Attached files

| file | filename |

|---|---|

| EX-99.2 - EXHIBIT 99.2 - FEDERAL NATIONAL MORTGAGE ASSOCIATION FANNIE MAE | q32018financialsupplemen.htm |

| 8-K - 8-K - FEDERAL NATIONAL MORTGAGE ASSOCIATION FANNIE MAE | a2018q38k.htm |

Resource Center: 1-800-732-6643

Exhibit 99.1

Contact: Pete Bakel

202-752-2034

Date: November 2, 2018

Fannie Mae Reports Net Income of $4.0 Billion and

Comprehensive Income of $4.0 Billion for Third Quarter 2018

Third Quarter 2018 Results | “Fannie Mae’s strong third quarter results reflect the company’s positive momentum, the strength of our business, and our strategic direction. “We are focused on serving our customers, helping them navigate market headwinds, and enabling a mortgage process that is better, faster, cheaper, and safer. “That means we have a responsibility to innovate, while maintaining our strong commitment to safety, soundness, and stewardship on behalf of taxpayers.” Hugh Frater, Interim Chief Executive Officer | |

• Fannie Mae reported net income of $4.0 billion and comprehensive income of $4.0 billion for the third quarter of 2018 reflecting the strength of the company’s business fundamentals. Fannie Mae’s pre-tax income was $5.1 billion for the third quarter of 2018. | ||

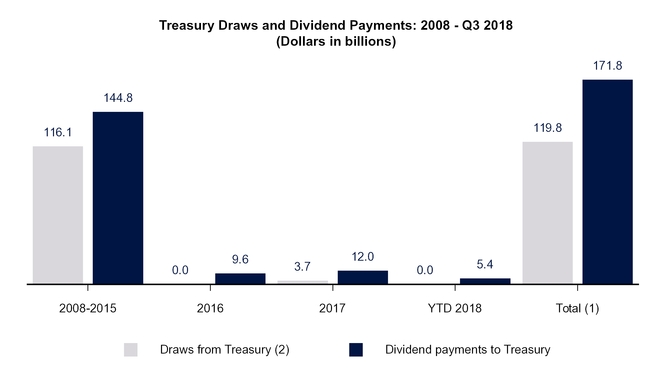

• Fannie Mae expects to pay a $4.0 billion dividend to Treasury by December 31, 2018. Through the third quarter of 2018, the company has paid $171.8 billion in dividends to Treasury. | ||

Business Highlights | ||

• Fannie Mae provided $122 billion in liquidity to the single-family mortgage market in the third quarter of 2018 while serving as the largest issuer of single-family mortgage-related securities in the secondary market. The company’s estimated market share of new single-family mortgage-related securities issuances was 40% for the third quarter of 2018. | ||

• Fannie Mae has transferred a portion of the mortgage credit risk on single-family mortgages with an unpaid principal balance of approximately $1.5 trillion at the time of the transactions since 2013, and approximately 38% of the loans in the company’s single-family conventional guaranty book of business were covered by a credit risk transfer transaction as of September 30, 2018. | ||

• Fannie Mae expects to complete a new CAS REMIC transaction in November 2018. Under the CAS REMIC program, the company will be able to align the timing of its recognition of provisions for credit losses with the related recovery from CAS transactions, limit investors’ exposure to Fannie Mae counterparty risk, and broaden the investor base by expanding participation for real estate investment trusts (REITs) and international investors. | ||

• Fannie Mae provided $18.2 billion in multifamily financing in the third quarter of 2018, which enabled the financing of 206,000 units of multifamily housing. More than 90% of the multifamily units the company financed were affordable to families earning at or below 120% of the area median income, providing support for both affordable and workforce housing. | ||

• Fannie Mae continued to share credit risk with lenders on nearly 100% of the company’s new multifamily business volume through its Delegated Underwriting and Servicing (DUS®) program. To complement the company’s lender loss sharing program, in August 2018 the company completed its third multifamily Credit Insurance Risk Transfer™ (CIRT™) transaction, which covered multifamily loans with an unpaid principal balance of approximately $11.1 billion. | ||

Third Quarter 2018 Results | 1 | |

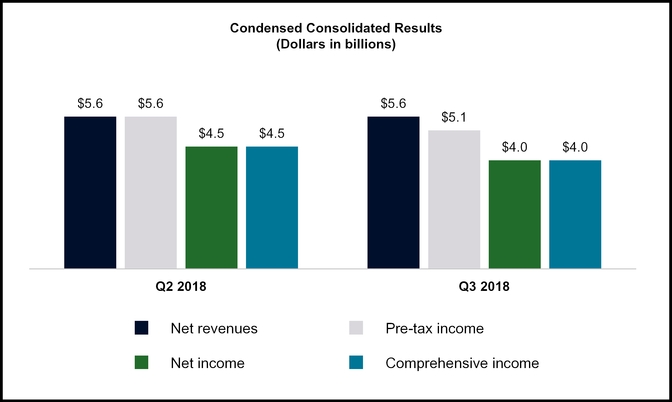

WASHINGTON, DC — Fannie Mae (FNMA/OTC) reported net income of $4.0 billion, pre-tax income of $5.1 billion, and comprehensive income of $4.0 billion for the third quarter of 2018. The company reported a net worth of $7.0 billion as of September 30, 2018. As a result, Fannie Mae expects to pay a $4.0 billion dividend to Treasury by December 31, 2018.

