Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Intercontinental Exchange, Inc. | ice2018930ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - Intercontinental Exchange, Inc. | ice2018930ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - Intercontinental Exchange, Inc. | ice2018930ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - Intercontinental Exchange, Inc. | ice2018930ex311.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One) | |

þ | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended September 30, 2018 | |

Or | |

¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to | |

Commission File Number 001-36198

INTERCONTINENTAL EXCHANGE, INC.

(Exact name of registrant as specified in its charter)

Delaware | 46-2286804 |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification Number) |

5660 New Northside Drive, Atlanta, Georgia | 30328 (Zip Code) |

(Address of principal executive offices) | |

(770) 857-4700

Registrant’s telephone number, including area code

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

As of October 26, 2018, the number of shares of the registrant’s Common Stock outstanding was 569,583,956 shares.

INTERCONTINENTAL EXCHANGE, INC.

Form 10-Q

Quarterly Period Ended September 30, 2018

TABLE OF CONTENTS

PART I. | Financial Statements | |

Item 1. | ||

Consolidated Balance Sheets as of September 30, 2018 and December 31, 2017 | ||

Consolidated Statements of Income for the nine and three months ended September 30, 2018 and 2017 | ||

Consolidated Statements of Comprehensive Income for the nine and three months ended September 30, 2018 and 2017 | ||

Consolidated Statements of Changes in Equity, Accumulated Other Comprehensive Loss and Redeemable Non-Controlling Interest for the nine months ended September 30, 2018 and for the year ended December 31, 2017 | ||

Consolidated Statements of Cash Flows for the nine months ended September 30, 2018 and 2017 | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II. | Other Information | |

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

PART I. Financial Statements

Item 1. Consolidated Financial Statements (Unaudited)

Intercontinental Exchange, Inc. and Subsidiaries

Consolidated Balance Sheets

(In millions, except per share amounts)

(Unaudited)

As of | As of | ||||||

September 30, 2018 | December 31, 2017 | ||||||

Assets: | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 515 | $ | 535 | |||

Short-term restricted cash and cash equivalents | 817 | 769 | |||||

Customer accounts receivable, net of allowance for doubtful accounts of $7 and $6 at September 30, 2018 and December 31, 2017, respectively | 1,020 | 903 | |||||

Margin deposits, guaranty funds and delivery contracts receivable | 58,764 | 51,222 | |||||

Prepaid expenses and other current assets | 179 | 133 | |||||

Total current assets | 61,295 | 53,562 | |||||

Property and equipment, net | 1,206 | 1,246 | |||||

Other non-current assets: | |||||||

Goodwill | 12,934 | 12,216 | |||||

Other intangible assets, net | 10,445 | 10,269 | |||||

Long-term restricted cash and cash equivalents | 330 | 264 | |||||

Other non-current assets | 1,032 | 707 | |||||

Total other non-current assets | 24,741 | 23,456 | |||||

Total assets | $ | 87,242 | $ | 78,264 | |||

Liabilities and Equity: | |||||||

Current liabilities: | |||||||

Accounts payable and accrued liabilities | $ | 486 | $ | 462 | |||

Section 31 fees payable | 21 | 128 | |||||

Accrued salaries and benefits | 217 | 227 | |||||

Deferred revenue | 249 | 125 | |||||

Short-term debt | 1,198 | 1,833 | |||||

Margin deposits, guaranty funds and delivery contracts payable | 58,764 | 51,222 | |||||

Other current liabilities | 130 | 178 | |||||

Total current liabilities | 61,065 | 54,175 | |||||

Non-current liabilities: | |||||||

Non-current deferred tax liability, net | 2,275 | 2,298 | |||||

Long-term debt | 6,488 | 4,267 | |||||

Accrued employee benefits | 235 | 243 | |||||

Other non-current liabilities | 325 | 296 | |||||

Total non-current liabilities | 9,323 | 7,104 | |||||

Total liabilities | 70,388 | 61,279 | |||||

Commitments and contingencies | |||||||

Equity: | |||||||

Intercontinental Exchange, Inc. stockholders’ equity: | |||||||

Preferred stock, $0.01 par value; 100 shares authorized; no shares issued or outstanding at September 30, 2018 and December 31, 2017 | — | — | |||||

Common stock, $0.01 par value; 1,500 shares authorized; 603 and 600 shares issued at September 30, 2018 and December 31, 2017, respectively, and 571 and 583 shares outstanding at September 30, 2018 and December 31, 2017, respectively | 6 | 6 | |||||

Treasury stock, at cost; 32 and 17 shares at September 30, 2018 and December 31, 2017, respectively | (2,213 | ) | (1,076 | ) | |||

2

Additional paid-in capital | 11,495 | 11,392 | |||||

Retained earnings | 7,818 | 6,858 | |||||

Accumulated other comprehensive loss | (274 | ) | (223 | ) | |||

Total Intercontinental Exchange, Inc. stockholders’ equity | 16,832 | 16,957 | |||||

Non-controlling interest in consolidated subsidiaries | 22 | 28 | |||||

Total equity | 16,854 | 16,985 | |||||

Total liabilities and equity | $ | 87,242 | $ | 78,264 | |||

See accompanying notes.

3

Intercontinental Exchange, Inc. and Subsidiaries

Consolidated Statements of Income

(In millions, except per share amounts)

(Unaudited)

Nine Months Ended September 30, | Three Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues: | |||||||||||||||

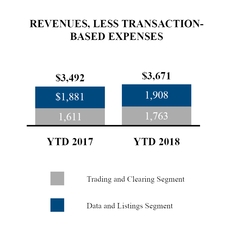

Transaction and clearing, net | $ | 2,522 | $ | 2,373 | $ | 760 | $ | 758 | |||||||

Data services | 1,576 | 1,559 | 530 | 518 | |||||||||||

Listings | 332 | 322 | 112 | 105 | |||||||||||

Other revenues | 169 | 148 | 61 | 54 | |||||||||||

Total revenues | 4,599 | 4,402 | 1,463 | 1,435 | |||||||||||

Transaction-based expenses: | |||||||||||||||

Section 31 fees | 272 | 275 | 61 | 92 | |||||||||||

Cash liquidity payments, routing and clearing | 656 | 635 | 202 | 197 | |||||||||||

Total revenues, less transaction-based expenses | 3,671 | 3,492 | 1,200 | 1,146 | |||||||||||

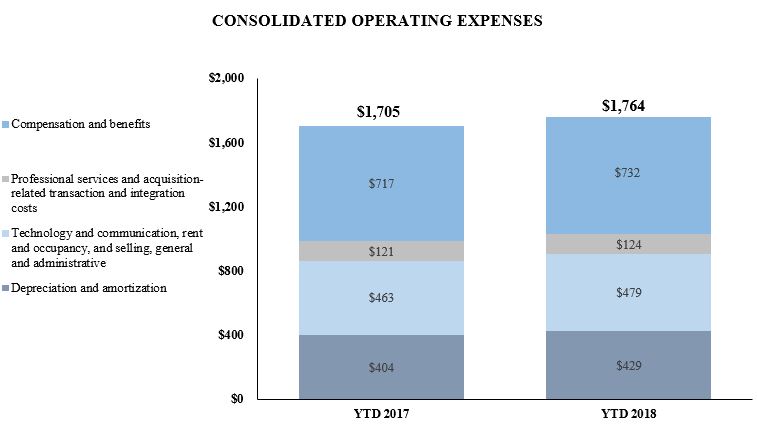

Operating expenses: | |||||||||||||||

Compensation and benefits | 732 | 717 | 251 | 234 | |||||||||||

Professional services | 91 | 94 | 32 | 30 | |||||||||||

Acquisition-related transaction and integration costs | 33 | 27 | 6 | 4 | |||||||||||

Technology and communication | 320 | 294 | 107 | 99 | |||||||||||

Rent and occupancy | 50 | 52 | 17 | 17 | |||||||||||

Selling, general and administrative | 109 | 117 | 37 | 38 | |||||||||||

Depreciation and amortization | 429 | 404 | 148 | 128 | |||||||||||

Total operating expenses | 1,764 | 1,705 | 598 | 550 | |||||||||||

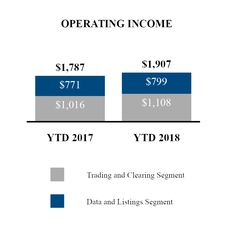

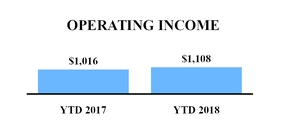

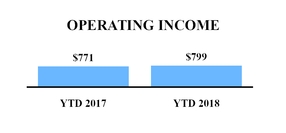

Operating income | 1,907 | 1,787 | 602 | 596 | |||||||||||

Other income (expense): | |||||||||||||||

Interest expense | (173 | ) | (137 | ) | (66 | ) | (47 | ) | |||||||

Other income, net | 48 | 205 | 18 | 14 | |||||||||||

Other income (expense), net | (125 | ) | 68 | (48 | ) | (33 | ) | ||||||||

Income before income tax expense | 1,782 | 1,855 | 554 | 563 | |||||||||||

Income tax expense | 381 | 540 | 89 | 186 | |||||||||||

Net income | $ | 1,401 | $ | 1,315 | $ | 465 | $ | 377 | |||||||

Net income attributable to non-controlling interest | (24 | ) | (22 | ) | (7 | ) | (6 | ) | |||||||

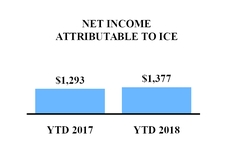

Net income attributable to Intercontinental Exchange, Inc. | $ | 1,377 | $ | 1,293 | $ | 458 | $ | 371 | |||||||

Earnings per share attributable to Intercontinental Exchange, Inc. common stockholders: | |||||||||||||||

Basic | $ | 2.39 | $ | 2.19 | $ | 0.80 | $ | 0.63 | |||||||

Diluted | $ | 2.37 | $ | 2.17 | $ | 0.79 | $ | 0.63 | |||||||

Weighted average common shares outstanding: | |||||||||||||||

Basic | 577 | 591 | 572 | 588 | |||||||||||

Diluted | 581 | 595 | 576 | 592 | |||||||||||

Dividend per share | $ | 0.72 | $ | 0.60 | $ | 0.24 | $ | 0.20 | |||||||

See accompanying notes.

