees of ZAR 2.6 million ($0.2 million), and the carrying amount approximated its fair value. Interest on these term loans is payable on the last business day of March, June, September and December of each year and on the final maturity date based on the Johannesburg Interbank Agreed Rate (“JIBAR”) in effect from time to time plus a margin of 2.75% . The JIBAR has been set at 7.00% for the period to December 28, 2018, in respect of the loans provided under the South African long-term facilities agreement. The next scheduled principal repayment of ZAR 151.3 million ($10.7 million, translated at exchange rates applicable as of September 30, 2018) is due on December 28, 2018.

Short-term facility - Facility E

On September 26, 2018, Net1 Applied Technologies South Africa Proprietary Limited (“Net1 SA”) further amended its amended July 2017 Facilities agreement with Rand Merchant Bank, a division of FirstRand Bank Limited (“RMB”) to include an overdraft facility (“Facility E”) of up to ZAR 1.5 billion ($106.1 million) to fund the Company’s ATMs. Interest on the overdraft facility is payable on the last day of each month and on the final maturity date based on South African prime rate less a margin of 1.00% . The overdraft facility matures on September 26, 2019. The overdraft facility amount utilized must be repaid in full within one month of utilization and at least 90% of the amount utilized must be repaid with 25 days. The overdraft facility is secured by a pledge by Net1 SA of, among other things, cash and certain bank accounts utilized in the Company’s ATM funding process, the cession of an insurance policy with Senate Transit Underwriters Managers Proprietary Limited, and any rights and claims Net1 SA has against Grindrod Bank Limited. The Company paid a non-refundable origination fee of approximately ZAR 3.6 million ($0.2 million) in October 2018. As at September 30, 2018, the Company had utilized approximately ZAR 1.1 billion ($76.6 million translated at exchange rates applicable as of September 30, 2018) of this overdraft facility. This ZAR 1.5 billion overdraft facility may only be used to fund ATMs and therefore the overdraft utilized and converted to cash to fund the Company’s ATMs is considered restricted cash. The prime rate on September 30, 2018, was 10.0% .

Nedbank facility, comprising short-term facilities

As of September 30, 2018, the aggregate amount of the Company’s short-term South African credit facility with Nedbank Limited was ZAR 700.0 million ($49.5 million) and consists of (i) a primary amount of up to ZAR 450 million ($31.8 million), (ii) a temporary amount of ZAR 250.0 million ($17.7 million), and (iii) a secondary amount, which has been temporarily withdrawn as discussed below. The primary amount comprises an overdraft facility of (i) up to ZAR 300 million ($21.2 million), which is further split into (a) a ZAR 250.0 million ($17.7 million) overdraft facility which may only be used to fund ATMs used at pay points and (b) a ZAR 50 million ($3.5 million) general banking facility and (ii) indirect and derivative facilities of up to ZAR 150 million ($10.6 million), which include letters of guarantees, letters of credit and forward exchange contracts. The temporary amount has been made available until January 31, 2019, at which time any amount utilized must be repaid in full and the secondary amount of ZAR 200.0 million ($14.1 million) will be made available again. The ZAR 250.0 million component of the primary amount may only be used to fund ATMs and therefore this component of the primary amount utilized and converted to cash to fund our ATMs is considered restricted cash.

As of September 30, 2018, the interest rate on the overdraft facility was 8.85% . The Company has ceded its investment in Cash Paymaster Services Proprietary Limited (“CPS”), a South African subsidiary, as well as all of its rights, title and interest in an insurance policy issued by Fidelity Risk Proprietary Limited as security for its repayment obligations under the facility. A commitment fee of 0.35% per annum is payable on the monthly unutilized amount of the overdraft portion of the short-term facility. The Company is required to comply with customary non-financial covenants, including, without limitation, covenants that restrict its ability to dispose of or encumber its assets, incur additional indebtedness or engage in certain business combinations.