SUMMARY OF FANNIE MAE’S FINANCIAL PERFORMANCE

Fannie Mae’s net income of $4.0 billion for the third quarter of 2018 compares to net income of $4.5 billion for the second quarter of 2018. The primary driver of the decrease in net income was a decrease in credit-related income due primarily to a reduction in the benefit from the redesignation of loans from held-for-investment to held-for-sale and a smaller improvement in home prices compared with the second quarter of 2018. The decrease was partially offset by higher fair value gains in the third quarter of 2018 compared with the second quarter of 2018.

Third Quarter 2018 Results | 2 | |

Summary of Financial Results |

(Dollars in millions) | 3Q18 | 2Q18 | Variance | 3Q18 | 3Q17 | Variance | ||||||||||||||||||

Net interest income | $ | 5,369 | $ | 5,377 | $ | (8 | ) | $ | 5,369 | $ | 5,274 | $ | 95 | |||||||||||

Fee and other income | 271 | 239 | 32 | 271 | 1,194 | (923 | ) | |||||||||||||||||

Net revenues | 5,640 | 5,616 | 24 | 5,640 | 6,468 | (828 | ) | |||||||||||||||||

Investment gains, net | 166 | 277 | (111 | ) | 166 | 313 | (147 | ) | ||||||||||||||||

Fair value gains (losses), net | 386 | 229 | 157 | 386 | (289 | ) | 675 | |||||||||||||||||

Administrative expenses | (740 | ) | (755 | ) | 15 | (740 | ) | (664 | ) | (76 | ) | |||||||||||||

Credit-related income (expense) | ||||||||||||||||||||||||

Benefit (provision) for credit losses | 716 | 1,296 | (580 | ) | 716 | (182 | ) | 898 | ||||||||||||||||

Foreclosed property expense | (159 | ) | (139 | ) | (20 | ) | (159 | ) | (140 | ) | (19 | ) | ||||||||||||

Total credit-related income (expense) | 557 | 1,157 | (600 | ) | 557 | (322 | ) | 879 | ||||||||||||||||

Temporary Payroll Tax Cut Continuation Act of 2011 (TCCA) fees | (576 | ) | (565 | ) | (11 | ) | (576 | ) | (531 | ) | (45 | ) | ||||||||||||

Other expenses, net | (377 | ) | (366 | ) | (11 | ) | (377 | ) | (427 | ) | 50 | |||||||||||||

Income before federal income taxes | 5,056 | 5,593 | (537 | ) | 5,056 | 4,548 | 508 | |||||||||||||||||

Provision for federal income taxes | (1,045 | ) | (1,136 | ) | 91 | (1,045 | ) | (1,525 | ) | 480 | ||||||||||||||

Net income | $ | 4,011 | $ | 4,457 | $ | (446 | ) | $ | 4,011 | $ | 3,023 | $ | 988 | |||||||||||

Other comprehensive income (loss) | (36 | ) | 2 | (38 | ) | (36 | ) | 25 | (61 | ) | ||||||||||||||

Total comprehensive income | $ | 3,975 | $ | 4,459 | $ | (484 | ) | $ | 3,975 | $ | 3,048 | $ | 927 | |||||||||||

Net revenues, which consist of net interest income and fee and other income, were $5.6 billion for both the third and second quarters of 2018.

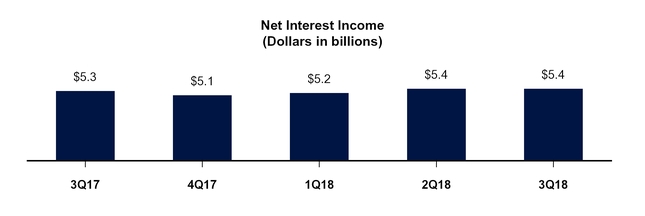

Net interest income was $5.4 billion for both the third and the second quarters of 2018. The company’s net interest income in the third quarter of 2018 was derived primarily from guaranty fees on its $3.3 trillion guaranty book of business.

More than 75 percent of Fannie Mae’s net interest income in the third quarter of 2018 was derived from the loans underlying Fannie Mae MBS in consolidated trusts, which primarily generate income through guaranty fees.

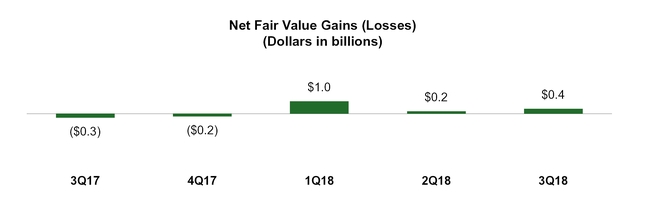

Net fair value gains were $386 million in the third quarter of 2018, compared with $229 million in the second quarter of 2018. Net fair value gains in the third quarter of 2018 were driven primarily by increases in the fair value of the company’s mortgage commitment and risk management derivatives due to rising interest rates and longer-term swap rates.

Third Quarter 2018 Results | 3 | |

The estimated fair value of the company’s derivatives, trading securities, and other financial instruments carried at fair value may fluctuate substantially from period to period because of changes in interest rates, the yield curve, mortgage and credit spreads, implied volatility, and activity related to these financial instruments.

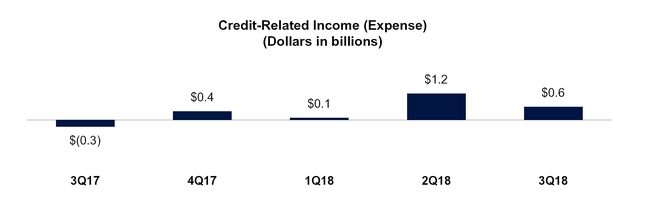

Credit-related income (expense) consists of a benefit (provision) for credit losses and foreclosed property expense. Credit-related income was $557 million in the third quarter of 2018, compared with $1.2 billion in the second quarter of 2018. The decrease in credit-related income in the third quarter of 2018 was due to a reduction in the benefit from the redesignation of loans from held-for-investment to held-for-sale and a smaller improvement in home prices compared with the second quarter of 2018.