4

Intercontinental Exchange, Inc. and Subsidiaries

Consolidated Statements of Comprehensive Income

(In millions)

(Unaudited)

Nine Months Ended September 30, | Three Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Net income | $ | 1,401 | $ | 1,315 | $ | 465 | $ | 377 | |||||||

Other comprehensive income (loss): | |||||||||||||||

Foreign currency translation adjustments, net of tax benefit (expense) of $1 and ($11) for the nine months ended September 30, 2018 and 2017, respectively, and ($4) for the three months ended September 30, 2017 | (51 | ) | 130 | (9 | ) | 45 | |||||||||

Change in fair value of available-for-sale securities | — | 68 | — | — | |||||||||||

Reclassification of realized gain on available-for-sale investment to other income | — | (176 | ) | — | — | ||||||||||

Other comprehensive income (loss) | (51 | ) | 22 | (9 | ) | 45 | |||||||||

Comprehensive income | $ | 1,350 | $ | 1,337 | $ | 456 | $ | 422 | |||||||

Comprehensive income attributable to non-controlling interest | (24 | ) | (22 | ) | (7 | ) | (6 | ) | |||||||

Comprehensive income attributable to Intercontinental Exchange, Inc. | $ | 1,326 | $ | 1,315 | $ | 449 | $ | 416 | |||||||

See accompanying notes.

5

Intercontinental Exchange, Inc. and Subsidiaries

Consolidated Statements of Changes in Equity, Accumulated Other Comprehensive Loss

and Redeemable Non-Controlling Interest

(In millions)

(Unaudited)

Intercontinental Exchange, Inc. Stockholders’ Equity | Non- Controlling Interest in Consolidated Subsidiaries | Total Equity | Redeemable Non-Controlling Interest | ||||||||||||||||||||||||||||||||||

Common Stock | Treasury Stock | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Loss | |||||||||||||||||||||||||||||||||

Shares | Value | Shares | Value | ||||||||||||||||||||||||||||||||||

Balance, as of December 31, 2016 | 596 | $ | 6 | (1 | ) | $ | (40 | ) | $ | 11,306 | $ | 4,810 | $ | (344 | ) | $ | 37 | $ | 15,775 | $ | 36 | ||||||||||||||||

Other comprehensive income | — | — | — | — | — | — | 121 | — | 121 | — | |||||||||||||||||||||||||||

Exercise of common stock options | — | — | — | — | 17 | — | — | — | 17 | — | |||||||||||||||||||||||||||

Repurchases of common stock | — | — | (15 | ) | (949 | ) | — | — | — | — | (949 | ) | — | ||||||||||||||||||||||||

Payments relating to treasury shares | — | — | (1 | ) | (88 | ) | — | — | — | — | (88 | ) | — | ||||||||||||||||||||||||

Stock-based compensation | — | — | — | — | 152 | — | — | — | 152 | — | |||||||||||||||||||||||||||

Issuance of restricted stock | 4 | — | — | 1 | (1 | ) | — | — | — | — | — | ||||||||||||||||||||||||||

Acquisition of non-controlling interest | — | — | — | — | (82 | ) | — | — | (10 | ) | (92 | ) | — | ||||||||||||||||||||||||

Distributions of profits | — | — | — | — | — | — | — | (26 | ) | (26 | ) | — | |||||||||||||||||||||||||

Dividends paid to stockholders | — | — | — | — | — | (476 | ) | — | — | (476 | ) | — | |||||||||||||||||||||||||

Acquisition of redeemable non-controlling interest | — | — | — | — | — | (2 | ) | — | — | (2 | ) | (37 | ) | ||||||||||||||||||||||||

Net income attributable to non-controlling interest | — | — | — | — | — | (28 | ) | — | 27 | (1 | ) | 1 | |||||||||||||||||||||||||

Net income | — | — | — | — | — | 2,554 | — | — | 2,554 | — | |||||||||||||||||||||||||||

Balance, as of December 31, 2017 | 600 | 6 | (17 | ) | (1,076 | ) | 11,392 | 6,858 | (223 | ) | 28 | 16,985 | — | ||||||||||||||||||||||||

Other comprehensive loss | — | — | — | — | — | — | (51 | ) | — | (51 | ) | — | |||||||||||||||||||||||||

Exercise of common stock options | — | — | — | — | 19 | — | — | — | 19 | — | |||||||||||||||||||||||||||

Repurchases of common stock | — | — | (14 | ) | (1,059 | ) | — | — | — | — | (1,059 | ) | — | ||||||||||||||||||||||||

Payments relating to treasury shares | — | — | (1 | ) | (78 | ) | — | — | — | — | (78 | ) | — | ||||||||||||||||||||||||

Stock-based compensation | — | — | — | — | 107 | — | — | — | 107 | — | |||||||||||||||||||||||||||

Issuance of restricted stock | 3 | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Acquisition of non-controlling interest | — | — | — | — | (23 | ) | — | — | (2 | ) | (25 | ) | — | ||||||||||||||||||||||||

Distributions of profits | — | — | — | — | — | — | — | (28 | ) | (28 | ) | — | |||||||||||||||||||||||||

Dividends paid to stockholders | — | — | — | — | — | (417 | ) | — | — | (417 | ) | — | |||||||||||||||||||||||||

Net income attributable to non-controlling interest | — | — | — | — | — | (24 | ) | — | 24 | — | — | ||||||||||||||||||||||||||

Net income | — | — | — | — | — | 1,401 | — | — | 1,401 | — | |||||||||||||||||||||||||||

Balance, as of September 30, 2018 | 603 | $ | 6 | (32 | ) | $ | (2,213 | ) | $ | 11,495 | $ | 7,818 | $ | (274 | ) | $ | 22 | $ | 16,854 | $ | — | ||||||||||||||||

As of | As of | ||||||

September 30, 2018 | December 31, 2017 | ||||||

Accumulated other comprehensive loss was as follows: | |||||||

Foreign currency translation adjustments | $ | (187 | ) | $ | (136 | ) | |

Comprehensive income from equity method investment | 2 | 2 | |||||

Employee benefit plans adjustments | (89 | ) | (89 | ) | |||

Accumulated other comprehensive loss | $ | (274 | ) | $ | (223 | ) | |

See accompanying notes.

6

Intercontinental Exchange, Inc. and Subsidiaries

Consolidated Statements of Cash Flows

(In millions)

(Unaudited)

Nine Months Ended September 30, | |||||||

2018 | 2017 | ||||||

Operating activities: | |||||||

Net income | $ | 1,401 | $ | 1,315 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 429 | 404 | |||||

Stock-based compensation | 93 | 102 | |||||

Deferred taxes | (2 | ) | 58 | ||||

Cetip realized investment gain, net | — | (114 | ) | ||||

Other | (11 | ) | (13 | ) | |||

Changes in assets and liabilities: | |||||||

Customer accounts receivable | (119 | ) | (153 | ) | |||

Other current and non-current assets | (24 | ) | (29 | ) | |||

Section 31 fees payable | (117 | ) | (99 | ) | |||

Deferred revenue | 124 | 129 | |||||

Other current and non-current liabilities | (39 | ) | (190 | ) | |||

Total adjustments | 334 | 95 | |||||

Net cash provided by operating activities | 1,735 | 1,410 | |||||

Investing activities: | |||||||

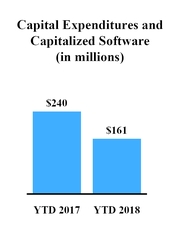

Capital expenditures | (49 | ) | (136 | ) | |||

Capitalized software development costs | (112 | ) | (104 | ) | |||

Proceeds from sale of Cetip, net | — | 438 | |||||

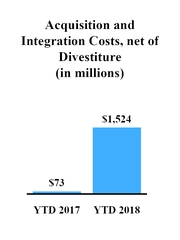

Cash paid for acquisitions, net of cash received for divestiture | (1,151 | ) | 9 | ||||