As of September 30, 2018, the Company has utilized approximately ZAR 115.6 million ($8.2 million) of its ZAR 250 million overdraft facility to fund ATMs. As of September 30, 2018 and June 30, 2018, the Company had utilized approximately ZAR 132.2 million ($9.3 million) and ZAR 108.0 million ($7.9 million), respectively, of its indirect and derivative facilities of ZAR 150 million to enable the bank to issue guarantee, letters of credit and forward exchange contracts, in order for the Company to honor its obligations to third parties requiring such guarantees (refer to Note 19).

22

10. Borrowings (continued)

South Africa (continued)

June 2018 Facility, a long-term borrowing

The Company’s South African long-term facility agreement is described in Note 14 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2018. The current carrying value as of September 30, 2018, was ZAR 115.0 million ($8.1 million). Interest on the revolving credit facility is payable quarterly based on JIBAR in effect from time to time plus a margin of 2.75% . The Company paid a non-refundable origination fee of approximately ZAR 2.0 million ($0.1 million) during the three months ended September 30, 2018.

United States, a short-term facility

On September 14, 2018, the Company renewed its $10.0 million overdraft facility from Bank Frick. The interest rate on the facilities is 4.50% plus 3-month US dollar LIBOR and interest is payable quarterly commencing on September 30, 2018. The 3-month US dollar LIBOR rate was 2.39838% on September 28, 2018. The facility has no fixed term, however, it may be terminated by either party with six weeks written notice. The facility is secured by a pledge of the Company’s investment in Bank Frick. As of September 30, 2018, the Company had utilized approximately $3.3 million of this facility.

South Korea, comprising long-term borrowings

The Company’s South Korean senior secured loan facility is described in Note 14 to its audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2018. On July 29, 2017, the Company utilized approximately KRW 0.3 billion ($0.3 million) of its Facility C revolving credit facility to pay interest due on the Company’s South Korean senior secured loan facility. On October 20, 2017, the Company made an unscheduled repayment of $16.6 million and settled the full outstanding balance, including interest, related to these borrowings.

Movement in short-term credit facilities

Summarized below are the Company’s short-term facilities as of September 30, 2018, and the movement in the Company’s short-term facilities from as of June 30, 2018 to as of September 30, 2018:

| South Africa | United States | ||||||||||||||

| Amended | |||||||||||||||

| July 2017 | Nedbank | Bank Frick | Total | ||||||||||||

| Short-term facilities as of September 30, 2018: | $ | 106,054 | $ | 49,492 | $ | 10,000 | $ | 165,546 | |||||||

| Overdraft | - | 21,211 | 10,000 | 31,211 | |||||||||||

| Overdraft restricted as to use for ATM funding only | 106,054 | 17,676 | - | 123,730 | |||||||||||

| Indirect and derivative facilities | - | 10,605 | - | 10,605 | |||||||||||

| Movement in utilized overdraft facilities: | |||||||||||||||

| Balance as of June 30, 2018 | - | - | - | - | |||||||||||

| Utilized | 73,500 | 7,842 | 3,313 | 84,655 | |||||||||||

| Foreign currency adjustment(1) | 3,105 | 331 | - | 3,436 | |||||||||||

| Balance as of September 30, 2018 | 76,605 | 8,173 | 3,313 | 88,091 | |||||||||||

| Restricted as to use for ATM funding only | 76,605 | 8,173 | - | 84,778 | |||||||||||

| No restrictions as to use | - | - | 3,313 | 3,313 | |||||||||||

| Movement in utilized indirect and derivative facilities: | |||||||||||||||

| Balance as of June 30, 2018 | - | 7,871 | - | 7,871 | |||||||||||

| Guarantees cancelled | - | (848 | ) | - | (848 | ) | |||||||||

| Utilized | - | 2,436 | - | 2,436 | |||||||||||

| Foreign currency adjustment(1) | - | (110 | ) | - | (110 | ) | |||||||||

| Balance as of September 30, 2018 | $ | - | $ | 9,349 | $ | - | $ | 9,349 | |||||||