Third Quarter 2018 Results | 4 | |

PROVIDING LIQUIDITY AND SUPPORT TO THE MARKET

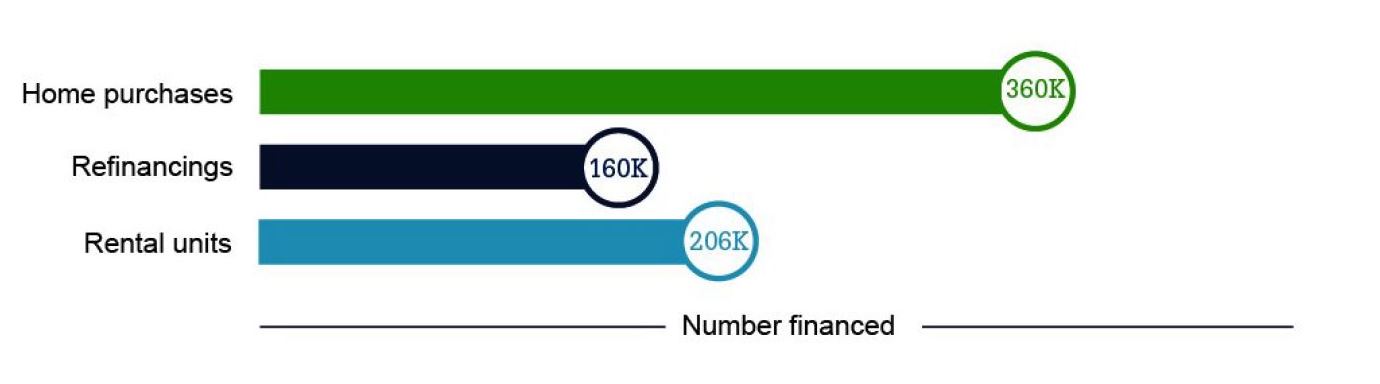

Through Fannie Mae’s single-family and multifamily business segments, the company provided $140 billion in liquidity to the mortgage market in the third quarter of 2018, which enabled the financing of 726,000 home purchases, refinancings, and rental units.

Fannie Mae Provided $140 Billion in Liquidity in the Third Quarter of 2018

SUMMARY OF THIRD QUARTER 2018 BUSINESS SEGMENT RESULTS

Fannie Mae’s two reportable business segments—Single-Family and Multifamily—engage in complementary business activities in pursuit of Fannie Mae’s vision to be America’s most valued housing partner and to provide liquidity, access to credit, and affordability in all U.S. housing markets at all times. Fannie Mae does this while effectively managing and reducing risk to its business, taxpayers, and the housing finance system. Fannie Mae is advancing this vision by pursuing four strategic objectives: advancing a sustainable and reliable business model that reduces risk to the housing finance system and taxpayers; providing great service to its customers and partners, enabling them to serve the needs of American households more effectively; supporting and sustainably increasing access to credit and affordable housing; and building a simple, efficient, innovative, and continuously improving company.

Third Quarter 2018 Results | 5 | |

Business Segments |

Single-Family Business

Single-Family Segment Financial Results | 3Q18 | 2Q18 | Variance | 3Q18 | 3Q17 | Variance | ||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||||

Net interest income | $ | 4,670 | $ | 4,723 | $ | (53 | ) | $ | 4,670 | $ | 4,627 | $ | 43 | |||||||||||

Fee and other income | 79 | 69 | 10 | 79 | 1,005 | (926 | ) | |||||||||||||||||

Net revenues | 4,749 | 4,792 | (43 | ) | 4,749 | 5,632 | (883 | ) | ||||||||||||||||

Investment gains, net | 146 | 252 | (106 | ) | 146 | 286 | (140 | ) | ||||||||||||||||

Fair value gains (losses), net | 417 | 278 | 139 | 417 | (300 | ) | 717 | |||||||||||||||||

Administrative expenses | (636 | ) | (649 | ) | 13 | (636 | ) | (580 | ) | (56 | ) | |||||||||||||

Credit-related income (expense) | 582 | 1,159 | (577 | ) | 582 | (294 | ) | 876 | ||||||||||||||||

TCCA fees | (576 | ) | (565 | ) | (11 | ) | (576 | ) | (531 | ) | (45 | ) | ||||||||||||

Other expenses, net | (282 | ) | (270 | ) | (12 | ) | (282 | ) | (320 | ) | 38 | |||||||||||||

Income before federal income taxes | 4,400 | 4,997 | (597 | ) | 4,400 | 3,893 | 507 | |||||||||||||||||

Provision for federal income taxes | (938 | ) | (1,044 | ) | 106 | (938 | ) | (1,361 | ) | 423 | ||||||||||||||

Net income | $ | 3,462 | $ | 3,953 | $ | (491 | ) | $ | 3,462 | $ | 2,532 | $ | 930 | |||||||||||

Financial Results

• | Single-Family net income was $3.5 billion in the third quarter of 2018, compared with $4.0 billion in the second quarter of 2018. The decrease in net income in the third quarter of 2018 was driven primarily by a decrease in credit-related income due to a reduction in the benefit from the redesignation of loans from held-for-investment to held-for-sale and a smaller improvement in home prices compared with the second quarter of 2018. |

• | The decrease was partially offset by higher fair value gains due to an increase in rates in the third quarter of 2018 compared with the second quarter of 2018. |