Purchases of investments | (305 | ) | — | ||||

Net cash provided by (used in) investing activities | (1,617 | ) | 207 | ||||

Financing activities: | |||||||

Proceeds from debt facilities | 2,213 | 985 | |||||

Repayments of debt facilities | (600 | ) | (850 | ) | |||

Repayments of commercial paper, net | (35 | ) | (445 | ) | |||

Repurchases of common stock | (1,059 | ) | (709 | ) | |||

Dividends to stockholders | (417 | ) | (358 | ) | |||

Payments relating to treasury shares received for restricted stock tax payments and stock option exercises | (78 | ) | (85 | ) | |||

Acquisition of non-controlling interest and redeemable non-controlling interest | (35 | ) | (55 | ) | |||

Other | (8 | ) | (17 | ) | |||

Net cash used in financing activities | (19 | ) | (1,534 | ) | |||

Effect of exchange rate changes on cash, cash equivalents and restricted cash and cash equivalents | (5 | ) | 9 | ||||

Net increase in cash, cash equivalents, and restricted cash and cash equivalents | 94 | 92 | |||||

Cash, cash equivalents, and restricted cash and cash equivalents, beginning of period | 1,568 | 1,350 | |||||

Cash, cash equivalents, and restricted cash and cash equivalents, end of period | $ | 1,662 | $ | 1,442 | |||

Supplemental cash flow disclosure: | |||||||

Cash paid for income taxes | $ | 424 | $ | 511 | |||

Cash paid for interest | $ | 136 | $ | 99 | |||

See accompanying notes.

7

Intercontinental Exchange, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

(Unaudited)

1. | Description of Business |

We are a leading global operator of regulated exchanges, clearing houses and listings venues, and a provider of data services for commodity, fixed income and equity markets. We operate regulated marketplaces for listing, trading and clearing a broad array of derivatives and securities contracts across all major asset classes, including energy and agricultural commodities, interest rates, equities, equity derivatives, exchange-traded funds, or ETFs, credit derivatives, bonds and currencies. We also offer end-to-end data services and solutions to support the trading, investment, risk management and connectivity needs of customers around the world across all major asset classes.

Our exchanges include derivative exchanges in the United States, or U.S., United Kingdom, or U.K., European Union, or EU, Canada and Singapore, and cash equities, equity options and bond exchanges in the U.S. We also operate over-the-counter, or OTC, markets for physical energy, fixed income and credit default swaps, or CDS, trade execution. To serve global derivatives markets, we operate central counterparty clearing houses, or CCPs, in the U.S., U.K., EU, Canada and Singapore (Note 10). We offer a range of data services for global financial and commodity markets, including pricing and reference data, exchange data, analytics, feeds, index services, desktops and connectivity solutions. Through our markets, clearing houses, listings and data services, we provide end-to-end solutions for our customers through liquid markets, benchmark products, access to capital markets, and related services to support their ability to manage risk and raise capital. Our business is currently conducted as two reportable business segments, our Trading and Clearing segment and our Data and Listings segment, and the majority of our identifiable assets are located in the U.S., U.K. and Canada (Note 13).

2. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited consolidated financial statements have been prepared by us in accordance with U.S. generally accepted accounting principles, or U.S. GAAP, pursuant to the rules and regulations of the Securities and Exchange Commission, or SEC, regarding interim financial reporting. Accordingly, the unaudited consolidated financial statements do not include all of the information and footnotes required by U.S. GAAP for complete financial statements and should be read in conjunction with our audited consolidated financial statements and related notes thereto for the year ended December 31, 2017. The accompanying unaudited consolidated financial statements reflect all adjustments that are, in our opinion, necessary for a fair presentation of results for the interim periods presented. We believe that these adjustments are of a normal recurring nature.

Preparing financial statements requires us to make certain estimates and assumptions that affect the amounts that are reported in the consolidated financial statements and accompanying disclosures. Actual results may be different from these estimates. The results of operations for the nine and three months ended September 30, 2018 are not necessarily indicative of the results to be expected for any future period or the full fiscal year.

The accompanying unaudited consolidated financial statements include our accounts and those of our wholly-owned and controlled subsidiaries. All intercompany balances and transactions between us and our wholly-owned and controlled subsidiaries have been eliminated in the consolidation. For those consolidated subsidiaries in which our ownership is less than 100% and for which we have control over the assets and liabilities and the management of the entity, the outside stockholders’ interests are shown as non-controlling interests.

Reclassifications

Certain prior period amounts have been reclassified to conform to the current period’s financial statement presentation. See "Recently Adopted Accounting Pronouncements" below for a discussion of our adoption of new accounting standards.

Recently Adopted Accounting Pronouncements

On January 1, 2018, we adopted Accounting Standards Codification, or ASC, Topic 606, Revenue from Contracts with Customers, and ASC 340-40, Other Assets and Deferred Costs - Contracts with Customers, collectively referred to as ASC 606. ASC 606 provides guidance outlining a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers. ASC 606 superseded most revenue recognition guidance and requires us to recognize revenue when we transfer promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. ASC 606 requires enhanced disclosures, including (i) revenue recognition policies used to identify performance obligations to customers and (ii) the use of significant judgments in measurement and recognition. We adopted ASC 606 retrospectively and restated each prior period presented to reflect our adoption thereof. The impacts of our

8

adoption of ASC 606 on our results for the years ended December 31, 2017, 2016 and 2015, respectively, were disclosed in our 2017 Form 10-K.

The adoption of ASC 606 accelerated the timing of recognition of a portion of original listing fees related to our New York Stock Exchange, or NYSE, businesses. In addition, and to a lesser extent, the adoption decelerated the timing of recognition of a portion of clearing fee revenues. Revenue recognition related to all other trading, clearing and data businesses remains unchanged.

Our adoption of ASC 606 had the following impact on our reported results for the prior periods presented, driven primarily by the accelerated recognition of listings fee revenue in our NYSE businesses (in millions, except earnings per share):

As Reported | New Revenue Standard Adjustment | As Adjusted | |||||||||

Nine months ended September 30, 2017 | |||||||||||

Total revenues | $ | 4,395 | $ | 7 | $ | 4,402 | |||||

Total revenues, less transaction-based expenses | 3,485 | 7 | 3,492 | ||||||||

Income tax expense | 537 | 3 | 540 | ||||||||

Net income attributable to Intercontinental Exchange, Inc. | 1,289 | 4 | 1,293 | ||||||||

Basic earnings per share | $ | 2.18 | $ | 0.01 | $ | 2.19 | |||||

Diluted earnings per share | $ | 2.17 | $ | — | $ | 2.17 | |||||

As Reported | New Revenue Standard Adjustment | As Adjusted | |||||||||

Three months ended September 30, 2017 | |||||||||||

Total revenues | $ | 1,432 | $ | 3 | $ | 1,435 | |||||

Total revenues, less transaction-based expenses | 1,143 | 3 | 1,146 | ||||||||

Income tax expense | 185 | 1 | 186 | ||||||||

Net income attributable to Intercontinental Exchange, Inc. | 369 | 2 | 371 | ||||||||

Basic earnings per share | $ | 0.63 | $ | — | $ | 0.63 | |||||

Diluted earnings per share | $ | 0.62 | $ | 0.01 | $ | 0.63 | |||||

As Reported | New Revenue Standard Adjustment | As Adjusted | |||||||||

As of December 31, 2017 | |||||||||||

Deferred revenue, current | $ | 121 | $ | 4 | $ | 125 | |||||

Deferred revenue, non-current | 143 | (52 | ) | 91 | |||||||

Net deferred tax liabilities | 2,280 | 15 | 2,295 | ||||||||

Retained earnings | 6,825 | 33 | 6,858 | ||||||||

Additional disclosures related to our adoption of ASC 606 are provided in Note 4.

The Financial Accounting Standards Board, or FASB, has issued Accounting Standards Update, or ASU, No. 2017-07, Compensation-Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost, or ASU 2017-07. The amendments in ASU 2017-07 require that an employer disaggregate the service cost component from the other components of net benefit cost. The amendments also provide explicit guidance on how to present the service cost component in the same line item as other related compensation costs, and the other components of net benefit cost in the income statement outside of operating income. The guidance only allows the service cost component of net benefit cost to be eligible for capitalization. We adopted ASU 2017-07 on January 1, 2018 and applied it retrospectively to each prior period presented. We have a pension plan, a U.S. nonqualified supplemental executive retirement plan, and post-retirement defined benefit plans that are all impacted by the guidance. Each of the foregoing plans are frozen and do not have a service cost component, which means the expense or benefit recognized under each plan represents other components of net benefit cost as defined in the guidance. The combined net periodic (expense) benefit of these plans was ($6 million) and $6 million for the nine months ended September 30, 2018 and 2017, respectively, and ($2 million) and $2 million for the three months ended September 30, 2018 and 2017, respectively, and was previously reported as an adjustment to compensation and benefits expenses in the accompanying consolidated statements of income. Following our adoption of ASU 2017-07, these amounts were reclassified to be

9

included in other income, net, in the accompanying consolidated statements of income, and these adjustments had no impact on net income.