Business Highlights

• | The single-family guaranty book of business continued to grow in the third quarter of 2018, while the average charged guaranty fee (net of TCCA fees) on the single-family guaranty book in the third quarter was relatively consistent with the prior quarter at 43 basis points. |

• | Fannie Mae’s Single-Family business provided $122 billion in liquidity to the mortgage market in the third quarter of 2018, which enabled 360,000 home purchases and 160,000 refinancings. |

• | The single-family serious delinquency rate was 0.82% as of September 30, 2018, compared with 1.24% as of December 31, 2017 and 1.01% as of September 30, 2017. |

◦ | The single-family serious delinquency rate increased in the latter part of 2017 due to the impact of Hurricanes Harvey, Irma, and Maria in 2017, but has since resumed its prior downward trend because many delinquent borrowers in the affected areas have resolved their loan delinquencies by obtaining loan modifications or through resuming payments and becoming current on their loans. The company’s single-family serious delinquency rate may be negatively impacted in the near term as a result of the hurricanes that occurred late in the third quarter of 2018 and early in the fourth quarter of 2018, which may cause some borrowers in the affected regions to miss their payments, including through forbearance arrangements that may be extended. The company is still evaluating the impact, but it does not believe that the hurricanes to date in 2018, individually or in aggregate, will have a material impact on the company’s credit losses or loss reserves. In the longer term, the company expects its single-family serious delinquency rate to continue to decline, but at a more modest pace than in the past several years, and to experience period-to-period fluctuations. |

Third Quarter 2018 Results | 6 | |

Multifamily Business

Multifamily Segment Financial Results | 3Q18 | 2Q18 | Variance | 3Q18 | 3Q17 | Variance | ||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||||

Net interest income | $ | 699 | $ | 654 | $ | 45 | $ | 699 | $ | 647 | $ | 52 | ||||||||||||

Fee and other income | 192 | 170 | 22 | 192 | 189 | 3 | ||||||||||||||||||

Net revenues | 891 | 824 | 67 | 891 | 836 | 55 | ||||||||||||||||||

Fair value gains (losses), net | (31 | ) | (49 | ) | 18 | (31 | ) | 11 | (42 | ) | ||||||||||||||

Administrative expenses | (104 | ) | (106 | ) | 2 | (104 | ) | (84 | ) | (20 | ) | |||||||||||||

Credit-related expense | (25 | ) | (2 | ) | (23 | ) | (25 | ) | (28 | ) | 3 | |||||||||||||

Other expenses, net | (75 | ) | (71 | ) | (4 | ) | (75 | ) | (80 | ) | 5 | |||||||||||||

Income before federal income taxes | 656 | 596 | 60 | 656 | 655 | 1 | ||||||||||||||||||

Provision for federal income taxes | (107 | ) | (92 | ) | (15 | ) | (107 | ) | (164 | ) | 57 | |||||||||||||

Net income | $ | 549 | $ | 504 | $ | 45 | $ | 549 | $ | 491 | $ | 58 | ||||||||||||

Financial Results

• | Multifamily net income was $549 million in the third quarter of 2018, compared with $504 million in the second quarter of 2018. The increase in net income in the third quarter of 2018 was driven primarily by an increase in guaranty fee revenue as the multifamily guaranty book grew during the quarter. |

• | Credit-related expense in the third quarter of 2018 was due to an increase in the allowance for loan losses driven primarily by a slight increase in downgrades in loan risk ratings. Credit-related expense continued to remain low in the third quarter due to the stability of the multifamily market. |

Business Highlights

• | The multifamily guaranty book of business continued to grow in the third quarter of 2018, while the average charged guaranty fee on the multifamily guaranty book decreased slightly from June 30, 2018 to 77 basis points as of September 30, 2018. |

• | New multifamily business volume was $18.2 billion in the third quarter of 2018, an increase from $14.5 billion in the second quarter of 2018. Multifamily new business volume totaled $44.0 billion for the first nine months of 2018, of which approximately 42% counted toward the Federal Housing Finance Agency’s (FHFA) 2018 multifamily volume cap. |

• | Fannie Mae enabled the financing of 206,000 units of multifamily housing in the third quarter of 2018. More than 90% of the multifamily units the company financed were affordable to families earning at or below 120% of the area median income, providing support for both affordable and workforce housing. |

• | The multifamily serious delinquency rate decreased to 0.07% as of September 30, 2018 from 0.11% as of December 31, 2017. The decrease in the multifamily serious delinquency rate since December 31, 2017 resulted mostly from a decrease in delinquent loans subject to forbearance agreements granted to borrowers in the areas affected by the hurricanes in the latter part of 2017. |

Third Quarter 2018 Results | 7 | |

CREDIT RISK TRANSFER TRANSACTIONS

In late 2013, Fannie Mae began entering into credit risk transfer transactions with the goal of transferring, to the extent economically sensible, a portion of the mortgage credit risk on some of the recently acquired loans in its single-family book of business in order to reduce the economic risk to the company and taxpayers of future borrower defaults. Fannie Mae’s primary method of achieving this goal has been through the issuance of its Connecticut Avenue Securities® (CAS) and its Credit Insurance Risk Transfer™ (CIRT™) transactions. In these transactions, the company transfers to investors a portion of the credit risk associated with losses on a reference pool of mortgage loans and in exchange pays investors a premium that effectively reduces the guaranty fee income the company retains on the loans.

As a part of Fannie Mae’s continued effort to innovate and improve its credit risk transfer programs, the company is in the process of executing an enhancement to its credit risk transfer securities that will enable the company to structure future CAS offerings as notes issued by a trust that qualifies as a Real Estate Mortgage Investment Conduit (REMIC). The new REMIC structure will differ from the prior CAS notes that were issued as Fannie Mae corporate debt. Under the prior CAS structure, there can be a significant lag between the time when Fannie Mae recognizes a provision for credit losses and when the company recognizes the related recovery from the CAS transaction. Under current accounting rules, while a credit expense on a loan in a reference pool for a CAS transaction is recorded when it is probable that Fannie Mae has incurred a loss, for the company’s CAS issued beginning in 2016, a recovery is recorded only when an actual loss event occurs, which is typically several months after the collateral has been liquidated. The new CAS structure will eliminate this timing mismatch, allowing Fannie Mae to recognize the credit loss protection benefit at the same time the credit loss is recognized in the company’s condensed consolidated financial statements.

The enhancements to the company’s CAS program are designed to promote the continued growth of the market by expanding the potential investor base for these securities and limiting investor exposure to Fannie Mae counterparty risk, without disrupting the To-Be-Announced (TBA) MBS market. Fannie Mae expects to issue CAS under the new REMIC structure in November 2018.

Fannie Mae continued to transfer a portion of the credit risk on multifamily mortgages, and nearly 100% of the company’s new multifamily business volume had lender risk-sharing primarily through the company’s Delegated Underwriting and Servicing (DUS®) model in the third quarter of 2018. To complement the company’s lender loss sharing program through DUS, Fannie Mae also transferred a portion of the mortgage credit risk on multifamily loans in its multifamily guaranty book of business to insurers or reinsurers through multifamily Credit Insurance Risk Transfer™ (CIRT™) transactions. In August 2018, the company completed its third multifamily CIRT transaction since the inception of the program, which covered multifamily loans with an unpaid principal balance of approximately $11.1 billion.

FINANCIAL PERFORMANCE OUTLOOK

Fannie Mae expects to remain profitable on an annual basis for the foreseeable future; however, certain factors could result in significant volatility in the company’s financial results from quarter to quarter or year to year. Fannie Mae expects volatility from quarter to quarter in its financial results due to a number of factors, particularly changes in market conditions that result in fluctuations in the estimated fair value of the financial instruments that it marks to market through its earnings. Other factors that may result in volatility in the company’s quarterly financial results include developments that affect its loss reserves, such as changes in interest rates, home prices or accounting standards, or events such as natural disasters.

The potential for significant volatility in the company’s financial results could result in a net loss in a future quarter. The company is permitted to retain up to $3.0 billion in capital reserves as a buffer in the event of a net loss in a future quarter. However, any net loss the company experiences in the future could be greater than the amount of its capital reserves, resulting in a net worth deficit for that quarter. See “Risk Factors” in the company’s Form 10-K for the year ended December 31, 2017 (2017 Form 10-K) for a discussion of the risks associated with the limitations on the company’s ability to rebuild its capital reserves, including factors that could result in a net loss or net worth deficit in a future quarter.

Third Quarter 2018 Results | 8 | |

ABOUT FANNIE MAE’S CONSERVATORSHIP AND AGREEMENTS WITH TREASURY

Fannie Mae has operated under the conservatorship of FHFA since September 6, 2008. Treasury has made a commitment under a senior preferred stock purchase agreement to provide funding to Fannie Mae under certain circumstances if the company has a net worth deficit. Pursuant to this agreement and the senior preferred stock the company issued to Treasury in 2008, the conservator has declared and directed Fannie Mae to pay dividends to Treasury on a quarterly basis for every dividend period for which dividends were payable since the company entered into conservatorship in 2008.

The chart below shows the funds Fannie Mae has drawn from Treasury pursuant to the senior preferred stock purchase agreement, as well as the dividend payments the company has made to Treasury on the senior preferred stock, since entering into conservatorship.

__________

(1) | Under the terms of the senior preferred stock purchase agreement, dividend payments the company makes to Treasury do not offset prior draws of funds from Treasury, and the company is not permitted to pay down draws it has made under the agreement except in limited circumstances. Amounts may not sum due to rounding. |

(2) | Treasury draws are shown in the period for which requested, not when the funds were received by the company. Draw requests have been funded in the quarter following a net worth deficit. |

Fannie Mae expects to pay Treasury a fourth quarter 2018 dividend of $4.0 billion by December 31, 2018. The current dividend provisions of the senior preferred stock provide for quarterly dividends consisting of the amount, if any, by which the company’s net worth as of the end of the immediately preceding fiscal quarter exceeds a $3.0 billion capital reserve amount. The company refers to this as a “net worth sweep” dividend. The company’s net worth was $7.0 billion as of September 30, 2018.

If Fannie Mae experiences a net worth deficit in a future quarter, the company will be required to draw additional funds from Treasury under the senior preferred stock purchase agreement to avoid being placed into receivership. As of the date of this release, the maximum amount of remaining funding under the agreement is $113.9 billion. If the company were to draw additional funds from Treasury under the agreement with respect to a future period, the amount of remaining funding under the agreement would be reduced by the amount of its draw. Dividend payments Fannie Mae makes to Treasury do not restore or increase the amount of funding available to the company under the

Third Quarter 2018 Results | 9 | |

agreement. For a description of the terms of the senior preferred stock purchase agreement and the senior preferred stock, see “Business—Conservatorship and Treasury Agreements—Treasury Agreements” in the company’s 2017 Form 10-K.