The FASB has issued ASU No. 2016-01, Financial Instruments - Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities, or ASU 2016-01. ASU 2016-01 provides updated guidance for the recognition, measurement, presentation, and disclosure of certain financial assets and liabilities, including the requirement that equity investments (except (i) those accounted for under the equity method of accounting or (ii) those that result in consolidation of the investee) are to be measured at fair value with changes in fair value recognized in net income. We adopted ASU 2016-01 on January 1, 2018. Our equity investments, including our investments in Euroclear plc, or Euroclear (Note 3), and Coinbase Global, Inc., or Coinbase, among others, are now subject to valuation under ASU 2016-01. These investments do not currently have readily determinable fair market values as they are not publicly-listed companies. ASU 2016-01 permits a policy election to only adjust the fair value of such investments if and when there is an observable price change in an orderly transaction of a similar or identical investment occurring after adoption, with any change in fair value recognized in net income. We have made this policy election for all of our equity investments without readily determinable fair values, and our adoption of ASU 2016-01 did not result in any fair value adjustments as of September 30, 2018.

In December 2017, the SEC staff issued Staff Accounting Bulletin No. 118, or SAB 118, which provided guidance for companies that have not completed their accounting for the income tax effects of the Tax Cuts and Jobs Act of 2017, or TCJA, in the period of enactment, allowing for a measurement period of up to one year after the enactment date to finalize the recording of the related tax impacts. We are applying the guidance in SAB 118 when accounting for the enactment-date effects of the TCJA. As of September 30, 2018, our estimates recorded as of December 31, 2017 for the tax effects of the TCJA, are not final. Our estimates recorded as of December 31, 2017 and as of September 30, 2018 may be affected due to changes in interpretations of the legislation, changes in accounting standards or related interpretations in response to the TCJA. We have also made reasonable estimates of the TCJA’s impact on state income tax. Our estimates are based on the best available information as of September 30, 2018 and our interpretation of the TCJA and related state tax implications as currently enacted. Our estimates do not include any potential federal or state administrative and/or legislative adjustments to certain provisions of the TCJA and related state provisions. We will continue to analyze the TCJA in order to finalize related federal and state impacts within the measurement period.

In January 2018, the FASB staff issued Question & Answer Topic 740, No. 5, Accounting for Global Intangible Low-Taxed Income, stating that a company may either elect to treat taxes due on future inclusions of its non-U.S. income in its U.S. taxable income under the newly enacted Global Intangible Low-Taxed Income provisions as a current period expense when incurred, or factor them into the company’s measurement of its deferred taxes. As of September 30, 2018, we have completed our analysis of the two different accounting policies and have made an election to recognize such taxes as a current period expense when incurred.

In the fourth quarter of 2017, we adopted ASU 2016-18, Statement of Cash Flows: Restricted Cash, or ASU 2016-18, which requires us to show the changes in the total of cash, cash equivalents and restricted cash and cash equivalents in the statement of cash flows. As a result, we no longer present transfers between cash, cash equivalents and restricted cash and cash equivalents in the statement of cash flows. We have reclassified changes in restricted cash from cash flows provided by (used in) investing activities, to the total change in beginning and end-of-period balances. Our statements of cash flows for the nine months ended September 30, 2018 and 2017 reflect this change.

Accounting Pronouncements Not Yet Adopted

The FASB has issued ASU No. 2016-02, Leases, or ASU 2016-02. ASU 2016-02 requires an entity to recognize both assets and liabilities arising from finance and operating leases, along with additional qualitative and quantitative disclosures. It requires a lessee to recognize a liability in its balance sheet to make lease payments (the lease liability) and a right-of-use asset representing its right to use the underlying asset for the lease term. In transition, lessees and lessors are required to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach. ASU 2016-02 is required to be adopted at the beginning of our first quarter of fiscal year 2019, with early adoption permitted. We do not expect to adopt ASU 2016-02 early and we expect to record a material right-of-use asset and offsetting lease liability on our adoption date of January 1, 2019, primarily related to our leased office space and data center facilities. We expect that we will elect the alternative transition approach allowed under ASU 2016-02, under which we will record a cumulative effect adjustment to retained earnings on January 1, 2019, and will not restate prior periods. We expect to implement new accounting policies as well as to elect certain practical expedients available to us under ASU 2016-02, including those related to capitalization thresholds, leases with terms of less than 12-months and our application of discount rates. We are continuing to evaluate this guidance to determine the actual impact on our consolidated financial statements. Our implementation of the amended lease guidance is subject to the same internal controls over financial reporting that we apply to our consolidated financial statements.

10

The FASB has issued ASU No. 2016-13, Financial Instruments - Measurement of Credit Losses on Financial Instruments, or ASU 2016-13. ASU 2016-13 applies to all financial instruments carried at amortized cost including held-to-maturity debt securities as well as trade receivables. ASU 2016-13 requires financial assets carried at amortized cost to be presented at the net amount expected to be collected and available-for-sale debt securities to record credit losses through an allowance for credit losses. ASU 2016-13 is required to be adopted at the beginning of our first quarter of fiscal year 2020, with early adoption permitted. We do not expect to adopt ASU 2016-13 early and we are currently evaluating this guidance to determine the potential impact on our consolidated financial statements.

The FASB has issued ASU No. 2018-02, Reclassification of Certain Tax Effects from Accumulative Other Comprehensive Income, or ASU 2018-02. ASU 2018-02 gives entities the option to reclassify certain tax effects related to items in accumulated other comprehensive income, or OCI, that have been stranded in OCI as a result of the enactment of the TCJA to retained earnings. The guidance is effective for fiscal years beginning after December 15, 2018 with early adoption permitted. As of September 30, 2018 we have not adopted ASU 2018-02 early and we currently expect our adoption of ASU 2018-02 to result in a balance sheet reclassification from OCI to retained earnings of approximately $26 million. We are continuing to evaluate this guidance to determine the final impact on our consolidated financial statements.

3. | Acquisitions and Investments |

Acquisitions

On January 2, 2018, we acquired BondPoint from Virtu Financial, Inc. for $400 million in cash. BondPoint is a provider of electronic fixed income trading solutions for the buy-side and sell-side, offering access to centralized liquidity and automated trade execution services through its alternative trading system, or ATS, and provides trading services to more than 500 financial services firms. BondPoint is primarily included in our Trading and Clearing segment. The BondPoint purchase price was allocated to the preliminary net tangible and identifiable intangible assets and liabilities based on their estimated fair values as of January 2, 2018. The identifiable intangible assets acquired were $130 million and included (i) customer relationships of $123 million, which have been assigned a useful life of 15 years, and (ii) developed technology of $7 million, which has been assigned a life of three years. The excess of the purchase price over the preliminary net tangible and identifiable intangible assets was $267 million and was recorded as goodwill.

On July 18, 2018, we acquired CHX Holdings, Inc., the parent company of the Chicago Stock Exchange, or CHX, a full-service stock exchange, including trading, data and corporate listings services. CHX operates as a registered national securities exchange, and is primarily included in our Trading and Clearing segment.

On July 23, 2018, we acquired TMC Bonds, LLC, or TMC Bonds, for $701 million in cash. The cash consideration is gross of $14 million cash held by TMC Bonds on the date of acquisition. TMC Bonds is an electronic fixed income marketplace, supporting anonymous trading across multiple protocols in various asset classes, including municipals, corporates, treasuries, agencies and certificates of deposit. TMC Bonds is primarily included in our Trading and Clearing segment. The purchase price of TMC Bonds was allocated to the preliminary net tangible and identifiable intangible assets and liabilities based on their estimated fair values as of July 23, 2018. The identifiable intangible assets acquired were $261 million and primarily included (i) customer relationships of $253 million, which have been assigned a useful life of 15 years, and (ii) developed technology of $7 million, which has been assigned a useful life of three years. The excess of the purchase price over the preliminary net tangible and identifiable intangible assets was $423 million and was recorded as goodwill.

On July 20, 2018, we exercised our option to purchase all of the remaining equity interests of MERSCORP Holdings, Inc., owner of Mortgage Electronic Registrations Systems, Inc., or collectively, MERS, as a result of satisfying our deliverables under the software development agreement to rebuild the MERS® System to benefit the U.S. residential mortgage finance market. As of September 30, 2018, we owned a majority stake in MERS, which we treated as an equity investment since we did not have the ability to control the operations of MERS. On October 3, 2018, we completed the purchase of all remaining interests and accordingly, own 100% of MERS. On that date, we gained control of MERS and began to include MERS's results as part of our consolidated operations. In connection with the purchase and upon consolidation, we expect to record a $110 million gain on our initial investment value, which would be included in other non-operating income on October 3, 2018. MERS is included in our Trading and Clearing segment.

Investment in Euroclear

During the year ended December 31, 2017, we purchased a 4.7% stake in Euroclear valued at €276 million ($327 million). Upon purchasing this stake, we agreed to participate on the Euroclear Board of Directors. During the same period, we negotiated an additional purchase which closed on February 21, 2018 following regulatory approval. This provided us with an additional 5.1% stake in Euroclear for a purchase price of €246 million in cash ($304 million). As of September 30, 2018, we owned a 9.8% stake in

11

Euroclear for a total investment of $631 million. Euroclear is a provider of post-trade services, including settlement, central securities depositories and related services for cross-border transactions across asset classes.