Fannie Mae’s financial statements for the third quarter of 2018 are available in the accompanying Annex; however, investors and interested parties should read the company’s quarterly report on Form 10-Q for the quarter ended September 30, 2018 (Third Quarter 2018 Form 10-Q), which was filed today with the Securities and Exchange Commission and is available on Fannie Mae’s website, www.fanniemae.com. The company provides further discussion of its financial results and condition, credit performance, and other matters in its Third Quarter 2018 Form 10-Q. Additional information about the company’s financial and credit performance is contained in the “Fannie Mae Quarterly Financial Supplement” for the third quarter of 2018 at www.fanniemae.com.

# # #

In this release, the company has presented a number of estimates, forecasts, expectations, and other forward-looking statements, including statements regarding: future dividend payments on the senior preferred stock; the company’s profitability, financial condition and results of operations, and the factors that will affect the company’s profitability, financial condition and results of operations; the company’s future credit risk transfer activity and the impact of such activity; and the company’s future serious delinquency rates and the factors that will affect the company’s single-family serious delinquency rates. These estimates, forecasts, expectations, and statements are forward-looking statements based on the company’s current assumptions regarding numerous factors. Actual results, and future projections, could be materially different from what is set forth in the forward-looking statements as a result of: home price changes; interest rate changes; unemployment rates; other macroeconomic and housing market variables; the company’s future serious delinquency rates; the company’s future guaranty fee pricing and the impact of that pricing on the company’s guaranty fee revenues and competitive environment; government policy; credit availability; changes in borrower behavior; the volume of loans it modifies; the effectiveness of its loss mitigation strategies; significant changes in modification and foreclosure activity; the volume and pace of future nonperforming and reperforming loan sales and their impact on the company’s results and serious delinquency rates; the effectiveness of its management of its real estate owned inventory and pursuit of contractual remedies; changes in the fair value of its assets and liabilities; future legislative or regulatory requirements or changes that have a significant impact on the company’s business, such as the enactment of housing finance reform legislation; actions by FHFA, Treasury, the Department of Housing and Urban Development or other regulators that affect the company’s business; the size, composition and quality of the company’s guaranty book of business and retained mortgage portfolio; the company’s market share; the life of the loans in the company’s guaranty book of business; future updates to the company’s models relating to loss reserves, including the assumptions used by these models; changes in generally accepted accounting principles; changes to the company’s accounting policies; whether the company’s counterparties meet their obligations in full; effects from activities the company takes to support the mortgage market and help borrowers; the company’s future objectives and activities in support of those objectives, including actions the company may take to reach additional underserved creditworthy borrowers; actions the company may be required to take by FHFA, in its role as the company’s conservator or as its regulator, such as changes in the type of business the company does or the implementation of the Single Security Initiative; limitations on the company’s business imposed by FHFA, in its role as the company’s conservator or as its regulator; the conservatorship and its effect on the company’s business; the investment by Treasury and its effect on the company’s business; the uncertainty of the company’s future; challenges the company faces in retaining and hiring qualified executives and other employees; the deteriorated credit performance of many loans in the company’s guaranty book of business; a decrease in the company’s credit ratings; defaults by one or more institutional counterparties; resolution or settlement agreements the company may enter into with its counterparties; operational control weaknesses; changes in the fiscal and monetary policies of the Federal Reserve, including implementation of the Federal Reserve’s balance sheet normalization program; changes in the structure and regulation of the financial services industry; the company’s ability to access the debt markets; disruptions in the housing, credit, and stock markets; government investigations and litigation; the company’s reliance on and the performance of the company’s servicers; conditions in the foreclosure environment; global political risks; natural disasters, environmental disasters, terrorist attacks, pandemics, or other major disruptive events; cyber attacks or other information security breaches or threats; and many other factors, including those discussed in the “Risk Factors” and “Forward-Looking Statements” sections of and elsewhere in the company’s 2017 Form 10-K, Third Quarter 2018 Form 10-Q, and elsewhere in this release.

Fannie Mae provides website addresses in its news releases solely for readers’ information. Other content or information appearing on these websites is not part of this release.

Fannie Mae helps make the 30-year fixed-rate mortgage and affordable rental housing possible for millions of Americans. We partner with lenders to create housing opportunities for families across the country. We are driving positive changes in housing finance to make the home buying process easier, while reducing costs and risk. To learn more, visit fanniemae.com and follow us on twitter.com/fanniemae.

Third Quarter 2018 Results | 10 | |

ANNEX

FANNIE MAE

(In conservatorship)

Condensed Consolidated Balance Sheets — (Unaudited)

(Dollars in millions, except share amounts)

As of | |||||||||||

September 30, | December 31, | ||||||||||

2018 | 2017 | ||||||||||

ASSETS | |||||||||||

Cash and cash equivalents | $ | 27,789 | $ | 32,110 | |||||||

Restricted cash (includes $17,835 and $22,132, respectively, related to consolidated trusts) | 23,242 | 28,150 | |||||||||

Federal funds sold and securities purchased under agreements to resell or similar arrangements | 26,598 | 19,470 | |||||||||

Investments in securities: | |||||||||||

Trading, at fair value (includes $3,734 and $747, respectively, pledged as collateral) | 43,901 | 34,679 | |||||||||

Available-for-sale, at fair value | 3,537 | 4,843 | |||||||||

Total investments in securities | 47,438 | 39,522 | |||||||||

Mortgage loans: | |||||||||||

Loans held for sale, at lower of cost or fair value | 10,572 | 4,988 | |||||||||

Loans held for investment, at amortized cost: | |||||||||||

Of Fannie Mae | 126,674 | 162,809 | |||||||||

Of consolidated trusts | 3,111,551 | 3,029,812 | |||||||||

Total loans held for investment (includes $9,153 and $10,596, respectively, at fair value) | 3,238,225 | 3,192,621 | |||||||||