We classify our investment in Euroclear as an equity investment included in other non-current assets in the accompanying consolidated balance sheets. As discussed in Note 2, we adopted ASU 2016-01 on January 1, 2018. Under ASU 2016-01, for equity investments without a readily determinable fair value, we may elect to measure them at cost, less any impairment, plus or minus changes resulting from observable price changes in orderly transactions in similar or identical investments. We have elected to use this approach to estimate the value of the Euroclear investment. During the nine and three months ended September 30, 2018, there were no downward or upward adjustments made to the carrying amount of our investment in Euroclear.

Purchase of Non-Controlling Interest

For consolidated subsidiaries in which our ownership is less than 100% and for which we have control over the assets, liabilities and management of the entity, the outside stockholders’ interests are shown as non-controlling interest in our consolidated financial statements. As of December 31, 2017, non-controlling interest consisted of the operating results of our CDS clearing subsidiaries in which non-ICE limited partners held a 29.9% ownership interest. During September 2018, we purchased 3.2% of the ownership interest from a non-ICE limited partner and the remaining non-ICE limited partners hold a 26.7% ownership interest as of September 30, 2018.

4. | Revenue Recognition |

We adopted ASC 606 on January 1, 2018 on a full retrospective basis and have restated the prior reporting periods presented as if ASC 606 had always been applied (Note 2). Our adoption of ASC 606 did not have a material impact on the measurement or recognition of revenue in any prior or current reporting periods. Our adoption of ASC 606 was subject to the same internal controls over financial reporting that we apply to our consolidated financial statements.

Substantially all of our revenues are considered to be revenues from contracts with customers. The related accounts receivable balances are recorded in our balance sheets as customer accounts receivable. We do not have obligations for warranties, returns or refunds to customers, other than the rebates discussed below, which are settled each period and therefore do not result in variable consideration. We do not have significant revenue recognized from performance obligations that were satisfied in prior periods and we do not have any transaction price allocated to unsatisfied performance obligations other than in our deferred revenue. Deferred revenue represents our contract liabilities related to our annual, original and other listings revenues as well as certain data services, clearing services and other revenues. Deferred revenue is the only significant contract asset or liability impacted by our adoption of ASC 606. See Note 6 for our discussion of deferred revenue balances, activity, and expected timing of recognition. As permitted by ASC 606, we have elected not to provide disclosures about transaction price allocated to unsatisfied performance obligations if contract durations are less than one year, or if we are not required to estimate the transaction price. For all of our contracts with customers, except for listings and certain data and clearing services, our performance obligations are short-term in nature and there is no significant variable consideration. See the bullets below for further descriptions of our revenue contracts. In addition, we have elected the practical expedient of excluding sales taxes from transaction prices. We have assessed the costs incurred to obtain or fulfill a contract with a customer and determined them to be immaterial.

Certain judgments and estimates were used in the identification and timing of satisfaction of performance obligations and the related allocation of transaction price. We believe that these represent a faithful depiction of the transfer of services to our customers.

Our primary revenue contract classifications are described below. Although we discuss additional revenue details in our “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the categories below best represent those that depict similar economic characteristics of the nature, amount, timing and uncertainty of our revenues and cash flows.

• | Transaction and clearing, net - Transaction and clearing revenues represent fees charged for the performance obligations of derivatives trading and clearing, and from our cash trading, equity options and fixed income exchanges. The derivatives trading and clearing fees contain two performance obligations: (1) trade execution/clearing novation and (2) risk management of open interest. We allocate the transaction price between these two performance obligations; however, both of these generally occur almost simultaneously and no significant deferral results. The impact of our adoption of ASC 606 on our performance obligations in our clearing business was minimal. Cash trading, equity options and fixed income fees contain one performance obligation related to trade execution which occurs instantaneously. Our transaction and clearing revenues are reported net of rebates, except for the NYSE transaction-based expenses. Transaction and clearing fees can be variable based on trade volume discounts used in the determination of rebates; however, virtually all volume discounts are calculated and recorded on a monthly basis. Transaction and clearing fees, as well as any volume discounts rebated to our customers, are calculated and billed monthly in accordance with our published fee schedules. We make liquidity payments to certain customers in our NYSE businesses and recognize those payments as a cost of revenue. In addition, we pay NYSE regulatory |

12

oversight fees to the SEC and collect equal amounts from our customers. These are also considered a cost of revenue, and both of these NYSE-related fees are included in transaction-based expenses. Transaction and clearing revenues and the related transaction-based expenses are all recognized in our Trading and Clearing segment.

• | Data services - Data service revenues represent the following: |

◦ | Pricing and analytics services consist of an extensive set of independent continuous and end-of-day evaluated pricing services focused primarily on fixed income and international equity securities, valuation services, reference data, index services and multi-asset class portfolio and risk management analytics. |

◦ | Desktops and connectivity services comprise hosting, colocation, infrastructure, technology-based information platforms, workstations, feeds and connectivity solutions through the ICE Global Network. |

◦ | Exchange data services represent subscription fees for the provision of our market data that is created from activity in our Trading and Clearing segment. |

The nature and timing of each contract type for the data services above are similar in nature. Data services revenues are primarily subscription-based, billed monthly, quarterly or annually in advance and recognized ratably over time as our performance obligations of data delivery are met consistently throughout the period. Because these contracts primarily consist of single performance obligations with fixed prices, there is no variable consideration and no need to allocate the transaction price. In certain of our data contracts, where third parties are involved, we arrange for the third party to transfer the services to our customers. In these arrangements we are acting as an agent and revenue is recorded net. All data services fees are recognized in our Data and Listings segment.

• | Listings - Listings revenues include original and annual listing fees, and other corporate action fees. Under ASC 606, each distinct listing fee is allocated to multiple performance obligations including original and incremental listing and investor relations services, as well as a customer’s material right to renew the option to list on our exchanges. In performing this allocation, the standalone selling price of the listing services is based on the original and annual listing fees and the standalone selling price of the investor relations services is based on its market value. All listings fees are billed upfront and the identified performance obligations are satisfied over time. Upon our adoption of the ASC 606 framework, the amount of revenue related to the investor relations performance obligation is recognized ratably over a two-year period, with the remaining revenue recognized ratably over time as customers continue to list on our exchanges, which is generally estimated to be over a period of up to nine years for NYSE and up to five years for NYSE Arca and NYSE American. Listings fees related to other corporate actions are considered contract modifications of our listing contracts and are recognized ratably over time as customers continue to list on our exchanges, which is generally estimated to be a period of six years for NYSE and three years for NYSE Arca and NYSE American. All listings fees are recognized in our Data and Listings segment. |

• | Other revenues - Other revenues primarily include interest income on certain clearing margin deposits, regulatory penalties and fines, fees for use of our facilities, regulatory fees charged to member organizations of our U.S. securities exchanges, designated market maker service fees, exchange membership fees and agricultural grading and certification fees. Generally, fees for other revenues contain one performance obligation. Because these contracts primarily consist of single performance obligations with fixed prices, there is no variable consideration and no need to allocate the transaction price. Services for other revenues are primarily satisfied at a point in time. Therefore, there is no need to allocate the fee and no deferral results as we have no further obligation to the customer at that time. Other revenues are recognized in our Trading and Clearing segment. |

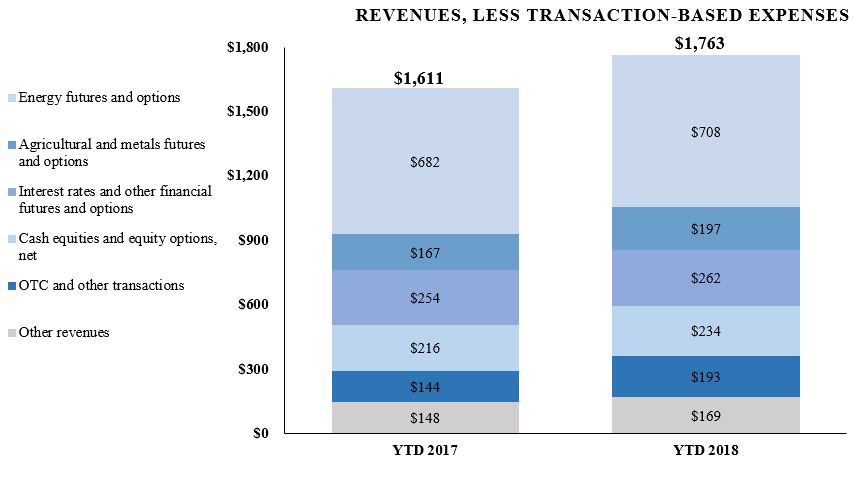

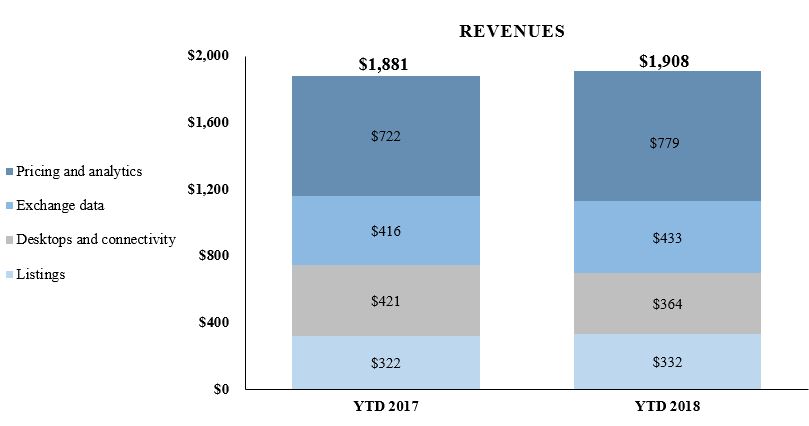

The following table depicts the disaggregation of our revenue according to business line and segment (in millions). Segment totals are consistent with the segment totals in Note 13:

13

Trading and Clearing Segment | Data and Listings Segment | Total Consolidated | |||||||||

Nine months ended September 30, 2018 | |||||||||||

Transaction and clearing, net | $ | 2,522 | $ | — | $ | 2,522 | |||||

Data services | — | 1,576 | 1,576 | ||||||||

Listings | — | 332 | 332 | ||||||||

Other revenues | 169 | — | 169 | ||||||||

Total revenues | 2,691 | 1,908 | 4,599 | ||||||||

Transaction-based expenses | 928 | — | 928 | ||||||||

Total revenues, less transaction-based expenses | $ | 1,763 | $ | 1,908 | $ | 3,671 | |||||

Timing of Revenue Recognition | |||||||||||

Services transferred at a point in time | $ | 1,507 | $ | — | $ | 1,507 | |||||

Services transferred over time | 256 | 1,908 | 2,164 | ||||||||

Total revenues, less transaction-based expenses | $ | 1,763 | $ | 1,908 | $ | 3,671 | |||||

Trading and Clearing Segment | Data and Listings Segment | Total Consolidated | |||||||||

Nine months ended September 30, 2017 | |||||||||||

Transaction and clearing, net | $ | 2,373 | $ | — | $ | 2,373 | |||||

Data services | — | 1,559 | 1,559 | ||||||||

Listings | — | 322 | 322 | ||||||||

Other revenues | 148 | — | 148 | ||||||||

Total revenues | 2,521 | 1,881 | 4,402 | ||||||||

Transaction-based expenses | 910 | — | 910 | ||||||||

Total revenues, less transaction-based expenses | $ | 1,611 | $ | 1,881 | $ | 3,492 | |||||

Timing of Revenue Recognition | |||||||||||

Services transferred at a point in time | $ | 1,373 | $ | — | $ | 1,373 | |||||

Services transferred over time | 238 | 1,881 | 2,119 | ||||||||

Total revenues, less transaction-based expenses | $ | 1,611 | $ | 1,881 | $ | 3,492 | |||||

Trading and Clearing Segment | Data and Listings Segment | Total Consolidated | |||||||||

Three months ended September 30, 2018 | |||||||||||

Transaction and clearing, net | $ | 760 | $ | — | $ | 760 | |||||

Data services | — | 530 | 530 | ||||||||

Listings | — | 112 | 112 | ||||||||

Other revenues | 61 | — | 61 | ||||||||

Total revenues | 821 | 642 | 1,463 | ||||||||

Transaction-based expenses | 263 | — | 263 | ||||||||

Total revenues, less transaction-based expenses | $ | 558 | $ | 642 | $ | 1,200 | |||||

Timing of Revenue Recognition | |||||||||||

Services transferred at a point in time | $ | 477 | $ | — | $ | 477 | |||||

Services transferred over time | 81 | 642 | 723 | ||||||||

Total revenues, less transaction-based expenses | $ | 558 | $ | 642 | $ | 1,200 | |||||

14

Trading and Clearing Segment | Data and Listings Segment | Total Consolidated | |||||||||

Three months ended September 30, 2017 | |||||||||||

Transaction and clearing, net | $ | 758 | $ | — | $ | 758 | |||||

Data services | — | 518 | 518 | ||||||||

Listings | — | 105 | 105 | ||||||||

Other revenues | 54 | — | 54 | ||||||||

Total revenues | 812 | 623 | 1,435 | ||||||||

Transaction-based expenses | 289 | — | 289 | ||||||||

Total revenues, less transaction-based expenses | $ | 523 | $ | 623 | $ | 1,146 | |||||

Timing of Revenue Recognition | |||||||||||

Services transferred at a point in time | $ | 445 | $ | — | $ | 445 | |||||

Services transferred over time | 78 | 623 | 701 | ||||||||

Total revenues, less transaction-based expenses | $ | 523 | $ | 623 | $ | 1,146 | |||||

The Trading and Clearing segment revenues above include $184 million and $172 million for the nine months ended September 30, 2018 and 2017, respectively, and $56 million and $56 million for the three months ended September 30, 2018 and 2017, respectively, for services transferred over time related to risk management of open interest performance obligations. A majority of these performance obligations are performed over a short period of time of one month or less.

5. | Goodwill and Other Intangible Assets |

The following is a summary of the activity in the goodwill balance for the nine months ended September 30, 2018 (in millions):

Goodwill balance at December 31, 2017 | $ | 12,216 | |

Acquisitions | 721 | ||

Foreign currency translation | (20 | ) | |

Other activity, net | 17 | ||

Goodwill balance at September 30, 2018 | $ | 12,934 | |

The following is a summary of the activity in the other intangible assets balance for the nine months ended September 30, 2018 (in millions):

Other intangible assets balance at December 31, 2017 | $ | 10,269 | |

Acquisitions | 435 | ||

Foreign currency translation | (25 | ) | |

Amortization of other intangible assets | (215 | ) | |

Other activity, net | (19 | ) | |

Other intangible assets balance at September 30, 2018 | $ | 10,445 | |

We completed our acquisitions of BondPoint, CHX Holdings, Inc. and TMC Bonds during the nine months ended September 30, 2018 (Note 3). The foreign currency translation adjustments in the tables above result from a portion of our goodwill and other intangible assets being held at our U.K., EU and Canadian subsidiaries, whose functional currencies are not the U.S. dollar. The changes in other activity, net, in the tables above primarily relate to adjustments to the fair value of the net tangible assets and intangible assets relating to the acquisitions, with a corresponding adjustment to goodwill. Amortization of other intangible assets in the table above includes an impairment charge of $4 million recorded during the nine months ended September 30, 2018 on the remaining value of exchange registration intangible assets in connection with the July 2018 closure of ICE Futures Canada and ICE Clear Canada (Note 10). We did not recognize any other impairment losses on goodwill or other intangible assets during the nine and three months ended September 30, 2018 and 2017.

6. | Deferred Revenue |

Our contract liabilities, or deferred revenue, represent consideration received that is yet to be recognized as revenue. Total deferred revenue was $339 million as of September 30, 2018, including $249 million in current deferred revenue and $90 million in non-current deferred revenue. The changes in our deferred revenue during the nine months ended September 30, 2018 are as

15

follows (in millions), adjusted to reflect the adoption of ASC 606 as discussed in Note 2:

Annual Listings Revenues | Original Listings Revenues | Other Listings Revenues | Data Services and Other Revenues | Total | |||||||||||||||

Deferred revenue balance at December 31, 2017 | $ | — | $ | 25 | $ | 98 | $ | 93 | $ | 216 | |||||||||

Additions | 383 | 17 | 36 | 291 | 727 | ||||||||||||||

Amortization | (288 | ) | (17 | ) | (27 | ) | (272 | ) | (604 | ) | |||||||||

Deferred revenue balance at September 30, 2018 | $ | 95 | $ | 25 | $ | 107 | $ | 112 | $ | 339 | |||||||||

The changes in our deferred revenue during the nine months ended September 30, 2017 are as follows (in millions), adjusted to reflect the adoption of ASC 606 as discussed in Note 2:

Annual Listings Revenues | Original Listings Revenues | Other Listings Revenues | Data Services and Other Revenues | Total | |||||||||||||||

Deferred revenue balance at December 31, 2016 | $ | — | $ | 23 | $ | 83 | $ | 92 | $ | 198 | |||||||||

Additions | 367 | 17 | 49 | 307 | 740 | ||||||||||||||

Amortization | (276 | ) | (15 | ) | (31 | ) | (286 | ) | (608 | ) | |||||||||

Divestitures | — | — | — | (10 | ) | (10 | ) | ||||||||||||

Deferred revenue balance at September 30, 2017 | $ | 91 | $ | 25 | $ | 101 | $ | 103 | $ | 320 | |||||||||