Allowance for loan losses | (15,663 | ) | (19,084 | ) | |||||||

Total loans held for investment, net of allowance | 3,222,562 | 3,173,537 | |||||||||

Total mortgage loans | 3,233,134 | 3,178,525 | |||||||||

Deferred tax assets, net | 14,368 | 17,350 | |||||||||

Accrued interest receivable, net (includes $8,234 and $7,560, respectively, related to consolidated trusts) | 8,792 | 8,133 | |||||||||

Acquired property, net | 2,722 | 3,220 | |||||||||

Other assets | 17,022 | 19,049 | |||||||||

Total assets | $ | 3,401,105 | $ | 3,345,529 | |||||||

LIABILITIES AND EQUITY (DEFICIT) | |||||||||||

Liabilities: | |||||||||||

Accrued interest payable (includes $8,942 and $8,598, respectively, related to consolidated trusts) | $ | 10,105 | $ | 9,682 | |||||||

Debt: | |||||||||||

Of Fannie Mae (includes $7,251 and $8,186, respectively, at fair value) | 246,682 | 276,752 | |||||||||

Of consolidated trusts (includes $24,948 and $30,493, respectively, at fair value) | 3,127,688 | 3,053,302 | |||||||||

Other liabilities (includes $322 and $492, respectively, related to consolidated trusts) | 9,655 | 9,479 | |||||||||

Total liabilities | 3,394,130 | 3,349,215 | |||||||||

Commitments and contingencies (Note 14) | — | — | |||||||||

Fannie Mae stockholders’ equity (deficit): | |||||||||||

Senior preferred stock, 1,000,000 shares issued and outstanding | 120,836 | 117,149 | |||||||||

Preferred stock, 700,000,000 shares are authorized—555,374,922 shares issued and outstanding | 19,130 | 19,130 | |||||||||

Common stock, no par value, no maximum authorization—1,308,762,703 shares issued and 1,158,087,567 shares outstanding | 687 | 687 | |||||||||

Accumulated deficit | (126,591 | ) | (133,805 | ) | |||||||

Accumulated other comprehensive income | 313 | 553 | |||||||||

Treasury stock, at cost, 150,675,136 shares | (7,400 | ) | (7,400 | ) | |||||||

Total stockholders’ equity (deficit) (See Note 1: Senior Preferred Stock Purchase Agreement and Senior Preferred Stock for information on our dividend obligation to Treasury) | 6,975 | (3,686 | ) | ||||||||

Total liabilities and equity (deficit) | $ | 3,401,105 | $ | 3,345,529 | |||||||

See Notes to Condensed Consolidated Financial Statements in the Third Quarter 2018 Form 10-Q

Third Quarter 2018 Results | 11 | |

FANNIE MAE

(In conservatorship)

Condensed Consolidated Statements of Operations and Comprehensive Income — (Unaudited)

(Dollars in millions, except share amounts)

For the Three Months | For the Nine Months | ||||||||||||||||||||||

Ended September 30, | Ended September 30, | ||||||||||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||||||||||

Interest income: | |||||||||||||||||||||||

Trading securities | $ | 363 | $ | 195 | $ | 917 | $ | 513 | |||||||||||||||

Available-for-sale securities | 54 | 77 | 175 | 269 | |||||||||||||||||||

Mortgage loans (includes $27,058 and $25,168, respectively, for the three months ended and $79,877 and $75,155, respectively, for the nine months ended related to consolidated trusts) | 28,723 | 27,047 | 85,064 | 81,105 | |||||||||||||||||||

Other | 204 | 142 | 559 | 351 | |||||||||||||||||||

Total interest income | 29,344 | 27,461 | 86,715 | 82,238 | |||||||||||||||||||

Interest expense: | |||||||||||||||||||||||

Short-term debt | (114 | ) | (72 | ) | (331 | ) | (173 | ) | |||||||||||||||

Long-term debt (includes $22,361 and $20,609, respectively, for the three months ended and $65,972 and $61,622, respectively, for the nine months ended related to consolidated trusts) | (23,861 | ) | (22,115 | ) | (70,406 | ) | (66,443 | ) | |||||||||||||||

Total interest expense | (23,975 | ) | (22,187 | ) | (70,737 | ) | (66,616 | ) | |||||||||||||||

Net interest income | 5,369 | 5,274 | 15,978 | 15,622 | |||||||||||||||||||

Benefit (provision) for credit losses | 716 | (182 | ) | 2,229 | 1,481 | ||||||||||||||||||

Net interest income after benefit (provision) for credit losses | 6,085 | 5,092 | 18,207 | 17,103 | |||||||||||||||||||

Investment gains, net | 166 | 313 | 693 | 689 | |||||||||||||||||||

Fair value gains (losses), net | 386 | (289 | ) | 1,660 | (1,020 | ) | |||||||||||||||||

Fee and other income | 271 | 1,194 | 830 | 1,796 | |||||||||||||||||||

Non-interest income | 823 | 1,218 | 3,183 | 1,465 | |||||||||||||||||||

Administrative expenses: | |||||||||||||||||||||||

Salaries and employee benefits | (355 | ) | (331 | ) | (1,101 | ) | (1,007 | ) | |||||||||||||||

Professional services | (247 | ) | (218 | ) | (744 | ) | (681 | ) | |||||||||||||||

Other administrative expenses | (138 | ) | (115 | ) | (400 | ) | (346 | ) | |||||||||||||||

Total administrative expenses | (740 | ) | (664 | ) | (2,245 | ) | (2,034 | ) | |||||||||||||||

Foreclosed property expense | (159 | ) | (140 | ) | (460 | ) | (391 | ) | |||||||||||||||