Adjustments for divestitures in the table above resulted from our June 2017 divestiture of NYSE Governance Services and our March 2017 divestiture of Interactive Data Managed Solutions, or IDMS, as well as our classification of Trayport deferred revenue as held for sale during the nine months ended September 30, 2017. Included in the amortization recognized for the nine months ended September 30, 2018, is $98 million related to the deferred revenue balance as of January 1, 2018. Included in the amortization recognized for the nine months ended September 30, 2017, is $87 million related to the deferred revenue balance as of January 1, 2017. As of September 30, 2018, we estimate that our deferred revenue will be recognized in the following years (in millions):

Annual Listings Revenues | Original Listings Revenues | Other Listings Revenues | Data Services and Other Revenues | Total | |||||||||||||||

Remainder of 2018 | $ | 95 | $ | 8 | $ | 8 | $ | 68 | $ | 179 | |||||||||

2019 | — | 15 | 34 | 39 | 88 | ||||||||||||||

2020 | — | 2 | 27 | 3 | 32 | ||||||||||||||

2021 | — | — | 19 | 2 | 21 | ||||||||||||||

2022 | — | — | 13 | — | 13 | ||||||||||||||

Thereafter | — | — | 6 | — | 6 | ||||||||||||||

Total | $ | 95 | $ | 25 | $ | 107 | $ | 112 | $ | 339 | |||||||||

7. | Debt |

Our total debt, including short-term and long-term debt, consisted of the following as of September 30, 2018 and December 31, 2017 (in millions):

16

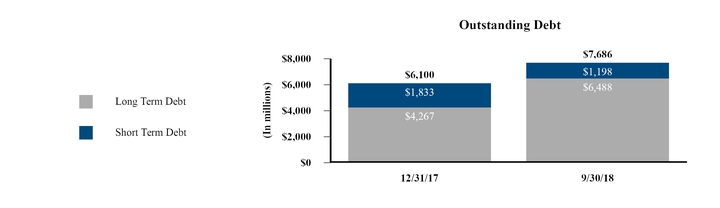

As of September 30, 2018 | As of December 31, 2017 | ||||||

Debt: | |||||||

Short-term debt: | |||||||

Commercial Paper | $ | 1,198 | $ | 1,233 | |||

2018 Senior Notes (2.50% senior unsecured notes due October 15, 2018) | — | 600 | |||||

Total short-term debt | 1,198 | 1,833 | |||||

Long-term debt: | |||||||

2020 Senior Notes (2.75% senior unsecured notes due December 1, 2020) | 1,245 | 1,244 | |||||

2022 Senior Notes (2.35% senior unsecured notes due September 15, 2022) | 496 | 495 | |||||

2023 Senior Notes (3.45% senior unsecured notes due September 21, 2023) | 397 | — | |||||

2023 Senior Notes (4.00% senior unsecured notes due October 15, 2023) | 793 | 791 | |||||

2025 Senior Notes (3.75% senior unsecured notes due December 1, 2025) | 1,243 | 1,242 | |||||

2027 Senior Notes (3.10% senior unsecured notes due September 15, 2027) | 495 | 495 | |||||

2028 Senior Notes (3.75% senior unsecured notes due September 21, 2028) | 591 | — | |||||

2048 Senior Notes (4.25% senior unsecured notes due September 21, 2048) | 1,228 | — | |||||

Total long-term debt | 6,488 | 4,267 | |||||

Total debt | $ | 7,686 | $ | 6,100 | |||

Amended Credit Facility

We have a $3.4 billion senior unsecured revolving credit facility, or the Credit Facility, pursuant to a credit agreement with Wells Fargo Bank, N.A., as primary administrative agent, issuing lender and swing-line lender, Bank of America, N.A., as syndication agent, backup administrative agent and swing-line lender, and the lenders party thereto. On August 9, 2018, we agreed with the lenders to extend the final maturity date of the Credit Facility from August 18, 2022 to August 9, 2023 and make certain other changes, herein referred to as the Amended Credit Facility. We incurred debt issuance costs of $2 million relating to the Amended Credit Facility and these costs are included in the accompanying consolidated balance sheet as other non-current assets and will be amortized over the life of the Amended Credit Facility.

The Amended Credit Facility includes an option for us to propose an increase in the aggregate amount available for borrowing by up to $975 million, subject to the consent of the lenders funding the increase, and certain other conditions. No amounts were outstanding under the Amended Credit Facility as of September 30, 2018. As of September 30, 2018, of the $3.4 billion that is currently available for borrowing under the Amended Credit Facility, $1.2 billion is required to back-stop the amount outstanding under our Commercial Paper Program and $105 million is required to support certain broker-dealer subsidiary commitments.

The amount required to back-stop the amounts outstanding under the Commercial Paper Program will fluctuate as we increase or decrease our commercial paper borrowings. The remaining $2.1 billion available under the Amended Credit Facility as of September 30, 2018 is available for us to use for working capital and general corporate purposes including, but not limited to, acting as a back-stop to future increases in the amounts outstanding under the Commercial Paper Program.

Commercial Paper Program

We have entered into a U.S. dollar commercial paper program, or the Commercial Paper Program. Our Commercial Paper Program is currently backed by the borrowing capacity available under the Amended Credit Facility, equal to the amount of the commercial paper that is issued and outstanding at any given point in time. The effective interest rate of commercial paper issuances does not materially differ from short-term interest rates (such as USD LIBOR). The fluctuation of these rates due to market conditions may impact our interest expense. During the nine months ended September 30, 2018, we repaid a net amount of $35 million of outstanding Commercial Paper.

Commercial paper notes of $1.2 billion with original maturities ranging from one to 81 days were outstanding as of September 30, 2018 under our Commercial Paper Program. As of September 30, 2018, the weighted average interest rate on the $1.2 billion outstanding under our Commercial Paper Program was 2.15% per annum, with a weighted average maturity of 23 days.

Senior Notes

On August 13, 2018, we issued $2.25 billion in new aggregate senior notes. The senior notes comprise $400 million in aggregate principal amount of 3.45% senior notes due in 2023, or the 2023 Senior Notes, $600 million in aggregate principal amount of 3.75% senior notes due in 2028, or the 2028 Senior Notes, and $1.25 billion in aggregate principal amount of 4.25% senior notes due in 2048, or the 2048 Senior Notes, and together with the 2023 Senior Notes and the 2028 Senior Notes, the Newly-Issued Senior Notes. We

17

used the net proceeds from the offering of the Newly-Issued Senior Notes for general corporate purposes, including to fund the redemption of the $600 million aggregate principal amount of 2.50% Senior Notes due October 2018 and to refinance all of our issuances under our Commercial Paper Program that resulted from acquisitions and investments in the last nine months.

We incurred debt issuance costs of $21 million relating to the issuance of the Newly-Issued Senior Notes and they are presented in the accompanying consolidated balance sheet as a deduction from the carrying amount of the related debt liability and will be amortized over their respective lives. The Newly-Issued Senior Notes contain affirmative and negative covenants, including, but not limited to, certain redemption rights, limitations on liens and indebtedness and limitations on certain mergers, sales, dispositions and lease-back transactions.

8. | Equity |

We currently sponsor employee and director stock option and restricted stock plans. Stock options and restricted stock are granted at the discretion of the Compensation Committee of the Board of Directors. All stock options and restricted stock awards are granted at an exercise price equal to the fair value of the common stock on the date of grant. The grant date fair value is based on the closing stock price on the date of grant. The fair value of the stock options and restricted stock on the date of grant is recognized as expense over the vesting period, net of forfeitures. The non-cash compensation expenses recognized in our consolidated statements of income for stock options and restricted stock were $93 million and $102 million for the nine months ended September 30, 2018 and 2017, respectively, and $32 million and $34 million for the three months ended September 30, 2018 and 2017, respectively.

Stock Option Plans

The following is a summary of stock option activity for the nine months ended September 30, 2018:

Number of Options | Weighted Average Exercise Price per Option | |||||

Outstanding at December 31, 2017 | 4,013,388 | $ | 41.13 | |||

Granted | 534,576 | 67.23 | ||||

Exercised | (604,345 | ) | 31.58 | |||

Forfeited | (18,340 | ) | 55.07 | |||

Outstanding at September 30, 2018 | 3,925,279 | 46.09 | ||||

Details of stock options outstanding as of September 30, 2018 are as follows:

Number of Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (Years) | Aggregate Intrinsic Value (In millions) | |||||||||

Vested or expected to vest | 3,925,279 | $ | 46.09 | 6.4 | $ | 113 | ||||||

Exercisable | 2,842,961 | $ | 40.14 | 5.6 | $ | 99 | ||||||

The total intrinsic value of stock options exercised was $25 million and $15 million for the nine months ended September 30, 2018 and 2017, respectively, and $6 million and $8 million for the three months ended September 30, 2018 and 2017, respectively. As of September 30, 2018, there were $10 million in total unrecognized compensation costs related to stock options. These costs are expected to be recognized over a weighted average period of 1.8 years as the stock options vest.