Temporary Payroll Tax Cut Continuation Act of 2011 (“TCCA”) fees | (576 | ) | (531 | ) | (1,698 | ) | (1,552 | ) | |||||||||||||||

Other expenses, net | (377 | ) | (427 | ) | (946 | ) | (1,100 | ) | |||||||||||||||

Total expenses | (1,852 | ) | (1,762 | ) | (5,349 | ) | (5,077 | ) | |||||||||||||||

Income before federal income taxes | 5,056 | 4,548 | 16,041 | 13,491 | |||||||||||||||||||

Provision for federal income taxes | (1,045 | ) | (1,525 | ) | (3,312 | ) | (4,495 | ) | |||||||||||||||

Net income | 4,011 | 3,023 | 12,729 | 8,996 | |||||||||||||||||||

Other comprehensive income (loss): | |||||||||||||||||||||||

Changes in unrealized gains on available-for-sale securities, net of reclassification adjustments and taxes | (33 | ) | 27 | (349 | ) | (46 | ) | ||||||||||||||||

Other | (3 | ) | (2 | ) | (8 | ) | (6 | ) | |||||||||||||||

Total other comprehensive income (loss) | (36 | ) | 25 | (357 | ) | (52 | ) | ||||||||||||||||

Total comprehensive income | $ | 3,975 | $ | 3,048 | $ | 12,372 | $ | 8,944 | |||||||||||||||

Net income | $ | 4,011 | $ | 3,023 | $ | 12,729 | $ | 8,996 | |||||||||||||||

Dividends distributed or available for distribution to senior preferred stockholder | (3,975 | ) | (3,048 | ) | (9,372 | ) | (8,944 | ) | |||||||||||||||

Net income (loss) attributable to common stockholders | $ | 36 | $ | (25 | ) | $ | 3,357 | $ | 52 | ||||||||||||||

Earnings (loss) per share: | |||||||||||||||||||||||

Basic | $ | 0.01 | $ | 0.00 | $ | 0.58 | $ | 0.01 | |||||||||||||||

Diluted | 0.01 | 0.00 | 0.57 | 0.01 | |||||||||||||||||||

Weighted-average common shares outstanding: | |||||||||||||||||||||||

Basic | 5,762 | 5,762 | 5,762 | 5,762 | |||||||||||||||||||

Diluted | 5,893 | 5,762 | 5,893 | 5,893 | |||||||||||||||||||

See Notes to Condensed Consolidated Financial Statements in the Third Quarter 2018 Form 10-Q

Third Quarter 2018 Results | 12 | |

FANNIE MAE

(In conservatorship)

Condensed Consolidated Statements of Cash Flows — (Unaudited)

(Dollars in millions)

For the Nine Months Ended September 30, | |||||||||||

2018 | 2017 | ||||||||||

Net cash provided by (used in) operating activities | $ | (1,796 | ) | $ | 172 | ||||||

Cash flows provided by investing activities: | |||||||||||

Proceeds from maturities and paydowns of trading securities held for investment | 163 | 1,088 | |||||||||

Proceeds from sales of trading securities held for investment | 96 | 149 | |||||||||

Proceeds from maturities and paydowns of available-for-sale securities | 564 | 1,671 | |||||||||

Proceeds from sales of available-for-sale securities | 729 | 1,207 | |||||||||

Purchases of loans held for investment | (135,913 | ) | (142,565 | ) | |||||||

Proceeds from repayments of loans acquired as held for investment of Fannie Mae | 11,651 | 17,721 | |||||||||

Proceeds from sales of loans acquired as held for investment of Fannie Mae | 10,637 | 5,399 | |||||||||

Proceeds from repayments and sales of loans acquired as held for investment of consolidated trusts | 306,374 | 323,424 | |||||||||

Advances to lenders | (83,643 | ) | (89,348 | ) | |||||||

Proceeds from disposition of acquired property and preforeclosure sales | 7,090 | 9,671 | |||||||||

Net change in federal funds sold and securities purchased under agreements to resell or similar arrangements | (7,128 | ) | 6,675 | ||||||||

Other, net | (56 | ) | 344 | ||||||||

Net cash provided by investing activities | 110,564 | 135,436 | |||||||||

Cash flows used in financing activities: | |||||||||||

Proceeds from issuance of debt of Fannie Mae | 636,466 | 776,380 | |||||||||

Payments to redeem debt of Fannie Mae | (666,888 | ) | (809,299 | ) | |||||||

Proceeds from issuance of debt of consolidated trusts | 278,357 | 282,433 | |||||||||

Payments to redeem debt of consolidated trusts | (364,942 | ) | (383,969 | ) | |||||||

Payments of cash dividends on senior preferred stock to Treasury | (5,397 | ) | (11,367 | ) | |||||||

Proceeds from senior preferred stock purchase agreement with Treasury | 3,687 | — | |||||||||

Other, net | 720 | 88 | |||||||||

Net cash used in financing activities | (117,997 | ) | (145,734 | ) | |||||||

Net decrease in cash, cash equivalents and restricted cash | (9,229 | ) | (10,126 | ) | |||||||

Cash, cash equivalents and restricted cash at beginning of period | 60,260 | 62,177 | |||||||||

Cash, cash equivalents and restricted cash at end of period | $ | 51,031 | $ | 52,051 | |||||||

Cash paid during the period for: | |||||||||||

Interest | $ | 82,010 | $ | 82,652 | |||||||

Income taxes | 460 | 1,670 | |||||||||

See Notes to Condensed Consolidated Financial Statements in the Third Quarter 2018 Form 10-Q

Third Quarter 2018 Results | 13 | |