We use the Black-Scholes option pricing model for purposes of valuing stock option awards. During the nine months ended September 30, 2018 and 2017, we used the weighted-average assumptions in the table below to compute the value of all options for shares of common stock granted to employees:

18

Nine Months Ended September 30, | |||||||

Assumptions: | 2018 | 2017 | |||||

Risk-free interest rate | 2.67 | % | 1.84 | % | |||

Expected life in years | 6.0 | 5.0 | |||||

Expected volatility | 20 | % | 21 | % | |||

Expected dividend yield | 1.43 | % | 1.40 | % | |||

Estimated weighted-average fair value of options granted per share | $ | 14.08 | $ | 10.50 | |||

The risk-free interest rate is based on the zero-coupon U.S. Treasury yield curve in effect at the time of grant. The expected life computation is derived from historical exercise patterns and anticipated future patterns. Expected volatilities are based on historical volatility of our stock.

Restricted Stock Plans

In February 2018, we reserved a maximum of 1,303,151 restricted shares for potential issuance as performance-based restricted shares to certain of our employees. The number of shares that will ultimately be granted under this award will be based on our actual financial performance as compared to financial performance targets set by our Board of Directors and the Compensation Committee of the Board of Directors for the year ending December 31, 2018, as well as our 2018 total stockholder return, or TSR, as compared to that of the S&P 500 Index. The maximum compensation expense to be recognized under these performance-based restricted shares is $84 million if the maximum financial performance target is met and all 1,303,151 shares vest. The compensation expense to be recognized under these performance-based restricted shares will be $42 million if the target financial performance is met, which would result in 651,576 shares vesting. We recognize expense on an accelerated basis over the three-year vesting period based on our quarterly assessment of the probable 2018 actual financial performance as compared to the 2018 financial performance targets. As of September 30, 2018, we determined that it is probable that the financial performance level will be at target for 2018. Based on this assessment, we recorded non-cash compensation expense of $18 million and $7 million for the nine and three months ended September 30, 2018, respectively, related to these shares and the remaining $24 million in non-cash compensation expense will be recorded on an accelerated basis over the remaining vesting period, including $5 million of which will be recorded over the remainder of 2018.

The following is a summary of the non-vested restricted share activity for the nine months ended September 30, 2018:

Number of Restricted Stock Shares | Weighted Average Grant-Date Fair Value per Share | ||||

Non-vested at December 31, 2017 | 5,748,408 | $ | 52.78 | ||

Granted | 1,873,785 | 67.70 | |||

Vested | (2,751,637) | 49.95 | |||

Forfeited | (379,218) | 57.97 | |||

Non-vested at September 30, 2018 | 4,491,338 | 60.30 | |||

Restricted stock shares granted in the table above include both time-based and performance-based grants. Performance-based restricted shares have been presented to reflect the actual shares to be issued based on the achievement of past performance targets. Non-vested performance-based restricted shares granted are presented in the table above at the target number of restricted shares that would vest if the performance targets are met. As of September 30, 2018, there were $148 million in total unrecognized compensation costs related to time-based and performance-based restricted stock. These costs are expected to be recognized over a weighted-average period of 1.4 years as the restricted stock vests. These unrecognized compensation costs assume that a target performance level will be met on the performance-based restricted shares granted in February 2018. During the nine months ended September 30, 2018 and 2017, the total fair value of restricted stock vested under all restricted stock plans was $201 million and $199 million, respectively.

Employee Stock Purchase Plan

In May 2018, our stockholders approved our Employee Stock Purchase Plan, or ESPP, under which we have reserved and may sell up to 25,000,000 shares of our common stock to employees. The ESPP grants participating employees the right to acquire our stock in increments of 1% of eligible pay, with a maximum contribution of 25% of eligible pay, subject to applicable annual Internal Revenue Service, or IRS, limitations. Under our ESPP, participating employees are limited to $25,000 of common stock annually, and a maximum of 1,250 shares of common stock each offering period. There will be two offering periods each year, which will run from January 1st (or the first trading day thereafter) through June 30th (or the last trading day prior to such date) and from July 1st (or the first trading day thereafter) through December 31st (or the last trading day prior to such date). The first offering period began on July 2, 2018 and will run through December 31, 2018. The purchase price per share of common stock will be 85% of the lesser of the fair

19

market value of the stock on the first or the last trading day of each offering period, and the price on the first day of the current trading period was $73.73 per share. We recorded compensation expenses of $2 million during the three months ended September 30, 2018 related to the 15% discount that is given to our participating employees.

Stock Repurchase Program

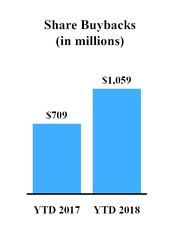

In September 2017, our Board of Directors approved an aggregate of $1.2 billion for future repurchases of our common stock with no fixed expiration date that became effective on January 1, 2018. During the nine months ended September 30, 2018, we repurchased 14,394,028 shares of our outstanding common stock at a cost of $1.1 billion, excluding shares withheld upon vesting of equity awards. The shares repurchased are held in treasury stock and were completed on the open market and under our Rule 10b5-1 trading plan. The timing and extent of future repurchases, if any, will depend upon many conditions. Our management periodically reviews whether to be active in repurchasing our stock. In making a determination regarding any stock repurchases, we consider multiple factors. The factors may include: overall stock market conditions, our common stock price movements, the remaining amount authorized for repurchases by our Board of Directors, the potential impact of a stock repurchase program on our corporate debt ratings, our expected free cash flow and working capital needs, our current and future planned strategic growth initiatives, and other potential uses of our cash and capital resources.

As of September 30, 2018, up to $141 million remains from the board authorization for repurchases of our common stock. In September 2018, our Board of Directors approved an aggregate of $2.0 billion for future repurchases of our common stock with no fixed expiration date that becomes effective January 1, 2019. We expect funding for any stock repurchases to come from our operating cash flow or borrowings under our debt facilities or our Commercial Paper Program. Repurchases may be made from time to time on the open market, through established trading plans, in privately-negotiated transactions or otherwise in accordance with all applicable securities laws, rules and regulations. We have entered into a Rule 10b5-1 trading plan, as authorized by our Board of Directors, to govern some or all of the repurchases of our shares of common stock. We may discontinue the stock repurchases at any time and may amend or terminate the Rule 10b5-1 trading plan at any time. The approval of our Board of Directors for the share repurchases does not obligate us to acquire any particular amount of our common stock. In addition, our Board of Directors may increase or decrease the amount available for repurchases from time to time.

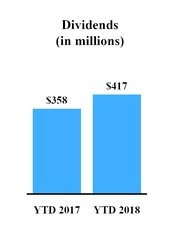

Dividends

During the nine months ended September 30, 2018 and 2017, we paid cash dividends per share of $0.72 and $0.60, respectively, for an aggregate payout of $417 million and $358 million, respectively. The declaration of dividends is subject to the discretion of our Board of Directors, and may be affected by various factors, including our future earnings, financial condition, capital requirements, levels of indebtedness, credit ratings and other considerations which our Board of Directors deem relevant. Our Board of Directors has adopted a quarterly dividend declaration policy providing that the declaration of any dividends will be determined quarterly by the Board of Directors or the Audit Committee of the Board of Directors taking into account such factors as our evolving business model, prevailing business conditions and our financial results and capital requirements, without a predetermined annual net income payout ratio.

9. | Income Taxes |

Our effective tax rate was 21% and 29% for the nine months ended September 30, 2018 and 2017, respectively, and 16% and 33% for the three months ended September 30, 2018 and 2017, respectively. The effective tax rates for the nine and three months ended September 30, 2018 are lower than the effective tax rates for the comparable periods in 2017 primarily due to the enactment of the TCJA on December 22, 2017, which reduced the U.S. federal corporate income tax rate from 35% to 21%, effective January 1, 2018. In addition, for the three months ended September 30, 2018, the effective tax rate was further reduced due to deferred tax benefits associated with the U.S. tax rate reduction resulting from changes in estimates, along with additional tax benefits associated with our sale of Trayport in 2017.

We recorded our income tax provision based on the TCJA as enacted as of September 30, 2018. We have also made reasonable estimates of the TCJA’s impact on state income tax. Our estimates are based on the best available information as of September 30, 2018 and our interpretation of the TCJA and related state tax implications, as currently enacted. Our estimates do not include any potential federal or state administrative and/or legislative adjustments to certain provisions of the TCJA and related state provisions.

SAB 118 provides guidance for companies that have not completed their accounting for income tax effects of the TCJA in the period of enactment, allowing for a measurement period of up to one year after the enactment date to finalize the recording of the related tax impacts. As of September 30, 2018, we have not completed our accounting for the tax effects of the enactment of the TCJA. We will continue to analyze the TCJA in order to finalize its enactment-date effects within the measurement period.

As of September 30, 2018, we have adopted an accounting policy regarding the treatment of taxes due on future inclusion of non-U.S. income in U.S. taxable income under the Global Intangible Low-Taxed Income provisions as a current period expense when incurred. Therefore, no deferred tax related to these provisions has been recorded as of September 30, 2018.

20

10. | Clearing Organizations |

We operate regulated CCPs for the settlement and clearance of derivative contracts. The clearing houses include ICE Clear Europe, ICE Clear Credit, ICE Clear U.S., ICE Clear Netherlands, ICE Clear Singapore and ICE NGX (referred to herein collectively as the “ICE Clearing Houses”).